Altius Telecom: The Quiet Giants of India's Digital Sky

I. Introduction & Episode Roadmap

Picture the most ordinary moment in modern Indian life. A street vendor in Lucknow taps a QR code to accept eleven rupees for a cup of chai. A college student in Coimbatore streams an IPL match on her phone while squeezed into a crowded bus. A farmer in rural Maharashtra checks the day's mandi prices before deciding whether to send his onions to market. Every one of these acts—billions of them, every single day—travels as an invisible pulse of radio energy up to a piece of galvanized steel bolted to a rooftop or planted in a field, then down a strand of glass fiber, and out across the country.

We all know the names painted on the SIM cards. Reliance Jio. Bharti Airtel. Vodafone Idea. We argue about their data plans and their call-drop rates. But here is the question almost nobody in India asks: who owns the steel? Who owns the towers, the diesel generators, the battery banks, the land leases, and the backhaul fiber that the telecom operators simply rent? The answer, increasingly, is a company most retail investors have never heard of, listed under a forgettable five-digit code on the Bombay Stock Exchange.

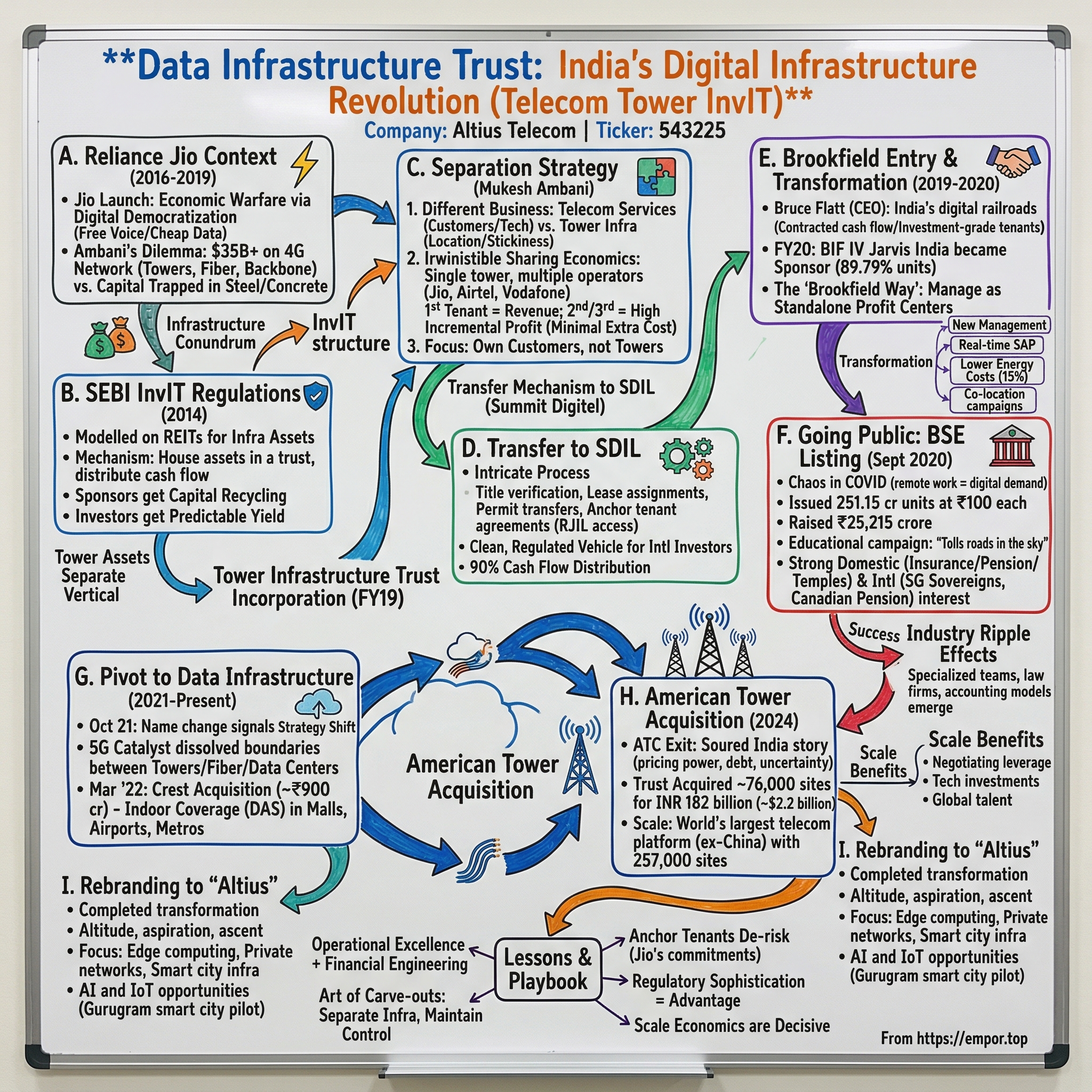

Meet Altius Telecom Infrastructure Trust (BSE: 543225), an entity that has worn three names in less than a decade. It was born as Tower Infrastructure Trust, spent years as Data Infrastructure Trust, and only recently took the name Altius—Latin for "higher."4[^6] It is not a company in the ordinary sense. It is an Infrastructure Investment Trust, or InvIT, a peculiar financial vehicle that Indian regulators designed to let patient global capital own roads, power lines, and—in this case—the physical bones of the mobile internet. Its sponsor is Brookfield Asset Management, the Canadian alternative-asset behemoth that has quietly become one of the largest private owners of infrastructure on the planet.

This is not a tidy story of a founder with a dream and a garage. There is no charismatic entrepreneur sketching the People's Tower on a napkin. This is a story about financial engineering as a competitive weapon. It is a story about a corporate carve-out so large it helped reshape a trillion-dollar industry, about a distressed-asset takeover executed while an American giant was fleeing the country in panic, and about the strange and powerful alchemy by which Canadian teachers' pensions and a Singaporean sovereign wealth fund came to own the toll bridge for India's entire digital economy.

Here is the road we will travel. First, the genesis: how Reliance Jio's staggering debt load forced the creation of the trust, and how Brookfield walked through the door. Second, the distressed M&A masterclass—how Altius bought American Tower's Indian business for cents on the dollar at the exact moment everyone else had given up. Third, the core economics of passive tower infrastructure and the duopoly war between Altius and Indus Towers. Fourth, the hidden 5G growth engine hiding inside a small subsidiary called Crest Digitel. Fifth, the Brookfield governance machine and the dramatic capital-markets moves of June 2026. And finally, the strategic frameworks—Hamilton Helmer's 7 Powers and Porter's Five Forces—and the bull and bear cases for anyone trying to understand whether the quiet giant is a fortress or a house of leverage.

Let's begin where every great infrastructure story in modern India begins: with a man who decided to give away mobile data for free.

II. The Genesis: Reliance Jio's Deleveraging & The InvIT Carve-Out

In the autumn of 2016, India's telecom industry was a comfortable, crowded, profitable mess. A dozen operators jostled for subscribers. Call rates were among the cheapest in the world, but mobile data was still a luxury, metered out in expensive megabytes. Then Mukesh Ambani's Reliance Industries flipped a switch.

Jio launched with an offer so audacious it looked like a typo: free voice calls, forever, and months of free 4G data. The strategy was not subtlety; it was shock and awe. Within months, Jio had vacuumed up tens of millions of subscribers. Data consumption in India did not rise—it exploded, with the country leaping to become one of the largest mobile-data markets on earth almost overnight. The competitive carnage was total. Within roughly three years, a field of a dozen operators collapsed into effectively three private players: Jio, a defensive and merging Airtel, and the wounded combination of Vodafone and Idea.

But here is the part of the Jio story that gets less attention than the price war. Building a brand-new, all-IP, greenfield 4G network across a subcontinent of 1.4 billion people is not cheap. It is one of the most capital-intensive undertakings a private company can attempt. Reliance had poured something on the order of $35 billion into spectrum, equipment, fiber, and—crucially—a vast forest of telecom towers. The towers alone numbered well over a hundred thousand. And every one of those towers, every battery bank and diesel genset and steel lattice, sat on the balance sheet as debt-funded capital expenditure. Reliance had won the war for subscribers, but it was carrying the weight of the entire physical network on its books.

The 2019 Master Stroke

Here the financiers stepped in front of the engineers. Why, the logic went, should a company that wants to be in the business of selling connectivity and retail goods and digital services also tie up tens of billions of dollars owning steel poles? A tower is a long-life, low-volatility, utility-like asset. The natural owner of such a thing is not a fast-moving consumer business; it is a pool of long-duration, low-cost capital—a pension fund, an insurer, a sovereign wealth fund. The natural owner is patient money.

So in fiscal year 2019, Reliance Industrial Investments and Holdings Limited (RIIHL) carved its enormous tower division out of the operating business and dropped it into a newly created vehicle: Tower Infrastructure Trust, the seed from which Altius would grow.[^6] This was financial engineering of the highest order. In one structural move, Reliance could recycle billions of dollars of capital, shift a mountain of debt off the operating company's books, and free Jio to do what it did best—sign up subscribers and fight the price war—without the dead weight of owning the real estate underneath its own antennas.

Enter Brookfield

If Reliance was the seller of patient-money assets, Brookfield was its ideal buyer. The Canadian giant had spent decades assembling exactly the kind of long-duration capital that loves boring, contracted, inflation-linked cash flows. And in the InvIT structure, it found the perfect wrapper.

In fiscal 2020, Brookfield, alongside a consortium of institutional co-investors that would come to include Singapore's sovereign wealth fund GIC and the British Columbia Investment Management Corporation (BCI), executed what was then the largest foreign infrastructure investment in India's history. The deal: roughly ₹25,215 crore—about $3.4 billion—to acquire 89.79% of the trust's units.[^6]3 Brookfield was not buying a company so much as buying a contract, and it is worth pausing on what that contract was.

The Foundations of Summit Digitel

The trust held, through its wholly owned operating subsidiary Summit Digitel Infrastructure Limited (SDIL), a portfolio of more than 135,000 of Jio's telecom towers.9 But the steel was almost beside the point. The crown jewel of the entire structure was a piece of paper: a 30-year, non-cancelable Master Services Agreement with Jio as the anchor tenant.9

Think about what that means. For three decades, Jio committed to paying rent on those towers, with the payments contractually escalating to track inflation. This is the closest thing the infrastructure world has to a government bond with an equity kicker. The single largest, fastest-growing telecom operator in India—a Reliance company with the deepest pockets in the country—had locked itself into paying a predictable, inflation-indexed stream of cash to the tower owner for thirty years, regardless of recessions, regulatory shocks, or price wars. For an owner of patient capital, this was not an investment. It was an annuity wearing a steel costume.

That bulletproof anchor contract is the bedrock on which everything else was built. But a single anchor tenant, however reliable, is a one-legged stool. To understand how Altius became the largest tower platform in the country—and one of the largest on earth—we have to follow Brookfield into the most contrarian deal of the entire saga: the moment it bought the assets that an American giant was desperate to abandon.

III. The Distressed M&A Masterclass: The ATC India Acquisition

For most of the 2010s, the smart money in India's tower business was American. American Tower Corporation, the Boston-headquartered real estate investment trust that had become the world's largest owner of communications towers, looked at India's data explosion and saw the future. ATC expanded aggressively, buying up tens of thousands of sites and betting that India's three-operator market would generate years of densification and rent growth.

For a while, the thesis worked. Then it didn't.

The Capitulation of American Tower

The problem had a name: Vodafone Idea, the merged entity that everyone in India simply calls Vi. Crushed by Jio's price war and saddled with an enormous regulatory liability over disputed government dues, Vi spent years teetering on the edge of insolvency. And Vi was one of ATC India's most important tenants. As Vi's financial distress deepened, it began stretching and missing payments to its tower landlords. ATC India found itself in the worst position an infrastructure owner can occupy: it had built and was maintaining tens of thousands of sites, incurring real costs every month, while a major customer simply stopped reliably paying the rent.

The numbers turned ugly. ATC India's unit economics, once a growth story, became a drag on the parent company's earnings and a stain on its share price. The Boston headquarters, answerable to American shareholders who wanted clean, predictable REIT cash flows, ran out of patience. In late 2023 and into early 2024, American Tower concluded a strategic review and decided to do something dramatic: exit India entirely, write off a substantial chunk of value, and sell the whole Indian business.1 On January 4-5, 2024, the company announced an agreement to sell its India operations to a Brookfield-led InvIT for an enterprise value of approximately $2.5 billion.16

This is the moment to appreciate the psychology. To American Tower, India had become a toxic asset—a place where a major customer wouldn't pay, where regulatory risk loomed, and where the stock market punished every quarter of disappointing Indian numbers. Getting out was a relief. The market applauded the exit.

Brookfield's Bold Play

Where a corporate operator saw a problem to escape, the distressed-value investor saw an opportunity to seize. Brookfield's entire institutional DNA is built around buying high-quality physical assets when they are temporarily unloved, financing them patiently, and waiting for the cycle to turn. ATC India was, beneath the bad headlines, a portfolio of real towers on real land serving real subscribers in the fastest-growing data market on earth. The cash flows were impaired, not destroyed.

Through the trust—by now renamed Data Infrastructure Trust—Brookfield agreed to acquire 100% of ATC's Indian business for approximately ₹18,200 crore, an enterprise value in the range of $2.2 to $2.5 billion.62 The deal closed in September 2024.23 The acquired business was eventually rebranded Elevar Digitel, taking its place alongside Summit Digitel inside the trust.

The strategic impact was seismic. The ATC India portfolio added roughly 76,000 sites to the platform in a single stroke. Combined with the Summit Digitel base, this catapulted Altius's total footprint to over 257,000 towers—vaulting it past Indus Towers to become the largest telecom tower platform in India and one of the largest in the world.23 Brookfield had used a competitor's panic to buy its way to the number-one position in a market it believed in.

Benchmarking the Acquisition

But scale alone is not what makes this a masterclass. The genius was in the price. Consider three lenses.

The first is the valuation arbitrage. Altius acquired ATC India at an implied EV/EBITDA multiple of under 6.0x. To put that in context, the listed corporate peer, Indus Towers, was trading at roughly 7.0x to 8.4x EBITDA over this period, and the Altius trust's own units commanded a richer listed InvIT multiple of around 10.3x.7 In plain English: Brookfield bought a portfolio of towers at a meaningfully lower multiple than the public market was assigning to comparable assets—including the multiple the market was assigning to Altius's own existing towers. The instant the assets crossed into the trust and began earning the trust's valuation multiple, value was created out of thin air. This is the oldest trick in the private-equity playbook—buy private and cheap, hold inside a publicly valued vehicle—and Brookfield executed it at multibillion-dollar scale.

The second lens is cost per tower. Brookfield bought ATC India's assets at roughly $28,000 to $32,000 per tower, in the neighborhood of ₹23 to ₹27 lakh apiece. Compare that to the estimated replacement cost of an Indus tower at $33,000 to $36,000, or to the historical valuation embedded in Altius's own core Summit portfolio of around $41,000 per tower. Brookfield was buying steel-and-concrete infrastructure at a discount to what it would cost to build the same thing new. When you can buy an asset for less than its replacement cost, in a market where building new supply is slow and difficult, you have bought yourself a structural margin of safety.

The third lens, and the most subtle, is the structuring shield. The brilliance was in how Brookfield handled the Vi problem—the very issue that had driven American Tower out. Rather than pay full price for impaired Vi cash flows and pray for recovery, Brookfield effectively absorbed Vi's current cash-flow stream at a deep discount baked into the purchase price. If Vi survived and paid, that was upside. If Vi faltered, the downside had already been priced in. Meanwhile—and this is the real prize—those same ATC towers stood ready to host the network densification programs of the healthy operators, Jio and Airtel, as they rolled out 5G. Brookfield had bought a portfolio priced for a dying Vi while owning the option on a booming Jio and Airtel. Heads, it wins big; tails, it loses little.

To understand why that option is so valuable—why putting a second or third tenant on an existing tower is close to alchemy—we need to step back and look under the hood of the tower business itself.

IV. Core Business Deep Dive: Tower Economics & The Duopoly Battle

Drive past a telecom tower and ask yourself what you are actually looking at. Most people see the antennas—the panels and dishes bristling near the top. But Altius doesn't own those. The antennas, the radios, the transmitters, the active electronics that actually send and receive your phone's signal—all of that belongs to the telecom operators. Jio mounts its own gear. Airtel mounts its own. Vi mounts its own.

So what does Altius own? Everything else. The "passive" infrastructure. The steel lattice or monopole itself. The secured land lease or the rooftop rights underneath it. The diesel generators and battery banks that keep the site powered through India's frequent grid outages. The shelter, the air conditioning, the security, and increasingly the optical fiber that runs from the base of the tower back into the core network. Altius is, in essence, a landlord that rents out vertical real estate plus power and connectivity, while the tenants bring their own electronics.

This sounds mundane. It is, in fact, one of the most beautiful business models in infrastructure, and the reason is a single number.

The Tenancy Engine and Operating Leverage

The magic word in the tower business is tenancy ratio—the average number of operators sharing a single tower. And the economics of that ratio are where the whole story lives.

Build a tower and sign a single tenant—say, Jio. That anchor tenant's rent has to cover the big fixed costs: the land lease, the power and fuel, the maintenance, the security. At a tenancy ratio of one, the tower is a modest, utility-like business. It pays its bills and earns a reasonable return. Fine.

Now add a second tenant. Say Airtel decides it needs coverage in that exact spot and mounts its antennas on the same tower. Here is the crucial fact: the land lease was already paid. The tower was already standing. The generator was already running. The incremental cost of letting Airtel bolt its gear onto the structure is tiny—some additional power, a bit more wear, a marginally larger genset. But the incremental rent is nearly a full second tenancy. The result is that the second tenant's revenue flows almost entirely to the bottom line. We're talking about incremental EBITDA margins approaching 100%.

Add a third tenant—Vi—and the same magic compounds. This is operating leverage in its purest, most elegant form. The first tenant pays the rent; the second and third tenants pay the profit. Every fractional increase in the portfolio-wide tenancy ratio is, quite literally, money for almost nothing. This is why Brookfield's ATC option matters so much: those acquired towers, many of them sitting at low tenancy, are loaded springs. Get Jio or Airtel to co-locate on a tower that today carries only Vi, and you have manufactured high-margin revenue without pouring a single new foundation.

Segment Breakdown & Revenue Contribution

Where does the money actually live inside Altius? Overwhelmingly in passive macro towers. The combination of Summit Digitel and Elevar—the big steel-and-land business—drives over 97% of the trust's consolidated revenues and profits.5 For fiscal year 2026, consolidated revenue stood at approximately ₹24,165 crore.5 Everything else we will discuss—the indoor 5G systems, the small cells—is strategically interesting but financially a rounding error against this engine. When you own Altius, you are overwhelmingly owning macro towers anchored by Jio.

The Duopoly Battle: Altius vs. Indus Towers

For most of the past decade, when Indians thought about tower companies at all, they thought about Indus Towers—the listed giant born from the towers of Bharti Airtel, Vodafone, and Idea. Indus was the establishment incumbent. Altius, growing quietly inside the Brookfield wrapper, has now overtaken it, and the contrast between the two is the central competitive drama of the sector.

Start with scale. Altius has roughly 257,000 towers; Indus operates around 226,000.2 Altius is now the bigger platform—but raw count is the least interesting part of the comparison.

Consider asset quality and fiberization. Altius's portfolio, anchored by Jio's relatively young, all-4G/5G-era network, skews newer and is far more fiberized—roughly 70% of its towers have physical optical fiber running to the base. Why does fiber at the tower matter? Because 5G is not just about the radio in the air; it is about the pipe behind it. A 5G antenna can pull torrents of data out of the sky, but if it is connected to the core network by an old microwave link instead of glass fiber, that torrent gets squeezed into a garden hose. High fiberization is what makes a tower genuinely 5G-ready, enabling the high bandwidth and low latency that 5G promises. Indus, with its legacy ground-based footprint built largely in the 2G and 3G eras, runs at materially lower fiberization. Altius's towers are, in a technical sense, a generation ahead.

And then there is the anchor tenant question—the difference between a fortress and an exposure. Altius's bedrock is Jio, locked in for thirty years on an inflation-indexed contract. Indus, by contrast, leans heavily on Airtel and carries significant exposure to the troubled Vi, whose payment reliability has been the sword hanging over the entire sector. Both companies serve the same three customers, but the quality of the anchor relationship is not the same. Altius's foundation is the strongest balance sheet in Indian telecom; a meaningful slice of Indus's is tied to the weakest.

The strategic takeaway for an investor is this: the tower business is not a commodity scramble but a duopoly of scale, where asset quality, fiberization, and anchor-tenant credit quality separate the winners. Altius has engineered itself to lead on all three. But scale and fiber are the macro story. The next, smaller chapter is about what happens when 5G signals hit a concrete wall—and why Altius quietly bought a company to solve exactly that.

V. The "Hidden" Growth Engine: Crest Digitel & 5G Densification

Walk into the underground concourse of a Delhi Metro station, or the departures hall of Bengaluru's airport, or the food court of a packed Mumbai shopping mall, and pull out your phone. If your 5G signal holds strong in those dense, concrete-wrapped, human-packed spaces, there is a decent chance you have Crest Digitel to thank—though you will never see its name anywhere.

In March 2022, the trust completed the 100% acquisition of Crest Digitel, formerly known as Space Teleinfra, for ₹1,283 crore, roughly $155 million.[^6]8 In the context of a platform worth billions, this was a small bet—Crest represents only about 3% of the trust's total asset value. That sizing is deliberate. It is large enough to give Altius a strategic capability and small enough that it cannot distract from or crowd out the enormous macro-tower story. Crest is the spice, not the meal.

Why Indoor Coverage Is a Real Problem

To understand why Altius bothered, you have to understand a piece of physics that quietly haunts every 5G network. The whole promise of 5G—blazing speeds, near-instant response—depends heavily on higher-frequency radio bands, the so-called mid-band and millimeter-wave spectrum. Higher frequencies carry more data. But there is a brutal trade-off: the higher the frequency, the worse the signal is at penetrating physical barriers. A low-frequency 2G signal will pass through several brick walls without much trouble. A high-frequency 5G signal can be badly weakened by a single pane of coated glass or a reinforced concrete wall.

This is why a forest of giant macro towers, however dense, cannot fully deliver urban 5G. Those towers blanket the outdoors beautifully, but their high-frequency signals struggle to reach deep inside the very places where data demand is most intense—the malls, the airports, the metro tunnels, the high-rise offices where thousands of people congregate and stream simultaneously. The solution is not bigger towers but smaller, distributed infrastructure placed inside the buildings: in-building solutions, or IBS, and small cells—compact antennas tucked into ceilings and walls that bring the signal right to where the people are.

Crest's Neutral-Host Strategy

Crest operates as a neutral-host provider. Rather than each operator building its own tangle of indoor antennas in a given mall or airport, Crest builds one shared indoor system and rents capacity on it to all three operators at once. It has deployed these systems in exactly the high-traffic venues where indoor coverage is hardest and most valuable—Delhi Metro stations, the Bengaluru and Mumbai airports, and premier shopping malls across the country.8

The neutral-host model means Crest enjoys the same tenancy magic as the macro towers, just at a smaller scale: build the indoor system once, then layer on multiple operators, each adding high-margin revenue. The business is growing at roughly a 12% compound annual rate and generated around ₹418 crore in revenue—real growth, even if modest against the macro engine.[^6]

Strategic Value Beyond the Numbers

So why does a 3% subsidiary matter? Because it makes Altius a one-stop shop. An operator like Airtel rolling out 5G in a city does not just need outdoor towers; it needs outdoor coverage and indoor coverage and small-cell densification on busy streets. With Summit and Elevar providing macro towers and Crest providing small cells and in-building systems, Altius can offer a single-window, end-to-end infrastructure partnership—macro towers plus small cells plus indoor solutions. For a telecom operator that would rather sign one contract than negotiate with five different vendors, that completeness is genuinely valuable. Crest is small, but it turns Altius from a tower landlord into a full-spectrum connectivity-infrastructure platform.

A platform of this complexity—three operating businesses, a quarter-million towers, billions in debt, and a roster of global pension-fund co-investors—does not run itself. It is run by a very particular kind of organization, with a very particular philosophy about capital. To understand how Altius is steered, we have to step inside the Brookfield machine.

VI. Under the Brookfield Microscope: Management, Governance, & Alignment

Most great Indian business stories have a face. There is a founder, a family, a patriarch whose personality is stamped on every decision. Altius has no such face, and that absence is itself the point. This is not a family enterprise; it is an institutional one, run according to the disciplined, repeatable, unsentimental playbook that Brookfield applies to infrastructure assets all over the world.

The trust is managed through a layered structure—Brookfield's India infrastructure manager and an associated investment manager sitting atop the operating subsidiaries.[^6] If that sounds bureaucratic, it is meant to be. The whole design philosophy of an InvIT is to separate ownership from management and to wrap the entire thing in regulatory guardrails that protect the unitholders from the kind of empire-building, related-party shenanigans, and capital misallocation that have plagued more than a few founder-controlled Indian conglomerates.

Meet the Key Decision Makers

At the top sits Arpit Agrawal, Chairman and Non-Executive Director of Altius and, in his Brookfield role, the Managing Partner heading infrastructure for India and the Middle East. Agrawal is the strategist—the person who decides where capital flows, which acquisitions to pursue, and how aggressively to consolidate the sector. The ATC India deal bore his fingerprints: it is precisely the kind of large, contrarian, consolidating move that defines Brookfield's infrastructure approach. His mandate is not to fall in love with steel; it is to compound capital.

Running the operating reality day to day is Munish Seth, Group Managing Director of Altius Telecom. Seth's challenge is one of integration. He oversees three distinct operating units—Summit, Crest, and Elevar—each with its own history, systems, and culture. The hardest, least glamorous work in any roll-up is making the acquired pieces actually function as one: harmonizing the maintenance contracts, merging the operating systems, and, above all, executing on that tenancy upside by getting new tenants onto the freshly acquired ATC towers. That operational grind is where the financial-engineering thesis either gets proven or quietly fails.

Leading the investment manager is Pooja Aggarwal, the CEO responsible for the regulated machinery of the trust—the distributions, the disclosures, the compliance with the InvIT framework that governs everything Altius does.

Incentives & Alignment

Here is where the InvIT structure does something genuinely clever. In a normal corporation, management can be tempted to grow for growth's sake—to chase revenue, headlines, and empire even when it destroys per-share value. Altius is wired differently. As a regulated trust, its distributions are tightly governed, and the investment manager's fees are tied directly to the growth of Net Distributable Cash Flow per unit. That single phrase—per unit—is the alignment mechanism. Management gets paid for growing the cash that flows to each unitholder, not for growing the gross size of the empire. It is hard to overstate how much this discipline matters in a market where "diworsification" and value-destructive expansion are common. The structure itself nudges the managers toward yield and away from vanity.

The June 2026 Sell-Down & Pre-IPO Movements

For years, the public could only watch this machine from the outside, since the sponsors owned the overwhelming majority of units. That began to change dramatically in the middle of June 2026, in a flurry of capital-markets activity that signaled Brookfield's next act.

In mid-June 2026, the sponsor consortium—Brookfield, BCI, and GIC—executed a coordinated sell-down of a 7.3% stake for ₹3,656 crore, placing the units through open-market block deals into the hands of domestic mutual funds and insurance companies.[^7] This was not an exit; with hundreds of thousands of towers and a controlling position, the sponsors remained firmly in command. It was a calibrated broadening of the ownership base, seeding the units with respected local institutions who would form the bedrock of a wider public float.

Running in parallel, Brookfield set in motion a roughly $300 million pre-IPO private placement, designed to establish a credible valuation benchmark—pegging the trust at around $5 billion—ahead of a planned public offering of approximately $630 million intended to dramatically expand the public unitholder base.[^9] The sequencing tells you exactly how an institution thinks: first place stock with sophisticated domestic institutions to set a price, then validate that price through a private placement, then open the doors to the broader public. Each step de-risks the next. This is patient capital choreographing its own liquidity, and it is the clearest sign yet that Brookfield intends to make Altius a permanent, widely held fixture of Indian public markets rather than a private holding to be flipped.

With the people and the incentives mapped, we can now do what Acquired listeners come for: run the whole thing through the strategic frameworks and ask the hard question—just how durable is this moat, really?

VII. Strategic Analysis: Hamilton's 7 Powers & Porter's 5 Forces

Strip away the financial engineering and ask the fundamental question: why can't someone else simply do what Altius does? Two frameworks help dissect the answer—Hamilton Helmer's 7 Powers, which catalogs the sources of durable competitive advantage, and Michael Porter's Five Forces, which maps the structural pressures on an industry. Let's run Altius through both.

Hamilton's 7 Powers Applied

The most distinctive power Altius possesses is what Helmer calls a Cornered Resource—a valuable asset that a company controls and that others cannot replicate. For Altius, that resource is the 30-year, non-cancelable, inflation-indexed Jio Master Services Agreement. No competitor can go out and sign an identical contract with Jio, because Jio is already locked into Altius's towers for three decades. This single document guarantees a baseline of revenue and, critically, debt serviceability through any conceivable macroeconomic storm. It is the bedrock beneath all the leverage, and it is, quite literally, cornered.

The second power is Scale Economies. With a quarter-million towers, Altius is the largest buyer of nearly everything a tower needs—steel, diesel, batteries, maintenance labor, and land. That buying power translates into lower per-tower costs that a smaller rival simply cannot match. Scale also unlocks something subtler but equally powerful: access to cheap capital. Altius operates with a CRISIL AAA credit rating, the highest in the land, which means it can borrow more cheaply than almost any peer.[^6] In a business where the entire model is built on financing long-life assets with long-life debt, a structurally lower cost of capital is itself a moat. Cheap money begets more assets begets more scale begets cheaper money.

The third power is Switching Costs. Once a telecom operator has mounted its heavy active radio equipment on an Altius tower, calibrated its antennas, and—crucially—run its fiber backhaul into that specific site, moving to a competitor's tower a few hundred meters away is enormously expensive and disruptive. It means dismantling live equipment, re-permitting, re-fibering, and risking coverage gaps for subscribers during the transition. The physical and operational friction of switching keeps tenants glued in place. Towers are not interchangeable commodities once the gear is bolted on; they are sticky.

Porter's 5 Forces Analysis

Now the pressures. The single most important force—and the one that should keep any Altius investor up at night—is the Bargaining Power of Buyers, which is HIGH. This is the central vulnerability of the entire business. Altius sells to essentially three customers: Jio, Airtel, and Vi. That is severe customer concentration. When your revenue depends on a handful of buyers, those buyers have leverage in negotiations, and the health of your business is hostage to the health of theirs. The 30-year Jio MSA blunts this risk enormously on the anchor side, but it does not eliminate the structural reality that Altius lives or dies by the fortunes of three companies. This force is the reason the bull case is never a slam dunk.

Against that, the Threat of New Entrants is VERY LOW. To replicate Altius, a newcomer would have to raise tens of billions of dollars, acquire hundreds of thousands of land rights, build a quarter-million towers, and somehow sign anchor tenants who are already locked into the incumbents. The capital intensity alone is an almost impenetrable barrier. Nobody is going to greenfield a competing nationwide tower platform from scratch. The incumbents' positions are, for practical purposes, unassailable by new players.

Finally, the Threat of Substitutes is LOW, though not zero, and here is where the savvy investor should keep a watchful eye on the sky. The most-discussed potential substitute is satellite connectivity—the low-earth-orbit constellations like Starlink that promise to beam internet directly from space. Could satellites make ground towers obsolete? For the foreseeable future, no. Satellites are a genuine boon for remote and rural coverage where towers are uneconomic, but they lack the raw capacity, the spectrum density, and the low-latency profile required to serve the crushing data loads of dense urban and semi-urban 5G networks. A single Mumbai neighborhood at rush hour generates more simultaneous data demand than a satellite beam can handle. Satellites will complement the terrestrial network at its thin edges; they will not replace the steel in the cities where the data—and the money—actually lives.

Taken together, the frameworks paint a clear picture: a business with formidable, multi-layered moats whose single great vulnerability is the concentration of its customers. That tension—fortress economics resting on a narrow customer base—is exactly what the bull and bear cases are about.

VIII. The Investor's Playbook: Bull vs. Bear Case & Key KPIs

If you owned a piece of this trust, what would you actually watch? Not the daily price ticks, and not the dozens of operational metrics that clutter an investor presentation. For a business like Altius, the signal hides in a very small number of figures. Track these, and you understand the company; ignore them, and you are flying blind.

The KPIs That Matter Most

The first and most important is the tenancy ratio, currently sitting at roughly 1.4x across the combined portfolio. We have already seen why this number is the beating heart of tower economics: because incremental tenants carry near-100% margins, every fractional move in this ratio flows almost directly to distributable cash. The single most important operational question facing Altius is whether management can lift the tenancy on the freshly acquired, lower-occupancy ATC towers by convincing Jio and Airtel to co-locate. Watch this number quarter by quarter. A rising tenancy ratio is the whole thesis playing out; a stagnant one is a warning that the synergy story is stalling. Investors should track it themselves rather than trust any single headline figure.

The second KPI is Net Distributable Cash Flow per unit. Because Altius is an InvIT whose entire reason for existing is to pass cash through to unitholders, NDCF per unit is the metric that governs the distribution. It currently supports a quarterly payout of approximately ₹4.01 per unit, which translates to a distribution yield of around 9.36%.[^6]7 For a yield-oriented investor, the durability and growth of that per-unit cash flow is the whole game. A high headline yield means little if the underlying NDCF is shrinking or being propped up by leverage; a steadily growing NDCF per unit is the sign of a healthy, compounding annuity.

The third KPI is average rent per tenant, which tracks whether the contractual lease escalations—typically indexed to consumer-price inflation at roughly 3-4% annually—are actually flowing through. This is the organic, do-nothing growth embedded in the business: even with zero new towers and zero new tenants, rents should ratchet upward with inflation each year. Watching this metric confirms that the inflation-protection built into those long contracts is real and being realized.

The Bull Case

The optimistic view is straightforward and powerful. Altius is the largest player in a market that has consolidated into a stable duopoly of scale, insulated from new entrants by impossible capital barriers. Its income is annuity-like, anchored by Jio's dominant and growing market share and protected by a 30-year inflation-indexed contract. It sits on a deep well of accretive synergy—the loaded springs of those low-tenancy ATC towers waiting to be filled. And it pairs a generous current yield of roughly 9.36% with a genuine secular tailwind: India's relentless 5G data densification, which demands more tenants, more fiber, and more small cells on exactly the infrastructure Altius owns. For an investor who wants infrastructure-grade cash flows with an emerging-market growth kicker, the package is rare.

The Bear Case

The skeptical view is equally coherent, and it rests on three pillars. The first is customer concentration, the high-buyer-power risk we have already named: a serious downturn in the health of Jio or Airtel would ripple straight through Altius's revenue, and no amount of operational excellence can fully hedge a three-customer market.

The second is the specific credit risk of Vi. The very same Vodafone Idea distress that drove American Tower out of India now sits inside Altius's own Elevar portfolio. Brookfield bought those assets at a discount that prices in trouble, which is prudent—but if Vi were to collapse outright rather than limp along, a meaningful slice of the acquired tenancy would evaporate, and the synergy math would need rapid backfilling from Jio and Airtel to compensate. Vi's survival is a live, material variable, and it is the single biggest qualitative risk concentration in the entire structure.

The third pillar is leverage. This is, by design, a highly geared vehicle—the whole InvIT model is built on financing stable assets with substantial debt, and Altius carries a debt-to-equity ratio in the neighborhood of 4.59x.7 In a benign or falling interest-rate environment, leverage is the investor's friend, amplifying the distributable yield. But high gearing cuts both ways. A sudden, sustained rise in systemic interest rates would raise refinancing costs and squeeze the cash available for distribution. The AAA rating and the laddered, long-dated debt profile mitigate this considerably, but they do not erase it. An owner of Altius is, ultimately, expressing a view not just on Indian data growth but on the stability of Indian interest rates over a very long horizon.

The honest synthesis is that Altius is neither a riskless bond nor a high-flying growth stock. It is a leveraged, concentrated, contractually fortified annuity on the growth of Indian mobile data—magnificent if the duopoly stays healthy and rates stay tame, painful if either assumption breaks. Which brings us, finally, to the larger lessons of the whole strange and elegant saga.

IX. Lessons & Epilogue

Step back from the towers and the tenancy ratios, and three larger lessons emerge from the Altius story—lessons that reach well beyond one trust on the Bombay Stock Exchange.

The first is the power of the financial-engineering playbook itself. The InvIT framework, a relatively young Indian regulatory innovation, did something genuinely transformative: it built a bridge between two worlds that had struggled to meet. On one side stood capital-hungry physical infrastructure—towers, fiber, the unglamorous steel of a developing nation's network—that demanded enormous, patient, long-duration funding. On the other side stood the largest pools of patient capital on earth: Canadian and global pension funds, sovereign wealth funds like GIC, institutional investors like BCI, all hunting for stable, inflation-linked, long-dated returns. The InvIT wrapper let them shake hands. Through that structure, billions of dollars of the world's most patient money flowed into financing the physical backbone of India's mobile revolution—capital that, structured as ordinary corporate debt or equity, might never have come. This is how emerging-market infrastructure increasingly gets built: not on government balance sheets, but through financial vehicles engineered to convert long-life assets into investable yield.

The second lesson is about the discipline of opportunistic M&A. The defining move of the Altius story was not building towers; it was buying them at the moment of maximum pessimism. American Tower, a sophisticated and successful global operator, walked away from India because the operational pain of Vi's distress had become intolerable to its shareholders. Brookfield recognized that the pain was real but the assets were sound, that the cash flows were impaired but not destroyed, and that a price reflecting panic was a price worth paying. Buying premium infrastructure below replacement cost, from a motivated seller, in a market you believe in, is one of the oldest and most reliable ways to create value—and it requires the temperament to move toward distress when others are fleeing it. That is a cultural and institutional capability, not a spreadsheet trick.

And the third lesson is the quiet one, the one embedded in the company's own invisibility. Every swipe of a payment app, every streamed cricket match, every video call between a migrant worker and the family back home, every government benefit delivered to a bank account in a remote village—all of it rides, at some point, up a piece of Altius steel and down a strand of Altius fiber. The company is the toll collector for the digital life of a subcontinent, and almost none of the 1.4 billion people paying that toll will ever know its name. There is a certain poetry in that. The loudest names in Indian telecom fight their price wars in television ads and billboards. The quiet giant simply owns the ground beneath the battle, collects its inflation-indexed rent, and passes the cash through to pension funds half a world away.

Whether Altius proves to be the fortress its bulls believe or the leveraged bet its bears fear, its existence marks a genuine shift in how the physical internet of the developing world gets financed and owned. The steel will stand for decades. The question that remains, for every investor watching that 9.36% yield and that 1.4x tenancy ratio, is whether the cash flowing through it will compound as quietly and reliably as the engineers who bolted the antennas to the sky once promised it would.

References

-

American Tower Completes Strategic Review, Announces Agreement to Sell Operations in India to Brookfield — American Tower Corp, 2024-01-04 ↩↩

-

American Tower Closes the Sale of Operations in India to Brookfield — American Tower Corp, 2024-09-12 ↩↩↩↩

-

Brookfield-led Consortium Completes Acquisition of Indian Tower Business of American Tower Corporation — British Columbia Investment Management Corp (BCI), 2024-09-12 ↩↩↩

-

Altius Telecom Infrastructure Trust (Formerly Data Infrastructure Trust) Corporate Announcements — Bombay Stock Exchange (BSE), 2026-06-19 ↩

-

Altius Telecom Infrastructure Trust (Formerly Data Infrastructure Trust) Financial Filings & Results — Bombay Stock Exchange (BSE), 2026-06-19 ↩↩

-

Brookfield-led InvIT to Acquire American Tower's India Unit for $2.5 Billion — Reuters, 2024-01-05 ↩↩

-

Data Infrastructure Trust Profile and Financial Multiples — Screener.in, 2026-06-19 ↩↩↩

-

Crest Digitel Private Limited Operational Overview & Small Cell Coverage — Crest Digitel, 2026-06-19 ↩↩

-

Summit Digitel Infrastructure Limited Portfolio & Anchor Tenancy — Summit Digitel, 2026-06-19 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube