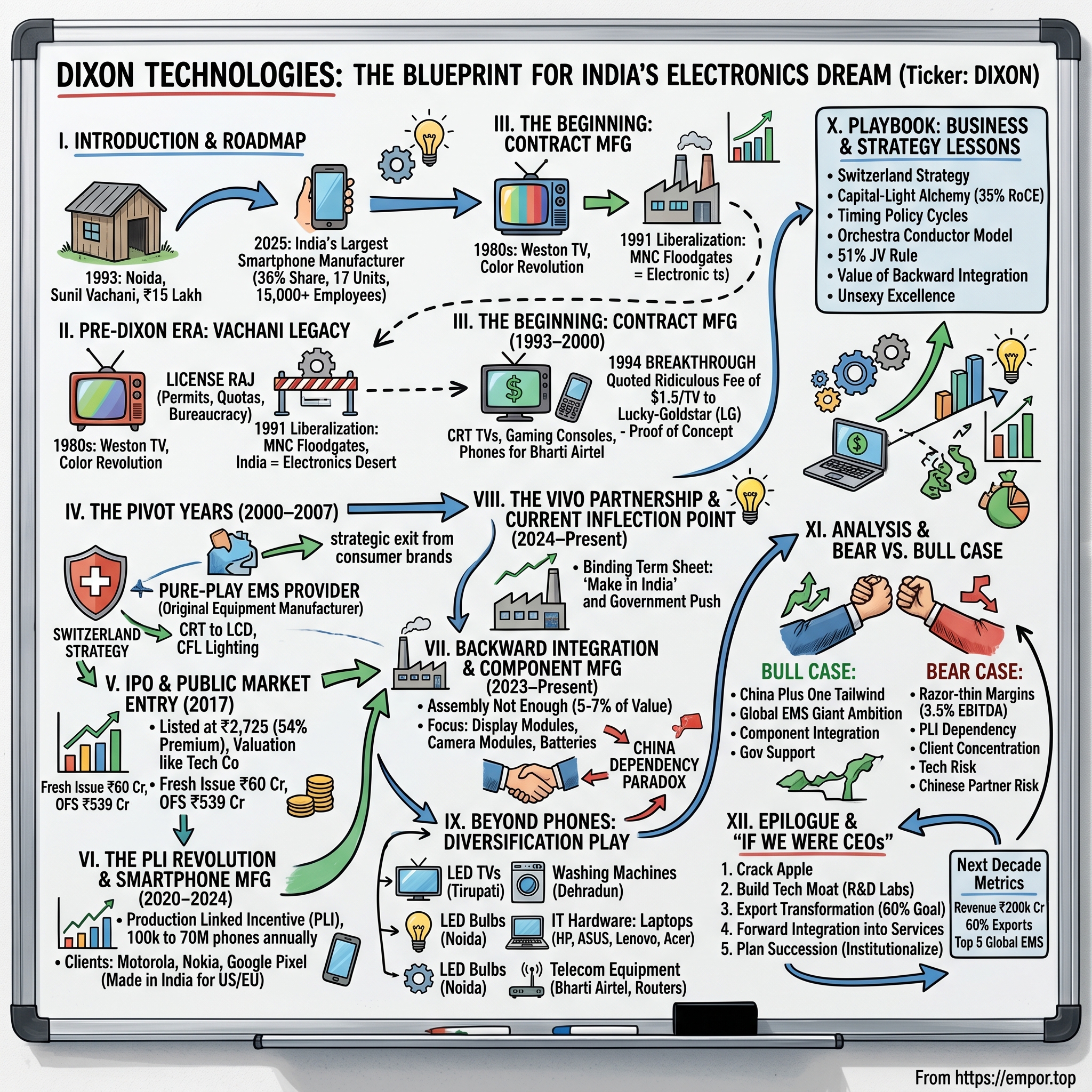

Dixon Technologies: The Blueprint for India's Electronics Manufacturing Dream

I. Introduction & Episode Roadmap

Picture this: A small rented shed in Noida, 1993. A 10,000 sq ft facility, a few machines, 15 employees and ₹15 lakh borrowed from his father. That's all Sunil Vachani had when he started Dixon Technologies. Fast forward three decades: Dixon has 17 manufacturing units in India with over 15,000 employees. The company that began assembling 14-inch CRT televisions is now India's largest smartphone manufacturer, capturing a record 36 per cent share of total smartphone production volumes in Q2 CY2025, marking a fourfold jump from 9 per cent in the same period last year.

How did a contract manufacturer that nobody had heard of become India's answer to Foxconn? How did a company with fixed assets of just Rs. 140 crore generate a topline of Rs. 2,500 crore and bottomline of Rs.50 crore by 2017? And perhaps most intriguingly—how did a business built on razor-thin margins and zero brand ownership become one of India's most celebrated manufacturing stories?

This is the untold saga of Dixon Technologies—a company that chose to remain invisible while powering the gadgets in millions of Indian homes. It's the story of how India's electronics manufacturing desert transformed into an oasis, with Dixon as its most unlikely architect. It's about riding government policy waves, managing Chinese partnerships with surgical precision, and building a business model so capital-efficient that it defies conventional manufacturing wisdom.

What you're about to discover: The strategic brilliance of never competing with customers. The art of backward integration in a component-starved ecosystem. The delicate dance with Chinese joint ventures in an era of geopolitical tensions. And ultimately, how a company with 5-year average EBITDA margin of just 3.5% became the poster child of India's manufacturing ambitions.

Buckle up. This isn't just Dixon's story—it's the blueprint for how India plans to challenge the world's electronics manufacturing order.

II. Pre-Dixon Era: The Vachani Legacy & India's Electronics Desert

The year was 1985. India's television market was experiencing its first color revolution. Sundar Vachani had been manufacturing televisions under the Weston brand, which had launched the first colour television in India. They made the country's first color televisions and video recorders — and operated a string of video game parlors on the side. For a brief moment, Weston was synonymous with Indian innovation in consumer electronics.

But success in the License Raj era was a double-edged sword.

The pre-1991 Indian economy operated on a system of permits, quotas, and bureaucratic mazes that would make Kafka blush. Want to expand your factory? Get in line for a license that might take years. Want to import components? Navigate foreign exchange restrictions that changed with political winds. Want to innovate? First, convince a committee of bureaucrats why India needed your innovation.

Weston, like many Indian brands of that era, found itself caught in a perfect storm. His business struggled later on due to the emergence of other companies. The 1991 liberalization that was meant to unleash Indian enterprise instead opened floodgates to multinational corporations armed with decades of R&D, global supply chains, and deep pockets.

By the early 1990s, India's electronics manufacturing landscape resembled a desert. The country that had sent a spacecraft to space couldn't manufacture a decent television at scale. The irony was palpable—a nation of 900 million people, with engineers manning Silicon Valley's biggest companies, was importing nearly everything electronic.

The numbers told a brutal story. India's electronics production in 1990 was less than $2 billion—smaller than Thailand's. Manufacturing contributed just 15% to GDP. The trade deficit in electronics was ballooning. Every middle-class aspiration—a color TV, a VCR, a music system—meant dollars flowing out of the country.

This was the inheritance awaiting the next generation. A legacy of what could have been. An ecosystem that existed more in government files than factory floors. A market massive in potential but minuscule in domestic production capability.

Into this landscape stepped Sunil Vachani, freshly back from London after completing his Associates in Business Administration from American College. He could have joined the family business, but he says, "I wanted to do something of my own, that was my passion". His first venture—a cordless telephone factory in 1989-90—failed because of "missteps," as he would later admit. But failure in the Vachani household wasn't an ending; it was data.

Thereafter, he started training at his father's TV manufacturing company, Weston, in the components department. After a year-and-a-half, he mustered the courage to tell his father that he wanted to set up his own venture—manufacturing electronics.

The idea Sunil pitched to his father was radical for its time: "to set up a company that would specialise in manufacturing electronic components and products on behalf of other firms." At that time, the concept of manufacturing for other people was alien; everybody believed that manufacturing is sacred, it has to be in-house and not outsourced.

Sundar Vachani must have seen something in his son's eyes—perhaps the same hunger that had driven him to launch India's first color television. Or perhaps he recognized that the old ways of doing business were dying, and survival meant reimagining the game entirely. Whatever the reason, he agreed to lend Sunil ₹15 lakh.

The name 'Dixon' was suggested by Sunil's father. Atul Lall, a trusted protégé of Sundar Vachani, joined Sunil in this venture—a partnership that would prove crucial in the years to come.

The stage was set. India's electronics manufacturing revolution wouldn't come from government committees or five-year plans. It would come from a borrowed factory in Noida, a father's faith translated into a ₹15 lakh loan, and a young man's conviction that India could build for the world—even if the world didn't know it yet.

III. The Beginning: From CRT TVs to Contract Manufacturing (1993–2000)

December 1993. The monsoon had passed, leaving Noida's industrial sector B-14 & 15 in that peculiar state between Delhi's scorching summers and freezing winters. Sunil Vachani established Dixon in 1993 at a small, rented facility in Noida with just one factory. Dixon initially manufactured 14-inch televisions, Sega video game consoles, Philips video recorders, and push-button phones for Bharti Airtel.

The early months tested every assumption Sunil had about business. Manufacturing for others meant you had no brand premium to hide behind. Your only currency was trust, delivery, and an ability to produce at costs that made your customers' spreadsheets sing.

But 1994 brought the breakthrough that would define Dixon's trajectory. Lucky-Goldstar—now LG Electronics—which, in those days, only had a representative office, was looking for a subcontractor to manufacture a few thousand TVs for exports. "We were one of the companies who sent in a quote for the order and were so desperate for business that we quoted a ridiculous fee of $1.5 per television," says Vachani.

Think about that number. $1.5 per television. In an industry where margins were already thin, Dixon was essentially working for pocket change. But Vachani understood something his competitors didn't: in contract manufacturing, your first client isn't a customer—they're a reference, a proof of concept, a foot in the door of credibility.

It was a great learning experience, dealing with tough negotiations. Vachani credits Lucky-Goldstar for trusting new players with no prior experience. "I do think my late father's legacy helped. People in the electronics business knew him and that's what helped us get started," he adds.

That first order from LG—just 2,000 television sets—would cascade into something much larger. Goldstar was happy with the job and went on to become its major client as LG. The relationship that started with a desperate bid became the foundation of Dixon's manufacturing credibility.

What's remarkable about Dixon's early years wasn't just survival—it was profitability. Unlike a lot of startups today, Dixon Technologies made money from the first quarter. In the first year, it made a profit of ₹3 lakh, making a few thousand TV sets. The company was profitable from its first quarter, earning a profit of ₹3 lakh in its first year. The ability to secure and fulfill its first major order from LG Electronics was a significant milestone, demonstrating its manufacturing capabilities.

How did they achieve profitability from day one? Lall says, "is that we've been conservative with our capital allocation. We are in the business of outsourcing, which means you have to be frugal and cost conscious, and capital efficiency has to be of the highest order". This belief has been at the core of Dixon's operations.

The philosophy was simple but revolutionary for Indian manufacturing: Don't own what you can rent. Don't build what you can buy. Don't employ who you can contract. Every rupee saved on fixed costs was a rupee that could be deployed in winning the next order.

Lall and Vachani have had a great working relationship—with Lall focusing on numbers and Vachani looking at strategy, vision and government relationships. This division of labor would prove crucial. While Vachani navigated the relationships and pitched the vision, Lall ensured that every television rolling off the assembly line contributed to the bottom line.

The late 1990s saw Dixon quietly expanding its portfolio. CRT televisions for LG led to video cassette recorders for Philips. Push-button phones for the nascent Airtel network demonstrated capability beyond television. The Sega video game console manufacturing showed they could handle complex electronics requiring precision assembly.

Each new product wasn't just revenue—it was learning. How to manage multiple supply chains. How to maintain quality across different product categories. How to keep customers happy while keeping margins viable. These lessons, learned in the crucible of 1990s Indian manufacturing, would become the playbook for massive expansion.

By 2000, Dixon had graduated from being a small subcontractor to a serious player in India's contract manufacturing space. The company that had started with 15 employees in a rented shed was now managing multiple product lines for global brands. Revenue had crossed the significant psychological barrier of sustainability.

"I remember someone telling me, that I was too young to be a managing director. So I'd be lying if I told you that I had a five-year or 10-year plan, Vachani would later recall.

But sometimes, not having a rigid plan is the best plan. Dixon's flexibility—its ability to pivot from CRT TVs to gaming consoles to phones based on market opportunity—would become its signature strength.

The foundation was set. The credentials established. The relationships built. As India entered the new millennium, Dixon was no longer just Sunil Vachani's experiment in contract manufacturing. It was a proven model, ready to scale with an India that was finally waking up to its manufacturing potential.

IV. The Pivot Years: From Consumer Brand to Pure EMS (2000–2007)

The new millennium brought a revelation that would fundamentally reshape Dixon's identity. The company faced a choice that would define its next two decades: compete with customers or become the invisible force behind their success.

The early 2000s marked Dixon's first major validation beyond commercial clients. A government contract to manufacture televisions signaled something profound—Dixon was no longer just another vendor; it had become infrastructure for India's electronics ambitions.

But the real transformation was philosophical. Dixon made the strategic decision to completely exit consumer-facing brands and become a pure-play electronics manufacturing services (EMS) provider. Their business model was focused on being an Original Equipment Manufacturer (OEM), assembling products based on client specifications. No Dixon-branded TVs would compete with LG in showrooms. No Dixon phones would battle Samsung for shelf space.

This wasn't retreat—it was sophisticated strategy. In choosing invisibility, Dixon chose invincibility. Brands could come to them without fear of creating a future competitor. The "Switzerland strategy," as they would later call it, meant permanent neutrality in the brand wars while profiting from all sides.

The numbers validated the strategy. The company achieved revenue from operations of more than Rs 1000 crore on standalone basis during the financial year ended 31 March 2014—though this milestone would come a few years after this period, the foundation was being laid in these crucial years through manufacturing CRT televisions for giants like LG, Sony, and Philips.

The client roster during this period read like a who's who of global electronics. Each relationship brought not just revenue but knowledge transfer. LG taught them Korean efficiency. Philips brought Dutch precision to quality control. Sony's requirements pushed them to levels of perfection that seemed impossible in an Indian factory.

During the year under review, IBEF I and IBEF, whose investments are advised and managed by MOPE Investment Advisors Private Limited, subsidiary of Motilal Oswal Financial Services Limited, made investment in the company. Its first funding round was on Nov 13, 2007. Its latest funding round was a PE round on Jun 18, 2008 for $9.32M.

This first institutional funding marked a critical transition. Dixon was no longer just a family business; it was an institution worthy of professional investor attention. Motilal Oswal's entry brought not just capital but validation that the EMS model could scale.

The discipline that Atul Lall brought to operations became legendary within Dixon. "Everyone who reports to Atul, even engineers or heads of departments… he's turned them into chartered accountants. Under his leadership, we've never lost money, except one year when the exchange rate of INR-USD turned against us and we were not completely hedged," says Vachani.

This financial discipline in an industry known for cash burn and working capital stress made Dixon an anomaly. They were proving that Indian manufacturing didn't need to be capital-intensive to be world-class.

In 2007, the Company commenced manufacturing of LCD TVs. In 2008, the company entered the lighting products vertical with manufacture of CFL products. These weren't just product additions—they were strategic bets on technology transitions. While competitors clung to CRT technology, Dixon was already moving to LCD. While others ignored lighting, Dixon saw an opportunity to diversify beyond consumer electronics.

The period also saw Dixon master the art of the possible in Indian manufacturing. They learned to navigate infrastructure challenges that would make Western manufacturers weep—power cuts, monsoon logistics, bureaucratic delays. Each challenge overcome became competitive advantage. If you could manufacture electronics profitably in Noida in 2005, you could manufacture anywhere.

What's fascinating about this period is what Dixon didn't do. They didn't chase valuations. They didn't expand internationally. They didn't launch a consumer brand to capture higher margins. Every temptation to deviate from the pure EMS model was resisted.

The wisdom of this focus would only become apparent later. While competitors who tried to straddle both manufacturing and branding struggled with channel conflicts and divided focus, Dixon's singular commitment to being the best manufacturer—not the most visible—created a moat that brands increasingly valued.

By 2007, Dixon had transformed from a small contract manufacturer to India's most trusted EMS partner. The company that had started by desperately quoting $1.5 per TV was now the first choice for global brands entering India. The foundation was complete. The model was proven. The only question was how big this could become.

V. IPO and Public Market Entry (2017)

September 6, 2017. The investment banking teams at IDFC Bank had been working around the clock. After years of private growth, Dixon Technologies was about to test public market appetite for an unusual proposition: a company with no consumer brand, operating on wafer-thin margins, in the decidedly unsexy business of contract manufacturing.

The IPO structure told its own story. The issue is a combination of fresh issue of 0.03 crore shares aggregating to ₹60.00 crores and offer for sale of 0.31 crore shares aggregating to ₹539.28 crores. The fresh issue was deliberately small—just ₹60 crores—because Dixon didn't really need the money. This was about liquidity for early investors and creating currency for future growth.

Motilal Oswal PE owns 23.68%, which will reduce to 5.8% post OFS, with the PE fund contributing 64% of the offer for sale. After a decade of nurturing Dixon from a small manufacturer to IPO-ready enterprise, Motilal Oswal was ready to book profits.

The pricing at ₹1766 per share raised eyebrows. At nearly 36 times trailing earnings, Dixon was asking public markets to value it like a technology company, not a manufacturer. The banker's pitch was simple but powerful: Dixon wasn't selling manufacturing; it was selling India's manufacturing dream.

September 18, 2017. D-Day.

The opening bell at BSE saw something extraordinary. Dixon Technologies listed at Rs 2,725, a 54% premium on its initial public offering (IPO) price of Rs 1,766 per share on the National Stock Exchange (NSE) and BSE. The stock hit a high of Rs 3,024 on NSE after few seconds of its listing.

The first day's closing told an even more emphatic story. It ended at Rs 2,903, up 64% from its IPO price. The market had delivered its verdict: Dixon wasn't just another manufacturer; it was a proxy for India's manufacturing ambitions.

The subscription data revealed who was betting on Dixon. IPO oversubscribed by 117.11 times. Retail investors, typically wary of manufacturing stocks, had embraced Dixon's story. Institutional investors, both domestic and foreign, saw it as a play on India's consumption growth without consumer brand risks.

What's remarkable is what Dixon did with the IPO proceeds. The Company proposes to utilize the Net Proceeds towards funding the following objects: Repayment/pre-payment, in full or in part, of certain borrowings availed by DTIL. Setting up a unit for manufacturing of LED TVs at the Tirupati Facility. Enhancement of backward integration capabilities in the lighting products vertical at Dehradun I Facility.

No vanity projects. No aggressive expansion into unrelated areas. Just boring, practical investments in capacity and capability. The Tirupati LED TV facility would later become India's largest. The backward integration in lighting would prove prescient as component shortages hit global markets.

The post-IPO performance validated early believers beyond their wildest dreams. By March 2021, the stock had touched Rs 19,006.25—a 697% return from listing price in just 3.5 years. Dixon had created more wealth for public shareholders in three years than most companies create in decades.

But the real transformation wasn't in stock price—it was in ambition. The IPO proceeds, though modest, combined with the credibility of being publicly listed, opened doors that had been previously shut. Global brands that had hesitated to work with a private Indian company now saw Dixon as a transparent, professionally-managed partner.

Currently, promoters hold 46.20% stake, which will shrink to 38.93% post IPO. This dilution didn't diminish Sunil Vachani's control—it enhanced his influence. As chairman of a listed company worth thousands of crores, his voice carried weight in policy corridors and corporate boardrooms alike.

The IPO also marked a subtle but crucial shift in Dixon's narrative. Pre-IPO, it was the efficient manufacturer. Post-IPO, it became the standard-bearer for Make in India, the poster child for domestic manufacturing capability, the inevitable beneficiary of every government scheme to boost local production.

Moreover, on 3rd May 2017, promoter of Dixon had purchased 233 shares from Times Group—a small transaction that showed promoter confidence just months before the IPO. Such signals mattered to a market looking for conviction from insiders.

Looking back, Dixon's IPO wasn't just a financial event—it was an inflection point. The company that had spent 24 years building credibility one television at a time was now ready for its next act: riding the smartphone revolution that was about to transform India's manufacturing landscape forever.

VI. The PLI Revolution & Smartphone Manufacturing (2020–2024)

March 2020. As the world locked down and global supply chains shattered, a quiet revolution was brewing in India's policy corridors. The Production Linked Incentive (PLI) scheme for mobile phones was about to transform Dixon from a successful manufacturer into a national champion.

Prior to PLI, Dixon assembled 100,000 phones monthly. However, with new facilities in the works and existing ones operational, its capacity is set to reach 70 million phones annually. This includes 40 million feature phones and 30 million smartphones.

The transformation was staggering. From 100,000 phones monthly to nearly 6 million monthly capacity—a 60-fold increase. But capacity was just one part of the story. The real revolution was in Dixon's client roster and strategic positioning.

December 2020 marked the first major breakthrough. Dixon's subsidiary Padget Electronics would manufacture smartphones for Motorola. This wasn't just another client—Motorola's return to Indian manufacturing through Dixon signaled that global brands were ready to bet on Indian EMS players.

January 2021 brought another coup. Padget Electronics signed a contract with HMD Global to manufacture Nokia smartphones at its Noida plant. The Nokia brand, once synonymous with mobile phones, choosing Dixon for its India resurrection was poetic justice for a company that had started with simple push-button phones.

But the crown jewel announcement came in 2024. The company said the initial batch of India-made phones will be available in the market by September, as trial production has recently started. The initial batch of India-made phones will be available in the market by September. Dixon would manufacture Google Pixel smartphones—not just for India, but For the US and European markets.

Dixon's production capacity for Pixel smartphones will reach 100,000 units monthly, with an estimated 25-30 per cent designated for export. Think about that: An Indian company manufacturing Google's flagship phones for American and European consumers. The same markets that had once dismissed Indian manufacturing as low-quality were now receiving premium smartphones Made in India.

The numbers tell a story of explosive growth. Dixon's revenue soared about 500% to nearly Rs 18,000 crore in the five years to FY24. "In a short period of just 5–6 years, we have grown from Rs 1,500 crore, and this year, we should close at around Rs 19,000 crore".

The employee count tells another dimension of this transformation. From 1,700 people to 27,000 people, with plans to double headcount again in two years. Each job created wasn't just employment—it was skill development in precision manufacturing, quality control, and supply chain management.

But the smartphone revolution came with its own challenges. Dixon has benefited from the PLI scheme, which adds about 0.6 to 0.7 per cent to its mobile phone revenue margins, mostly passed to customers. The harsh reality: Even with government incentives, margins remained razor-thin. Dixon was essentially passing through PLI benefits to brands, keeping just enough to justify the investment.

Led by Dixon Technologies (India), homegrown smartphone electronic manufacturing services players captured a record 36 per cent share of total smartphone production volumes in the second quarter (April–June) of calendar year 2025. This marks a fourfold jump from 9 per cent in the same period last year. Dixon had quietly become India's largest smartphone manufacturer, overtaking even Samsung's Indian operations.

The client list by 2024 read like a global who's who: Samsung, Xiaomi, Oppo, Ismartu (brands like Itel, Infinix, Tecno), Motorola, Google Pixel, and Nothing. Each brand brought different requirements, different quality standards, different supply chain complexities. Managing this orchestra of demands while maintaining profitability required operational excellence that few Indian companies had achieved.

Dixon plans to produce 40 to 44 million smartphones in the current fiscal year, rising to 60 to 65 million by FY27. Export volumes to North America alone are expected to grow from 10 to 12 million in FY26. The ambition was clear: Dixon wasn't content being India's largest; it wanted to be globally relevant.

The smartphone boom also forced Dixon to confront an uncomfortable truth about Indian manufacturing. Assembly was just 5-7% of a phone's value. The real value—and margins—lay in components: displays, cameras, batteries, semiconductors. Without a component ecosystem, India would remain a glorified assembly shop.

This realization would drive Dixon's next phase of evolution. But for now, the company had achieved something remarkable. In less than five years, it had transformed from a TV manufacturer to India's smartphone assembly powerhouse. The boy who had borrowed ₹15 lakh from his father was now running an operation that assembled phones worth thousands of crores annually.

Yet Sunil Vachani knew this was just the beginning. The real test wasn't whether Dixon could assemble smartphones—it was whether India could build a complete electronics ecosystem. And Dixon was about to place its biggest bet yet on that possibility.

VII. Backward Integration & Component Manufacturing (2023–Present)

"Assembly is not enough."

Atul Lall's words at Dixon's 2023 investor call marked a fundamental shift in strategy. After conquering smartphone assembly, Dixon was ready to attack the real challenge: building India's component ecosystem from scratch.

The math was brutal but simple. In a smartphone costing $200, assembly added $10-14 of value. The display alone was worth $40-60. The camera module: $20-30. Battery pack: $10-15. Dixon was capturing 5% of value while letting 95% flow to component suppliers, mostly in China and Vietnam.

Dixon's CEO Atul Lal told PTI that electronics component is the next phase of growth for the company. Dixon has reportedly started working on a project for display modules and is now looking at manufacturing components like camera modules, mechanical enclosures and lithium ion batteries.

The transformation began with strategic acquisitions that would have been impossible without the war chest and credibility built from smartphone assembly success. The first major move sent shockwaves through the industry: Dixon acquired a 56% stake in Ismartu India for ₹2.4 billion, gaining access to additional smartphone and feature phone manufacturing facilities and becoming the sole supplier for Transsion brands such as Itel, Infinix and Tecno.

But Ismartu wasn't just about capacity—it was about knowledge transfer. Transsion's Africa-first strategy had forced innovations in battery life, durability, and cost engineering that were directly applicable to India's price-sensitive market.

The real game-changer came with camera modules. Recognizing that every smartphone needed cameras and that India imported nearly 100% of them, Dixon made a calculated move. The company announced acquisition of 51% stake in Qtech India for camera and fingerprint modules. Back then, Lall said that around $3 Bn will be infused in the project initially with 60% allocation to televisions and 15%-12% allocation to mobile phone manufacturing.

The display gambit was even bolder. Dixon is in discussions to set up a $3 Bn display fabrication facility in India. Around $3 Bn will be infused in the project initially with 60% allocation to televisions and 15%-12% allocation to mobile phone manufacturing. This wasn't just backward integration—it was an attempt to build an entire industry vertical that didn't exist in India.

But here's where the story gets complicated. Building a component ecosystem meant dancing with the dragon. Every major component technology was controlled by Chinese, Korean, or Taiwanese companies. Dixon needed their technology, but India wanted supply chain independence. The solution? Carefully structured joint ventures.

The HKC joint venture for display modules exemplified this delicate balance. Dixon would hold majority stake, ensuring Indian control. HKC would provide technology and training. The facility would serve both domestic and export markets. But government approval remained pending, caught in the crosswinds of geopolitical tensions.

Another strategic partnership emerged: a 74% stake JV with Chongqing Yuhai for precision mechanical and metal parts. Among component manufacturing, we expect component supplies for 60 million smartphones by volume to generate $600 million in annual revenue. Similarly, the revenue addition from laptops could be $100 million, and we expect to see a further $60 million from television display manufacturing and $140 million from automotive display manufacturing—all adding up to at least $900 million ( ₹8,000 crore) over the next two years.

The ambition was breathtaking: $900 million in component revenue within two years. For context, that would be larger than most Indian electronics companies' total revenue.

The China dependency paradox created constant tensions. Dixon needed Chinese technology to reduce dependence on Chinese imports. Every JV announcement triggered scrutiny from security agencies. Every technology transfer required navigating export controls and intellectual property concerns.

"Some of our components-linked joint ventures, such as with Q Tech for camera modules, are already leading to revenue realization since these are running factories. Others, such as display modules, will start adding revenue by the end of this fiscal or the first quarter of the next fiscal," Lall said.

The component push wasn't just about margins—it was about survival. Dixon's stock has fallen over 20% since the start of 2025, even as the broader BSE India Manufacturing Index lost just about 5%. Investors were nervous. PLI benefits were ending. Chinese brands faced regulatory scrutiny. Without component manufacturing, Dixon risked becoming just another low-margin assembler.

The strategic logic was compelling. Dixon aims to capture 27% of the BOM in-house by focusing on camera modules, mechanicals, and displays. The CapEx for the HKC plant is around INR375 crores, with expected asset turns of 7-8x. The component business is margin-accretive and will enhance Dixon's competitiveness.

Capturing 27% of Bill of Materials (BOM) in-house would transform Dixon's economics. Margins could expand from 3-4% to 6-8%. More importantly, it would create switching costs for customers. A brand working with Dixon wouldn't just get assembly—they'd get an integrated solution from components to finished product.

The execution challenges were immense. Component manufacturing required different skills than assembly. Quality standards were even more stringent—a defective display meant scrapping an entire phone. Investment requirements were massive, with payback periods extending years, not months.

Yet Dixon pressed forward with the confidence of a company that had defied odds before. The same firm that had started assembling CRT TVs in a rented shed was now planning billion-dollar display fabs. The ambition might seem audacious, but then again, so did manufacturing Google Pixels in Noida just five years ago.

VIII. The Vivo Partnership & Current Inflection Point (2024–Present)

December 15, 2024. The news that flashed across trading terminals sent Dixon's stock soaring to an all-time high of ₹19,148. Dixon Technologies and Vivo India, one of the top smartphone brands, signed a binding term sheet. This 51:49 joint venture positions Dixon as the majority stakeholder, aligning with the Indian government's push for local manufacturing under the 'Make in India' initiative.

But this wasn't just another joint venture. This was a tectonic shift in India's smartphone manufacturing landscape.

To understand the significance, consider the context. The Indian government has been urging Chinese smartphone manufacturers to collaborate with Indian firms to comply with regulatory guidelines and enhance local capabilities. Behind closed doors, the message to Chinese brands was clear: find Indian partners or face an increasingly hostile regulatory environment.

While Vivo was reportedly in talks with other Indian firms like the Tata Group earlier this year, Dixon's proven expertise and existing infrastructure made it the perfect fit for this ambitious venture. Where Tata brought conglomerate prestige, Dixon brought something more valuable: a decade of experience managing the chaos of smartphone manufacturing in India.

The structure of the deal revealed sophisticated thinking on both sides. Dixon will hold a 51 per cent stake in the joint venture, while Vivo India will own the remaining 49 per cent. Despite the partnership, both companies will remain independent, with no ownership in each other. This wasn't a merger or acquisition—it was a strategic alliance that preserved both companies' independence while creating synergies.

Vivo's Greater Noida plant now has a capacity of 120 million units annually, marking a significant increase from its previous capacity of 40 million units. Combined with Dixon's existing capacity, the JV would control infrastructure capable of producing nearly 200 million phones annually—more than half of India's total smartphone market.

The numbers were staggering. As per media estimates, this JV can help Dixon grab over 1/5th of India's 288 million overall mobile phone assembly market and close to 45 million smartphone manufacturing volume. If realized, Dixon-Vivo would become one of the largest smartphone manufacturing entities outside China.

The proposed joint venture will undertake part of vivo's OEM orders of smartphones in India, and can also engage in OEM business of various electronic products of other brands. "This partnership will effectively complement the current manufacturing operations of vivo India," said Jerome Chen, CEO of vivo India.

The "can also engage in OEM business of other brands" clause was crucial. This wasn't just about Vivo phones. The JV could potentially manufacture for Oppo, OnePlus (both sister companies of Vivo), or even Western brands looking for India capacity. Dixon had essentially gained access to one of the world's most advanced smartphone manufacturing operations.

For Vivo, the logic was equally compelling. Facing regulatory scrutiny and frozen bank accounts earlier in 2024, the company needed an Indian face. Dixon provided not just compliance cover but genuine local expertise in navigating India's complex regulatory and political landscape.

'Vivo will be Dixon's marquee client for the business. That said, we do hope to have both Vivo and Motorola as two anchor clients for Dixon, and not just one', Lall said, acknowledging the delicate balance Dixon needed to maintain.

The Motorola relationship, Dixon's anchor client for years, was showing signs of strain. Revenue from pure-play mobile phone manufacturing dropped 5% sequentially to ₹9,312 crore, even though mobile phone revenue received a 130% sequential boost from Dixon's subsidiary Ismartu. This clearly reflected a slowdown in Dixon's production of phones from Motorola.

The Vivo JV was thus both opportunity and insurance policy. Opportunity to scale beyond imagination. Insurance against over-dependence on any single client.

Market reaction was euphoric but complex. Dixon Technologies shares made a 52-week record high of ₹19,148 on the NSE on December 17. The company has gained around 200% in one year. Yet beneath the celebration lay uncomfortable questions.

Was Dixon becoming too dependent on Chinese partnerships? The company now had JVs with Vivo (smartphones), HKC (displays), Longcheer (smartphones), and Chongqing Yuhai (mechanical parts). Critics argued Dixon was becoming a front for Chinese companies rather than building indigenous capability.

The government's position remained deliberately ambiguous. Publicly, they welcomed the JV as validation of Make in India. Privately, security agencies scrutinized every detail. The approval process would be long and uncertain.

Dixon Technologies and Vivo India have announced a joint venture to establish an OEM facility in India, focusing on manufacturing smartphones and electronics for Vivo. The facility may also offer OEM services to other brands like Samsung, Xiaomi, Motorola, Oppo, Transsion, Google, and Nothing.

As 2024 drew to a close, Dixon stood at its most crucial inflection point. The Vivo JV could catapult it into the global electronics manufacturing elite. Or it could become a cautionary tale about the perils of dancing too closely with Chinese partners in an era of techno-nationalism.

Sunil Vachani, now a billionaire, remained philosophical. The boy who had started with ₹15 lakh understood that every big opportunity came with proportional risk. The question wasn't whether to take risks—it was whether India was ready to pay the price for electronics manufacturing greatness.

IX. Beyond Phones: The Diversification Play

While the world watched Dixon's smartphone theatrics, a quieter revolution was unfolding across its other divisions. The company that had mastered the art of invisible manufacturing was building an empire that touched every corner of India's electronics consumption.

Dixon has India's largest manufacturing plants for LED televisions (in Tirupati), washing machines (in Dehradun) and LED bulbs (in Noida). These weren't just factories—they were statements of intent. The Tirupati LED TV facility, spread across 50 acres, could produce 3 million televisions annually. When Xiaomi needed someone to manufacture their Mi TVs for India, they didn't go to China—they came to Tirupati.

The washing machine facility in Dehradun told another story of strategic positioning. 40% market share in Washing Machine. Dixon manufactured for LG, Samsung, Bosch, and even Voltas. The same facility that produced premium Bosch washing machines in the morning could switch to value-segment Voltas models by afternoon. This flexibility—the ability to manage multiple brands with different quality requirements and price points—was Dixon's secret sauce.

But the real sleeper hit was lighting. Accounts for around 34% of domestic volumes of LED Lighting. In a market dominated by hundreds of small players, Dixon had quietly built scale that mattered. When the government's UJALA scheme needed millions of LED bulbs for distribution, Dixon's Noida facility ran three shifts to meet demand.

The IT hardware opportunity emerged as potentially Dixon's biggest bet outside smartphones. Dixon Technologies, committed to a cumulative production value of Rs 48,000 crore over six years, has been deemed eligible under the restructured production-linked incentive scheme for IT products. With this, the company accounts for one-seventh of the extra production value of Rs 350,000 crore committed collectively by 27 eligible companies over a period of six years.

₹48,000 crores over six years. Let that sink in. That's more revenue than most Indian IT services companies generate. Dixon wasn't just entering laptop manufacturing—it was positioning itself as India's answer to Taiwanese ODMs like Compal and Quanta.

The Inventec joint venture for laptops and servers represented this ambition. The company is setting up an IT hardware manufacturing unit in Chennai for the mass production of laptops for HP and ASUS. Dixon already manufactured for Lenovo and Acer. Adding HP and ASUS would make it India's largest laptop manufacturer by client diversity.

The agency is involved in five out of the 14 PLIs it qualifies for — mobile devices, IT products, refrigerators, LED components, and telecom networks. This wasn't random diversification—it was strategic portfolio construction. Each category supported the others. LED expertise helped in TV backlighting. Mobile phone assembly skills transferred to laptop manufacturing. Washing machine motors informed refrigerator compressor assembly.

The telecom equipment venture with Bharti Airtel for routers and modems opened another frontier. Revenue from telecom equipment such as Wi-Fi routers grew 116% sequentially to ₹3,045 crore in September. As India rolled out 5G and fiber broadband reached rural areas, Dixon was manufacturing the devices that connected India to the digital economy.

Consumer durables remained the steady cash generator that funded ambitious expansions elsewhere. More than 50% market share in Flat Panel Display TV. When Amazon wanted to launch Fire TV in India, they came to Dixon. When OnePlus entered the TV market, Dixon manufactured for them. Even Chinese giant Hisense chose Dixon over its own Chinese facilities for India production.

The refrigerator entry marked Dixon's confidence in attacking established categories. Starting with small-capacity refrigerators for brands like Voltas, the company systematically moved up the value chain. By 2024, it was manufacturing frost-free refrigerators with IoT capabilities—products that would have been unimaginable in an Indian factory a decade ago.

What tied all these diverse categories together was Dixon's operating philosophy: capital efficiency above all else. On existing fixed assets of Rs. 140 crore, as of 31-3-17, company is able to garner topline of Rs. 2,500 crore and bottomline of Rs.50 crore, where utilization levels are between 35-70% for different product streams. High RoCE of 35% (for FY17).

The ability to generate ₹2,500 crores revenue from ₹140 crores of fixed assets was alchemy that befuddled traditional manufacturers. How did Dixon do it? By treating manufacturing as a service, not an asset-heavy business. By sharing facilities across products. By convincing brands to fund working capital. By turning inventory faster than anyone thought possible.

The diversification strategy also provided crucial resilience. When smartphone production slowed, TV manufacturing picked up. When washing machine demand was seasonal, LED bulbs provided steady revenue. This portfolio approach—unsexy but effective—ensured Dixon never faced the feast-or-famine cycles that plagued single-product manufacturers.

Yet questions remained. Could Dixon maintain its capital efficiency as it moved into more complex products? Could it manage the different dynamics of B2B telecom equipment and B2C consumer durables? Most importantly, could it resist the temptation to launch its own brands as margins beckoned?

Sunil Vachani's answer was always the same: "We are manufacturers, not brand builders. The moment we compete with our customers, we lose our reason to exist." It was discipline that few companies maintained once they tasted success. But then again, Dixon had built its empire on doing things few companies would do.

X. Playbook: Business & Strategy Lessons

Inside Dixon's Noida headquarters, there's a framed quote that every employee knows by heart: "The best place to be in a war is Switzerland." This philosophy—absolute neutrality in brand battles while profiting from all combatants—has been Dixon's north star for three decades.

The Switzerland Strategy: Never Compete with Customers

The temptation to launch a Dixon-branded TV or smartphone must have been overwhelming. When you're manufacturing millions of units, why not keep those brand margins for yourself? Company's 5-year average EBITDA margin stood at just 3.5% while the brands Dixon manufactured for enjoyed margins of 8-15%.

But Vachani understood what others didn't: the moment Dixon launched a consumer brand, it would lose Samsung, LG, Xiaomi, and every other client. The ₹18,000 crore revenue would evaporate overnight. Trust, once broken in contract manufacturing, is impossible to rebuild.

This discipline extended to seemingly minor decisions. Dixon never showcased client products at trade shows. Employee NDAs were stricter than intelligence agencies. When one brand's representatives visited, all evidence of other brands was hidden. Dixon's factories were Switzerland—neutral territory where competing brands could manufacture without fear.

Capital-Light Alchemy: The 35% RoCE Magic

Rs. 140 crore fixed assets generating Rs. 2,500 crore revenue, 35% RoCE. These numbers shouldn't be possible in manufacturing. Here's how Dixon achieved the impossible:

First, the company convinced brands to own inventory. Raw materials sitting in Dixon factories were technically owned by Samsung or Xiaomi until the moment of assembly. This freed billions in working capital.

Second, Dixon mastered the art of the negative cash conversion cycle. The company has a negative cash conversion cycle of three days. Dixon collected payment from brands before paying suppliers. In effect, suppliers were funding Dixon's operations.

Third, multi-product facilities created leverage. The same assembly line that made Samsung phones in the morning could make Xiaomi phones by afternoon. The same testing equipment for TVs worked for monitors. Every asset sweated multiple times over.

Fourth, Dixon refused to own what it could lease. Buildings were rented. Expensive equipment was leased. Even some workers were on contract. Fixed costs remained variable, providing flexibility to scale up or down with demand.

Timing the Cycles: Riding Government Waves

Dixon's growth trajectory perfectly aligned with government policy cycles. Make in India (2014), Digital India (2015), PLI schemes (2020)—each wave was caught at exactly the right moment.

This wasn't luck. Dixon maintained deep government relationships without being politically aligned. Bureaucrats trusted them because they delivered on promises. Politicians liked them because they created jobs. Dixon became the go-to example whenever the government needed to showcase manufacturing success.

Sunil Vachani, executive chairman, envisions Dixon concluding this calendar year as the 15th or 16th largest EMS player globally, reaching to the top 10 within five years, and aiming for a top-five position in the next decade. Dixon held the 21st position in 2022.

The PLI game was played masterfully. While competitors fought for allocations, Dixon quietly qualified for five different schemes. When others worried about meeting targets, Dixon exceeded them. When PLI benefits ended, Dixon had already moved to the next scheme.

Managing Complexity: The Orchestra Conductor Model

17 plants, multiple product categories, hundreds of SKUs across 23 manufacturing units across the country. The complexity would break most companies. Dixon thrived on it.

The secret was treating each facility as an independent profit center while maintaining central control over strategy. Plant managers had P&L responsibility but couldn't make capital allocation decisions. Quality standards were non-negotiable centrally but implementation was localized.

Information systems were Dixon's hidden advantage. Real-time visibility into every production line, every inventory position, every quality metric. When a brand called asking about order status, Dixon could tell them exactly which assembly line their products were on.

Structuring JVs: The 51% Rule

Every joint venture followed the same template: Dixon held 51-76% control. Always. No exceptions. Dixon will hold a 51 per cent stake in the joint venture, while Vivo India will own the remaining 49 per cent. This wasn't about ego—it was about ensuring Indian control in an era of techno-nationalism.

The JV structures were sophisticated. Technology transfer obligations were front-loaded. Exit clauses favored Dixon. Intellectual property remained accessible even after partnership dissolution. Dixon learned from every JV, building capabilities that survived beyond individual partnerships.

The Importance of Backward Integration

"Within the next two fiscals, we expect displays, mechanicals, power supplies and other components to represent a $12-billion net addressable industry in India with available margins of around 8%. Of these, Dixon's revenue opportunity can be around $1.5 billion ( ₹13,000 crore) annually".

Backward integration wasn't just about margins—it was about survival. Every component manufactured in-house reduced supply chain risk. Every technology absorbed decreased dependence on foreign partners. The journey from assembler to component manufacturer was Dixon's evolution from contractor to ecosystem builder.

The Unsexy Excellence

Perhaps Dixon's greatest strategic insight was that unsexy businesses could create sexy returns. While India's startup ecosystem chased valuations, Dixon chased cash flows. While consultants preached disruption, Dixon practiced execution. While competitors pursued glamour, Dixon pursued grinding operational excellence.

"We are in the business of outsourcing, which means you have to be frugal and cost conscious, and capital efficiency has to be of the highest order". This belief has been at the core of Dixon's operations.

This wasn't a strategy that made headlines or won business school case studies. But it was a strategy that turned ₹15 lakh into a ₹100,000 crore empire. Sometimes, the best strategies are the ones that nobody wants to copy because they're just too hard to execute.

XI. Analysis & Bear vs. Bull Case

Dixon Technologies stands at a fascinating crossroads—simultaneously India's greatest manufacturing success story and its most polarizing industrial bet. The stock that has created enormous wealth also divides investors like few others. Let's examine both sides of this heated debate.

Bull Case: The Inexorable Rise

The optimists see Dixon as surfing multiple megatrends that will define the next decade of global manufacturing.

Dixon concluding this calendar year as the 15th or 16th largest EMS player globally, reaching to the top 10 within five years, and aiming for a top-five position in the next decade. Dixon held the 21st position in 2022. From 21st to potentially 5th globally—that's not growth, that's transformation. If achieved, Dixon would sit alongside Foxconn, Pegatron, and Flex as a global EMS giant.

The export trajectory provides compelling evidence. Dixon Technologies is expanding its presence in international markets, with a goal of 30-40% of turnover from exports. Export volumes to North America alone are expected to grow from 10 to 12 million in FY26. Manufacturing Google Pixels for the US market isn't just revenue—it's validation that Indian manufacturing can meet the world's highest standards.

China Plus One tailwinds are accelerating, not abating. Every US-China trade skirmish, every supply chain disruption, every geopolitical tension pushes global brands to diversify. India, with its massive domestic market and improving infrastructure, is the obvious beneficiary. Dixon, as India's largest EMS player, captures this shift by default.

The component ecosystem Dixon is building could be the real game-changer. Dixon aims to capture 27% of the BOM in-house by focusing on camera modules, mechanicals, and displays. The CapEx for the HKC plant is around INR375 crores, with expected asset turns of 7-8x. The component business is margin-accretive. If successful, Dixon transforms from low-margin assembler to value-added manufacturer.

The order book visibility is unprecedented. This JV can help Dixon grab over 1/5th of India's 288 million overall mobile phone assembly market and close to 45 million smartphone manufacturing volume. With Vivo, Transsion, Motorola, Google, and others locked in, Dixon has revenue visibility that most manufacturers can only dream of.

Government support remains unwavering. Dixon participates in 5 of 14 PLI schemes. It's the poster child for Make in India. Every new manufacturing initiative features Dixon as a success story. This isn't just about current benefits—it's about being first in line for future support.

The management track record speaks for itself. From ₹15 lakh to ₹100,000 crore market cap. Consistent profitability from day one. Successfully navigating technology transitions from CRT to LCD to LED to smartphones. Few management teams anywhere have delivered such consistent execution over three decades.

Bear Case: The Uncomfortable Truths

The skeptics see fundamental challenges that threaten Dixon's narrative.

Company's 5-year average EBITDA margin stood at just 3.5%. These aren't margins—they're rounding errors. One supply chain disruption, one client loss, one technology transition gone wrong, and profitability evaporates. Operating at such thin margins leaves zero room for error.

Dixon's stock has fallen over 20% since the start of 2025, even as the broader BSE India Manufacturing Index lost just about 5%. The market is clearly worried about something. Smart money doesn't exit a growth story without reason.

The PLI dependency is concerning. PLI scheme adds about 0.6 to 0.7 per cent to its mobile phone revenue margins, mostly passed to customers. When PLI ends in 2026, what happens? Dixon claims volumes will sustain, but without incentives, will brands stay?

Chinese joint venture overdependence creates multiple risks. Vivo, HKC, Longcheer, Chongqing Yuhai—Dixon's growth is increasingly tied to Chinese partners. In an era of techno-nationalism, this is a ticking time bomb. One adverse government decision could unravel years of work.

Revenue from pure-play mobile phone manufacturing dropped 5% sequentially to ₹9,312 crore. This clearly reflected a slowdown in Dixon's production of phones from Motorola. Ismartu alone accounted for 31% of Dixon's quarterly revenue in Q2. Client concentration is dangerous. Losing Motorola or Transsion would crater revenues.

The technology risk is underappreciated. Dixon excels at current-generation manufacturing, but what about next-generation? Can they handle advanced packaging for AI chips? Micro-LED displays? Solid-state batteries? Technology transitions have killed bigger manufacturers.

Competition is intensifying. Tata Electronics has Apple's backing. Foxconn is expanding aggressively. Homegrown players like Kaynes Technology are scaling up. Dixon's first-mover advantage is eroding.

The backward integration bet might backfire. Around $3 Bn will be infused in the project initially with 60% allocation to televisions and 15%-12% allocation to mobile phone manufacturing. That's massive capital in a business Dixon has never operated. Component manufacturing requires different capabilities than assembly. Many have tried and failed.

Valuation concerns are valid. At 65-85x P/E multiples, Dixon is priced for perfection. Any disappointment—a missed quarter, delayed JV approval, client loss—could trigger a brutal correction. The stock has already given multi-bagger returns; how much upside remains?

The Verdict: Schrodinger's Stock

Dixon Technologies exists in a quantum state—simultaneously India's best manufacturing story and its riskiest manufacturing bet. The bull case assumes flawless execution in an increasingly complex world. The bear case sees fragility where others see strength.

Perhaps the truth is that both views are correct. Dixon is building something remarkable—a globally competitive Indian electronics manufacturer. But it's building on foundations that could shift with political winds, technology transitions, or global economic cycles.

For investors, Dixon represents a fundamental question: Do you believe in India's manufacturing destiny? If yes, Dixon is the purest play on that theme. If no, those 3.5% margins should terrify you.

The next 24 months will likely resolve this debate. Either Dixon emerges as a global EMS giant, validating the bulls, or margins compress and growth stalls, vindicating the bears. There's little room for middle ground when you're operating at the edge of possibility.

XII. Epilogue & "If We Were CEOs"

Standing in Dixon's Noida facility, watching thousands of smartphones roll off assembly lines with choreographed precision, one can't help but wonder: What would we do if handed the reins of this industrial empire?

The Apple Imperative

The elephant in every room where Dixon's future is discussed: Apple. While Dixon manufactures for Google, Samsung, Xiaomi, and virtually every major Android brand, the Cupertino giant remains conspicuously absent. Apple's India manufacturing, worth billions, flows through Foxconn, Pegatron, and now Tata Electronics.

If we were CEO, cracking Apple would be Priority #1. Not for the revenue—though that would be massive—but for what it represents. Apple partnership is the ultimate validation of manufacturing excellence. It opens doors globally that no amount of marketing could achieve.

The approach wouldn't be direct. Apple doesn't switch suppliers lightly. Instead, we'd target Apple's peripheral products first—AirPods, cables, accessories. Build trust with smaller orders. Demonstrate capability on less critical products. Then gradually move up the value chain. It might take five years, but the payoff would transform Dixon from Indian champion to global player.

The Technology Moat

Scope for margin expansion and sustainability is both challenging and limited, given the rapid technological changes in the electronics industry, high risk of obsolescence. This is Dixon's Achilles heel—technological dependence on partners.

If we were CEO, we'd launch "Dixon Labs"—not for basic R&D, but for next-generation manufacturing technologies. Partner with IITs and IISc for advanced materials research. Collaborate with global universities on manufacturing automation. The goal isn't to compete with Samsung's R&D, but to become indispensable in manufacturing innovation.

Imagine Dixon developing proprietary assembly techniques that reduce manufacturing time by 20%. Or quality control systems that cut defect rates in half. These aren't product innovations—they're process innovations that create genuine competitive advantages in contract manufacturing.

The Export Transformation

Dixon Technologies is expanding its presence in international markets, with a goal of 30-40% of turnover from exports. This target is too modest. If we were CEO, the goal would be 60% exports by 2030.

Why? Because India's domestic market, while large, is price-sensitive and low-margin. Global markets pay premiums for reliability and quality. More importantly, export success would force Dixon to meet global standards consistently, creating a virtuous cycle of capability building.

The strategy would be targeted: Focus on products where India has comparative advantage. Leverage government relationships for bilateral trade deals. Most importantly, establish Dixon subsidiaries in key markets—not manufacturing, but sales and service centers that provide local support to global brands.

The Vertical Integration Question

The current backward integration strategy focuses on components. If we were CEO, we'd go further—forward integration into services. Not consumer-facing, but brand-facing services that increase stickiness.

Imagine Dixon offering inventory management for brands—holding finished goods and shipping directly to retailers. Or providing after-sales service infrastructure—repair centers that handle warranty claims. Or even financial services—working capital financing for smaller brands that can't match Samsung's payment terms.

These services would transform Dixon from vendor to partner. Switching costs would increase dramatically. Margins would expand without competing with customers.

The Succession Challenge

Sunil Vachani built Dixon from nothing. But founder-led companies face inevitable succession challenges. If we were CEO, institutionalizing Dixon would be paramount.

This means building leadership depth beyond the Vachani-Lall partnership. Creating an employee stock ownership culture that aligns thousands of workers with Dixon's success. Establishing governance structures that survive founder transition. Most importantly, documenting the unwritten rules and relationships that make Dixon work.

The model here is Taiwan's TSMC—a company that successfully transitioned from founder Morris Chang while maintaining excellence. Dixon needs similar institutional strength.

The Next Decade Metrics

If we were CEO, these would be the metrics that matter for 2035: - Revenue: ₹200,000 crores (10x current) - Export percentage: 60% (vs. current 15-20%) - EBITDA margins: 6-8% (vs. current 3.5%) - Component value capture: 40% of BOM (vs. target 27%) - Global EMS ranking: Top 5 (vs. current 15-16) - Employee strength: 100,000 (creating massive employment) - Stock price: ₹50,000 (another 3x from current levels)

Ambitious? Absolutely. Achievable? If the last 30 years are any indication, betting against Dixon would be foolish.

The Real Question

But perhaps the most important question isn't what we would do as CEO—it's whether Dixon's model is the right one for India. Should India's manufacturing champion remain invisible, letting foreign brands capture consumer mindshare? Should Indian companies be satisfied with 3.5% margins while brands earn 15%?

These aren't questions with easy answers. But they're questions that Dixon—and India—must grapple with. The next decade will determine whether Dixon becomes India's Foxconn or transcends that model entirely.

For Sunil Vachani, who started with ₹15 lakh and built a ₹100,000 crore company, the answer might be simple: Keep doing what works. Stay invisible. Stay neutral. Stay focused on execution. Let others chase glory while Dixon quietly builds the infrastructure for India's electronic future.

After all, in manufacturing as in life, the real power often lies not in being seen, but in being essential. And Dixon Technologies, for all its challenges and controversies, has become exactly that—essential to India's manufacturing dreams.

The boy from Noida who borrowed from his father didn't just build a company. He built a template for how India could compete globally—not by copying others, but by finding its own path. Whether that path leads to global dominance or domestic consolidation, only time will tell.

But one thing is certain: The next chapter of Dixon's story will be even more interesting than the first.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube