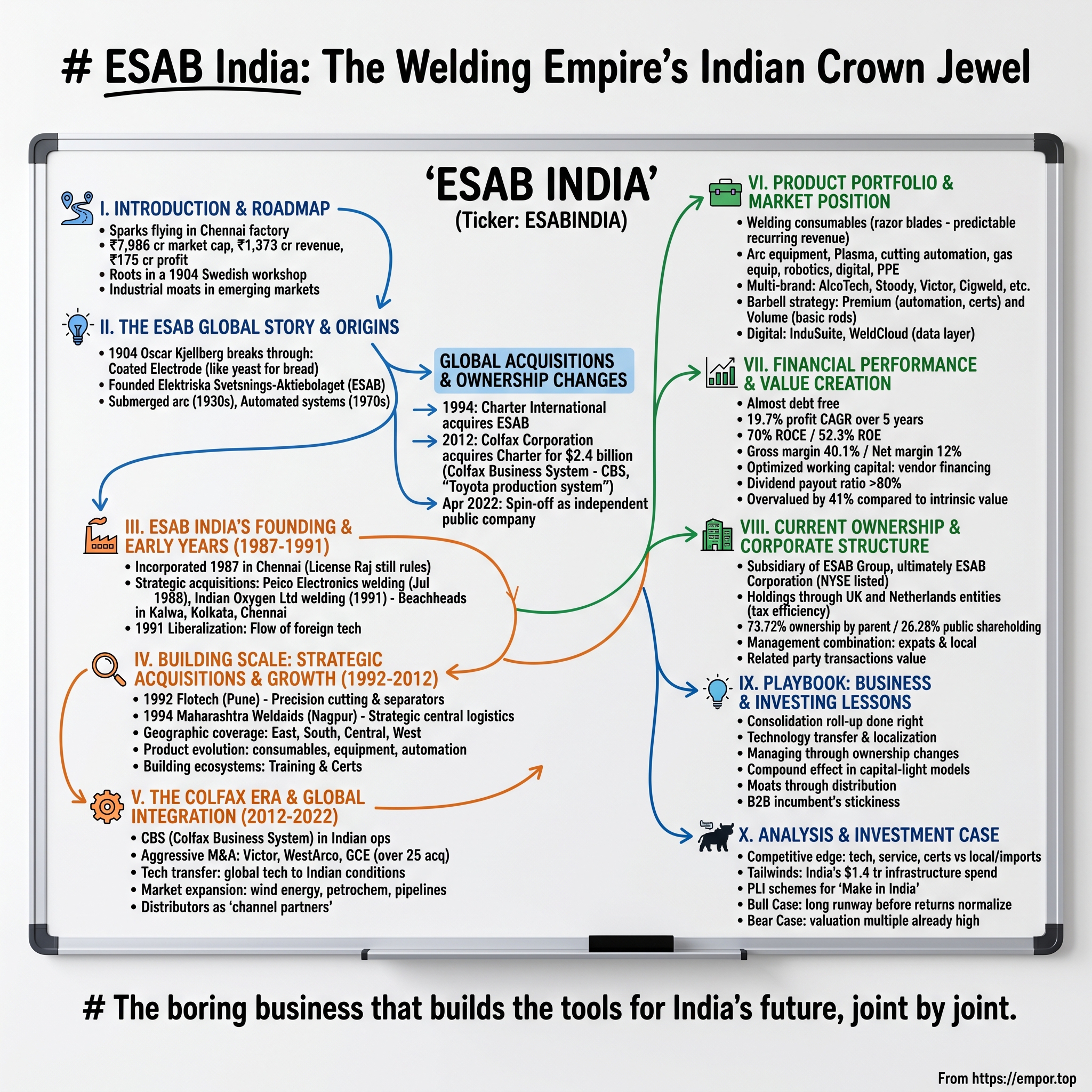

ESAB India: The Welding Empire's Indian Crown Jewel

I. Introduction & Episode Roadmap

Picture this: Inside a sprawling factory in Chennai, sparks fly as robotic arms perform precise welds on wind turbine components destined for offshore farms. The equipment bears the ESAB logo—a brand that has quietly become synonymous with industrial welding across India. From the shipyards of Kolkata to the pipeline projects crossing the Thar Desert, ESAB India's products are literally holding the country's infrastructure together.

Here's what's remarkable: This ₹7,986 crore market cap company, generating ₹1,373 crore in revenue and ₹175 crore in profit, traces its roots not to India's industrial heartland, but to a Swedish inventor's workshop in 1904. The mystery we're unraveling today is how a Scandinavian welding innovation became the backbone of India's industrial revolution—and why international investors are paying attention to what might be the most boring-sounding business with the most exciting fundamentals.

ESAB India isn't just a welding company. It's a case study in technology transfer, market consolidation, and the art of building industrial moats in emerging markets. With a return on capital employed of 70% and virtually no debt, this company has engineered something remarkable: turning metal joining into a high-margin, capital-light business model that would make software companies envious.

What we'll explore today is a century-spanning saga of innovation, strategic acquisitions, and the peculiar dynamics of B2B industrial markets. We'll trace the journey from Oscar Kjellberg's breakthrough in covered electrodes to ESAB India's current position as the dominant force in one of the world's fastest-growing industrial markets. Along the way, we'll unpack the playbook for how global industrial companies can successfully localize in emerging markets, why distribution matters more than technology in certain sectors, and what happens when a company changes ownership three times while maintaining operational excellence.

This is the story of how welding—yes, welding—became a window into India's manufacturing ambitions, and why the companies that build the tools often matter more than the companies that use them.

II. The ESAB Global Story & Origins

The year is 1904. In a modest workshop in Gothenburg, Sweden, a naval engineer named Oscar Kjellberg is wrestling with a problem that has plagued metalworkers since the discovery of electric arc welding: the arc is unstable, the welds are inconsistent, and the process is more art than science. Ships leak, bridges fail, and industrial progress stutters because humans haven't figured out how to reliably join two pieces of metal.

Kjellberg's breakthrough wasn't just technical—it was philosophical. While others were trying to perfect the arc itself, he focused on what surrounded it. His innovation: the coated electrode, a welding rod covered in flux that stabilized the arc, protected the weld from atmospheric contamination, and made consistent, strong welds possible for the first time. It was like discovering that the secret to perfect bread wasn't the oven, but the yeast.

He founded Elektriska Svetsnings-Aktiebolaget—ESAB—that same year, and the company quickly became synonymous with welding innovation. The Swedish industrial tradition of precision engineering and methodical improvement found its perfect expression in welding technology. While American companies were building bigger, ESAB was building better.

The company's early decades read like a highlight reel of industrial breakthroughs. Submerged arc welding in the 1930s—hiding the arc under a blanket of granular flux—allowed for deeper penetration and faster welding speeds. Gas metal arc welding developments in the 1950s. Automated welding systems in the 1970s. Each innovation wasn't just a product; it was a step toward making welding more science than craft.

But here's where the story takes an unexpected turn. By the 1990s, ESAB had built a global empire of welding excellence, yet it found itself at a crossroads. The welding industry was fragmenting—hundreds of regional players, each with local relationships and specialized knowledge. ESAB's Swedish perfectionism had created world-class products, but distribution and local presence would determine the winners in this new landscape.

In 1994, Charter International acquired ESAB, beginning a series of ownership changes that would reshape the company's destiny. Charter saw what others missed: welding wasn't about the best technology winning; it was about being everywhere your customers needed you. They initiated an aggressive acquisition strategy, absorbing regional players and their distribution networks. The real transformation came in 2012 when Colfax Corporation acquired Charter International, and with it ESAB, for $2.4 billion on January 13, 2012. The Rales brothers' Colfax wasn't just another industrial conglomerate—it was a laboratory for operational excellence, armed with the Colfax Business System (CBS), their answer to Toyota's production system. Colfax was "solidly focused on customer needs and the development of strong brands", and they saw in ESAB what private equity sees in fragmented industries: a platform for consolidation.

Under Colfax's ownership from 2012 to 2022, ESAB transformed from a product company into a solutions empire. The acquisition spree was breathtaking in its scope and strategic coherence. Victor Technologies brought gas equipment expertise. Thermal Dynamics added plasma cutting technology. Each acquisition wasn't just about adding revenue; it was about completing the puzzle of becoming the one-stop shop for any fabrication need.

The Colfax decade ended with another twist: On April 5, 2022, Colfax Corp. distributed 100% of the shares of ESAB Corporation to Colfax shareholders, spinning off ESAB as an independent public company. The welding giant was free again, but now armed with global scale, technological breadth, and—critically for our story—dominant positions in emerging markets like India.

III. ESAB India's Founding & Early Years (1987-1991)

The India that ESAB entered in 1987 was a nation at an inflection point. The License Raj still ruled—every business decision required government permission, foreign companies were viewed with suspicion, and industrial policy was more about protection than productivity. Yet beneath this bureaucratic surface, India's industrial sector was stirring. The country needed infrastructure, and infrastructure needed welding.

ESAB India's incorporation in 1987 wasn't a greenfield venture born of Swedish ambition. It was something more pragmatic and, in retrospect, more brilliant: a series of strategic acquisitions that would piece together a national footprint from the remnants of struggling local players. The company set up headquarters in Chennai, a choice that would prove prescient given Tamil Nadu's emergence as an industrial powerhouse.

The real beginning came in July 1988 with a move that defined ESAB India's playbook for decades: acquiring the welding division of Peico Electronics & Electricals Ltd. (later Philips India Limited) located at Kalwa, Maharashtra. Think about what this meant—instead of building from scratch, ESAB inherited existing customer relationships, trained workers, and most importantly, local market knowledge. The Kalwa facility wasn't just a factory; it was a beachhead into Western India's industrial corridor.

But the masterstroke came in 1991. While the rest of India was transfixed by economic liberalization and Manmohan Singh's budget speech, ESAB quietly executed what would become the foundation of its dominance: acquiring the entire welding division of Indian Oxygen Ltd (now BOC India Ltd). This wasn't just any acquisition—it came with three manufacturing units, two in Kolkata and one in Chennai.

Consider the strategic brilliance here. Kolkata gave ESAB access to Eastern India's heavy engineering sector—shipbuilding, railways, and the industrial belt stretching into Jharkhand's steel country. Chennai reinforced their Southern stronghold, positioning them perfectly for the automotive and light engineering boom that would follow. In one move, ESAB had transformed from a single-factory operation to a pan-Indian presence.

The timing was exquisite. India's liberalization in 1991 meant that for the first time, foreign technology could flow freely into the country. While competitors were still figuring out joint venture agreements and technology transfer protocols, ESAB India already had the infrastructure to absorb and deploy global innovations. They had solved the hardest part of doing business in India—distribution and local presence—before the game even began.

What's often missed in this story is the human element. The workers and managers from Indian Oxygen and Peico didn't just bring technical skills; they brought something more valuable—relationships. In India's relationship-driven B2B market, knowing the purchasing manager at Larsen & Toubro or having tea with the workshop supervisor at Mazagon Dock mattered more than having the best product catalog. ESAB inherited these relationships wholesale.

The early years also revealed ESAB India's cultural adaptability. While the parent company pushed Swedish precision and standardization, the Indian operations learned to navigate local realities—monsoon disruptions, power cuts, and the intricate dance of managing union relations. They developed what you might call "jugaad engineering"—maintaining Swedish quality standards while adapting to Indian conditions.

By the end of 1991, ESAB India had achieved something remarkable: they were simultaneously foreign and local, global and Indian. They had Swedish technology flowing through Indian factories, sold by Indian salespeople who had been calling on Indian customers for decades. This hybrid identity would become their greatest competitive advantage as India opened up to the world.

IV. Building Scale: Strategic Acquisitions & Growth (1992-2012)

The 1990s in India were like a gold rush in slow motion. Economic liberalization had opened the floodgates, but the infrastructure to support growth was still being built. Roads, ports, power plants, refineries—everything needed to be constructed or upgraded. For a welding company, this was the equivalent of a breakfast buffet at the Ritz. ESAB India didn't just participate in this boom; they orchestrated their expansion with the precision of a chess grandmaster.

The 1992 acquisition of controlling interest in Flotech Welding & Cutting Systems Ltd. in Pune wasn't random. Pune was emerging as India's Detroit—home to Bajaj, soon to host Volkswagen, and the epicenter of India's automotive component industry. But Flotech brought something specific: cutting machines. If ESAB's previous acquisitions were about joining metals, Flotech was about precision separation. Together, they could offer complete fabrication solutions.

Then came 1994, when Maharashtra Weldaids Ltd merged with the company, bringing a manufacturing unit at Nagpur. Look at a map of India's industrial geography, and Nagpur's importance becomes clear—it's literally the center of India, equidistant from major metros, with rail connections radiating like spokes. For a company selling heavy industrial products where logistics costs matter, Nagpur was strategic gold.

By the late 1990s, ESAB India had assembled something unique: manufacturing facilities in Kolkata (East), Chennai (South), and Nagpur (Central), with Pune covering the West. This wasn't just geographic coverage; it was a hedge against regional disruptions, a logistics optimization play, and a statement to customers—wherever you are, we're nearby.

The product portfolio evolution during this period reads like a technical manual, but it tells a story of industrial sophistication. Welding consumables—the bread and butter—were now complemented by arc welding equipment, plasma cutting systems, and increasingly, automation solutions. Each product line addressed a different customer segment, from the small fabrication shop using basic electrodes to the shipyard requiring sophisticated submerged arc welding systems.

But here's what the financial statements don't capture: ESAB India was building an ecosystem, not just a business. They established training centers where welders could learn new techniques. They created certification programs that became industry standards. When a young welder in Coimbatore got ESAB-certified, it meant better job prospects. When a fabrication shop in Ludhiana bought ESAB equipment, it came with training, support, and a path to upgrade.

The distribution network that emerged during this period was perhaps ESAB India's most underappreciated asset. In a country where the last-mile problem defeats even Amazon, ESAB built a network of dealers and distributors that could deliver welding rods to a construction site in Assam or a replacement part to a factory in Rajasthan. This wasn't just logistics; it was a trust network, built relationship by relationship.

The early 2000s brought new challenges and opportunities. India's entry into the WTO meant more competition from imports, but also access to global supply chains. The IT boom was creating a new India, but manufacturing still mattered—in fact, it mattered more as India aspired to become the world's factory. ESAB India positioned itself as the arms dealer to this manufacturing ambition.

Product innovation during this period focused on localization with a twist. Yes, they adapted global products for Indian conditions—welding equipment that could handle voltage fluctuations, consumables designed for the specific metallurgy of Indian steel. But they also began innovating for India. Products designed for the unique requirements of Indian Railways, solutions for the specific challenges of monsoon-season construction.

The subsidiary relationship with the global ESAB organization, ultimately owned by Colfax Corporation since 2012, brought technology transfer that was transformative. Suddenly, Indian customers had access to the same welding technology being used to build offshore platforms in the North Sea or aerospace components in Seattle. But more importantly, Indian engineers were contributing to global R&D, creating solutions that would be deployed worldwide.

By 2012, ESAB India had transformed from an acquirer of distressed assets into India's welding powerhouse. Revenue was climbing, margins were expanding, and the company had achieved something rare in Indian manufacturing: they were simultaneously the premium choice and the value option, depending on the product line. They could sell high-end automated welding systems to Larsen & Toubro while also supplying basic electrodes to small fabrication shops. This barbell strategy—premium and volume—would define their market approach.

V. The Colfax Era & Global Integration (2012-2022)

When Colfax Corporation completed its acquisition of Charter International in January 2012, ESAB India found itself with new corporate parents who viewed the world through a different lens. The Rales brothers' Colfax wasn't just another industrial holding company—it was a laboratory for operational transformation, armed with the Colfax Business System (CBS), their proprietary operating philosophy that married lean manufacturing with aggressive growth through acquisition.

For ESAB India, this meant a fundamental shift in how business was conducted. CBS wasn't just another corporate initiative with PowerPoints and consultants. It was a complete rewiring of operations, from shop floor to boardroom. Indian managers who had run their divisions like fiefdoms suddenly found themselves in daily huddles, tracking metrics they'd never measured, questioning processes they'd never examined.

The integration was fascinating to watch. Here was an American company imposing a Japanese-inspired management system on a Swedish company's Indian subsidiary. The cultural translation required was immense. But something unexpected happened: the Indian operations didn't just adapt CBS; they enhanced it with their own innovations. The concept of "jugaad"—frugal innovation—merged with CBS's continuous improvement philosophy to create something uniquely powerful. From 2012 to 2019 the company completed more than 25 acquisitions including Victor Technologies, WestArco, Soldexa, TBi Industries, EWAC, Thermal Dynamics, and GCE. This acquisition frenzy wasn't random; it was strategic portfolio completion. Victor Technologies brought gas equipment leadership. Thermal Dynamics added plasma cutting expertise. Each piece filled a gap, expanded geographic reach, or deepened technological capabilities.

For ESAB India, being part of this global M&A machine meant access to technology and products that would have taken decades to develop independently. When a customer in Gujarat needed specialized aluminum welding solutions for the emerging solar panel industry, ESAB India could tap into technology from recent acquisitions. When Indian shipyards required advanced automation for competitiveness, solutions from European acquisitions could be adapted and deployed.

The technology transfer during this period was transformative. It wasn't just about importing products; it was about localizing global innovations for Indian conditions. The engineering teams in Chennai and Kolkata weren't just assembling foreign designs—they were adapting them for India's unique challenges: extreme temperature variations, inconsistent power quality, and the need for equipment that could handle everything from precision aerospace work to rough field repairs.

The market expansion during the Colfax era was equally impressive. ESAB India's products began appearing in sectors that barely existed a decade earlier. Wind energy—India was becoming a global player, and every wind turbine needed specialized welding for tower construction and nacelle assembly. The petrochemical boom along Gujarat's coast created demand for high-specification welding consumables that could meet international standards. Pipeline projects crossing thousands of kilometers required not just products but complete solutions—equipment, consumables, training, and support.

What made this period remarkable was how ESAB India maintained its local identity while becoming more global. The company understood that in India, business is personal. While implementing CBS's data-driven approach, they never lost sight of the importance of relationships. The salesperson who had been calling on a customer for twenty years wasn't replaced by a CRM system; instead, the CRM system was built around preserving and enhancing those relationships.

The financial performance during this period validated the strategy. Margins expanded as operational improvements took hold. Working capital management improved dramatically—a critical factor in India where payment cycles can stretch for months. The company learned to balance the demands of a publicly-traded American parent with the realities of doing business in India, where a handshake still matters more than a contract.

Training and skill development became a cornerstone of ESAB India's market strategy during this period. They established the ESAB India Technical Centre, not just as a training facility but as a center of excellence. Young welders from ITIs (Industrial Training Institutes) across India would come for advanced training, returning to their regions as ambassadors for ESAB products and techniques. This wasn't corporate social responsibility; it was market development at its most fundamental level.

The distribution network evolution during the Colfax era deserves special attention. ESAB India moved from a traditional dealer model to what they called "channel partners"—dealers who weren't just resellers but extensions of ESAB's technical support network. These partners received extensive training, marketing support, and crucially, protection—ESAB wouldn't undercut them by selling directly to their customers. This trust-based approach created fierce loyalty in a market where brand-switching is common.

By 2022, when Colfax spun off ESAB as an independent company, ESAB India had been transformed. It was no longer just the Indian subsidiary of a global welding company; it was a critical node in ESAB's global network, contributing not just revenue but innovation and market insights that would shape global product development. The Indian operations had proven that emerging markets weren't just places to sell simplified versions of developed-market products—they were laboratories for frugal innovation that could benefit the entire organization.

VI. Product Portfolio & Market Position

Walk into any major industrial facility in India—from the shipyards of Cochin to the automobile plants of Gurgaon—and you'll find ESAB products doing the heavy lifting of joining metal. But understanding ESAB India's product portfolio requires more than cataloging equipment; it's about comprehending how each product line represents a strategic choice about where and how to compete.

The company's products include welding consumables, arc welding equipment, plasma, cutting automation, gas equipment, welding automation & robotics, digital solutions, and PPE & accessories. This isn't just a product list; it's a value chain strategy. Welding consumables—the electrodes, wires, and fluxes that are consumed in the welding process—are the razor blades of this business. Customers might deliberate for months before buying welding equipment, but consumables are purchased continuously, creating predictable, recurring revenue streams.

The genius of ESAB India's product strategy lies in how they've structured their portfolio to capture value at every point of the customer journey. A small fabrication shop might start with basic electrodes, move up to a simple welding machine, then gradually adopt more sophisticated equipment as their business grows. At each step, ESAB has a product waiting, and more importantly, a relationship already established.

The brand portfolio tells its own story of strategic accumulation. Products are sold under an alphabet soup of names: AlcoTech, AMI, Arcair, Conarco, Exaton, Gasarc, Losarc, Soldexa, Stoody, Thermal Dynamics, Turbotorch, Tweco, Victor, West Arco, Ewac, Cigweld, Condor, InduSuite, Firepower, GCE, Octopue, and TBi Industries. Each brand carries its own heritage, customer loyalty, and market position. Rather than forcing everything under the ESAB umbrella, the company has maintained these identities, understanding that in B2B markets, trust is built over decades and shouldn't be casually discarded.

The consumables business deserves special attention because it's the cash cow that funds everything else. In welding, the consumable must match the base metal, the welding process, and the application requirements. This creates thousands of SKUs and significant barriers to entry—a new competitor can't just offer a few products and compete effectively. ESAB India's consumables range from basic mild steel electrodes selling for a few rupees to specialized alloy wires for aerospace applications costing thousands per kilogram.

Arc welding equipment represents the installed base strategy. Once a customer buys an ESAB welding machine, they're likely to buy ESAB consumables, spare parts, and eventually, replacement equipment. The equipment range spans from simple stick welding machines that cost less than a smartphone to sophisticated multi-process inverters that can automatically adjust parameters based on joint configuration.

The plasma cutting business showcases ESAB India's ability to ride technology transitions. As Indian industry moved from oxy-fuel cutting to plasma, ESAB was there with solutions ranging from hand-held plasma cutters for small workshops to CNC plasma tables for large fabrication facilities. They didn't just sell equipment; they sold productivity—showing customers how plasma could cut faster, cleaner, and ultimately cheaper than traditional methods.

Cutting automation represents the future that's already here for progressive Indian manufacturers. ESAB's automation solutions aren't just about replacing human welders—in India, where labor is still relatively affordable, that's not always the value proposition. Instead, automation is sold on consistency, quality, and the ability to handle applications that are dangerous or impossible for human welders.

Gas equipment might seem like a commodity business, but ESAB has turned it into a differentiation tool. Through brands like Victor, they offer everything from basic regulators to sophisticated gas control systems. In a market where gas purity and flow control can make the difference between a good weld and a failed one, this equipment becomes mission-critical.

The welding automation and robotics segment reveals ESAB India's dual strategy: serving both the cutting edge and the mainstream. For automotive manufacturers requiring consistent, high-speed welding, they offer fully automated robotic cells. For smaller manufacturers taking their first steps toward automation, they provide simple mechanized solutions that can be operated by existing workers with minimal training.

Digital solutions represent ESAB's newest frontier. Products like InduSuite and WeldCloud aren't just software; they're ESAB's attempt to own the data layer of welding operations. By helping customers track welding parameters, consumable usage, and quality metrics, ESAB embeds itself deeper into customer operations, making switching costs prohibitive.

The PPE and accessories business might seem like an afterthought, but it's strategic. Safety regulations in India are tightening, and ESAB positions itself as a complete safety partner, not just an equipment supplier. When a company buys welding helmets, gloves, and safety equipment from ESAB, it deepens the relationship and increases wallet share.

The market segmentation strategy is equally sophisticated. ESAB India serves wind energy, petrochemical, pipeline, LNG, repair and maintenance, mobile machinery, and shipbuilding industries, but each is approached differently. Wind energy customers need specialized consumables for welding thick sections and meeting fatigue requirements. Shipbuilders need high deposition rate processes and position welding capabilities. Pipeline contractors need field-ready equipment that can handle harsh conditions.

Export markets have become increasingly important, with ESAB India leveraging cost advantages and growing quality reputation to serve international markets. But this isn't just about labor arbitrage; Indian engineers have developed specific expertise in areas like welding in high-temperature conditions and working with locally-sourced steel grades that have global applications.

The competitive positioning is nuanced. Against local competitors, ESAB India plays the technology and quality card. Against international competitors, they emphasize local presence, service, and cost-effectiveness. They've managed to occupy the sweet spot—premium enough to command price premiums, accessible enough to compete for volume business.

VII. Financial Performance & Value Creation

The numbers tell a story that would make any investor lean forward: Company is almost debt free. Company has delivered good profit growth of 19.7% CAGR over last 5 years. But the real story isn't in the headline numbers—it's in understanding how a company selling industrial commodities in a competitive market achieved returns that would embarrass software companies.

Let's start with the jaw-dropping return metrics. A Return on Capital Employed (ROCE) of 70% and Return on Equity (ROE) of 52.3% aren't typos. These are the kinds of returns typically associated with asset-light, high-margin businesses like luxury brands or software companies, not industrial manufacturers. How does a company that makes welding rods achieve returns that Warren Buffett would envy?

The answer lies in a business model that's been refined over decades. ESAB India has engineered a beautiful balance between asset intensity and operational leverage. The manufacturing facilities in Kolkata, Chennai, and Nagpur aren't gleaming showcases of automation; they're functional, efficient, and critically, largely depreciated. The company has resisted the temptation to over-invest in manufacturing capacity, understanding that in their business, distribution and service matter more than production scale.

The working capital management deserves a Harvard case study. In Indian B2B markets, where payment terms can stretch to 90-120 days and inventory needs to be maintained across thousands of SKUs, working capital can become a black hole. ESAB India has turned this challenge into a competitive advantage. They've structured payment terms with suppliers and customers that essentially make their vendors finance their growth. The cash conversion cycle has been optimized to the point where growth actually generates cash rather than consuming it.

The gross profit margin of 40.1% reveals the pricing power hidden in apparent commodities. Welding consumables might seem like undifferentiated products, but ESAB has created differentiation through certification, consistency, and availability. When a critical welding job needs to meet international standards, customers don't haggle over the price of electrodes—they pay for certainty.

The progression from gross margin to operating margin—from 40.1% to 16.2%—tells us about the cost of maintaining market leadership. That 24 percentage point difference isn't waste; it's investment in the distribution network, technical support, training programs, and brand building that creates the moat. The operating profit margin of 16.2% is healthy but not excessive, suggesting the company invests appropriately in maintaining its competitive position.

The net profit margin of 12% is where financial engineering meets operational excellence. With minimal debt, ESAB India doesn't leak value through interest payments. The tax efficiency achieved through manufacturing operations and export incentives further preserves shareholder value. This is a company that has optimized every line of the P&L statement.

The dividend policy reveals management's confidence and shareholder orientation. With a payout ratio exceeding 80%, ESAB India essentially functions as a cash machine for shareholders. This isn't a company hoarding cash for undefined future opportunities; it's returning capital to owners while maintaining enough retention for organic growth.

The capital allocation framework is elegantly simple. Organic growth requires minimal capital—new products can be launched using existing infrastructure, new markets can be entered through the existing distribution network. The occasional acquisition is funded through internal accruals. There's no grand capital expenditure program, no massive R&D budget, no transformation initiative requiring billions. Just steady, profitable growth funded by operations.

The stock performance reflects this financial excellence but also reveals market skepticism. Trading at 22.1 times book value suggests the market recognizes the quality of the business. However, the current valuation showing the company is overvalued by 41% compared to intrinsic value suggests investors are pricing in either slower growth or margin pressure going forward.

The revenue evolution from ₹1,373 crore tells a story of steady expansion rather than explosive growth. This isn't a company chasing revenue at any cost; it's one that grows in line with industrial demand while maintaining pricing discipline. The revenue per employee metrics would reveal how productivity improvements have driven margin expansion even as labor costs have increased.

The financial resilience was tested during COVID-19, and ESAB India passed with flying colors. While many industrial companies saw demand evaporate and working capital balloon, ESAB's diverse end-market exposure and variable cost structure allowed it to navigate the crisis while maintaining profitability. The quick recovery post-pandemic demonstrated the essential nature of their products—when construction and manufacturing resumed, welding consumables were needed immediately.

The currency dynamics add another layer of complexity. With imported raw materials and export sales, ESAB India navigates currency fluctuations that could devastate a less sophisticated operator. Their natural hedging through import-export balance and operational flexibility in pricing has minimized currency impact on margins.

Looking at segment performance, the domestic market contributes the majority of revenue, but exports provide higher margins and currency diversification. The balance between serving price-sensitive domestic customers and quality-focused export markets has been carefully calibrated to optimize overall returns.

The cash flow characteristics deserve special mention. This is a business where customer advances for large projects provide working capital, where suppliers extend credit based on long-term relationships, and where the cash flows are predictable enough to run with minimal cash buffers. The result is a capital-efficient machine that generates cash returns far exceeding accounting profits.

VIII. Current Ownership & Corporate Structure

The ownership structure of ESAB India reads like a masterclass in maintaining control while accessing public markets. It is a subsidiary of ESAB Group which was ultimately owned by the Colfax Corporation of USA, though this has since changed with the 2022 spin-off. Today, ESAB Corporation holds 73.72% of equity shares through a carefully constructed ownership cascade: ESAB Holdings Limited, UK and Exelvia Group India BV, Netherlands, both indirect wholly-owned subsidiaries of ESAB Corporation, which is now independently listed on the New York Stock Exchange.

This byzantine structure isn't corporate gymnastics for its own sake—it's tax efficiency meets regulatory compliance meets strategic flexibility. The use of Netherlands and UK holding companies provides treaty benefits, the Indian listing provides local currency access and regulatory legitimacy, and the 73.72% ownership ensures complete control while leaving enough float for liquidity.

The 26.28% public shareholding creates an interesting dynamic. These minority shareholders include some of India's most sophisticated institutional investors, high-net-worth individuals who understand industrial businesses, and retail investors attracted by the dividend yield. This diverse shareholder base provides market feedback through stock price movements while having no real influence on strategic decisions.

The governance structure reflects this ownership reality. The board composition carefully balances independent directors required by Indian regulations with nominees representing ESAB Corporation's interests. The independent directors aren't mere compliance checkboxes—they bring deep understanding of Indian industrial markets, regulatory expertise, and local relationships that help navigate the complexities of doing business in India.

The management structure reveals how global companies can successfully operate in India. The senior leadership team combines expatriate executives who ensure alignment with global ESAB strategy and Indian managers who understand local market dynamics. This isn't the revolving door of expat assignments seen at many multinationals; these are long-term positions with executives who have spent years understanding India's unique business environment.

The reporting lines create productive tension. The India CEO reports both to the ESAB Asia-Pacific regional head and has direct access to global leadership. This dual reporting ensures India isn't lost in regional aggregation while maintaining integration with global operations. The functional heads—finance, operations, sales—have similar dual reporting structures that ensure best practice transfer while maintaining local autonomy.

The related party transactions reveal the interconnected nature of global operations. ESAB India sources specialized raw materials from global ESAB entities, sells products to other ESAB subsidiaries for their local markets, and pays royalties for technology and brand usage. These transactions, while creating complexity, also demonstrate the value of being part of a global network.

The dividend policy mechanics are particularly interesting. With the parent holding 73.72%, the majority of dividends flow back to ESAB Corporation. This creates a efficient cash repatriation mechanism that avoids the complexity of other transfer methods. The high dividend payout ratio makes sense when viewed through this lens—it's not just returning cash to shareholders; it's funding global operations.

The compliance framework straddles multiple worlds. ESAB India must satisfy Indian securities regulations, including quarterly reporting, related party transaction approvals, and corporate governance norms. Simultaneously, as part of a NYSE-listed company, they're subject to Sarbanes-Oxley requirements, FCPA compliance, and global ESAB policies. This dual compliance burden creates costs but also ensures institutional-quality governance.

The subsidiary ecosystem within India includes various step-down subsidiaries and joint ventures that serve specific purposes—manufacturing units organized as separate entities for regulatory benefits, distribution subsidiaries for tax optimization, and service entities for specialized operations. This structure, while complex, provides flexibility in operations and tax planning.

The capital structure simplicity—almost no debt, no complex instruments, no preference shares—stands in contrast to the organizational complexity. This is deliberate. Financial engineering happens at the parent level if needed; the operating subsidiary maintains a clean, simple capital structure that minimizes financial risk and maximizes operational flexibility.

The alignment mechanisms ensure that India management's interests align with global shareholders. Performance bonuses tied to both local and global metrics, stock options in ESAB Corporation for senior executives, and long-term incentive plans that vest based on multi-year performance create appropriate incentives without the complexity of local equity participation.

The regulatory relationships matter more than org charts suggest. ESAB India's standing with the Ministry of Commerce, relationships with industry bodies like the Confederation of Indian Industry (CII), and engagement with technical standard organizations create soft power that transcends formal corporate structure. The company's ability to influence welding standards, participate in policy formation, and shape industry development provides strategic value beyond financial returns.

The information architecture supporting this structure is sophisticated. ERP systems that provide real-time visibility to global management, standardized reporting that allows benchmarking across countries, and audit mechanisms that ensure compliance—these systems represent millions in investment but enable the delicate balance of control and autonomy.

IX. Playbook: Business & Investing Lessons

The ESAB India story isn't just corporate history—it's a masterclass in strategy execution that offers lessons far beyond welding. Each strategic decision, when examined closely, reveals principles that apply across industries and markets.

The Consolidation Playbook: Roll-up Done Right

Most roll-ups fail. They overpay for acquisitions, struggle with integration, and destroy value through complexity. ESAB India's approach from 1988 to 1994 shows how to do it right. They didn't buy companies; they bought market positions, customer relationships, and manufacturing capabilities at distressed valuations. The integration wasn't about synergy capture through headcount reduction—it was about network effects through combined distribution and product range.

The lesson for investors: Look for roll-ups that buy orphaned assets from larger companies rather than competing with private equity for standalone businesses. The former provides better valuations and easier integration; the latter creates bidding wars and cultural clashes.

Technology Transfer and Localization: The Goldilocks Approach

ESAB India found the sweet spot between over-localization (losing global product advantages) and under-localization (offering products unsuited for local markets). They maintained global quality standards while adapting products for Indian conditions—welding rods that could handle the specific metallurgy of Indian steel, equipment that could tolerate voltage fluctuations, and service models that worked with Indian payment terms.

The deeper insight: Technology transfer isn't about moving products from developed to developing markets. It's about creating bi-directional innovation flows where emerging market constraints drive frugal innovations that have global applications. ESAB India's solutions for welding in extreme heat or with inconsistent power supply have applications far beyond India.

Managing Through Ownership Changes: The Permanent Beta Principle

From Swedish ownership to Charter International to Colfax to independence—ESAB India navigated multiple ownership changes while maintaining operational excellence. How? By treating ownership as a variable, not a constant. The local management focused on building capabilities that would be valuable regardless of ownership: market position, customer relationships, operational efficiency.

This teaches a crucial lesson: In businesses subject to ownership changes, invest in capabilities that transcend ownership. Distribution networks, customer relationships, and local market knowledge retain value regardless of who owns the equity.

Capital Allocation in Capital-Light Models: The Compound Effect

ESAB India's capital allocation seems boring—no massive capex programs, no transformational acquisitions, no financial engineering. But this simplicity is its genius. By maintaining capital discipline, the company compounds returns through operational improvement rather than financial leverage. The 19.7% profit CAGR over five years wasn't achieved through one big bet but through thousands of small improvements.

The investor takeaway: In mature industries, boring capital allocation often beats bold moves. Companies that resist the temptation to transform and instead focus on continuous improvement can generate exceptional returns with minimal risk.

Building Moats Through Distribution: The Last Mile Advantage

ESAB India's true moat isn't technology or manufacturing—it's the distribution network that can deliver welding consumables to a construction site in Assam or a replacement part to a factory in Rajasthan within days. This network, built over decades through relationships and trust, can't be replicated with capital alone.

The strategic insight: In B2B markets, distribution is often more valuable than production. Investors should value companies that control distribution channels higher than those that merely manufacture products, especially in markets where logistics infrastructure is challenging.

The Barbell Strategy: Premium and Volume

ESAB India simultaneously serves sophisticated customers buying high-end automation and price-sensitive customers buying basic consumables. This isn't strategy confusion—it's portfolio optimization. The premium products provide margin and technology showcase; the volume products provide scale and market presence. Together, they create a full-spectrum dominance that's hard to attack.

For investors, this suggests looking for companies that can credibly serve multiple market segments without brand dilution. The key is having separate value propositions for each segment rather than trying to be everything to everyone.

Why Industry Leaders Matter in B2B Markets

Unlike consumer markets where challengers can disrupt through marketing or innovation, B2B industrial markets favor incumbents. Why? Because switching costs aren't just financial—they're operational. Changing welding consumable suppliers means requalifying processes, retraining workers, and risking production quality. ESAB India has weaponized these switching costs through certification programs, training centers, and technical support that embed them in customer operations.

The lesson: In B2B industrial markets, market share is sticky. Leaders tend to stay leaders unless they badly misexecute. For investors, this means paying premium valuations for market leaders can be justified if the leadership position is entrenched.

The Services Layer Strategy

ESAB India doesn't just sell products; they sell outcomes. Training programs, certification services, application engineering support—these services create revenue streams beyond product sales while increasing switching costs. A customer might be willing to switch welding rod suppliers, but they're less likely to switch if it means losing access to training programs their workers depend on.

The broader principle: Industrial companies that layer services on products create more resilient business models. The services provide recurring revenue, deepen customer relationships, and create differentiation in commoditized markets.

Local Execution, Global Standards

ESAB India operates with Swedish quality standards, American management systems, and Indian market sensibilities. This hybrid approach—global standards with local execution—provides the best of both worlds. Quality and consistency that international customers demand, with the flexibility and relationships that Indian business requires.

The investment implication: Look for companies that have successfully adapted global best practices to local conditions rather than those that simply transplant foreign models or remain purely local. The hybrid approach creates competitive advantages that pure-play local or global companies can't match.

X. Analysis & Investment Case

The investment case for ESAB India requires peeling back layers of industrial complexity to reveal fundamental truths about value creation in emerging markets. This isn't a simple growth story or a value play—it's something more nuanced and potentially more rewarding.

Competitive Positioning: The Incumbent's Advantage

ESAB India faces competition from three directions: local players like Ador Welding and Advani Oerlikon, international competitors trying to enter India, and Chinese imports competing on price. Against each, ESAB has distinct advantages. Local competitors lack the technology breadth and global R&D access. International entrants face the chicken-and-egg problem of building distribution without volume and achieving volume without distribution. Chinese imports compete on price but can't match ESAB's service, certification support, and quality consistency for critical applications.

The competitive moat is widening, not narrowing. As Indian manufacturing becomes more sophisticated, moving from simple fabrication to precision work for global supply chains, quality and certification matter more. ESAB's ability to provide welding procedures that meet international standards becomes increasingly valuable.

India's Infrastructure and Manufacturing Growth Story

The macro tailwinds are powerful. India needs $1.4 trillion in infrastructure investment over the next five years. Every bridge, pipeline, power plant, and factory requires welding. But this isn't just about volume—it's about sophistication. India's infrastructure ambitions require welding technology that can handle high-strength steels, exotic alloys, and extreme conditions.

The manufacturing renaissance adds another dimension. As companies diversify supply chains away from China, India emerges as an alternative. But manufacturing for global markets requires meeting international quality standards, and this is where ESAB's global certification and process knowledge becomes invaluable. They're not just selling welding products; they're enabling India's manufacturing ambitions.

The Valuation Conundrum

The current valuation showing company is overvalued by 41% compared to intrinsic value creates an interesting tension. The market is pricing ESAB India like a mature industrial company with limited growth prospects. But is this accurate?

The bear case has merit: GDP growth is slowing, industrial capex cycles are volatile, and competition from imports is intensifying. The 22.1 times book value multiple suggests the market has already priced in significant growth. With ROE at 52.3%, sustaining these returns as the business scales will be challenging.

But the bull case is compelling: India's infrastructure deficit ensures decades of demand, import substitution policies favor local manufacturing, and ESAB's technology leadership becomes more valuable as specifications tighten. The company's ability to generate 70% ROCE suggests significant runway before returns normalize.

Critical Success Factors Going Forward

Several factors will determine whether ESAB India justifies its premium valuation or faces a correction:

Technology Transition Management: As welding moves toward automation and digitalization, ESAB must balance serving traditional customers while preparing for the future. The risk isn't just technological obsolescence—it's moving too fast and alienating the core customer base that still uses manual welding.

Supply Chain Resilience: With global supply chains under stress, ESAB's ability to maintain product availability while managing costs becomes critical. Their mix of local manufacturing and strategic imports provides flexibility, but executing this balance during disruptions will test operational capabilities.

Talent Development: The welding industry faces a skilled worker shortage globally. ESAB India's training programs aren't just corporate social responsibility—they're creating the ecosystem that ensures future demand for their products. The company that trains the most welders will sell the most welding equipment.

Regulatory Navigation: India's regulatory environment is improving but remains complex. Changes in import duties, safety regulations, or environmental standards could significantly impact business models. ESAB's relationships and local presence provide early warning and influence, but regulatory surprises remain a risk.

The ESG Angle

Environmental, Social, and Governance factors are becoming increasingly important for Indian companies. ESAB India's position here is nuanced. Welding is energy-intensive and produces emissions, but it's also essential for renewable energy infrastructure. The company's training programs have significant social impact, creating skilled employment opportunities. Governance, backed by NYSE-listed parent standards, is institutional quality.

The ESG opportunity lies in positioning ESAB India as an enabler of India's energy transition. Every wind turbine, solar panel mount, and electric vehicle requires welding. By developing products and processes that reduce energy consumption and emissions in welding while enabling green infrastructure, ESAB can align with ESG mandates while driving growth.

Scenario Analysis

In the optimistic scenario, India achieves 8% GDP growth, infrastructure spending accelerates, and manufacturing exports boom. ESAB India rides these trends to 15% revenue growth and margin expansion through operating leverage. The stock re-rates to reflect this growth, delivering 20%+ annual returns.

In the base case, India grows at 6-7%, infrastructure spending continues but at a measured pace, and manufacturing gradually gains share. ESAB India grows in line with industrial production, maintains margins through efficiency improvements, and delivers returns in line with ROE through dividends and modest appreciation.

In the pessimistic scenario, global recession impacts India, infrastructure spending slows, and manufacturing struggles with competition. ESAB India's revenue stagnates, margins compress from competition, and the stock corrects to reflect slower growth prospects. However, even in this scenario, the strong balance sheet and cash generation provide downside protection.

The Investment Decision Framework

For long-term fundamental investors, ESAB India presents a classic quality-at-a-price dilemma. The business quality is undeniable—market leadership, strong returns, excellent capital allocation. But the price reflects these qualities and possibly more.

The decision hinges on your view of India's industrial future. If you believe India will successfully execute its infrastructure and manufacturing ambitions, ESAB India provides leveraged exposure to this theme with lower risk than pure-play infrastructure or manufacturing companies. If you're skeptical about India's execution capabilities or worried about global industrial cycles, the current valuation offers limited margin of safety.

XI. Epilogue & Future Outlook

As we stand at the intersection of India's industrial past and digital future, ESAB India occupies a fascinating position. This is a company selling 120-year-old technology—joining two pieces of metal—yet preparing for a future where every weld is data-tagged, AI-optimized, and robotically executed.

Digital Transformation and Industry 4.0: The Next S-Curve

The welding industry is undergoing its own digital revolution, though it's less visible than consumer-facing transformations. ESAB's WeldCloud platform represents the beginning of welding's evolution from craft to data science. Imagine every welding machine as an IoT device, streaming data about parameters, consumable usage, and quality metrics. This data, properly analyzed, can predict failures, optimize parameters, and reduce costs.

For ESAB India, this digital transformation presents both opportunity and challenge. The opportunity lies in moving up the value chain from product supplier to solution provider, charging not just for consumables but for productivity improvements. The challenge is that Indian customers, particularly smaller ones, may be slower to adopt digital solutions than global peers.

The company's approach has been pragmatic—offering digital solutions for sophisticated customers while maintaining traditional products for the mass market. This dual-track strategy prevents alienating current customers while building capabilities for the future.

ESG Initiatives: From Compliance to Competitive Advantage

ESAB India's ESG journey reflects the broader evolution of Indian industry. What started as compliance with environmental regulations has evolved into strategic differentiation. The company's focus on developing welding processes that reduce energy consumption and emissions positions them well for increasingly environmentally conscious customers.

The social impact through skill development is particularly noteworthy. India faces a massive skill gap in manufacturing, and ESAB's training programs directly address this challenge. By creating certified welders, they're not just developing customers—they're building human infrastructure essential for India's industrial growth.

Governance improvements, driven by global ESAB standards and Indian regulatory requirements, have created institutional-quality oversight that differentiates ESAB India from local competitors. This governance premium becomes increasingly valuable as institutional investors grow their presence in Indian markets.

India's Manufacturing Renaissance: Riding the Megatrend

The "Make in India" initiative, supply chain diversification from China, and the Production Linked Incentive (PLI) schemes are creating a manufacturing opportunity that could define India's next decade. ESAB India is positioned to benefit regardless of which sectors lead this growth—electronics need precision welding, automobiles need automated welding, defense needs specialized alloys, and infrastructure needs volume welding.

The key insight is that ESAB India is a derivative play on manufacturing growth with lower execution risk. They don't need to predict which sectors will succeed or which companies will win. They just need manufacturing activity to increase, and welding demand follows.

Key Metrics to Watch

For investors monitoring ESAB India, several metrics beyond traditional financials warrant attention:

Market Share Trends: In a consolidating market, relative performance matters more than absolute growth. Watch for share gains in strategic segments like renewable energy and automation.

Training Program Enrollment: The number of welders trained is a leading indicator of future consumable demand and ecosystem health.

Digital Solution Adoption: Revenue from digital services and percentage of connected equipment indicate success in transformation.

Import Substitution Progress: The percentage of revenue from products previously imported shows success in localization and value addition.

Working Capital Efficiency: In an inflationary environment with supply chain stress, maintaining working capital efficiency indicates operational excellence.

Final Reflections: The Boring Business That Isn't

ESAB India challenges conventional investment wisdom. It's an industrial company with software-like returns, a mature business with growth characteristics, a subsidiary with entrepreneurial culture. It's simultaneously boring—making welding rods—and exciting—enabling India's industrial transformation.

The investment merit depends on time horizon and temperament. For traders seeking quick gains, the stock's steady appreciation and high dividend yield offer limited excitement. For long-term investors who understand that India's infrastructure and manufacturing ambitions will take decades to fulfill, ESAB India offers a way to participate with a proven operator rather than speculative bets.

The broader lesson from ESAB India's journey is that in emerging markets, the picks-and-shovels providers often generate better risk-adjusted returns than the gold miners. While others bet on which infrastructure projects will succeed or which manufacturers will thrive, ESAB India profits from the entire ecosystem's growth.

As India stands at the cusp of potentially its greatest industrial expansion, companies like ESAB India remind us that transformation doesn't always require transformation companies. Sometimes, the oldest businesses selling the most basic products—like joining two pieces of metal—create the foundation upon which modern economies are built.

The ESAB India story isn't finished. In fact, as India's industrial ambitions accelerate, the most interesting chapters may lie ahead. The company that helped build India's industrial past is positioning itself to enable India's manufacturing future. For investors willing to look beyond the mundane description of "welding consumables manufacturer," ESAB India offers a window into India's industrial soul—and potentially, exceptional returns for those patient enough to wait for the future to be welded together, one joint at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube