Cyient DLM: India's Design-Led Manufacturing Powerhouse

I. Introduction & Episode Roadmap

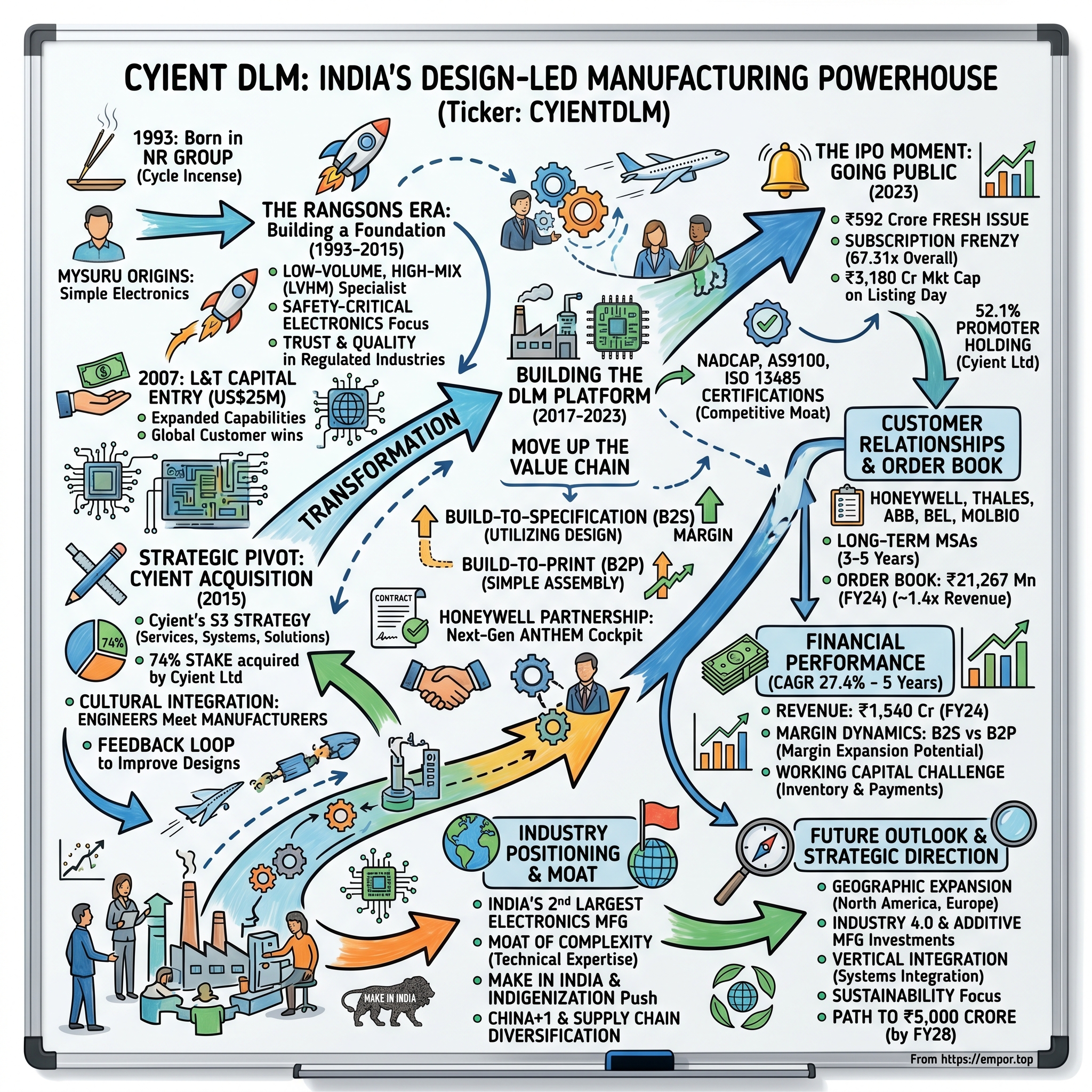

Picture the industrial landscape of Mysuru in 1993—a city known more for its silk and sandalwood than sophisticated electronics. Against this backdrop, a small electronics manufacturing company was taking shape within the NR Group, a South Indian business house whose fragrant Cycle brand incense sticks had already become a household name across India. This was the birth of Rangsons Electronics, the company that would evolve into today's Cyient DLM.

Fast forward three decades: Cyient DLM commands a market capitalization of ₹3,627 crore, generates revenue of ₹1,540 crore, and delivers profits of ₹64.9 crore. But the journey from a regional electronics assembler to India's second-largest electronics manufacturer wasn't just about growth—it was about transformation, strategic pivots, and the audacious vision of becoming a design-led manufacturing champion.

The question that drives our story today: How did a company born in the incense-scented corridors of the NR Group transform into a critical supplier of safety-critical electronics for Honeywell's next-generation cockpit avionics and other Fortune 500 aerospace giants?

This is a tale of patient capital, strategic acquisitions, and the convergence of Indian manufacturing ambition with global aerospace precision. It's about navigating the complex transition from simple contract manufacturing to sophisticated design-led solutions. And ultimately, it's about timing—entering the public markets at exactly the moment when India's manufacturing renaissance captured global imagination.

II. The Rangsons Era: Building from Scratch (1993–2015)

The monsoon of 1993 brought more than rain to Mysuru. Rangsons Electronics was incorporated on June 30, 1993, emerging as an unlikely diversification play for the NR Group, a leading business house in South India with interests in incense sticks, essential oils, perfumery and bio-chemicals. The juxtaposition was almost poetic—a company that had mastered the ancient art of fragrance manufacturing now venturing into the precision world of electronics.

But this wasn't mere diversification whimsy. The founders recognized something prescient: India's electronics manufacturing services (EMS) industry was at an inflection point. The company's relationship with Fortune 500 industrial clients dates back to 1996, when the EMS industry in India was at a nascent stage. While others saw India merely as a software services destination, Rangsons was quietly building capabilities in hardware—specifically, the kind of complex, low-volume, high-mix electronics that would later become its calling card.

The early years were about establishing credibility in an industry where trust is everything. When you're manufacturing safety-critical electronics—the kind that go into aircraft cockpits or medical devices—there's zero tolerance for error. A 99% success rate means failure. Rangsons understood this implicitly, investing heavily in quality certifications and process excellence long before Indian manufacturing became fashionable.

The Turning Point: L&T Capital's Entry

August 2007 marked a watershed moment. The company raised $25 million in a Series B funding round led by L&T Capital. This wasn't just capital—it was validation from one of India's most respected industrial conglomerates. The funds enabled Rangsons to dramatically expand its capabilities, building world-class production facilities that could meet the exacting standards of global aerospace and defense OEMs.

The timing was fortuitous. The global financial crisis of 2008-09 forced Western manufacturers to urgently seek cost-effective alternatives without compromising quality. Rangsons, with its newly expanded facilities and proven track record, was perfectly positioned. The company began winning contracts from marquee clients across defense and aerospace, medical, automotive, telecommunications, and industrial segments.

Building the Foundation

What distinguished Rangsons wasn't just its manufacturing capabilities—it was its strategic focus on complexity. While competitors chased high-volume consumer electronics contracts, Rangsons specialized in low-volume, high-mix (LVHM) products. This meant producing small batches of highly customized, technically sophisticated products where margins were determined by expertise, not scale.

By 2014, the company had built an enviable position. With revenues of $66 million (₹390 crore at 2014 exchange rates), Rangsons had become a trusted partner to global OEMs. More importantly, it had developed what would become its key differentiator: the ability to handle safety-critical electronics in highly regulated industries—a capability that created significant barriers to entry for competitors.

The two-decade journey from 1993 to 2015 was about patient building—capabilities, relationships, and reputation. But as 2014 drew to a close, Rangsons' trajectory was about to intersect with a much larger ambition.

III. The Cyient Acquisition: Strategic Transformation (2015–2017)

January 2, 2015, began like any other Friday in India's corporate corridors, but for Cyient Limited—the Hyderabad-based engineering services giant—it marked the beginning of a transformative bet on manufacturing. Cyient signed a definitive agreement to acquire 74% stake in Rangsons Electronics from NR Group for INR 2.9 billion in cash.

The deal valued Rangsons at approximately ₹390 crore, representing a significant premium to its book value. But Krishna Bodanapu, Cyient's CEO, wasn't buying assets—he was buying a gateway to realize the company's S3 strategy: Services, Systems, and Solutions. "With its strong domain expertise coupled with a comprehensive solution portfolio, industry-relevant processes, certifications, and global customers, Rangsons Electronics fits extremely well in Cyient's business. The new relationship will help Cyient expand its core business while deepening partnerships with OEM customers", Bodanapu explained.

Strategic Rationale: More Than Manufacturing

The acquisition wasn't just about adding manufacturing capabilities—it was about fundamentally repositioning Cyient in the value chain. For years, Cyient had been designing sophisticated systems for aerospace and industrial clients. Now, they could manufacture them too. This end-to-end capability—from design to delivery—was rare in India's fragmented engineering services landscape.

The acquisition helped Cyient position itself as a strong offset partner and strengthen its contribution to the 'Make in India' program, which Prime Minister Modi had launched just months earlier. The timing was impeccable. Global OEMs, particularly in aerospace and defense, were under increasing pressure to localize their supply chains in India. Cyient-Rangsons could now offer them a complete solution.

Cultural Integration: Engineers Meet Manufacturers

The integration challenge was real. Cyient's 12,000+ engineers, accustomed to CAD workstations and simulation software, had to mesh with Rangsons' manufacturing teams who lived by the rhythm of production lines and quality audits. The cultures couldn't have been more different—one focused on intellectual property and design elegance, the other on operational excellence and zero-defect manufacturing.

But there was unexpected synergy. Cyient's engineers could now see their designs come to life on Rangsons' shop floor, creating a feedback loop that improved both design and manufacturing. Rangsons' manufacturing teams gained access to Cyient's design expertise, enabling them to move up the value chain from Build-to-Print (B2P) to Build-to-Specification (B2S) services.

The Rebranding and Expansion

On January 18, 2017, Rangsons Electronics was renamed to Cyient DLM—Design-Led Manufacturing—a name that captured the company's evolved identity. This wasn't just a rebranding exercise; it was a declaration of intent. The "DLM" model would differentiate them from traditional contract manufacturers who competed primarily on cost.

February 2018 brought another strategic move: the merger with Techno Tools Precision Engineering Private Limited, adding precision machining capabilities that would prove crucial for aerospace applications. Each acquisition and integration was carefully orchestrated to build a comprehensive manufacturing platform that could handle everything from circuit board assembly to complex box builds.

The transformation from Rangsons to Cyient DLM represented more than a change in ownership—it was a reimagination of what Indian manufacturing could be. No longer content to be the world's low-cost assembly hub, Cyient DLM was positioning itself as a sophisticated partner capable of handling the most complex, safety-critical manufacturing challenges.

IV. Building the Design-Led Manufacturing Platform (2017–2023)

The concept of Design-Led Manufacturing (DLM) sounds deceptively simple, but executing it required a fundamental reimagination of the traditional EMS model. Where conventional manufacturers waited for clients to provide complete designs (Build-to-Print), Cyient DLM could take a rough specification and engineer the entire solution (Build-to-Specification). This capability gap was worth billions in addressable market.

The DLM Advantage

Consider the difference: A B2P provider receives detailed blueprints and manufactures to spec—essentially a sophisticated assembly operation. But B2S requires deep engineering expertise to translate customer requirements into manufacturable designs. B2P solutions involve clients providing the design while B2S involves utilizing Cyient's design capabilities to design products based on client specifications and then manufacturing them.

This distinction mattered enormously in safety-critical industries. When Honeywell needed a partner for its next-generation avionics, they weren't just looking for someone who could populate circuit boards—they needed a partner who understood the intricacies of aerospace systems, could optimize designs for manufacturability, and ensure compliance with stringent aviation standards.

Capacity Expansion and Capability Building

The period from 2017 to 2023 was marked by aggressive capacity expansion. 2020 saw the establishment of a new manufacturing facility in Hyderabad, strategically located in an SEZ to serve export markets. But the real story wasn't just square footage—it was about building specialized capabilities.

In 2022, Cyient partnered with Honeywell to manufacture Honeywell Anthem, the first cloud-connected cockpit system. This wasn't a typical manufacturing contract. Cyient provided turnkey manufacture and testing of multiple line replaceable units (LRUs) that comprise the Honeywell Anthem avionics suite, with supply chain management technologies and Industry 4.0 linked plants ensuring predictable delivery schedules and continuous quality improvement.

The Honeywell partnership exemplified the DLM model's power. Cyient DLM wasn't just manufacturing to Honeywell's specifications—they were collaborating on design validation, managing complex supply chains, and ensuring that every unit met the zero-defect standards required for aviation.

Geographic and Vertical Expansion

By 2024, Cyient DLM had inaugurated two more facilities, including a precision machining facility in Bengaluru. The precision machining facility in Bengaluru would cater to incremental demand from existing customers and enable new opportunities and partnerships. Each facility was specialized—Mysuru focused on complex electronics assembly, Bengaluru on precision machining, and Hyderabad on high-volume production for export markets.

The company's manufacturing footprint had expanded to 300,000 square feet across three locations, but more importantly, each facility represented a center of excellence for specific capabilities. This distributed specialization model allowed Cyient DLM to serve diverse industries—from aerospace companies requiring AS9100-certified production to medical device manufacturers needing ISO 13485 compliance.

Industry Recognition and Certifications

The period also saw Cyient DLM accumulate an impressive array of certifications and recognitions. They became the first Indian company to obtain NADCAP certification for circuit card assembly—a credential that opened doors to the most demanding aerospace customers. The company received the Supplier Excellence Award from Honeywell Aerospace, the 2024 National Export Excellence Award from ESC, was recognized as "Best Performer Electronic Hardware Exports" at the STPI IT Exports Award 2023, and IPC acknowledged Cyient DLM as a top Indian company significantly contributing to the electronics industry.

These weren't participation trophies—each recognition represented validation from customers and industry bodies that Cyient DLM had successfully made the leap from contract manufacturer to strategic partner. The company had built something rare: an Indian manufacturing platform capable of competing not on cost, but on capability.

V. The IPO Moment: Going Public (2023)

The boardroom at Cyient DLM's Hyderabad headquarters buzzed with anticipation in early 2023. The Indian capital markets were experiencing a renaissance—retail participation had exploded post-COVID, and the India manufacturing story was capturing global attention. After months of preparation, the company was ready for its public market debut.

The Preparation

The IPO preparation was methodical. The company filed for a fresh issue of 2,23,64,653 equity shares aggregating ₹592 crores, priced at ₹265 per share. The pricing was aggressive—at 3.85 times book value—but the company's growth trajectory and parent backing provided confidence.

On June 26, 2023, Cyient DLM raised ₹259.65 crore from anchor investors, including marquee names like ICICI Prudential, HDFC Mutual Fund, and Tata Infrastructure Fund. The anchor book was a who's who of India's smartest institutional money—a strong vote of confidence before the public offering opened.

The Subscription Frenzy

The IPO opened on June 27, 2023, and closed on June 30, 2023. What followed was extraordinary even by the standards of India's hot IPO market. The issue was subscribed 67.31 times overall—49.22 times in the retail category, 90.44 times in the QIB category, and 45.05 times in the NII category.

The subscription numbers told a story: institutional investors (QIBs) were the most aggressive, seeing in Cyient DLM a pure-play bet on India's manufacturing renaissance. Retail investors, energized by the Make in India narrative, weren't far behind. Even high-net-worth individuals (NIIs), typically more selective, showed strong interest.

The Listing Day Fireworks

July 10, 2023, arrived with the kind of anticipation usually reserved for cricket matches. As the opening bell rang at 9:15 AM, Cyient DLM's stock opened at a spectacular premium. The stock listed at ₹401 on BSE (51% premium) and ₹403 on NSE (52% premium), beating grey market expectations of ₹125 premium.

The company's market capitalization stood at ₹3,180 crore on listing day, instantly creating significant wealth for investors who had received allocations. The stellar listing wasn't just about market exuberance—it reflected genuine investor conviction in Cyient DLM's unique positioning at the intersection of engineering and manufacturing.

Post-IPO Structure

After the IPO, Cyient Limited remained the promoter with 52.1% holding, ensuring continuity of strategic direction while bringing in public market discipline. The funds raised would fuel the next phase of growth—capacity expansion, technology upgrades, and working capital to support larger contracts.

The IPO wasn't just a financial milestone—it was a coming-of-age moment for Indian manufacturing. Here was a company that had started in the shadow of an incense stick manufacturer, transformed through strategic acquisition, and emerged as a publicly-traded champion of sophisticated manufacturing. The market's enthusiastic response validated not just Cyient DLM's journey, but the broader India manufacturing story.

VI. Customer Relationships & Order Book

Trust in aerospace manufacturing isn't built in quarters—it's built over decades. When a pilot pushes the throttle forward at 35,000 feet, the electronics controlling the aircraft's systems cannot fail. This zero-tolerance reality shapes every customer relationship in Cyient DLM's portfolio.

The Anchor Relationships

The company's client list includes Honeywell International Inc., Thales Global Services S.A.S, ABB Inc, Bharat Electronics Limited, and Molbio Diagnostics Private Limited. But these aren't just names on a client roster—each represents years of trust-building, qualification processes, and collaborative problem-solving.

Take the Honeywell relationship. The trust developed over years led to the award of a mega multi-year next-gen aero cockpit cloud-connected avionics suite contract, which includes manufacture and testing of multiple LRUs. This wasn't won through competitive bidding alone—it was earned through years of flawless execution on smaller projects, gradually earning the right to handle mission-critical systems.

The ABB relationship tells a different story. Dating back to 1996, when the EMS industry in India was at a nascent stage, this partnership predates Cyient's acquisition by nearly two decades. Through multiple technology cycles and ownership changes, this relationship endured—a testament to the deep operational trust Cyient DLM had built.

The Order Book Dynamics

The company enters into 3-5 year master service agreements (MSA) with its customers, providing revenue visibility that's rare in manufacturing. As of March 31, 2024, the company had a strong order book of ₹21,267 million—approximately 1.4 times annual revenue, providing a robust growth runway.

But the order book tells only part of the story. Large deals in aerospace and defense constitute the major portion of the order book and pipeline, expected to contribute towards FY25 and FY26 growth. These aren't commodity manufacturing contracts—they're strategic partnerships where switching costs are prohibitively high for customers.

The LVHM Sweet Spot

The company develops low volume, high mix (LVHM) products with high emphasis on quality and customization according to customer requirements. This positioning is deliberate and powerful. While large EMS players chase high-volume contracts where margins are razor-thin, Cyient DLM occupies a niche where expertise commands premium pricing.

Consider what LVHM means in practice: producing 100 units of 50 different products rather than 5,000 units of one product. Each requires different components, assembly processes, and testing protocols. It's manufacturing gymnastics that most providers avoid—but where Cyient DLM thrives.

Recent Wins and Momentum

The 2024 fiscal year brought significant commercial momentum. The company added two new logos in aerospace and defense and won key large deals, expanding beyond existing relationships. In November 2024, Cyient DLM announced a 16-year program with Honeywell Aerospace Technologies to develop liquid cooling loops for micro vapor cycle systems—a next-generation aircraft cooling technology that's 35% lighter and 20% more efficient than comparable systems.

Each new contract builds on existing capabilities while pushing into adjacent technologies. The micro VCS deal, for instance, leverages Cyient DLM's electronics expertise while moving into thermal management—a critical technology for next-generation aircraft where heat dissipation becomes increasingly challenging.

The customer concentration risk is real—the top five customers likely account for over 60% of revenue. But in safety-critical manufacturing, concentration is almost inevitable. The qualification barriers are so high, the trust requirements so stringent, that both customers and suppliers tend toward deep, long-term partnerships rather than transactional relationships.

VII. Financial Performance & Growth Trajectory

The numbers tell a story of explosive growth meeting operational challenges. Over the past 5 years, Cyient DLM's revenue has grown at a CAGR of 27.4%—the kind of sustained rapid growth that's rare in manufacturing. But beneath the headline numbers lies a more nuanced narrative of margin pressure, working capital intensity, and the growing pains of scaling a complex business.

The Revenue Rocket

Fiscal 2024 was a watershed year. Operating income rose 43.2% year-on-year, while operating profit increased 23.1%. The revenue surge to ₹1,223 crore represented not just organic growth but the fruition of investments made over the previous five years in capacity and capability.

Revenue jumped from ₹4,649 million in FY20 to ₹12,233 million in FY24—a near tripling in four years. This wasn't the steady, predictable growth of mature manufacturers but the hockey-stick trajectory of a company hitting its stride.

Margin Dynamics: The Profitability Puzzle

Yet profitability tells a more complex story. Operating margins fell from 10.5% in FY23 to 9.0% in FY24, even as absolute profits grew. This margin compression reflected multiple factors: aggressive pricing to win strategic contracts, upfront investments in new facilities, and the working capital intensity of rapid growth.

However, net margins improved from 3.8% in FY23 to 5.1% in FY24, driven by operational leverage and better interest cost management. Net profit grew 92.9% year-on-year to ₹612 million in FY24—nearly doubling in a single year.

The Working Capital Challenge

Manufacturing is a working capital-intensive business, and Cyient DLM's rapid growth exacerbated this challenge. Cash flow from operations turned negative at ₹-705 million in FY24, compared to positive ₹540 million in FY23. This wasn't operational weakness but growth investment—inventory buildup for new contracts and extended payment terms for strategic customers.

The company addressed this through the IPO proceeds, using funds for working capital normalization. But the structural challenge remains: in a business with 90-120 day payment cycles and 60-90 day inventory requirements, growth consumes cash before it generates returns.

Capital Allocation and Investment

Capital expenditure surged to ₹4,277 million in FY24 from ₹1,418 million in FY23—a threefold increase reflecting aggressive capacity expansion. This included the new Bengaluru precision machining facility and technology upgrades across existing facilities.

The investment thesis is clear: build capacity ahead of demand in a market where customers make multi-year commitments. With visibility from the ₹21,267 million order book, management bet on preemptive expansion rather than reactive capacity addition.

The Dividend Dilemma

Despite reporting repeated profits, the company hasn't paid dividends—a point of frustration for some investors. But this reflects strategic prioritization: in a high-growth phase with significant capital requirements, retaining earnings for growth investments makes more sense than distributing cash to shareholders.

The financial trajectory suggests a company in transition—from startup-like growth rates to the steadier rhythms of a mature manufacturer. The challenge ahead is maintaining growth momentum while improving margins and cash generation. With the aerospace and defense sectors driving order book growth, and new customer additions providing diversification, the financial foundation appears solid even if the path to profitability optimization remains a work in progress.

VIII. Market Context & Industry Positioning

India's electronics manufacturing landscape in 2024 looks nothing like it did when Rangsons started in 1993. The industry has transformed from a peripheral player to a global force, and Cyient DLM sits at the epicenter of this revolution.

The EMS Explosion

The numbers are staggering: India's EMS industry is growing at a CAGR of over 32%, expected to contribute 7% ($80 billion) of the global EMS market by 2026. This isn't incremental growth—it's a tectonic shift in global manufacturing geography. The convergence of China+1 strategies, Make in India initiatives, and global supply chain diversification has created a perfect storm of opportunity.

Cyient DLM stands as the second-largest electronics manufacturer in India after Dixon Technologies. But the comparison is almost unfair—Dixon focuses on consumer electronics and high-volume production, while Cyient DLM operates in the rarefied air of safety-critical, low-volume, high-complexity manufacturing. They're both electronics manufacturers like both Ferrari and Toyota make cars.

The Moat of Complexity

High entry barriers exist due to technical expertise and capabilities in safety-critical electronics in highly regulated industries. These aren't barriers you can overcome with capital alone. When you're manufacturing avionics that must perform flawlessly at -55°C at 40,000 feet, or medical devices where failure means death, the qualification process takes years, not months.

Consider what it takes to become a supplier to Honeywell or Thales: AS9100 certification for aerospace, NADCAP accreditation for special processes, years of audit history, proven financial stability, and most importantly, a track record of zero-defect delivery. Cyient DLM has all of these—credentials that took decades to accumulate and would take competitors years to replicate.

Government Tailwinds: Policy as Catalyst

The Indian government's Production Linked Incentive (PLI) schemes have added rocket fuel to the sector's growth. While Cyient DLM doesn't directly benefit from consumer electronics PLI schemes, the overall ecosystem development—component suppliers, skilled workforce, infrastructure—creates positive spillovers.

More importantly, the defense indigenization push directly benefits Cyient DLM. With India targeting 70% indigenous content in defense procurement by 2027, global defense OEMs need local partners for offset obligations. Cyient DLM, with its proven capabilities and security clearances, is perfectly positioned to capture this opportunity.

Competitive Dynamics

The competitive landscape is fragmented but evolving. Global giants like Foxconn and Flex have massive scale but focus on high-volume consumer electronics. Indian players like Syrma SGS and Amber Enterprises are growing rapidly but lack Cyient DLM's design capabilities and aerospace certifications.

The real competition comes from specialized aerospace and defense electronics manufacturers—companies like Aequs or Dynamatic Technologies. But even here, Cyient DLM's integration with parent Cyient's engineering capabilities provides a unique advantage. They can offer end-to-end solutions from conceptual design to manufactured product—a capability few competitors can match.

The China Factor

The elephant in the room is China's dominance in global electronics manufacturing. But Cyient DLM operates in segments where China's cost advantages matter less and trust matters more. Western aerospace and defense companies are increasingly uncomfortable with Chinese manufacturing for sensitive components—creating opportunity for trusted partners in democratic nations.

The geopolitical tailwinds are strong. The Quad alliance, India-US defense cooperation, and Europe's strategic autonomy push all point toward increased sourcing from India. Cyient DLM, with its Western-standard processes and Indian cost base, sits at the sweet spot of this shift.

The market context suggests Cyient DLM is surfing multiple waves simultaneously—India's manufacturing rise, global supply chain diversification, and the aerospace/defense modernization cycle. The challenge isn't finding growth but managing it profitably while building the organizational capabilities to scale from a ₹1,500 crore company to potentially ₹5,000 crore over the next five years.

IX. Playbook: Business & Investing Lessons

The Patient M&A Masterclass

Cyient's acquisition of Rangsons offers a textbook case in strategic M&A. They didn't rush to integrate or impose their culture. Instead, they let Rangsons maintain its manufacturing DNA while gradually infusing design capabilities. The two-year gap between acquisition (2015) and rebranding (2017) wasn't delay—it was deliberate cultural integration.

The lesson: In capability-building acquisitions, preserve what works while adding what's missing. Cyient kept Rangsons' manufacturing excellence and customer relationships intact while adding design capabilities and global reach. Too many acquirers destroy value by forcing rapid integration.

The Value Migration Strategy

Cyient DLM's journey from B2P to B2S represents a classic value migration—moving from commoditized manufacturing to differentiated solutions. The financial impact is striking: B2S commands 20-30% higher margins than pure B2P work.

But the migration wasn't just about capabilities—it was about customer education. Cyient DLM had to convince customers accustomed to controlling design to trust them with specification-based development. This required patient relationship building and proving competence through progressively complex projects.

Trust as Currency

In safety-critical manufacturing, trust is literally priceless. A single quality failure can end a decades-long relationship and trigger massive liability. Cyient DLM understood this, accepting lower margins initially to build unimpeachable quality credentials.

The investment in certifications—AS9100, NADCAP, ISO 13485—wasn't compliance theater but competitive moat-building. Each certification requires not just meeting standards but maintaining them through regular audits. This continuous compliance creates switching costs that protect incumbent suppliers.

The Parent-Subsidiary Tightrope

Managing the post-IPO relationship between Cyient Limited (parent) and Cyient DLM (now publicly traded subsidiary) requires delicate balance. The parent provides strategic direction and technical support but must respect minority shareholders' interests.

The 52.1% ownership stake is optimal—enough for control but not so much that minority shareholders feel marginalized. The parent's engineering capabilities remain accessible to DLM through formal agreements, maintaining synergies while ensuring arm's-length pricing.

Capital Intensity Reality

Manufacturing is inherently capital-intensive, and sophisticated manufacturing even more so. Cyient DLM's capex-to-revenue ratio of ~35% in FY24 might alarm software-conditioned investors, but it's necessary for growth in this sector.

The lesson for investors: judge manufacturing companies differently than asset-light businesses. Focus on return on capital employed (ROCE) trend rather than absolute margins, and understand that growth investments precede revenue realization by 12-18 months.

The Concentration Paradox

Customer concentration—often seen as risk—can be a strength in specialized manufacturing. Deep relationships with few customers allow for collaborative innovation, efficient operations, and predictable revenue. The key is ensuring no single customer exceeds 30-40% of revenue and continuously adding new logos to dilute concentration over time.

Cyient DLM's approach—maintaining anchor relationships while gradually diversifying—balances stability with risk management. The 16-year Honeywell contract for micro VCS exemplifies this: long-term revenue visibility from a trusted partner while pursuing new customers in adjacent segments.

The playbook reveals that successful manufacturing businesses are built through patient capital allocation, strategic capability building, and relentless focus on trust and quality. Financial metrics matter, but in safety-critical manufacturing, operational excellence and customer relationships are the true value drivers.

X. Bear vs. Bull Case

Bull Case: Riding Multiple Tailwinds

The optimists see Cyient DLM as perfectly positioned at the intersection of multiple megatrends. Start with the order book—₹21,267 million provides visibility well into FY26, with aerospace and defense contracts typically extending even further. When Honeywell signs a 16-year contract, they're not experimenting—they're making a strategic commitment.

The Make in India story is just beginning. With India targeting $300 billion in electronics production by 2026, even capturing a small share of the high-value segment represents massive opportunity. More importantly, the shift isn't just about cost—it's about supply chain resilience. Post-COVID, single-source dependence on China for critical electronics is seen as strategic vulnerability.

Cyient's aerospace engineering experience spans over 20 years with over 3,000 aerospace engineers, having delivered over 42 million hours of engineering solutions. This parent company backing provides unmatched design capabilities that pure-play manufacturers cannot replicate. When customers need design optimization or value engineering, Cyient DLM can tap into this vast expertise pool.

The margin expansion story remains untold. As B2S revenues grow from current ~30% to potentially 50% of mix, margins should expand by 200-300 basis points. Additionally, operational leverage from capacity utilization improvements and automation investments could add another 150-200 basis points over three years.

Valuation at 3.85x book value might seem rich, but compared to global aerospace electronics manufacturers trading at 5-7x book, there's room for multiple expansion as the company scales and margins improve.

Bear Case: Structural Challenges Persist

The skeptics point to persistent red flags. Despite repeated profits, the company hasn't paid dividends—suggesting either cash flow challenges or aggressive capital requirements that could continue indefinitely.

Customer concentration remains alarming. While long-term contracts provide stability, losing even one major customer could devastate revenues. The aerospace industry's cyclicality adds another layer of risk—a downturn in aircraft orders would immediately impact Cyient DLM's order book.

Negative operating cash flow of ₹705 million in FY24 raises sustainability questions. If the company needs continuous capital infusion to grow, returns to shareholders could remain elusive. The working capital intensity appears structural, not temporary.

Competition is intensifying. Global EMS giants are establishing Indian operations, armed with superior technology and deeper pockets. Local players are moving upmarket, acquiring certifications and capabilities. Cyient DLM's niche could become crowded, pressuring margins.

The parent relationship, while providing capabilities, also creates conflicts. Transfer pricing, resource allocation, and strategic priorities must balance parent and minority shareholder interests—a perpetual source of potential friction.

The Verdict Balance

The truth, as always, lies between extremes. Cyient DLM is neither a guaranteed multibagger nor a value trap. It's a complex manufacturing business navigating the transition from high growth to sustainable profitability.

The bull case rests on execution—converting the order book to revenue, improving margins through mix shift, and generating positive free cash flow. These are achievable but require flawless execution in an increasingly competitive market.

The bear case highlights structural challenges that won't disappear—customer concentration, capital intensity, and competitive threats are permanent features of this business. Success requires continuously earning the right to win, not resting on past achievements.

For investors, the key question isn't whether Cyient DLM will grow—the order book ensures that—but whether it can grow profitably while generating adequate returns on invested capital. The next 24 months will likely provide the answer.

XI. Future Outlook & Strategic Direction

Anthony Montalbano, CEO of Cyient DLM, faces a strategic crossroads as 2025 unfolds. The company has successfully transitioned from acquisition to integration to public listing. Now comes the harder challenge: building a sustainable, profitable growth engine while managing stakeholder expectations across customers, employees, and investors.

Geographic Expansion Ambitions

The company is planning to focus on expanding its geographic footprint worldwide through inorganic expansion. But this isn't about planting flags—it's about following customers. As aerospace OEMs establish global supply chains, they need partners who can support them across geographies. A presence in North America or Europe would position Cyient DLM as a truly global partner, not just an Indian offshore provider.

The inorganic route makes sense. Acquiring a small European aerospace electronics manufacturer would provide instant customer relationships, certifications, and local presence. The Cyient group's experience with multiple international acquisitions provides the playbook.

Technology Investments: Industry 4.0 and Beyond

The future of manufacturing isn't just about machines—it's about intelligence. Cyient DLM's investments in Industry 4.0 technologies—IoT sensors, predictive maintenance, digital twins—aren't tech buzzwords but operational imperatives. When you're producing safety-critical components, predictive quality control isn't nice-to-have; it's essential.

The company is also exploring additive manufacturing (3D printing) for aerospace applications. While still nascent, additive manufacturing could revolutionize low-volume, complex parts production—exactly Cyient DLM's sweet spot. Being early in this technology curve could provide significant competitive advantage.

Vertical Integration Considerations

The strategic question is how far up the value chain to move. Should Cyient DLM remain focused on electronics manufacturing or expand into complete systems integration? The recent precision machining facility suggests appetite for vertical integration.

Complete aerostructures assembly or medical device manufacturing could be logical extensions. But each step up the value chain requires exponentially more capital and capability. The balance between ambition and execution risk will determine success.

The Sustainability Imperative

Through the year, Cyient DLM improved its focus on environmental sustainability through green interventions and conservation projects. This isn't corporate virtue signaling—aerospace customers increasingly demand carbon-neutral supply chains. Companies that can demonstrate sustainable manufacturing practices will win preferential treatment in contract awards.

The company's new facilities incorporate renewable energy, water recycling, and waste reduction systems. These investments might pressure near-term margins but position Cyient DLM favorably for long-term contracts with sustainability-conscious customers.

The Path to ₹5,000 Crore

The company's outlook for FY25 continues to remain strong, anticipating growth backed by order book and strong relationships with essential clients. With current revenue at ₹1,540 crore and a robust order book, reaching ₹5,000 crore by FY28 isn't fantasy—it requires 35% CAGR, in line with historical growth rates.

But scale brings complexity. Managing 3x current revenue requires different organizational capabilities—ERP systems, middle management depth, quality systems, and working capital management all need upgrading. The company that got to ₹1,500 crore won't be the same one that reaches ₹5,000 crore.

The strategic direction is clear: leverage the design-led manufacturing model to capture higher-value contracts, expand geographically to serve global customers, and continuously invest in technology to maintain competitive advantage. The challenge is execution—maintaining quality and customer trust while scaling rapidly.

Success will require balancing multiple stakeholders' interests, managing capital allocation wisely, and most importantly, maintaining the operational excellence that earned customers' trust over three decades. The foundation is solid; the opportunity is massive; execution will determine whether Cyient DLM becomes India's aerospace manufacturing champion or remains a promising but subscale player.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube