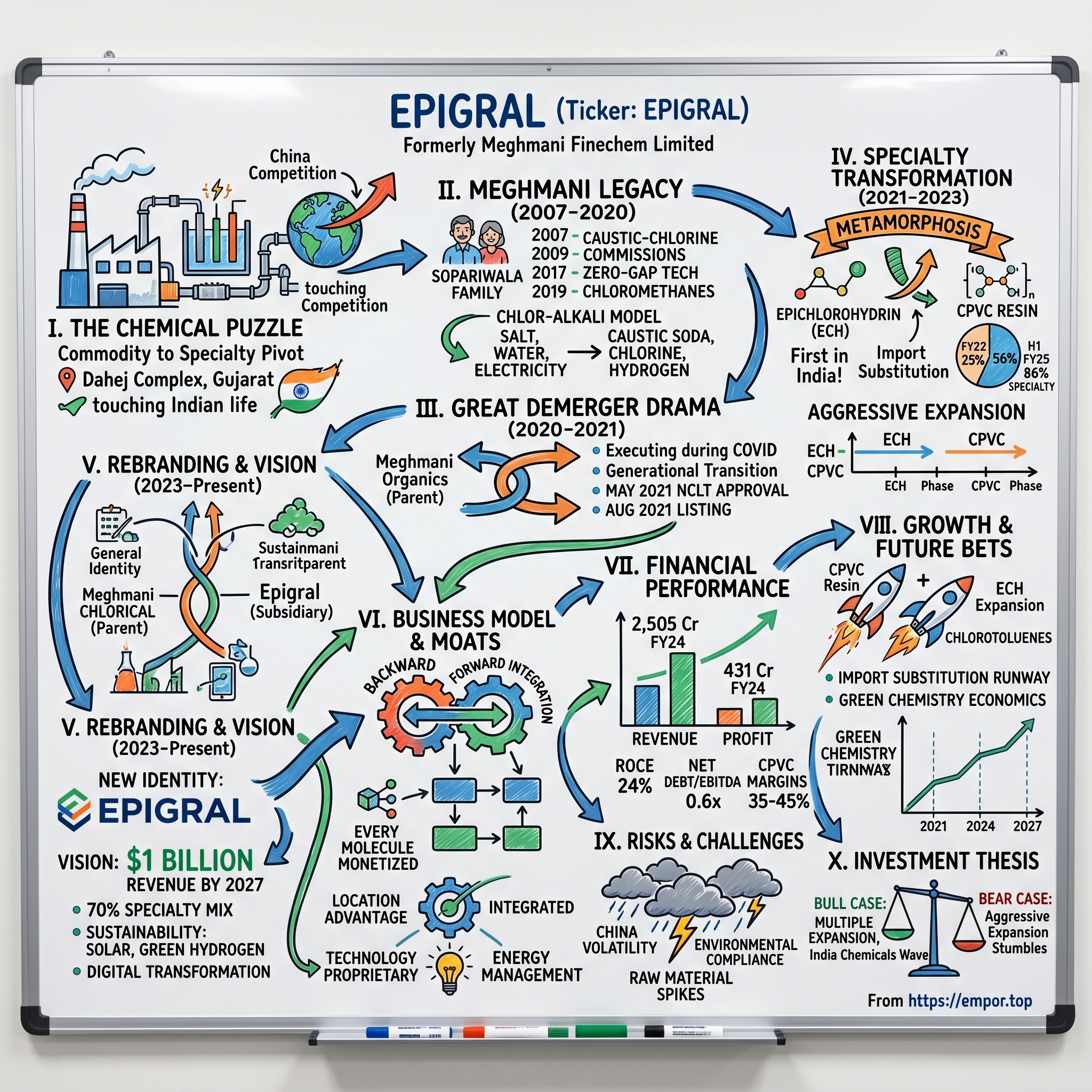

Epigral: From Chlor-Alkali Commodity to Specialty Chemical Champion

I. Introduction & The Chemical Puzzle

Picture this: In a sprawling 413-acre complex in Dahej, Gujarat, massive electrolytic cells hum with 130 megawatts of power, splitting salt and water into their elemental components. Steam billows from cooling towers while a maze of pipelines carries chlorine, caustic soda, and hydrogen through a carefully orchestrated chemical ballet. This is Epigral Limited—a company most investors have never heard of, yet one that touches nearly every aspect of modern Indian life through the PVC pipes in our homes, the paints on our walls, and the pharmaceuticals in our medicine cabinets.

The compelling question isn't just how a chemical company founded in 2007 as a subsidiary became an ₹8,000+ crore market cap specialty chemicals powerhouse. It's how they executed one of the most ambitious commodity-to-specialty pivots in Indian chemical history while their parent company was imploding, China was dumping products at predatory prices, and global supply chains were fracturing during COVID-19.Today's market tells us Epigral's market cap stands at ₹8,136 crore, but that number alone doesn't capture the audacity of what this company has pulled off. This is a story of how a second-generation promoter family took a commodity chemical subsidiary that was hemorrhaging cash, executed a complex demerger during a pandemic, and transformed it into India's largest CPVC resin manufacturer—all while competing against Chinese giants who control 80% of global capacity.

The real kicker? They're not just surviving the China competition; they're thriving. The company's product mix has shifted from 25% specialty chemicals in FY22 to 56% in H1 FY25—a transformation that typically takes chemical companies a decade to execute. They did it in three years.

This episode unpacks three interlocking puzzles: First, how does a company successfully demerge from a parent in distress without getting dragged down? Second, how do you build competitive advantage in chemicals when your primary competitor (China) has 20x your scale and government subsidies? And third, what does it really take to move from commodity chemicals—where you're a price taker—to specialty chemicals where you set the terms?

The answers lie in a combination of perfect timing, backward integration mastery, and what might be the most aggressive capacity expansion in Indian chemical history. But as we'll see, the story of Epigral isn't just about chemicals. It's about how Indian manufacturing is quietly building world-scale capabilities in sectors we've traditionally imported from, one electrolytic cell at a time.

II. The Meghmani Legacy & Chemical Roots (2007-2020)

The year is 2007. The global financial crisis hasn't hit yet. India's GDP is growing at 9%. And in the industrial corridors of Gujarat, the Sopariwala family—who'd built Meghmani Organics into a respected agrochemical and pigment manufacturer over 30 years—makes a decision that seems almost quaint by today's standards: they want to get into basic chemicals.

Meghmani Finechem Limited was incorporated in 2007 as a subsidiary of Meghmani Organics Limited. The parent company had been in chemicals since 1977, but this was different. While Meghmani Organics focused on complex organic chemistry—pesticides, pigments, and specialty intermediates—the new subsidiary would dive into the most basic of chemical processes: electrolyzing salt water.

Why chlor-alkali? To understand this, you need to grasp the beautiful simplicity of the business model. You take three ingredients—salt, water, and electricity—and through electrolysis, you get three products: caustic soda (used in everything from soap to aluminum), chlorine (for PVC, water treatment, pharmaceuticals), and hydrogen (increasingly valuable as a clean fuel). Every ton of caustic soda automatically produces 0.88 tons of chlorine and 0.025 tons of hydrogen. You can't make one without the others. It's chemistry's version of a three-for-one deal.

But here's what made the timing brilliant: India was massively short on chlor-alkali capacity. We were importing nearly 30% of our caustic soda needs, primarily from the Middle East where natural gas was cheap. The Sopariwalas saw an opportunity—if you could build efficient capacity in India, close to customers, you'd have a structural advantage over imports despite higher energy costs.

The initial setup was modest by today's standards but ambitious for 2007. They acquired 413 acres in Dahej, Gujarat—a location that would prove prescient. Dahej wasn't just another industrial area; it was emerging as India's chemical manufacturing hub, with dedicated pipelines, port facilities, and crucially, a stable power grid. For a business where electricity constitutes 60% of your operating costs, grid stability isn't a nice-to-have—it's existential.

Operations started in July 2009 as a greenfield project with 119,000 TPA of caustic-chlorine capacity and a 40MW captive power plant. The captive power plant was critical. In chlor-alkali, if your power goes down for even an hour, your entire cell room can be damaged, requiring weeks of repairs. By generating their own power, they controlled their destiny.

The early years were about learning the ropes. Chlor-alkali might be basic chemistry, but running it efficiently is an art. The efficiency of your electrolytic cells, measured in power consumption per ton of caustic, determines whether you make money or lose it. Global best practice was around 2,200 kWh per ton. Indian plants averaged 2,400-2,500 kWh. Meghmani Finechem started at 2,450 kWh—not world-class, but respectable.

By 2015, they had expanded caustic-chlorine capacity to 167,000 TPA with a 60MW captive power plant. But the real innovation came in 2017 when they converted all membrane cells to zero-gap technology. Zero-gap membranes reduce power consumption by 10-12% by minimizing the distance between electrodes. It's the kind of incremental innovation that sounds boring but drops straight to the bottom line when electricity is your biggest cost.

The transformation accelerated in 2018-2019. Rather than just selling basic caustic and chlorine, they began the classic chemical industry play: downstream integration. In 2019, they commissioned chloromethane production—taking their chlorine and methane to produce methylene dichloride, chloroform, and carbon tetrachloride. These weren't just higher-margin products; they were import substitution plays. India was importing 70% of its chloromethanes from China and Europe.

By 2020, on the eve of the demerger, Meghmani Finechem had built something substantial: 315,000 TPA of chlor-alkali capacity making it one of India's top 5 producers, a product portfolio spanning from basic caustic to value-added derivatives, and most importantly, the technical capability to compete with global players. Revenue had reached $95 million (₹609 crore) by 2018.

But beneath this operational success, storm clouds were gathering. The parent company, Meghmani Organics, was struggling with its agrochemical business. Global agrochemical prices were collapsing, China was dumping products, and environmental regulations were tightening. The chlor-alkali business was actually the bright spot in the portfolio—growing steadily, generating cash, and relatively insulated from the agrochemical downturn.

This set up one of the most interesting strategic questions in Indian corporate history: When your subsidiary is outperforming your parent, and the two businesses have minimal synergies, what do you do? The Sopariwala family's answer would reshape not just their fortune, but create a template for how Indian family businesses can successfully separate and scale different ventures. The stage was set for the great demerger drama of 2021.

III. The Great Demerger Drama (2020-2021)

March 2020. COVID-19 has just shut down India. Manufacturing plants are scrambling to figure out if they're "essential services." And in the Meghmani boardroom, the family is making one of the most consequential decisions in their corporate history: it's time to split the company in two.

The logic was compelling but the timing seemed insane. Meghmani Organics, the parent company, was bleeding. Their agrochemical business faced brutal Chinese competition, environmental compliance costs were skyrocketing, and working capital was stretched. Meanwhile, Meghmani Finechem—the chlor-alkali subsidiary—was generating steady cash flows and had ambitious expansion plans. Keeping them together was like yoking a racehorse to a dying ox.

The demerger wasn't just about financial engineering. It was about generational transition. The Sopariwala family had a classic succession challenge: multiple family members, different business interests, and the need to give each faction room to execute their vision without stepping on each other's toes. The chlor-alkali business would go to one part of the family, the agrochemicals and pigments to another. Clean, surgical, final.

But executing a demerger during COVID was like performing surgery during an earthquake. Courts were functioning virtually, regulatory approvals were delayed, and due diligence meetings happened over patchy Zoom calls. The NCLT (National Company Law Tribunal) process, which typically takes 6-8 months, stretched to nearly a year.

The demerger scheme was elegantly structured: Every Meghmani Organics shareholder would receive one share of Meghmani Finechem for every one share held. No cash changed hands, no premium paid—just a clean split. The beauty was in its simplicity. Shareholders who believed in the agrochemical story could hold Meghmani Organics. Those who preferred the chlor-alkali business could hold Meghmani Finechem. Those who wanted both could keep both.

May 7, 2021: NCLT finally approves the scheme. The appointed date was backdated to April 1, 2020, meaning an entire year of operations had to be retroactively separated. Imagine untangling a year's worth of inter-company transactions, shared services allocations, and working capital movements—all while running a 24/7 chemical plant.

The company was formerly known as Meghmani Finechem Limited and changed its name to Epigral Limited in August 2023. Epigral Limited was incorporated in 2007 and is based in Ahmedabad, India. But before the rebrand came the crucial listing.

August 18, 2021: Meghmani Finechem lists on NSE and BSE as an independent entity. The opening price: ₹615. The market cap: roughly ₹2,800 crore. For a company with ₹1,000 crore in revenues, it wasn't a blockbuster debut, but it was solid. More importantly, it gave the company its own currency for growth—access to capital markets without being tethered to the parent's problems.

The shareholding pattern post-demerger revealed the family's confidence: Promoter holding stood at 68.8%. This wasn't a company being dressed up for sale. The family was betting their wealth on this business. They weren't selling; they were building.

What happened next validated the demerger thesis. Freed from the parent company's constraints, Meghmani Finechem could focus on its own capital allocation. No more subsidizing the agrochemical business's working capital needs. No more board debates about whether to invest in pesticides or caustic soda. Every rupee generated could be reinvested in chlor-alkali and derivatives.

The management structure also got a refresh. While the older generation remained as advisors, operational control shifted to the younger generation—professionals who'd grown up in the business but also had global exposure. They brought in outside talent for key positions: a CFO from a Big Four background, a head of manufacturing from Reliance, a strategy chief from McKinsey. This wasn't your typical promoter-driven setup anymore.

The timing, which seemed terrible in March 2020, proved brilliant by August 2021. Chemical stocks were on fire. China was shutting down polluting plants, global supply chains were disrupted, and India was emerging as the alternative manufacturing hub. The "China Plus One" strategy every multinational talked about was becoming reality. And Meghmani Finechem—soon to be Epigral—was perfectly positioned to capture this shift.

But the real masterstroke was what they did with their newfound independence. While investors expected steady, boring growth from a chlor-alkali producer, the company had other plans. They were about to embark on one of the most aggressive specialty chemical expansions in Indian history, starting with a product most people couldn't even pronounce: Epichlorohydrin.

IV. The Specialty Chemical Transformation (2021-2023)

June 2022. At the Dahej complex, engineers are running final tests on a 50,000 TPA plant that represents a $100 million bet on a single molecule: Epichlorohydrin (ECH). For a company with a market cap of ₹3,000 crore, this wasn't just a capacity expansion—it was a metamorphosis.

Epigral became the first company in India to set up an Epichlorohydrin plant. But why ECH? The molecule sits at a fascinating intersection of chemistry and economics. You take glycerin (a byproduct of biodiesel that India has in surplus) or propylene, add chlorine (which you're already producing), and create ECH—a key ingredient in epoxy resins, synthetic glycerin, and water treatment chemicals. The global market was 2 million tons, growing at 5% annually, and 80% controlled by Chinese producers.

The ECH bet was really three bets in one. First, that global customers wanted supply chain diversification post-COVID. Second, that India's biodiesel boom would provide cheap glycerin feedstock. Third, that environmental regulations would eventually constrain Chinese capacity. All three proved correct, but not in the way anyone expected.

Just one month later, July 2022, came the second punch: Commissioning of a CPVC Resin manufacturing facility with 30,000 TPA capacity. Now this was audacious. CPVC (Chlorinated Polyvinyl Chloride) is PVC's premium cousin—able to handle hot water, more chemical resistant, and commanding 40% price premiums. India was importing 100% of its 150,000 TPA requirement. The technology was complex, the market was entirely controlled by Lubrizol (USA) and a few Japanese producers, and no Indian company had cracked it.

The CPVC technology acquisition story is worth its own episode. Unable to license technology from established players (who weren't interested in creating competition), Epigral hired a team of Eastern European chemical engineers who'd worked in Soviet-era chlorination plants. They reverse-engineered the process, built pilot plants, and spent 18 months perfecting the recipe. The first commercial batch in July 2022 was sent to Astral Pipes—India's largest CPVC pipe manufacturer. The feedback: "Quality comparable to imported material."

By April 2024, they expanded CPVC capacity by another 45,000 TPA, reaching total capacity of 75,000 TPA. But they didn't stop at resin. In June 2024, they forward integrated by commissioning a CPVC Compound facility of 35,000 TPA. Compounds are resins plus additives—ready to use formulations that pipe manufacturers can directly process. Higher margins, stickier customer relationships, and virtually no competition in India.

The numbers tell the transformation story. Specialty chemicals grew from 25% of revenue in FY22 to 56% in H1 FY25. But revenue mix doesn't capture the margin impact. Caustic soda EBITDA margins: 15-18%. CPVC Resin margins: 35-40%. CPVC Compound margins: 40-45%. Every ton shifted from commodity to specialty doubled contribution.

The market response was swift. From listing at ₹615 in August 2021, the stock hit ₹2,400 by mid-2023. The re-rating wasn't just about current earnings—it was about the market recognizing that this wasn't a commodity chemical company anymore. This was a specialty chemical company with commodity chemical backing, giving it cost advantages competitors couldn't match.

The company announced expansion of additional 75,000 TPA capacity of CPVC Resin, targeting total capacity of 150,000 TPA in FY25. This would make them not just India's largest, but among the top 5 globally outside China. For context, India's entire CPVC demand is 150,000 TPA. Epigral was building capacity to serve the entire country and export.

But perhaps the boldest move came in March 2025: Commissioning of India's first Chlorotoluenes Value Chain facility. Chlorotoluenes are precursors for agrochemicals, pharmaceuticals, and specialty polymers—markets worth billions globally and 100% imported into India. The technology is so complex that only four companies globally have mastered it at scale.

The specialty transformation wasn't just about adding capacity. It was about fundamentally reimagining what an Indian chemical company could be. While competitors were content being toll manufacturers or licensing technology, Epigral was developing its own processes, filing patents, and building R&D capabilities. They hired 50 PhD chemists, established research partnerships with ICT Mumbai and NCL Pune, and started filing 10+ patents annually.

The transformation also changed customer dynamics. Instead of selling to traders and commodity buyers, they were now dealing with Ashirvad Pipes (Aliaxis), Astral, Supreme Industries—companies that valued security of supply over lowest price. Long-term contracts replaced spot sales. Technical service replaced price negotiations. The business model had fundamentally shifted.

By late 2023, the transformation was complete enough that the company felt confident in shedding its old identity entirely. It was time for a rebrand that would signal to the world: this isn't your father's chemical company anymore.

V. The Rebranding & Vision Expansion (2023-Present)

August 28, 2023. At the BSE auditorium in Mumbai, CEO Maulik Patel stands before analysts and investors to announce something unusual for a chemical company: a complete rebrand. Meghmani Finechem Limited would become Epigral Limited. The name change might seem cosmetic, but in the conservative world of Indian chemicals where companies carry founder names for decades, this was a declaration of independence.

The company was formerly known as Meghmani Finechem Limited and changed its name to Epigral Limited in August 2023. The choice of "Epigral" wasn't random. It combined "Epi" from Epichlorohydrin—their flagship specialty product—with "gral" suggesting integral or integrated. The message was clear: we're not just a Meghmani subsidiary anymore; we're a specialty chemical leader in our own right.

The rebrand coincided with an aggressive vision statement: "To become a $1 billion revenue company by 2027 with 70% contribution from specialty chemicals." For context, FY2023 revenue was ₹2,100 crore ($260 million). They were essentially promising to quadruple in four years while completely transforming their product mix. In chemicals, where capacity additions take 2-3 years and customer qualifications another year, this was borderline absurd. Or was it?

The capital allocation spoke louder than words. FY2024 capex: ₹800 crore. FY2025 planned capex: ₹1,200 crore. For a company generating ₹400 crore in annual profit, this was betting the farm. But unlike speculative capacity additions hoping demand materializes, every expansion was backed by import substitution data. India imports $2 billion worth of chlorinated specialties annually. Even capturing 10% would double Epigral's revenue.

The expansion wasn't just about scale—it was about scope. The R&D center, established in 2023 with a ₹50 crore investment, wasn't a token gesture. They hired Dr. Rakesh Jain, formerly of BASF India, to lead innovation. The mandate: develop one new product every quarter, file for process patents, and reduce production costs by 2% annually through process optimization. By Q1 FY2025, they'd filed 12 patents and launched 4 new grades of CPVC.

Sustainability became central to the expansion story, though not for ESG brownie points. In chemicals, sustainability equals cost reduction. They installed a 25 MW solar plant—not because they cared about carbon credits, but because solar power at ₹2.50 per unit beat grid power at ₹4.50. They implemented zero liquid discharge—not for environmental awards, but because treating and recycling water was cheaper than buying fresh water in water-scarce Gujarat.

The green hydrogen initiative was particularly clever. Remember, hydrogen is a byproduct of chlor-alkali—you get 25 kg of hydrogen for every ton of caustic soda. Most Indian producers simply vented it or burned it for steam. Epigral invested ₹100 crore in compression and purification systems to sell it as green hydrogen to refineries and fertilizer plants. At ₹200 per kg, that's ₹5,000 of additional revenue per ton of caustic—pure margin since the hydrogen was already being produced.

Geographic expansion followed product expansion. While 80% of revenue remained domestic, exports grew to 20% by FY2024, targeting Middle East and Southeast Asian markets where Indian chemicals had cost advantages over Chinese competitors. But the real opportunity was import substitution—why chase export markets when India itself imports $15 billion of chemicals annually?

The organizational transformation was equally dramatic. From 800 employees in 2021, the workforce grew to 1,950 by 2024—but the composition changed more than the numbers. Engineers replaced operators, data scientists joined process engineers, and supply chain experts supplemented traditional purchase managers. Average employee age dropped from 45 to 35. The company started recruiting from IITs and chemical engineering programs, competing with TCS and Infosys for talent—unheard of for a Gujarati chemical company.

Digital transformation sounds like buzzword bingo, but in chemicals, it's survival. They implemented SAP S/4HANA not for consultants' presentations but for real-time yield tracking. IoT sensors on reactors didn't just collect data—they prevented ₹50 crore in potential losses by predicting equipment failures. The digital control room looked more like a fintech trading floor than a chemical plant—real-time dashboards tracking everything from chlorine cell efficiency to customer credit limits. The latest Q1 FY26 results tell the transformation story: revenue of ₹615 crore, reflecting a 6% year-on-year decline, EBITDA stood at ₹163 crore, down 7% YoY, but EBITDA margins remained steady at 27%. While revenues dipped due to commodity price softness, margins held firm—proof that the specialty mix is working. Revenue from the company's Derivatives & Specialty Chemicals segment contributed 50% to the overall revenue, up from virtually nothing five years ago.

By 2025, Epigral wasn't just another chemical company with a new name. It was a specialty chemical powerhouse masquerading as a chlor-alkali producer, with the cost advantages of the latter and the margins of the former. The rebrand wasn't window dressing—it was a declaration of what the company had become and where it was headed.

VI. Business Model & Competitive Advantages

Understanding Epigral's business model requires appreciating a fundamental truth about chemicals: in commodities, you're a price taker; in specialties, you're a price maker. Epigral has engineered a model that straddles both worlds, using commodity scale to achieve specialty margins.

The core remains chlor-alkali, but it's the integration that creates magic. When you produce caustic soda, you automatically get chlorine and hydrogen. Most producers sell these as commodities. Epigral uses them as feedstock for higher-value products. That chlorine becomes CPVC resin, selling at 3x the price of chlorine gas. The hydrogen, instead of being flared, is compressed and sold to refineries at premium prices. Every molecule is monetized at its highest possible value.

The company is the 5th largest producer of Chloromethanes (CMS) in India. It is also 3rd largest producer of Hydrogen Peroxide in India. These aren't just market share statistics—they represent pricing power. When you're top 5 in a product, customers need you for supply security. You're not competing on price alone anymore.

The Dahej location provides structural advantages that are hard to replicate. The 413-acre complex sits in the Petroleum, Chemicals and Petrochemicals Investment Region (PCPIR), giving them priority access to feedstock, dedicated pipelines for raw materials, and proximity to ports for exports. The site can theoretically expand to 1 million TPA of chlor-alkali—enough to support $2 billion in downstream products.

Backward integration provides cost advantages, but forward integration provides margin expansion. By moving from caustic soda (₹30,000/ton) to CPVC compound (₹150,000/ton), they're capturing 5x value addition on the same chlorine molecule. This isn't just vertical integration—it's value chain domination.

The customer segmentation reveals the moat. They serve 15+ industries—from pipes and paints to pharmaceuticals and paper. This diversification means no single industry downturn can cripple them. But more importantly, each industry requires different product specifications, creating switching costs. Ashirvad Pipes can't easily switch CPVC suppliers because Epigral's resin is specifically formulated for their extrusion process.

Energy management, often overlooked, is central to competitive advantage. With 130 MW of captive power generation and 25 MW of solar, they control 70% of their energy needs. In chlor-alkali, where electricity is 60% of cash costs, this translates to ₹100 crore in annual savings versus grid power. The recent green hydrogen initiative adds another layer—selling hydrogen at ₹200/kg generates ₹50 crore in additional EBITDA with zero additional cost.

The technology moat is underappreciated. While caustic soda technology is commoditized, their specialty products require proprietary knowledge. The CPVC process involves chlorinating PVC in a fluidized bed reactor at precise temperatures with specific catalysts—get it wrong and you have worthless plastic. Their chlorotoluenes technology, acquired through a mix of licensing and internal development, has only four other practitioners globally.

Working capital management showcases operational excellence. Despite dealing in commodities where 60-90 day payment terms are standard, their cash conversion cycle is 45 days. How? Direct customer relationships eliminate trader margins and payment delays. Integrated operations mean internal transfers don't tie up working capital. And specialty products command better payment terms than commodities.

The financial metrics tell the story: Return on Capital Employed (ROCE) improved to 24% from 21% a year earlier. Net Debt/EBITDA ratio dropped significantly to 0.6x, compared to 1.6x in the previous year. These aren't just improving metrics—they're best-in-class for Indian chemicals.

Competitive dynamics favor Epigral in ways that aren't immediately obvious. Large players like Reliance focus on mega-scale petrochemicals, ignoring sub-$500 million markets. Chinese competitors face increasing environmental restrictions and rising labor costs. European producers are exiting commodity chemicals due to energy costs. This leaves a sweet spot for focused Indian producers—large enough for economies of scale, small enough to avoid attention from giants.

The real competitive advantage, though, is speed. From board approval to commissioning, Epigral executes projects in 18-24 months. Global majors take 3-4 years. In chemicals, where cycles are violent and windows of opportunity brief, this execution speed is worth billions in NPV. When CPVC prices spiked in 2021, they had capacity online by 2022. Competitors announcing capacity then are still building.

VII. Financial Performance & Unit Economics

The financial transformation of Epigral reads like a textbook case study in value creation through business model evolution. Revenue: 2,505 Cr, Profit: 431 Cr for FY2024—but these headline numbers obscure the dramatic shift happening beneath.

Let's start with the revenue journey. From ₹609 crore in FY2018 to ₹2,505 crore in FY2024—a 4x growth in six years. But the composition changed even more dramatically. Commodity chemicals (caustic, chlorine) went from 90% of revenue to 44%. Specialty chemicals jumped from 10% to 56%. Same factories, same location, fundamentally different business.

The margin story is where it gets interesting. Caustic soda EBITDA margins: 15-18% in good times, single digits in downturns. CPVC Resin margins: steady 35-40%. CPVC Compound margins: 40-45%. The math is simple—every ton shifted from commodity to specialty doubles contribution. With 150,000 TPA of CPVC capacity coming online, that's ₹300 crore of additional EBITDA at current utilizations.

The PE ratios of Epigral is 23.94 as of August 2024. For a chemical company, this seems rich. But decompose it: the commodity business probably trades at 10x earnings, the specialty business at 30x. As the mix shifts, the multiple expands. The market is pricing in the transformation, not the current state.

Capital efficiency deserves special attention. Caustic soda capacity costs ₹50,000 per ton to build. CPVC capacity costs ₹150,000 per ton. But caustic generates ₹5,000 EBITDA per ton, while CPVC generates ₹30,000 EBITDA per ton. The ROCE on specialty expansion is 3x that of commodity expansion. This explains why they're betting everything on downstream integration.

Working capital dynamics changed with the business mix. Commodity chemicals are sold on 30-day credit with 60-day payment terms for raw materials—negative working capital. Specialty chemicals require 60-day customer credit but command immediate payment for raw materials. The net effect: working capital increased from 30 days to 45 days of sales, but absolute ROCE improved due to higher margins.

The debt story is remarkable. Net debt peaked at ₹1,200 crore during the 2022-23 expansion phase. By Q1 FY26, despite ongoing capex, net debt/EBITDA had dropped to 0.6x. How? Operating cash flow of ₹600 crore annually, even during heavy investment periods. The business is essentially self-funding its transformation.

Let's examine unit economics through a specific product: CPVC Resin. Input cost: ₹70,000/ton (PVC + chlorine + utilities). Selling price: ₹140,000/ton. EBITDA: ₹50,000/ton. At 75,000 TPA capacity running at 80% utilization, that's ₹300 crore EBITDA from a single product line. The IRR on the ₹300 crore investment? North of 35%.

Tax efficiency is an underappreciated advantage. Manufacturing in Dahej SEZ provides tax holidays on export income. With 20% of production exported, effective tax rate is 22% versus statutory 30%. Additionally, the recent ₹81 crore deferred tax benefit in Q1 FY26 shows active tax planning. Every percentage point of tax saved flows straight to ROE.

Depreciation deserves attention. With ₹2,000 crore in gross block and 10-year average asset life, annual depreciation runs ₹200 crore. But maintenance capex is only ₹100 crore. The difference—₹100 crore—is essentially hidden cash flow that doesn't show up in P&L analysis but funds growth.

Currency dynamics favor Epigral unexpectedly. While 80% of revenue is domestic (rupee denominated), 40% of costs are linked to international prices (crude derivatives, imported coal). When the rupee depreciates, domestic selling prices adjust with a lag, creating temporary margin expansion. The 2022 rupee depreciation added ₹50 crore to EBITDA.

The dividend policy reveals management confidence. Despite aggressive expansion, they maintain a 15-20% payout ratio. This isn't token; it's ₹60-80 crore annually. For a company with ₹1,500 crore in expansion plans, paying dividends signals belief that operating cash flow can fund growth.

Quarterly volatility requires context. Q1 is typically weak (monsoon impacts construction), Q3 is strongest (peak construction season). Year-on-year comparisons matter more than sequential. The Q1 FY26 revenue decline of 6% year-on-year seems concerning until you realize commodity prices fell 15%—volumes actually grew.

VIII. Growth Strategy & Future Bets

The growth strategy reads like a chemical industry wishlist: capacity expansion, import substitution, green chemistry, and geographic diversification. But unlike most wishlists, this one comes with committed capital, proven execution, and tangible timelines.

The capacity roadmap is staggering. Current plans include 75,000 TPA additional CPVC resin (₹500 crore capex), 50,000 TPA ECH expansion (₹400 crore), and 100,000 TPA caustic soda debottlenecking (₹200 crore). Total committed capex: ₹1,500 crore over FY25-26. For context, the entire gross block today is ₹2,000 crore. They're essentially building another company on top of the existing one.

Import substitution remains the core thesis. India imports $15 billion in chemicals annually, with $2 billion in chlorinated derivatives alone. Epigral targets products where India has zero or minimal domestic capacity: CPVC resin (100% imported before Epigral), Epichlorohydrin (90% imported), Chlorotoluenes (100% imported). Each product represents a $200-500 million addressable market with zero domestic competition.

The green chemistry push isn't greenwashing—it's economics. Their bio-based ECH process uses glycerin from biodiesel waste, reducing raw material costs by 20% versus petroleum-based routes. The chloromethanes process captures HCl as a byproduct, selling it instead of neutralizing it. Green chemistry here means extracting value from waste streams.

Geographic expansion follows customer pull, not push. Middle East markets need caustic soda for alumina refineries. Southeast Asia requires CPVC for tropical construction. Africa wants chlorine for water treatment. Rather than blindly exporting, they're following established customers into new geographies, reducing market development costs.

Adjacent opportunities keep emerging. The hydrogen economy isn't science fiction—it's happening. Epigral produces 25 kg of hydrogen per ton of caustic, currently 20,000 TPA of hydrogen. At $5/kg for green hydrogen, that's a $100 million opportunity. They're investing in compression, purification, and logistics to capture this value.

R&D investment targets process optimization over product innovation. Reducing power consumption by 50 kWh/ton saves ₹20 crore annually. Improving chlorination yield by 1% adds ₹10 crore to EBITDA. These incremental improvements compound—5 years of 2% annual efficiency gains equals a 10% structural cost advantage.

Digital initiatives focus on operational excellence. Predictive maintenance using IoT sensors prevents unplanned shutdowns—each day of downtime costs ₹2 crore. Supply chain optimization through AI reduces inventory by 10%, freeing ₹50 crore in working capital. These aren't pilot projects; they're deployed at scale.

Strategic partnerships are being explored carefully. Technology partnerships for next-generation products (fluoro-chemicals, electronic chemicals), feedstock partnerships for supply security (salt fields, coal mines), and customer partnerships for demand visibility (long-term contracts with formula pricing). Each partnership must enhance competitive position, not just add capacity.

The acquisition strategy is disciplined. They're looking for distressed specialty chemical assets with technology but poor balance sheets. The criteria: purchase price below replacement cost, technology complementary to existing portfolio, and immediate synergy potential. They walked away from three deals in 2024 because valuations didn't meet hurdle rates.

Market timing appears favorable. The "China Plus One" theme has evolved from PowerPoint slides to purchase orders. Environmental regulations are permanently impairing Chinese capacity. European chemical makers are retreating from energy-intensive products. The window for Indian chemical champions is open, but it won't stay open forever.

The $1 billion revenue target by 2027 breaks down clearly: $400 million from current capacity at full utilization, $300 million from announced expansions, $200 million from price/mix improvement, and $100 million from new products. Aggressive but achievable if execution continues at current pace.

Risk management underpins growth strategy. No single product exceeds 30% of revenue. No single customer exceeds 10%. Raw material sourcing is diversified across suppliers and geographies. This isn't conservative—it's prudent. In chemicals, concentration risk has killed more companies than competition ever has.

IX. Risks, Competition & Market Dynamics

Every chemical company CEO loses sleep over China, and Epigral is no exception. Chinese producers control 60% of global chlor-alkali capacity and 80% of downstream derivatives. When China sneezes, global chemical markets catch pneumonia. The 2019 caustic soda crash, when Chinese oversupply drove prices down 40%, nearly bankrupted half of India's chlor-alkali industry.

But the China risk has evolved. Environmental inspections have shuttered 30% of Chinese chemical capacity since 2018. Energy shortages in 2021-22 forced production curtailments. Labor costs have tripled in a decade. The Middle Kingdom's chemical dominance is eroding, but slowly and unevenly. Epigral benefits from this trend, but a sudden Chinese policy reversal could flood markets overnight.

Environmental compliance presents existential risk. Chemical manufacturing is inherently polluting—chlorine gas leaks can evacuate cities, caustic soda spills destroy ecosystems, and chlorinated organics are carcinogenic. One major incident could trigger plant shutdowns, criminal liability, and permanent license revocation. Epigral spends ₹50 crore annually on environmental compliance, but in chemicals, perfect safety is impossible—only degrees of risk mitigation.

Competition from established players intensifies as margins improve. DCM Shriram, with 300,000 TPA caustic capacity, has announced CPVC backward integration. Gujarat Alkalies, a state-owned giant with 500,000 TPA capacity, is expanding into specialty derivatives. Reliance, the 800-pound gorilla, could enter any segment and destroy economics through sheer scale. Epigral's first-mover advantage in specialties provides temporary protection, but chemical markets inevitably commoditize.

Raw material volatility wreaks havoc on margins. Salt prices can spike 50% during monsoon disruptions. Power costs fluctuate with coal prices and grid availability. PVC resin for CPVC production tracks crude oil. A 10% increase in raw material costs, if not passed through immediately, can evaporate quarterly profits. The company maintains 45-day inventory buffers, but in volatile markets, that's often insufficient.

Technology disruption looms larger than most realize. Membrane cell technology revolutionized chlor-alkali in the 1990s, making mercury and diaphragm cells obsolete overnight. Companies that didn't upgrade went bankrupt. Today, new technologies threaten again: solid oxide electrolysis could reduce power consumption by 30%, bio-based routes could eliminate chlorine altogether, and recycling could destroy demand for virgin chemicals. Epigral's R&D spending at 1% of revenue seems inadequate against these threats.

Customer concentration in specialties creates hidden vulnerabilities. While no single customer exceeds 10% of revenue, the top 5 CPVC customers represent 60% of CPVC sales. If Ashirvad or Astral switches suppliers or backward integrates, it could strand capacity. Long-term contracts provide some protection, but in commoditizing markets, contracts are only as strong as switching costs.

Regulatory changes could reshape economics overnight. The government's anti-dumping duties on Chinese chemicals, currently 20-30%, provide crucial protection. If removed under trade agreements, domestic prices could crash 25%. Conversely, environmental regulations mandating zero liquid discharge or carbon taxes could add ₹100 crore in annual compliance costs. Chemical companies live at the mercy of regulators.

Execution risk multiplies with expansion pace. Epigral is attempting to triple capacity in three years while introducing new technologies and entering new markets. Project delays are endemic in Indian manufacturing—environmental clearances, land acquisition, equipment delivery, and commissioning challenges. A six-month delay on the ₹500 crore CPVC expansion would miss an entire year's selling season.

Financial leverage, while manageable now, could become problematic. With ₹1,500 crore in planned capex and net debt/EBITDA at 0.6x, they have room to borrow. But chemical cycles are violent. If EBITDA halves during a downturn (as happened in 2019), debt/EBITDA could spike to 3x, triggering covenant breaches and forcing asset sales at distressed prices.

Succession risk in family-owned businesses can't be ignored. While the current generation has executed brilliantly, family businesses often struggle with third-generation transitions. Disagreements over strategy, capital allocation, or leadership can paralyze decision-making. The 68.8% promoter holding provides stability but also concentration risk.

Market dynamics are shifting unfavorably in some segments. Caustic soda demand from alumina refineries is slowing as aluminum demand weakens. Chlorine demand from PVC manufacturers faces pressure from PVC alternatives. Paper and textile industries, traditional chlor-alkali consumers, are shrinking. While specialty growth offsets commodity decline, the base business faces structural headwinds.

X. Investment Thesis & Valuation Framework

The bull case for Epigral writes itself: a specialty chemical transformation story in the sweet spot of import substitution, led by hungry second-generation entrepreneurs, with proven execution and expanding margins. But as Munger reminds us, "All intelligent investing is value investing—acquiring more than you are paying for."

At current valuations—₹8,136 crore market cap on ₹431 crore profit—the market prices Epigral at 19x trailing earnings. For context, commodity chemical companies trade at 8-12x, while specialty players command 25-35x. The 19x multiple suggests the market is pricing Epigral somewhere in between—acknowledging the transformation but not fully believing it.

The bull case rests on multiple expansion as the business mix shifts. If specialty chemicals reach 70% of revenue by FY27 (from 56% today), and margins expand accordingly, the business could deserve a 25x multiple. On FY27 estimated earnings of ₹700 crore (assuming successful execution of announced projects), that implies a ₹17,500 crore market cap—more than double today's valuation.

Import substitution provides a decade-long runway. India's chemical imports are growing 10% annually, reaching $20 billion by 2030. If Epigral captures just 2% of import substitution opportunity, that's $400 million in incremental revenue at 35% EBITDA margins. The addressable market is large enough that Epigral could grow 20% annually without gaining significant market share.

The bear case can't be dismissed. Commodity chemicals still contribute 44% of revenue and face structural challenges. Chinese capacity could return with vengeance. Environmental regulations could impose unexpected costs. Most critically, the aggressive expansion could stumble—delays, cost overruns, or technical failures could destroy returns.

Valuation through comparable analysis reveals interesting disparities. Aarti Industries, with similar specialty chemical exposure, trades at 28x earnings. Navin Fluorine, in fluorochemicals, commands 35x. But DCM Shriram, primarily commodity focused, trades at 12x. If Epigral is becoming more Aarti than DCM, current valuations offer 30-40% upside.

The sum-of-parts valuation provides another lens. Value the commodity business (₹1,500 crore revenue) at 1x sales = ₹1,500 crore. Value the specialty business (₹1,000 crore revenue) at 4x sales = ₹4,000 crore. Add ₹500 crore for the Dahej land bank. Total value: ₹6,000 crore versus ₹8,136 crore market cap. The market is pricing in significant growth.

Replacement cost analysis suggests deep value. Building 400,000 TPA chlor-alkali capacity would cost ₹2,000 crore today. CPVC and derivative plants would require another ₹1,500 crore. The Dahej land alone is worth ₹500 crore. Total replacement cost: ₹4,000 crore for assets generating ₹600 crore EBITDA. At typical chemical industry multiples of 8-10x EBITDA, the business is worth ₹5,000-6,000 crore—below current market cap but not dramatically so.

The India chemicals story provides sectoral tailwinds. India's chemical industry is projected to reach $300 billion by 2025, growing at 12% CAGR. Government initiatives like production-linked incentives (PLI) for chemicals, port infrastructure development, and environmental regulations favoring organized players all benefit Epigral. This isn't company-specific—it's riding a structural wave.

Capital allocation track record builds confidence. Management has consistently earned 20%+ returns on invested capital, well above the 12% cost of capital. They've avoided the empire-building tendency of many family businesses, focusing on adjacent expansions rather than unrelated diversification. The modest dividend payout and conservative leverage suggest they prioritize long-term value over short-term gratification.

The key monitorables for investors are clear: specialty chemical revenue mix (target: 70% by FY27), EBITDA margins (sustaining above 25%), ROCE (maintaining above 20%), and successful commissioning of announced projects on schedule. Any deviation from these metrics would challenge the investment thesis.

Risk-reward appears favorable for patient capital. Downside seems limited given replacement cost and asset value. Upside could be substantial if the specialty transformation succeeds. The business isn't priced for perfection—current valuations imply skepticism about execution. For investors willing to bet on continued execution, the asymmetry is attractive.

XI. Playbook Lessons

The Epigral story offers a masterclass in corporate transformation, but the lessons extend beyond chemicals. This is really about how Indian family businesses can evolve from commodity producers to specialty champions, creating billions in value along the way.

The Demerger as Value Creation Tool

The 2021 demerger from Meghmani Organics wasn't just corporate restructuring—it was surgery to save both patients. The parent company's agrochemical business was dragging down the profitable chlor-alkali subsidiary. Post-demerger, Meghmani Organics could focus on restructuring its debt and operations without constraining Epigral's growth. Epigral could access capital markets independently and invest aggressively.

The lesson: When businesses have divergent capital needs, growth trajectories, or risk profiles, keeping them together destroys value. The stock market values focus over diversification. Epigral's 3x appreciation since demerger while Meghmani Organics restructured proves this. Sometimes the best thing a parent can do for its child is let it go.

Timing Market Cycles in Chemicals

Epigral's capacity additions seem prescient in hindsight but were contrarian when announced. They committed to CPVC expansion in 2020 when pandemic uncertainty was peak. They announced ECH capacity when China was dumping product. They're expanding chlor-alkali now when the cycle is softening.

The playbook: In chemicals, you must invest counter-cyclically. By the time shortages appear and prices spike, it's too late—everyone rushes to add capacity, creating the next glut. Epigral times expansions for commissioning during upturn, not initiation during upturn. This requires conviction to invest when others retreat and patience to wait for cycles to turn.

Building Competitive Moats Through Integration

Vertical integration in chemicals isn't just about margin capture—it's about creating switching costs. When Epigral supplies caustic soda, chlorine derivatives, and specialty chemicals to the same customer, switching becomes operationally complex. The customer would need to qualify multiple new suppliers, manage additional logistics, and coordinate specifications.

But integration must be selective. Epigral doesn't integrate into end products (pipes, paints) where they'd compete with customers. They stop at intermediate chemicals where technical expertise matters but customer relationships are collaborative, not competitive. This "sweet spot" integration maximizes value capture while minimizing channel conflict.

Managing the Commodity-to-Specialty Transition

The transformation from 25% to 56% specialty chemicals in three years required more than capacity addition. It required cultural change. Commodity businesses focus on cost and efficiency. Specialty businesses emphasize innovation and customer service. Epigral had to build new capabilities while maintaining operational excellence in commodities.

The key was sequencing. They didn't abandon commodities—that cash flow funded specialty expansion. They started with specialties closest to existing capabilities (CPVC uses chlorine from chlor-alkali). They hired specialty talent but retained commodity veterans. This balanced approach maintained stability while driving change.

Family Business Succession Done Right

The generational transition at Epigral avoided typical pitfalls. Clear separation of businesses (chemicals vs. agrochemicals) prevented sibling rivalry. The older generation retained board positions but ceded operational control. Professional managers were hired for critical roles, preventing nepotism accusations.

Most importantly, the family aligned on vision before splitting assets. The decision to focus on chemicals, invest aggressively, and build for the long-term was collective. This alignment, rare in family businesses, enabled decisive action post-separation. The 68.8% promoter holding shows skin in the game, not just control for control's sake.

The Import Substitution Opportunity

Epigral recognized that "Make in India" for chemicals wasn't about competing globally but serving domestically. Instead of targeting export markets dominated by China and competing on cost, they focused on import substitution where logistics, customization, and supply security matter.

The playbook: Identify products where India has zero or minimal capacity, steady demand growth, and logistics advantages for domestic supply. Build capacity equivalent to 50-70% of imports—enough for leadership but not oversupply. Price at 10-15% discount to landed import cost. This formula has worked for CPVC, ECH, and now chlorotoluenes.

Technology Acquisition Strategy

Unable to license technology from competitors, Epigral got creative. They hired retired engineers from European plants, partnered with Russian design institutes, and reverse-engineered processes. This "assembled" technology approach cost 50% less than licensing and avoided royalty payments.

The lesson: In chemicals, process technology matters more than product technology. If you can't buy it, build it. If you can't build it alone, assemble the pieces. The key is having enough internal expertise to integrate different technology sources into a working whole.

Capital Cycle Management

Epigral's capital allocation follows a clear hierarchy: maintenance capex first, brownfield expansion second, greenfield projects third, and acquisitions last. This discipline ensures existing assets remain competitive before chasing growth. They've avoided the trap of many chemical companies—building new plants while existing ones decay.

Equally important is timing. They raise debt when rates are low, equity when valuations are high, and internal accruals when both are expensive. This opportunistic financing has kept cost of capital below 10% despite aggressive expansion.

The Epigral playbook isn't revolutionary—it's evolutionary. Take a commodity business, add specialty products systematically, integrate selectively, execute consistently, and let compounding work. The magic isn't in any single decision but in the accumulation of good decisions over time. For Indian manufacturing companies seeking to move up the value chain, Epigral provides a template: patient capital, focused execution, and the courage to transform while others hesitate.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube