Coal India: From Nationalization to Global Giant

I. Introduction & Episode Roadmap

Picture this: A single company controls 80% of a nation's coal production, employs nearly a quarter million people, and powers the lights for 1.4 billion citizens. Its market capitalization exceeds $40 billion, making it more valuable than most Fortune 500 companies. Yet this behemoth was born not from entrepreneurial ambition or venture capital, but from an ideological decision in Indira Gandhi's socialist India to nationalize an entire industry overnight.

Coal India Limited stands as one of the most fascinating paradoxes in global business. How does a government monopoly, created through forced nationalization and operating under socialist principles for decades, become the world's largest coal producer? How does a company that was never meant to be profitable generate more cash than it knows what to do with? And perhaps most intriguingly, how does the world's biggest coal company navigate a future where its very product is increasingly seen as an environmental pariah?

This is not your typical Silicon Valley success story. There are no garage startups, no venture rounds, no pivots to product-market fit. Instead, this is a tale of nation-building through natural resources, of employment over efficiency, of political power plays and Supreme Court earthquakes. It's about how a collection of 700+ scattered mines became a unified giant that would eventually list in India's largest-ever IPO, only to see its monopoly shattered by judicial intervention years later.

The journey takes us from the steam locomotives of British India to the boardrooms of Mumbai, from the coal fields of Jharkhand to the trading floors of global commodity markets. Along the way, we'll encounter powerful unions, political scandals that toppled governments, and the eternal tension between state control and market forces.

What makes Coal India particularly compelling for students of business is that it operates at the intersection of multiple contradictions. It's a fossil fuel company in the age of climate change. A state-owned enterprise competing with private players. A company with monopolistic roots facing market competition. An employer of 240,000 in an era demanding automation. Understanding Coal India means understanding India itself—its development trajectory, its energy security anxieties, and its struggle to balance growth with sustainability.

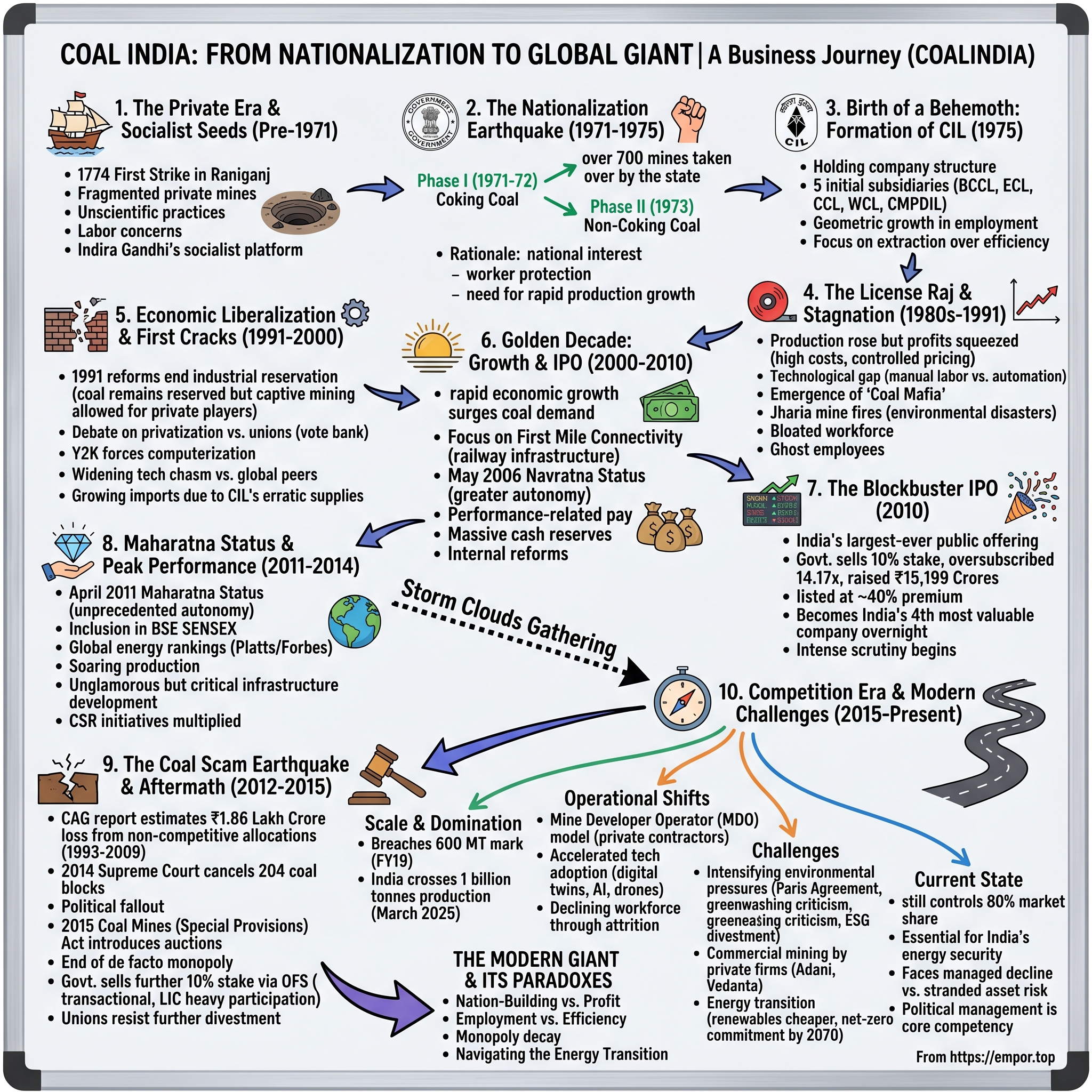

Our story begins in 1774, when the East India Company first struck coal in the Raniganj fields. But the real drama starts two centuries later, when a Prime Minister's socialist vision would create what remains one of the world's most powerful energy companies. This is the Acquired-style deep dive into Coal India—from nationalization to global giant, from monopoly to competition, from the coal scam that shook a nation to the energy transition that threatens its future.

II. Pre-Nationalization Era & The Socialist Dream (1774-1975)

The monsoon clouds gathered heavy over the Raniganj coalfields in 1774 when two employees of the East India Company—John Sumner and Suetonius Grant Heatly—struck coal along the western banks of the Damodar River. They couldn't have known they were birthing an industry that would, two centuries later, become the backbone of a nation's energy security and the subject of its most contentious political scandals.

The discovery itself was almost accidental, born from the Company's insatiable hunger for resources to fuel its colonial machinery. The early exploration and mining operations were carried out in a haphazard manner, more plunder than industry. Yet this chaotic beginning would set the pattern for Indian coal mining for the next century—foreign control, unscientific methods, and the treatment of natural resources as colonial spoils rather than national assets.

For nearly five decades after that first strike, coal mining in India remained a curiosity rather than an industry. The introduction of steam locomotives in 1853 gave a fillip to production, suddenly transforming coal from a geological oddity into the fuel of empire. Production rose to an annual average of 1 million tonnes and India could produce 6.12 million tonnes per year by 1900 and 18 million tonnes per year by 1920.

The real story, though, wasn't in the tonnage figures but in who controlled the mines. In 1835, Prince Dwarkanath Tagore bought over the collieries and Carr, Tagore and Company led the field—marking one of the first instances of Indian capital entering the sector. This was the era of the zamindars and managing agencies, where coal fortunes built palatial homes in Calcutta while miners worked in conditions that would later horrify even the colonial administration.

By independence in 1947, India's coal industry was a patchwork of over 900 private mines, mostly small operations run with minimal investment and maximum extraction. The sector produced around 30 million tonnes annually, but inefficiency was rampant. Mine owners, focused on short-term profits, employed what the government would later describe as "unscientific mining practices" that not only endangered workers but also destroyed vast reserves through improper extraction methods.

The newly independent India faced a paradox. Coal was essential for industrialization—it powered the railways, fed the steel plants, and generated electricity. Yet the private mine owners showed little interest in the massive capital investments needed for modernization. Adequate capital investment to meet the burgeoning energy needs of the country was not forthcoming from the private coal mine owners. They preferred to skim the easily accessible seams, leaving the deeper, more challenging deposits untouched.

Enter Indira Gandhi and the socialist dream. The year was 1971, and India was riding high on military victory over Pakistan. Gandhi, having split the Congress party and won a massive electoral mandate on the slogan of "Garibi Hatao" (Remove Poverty), was ready to reshape India's economic landscape. Having been re-elected in 1971 on a nationalisation platform, Gandhi proceeded to nationalise the coal, steel, copper, refining, cotton textiles, and insurance industries.

The nationalization of coal wasn't a single dramatic stroke but a calculated two-phase operation. The first phase came with the coking coal mines in 1971-72 and then with the non-coking coal mines in 1973. The distinction mattered—coking coal was crucial for steel production, the crown jewel of industrial planning, while non-coking coal powered everything else.

In October 1971, the Coking Coal Mines (Emergency Provisions) Act provided for taking over the management of coking coal mines, followed by the Coking Coal Mines (Nationalization) Act, 1972, under which these mines were nationalized on 1 May 1972 and brought under Bharat Coking Coal Limited. The government's rationale was wrapped in the language of national interest, but the underlying message was clear: natural resources belonged to the nation, not to private profiteers.

The second wave came swiftly. The Coal Mines (Nationalization) Act, 1973 nationalized all remaining mines on 1 May 1973. Overnight, the Indian state became the owner of over 700 coal mines, inheriting not just assets but also decades of mismanagement, dangerous working conditions, and a workforce that had been treated more as expendable resources than human beings.

What drove this massive appropriation? Poor working conditions of labour in some of the private coal mines became matters of concern for the Government. But beyond the humanitarian rhetoric lay hard economic logic—India needed coal production to grow dramatically to fuel its industrialization plans, and the fragmented private sector simply couldn't deliver.

The nationalization reflected the Indira Gandhi doctrine in its purest form: commanding heights of the economy must be controlled by the state. This wasn't just about coal; it was about asserting that India's natural resources were sovereign assets, not commodities for private enrichment. Most of these nationalisations were made to protect employment and the interest of the organised labour—a political calculation that would define Coal India's trajectory for decades to come.

As 1975 approached, the stage was set for the birth of a behemoth. The government had successfully wrested control of the entire coal industry, but now faced the monumental task of organizing these scattered mines into a coherent, productive whole. The solution would be Coal India Limited—a structure designed not for efficiency or profit, but for control, employment, and the socialist vision of natural resources serving national development.

III. Birth of a Behemoth: Coal India's Formation (1975-1990)

The morning of November 1, 1975, marked a watershed moment in India's industrial history. In a nondescript government office in Calcutta (now Kolkata), bureaucrats gathered to sign into existence Coal India Limited—a holding company that would eventually become the world's largest coal producer. But on that day, it was simply an organizational solution to an administrative nightmare: how to manage 700+ nationalized mines spread across a subcontinent.

The restructuring was surgical in its precision. All four divisions of the Coal Mines Authority Limited (CMAL) were given company status and brought under CIL's umbrella. Even the 45% shareholding that CMAL held in Singareni Collieries was transferred to the new entity before CMAL was shuttered. Thus, CIL started functioning in 1975 with five subsidiary companies under it: Bharat Coking Coal Limited (BCCL), Eastern Coalfields Limited (ECL), Central Coalfields Limited (CCL), Western Coalfields Limited (WCL), and Central Mine Planning & Design Institute Limited (CMPDIL).

The structure revealed the socialist planner's mindset—geographic division for operational efficiency, but centralized control for political management. BCCL, headquartered in Dhanbad, inherited the crown jewels: the coking coal mines essential for steel production. ECL at Sanctoria took over the historic Raniganj fields. CCL at Ranchi managed the central Indian deposits. WCL at Nagpur controlled the western territories. And CMPDIL, the technical brain, provided exploration and planning support from Ranchi.

With a modest production of 79 million tonnes at the year of its inception, CIL faced a herculean task. The company inherited not just mines but decades of accumulated problems—unsafe working conditions, outdated technology, and a workforce accustomed to the exploitative practices of private owners. The government's solution was quintessentially socialist: throw manpower at the problem. Employment became as important as extraction, setting a pattern that would define Coal India for generations.

The early years were marked by organizational chaos masquerading as planned development. As a result of the nationalizations, some rationalization took place in the sector. The mines were regrouped and reduced to 350 individual mines. New technology was introduced, and there was a shift from pick mining to blast mining, which resulted in considerable increases in production. Production totaled 87 million tons in 1975, and 99 million tons in 1976.

But these headline numbers obscured deeper dysfunctions. The subsidiaries operated like feudal fiefdoms, each with its own culture, practices, and political patrons. Their shares in the total production of coal varied from 25 percent for the Central and Western Coalfields, and about 20 percent for Bharat Coking Coal and Eastern Coalfields. The financial performance of the subsidiaries also varied dramatically. BCCL made cumulative losses of Rs 4.5 billion over the five year period 1981-1986. Similarly, Eastern Coalfields made cumulative losses of Rs 3.6 billion over the same five year period. In 1988, BCCL made a loss of Rs 900 million on a turnover of Rs 5.3 billion.

The organizational expansion continued through the 1980s as political pressures mounted. In due course of time, three more companies were formed under CIL by carving out certain areas of CCL and WCL. These were Northern Coalfields Limited (NCL), South-Eastern Coalfields Limited (SECL), and Mahanadi Coalfields Limited (MCL). Each carve-out represented not just operational logic but political accommodation—new subsidiaries meant new headquarters, new employment opportunities, and new patronage networks.

Labor relations emerged as Coal India's defining challenge. The unions, empowered by nationalization's promise of worker dignity, became formidable political forces. Strikes were frequent, productivity negotiations interminable. A typical underground miner in the 1980s produced less than a tonne per day, compared to over 10 tonnes in mechanized Western mines. But firing workers was politically impossible—Coal India was as much an employment scheme as a mining company.

The technology gap widened yearly. While global mining moved toward computerization and automation, Coal India's mines remained labor-intensive. Safety standards, despite government ownership, barely improved. Mine disasters continued with depressing regularity—roof collapses in Bihar, flooding in Bengal, fires in Jharia that would burn for decades. The irony was stark: nationalization, meant to improve worker conditions, had merely institutionalized their neglect.

Yet something remarkable was happening beneath the dysfunction. Pursuant to the Fuel Policy of 1974, CIL also started the construction of India's first Low Temperature Carbonisation Plant at Dankuni in the late 1970s. It was renamed as Dankuni Coal Complex, and is one of the only operational coal gas plant of this kind in the world. This technical achievement, largely forgotten today, showed that Coal India could innovate when political will aligned with engineering expertise.

The financial architecture of this behemoth was equally paradoxical. The subsidiaries of CIL had an average authorized capital of Rs 1.5 billion each during the late 1980s. Massive by Indian standards, yet insufficient for the modernization desperately needed. The government, caught between its socialist rhetoric and fiscal constraints, starved Coal India of capital while demanding ever-higher production targets.

By 1990, Coal India had consolidated its position as India's energy gatekeeper. It controlled over 85% of national coal production, employed over 600,000 people, and operated more than 400 mines. The company had become too big to fail, too political to reform, and too important to ignore. It was a perfect socialist enterprise—massive, inefficient, and absolutely essential.

The creation of Coal India represented the apotheosis of the commanding heights philosophy. Natural resources would serve national development, not private profit. Employment would trump efficiency. Political control would override market signals. These weren't bugs in the system; they were features, carefully designed to serve the socialist vision of independent India.

As the 1980s drew to a close, storm clouds gathered on the economic horizon. The Soviet Union, India's socialist inspiration, was crumbling. The License Raj was choking growth. And Coal India, the crown jewel of nationalization, was producing barely enough coal to keep the lights on. Change was coming, but first, the behemoth would have to navigate the twilight years of Indian socialism.

IV. The License Raj Years & Slow Growth (1980s-1991)

The summer of 1982 in Dhanbad was particularly brutal. The temperature hit 47°C, power cuts lasted eighteen hours, and at the Bharat Coking Coal Limited headquarters, production figures were being massaged yet again to meet Plan targets that everyone knew were fiction. Welcome to the License Raj years—where reality bent to bureaucratic will, where five-year plans became exercises in creative accounting, and where Coal India discovered it could fail upward with remarkable consistency.

By the late 1980s the mechanisation drive rammed into the profit squeeze: out-put productivity might had been increased, total coal production doubled during the 1980s, but production costs per ton were not lowered to a more profitable level. The paradox was stunning—production rose, but profitability plummeted. In 1986-87 the Coal India Limited accumulated losses stood at 18,000 million Rs. In 1988 a committee which included top CIL officials and representatives of INTUC, AITUC and CITU concluded that "between 1980-81 and 1985-86 while the wage cost per tonne of coal went up from Rs 73.18 to Rs 103.51, the total cost per tonne of coal went up from Rs 123.12 to Rs 214.20 per tonne."

The License Raj wasn't just about licenses—it was a comprehensive system of economic control where every business decision required government approval, where production targets were set by planners who'd never seen a coal mine, and where inefficiency was institutionalized as policy. For Coal India, this meant operating in a bizarre parallel universe where meeting Plan targets mattered more than making money, where employment generation trumped productivity, and where political patronage determined everything from mine allocation to union leadership.

The Five-Year Plans, those Soviet-inspired monuments to central planning, set increasingly ambitious targets for coal production. The Sixth Plan (1980-85) demanded 165 million tonnes by 1985. The Seventh Plan raised it to 226 million tonnes by 1990. Coal India dutifully reported numbers approaching these targets, but the quality of coal, the cost of extraction, and the mounting losses were swept under the statistical carpet. It was easier to manipulate data than modernize mines.

Technology stagnation became Coal India's defining characteristic during this period. While global mining moved toward computerized longwall systems and automated extraction, Indian mines remained trapped in the 1950s. During the 1970s and 1980s to get a permanent job at CIL required personal connection—merit was secondary to political recommendation. The workforce ballooned to over 650,000 by 1990, making Coal India one of the world's largest employers, but productivity per worker remained abysmal.

Then there was the coal mafia—perhaps the most enduring legacy of the License Raj in the coalfields. The state-owned coal mines of Bihar (now Jharkhand after the division of Bihar state) were among the first areas in India to see the emergence of a sophisticated mafia, beginning with the mining town of Dhanbad. It is alleged that the coal industry's trade union leadership forms the upper echelon of this arrangement and employs caste allegiances to maintain its power. Pilferage and sale of coal on the black market, inflated or fictitious supply expenses, falsified worker contracts and the expropriation and leasing-out of government land have allegedly become routine. A parallel economy has developed with a significant fraction of the local population employed by the mafia in manually transporting the stolen coal for long distances over unpaved roads to illegal mafia warehouses and points of sale.

The mafia's emergence wasn't accidental—it was the natural outcome of a system where official channels were so clogged with bureaucracy that parallel structures became necessary for basic functioning. These intermediaries eventually assumed official positions in labor unions, which gave them a platform for electoral politics. When the coal industry was nationalized, the union leaders further solidified their position in the nationalized corporation. In this way, private labor intermediaries became local political leaders who controlled the state apparatus to some extent.

The illegal mining economy developed its own sophisticated ecosystem. In some cases, the same mine is operated both officially and unofficially, e.g. in a Bansra mine where 44 local brick kilns purchase the illegal coal mined from the 7 feet upper layer, whereas the 18-20 feet thick lower layer is worked by CIL. The mine then enters the labour intensive, low wage and precarious realm, where workers are under extra-pressure of law and mafia-type of middlemen.

Environmental disasters multiplied during these years, each one a testament to regulatory capture and administrative apathy. The Chasnala mining disaster of 1975, where 375 miners died in a flooded mine, set the tone for the decade. Underground fires in Jharia, sparked by unscientific mining, began spreading uncontrollably. By the late 1980s, over 70 fires burned continuously, destroying millions of tonnes of coal reserves and rendering vast areas uninhabitable.

Safety standards, despite being a government enterprise, remained primitive. Mine inspectors could be bought, safety equipment was routinely pilfered and sold, and accident statistics were massaged as creatively as production figures. The irony was profound—nationalization, ostensibly done to protect workers, had created conditions arguably worse than under private ownership.

Political interference reached absurd levels. Ministers would call to demand jobs for constituents, leading to situations where some mines had more workers on payroll than actual positions. Ghost employees proliferated—workers who existed only on paper but whose salaries were very real. One audit in 1987 found that Eastern Coalfields had 15,000 employees who couldn't be physically located.

The quality crisis deepened yearly. Indian power plants, designed for coal with 3,500-4,000 kcal/kg calorific value, increasingly received coal barely reaching 2,500 kcal/kg. The solution? Mix stones with coal and adjust the paperwork. The coal mafia has had a negative effect on Indian industry, with coal supplies and quality varying erratically. Steel plants complained, power plants broke down, but the system trudged on.

Labor relations during this period resembled trench warfare. Major unions—INTUC (Congress-affiliated), AITUC (Communist), CITU (CPM), and BMS (BJP)—carved up the coalfields into spheres of influence. Strikes were called not for worker welfare but for political positioning. The 1981 strike lasted 47 days, the 1983 strike 35 days, each costing millions in lost production and pushing Coal India deeper into the red.

The mafia is an economical and political network, which reaches from money-lending, illegal liquor shops, paid goons to illegal mining and transport contracts, which are connected to the high ranks of CIL management department. The Dhanbad mafia controlled the main trade unions, bought off the police and local administration and was well represented in the Bihar state parliament.

By 1989, the contradictions had become unsustainable. Coal India was producing around 200 million tonnes annually but losing money on every tonne. It employed hundreds of thousands but had among the world's lowest productivity rates. It controlled 85% of India's coal but couldn't meet either quality or quantity demands. The company had become a metaphor for everything wrong with the License Raj—bloated, inefficient, corrupt, and yet absolutely essential.

The fall of the Berlin Wall in 1989 sent shockwaves through India's political establishment. The Soviet model, which had inspired India's planned economy, was crumbling. In Coal India's boardrooms and mining townships, there was a sense that change was inevitable. The question was whether the behemoth could reform itself or whether external shock would force transformation.

As 1991 approached, India's foreign exchange reserves dwindled to barely three weeks of imports. The economic crisis that would force liberalization was gathering steam. For Coal India, cocooned in its monopoly comfort, the coming changes would be seismic. The License Raj was dying, but its ghost would haunt the coalfields for decades to come.

V. Economic Liberalization & The Awakening (1991-2000)

July 24, 1991. Finance Minister Manmohan Singh stood in Parliament, his soft voice carrying words that would shatter four decades of socialist certainty: "Let the whole world hear it loud and clear. India is now wide awake." The country had barely $1 billion in foreign reserves, enough for just three weeks of imports. Gold bars were being secretly flown to London as collateral for emergency loans. The License Raj was dying, and with it, the comfortable monopolies that had defined Indian business—including Coal India's iron grip on the nation's energy.

For Coal India's bureaucrats in their Kolkata headquarters, liberalization arrived like an unwelcome monsoon. The New Industrial Policy reduced the number of industries reserved for the public sector from 17 to just 3—but coal remained on that exclusive list. It was a pyrrhic victory. While Coal India kept its monopoly on paper, the first cracks in the fortress had appeared. As a part of the 1991 economic reforms, the mining sector was thrown open to private players, but only for captive purposes in specific industries.

The captive mining provision was revolutionary in its implications. Private companies in steel, cement, and power generation could now mine coal for their own use. Although the Coal Mines (Nationalisation) Act, 1973 restricted the role of private players in coal mining, subsequent amendments were made to the act to allow captive mining by private companies for selected end-use sectors such as power, iron and steel, cement, washing and coal gasification. This wasn't privatization, the government insisted—it was merely allowing companies to meet their own needs. But everyone knew it was the thin edge of the wedge.

The debate over Coal India's privatization became the defining economic argument of the 1990s. On one side stood the reformers, armed with damning statistics: productivity per worker was one-tenth of global standards, losses had mounted to tens of billions of rupees, and India was importing coal despite sitting on the world's fourth-largest reserves. On the other side stood the unions, 650,000 strong, backed by political parties across the spectrum who saw Coal India not as a company but as a vote bank.

The political calculus was brutal. Coal India employed more people than the entire population of several Indian cities. Each employee supported, on average, five family members. That meant over 3 million voters directly dependent on Coal India's survival as a public sector behemoth. No politician, however reform-minded, wanted to touch this third rail.

Yet liberalization's logic was seeping into the coalfields like water through sandstone. The Y2K preparations forced Coal India to finally computerize operations that had been paper-based since the British Raj. Younger engineers, educated in the post-liberalization era, began questioning why Coal India's productivity was a fraction of global standards. The old guard's response—"This is India, not America"—rang increasingly hollow.

The technology gap had become a chasm. While Coal India still relied on the blast mining techniques of the 1970s, global competitors were using GPS-guided excavators, automated haul trucks, and real-time production monitoring. A single Australian mine could produce more coal with 500 workers than an Indian mine with 5,000. The comparison was so embarrassing that Coal India stopped participating in international mining conferences.

Environmental pressures, dormant during the socialist years, suddenly mattered in the globalized economy. International buyers began demanding environmental clearances, quality certifications, and safety standards that Coal India had never bothered with. The company discovered, to its horror, that being a monopoly was poor preparation for being competitive.

Labor relations evolved in unexpected ways. The unions, sensing existential threat from privatization talks, became paradoxically more cooperative. Strikes decreased from dozens annually in the 1980s to just a handful by the late 1990s. Productivity actually improved marginally—not from technology or training, but from fear. Workers understood that the worse Coal India performed, the stronger the case for privatization became.

The first private power plants exposed Coal India's quality crisis starkly. These plants, built with modern technology and international financing, required consistent, high-quality coal. Coal India's product—varying wildly in calorific value, moisture, and ash content—caused repeated breakdowns. Some private operators began importing coal from Indonesia and Australia, paying premium prices rather than rely on Coal India's erratic supplies.

Competition fears dominated boardroom discussions. Even now, Coal India Limited (CIL) and its subsidiaries continue to hold a strapping monopoly over the coal sector in India with a massive 80 percent of the total market share. But monopoly market share meant nothing if customers were fleeing to imports. The company tried various reforms—quality monitoring systems, customer complaint cells, even a short-lived attempt at branding different grades of coal. Nothing worked because the fundamental problem wasn't systems but culture—decades of monopolistic thinking couldn't be wished away.

The Asian Financial Crisis of 1997 provided unexpected breathing room. As Southeast Asian economies crashed, coal prices plummeted globally. Suddenly, Coal India's inefficiencies seemed less pressing compared to the economic chaos elsewhere. The reform momentum stalled. Politicians who had tentatively supported privatization now argued that public sector companies were stability anchors in turbulent times.

By 1999, a new dynamic had emerged. Successful liberalisation of the mining sector is contingent upon the liberalisation of the coal sector, which is the largest mining sector and is still being effectively controlled. Only after the liberalisation of the coal sector, larger private participation could be feasible, which in turn would reduce the cost of production and improve efficiency by introducing the state of the art technologies. The liberalisation of the coal sector is also important from the point of view of growing energy needs of India.

The Y2K transition passed without the predicted catastrophes, but it marked a psychological shift. Coal India had successfully computerized its operations—proof that change, however slow, was possible. Young officers, recruited through competitive examinations, began occupying middle management positions. They brought spreadsheets to organizations that had operated on ledgers, email to companies that relied on physical files, and questions to institutions that had survived on inertia.

As the millennium approached, Coal India found itself in a peculiar position. It remained a monopoly but felt besieged. It was profitable on paper but hemorrhaging talent to the private sector. It controlled 85% of Indian coal production but watched helplessly as imports grew yearly. The company was too big to fail but too important to ignore.

The 1990s hadn't privatized Coal India, but they had privatized the conversation around it. Economic efficiency, shareholder value, and global competitiveness—concepts alien to the socialist era—now dominated discussions. The question was no longer whether Coal India needed to change, but how much change its political masters would allow.

The new millennium would bring new pressures—explosive economic growth that would strain coal supplies, environmental movements that would question coal's future, and eventually, a government bold enough to take Coal India public. But first, the company would experience its golden decade, riding the commodity boom to heights that would have seemed impossible during the dark days of 1991.

VI. The 2000s Transformation: From Navratna to IPO (2000-2010)

The new millennium began with India's GDP growth accelerating past 6%, then 7%, then incredibly touching 9%. Every percentage point of growth demanded more electricity, more steel, more cement—and all of it needed coal. Between 2000 and 2010, India's coal demand would nearly double from 350 million tonnes to over 650 million tonnes. Coal India, despite its monopoly, found itself racing to keep pace with an economy suddenly unleashed.

The infrastructure bottleneck revealed itself immediately. Coal India could mine the coal, but getting it to power plants became the crisis. The Indian Railways, creaking under decades of underinvestment, simply couldn't move enough wagons. Power plants in Tamil Nadu and Karnataka sat idle while coal piled up at pitheads in Orissa and Chhattisgarh. The absurdity peaked in 2003 when India simultaneously had 30 million tonnes of coal stuck at mines and was importing 20 million tonnes to feed coastal power plants.

Railway capacity became Coal India's obsession. The company began investing billions in railway sidings, convinced that production meant nothing if the coal couldn't reach customers. Between 2000 and 2010, Coal India would spend over ₹5,000 crores on railway infrastructure alone—more than it had invested in the previous two decades combined. The First Mile Connectivity projects, though unglamorous, would prove more transformative than any mining technology.

The Navratna recognition came on May 3, 2006, a validation that seemed overdue. Coal India joined an exclusive club of just nine public sector enterprises granted enhanced autonomy. The designation brought real power—the ability to invest up to ₹1,000 crores without government approval, enter joint ventures, and most importantly, set its own HR policies. For a company long strangled by bureaucratic oversight, it was like being handed oxygen after decades of suffocation.

The autonomy immediately showed results. Coal India began poaching talent from private sector mining companies, offering salaries that would have been unthinkable in the socialist era. Young MBAs from IIMs, previously headed straight to investment banks, suddenly considered Coal India a viable career option. The company launched ambitious expansion plans, targeting 500 million tonnes production by 2012.The financial trajectory was remarkable. Coal India produced 554.14 million tonnes of raw coal in 2016–17 and earned revenue of ₹95,435 crore, representing a dramatic increase from earlier periods. This growth wasn't just about volume—it was about building the financial muscle that would make the upcoming IPO attractive to investors.

Internal reforms accelerated after 2005. Performance-related pay was introduced, shocking a workforce accustomed to automatic annual increments. The company began benchmarking operations against international standards, even if meeting them remained aspirational. Management information systems were upgraded, bringing real-time production data to decision-makers who had previously relied on month-old reports.

The cash accumulation was staggering. By 2009, Coal India sat on reserves exceeding ₹30,000 crores, earning more from treasury operations than some subsidiaries made from mining. The irony wasn't lost on observers—a company created to serve socialist goals had become one of India's most profitable enterprises. The cash pile created its own problems. The government viewed it as a piggy bank for fiscal deficit reduction. Unions demanded higher wages and benefits. Equipment suppliers inflated prices knowing Coal India could pay. The decision to take Coal India public crystallized in early 2010. The government faced mounting fiscal pressure, with the deficit ballooning after the 2008 financial crisis response. Coal India's cash-rich balance sheet and monopoly status made it the perfect candidate for what would become India's largest-ever IPO. The political calculation was delicate—the government needed the money, but couldn't be seen as privatizing the family silver.

VII. The Blockbuster IPO: India's Biggest Public Offering (2010)

In October 2010, the Government of India made an initial public offering (IPO) of 10% of the equity shares of CIL (631.6 million equity shares) to public at an offer price of ₹245 per share (at face value of ₹ 10 per share). The IPO was oversubscribed by 14.17 times. The numbers were staggering by any measure—₹15,199 crores raised in what would become India's largest-ever public offering, a record that would stand for years.

The pricing debate consumed months of preparation. Investment bankers from Citigroup, Morgan Stanley, and Bank of America Merrill Lynch argued for aggressive pricing, citing Coal India's monopoly position and massive reserves. The government, wary of political backlash if the IPO flopped, pushed for conservative pricing. CIL's IPO, which closed on October 21, was subscribed 15.17 times, and mopped up Rs 2.35 lakh crore.

The employee reservation became a flashpoint. The unions were assured at the time of CIL's IPO in 2010 that there would be no further disinvestment. This promise, extracted through threats of strikes and political pressure, would haunt the government when it attempted further stake sales. The reservation of 63.16 million shares for Coal India's 400,000 employees at a 5% discount was both a sweetener and a political necessity.

The roadshows revealed global appetite for India's growth story. "The response from the investors' community was overwhelming in all cities we visited, like London, Los Angeles, Sidney and Singapore," Coal India's chairman reported. International investors saw past the inefficiencies to the fundamental reality—India needed coal, and Coal India controlled the supply.

The anchor investor controversy nearly derailed the offering. State-run Coal India may scrap allotment under anchor investor plan of its mega initial public offering, as the government feels the selection of such investors - in case their demand for the issue exceeds the limit - may not be transparent. "This is something which the government is not comfortable with, as the process of selection of such investors may not be transparent." The government's solution was typically bureaucratic—eliminate the anchor investor portion entirely rather than risk accusations of favoritism.

The government on Monday fixed Coal India's IPO price at Rs 245 per share, the upper end of the range. The government will fetch Rs 15,100 crore by selling 631.6 million shares, or 10 per cent stake, at Rs 245 per share. The aggressive pricing reflected confidence built during the book-building process, where institutional demand far exceeded expectations.

Listing day, November 4, 2010, saw pandemonium at the exchanges. The stock opened at ₹342, a 40% premium to the IPO price. Within minutes, Coal India's market capitalization exceeded ₹2.16 lakh crores, making it India's fourth most valuable company overnight. Retail investors who had received allocations through the lottery system celebrated windfalls. The grey market premium, which had touched ₹100 before listing, proved conservative.

The IPO's success reverberated beyond financial markets. It validated the government's disinvestment strategy, proving that public sector companies could attract serious investor interest. For Coal India, it meant unprecedented scrutiny—quarterly earnings calls, analyst coverage, and shareholder activism were alien concepts for a company accustomed to operating as a government department.

The transformation was immediate and jarring. Coal India now had to produce quarterly results, respond to analyst queries, and justify operational decisions to shareholders beyond just the government. The company discovered that public markets were less forgiving than political masters. When production targets were missed, the stock price reflected disappointment instantly, unlike the previous era when such failures resulted in, at worst, a parliamentary question months later.

VIII. Maharatna Status & Peak Performance (2011-2014)

In April 2011, CIL was conferred the Maharatna status by the Government of India, making it one of the seven companies with that status. The timing couldn't have been better—fresh from IPO success, Coal India entered its golden age with unprecedented autonomy and soaring commodity prices.

The Maharatna designation brought powers that previous generations of Coal India executives could only dream about. Investment decisions up to ₹5,000 crores could be made without government approval. Joint ventures, even international ones, could be pursued at board discretion. Most importantly, the company could finally set competitive salaries for senior management, stemming the talent exodus to private sector.CIL was included in the 30-member BSE SENSEX on 8 August 2011. This inclusion in India's most prestigious stock index validated Coal India's transformation from government department to blue-chip company. The psychological impact was immense—Coal India now rubbed shoulders with Reliance, Infosys, and HDFC Bank in the index that defined Indian markets. The international recognition was equally impressive. For 2012, CIL earned a ranking of 48 on overall global performance in the 'Platts Top 250 Global Energy Company Rankings'—remarkable for a company that had been public for barely two years. CIL features on the Forbes Global 2000 rankings for 2012 at position 377. These rankings mattered beyond prestige—they attracted international investors who saw Coal India as a proxy bet on India's growth story.

The production momentum during this period was unprecedented. From a base of around 430 million tonnes in 2010, Coal India pushed toward the 500 million tonne mark, driven by both increased mechanization and sheer expansion of mining areas. Open cast mining, which accounted for over 90% of production, allowed for rapid scaling that underground operations could never match.

Financial performance reached dizzying heights as global commodity prices soared. Coal prices, both domestic and international, hit record levels driven by China's insatiable demand and supply constraints worldwide. Coal India's regulated pricing model meant it couldn't fully capture the upside, but even the modest price increases translated to massive profit gains given the volume.

The cash generation machine went into overdrive. By 2014, Coal India's cash reserves exceeded ₹50,000 crores, creating its own set of problems. The government viewed this cash pile with increasing interest, demanding special dividends to shore up fiscal deficits. Shareholders complained about capital allocation, arguing the company should either invest aggressively or return cash. Coal India, caught between political masters and market expectations, tried to do both, often satisfying neither.

Infrastructure development during the Maharatna years laid the foundation for future growth. The company invested heavily in railway sidings, crushing plants, and coal handling facilities. These unglamorous investments wouldn't show immediate returns but would prove critical when production targets escalated further in subsequent years.

Labor relations, surprisingly, stabilized during this golden period. The prosperity allowed Coal India to be generous with wage settlements, buying peace with its 300,000-strong workforce. Productivity per worker improved marginally, though it remained a fraction of global standards. The unions, sensing good times, moderated their demands, understanding that killing the golden goose served no one's interests.

CSR initiatives multiplied as Coal India embraced its role as a corporate citizen. Schools, hospitals, and community centers sprouted in mining areas. The company planted millions of trees, attempting to offset its environmental footprint. Critics dismissed these as greenwashing, but for communities dependent on Coal India, these investments represented real improvements in quality of life.

The period also saw ambitious international forays. Coal India explored opportunities in Australia, South Africa, and Indonesia, seeking to secure coking coal assets that India desperately lacked. Most of these ventures would ultimately fail, victims of poor due diligence, political opposition, and Coal India's inability to operate effectively outside its home turf. But in 2011-2014, with commodity prices soaring and India's growth story intact, anything seemed possible.

Technology adoption accelerated, driven by younger managers who understood that Maharatna status meant competing with global peers. GPS-enabled trucks, real-time production monitoring, and computerized dispatch systems were introduced. The changes were incremental rather than revolutionary, but they represented a significant shift from the technological stagnation of previous decades.

Environmental challenges, dormant during the socialist era, suddenly mattered. In September 2011, CAG criticised of for operating 239 mines in seven coal producing subsidiaries, which existed prior to 1994, without environmental clearance. These mines included 48 open-cast, 170 underground and 21 combined mines. In its report, the CAG also pointed out that of the 18 sample open-cast and eight underground mines, ten mines had undertaken capacity expansion without environmental clearances. The company, in its reply, said that applications for clearances to the projects have already been submitted to the Ministry of Environment and Forests.

Safety metrics improved during this period, though they remained poor by global standards. CIL reported lowest ever figures of average 66 deaths and 251 serious accidents per year for the period 2010–2012, indicating that safety at workplace is improving over the years. Critics argued these figures underreported actual casualties, but even the official statistics represented progress from the horrific safety record of earlier decades.

The Maharatna years represented Coal India at its most confident. Flush with cash, recognized globally, and operating with unprecedented autonomy, the company seemed to have transcended its socialist origins to become a genuine corporate powerhouse. Stock analysts issued bullish reports, institutional investors accumulated positions, and the financial media celebrated Coal India as a successful privatization story.

But storm clouds were gathering. In 2012, the Comptroller and Auditor General of India released a report that would shake the foundations of India's coal sector. The "Coalgate" scandal was about to erupt, and Coal India, despite not being directly implicated, would find its world transformed. The golden age was ending, though few recognized it at the time.

IX. The Coal Scam Earthquake & Aftermath (2012-2015)

The Comptroller and Auditor General's report, released in August 2012, landed like a bomb in India's political landscape. The headline number was staggering: ₹1.86 lakh crore—the estimated loss to the exchequer from allocating coal blocks without competitive bidding between 1993 and 2009. While Coal India wasn't directly accused, the scandal would reshape the entire coal sector and end the company's comfortable monopoly forever.

The CAG's logic was simple but devastating. By giving away coal blocks through a screening committee process rather than auctions, the government had foregone potential revenues. Private companies had received windfall gains from coal blocks allocated at negligible cost. The report noted that while Coal India paid royalties and taxes on every tonne extracted, private players with captive blocks enjoyed massive economic benefits without corresponding payments to the public exchequer. Political theatre erupted immediately. The opposition demanded Prime Minister Manmohan Singh's resignation, noting that he had held the coal portfolio during the critical 2006-2009 period. The CBI launched investigations into coal block allocations, raiding offices and questioning politicians and businessmen. The image of India's most powerful industrialists being summoned for questioning became a defining visual of the era.

Coal India watched from the sidelines with mixed emotions. The company wasn't directly implicated—it hadn't received any of the controversial allocations. But the scandal tarnished the entire coal sector's reputation. More importantly, the inevitable reforms would end Coal India's comfortable monopoly, introducing competition that the company had successfully avoided for four decades.

In September 2014, the Supreme Court declared all allocations of coal blocks, made through the Screening Committee and through Government Dispensation route since 1993, as illegal. It cancelled the allocation of 204 out of 218 coal blocks. The judgment was stunning in its sweep—decades of allocations wiped out in a single order. The court noted that blocks were allocated by the inter-ministerial screening committee in a non-transparent manner to private parties for captive mining due to which "common good" and "public interest" had "suffered heavily".

The immediate impact was chaos. Companies that had invested billions in developing coal blocks suddenly found their assets worthless. Power plants built assuming captive coal supply faced fuel uncertainty. Banks that had lent against these projects stared at massive non-performing assets. The operational companies were asked to pay a fine of Rs 295 for every tonne of coal mined since they started producing—a penalty that would run into thousands of crores for some.

For Coal India, the crisis was also an opportunity. With private coal supply disrupted, the company became even more critical to India's energy security. Production targets were raised urgently. Coal India's unions, sensing their increased importance, extracted generous wage settlements. The stock price, after initial volatility, actually strengthened as investors realized Coal India would benefit from supply disruptions.

The political fallout was severe. The UPA government's credibility, already battered by corruption scandals, took another hit. CBI launches investigations, multiple politicians and business leaders questioned and charged. The coal scam became a defining issue in the 2014 general elections, contributing to the Congress party's historic defeat. The government's response came through the Coal Mines (Special Provisions) Act, 2015, which introduced auction-based allocation system. The Act was designed to reallocate coal mines through a transparent auction process, promote optimal utilisation of coal resources, and encourage private sector participation in coal mining activities. This legislation represented a fundamental shift—from discretionary allocation that had enabled corruption to transparent auctions that would maximize government revenue.

For Coal India, the implications were profound. The company would no longer enjoy de facto monopoly over commercial coal mining. Private players could now mine and sell coal commercially, competing directly with Coal India in the market. The comfortable world of administered pricing and guaranteed market share was ending. The government's immediate response was another divestment. On 30 January 2015, in an offer for sale (OFS), Government of India sold a further 10% stake in CIL. Priced at ₹358 per share, the sale fetched the government ₹22,557.63 crore, making it the largest ever equity offering in the Indian share market. The timing was politically motivated—the government needed to shore up finances to meet its fiscal deficit target while demonstrating that reforms continued despite the coal scam fallout.

The OFS mechanism represented a stark contrast to the 2010 IPO. Where the IPO had been a celebration of Coal India's transformation, the 2015 stake sale felt transactional, even desperate. Insurance giant Life Insurance Corporation (LIC) was the biggest investor, with investment of around Rs 8,000 crore. The heavy participation by government-owned institutions raised questions about whether this was genuine market demand or orchestrated support.

Union resistance to the stake sale was fierce but ultimately ineffective. The workers had been promised during the 2010 IPO that no further divestment would occur. This broken promise deepened distrust between management and labor, setting the stage for more confrontational relations in coming years. The unions threatened strikes but ultimately backed down, recognizing that disrupting operations when Coal India was under scrutiny would be counterproductive.

The coal scam's most lasting impact was ending Coal India's monopoly. With the new auction regime in place, private companies could now mine coal commercially. The first auctions in 2015 saw aggressive bidding, with some blocks going for premiums that shocked even the government. Private players, freed from decades of restriction, were eager to enter the sector.

Coal India's response to competition was mixed. On one hand, the company accelerated modernization plans, recognizing that operational efficiency was no longer optional. On the other hand, decades of monopolistic thinking couldn't be wished away overnight. Many within Coal India believed private miners would struggle with India's complex mining environment and eventually fail, leaving Coal India to pick up the pieces.

The period also saw significant leadership changes. A new generation of technocrats took charge, understanding that Coal India needed fundamental transformation, not cosmetic changes. Production targets were made more realistic, technology adoption accelerated, and customer service—long an oxymoron at Coal India—became a focus area.

Environmental pressures intensified during this period. The Paris Climate Agreement of 2015, though not directly targeting Coal India, created a global context where coal was increasingly seen as problematic. International investors began questioning exposure to coal assets. Some global funds divested from Coal India, citing ESG concerns. The company that had been celebrated during its IPO was becoming a pariah in environmentally conscious investment circles.

The financial performance during 2012-2015 remained robust despite the turmoil. Coal India's monopolistic market position, even if weakening, still generated substantial cash flows. The company continued paying hefty dividends, with the government as the primary beneficiary. This cash generation ability would prove crucial as Coal India faced its next challenge: the opening of commercial mining to private players.

By 2015's end, Coal India stood at a crossroads. The coal scam had shattered the old certainties. The monopoly was ending. Environmental pressures were mounting. Yet the company remained indispensable to India's energy security, producing over 80% of domestic coal. The question was whether Coal India could transform from a socialist-era monopoly into a competitive, modern mining company. The next phase would provide the answer.

X. Competition Era & Commercial Mining (2015-2020)

March 2015 marked the beginning of Coal India's most fundamental transformation since nationalization. The Coal Mines (Special Provisions) Act, 2015 was passed by the Parliament which was notified as an Act on 30.03.2015. For the first time in four decades, private companies could mine coal not just for captive use but for commercial sale. The monopoly that had defined Coal India since 1975 was officially dead. The watershed moment came with unprecedented clarity. The Coking Coal Mines (Nationalization) Act, 1972 and the Coal Mines (Nationalization) Act, 1973 were repealed by the Repealing and Amending (Second) Act, 2017 on 8 January 2018. On 20 February 2018, the Cabinet Committee on Economic Affairs permitted private firms to enter the commercial coal mining industry. The monopoly that had defined Coal India for 45 years was legally terminated.

The initial response within Coal India was denial mixed with defiance. Many executives believed private miners would fail, unable to navigate India's complex regulatory environment, challenging geology, and politically powerful unions. "Let them try mining in Jharia with its underground fires," scoffed one senior manager. "They'll come running back in two years."

But the private sector's entry was more sophisticated than Coal India anticipated. Companies like Adani, Vedanta, and JSW brought international expertise, modern equipment, and most importantly, a hunger that Coal India had lost decades ago. They cherry-picked the best deposits, employed cutting-edge technology, and offered wages that lured away Coal India's best engineers and geologists.

The competitive pressure forced Coal India into uncharacteristic action. Technology modernization, discussed for decades, suddenly became urgent. The company began deploying high-capacity equipment, continuous miners, and automated systems. Productivity metrics, long ignored, became board-level discussions. Customer service centers were established, a concept that would have been laughable in the monopoly era. Production achievements during this period validated Coal India's resilience. FY 2019: Coal India breaches 600 MT mark, producing 606.89 MT - leap from 500 to 600 MT in just three years. This achievement, coming amid competition fears, demonstrated that Coal India could still deliver when pushed. The company's sheer scale—over 400 mines, 300,000 employees, vast reserves—remained formidable advantages that private players couldn't quickly replicate.

Labor dynamics evolved significantly during 2015-2020. The unions, recognizing that competition threatened not just wages but jobs themselves, became more cooperative on productivity improvements. Voluntary retirement schemes were introduced, reducing the workforce while avoiding confrontation. Younger workers, seeing opportunities in the private sector, began viewing Coal India employment differently—no longer a lifetime sinecure but a stepping stone.

The environmental narrative intensified dramatically. Climate activists targeted Coal India as a symbol of India's fossil fuel addiction. Protests at mine sites became common. International media coverage was uniformly negative. The company's attempts at greenwashing—tree planting, renewable energy investments—were dismissed as inadequate. For the first time, Coal India executives had to defend not just operational performance but the company's very existence.

Financial performance remained robust despite headwinds. Coal India continued generating substantial cash, paying hefty dividends, and funding government fiscal needs. But investors began questioning long-term viability. ESG funds divested. Some analysts initiated coverage with "sell" recommendations, citing stranded asset risks. The stock price, while supported by dividend yield, underperformed broader markets.

Technology adoption accelerated under competitive pressure. Mine planning software, previously resisted as threatening jobs, was rapidly deployed. Drone surveys replaced manual measurements. IoT sensors monitored equipment performance. The digital transformation, forced by competition, achieved more in five years than previous decades of government exhortation.

International ventures, long discussed, finally materialized—though mostly unsuccessfully. Coal India's attempts to acquire mines in Australia, Indonesia, and Mozambique foundered on cultural mismatches, regulatory hurdles, and lack of international operating experience. The company discovered that its India-specific expertise didn't translate globally.

The COVID-19 pandemic in early 2020 created unprecedented challenges. Mines operated with skeleton crews. Migrant workers fled. Production plummeted. Yet the crisis also demonstrated Coal India's essential nature—when power plants ran low on coal, threatening blackouts, Coal India's ability to rapidly ramp up production proved irreplaceable.

By 2020's end, Coal India stood transformed yet unchanged. The monopoly was gone, but market dominance remained. Private competition existed but hadn't yet significantly eroded market share. Technology adoption had accelerated, but productivity still lagged global standards. The company had survived its first real competition, but greater challenges loomed as India grappled with energy transition and climate commitments.

XI. The Modern Giant: Scale, Operations & Challenges (2020-Present)

The pandemic's arrival in March 2020 found Coal India uniquely vulnerable. With 239,210 employees spread across 322 mines in 83 mining areas across 8 states, coordinating response to a respiratory pandemic in dusty, crowded mining environments seemed impossible. Yet the crisis would catalyze changes that decades of reform attempts hadn't achieved.

Production initially crashed as lockdowns halted operations. But Coal India's designation as an essential service meant rapid restart. The company implemented digital monitoring, contactless operations, and health protocols with surprising efficiency. By mid-2020, production had recovered, demonstrating operational resilience that surprised critics who had written off the PSU as a lumbering dinosaur.

The post-pandemic period saw unprecedented production push. FY 2024: Achieves 78% of production target in just 10 months. India's achievement of crossing 1 billion tonnes in coal production in March 2025 marked a historic milestone, with Coal India contributing the lion's share. This production surge came despite increasing competition, environmental pressures, and workforce challenges. Financial performance remains robust despite operational challenges. Q3FY25: Net profit rises 3.54% to ₹9,646.26 crore, though this represents volatility quarter-to-quarter. The company continues generating substantial cash, maintaining its position as one of India's most profitable PSUs. Dividend payments remain generous, with the government as primary beneficiary—a crucial source of non-tax revenue for fiscal management.

The Mine Developer Operator (MDO) model emerged as Coal India's attempt to boost production without adding employees. Private contractors operate mines while Coal India retains ownership. The model promises efficiency gains but has sparked controversy over contract terms, profit-sharing arrangements, and concerns about backdoor privatization. Unions view MDOs suspiciously, seeing them as the thin edge of the outsourcing wedge.

Environmental pressures have intensified exponentially. International climate commitments, domestic air pollution crises, and renewable energy's improving economics create an existential challenge. Coal India has responded with token investments in solar power and coal gasification, but these remain marginal to core operations. The company finds itself in an impossible position—criticized for mining coal yet essential for keeping lights on.

Technology adoption has accelerated dramatically post-2020. Digital twins of mines enable better planning. AI-powered predictive maintenance reduces equipment downtime. Drones survey areas previously requiring weeks of manual measurement in hours. The irony is palpable—Coal India is becoming a high-tech company just as its product faces obsolescence.

Labor relations have evolved toward uneasy cooperation. The workforce has declined through attrition and voluntary retirement to around 240,000. Younger workers, seeing limited future in coal, pursue opportunities elsewhere. The unions, recognizing existential threats, have moderated demands. Strikes are rare, productivity discussions more constructive. Yet underlying tensions remain—between efficiency and employment, between modernization and job security.

Commercial mining's impact is becoming visible. Private miners now produce over 100 million tonnes annually, though Coal India still dominates with 80% market share. The competition has improved Coal India's customer focus, operational efficiency, and cost consciousness. Yet fundamental challenges remain—legacy workforce, political interference, social obligations that private miners avoid.

Infrastructure development continues aggressively. Railway sidings, coal handling plants, and washeries receive billions in investment. The First Mile Connectivity projects aim to eliminate the truck transportation that adds cost and environmental damage. These investments, unglamorous but essential, position Coal India to maintain relevance even as competition intensifies.

International ventures remain minimal. Coal India's attempts to secure coking coal assets abroad have largely failed. The company lacks international operating experience, risk appetite, and cultural flexibility for global expansion. Its future remains tied to India's domestic energy needs.

The energy transition poses Coal India's greatest challenge. India has committed to net-zero by 2070, implying coal's eventual phase-out. Renewable energy costs have plummeted below new coal plant costs. International pressure to abandon coal intensifies yearly. Yet India's energy reality—massive demand growth, renewable intermittency, lack of alternatives—means coal remains essential medium-term.

Coal India's response has been schizophrenic. Publicly, it embraces energy transition, announcing solar investments and clean coal technologies. Privately, it banks on coal demand growing through 2040. The company invests just enough in alternatives to claim transformation while focusing on core coal operations. This hedging strategy reflects political reality—neither full commitment to coal nor genuine transition is politically viable.

As of late 2024, Coal India remains a paradox. It's a profitable company in a dying industry. A technological modernizer mining a nineteenth-century fuel. A commercial entity with social obligations. A climate villain that keeps India's lights on. These contradictions define Coal India's present and will determine its future.

XII. Playbook: Lessons from a State-Owned Giant

How to Operate a Monopoly Responsibly (and Irresponsibly)

Coal India's monopoly years offer a masterclass in both the benefits and perils of market dominance. The responsible elements included ensuring energy security, maintaining strategic reserves, and serving unprofitable markets that private players would abandon. The company kept power plants supplied during crises, subsidized coal for essential industries, and maintained employment in economically depressed regions.

The irresponsible aspects were equally instructive. Quality control was abysmal—customers received whatever Coal India produced. Innovation stagnated—why improve when customers have no choice? Customer service was non-existent—complaints went into black holes. The monopoly bred complacency that took decades to partially overcome. The lesson: monopolies can serve social purposes but require extraordinary governance to avoid decay.

The Paradox of Efficiency in a Socialist Framework

Coal India embodies the fundamental contradiction of expecting commercial efficiency from an organization designed for social objectives. Every efficiency drive crashed against political reality. Mechanization meant job losses—politically impossible. Mine closures for economic reasons faced violent protests. Performance-based promotion threatened patronage networks.

The company developed workarounds that satisfied no one but avoided crisis. Voluntary retirement schemes reduced workforce without confrontation. Outsourcing non-core activities improved efficiency while maintaining permanent employee numbers. Technology was introduced gradually, with extensive retraining to minimize resistance. The result was incremental improvement rather than transformation—perhaps the best possible outcome given constraints.

Managing 200,000+ Employees and Powerful Unions

Coal India's labor management offers lessons applicable far beyond mining. The company learned that confrontation with organized labor was pyrrhic—strikes cost more than wage increases. Instead, it developed sophisticated co-optation strategies. Union leaders were included in decision-making, creating stake in outcomes. Welfare measures—housing, healthcare, education—created dependency that moderated demands.

The company also mastered divide-and-rule tactics. Multiple unions were encouraged, preventing unified opposition. Regional differences were exploited. Contract workers, now nearly equal to permanent employees, were kept separate from union structures. These strategies maintained operational continuity but at the cost of genuine worker participation or productivity improvement.

Political Management as Core Competency

Coal India's survival required mastering political navigation across multiple levels. At the national level, this meant serving whichever party held power while maintaining bureaucratic neutrality. The company learned to frame every decision in terms of national interest—production targets became patriotic duties, losses became investments in energy security.

At state level, Coal India became adept at managing competing demands. State governments wanted employment, revenue, and development projects. The company provided all three, buying operational freedom. Local politicians were co-opted through CSR spending, contract allocation, and employment promises. This political management consumed enormous resources but was essential for operational continuity.

Capital Allocation in Government-Controlled Entity

Coal India's capital allocation reveals the constraints of state ownership. Investment decisions were political as much as economic. Unprofitable mines in politically important constituencies remained open. Technology investments were delayed if they threatened employment. Dividend payments to government often exceeded retained earnings needed for growth.

Yet within these constraints, Coal India developed sophisticated strategies. It built massive cash reserves during good years, providing buffer during political extraction. Investments were packaged as job creation or regional development to gain political support. The company learned to game the system—proposing inflated budgets knowing they'd be cut, slow-rolling politically motivated projects until governments changed.

The Challenge of Modernization with Employment Guarantees

Coal India's modernization attempts reveal the near-impossibility of technological transformation when job preservation is paramount. Every efficiency improvement was evaluated not on ROI but on employment impact. Automation was introduced only where it created new job categories offsetting those eliminated.

The company developed creative solutions. Technology was positioned as skill enhancement rather than replacement. Workers were retrained extensively, even if uneconomically. Productivity improvements came through better organization rather than workforce reduction. Natural attrition was maximized while hiring was minimized. These strategies achieved modest productivity gains while maintaining social peace.

Navigating Energy Transition While Being Fossil Fuel Company

Coal India faces an existential challenge few companies confront—its core product is increasingly seen as destructive. The playbook involves strategic ambiguity. The company acknowledges climate change while emphasizing coal's continued necessity. It invests in renewable energy while expanding coal production. It promotes "clean coal" technologies that marginally reduce emissions while maintaining coal centrality.

This balancing act requires sophisticated messaging. To government, Coal India emphasizes energy security and employment. To investors, it highlights cash generation and dividends. To environmentalists, it points to renewable investments and efficiency improvements. To workers, it promises gradual transition with protection. This multiple messaging is inherently unstable but necessary given contradictory stakeholder demands.

IPO and Divestment Execution for Government Companies

Coal India's IPO and subsequent stake sales offer templates for government divestment. Key lessons include: pricing below market ensures success but leaves money on table; retail reservation creates political support but reduces institutional demand; employee reservation buys union acquiescence but complicates allocation; anchor investors provide confidence but require transparency government is uncomfortable with.

The execution revealed that financial success doesn't equal political success. The IPOs raised record amounts but were criticized for underpricing. Foreign institutional investment was welcomed economically but criticized politically. The promise not to divest further, extracted by unions, constrained future flexibility. The lesson: government IPOs must balance multiple objectives beyond maximizing proceeds.

Building Operational Excellence Despite Bureaucratic Constraints

Coal India achieved operational improvements despite, not because of, its governance structure. Success came through working around constraints rather than removing them. Autonomous subsidiaries were created to escape headquarters bureaucracy. Joint ventures provided flexibility forbidden to the parent. Outsourcing achieved what direct employment couldn't.

Excellence emerged in pockets—specific mines, particular technologies, individual managers—rather than systematically. The company learned to celebrate these successes while tolerating broader mediocrity. Best practices were shared informally through networks rather than mandated through hierarchy. This organic improvement was slow but sustainable given political realities.

The playbook reveals that state-owned enterprises can achieve limited success through creative adaptation rather than fundamental reform. Coal India survived and sometimes thrived not by becoming a normal company but by mastering the abnormal environment of Indian PSU operation. These lessons—unsatisfying to free-market advocates and socialists alike—reflect the messy reality of managing public assets in democratic contexts.

XIII. Power Dynamics & Future Trajectory

Coal India vs. Private Miners: David Becomes Goliath's Competitor

The competitive landscape has inverted dramatically. Private miners, once begging for small allocations, now operate sophisticated mines rivaling Coal India's best. Adani has emerged as the most formidable competitor, leveraging its port infrastructure and power plant integration. The company produces over 100 million tonnes annually, approaching 15% of India's production.

But Coal India retains structural advantages private players struggle to replicate. Its 400+ mines provide diversification no private player matches. Existing infrastructure, built over decades, would cost hundreds of billions to replicate. Most importantly, Coal India's relationship with Indian Railways, built over 50 years, ensures evacuation capacity private miners struggle to secure.

The competition is evolving from confrontation to coexistence. Private miners cherry-pick profitable opportunities while Coal India maintains universal service obligations. This division of labor—private efficiency in select areas, public reliability across the board—may represent sustainable equilibrium rather than transitional phase.

India's Energy Security Dilemma: Coal Dependency Reality

India faces an energy trilemma—ensuring supply security, affordability, and sustainability simultaneously. Coal currently provides 70% of electricity generation, supporting base load that renewables can't yet replace. The math is sobering: India needs to add 400-500 GW of renewable capacity to replace coal, requiring investments exceeding $500 billion and land area equivalent to entire states.

Coal India sits at this trilemma's center. Reduce coal too fast, and India faces energy shortage threatening economic growth. Continue current trajectory, and climate commitments become impossible. The solution involves managed transition—Coal India providing bridge fuel while renewables scale. This positions Coal India as essential medium-term, even as long-term outlook darkens.

The Renewable Energy Transition Threat/Opportunity

Solar and wind costs have plummeted below coal for new capacity. Battery storage is approaching economic viability. Green hydrogen promises industrial heat without coal. These developments suggest coal's dominance will end, though timing remains uncertain.

Coal India's response has been tentative. Solar investments remain token relative to coal operations. Coal gasification projects proceed slowly. Carbon capture remains experimental. The company seems to be betting on transition taking decades, allowing gradual adaptation. This may prove correct—India's energy demand growth could require both maximum renewable deployment and continued coal use.

Import Substitution and Self-Reliance Goals

India imports 200+ million tonnes of coal annually despite massive domestic reserves. This reflects quality mismatch—Indian coal is high-ash, low-calorific compared to imports. Coal India is positioned as import substitution champion, aligning with government's self-reliance agenda.

But substitution faces geological reality. India lacks significant coking coal required for steel production. Coastal power plants designed for imported coal can't easily switch to domestic. Coal India's attempts to improve quality through washing have been marginally successful. Import substitution may prove more political slogan than achievable goal.

Technology Disruption: Automation, AI, and Workforce Implications

Mining technology is transforming globally. Autonomous haul trucks, AI-powered planning, and remote operations are becoming standard. Coal India faces the challenge of adopting these technologies while managing massive workforce.

The company is pursuing selective automation—deploying technology where it doesn't directly displace workers. AI is used for planning rather than operations. Automation targets greenfield sites rather than existing mines. This gradual approach avoids labor confrontation but risks Coal India falling further behind global productivity standards.

Environmental Litigation and Regulatory Pressures

Coal India faces escalating environmental challenges. The National Green Tribunal regularly halts operations for violations. Forest clearances take years. Local communities protest expansions. International climate litigation may eventually target Coal India directly.

The regulatory environment is tightening inexorably. Emission norms are strengthening. Water usage faces restrictions. Land acquisition has become nearly impossible. Coal India must operate within shrinking environmental space while maintaining production. This may prove unsustainable, forcing production decline regardless of demand.

The Geopolitics of Coal in Asia

Asian coal dynamics will determine Coal India's future. China, producing 4 billion tonnes annually, dominates global market. Indonesia and Australia control seaborne trade. India is increasingly isolated in expanding coal use while neighbors transition away.