Delhivery: India's Logistics Revolution

I. Introduction & Episode Roadmap

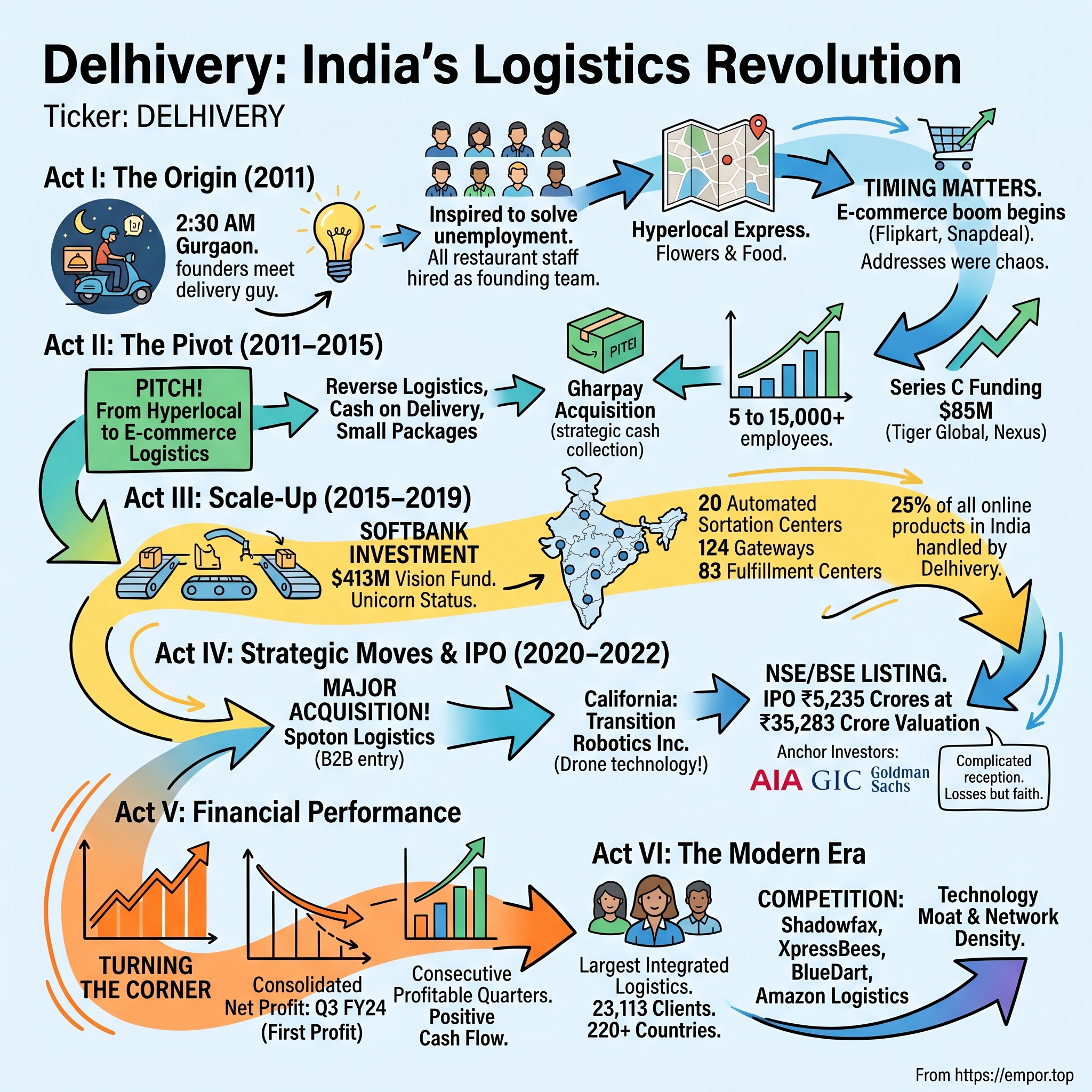

Picture this: It's 2:30 AM in Gurgaon, 2011. Two former Bain consultants are waiting for their late-night food order, making small talk with the delivery guy about unemployment in the city. That conversation—seemingly mundane, utterly forgettable—would spark the creation of India's largest integrated logistics company, now worth over ₹35,000 crores on the public markets.

This is the Delhivery story—how a hyperlocal flower and food delivery startup transformed into the backbone of India's e-commerce infrastructure, handling a quarter of all online products in the country at its peak. It's a tale of perfect timing, relentless pivots, and building physical infrastructure in a country where logistics meant chaos, corruption, and complexity.

Today, Delhivery stands as India's logistics giant, listed on the NSE with operations spanning 220+ countries, 23,000+ clients, and a network that touches nearly every pin code in India. But the journey from those Gurgaon restaurants to unicorn status to public markets wasn't just about riding the e-commerce wave—it was about fundamentally reimagining how goods move through one of the world's most challenging logistics landscapes.

We'll trace this evolution through three distinct acts: First, the origin story and the pivot that saved the company. Second, the scale-up years when they built India's parallel logistics infrastructure from scratch. And finally, the public market debut and the ongoing battle for profitability in a notoriously thin-margin business.

The themes we'll explore resonate far beyond logistics: How do you build infrastructure in emerging markets? Can technology truly differentiate in traditional industries? And perhaps most critically—in a world obsessed with asset-light models, what happens when you bet everything on being asset-heavy?

II. The Origin Story: A Late-Night Food Order

The legend goes like this: It's 11:30 PM in Gurgaon, 2011. Suraj and Sahil ordered food from a nearby restaurant, striking up what should have been a forgettable conversation with the delivery guy. But the delivery person spoke of the problem of unemployment that was about to break out, mentioning how the restaurant was planning to shut down and everyone would lose their jobs.

Something about that moment struck a nerve. This made the founders rush down to the store and talk to the manager. Soon they were at the restaurant, talking to the owner, who further elaborated on his plans of closing down the business and moving his staff elsewhere. The owner was Anuj Bajaj, still there at that ungodly hour, perhaps contemplating the end of his venture.

What happened next defied all consulting logic. Here's where Sahil and Suraj decided to start their delivery business, Delhivery. Yes, they hired all of them! Every single employee from that shuttering restaurant became the founding team of what would become India's logistics backbone.

This wasn't your typical Silicon Valley garage startup story. This was five engineers—Sahil Barua, Mohit Tandon, Bhavesh Manglani, Suraj Saharan, and Kapil Bharati—deciding to solve unemployment by creating a hyperlocal delivery company. The backgrounds were impressive enough to raise eyebrows: Sahil Barua holds a Bachelor of Engineering in Mechanical Engineering from the National Institute of Technology, Karnataka, and is a post-graduate from the Indian Institute of Management, Bangalore. His father, Samir Kumar Barua, served as a professor at IIM Ahmedabad—the academic pedigree ran deep.

Barua and Tandon weren't just any consultants—they were Bain & Company associates, trained in the art of strategic thinking and market analysis. They knew how to build PowerPoints that could convince Fortune 500 CEOs to restructure entire divisions. Yet here they were, setting up their first corporate office at Gurgaon with a sum of 10 individuals, including 4 delivery individuals.

Delhivery was established in May 2011 as SSN Logistics Ltd, initially conceptualised as a hyperlocal express delivery service provider for offline stores, delivering flowers and food in Gurgaon. The company started with an absurdly simple model: they started connecting with local restaurants and fulfilling their orders within half an hour. No algorithms, no machine learning—just raw hustle and a promise of 30-minute delivery in a country where "on time" was a foreign concept.

But timing, as they say in venture capital, is everything. During that time, the online retailing and e-commerce segment was expanding rapidly in India, with global investors showing significant interest in the industry. Flipkart had just raised its Series C. Snapdeal was gaining momentum. The e-commerce gold rush was beginning, and nobody had figured out how to actually deliver all those packages in a country with addresses like "opposite the big banyan tree, next to Sharma ji's house."

The founding quintet brought complementary skills: Sahil Barua is the CEO of Delhivery and Co-Founder Kapil Bharati is the CTO of Delhivery. Bharati wasn't just another IIT grad—he had worked as the technical lead for livemint.com and the ht blogs at Hindustan Times, and had previously co-founded two other businesses, 11Rupees and Contify.com. This wasn't his first rodeo.

The initial phase was pure chaos meets determination. They had no infrastructure, no technology platform, and were competing against established players who'd been moving packages since before the internet existed. But they had one insight that would change everything: they understood that e-commerce logistics wasn't just traditional logistics with a website slapped on top. It was fundamentally different—requiring reverse logistics, cash on delivery, and the ability to handle millions of small packages instead of thousands of large shipments.

With an undisclosed sum from Abhishek Goyal (urbantouch.com), they started the initial period of Delhivery. Urban Touch would become their first e-commerce client, marking the beginning of a pivot that would define their destiny. Because while the flower and food delivery business was working, the founders could see a much bigger opportunity emerging. India was about to experience an e-commerce explosion, and someone needed to build the pipes.

III. The Pivot: From Hyperlocal to E-commerce Logistics (2011–2015)

By August 2011, Delhivery had switched completely to offering logistics services to a number of e-commerce companies. Three months. That's all it took for the founders to realize their flower and food delivery model wasn't where the real opportunity lay. The insight came not from consultants' frameworks or market research, but from watching the chaos unfold around them.

It began as a courier service for e-commerce companies such as Snapdeal and Myntra. But this wasn't just adding new clients—it was a fundamental reimagining of what logistics meant in the digital age. The founders grasped the key component which had been overlooked by many other players: traditional delivery and e-commerce delivery are very different, there is a lot of scope in the e-commerce sector.

Think about it: Traditional logistics moved pallets between warehouses. E-commerce logistics meant delivering a single phone case to an address that might not even have a proper street name. Traditional logistics dealt with scheduled shipments. E-commerce meant customers tracking packages every five minutes, expecting delivery yesterday. And perhaps most critically—in a country where credit card penetration was under 2%—e-commerce logistics meant handling cash on delivery, turning delivery boys into mobile ATMs.

The early clients tell the story of India's e-commerce explosion. Delhivery began as a last-mile logistics partner for Urbantouch and Healthkart in Gurgaon. But the real game-changer came with Snapdeal and Myntra. Within two years of its launch, the company expanded rapidly because demand for home deliveries increased exponentially as a result of the rise in online shopping on these sites.

The infrastructure build-out was nothing short of miraculous. Having started in 2011 with just 5 employees, Delhivery has come a long way with more than 3500 employees. By 2013, they were delivering around 15,000 to 20,000 shipments everyday... handling logistics for more than 100 clients including Snapdeal, Myntra and Indiatimes Shopping.

The funding story paralleled the operational scale-up. In June 2012, Indiatimes Shopping, an online retail arm of Times Internet Limited (TIL), bought minority stake in Delhivery after investing an undisclosed sum... said to be in the range of $2-5 million. This wasn't just capital—it was validation from one of India's largest media conglomerates that these ex-consultants were onto something big.

Earlier this year [2013], Delhivery acquired offline cash collection network of Gharpay for an undisclosed amount. This acquisition was strategic genius—Gharpay had cracked the cash-on-delivery problem that plagued every e-commerce company. As Tandon explained, "Even before acquiring GharPay, we have been offering multiple payment options to our clients' customers through different mediums like cash, cheque or POS credit and debit card swipe. GharPay's strong network and expertise will give us greater control on cash collection for our partners."

By 2015, the transformation was complete. The company raised $85M in Series C funding in May 2015 from Tiger Global Management and Nexus Venture Partners. This wasn't seed money anymore—this was growth capital from some of the smartest money in venture capital, betting that Delhivery would become the logistics backbone of India's e-commerce revolution.

The numbers told a story of breakneck growth. From 5 members to 15,000 employees. From one Gurgaon restaurant to serving over 1500 pincodes. From handling a few food orders to moving 20,000 packages daily. The company was growing at 65% annually between 2015-2018, a pace that would make even software companies jealous.

But perhaps the most impressive pivot wasn't operational—it was psychological. These founders had transformed from building a hyperlocal delivery service to save a few jobs into architecting India's e-commerce infrastructure. They weren't just moving packages anymore; they were enabling an entire generation of online businesses to exist. Without Delhivery and companies like it, India's e-commerce miracle simply couldn't have happened.

IV. The Scale-Up Years: Building India's Logistics Network (2015–2019)

March 25, 2019. The headlines screamed across financial media: Delhivery has become the first Indian logistics company to enter the coveted unicorn club (companies valued over $1 billion) after SoftBank invested $413 million from its Vision Fund into the company on Sunday. But this wasn't just another unicorn story. This was validation that physical infrastructure could be as valuable as software in the digital age.

The journey from 2015 to 2019 reads like a masterclass in operational excellence at breakneck speed. Consider the scale: By 2019, a quarter of all online products in India were passing through Delhivery's channel. Not a quarter of packages from one e-commerce company—a quarter of everything ordered online in a nation of 1.3 billion people.

The infrastructure build-out during these years was staggering. At present, Delhivery already operates 20 automated sortation centres, 124 gateways, and 83 fulfillment centres across India. Each of these wasn't just a warehouse—it was a node in India's emerging digital commerce nervous system. The company had built 45 automated sortation centers and 119 gateways across India, with a rated automated sort capacity of 7.1 million shipments per day.

But automation wasn't just about buying machines. It was about reimagining how packages move through a country where addresses could be "third house from the temple" and where monsoons could shut down entire cities. The company has set up two sortation machines, one for handling B2B shipments and the other for B2C, with the latter having a capacity of up to 48,000 parcels per hour. To put that in perspective, that's processing a package every 0.075 seconds—faster than you can blink.

The technology investments went beyond hardware. Machine learning algorithms predicted delivery times in cities where traffic could vary from free-flowing to complete gridlock within hours. Data intelligence systems tracked patterns across millions of shipments, learning that packages to Bangalore's IT corridor needed different handling than those going to old Delhi's narrow lanes.

The full suite expansion was methodical yet aggressive. Last-mile delivery—check. Warehousing—check. But then came the harder problems: reverse logistics (because Indians returned 30% of what they ordered online), payment collection (remember, this was still largely a cash economy), vendor shipping (helping sellers get products to warehouses), and cross-border services (because Indian SMEs wanted to sell globally).

The SoftBank moment deserves deeper examination. Valuing the delivery firm at close to $2 billion, SoftBank picked a massive 22.4 per cent stake. According to sources in the company, this stake buy gives SoftBank a seat on the board of Delhivery. This wasn't just capital—it was Masayoshi Son betting that India's e-commerce revolution needed physical infrastructure as much as it needed apps.

"We will be scaling up our newer warehousing and freight services through large investments in infrastructure and technology and global partnerships in addition to improving the reach, reliability and efficiency of our transportation operations and sharing these benefits with our customers and partners," Delhivery Chief Executive Officer Sahil Barua said.

The funding came with existing heavy-hitters doubling down. Existing investors Carlyle Group and Fosun international also participated in the latest round of equity financing at Delhivery, raising its valuation to more than $1.5 billion. When private equity giants and Chinese conglomerates join hands with SoftBank, you know something fundamental is shifting in the market.

The operational metrics by 2019 painted a picture of controlled chaos at massive scale: 3,645 Number of Express delivery centres, 853 Partner centres, 159 processing centres and Team Size of 73,748 members serving 38044 Active Customers and manages a daily average fleet size of 16,357 overall. This wasn't just growth—it was building a parallel postal system for the digital age.

The strategic moves during this period showed sophisticated thinking. Delhivery plans to work closely with Falcon Autotech to design and implement new automation solutions for transportation and warehousing operations. The partnership will also enable the bundling of the hardware automated solutions along with Delhivery's SaaS platform; one of the proposed growth verticals for Delhivery in the national and international market.

By 2019, Delhivery had achieved something remarkable: it had made logistics sexy. In a country where "supply chain" meant trucks stuck at state borders paying bribes, they had built a network that could move a package from Kashmir to Kanyakumari faster than the postal service could move it across Delhi. They had taken an industry associated with sweat and diesel and infused it with algorithms and automation.

The plans to add 5,000 new pin codes to the current 15,000 by the first half of 2020 showed ambition that went beyond the metros and tier-1 cities. This was about bringing e-commerce to Bharat, not just India—to the small towns and villages where the next billion consumers lived.

V. Major Acquisitions & Strategic Moves

August 2021. The boardroom at Delhivery must have been electric. They were about to write a check for ₹1,600 crore (US$190 million) to acquire Spoton Logistics—their biggest acquisition ever and a move that would fundamentally reshape India's B2B logistics landscape.

This wasn't just buying market share. Spoton was everything Delhivery wasn't. Headquartered in Bengaluru, Spoton grew from ₹180 crore revenue in 2012 to more than a ₹1,000 crore run rate in 2020. The company had grown close to 10 percent YoY in revenue in FY2021 and closed H2 with a growth of 34 percent. More importantly, Spoton ticks all the right boxes for Delhivery as it has shown consistent growth, has professional management, is profitable and is debt-free with a very healthy cash flow.

The strategic logic was impeccable. Since the operational nuances of B2C and B2B are different, it is the highlight of this acquisition. While Delhivery had mastered the chaos of e-commerce—unpredictable volumes, cash on delivery, high returns—Spoton had built trust with enterprises that shipped predictably, paid on time, and valued reliability over speed.

It has a team of more than 1600 plus employees and operates a pan India network covering 300+ locations and over 22,000+ pin codes. It has 13 major depots and 35 transit hubs to facilitate the timely and secure movement of goods. Each of these assets would now plug into Delhivery's network, creating synergies that spreadsheets could barely capture.

Sahil Barua's statement revealed the ambition: Over 10 years, Delhivery has established a leading position in B2C logistics and now by combining our part truckload business with Spoton's, we will be on the path to the same position in B2B express as well. This wasn't consolidation—it was category creation. They were building something that didn't exist: a logistics company that could handle everything from a single mobile phone case to a truckload of automotive parts.

The cultural integration challenges couldn't be ignored. We feel that integration of two competing express businesses might be a challenge for Delhivery considering the difference in the culture of both organizations. Spoton was traditional, relationship-driven, focused on operational excellence. Delhivery was tech-first, venture-backed, moving at startup speed. Making these cultures mesh would be like merging a Swiss watch manufacturer with a Silicon Valley software company.

But the boldest move came four months later. In December 2021, it acquired California-based unmanned aircraft system company Transition Robotics Inc. This wasn't about today or tomorrow—this was about 2030. In a country where drone regulations were just being written, where last-mile delivery still meant motorcycles navigating narrow lanes, Delhivery was buying drone technology from Santa Cruz.

TRI was founded in 2011, and the company has worked on unmanned aerial drones since its beginning. Today, TRI specializes in vehicle design, electronic design, software and controls, ground testing and flight testing. The crown jewel was JumpShip—JumpShip is a fully autonomous drone platform that allows operators to combine the operational flexibility of a multi-rotor with the fast flight of a fixed-wing aircraft.

The intellectual property transfer was comprehensive. With the acquisition, all of TRI's intellectual property registered in the U.S. will be assigned to Delhivery. This strengthens Delhivery's capabilities in many different applications, including aerial photography, remote sensing, inspection and surveys. While competitors were still figuring out how to deliver packages on time, Delhivery was preparing for a world where drones would handle last-mile delivery.

Kapil Bharati, the CTO, framed it perfectly: While we continue to build our supply chain platform, we must look at the long-term developments poised to shape the industry. This was chess, not checkers. While everyone else was optimizing today's logistics, Delhivery was building tomorrow's.

The expansion plans went beyond acquisitions. Adding 5,000 new pin codes meant reaching the real India—the small towns where Amazon and Flipkart were just names on smartphones, where reliable delivery could unlock entire markets. The SME supply chain platform wasn't just about serving small businesses; it was about becoming the operating system for India's vast unorganized retail sector.

The technology stack development showed sophisticated thinking. This wasn't about buying off-the-shelf warehouse management systems. They were building proprietary systems that understood Indian addresses ("near the temple" actually meant something to their algorithms), Indian payment habits (cash on delivery wasn't going away), and Indian shopping patterns (festival sales could 10x normal volumes).

By the end of 2021, Delhivery had transformed from a logistics company into something more ambitious—a commerce enabler. They weren't just moving packages; they were building the infrastructure for India's economic transformation. Every acquisition, every technology investment, every new pin code added was a bet that India's consumption story was just beginning.

VI. The IPO Journey: Testing Public Markets (2022)

May 24, 2022. 9:15 AM. The pre-market session at the NSE had just opened, and thousands of investors were glued to their screens. Delhivery, the poster child of India's logistics revolution, was about to test whether public markets had appetite for loss-making new-age companies in a world where interest rates were rising and tech stocks were crashing globally.

The IPO had been a marathon in the making. Delhivery raised ₹2,347 crore (US$280 million) of funding from 64 anchor investors ahead of its initial public offering in May 2022. In May 2022, Delhivery launched its initial public offering (IPO) of ₹5,235 crore (US$620 million) at a valuation of ₹35,283 crore (US$4.2 billion) and got listed on the BSE and the NSE.

The structure told a story of ambition and necessity. The IPO is a combination of fresh issue of 8.21 crore shares aggregating to ₹4,000.00 crores and offer for sale of 2.54 crore shares aggregating to ₹1,235.00 crores. The fresh capital wasn't for vanity metrics—it was for survival and growth in a capital-intensive business where every new pin code meant building infrastructure.

The anchor investor round had been a masterclass in institutional fundraising. Delhivery raises Rs 2,347 crores from anchor investors ahead of IPO. The participants in anchor round of Delhivery IPO include AIA Singapore, Amansa Holdings, Aberdeen New India Investment Trust Plc, Goldman Sachs, The Master Trust Bank of Japan, Government of Singapore, Monetary Authority of Singapore, Fidelity, Tiger Global Investments Fund, Steadview Capital Master Fund, Morgan Stanley Asia (Singapore) Pte, Societe Generale and Segantii India Mauritius are among the anchor investors. SBI Mutual Fund (MF), HDFC MF, ICICI Prudential MF, Mirae MF, ICICI Prudential MF, Invesco MF and Nippon India too participated in the anchor round.

When the global titans and domestic mutual funds write checks of this size, it's validation. But public markets are different beasts—retail investors don't care about TAM slides or cohort analyses. They care about profits, and Delhivery didn't have any.

The market reception was... complicated. The IPO of Delhivery was subscribed to 1.63 times. Not the blockbuster 50x oversubscription that Indian IPOs often see, but solid enough given the market conditions. This was May 2022—the NASDAQ was in freefall, the Fed was hiking rates, and anything that looked like a tech stock was getting murdered.

The price band had been set at ₹462-487 per share, valuing the company at ₹35,283 crore at the upper end. The math was aggressive: enterprise value of around ₹29,000 crores, trading at 4.5 times annualized revenue. For a company that had never turned a profit, this required faith in the India story and the logistics opportunity.

Then came listing day drama. The grey market was whispering disaster. According to data available online, the Delhivery IPO GMP stands at minus 5 rupees. This means the shares could list at a discount of Rs 5 per share. The company had fixed the share price at Rs 487 per share. After considering the GMP, the IPO may list at Rs 482 tomorrow.

But markets have a way of surprising. The shares opened with a 1.7% premium and closed the day up nearly 10%. Not spectacular, but in a market where Paytm had crashed 27% on listing day just months earlier, this was victory. Delhivery had crossed the public market rubicon without drowning.

The significance went beyond the numbers. This was the first major new-age tech startup IPO in 2022 amid a global slowdown. Every other unicorn was watching—if Delhivery could make it work, maybe there was hope for others. If it failed, the IPO window would slam shut for years.

The offering structure revealed strategic thinking about the future. The ₹4,000 crore fresh issue wasn't just growth capital—it was a war chest for what management saw coming. Funding Organic Growth Initiatives. Funding Inorganic Growth Through Acquisitions & Other Strtegic Initiatives. General Corporate Purposes. Translation: We're going to keep burning cash to build infrastructure, we're going to buy more companies, and we need a buffer because this is going to be a long journey.

The exit of selling shareholders was equally telling. 200.00 crores by Deli CMF Pte. Ltd., 9,322,586 equity shares aggregating to Rs. 454.00 crores by CA Swift Investments, 7,495,031 equity shares aggregating to Rs. 365.00 crores by SVF Doorbell (Cayman) Ltd, 3,388,164 equity shares aggregating to Rs. 165.00 crores by Times Internet Limited. The VCs were taking chips off the table—not a full exit, but enough to return their funds and then some.

The retail participation painted a picture of cautious optimism. Retail Portion10% (Number of Retail Applications : 3,56,870 Approx) Nearly 360,000 retail applications—decent but not overwhelming. The Indian retail investor, burned by recent IPO disasters, was being selective.

But perhaps the most important aspect of the IPO was what it represented for India's startup ecosystem. For a decade, Indian startups had been valued on promise and potential, funded by private capital that could afford to wait. Public markets demand quarterly results, profitability paths, and predictable growth. Delhivery's IPO was the first test of whether Indian investors would buy into the "we'll be profitable eventually" narrative that had worked so well in private markets.

The company's disclosure in the prospectus was brutally honest about the challenges ahead. Losses had been mounting, competition was intensifying, and the path to profitability was uncertain. Yet here they were, asking public investors to bet ₹35,000 crores on a vision of India where every package could be delivered anywhere, anytime, profitably.

The IPO also marked a generational transition in Indian capital markets. This wasn't a family-owned conglomerate or a profitable IT services company going public. This was a venture-backed, technology-enabled, loss-making logistics company asking to be valued like a tech company while operating in the physical world. The fact that it worked—even modestly—opened doors for every other startup dreaming of public markets.

VII. Financial Performance & Unit Economics

VII. Financial Performance & Unit Economics

The numbers tell a story of transformation. Operating income during FY24 rose 12.7% YoY, while the net loss narrowed dramatically from ₹10,078 million in FY23 to ₹2,492 million in FY24. Over the past 5 years, despite losses, revenue has grown at a 30.2% CAGR—a testament to the scale-up strategy working even as profitability remained elusive.

But the real story isn't in the annual numbers—it's in the quarterly trajectory. Delhivery turned profitable in Q3 FY24, posting a consolidated profit after tax of ₹11.7 crore—the first time the company had seen black ink on its bottom line. This wasn't a one-off event driven by exceptional items. The company reported an EBITDA of ₹109 crore during Q3 FY24 against an EBITDA loss of ₹72 crore in the year-ago quarter, showing operational leverage finally kicking in.

The momentum continued into Q4 FY24, though with a stumble. After reporting its maiden profitable quarter in Q3, Delhivery slipped back into losses in Q4 with a consolidated net loss of ₹69 crore, though this was an improvement from the ₹159 crore loss in Q4 FY23. The culprit? Seasonality and a broader e-commerce slowdown that hit express parcel volumes.

Yet the full-year FY24 picture showed undeniable progress. FY24 was the first full year of Delhivery's EBITDA profitability at ₹127 crore, with losses narrowing 75% YoY to ₹249.2 crore and operating revenue increasing 13% YoY to ₹8,142 crore. The path to profitability wasn't theoretical anymore—it was happening quarter by quarter.

The cash flow turnaround was perhaps even more impressive. Cash flow from operations turned positive in FY24 at ₹4,724 million compared to negative ₹297 million in FY23, while cash flow from investments improved to negative ₹991 million from negative ₹34,107 million in FY23. This wasn't just accounting profits—this was real cash generation, the lifeblood of any capital-intensive business.

By Q1 FY25, the profitability wasn't a fluke. Delhivery's net profit jumped 67.49% YoY to ₹91.05 crore in Q1 FY25, with net profit margins jumping 57.7% YoY to 3.76%. The company had turned the corner, posting consecutive profitable quarters and showing that the business model could generate returns at scale.

Q2 FY25 continued the streak with a consolidated net profit of ₹10.2 crore versus a loss of ₹102.9 crore in the year-ago quarter—the second consecutive profitable quarter. Revenue from services jumped 13% to ₹2,189.7 crore, with Express Parcel and Part Truckload revenue rising 7% and 27% YoY respectively.

The unit economics breakdown revealed where the leverage was coming from. Operating profit margins had compressed from 6.1% in FY23 to 1.4% in FY24, but this masked the quarterly improvement trajectory. Express parcel economics were improving with scale—each additional package through the network carried minimal incremental cost once the infrastructure was in place.

The expense management showed discipline. Delhivery managed to trim employee costs by 4.7% to ₹349.3 crore in Q2 FY25 from ₹366.7 crore in the year-ago quarter, even as volumes grew. This wasn't about cutting muscle—it was about automation and efficiency gains finally showing up in the P&L.

Return metrics remained challenging but improving. ROCE improved to negative 1.8% in FY24 from negative 11.0% in FY23, while ROA improved to negative 1.4% from negative 8.2%. Still negative, but the trajectory was unmistakable—each quarter brought the company closer to generating positive returns on capital.

The balance sheet had also strengthened considerably. Long-term debt fell 64.9% to ₹402 million from ₹1 billion in FY23, reducing financial risk. Cash and cash equivalents stood at ₹5,488 crore as of September 30, 2024—a war chest for growth without dilution.

Market perception was shifting too. The trailing twelve-month EPS improved to negative ₹3.4 from negative ₹13.8 the previous year. Still loss-making on an annual basis, but the quarterly profits were changing the narrative. This wasn't a cash-burning startup anymore—it was a business approaching sustainable profitability.

The segment performance told different stories. Express parcel, the core business, was showing steady growth but margin pressure from competition. Part Truckload (PTL) was the star, growing rapidly with better economics. Supply chain services showed volatility but higher margins. Each segment was at a different point in its maturity curve, providing natural hedging against market cycles.

VIII. The Modern Era: Market Position & Competition (2020–Today)

Today's Delhivery operates at a scale that would have seemed impossible during those early Gurgaon days. The company has emerged as the largest and fastest-growing fully integrated logistics company in India by revenue in FY24, providing services across 220+ countries and territories. The transformation from startup to incumbent happened faster than anyone expected.

The customer base tells the story of market dominance. With 23,113 active clients spanning e-commerce giants, D2C brands, enterprises, and SMEs, Delhivery has become the default logistics partner for digital India. From the smallest Shopify store to the largest e-commerce platforms, everyone needs Delhivery's network to reach customers.

But dominance breeds competition. The landscape has evolved dramatically since 2020, with new players backed by serious capital challenging Delhivery's position. Shadowfax, backed by Flipkart, focuses on same-day delivery in metros. XpressBees, spun out from FirstCry, leverages its e-commerce DNA. Holisol Logistics brings traditional logistics expertise to the e-commerce game.

The international competition is equally fierce. BlueDart, backed by DHL's global network, maintains premium positioning. Mahindra Logistics leverages the conglomerate's reach. FedEx and UPS nibble at the high-margin express segments. Amazon's captive logistics threatens to internalize volumes. Each competitor attacks a different flank, forcing Delhivery to defend on multiple fronts.

The leadership transition in March 2021 marked a pivotal moment. Two of the five founders exited, leaving Sahil Barua to steer the ship alone. In startup mythology, founder exits often signal trouble. But Delhivery's performance post-exit suggested institutional strength beyond individual founders. The company had grown beyond its creators.

Current ownership reflects the institutional maturity: market cap of ₹34,950 crore with SoftBank holding 11.74%, though the company shows a concerning -4.42% return on equity over the last 3 years. The negative ROE reflects the accumulated losses, but also the massive capital invested in building infrastructure that's yet to fully monetize.

The strategic partnerships reveal ambition beyond logistics. The RCB sponsorship in IPL 2024 wasn't just marketing—it was a statement that Delhivery had arrived as a consumer brand. In a country where cricket is religion, associating with IPL meant mainstream recognition, crucial for hiring, partnerships, and brand value.

Technology differentiation has become the competitive moat. While competitors can replicate trucks and warehouses, Delhivery's years of data on Indian addresses, delivery patterns, and customer behavior create algorithms that newcomers can't easily match. The machine learning models that predict delivery times in Bangalore traffic or optimize routes during Mumbai monsoons represent billions of data points processed over a decade.

The network density provides another advantage. In logistics, density drives economics—more packages per route means lower cost per package. Delhivery's scale allows it to aggregate demand in ways smaller players cannot, creating a virtuous cycle where scale begets efficiency begets more scale.

The market segmentation strategy shows sophistication. Express parcel for e-commerce speed. PTL for SME cost-efficiency. Supply chain services for enterprise complexity. Cross-border for global ambitions. Each segment requires different capabilities, but all leverage the same underlying infrastructure, creating operating leverage competitors struggle to match.

Recent contract wins validate the strategy. Important contracts from marquee clients like Havells, TATA Motors, and MamaEarth in Q1 FY24 show that Delhivery isn't just an e-commerce play anymore—it's becoming the logistics partner for corporate India's digital transformation.

The infrastructure expansion continues relentlessly. In December 2023, Delhivery launched its trucking terminal near Bhiwandi in Maharashtra, strategically located to serve Mumbai, India's commercial capital. Each new facility isn't just capacity—it's a node that makes the entire network more valuable.

But challenges loom large. The e-commerce growth rates that powered Delhivery's rise are moderating. Quick commerce players like Blinkit and Zepto are building their own delivery networks for 10-minute delivery, potentially fragmenting the market. International players are getting aggressive, and Amazon's logistics ambitions threaten to internalize significant volumes.

The regulatory environment adds complexity. State-level regulations, GST complications, and labor laws create operational challenges that pure-play tech companies don't face. Environmental regulations around emissions and packaging will require significant investments. Data privacy laws affect the algorithms that power operations.

Yet Delhivery's response has been to double down on its integrated model. While others specialize, Delhivery builds the full stack. While others focus on metros, Delhivery expands to Bharat. While others chase profitability through cost-cutting, Delhivery invests in automation and technology. It's a bet that India's logistics winner will be whoever can serve everyone, everywhere, everything.

Management's confidence shows in their guidance: "H2 has begun as per our expectations, with October Express volumes of 70M and daily PTL volumes beginning to touch 4,700-5,000MT levels. Service quality remained robust throughout H1 and network utilization remained stable even as we expanded capacity". This isn't the language of a company playing defense—it's the confidence of a market leader extending its lead.

IX. Playbook: Business & Investing Lessons

The Delhivery story offers a masterclass in building physical infrastructure businesses in emerging markets—a playbook that challenges Silicon Valley's asset-light orthodoxy.

Lesson 1: Timing Isn't Everything, But It's Close

Delhivery didn't invent logistics or e-commerce. They simply existed at the intersection when India's digital commerce explosion met inadequate logistics infrastructure. Starting in 2011 meant riding a decade-long e-commerce boom that took GMV from $2 billion to over $100 billion. Earlier, and they'd have burned out waiting for demand. Later, and entrenched players would have locked up the market. The lesson: In emerging markets, infrastructure plays require perfect timing between demand emergence and supply inadequacy.

Lesson 2: Network Effects in Physical Businesses Are Real but Different

Unlike social networks where users attract users, logistics network effects are about density economics. Each additional package makes the network more efficient, lowering per-unit costs, enabling lower prices, attracting more volume. It's a slower flywheel than software, requiring massive upfront capital, but once spinning, it's harder to disrupt. Delhivery's 200+ million packages per quarter create route density no competitor can match without similar scale.

Lesson 3: Technology as Enabler, Not Product

Delhivery never positioned itself as a tech company, despite employing hundreds of engineers. Technology was always the means—to route better, track accurately, predict reliably—never the end. This pragmatic approach avoided the trap of over-engineering solutions for problems that didn't exist. Their address parsing algorithm doesn't win Computer Science awards, but it can decode "opposite temple, blue gate" into deliverable coordinates.

Lesson 4: Capital Intensity as Moat

Conventional wisdom says capital-light businesses are superior. Delhivery proves the opposite can be true in emerging markets. The ₹35,000+ crore invested in infrastructure isn't just sunk cost—it's a moat competitors must match to compete. In developed markets with existing infrastructure, asset-light makes sense. In India, owning the assets means controlling destiny.

Lesson 5: The J-Curve of Physical Infrastructure

Software companies can show positive unit economics from day one, scaling profits with revenue. Physical infrastructure follows a J-curve: massive losses while building capacity, breakeven as utilization improves, then exponential profitability as fixed costs spread over growing volumes. Delhivery's journey from ₹10,000 crore losses to quarterly profits exemplifies this pattern. Investors who understand this J-curve can find opportunities others miss.

Lesson 6: Vertical Integration in Chaotic Markets

In organized markets, specialization works. In India's chaotic logistics landscape, vertical integration was survival. Delhivery built everything: first-mile pickup, middle-mile transport, sortation centers, last-mile delivery, even cash collection. Each piece they didn't control was a point of failure. The lesson: In emerging markets, own the full stack or risk the weakest link breaking your chain.

Lesson 7: Patient Capital's Competitive Advantage

SoftBank's $400+ million investment wasn't just capital—it was patient capital. Unlike traditional VCs expecting 3-5 year exits, SoftBank could wait a decade for profitability. This patience allowed Delhivery to make long-term infrastructure investments competitors couldn't match. The investing lesson: In infrastructure plays, time horizon is alpha.

Lesson 8: Founder Evolution or Exit

Most founders can't evolve from startup hustlers to public company CEOs. Delhivery's founder transition—two exits, three remaining—shows pragmatic recognition that different stages need different skills. Sahil Barua's evolution from Bain consultant to startup founder to public company CEO is rare. For investors, founder quality matters, but institutional strength matters more.

Lesson 9: Market Creation vs. Market Share

Delhivery didn't steal market share from incumbents—they created new markets. Traditional logistics couldn't handle e-commerce's requirements: small packages, cash on delivery, reverse logistics, address complexity. By solving these unique problems, Delhivery expanded the pie rather than fighting for slices. The lesson: In emerging markets, creating markets often beats competing in existing ones.

Lesson 10: The Bharat Opportunity

While competitors fight over metros, Delhivery's expansion to 20,000+ pin codes targets Bharat—small-town India where e-commerce is just beginning. Lower competition, loyal customers, and eventual higher margins make rural expansion strategic despite current losses. The investing insight: In emerging markets, go where others won't, not where others are.

Lesson 11: Losses Aren't Always Bad

Delhivery burned over ₹15,000 crore before turning profitable. Traditional value investors would have avoided it. But these losses built infrastructure worth multiples of the burn. The lesson: Distinguish between losses from building assets versus losses from subsidizing customers. The former creates value; the latter destroys it.

Lesson 12: Public Markets as Validation and Discipline

Going public at losses was risky but necessary. Public markets provided permanent capital, acquisition currency, and credibility with enterprise clients. More importantly, quarterly scrutiny forced operational discipline that private markets might not have demanded. Sometimes, public market pressure accelerates the path to profitability.

X. Analysis & Bear vs. Bull Case

Bull Case: The Infrastructure Monopoly Thesis

The optimists see Delhivery as India's logistics railroad—critical infrastructure that becomes more valuable as the economy digitizes. With e-commerce penetration at just 5% versus 15%+ in China and 20%+ in developed markets, the runway appears massive. If India's e-commerce reaches $350 billion by 2030 as projected, logistics spend could hit $35 billion, with Delhivery capturing significant share.

The profitability inflection supports this thesis. After years of losses, consecutive profitable quarters with improving margins—net profit jumped 67.49% YoY to ₹91.05 crore in Q1 FY25 with margins improving to 3.76%—suggest the J-curve is finally bending upward. Once infrastructure utilization hits optimal levels, incremental revenue drops straight to the bottom line.

The competitive moat appears sustainable. Building Delhivery's network today would require $2+ billion and a decade of losses—barriers few can cross. Network density advantages compound daily. Technology differentiation from billions of data points can't be replicated overnight. Customer relationships spanning 23,000+ clients create switching costs. Together, these create a fortress that gets stronger with scale.

Strategic acquisitions have expanded capabilities without dilution. Spoton brought B2B expertise and profitable operations. Transition Robotics provides future technology options. The M&A pipeline could accelerate consolidation, with Delhivery as the natural acquirer given its public currency and scale advantages.

The management evolution from founder-led to professionally-run demonstrates institutional maturity. Sahil Barua has proven capable of managing public market expectations while maintaining growth momentum. The board includes independent directors with global experience. Governance improvements satisfy institutional investors demanding transparency.

International expansion potential remains untapped. Cross-border services are growing 40%+ annually. Indian SMEs increasingly sell globally through platforms like Amazon Global and eBay. Delhivery's infrastructure could enable millions of small exporters, creating new revenue streams with higher margins than domestic delivery.

Bear Case: The Commoditization Trap

Skeptics see a capital-intensive, low-margin business in a commoditizing industry where scale doesn't guarantee profitability. The concerning -4.42% return on equity over the last 3 years despite ₹34,950 crore market cap suggests the business model might never generate acceptable returns on invested capital.

Competition is intensifying from every angle. Amazon's logistics buildout threatens to internalize 20-30% of e-commerce volumes. Quick commerce players like Blinkit bypass traditional logistics entirely. Regional players offer lower prices by focusing on specific routes. BlueDart maintains premium positioning with better service quality. This multi-front battle compresses margins permanently.

The unit economics remain questionable despite recent profitability. Operating margins under 2% leave no room for error. Express parcel yields are declining as e-commerce platforms demand lower rates. PTL faces trucking industry cyclicality. Any economic slowdown could push the company back into losses, questioning the sustainability of recent profits.

Technology disruption looms large. Autonomous vehicles could eliminate driver costs—Delhivery's largest expense. Drone delivery might bypass ground infrastructure entirely. Platform models like Uber Freight could disintermediate asset-heavy players. Delhivery's physical infrastructure could become stranded assets in a digitized logistics future.

Customer concentration creates vulnerability. Top 10 clients likely contribute 40%+ of revenue. Losing any major e-commerce platform would devastate utilization rates. These platforms have leverage to demand price reductions, keeping Delhivery's margins perpetually compressed.

The India macro story might disappoint. E-commerce growth is slowing from 30%+ to 15-20%. GST and regulatory complexity add costs. Infrastructure development remains slower than needed. If India's consumption story stumbles, Delhivery has limited international options unlike global logistics players.

Working capital requirements could strain growth. Logistics businesses typically offer credit while paying suppliers quickly, creating negative working capital cycles. As growth accelerates, cash needs multiply. Despite recent profitability, free cash flow generation remains modest relative to capital employed.

Valuation appears stretched relative to global peers. Trading at 3.7x book value while generating negative ROE seems optimistic. Global logistics leaders like FedEx trade at lower multiples despite higher margins and returns. The "India premium" might not be justified given execution risks.

The talent challenge could constraint scaling. Logistics requires operational excellence at thousands of touchpoints. Finding and training quality workforce across India's diverse geography is difficult. Technology can't fully substitute for human judgment in last-mile delivery. Labor costs will likely increase faster than automation can offset.

The Verdict: A Calculated Bet on India's Future

The truth likely lies between extremes. Delhivery isn't the next Amazon, but neither is it a value trap. It's a leveraged bet on India's consumption story with asymmetric risk-reward. If India's e-commerce doubles every five years, Delhivery shareholders win big. If growth moderates to GDP levels, the investment struggles to generate acceptable returns.

For growth investors comfortable with volatility, Delhivery offers exposure to India's digital transformation with improving fundamentals. For value investors seeking predictable cash flows, better opportunities exist elsewhere. The investment case ultimately depends on one's conviction in India's economic trajectory and patience to wait for infrastructure investments to mature.

XI. Epilogue & Future Outlook

Five years from now, success for Delhivery looks like sustainable 15%+ operating margins, ROE exceeding 20%, and free cash flow funding growth without dilution. The company would handle 500 million packages monthly, operate 100+ automated sortation centers, and generate ₹20,000+ crore annual revenue. International operations would contribute 20% of revenue. The stock would trade at ₹1,000+, validating patient shareholders.

But the path there requires navigating multiple transitions. From growth to profitability—already underway but fragile. From e-commerce specialist to integrated logistics provider—progressing but incomplete. From founder-led to institutionally-run—in process with uncertain outcome. From India-focused to regional player—barely started but essential for long-term growth.

Technology disruptions present both opportunity and threat. Delhivery's drone acquisition positions it for autonomous delivery, but execution remains uncertain. AI could optimize operations further, but also enable asset-light competitors. Blockchain might revolutionize supply chain transparency, requiring new capabilities. The company that built physical infrastructure must now build digital infrastructure too.

India's logistics market will undoubtedly transform over the next decade. The question is whether Delhivery leads, follows, or gets disrupted by that transformation. Its scale, infrastructure, and improving profitability suggest leadership potential. But logistics history is littered with former leaders who missed technology transitions.

The macro tailwinds remain compelling. India's young demographics, rising income levels, smartphone penetration, and digital payment adoption all support e-commerce growth. Government initiatives like Production Linked Incentive schemes boost manufacturing, requiring logistics support. Infrastructure development—roads, dedicated freight corridors, ports—improves logistics efficiency. These secular trends benefit any logistics player, but especially the market leader.

Yet structural challenges persist. India's logistics costs at 13% of GDP remain high versus 8-10% in developed markets. State-level regulatory complexity adds friction. Inadequate warehousing infrastructure constrains growth. Address standardization remains poor. These challenges create opportunity for problem-solvers but also perpetual headwinds for operators.

The competitive endgame likely involves consolidation. India doesn't need 50+ logistics companies struggling for profitability. Scale economics favor 3-5 large players dominating 70%+ market share, similar to other markets globally. Delhivery seems positioned as a consolidator, but execution risk remains high. Failed acquisitions could destroy value faster than organic growth creates it.

Environmental considerations will reshape operations. Pressure to reduce emissions will require electric vehicle adoption, adding capital requirements. Packaging waste regulations might mandate recyclable materials, increasing costs. Carbon taxes could affect pricing. Companies ahead on sustainability might gain competitive advantage. Delhivery's current environmental initiatives appear reactive rather than proactive.

The ultimate question facing Delhivery is identity: Is it a logistics company using technology, or a technology company doing logistics? The answer determines strategy, talent acquisition, capital allocation, and valuation multiples. Amazon chose the latter and built a trillion-dollar business. FedEx chose the former and built a hundred-billion-dollar business. Both are successful, but the paths diverge dramatically.

For Delhivery, the next five years will determine whether it becomes India's defining logistics infrastructure—essential, profitable, and valuable—or merely another logistics company in a commoditizing industry. The pieces are in place for the former, but execution will determine outcome. In logistics, as in life, the last mile is always the hardest.

The Delhivery story continues to unfold, written daily in millions of packages delivered across India's vast geography. From that late-night conversation in Gurgaon to potentially becoming India's logistics backbone, it's been an improbable journey. Whether the next chapter brings triumph or disappointment, the ambition to transform how 1.4 billion people receive goods deserves recognition. In the end, infrastructure businesses aren't built for quarterly earnings—they're built for generations. Time will tell if Delhivery built something lasting or merely burned capital chasing an impossible dream.

But perhaps that's the point. In emerging markets, building infrastructure requires equal parts vision and delusion, capital and courage, patience and urgency. Delhivery embodies these contradictions, making it either a brilliant investment or an expensive education in the limits of ambition. For India's sake, one hopes it's the former. For investors' sake, one watches the quarterly numbers, tracks the competition, and remembers that in logistics, there are no permanent winners—only companies that execute better today than yesterday, and tomorrow than today.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube