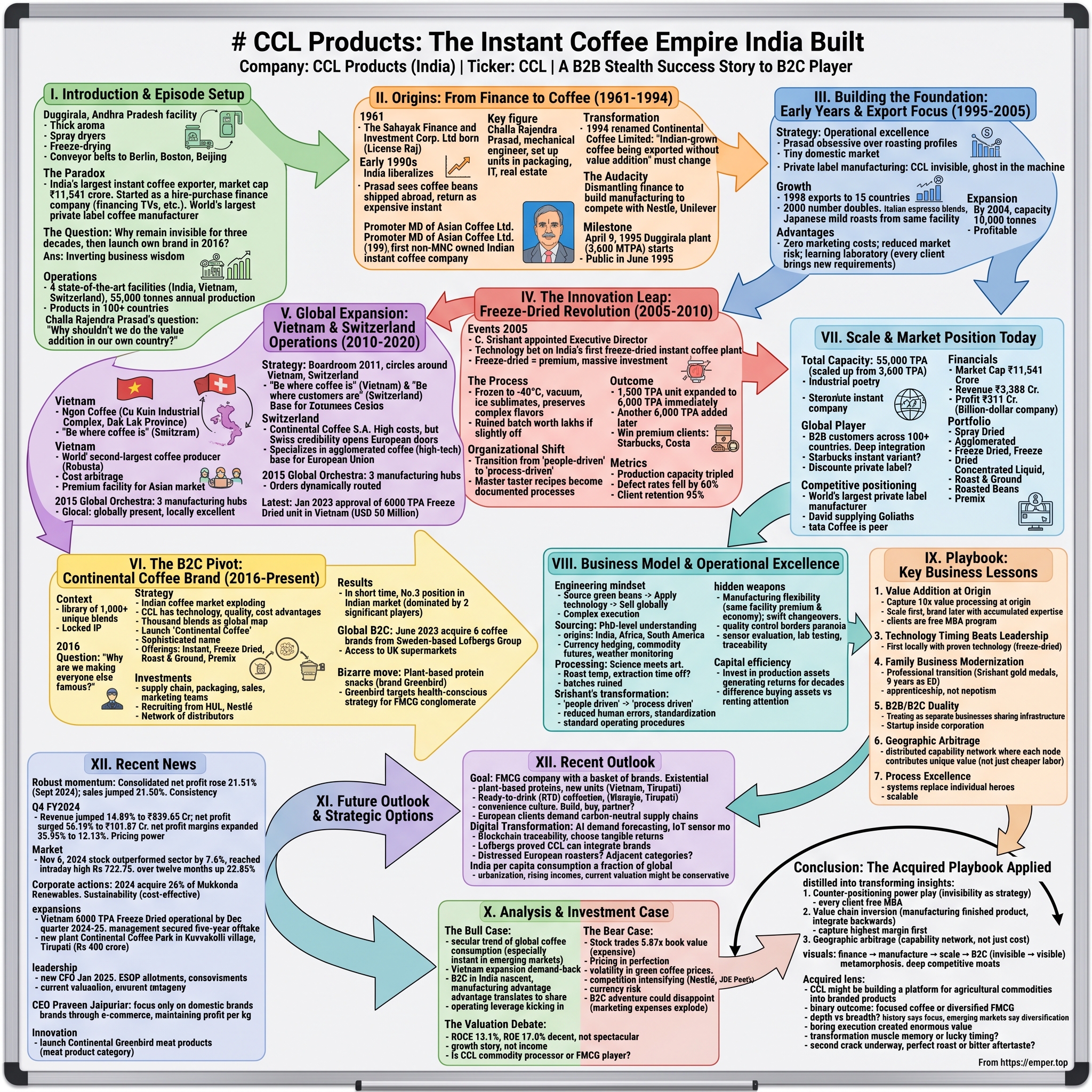

CCL Products: The Instant Coffee Empire India Built

I. Introduction & Episode Setup

Picture this: A sprawling facility in Duggirala, Andhra Pradesh, where the air is thick with the aroma of roasting coffee beans. Giant spray dryers tower overhead, freeze-drying chambers hum with precision, and conveyor belts carry millions of tiny coffee granules destined for cups in Berlin, Boston, and Beijing. This is CCL Products—a company most Indians have never heard of, yet whose coffee they've likely consumed under a hundred different labels.

Here's the paradox: India's largest instant coffee exporter, with a market cap of ₹11,541 crore, started life as a hire-purchase finance company. Yes, you read that right—from financing TVs and refrigerators to becoming the world's largest private label coffee manufacturer. It's a transformation so improbable that if you pitched it as fiction, publishers would reject it as unrealistic.

The central question driving this story isn't just how CCL pulled off this metamorphosis—it's why a company that manufactures coffee for Nestlé, Unilever, and virtually every major global brand decided to remain largely invisible for three decades, then suddenly pivoted to launch its own consumer brand in 2016. The answer reveals fundamental truths about how emerging market companies can build global empires by inverting traditional business wisdom.

Today, CCL operates four state-of-the-art facilities across India, Vietnam, and Switzerland, producing 55,000 tonnes of instant coffee annually. Their products reach over 100 countries, yet most consumers drinking their coffee have no idea CCL exists. It's the ultimate B2B stealth success story—until recently, when the company decided anonymity was no longer enough.

What follows is the story of how Challa Rajendra Prasad built a coffee empire by asking one simple question that challenged India's entire export paradigm: "Why shouldn't we do the value addition in our own country?" That question, posed in the early 1990s when India was just opening its economy, would reshape not just CCL's destiny but demonstrate an entirely new playbook for Indian manufacturing on the global stage.

II. Origins: From Finance to Coffee (1961-1994)

The year is 1961. Jawaharlal Nehru is Prime Minister, the License Raj throttles Indian enterprise, and in this environment, The Sahayak Finance and Investment Corporation Limited is born—a hire-purchase finance company that would have remained a footnote in Indian corporate history if not for what happened three decades later.

Fast forward to the early 1990s. India is liberalizing, the world is globalizing, and Challa Rajendra Prasad is watching Indian coffee beans being shipped abroad only to return as expensive instant coffee. The irony burns: India grows some of the world's finest coffee, yet captures none of the value addition. Prasad, who had already pioneered soluble coffee exports during his tenure at Asian Coffee Ltd., saw an opportunity hiding in plain sight. Prasad, a mechanical engineer from Osmania University (1975), wasn't your typical entrepreneur. He had already set up several units in packaging materials, tubes and ducts, IT, real estate and construction. But coffee was different—this wasn't just another business opportunity. As Promoter Managing Director of Asian Coffee Ltd., set up in 1989, he had created the first Indian non-multinational owned company engaged in instant coffee, earning recognition from the Coffee Board of India where he served three consecutive terms from 1990 to 1999.

The transformation began in 1994 when The Sahayak Finance and Investment Corporation Limited was rechristened Continental Coffee Limited. The name change signaled more than a corporate rebranding—it represented a fundamental reimagining of what an Indian company could achieve in global markets. Prasad's vision was elegantly simple yet revolutionary for its time: "Indian-grown coffee being exported without value addition" needed to change—he would establish an instant coffee plant, "adding value by converting green coffee beans into high-quality instant coffee".

Consider the audacity of this pivot. In 1994, India's economy had barely opened up. The Harshad Mehta scam had just rocked financial markets. Most Indian companies were still figuring out how to compete domestically, let alone globally. And here was Prasad, dismantling a finance company to build a manufacturing enterprise that would compete with Nestlé and Unilever.

On April 9, 1995, CCL's instant coffee plant roared to life in Duggirala with an initial capacity of 3,600 metric tonnes per annum. The location wasn't accidental—Andhra Pradesh offered proximity to both coffee-growing regions and ports, crucial for an export-focused strategy. Within months, the company went public in June 1995, raising capital for what would become one of India's most ambitious manufacturing stories.

The timing was everything. Post-liberalization India was hungry for foreign exchange, and here was a company proposing to capture the entire value chain—from bean to cup—within Indian borders. It was economic nationalism wrapped in entrepreneurial ambition, and it would set the template for how emerging market companies could insert themselves into global supply chains not as suppliers of raw materials, but as sophisticated manufacturers of finished products.

III. Building the Foundation: Early Years & Export Focus (1995-2005)

The morning shifts at Duggirala in 1995 began before dawn. Workers would arrive to find Prasad already there, tasting samples, adjusting roasting profiles, obsessing over moisture content. This wasn't a chairman playing factory manager—this was an engineer-entrepreneur who understood that in the global coffee business, consistency wasn't just important; it was everything.

Starting with 3,000 tonnes per annum capacity sounds modest today, but in 1995 India, it represented a massive bet. The domestic instant coffee market was tiny—Indians preferred their filter coffee fresh. The entire business model depended on convincing global brands to trust an unknown Indian company with their most precious asset: their brand reputation.

Prasad leveraged his reputation as "Pioneer and First Entrepreneur in India to have placed Indian Soluble Coffee in the hard currency world markets" to open doors. But reputation only gets you the meeting—keeping the contract required delivering Swiss-level quality from an Indian factory. The early years were a masterclass in operational excellence under constraints.

CCL's strategy was counterintuitive: instead of building a brand, they would become invisible. Private label manufacturing meant CCL's coffee would sit on shelves from Berlin to Boston, but always under someone else's name. It was ego-destroying and brilliant. While Indian companies were obsessed with putting their names on products, CCL was content to be the ghost in the machine.

The numbers tell the story of gradual conquest. By 1998, CCL was exporting to 15 countries. By 2000, that number had doubled. Each new market required different taste profiles, packaging specifications, regulatory compliance. The Duggirala facility became a babel of coffee—producing Italian espresso blends in one line while manufacturing Japanese mild roasts in another.

The real innovation wasn't technological—it was philosophical. CCL treated private label not as a stepping stone to building their own brand, but as the strategy itself. They would be the Intel Inside of coffee, powerful but invisible. This approach had three massive advantages:

First, it eliminated marketing costs. While competitors spent millions building brands, CCL invested in production capacity. Second, it reduced market risk—when you supply twenty brands across forty countries, no single market downturn can kill you. Third, it created a learning laboratory—every client brought new requirements, forcing continuous innovation.

By 2004, CCL had expanded capacity to 10,000 tonnes and was profitable enough to consider their next big bet. The company had proven Indians could manufacture to global standards. Now Prasad wanted to prove they could innovate beyond them. The freeze-dried revolution was about to begin, but first, the company needed fresh blood—enter the second generation.

IV. The Innovation Leap: Freeze-Dried Revolution (2005-2010)

In 2005, two events would reshape CCL's trajectory: C. Srishant was appointed as Executive Director, and the company made a technology bet that industry veterans called reckless—building India's first freeze-dried instant coffee plant.

Srishant brought impressive credentials—a law degree from NALSAR University, a diploma in Information Technology Law, and gold medals in both Corporate Law and Mathematics. But credentials don't run factories. What mattered was his ability to bridge his father's entrepreneurial instincts with modern management practices.

The freeze-dried decision exemplified this new approach. Spray-dried coffee, CCL's bread and butter, was adequate for most instant coffee needs. Freeze-dried coffee was premium—it preserved more flavor, commanded higher prices, but required massive capital investment and technical expertise India didn't possess. Setting up the freeze-dried unit was "innovative and way ahead of its time".

The technology works like science fiction: coffee is frozen to -40°C, then placed in a vacuum where ice sublimates directly to vapor, leaving behind porous coffee crystals that dissolve instantly while retaining complex flavors. The process requires precise control—one degree off, one bar of pressure wrong, and you've ruined an entire batch worth lakhs.

The gamble paid off spectacularly: "The product became such an instant success that a 1,500 TPA FD unit got expanded to 6,000 TPA immediately and another 6,000 TPA got added over a period of time". This wasn't just expansion—it was validation that an Indian company could compete in premium segments.

The freeze-dried success created a virtuous cycle. Premium products meant premium clients. Starbucks, Costa, and other specialty coffee brands began sourcing from CCL. Each new client brought stricter requirements, forcing further innovation. The Duggirala facility transformed from a factory into what employees called "the laboratory"—a place where coffee science happened.

But the real transformation was organizational. Under Srishant's influence, CCL began its shift from "people-driven" to "process-driven" operations. This wasn't about replacing human judgment—it was about encoding expertise into systems. When a master taster identified the perfect roast profile, it became a documented process. When an engineer solved a production bottleneck, the solution became standard operating procedure.

The metrics from this period are staggering. Production capacity tripled. Defect rates fell by 60%. Client retention hit 95%. But the number that mattered most was this: by 2010, CCL's freeze-dried coffee was winning blind taste tests against Swiss and German manufacturers. An Indian company wasn't just competing globally—it was setting standards.

In 2014, recognizing his contributions, Srishant was elevated to Managing Director. The transition from founder to second generation was complete, and with it came an even bolder vision: why should CCL remain confined to India when coffee is a global game?

V. Global Expansion: Vietnam & Switzerland Operations (2010-2020)

The boardroom in Hyderabad, 2011. Srishant presents a map with two circles: one around Vietnam, another around Switzerland. "We need to be where the coffee is," he points to Vietnam, "and where the customers are," gesturing toward Switzerland. The board's skepticism is palpable—Indian companies acquiring abroad often ended in tears. But CCL's logic was irrefutable.

Vietnam made perfect sense. The country had emerged as the world's second-largest coffee producer, primarily Robusta beans perfect for instant coffee. Land was affordable, labor costs competitive, and the government welcomed foreign investment. More importantly, Vietnam offered something India couldn't: proximity to Asian markets and access to different bean varieties.

The Ngon Coffee facility in Dak Lak Province wasn't just a factory—it was CCL's statement of intent. Built in the Cu Kuin Industrial Complex, the plant represented CCL's largest single investment to date. The name "Ngon"—Vietnamese for "delicious"—signaled this wasn't just about cost arbitrage. CCL was building a premium facility that would serve the booming Asian instant coffee market.

Switzerland was the opposite bet entirely. Here, costs were astronomical—labor, land, utilities, everything cost multiples of India. But Continental Coffee S.A. in Switzerland offered something invaluable: proximity to European customers and, crucially, Swiss credibility. When you're selling to German supermarket chains, "Made in Switzerland" opens doors that "Made in India" might not.

The Swiss operation specialized in agglomerated coffee—a process that creates granules with better dissolution and mouthfeel. It was high-tech, high-touch manufacturing that justified Swiss costs. More strategically, it gave CCL a European Union base, simplifying regulatory compliance and logistics for their largest export market.

By 2015, CCL was running a complex global orchestra. Green coffee beans from Africa and South America arrived at three manufacturing hubs. Each facility had its specialization—India for scale and variety, Vietnam for Robusta-based blends, Switzerland for premium European products. Orders were dynamically routed based on capacity, cost, and customer preference.

The integration challenges were immense. Three facilities meant three regulatory regimes, three cultures, three sets of labor laws. Srishant spent months shuttling between locations, standardizing processes while respecting local contexts. The Swiss wanted precision and documentation. The Vietnamese valued relationships and flexibility. Indians brought jugaad—creative problem-solving. The magic was making these differences complementary rather than conflicting. By 2020, the results spoke for themselves. CCL today has four manufacturing plants, two in India and one each in Vietnam and Switzerland. The Vietnam expansion continued to accelerate—in January 2023, the Board approved the proposal of Ngon Coffee Company for setting up of 6000 TPA Freeze Dried Coffee Manufacturing Facility within the existing premises at Dak Lak Province, Vietnam at an estimated project cost of USD 50 Million.

The global footprint wasn't just about capacity—it was about credibility. When European buyers visited the Swiss facility, they saw precision. When Asian customers toured Vietnam, they witnessed scale. When global brands came to India, they discovered innovation. CCL had become what business schools call a "glocal" company—globally present, locally excellent.

VI. The B2C Pivot: Continental Coffee Brand (2016-Present)

For two decades, CCL was coffee's best-kept secret. They had created a library of more than 1,000 unique blends of coffee for customers over the years. Each blend represented hours of experimentation, customer feedback, market understanding. It was intellectual property worth billions, locked away in formula books and production databases.

By 2016, the question became inevitable: Why are we making everyone else famous?

The boardroom debates were fierce. Launching a consumer brand meant competing with clients. It meant marketing expenses that could destroy margins. It meant transitioning from B2B's predictable orders to B2C's chaotic consumer preferences. Conservative board members pointed to countless B2B companies that had failed trying to go direct-to-consumer.

But Srishant saw it differently. The Indian coffee market was exploding—urbanization, café culture, premiumization. CCL had technology, quality, cost advantages. Most importantly, they had knowledge—those thousand blends weren't just recipes; they were a map of global coffee preferences. If anyone could crack the Indian consumer market, it was them.

In 2016, the company took a bold step forward by launching 'Continental Coffee'. The name was deliberate—not CCL Coffee, which would mean nothing to consumers, but Continental, evoking sophistication and global standards. Their offerings ranged across Instant Coffee, Freeze Dried, Roast & Ground and Premix.

The transformation required more than just slapping a label on existing products. CCL made significant investments in various areas such as supply chain management, packaging, sales, and marketing teams. For a company that had never hired a brand manager, suddenly they were recruiting from HUL and Nestlé. Additionally, the coffee major established a strong network of distributors and retailers to establish and reinforce their presence in the B2C market segment.

The results exceeded expectations: In a short period of time, in a market dominated by two significant players, Continental Coffee stood at the No.3 position in the Indian market. This wasn't just market share—it was validation that B2B excellence could translate to B2C success.

The ambition didn't stop at India's borders. In June 2023, CCL acquired 6 coffee brands from Sweden-based coffee roasters Lofbergs Group. This acquisition is part of CCL's strategy to strengthen their B2C business and accelerate growth globally giving them access to major supermarkets in the UK—Europe's largest instant coffee market.

But perhaps the boldest move was yet to come. CCL entered the plant-based protein snacks category with the brand Greenbird under which it launched 100% vegetarian products like 'Chicken like nuggets', 'chicken like sausages', 'chicken like kababs' and 'keema'. For a coffee company to enter plant-based proteins seemed bizarre—until you understood CCL's deeper strategy. They weren't building a coffee company; they were building an FMCG conglomerate.

VII. Scale & Market Position Today

Stand in CCL's Duggirala facility today and you're witnessing industrial poetry. From that initial 3,600 TPA capacity in 1995, the company scaled up, reaching a staggering capacity of 55,000 TPA in the last 28 years. The numbers tell a story of relentless expansion, but the real achievement is maintaining quality at this scale.

Market Cap: 11,541 Crore, Revenue: 3,388 Cr, Profit: 311 Cr—these aren't just financial metrics; they represent CCL's transformation into a billion-dollar company in market capitalisation. To put this in perspective, CCL's market cap exceeds many established FMCG brands despite being virtually unknown to most Indian consumers.

The company has become a powerful player in the global coffee industry with B2B customer base across more than 100 countries. This isn't just export—it's deep integration into global supply chains. When Starbucks launches a new instant variant, CCL might be formulating it. When a German discounter needs private label coffee, CCL's Swiss facility springs into action.

The product portfolio reads like a coffee encyclopedia: Spray Dried Coffee Powder, Spray-Dried Agglomerated Coffee, Freeze Dried Coffee, Freeze Concentrated Liquid Coffee, Roast & Ground Coffee, Roasted Coffee Beans, and Premix Coffee. Each category represents different technology, different customers, different margins. It's complexity that would break most companies, but CCL has turned it into competitive advantage.

What's remarkable is CCL's position relative to giants. Nestlé invented instant coffee. JDE Peet's owns iconic brands like Jacobs and Douwe Egberts. Yet CCL claims to be the world's largest private label manufacturer—David not just competing with Goliaths, but in many ways, supplying them.

The competitive positioning versus Indian peers is equally interesting. Tata Consumer Products gets the headlines with Tata Coffee. But CCL's pure-play focus on instant coffee, combined with global scale, gives them advantages in procurement, technology, and customer relationships that diversified FMCG players struggle to match.

VIII. Business Model & Operational Excellence

CCL's business model is deceptively simple: source green coffee beans, apply technology to create instant coffee, sell globally. But execution complexity rivals semiconductor manufacturing. Challa Rajendra Prasad completed his Mechanical Engineering from Osmania University in 1975. He set up several units connected with packaging materials, tubes and ducts, Information Technology, real estate and construction—this engineering mindset permeates CCL's operations.

The sourcing strategy alone requires PhD-level understanding of global coffee markets. Arabica from Colombia behaves differently from Ethiopian beans. Vietnamese Robusta has different oil content than Indian varieties. CCL sources from India, Africa, South America—each origin requiring different relationships, payment terms, quality controls. Currency hedging, commodity futures, weather monitoring—it's financial engineering married to agricultural expertise.

Processing is where science meets art. Instant coffee seems simple—just add water—but creating it requires multiple steps: cleaning, roasting, grinding, extracting, concentrating, drying. Each step has dozens of variables. Roasting temperature off by two degrees? The entire batch tastes burnt. Extraction time too long? You get bitterness without body. CCL has codified this expertise into processes, but it took decades of learning.

Srishant has been transforming the company from being 'people driven' to 'process driven' resulting in reduced human errors, enhanced standardization and seamless operations. This isn't about replacing craftsmen with machines—it's about capturing craftsmanship in systems. When a master roaster retires, their expertise doesn't walk out the door; it's embedded in standard operating procedures.

The manufacturing flexibility is CCL's hidden weapon. The same facility can produce premium freeze-dried for Switzerland and economy spray-dried for Africa. Changeovers that take competitors days, CCL does in hours. This agility allows them to serve hundred-container orders for Walmart and single-pallet shipments for boutique roasters.

Quality control borders on paranoia. Every batch undergoes sensory evaluation—trained tasters who can detect minute variations. Laboratory testing for moisture, caffeine content, microbiological parameters. Traceability systems that can track a consumer complaint back to specific farms. For private label manufacturers, one quality failure doesn't just lose a sale—it destroys relationships built over decades.

The capital efficiency deserves attention. While competitors build brands requiring massive marketing spend, CCL invests in production assets that generate returns for decades. A freeze-drying line costs millions but runs 24/7 for twenty years. Marketing campaigns cost similar amounts but need constant refresh. It's the difference between buying assets and renting attention.

IX. Playbook: Key Business Lessons

CCL's journey offers a masterclass in emerging market strategy, but the lessons aren't what MBA programs typically teach. This is the playbook for building global champions from unlikely origins.

Lesson 1: Value Addition at Origin Changes Everything Prasad's fundamental insight—the untapped potential of Indian-grown coffee being exported without value addition—challenged India's entire export paradigm. For decades, India exported raw materials and imported finished goods. CCL proved you could capture 10x value by processing at origin. This isn't just about coffee—it's about questioning why emerging markets accept commodity supplier status.

Lesson 2: Private Label as Trojan Horse Strategy Conventional wisdom says build a brand, then scale. CCL inverted this—scale first through private label, brand later with accumulated expertise. CCL Products is the world's largest private label coffee manufacturer—they achieved global scale without spending a rupee on consumer advertising. Private label isn't just cost-effective; it's education. Every client teaches you something—German precision, American scale, Japanese quality obsession.

Lesson 3: Technology Timing Beats Technology Leadership CCL didn't invent freeze-drying or spray-drying. But setting up a freeze-dried unit in 2005 was innovative and way ahead of its time for an Indian company. They understood that in emerging markets, you don't need to be first globally—you need to be first locally with proven technology. The arbitrage between global technology maturity and local market readiness creates sustainable advantages.

Lesson 4: Family Business Modernization Without Drama The transition from Prasad to Srishant could have been a soap opera. Instead, it was orchestrated professionally. Mr. Srishant was appointed as the Executive Director of CCL Products (India) Limited in 2005 and elevated to the position of Managing Director in 2014. Nine years as Executive Director before becoming MD—that's apprenticeship, not nepotism. The lesson: succession is a process, not an event.

Lesson 5: B2B/B2C Duality Requires Different DNA Most companies fail trying to straddle B2B and B2C because they require opposing capabilities. B2B rewards consistency, relationships, technical excellence. B2C demands innovation, marketing, consumer insight. CCL succeeded by treating them as separate businesses sharing infrastructure. Continental Coffee has its own team, metrics, culture—it's a startup inside a corporation.

Lesson 6: Geographic Arbitrage in Manufacturing Having facilities in India, Vietnam, and Switzerland isn't about risk diversification—it's about capability arbitrage. India for engineering and scale, Vietnam for raw material access and Asian markets, Switzerland for European credibility and premium products. Each geography contributes unique advantages that competitors with single-country operations can't match.

Lesson 7: Process Excellence Beats Individual Brilliance Transforming the company from being 'people driven' to 'process driven' sounds boring but it's revolutionary. In emerging markets, companies often depend on individual heroes—the genius engineer, the relationship manager who knows everyone. CCL systematically replaced heroes with systems. It's less exciting but infinitely more scalable.

X. Analysis & Investment Case

Let's talk about CCL through an investor's lens—not the promotional fluff, but the hard analysis that determines whether this coffee story is worth your capital.

The Bull Case:

The global coffee consumption narrative is compelling. Coffee is the world's second-most traded commodity after oil. Consumption grows 2-3% annually, but instant coffee in emerging markets grows faster—5-7% as urbanization accelerates and café culture spreads. CCL is perfectly positioned for this secular trend.

The company presently produces 30,000 tn of freeze-dried goods annually in Vietnam, with expansion underway. The capital allocation is disciplined—unless there was a clear commitment from customers, CCL Products will never go for expansion. The company has secured a five-year commitment for the offtake from the new capacity in Vietnam. This isn't speculative capacity addition; it's demand-backed expansion.

The B2C opportunity in India remains nascent. Continental Coffee at #3 position sounds impressive, but the market is tiny compared to potential. As Indians shift from tea to coffee, from instant to premium, CCL's manufacturing advantage could translate to market share gains. The acquired Swedish brands provide European distribution—suddenly CCL has global B2C optionality.

Operating leverage is kicking in. Fixed costs spread over growing volumes mean margin expansion. The freeze-dried facilities running at higher utilization drive profitability. Every incremental tonne sold drops disproportionately to the bottom line.

The Bear Case:

But let's address the elephant in the room: Stock is trading at 5.87 times its book value. For a manufacturing company, that's expensive. The market is pricing in perfection—any execution stumble could trigger re-rating.

Coffee commodity volatility is real. Green coffee prices can swing 50% in a year based on Brazilian weather or Vietnamese politics. Yes, CCL passes through costs, but there's always lag. In volatile periods, working capital balloons and margins compress.

Competition is intensifying. Nestlé and JDE Peet's aren't sleeping. They're investing in capacity, buying brands, defending turf. Regional players in Vietnam and Brazil are scaling up. The private label moat isn't impregnable—clients can switch suppliers.

Currency risk cuts both ways. CCL benefits from rupee depreciation on exports, but raw material imports become expensive. The Vietnam and Switzerland operations add complexity—multiple currency exposures that can't be perfectly hedged.

The B2C adventure could disappoint. Building brands requires different muscles than manufacturing. Marketing expenses could explode without corresponding revenue gains. Channel conflicts between B2B and B2C businesses could emerge. Continental Coffee could remain perpetually #3, burning cash chasing leaders.

The Valuation Debate:

ROCE at 13.1% and ROE at 17.0% are decent but not spectacular. For the valuations CCL commands, investors expect improvement. The dividend yield at 0.58% offers little cushion—this is a growth story, not income play.

The key question: Is CCL a commodity processor deserving industrial multiples, or an emerging FMCG player warranting consumer valuations? The market seems to be betting on transformation, but execution risk remains.

XI. Future Outlook & Strategic Options

CCL will pursue its dream goal of becoming an FMCG company with a basket of brands. This isn't just corporate ambition—it's existential evolution. Pure-play instant coffee manufacturing, however excellent, has growth limits. The FMCG transformation opens infinite possibilities.

The immediate future is about execution. CCL Products India Ltd expects its newly announced $50-mln freeze-dried coffee unit in Vietnam to be ready by the December quarter of 2024-25. CCL Products is setting up new manufacturing plant at Continental Coffee Park in Kuvvakolli village in Tirupati district in Andhra Pradesh, with an investment of Rs 400 crore. These aren't just capacity additions—they're capability expansions.

The ready-to-drink (RTD) coffee opportunity looms large. Globally, RTD coffee is exploding—convenience culture meets coffee obsession. CCL has the coffee expertise but needs packaging technology, cold chain distribution, and different marketing. Build, buy, or partner? Each path has merits and risks.

Sustainability isn't just corporate responsibility—it's business necessity. European clients increasingly demand carbon-neutral supply chains, ethical sourcing, circular packaging. CCL's investment in sustainable practices isn't altruism; it's table stakes for global business.

Digital transformation offers efficiency gains. AI-powered demand forecasting could optimize inventory. IoT sensors could monitor roasting in real-time. Blockchain could provide bean-to-cup traceability. But technology for technology's sake is a trap—CCL must choose investments that drive tangible returns.

The M&A pipeline deserves attention. The Lofbergs acquisition proved CCL can integrate brands. More opportunities exist—distressed European roasters, emerging market instant coffee players, adjacent categories like tea or chocolate. But acquisition discipline matters more than acquisition activity.

The strategic options crystallize around a central question: Does CCL remain a focused coffee player leveraging scale and expertise, or does it become a diversified FMCG company using coffee as the core? The answer will determine whether CCL remains a hidden champion or emerges as a household name.

The India opportunity alone could drive decades of growth. Per capita coffee consumption remains a fraction of global averages. Urbanization, rising incomes, and cultural shifts favor coffee adoption. If CCL can capture even a portion of this growth through Continental Coffee while maintaining B2B leadership, the current valuation might prove conservative.

But execution separates vision from value creation. CCL must manage multiple transitions simultaneously—B2B to B2C, manufacturing to marketing, Indian to global, coffee to FMCG. Each transition carries risk. Success requires not just operational excellence but strategic clarity and organizational capability.

The CCL story ultimately is about transformation—of coffee beans into instant granules, of an Indian company into a global player, of a finance firm into a manufacturing powerhouse, of a B2B supplier into an FMCG aspirant. Whether the next transformation succeeds will determine if CCL becomes India's answer to JDE Peet's or remains the best company you've never heard of.

For investors, CCL represents a fascinating study in emerging market capitalism. It's a company that succeeded by being invisible, now trying to become visible. It built global scale without global brands, created technology leadership without technology invention, achieved market leadership without market recognition.

The question isn't whether CCL is a good company—operational excellence is evident. The question is whether it's a good investment at current valuations. The answer depends on your belief in India's coffee consumption story, CCL's FMCG transformation capability, and management's ability to execute multiple strategic initiatives simultaneously.

What's undeniable is that CCL has already achieved something remarkable: proving that an Indian company can dominate a global industry through operational excellence, strategic focus, and patient capital allocation. Whether the next chapter matches the first remains to be seen, but the playbook CCL has written deserves study by every emerging market entrepreneur and investor.

The coffee industry often talks about the "first crack" and "second crack"—stages in roasting where beans transform character. CCL has successfully navigated its first crack, transforming from finance to manufacturing, from domestic to global, from small to scale. The second crack—from B2B to B2C, from manufacturing to FMCG, from hidden to visible—is underway. Whether it produces the perfect roast or bitter aftertaste will determine CCL's next decade.

XII. Recent News

The quarterly numbers paint a picture of robust momentum. In the September 2024 quarter, CCL's consolidated net profit rose 21.51% to Rs 73.95 crore compared to Rs 60.86 crore in September 2023, while sales jumped 21.50% to Rs 738.20 crore versus Rs 607.57 crore in the previous year period. The consistency is impressive—double-digit growth in both revenue and profits, suggesting the business model is firing on all cylinders.

But it's the Q4 FY2024 results that truly showcase CCL's acceleration. Revenue jumped 14.89% year-over-year to ₹839.65 Cr in Q4 2024-2025, while net profit surged 56.19% to ₹101.87 Cr. More remarkably, net profit margins expanded 35.95% year-over-year to 12.13%—a massive margin expansion that suggests pricing power and operational leverage are both working in CCL's favor.

The stock market has taken notice. On November 6, 2024, CCL Products saw a significant increase in its stock price, outperforming the sector by 7.6%, opening with a gain of 2.49% and reaching an intraday high of Rs 722.75. Over the last month, CCL's share price moved up 3.29%, over three months up 7.80%, and over twelve months up 22.85%—solid returns that reflect growing investor confidence.

Corporate actions reveal strategic priorities. In August 2024, CCL acquired 26% of Mukkonda Renewables for Rs 9.57 crore to access approximately 7.9 MW renewable power—a move toward sustainability that's both ESG-friendly and cost-effective. The renewable energy investment isn't just greenwashing; it's about securing long-term cost advantages in an energy-intensive manufacturing process.

The Vietnam expansion continues to accelerate at breakneck pace. The Board's January 2023 approval for a 6000 TPA Freeze Dried Coffee Manufacturing Facility in Dak Lak Province at USD 50 million is now bearing fruit, with the facility expected to be operational by December quarter of 2024-25. This isn't speculative capacity—management has secured five-year offtake commitments before breaking ground.

Meanwhile, the domestic expansion proceeds apace. CCL is setting up a new manufacturing plant at Continental Coffee Park in Kuvvakolli village, Tirupati district, with an investment of Rs 400 crore. The location choice is strategic—proximity to ports, available skilled labor, and state government incentives all factor into the decision.

Leadership transitions have been managed smoothly. The appointment of new CFO in January 2025 following the previous CFO's resignation shows succession planning extends beyond family members. The company continues its ESOP allotments, aligning employee interests with shareholder value—a progressive approach for an Indian manufacturing company.

CEO Praveen Jaipuriar's recent comments reveal strategic thinking: "Focus only on domestic brands through e-commerce, focus on maintaining profit per kg"—this isn't about volume at any cost but profitable growth. The emphasis on e-commerce for domestic brands shows CCL understands changing distribution dynamics.

The coffee commodity environment has turned favorable. "Coffee demand is strong...prices fall by 10-15%" noted Jaipuriar in late 2022. This combination—strong demand with falling raw material costs—is the sweet spot for processors like CCL. While green coffee prices fluctuate, CCL's ability to pass through costs while maintaining margins demonstrates pricing discipline.

Product innovation continues quietly. In 2023, CCL Products launched Continental Greenbird products in the meat product category—the plant-based protein play that seemed bizarre initially but makes strategic sense. It leverages CCL's B2C distribution, targets health-conscious consumers, and diversifies revenue streams without massive capital investment.

XIII. Links & Resources

Primary Sources: - CCL Products Official Website: www.cclproducts.com - Annual Reports: Available on company website investor section - BSE Filings: BSE Code 519600 - NSE Symbol: CCL

Industry Research: - International Coffee Organization (ICO) Reports - Indian Coffee Board Statistics - Euromonitor International Coffee Reports - Technavio Global Instant Coffee Market Analysis

Financial Analysis: - Quarterly Results and Conference Call Transcripts - Antique Stockbroking Research Reports - ICICI Direct Coverage - Motilal Oswal Equity Research

Books on Indian Business History: - "India's Business Houses" by Dwijendra Tripathi - "The Indian Family Business" by Kavil Ramachandran - "From Trade to Territory" examining colonial coffee trade

Global Coffee Industry Resources: - Specialty Coffee Association Reports - World Coffee Research Publications - Coffee Quality Institute Standards - Global Coffee Platform Sustainability Reports

Private Label Manufacturing Studies: - "Private Label Strategy" by Nirmalya Kumar - McKinsey Reports on Private Label Growth - Nielsen Private Label Reports - PLMA International Research

Family Business Literature: - "Generation to Generation" by Kelin Gersick - Indian School of Business Family Business Studies - Harvard Business Review Family Business Collection

FMCG Industry Analysis: - India Brand Equity Foundation (IBEF) FMCG Reports - Deloitte India Consumer Products Analysis - PwC India Retail and Consumer Reports - KPMG FMCG in India Reports

Conclusion: The Acquired Playbook Applied

If Ben and David from Acquired were to distill CCL's story into their signature analysis, they'd likely focus on three transformative insights that separate this from typical emerging market success stories.

First, the counter-positioning power play. While every Indian company in the 1990s wanted to build brands, CCL chose invisibility. This wasn't weakness—it was strategy. By becoming the manufacturing backbone for global brands, they learned without paying tuition. Every client became a free MBA program. Nestlé taught them quality systems. Unilever taught them scale. Starbucks taught them premiumization. By the time CCL launched Continental Coffee in 2016, they had two decades of accumulated wisdom—paid for by their customers.

Second, the value chain inversion. Conventional wisdom says you start at the bottom of the value chain and work up. CCL started at the top—manufacturing the finished product—and worked backwards. They began with instant coffee, then moved to roasting, and only recently started thinking about farming partnerships. This inversion gave them pricing power from day one. They captured the highest margin part of the chain first, then used those profits to integrate backwards.

Third, the geographic arbitrage model that goes beyond cost. Yes, India offers lower costs than Switzerland. But CCL's genius was recognizing that geography provides more than cost advantages—it provides capability advantages. Indian engineers solve problems differently than Swiss engineers. Vietnamese workers have different skills than Indian workers. CCL built a distributed capability network where each node contributes unique value, not just cheaper labor.

The financials validate the strategy. From a hire-purchase finance company to an 11,785 crore market cap coffee giant—that's not just growth; it's metamorphosis. The numbers that matter: 55,000 TPA capacity across four facilities, presence in 100+ countries, 1000+ unique blends, #3 position in Indian retail in just seven years. These aren't vanity metrics—they represent deep competitive moats.

But here's where the Acquired lens gets interesting: CCL might be playing an entirely different game than investors realize. The market sees a coffee company with FMCG aspirations. But what if CCL is building something more fundamental—a platform for turning agricultural commodities into branded consumer products? Coffee is just the first app on this platform. Plant-based proteins are the second. What's the third, fourth, fifth?

The bear case is real—valuation is rich, competition is fierce, commodity volatility is inherent. But the bull case is about transformation potential. If CCL can replicate their coffee playbook in adjacent categories, current valuation might be cheap. If they can't, it's expensive. The binary outcome makes this fascinating.

The strategic options crystallize around a fundamental choice: depth or breadth? Does CCL double down on coffee, leveraging their undisputed expertise to dominate globally? Or do they become India's next FMCG conglomerate, using coffee profits to fund diversification? History suggests the focused players win—Starbucks, not General Foods. But emerging markets might be different—Tata and Reliance succeeded through diversification.

The succession from Prasad to Srishant provides a clue. First-generation entrepreneurs build; second-generation leaders scale. Prasad built a coffee company. Srishant is building something larger—though what exactly remains unclear. The Greenbird plant-protein venture and Lofbergs acquisition suggest experimentation, not just expansion.

For investors, CCL represents a test case in emerging market investing. Can operational excellence justify premium valuations? Can B2B companies successfully pivot to B2C? Can family businesses professionalize without losing entrepreneurial edge? The answers determine not just CCL's future but provide a template for how emerging market companies can build global champions.

The ultimate Acquired insight might be this: CCL succeeded by being boring. No flashy acquisitions, no celebrity endorsements, no aggressive marketing. Just relentless focus on making better coffee cheaper. In a world obsessed with disruption, CCL proves that consistent execution of obvious strategies—done exceptionally well—creates enormous value.

Whether CCL becomes India's Nestlé or remains the best company you've never heard of depends on choices being made in boardrooms from Hyderabad to Hanoi. But one thing is certain: they've already written a playbook for how emerging market manufacturers can compete globally—not by being cheaper, but by being better.

The coffee industry has a saying: "From seed to cup." CCL has mastered everything except the seed. Their next decade will determine if they need to own that too, or if controlling cup to lip—the consumer relationship—matters more. That strategic choice, more than quarterly earnings or commodity prices, will determine if CCL's transformation from invisible supplier to visible brand creates lasting value or proves that some companies are destined to remain behind the scenes.

In true Acquired fashion, the story isn't really about coffee—it's about the patterns of business success. CCL demonstrates that in the global economy, comparative advantage isn't static. An Indian company can out-Swiss the Swiss at precision manufacturing. A B2B supplier can build consumer brands. A family business can professionalize while remaining entrepreneurial. These inversions of conventional wisdom are what make CCL not just an investment opportunity, but a business school case study in real-time.

The next chapters of the CCL story are being written now—in Vietnamese factories coming online, in Swiss facilities pursuing automation, in Indian laboratories developing new blends, in boardrooms debating strategy. Whether those chapters describe continued transformation or reversion to the mean will determine if CCL joins the pantheon of great global companies or remains a remarkable but ultimately regional success story.

For now, CCL stands as proof that the Acquired playbook—focus, execution, patient capital allocation, strategic positioning—works everywhere, even in the coffee fields of Andhra Pradesh. The question isn't whether CCL has been successful—that's undeniable. The question is whether their best days are behind or ahead. Given their track record of transformation, betting against them seems unwise. But at current valuations, betting on them requires faith that the next transformation will be as successful as the last.

That's the ultimate investment question: Is CCL's transformation muscle memory or lucky timing? The answer lies not in spreadsheets but in strategy—and only time will tell if the strategy that built a billion-dollar coffee company can build something even greater.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube