XPO Logistics: The Asset-Light to Asset-Based Transformation

I. Introduction & Episode Roadmap

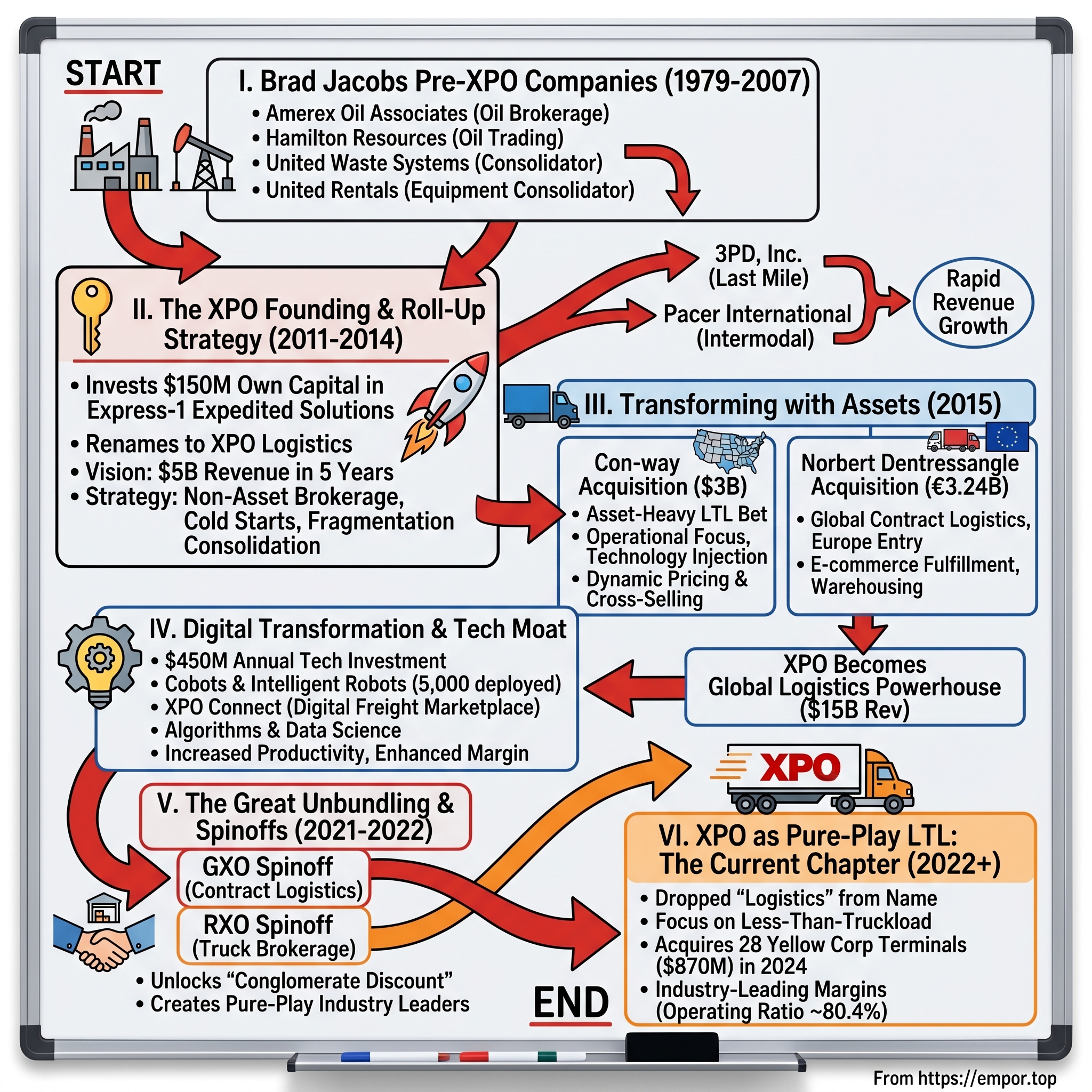

Picture this: A 55-year-old serial entrepreneur walks into a boardroom in 2011 with $150 million of his own money and declares he's going to build a $5 billion logistics empire in five years. The bankers smirk. The industry veterans roll their eyes. Another rich guy thinking he can disrupt trucking? Please.

Fast forward thirteen years. That $150 million seed has sprouted into eight separate companies with a combined market value exceeding $20 billion. Six are publicly traded. The original XPO stock became a "50-bagger" by 2024—turning every dollar invested into fifty. Brad Jacobs didn't just disrupt logistics; he built it up, tore it apart, and rebuilt it three times over, creating more shareholder value through corporate fission than most CEOs create through growth.

How does someone with zero logistics experience waltz into one of America's oldest, most fragmented industries and create the second-largest less-than-truckload carrier in North America? How do you convince Wall Street that breaking up your $20 billion conglomerate into pieces will somehow make the sum worth more than the whole? And perhaps most puzzling: why would you spend a decade assembling a logistics empire only to systematically dismantle it?

This is the story of XPO Logistics—though calling it just "XPO" now, since they dropped the "Logistics" in 2022 after spinning off most of their logistics businesses. It's a masterclass in roll-up economics, the power of technology in traditional industries, and the art of knowing when to hold versus when to fold. It's about recognizing when conglomerate discounts become too painful to ignore and having the courage to blow up your own creation.

We'll trace Brad Jacobs' journey from waste management wunderkind to rental equipment consolidator to logistics revolutionary. We'll dissect the Con-way acquisition that transformed XPO from asset-light broker to asset-heavy operator overnight. We'll explore why Jacobs invested billions in European logistics only to spin it all off five years later. And we'll examine what XPO has become today: a pure-play LTL carrier competing against century-old trucking dynasties with algorithms and automation.

The Brad Jacobs playbook isn't just about buying companies—anyone with capital can do that. It's about recognizing inefficient markets, injecting technology where others see only diesel and asphalt, and understanding that sometimes the best way to create value is to break things apart. As Jacobs himself puts it: "M&A is a tool in the toolkit, but it's not the only tool when you define the job as building an integrated company that creates lots of value for shareholders."

Buckle up. This ride covers three decades, five hundred acquisitions, eight companies, and one very unconventional approach to value creation.

II. The Brad Jacobs Origin Story & Pre-XPO Companies

The story begins not in a boardroom but in Providence, Rhode Island, 1956. Bradley S. Jacobs was the son of Charlotte Sybil (née Bander) and Albert Jordan Jacobs, with his father working as a fashion jewelry importer. Young Brad grew up watching his father navigate the import business, learning early that commerce was about finding value where others didn't see it.

He graduated from Northfield Mount Hermon School and then went on to attend Bennington College and Brown University, studying math and music. Picture a young Jacobs at Brown in 1976, torn between equations and etudes. He was a trained classical pianist, good enough to consider a career in music. But something gnawed at him. He dropped out in 1976, walking away from the ivory tower with a decision that would define his approach to business: when opportunity knocks, you don't wait for permission.

In 1979, Jacobs co-founded Amerex Oil Associates, an oil brokerage firm, serving as the company's CEO until it was sold in 1983. Three years, one exit. Not bad for a college dropout's first venture. In 1984, Jacobs moved to London and founded Hamilton Resources, where he conducted oil trading deals. The oil markets of the 1980s were volatile, perfect for someone who understood that chaos creates opportunity.

But it was 1989 when Jacobs discovered his true calling. In 1989, Jacobs founded United Waste Systems in Greenwich, Connecticut, and began consolidating small waste collection companies that had overlapping routes in rural areas. Think about the genius of this model: dozens of small haulers, each driving their trucks past the same houses, burning diesel to service overlapping territories. Jacobs saw inefficiency as opportunity. Buy them up, rationalize the routes, cut costs, boost margins.

Jacobs was chairman and chief executive officer, and in 1992 he took the company public. The consolidation playbook was elegant: find family-owned businesses too small to achieve scale, offer them liquidity they couldn't get elsewhere, then optimize operations they never had the resources to improve. Jacobs sold United Waste Systems to USA Waste Services for $2.5 billion in August 1997. Eight years, $2.5 billion. The Jacobs formula was proven.

But here's where most entrepreneurs would retire to a beach. Not Jacobs. In September 1997, Jacobs formed United Rentals, and became the new company's chairman and chief executive officer. During late 1997 and early 1998, Jacobs grew the company through a strategy of consolidating equipment rental dealers in North America. He took the company public in December 1997 on the New York Stock Exchange.

Notice the pattern? Same playbook, different industry. Equipment rental in 1997 looked exactly like waste management in 1989: fragmented, family-owned, ripe for consolidation. Small rental shops couldn't afford the latest equipment. They couldn't offer one-stop shopping for large contractors. They couldn't leverage technology to optimize fleet utilization. Jacobs could do all three.

The United Rentals story wasn't without drama. The company grew explosively through acquisitions, becoming the largest equipment rental company in the world. But by 2003, after disagreements with the board about strategy and pace, Jacobs stepped down. The company he built would continue to thrive—it's worth over $50 billion today—but Jacobs was already looking for his next mountain to climb.

Jacobs has frequently recognized Ludwig Jesselson as an influential mentor. Jesselson, who ran Philipp Brothers, taught Jacobs a critical lesson: in commodity businesses, the only sustainable advantage is operational excellence. You can't differentiate garbage or bulldozers. You can only be better at the business of running the business.

By 2010, Jacobs had been out of the CEO chair for seven years. He'd made serious money—hundreds of millions from his two previous ventures. Most people in his position would become venture capitalists, angel investors, or professional board members. Jacobs had a different idea. He formed Jacobs Private Equity with a specific mandate: find one industry, make one massive bet, and build something transformational.

He has completed about 500 M&A transactions across his career, but here's the crucial insight: the volume of deals matters less than the pattern recognition it develops. After 500 acquisitions, Jacobs could walk into any business and immediately spot the inefficiencies, the synergies, the hidden value. He'd developed what he calls "pattern recognition"—the ability to see through the complexity to the simple truths underneath.

As we transition to the XPO story, consider what Jacobs brought to the table: Two successful multi-billion dollar exits. A proven consolidation playbook. Deep relationships with Wall Street. And perhaps most importantly, the patience to wait for the right opportunity and the courage to go all-in when he found it. The logistics industry in 2011 had no idea what was about to hit it.

III. The XPO Founding & Early Strategy (2011–2014)

The scene opens in Buchanan, Michigan, September 2011. Express-1 Expedited Solutions is holding what most employees think will be another routine shareholder meeting. The company, trading on the American Stock Exchange under the ticker XPO, has been struggling. Total revenue from continuing operations for the second quarter was $44.1 million, and while that represented modest growth, margins were under pressure and the expedited freight business was choppy.

Then Brad Jacobs walks in.

In 2011, Jacobs invested approximately $150 million in XPO (then named Express-1 Expedited Solutions), a transportation and third-party logistics provider. He became chairman of the board and CEO and gained ownership of approximately 71 percent of the company. This wasn't venture capital or private equity money. This was Jacobs' own cash, accumulated from his previous ventures. He wasn't buying a stake; he was buying control.

Why logistics? Jacobs had spent 2010 studying industries, looking for his next consolidation play. In 2010, he formed Jacobs Private Equity to make a substantial equity investment in a single company with the potential for superlative value creation and, in 2011, he identified the transportation and logistics industry as being large, fragmented and ripe for consolidation, with the right attributes to leverage scale and technology.

The numbers were compelling. The North American logistics market was approaching $1 trillion. The truck brokerage segment alone was worth $50 billion and growing 15% annually. Yet the largest player, C.H. Robinson, had less than 5% market share. The top 25 brokers combined controlled less than 40%. Thousands of small operators, many running on spreadsheets and whiteboards, competed for the same freight. It was United Waste and United Rentals all over again, but bigger.

Last year, Jacobs led a team that invested $150 million in cash in a non-asset-based expedited transportation company called Express-1 Expedited Solutions Inc. He renamed the company XPO Logistics and installed himself as CEO. From this platform, Jacobs aims to construct a $5 billion to $6 billion-a-year powerhouse mostly by unifying a scattered truck brokerage segment through a combination of acquisitions and organic expansion XPO refers to as "cold starts."

The audacity of the vision was breathtaking. No one recalls a transportation logistics company of this size (XPO is expected to report about $225 million in annual revenue in 2011) achieving a 20- to 30-fold increase in its top line in five years. Jacobs wasn't proposing incremental growth. He was proposing to grow revenue by 2,500% in five years.

In 2012, Jacobs made his intentions even clearer. In 2012, Jacobs announced his intention to grow XPO's revenue from $175 million to $5 billion within five years, primarily through M&A. Instead, he grew revenue to $15 billion in just over four years. But we're getting ahead of ourselves.

The early strategy had four pillars. First, truck brokerage—the non-asset business of matching shippers with carriers. Second, freight forwarding—international logistics and customs clearance. Third, expedited services—time-critical shipments that command premium pricing. XPO's Express-1 unit is already a major player in expedited; it's ranked as the fifth largest expeditor in the U.S. by the Journal of Commerce. Fourth, intermodal—using rail for the long haul and trucks for the first and last mile.

Express-1 gave Jacobs platforms in three of the four verticals. Now he needed to scale them. Jacobs, who opened an office late last year in Phoenix, envisions launching about 20 cold-start offices over the next 18 months to three years. He said he expects each location to generate between $25 million and $200 million in revenue a year. In addition, Jacobs projected that XPO would make five to seven brokerage acquisitions a year.

The "cold start" concept was particularly clever. Instead of waiting for acquisition targets, XPO would open new brokerage offices from scratch in strategic locations, hire experienced brokers from competitors, and grow organically. Phoenix was the test case. If you could make it work there—a major freight hub with plenty of competition—you could replicate it anywhere.

But the real innovation was technology. While competitors relied on phone calls and fax machines, Jacobs envisioned a unified platform connecting shippers, carriers, and brokers in real-time. XPO plans to have one IT platform extending across its brokerage, freight forwarding, and expedited transport businesses. This wasn't just about efficiency; it was about creating network effects that would compound as the company grew.

The early acquisitions began in 2013. 3PD, Inc. in August 2013 brought last-mile delivery capabilities. Then came the big one: Pacer International in March 2014, a $335 million deal that instantly made XPO a major player in intermodal. Pacer brought relationships with all the major railroads and a network of terminals across North America.

Wall Street was skeptical. XPO's publicly traded shares took a hit in the fall after the company reported a $5.38 per-share third-quarter loss. The stock price fell steadily through November, though it had recovered some of its losses by the middle of December. Building a logistics giant through roll-ups had been tried before. Most failed. What made Jacobs think he could succeed where others hadn't?

The answer lay in the details. If you buy a brokerage with $30 million of revenue and you add 30 to 40 bodies, you can double the revenue in time. It wasn't just about buying companies; it was about injecting talent, technology, and capital to accelerate their growth. Each acquisition became a platform for organic expansion.

As 2014 ended, XPO had grown revenue to nearly $2.4 billion through a combination of acquisitions and organic growth. The company was ahead of schedule on Jacobs' five-year plan. But the biggest moves were yet to come. The asset-light strategy had taken XPO far, but Jacobs was beginning to see the limitations. In a capacity-constrained market, brokers were at the mercy of carriers. To truly control its destiny, XPO needed assets. It needed trucks. It needed scale that would make customers and carriers alike take notice.

The stage was set for the transformation that would shock the logistics world.

IV. The Con-way Acquisition: Going Big on LTL (2015)

The news broke on September 9, 2015, like a thunderclap across the logistics industry. XPO Logistics—still seen by many as an upstart broker playing with acquisitions—announced it would acquire Con-way Inc. for $3 billion in cash. The total transaction value is approximately $3.0 billion, including $290 million of net debt. The transaction value represents a multiple of approximately 5.7 times Con-way's 2015 consensus EBITDA of $528 million.

Wall Street was stunned. Industry veterans were speechless. Con-way wasn't just any trucking company—it was a 86-year-old institution with 30,000 employees, 365 service centers, and one of the most respected LTL networks in North America. And Brad Jacobs, the guy who'd been preaching the gospel of asset-light logistics for four years, was about to go all-in on trucks, terminals, and trailers.

Bradley Jacobs, chairman and chief executive officer of XPO Logistics, said, "Our opportunistic acquisition of Con-way will make XPO the second largest provider of less-than-truckload transportation in North America, a $35 billion market. LTL is a non-commoditized, high-value-add business that's used by nearly all of our customers. Con-way is a premier platform that we will run with a fresh set of eyes as part of our broader offering. Importantly, we'll gain strategic ownership of assets that will benefit our company and our customers during periods of tight capacity."

The strategic rationale represented a complete philosophical pivot. For four years, Jacobs had evangelized the asset-light model: Why own trucks when you can broker them? Why maintain terminals when you can outsource? Why deal with drivers when you can let others handle the headaches? But 2014 and 2015 had taught him a harsh lesson. When capacity tightened—as it did during the economic recovery—brokers got squeezed. Carriers held the power. Customers wanted reliability, not excuses about market conditions.

LTL was different from truckload. In truckload, you pick up a full trailer from point A and deliver it to point B. Simple. Commoditized. Price-driven. LTL involved collecting multiple smaller shipments, consolidating them at terminals, running them through a hub-and-spoke network, and delivering them to multiple destinations. It required density, scale, and operational excellence. The barriers to entry were massive—you couldn't just rent some trucks and call yourself an LTL carrier.

The transaction makes XPO the second largest less-than-truckload (LTL) provider in North America; expands the company's global contract logistics, managed transportation and freight brokerage businesses; and adds truckload transportation in North America. Overnight, XPO would control 7% of the North American LTL market, second only to FedEx Freight's 18% share.

But the real prize wasn't market share—it was the network effect. Con-way Freight operated with a 95.6% operating ratio in Q1 2015, meaning it spent $95.60 to generate $100 in revenue. That left plenty of room for improvement. Revenue of $855.6 million, a 0.9 percent increase from $848.0 million in the first quarter of the prior year. Operating income of $37.4 million, more than double the $18.6 million in the previous-year first quarter. Revenue per hundredweight, or yield, increased 3.6 percent compared to the prior-year first quarter. Excluding fuel surcharge, yield rose 8.6 percent. Operating ratio of 95.6 compared to 97.8 in the first quarter of the prior year.

Jacobs saw what others didn't: Con-way was a sleeping giant, weighed down by legacy thinking and underinvestment in technology. The company still used mainframe systems from the 1980s. Dock workers filled out paper forms. Dispatchers relied on whiteboards and intuition rather than algorithms and data. For someone who'd built his career on operational transformation, Con-way was a candy store.

The integration plan was audacious. Within 100 days, XPO would:

- Implement dynamic pricing algorithms to optimize yield

- Deploy mobile technology to every driver and dock worker

- Create a unified customer portal combining LTL, brokerage, and last-mile services

- Rationalize overlapping terminals and routes

- Invest $90 million annually in technology upgrades

The cultural integration would be even trickier. Con-way's employees had worked for a traditional trucking company with a traditional trucking culture. XPO was a technology company that happened to move freight. Jacobs addressed this head-on, meeting with terminal managers across the country, emphasizing that XPO wasn't there to cut jobs but to invest in growth.

The quick wins came faster than expected. By Q1 2016, just months after closing, XPO had already improved Con-way Freight's operating ratio by 210 basis points. Pricing discipline kicked in immediately—XPO walked away from unprofitable freight that Con-way had been hauling for years out of customer loyalty. Technology adoption accelerated: tablets replaced clipboards, algorithms replaced guesswork, data replaced intuition.

But the real transformation was in cross-selling. XPO's brokerage customers suddenly had access to guaranteed LTL capacity. Con-way's LTL customers discovered XPO's last-mile delivery network. The company that had been eight separate acquisitions operating in silos began to function as an integrated logistics ecosystem.

The market's initial skepticism turned to grudging respect. XPO's stock, which had traded at $33 before the Con-way announcement, climbed steadily as the integration progressed smoothly. By year-end 2016, it had nearly doubled. The asset-heavy strategy that everyone thought would sink XPO had instead given it the scale and capabilities to compete with anyone.

Looking back, the Con-way acquisition was the moment XPO transformed from disruptor to incumbent, from upstart to establishment. It also marked the moment Brad Jacobs proved that sometimes the best contrarian bet is to go against your own conventional wisdom. The asset-light evangelist had become asset-heavy, and it was working brilliantly.

V. The European Expansion & Norbert Dentressangle

Five months before announcing the Con-way deal, Brad Jacobs had already been playing three-dimensional chess. On April 28, 2015, XPO announced it would acquire Norbert Dentressangle SA for €3.24 billion ($3.53 billion USD). The acquisition will more than triple XPO's EBITDA run rate to approximately $545 million, and increase its revenue to approximately $8.5 billion, nearly achieving the company's 2017 targets two years ahead of plan.

The timing was exquisite. "Europe has had a tough last few years," Jacobs said. "My sense of the situation is that you're seeing the beginnings of a rebound in the Euro area." The euro had weakened significantly against the dollar, making European assets cheap for American buyers. But Jacobs saw beyond currency arbitrage—he saw a continent where logistics was still fragmented, where technology adoption lagged North America, and where e-commerce was about to explode.

Headquartered in Lyon, France, Norbert Dentressangle has 662 locations and approximately 42,350 employees, and serves a blue chip customer base that includes some of the world's largest companies. The company wasn't just big—it was iconic. Those red trucks with the Norbert Dentressangle logo were as recognizable in Europe as FedEx trucks in America. It was founded in 1979, initially concentrating on cross channel transport between France and the United Kingdom. In December 2007, Norbert Dentressangle doubled its size, and significantly strengthened its position in Europe, with the acquisition of Christian Salvesen, and in March 2011, it bought the British company TDG.

The purchase price represents an aggregate consideration of 9.1 times consensus 2015 EBITDA of €357 million (approximately $388 million USD). The per-share cash price represents a premium of approximately 34 percent compared to the closing price of Norbert Dentressangle ordinary shares on April 27, 2015. Some analysts thought Jacobs was overpaying. But he understood something they didn't: European logistics was about to undergo the same e-commerce transformation that had already swept North America.

The strategic rationale went beyond geography. Norbert Dentressangle brought world-class contract logistics capabilities—massive warehouses operated for blue-chip clients like Unilever, Procter & Gamble, and Nestlé. These weren't just storage facilities; they were sophisticated fulfillment centers with automation, robotics, and advanced warehouse management systems. XPO suddenly had the capability to manage entire supply chains for Fortune 500 companies on both sides of the Atlantic.

Hervé Montjotin, chairman of the executive board and chief executive officer of Norbert Dentressangle, will serve as chief executive officer of XPO's European business and president of the parent company. XPO intends not to reduce the total number of full-time employees in France for a period of at least 18 months from closing. Additionally, XPO intends to maintain the European headquarters of Norbert Dentressangle in Lyon. This wasn't corporate raiding—it was cultural diplomacy. Jacobs understood that acquiring a French national champion required sensitivity. Keeping management, maintaining headquarters, and guaranteeing jobs showed respect for what Norbert Dentressangle had built.

The integration faced an unexpected challenge. The Paris Commercial Court granted a temporary injunction to XPO Logistics Tuesday that would prevent the hedge fund Elliott Capital Advisors LP from selling its shares in Norbert Dentressangle to any party other than XPO Logistics. XPO agreed in principle to purchase Norbert Dentressangle for $3.5 billion in April 2015 and it appeared the acquisition would go through with little to no resistance until Elliot Capital stepped into the picture. Elliot, which is headquartered in New York, owns a 7.5 percent stake in ND. Elliott was trying to extract a premium by threatening to prevent XPO from reaching the 95% ownership threshold needed to delist Norbert Dentressangle from Euronext Paris.

Jacobs didn't blink. He went to court, got the injunction, and eventually squeezed out Elliott at the original price. The message was clear: XPO would be aggressive in pursuing its strategy but wouldn't be held hostage by opportunistic investors.

The cultural transformation was as important as the financial one. In Europe, the iconic red trucks formerly representing Norbert Dentressangle are being repainted to announce #WeAreXPO. XPO Logistics trucks will debut at the Grand Départ of the Tour de France in July, continuing a long-standing partnership as the official logistics partner of the Tour de France. The symbolism was perfect—XPO wasn't erasing Norbert Dentressangle's legacy but evolving it. The Tour de France sponsorship continued, showing continuity with tradition while signaling change.

The technology injection began immediately. European operations that had relied on regional systems were connected to XPO's global platform. Cross-selling opportunities emerged instantly: Norbert Dentressangle's European customers needed North American distribution, while XPO's American clients wanted European logistics solutions. The promised synergies materialized faster than even Jacobs had projected.

But the real genius of the Norbert Dentressangle acquisition became clear only in retrospect. By building a massive European footprint before Brexit, before the e-commerce explosion, before supply chain resilience became a boardroom priority, XPO positioned itself perfectly for the disruptions to come. When COVID hit five years later and companies desperately needed flexible, technology-enabled logistics solutions on both sides of the Atlantic, XPO had already built the infrastructure.

The combined impact of Norbert Dentressangle and Con-way was staggering. XPO paid US$3.56 billion, which included acquired debt, for European transport company Norbert Dentressangle and $3 billion for Con-way. In less than six months, Jacobs had deployed nearly $7 billion to transform XPO from a North American broker into a global logistics powerhouse. Revenue jumped from $2.4 billion to $15 billion. EBITDA soared. The stock price doubled, then doubled again.

Yet even as Wall Street celebrated, Jacobs was already thinking about the next move. The conglomerate he'd built was impressive, but was it optimal? Could the sum of the parts be worth more than the whole? The seeds of XPO's great unbundling were being planted even as the integration celebrations continued.

VI. Technology Innovation & Digital Transformation

Walk into an XPO warehouse in 2016, and you'd see what logistics had looked like for decades: workers with clipboards, forklifts buzzing around, manual picking and packing. Walk into the same warehouse a year later, and you'd witness a transformation so dramatic it seemed like science fiction. Robots glided silently between racks, collaborative machines worked alongside humans, and algorithms orchestrated the entire ballet.

Jacobs came in and soon realized XPO needed better technology to be a world-class logistics company. "XPO focused on having best-in-class technology," said Seidl. CEO Bradley Jacobs moved quickly to add technology, but he wasn't content with merely the best software. XPO began to develop robots and "cobots," a collaborative robot that can interact with humans and help with tasks.

The technology transformation wasn't just about buying gadgets—it was about fundamentally reimagining how logistics worked. XPO's latest robotics implementation is part of the company's planned $450 million investment in technology this year. This wasn't R&D spending; this was a massive capital commitment to revolutionizing operations.

The crown jewel of the transformation was the deployment of collaborative robots. XPO Logistics, Inc. (NYSE: XPO), a leading global provider of transportation and logistics solutions, today announced plans to deploy 5,000 intelligent robots throughout its logistics sites in North America and Europe. The robots, which are designed to collaborate with humans, will supplement XPO's existing workforce and support future growth. XPO has a strategic partnership with robotics manufacturer GreyOrange Pte. Ltd. that makes XPO the exclusive logistics provider for use of its robots in North America, the United Kingdom and eight European countries.

These weren't your grandfather's industrial robots—massive, dangerous machines behind safety cages. The autonomous robots are part of a modular goods-to-person system that also includes mobile storage racks and fulfillment stations. Each robot can move a rack weighing approximately 1,000 to 3,500 lbs., bringing it to a station where a worker fulfills up to 48 orders simultaneously. The entire process is controlled by XPO's proprietary warehouse management system. This high-speed, flexible solution supports same-day and next-day deliveries by shortening order-to-shipment times and helping workers minimize walk-time and manual errors.

The results were staggering. With the use of robotics and machine learning technology, XPO Logistics has seen productivity doubled and rates on average improve by as much as 40%. In addition XPO Logistics has seen enhanced safety as a result of reduced repetition and reduced time walking. XPO says this process will now take 20 to 40 minutes — compared to a couple hours with just human labor — while reducing manual errors.

But robots were just the visible part of the iceberg. The real revolution was happening in software. XPO Connect became the digital nervous system of the company, connecting every truck, terminal, warehouse, and customer into a single platform. Dynamic routing algorithms optimized delivery paths in real-time. Predictive analytics forecasted demand spikes before they happened. Machine learning models priced freight based on thousands of variables, maximizing yield while maintaining competitiveness.

Other recent innovations include the XPO Direct shared-space distribution network, voice integration with Amazon Echo and Google Home to track the last mile delivery of heavy goods, and the XPO Connect digital freight marketplace with multimodal infrastructure. The company wasn't just adopting consumer technology; it was pioneering its application in logistics.

The security innovation was particularly creative. XPO Logistics (NYSE: XPO), a leading global provider of transport and logistics solutions, today announced that its security robot program, launched in October 2017, has reduced incidents at its Atlanta, Ga., logistics facility to zero in the first six months. The autonomous security robot, named C3-XPO, monitors the parking lot and exterior of the site 24 hours a day. XPO contracted with robotics manufacturer Knightscope, Inc. to deploy a solution that provides a physical presence and interprets data in real time. In addition to eliminating parking lot incidents, C3-XPO has saved more than $125,000 in costs associated with six months of traditional security services.

The human element was carefully considered. At XPO Logistics, which has used 6 River Systems technology since 2017, Chuck both helps train new employees and saves employees time. The autonomous cart knows the map of each of XPO Logistics' warehouses and mimics the paths employees need to take. By following Chuck, new employees can quickly understand the layout of the warehouse and which areas they need to pick in. Chuck's screen, meanwhile, can show information about what items employees need to pull. "The training is very quick with Chuck," Lewis said.

This wasn't about replacing workers—it was about augmenting them. At the beginning of the year, XPO said it shipped roughly five-times more units using robotic technology in 2020 than it did in 2019. And the company used advanced automation, including robots and cobots, in more than 25% of e-commerce volume in North America last year.

The competitive advantage became clear during peak seasons. While competitors struggled with labor shortages and capacity constraints, XPO's automated systems scaled seamlessly. Based on our pilots with retail apparel, the system handles peaks in consumer demand with near-perfect accuracy by complementing the work performed by our employees. The synergies are ideal for retail and e-commerce fulfillment this holiday season," commented Mario Harik, chief information officer of XPO Logistics.

The digital freight marketplace was another game-changer. XPO Connect wasn't just an internal system—it became a platform connecting shippers and carriers across the industry. Think of it as the NYSE for freight capacity. Shippers could post loads, carriers could bid, and XPO's algorithms matched supply with demand in real-time. The company that had started as a broker was now building the infrastructure for the entire industry.

Data science became the secret weapon. The company focuses on four areas of innovation: automation and intelligent machines, visibility and customer service, the digital freight marketplace and dynamic data science. Every package scanned, every mile driven, every delivery completed generated data. XPO's data scientists mined this information for insights that human managers could never spot. Which routes consistently ran late? Which customers' shipments damaged most frequently? Which carriers delivered on time? The answers drove continuous improvement.

The Mars partnership showcased the sophistication. The system's major innovation lies in the preparation stage. The robot's articulated arm can pick up as many as five stacks of packages at one time to assemble pallets with multiple product codes. Equipped with grippers and a pneumatic system, the robot ensures product safety at each stage. Nearly 90% of Mars products are compatible with the automation, which has the flexibility to adapt to the constraints of the various packaging options (glass, cardboard or plastic bags).

By 2019, XPO wasn't just using technology—it was a technology company that happened to move freight. The $450 million annual technology investment exceeded what many pure-play tech companies spent on R&D. The company employed more software engineers than truck drivers. Patents were filed for proprietary algorithms. Silicon Valley started recruiting from XPO, not the other way around.

Yet even as the technology transformation reached its zenith, Brad Jacobs was having second thoughts. The market still valued XPO as a transportation company, not a technology company. The stock traded at trucking multiples, not software multiples. The conglomerate structure that had enabled the transformation was now constraining valuation. It was time for the next act.

VII. The Great Unbundling: GXO and RXO Spinoffs (2021–2022)

December 1, 2020. Brad Jacobs stood before analysts and investors with an announcement that shocked nobody and surprised everyone. XPO Logistics, Inc. (NYSE: XPO) ("XPO") today announced that its board of directors has unanimously approved a plan to pursue a spin-off of 100% of its logistics segment as a separate publicly traded company. XPO intends to structure the spin-off as a transaction that is tax-free to XPO shareholders and would result in XPO shareholders owning stock in both companies. After a thorough examination of all strategic alternatives, the XPO board currently believes that the optimal path to unlock aggregate equity value is to create two independent companies that are each well-equipped to capitalize on secular growth trends in their sectors.

The conglomerate discount had become too painful to ignore. The pre-spin XPO was routinely accorded high-single-digit to low-single-digit multiples to earnings before interest, taxes, depreciation and amortization (EBITDA). Old Dominion's, Saia's and Robinson's multiples were typically higher. For example, Old Dominion and Saia shares trade today at 20 and 15.6 times their respective 2021 EBITDA. XPO, despite superior growth and technology, traded at half those multiples.

Jacobs' message for several years is that XPO has been penalized with a multiple-compressing "conglomerate's discount" because the company had too many moving parts for investors to appropriately and accurately value. By separating the two businesses into stand-alone, simpler-to-understand models, Jacobs believes the strategy will help the post-spin XPO escape the penalty box.

The logic was elegant. If completed, the spin-off will result in separate businesses with clearly delineated service offerings: XPORemainCo, a global provider of less-than-truckload (LTL) and truck brokerage transportation services; and NewCo, the second largest contract logistics provider in the world. Each business could tell its own story, attract its own investors, and trade at multiples appropriate to its industry.

GXO Logistics (the eventual name for NewCo) would be the crown jewel of the contract logistics world. Post-separation, NewCo will be the second largest contract logistics company in the world, with approximately 200 million square feet of warehouse space. The business will comprise: A range of innovative services enabled by intelligent technology, including high-value-add warehousing, omnichannel fulfillment, reverse logistics, cold-chain logistics and supply chain optimization; The largest outsourced e-commerce fulfillment platform in Europe.

The execution was flawless. GXO Logistics today began its first day of "regular way" trading on the New York Stock Exchange as its leadership team and board members celebrated GXO becoming an independent, publicly traded company by ringing the Opening Bell®. Under the terms of the previously announced separation, XPO stockholders received one share of GXO common stock for every one share of XPO common stock held as of the close of business on the record date for the distribution, July 23, 2021. GXO shares were distributed at 12:01 a.m. Eastern Time on August 2, 2021 in a distribution that is intended to be tax-free to XPO stockholders for U.S. federal income tax purposes.

Malcolm Wilson, chief executive officer of GXO, said, "This is an exciting milestone in GXO's history. We consider it a privilege to launch GXO as a new company at the top of the industry — the world's largest pure-play logistics provider. We have a powerful platform for future growth, including our culture of innovation, strong customer relationships, seasoned leaders and a world-class team. This is day one of unlocking vast new potential for our company."

The market loved it. GXO shares soared in the months after the separation before falling in the broader market sell-off. But the success of GXO proved the thesis: pure-play companies commanded higher valuations than conglomerates.

Jacobs wasn't done. Less than a year later, he announced the next unbundling. XPO (NYSE: XPO) today announced that it has completed the previously announced spin-off of RXO, Inc., creating two independent, publicly traded companies. XPO is a leading provider of less-than-truckload transportation in North America, and RXO is the fourth largest US truckload broker.

The RXO spinoff followed the same playbook. RXO is the former tech-enabled brokered transportation platform of XPO (NYSE: XPO) and is the fourth largest full truckload broker in the United States. The brokerage, now known as RXO, grew volume by 9% YoY and reported a gross profit margin of 19%, Jacobs said.

The financial engineering was sophisticated. In connection with the separation, GXO made a $794 million cash payment to XPO. This wasn't just about creating separate companies; it was about optimizing capital structures, achieving appropriate leverage ratios, and ensuring each entity had the resources to compete independently.

But the human element was carefully managed too. If the spin-off is completed as expected: Jacobs will continue to serve as chairman and chief executive officer of XPORemainCo, and will become chairman of the NewCo board; Troy Cooper will continue to serve as XPORemainCo's president; and the executives currently leading XPO's global logistics segment will continue to serve in senior positions with NewCo. This wasn't a fire sale or a breakup driven by distress. It was a deliberate, strategic restructuring with continuity of leadership.

The critics had questions. Amit Mehrotra, the longtime Deutsche Bank analyst whose propensity for raising inconvenient truths has earned the transport C-suites' grudging respect and perhaps a slug of enmity, wondered on the call if XPO would still feel the weight of the conglomerate's discount post-spin. Mehrotra asked Jacobs if shedding the brokerage and final-mile businesses — both of which are performing at high levels and would presumably fetch handsome sums if put on the market — might be the path to elevating XPO's multiple to the level of pure-play LTL providers.

Jacobs replied that XPO has no plans to divest the non-LTL businesses, and that it will not be weighed down by the dreaded "discount." Jacobs preached patience and advised all concerned to look beyond the first two weeks or so of trading.

There was also the question of synergies. Will an XPO account executive feel pressure to steer a customer to GXO if that customer wants contract logistics services? The ability to sell a broad transport and logistics portfolio was an important part of XPO's value proposition through the latter part of the past decade. However, Jacobs has said in recent years that most of the cross-selling did not occur across the transportation and logistics businesses, but within the transportation portfolio where an LTL customer may also want final-mile and intermodal coverage.

The results spoke for themselves. That low valuation is part of the justification for the RXO spin-off, as CEO Brad Jacobs has long argued that the stock is undervalued because of a "conglomerate discount." Post-spinoffs, each company began trading at multiples more appropriate to their pure-play peers. The sum of the parts was indeed worth more than the whole.

"With the spin-off complete, XPO and RXO have both launched from positions of strength as independent public companies," Jacobs said in a statement Tuesday. "I want to thank the many people who have worked to make our strategic plan a success and created powerful new avenues for value creation."

The great unbundling transformed one $20 billion conglomerate into three focused companies, each a leader in its segment. GXO became the world's largest pure-play contract logistics provider. RXO emerged as the fourth-largest truck broker in America. And XPO itself was reborn as a pure-play LTL carrier, finally able to command the valuation multiples it deserved.

For Jacobs, it was the ultimate validation of his philosophy: sometimes the best way to create value is to know when to break things apart. The man who spent a decade assembling a logistics empire had spent two years systematically dismantling it, creating more value in the destruction than in the construction. It was financial engineering at its finest.

VIII. XPO as Pure-Play LTL: The Current Chapter

December 2022. The transformation was complete. XPO dropped "Logistics" from its name in December 2022 and remains solely an LTL carrier, which allows multiple customers to transport goods in the same truck. No more confusion about what XPO was. No more conglomerate discount. Just a pure-play LTL carrier with technology in its DNA.

The leadership transition was equally significant. In August 2022, Brad Jacobs announced he was stepping down as CEO and would serve as executive chairman. Mario Harik, XPO's former chief information officer, who also serves as the company's president, was appointed as CEO. This wasn't a founder being pushed out—it was a carefully orchestrated succession. Harik, the architect of XPO's technology transformation, represented continuity with evolution.

Harik's background was telling. He wasn't a trucking guy who learned technology; he was a technology guy who learned trucking. Under his leadership, XPO would maintain its operational excellence while pushing even harder on digital innovation. The message was clear: XPO's future was as much about algorithms as axles.

Then came the opportunity of a lifetime. Yellow Corporation, the third-largest LTL carrier in America with a 99-year history, collapsed in August 2023. Yellow filed for Chapter 11 bankruptcy protection in August 2023, permanently ending operations and laying off approximately 30,000 union and non-union workers. Yellow was the nation's third-largest LTL carrier, with 12,000 trucks and 35,000 trailers at the time of the bankruptcy filing. The failure of the 99 year old company was the largest in U.S. history.

For XPO, Yellow's demise wasn't just the removal of a competitor—it was a once-in-a-generation opportunity to acquire prime assets at distressed prices. United States Bankruptcy Court for the District of Delaware has approved the company's offer to acquire 28 service center locations previously operated by Yellow Corporation. In December 2023, XPO received approval from a Delaware bankruptcy court to acquire 28 service centers of Yellow Corporation for $870 million as a part of Chapter 11 bankruptcy. The acquisition was finalized in January 2024.

Mario Harik, chief executive officer of XPO, said, "This acquisition of real estate is a once-in-a-generation opportunity to increase capacity in critical, growing freight markets, create more jobs and serve our customers even more effectively. We look forward to integrating these prime sites to enhance network efficiency and drive our next decade of growth."

The strategic brilliance of the Yellow acquisition wasn't just about adding terminals. The transaction will complement XPO's national network with prime real estate in fast-growing freight markets, including Atlanta, Brooklyn, Columbus, Greensboro, Houston, Indianapolis, Las Vegas, Minneapolis, Nashville, and other key locations. These weren't random properties—they were carefully selected to fill gaps in XPO's network, reduce stem miles, and improve service to high-growth markets.

The financial engineering was sophisticated. The company has also entered into an $870 million credit agreement which it may use to finance a deal it said would help optimize routes for its less-than-truckload transportation in North America. XPO expects the deal, which is subject to court approval, to add to core profit in 2024 and adjusted profit per share from continuing operations from 2025.

The integration moved at lightning speed. XPO was able to acquire several locations, and will now restart operations in Las Vegas; Sherman, Texas; and Landover, Md. The Landover facility was brought online earlier than planned to help alleviate some of the shipping delays across the areas created by the closure of the Key Bridge in Baltimore. The newly renovated 20,000-square-foot service center is about 10 miles east of Washington, D.C., and 30 miles southwest of Baltimore.

The operational improvements continued unabated. The LTL business delivered a record adjusted operating ratio of 80.4%, meaning an adjusted operating margin of 19.6%, showing how profitable the LTL business has become. This wasn't just good for an LTL carrier—it was approaching best-in-class territory. Old Dominion, long considered the gold standard in LTL, operated with similar margins.

The market dynamics were increasingly favorable. With Yellow's exit removing significant capacity from the market, pricing power shifted to the remaining carriers. XPO, with its expanded network and technological advantages, was perfectly positioned to capture share while maintaining pricing discipline. The deal will add "significant footprint in areas where XPO was previously capacity constrained, the path towards the company's 2027 goals," said Jonathan Chappell, analyst at Evercore ISI.

The technology differentiation became even more pronounced. While competitors struggled with legacy systems and manual processes, XPO's dynamic pricing algorithms optimized yield in real-time. Mobile apps connected drivers, dock workers, and customers seamlessly. Predictive analytics anticipated service failures before they happened. The company that had started as a roll-up of traditional trucking assets had become a technology platform that happened to own trucks.

Competition remained fierce. Old Dominion continued to set the standard for operational excellence. FedEx Freight leveraged its parent company's resources and brand. Regional carriers like Saia and Estes competed aggressively on service and price. But XPO had something unique: the scale of a major carrier combined with the technology DNA of a Silicon Valley startup.

Labor relations presented ongoing challenges. Jacobs will also be dealing with a Teamsters union that XPO held at bay for a decade but that recently secured its first two collective-bargaining agreements with the company. The union believes it has momentum to further organize at XPO, but in Jacobs it faces an implacable foe. The company's non-union status in most locations provided flexibility that unionized competitors lacked, but it also required constant attention to employee satisfaction and competitive compensation.

The pure-play strategy was working. The stock, which had languished in the $30-40 range as a conglomerate, soared past $100 as investors finally gave XPO credit for its operational excellence and growth potential. The company that had been penalized for complexity was now rewarded for focus.

Looking forward, XPO's roadmap was clear: Continue integrating the Yellow terminals to optimize the network. Invest in technology to maintain competitive advantage. Pursue disciplined pricing to expand margins. And perhaps most importantly, resist the temptation to diversify. The lesson of the spinoffs was clear: focus creates value.

As one industry analyst put it: "XPO has completed one of the most remarkable transformations in transportation history. From a $150 million investment to creating eight companies worth over $20 billion. From asset-light broker to asset-heavy operator and back to focused pure-play. From roll-up artist to break-up specialist. And through it all, creating extraordinary value for shareholders."

The current chapter of XPO is still being written, but the trajectory is clear: a technology-enabled LTL carrier competing on operational excellence rather than just price, expanding strategically rather than acquisitively, and finally trading at multiples that reflect its true value. The conglomerate discount is gone. The pure-play premium has arrived.

IX. Playbook: The Brad Jacobs Method

After five decades and eight companies, Brad Jacobs has distilled his approach into a repeatable formula that turns fragmented industries into consolidated powerhouses. The pattern is so consistent it's almost algorithmic, yet each implementation is uniquely tailored to its market. Pattern recognition isn't just about seeing what's there—it's about seeing what could be.

Finding the Right Industry

We have always looked for large, fragmented sectors with secular growth, ample efficiency gains, and where scale plus tech confers real advantage. Building‑products distribution checks every box—$800 billion in global sales, family‑owned operators, low tech penetration, strong free‑cash‑flow tailwinds from housing and infrastructure. The Jacobs method starts with industry selection, and the criteria are non-negotiable: massive addressable markets (preferably over $100 billion), thousands of small operators, minimal technology adoption, and clear paths to operational improvement.

He has completed about 500 M&A transactions. But volume isn't the goal—pattern recognition is. Each deal teaches something: which owners are ready to sell, what multiple makes sense, how to integrate quickly. After 500 transactions, Jacobs can walk into any business and immediately spot the inefficiencies others miss.

The Capital Allocation Discipline

Brad Jacobs: I did most of those acquisitions at United Waste and United Rentals, but in the past decade at XPO, we did only 18 acquisitions. M&A is a tool in the tool kit and it's not the only tool when you define the job as building an integrated company that creates lots of value for the shareholders. The evolution from high-volume acquisitions to selective, transformational deals shows sophistication. It's not about buying everything—it's about buying the right things at the right price.

Jacobs' M&A playbook has powered more than 500 acquisitions. By pursuing multiple targets simultaneously, negotiating several earnings multiples below his expected valuation after investment—and reinvesting that free cash flow into technology upgrades—he has routinely doubled profits within five years of closing. The financial engineering is crucial: never overpay on entry, always have multiple deals in parallel to maintain negotiating leverage, and immediately reinvest savings into technology and operations.

Technology as Differentiator

We're embedding sophisticated tools everywhere. Dynamic pricing engines adjust in real-time based on elasticity curves and customer-level profitability. Agentic AI helps our sales force prioritize leads and optimize margins. A next‑gen data lake and ERP layer drive live P&L dashboards. Machine‑learning forecasts boost item availability. Barcode-driven WMS [warehouse management system] and AI-powered TMS [transportation management systems] standardize warehouse workflows and delivery routes. Even our new POS [point-of-sale] system offers voice‑to‑text entry, real‑time margin visibility, and full CRM integration.

This isn't technology for technology's sake. Every system serves a purpose: improve margins, reduce errors, accelerate decisions. The companies Jacobs acquires typically run on spreadsheets and legacy systems. The technology injection creates immediate competitive advantage.

Quite the opposite. Technology has underpinned every one of my businesses for decades, but people always come first. The human element is carefully managed. Technology augments workers rather than replacing them. Training programs help employees adapt. Career paths open up as companies grow. The message is consistent: we're investing in you, not replacing you.

Building Management Depth

Leadership development is perhaps the most underappreciated aspect of the Jacobs playbook. Each company he builds becomes a training ground for the next generation of executives. Mario Harik went from XPO's CIO to CEO. Malcolm Wilson ran European operations before leading GXO. The bench strength compounds over time.

Management, too, has serious skin in the game: collectively, the board and the executive team, including me, own about 36% of [QXO's] equity, and that level of shareholder alignment is rare and powerful. Alignment matters. Executives aren't just employees—they're owners. Stock options, equity grants, and co-investment opportunities ensure everyone wins when shareholders win.

The Integration Playbook

Integration remains about speed: immediate rebranding across signage and swag, rapid systems consolidation, and creating one unified culture via our internal social platform so that every branch, every employee, and every customer sees "one QXO" from day one. Speed is essential. The longer integration takes, the more value leaks away. Jacobs doesn't believe in gradual transitions. Rip off the band-aid. Change everything at once. Create momentum that becomes self-sustaining.

When to Hold vs. When to Spin

The decision to break up XPO showed another dimension of the Jacobs method: knowing when consolidation has run its course. The conglomerate discount was real and painful. Pure-play companies commanded higher multiples. The math was simple: three companies worth more apart than together. Create them, let the market value them appropriately, move on.

The Network Effect

I've really been fortunate to have investors … who are the smartest of smart money. Sequoia Heritage has been an investor of mine in all my companies at the ground floor; Orbis … was one of our largest investor at XPO and is my largest investor after me in QXO. This is a kitchen cabinet, so to speak, that I can pick up the phone and get opinions—input and advice—that's extremely valuable. [Other investors include Jorge Paolo Lemann, Madrone Capital (which manages the Walton family's money) and Cercano Management (which manages Paul Allen's estate among other ultra-high net worth families).

The investor base isn't just capital—it's a brain trust. These aren't passive limited partners writing checks. They're strategic advisors who've seen every business model, every market cycle, every management mistake. Access to this network is worth more than the capital itself.

The Current Play: QXO

In June 2024, Jacobs founded QXO with the intention to consolidate the $800 billion building products distribution industry. The building products distribution industry is highly fragmented, with approximately 7,000 distributors in North America and 13,000 in Europe, according to industry observers. The industry has generated compound annual revenue growth of 7% over the last five years, based on industry data, and continues to benefit from powerful secular growth drivers for building products distribution in the residential, nonresidential and infrastructure sectors. For example, industry reports estimate that the current supply of U.S. homes is 3 million units short of demand, potentially creating long-term tailwinds for both new construction and the repair and remodeling of aging homes.

QXO represents the Jacobs playbook at its most refined. The industry selection is perfect: massive, fragmented, undercapitalized, ripe for technology injection. The capital raising was unprecedented—And he has $4.5 billion of his and his investors' money to go out and buy and build. The execution has been flawless: Brad Jacobs' QXO successfully acquired Beacon Roofing Supply for approximately $11 billion, initially facing resistance but ultimately reaching a deal at $124.35 per share.

Lessons for Entrepreneurs and Investors

The Jacobs method isn't easily replicated—it requires capital, credibility, and decades of pattern recognition. But the principles are universal:

-

Industry Selection Matters More Than Execution - Even perfect execution in a bad industry yields mediocre returns. Choose massive, fragmented markets with clear consolidation logic.

-

Technology Is The Ultimate Differentiator - In traditional industries, even basic technology creates competitive advantage. In commoditized businesses, technology is the only sustainable moat.

-

Speed Compounds - Fast integration, fast decision-making, fast capital deployment. Velocity creates momentum. Momentum attracts talent and capital. The flywheel accelerates.

-

People and Incentives Drive Everything - Technology has underpinned every one of my businesses for decades, but people always come first. Align incentives, develop talent, create ownership mentality. The best technology and strategy mean nothing without execution.

-

Know When to Pivot - The courage to break up XPO after building it for a decade shows intellectual flexibility. When facts change, change your strategy. Ego is expensive.

-

Capital Structure Is Strategy - How you finance determines what you can build. Patient capital enables long-term thinking. Aligned investors provide more than money.

The Brad Jacobs playbook isn't just about building companies—it's about recognizing inefficiency at scale and having the courage, capital, and capability to fix it. In an economy increasingly dominated by technology giants, Jacobs proves that enormous value still exists in transforming traditional industries. The opportunities are hiding in plain sight. You just need to know how to see them.

X. Analysis & Investment Case

The transformation of XPO from a $150 million investment to a pure-play LTL powerhouse trading above $125 per share presents a compelling case study in value creation. But past performance, as they say, doesn't guarantee future results. Let's examine XPO through the lens of a fundamental investor considering the stock today.

The LTL Economics

Less-than-truckload is one of the best business models in transportation. Unlike truckload where barriers to entry are low (buy a truck, get a license, start hauling), LTL requires massive infrastructure: terminals, cross-docks, local delivery fleets, and sophisticated routing systems. The network effects are powerful—each additional terminal makes the entire network more valuable. Density drives profitability.

XPO's unit economics have steadily improved since becoming a pure-play. Operating ratios in the low 80s put XPO in elite company, approaching Old Dominion's industry-leading margins. Every 100 basis points of operating ratio improvement on $4.5 billion of LTL revenue translates to $45 million of additional operating income. The leverage is enormous.

Pricing power remains robust. With Yellow's exit removing 8-10% of industry capacity and e-commerce driving sustained demand for LTL services, carriers can be selective about freight. XPO's technology enables dynamic pricing that optimizes yield while maintaining utilization. This isn't the commoditized trucking market of old—it's a sophisticated service where reliability commands premiums.

Competitive Positioning

XPO sits in an interesting position competitively. It lacks Old Dominion's decades of operational excellence and pristine service metrics. It doesn't have FedEx Freight's parent company resources or brand recognition. But it has something potentially more valuable: a technology platform built from the ground up for the digital age.

While competitors retrofit technology onto legacy operations, XPO designed its systems holistically. The dynamic pricing algorithms, real-time visibility tools, and predictive analytics aren't bolted on—they're fundamental to how XPO operates. This shows up in the numbers: XPO generates similar margins to Old Dominion despite being less than half the size.

The Yellow terminal acquisitions fundamentally changed XPO's competitive position. Adding 28 strategic locations filled critical gaps in the network, reduced stem miles, and improved service to key markets. More importantly, XPO cherry-picked the best locations while competitors fought over the scraps. The integration has proceeded flawlessly, with several terminals already operational and contributing to earnings.

Technology Moat

The technology advantage is real but difficult to quantify. XPO invests over $100 million annually in technology—more than most LTL carriers' entire IT budgets. But it's not just the spending level; it's the quality of talent. XPO employs more software engineers than some Silicon Valley startups. The company files patents on logistics algorithms. Tech companies recruit from XPO, not the other way around.

This technology moat manifests in multiple ways. Customer acquisition costs are lower because the digital experience is superior. Driver retention is higher because the tools make their jobs easier. Pricing optimization yields 2-3% higher revenue per hundredweight than competitors on similar freight. Small advantages compound over time.

The risk is that technology advantages erode. Competitors are investing heavily in digital capabilities. New entrants could emerge with even better technology. But XPO's combination of physical network and digital platform creates barriers that pure-play tech companies can't easily overcome. You need both atoms and bits to succeed in modern logistics.

Bear Case

The bear case for XPO centers on cyclicality and execution risk. LTL transportation is inherently tied to economic activity. When GDP contracts, freight volumes decline. When manufacturing slows, LTL tonnage drops. XPO may have technology advantages, but it can't overcome gravity.

Labor remains a persistent challenge. While XPO has successfully resisted widespread unionization, the Teamsters have gained footholds in certain terminals. Labor costs are rising across the industry. Driver shortages persist despite wage increases. Automation can help but can't eliminate the human element in last-mile delivery.

Competition is intensifying. Old Dominion continues to take share with superior service. Regional carriers like Saia and Estes are expanding aggressively. Amazon is building its own logistics network that could eventually compete with traditional LTL. The industry that consolidated after deregulation might fragment again as new models emerge.

Valuation is no longer cheap. At 15-20x forward earnings, XPO trades at a premium to historical trucking multiples. The market is pricing in continued margin expansion and market share gains. Any operational stumble or economic downturn could trigger multiple compression. The easy money from re-rating has been made.

Bull Case

The bull case starts with secular growth drivers. E-commerce penetration continues to increase, driving demand for LTL services. Manufacturing reshoring creates new freight lanes. Infrastructure spending generates industrial demand. These aren't cyclical trends—they're structural shifts that benefit LTL carriers for years to come.

Margin expansion has room to run. XPO's operating ratio can improve another 300-400 basis points to match best-in-class competitors. The Yellow terminals provide capacity for growth without proportional cost increases. Technology investments are starting to pay off in improved asset utilization and pricing optimization. Operating leverage remains substantial.

The consolidation opportunity is underappreciated. With Yellow gone, the top 10 LTL carriers control less than 75% of the market. Hundreds of small, subscale carriers struggle with rising costs and technology requirements. XPO has the balance sheet and expertise to roll up smaller competitors at attractive multiples. Each acquisition strengthens the network effect.

XPO was the seventh best-performing stock of the last decade in the Fortune 500 and became a "50-bagger" by the end of 2024 — meaning initial investors in XPO made more than 50 times their money. While past performance doesn't guarantee future results, management's track record of value creation is exceptional. Brad Jacobs remains executive chairman with significant skin in the game. Mario Harik brings technology expertise and operational discipline. The culture of innovation and execution persists.

The Investment Decision

XPO today isn't the undiscovered gem it was in 2011. It's a recognized leader trading at a premium multiple. But that doesn't mean the opportunity is gone. The company has transformed from a complex conglomerate to a focused LTL carrier with technology advantages, expanding margins, and strategic assets from the Yellow acquisition.

For growth investors, XPO offers exposure to secular trends in e-commerce and logistics with a management team that has consistently exceeded expectations. For value investors, the margin expansion opportunity and market share gains from Yellow's exit provide clear catalysts for earnings growth. For income investors... well, XPO doesn't pay a dividend and likely won't anytime soon, prioritizing growth investment over distributions.

The key question isn't whether XPO is a good company—it clearly is. The question is whether it's a good stock at current prices. With the stock trading near all-time highs and multiples expanded, the margin of safety has narrowed. Future returns will likely come from earnings growth rather than multiple expansion.

So What for Investors?

XPO represents a new breed of industrial company: operationally excellent like the old-line leaders but technology-enabled like modern disruptors. It's neither a pure trucking play nor a tech stock, but something in between. Investors must understand both the traditional LTL industry dynamics and the potential for technology to reshape those dynamics.

The company's evolution from roll-up to pure-play demonstrates management's willingness to adapt and optimize for value creation. This flexibility is valuable in a rapidly changing industry. XPO won't hesitate to pivot again if circumstances warrant.

Risk management is crucial. Position sizing should reflect the cyclical nature of transportation, even for a best-in-class operator. Diversification across the logistics value chain might mean owning XPO alongside RXO, GXO, or competitors. Understanding your own investment timeline matters—XPO could underperform during recessions but outperform over full cycles.

The investment case ultimately depends on your view of three factors: the sustainability of LTL industry dynamics, XPO's ability to gain share and expand margins, and the value of technology differentiation in a traditional industry. Bulls see a company early in its transformation with years of growth ahead. Bears see a cyclical business trading at peak multiples late in the economic cycle.

The truth, as usual, likely lies somewhere in between. XPO has proven its ability to create extraordinary value, but the easy gains are behind it. Future returns will require continued execution, favorable industry dynamics, and perhaps a bit of the magic that has characterized Brad Jacobs' entire career. For investors willing to bet on all three, XPO remains one of the most interesting stories in American business.

XI. Epilogue: Brad Jacobs' Next Act & XPO's Future

In June 2024, Jacobs founded QXO with the intention to consolidate the $800 billion building products distribution industry. Just when you thought Brad Jacobs might finally rest on his laurels—eight companies created, six publicly traded, billions in value generated—he launches his most ambitious project yet.

As previously announced, on December 3, 2023, Jacobs Private Equity II, LLC ("JPE"), which is led by Brad Jacobs, and minority co-investors entered into an investment agreement (the "Investment Agreement") with SilverSun Technologies, Inc. (Nasdaq: SSNT) ("SilverSun" or the "Company"), pursuant to which JPE and the minority co-investors will invest $1 billion in cash into SilverSun. The proposed investment is comprised of $900 million by JPE and $100 million by co-investors, including Sequoia Heritage. Upon the closing of the equity investment, JPE will become SilverSun's majority stockholder, Jacobs will become its chairman and chief executive officer, and SilverSun will be renamed QXO.

The QXO playbook is pure Jacobs, refined to its essence. Find a massive, fragmented industry ($800 billion globally). Identify inefficiencies (13,000 distributors in Europe, 7,000 in North America). Raise unprecedented capital ($5 billion and counting). Move fast (Beacon Roofing Supply acquired for $11 billion within months). Apply technology ruthlessly. Create value relentlessly.

What makes QXO fascinating isn't just its ambition—it's what it says about Jacobs' evolution as an entrepreneur. At 68, when most executives are writing memoirs and joining boards, Jacobs is building his largest company yet. QXO is targeting $50 billion in annual revenues within the next decade through accretive acquisitions and organic growth. That would make it larger than XPO, GXO, and RXO combined.

The building products distribution industry is perfect for the Jacobs treatment. It's massive but fragmented. Essential but inefficient. Traditional but ripe for technology disruption. It's logistics-intensive, making it a natural extension of his expertise. And unlike his previous ventures, it's somewhat recession-resistant—buildings always need maintenance, repairs, renovations.

For XPO, Jacobs' new venture is both validation and challenge. Validation because it shows the model works—the same playbook can create value across industries. Challenge because Jacobs' attention, while still present as executive chairman, is inevitably divided. The company must prove it can thrive without its founder's daily involvement.

Mario Harik's leadership represents continuity with evolution. As the architect of XPO's technology transformation, he understands what differentiates the company. But he's also his own leader, with his own vision. Under Harik, XPO has become more operationally focused, more disciplined about capital allocation, more systematic about improvement. The cowboy era of rapid-fire acquisitions is over. The era of operational excellence has begun.

The competitive landscape continues to evolve. Amazon's logistics ambitions grow daily. Autonomous vehicles promise to revolutionize transportation, though the timeline remains uncertain. Digital freight brokers are attracting venture capital and challenging traditional models. The industry that seemed stable for decades faces more disruption in the next five years than the previous fifty.

XPO is well-positioned for this disruption. Its technology platform can adapt to autonomous vehicles when they arrive. Its data advantage compounds daily. Its culture of innovation means it will more likely disrupt than be disrupted. But nothing is guaranteed. Success requires continued investment, continued innovation, continued execution.

The broader lesson of XPO transcends logistics. In an economy increasingly dominated by technology giants and platform monopolies, XPO proves that enormous value still exists in traditional industries. You don't need to invent the next social network or artificial intelligence to create billions in value. Sometimes you just need to make trucks run better.

Brad Jacobs' legacy is already secure. Jacobs has created eight companies, six of which are publicly traded: QXO (2024); XPO (2011) and its spin-offs, GXO Logistics (2021) and RXO (2022); United Rentals (1997); and United Waste Systems, now Waste Management (1989). Few entrepreneurs can claim one successful exit. Jacobs has eight and counting. His returns aren't measured in multiples but in orders of magnitude.

Yet the story feels unfinished. QXO is just getting started. XPO has room to grow. The logistics industry continues to evolve. And somewhere, in some overlooked corner of the economy, there's probably another fragmented industry waiting for someone with capital, vision, and courage to transform it.

The XPO story teaches us that value creation isn't about invention—it's about improvement. It's not about disrupting industries—it's about consolidating them. It's not about building from scratch—it's about buying and transforming. And most importantly, it's not about doing one thing forever—it's about knowing when to build, when to hold, and when to break apart what you've created.

For investors, the lesson is clear: look for inefficiency at scale. Find industries where technology hasn't penetrated. Identify consolidation opportunities. And when you find the right combination of fragmentation, inefficiency, and transformation potential, be prepared to bet big.

For entrepreneurs, the message is equally clear: think bigger. Jacobs didn't start with $150 million aiming to build a nice little trucking company. He aimed to transform an entire industry. That audacity, backed by discipline and execution, is what separates value creators from value extractors.

As for XPO itself, the future remains unwritten. Will it become the Old Dominion of the next generation—operationally excellent, consistently profitable, boringly successful? Will it use its technology advantages to redefine what an LTL carrier can be? Will it eventually reconsolidate with GXO or RXO as industry dynamics shift? Or will it become an acquisition target itself, purchased by Amazon or another giant seeking instant logistics capabilities?

The only certainty is change. The logistics industry will continue evolving. Technology will continue advancing. New competitors will emerge. Old ones will fail. Through it all, the companies that survive and thrive will be those that combine operational excellence with technological innovation, scale with agility, tradition with transformation.

XPO embodies all these contradictions. It's a century-old business model powered by cutting-edge technology. It's a pure-play LTL carrier that thinks like a software company. It's a company built through acquisitions that created value through divestitures. It's proof that in business, as in life, the most interesting stories are never quite what they seem.

The road ahead for XPO is long and uncertain. But if the past is any guide, it will be anything but boring. And for those paying attention—investors, entrepreneurs, students of business—there will be lessons to learn, patterns to recognize, and value to be created.

The Brad Jacobs playbook isn't finished being written. Neither is XPO's story. The best chapters may be yet to come.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube