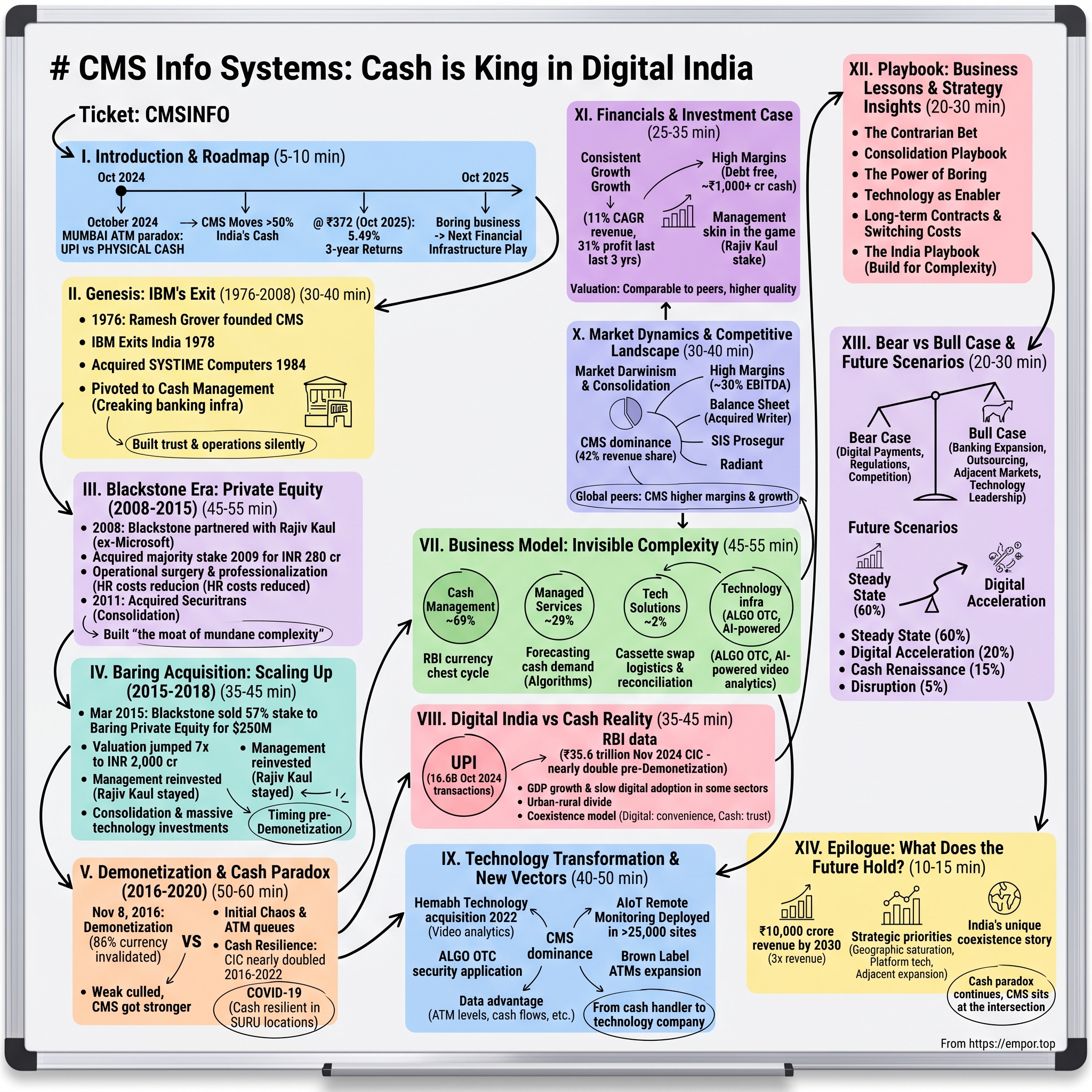

CMS Info Systems: Cash is King in Digital India

I. Introduction & Episode Roadmap (5–10 min)

The automatic glass doors of State Bank of India's flagship Mumbai branch slide open. It's 9:47 AM on a Tuesday morning in October 2024, and already a queue has formed at the ATM vestibule. A young software engineer withdraws ₹10,000 for his sister's wedding expenses. An elderly woman carefully counts ₹3,000 for her monthly medicines. A street vendor deposits the weekend's earnings through the cash recycler. Each transaction, seemingly mundane, is part of an extraordinary paradox: in an India racing toward digital payments supremacy—where UPI processes 16.6 billion transactions monthly—physical cash refuses to die.

Behind every one of these cash movements stands a company most Indians have never heard of, yet one that touches their lives daily. CMS Info Systems moves more than 50% of the cash in the entire country. Think about that for a moment. Every second rupee note that passes through an ATM, every other cash collection from a Big Bazaar store, every alternate currency chest movement between banks—CMS handles it.

The stock trades at ₹372 (as of October 2025), delivering 8.49% returns over three years—hardly the stuff of momentum investor dreams. Yet this understated performance masks one of Indian business's most fascinating contrarian stories. How does a company built entirely around physical cash not just survive but thrive in the age of digital payments? Why did cash in circulation nearly double after demonetization was supposed to kill it? And what happens when the boring, unsexy business of moving money becomes the foundation for India's next financial infrastructure play?

Today's journey takes us from a small computer maintenance shop in 1976 Mumbai to India's cash management behemoth. We'll explore how three private equity transformations, one demonetization shock, a global pandemic, and the world's most successful digital payment revolution all somehow made CMS stronger. We'll decode why currency in circulation at ₹35.6 trillion in November 2024 stands at nearly double the demonetization era amount, despite every prediction to the contrary.

This is the story of how Ramesh Grover's accidental entrepreneurship became Blackstone's masterclass in operational transformation, how Rajiv Kaul's Microsoft pedigree met India's cash reality, and why betting against cash in India might be the most expensive mistake an investor can make. It's a tale of consolidation in chaos, technology enhancing tradition, and the power of solving problems others find too mundane to notice.

Buckle up. We're about to discover why, in the world's fastest-growing digital economy, cash remains king—and why the company managing that crown might be sitting on India's most underappreciated business moat.

II. Genesis: From IBM's Exit to India's Cash Backbone (1976–2008) (30–40 min)

In 1976, Ramesh D. Grover and two friends saw an opportunity. It was the height of business xenophobia in Delhi with multinational companies in the cross hairs of then industries minister George Fernandes's sights. With International Business Machines, better known as IBM, set to exit India over new foreign exchange rules, the techies eyed maintaining IBM machines the company was leaving behind in India.

Picture the scene: India's socialist fervor at its peak, foreign companies fleeing, and three IBM engineers staring at an industrial graveyard of abandoned mainframes. Grover was born in Lahore in 1945. His father worked in the Northern Railways. Though he was young during the Partition, he remembered the chaos. His father had just bought a house in Lahore when riots broke out over Punjab. They had to move to India with nothing but their clothes. This childhood of displacement would paradoxically prepare him for a career built on creating stability from chaos.

After Grover graduated in 1966, he came to Mumbai to look for a job. IBM was already a big name, and he dreamt of working there. His first job, though, was for L&T, where he worked for six months before IBM offered him a job. He joined them at a princely salary of 600 per month, and stayed on for 13 years. At IBM, he was known as the man who could fix any machine.

But Grover wasn't a natural entrepreneur. Far from it. No one in his family had been in business—it signified risk. He preferred the comfort of a job. The NRI group convinced him by agreeing to pay him five years' salary, irrespective of what happened to the firm. In August 1976, he started CMS. He convinced two IBM colleagues to join. They were India's first computer maintenance firm.

The name choice itself tells you everything about Grover's accidental entrepreneurship. Grover decided to call their venture Computer Maintenance Services or CMS - almost similar to its state-owned rival Computer Maintenance Corporation, which won most of IBM's maintenance work channelled its way because most of IBM's customers were government agencies or companies. He had no idea what to call them, so he thought of a simple name, Computer Maintenance Services. None of them knew then that it would be such a large organisation in three decades. He could confess that he was convinced he would have to go back to a regular job after five years. Fate obviously had other plans.

In 1978, IBM left India completely. Suddenly, CMS found itself as one of the only games in town for maintaining the sophisticated computer systems that Indian companies had grown dependent on. The small set-up, 'Computer Maintenance Services', rapidly grew from a maintenance and outsourcing firm to a diversified conglomerate serving the IT and ITES needs of Indian and global enterprises in India.

CMS grew by leaps and bounds as it acquired accounts from companies like Philips, ACC, Premier Automobiles and Union Carbide for their maintenance business. The company wasn't just fixing computers anymore—it was becoming India's IT backbone during the pre-liberalization era when foreign technology companies were persona non grata.

In 1984, CMS acquired Europe-based SYSTIME computers and became India's first end-to-end IT solutions company. This was audacious. Here was a company born from IBM's forced exit, now acquiring European firms and bringing technology back to India through the back door. Given this new start, the restless Grover expanded the business to areas like smart cards, traffic signals, printing systems, cash management and ERP.

The cash management pivot didn't happen overnight. It emerged from a simple observation: banks were drowning in paper and physical logistics. India's banking infrastructure in the 1990s was creaking under the weight of economic liberalization. New private banks were launching, ATMs were being deployed, but nobody had figured out the unglamorous backend—how do you actually move, count, sort, and secure billions of rupees in physical currency across a subcontinent?

Aarti Grover, current Managing Director, CMS computers, and daughter of Ramesh Grover, says "The key to what makes CMS different is an insight into customer need. For core infrastructure services, India had the need but didn't have 'Indian prices'. So my father created three R&D centers across the country in Pune, Bombay and Trivandrum, where we created products and innovated".

By the early 2000s, CMS had quietly built relationships with every major bank in India. They weren't the sexiest vendor—that honor went to the software companies building core banking systems. But when a bank needed someone to ensure their ATMs never ran dry, their branches reconciled perfectly, and their cash moved securely, they called CMS.

As an entrepreneur, Grover had always gone with his gut instinct. There had been failures, but that's what business is about. His biggest weakness was that he was not a commercially-minded man. It probably sounds ridiculous. But he was sure they would have grown 10 times faster had he been more 'business minded'. It's not like they lost contracts or deals. But he didn't have the unending appetite for growth that other Indian entrepreneurs had shown.

This self-deprecating assessment from Grover masks a profound truth: sometimes not being "business-minded" is exactly the right strategy. While aggressive entrepreneurs were chasing the next hot sector, Grover was methodically building switching costs and operational moats in the most boring business imaginable. By 2008, CMS had become indispensable to India's banking system. You couldn't see it, touch it, or understand it unless you worked in banking operations. But try running India's cash economy without it.

CMS served over thousands of customers and had more than 4,000 employees with 100 offices in India and the company's relationship with pioneering firms of various industries spanned decades. The stage was set for the next act—one that would require a very different kind of leadership. The comfortable family business was about to meet the sharp edge of private equity, and Ramesh Grover was about to hand over his life's work to the suits from Blackstone.

III. The Blackstone Era: Private Equity Transformation (2008–2015) (45–55 min)

The Oberoi hotel conference room in Mumbai, December 2008. The city still bore fresh wounds from the 26/11 attacks just weeks earlier. In this atmosphere of uncertainty, an unlikely partnership was being forged. Private equity firm Blackstone partnered with former Microsoft India CEO Rajiv Kaul and together they convinced the promoters of CMS Group, one of the largest IT infrastructure businesses in the country, to give up its majority stake.

CMS Info Systems was formed in 2009 following an investment by the Blackstone Group to acquire majority stake in certain key businesses of CMS Computers. This wasn't just a financial transaction—it was corporate surgery. Blackstone and Kaul carved out CMS Info Systems from CMS Group to build capabilities to tap the huge IT infrastructure and managed services potential in the country.

The numbers tell only part of the story. The Blackstone Group, in collaboration with Mr. Rajiv Kaul (ex-CEO of Microsoft India), invested in 2009 with the goal of acquiring the majority ownership (53%) in CMS for INR 280 cr. Blackstone reportedly paid approximately $65 million for the acquisition, with the Grover family retaining a significant minority stake.

But who was this Rajiv Kaul, and why did Blackstone bet on him to transform a three-decade-old family business?

Once the youngest managing director of Microsoft India—he had moved into the corner office at the age of 33 in 2001—Kaul is now the executive vice-chairman and chief executive officer of CMS Info Systems. Prior to Actis, he was with Microsoft Corporation for over 10 years. Rajiv joined Microsoft India in 1996 and in 2001 rose to become one of the youngest Country Managers at Microsoft and in corporate India.

He had a meteoric rise to become CEO of Microsoft India at the age of 33 and pioneered the early efforts for software consumption on subscription and prepaid models. During his tenure, Microsoft India business was the fastest growing globally and was the largest in emerging markets. Prior to CMS Info Systems, Rajiv made history as the youngest CEO of Microsoft India at just 33, and was instrumental in pioneering subscription-based software models in the country, well ahead of the curve.

Kaul partnered Blackstone after a two-year stint as a Partner with Actis LLP, another private equity and buyout fund. Blackstone was eyeing CMS for a while and Kaul was looking for a challenge.

The first order of business was brutal honesty about what CMS had become. As president and Chief Financial Officer Pankaj Khandelwal says, the company was privately-run with a decades-old culture. That needed to change. Earlier, the approach was of a responsive organisation; based on relationships. Today, it is a much broader professional organisation. What this means is empowerment and professionalism among the employees and the service at CMS.

The operational transformation was surgical and systematic. Kaul didn't come in with a machete—he came with a scalpel and a blueprint. CMS managed to pull in Sudev Muthiya from Microsoft to head the information technology (IT) business. Raja Roy, who was with HCL Infosystems, heading its institute business, was now spearheading CMS Institute Systems. Anand Sunderesan quit HCL Technologies and took over the role of vice-president, Sales.

The impact on operational metrics was immediate and dramatic. Between 2009 and 2014, HR costs as a percentage of revenue dropped from 65% to 50%. This wasn't about firing people—it was about technology leverage and operational efficiency. The company built proprietary software for cash tracking that eliminated thousands of manual reconciliation hours. Routes were optimized using algorithms instead of intuition. Cash forecasting moved from Excel sheets to predictive analytics.

CMS has a unique strength which not many companies in India have. And that is what attracted me when we did this investment three years ago—it is CMS' massive reach and presence in the country. Today, we have around 23,000 people working for us. We have our own offices in 120 towns and cities; and we have our people based in, say, 800 more towns. Reach is a great strength. In India, there is the last mile for everything. If you build it—it takes time and money—you have a unique asset. CMS has that unique asset.

But the real genius of the Blackstone-Kaul partnership wasn't in cost-cutting or hiring. It was in recognizing that CMS's boring business was actually a platform with enormous operating leverage. The centre point of CMS' business today is other people's risk. For an economy its size, India deals extensively in cash and cash is at risk from multiple fronts. There are possibilities of heists and robberies, and more mundane issues of counterfeit currency, bottlenecks in delivering cash and faulty ATMs.

In 2011, came the move that would define CMS's trajectory: CMS Info Systems acquired Securitrans India Private Limited (SIPL), the second largest cash management company in India, thus consolidating its position as the leading cash management services company in India. CMS Securitas currently owns 40% market share. This acquisition will help us expand our reach to more than 2,100 towns in India and the combined entities will have a 55 per cent share of the market and manage 35,000 ATMs.

The Securitrans acquisition wasn't just about scale—it was about creating an unassailable market position before the coming consolidation. Kaul saw what others didn't: India's cash management industry was about to go through a massive shakeout driven by regulation, technology requirements, and banking consolidation.

Since the promoters were in a sell-mode for over a year, critical investments that are required in a services firm were not made. Of the six verticals that we are in, three are doing very well—card services, cash management and print services—but three need to gear up. We will leverage Blackstone to get customers.

By 2014, the transformation was complete. CMS is today a company with about Rs 800 crore revenue—up from less than Rs 500 crore when Blackstone entered. More importantly, it had transformed from a family-run services company to a professionally-managed platform business with genuine competitive advantages.

For Kaul, a seasoned professional, joining CMS was an entrepreneurial bet. I think there is a huge domestic opportunity. If you look at the domestic market, there are three large players—IBM, TCS and Wipro. After Wipro, there is a huge gap and enough room for another player to emerge in the domestic market and that's what we are aiming at.

The metrics spoke for themselves. EBITDA margins expanded from low teens to over 20%. Customer concentration reduced as CMS diversified across banks. The technology platform that once existed in PowerPoints became operational reality. Most critically, CMS had built what Kaul called "the moat of mundane complexity"—the business was so operationally complex, so deeply embedded in bank processes, and required such massive upfront investment that new entrants simply couldn't compete.

The transaction marks Blackstone's highest return since setting up its India office in 2005—though this wouldn't be clear until the next chapter of the story. As 2015 approached, whispers in Mumbai's financial circles suggested Blackstone was ready to exit. The transformation was complete, the business was humming, and private equity's five-year clock was ticking.

What Blackstone had built wasn't just a better CMS—it was a cash management platform positioned perfectly for India's next decade. The only question was: who would be brave enough to take it forward? The answer would come from an unexpected source—Asia's largest private equity firm was about to make one of its biggest India bets.

IV. The Baring Acquisition: Scaling Up (2015–2018) (35–45 min)

March 2015. The deal-making season in Mumbai was in full swing, but one transaction would redefine India's cash management landscape. Blackstone Group LP agreed to sell its 57 percent stake in CMS Info Systems Ltd to Baring Private Equity (Asia) for $250 million.

The headline numbers were staggering. Under the deal, Baring Private Equity acquired 100% of CMS Info Systems—53% from Blackstone, 37% from the Grover family and the balance 10% from the management team led by Kaul. Blackstone Group LP sold 53 per cent stake in CMS Info Systems Ltd., India's largest cash-management company, to Baring Private Equity (Asia) for Rs 2,000 crore ($301 million).

The valuation told the story of Blackstone's operational magic. Back in 2015, Baring Private Equity Asia made a deal to purchase Blackstone's 57% stake in CMS Info Systems at a valuation of INR 2,000 cr. In just six years, the company's valuation had jumped from INR 280 crore to INR 2,000 crore—a 7x multiple that would make any private equity fund's partners pop champagne.

But here's where it gets interesting: After cashing out, Kaul and the management team decided to reinvest in the company and stay on. Kaul and the management team opted to reinvest in the company to foster growth and remain at the helm. This wasn't just a financial decision—it was a statement of belief. When management teams reinvest their own exit proceeds back into the company under new ownership, they're betting their personal wealth on continued growth.

Sion Investment Holdings Pte. Limited, an affiliate of Baring Private Equity Asia, acquired 100% stake in CMS Info Systems. Sion wasn't just any investor—Baring Private Equity Asia was one of the largest and most successful PE firms in Asia, with a track record of transforming middle-market companies into regional champions.

The timing of Baring's entry was either incredibly prescient or extraordinarily lucky. They were taking control of India's largest cash management company just 18 months before an event that would shock the nation's financial system: demonetization.

Under Baring's ownership, CMS didn't radically change strategy—instead, it doubled down on what was working. The focus shifted from transformation to consolidation. While Blackstone had professionalized the company, Baring would help it dominate.

The market dynamics were shifting in CMS's favor. Post demonetization, this market has been consolidating at a rapid pace, and existing players are either conceding market share, exiting parts of their business, or leaving the industry all together. This is also partly driven by regulation—the regulator has over the years increased compliance. Example of these include the requirement to upgrade all ATMs to a cassette swap instead of traditional locker based, live tracking of all cash vans and timelines to reconcile cash. This increasing cost of compliance is driving smaller players out of the industry and acting favorably for larger players, like CMS.

Baring brought something Blackstone couldn't: Asian operational expertise and a longer-term horizon. While Blackstone typically looked for 3-5 year exits, Baring was known for holding assets longer if the growth story remained intact. This patient capital approach would prove crucial as CMS navigated the tsunami about to hit India's cash economy.

The company continued its technology investments, building what would become India's most sophisticated cash tracking system. Every cash van was GPS-enabled with real-time tracking. Every ATM cassette had a unique identifier that could be traced from currency chest to final dispensation. Every retail pickup was digitally documented with photographic evidence and timestamp verification.

Within six years of leading the Blackstone-backed buyout of CMS Computers into a new company, CMS Info Systems, in 2009, Kaul led a radical restructuring and transformation that saw revenues almost tripling to around Rs 1,500 crore. CMS today handles almost 53 per cent of all cash in circulation in the country, manages more than 55,000 ATMs and covers 35,000 retail outlets for their cash management and processing functions. CMS has also aggressively built the network across 2,200-plus towns.

But Baring's real contribution wasn't operational—it was strategic positioning. They understood that CMS wasn't really in the cash management business. It was in the trust business. Banks trusted CMS with billions of rupees daily. Retailers trusted them with their entire cash operations. The RBI trusted them to maintain the integrity of currency circulation.

This trust, painstakingly built over decades and fortified through PE-driven professionalization, was about to be tested in ways nobody could have imagined.

The leadership team under Baring expanded its vision. Anush Raghavan is the President- Cash Management Business of our Company. He has been associated with our Company since October 1, 2009. He is currently heading the cash management business of our Company. Raghavan would become instrumental in navigating the chaos about to unfold.

Pankaj Khandelwal is the President and Chief Financial Officer of our Company. He has been associated with our Company since July 1, 2009 and prior to the demerger was associated with CMS Computers Limited as a chief financial officer since May 8, 2006. He is currently responsible for finance, legal and secretarial function of our Company.

The team was battle-tested, well-funded, and strategically positioned. They controlled over half of India's cash movement infrastructure. They had the technology platform to handle massive scale. They had the operational expertise from two PE transformations.

What they didn't have was any idea that in a few months, the Prime Minister of India would stand on national television and announce that 86% of the country's currency was now worthless paper.

As 2016 dawned, CMS was processing over ₹9 trillion annually through its network. The company had achieved everything Baring had hoped for—market dominance, operational excellence, and steady growth. The cash management industry in India seemed predictable, stable, almost boring.

It was about to become anything but.

V. Demonetization & The Great Cash Paradox (2016–2020) (50–60 min)

November 8, 2016. 8:00 PM.

"Mitron..." Prime Minister Narendra Modi's voice crackled across millions of television screens. What followed would become one of the most dramatic economic experiments in modern history. With four hours' notice, 86% of India's currency—all ₹500 and ₹1,000 notes—became illegal tender.

In CMS's Mumbai war room, Rajiv Kaul and his leadership team watched in stunned silence. Their entire business model had just been declared obsolete—or so everyone thought.

The immediate aftermath was chaos. In November-December 2016, after demonetisation, there was a sharp fall in CCI (CMS Cash Index) while S&P Global India Purchase Manager Index saw much lesser decline. Subsequently, the CCI saw a spell of relative underperformance until cash supply stabilised.

ATMs ran dry. Banks were overwhelmed. The nation joined serpentine queues that became the defining image of demonetization. For a cash management company, this should have been an existential crisis. The very currency they moved, counted, and protected had been invalidated overnight.

The Indian cash management market grew at a CAGR of c.10% between FY10 to FY21; it declined during FY16-17 owing to demonetisation. After India declared demonetization of all 500 and 1,000 rupee notes in 2016, the currency in circulation had dropped to 13.35 trillion rupees in financial year 2017. However, the CIC increased rapidly to over 34 trillion rupees as of financial year 2024.

But here's where the story takes its most fascinating turn. CIC (Cash in Circulation) pre demonetization i.e. before 2016 was around 16L Crores and now i.e. 2022 the CIC is 31L Crores. The death of cash had been greatly exaggerated.

During demonetisation, they said cash would die. During the pandemic, they said cash was dying. How many times can it die? Kaul's rhetorical question captured the paradox perfectly. Instead of killing cash, demonetization had somehow made it more important.

The numbers tell an extraordinary story. According to the report, the ATM cash withdrawals zoomed 235 per cent to Rs 2.84 lakh crore in March 2023 in a matter of 76 months after demonetization. The number of ATMs grew at a CAGR of 20% between Fiscal Year 2011 and Fiscal Year 2016, but the increase between the Fiscal Year 2016 and Fiscal Year 2021 slowed down to a 3% CAGR (reaching 255,000 ATMs) due to demonetization, PSB consolidation, and the balance sheet difficulties of PSBs.

For CMS, demonetization became an unexpected catalyst. While smaller competitors struggled with the operational complexity of managing new currency, handling unprecedented volumes, and meeting regulatory requirements, CMS's scale and technology platform gave it an insurmountable advantage.

Post demonetization, this market has been consolidating at a rapid pace, and existing players are either conceding market share, exiting parts of their business, or leaving the industry all together. The weak were culled. The strong got stronger. CMS was the strongest of them all.

Then came COVID-19, another supposed death knell for cash. The narrative was compelling: contactless payments would finally drive the shift to digital. Who would want to handle potentially contaminated currency during a pandemic?

At the peak of the COVID-19 pandemic and the lockdown, the fall in S&PGIPMI was much starker compared to the decline seen in the CCI. Cash showed remarkable resilience. The industry was affected by Covid-19, particularly the RCM and DCV businesses, though it is now recovering to pre-Covid levels.

Given the lower penetration of financial and digital literacy in SURU (Semi-Urban and Rural) locations, there was a relatively higher dependence on cash. During the second wave of COVID-19 pandemic in April-July 2021, SURU ATMs saw 15.47% growth in average cash replenishment per ATM compared to metro and semi-metro locations.

The pandemic revealed a fundamental truth about India: in times of crisis, people trust cash. When digital systems could fail, when internet connectivity was uncertain, when smartphone batteries died, cash worked. Always.

Cash in Circulation - a metric used by RBI to describe cash usage has essentially increased at an annual rate of 5.33%. The currency in circulation (CIC) has gone up to Rs 31.33 lakh crore in March 2022, from Rs 13 lakh crore in 2014, finance minister Nirmala Sitharaman said in the Lok Sabha in March 2023. India's CIC to GDP ratio has averaged close to 12.4 per cent which is higher than the 10-year average of 11.8 per cent.

The reasons for cash's resilience run deep into India's economic structure. The economic and social growth of tier 3 or tier 4 towns and rural areas in India is severely hampered by the low penetration of banking services. Access to formal banking services is restricted by things like low income, low literacy, poor infrastructure (such as branches or ATMs), and lack of awareness & trust. Since they are unable to access loans, savings, insurance, and other financial products and services that can enhance their livelihoods and well-being, it hinders their financial inclusion and empowerment. Their ability to make use of the advantages of online transactions, e-commerce, and fintech solutions also restricts their engagement in the digital economy. Additionally, it puts individuals in danger of financial shocks brought on by calamities or natural disasters, theft, fraud, cash loss, and destruction. Cash-on-delivery transactions account for more than 90% of e-commerce transactions in these areas.

For CMS, each crisis became an opportunity to prove its indispensability. During demonetization, they managed the logistics of replacing an entire nation's currency. During COVID, they ensured ATMs stayed filled despite lockdowns. When digital payment systems faced outages, cash was the backup that never failed.

The technology investments made during the Blackstone and Baring eras paid massive dividends. For Fiscal 2021, the total currency throughput of the company, or the total value of the currency passing through all ATM and retail cash management businesses, amounted to ₹9,158.86 billion with 255,000 ATMs, across India. Managing this scale during crisis required sophisticated systems that smaller players simply didn't have.

By 2020, CMS had emerged from successive crises stronger than ever. Market share had increased. Competitors had exited. The narrative of cash's death had been thoroughly debunked. This increase in cash usage is not just across rural and semi urban areas but even within developed metros.

In September 2021, Rajiv Kaul, vice-chairman and CEO of CMS Info Systems, faced a challenging audience. Investors questioned the future of his cash management business amidst the growing wave of digital payments. CMS, India's largest cash management company, depended significantly on the circulation and movement of physical currency—at a time when digital payments seemed to dominate headlines.

But Kaul had data on his side. And he had something else: a plan to take this battle-tested, crisis-hardened company public. The boy from Delhi who had reluctantly left Microsoft to join a cash management company was about to face his biggest test yet—convincing public market investors that cash was still king.

The stage was set for CMS's next transformation. From family business to PE-backed professional firm to crisis-tested market leader, the company was ready for its public debut. The only question was whether investors would buy the story of cash in digital India.

VI. Going Public: The IPO Story (2021) (40–50 min)

The Trident Hotel ballroom in Mumbai's Bandra Kurla Complex was packed with fund managers, all armed with the same question: "Why should we invest in cash when India is going digital?" It was September 2021, and Rajiv Kaul was in the middle of CMS Info Systems' IPO roadshow, fighting the narrative battle of his life.

This wasn't CMS's first attempt at going public. The company had received SEBI approval in 2017 but let it lapse, waiting for better market conditions. Now, four years later, with digital payments grabbing headlines and cash seemingly anachronistic, they were trying again.

Initial public offer of 50,925,925 equity shares of face value of Rs. 10 each of CMS Info Systems Limited for cash at a price of Rs. 216 per equity share including a premium of Rs. 206 per equity share (Offer Price) aggregating to Rs. 1100.00 crores through an offer for sale by Sion Investment Holdings Pte. Limited (Promoter Selling Shareholder).

The structure was telling—this was a pure offer for sale (OFS), with no fresh capital being raised. This initial public offering will include only an OFS by its existing promoter Sion Investment Holdings Pte. Baring Private Equity, through Sion Investment Holdings, was cashing out completely after six successful years.

CMS Info Systems IPO bidding started from Dec 21, 2021 and ended on Dec 23, 2021. The shares got listed on BSE, NSE on Dec 31, 2021. The timing seemed almost deliberately challenging—listing on the last day of the year, when most investors were on holiday.

The IPO details revealed the scale of the operation: CMS Info Systems IPO lot size is 69, and the minimum amount required for application is ₹14,904. CMS Info Systems IPO to raise around ₹1100 crores via IPO that comprises fresh issue of ₹- crores and offer for sale up to ₹1100 crores of ₹10 each. The IPO size was reduced from 2000 crores to 1100 crores.

The roadshow presentations were a masterclass in narrative management. Kaul didn't deny digital payments' growth—he embraced it. His argument was counterintuitive but compelling: digital payments and cash weren't competitors; they were complements. Every UPI transaction started or ended with cash somewhere. Every e-commerce COD order needed physical money collection. Every digital wallet needed cash-in points.

Yet, his investors wanted more than a confident retort—they needed a long-term vision. Kaul presented one: the company was investing in remote monitoring systems for ATMs, a service designed to oversee automated teller machines and reduce operational inefficiencies.

The numbers in the prospectus told a story of remarkable consistency. The Issuer posted total revenues of Rs 629.72 for 5MFY22 and earned PAT of Rs 84.47 crore during the same period. The total revenues for FY21 reduced by 5% to Rs 1321.92 crore in FY21 from Rs 1388.29 crore in FY20 due to impact of the pandemic on the business operations of the Issuer. However, PAT rose by 19.5% to Rs 168.52 crore in FY21 from Rs 134.71 crore in FY20.

Market reception was skeptical. CMS Info Systems IPO raises ₹330.00 crore from anchor investors, but the broader market remained unconvinced. The IPO was subscribed approximately 2x—decent but not spectacular.

Opening Price on NSE: INR220.2 per share (up 1.94% from IPO price) Closing Price on NSE: INR241 per share (up 11.57% from IPO price). CMS made its debut on the NSE and BSE on December 31, 2021, via a successful IPO at INR 216 per share. The shares opened at INR 218.5 on the NSE, representing a ~1% premium over the IPO price, and closed at INR 220.

The muted listing was actually a blessing in disguise. It kept away momentum traders and attracted long-term investors who understood the business. Fund managers who had done their homework recognized what others missed: CMS wasn't a cash company trying to survive digitization—it was an infrastructure company benefiting from India's formalization.

Sion Investment Pvt Ltd is the promoter company (Sion's parent is Baring Private Equity Asia Holding). Promoter shareholding would reduce to 65.59% through OFS. Post-IPO, Baring still retained majority control, signaling continued confidence in the business.

The investor presentations revealed fascinating insights into the business model. Cash management services includes end-to-end ATM replenishment services; cash pick-up and delivery; network cash management and verification services (together known as "retail cash management services"); and cash-in-transit services for banks. This segment accounted for 68.61% and 66.74% of revenue respectively in FY21 and 5MFY22.

But the real revelation was the economics. The revenue structure is based on a fee per trip along with a fixed yearly fee. CMS has over 72,000+ ATMs across India under its management. Each ATM relationship was a mini-annuity, generating predictable revenue with minimal customer acquisition cost.

As of December 31, 2022, the order book is around INR 3,000 crore. These contracts are of longer duration, ranging from four to seven years, and are expected to generate recurring revenue, thereby providing revenue visibility for the near to medium term.

The IPO documents also revealed the depth of CMS's competitive moat. The Issuer has a pan-India fleet of 3,965 cash vans and network of 238 branches and offices, which as of August 31, 2021 cover all of Indian states and union territories except remote union territory of Lakshadweep. CMS covers 97.04% of India's 742 districts and 14,949 or 77.46% Indian postal codes, including difficult to reach and remote rural and semi-urban areas. CMS has served 141,977 business points across ATM cash management, retail cash management and managed services businesses as of August 31, 2021.

The listing also brought transparency to ownership and governance. Listed on Indian bourses (NSE, BSE: CMS INFO). Few unique companies in India with 100% public shareholder base post the complete exit of Baring in subsequent years.

What made the IPO particularly interesting was management's skin in the game. His confidence is backed not just by his leadership position, but also by the fact that he has skin in the game, holding a 6.43% stake in the company. Kaul hadn't just stayed on as a professional CEO—he was a significant shareholder betting his personal wealth on the company's future.

The IPO marked a watershed moment. CMS had transitioned from a closely-held family business to a PE-backed transformation story to a public company. Each phase had brought professionalization, scale, and sophistication. Now, as a listed entity, it would face the quarterly scrutiny of public markets while executing its long-term vision.

The market's initial skepticism would prove to be misplaced. Over the next three years, as digital payments continued their explosive growth, something unexpected happened—cash kept growing too. And CMS, now battle-tested through crisis and validated by public markets, was perfectly positioned to capture this paradoxical growth.

VII. The Business Model: How Cash Management Actually Works (45–55 min)

Inside CMS's command center in Mumbai, screens flicker with real-time data from across India. A red dot indicates an ATM in Ladakh running low on cash. A green line tracks a cash van navigating Bangalore traffic. Yellow alerts flash for cassettes awaiting pickup in Chennai. This is the nerve center of India's cash economy, and every second, millions of rupees flow through its digital oversight.

To understand CMS's dominance, you need to understand the invisible complexity of moving physical money. It's a ballet of logistics, technology, and trust that most people never think about—until an ATM runs dry on a Sunday evening.

CMS Info Systems has three main business segments: Cash Management (~69% of revenue in FY23): This segment provides cash-in-transit, cash processing, ATM replenishment and maintenance, retail cash management, and other related services to banks and retail outlets. Managed Services (~29% of revenue in FY23): This division offers comprehensive outsourcing solutions for ATM network management, banking automation, card personalization, remote monitoring, and multi-vendor software for banks and financial institutions. Tech Solutions (~2% of revenue in FY23): This segment provides technology products and solutions for digital payments, artificial intelligence, blockchain, cybersecurity, and other emerging domains.

Let's follow a single rupee note through the CMS network to understand the business model's elegance.

The journey begins at an RBI currency chest—high-security vaults where fresh currency waits for distribution. The cycle of cash starts from the Reserve Bank of India's (RBI) mints and vaults and moves through bank currency chests and branches, ATMs, post offices, businesses big to tiny and individuals, with innumerable stops in between. CMS covers all that—it feeds ATM machines, delivers and picks up cash from retail and other outlets, moves cash between currency chests and bank branches, runs dedicated cash vans, processes and sorts cash and offers cashiering services. After consumers take the money out, they spend it and it eventually flows back to banks and then to the RBI. The whole cycle, Kaul says, is not only about the movement, which is a big part of it, but also about the processing.

The sophistication begins with forecasting. CMS's algorithms predict cash demand at each ATM by analyzing historical patterns, local events, holidays, weather, and even cricket match schedules. A Diwali weekend in Delhi needs different cash positioning than a regular Tuesday in Trivandrum.

Our services include cash processing, cassette management, ATM replenishment, cash evacuation for banknote accepting/recycling, day-end reporting, and reconciliation. Each service layer adds complexity and switching costs.

Consider cassette management alone. Modern ATMs use sealed cassettes that must be swapped entirely rather than refilled on-site. The requirement to upgrade all ATMs to a cassette swap instead of traditional locker based created massive operational complexity. CMS maintains cassette float inventories, manages the swap logistics, and handles reconciliation—all while maintaining chain-of-custody documentation that would satisfy audit requirements.

The company possesses over 4,000 cash vans and a strong network of 240 branches and offices, allowing it to manage over 150,000 business points. But these aren't just vehicles—they're rolling fortresses with GPS tracking, biometric locks, panic buttons, and real-time communication systems.

The technology infrastructure is where CMS's moat becomes apparent. ALGO OTC is a fully automated, mobility-based ATM security software application that provides E2E password management and facial recognition. This proprietary system manages the complex authentication required when service personnel access ATMs.

CMS monitors over 21,000 sites using AI-powered video analytics to detect unusual activities such as intrusions, glass breaks, or smoke. Its proprietary ALGO platform already supports over 50,000 ATMs across India, ensuring optimal uptime and seamless customer experiences.

The retail cash management vertical reveals another layer of complexity. We have seen 10.1 per cent growth in monthly average cash replenishment at ATMs and a strong 1.3 times increase in average cash collection per point with e-commerce companies in FY23, said Anush Raghavan. Maharashtra, Gujarat, Tamil Nadu, Karnataka, and Uttar Pradesh together accounted for 43.1 per cent of the total ATM cash replenished by CMS Info Systems across the country in FY 2023.

E-commerce companies present unique challenges. Cash-on-delivery orders mean thousands of small cash collections from individual delivery points. CMS developed specialized solutions: An end-to-end integrated solution developed for cash-on-delivery and UPI payments · Real-time transaction details and instant receipts available across all payment modes · Centralized reconciliation achieved through 850 unique QR codes generated at the distributor level.

The managed services business is where technology leverage becomes clear. We provide comprehensive management of ATM networks from start to finish through a single point of accountability. We integrate various offerings from the CMS platform, including automation, cash management, and AIoT Remote Monitoring Solution, to deliver an enhanced experience and ensure 24x7 availability to banks and customers.

Brown Label ATMs represent a particularly clever model. CMS operates 5,500 brown-label ATMs, a figure expected to rise with outsourcing trends. In this arrangement, CMS owns and operates the ATM hardware while banks provide the branding and customer interface. It's capital-light for banks and generates recurring revenue for CMS.

The numbers reveal staggering scale. Alongside its subsidiary, Securitrans India Private Limited, it oversees nearly 70,000 ATMs as of March 2022, representing approximately 46% of all outsourced ATMs in India and about 28% of all ATMs in the country. CMS has increased its share in the ATM cash management business from 39% to 49% over four years.

Risk management is embedded in every process. Over the last 16 years, we have developed robust governance processes to ensure the reliability and safety of operations. Our systematic risk management framework helps us assess and minimise risks. Our 200+ person strong audit team reinforces our risk management efforts continuously.

The technology platform serves as both operational backbone and competitive moat. An automated reconciliation system for predictive risk management, which handles millions of automated transactions annually with accuracy. Automates real-time reporting to access transactions such as indent upload, trip sheet generation, etc. across the business points at pan-India level centrally.

Customer relationships reveal the business model's stickiness. Among its clients are SBI, HDFC Bank, Axis Bank, ICICI Bank, Citi Bank, Hitachi Payment Services Private Limited, Financial Software, and Systems Private Limited. CMS' revenue growth has been supported over the years by incremental business from these key clients.

The economics are compelling. More than one-third of the cost running an ATM is that of cash management. Banks face a build-versus-buy decision, and increasingly, they're choosing to buy. Building internal cash management capabilities requires massive capital investment, operational expertise, regulatory compliance, and geographic coverage—all for non-core activities.

The contract structure provides visibility and stability. These contracts are of longer duration, ranging from four to seven years, and are expected to generate recurring revenue. Multi-year contracts with price escalation clauses protect against inflation while switching costs protect against competition.

The company is debt free, growing its topline by 20% every quarter and boasts return ratios greater than 25% with an EBITDA margin of almost 30%. Its return on capital employed (ROCE), excluding cash, stands at an impressive 37%.

The business model's genius lies in its inevitability. As long as India uses cash—and all evidence suggests it will for decades—someone needs to manage its movement. CMS has positioned itself as that someone, with scale, technology, and trust barriers that make displacement nearly impossible.

VIII. Digital India vs Cash Reality: The Great Debate (35–45 min)

The Unified Payments Interface (UPI) logo gleams from every street vendor's cart. QR codes paper the walls of tea stalls. Digital payment soundboxes chirp their confirmations in multiple languages. By every visible measure, India has gone digital. Yet as of November 15, 2024, RBI data showed currency in circulation at ₹35.6 trillion, nearly double the amount during the demonetization era.

This paradox sits at the heart of CMS's investment thesis and India's economic reality.

India's digital payment ecosystem has transformed dramatically, with retail transactions increasing 90-fold in just 12 years. According to the Reserve Bank of India (RBI), the Unified Payments Interface (UPI) alone handled over 16.6 billion transactions in October 2024. PwC's India Payments Handbook, released earlier this year, revealed that India now accounts for 46% of global digital transactions.

The numbers are staggering. UPI's growth trajectory defies comparison—from 17.9 million transactions in August 2016 to 16.6 billion in October 2024. Every financial technology conference celebrates India's digital payment miracle. Every startup pitch deck shows the hockey stick growth curve.

So why isn't cash dying?

The Reserve Bank of India (RBI) has reported that currency in circulation edged up by 0.1% on the week to stand at Rs 35.66 lakh crore as on November 8, 2024. Currency in circulation rose 6.1% on a year ago basis compared to 4.3% rise at the same time last year. In the current fiscal, the currency in circulation gained 1.6% so far.

The answer lies in understanding what UPI actually does versus what it's perceived to do. UPI primarily replaces small-value cash transactions and person-to-person transfers that would have happened through other electronic means. It's not replacing the fundamental need for cash in India's economy.

Analysts attribute this trend to India's GDP growth and the slower-than-expected adoption of digital payments in certain sectors. Bhavik Hathi, managing director at Alvarez and Marsal, explains, "India's business volumes are growing at 6–7% annually, and cash in circulation naturally increases alongside".

Consider India's economic structure. The supply of money (M3) in the Indian economy increased by 22% in 2024-25 to touch ₹272,866 billion, in comparison to 223,332 billion in 2023-24. ₹32,783 billion (13.3% of the total money supply) in 2024-25 was in the form of currency notes and coins in circulation with the general public.

The urban-rural divide tells another story. While Mumbai and Bangalore residents tap their phones for everything, rural India—home to 65% of the population—operates differently. As per CMS ATM Dispensed data, the average ticket size (ATS) of ATM withdrawals in FY25 was INR 5,658, registering a y-o-y growth of 3%. Further, select months like October 2024, January 2025, February 2025, and March 2025 witnessed a higher growth in ticket size at 4%, 4%, 5%, and 6% respectively.

The behavioral economics of cash run deeper than infrastructure. Cash provides tangibility in a country where financial abstraction remains alien to many. It offers privacy in transactions many prefer to keep discrete. It works when networks fail, power cuts strike, or smartphones die.

RBI has reported that the cash in circulation has risen by 83 per cent since 2016. The cash flow in the economy has also propelled in the last six years due to the increase in our GDP. Economic growth itself drives cash demand—more businesses, more transactions, more currency needed for circulation.

However, even as Indians embrace digital payments, cash continues to rule the roost. Cash remains an integral part of the Indian economy and ATMs remain an important touchpoint that facilitate easy access to cash for India's large and widespread population.

The data reveals fascinating consumption patterns. 4 key retail consumption trends highlight the positive shift in consumption-class Indians due to increased spending in Media & Entertainment, Aviation, Railways and E-commerce sectors. Entertainment sector increased by 29.30%. Over a two-year period, from FY22 to FY24, the average spending in the sector increased by nearly 100%. The latter is endorsed by a robust 16.76% annual growth in the average spending in the FMCG sector in FY24, which is a remarkable recovery compared to the 21.94% decline observed in FY23.

These consumption patterns matter because many occur in cash. Cinema tickets might be booked online, but popcorn is bought with cash. Flight tickets use credit cards, but airport porters prefer notes. The formal and informal economies interweave in ways that make pure digitization impossible.

However, this move hasn't impacted the cash usage in the economy. The coexistence model is becoming clear—digital payments handle convenience transactions while cash manages trust transactions.

Geographic patterns reveal another dimension. Maharashtra, Gujarat, Tamil Nadu, Karnataka, and Uttar Pradesh are the Top 5 states with maximum GSDP in FY 2022. Together these states accounted for 43.10% of the ATM cash replenished by CMS Info Systems during FY 2023. Even wealthy states with high digital adoption maintain robust cash usage.

The ATM story itself is telling. Despite predictions of obsolescence, The ATM base in India is expected to increase from 255,000 in FY21 to 365,000 by FY27E. Banks are adding ATMs, not removing them. With banks like SBI, HDFC, and Kotak Mahindra planning significant branch and ATM expansions, the physical infrastructure for cash is growing, not shrinking.

Overall, the average cash dispensed per ATM has increased from INR 1.02 Cr in FY17 to 1.30 Cr in FY25. Each ATM is working harder, dispensing more cash, serving more customers—hardly signs of a dying payment method.

The regulatory environment adds complexity. While the government promotes digital payments through incentives and infrastructure, it also recognizes cash's necessity. Financial inclusion efforts often begin with cash—bank accounts need to be funded, benefits need to be withdrawn, trust needs to be established before behavioral change can occur.

India continues to forge ahead on its unique economic growth journey that successfully manages the tenuous balance between being a cash-led economy and a digital economy. This isn't a transition from cash to digital—it's an expansion of both.

For CMS, this reality creates opportunity. This shift toward digitalization might appear detrimental for a company like CMS. But Kaul and his team are betting on two things: the enduring role of cash in India's economy and their ability to diversify into emerging revenue streams.

The debate isn't really about cash versus digital—it's about understanding India's unique payment ecosystem evolution. In developed economies, digital payments replaced cash. In India, they're supplementing it. The pie is growing for everyone.

Although cash is still the ruler in the Indian market, digitization is drawing alongside at a good pace, said Tashwinder Singh, the MD & CEO of Niyogin Fintech. The adoption of digital financial services has helped bring more individuals into the formal banking sector, promoting financial inclusion and supporting economic growth. With the expansion of financial literacy, neo-banking and fintechs, India is gradually transitioning towards becoming a cashless economy.

"Gradually" being the operative word. And in that gradual transition—likely measured in decades, not years—lies CMS's opportunity. They're not betting against digital payments. They're betting on India's growth, complexity, and the enduring human preference for physical value in an increasingly virtual world.

IX. Technology Transformation & New Growth Vectors (40–50 min)

The acquisition announcement came quietly in 2022, buried in regulatory filings that few noticed. CMS's foray into remote monitoring began in earnest with the acquisition of Hemabh Technology in 2022. For a cash management company to buy a video analytics startup seemed odd. Unless you understood where Rajiv Kaul was steering the ship.

"We're not a cash management company anymore," Kaul told his leadership team. "We're a trust infrastructure company that happens to move cash."

This technology allows CMS to oversee ATMs and detect unusual activities such as intrusions, glass breaks, or smoke using AI-powered video analytics. But the vision went far beyond ATM monitoring.

Deployed in >25,000 sites across India and connected to >500,000 devices, our service leverages AI and IoT technologies to deliver comprehensive business insights, optimize performance and address site security issues effectively. Each site generates terabytes of data—foot traffic patterns, transaction anomalies, maintenance predictions, security threats.

ALGO OTC solution prevented 19,000 errors and minimized risk throughout the cash replenishment cycle across the ATM network · The 24x7 on-premise automation solution enabled real-time tracking, delivered e-receipts, and facilitated central reconciliation · The integration of advanced technology with existing systems helped minimize pilferage costs and ensured accurate financial reporting.

The AI transformation isn't just about efficiency—it's about creating new revenue streams. The move aligns with an RBI directive encouraging banks to adopt e-surveillance mechanisms to reduce dependence on on-site security personnel. Elara Securities, in a report from October 2024, noted that over 60% of ATMs and bank branches in India are yet to adopt advanced AI-driven monitoring systems. This leaves a significant opportunity for companies like CMS to capitalize on the growing demand. Analysts estimate the total addressable market for ATM and bank monitoring solutions to be between ₹6,000 and ₹9,000 crore annually.

The technology stack CMS has built is staggering in scope. ALGO MVS enables financial institutions to streamline their development and operations by eliminating the need to maintain and enhance several distinct delivery infrastructures. This multi-vendor software platform allows banks to manage ATMs from different manufacturers through a single interface—a seemingly simple capability that required years of development.

We are gaining market share, maintaining world-class margins, and increasing our share of recurring revenue streams. We are also making the right long-term investments with an increase in our tech spends from 1% to 1.5% of revenues. As we gain momentum from order win execution, market share growth, and the expansion of our AIoT platform, we are positioned well for strong growth in FY26.

The remote monitoring platform reveals the strategic evolution. Traditional ATM surveillance involved security guards watching CCTV feeds—expensive, unreliable, and reactive. CMS's AI-powered system is predictive and proactive. It identifies suspicious behavior patterns before incidents occur. It detects when an ATM's cash dispensing pattern suggests a skimming device. It alerts when environmental conditions might affect equipment performance.

A game-changer for businesses, transforming traditional CCTV systems into smart, intuitive Vision AI surveillance solution that thinks ahead. The platform now monitors retail stores, bank branches, warehouses, even ambulances.

Consider the e-commerce integration: Generated instant e-receipts for store cashiers via a customized mobile app through API integration, reducing disputes, enhancing accuracy, and ensuring a smoother transaction experience across stores. Every cash-on-delivery transaction is digitally documented, geocoded, and instantly reconciled.

The Brown Label ATM expansion represents another technology-enabled growth vector. It also provides managed services, such as banking automation services comprising ATM manufacturing and maintenance, currency recyclers, and self-service kiosks; brown label ATM deployment and managed services for banks. CMS doesn't just manage these ATMs—it owns and operates them, selling transaction services to banks.

Remote Monitoring Growth: With AI-driven insights, CMS monitors over 21,000 sites, reducing fraud and improving operational efficiency. Enhanced ATM Features: Modern ATMs serve as digital banking hubs, offering services like credit card payments, cheque book requests, and more, creating new revenue streams for CMS.

The card personalization business, though small, showcases technological capability. At our state-of-the-art facility, we offer comprehensive financial card issuance and management services for banks, including card personalization. Using advanced printing, encoding, and security technologies, CMS produces millions of payment cards annually.

We have integrated technology within the operational process by automating tasks and eliminating manual risks with in‑house solutions customized for the Indian market. This isn't off-the-shelf software—it's purpose-built for India's unique requirements.

The data advantage is becoming clear. CMS processes information from: - 72,000+ ATMs monitoring cash levels and transaction patterns - 150,000+ business points tracking retail cash flows - 4,000+ cash vans reporting real-time locations and status - 25,000+ monitored sites generating security and operational data

This data exhaust, properly analyzed, reveals economic patterns invisible to others. Which neighborhoods see cash demand spike before festivals? Which ATMs face higher fraud risk? Which retail categories are shifting from cash to digital? CMS knows.

He has been the visionary force at CMS since 2009, leading with a people-first approach. Kaul's technology vision extends beyond operational efficiency. He's building platforms that become indispensable to customers.

The AIoT (Artificial Intelligence of Things) platform represents the culmination of this vision. Our AIoT Remote Monitoring Solution is a game-changer in the industry, offering businesses valuable insights for energy management, staff monitoring, and site compliance tracking in addition to plain vanilla monitoring services. With real-time monitoring and reporting, it drives efficiency and productivity.

Banks are beginning to understand the value proposition. Instead of managing thousands of vendor relationships for ATM maintenance, cash management, monitoring, and software, they can partner with CMS for integrated solutions. The switching costs become enormous—not just operational, but technological.

As of Q3 FY25, it holds a 42% revenue share in India's organized cash logistics market. But the ambition goes beyond market share. CMS is building the operating system for India's physical payment infrastructure.

The innovation pipeline remains robust. Blockchain for cash tracking, IoT sensors for predictive maintenance, computer vision for security enhancement—each technology layer adds capability and competitive advantage.

With ₹1,000+ crore in cash on the balance sheet, his focus on deploying capital through inorganic growth will be key to driving diversification and value creation. The war chest exists for strategic acquisitions that add technological capability or market access.

The transformation from cash handler to technology company isn't complete, but the trajectory is clear. In five years, CMS might still move cash, but its value will come from the intelligence layer wrapped around those movements. Every rupee will be smart, tracked, and optimized. And CMS will be the brain making it happen.

X. Market Dynamics & Competitive Landscape (30–40 min)

The conference room at Writer Corporation's Mumbai headquarters was somber. After 40 years in the cash management business, they were throwing in the towel. Hitachi Payment Services had just acquired their cash logistics operations, another casualty in the great consolidation reshaping India's cash management industry.

Post demonetization, this market has been consolidating at a rapid pace, and existing players are either conceding market share, exiting parts of their business, or leaving the industry all together. This wasn't just market dynamics—it was market Darwinism.

Its dominance allows the company to capitalize on industry trends like consolidation, triggered by tighter regulations and public sector bank mergers. Smaller players are exiting, leaving more business opportunities for established entities like CMS.

The regulatory tightening has been relentless. The regulator has over the years increased compliance. Examples of these include the requirement to upgrade all ATMs to a cassette swap instead of traditional locker based, live tracking of all cash vans and timelines to reconcile cash. This increasing cost of compliance is driving smaller players out of the industry and acting favorably for larger players, like CMS.

Each new regulation—while improving security and efficiency—requires significant capital investment. Smaller players face an impossible choice: invest millions in compliance infrastructure or exit the business. Most choose the latter.

The company is a market leader in the Cash Logistics sector, having a strong presence across all major segments, including ATM Cash Management, Retail Cash Management (RCM), and Cash-in-Transit (CIT). As of Q3 FY25, it holds a 42% revenue share in India's organized cash logistics market.

The competitive landscape has evolved dramatically from the fragmented market of the 2000s. Today, it's an oligopoly with clear leaders:

CMS Info Systems - The undisputed leader with 49% market share in ATM cash management, up from 39% four years ago. Managing approximately 46% of all outsourced ATMs in India and about 28% of all ATMs in the country.

Hitachi Payment Services - The aggressive acquirer, buying up Writer Corporation and other smaller players. Strong in white-label ATM deployment but lacking CMS's operational depth.

SIS Prosegur - The security services giant's cash management arm. Strong brand and international backing but limited technology differentiation.

Radiant Cash Management - Regional player with pockets of strength but lacking national scale.

The global comparison is illuminating. While the global players are 5x larger in size than CMS, their margins are at best less than half of what CMS is able to deliver. CMS is also growing much faster (~20% quarterly growth rate) than its global peers, who, being much larger and in more mature markets, average at a single-digit growth rate.

Why does CMS generate 30% EBITDA margins while global peers like Brinks and Loomis struggle to exceed 15%? The answer lies in India's unique market structure:

Labor Arbitrage: India's lower labor costs allow for human-intensive operations at profitable margins.

Regulatory Capture: Compliance requirements create barriers that protect incumbents.

Relationship Depth: Multi-decade banking relationships create switching costs beyond pure economics.

Geographic Complexity: India's diverse terrain and infrastructure make nationwide coverage a massive competitive advantage.

Over 40% of ATMs in India are still managed by banks, presenting a massive outsourcing opportunity. Banks increasingly recognize that managing cash infrastructure isn't core to their business. The question isn't whether they'll outsource, but when and to whom.

Public sector bank consolidation accelerates this trend. When banks merge, redundant cash management contracts get rationalized. The survivor typically chooses the vendor with superior technology and coverage—invariably CMS.

Moreover, CMS faces increasing competition from companies like Hitachi Payment Services, which recently acquired Writer Corporation's cash management business. But acquisition doesn't equal integration. Hitachi faces the challenge of merging different operational cultures, technology platforms, and customer relationships.

The competitive moats are deepening:

Scale Economics: Over 4,000 cash vans and a strong network of 240 branches create density economics that competitors can't match.

Technology Platform: Years of investment in proprietary systems create capabilities that can't be quickly replicated.

Trust and Track Record: Zero major security breaches in handling trillions of rupees over decades.

Regulatory Relationships: Deep understanding of and compliance with RBI requirements.

The IT services market is very fragmented in India. You have IBM, TCS and Wipro, and the rest have very small percentages of the business. Right now two-three of my competitors are quite weak. So all I want to do is to take a little share from them. By doing so I can double my market share right now. So our job is really to focus on some of their clients, which one of the competitor is weak, whose strategy for customer service is not perfect—some of the biggest names in the country are a little weak because their strategy is wrong. Their customers have been saying they are not happy with them. I tell them our biggest advantage is that we do many things that they don't.

The market structure favors consolidation. While globally, the industry is consolidated and oligopolistic, in India, there are a large number of international as well as domestic players competing in various sub-segments of the market. This fragmentation is unsustainable given rising compliance costs and customer demands for integrated solutions.

New entrants face formidable barriers:

Capital Requirements: Billions needed for vehicles, vaults, technology, and working capital.

Geographic Coverage: Building nationwide presence takes decades.

Trust Building: Banks won't entrust cash management to unproven operators.

Regulatory Approval: RBI authorization requirements are stringent and time-consuming.

Talent Acquisition: Experienced cash management professionals are scarce and typically locked into competitors.

The Company has a P/E (TTM) ratio of 17x, while its competitors, Radiant Cash, and SIS, trades at a slightly lower P/E multiple of 16x. This indicates that the Company's valuation is comparable to that of its peers.

The valuation parity masks operational superiority. CMS generates higher margins, grows faster, and has superior technology, yet trades at similar multiples. This suggests either CMS is undervalued or the market doesn't fully appreciate its competitive advantages.

Looking ahead, the competitive landscape will likely consolidate further. The end state might be 2-3 national players controlling 80%+ of the organized market, with CMS holding the dominant position. The question isn't if this will happen, but how quickly and profitably CMS can capture share during the transition.

XI. Financials & Investment Case (25–35 min)

The numbers tell a story of remarkable consistency in an inconsistent world. Company revenue and net profit have grown at a CAGR of 11% and 31% respectively in the last 3 years. In a business handling physical cash—supposedly dying—these aren't survival metrics; they're dominance indicators.

Revenue from operations marginally declined to Rs 581.49 crore in the December 2024 quarter from Rs 582.30 crore in the same quarter last year, due to slower order execution. Profit before tax in the third quarter of FY25 was at Rs 125.42 crore, up 7.22% as against Rs 116.97 crore reported in the same period a year ago.

But quarterly fluctuations mask structural strength. On a 9-month basis, the company's consolidated net profit fell 7.5% to Rs 274.90 crore despite a 10.25% YoY rise in revenue from operations to Rs 1,805.46 crore in 9M FY25 over 9M FY24. The profit decline reflects investment in technology and expansion rather than operational weakness.

In FY24, the company reported an operating revenue of ₹2,265 crore and a consolidated net profit of ₹347 crore—marking consistent growth from ₹168.5 crore in FY21. The profit trajectory through demonetization, COVID, and digital payment explosion demonstrates antifragility—getting stronger from stress.

The margin profile reveals operational excellence:

EBITDA stood at Rs 160 crore in the December 2024 quarter, registering a growth of 6% YoY. EBITDA margin improved to 27.5% in Q3 FY25, compared to 25.9% reported in the corresponding quarter previous year.

The company is debt free, growing its topline by 20% every quarter and boasts return ratios greater than 25% with an EBITDA margin of almost 30%. These aren't commodity business margins—they're software company margins in a logistics business.

Its return on capital employed (ROCE), excluding cash, stands at an impressive 37%. This ROCE exceeds most celebrated technology companies, yet CMS trades at pedestrian multiples.

The balance sheet strength provides optionality:

₹1,000+ crore in cash on the balance sheet represents nearly 20% of market capitalization—a war chest for acquisitions or a cushion against disruption.

Zero debt means no financial leverage risk. In a business handling others' money, financial conservatism is a competitive advantage. Banks prefer vendors who won't face financial stress.

The order book provides visibility:

As of December 31, 2022, the order book is around INR 3,000 crore. These contracts are of longer duration, ranging from four to seven years, and are expected to generate recurring revenue, thereby providing revenue visibility for the near to medium term.

Multi-year contracts with price escalations protect against inflation while providing predictable cash flows. This isn't a quarter-to-quarter business—it's an annuity disguised as operations.

Working capital dynamics favor CMS. Banks pay promptly for cash management services—they can't afford disruption. Meanwhile, CMS's suppliers (vehicle vendors, fuel companies, technology providers) extend standard credit terms. The result: negative working capital cycles generating cash for growth.

Let's examine the unit economics:

The revenue structure is based on a fee per trip along with a fixed yearly fee. Each ATM generates approximately ₹2-3 lakhs in annual revenue for CMS. With 72,000 ATMs under management, that's ₹1,400-2,100 crores in recurring revenue just from ATM services.

The cost structure is largely variable—fuel, labor, and vehicle maintenance scale with activity. Fixed costs concentrate in technology and management infrastructure, already built and amortized. This operating leverage means incremental revenue drops largely to the bottom line.

Despite a 35% increase in stock price over the last year, CMS trades at a trailing price-to-earnings (P/E) ratio of 24x, well below its 28% earnings growth over the past three years. This presents a compelling valuation for investors seeking long-term growth.

The valuation disconnect is striking. Growth companies with 30% earnings growth typically trade at 35-40x P/E. CMS at 24x implies either: 1. The market doesn't believe the growth is sustainable 2. The market applies a "cash business discount" 3. The company is genuinely undervalued

Management's capital allocation builds confidence:

The board declared an interim dividend of Rs 3.25 per equity share. Current dividend yield is 2.66%. Regular dividends signal confidence in cash generation while retaining capital for growth.

His confidence is backed not just by his leadership position, but also by the fact that he has skin in the game, holding a 6.43% stake in the company. His commitment is underscored by an increase in his personal stake to 6.19% in the past year. When CEOs buy their own stock with personal money, it's the ultimate endorsement.

The investment case crystallizes around several factors:

Structural Growth: The ATM base in India is expected to increase from 255,000 in FY21 to 365,000 by FY27E. CMS captures disproportionate share of new ATMs given its scale advantages.

Margin Expansion: Technology investments reduce cost-to-serve while pricing power remains intact.

Market Share Gains: CMS has increased its share in the ATM cash management business from 39% to 49% over four years. Another 10 percentage points of share gains seems achievable.

Adjacency Expansion: Remote monitoring, debt collection, and bullion logistics offer new revenue pools without significant new investment.

Cash Generation: CAGR in FCF (FY21-24E) funds both growth and returns to shareholders.

The risks are real but manageable: - Digital payment adoption could accelerate beyond expectations - Regulatory changes could compress margins - Competition could intensify with irrational pricing - Key person risk with Rajiv Kaul's central role

But the margin of safety appears substantial. Even if cash usage plateaus, cost optimization and market share gains can drive earnings growth. If cash continues growing with GDP, the upside is substantial.

At current valuations, investors aren't paying for growth—they're getting it for free. The market prices CMS like a declining cash handler. The reality is a growing platform company with expanding moats and multiplying opportunities.

XII. Playbook: Business Lessons & Strategy Insights (20–30 min)

The Contrarian Bet: Building for Physical Infrastructure When Everyone Goes Digital

In 2009, when Rajiv Kaul left Microsoft to join CMS, his tech industry friends thought he'd lost his mind. Why leave the digital future for physical cash? The decision seemed like career suicide—trading software's infinite scalability for trucks, vaults, and armed guards.

Fifteen years later, that contrarian bet looks genius. While hundreds of fintech startups fought over digital payments' 10% of transaction value, CMS quietly dominated the 90% that remained physical. The lesson: the biggest opportunities often lie where nobody's looking.

For Kaul, a seasoned professional, joining CMS was an entrepreneurial bet. I think there is a huge domestic opportunity. If you look at the domestic market, there are three large players—IBM, TCS and Wipro. After Wipro, there is a huge gap and enough room for another player to emerge in the domestic market and that's what we are aiming at.

Consolidation Playbook: How to Win When an Industry is Restructuring

CMS's consolidation strategy wasn't about predatory pricing or aggressive acquisition. It was about patience and preparation. While competitors struggled with compliance costs, CMS invested in technology. While others cut service quality to maintain margins, CMS expanded coverage.

The playbook had four elements:

1. Build Scale Before You Need It: CMS expanded its network during downturns when assets were cheap and competitors were retrenching.

2. Invest in Compliance as Competitive Advantage: Every new regulation was viewed not as a cost but as a barrier to entry.

3. Let Competitors Exit Gracefully: CMS often hired talent from exiting competitors, preserving industry knowledge while eliminating competition.

4. Technology as Force Multiplier: Not technology for its own sake, but technology that specifically addressed Indian market realities.

The Power of Boring: Why Unsexy Businesses Can Be Great Investments

Warren Buffett loves boring businesses, and CMS validates why. Cash logistics has zero glamour. No magazine covers feature cash van drivers. No business school cases study ATM replenishment optimization. Yet:

Return on capital employed (ROCE), excluding cash, stands at an impressive 37%. Most "exciting" tech companies would kill for these returns.

Boring businesses have hidden advantages: - No talent wars: The best engineers chase AI startups, not cash management - Limited competition: Ambitious entrepreneurs ignore unglamorous sectors - Pricing power: Customers care more about reliability than cost - Stable demand: Boring needs don't disappear in recessions

Technology as Enabler, Not Disruptor: Using AI/IoT to Enhance Traditional Services

CMS never positioned technology as replacing human operations. Instead, technology amplified human capability. The cash van driver still drives, but GPS ensures optimal routing. The vault custodian still counts, but machines verify accuracy. The security guard still watches, but AI flags anomalies.

We have integrated technology within the operational process by automating tasks and eliminating manual risks with in-house solutions customized for the Indian market.