PG Electroplast: India's Hidden Manufacturing Champion

I. Introduction & Cold Open

Picture this: It's a sweltering May afternoon in Delhi, the mercury touching 47°C. Inside millions of homes across North India, air conditioners hum quietly, providing relief from the brutal heat. The brand on the AC might read Voltas, Blue Star, or Daikin—household names everyone recognizes. But here's what most people don't know: there's a 70% chance that the actual machine keeping them cool was manufactured by a company they've never heard of—PG Electroplast.

With a market capitalization of ₹14,614 crores, PGEL operates in the shadows of India's consumer durables industry, yet it's arguably more critical to the ecosystem than many of the brands whose logos adorn the products. This is the story of how a DRDO scientist named Promod Gupta built one of India's largest electronics manufacturing services (EMS) players—a company that went from making plastic components to becoming the backbone of India's white goods revolution.

The numbers tell a staggering story of transformation. From ₹639 crores in revenue in FY20 to ₹4,905 crores in FY25—a growth trajectory that would make even software companies envious. But unlike the celebrated unicorns of Bangalore, PGEL's story unfolded in the unglamorous industrial estates of Greater Noida, Bhiwadi, and Roorkee, where the real business of building India's manufacturing muscle happens.

What makes PGEL fascinating isn't just its growth—it's the strategic chess game it played to get here. How do you build a multi-thousand crore business by making products for companies that could easily be your competitors? How do you convince global giants like Whirlpool and Daikin to trust you with their manufacturing while simultaneously building capabilities that could theoretically threaten them? And perhaps most intriguingly, how did a company that started by making plastic buckets and chairs end up manufacturing sophisticated room air conditioners and washing machines?

This is a story about patience, about building capabilities brick by brick over decades, about the unglamorous work of operational excellence, and about timing the India manufacturing story perfectly. It's about understanding that in manufacturing, unlike software, there are no shortcuts—only the slow, methodical accumulation of expertise, trust, and scale.

As we unpack PGEL's journey from plastic molds to becoming India's second-largest room air conditioner manufacturer for OEMs, we'll discover lessons about B2B excellence, the art of being indispensable without being threatening, and why sometimes the most boring businesses make the best investments. This isn't just PGEL's story—it's a masterclass in how India's manufacturing champions are quietly being built, one component at a time.

II. Origins: The DRDO Scientist's Vision (1977-2003)

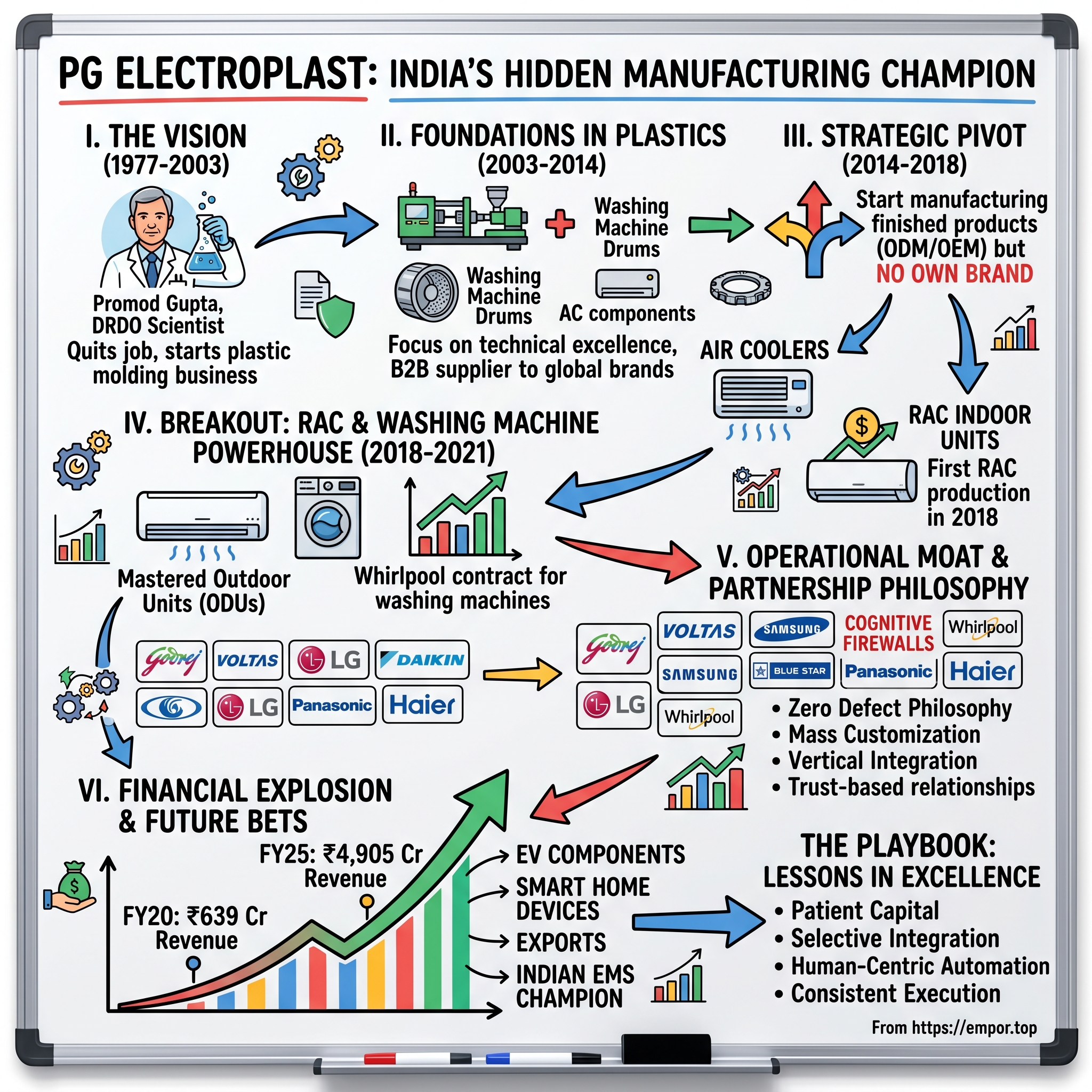

The year was 1977. India was emerging from the darkness of the Emergency, Indira Gandhi had just been voted out of power, and the country was taking its first tentative steps toward economic liberalization—though nobody knew it yet. In this environment of political upheaval and economic stagnation, a scientist at the Defence Research and Development Organisation made a decision that would seem almost quixotic: leave the security of a government job to start a plastics manufacturing business.

Promod Gupta wasn't your typical entrepreneur. Trained as a scientist, he had spent years at DRDO working on defense projects, understanding materials, precision manufacturing, and the importance of process discipline. But he saw something that others didn't—India's manufacturing deficit wasn't just about big-ticket items like cars or electronics. It started with the basics: the plastic components that went into everything from household items to industrial equipment.

The PG Group's founding in 1977 was, in many ways, an act of rebellion against the prevailing wisdom of the License Raj era. Starting a manufacturing business meant navigating a byzantine maze of permits, licenses, and quotas. Getting raw materials required connections; scaling production required government approval; even hiring beyond a certain number of employees needed clearance. Yet Gupta persisted, driven by a belief that India needed to build fundamental manufacturing capabilities from the ground up.

What distinguished Gupta from other entrepreneurs of his era was his scientific approach to business. While others chased quick profits in trading or sought licenses for import substitution, he focused on building genuine technical capabilities. The early PG Group wasn't trying to make finished products that consumers would recognize. Instead, it focused on becoming a reliable supplier of plastic components to other manufacturers—a B2B play in an era when B2C was considered the only path to scale.

The pre-liberalization years were brutal for manufacturers. Interest rates routinely exceeded 15%, getting foreign technology required government approval that could take years, and the domestic market was protected but also stunted. Gupta's strategy during these years was survival through technical excellence. The PG Group became known not for scale—which was impossible under the License Raj—but for quality and reliability.

By the late 1990s, as India's economy began opening up post-1991 reforms, Gupta saw the next opportunity. The flood of foreign brands entering India needed local manufacturing partners. They needed someone who understood Indian conditions—the dust, the heat, the power fluctuations—but could also meet international quality standards. The PG Group had spent two decades building exactly these capabilities.

The decision to formally establish PG Electroplast in 2003 wasn't random. By then, Gupta's son Vishal had joined the business, bringing fresh perspectives and ambition. The Indian consumer durables market was at an inflection point—penetration rates were still in single digits for most appliances, but rising incomes and easier financing were about to change that. The Guptas made a strategic bet: instead of just supplying plastic components, they would integrate forward into more complex manufacturing.

Building credibility in India's trust-deficit market required more than just technical capabilities. The Guptas understood that in a market where payment delays were common and contract enforcement was weak, relationships mattered as much as capabilities. They cultivated a reputation for never missing a delivery deadline, for absorbing cost fluctuations without immediately passing them on, and for treating client information with absolute confidentiality—crucial when you're manufacturing for competing brands.

The strategic decision to remain focused on B2B rather than launching consumer brands was perhaps the most crucial early choice. Many component manufacturers of that era harbored ambitions of launching their own brands—after all, if you're making the product, why not capture the brand premium? But Gupta understood something profound: in manufacturing, you can either be a competitor or a partner, rarely both successfully. By explicitly choosing to be a partner, PGEL could work with everyone without threatening anyone.

This philosophy would become PGEL's core DNA—the art of being indispensable without being threatening. It's what would later allow them to manufacture for Voltas and Blue Star simultaneously, to be Whirlpool's partner while Whirlpool competed fiercely with other PGEL clients. The foundation was laid not in 2003, but in those difficult years of the 1980s and 1990s when Promod Gupta chose the harder path of building real capabilities rather than chasing quick profits.

III. The Plastic Foundation Years (2003-2014)

The workshop floor at PGEL's Greater Noida facility in 2003 was a symphony of industrial precision—injection molding machines hissing as they pressed molten plastic into steel molds, the rhythmic thud of hydraulic presses, the careful inspection of each component under harsh white lights. This wasn't glamorous work. While India's IT services companies were making headlines with multibillion-dollar deals, PGEL was perfecting the art of making plastic components that would never bear its name.

Starting with plastic molded components in 2003 might seem like a step backward for a company with ambitions of becoming a major EMS player. But the Guptas understood something that many missed: plastics were the foundation of the entire consumer durables industry. Every washing machine needed dozens of plastic components. Every air conditioner required precision-molded parts. Every refrigerator incorporated complex plastic assemblies. Master this, and you had the keys to the kingdom.

The early years were about accumulation—of capabilities, clients, and credibility. PGEL invested heavily in injection molding technology, bringing in machines from Taiwan and Japan at a time when many Indian manufacturers were still using second-hand European equipment. They hired polymer engineers and invested in in-house mold design capabilities, allowing them to move from simple components to complex assemblies.

The client acquisition strategy was methodical. Rather than chasing every opportunity, PGEL focused on becoming indispensable to a select set of clients. When Godrej needed a supplier for washing machine components, PGEL didn't just quote the lowest price—they embedded engineers at Godrej's facility to understand exact requirements. When Blue Star wanted someone to manufacture AC components, PGEL invested in cleanroom facilities even though the volumes didn't initially justify it.

By 2008, plastics weren't just a business segment—they were PGEL's identity. The segment contributed 68% of revenues even as late as FY20, generating the cash flows that would fund future expansions. But what made PGEL different from dozens of other plastic component manufacturers wasn't scale—it was the systematic approach to moving up the value chain.

Consider the evolution of their capabilities: In 2003, they made simple plastic buckets and containers. By 2005, they were manufacturing precision components for washing machine drums. By 2008, they had mastered two-shot molding for refrigerator components. By 2010, they were producing complete plastic assemblies for room air conditioners. Each step required new investments, new capabilities, and most importantly, deeper trust from clients.

The numbers from this period don't tell the full story—revenues grew steadily but not spectacularly, from about ₹50 crores in 2003 to ₹300 crores by 2014. But beneath these modest numbers, PGEL was building something more valuable than revenue—a reputation as India's most reliable component supplier. They never missed a delivery deadline. They absorbed raw material price fluctuations without immediately demanding price revisions. They maintained absolute confidentiality when working with competing brands.

The operational discipline developed during these years would become PGEL's moat. While competitors focused on getting more clients, PGEL focused on getting deeper with existing ones. They would station quality engineers at client facilities. They would maintain buffer inventory even when working capital was tight. They would invest in testing equipment that matched what their clients used, ensuring perfect compatibility.

The 2008 financial crisis provided an unexpected opportunity. As global supply chains fractured and Chinese suppliers became unreliable, Indian brands started looking for domestic alternatives. PGEL was ready. They had the capacity, the capabilities, and most importantly, the track record. Orders that might have taken years to win in normal times came through in months.

But the real validation came from an unexpected source. In 2012, LG Electronics—the Korean giant known for its exacting standards—approved PGEL as a component supplier. The approval process took 18 months, involving multiple audits, quality certifications, and capability demonstrations. For a company that started making plastic buckets, becoming LG's supplier was like receiving an industrial knighthood.

The decision to remain focused on plastics while others diversified might have seemed conservative. Dixon Technologies was already moving into electronics. Amber Enterprises was expanding into finished goods. But PGEL understood that in manufacturing, depth beats breadth. Every year they remained focused on plastics, they got better at it. Their rejection rates dropped from 2% to 0.2%. Their mold changeover times decreased from hours to minutes. Their ability to handle complex multi-material assemblies became unmatched.

By 2014, PGEL had built what the Guptas called a "platform"—not in the tech sense, but in the manufacturing sense. They had relationships with every major consumer durables brand. They had facilities capable of handling any plastic manufacturing challenge. They had the working capital to manage large orders. Most importantly, they had the trust that would allow them to make their next big move. The plastic foundation years weren't just about making components—they were about earning the right to do something bigger.

IV. The Strategic Pivot: From Components to Products (2014-2018)

The boardroom at PGEL's Noida headquarters in early 2014 witnessed one of the most consequential debates in the company's history. On one side sat Promod Gupta, now in his seventies, advocating for continued focus on components—the strategy that had worked for nearly four decades. On the other stood his son Vishal, armed with market data and a vision for transformation. The question on the table: Should PGEL start manufacturing finished products?

The younger Gupta's argument was compelling. India's air cooler market was growing at 15% annually, driven by rising temperatures and increasing electrification in tier-2 and tier-3 cities. More intriguingly, while room air conditioners grabbed headlines, air coolers—a distinctly Indian solution to heat—were selling 10 times more units. And unlike ACs, which required sophisticated technology and massive capital investment, coolers were essentially plastic shells with a fan and a water pump—capabilities PGEL already possessed.

But moving from components to finished products wasn't just an operational decision—it was an existential one. For over a decade, PGEL had built trust by explicitly not competing with its clients. Now, they were proposing to manufacture products that would sit on the same retail shelves as those of their component customers. It was like a trusted butler suddenly announcing he wanted to join the family business.

The solution was elegant in its simplicity: PGEL would manufacture finished products, but only for other brands. No PGEL-branded cooler would ever hit the market. They would be an Original Design Manufacturer (ODM) and Original Equipment Manufacturer (OEM), never a brand. This distinction—subtle to outsiders but crucial to industry insiders—would allow them to maintain client trust while moving up the value chain.

The air cooler project became PGEL's Manhattan Project. A dedicated team was assembled, working in a segregated facility to maintain confidentiality. They didn't just copy existing designs—they reimagined the air cooler from first principles. Using their deep knowledge of plastics, they reduced the number of components by 30%. They designed modular assemblies that could be customized for different brands without retooling. They integrated IoT capabilities before "smart appliances" became a buzzword.

The first client was a calculated choice—Symphony, India's largest air cooler brand, but one that outsourced most of its manufacturing. The pitch was simple: PGEL could manufacture coolers 15% cheaper than Symphony's existing suppliers while maintaining quality standards. But the real selling point was speed—PGEL promised to go from design approval to mass production in just 90 days, half the industry standard.

By mid-2015, PGEL was manufacturing 50,000 coolers monthly. But Vishal Gupta had bigger ambitions. The cooler project was never about coolers—it was a Trojan horse to enter the room air conditioner market, where the real value lay. Every cooler manufactured taught PGEL about thermal dynamics, motor integration, and assembly line management. Every client relationship deepened trust for the bigger ask that was coming.

The RAC (Room Air Conditioner) opportunity materialized faster than expected. In 2017, the Indian government announced new energy efficiency norms that would require significant retooling by AC manufacturers. Suddenly, brands needed additional manufacturing capacity, and they needed it fast. PGEL was ready with a proposal that seemed almost too good to be true: they would set up RAC indoor unit manufacturing with their own capital, taking the investment risk off the brands' balance sheets.

The complexity of manufacturing AC indoor units cannot be overstated. Unlike coolers, which were essentially mechanical devices, AC indoor units involved sophisticated electronics, precise refrigerant handling, and aesthetic requirements that varied by brand. PGEL had to master plastic molding, metal fabrication, electronic assembly, and quality testing—all while maintaining the confidentiality walls between competing brands manufacturing in the same facility.

The investment required was staggering—over ₹200 crores for the initial setup, at a time when PGEL's entire annual revenue was under ₹500 crores. The Guptas mortgaged personal properties, negotiated complex financing arrangements, and convinced skeptical board members that this was the moment to bet big. The facility that came up in Greater Noida in 2018 wasn't just a factory—it was a statement of intent.

The first RAC indoor unit rolled off PGEL's assembly line in March 2018, destined for installation as a Voltas-branded AC in a Mumbai apartment. The symbolism wasn't lost on anyone—a company that started making plastic buckets was now manufacturing one of the most sophisticated consumer durables in the Indian market. But more importantly, PGEL had successfully executed one of the most difficult pivots in manufacturing: moving from components to products without losing a single major client.

The numbers validated the strategy. Revenue from the consumer durables segment, which was negligible in 2014, reached ₹150 crores by 2018. More importantly, margins expanded—while plastic components yielded 8-10% EBITDA margins, finished products delivered 12-15%. But the real value was strategic: PGEL was no longer just a vendor; it was a partner capable of handling any manufacturing challenge its clients could throw at it.

V. The Breakout: Becoming India's AC & Washing Machine Powerhouse (2018-2021)

The summer of 2018 was the hottest on record in North India. As temperatures soared past 45°C, AC sales exploded, growing 50% year-over-year. But behind this surge lay a crisis—Indian AC brands were struggling to meet demand. Their Chinese suppliers, facing environmental crackdowns and rising labor costs, were becoming increasingly unreliable. PGEL's timing couldn't have been better.

Having mastered indoor unit manufacturing, the logical next step was outdoor units (ODUs)—the complex, compressor-containing heart of any air conditioning system. This wasn't just another capability addition; it was PGEL's moon landing. ODUs required metallurgical expertise, refrigerant handling capabilities, and sophisticated testing facilities. One faulty weld could lead to refrigerant leaks, warranty claims, and destroyed reputations.

The Guptas made another bold decision: instead of incremental capacity additions, they would build at global scale from day one. The ODU facility that came up in Roorkee in 2021 had an initial capacity of 300,000 units annually, expandable to 1 million. They brought in consultants from Japan, hired engineers from established AC manufacturers, and invested in testing equipment that exceeded even what some brands had in their own facilities.

But the real breakthrough came from an unexpected source—washing machines. In 2019, Whirlpool approached PGEL with an unusual request. They needed someone to manufacture semi-automatic washing machines—not the fully automatic variants that grabbed headlines, but the workhorses that powered Middle India's laundry needs. The catch? Whirlpool wanted to completely outsource manufacturing while retaining design and brand control.

The washing machine project revealed PGEL's evolved capabilities. Within six months, they had set up a dedicated line capable of producing 30,000 units monthly. They developed vendor ecosystems for motors, pumps, and control panels. They created quality systems that reduced defect rates to below 0.1%. Most impressively, they did this while simultaneously scaling up AC manufacturing—a testament to the operational discipline built over decades.

Then came COVID-19.

March 2020 should have been a disaster. Factories shut down, supply chains collapsed, and demand evaporated as India went into lockdown. PGEL's revenues dropped 40% in Q1 FY21. The Guptas faced pressure to cut capacity, reduce workforce, and hunker down. Instead, they did the opposite.

Viewing the pandemic as a "once-in-a-generation opportunity to gain share," PGEL accelerated every expansion plan. While competitors conserved cash, PGEL invested ₹300 crores in new capacity. While others laid off workers, PGEL retained its entire 5,000-person workforce and used the downtime for training. While brands struggled with Chinese supply chain disruptions, PGEL positioned itself as the reliable, local alternative.

The strategy paid off spectacularly when demand roared back in late 2020. Work-from-home drove unprecedented demand for air conditioning. Government stimulus put money in consumers' pockets. The China+1 strategy became corporate gospel. Suddenly, every brand wanted local manufacturing capacity, and PGEL had it in abundance.

The numbers from this period are staggering. RAC sales grew 4x in just three years. By 2021, PGEL had become India's second-largest player in RAC finished goods sales to OEMs, with a monthly capacity of 475,000 units. The company was manufacturing for virtually every major brand—Indian stalwarts like Voltas and Blue Star, global giants like Daikin and Panasonic, and e-commerce players like Croma and Amazon Basics.

The operational complexity of managing this scale while maintaining quality and confidentiality was mind-boggling. PGEL's Greater Noida facility had separate assembly lines for different brands, with physical barriers and different worker teams to prevent information leakage. They maintained separate inventory systems, different quality protocols, and even different cafeterias for workers from competing brand lines.

But what truly set PGEL apart during this period was speed. When Blue Star needed to launch a new energy-efficient AC model to meet revised government standards, PGEL delivered prototypes in 15 days and achieved mass production in 45 days. When Godrej wanted to enter the premium AC segment, PGEL developed a completely new aesthetic design language while maintaining cost targets. When Amazon wanted to launch private label ACs, PGEL handled everything from design to delivery.

The washing machine business, initially seen as a diversification, became a strategic masterpiece. By 2021, PGEL was manufacturing over 500,000 units annually across semi-automatic and fully automatic categories. The December 2024 announcement of a definitive agreement with Whirlpool for contract manufacturing validated the strategy—Whirlpool, one of the world's largest appliance manufacturers, was entrusting PGEL with its entire semi-automatic washing machine production.

The transformation was complete. A company that generated ₹639 crores in revenue in FY20 reached ₹2,747 crores in FY24. But more than the numbers, PGEL had achieved something remarkable: it had become indispensable to India's consumer durables ecosystem. Every major brand relied on PGEL for some part of their manufacturing. The company that nobody had heard of had become the company that nobody could do without.

VI. The Client Portfolio & Partnership Philosophy

Inside PGEL's Greater Noida facility, there's a wall that tells the entire story—logos of 50+ brands, from Indian champions like Godrej and Voltas to global giants like LG, Daikin, and Whirlpool. But what's remarkable isn't the number of logos; it's that many of these brands compete fiercely with each other in the market, yet trust PGEL with their most critical manufacturing secrets.

The art of managing competing clients starts with physical infrastructure. PGEL's facilities are designed like a collection of mini-factories within a factory. The Voltas section is separated from the Blue Star area by more than just walls—different entry points, separate inventory systems, distinct worker uniforms, even different shift timings. A Blue Star engineer visiting the facility would never accidentally see Voltas's new model being assembled.

But infrastructure is just the beginning. The real magic lies in what PGEL calls "cognitive firewalls"—human systems that prevent information leakage. Teams working on Daikin products sign additional NDAs that specifically prohibit them from working on Panasonic products for two years. Senior managers who have access to multiple brands' information undergo regular training on confidentiality and face personal liability for breaches.

Take the Whirlpool relationship as a masterclass in partnership evolution. It started in 2015 with PGEL supplying plastic components for washing machines—a transactional relationship worth ₹20 crores annually. By 2018, PGEL was assembling complete washing machine sub-systems. By 2021, they were manufacturing entire units. The December 2024 agreement for complete semi-automatic washing machine manufacturing wasn't just a contract—it was the culmination of a decade-long trust-building exercise.

What made Whirlpool comfortable handing over manufacturing to a company that also worked with Whirlpool's competitors? The answer lay in PGEL's track record of never launching its own brand despite having complete manufacturing capabilities. This self-imposed limitation—which many saw as leaving money on the table—became PGEL's greatest strategic asset.

The Godrej relationship showcased another dimension of PGEL's partnership philosophy. When Godrej wanted to enter the premium AC segment in 2019, they faced a challenge: their existing manufacturing partners were already committed to other brands in that segment. PGEL not only created separate capacity but also helped Godrej design products specifically for Indian conditions—ACs that could handle voltage fluctuations, had enhanced dust filters, and included features like mosquito-repellent technology that global brands overlooked.

With Blue Star, PGEL pioneered the "zero-inventory" model. Blue Star's products would be manufactured only after orders were received, eliminating Blue Star's inventory risk while giving PGEL better capacity utilization. This required PGEL to maintain component inventory worth crores, betting on Blue Star's sales forecasts. When Blue Star's sales exceeded expectations in 2021, PGEL's ability to rapidly scale production cemented a partnership that now accounts for over ₹200 crores in annual business.

The relationship with Asian brands like Daikin and Panasonic brought different challenges. These companies had exacting quality standards—defect rates measured in parts per million, not percentages. PGEL invested in Six Sigma training, brought in Japanese consultants, and implemented Total Quality Management systems. When Daikin's head of manufacturing visited PGEL's facility in 2020, he remarked that some processes were better than Daikin's own facilities in Thailand.

E-commerce players like Amazon and Croma represented a new breed of clients—brands without manufacturing DNA who needed end-to-end solutions. PGEL became their virtual manufacturing arm, handling everything from product design to after-sales service coordination. When Amazon wanted to launch ACs under its "AmazonBasics" brand, PGEL managed the entire project—from understanding Amazon's target customer through data analytics to ensuring the packaging could withstand Amazon's automated warehouses.

The numbers tell the partnership story eloquently. Client concentration, often seen as a risk, became a strength—no single client accounts for more than 15% of revenue, yet the top 10 clients contribute 70%. This isn't concentration risk; it's partnership depth. The average client relationship spans over 8 years, with several dating back to PGEL's component-only days.

But perhaps the most telling validation came from an unexpected source. In 2023, when Dixon Technologies—PGEL's primary competitor—faced capacity constraints, several brands approached PGEL to take over Dixon's orders. PGEL's response was characteristic: they would take the orders but wouldn't use the situation to poach Dixon's clients permanently. This restraint, seen as naive by some, reinforced PGEL's reputation as a trustworthy partner, leading to even more brands approaching them.

The ODM versus OEM balance became PGEL's strategic sweet spot. For mature brands like Whirlpool and LG, PGEL operated as an OEM—manufacturing to exact specifications. For emerging brands and e-commerce players, they offered ODM services—designing products based on market requirements. This dual capability meant PGEL could serve anyone from a startup launching its first AC to a multinational expanding capacity.

The partnership philosophy extended beyond manufacturing. When raw material prices spiked in 2021, PGEL absorbed the increase for three months, giving brands time to adjust their pricing. When semiconductor shortages hit in 2022, PGEL used its relationships to secure chips for all its clients, not just the largest ones. These gestures, seemingly against immediate financial interest, built a reservoir of goodwill that translated into sticky, long-term relationships worth thousands of crores.

VII. Financial Transformation & The Growth Explosion (2020-2024)

The numbers are so staggering they bear repeating: revenues growing from ₹639 crores in FY20 to ₹4,905 crores in FY25—a 7.7x increase in just five years. In the staid world of manufacturing, where 15% annual growth is considered excellent, PGEL achieved a 44% CAGR. But the real story isn't just the growth; it's how they achieved it while expanding margins, improving returns, and maintaining financial discipline.

The transformation started with a fundamental insight: in consumer durables manufacturing, scale isn't just about spreading fixed costs—it's about negotiating power, working capital efficiency, and the ability to invest in automation. As PGEL crossed ₹1,000 crores in revenue, suddenly everything changed. Suppliers who previously demanded advance payments started offering 60-day credit. Banks that quoted 12% interest rates dropped to 8%. Customers who negotiated every rupee started accepting annual price contracts.

The Q4 FY24 numbers revealed the operating leverage at work. Revenue grew 78% year-over-year, but profits doubled. The EBITDA margin expanded from 8% to 12%, defying the conventional wisdom that says rapid growth comes at the cost of profitability. The secret lay in PGEL's evolving product mix—while plastic components still formed the base, higher-margin finished products now contributed 60% of revenues.

Working capital management became PGEL's hidden weapon. In an industry notorious for cash conversion cycles exceeding 120 days, PGEL brought theirs down to 75 days by 2024. They achieved this through a combination of supplier financing programs, just-in-time inventory management, and most crucially, the trust to negotiate favorable payment terms with both suppliers and customers.

The unit economics transformation tells the strategic story. In FY20, PGEL generated ₹12.8 lakhs of revenue per employee. By FY24, this had increased to ₹54.9 lakhs—a 4x improvement. But employee costs as a percentage of revenue actually decreased from 8% to 5%, indicating massive productivity gains through automation and process improvement. Every assembly line installed in the 2020-2024 period had 40% fewer workers than lines installed just five years earlier.

Capital allocation during this period revealed the management's evolved thinking. Instead of the traditional manufacturing approach of building capacity and hoping for utilization, PGEL pioneered "confirmed capacity expansion"—they would only invest in new lines after securing letters of intent from customers. This reduced capital risk while ensuring day-one utilization. The ₹300 crore expansion announced in 2022 already had 80% capacity booked before construction began.

The margin expansion story had multiple layers. Gross margins improved from 18% to 25% through backward integration—PGEL started manufacturing components they previously purchased. Operating margins expanded through automation and scale. But the real kicker was the financial leverage—interest costs as a percentage of revenue dropped from 3.5% to 1.2% as PGEL's credit rating improved and they accessed cheaper capital.

Return metrics showed the quality of growth. Return on Capital Employed (ROCE) improved from 12% in FY20 to 24% in FY24. Return on Equity (ROE) expanded from 15% to 28%. These aren't just good numbers for a manufacturing company—they rival those of asset-light businesses. The secret was capital efficiency: PGEL generated ₹2.5 of revenue for every rupee of fixed assets, compared to an industry average of ₹1.6.

The FY25 numbers took the transformation to another level. Q4 profit of ₹146.38 crores represented a two-fold increase, while full-year profit of ₹290.92 crores doubled from the previous year. Revenue surged to ₹4,904.63 crores, approaching the psychological ₹5,000 crore mark that would officially make PGEL a large-cap company by Indian standards.

Cash flow generation became the ultimate validation. Operating cash flow grew from ₹50 crores in FY20 to ₹400 crores in FY24, even as the company invested heavily in capacity expansion. Free cash flow, after accounting for capital expenditure, remained positive throughout the growth phase—a rarity for companies growing at this pace. This self-funded growth model meant PGEL could expand without diluting equity or taking excessive debt.

The balance sheet strengthened remarkably. Debt-to-equity ratio improved from 1.2x to 0.6x despite massive capacity additions. The interest coverage ratio expanded from 3x to 12x. Current ratio improved from 1.1 to 1.4. These aren't just numbers—they represent a company that became financially antifragile even while growing at breakneck speed.

But perhaps the most impressive financial metric was one that doesn't appear in standard statements: customer funding. By 2024, PGEL's clients were effectively financing ₹200 crores of PGEL's working capital through advances for capacity booking and tool development. Customers were literally paying PGEL to expand capacity to serve them—a testament to how critical PGEL had become to their operations.

The stock market's recognition lagged the operational performance, creating opportunity for astute investors. While revenues grew 7.7x from FY20 to FY25, the stock price increased 25x from its March 2020 lows—multiple expansion on top of earnings growth. Yet even at ₹2,800 per share, PGEL traded at just 35x P/E, reasonable for a company growing at 40%+ with expanding margins and returns.

VIII. The Manufacturing Moat & Operational Excellence

At 4 AM in PGEL's Greater Noida facility, the first shift begins with a precision that would make Swiss watchmakers proud. Across 11 manufacturing units spread over 1.2 million square feet, 5,000 employees orchestrate one of India's most complex manufacturing operations. But the real moat isn't the scale—it's the intricate operational system that allows PGEL to manufacture competing products with zero defects and zero information leakage.

The complexity starts with geography. PGEL's facilities in Greater Noida handle plastic components and AC assembly. Ahmednagar focuses on washing machines. Bhiwadi manages metal components. Roorkee produces ODUs. This isn't random sprawl—it's strategic positioning. Greater Noida provides access to the North Indian market and skilled labor. Ahmednagar taps into Maharashtra's manufacturing ecosystem. Bhiwadi leverages Rajasthan's incentives. Roorkee offers proximity to component suppliers.

Managing multi-location, multi-product operations requires systems that go beyond traditional ERP. PGEL developed what they call the "Digital Thread"—every component, from a plastic knob to a compressor, gets a unique QR code at birth. This code tracks its journey through production, assembly, quality testing, and eventual integration into finished products. When a Voltas AC fails in Chennai, PGEL can trace the issue back to the specific machine, shift, and operator who made the problematic component.

The zero-defect philosophy isn't just a slogan—it's embedded in every process. Each production line has inline quality checks every 50 units. Statistical process control catches deviations before they become defects. Automated optical inspection systems check aesthetic quality. Most remarkably, PGEL maintains defect rates below 100 parts per million—better than many Japanese manufacturers.

The transition from contract manufacturing to ODM revealed another layer of capability. In contract manufacturing, you follow someone else's blueprint. In ODM, you create the blueprint. This requires deep understanding of not just manufacturing but design, materials science, thermal dynamics, and consumer behavior. PGEL built a 50-person R&D team, including PhDs in polymer science and mechanical engineering, who could design products from scratch.

Technology investments transformed traditional manufacturing. The injection molding machines installed in 2022 use AI to predict and prevent defects, adjusting parameters in real-time based on ambient conditions. Collaborative robots work alongside humans on assembly lines, handling repetitive tasks while workers focus on quality and customization. IoT sensors track everything from machine health to energy consumption, enabling predictive maintenance that has reduced downtime to below 2%.

But the real innovation lies in what PGEL calls "mass customization at mass production costs." The same assembly line that makes a basic ₹20,000 AC for Voltas in the morning can produce a premium ₹60,000 inverter AC for Daikin in the afternoon. This flexibility comes from modular design, quick-change tooling, and cross-trained workers who can handle multiple products.

The vendor ecosystem became an extension of PGEL's manufacturing system. Instead of the traditional adversarial supplier relationship, PGEL created partnerships. Key suppliers have dedicated space within PGEL facilities. PGEL shares demand forecasts, helps suppliers upgrade capabilities, and even provides working capital support. In return, suppliers guarantee quality, delivery, and price stability. This ecosystem of 200+ vendors became a moat—competitors couldn't just replicate PGEL's factories; they'd need to replicate the entire ecosystem.

Energy efficiency became both a cost advantage and a selling point. PGEL's facilities use 30% less energy per unit produced compared to industry average. Solar panels provide 20% of electricity needs. Heat recovery systems capture waste energy from injection molding machines. Water recycling systems achieve 90% reuse. These investments, initially seen as costs, now save ₹15 crores annually while meeting increasingly stringent environmental requirements from global clients.

The human element of operational excellence often gets overlooked. PGEL's 5,000 employees aren't just workers—they're craftsmen. The company invests 2% of revenues in training, far above the industry average of 0.5%. Every worker undergoes 100 hours of annual training. Supervisors attend leadership programs. Engineers get certified in Six Sigma and lean manufacturing. This investment in human capital shows in productivity metrics—defects caught by workers before reaching quality control, suggestions that save crores annually, and attrition rates below 10% in an industry where 25% is common.

The operational discipline extends to seemingly mundane areas. Inventory turns improved from 6x to 12x through better demand planning. Changeover times between products decreased from 4 hours to 45 minutes through SMED (Single-Minute Exchange of Die) techniques. Overall Equipment Effectiveness (OEE) increased from 65% to 85%, meaning machines produce good products 85% of the time they're supposed to be running.

Data became the nervous system connecting everything. PGEL processes 10 million data points daily—from machine parameters to quality metrics to worker productivity. Machine learning algorithms predict demand patterns, optimize production scheduling, and identify quality issues before they manifest. This digital infrastructure, built over five years at a cost of ₹50 crores, became as important as physical assets.

The proof of operational excellence lies in competitive benchmarking. PGEL's cost per unit is 10-15% lower than competitors despite paying above-market wages. Their lead time from order to delivery is 15 days versus industry average of 30 days. Their capacity utilization exceeds 80% even during off-seasons. These aren't incremental advantages—they're the compound effect of thousands of small improvements over two decades.

IX. India's EMS Opportunity & Competitive Dynamics

The conference room at the Electronics Industries Association of India is buzzing with an energy not seen since the 1991 liberalization. The numbers on the presentation screen tell a story of transformation: India's electronics manufacturing is projected to reach $300 billion by 2026. The room air conditioner market alone, currently at ₹25,000 crores, is expected to double by 2027. Everyone wants a piece of this pie, but few understand the competitive dynamics that will determine winners and losers.

The China+1 strategy, accelerated by COVID and geopolitical tensions, created a once-in-a-generation opportunity for Indian EMS players. Global brands, who had concentrated 80% of their manufacturing in China, suddenly needed alternatives. But this wasn't just about cost arbitrage—it was about supply chain resilience, geopolitical hedging, and market access. India, with its large domestic market and improving manufacturing ecosystem, became the obvious choice.

PGEL's timing in building capabilities was impeccable. While others were still debating whether to enter manufacturing, PGEL had already spent two decades building the foundation. When Daikin needed to reduce China dependence in 2021, PGEL had ready capacity. When the government announced PLI schemes for white goods, PGEL had already achieved the scale thresholds. When brands needed local manufacturing to avoid import duties, PGEL had the capabilities.

The competitive landscape in Indian EMS is fascinating in its diversity. Dixon Technologies, the largest player with ₹15,000 crores revenue, took a different path—focusing on electronics and mobile phones before entering white goods. Amber Enterprises, with ₹5,000 crores revenue, specialized in RACs from day one. Havells acquired Lloyd and integrated backward. Each had strengths, but PGEL's unique position straddled multiple categories.

What separates PGEL from competitors isn't just capabilities—it's the business model. Dixon operates more as a contract manufacturer, following client specifications exactly. Amber focuses on RACs, giving them depth but limiting breadth. PGEL's ODM+OEM model, combined with multi-category presence, created unique advantages. They could offer Godrej a complete solution—from design to manufacturing—while simultaneously doing pure contract manufacturing for LG.

The speed advantage became PGEL's signature. When Blue Star needed to launch a new model to counter Voltas's summer campaign, PGEL delivered in 45 days—Dixon quoted 90 days. When Amazon wanted to test private label ACs, PGEL had prototypes ready in two weeks—Amber needed six weeks. This speed came from vertical integration, flexible manufacturing systems, and most importantly, decision-making authority at the factory level.

Scale economics in EMS are brutal and beautiful. The minimum efficient scale for AC manufacturing is about 300,000 units annually—below this, unit costs are uncompetitive. But once you cross 1 million units, costs drop 20%. PGEL, producing 5.7 million units annually across categories, enjoys scale advantages that smaller players can't match. This shows in pricing—PGEL can offer prices 5-10% below smaller competitors while maintaining better margins.

The PLI (Production Linked Incentive) scheme became a game-changer, but not in the way most expected. The scheme offered 4-6% incentives on incremental sales for companies meeting investment and revenue thresholds. PGEL qualified for the highest tier, potentially receiving ₹400 crores over five years. But the real benefit wasn't the money—it was the signaling effect. Global brands saw PLI qualification as government validation of manufacturing capabilities.

Service became an unexpected differentiator. While competitors focused on manufacturing efficiency, PGEL built comprehensive service capabilities. They maintained spare parts inventory for every model manufactured in the last five years. They trained service technicians for their clients. They even managed reverse logistics for warranty claims. This end-to-end capability made them indispensable to brands that wanted to focus on marketing and sales.

The working capital advantage separated sustainable players from strugglers. EMS is a working capital-intensive business—you need to fund inventory, provide credit to customers, and manage payment timing with suppliers. PGEL's relationships allowed them to operate with 75-day working capital cycles versus 100+ days for smaller players. This 25-day advantage, on ₹5,000 crores revenue, meant ₹350 crores less capital locked up—capital that could fund growth.

Market share dynamics revealed the consolidation underway. The top 5 EMS players control 65% of the white goods manufacturing market, up from 45% five years ago. Smaller players, unable to match scale, technology, and working capital requirements, are exiting or becoming sub-suppliers. PGEL's share in RAC manufacturing grew from 8% to 15% in three years, gained not from competitors but from brands insourcing manufacturing.

The technology transition created new competitive vectors. As products became "smart"—ACs controlled by apps, washing machines with AI-powered wash cycles—manufacturing complexity increased exponentially. PGEL's investment in electronics manufacturing capability, including SMT (Surface Mount Technology) lines, positioned them for this transition. Competitors still outsourcing electronics found themselves at a disadvantage.

Regional dynamics added another layer. South India, with its electronics ecosystem, attracted mobile and laptop manufacturing. West India, with its proximity to ports, focused on exports. North India, with its large consumer base and existing vendor ecosystem, became the white goods hub. PGEL's strategic positioning in North India, with 80% of India's AC demand within 500 kilometers of its facilities, provided logistics advantages worth 2-3% of costs.

The competitive moat widened with each passing year. New entrants faced a daunting challenge: ₹500 crores minimum investment, 2-3 years to achieve quality certifications, 3-5 years to build vendor ecosystems, and competing against incumbents with decade-long customer relationships. The window for new players was closing, and PGEL was on the right side of the door.

X. Playbook: Lessons in B2B Manufacturing Excellence

The journey from commodity to value-added manufacturing is littered with failures. For every PGEL, there are dozens of component manufacturers who tried to move up the value chain and failed. Understanding why PGEL succeeded while others failed provides a masterclass in B2B manufacturing strategy.

The first lesson is counterintuitive: start with the unsexy stuff. While everyone chased glamorous products, PGEL spent a decade perfecting plastic buckets and components. This wasn't lack of ambition—it was deliberate foundation building. Every bucket manufactured taught them about polymer behavior. Every component delivered on time built trust. By the time they moved to finished products, they had capabilities competitors couldn't quickly replicate.

Customer concentration without customer risk became PGEL's signature strategy. Conventional wisdom says customer concentration is dangerous—lose one big client and you're finished. PGEL flipped this by making concentration work for them. Yes, their top 10 customers contribute 70% of revenue. But the average relationship spans 8+ years, contracts have 2-3 year tenure, and switching costs for customers are enormous. It's not concentration risk—it's relationship moat.

The art of capital allocation in manufacturing differs fundamentally from other sectors. In software, you can scale with minimal capital. In manufacturing, every expansion requires crores in machinery, working capital, and infrastructure. PGEL's rule: never invest speculatively. Every major capacity expansion was backed by customer commitments. This meant leaving some growth on the table but avoided the graveyards of unutilized capacity that plague manufacturing.

Building trust in India's low-trust ecosystem required extraordinary measures. PGEL institutionalized trust through systems: separate facilities for competing brands, financial penalties for information breaches, and most importantly, never launching their own brand despite having complete capabilities. This self-restraint, viewed as weakness by some, became their greatest strength—clients trusted them with innovations knowing PGEL wouldn't compete.

The discipline of being boring but excellent defined PGEL's culture. No flashy headquarters, no celebrity endorsements, no consumer brand ambitions. Just relentless focus on operational metrics: reducing defect rates by 10 basis points, cutting changeover time by 5 minutes, improving OEE by 1%. These incremental improvements, compounded over years, created insurmountable advantages.

Manufacturing in India requires understanding unique challenges. Power availability remains erratic—PGEL installed backup systems adding 5% to costs but ensuring zero production loss. Skilled labor is scarce—PGEL invested in training centers, creating their own talent pipeline. Vendor payments are chronically delayed—PGEL's prompt payment, even during COVID, created loyalty worth more than price negotiations.

The working capital puzzle in manufacturing has broken many companies. PGEL solved it through relationship arbitrage: getting 60-day credit from suppliers while offering 45-day terms to customers, effectively running negative working capital on incremental growth. This required trust from both sides, built over decades of consistent behavior.

Technology adoption in traditional manufacturing faces cultural resistance. PGEL's approach: implement technology that helps workers, not replaces them. Collaborative robots handle heavy lifting while workers focus on quality. AI predicts machine failures, preventing overtime stress. Digital systems reduce paperwork, not jobs. This human-centric automation gained worker buy-in, crucial for successful implementation.

The partnership philosophy extended beyond customers to competitors. When Dixon faced capacity constraints, PGEL took overflow orders without trying to poach clients. When Amber needed specific components, PGEL supplied them despite competing in finished goods. This "coopetition" built industry goodwill that returned manifold—recommendations for new clients, technology sharing, and even joint vendor development.

Scaling manufacturing requires different skills at different stages. Below ₹100 crores, it's about technical excellence. At ₹100-500 crores, it's about systems and processes. At ₹500-2000 crores, it's about capital efficiency and automation. Above ₹2000 crores, it's about ecosystem orchestration. PGEL's leadership evolved with each stage, bringing in professional managers while retaining entrepreneurial agility.

The importance of patient capital cannot be overstated. Manufacturing doesn't offer quick returns—new facilities take 2-3 years to optimize, customer relationships take 5+ years to mature, capabilities take decades to build. PGEL's promoter family, holding 60% equity, provided this patience. They refused private equity funding that would demand quick exits, chose debt over dilution, and reinvested profits rather than extracting dividends.

Vertical integration decisions shaped PGEL's trajectory. They integrated backward into components they could make better or cheaper—plastic parts, metal fabrication, some electronics. But they avoided integrating into areas requiring different DNA—compressors, motors, semiconductors. This selective integration balanced control with capital efficiency.

The multi-category strategy provided unexpected benefits. Capabilities developed for washing machines improved AC manufacturing. Vendor relationships for one category supported another. Seasonal complementarity—ACs peak in summer, washing machines in winter—improved capacity utilization. Most importantly, multi-category presence made PGEL indispensable to brands operating across categories.

Quality at scale requires systems, not just intentions. PGEL implemented Total Quality Management not as a certification exercise but as operating philosophy. Every worker is a quality inspector. Every defect triggers root cause analysis. Every customer complaint reaches senior management. This quality obsession, maintained even during rapid scaling, separated PGEL from competitors who let standards slip during growth.

The final lesson: manufacturing excellence is a marathon, not a sprint. While software companies can scale to billions in years, manufacturing requires decades. PGEL's 47-year journey from plastic components to becoming India's white goods manufacturing backbone couldn't be compressed. There are no shortcuts in manufacturing—only patient accumulation of capabilities, relationships, and trust.

XI. Bear vs Bull Case & Valuation Framework

The investment community remains divided on PGEL. Bulls see India's next Foxconn. Bears see customer concentration risk and capital intensity. Both have merit, but understanding the nuances separates successful investments from expensive mistakes.

The bull case starts with the India manufacturing megatrend. India's white goods market, currently at $15 billion, is expected to reach $50 billion by 2030. AC penetration at 8% versus China's 90% suggests massive headroom. Washing machine penetration at 11% implies similar potential. If PGEL maintains its 15% market share in manufacturing, revenues could reach ₹20,000 crores by 2030—a 4x from current levels.

Client stickiness provides the second pillar. PGEL's average client relationship spans 8+ years. Switching costs—new vendor qualification, quality stabilization, supply chain reconfiguration—can reach ₹50-100 crores for large brands. The recent Whirlpool contract for complete washing machine manufacturing validates this stickiness. Once embedded in a client's operations, PGEL becomes nearly impossible to dislodge.

Capacity expansion visibility offers unusual certainty. PGEL has announced ₹800 crores in capacity expansion over the next two years, funded through internal accruals. With 80% capacity pre-booked through customer commitments, revenue visibility extends to FY27. This isn't speculative expansion—it's confirmed growth.

The PLI tailwind provides both financial and strategic benefits. ₹400 crores in incentives over five years directly impacts bottom line. More importantly, PLI qualification signals government backing, attracting global brands seeking stable manufacturing partners. PGEL's early qualification positions them to capture disproportionate benefits.

Operating leverage remains underappreciated. With gross margins expanding from 18% to 25% and EBITDA margins reaching 12%, PGEL demonstrates pricing power rare in manufacturing. As revenues scale to ₹10,000 crores, fixed cost absorption could push EBITDA margins to 15%, implying ₹1,500 crores in EBITDA by FY27.

The bear case starts with customer concentration. Top 10 clients contributing 70% of revenue creates vulnerability. Loss of even one major client could impact 10-15% of revenues. While relationships are sticky, brands ultimately prioritize their economics. If a competitor offers significantly better terms, relationships can fracture.

Working capital intensity remains a structural challenge. Despite improvements, PGEL requires ₹1,000+ crores in working capital. As growth continues, working capital needs could outpace operating cash generation, requiring debt or dilution. The manufacturing business model inherently limits cash generation compared to asset-light businesses.

Competition intensification poses medium-term risks. Dixon's aggressive expansion, Amber's focus on premiumization, and potential entry by global EMS giants like Flex or Jabil could pressure margins. The PLI scheme, while benefiting PGEL, also encourages new entrants, potentially creating overcapacity.

The company's reliance on imported components raises supply chain concerns. Critical components like compressors, chips, and specialty plastics are imported, exposing PGEL to currency fluctuations, trade disputes, and supply disruptions. The 30% import content in finished products creates vulnerability to rupee depreciation and tariff changes.

Technology disruption could alter manufacturing dynamics. 3D printing, though nascent, could disrupt plastic components. Modular manufacturing might reduce the advantage of large-scale facilities. Brands developing in-house manufacturing capabilities, as Samsung did in Vietnam, could reduce outsourcing.

Valuation framework requires nuanced thinking. At ₹2,800 per share, PGEL trades at 35x FY25 earnings. For a manufacturer, this seems expensive. But PGEL isn't a typical manufacturer—it's growing at 40%+, expanding margins, and generating 25% ROE. Compared to Dixon at 45x or Amber at 40x, PGEL offers better value.

The DCF model suggests intrinsic value of ₹3,500-4,000, assuming 25% revenue CAGR for five years, margin expansion to 15%, and terminal growth of 10%. This implies 25-40% upside from current levels. However, DCF sensitivity to terminal growth rates means small assumption changes significantly impact valuation.

Relative valuation provides another lens. Global EMS players like Foxconn trade at 15-20x earnings, but grow at 10-15%. Indian EMS players command 35-45x, reflecting higher growth. PGEL's 35x multiple sits at the lower end of Indian peers despite superior execution, suggesting potential re-rating.

The sum-of-parts valuation reveals hidden value. The plastic components business, generating ₹1,500 crores revenue, could be valued at 1x sales. The consumer durables business, generating ₹3,400 crores, deserves 2x sales given higher margins. This implies ₹8,300 crores enterprise value versus current ₹12,000 crores, suggesting the market prices in significant growth.

Risk-reward analysis favors patient investors. Downside appears limited—even assuming 20% revenue decline and margin compression to 8%, PGEL would trade at ₹1,800, implying 35% downside. Upside, assuming successful execution of expansion plans and margin expansion, could reach ₹5,000, offering 80% returns. The asymmetric risk-reward appeals to long-term investors.

The path to mid-cap status seems clear. Reaching ₹10,000 crores revenue by FY27 and maintaining current multiples would result in ₹25,000 crores market cap, firmly in mid-cap territory. This isn't aggressive—it requires 35% annual growth, below recent performance, and stable multiples despite improving fundamentals.

What needs to go right for the next 5x? Revenue reaching ₹20,000 crores by 2030 (30% CAGR), margins expanding to 15% (from 12%), ROE sustaining at 25%, and multiples remaining at 35x. Aggressive but not impossible given India's manufacturing tailwinds and PGEL's execution track record.

XII. The Next Chapter & Future Bets

The strategic planning meeting at PGEL's headquarters in early 2025 feels different from previous years. The agenda has shifted from "how to grow" to "where to grow next." With dominance in white goods manufacturing established, the company stands at another inflection point, eerily similar to 2014 when they decided to move from components to finished products.

The PLI scheme for white goods, where PGEL already qualified, is just the beginning. The government has announced PLI for auto components, IT hardware, and telecom equipment—sectors where PGEL's manufacturing expertise could translate. The auto components PLI, offering 8-13% incentives, particularly intrigues management. Electric vehicles require plastic components, thermal management systems, and electronic assemblies—all within PGEL's capabilities.

The EV opportunity deserves special attention. Every electric two-wheeler needs 15-20 kg of engineered plastics. Every electric car requires sophisticated thermal management for batteries. PGEL's expertise in injection molding and thermal systems positions them perfectly. Initial discussions with Ola Electric and Ather Energy have begun. The strategy isn't to make batteries or motors but to become the integration partner—assembling battery packs, manufacturing cooling systems, producing aesthetic components.

New-age electronics present another avenue. Smart home devices—video doorbells, security cameras, smart switches—require capabilities PGEL possesses: plastic molding, electronic assembly, and aesthetic design. The Indian smart home market, currently $2 billion, is expected to reach $10 billion by 2027. PGEL could replicate its white goods strategy: manufacture for brands without competing.

International expansion possibilities are crystallizing. Global brands manufacturing in PGEL's facilities have started asking: "Can you manufacture for our other markets?" Whirlpool wants PGEL to supply washing machines for Bangladesh and Sri Lanka. Daikin is exploring PGEL manufacturing ACs for Southeast Asia. The opportunity isn't just exports—it's becoming a regional manufacturing hub.

The "Make in India for the World" vision aligns perfectly with PGEL's capabilities. India's free trade agreements with ASEAN, upcoming agreements with EU and UK, and improving logistics infrastructure create export opportunities. PGEL's cost structure—30% lower than Southeast Asia, 50% lower than China for comparable quality—makes exports viable.

But the most intriguing opportunity lies in becoming India's Foxconn—not just in scale but in model. Foxconn's genius wasn't just manufacturing; it was becoming so integral to clients that they couldn't leave. PGEL is implementing similar strategies: embedding engineers at client facilities, managing entire product lifecycles, even handling after-sales service. The vision: brands focus on design and marketing while PGEL handles everything else.

The technology investments reveal future ambitions. PGEL is building an IoT platform that allows real-time monitoring of products manufactured. Imagine Voltas knowing exactly how many ACs are running, their energy consumption, and failure patterns—data gold for product development and service. PGEL wouldn't own this data but would be the platform enabling it.

Sustainability initiatives, initially seen as compliance, are becoming competitive advantages. PGEL's commitment to carbon neutrality by 2030 resonates with global brands facing ESG pressure. The 100 MW solar project under development wouldn't just reduce costs—it would make PGEL one of India's few carbon-neutral manufacturers, a powerful differentiator for environmentally conscious brands.

The R&D center expansion hints at ODM ambitions. The new 100-person facility in Noida won't just support existing products—it will develop new categories. Early projects include portable air purifiers (post-COVID demand surge), smart water heaters (IoT-enabled), and modular kitchen appliances (targeting urban millennials). These aren't for PGEL brands—they're innovations offered to clients.

Acquisition possibilities are emerging. Several smaller EMS players, struggling with scale and working capital, are seeking buyers. PGEL's strong balance sheet and operational expertise make them natural consolidators. The strategy wouldn't be buying revenue but acquiring capabilities—a company with strong electronics manufacturing, another with export relationships, perhaps one with automotive expertise.

The government's focus on semiconductor assembly and testing creates longer-term opportunities. While PGEL won't manufacture chips, they could become assembly partners for semiconductor companies setting up in India. The capabilities required—clean rooms, precision handling, quality systems—exist within PGEL. It's a natural adjacency that could open entirely new revenue streams.

Supply chain finance initiatives could transform vendor relationships. PGEL is launching a platform where their suppliers can access working capital at PGEL's borrowing rates—typically 3-4% lower than what small suppliers pay. This isn't altruism—it's strategic. Financially healthy suppliers mean stable supply chains and better pricing.

The digital twin initiative represents manufacturing's future. PGEL is creating virtual replicas of their production lines, allowing simulation of new products before physical production. This reduces development time from months to weeks, crucial for fast-moving consumer electronics. Clients could test products virtually, accelerating time-to-market.

Can PGEL become India's Foxconn? The comparison is inevitable but imperfect. Foxconn generates $200 billion revenue; PGEL is at $1 billion. But Foxconn took 50 years to reach this scale. PGEL, leveraging India's manufacturing moment and learning from Foxconn's playbook, could compress this timeline. Reaching $10 billion by 2030 isn't impossible—it requires 60% CAGR, aggressive but achievable given the tailwinds.

The next five years will determine whether PGEL remains a successful Indian manufacturer or becomes a global manufacturing champion. The pieces are in place: capabilities, relationships, capital, and most importantly, timing. India's manufacturing renaissance is just beginning, and PGEL is positioned at the epicenter.

XIII. Epilogue & Reflections

Standing at PGEL's Greater Noida facility, watching thousands of air conditioners roll off assembly lines destined for homes across India, it's hard not to reflect on the deeper significance of this story. This isn't just about one company's success—it's about India's manufacturing ambitions, the power of patient capital, and the often-overlooked heroes building the physical economy while everyone celebrates the digital one.

PGEL's journey matters because it proves manufacturing excellence is possible in India. For decades, the narrative was that India could never compete with China in manufacturing—labor wasn't as disciplined, infrastructure was inadequate, and the ecosystem was missing. PGEL systematically demolished each excuse. They proved Indian workers, properly trained and motivated, match anyone globally. They worked around infrastructure limitations through ingenuity. They built ecosystems through patience and partnership.

The story challenges conventional business wisdom. In an era celebrating asset-light models, PGEL invested hundreds of crores in factories. While everyone chased B2C glory, they remained steadfastly B2B. When consultants preached diversification, they stayed focused on their core. They proved that boring businesses, executed brilliantly, create extraordinary value.

For entrepreneurs in "unsexy" industries, PGEL offers inspiration. You don't need to build the next unicorn app to create value. Manufacturing plastic components might not get TechCrunch coverage, but it can build a ₹15,000 crore company. The path requires different virtues—patience over speed, depth over breadth, relationships over transactions—but the destination is equally rewarding.

The power of patient capital deserves emphasis. The Gupta family, maintaining 60% ownership through PGEL's journey, never succumbed to quick-exit pressures. They reinvested profits for decades, accepted lower margins during capability building phases, and chose strategic value over financial optimization. This patient capital, increasingly rare in quarterly-earnings-obsessed markets, enabled long-term thinking that created lasting value.

What makes PGEL special isn't any single brilliant strategy—it's the compound effect of thousands of correct small decisions over decades. The decision to pay suppliers on time during COVID. The choice to maintain quality even when clients wouldn't notice. The discipline to not launch their own brand despite temptation. These decisions, individually minor, collectively created an unassailable position.

The India story embedded in PGEL's success is compelling. A nation of 1.4 billion people, with per-capita income crossing $3,000, is entering the sweet spot for consumer durables consumption. AC penetration at 8% versus China's 90% suggests a multi-decade growth runway. PGEL isn't just riding this wave—they're enabling it, making air conditioning affordable for millions of Indian families.

The human element shouldn't be forgotten. Behind the numbers are 5,000 families whose livelihoods depend on PGEL. The workers who take pride in zero-defect manufacturing. The engineers who solve complex problems daily. The managers who balance competing brand requirements. The Gupta family who built this over 47 years. Business, at its best, is about creating value for all stakeholders, and PGEL exemplifies this.

Looking forward, PGEL represents a new breed of Indian companies—globally competitive, professionally managed, but retaining entrepreneurial DNA. They're not trying to be the next Apple or Tesla. They're content being the company that enables other brands to serve customers better. This humility, combined with ambition, creates sustainable competitive advantages.

The macro implications are profound. If India achieves its $5 trillion economy ambition, manufacturing must contribute 25% of GDP versus current 15%. This requires hundreds of PGELs—companies that can manufacture at global quality and local costs. PGEL's playbook, refined over decades, provides a template others can follow.

For investors, PGEL offers lessons in identifying future champions. Look for companies building capabilities, not just revenues. Value customer relationships lasting decades, not quarters. Appreciate operational excellence even if it seems boring. Understand that in manufacturing, slow and steady doesn't just finish the race—it wins it.

The final reflection is personal. In a world increasingly disconnected from physical production, PGEL reminds us that someone, somewhere, makes the things we use daily. The AC cooling your room, the washing machine cleaning your clothes—they don't just appear in stores. They're manufactured by companies like PGEL, where thousands of people work to ensure quality, affordability, and availability.

PGEL's story is far from over. As India's manufacturing sector enters its golden decade, PGEL stands ready to capture disproportionate value. The company nobody heard of might become the company nobody can ignore. From plastic components to becoming India's manufacturing backbone—it's been an extraordinary journey. The next chapter promises to be even more interesting.

In the end, PGEL proves something profound: in business, as in life, the tortoise often beats the hare. Consistent execution beats brilliant strategy. Depth beats breadth. Trust beats transactions. And sometimes, the most boring businesses make the best investments. As India writes its manufacturing story, PGEL won't just be a footnote—it might be an entire chapter.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube