Emami: The Ayurvedic FMCG Empire That Challenged MNCs

I. Introduction & Cold Open

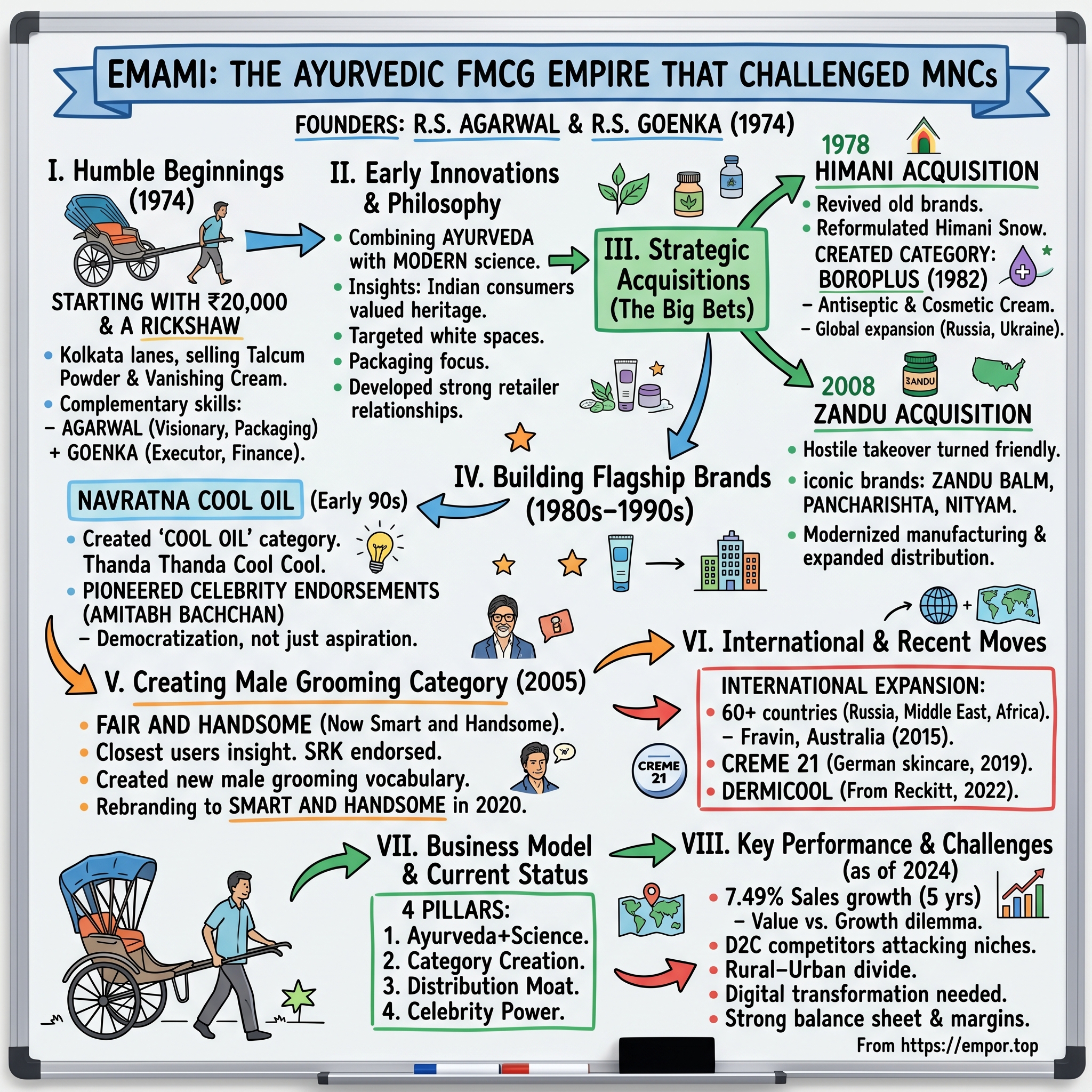

Picture this: Kolkata, 1974. Two chartered accountants at the prestigious Birla Group are having tea in their wood-paneled office, surrounded by the trappings of corporate success—leather chairs, mahogany desks, the hum of typewriters echoing through marble corridors. They're discussing an audacious plan that would make their colleagues think they'd lost their minds. R.S. Agarwal leans forward and tells his friend R.S. Goenka: "What if we leave all this behind and start selling cosmetics from a rickshaw?"

This wasn't just career suicide in 1970s India—it was financial madness. The Indian FMCG market was a playground for multinational giants like Hindustan Lever and Colgate. Local players were either struggling regional manufacturers or sick units waiting for bankruptcy. Yet these two men would go on to build Emami, a ₹20,000 crore empire that would create entirely new product categories, acquire century-old brands, and challenge the very foundations of how consumer goods are marketed in India.

Today, when you walk into any of India's 4.5 million retail outlets—from air-conditioned supermarkets in Mumbai to tiny kirana stores in Bihar—you'll find Emami's products. BoroPlus antiseptic cream sits next to Band-Aid. Navratna cool oil shares shelf space with Parachute. Fair and Handsome (now Smart and Handsome) competes with Nivea. Zandu Balm fights Tiger Balm for counter space. The company commands a market capitalization of ₹25,077 crores, operates seven manufacturing units across India plus one overseas, and exports to over 60 nations.

But here's what makes this story truly remarkable: Emami didn't just succeed by copying Western formulations or undercutting on price. They built their empire on a counterintuitive insight—that Indian consumers, even as they modernized, deeply valued their ayurvedic heritage. They weren't selling products; they were selling a philosophy that married 5,000-year-old wisdom with modern science. And they did it all starting with just ₹20,000 in capital—less than what a premium car costs today.

The central question isn't just how two accountants built a successful FMCG company. It's how they identified white spaces that multinationals ignored, created categories that didn't exist, turned around dying brands that others had written off, and built a distribution network that reaches the remotest corners of India. This is a story about seeing opportunity where others saw impossibility, about the power of patient capital in a market obsessed with quarterly results, and about building Indian brands that could stand toe-to-toe with century-old global giants.

II. The Founders' Story: Leaving the Birla Group

The year was 1974, and India was a very different place. The License Raj strangled entrepreneurship. Foreign exchange was scarce. Consumer goods meant whatever Hindustan Lever or Colgate decided to sell you. In this environment, R.S. Agarwal and R.S. Goenka were living what most Indians would consider the dream—senior positions as chartered accountants in the Birla Group, one of India's most prestigious business houses.

But something gnawed at them during those long evenings in Kolkata's business district. They watched multinationals dominate every category, from soaps to toothpaste, while Indian manufacturers struggled with outdated technology and limited capital. More importantly, they noticed something the MNCs missed—Indian consumers were using home remedies and ayurvedic preparations alongside modern products. Mothers still applied turmeric and sandalwood paste on their children's skin. Grandmothers trusted neem and tulsi more than any antibiotic cream. There was an entire universe of traditional knowledge that modern marketing had ignored.

The friendship between the two R.S.'s (as they became known in Kolkata business circles) was built on complementary skills. Agarwal was the visionary—constantly sketching product ideas, obsessing over packaging, studying consumer behavior with an anthropologist's eye. Goenka was the executor—a financial wizard who could make one rupee do the work of ten, who understood cash flows like a poet understands meter. Together, they saw an opening that required not millions in capital but something more valuable: the courage to challenge established players with Indian innovation.

Their philosophy was revolutionary for its time: combine the trust of Ayurveda with the convenience of modern formulations. While Hindustan Lever was selling Pond's cold cream with advertisements featuring Western models, they envisioned products that spoke to Indian sensibilities—a cream that combined antiseptic properties with traditional ingredients like neem and turmeric, oils that incorporated cooling herbs mentioned in ancient texts, medicines that modernized age-old remedies.

The name they chose for their venture revealed their ambition. EMAMI was inspired by the Italian word 'Amami,' meaning "Love Me." But in typical Indian fashion, they gave it their own twist—it also stood for their initials (EM for Agarwal and Goenka, AMI suggesting friendship). They registered Kemco Chemicals with a capital of ₹20,000—money they'd scraped together from personal savings and small loans from sympathetic relatives who thought they were throwing away promising careers.

Walking out of the Birla Group offices for the last time, briefcases in hand, they faced a torrent of disbelief. Colleagues whispered about mid-life crises. Family members worried about financial security. The business establishment of Kolkata, with its clubs and connections, essentially wrote them off. After all, who leaves the Birlas to sell cosmetics? But Agarwal and Goenka had something their critics lacked—they'd spent years inside the corporate machinery, understanding how big companies thought, where they were blind, and why they moved slowly. They were about to use that knowledge to run circles around giants.

III. Early Days: Building from a Rickshaw

The image is almost cinematic in its absurdity: two former Birla Group executives, still wearing their formal shirts (the ties had been abandoned), loading boxes of talcum powder and vanishing cream onto a hand-pulled rickshaw in the narrow lanes of Burrabazar, Kolkata's chaotic wholesale market. The year was 1974, and this was Emami's entire distribution network—one rickshaw, two founders, and more determination than capital.

Agarwal would later recall those early morning rounds with a mixture of nostalgia and disbelief. They'd start at 5 AM, before the Kolkata humidity became unbearable, visiting small retailers who looked at these educated men with suspicion. "Why should I stock your products when Pond's and Lakme are already selling?" was the constant refrain. The answer came not from sophisticated marketing but from something more basic—relationships and trust. They offered credit terms that MNCs wouldn't match, replaced unsold inventory without questions, and most importantly, they listened to what retailers actually wanted.

The first products were deliberately chosen to compete in established categories—Emami Talcum Powder and Emami Vanishing Cream. But here's where their approach diverged from typical Indian manufacturers who simply created cheaper copies. Agarwal obsessed over packaging with an intensity that seemed irrational given their shoestring budget. He studied French perfume boxes in import stores, analyzing why certain colors and fonts conveyed luxury. He examined Japanese labeling techniques, understanding how information hierarchy influenced perception. The result was packaging that looked international but cost a fraction of imported alternatives.

The vanishing cream formula itself revealed their philosophy. While others were copying Western formulations wholesale, Emami added subtle Indian touches—a hint of sandalwood for fragrance, turmeric extracts for skin brightening. These weren't marketed as features initially (that would come later) but created a subtle differentiation that consumers noticed. "It feels different, more suitable for our skin," became the word-of-mouth feedback that began building their reputation.

By 1976, something remarkable started happening. Orders began exceeding their tiny production capacity. Retailers who had reluctantly given them shelf space were now calling for more stock. The rickshaw was upgraded to a small van (secondhand, naturally). They hired their first employee—a young man from Agarwal's village who would later become their first plant manager. But the real validation came from an unexpected source: Hindustan Lever's internal market research showed a new player eating into their market share in West Bengal. David had gotten Goliath's attention.

The numbers from 1978 tell a story of explosive growth that seemed impossible given their humble beginnings. Emami Vanishing Cream had captured 22% market share nationally—ahead of several established brands. Their talcum powder had become the number two brand in India, trailing only Pond's. This wasn't gradual growth; it was a market disruption that happened so fast, competitors were still trying to understand who these newcomers were.

The distribution strategy they developed during these rickshaw days would become a cornerstone of Emami's success. Unlike MNCs that focused on urban markets and modern trade, they built relationships with small retailers in semi-urban areas. They understood that in India, the local kirana store owner was more than a shopkeeper—he was an influencer who recommended products to customers who trusted his judgment. By treating these retailers as partners rather than just another link in the supply chain, they built a loyalty that money couldn't buy.

But even as success arrived, Agarwal and Goenka knew they were still playing small ball. The real opportunity—the chance to build something transformational—would require a bigger bet. They found it in a dying company that others saw as a liability but they recognized as a sleeping giant.

IV. The Himani Acquisition: First Big Bet (1978)

In 1978, the board of Himani Limited gathered for what many assumed would be their final meeting. The company, founded in the 1880s, had a heritage almost as old as India's first war of independence. Its art deco factory in north Kolkata had once hummed with activity, producing cosmetics that graced the dressing tables of Bengali households for generations. Now it was a "sick unit"—that uniquely Indian classification for companies bleeding money but not quite dead. The machinery was outdated, workers hadn't been paid in months, and creditors were circling like vultures.

When word spread that two young entrepreneurs were interested in acquiring Himani, the reaction was incredulity mixed with pity. Established business houses had already examined and rejected the deal. The liabilities exceeded assets. The brand, while nostalgic, was seen as irrelevant in an era of modern marketing. But Agarwal and Goenka saw something others missed—they saw a brand with latent trust, a production facility that could be modernized, and most importantly, product formulations that contained decades of R&D that would cost millions to replicate.

The financial engineering required to pull off this acquisition would have impressed any private equity firm today. With limited capital (remember, they'd started with just ₹20,000 four years ago), they structured a deal that was part assumption of liabilities, part deferred payments, and part promise of employment to workers who'd been abandoned. They convinced creditors to convert debt to equity, promised suppliers future contracts, and somehow emerged with control of a company many times larger than their original venture.

But acquiring Himani was just the beginning. The real genius lay in what they did next. Instead of simply trying to revive old products, they reimagined the entire portfolio. Himani Snow, a basic cold cream that had been gathering dust in warehouses, was reformulated with glycerin and aromatic oils, repackaged in distinctive blue-and-white containers that stood out on shelves, and marketed as an affordable alternative to Pond's. Within six months, it was flying off shelves in rural markets where Pond's had never bothered to build distribution.

The masterstroke, however, was BoroPlus. Launched in 1982 under the Himani umbrella, this wasn't just another antiseptic cream—it was a category creator. The insight was brilliantly simple: Indian families used Boroline for cuts and burns, but it was medicinal, sticky, and left residue. What if you could create something that had antiseptic properties but felt like a cosmetic cream? What if the same product could be used for dry skin in winter, minor cuts, and as a general-purpose skin cream?

The formulation combined traditional antiseptic ingredients with ayurvedic herbs, creating a product that was uniquely positioned—not quite medicine, not quite cosmetic, but something in between that Indian families hadn't realized they needed until it existed. The marketing was equally innovative. Instead of medical claims that would require regulatory approval, they positioned it as a multipurpose skin cream with antiseptic benefits. The tagline was simple but effective: "Healthy skin, naturally."

The success was staggering. Within five years, BoroPlus wasn't just the largest-selling antiseptic cream in India—it had created an entirely new category that MNCs scrambled to enter. But here's the remarkable part: it also became the largest-selling antiseptic cream in Russia, Ukraine, and Nepal. How did a product created in a renovated factory in Kolkata end up dominating markets from Moscow to Kathmandu? The answer lay in understanding that emerging markets, regardless of geography, had similar needs—affordable, multipurpose products that delivered value without complexity.

The Himani acquisition proved that Agarwal and Goenka weren't just good operators—they were strategic thinkers who could see value where others saw scrap. It established a template they would follow for decades: acquire undervalued assets with strong brand heritage, modernize operations, innovate on formulations, and build distribution in markets that MNCs ignored. This wasn't just business; it was arbitrage on a massive scale.

V. Building Flagship Brands (1980s-1990s)

The 1990s arrived with liberalization, and with it came a flood of international brands. Procter & Gamble entered India. L'Oréal set up shop. Every business magazine predicted the death of Indian FMCG companies. But while others panicked, Agarwal and Goenka saw opportunity. If multinationals were going to play the premium game in urban markets, Emami would own everything else—and they'd do it by building brands that became part of India's cultural fabric.

Navratna Cool Oil, launched in the early 90s under the Himani umbrella, exemplified their approach to brand building. The insight came from a peculiarly Indian habit—applying oil to the head for cooling and relaxation. Traditional coconut oil was messy and had strong regional preferences. Modern hair oils focused on nourishment but ignored the therapeutic aspect. Navratna bridged this gap with a formulation that seemed to come straight from an ayurvedic text—nine herbs including mint, camphor, and thyme that created an actual cooling sensation.

But the masterstroke wasn't the formulation—it was the positioning. Instead of marketing it as another hair oil in a cluttered category, they created the "cool oil" category. The advertising showed stressed executives, tired students, and overworked housewives finding instant relief with Navratna. The tagline "Thanda Thanda Cool Cool" became so embedded in popular culture that it entered everyday vocabulary. Comics joked about it. Movies referenced it. It wasn't just a product; it had become a cultural meme before anyone knew what memes were.

The celebrity endorsement strategy that Emami pioneered during this period deserves its own business school case study. When they signed Amitabh Bachchan in the late 1980s, it wasn't just expensive—it was unprecedented for an Indian FMCG company. But they understood something fundamental about Indian consumers: they didn't just buy products; they bought into aspirations. And who better to embody aspiration than the angry young man who had become India's biggest superstar?

The Bachchan association wasn't a simple endorsement deal. They made him a brand ambassador for the company, not just individual products. His baritone voice saying "Yeh hai asli mardangi" (This is real manliness) for Navratna became iconic. When he suffered his near-fatal accident on the sets of Coolie, Emami's ads featuring him became almost memorial-like, creating an emotional connection that transcended commercial messaging.

In 1995, a crucial transformation occurred. Kemco Chemicals, which had been a partnership firm, was converted into Emami Limited, a public company. This wasn't just a legal restructuring—it was a signal that the rickshaw-pulling days were officially over. They were now ready to play in the big leagues, access capital markets, and think beyond regional expansion. The IPO was oversubscribed 21 times, validating that investors saw the same potential the founders had envisioned two decades earlier.

The southern expansion during this period revealed their strategic patience. South India was different—more literate, higher disposable incomes, and surprisingly, more resistant to North Indian brands. Instead of forcing their existing products, they adapted. They created region-specific variations, signed South Indian celebrities like Madhavan and Surya, and most importantly, built relationships with local distributors who understood the market's nuances. It took five years to become profitable in the South, but once they cracked the code, it became their fastest-growing region.

By the end of the 1990s, Emami had achieved something remarkable. In a market that was supposed to be conquered by multinationals, they had not only survived but thrived. Their brands weren't just products—they were household names. BoroPlus was to antiseptic creams what Xerox was to photocopying. Navratna owned the cool oil category so completely that competitors had essentially given up. The two chartered accountants who'd left the Birla Group had built something that even the Birlas would admire.

VI. Fair and Handsome: Creating a Category (2005)

The conference room at Emami's Kolkata headquarters was tense in early 2004. The research team had just presented findings that would either be Emami's biggest breakthrough or most controversial mistake. Their data showed something shocking: 30-35% of fairness cream users in India were men, applying products in secret, often stealing from their wives' or sisters' supplies. These "closet users," as the research termed them, represented a hundred-million-dollar opportunity that no one was addressing.

The debate that followed would define Emami's next decade. On one side were executives who saw the clear business opportunity—a completely untapped market segment with proven demand. On the other were those who worried about the social implications and potential backlash. Creating a fairness product specifically for men would mean explicitly acknowledging and potentially reinforcing problematic beauty standards. But it would also mean giving men a product designed for their skin type instead of forcing them to use products formulated for women.

Agarwal, now in his sixties but still sharp as ever, made the decisive argument: "We don't create social preferences; we respond to them. If men are already using fairness products, isn't it better to give them something safe and formulated for their skin?" It was pragmatic, perhaps morally ambiguous, but undeniably grounded in market reality.

Fair and Handsome launched in 2005 with a marketing campaign that was both bold and carefully calibrated. They didn't just shrink and repackage women's fairness cream—they created a completely different formulation. Men's skin is 25% thicker, produces more sebum, and has larger pores. The product addressed these differences while delivering the fairness benefit that research showed men wanted. The packaging was aggressively masculine—dark colors, bold fonts, nothing that would seem "borrowed" from the women's category.

The advertising strategy was brilliant in its psychological insight. Instead of showing men being rejected for being dark (a common trope in women's fairness cream ads), they showed confident men becoming more confident. Shah Rukh Khan, at the peak of his stardom, became the face of the brand. His endorsement legitimized what had been a secret desire. The tagline wasn't about becoming fair to get the girl or the job—it was about being your best self. "Hi Handsome!" became a greeting that normalized the conversation around male grooming.

The market response was explosive. Within six months, Fair and Handsome had created a ₹100 crore category. Competitors scrambled to launch their own versions—Hindustan Unilever came out with Fair & Lovely Menz Active, Nivea introduced whitening products for men. But Emami had the first-mover advantage and, more importantly, they had done the groundwork to understand male consumers in a way that others were still catching up to.

The international expansion of Fair and Handsome revealed interesting cultural nuances. In the Middle East, where Indian expatriates formed a significant population, the product flew off shelves. In Southeast Asian markets like Malaysia and Indonesia, local variations were created with different fragrances and textures. In each market, the core insight remained the same—men wanted grooming products designed specifically for them, not adapted from women's ranges.

But by the late 2010s, the conversation around fairness products had shifted dramatically. Social media campaigns like "Dark is Beautiful" gained momentum. Bollywood stars who had once endorsed fairness products publicly regretted it. The same social consciousness that Emami had navigated in 2005 had evolved into outright rejection of colorism. The company faced a choice: defend a successful but increasingly controversial product, or pivot.

The 2020 rebranding from Fair and Handsome to Smart and Handsome was more than cosmetic. It represented a strategic shift from fairness to holistic male grooming. The new portfolio included face washes, moisturizers, and even beard oils—products that addressed grooming needs without the fairness angle. It was a tacit admission that social values had evolved, but also a smart business move to capture the larger male grooming market, projected to reach ₹5,000 crores by 2025.

The Fair and Handsome story encapsulates Emami's greatest strength and its biggest challenge—the ability to identify and serve unmet consumer needs while navigating the complex social responsibilities that come with shaping beauty standards. They had created a category, dominated it for fifteen years, and then evolved it when the time came. That's not just business agility; it's cultural intelligence.

VII. The Zandu Acquisition: Hostile Turned Friendly (2008)

The boardroom battle for Zandu Pharmaceutical Works in 2008 was the stuff of corporate legend—family feuds, hostile takeover attempts, regulatory drama, and ultimately, a deal that would transform Emami from a successful FMCG company into an ayurvedic powerhouse. This wasn't just an acquisition; it was high-stakes corporate theater that played out in courtrooms, regulatory offices, and the business pages of national newspapers.

Zandu's history read like a subcontinental saga. Founded in 1910 by Vaidya Nagindas Shah, it had created iconic brands like Zandu Balm (the Indian answer to Tiger Balm), Pancharishta (an ayurvedic digestive), and Nityam Churna (a natural laxative). By the 2000s, however, the company was caught in a vicious family feud. The Parikh family (descendants of the founders) and the Vaidya family (who had acquired a stake) were locked in a battle for control that had paralyzed operations and destroyed value.

Emami's initial approach in late 2007 was friendly—they offered to buy out the Parikh family's stake and work with the Vaidyas. But the Vaidyas, led by Shriman Vaidya, had their own plans and blocked the deal. What followed was a masterclass in strategic acquisition. Agarwal and Goenka didn't retreat; they escalated. They began accumulating shares from the open market, building a war chest through careful financial planning that wouldn't strain their balance sheet.

The hostile takeover attempt triggered every regulatory alarm. SEBI got involved. The Bombay High Court was petitioned. The Vaidyas claimed the Parikhs didn't have the right to sell. The Parikhs argued the Vaidyas were destroying shareholder value. Meanwhile, Emami quietly kept accumulating shares, staying just within regulatory limits, playing a waiting game that required nerves of steel and deep pockets.

The breakthrough came through financial engineering that was elegant in its simplicity. Emami offered ₹730 crores for Zandu—a price that was too good for the warring families to refuse. But here's the clever part: they structured it as a merger where Zandu's FMCG business would be absorbed into Emami, while the pharmaceutical business would be hived off. This allowed both families to exit with dignity and value, while Emami got exactly what they wanted—the brands and the ayurvedic formulations.

To fund this massive acquisition, Emami raised ₹310 crores through a Qualified Institutional Placement (QIP), demonstrating that capital markets had confidence in their integration capabilities. The terms they negotiated were remarkable—they got 30-year-old inventory included in the deal (valuable for ayurvedic products that improve with age), trademark rights for formulations that weren't even being produced, and most importantly, access to Zandu's network of ayurvedic doctors and vaidyas who provided credibility that money couldn't buy.

The integration of Zandu revealed Emami's operational excellence. Within six months, they had modernized manufacturing processes that hadn't been updated in decades. Zandu Balm, which had been losing market share to Tiger Balm and Amrutanjan, was reformulated with a non-greasy base that didn't stain clothes. Pancharishta, which had been sold in old-fashioned bottles, was repackaged in modern, convenient packaging. Distribution, which had been limited to traditional chemists, was expanded to modern retail.

The financial transformation was stunning. Emami became debt-free within two years of the acquisition—an almost unheard-of achievement for a deal of this size. Zandu's revenues grew 300% in five years. Products that had been stagnating suddenly found new life. Zandu Balm became a ₹200 crore brand. Pancharishta entered new markets in the Middle East where ayurveda was gaining acceptance. The acquisition that many had called overpriced was now looking like the deal of the decade.

But beyond the numbers, the Zandu acquisition marked Emami's evolution from a consumer products company to a wellness company. They now had credibility in ayurveda that went beyond marketing claims—they owned formulations that were centuries old, had access to traditional knowledge that pharmaceutical companies would kill for, and most importantly, they had proven they could take heritage brands and make them relevant for modern consumers.

The hostile-turned-friendly nature of the deal also established Emami's reputation as serious acquirers. They had shown they could play hardball when needed, had the financial muscle to back their ambitions, and the operational capability to integrate complex acquisitions. The two accountants from the Birla Group had just pulled off a deal that would have made any private equity firm proud.

VIII. International Expansion & Recent Acquisitions

The map on the wall of Emami's international division tells a story of unlikely conquests. Colored pins mark their presence across 60+ nations—from Russia where BoroPlus outsells most local brands, to Nigeria where Navratna has become part of the local lexicon, to Bangladesh where their products compete with both Indian and global brands. This wasn't planned expansion following some McKinsey matrix; it was opportunistic growth that followed the Indian diaspora and then transcended it.

The Russia story deserves special attention because it defies conventional wisdom about international expansion. In the early 2000s, when Emami products first appeared in Moscow through grey market imports by Indian traders, the company noticed something odd in their inventory reconciliation—significant quantities were being diverted from Middle East shipments to Russia. Investigation revealed that Indian students and expatriates had created demand that local distributors were meeting through unofficial channels.

Instead of trying to control these grey market sales, Emami did something clever—they legitimized and scaled them. They partnered with local distributors who understood Russian consumers, adapted packaging to include Cyrillic script, and most importantly, tweaked formulations for extreme weather (Russian winters required a different BoroPlus formula than Indian winters). By 2010, Russia had become one of their largest international markets, contributing over ₹100 crores in revenue.

The 2015 acquisition of Fravin, an Australian company, for ₹200 crores marked their first developed market foray. This wasn't about selling BoroPlus to Australians—it was about acquiring manufacturing capabilities and regulatory approvals that would allow them to enter other developed markets. Fravin's portfolio of natural and organic brands also gave them insights into premium positioning that would prove valuable in evolving Indian metro markets.

But the real coup came in March 2022 with the acquisition of Dermicool from Reckitt for ₹432 crores. This wasn't just another brand acquisition—it was a strategic chess move. Dermicool, with its 85% market share in the prickly heat powder category, gave Emami dominance in a summer-specific category that complemented their portfolio perfectly. More importantly, buying from Reckitt—a company several times their size—signaled that Emami had arrived as a serious player in the global M&A market.

The Dermicool integration showcased how sophisticated Emami's acquisition playbook had become. Within months, they had expanded distribution from 100,000 outlets to 500,000. They launched line extensions—Dermicool soap, talc, and even a cream version. They leveraged their celebrity relationships to get Katrina Kaif as brand ambassador. The brand that Reckitt had considered non-core became a ₹500 crore jewel in Emami's crown.

The Creme 21 acquisition from German company Kelso for ₹100 crores represented another strategic angle—acquiring international brands to sell in India. Creme 21, a heritage German skincare brand, gave Emami credibility in the premium segment that their homegrown brands couldn't achieve. It was positioned as "German engineering for Indian skin"—a tagline that cleverly played on Indian respect for German quality while acknowledging local needs.

The international manufacturing footprint expanded strategically. The Sri Lankan facility wasn't just about serving that market—it was about getting preferential access to other South Asian markets through trade agreements. The proposed facility in Egypt wasn't just for the Middle East—it was positioned to serve African markets where regulatory requirements were easier to meet from an Egyptian base.

But perhaps the most interesting aspect of Emami's international expansion was what they didn't do. They didn't try to take Fair and Handsome to Western markets where such products would be culturally toxic. They didn't push ayurvedic products in markets that didn't have cultural context for them. They didn't chase prestige by opening loss-making subsidiaries in London or New York. Every international move had clear strategic logic and a path to profitability.

By 2024, international operations contributed about 15% of revenues but over 20% of profits—higher margins compensating for higher complexity. The 4.5 million retail touchpoints in India were complemented by selective but profitable international presence. The company that started with a rickshaw in Kolkata's streets had products in Moscow's supermarkets and Cairo's pharmacies.

IX. Business Model & Strategy Analysis

Strip away the glossy annual reports and celebrity endorsements, and Emami's business model reveals something profound about building wealth in emerging markets. This isn't a story of technological disruption or network effects—it's about understanding consumer psychology at a granular level and building distribution networks that reach places Amazon still can't. The model rests on four pillars that seem simple but are devilishly hard to execute.

First, the Ayurveda-plus-science positioning. While Western brands spent millions trying to convince Indians that their formulations were superior, Emami flipped the script. They took trusted traditional ingredients—neem, turmeric, camphor—and modernized delivery mechanisms. BoroPlus combined antiseptic properties with ayurvedic herbs. Navratna infused cooling oils with nine traditional herbs. This wasn't just marketing; it was cultural arbitrage. They understood that Indian consumers wanted progress, not abandonment of tradition.

Second, the category creation strategy. Instead of competing in crowded segments, Emami consistently identified white spaces and built categories around them. Cool oil didn't exist before Navratna. Men's fairness cream was a taboo nobody would touch. Antiseptic cream that doubled as cosmetic was an oxymoron. By creating categories rather than competing in them, they could define the rules, set price points, and achieve margins that would make FMCG giants envious.

Third, the capital efficiency is staggering. With a market cap of ₹25,077 crores and revenues of ₹3,807 crores, the company is almost debt-free. They've maintained a healthy dividend payout of 52.5% while delivering a 3-year average ROE of 29.9%. This isn't achieved through financial engineering but through operational excellence—seven manufacturing units producing hundreds of SKUs, yet maintaining ROCE above 30%.

The distribution architecture deserves special attention. Those 4.5 million retail touchpoints aren't just numbers—they represent relationships built over decades. In India, where organized retail still accounts for less than 15% of FMCG sales, the kirana store owner is king. Emami understood this when multinationals were still trying to replicate Western retail models. They offered credit terms that worked for small retailers, replaced unsold inventory without questions, and most importantly, treated these shopkeepers as partners rather than mere channel partners.

The celebrity endorsement strategy, pioneered with Amitabh Bachchan and perfected with Shah Rukh Khan, wasn't just about star power. It was about lending aspiration to everyday products. When Bachchan said "Thanda Thanda Cool Cool" for Navratna, he wasn't just selling oil—he was democratizing luxury. A rickshaw driver could use the same product as India's biggest superstar. This psychological positioning is worth more than any product innovation.

But the numbers tell a more complex story about current challenges. The company has delivered poor sales growth of 7.49% over the past five years. While Q3 FY2025 showed revenue of ₹1,064.41 crores with 5.07% year-over-year growth and 16.69% sequential quarterly growth, this is hardly the explosive growth of earlier decades. Net profit grew 7.96% year-over-year to ₹278.99 crores with impressive 31.19% sequential growth, suggesting improving operational efficiency even as top-line growth remains modest.

The margin story is more encouraging. Net profit margins improved to 26.21% in Q3 FY2025, up 2.75% year-over-year and 12.42% sequentially. For a company competing with both MNCs and aggressive D2C brands, maintaining margins above 25% while keeping prices competitive is no small feat. This is where the ayurvedic positioning pays dividends—consumers are willing to pay premium for perceived natural benefits.

The acquisition strategy continues to evolve. The Dermicool purchase from Reckitt for ₹432 crores in 2022 showed they could still identify undervalued assets. A brand that Reckitt considered non-core became a ₹500 crore revenue generator within two years under Emami's management. This isn't just about buying brands—it's about understanding which brands have latent potential that current owners can't or won't unlock.

International operations contribute about 15% of revenues but over 20% of profits—a reflection of premium pricing power in markets where "Made in India" ayurvedic products carry exotic appeal. The Russia story is particularly instructive. By adapting formulations for extreme weather and partnering with local distributors who understood Russian consumers, they built a ₹100 crore business in a market most Indian companies wouldn't dare enter.

The strategic pivot from Fair and Handsome to Smart and Handsome in 2020 reveals both vulnerability and adaptability. They read the cultural zeitgeist, understood that fairness products were becoming toxic, and pivoted to broader male grooming—a market projected to reach ₹5,000 crores by 2025. Not every company has the courage to rebrand a successful product at its peak.

Yet challenges loom large. D2C brands are attacking specific niches with digital-first strategies and influencer marketing that resonates with Gen Z. Urban consumption, which should be their growth driver, remains subdued. The company's digital transformation initiatives are still playing catch-up to digital-native competitors. Most concerning is the growth trajectory—high single digits in a market where new-age brands are growing at 50-100% annually.

The investment case presents a classic value-versus-growth dilemma. The company trades at relatively reasonable multiples given its profitability, but growth concerns cap upside potential. The debt-free balance sheet provides cushion for aggressive expansion or acquisitions, but management has been conservative, preferring steady dividends over bold bets.

For fundamental investors, Emami represents a study in contradictions. It's a company with exceptional execution capabilities operating in a structurally attractive market, yet struggling to reignite growth. It has brands that are household names but faces relevance challenges with younger consumers. It generates cash like a machine but deploys it conservatively in an era demanding aggression.

X. Current Performance & Challenges

The morning of January 27, 2025, Emami's board gathered to approve Q3 results that would encapsulate both the promise and predicament of Indian FMCG companies in the current era. Vice Chairman Harsha V Agarwal announced "healthy 9% growth in our core domestic business, driven by a healthy 6% increase in volume in Q3FY25," marking "the second quarter with high single-digit growth, coupled with expansion in both Gross margins and EBITDA margins despite rising input costs". The numbers seemed encouraging, yet the stock market's response—a 25% decline over the past year—suggested deeper concerns.

The rural-urban divide has become Emami's most pressing challenge. While international business showed resilience with double-digit growth (excluding Bangladesh), the domestic story was mixed. Modern trade, e-commerce, and institutional sales now contribute 26.6% to domestic business, a 190-basis point increase in the first half of FY2025. This shift toward organized retail, while positive for margins, exposed a vulnerability—Emami's traditional strength lay in rural and semi-urban markets where organized retail barely exists.

Management's commentary revealed a business in transition. Vice Chairman Mohan Goenka remained optimistic: "We remain committed to achieving high single-digit revenue growth and double-digit EBITDA growth for FY25. The Q3 relaunch of Fair and Handsome and focused efforts on Kesh King strengthen our confidence in driving H2 growth. With a favourable winter forecast, we expect strong performance from our winter portfolio". Yet this optimism was tempered by ground realities—consumption patterns had fundamentally shifted post-pandemic.

The digital transformation challenge looms larger than any competitor. While Emami built its empire on 4.5 million physical touchpoints, young consumers increasingly shop online, influenced by Instagram reels rather than television commercials. D2C brands like Mamaearth, Wow Skin Science, and The Man Company are eating into market share with targeted digital marketing and influencer partnerships that cost a fraction of celebrity endorsements. Emami's response—launching digital-first brands and strengthening e-commerce presence—feels reactive rather than proactive.

The Kesh King rejuvenation effort exemplifies both the potential and difficulty of reviving legacy brands. Once a ₹300 crore brand, Kesh King had been losing relevance despite its strong ayurvedic credentials. The company's renewed focus, including reformulation and fresh marketing campaigns, showed early signs of success but also highlighted how quickly established brands can lose momentum in today's fast-moving market.

Competition has intensified from unexpected quarters. Patanjali, leveraging Baba Ramdev's yoga empire, aggressively priced ayurvedic products that directly competed with Emami's portfolio. Global giants like Unilever and P&G launched naturals ranges, encroaching on territory Emami once owned. Most threatening were the hundreds of small D2C brands that could launch, test, and scale products in months, not years.

The male grooming segment, once Emami's blue ocean with Fair and Handsome, has become a battleground. Beardo, Ustraa, The Man Company, and dozens of others have created a new vocabulary around male grooming that makes Emami's offerings seem dated. The Smart and Handsome rebranding, while necessary, hasn't fully addressed the perception gap with younger consumers who view Emami as their father's brand.

Yet there were bright spots in the results. As Agarwal noted: "Our targeted distribution strategies for new-age channels have played a vital role in driving success across the business. Strategic initiatives for Kesh King and male grooming along with the expected revival of International Business, position us confidently for sustained, robust growth going ahead". The company's ability to expand margins despite cost pressures demonstrated operational resilience.

The innovation pipeline showed promise but also revealed structural challenges. New launches contributed 4% to domestic net sales—respectable but not transformational. The company's R&D spending, while adequate for incremental innovation, paled compared to the venture funding flowing into beauty and personal care startups. This raised a fundamental question: Could a company built on patient, methodical growth adapt to an environment demanding rapid experimentation?

Supply chain disruptions added another layer of complexity. Raw material costs, particularly for key ayurvedic ingredients, fluctuated wildly. Climate change affected herb cultivation cycles. Regulatory scrutiny on ayurvedic claims intensified globally. Each challenge individually was manageable; collectively, they strained an organization built for a more predictable era.

The generational transition within the founding families added another dimension. The second generation, educated at global business schools, brought fresh perspectives but also faced the classic innovator's dilemma—how aggressively to disrupt a successful but slowing business model. Their cautious approach suggested respect for what their fathers built but perhaps insufficient urgency for what the market demanded.

Financial metrics painted a picture of a business at an inflection point. Operating income rose 5.1% year-over-year in FY2024, with operating profit increasing 9.9%. Net profit grew 15.4% with margins expanding from 18.4% to 20.2%. These weren't the numbers of a dying business, but neither were they the metrics of a growth story that excites markets.

The investment community's skepticism reflected in the stock's underperformance wasn't entirely unwarranted. In a market that rewards either explosive growth or deep value, Emami sat uncomfortably in between—too slow for growth investors, too expensive for value hunters. The company's response—consistent dividends and share buybacks—pleased income investors but didn't address the core growth challenge.

XI. Investment Analysis & Valuation

The numbers tell a story of financial discipline that would make any CFO proud, yet leave growth investors cold. Trading at ₹576 per share against a book value of ₹61.7, the stock commands a price-to-book ratio of 9.25 times. The P/E ratio stands at 44 times trailing twelve-month earnings, while the price-to-sales ratio is 9.1 times. These aren't the multiples of a value stock, nor are they the stratospheric valuations of high-growth disruptors. Emami exists in valuation purgatory—too expensive for its growth rate, too high-quality to be cheap.

The bull case rests on several compelling pillars. First, the balance sheet strength is undeniable. The company is almost debt-free while maintaining a healthy dividend payout of 52.5% and a three-year average ROE of 29.9%. In an era of leveraged growth stories that can implode overnight, Emami's fortress balance sheet provides downside protection. The company could weather a severe recession, make opportunistic acquisitions, or return substantial cash to shareholders—optionality that debt-laden competitors lack.

Second, the brand moats remain formidable in specific categories. BoroPlus isn't just the market leader in antiseptic creams—it defined the category. Navratna doesn't compete in the cool oil segment—it owns it. Zandu Balm has survived every competitor for over a century. These aren't brands that can be disrupted by a viral marketing campaign or influencer endorsement. They're embedded in Indian consumer habits across generations.

Third, the distribution network represents an almost irreplaceable asset. Those 4.5 million retail touchpoints took decades to build and would cost billions to replicate. As India's consumption story shifts from metros to Tier 3 and 4 cities, this distribution becomes even more valuable. D2C brands can dominate Instagram but struggle to reach the shopkeeper in Gorakhpur who influences purchasing decisions for hundreds of families.

The bear case, however, is equally compelling. Sales growth of 7.49% over five years in a market where GDP grows faster is concerning. This isn't cyclical weakness—it's structural deceleration. Young consumers don't aspire to use their parents' brands. The ayurvedic positioning, once a differentiator, has been commoditized as every brand claims natural ingredients.

The comparison with peers is sobering. Hindustan Unilever, despite its size, consistently delivers double-digit earnings growth through premiumization and innovation. Dabur, the closest comparable in ayurvedic positioning, trades at lower multiples while growing faster. Marico has successfully premiumized its portfolio and expanded into foods. Each peer has found a growth lever that Emami seems to lack.

The five-year net profit CAGR of 24.4% looks impressive until you realize it's largely driven by margin expansion rather than top-line growth. There's a limit to how much costs can be cut and prices raised before volume growth stalls. The company may be approaching that limit, evidenced by the volume-value divergence in recent quarters.

The cash flow analysis reveals both strength and missed opportunities. Operating cash flow of ₹8 billion in FY2024 grew 4% year-over-year, while investing activities consumed only ₹2 billion. Financial activities, primarily dividends and buybacks, used ₹6 billion. This capital allocation satisfies income investors but raises questions about growth reinvestment. Why isn't more capital deployed toward acquisitions or new category development?

The international opportunity remains underexploited. Contributing just 15% of revenues despite presence in 60+ countries suggests either execution challenges or insufficient investment. Compare this to Dabur or Marico, where international operations contribute 25-30% of revenues. The Russia success story proves Emami can win abroad, but replication has been slow.

ESG considerations add another layer of complexity. The fairness cream controversy damaged brand equity with conscious consumers. While the Smart and Handsome rebrand addressed immediate concerns, questions remain about the company's social responsibility in perpetuating beauty standards. Younger investors increasingly factor such considerations into valuations.

The generational wealth transfer underway in India should theoretically benefit Emami. As millions enter the middle class, demand for personal care products should explode. Yet the company's recent performance suggests it's not capturing this opportunity. New-age brands are stealing share at the premium end while local players compete aggressively at the bottom.

Valuation models struggle with Emami because it defies easy categorization. Using a DCF with conservative growth assumptions yields a fair value around ₹500-550, suggesting limited downside. But applying growth stock multiples to peer growth rates implies the stock should trade at ₹400. The market's current pricing at ₹576 suggests cautious optimism—belief in the quality but skepticism about growth.

For value investors, Emami presents a paradox. The business quality metrics—ROE, ROCE, cash generation—are exceptional. The balance sheet is pristine. The brands have longevity. Yet the stock never gets cheap enough to offer compelling value because the market recognizes these qualities. It's a "quality trap"—too good to be cheap, too slow to be exciting.

Growth investors face a different dilemma. The company talks about digital transformation, new category expansion, and international growth, but execution has been modest. The risk is buying a value stock at growth multiples—a recipe for underperformance. Without clear catalysts for acceleration, growth investors remain skeptical.

XII. Playbook: Lessons for Entrepreneurs

The Emami story reads like a masterclass in entrepreneurial jujitsu—using competitors' strength against them, finding opportunity in constraints, and building empires from impossibly small beginnings. The playbook that emerged from those rickshaw days in Kolkata's streets offers lessons that transcend industries and generations.

Lesson 1: Start Where Giants Fear to Tread When Agarwal and Goenka launched with ₹20,000, Hindustan Lever's marketing budget for a single brand exceeded their entire net worth. Instead of competing head-on, they went where giants wouldn't—narrow lanes of old Kolkata, small towns in Bihar, markets where ROI calculations didn't justify corporate attention. The lesson: resource constraints force innovation. They couldn't afford traditional distribution, so they built direct retailer relationships. They couldn't match advertising budgets, so they created word-of-mouth through product quality.

Lesson 2: Acquire Distressed Assets, Not Success Stories Himani was dying. Zandu was trapped in family feuds. Dermicool was Reckitt's orphan brand. Emami's acquisition strategy targeted assets others had given up on—brands with heritage but poor execution, formulations with potential but wrong positioning. They paid fractions of replacement value, then applied operational excellence to extract multiples of returns. This wasn't financial engineering; it was operational arbitrage. The lesson: value lies not in what something is, but in what it could become under different management.

Lesson 3: Create Categories, Don't Compete in Them Fair and Handsome wasn't just a product launch—it was category creation. Men were already using fairness creams secretly; Emami just gave them permission to do it openly. Navratna didn't compete with hair oils; it created "cool oil." BoroPlus wasn't another antiseptic; it was antiseptic-plus-cosmetic. When you create a category, you write the rules, set the price points, define the metrics of success. Competitors can only follow.

Lesson 4: Celebrity Endorsements as Democratization, Not Aspiration While competitors used celebrities to create aspiration gaps (you could be like them if you used this product), Emami used stars to democratize luxury. When Amitabh Bachchan endorsed Navratna, the message wasn't "be like Amitabh"—it was "Amitabh uses what you use." This subtle psychological difference made products accessible rather than aspirational, inclusive rather than exclusive.

Lesson 5: Bootstrap Until You Can't, Then Bootstrap Some More Most startups today raise capital at the idea stage. Emami waited 21 years before going public. This wasn't stubborn pride—it was strategic patience. By bootstrapping through the hardest phase, they retained control, developed operational discipline, and most importantly, learned to generate cash from operations rather than investors. When they finally accessed capital markets, it was for expansion, not survival.

Lesson 6: Family Business Doesn't Mean Unprofessional Business The two R.S.'s structured their partnership with the precision of their chartered accountant training. Clear roles (Agarwal as visionary, Goenka as executor), defined responsibilities, and formal governance structures prevented the feuds that destroyed many family businesses. They brought in professional managers early, created performance-based incentives, and most remarkably, planned succession while still active. The second generation was groomed systematically, not thrown into leadership.

Lesson 7: Distribution Is the Ultimate Moat In the age of digital everything, Emami's 4.5 million retail touchpoints seem anachronistic. Yet they represent relationships that no algorithm can replicate. Each retailer is a micro-influencer who recommends products to customers who trust them implicitly. This human network, built over decades, provides resilience against digital disruption that pure online brands lack.

Lesson 8: Patience Pays Compound Interest Emami didn't pivot every quarter chasing trends. BoroPlus took years to become profitable. The South India expansion took five years to break even. International markets required decade-long investments. This patience—almost Buddhist in its acceptance of delayed gratification—allowed compound effects that quarterly-focused competitors never achieved.

Lesson 9: Culture Can Be Counter-Positioned While MNCs sold Western aspiration, Emami sold Indian tradition. While competitors chased urban markets, they built rural distribution. While others focused on premium segments, they democratized categories. This systematic counter-positioning wasn't contrarian for its own sake—it was finding gaps in market coverage that incumbents' business models prevented them from addressing.

Lesson 10: Know When to Fold The Fair and Handsome to Smart and Handsome rebrand showed rare corporate courage—admitting a successful strategy had become a liability. Most companies defend dying positions until forced to change. Emami read the cultural zeitgeist and pivoted before being forced, preserving brand value that stubborn resistance would have destroyed.

The Meta-Lesson: Constraints Create Innovation Every disadvantage Emami faced became an advantage through creative adaptation. No money for advertising? Build word-of-mouth. Can't afford premium retail space? Go direct to small retailers. Can't match R&D budgets? Leverage traditional knowledge. Can't compete on scale? Create new categories. The constraint wasn't the problem—it was the catalyst for innovation.

For today's entrepreneurs drowning in venture capital and growth-at-all-costs mentality, Emami offers an alternative model: patient capital, operational excellence, and building businesses that generate cash, not just valuations. It's unfashionable advice in an era of unicorns and moonshots, but the ₹25,000 crore market cap built from ₹20,000 initial capital suggests it might be worth considering.

XIII. Power & Counter-Positioning Analysis

In the framework of Hamilton Helmer's "7 Powers," Emami presents a fascinating study in how competitive advantages evolve, strengthen, and sometimes erode. The company's journey from rickshaw to retail empire wasn't just about execution—it was about systematically building and defending multiple forms of power that created barriers competitors couldn't easily breach.

Brand Power: The Compound Effect of Trust BoroPlus isn't just a product; it's a trust architecture built over four decades. When a mother in rural Bihar reaches for that familiar blue tube to treat her child's cut, she's not making a rational price-performance calculation—she's accessing inherited wisdom. Her mother used it, possibly her grandmother too. This intergenerational trust can't be manufactured through advertising spending or influencer campaigns. It must be earned through millions of consistent experiences over decades.

The depth of this brand power becomes apparent in competitive responses. When Hindustan Unilever launched competing antiseptic creams with superior marketing budgets, they captured urban market share but barely dented BoroPlus's rural dominance. When Patanjali offered similar products at 30% lower prices, consumers stuck with BoroPlus. This isn't brand loyalty—it's brand habit, embedded so deeply in consumer behavior that switching costs become psychological rather than economic.

Counter-Positioning: The Incumbent's Dilemma Emami's greatest strategic insight was recognizing what MNCs couldn't do, not what they could. Hindustan Unilever couldn't sell ₹5 sachets in villages where transportation costs exceeded product value—their economics wouldn't allow it. P&G couldn't create ayurvedic formulations without contradicting their global "scientific superiority" positioning. L'Oréal couldn't go down-market without diluting premium brand equity.

This counter-positioning created a protective moat. Even when competitors recognized the opportunity, their existing business models, cost structures, and brand positions prevented effective response. It's the classic innovator's dilemma in reverse—Emami innovated in spaces where innovation would damage incumbents' existing businesses.

Switching Costs: The Invisible Prison The switching costs in Emami's categories are subtle but powerful. They're not technological lock-ins or contractual obligations—they're behavioral. A consumer who's used Navratna for years has developed a ritual: the specific amount applied, the massage technique, the cooling sensation they expect. Switching to another oil means relearning these micro-behaviors. For a ₹50 product, the effort isn't worth it.

This behavioral lock-in extends to retailers. A shopkeeper who's stocked Emami products for decades knows exactly how much to order, which variants sell in which seasons, what credit terms to expect. Switching to a new supplier means rebuilding all these knowledge structures. For marginal economic gain, few bother.

Network Effects: The Distribution Web While not network effects in the traditional sense, Emami's distribution creates similar dynamics. Each additional retailer makes the next one easier to acquire ("everyone else stocks it"). Each additional consumer makes retailers more likely to stock. This virtuous cycle, once established, becomes self-reinforcing.

The 4.5 million touchpoints aren't just distribution—they're information networks. Retailers provide real-time market feedback that no amount of market research could replicate. They're early warning systems for competitive threats. They're testing grounds for new products. This bi-directional information flow creates advantages that pure digital players can't match.

Process Power: The Complexity of Simplicity Making BoroPlus seems simple—mix antiseptic ingredients with ayurvedic herbs, package, distribute. Yet dozens of competitors have tried and failed to replicate its exact formula, texture, and efficacy. The process isn't protected by patents but by accumulated knowledge—which herbs to source when, how to process them for stability, how to achieve the right consistency across climate conditions.

This tacit knowledge, embedded in everything from supplier relationships to factory workers' expertise, can't be documented or transferred. It must be learned through experience. Even if a competitor acquired Emami's factories and formulas, they'd struggle to replicate the outcomes without the human knowledge systems built over decades.

Scale Economies: The Paradox of Small Markets Paradoxically, Emami achieves scale economies by aggregating small markets. While competitors focus on metros where individual store volumes are high, Emami aggregates thousands of small retailers where individual volumes are tiny but collective scale is massive. The economics work because their cost structure is designed for this distribution—minimal working capital, low marketing costs, simple packaging.

The Erosion of Power: Digital Disruption Yet these powers show signs of erosion. Brand power matters less to generations that research on Instagram rather than trust inherited wisdom. Counter-positioning becomes harder when D2C brands can profitably serve any niche. Switching costs diminish when consumers experiment constantly with subscription boxes and trial offers.

Most critically, the distribution advantage erodes as e-commerce penetration increases. Those 4.5 million touchpoints become less valuable when consumers order directly from brands. The information advantage from retailer feedback diminishes when brands can track every click, view, and purchase digitally.

The New Power Game Emami's challenge isn't that their powers have disappeared—it's that new forms of power have emerged that they don't possess. Data analytics power that allows precise consumer targeting. Viral marketing power that creates overnight sensations. Venture capital power that funds losses for market share. Platform power that controls customer relationships.

The company's response—gradual digital transformation, selective new-age brand launches, measured e-commerce expansion—suggests recognition of these new power dynamics. But the pace of adaptation raises questions: Can old powers be maintained while new ones are built? Or does success require abandoning what worked to embrace what might work?

The answer may determine whether Emami's next chapter is renaissance or slow decline. The powers that built a ₹25,000 crore company from ₹20,000 capital remain formidable. But in business, as in evolution, it's not the strongest that survive but those most responsive to change.

XIV. Future Outlook & Conclusion

Standing at the crossroads of its fifth decade, Emami embodies the tensions reshaping Indian business—tradition versus modernity, physical versus digital, patience versus urgency, heritage versus disruption. The company that once revolutionized FMCG by making ayurveda accessible now faces its own disruption moment, not from a superior competitor but from a fundamentally different consumption paradigm.

The digital transformation initiatives underway read like a checklist of modern commerce: D2C platforms launched, influencer partnerships signed, data analytics implemented, e-commerce expanded. Yet these feel like additions to the existing model rather than reimagination of it. The company talks digital but thinks physical—evident in their pride about 4.5 million retail touchpoints even as consumers increasingly shop on their phones.

The sustainability and ESG initiatives present similar contradictions. The company promotes natural ingredients and ayurvedic heritage while selling skin-lightening products in a world increasingly conscious of colorism. They emphasize traditional knowledge while participating in consumption patterns that environmentalists question. These aren't just PR challenges—they're fundamental questions about what business Emami wants to be in for the next generation.

New category expansion opportunities abound, but execution has been tentative. The wellness boom should be Emami's moment—immunity boosters, stress relief, natural beauty, holistic health are all trending. Yet the company's new launches feel incremental rather than transformational. Where's Emami's answer to Ozempic using ayurvedic principles? Where's their Peloton-equivalent for yoga and meditation? The opportunities exist, but the appetite for bold bets seems absent.

Management's guidance of "high single-digit revenue growth and double-digit EBITDA growth for FY25" feels achievable but uninspiring. In a market where startups promise (and sometimes deliver) 100% growth, Emami's steady-as-she-goes approach satisfies neither growth investors seeking multibaggers nor value investors seeking deep discounts.

Can Emami regain growth momentum? The answer depends on which Emami shows up—the bold disruptors who created categories from nothing, or the cautious custodians protecting what exists. The resources are there: pristine balance sheet, powerful brands, vast distribution, accumulated knowledge. What's unclear is whether the will exists to deploy these resources aggressively rather than defensively.

The journey from ₹20,000 to ₹25,000 crore market cap represents one of Indian business's great success stories. Two chartered accountants who left secure jobs to sell cosmetics from a rickshaw built an empire that challenged multinationals and created products that became part of India's cultural fabric. They proved that Indian companies could innovate, not just imitate; create categories, not just compete in them; build global brands from local insights.

But past success doesn't guarantee future relevance. The very factors that enabled Emami's rise—patience, incremental innovation, distribution focus—may constrain its future. The market has changed from one that rewarded steady execution to one that demands constant reinvention. Consumer loyalty has shifted from lifelong commitment to temporary engagement. Competition has evolved from known rivals to unknown startups.

The investment implications remain complex. For those seeking steady dividends and capital preservation, Emami offers attractions—quality business, strong balance sheet, consistent cash generation. For those seeking growth and transformation, the story is less compelling—slowing top line, limited geographic expansion, tentative digital evolution. The stock price, trapped between these narratives, reflects this ambiguity.

Perhaps the most telling indicator of Emami's future lies not in financial statements but in recruitment patterns. Are they hiring seasoned FMCG executives or Silicon Valley engineers? Are they acquiring traditional brands or digital-first startups? Are board discussions about protecting market share or creating new markets? These qualitative signals may matter more than quarterly numbers.

The Emami story isn't finished. Companies far older have successfully reinvented themselves—IBM transformed from hardware to services, Netflix from DVDs to streaming, Microsoft from software to cloud. But such transformations require acknowledging that what got you here won't get you there—a recognition that comes hard to successful companies.

In the end, Emami stands as both inspiration and cautionary tale. Inspiration for entrepreneurs that empires can be built from nothing with intelligence, persistence, and courage. Cautionary tale that success itself becomes the enemy of future success, that moats can become prisons, that the greatest risk isn't failure but slow irrelevance.

The two friends who started with a rickshaw full of dreams built something remarkable. Whether their successors can rebuild it for a new era remains the ₹25,000 crore question. The answer will determine if Emami's greatest chapters are history or yet to be written.

[Note: This analysis is based on publicly available information through January 2025. Investment decisions should be based on individual research and risk tolerance. The author has no position in Emami securities and this does not constitute investment advice.]

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube