Cholamandalam Finance: The Story of India's Vehicle Finance Giant

I. Introduction & Cold Open

The numbers tell a remarkable story: Assets under management standing at Rs 1,99,876 crore as of March 2025, serving more than 54,000 employees across 1,387 branches, with the majority positioned strategically in smaller towns across India. This is Cholamandalam Investment and Finance Company Limited—a financial powerhouse that has quietly become one of India's most formidable non-banking financial companies.

But the story of Cholamandalam, or "Chola" as it's affectionately known in financial circles, isn't just about numbers. It's a tale of transformation, resilience, and strategic vision that spans nearly five decades. How did a company that began as an equipment financing startup in 1978 evolve into India's dominant vehicle and SME lending powerhouse? How did it navigate economic liberalization, global financial crises, failed partnerships, and intense competition to emerge stronger each time?

The answer lies in a unique combination of factors: the century-old trust of the Murugappa Group heritage, a contrarian bet on rural India when others chased metros, a driver-to-owner philosophy that transformed millions of lives, and an uncanny ability to spot opportunities where others saw only risk. Almost half of CIFCL's clients are in low-income states and 80 percent of them are first-time buyers or drivers-turned-owners—a testament to the company's mission of financial inclusion long before it became fashionable.

This is the Acquired-style deep dive into Cholamandalam Finance—a company that has mastered the art of lending in India's most challenging markets, built distribution moats that competitors struggle to replicate, and created a playbook for profitable growth in the NBFC sector. We'll explore how a Chennai-based conglomerate's financial arm became the bridge between India's informal economy and its formal financial system, enabling millions to "enter a better life"—the company's enduring mission.

From the dusty roads where truck drivers dream of ownership to the bustling small towns where SMEs seek growth capital, from boardroom battles with global banking giants to technology-driven transformations, this is the comprehensive story of how Cholamandalam became synonymous with vehicle finance in India. It's a story of patient capital meeting urgent needs, of traditional values embracing modern technology, and ultimately, of how understanding India's unique socio-economic fabric can create extraordinary business outcomes.

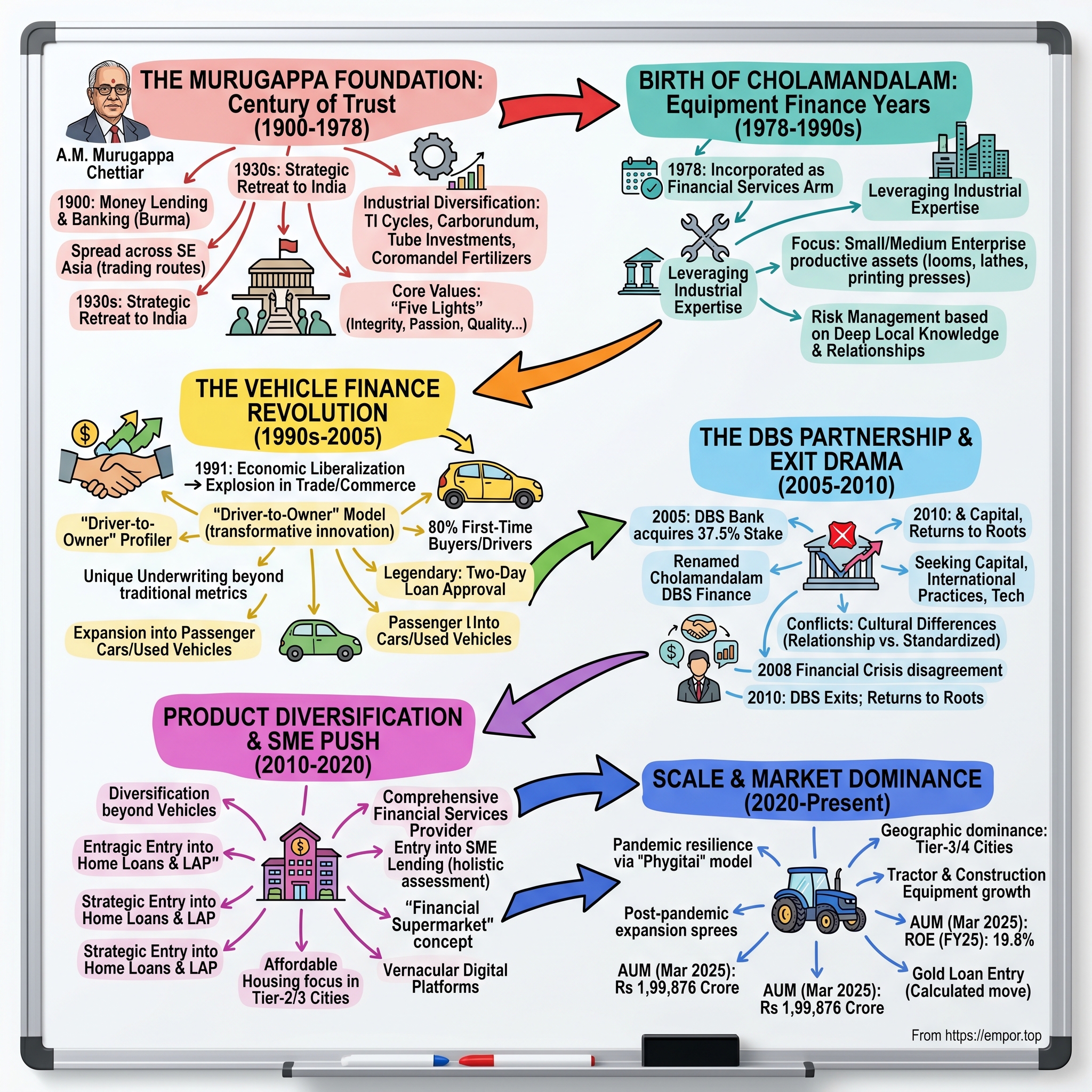

II. The Murugappa Foundation: A Century of Trust (1900-1978)

To understand Cholamandalam's DNA, we must first journey back to the dawn of the 20th century, to the entrepreneurial vision of Dewan Bahadur A.M. Murugappa Chettiar. In 1900, when India was still under British colonial rule, Murugappa Chettiar established what would become one of India's most enduring business empires. The foundation wasn't laid in the comfort of Indian shores but in the challenging terrain of Moulmein, Burma (now Myanmar), where he started a money-lending and banking business.

This wasn't merely a local operation. The Murugappa enterprise quickly spread its wings across the colonial trading routes—to British Malaya, Ceylon (now Sri Lanka), Dutch East Indies, and French Indo-China. The Chettiars, a merchant banking community from Tamil Nadu, had long been the informal bankers of Southeast Asia, financing trade and commerce across the region. Murugappa Chettiar was building on this tradition but with a vision that would outlast empires.

The 1930s brought dramatic change. As political winds shifted and nationalism rose across Asia, the Murugappa business made a strategic retreat to India. This wasn't a defeat but a homecoming that would lay the foundation for industrial greatness. The group's return to Indian soil coincided with the country's nascent industrialization, and Murugappa was perfectly positioned to capitalize on this transformation.

What followed was a remarkable diversification that would make any modern conglomerate envious. TI Cycles became India's bicycle giant, eventually commanding over 50% market share. Carborundum Universal emerged as a leader in abrasives and ceramics. Tube Investments pioneered precision steel tubes. Coromandel International transformed Indian agriculture through fertilizers. Each business wasn't just about profits; it was about nation-building, about providing products that India needed for its development journey.

But what truly set the Murugappa Group apart was its value system—the "Five Lights" that would guide every business decision: integrity, passion, quality, respect, and responsibility. These weren't just corporate buzzwords inscribed in annual reports. They were lived principles that governed how the group dealt with stakeholders, from the smallest supplier to the largest customer. This reputation for ethical business practices would become crucial when the group decided to enter financial services.

The company is part of the Murugappa Group, a prominent Chennai-based conglomerate founded in 1900. With a $9.3 billion portfolio, the group spans three sectors with 29 businesses and nine listed companies. It operates 113 manufacturing sites in 50 countries and employs over 83,000 people. By the 1970s, the Murugappa Group had established itself as one of South India's premier business houses, with a reputation that extended far beyond Tamil Nadu.

The decision to enter financial services in 1978 wasn't random. India was at an inflection point. The economy was slowly opening up, industrialization was accelerating, and there was a massive gap in equipment financing. Banks were conservative, focused on large corporates, and had little appetite for the kind of asset financing that small and medium businesses desperately needed. The Murugappa Group saw an opportunity to leverage its industrial expertise and reputation to fill this void.

The group's century-long journey from colonial-era money lending to modern industrial conglomerate had taught valuable lessons: the importance of trust in financial transactions, the need to understand local markets deeply, the value of patient capital, and the power of relationships over mere transactions. These lessons would prove invaluable as Cholamandalam Investment and Finance Company was born.

The timing was also significant. 1978 marked a period when India's non-banking financial sector was still in its infancy. The regulatory framework was evolving, competition was limited, and the opportunity to define the market was immense. The Murugappa Group wasn't just launching another business; it was creating a new model for how financial services could be delivered in India.

What's remarkable about this foundation story is how the group's industrial heritage would become Cholamandalam's secret weapon. Unlike pure-play financial companies, Chola understood machines, equipment, and the businesses that used them. They knew the depreciation curves of different assets, the maintenance requirements, the resale values. This deep domain knowledge would give them an edge in risk assessment that no amount of financial modeling could replicate.

The Murugappa ethos also meant that Cholamandalam would approach lending differently. This wasn't going to be about maximizing interest rates or aggressive recovery practices. It was about enabling businesses to grow, about being a partner in India's economic development. The company's eventual tagline—"Enabling customers to enter a better life"—wasn't marketing speak; it was a continuation of the Murugappa mission that began in 1900.

As we'll see, this foundation—built on trust, industrial expertise, ethical practices, and a deep understanding of India—would prove to be Cholamandalam's greatest asset as it navigated the challenges and opportunities of the next four decades. The company that was incorporated in 1978 as the financial services arm of the Murugappa Group wasn't starting from scratch; it was building on nearly eight decades of reputation, relationships, and business acumen.

III. Birth of Cholamandalam: The Equipment Finance Years (1978-1990s)

Cholamandalam Investment and Finance Company Limited (Chola), incorporated in 1978 as the financial services arm of the Murugappa Group. The late 1970s presented a unique moment in India's economic history. The country was still operating under the License Raj, where government permits determined business expansion, foreign exchange was tightly controlled, and the economy grew at what was derisively called the "Hindu rate of growth"—a mere 3.5% annually. Yet within these constraints, small and medium enterprises were beginning to stir, seeking capital to modernize and expand.

Chola commenced business as an equipment financing company, a deliberate strategic choice that leveraged the Murugappa Group's deep understanding of industrial India. While banks focused on working capital and large project financing, there was a gaping hole in the market for equipment finance. Small textile mills needed power looms, workshops required lathes and drilling machines, small factories needed generators and compressors. These businesses had orders, they had capability, but they lacked the capital to buy productive assets.

The early Cholamandalam team understood something fundamental that many financial institutions missed: equipment financing wasn't just about evaluating balance sheets and cash flows. It was about understanding the equipment itself—its productive capacity, maintenance requirements, resale value, and most importantly, how it fit into the borrower's business model. A textile mill owner in Coimbatore buying a power loom wasn't just acquiring an asset; he was expanding capacity to meet specific orders. Chola's officers, many drawn from the group's industrial businesses, could evaluate these nuances in ways that traditional bankers couldn't.

The company's initial approach was refreshingly hands-on. Rather than waiting for customers to come to them, Chola's officers would visit industrial clusters, understand local business dynamics, and build relationships with equipment dealers and manufacturers. They became trusted advisors, helping businesses choose the right equipment, structure the financing optimally, and even providing guidance on maintenance and operations. This wasn't just lending; it was partnership.

The 1980s brought both challenges and opportunities. India's economy was slowly liberalizing under Rajiv Gandhi's leadership, with reforms in industrial licensing and technology imports. This created a surge in demand for modern equipment as businesses sought to upgrade from outdated machinery. Chola was perfectly positioned to capitalize on this trend. The company's loan book grew steadily, but more importantly, it was building a reputation for reliability and expertise that money couldn't buy.

Risk management in these early years was more art than science. Without sophisticated credit scoring models or extensive bureau data, Chola relied on what might seem quaint today but proved remarkably effective: deep local knowledge, personal relationships, and understanding of business cycles. Loan officers would visit clients regularly, not just for collections but to understand their business health. They knew when the textile season was good, when engineering units got government orders, when monsoons affected agro-processing units. This granular understanding helped them anticipate and manage risks proactively.

The company also pioneered several innovations in equipment financing that would become industry standards. They introduced the concept of hypothecation, where the equipment itself served as collateral while remaining in the borrower's possession—crucial for maintaining business operations. They structured repayments to match business cash flows, with moratoriums during lean seasons and accelerated payments during peak periods. They even created specialized products for different industries, recognizing that a printing press had different financing needs than a construction crane.

But perhaps Chola's most important innovation was in documentation and processes. In an era when loan processing could take months, Chola streamlined approvals to weeks, sometimes days. They simplified documentation, making it accessible to small business owners who were often intimidated by banking bureaucracy. They conducted business in local languages, employed officers from local communities, and built trust through transparency. These might seem like obvious practices today, but in the 1980s, they were revolutionary.

The decision to expand beyond equipment financing came gradually but deliberately. By the late 1980s, Chola's officers were noticing something interesting: many of their equipment finance customers were asking about vehicle loans. The equipment they had financed had helped businesses grow, and now these entrepreneurs needed commercial vehicles to transport raw materials and finished goods. The leap from equipment finance to vehicle finance wasn't just logical; it was inevitable.

The transformation began with commercial vehicles—trucks, tempos, and light commercial vehicles that were essentially productive assets like the equipment Chola had been financing. The company's deep understanding of asset financing, combined with its relationships in industrial clusters, made this transition smooth. But more importantly, Chola was beginning to see a bigger opportunity: India's transportation sector was on the cusp of a revolution.

The groundwork laid during these equipment financing years would prove invaluable. The company had built a culture of understanding assets deeply, of being close to customers, of managing risks through relationships rather than just ratios. It had established systems and processes that could scale. Most importantly, it had earned trust—the Cholamandalam name meant something in small industrial towns across South India.

By the early 1990s, as India stood on the brink of economic liberalization, Cholamandalam had grown from a startup to a respected financial institution with assets under management crossing significant milestones. But this was just the beginning. The company had found its calling in asset financing, developed a unique approach to risk management, and built a distribution network that reached India's productive heartland. The stage was set for what would become one of India's most successful pivots in financial services—the move into vehicle finance that would define Cholamandalam's next three decades.

The equipment finance DNA never left the company, though. Even today, that discipline of understanding assets, of seeing lending as enabling productivity rather than just earning interest, of being partners rather than just lenders, continues to define Cholamandalam's approach. The lessons learned in those early years financing looms and lathes would prove remarkably applicable to financing trucks and tractors, and eventually, to building one of India's most successful NBFCs.

IV. The Vehicle Finance Revolution (1990s-2005)

The year 1991 changed everything. As Finance Minister Manmohan Singh stood in Parliament announcing the dismantling of the License Raj, he wasn't just liberalizing India's economy—he was unleashing forces that would transform how Indians moved goods, people, and dreams across the country's vast geography. For Cholamandalam, this moment represented the opportunity of a lifetime.

Economic liberalization triggered an explosion in trade and commerce. Suddenly, goods needed to move faster and farther than ever before. The old transportation infrastructure—dominated by railways and a handful of large fleet operators—couldn't keep pace with the new India's demands. Small entrepreneurs saw opportunity everywhere: in transporting agricultural produce from farms to cities, in moving manufactured goods from new industrial clusters, in connecting India's tier-2 and tier-3 cities to the mainstream economy. But they needed vehicles, and more importantly, they needed financing.

Cholamandalam's pivot to vehicle finance wasn't a sudden strategic shift—it was an evolution that built naturally on its equipment financing heritage. The company understood something profound: in India, a commercial vehicle wasn't just a mode of transport; it was a ticket to entrepreneurship, a means of social mobility, a family's path from poverty to prosperity. This insight would shape everything that followed.

The company's approach to vehicle finance was radically different from traditional lenders. While banks saw commercial vehicle loans as risky—borrowers often had minimal credit history, limited collateral, and uncertain income streams—Chola saw opportunity. They recognized that a truck driver who had spent years working for fleet operators understood the transportation business intimately. He knew the routes, the rates, the seasonal patterns, the maintenance requirements. What he lacked wasn't capability but capital.

This led to one of Cholamandalam's most transformative innovations: the "driver-to-owner" model. Instead of focusing on established transporters, Chola deliberately targeted first-time buyers, particularly drivers looking to own their first vehicle. 80 percent of them are first-time buyers or drivers-turned-owners. The company developed a unique underwriting approach that considered factors banks ignored: years of driving experience, knowledge of specific routes, relationships with transport contractors, even family support systems.

The execution of this strategy required building an entirely new distribution architecture. Chola couldn't rely on urban branches where truck drivers rarely ventured. Instead, they went where their customers were—transport nagars (transportation hubs), highway dhabas (roadside eateries), spare parts markets, used vehicle markets. Loan officers weren't just credit assessors; they became part of the transportation ecosystem, understanding route economics, freight rates, and seasonal demand patterns.

The company also pioneered what would become legendary in Indian financial services: the two-day loan approval. In an era when getting a vehicle loan from a bank could take weeks or months, Chola promised decisions in 48 hours. This wasn't just about speed; it was about understanding that in the transportation business, time literally meant money. A driver who had identified a good used truck couldn't wait weeks for approval—the opportunity would disappear.

Risk management in vehicle finance required a complete reimagination of traditional banking practices. Chola developed innovative approaches that seem obvious in hindsight but were revolutionary at the time. They created networks of approved mechanics who could assess vehicle condition, established relationships with RTO offices for quick registration transfers, built databases of resale values for different vehicle models across different geographies. They even stationed collection officers at key transport hubs, making it convenient for drivers to pay installments during their regular routes.

The mid-1990s saw Cholamandalam expand beyond commercial vehicles into the broader automotive finance market. The Indian passenger car market was exploding—Maruti had democratized car ownership, and new entrants like Hyundai, Honda, and Ford were entering India. The middle class was growing, aspirations were rising, and the car was becoming the ultimate symbol of having "arrived." Chola leveraged its vehicle finance expertise to enter this market, but with a twist—they focused on used cars and customers in smaller cities, segments that banks largely ignored.

The company's geographic expansion strategy during this period was masterful. While competitors concentrated on metros and large cities, Cholamandalam went deeper into India. They opened branches in places like Gorakhpur, Guntur, and Gwalior—cities that were growing rapidly but remained underserved by formal financial institutions. In these markets, the Cholamandalam brand, backed by the Murugappa reputation, carried immense weight. Local entrepreneurs, transporters, and small business owners trusted Chola in ways they would never trust a faceless national bank.

By the early 2000s, Cholamandalam had established itself as a major force in vehicle finance. The company was financing everything from two-wheelers to heavy commercial vehicles, from new cars to used trucks, from tractors to construction equipment. Each segment required different skills, different risk models, different distribution strategies—but the core philosophy remained constant: understand the asset, understand the customer, understand the business model, and structure financing that works for everyone.

The company also began innovating in product design. They introduced balloon payment schemes for seasonal businesses, step-up EMIs for growing businesses, and even Islamic finance-compliant products for specific communities. They created specialized products for specific segments: loans for school vans with repayment holidays during summer vacations, financing for tourist vehicles with seasonal payment structures, even specialized products for women entrepreneurs entering the transportation business.

Technology adoption during this period, while primitive by today's standards, was progressive for its time. Cholamandalam invested in dealer management systems, automated credit assessment tools, and even early forms of GPS tracking for high-value commercial vehicles. They built databases that tracked payment behaviors across hundreds of thousands of customers, creating proprietary credit scoring models that vastly outperformed generic bureau scores in predicting default rates for their specific customer segments.

But perhaps the most important development during this period was cultural. Cholamandalam had built an organization that thought differently about lending. Employees weren't trained just in finance and credit; they were educated about vehicles, about transportation economics, about the dreams and challenges of their customers. Branch managers were empowered to make decisions based on local knowledge. Collection officers were taught to be counselors, helping customers through difficult periods rather than simply pursuing recoveries.

The numbers tell the story of this transformation. By 2005, Cholamandalam had emerged as one of India's largest vehicle financiers, with a loan book that had grown exponentially, a distribution network that reached hundreds of cities and towns, and most importantly, hundreds of thousands of customers whose lives had been transformed through vehicle ownership. The company that had started as an equipment financier had successfully reinvented itself as India's transportation finance champion.

Yet even as Cholamandalam celebrated this success, the leadership knew that the next phase of growth would require new capabilities, new capital, and perhaps new partnerships. The Indian financial services sector was becoming increasingly competitive, technology was disrupting traditional business models, and customer expectations were evolving rapidly. It was in this context that Cholamandalam would make one of its most controversial decisions—a partnership with one of Asia's largest banks that would test the company's culture, strategy, and resilience in ways no one could have anticipated.

V. The DBS Partnership & Exit Drama (2005-2010)

The announcement in 2005 sent ripples through India's financial services industry. DBS Bank acquired a 37.5% stake in Cholamandalam Investment and Finance Company, with the Murugappa Group lowering its stake to 37.5%. The company was subsequently renamed as Cholamandalam DBS Finance. For many, this seemed like the perfect marriage—a leading Indian NBFC with deep local knowledge partnering with one of Asia's most sophisticated banks. The reality would prove far more complex.

To understand why Cholamandalam sought this partnership, we must examine the competitive landscape of 2005. India's financial services sector was heating up. Foreign banks were expanding aggressively, new private banks like ICICI and HDFC were scaling rapidly, and the vehicle finance market was becoming increasingly crowded. Cholamandalam needed capital to grow, but perhaps more importantly, the leadership believed they needed international best practices, sophisticated risk management systems, and technology capabilities that DBS could provide.

DBS, for its part, saw Cholamandalam as its gateway to Indian retail finance. The Singaporean bank had ambitions of becoming a pan-Asian financial powerhouse, and India, with its vast, underserved market, was crucial to this vision. Rather than building from scratch, partnering with an established player like Cholamandalam seemed like the fastest route to scale. The bank brought more than just capital—it brought decades of experience in retail banking, sophisticated credit models, and technology platforms that were far ahead of what most Indian financial institutions possessed.

The early days of the partnership showed promise. DBS infused fresh capital that allowed Cholamandalam to expand its branch network aggressively. The bank's risk management frameworks helped Chola strengthen its credit assessment processes, introducing concepts like portfolio stress testing, value-at-risk models, and automated credit scoring that were still novel in Indian NBFCs. DBS also brought technological capabilities—core banking systems, customer relationship management platforms, and digital channels that began modernizing Cholamandalam's operations.

Yet beneath the surface, tensions were brewing. The two organizations had fundamentally different DNAs. DBS came from Singapore's orderly, regulated environment where processes were standardized, decisions were data-driven, and risk management was paramount. Cholamandalam had thrived in India's chaotic, relationship-driven market where local knowledge trumped algorithms, where flexibility mattered more than standardization, and where understanding a customer's character often mattered more than their credit score.

These cultural differences manifested in countless daily frictions. DBS executives, many parachuted in from Singapore or Hong Kong, would question why loan officers spent time at transport nagars drinking tea with truck drivers. They couldn't understand why credit decisions sometimes favored long-standing customers with temporary difficulties over new customers with better paper credentials. They were puzzled by Cholamandalam's insistence on maintaining branches in small towns that barely broke even, not recognizing these as investments in future growth and brand building.

The Cholamandalam old guard, meanwhile, watched with growing alarm as DBS-imported policies began affecting the company's core strengths. Standardized credit policies meant less flexibility for branch managers. Centralized decision-making slowed down the legendary two-day approval process. Risk management frameworks designed for Singapore's developed market sometimes excluded good customers who didn't fit neat categories. The company that had built its success on understanding India's unique context was being forced into frameworks designed for very different markets.

The global financial crisis of 2008 became the crucible that tested this partnership. As markets crashed and credit dried up globally, DBS, like many international banks, became extremely risk-averse. The bank wanted to pull back from vehicle finance, seeing it as too risky in an uncertain environment. But Cholamandalam's leadership understood that this crisis was actually an opportunity—competitors were retreating, vehicle prices were dropping, and good customers were available for those willing to lend.

This fundamental disagreement over strategy during the crisis brought tensions to a breaking point. DBS wanted to preserve capital and minimize risk. Cholamandalam wanted to grab market share while competitors retreated. DBS favored urban markets and salaried customers. Cholamandalam's strength lay in rural markets and self-employed borrowers. DBS wanted to build a retail banking franchise. Cholamandalam's DNA was in vehicle and asset finance.

Behind closed doors, heated discussions were taking place. The Murugappa Group leadership realized that while DBS had brought valuable capabilities, the partnership was constraining Cholamandalam's entrepreneurial spirit. The company that had succeeded by understanding India deeply was being homogenized into a generic financial institution. Moreover, post-financial crisis, DBS itself was reconsidering its international expansion strategy, focusing more on Southeast Asian markets it understood better.

The resolution came in 2010 with an announcement that surprised few insiders: DBS Bank sold its entire stake back to Murugappa Group and exited the joint venture. The official statements spoke of strategic realignment and mutual agreement, but the message was clear—the partnership that had promised so much had failed to deliver for both parties.

Yet this wasn't a story of complete failure. The five years with DBS had transformed Cholamandalam in important ways. The company had absorbed international best practices in risk management that would serve it well in the coming decades. It had modernized its technology infrastructure, building capabilities that would have taken years to develop independently. Most importantly, it had learned valuable lessons about the importance of maintaining cultural authenticity while adopting global standards.

The immediate post-DBS period required careful management. Cholamandalam had to reassure employees, customers, and investors that the exit of a major international partner wouldn't affect its stability or growth plans. The company dropped the "DBS" from its name, reverting to Cholamandalam Investment and Finance Company, and launched a careful rebranding exercise that emphasized its Indian roots and customer-first philosophy.

Internally, there was a palpable sense of relief and renewed energy. Branch managers felt empowered again to make decisions based on local knowledge. The company could return to its core strength of understanding and serving India's unique markets. The focus shifted back to vehicle finance and asset financing, areas where Cholamandalam had built genuine competitive advantages.

The leadership also conducted a thorough review of what worked and what didn't during the DBS years. They retained the valuable additions—robust risk management frameworks, technology platforms, systematic training programs—while discarding elements that didn't fit India's context. This selective adoption of international practices while maintaining local relevance would become a hallmark of Cholamandalam's strategy going forward.

Financial performance in the immediate aftermath vindicated this approach. Freed from the constraints of the partnership, Cholamandalam aggressively expanded in its core markets. The company's understanding of the post-crisis opportunity proved correct—while competitors remained cautious, Chola gained market share by lending to good customers others were avoiding. Asset quality remained strong because the company's relationship-based model meant it could distinguish between temporary difficulties and fundamental credit problems.

The DBS episode also taught Cholamandalam important lessons about partnerships and foreign investment. The company learned that while foreign partners could bring valuable capabilities, maintaining strategic and cultural alignment was crucial. It reinforced the importance of patient capital that understood long-term value creation over short-term profit maximization. Most importantly, it validated the Murugappa Group's belief that deep local knowledge and relationships were sustainable competitive advantages that no amount of technology or sophisticated models could replace.

Looking back, the DBS partnership years represented a critical inflection point in Cholamandalam's journey. It was a period of learning, adaptation, and ultimately, reaffirmation of core values. The company emerged stronger, more sophisticated, yet more committed than ever to its founding mission of enabling customers to enter a better life. The stage was now set for the next phase of growth—one that would see Cholamandalam not just return to its roots but expand beyond vehicle finance into new frontiers of financial services.

VI. Product Diversification & SME Push (2010-2020)

The year 2010 marked a new beginning for Cholamandalam. Free from the constraints of the DBS partnership and armed with lessons learned from that experience, the company embarked on its most ambitious transformation yet. The vision was clear: evolve from a vehicle finance specialist to a comprehensive financial services provider offering vehicle finance, home loans, home equity loans, SME loans, investment advisory services, stock broking and a variety of other financial services to customers.

This diversification wasn't random experimentation—it was a carefully orchestrated strategy that built on Cholamandalam's core strengths while addressing adjacent opportunities. The company's leadership recognized that their existing customer base of vehicle owners, small businessmen, and entrepreneurs had financial needs beyond vehicle loans. Why should a transporter who trusted Chola for his truck financing go to another institution for working capital? Why should an SME owner who had built a relationship with Chola over years seek property loans elsewhere?

The push into SME lending became the cornerstone of this diversification strategy. India's SME sector—contributing nearly 30% of GDP and employing millions—remained chronically underserved by formal financial institutions. Banks found SME lending operationally intensive and risky. Cholamandalam saw an opportunity to leverage its deep understanding of small businesses, gained through decades of vehicle and equipment financing, to serve this market.

The company's approach to SME lending was characteristically different from traditional models. Instead of relying solely on financial statements and collateral, Chola developed a holistic assessment framework that considered business vintage, market reputation, supply chain relationships, and entrepreneurial capability. Loan officers were trained not just in credit assessment but in understanding different industries—how a rice mill operated, what working capital cycles looked like for textile traders, how seasonal patterns affected agro-processing units.

The SME loan product evolved to offer remarkable flexibility—loans ranging from Rs 10 lakhs to Rs 5 crores, tenures adapted to business cycles, and structures that could accommodate everything from working capital needs to expansion financing. But what truly differentiated Cholamandalam was speed and simplicity. While banks took weeks to process SME loans through multiple committees, Chola promised decisions in days, sometimes hours for existing customers.

Simultaneously, the company made a strategic entry into property-backed lending—home loans and loans against property (LAP). This wasn't an attempt to compete with housing finance giants like HDFC or LIC Housing. Instead, Cholamandalam focused on underserved segments: affordable housing in tier-2 and tier-3 cities, self-employed individuals without formal income proof, and properties in locations that traditional lenders avoided.

The company has recently forayed into affordable housing loans for low-income customers. This affordable housing initiative deserves special attention. While others chased high-ticket loans in metros, Cholamandalam built capabilities to assess and finance homes worth Rs 10-25 lakhs in places like Madurai, Vijayawada, and Nashik. They understood that a small businessman buying his first home in a tier-3 city was often a better credit risk than a salaried employee stretching to buy an expensive apartment in Mumbai.

The loan against property business leveraged Cholamandalam's existing customer relationships brilliantly. SME owners who needed growth capital but didn't want to dilute equity could unlock value from their properties. The company's deep local presence meant they could assess property values in markets where others had no presence. Their relationship-based model meant they understood the borrower's business and could structure loans appropriately.

Technology became a critical enabler of this diversification. The company invested heavily in digital infrastructure, but with a uniquely Indian twist. While building state-of-the-art loan origination systems and mobile apps, they also ensured these worked on basic smartphones with patchy internet connections. They created vernacular interfaces so customers could apply in Tamil, Telugu, or Hindi. They built systems that could handle the complexity of Indian documentation—from handwritten rent receipts to village panchayat certificates.

The company pioneered several technological innovations that would later become industry standards. They introduced tablet-based loan applications that officers could complete at the customer's location. They built algorithms that could assess creditworthiness using alternative data—utility payment histories, GST returns, even social media profiles. They created automated valuation models for vehicles and properties in hundreds of micro-markets across India.

But perhaps the most innovative use of technology was in creating an integrated ecosystem. A customer who had taken a vehicle loan could seamlessly apply for insurance, investment products, or additional loans through the same platform. The company built what they called a "financial supermarket" for their core customer base—the aspiring middle class and small business India.

The Consumer and Small Enterprise Loans (CSEL) product launched during this period represented another frontier. These were smaller ticket loans—Rs 50,000 to Rs 5 lakhs—for diverse needs from business expansion to education to medical emergencies. What made this product successful was Cholamandalam's ability to assess risk through relationships and data. A vegetable vendor who had successfully paid off a three-wheeler loan was a good risk for a small business loan. A driver who had graduated to owner-operator had proven entrepreneurial capability.

The Secured Business and Personal Loans (SBPL) product targeted a specific niche—business owners who needed personal loans but could offer business assets as collateral. This hybrid product recognized the reality of Indian small business where personal and business finances were often intertwined. A shop owner could borrow for his daughter's education against his shop inventory, or a small manufacturer could raise funds for his son's foreign education against machinery.

Throughout this diversification, Cholamandalam maintained strict risk management discipline. Each new product went through extensive pilot phases, starting in select geographies with limited exposure. The company built specialized credit teams for different products, ensuring expertise wasn't diluted. They also maintained portfolio limits, ensuring no single product or segment could endanger overall stability.

The distribution strategy evolved to support this multi-product approach. Branches were redesigned from transaction centers to relationship centers. Staff were trained to identify cross-selling opportunities—a customer coming for vehicle insurance might need a top-up loan, someone repaying a truck loan might be ready for home finance. The company also pioneered the concept of "financial health check-ups" where officers would review a customer's entire financial situation and suggest appropriate products.

Partnerships became crucial for scaling the diversified portfolio. Cholamandalam tied up with manufacturers for vendor financing programs, with e-commerce platforms for consumer loans, with hospitals for medical equipment financing. Each partnership was carefully structured to leverage Chola's financing capability while relying on the partner's industry expertise and customer access.

The results of this diversification were impressive. By 2020, while vehicle finance remained the largest contributor, the company had built substantial books in home loans, LAP, SME loans, and other products. More importantly, they had transformed from a monoline vehicle financier to a comprehensive financial services provider. Customer lifetime value increased dramatically as relationships deepened across multiple products.

The decade also saw Cholamandalam building capabilities that would prove crucial for future growth. They developed expertise in analyzing GST data for credit assessment, critical after the 2017 GST implementation. They built early capabilities in digital lending, partnering with fintech companies to reach new customer segments. They even experimented with blockchain for supply chain financing and artificial intelligence for collection optimization.

Yet through all this transformation, Cholamandalam never lost sight of its core philosophy. Every new product was evaluated not just for profitability but for its potential to improve customers' lives. The company that had enabled drivers to become owners now enabled small businesses to grow, families to own homes, and entrepreneurs to realize dreams. The mission of enabling customers to "enter a better life" had found new expressions in new products, but the underlying commitment remained unchanged.

VII. Scale & Market Dominance (2020-Present)

The COVID-19 pandemic of 2020 should have been catastrophic for a lender focused on vehicle finance and SME lending. With lockdowns paralyzing transportation, small businesses shuttered, and economic uncertainty at unprecedented levels, many predicted a bloodbath in the NBFC sector. Yet Cholamandalam not only survived but emerged stronger, using the crisis as a catalyst to accelerate its transformation into one of India's most formidable financial institutions.

The immediate response to the pandemic showcased the strength of Cholamandalam's relationship-based model. While competitors relied on call centers and digital channels that felt impersonal during crisis, Chola's field officers maintained contact with customers, understanding individual situations and offering customized solutions. The company quickly rolled out moratoriums for affected customers but, crucially, stayed engaged to distinguish between temporary disruptions and fundamental business failures.

What happened next surprised even industry veterans. As the economy reopened, Cholamandalam went on an aggressive expansion spree while others remained cautious. The logic was counterintuitive but brilliant: the pandemic had accelerated formalization of the economy, created pent-up demand for commercial vehicles as e-commerce boomed, and weakened smaller competitors who couldn't weather the storm. Cholamandalam had the capital, the distribution, and most importantly, the confidence to seize this opportunity.

The numbers tell a remarkable story of this post-pandemic expansion. As of 2024, the company has 1,387 branches across the country and more than 54,000 employees, with the majority being in smaller towns. But these aren't just statistics—they represent a fundamental reimagination of financial services distribution in India. Each branch is positioned strategically, not in expensive high streets but in locations accessible to truck drivers, small business owners, and farmers.

The company plans to expand further in these states and in rural and semi-urban geographies. This geographic strategy has been masterful. While competitors fight over market share in saturated urban markets, Cholamandalam has quietly built dominance in India's real growth markets—the tier-3 and tier-4 cities where economic activity is exploding as infrastructure improves and digital connectivity spreads.

The vehicle finance business, Cholamandalam's traditional stronghold, has reached unprecedented scale. The company now finances across the entire spectrum—from two-wheelers that represent aspiration for millions of Indians to heavy commercial vehicles that form the backbone of India's logistics industry. Each segment requires different capabilities, and Cholamandalam has built specialized expertise for each.

In commercial vehicles, covering the 1.5-tonne to 49-tonne gross vehicle weight range, Cholamandalam has become the partner of choice for fleet operators and first-time buyers alike. The company's understanding of route economics, freight rates, and utilization patterns is unmatched. They know that a truck operating on the Delhi-Mumbai route has different economics than one serving rural Maharashtra. This granular knowledge translates into better risk assessment and more appropriate loan structuring.

The used vehicle financing business has become a particular area of strength. While others shy away from the complexity of assessing used vehicle values and conditions, Cholamandalam has built sophisticated capabilities including networks of certified evaluators, partnerships with OEMs for certified pre-owned programs, and databases tracking resale values across thousands of models and locations. This has opened up vehicle ownership for millions who cannot afford new vehicles but need reliable transportation.

The tractor and construction equipment financing business leverages India's agricultural modernization and infrastructure boom. Cholamandalam doesn't just finance tractors; they understand cropping patterns, government subsidy programs, and rental markets for agricultural equipment. Similarly, in construction equipment, they comprehend utilization rates, project cycles, and the intricate ecosystem of contractors and sub-contractors that drives India's construction industry.

Assets under management as of 31st December 2024, stood at Rs 1,89,141 crore as compared to Rs 1,41,143 crore as of 31st December 2023, clocking a growth of 34% YoY. This explosive growth hasn't come at the cost of asset quality. The company has maintained strong portfolio quality through a combination of careful underwriting, proactive monitoring, and effective collection strategies.

Technology deployment has accelerated dramatically in this period. Cholamandalam has built what they call a "phygital" model—combining physical presence with digital capabilities. Customers can apply for loans online, but a field officer will visit for vehicle inspection. Documentation can be uploaded digitally, but relationship managers remain available for consultation. This hybrid model provides the convenience of digital with the trust of human interaction.

The company's digital initiatives have been particularly innovative. They've launched entirely digital loan products for existing customers, where approvals happen in minutes based on repayment history. They've created WhatsApp-based services for everything from EMI payments to insurance renewals. They've even built augmented reality tools that help customers visualize vehicles and calculate loan options.

But perhaps the most significant development has been Cholamandalam's emergence as a platform rather than just a lender. The company now offers insurance, investments, and payment solutions, creating a comprehensive financial ecosystem for its customers. A truck owner can finance his vehicle, insure it, invest his surplus, and even get working capital, all through Cholamandalam. This platform approach increases customer stickiness and lifetime value while reducing acquisition costs.

The SME lending business has evolved into a sophisticated operation. Cholamandalam now uses GST data, bank statement analysis, and even satellite imagery (to assess factory utilization) for credit assessment. They've built industry-specific credit models—understanding that a textile unit has different risk profiles than a food processing plant. They've also created supply chain financing solutions, funding vendors and dealers of large corporates.

Recent financial performance validates this strategy. Aggregate disbursements in Q3FY25 were at Rs 25,806 crore as against Rs 22,383 crore in Q3FY24 registering a growth of 15%. More impressively, PBT Growth for FY25 was at 25%. PBT-ROA for FY25 was at 3.3%. ROE for FY25 was at 19.8%. These metrics place Cholamandalam among the most profitable and efficient financial institutions in India.

The recent announcement of entry into gold loans signals continued evolution. New gold loan business disbursed Rs 100 crore in its initial phase, but this represents a significant opportunity. Gold loans are a massive market in India, traditionally dominated by unorganized players. Cholamandalam's brand trust and distribution network position it well to capture share in this market.

Looking at the competitive landscape, Cholamandalam has carved out a unique position. Unlike Bajaj Finance, which focuses on urban consumption finance, or Shriram Finance, which concentrates on used commercial vehicles, Cholamandalam has built a diversified portfolio serving multiple customer segments across geographies. This diversification provides resilience while maintaining focus on core competencies.

The international investment community has taken notice. IFC, a member of the World Bank Group, has anchored an investment round of $222 million into Cholamandalam Investment and Finance Company Ltd (CIFCL) to help expand access to finance for micro and small borrowers, especially in the rural and semi-urban parts of India. Of the total amount, $92 million is from IFC's own account and the rest syndicated from First Abu Dhabi Bank ($50 million), MUFG Bank Ltd ($50 million), National Bank of Ras Al-Khaimah PJSC ($20 million), and CTBC Bank Co., Ltd ($10 million). This international validation and capital access provides ammunition for continued growth.

The leadership transition has been smooth, with Ravindra Kumar Kundu appointed as Managing Director for a period of five years with effect from October 7, 2024. Kundu currently serves Cholamandalam Investment and Finance Company as its Executive Director. Under his leadership, Assets Under Management (AUM) grew to Rs 1,53,000 cr in FY'24 from Rs 67,000 cr in FY'20, demonstrating continuity in vision and execution.

As we stand in 2024, Cholamandalam isn't just a large NBFC—it's become critical infrastructure for India's economic growth. The company finances the trucks that move India's goods, the tractors that modernize its agriculture, the equipment that builds its infrastructure, and the small businesses that employ millions. With Assets under management as of 31st March 2025, stood at Rs 1,99,876 crore, crossing the significant Rs 2 lakh crore milestone seems imminent.

VIII. Playbook: The Chola Method

After nearly five decades of evolution, Cholamandalam has developed a distinctive playbook that sets it apart in India's competitive financial services landscape. This isn't just about financial metrics or market share—it's about a fundamental philosophy of how to build a sustainable lending business in one of the world's most complex markets. The "Chola Method" combines deep market understanding, relationship-based lending, and strategic positioning in ways that competitors struggle to replicate.

The cornerstone of Cholamandalam's strategy is its deep rural and semi-urban distribution. While competitors cluster in metros where acquisition costs are high and competition fierce, Chola has built an enviable presence in India's real growth markets. Almost half of CIFCL's clients are in low-income states and 80 percent of them are first-time buyers or drivers-turned-owners. The company plans to expand further in these states and in rural and semi-urban geographies. This isn't just about being present—it's about becoming embedded in local economies.

Consider a typical Cholamandalam branch in a place like Sitapur in Uttar Pradesh or Shimoga in Karnataka. The branch manager isn't just a banker; he's part of the local business ecosystem. He knows the transport contractors, the agricultural traders, the small manufacturers. He understands that the local economy peaks during harvest season, that transport demand spikes during festival times, that small businesses need working capital before the wedding season. This hyperlocal knowledge translates into better credit decisions and stronger customer relationships.

The relationship-based lending model that Cholamandalam has perfected stands in stark contrast to the algorithmic approach of many modern lenders. While fintech companies pride themselves on instant, algorithm-based decisions, Chola understands that in India's informal economy, relationships and local knowledge often matter more than credit scores. A transport contractor's reputation at the local transport nagar, a farmer's standing in his village, a small businessman's relationships with suppliers—these soft factors often predict repayment better than financial ratios.

This doesn't mean Cholamandalam ignores data or technology. Instead, they've created a unique synthesis where technology amplifies human judgment rather than replacing it. Their credit scoring models incorporate both traditional financial metrics and alternative data sources, but the final decision often involves human assessment of factors no algorithm can capture. This hybrid approach has resulted in portfolio quality that consistently outperforms purely automated lending models.

The "driver-to-owner" ecosystem approach represents one of Cholamandalam's most successful innovations. The company doesn't just provide loans; it enables economic transformation. A driver taking his first loan for a used commercial vehicle receives not just financing but guidance on route selection, maintenance schedules, and insurance. As he succeeds, Cholamandalam helps him upgrade to a new vehicle, then perhaps a second vehicle, eventually building a small fleet. Many of today's successful fleet operators started their journey with a single Cholamandalam loan.

This ecosystem thinking extends beyond individual customers. Cholamandalam has built networks that create value for all participants. They connect vehicle sellers with buyers, mechanics with vehicle owners, and transporters with cargo providers. They organize driver training programs, health camps at transport nagars, and even facilitate marriages within the transport community. This deep engagement creates switching costs that go far beyond financial considerations.

Technology deployment follows a distinctly practical approach. "Digitally-enabled financial services are a key driver for the nation-building efforts of the government." Cholamandalam has invested heavily in digital infrastructure but always with an eye on what works in Indian conditions. Their loan origination system works on basic smartphones with 2G connections. Their apps support vernacular languages and voice inputs for customers who aren't literate. Their collection systems integrate with local payment methods from post office transfers to village banking correspondents.

The company has also pioneered what might be called "appropriate innovation"—solutions that fit Indian realities rather than importing Western models. For instance, their vehicle tracking systems don't just monitor location for recovery purposes; they provide drivers with route optimization suggestions and alert them to nearby fuel stations with better prices. Their customer service doesn't just handle complaints; representatives proactively call before EMI dates to remind customers and help arrange payments if needed.

Cross-selling within the Murugappa ecosystem provides another competitive advantage. A customer buying Tube Investments cycles might need financing. A Coromandel fertilizers dealer requires working capital. A contractor using Carborundum abrasives needs equipment loans. These warm leads, backed by the Murugappa reputation, provide low-cost customer acquisition opportunities that standalone NBFCs can't match.

Managing asset quality through cycles has become a core competency. India's economy is volatile—monsoons affect agricultural income, government policies impact transport demand, and global factors influence commodity prices. Cholamandalam has developed sophisticated early warning systems that detect stress before it manifests in defaults. They track leading indicators like freight rates, capacity utilization at transport hubs, and even diesel consumption patterns to anticipate problems.

When stress does emerge, the response is calibrated and nuanced. Rather than aggressive recovery that might destroy customer relationships and businesses, Cholamandalam typically works with customers to restructure loans, providing breathing room during difficult periods. This approach might seem soft, but it's actually hardheaded business sense—a customer who survives a crisis with Chola's help becomes a loyal advocate, often bringing referrals worth far more than any short-term recovery.

Capital allocation reflects a long-term value creation philosophy rooted in the Murugappa tradition. The company maintains strong capital adequacy ratios—The Capital Adequacy Ratio (CAR) of the company as of 31st December 2024, was at 19.76% as against the regulatory requirement of 15%. Tier-I Capital was at 14.92%—providing a buffer for growth and stress. Dividend policy balances shareholder returns with reinvestment needs. The company declared an interim dividend of Rs 1.30 per share (65%) for the FY25, demonstrating commitment to consistent shareholder returns.

The organizational culture deserves special attention. Cholamandalam has created what might be called a "merchant banking" culture—employees think like business partners, not just lenders. Loan officers are trained to understand businesses, not just evaluate collateral. Collection teams are taught to preserve relationships while ensuring recovery. This culture is reinforced through incentive structures that reward long-term portfolio quality over short-term disbursement targets.

Training and development programs reflect this philosophy. New recruits don't just learn credit assessment; they spend time at transport nagars understanding vehicle economics. They visit small businesses to comprehend working capital cycles. They even spend time with customers, understanding their aspirations and challenges. This immersive training creates employees who can make nuanced decisions that pure classroom training could never enable.

The risk management framework balances entrepreneurial aggression with prudential conservatism. Every new product or geography goes through extensive pilots. Portfolio limits ensure diversification. Stress testing examines extreme scenarios. But within these guardrails, teams have significant autonomy to innovate and take calculated risks. This balance has allowed Cholamandalam to grow rapidly while maintaining asset quality.

Perhaps most importantly, the Chola Method maintains unwavering focus on the core mission: enabling customers to enter a better life. Every decision—from product design to collection strategies—is evaluated through this lens. This isn't corporate rhetoric but operational reality. Branch managers are measured not just on business metrics but on customer transformation stories. Annual reports feature customers who've grown from single vehicle owners to fleet operators, from small traders to established businesses.

This playbook isn't easily replicable. It requires patient capital willing to invest in distribution and relationships over years. It demands organizational commitment to serving challenging customer segments. It needs leadership that understands India's complexity and diversity. Most critically, it requires a value system that sees financial services as a means to enable economic progress, not just generate returns.

IX. Bull vs. Bear Case & Competitive Analysis

As Cholamandalam stands at the cusp of potentially crossing Rs 2 lakh crore in assets under management, investors and analysts are sharply divided on the company's future trajectory. The bull case sees an unstoppable force in Indian financial services, while bears worry about mounting challenges in an evolving landscape. Let's examine both perspectives with the rigor they deserve.

The Bull Case: A Decade of Unprecedented Growth Ahead

The optimists see Cholamandalam positioned perfectly for India's economic transformation. India's commercial vehicle market, despite recent growth, remains significantly under-penetrated compared to developed economies or even China. With the government's massive infrastructure push—from highways to dedicated freight corridors—demand for commercial vehicles is set to explode. Cholamandalam, with its dominant position in CV financing and deep understanding of the transport ecosystem, stands to capture a disproportionate share of this growth.

The formalization of India's economy presents another massive opportunity. As GST compliance improves and digital payments become ubiquitous, millions of small businesses are entering the formal credit system for the first time. These businesses—previously invisible to traditional lenders—are perfect candidates for Cholamandalam's relationship-based lending model. The company's ability to assess creditworthiness using alternative data and local knowledge gives it a sustainable advantage in serving this segment.

India's infrastructure and logistics boom is just beginning. The government's PM Gati Shakti program, aimed at multimodal connectivity, will require massive equipment financing. The production-linked incentive schemes are driving manufacturing growth, creating demand for industrial equipment and commercial vehicles. The push toward electric vehicles, rather than being a threat, represents an opportunity for Cholamandalam to finance the transformation of India's transport fleet.

The SME formalization trend accelerates Cholamandalam's growth prospects. As businesses register for GST, maintain digital records, and build credit histories, they become viable lending targets. Cholamandalam's early investments in understanding GST data and building SME-specific credit models position it ahead of competitors who are still learning this market.

The company's superior execution capabilities set it apart. ROE for FY25 was at 19.8%, among the best in the industry, demonstrating exceptional capital efficiency. The ability to maintain high returns while growing rapidly is rare in financial services. This execution excellence stems from decades of experience, refined processes, and most importantly, a culture that balances growth with risk management.

Parent group backing provides both stability and opportunities. The Murugappa Group's century-old reputation opens doors that remain closed to standalone NBFCs. The group's commitment to ethical business practices attracts customers who value trust over marginal price differences. Access to patient capital means Cholamandalam can make long-term investments in distribution and technology that quarterly earnings-focused companies cannot.

Governance standards at Cholamandalam are exemplary. In an industry often tainted by aggressive practices and regulatory issues, Cholamandalam's clean track record stands out. This isn't just about compliance—it's about building a sustainable business that regulators trust, customers respect, and employees take pride in.

The Bear Case: Storm Clouds Gathering

Skeptics, however, see significant challenges ahead. Asset quality concerns in unsecured lending are mounting across the industry. While Cholamandalam has maintained reasonable asset quality so far, the rapid growth in consumer and small enterprise loans raises red flags. These loans, typically unsecured or backed by weak collateral, could see sharp deterioration in an economic downturn.

Competition from banks entering vehicle finance is intensifying. Large private banks like HDFC and ICICI, armed with low-cost deposits and massive distribution networks, are aggressively targeting vehicle finance. Public sector banks, under pressure to grow retail assets, are offering loans at rates Cholamandalam cannot match. As competition intensifies, margins will compress and growth will become more expensive.

Regulatory changes in the NBFC sector pose ongoing risks. The Reserve Bank of India has been tightening regulations, from asset classification norms to provisioning requirements. The proposed changes in priority sector lending certificates could affect Cholamandalam's funding costs. Any adverse regulatory change could significantly impact profitability and growth prospects.

The electric vehicle disruption is more threat than opportunity, bears argue. EVs have fundamentally different economics—higher upfront costs, uncertain resale values, and rapidly evolving technology. Cholamandalam's expertise in ICE vehicles may not translate to EVs. New players, including OEMs themselves, are entering EV financing with innovative models that could disrupt traditional vehicle finance.

Interest rate sensitivity remains a structural challenge. NBFCs like Cholamandalam borrow at market rates while lending at fixed rates, creating asset-liability mismatches. In a rising rate environment, margins compress unless lending rates can be adjusted, which is difficult in competitive markets. The recent rate cycle has been benign, but any sharp increase could pressure profitability.

Technology disruption from fintech companies is accelerating. While Cholamandalam has invested in technology, pure-play digital lenders are offering instant loans with minimal documentation. Younger customers, comfortable with digital interfaces, might prefer the convenience of app-based lending over Cholamandalam's branch-based model.

Competitive Landscape Analysis

Benchmarking against key competitors reveals Cholamandalam's unique position. Compared to Shriram Finance, the largest competitor in commercial vehicle finance, Cholamandalam offers more diversified products and better asset quality, though Shriram's specialized focus gives it pricing power in certain segments. Shriram's deep penetration in used CV financing and relationships with driver communities remain formidable competitive advantages.

Against Bajaj Finance, India's most valued NBFC, Cholamandalam appears conservative but perhaps more sustainable. Bajaj's focus on urban consumption finance has delivered spectacular growth, but it's also more vulnerable to consumer credit cycles. Cholamandalam's asset-backed lending model provides more downside protection, though potentially lower growth rates.

M&M Financial, backed by the Mahindra Group, presents interesting parallels. Both leverage parent group relationships, focus on rural markets, and emphasize vehicle finance. However, Cholamandalam's broader product suite and superior technology infrastructure give it an edge. M&M Financial's recent asset quality issues also highlight the risks in rural lending that Cholamandalam has managed better.

New-age fintech lenders like Indifi, Lendingkart, and Capital Float are targeting SME lending with digital models. While they offer speed and convenience, they lack Cholamandalam's distribution network and relationship depth. Their higher credit costs and customer acquisition expenses also question long-term sustainability.

Banks remain the elephant in the room. With access to low-cost deposits and regulatory advantages, banks can undercut NBFC pricing when they choose to. However, banks' organizational structures and risk appetites often prevent them from serving segments where Cholamandalam excels. The key question is whether banks will become more aggressive in these segments as technology reduces operational costs.

The Balanced View

The truth likely lies between extreme optimism and pessimism. Cholamandalam has demonstrated remarkable resilience through multiple cycles—from the 2008 financial crisis to the 2020 pandemic. Its diversified product portfolio, strong distribution network, and conservative underwriting provide buffers against sector-specific shocks.

The company's track record of navigating challenges—from the failed DBS partnership to regulatory changes—suggests organizational adaptability. The ability to maintain PBT Growth for FY25 at 25% while keeping asset quality stable demonstrates execution capability that few competitors can match.

However, the bears' concerns about increasing competition, regulatory risks, and technology disruption are valid. Cholamandalam will need to continue evolving, investing in technology while maintaining its relationship-based model, expanding products while managing risk, and growing rapidly while preserving asset quality.

The key differentiator remains Cholamandalam's deep understanding of India's informal economy and its ability to serve customers that others find too difficult or unprofitable. As long as millions of Indians aspire to economic mobility through entrepreneurship, as long as small businesses need patient capital to grow, as long as the formal financial system struggles to serve India's diversity, Cholamandalam's model remains relevant and valuable.

X. Future & Strategic Questions

As Cholamandalam navigates toward the next decade, the strategic questions facing the company are both exciting and existential. The decisions made in the next few years will determine whether Cholamandalam becomes a trillion-rupee balance sheet NBFC, evolves into a comprehensive financial services platform, or perhaps even transforms into something entirely new—a techfin company that happens to have deep physical distribution.

The digital lending partnership ecosystem presents both the greatest opportunity and the most complex challenge. Fintech companies need balance sheets and regulatory licenses; Cholamandalam needs technology capabilities and access to digital-native customers. The company has begun exploring these partnerships, but the key question remains: should Cholamandalam be a platform that enables others or build its own digital brands? The answer isn't binary—the company is experimenting with both models, white-labeling its lending capabilities for digital platforms while building its own digital products.

The electric vehicle financing opportunity demands immediate strategic clarity. India has set ambitious EV adoption targets, and the transformation is accelerating, particularly in two-wheelers and three-wheelers. Cholamandalam faces crucial decisions: Should it partner with EV manufacturers for exclusive financing deals? How should it price loans for vehicles with uncertain resale values? What about financing charging infrastructure? The company's recent pilots with EV financing suggest a cautious but engaged approach, learning the market while avoiding large bets.

IFC anchored an investment round of $222 million. The new funds will help the company expand its reach and create jobs. This international capital injection opens possibilities for expansion beyond traditional markets. Should Cholamandalam venture into new geographies within India—the Northeast, for instance, where financial penetration remains minimal? Or should it consider adjacent markets like Bangladesh or Sri Lanka, where similar customer segments exist?

The question of whether Cholamandalam can maintain its moat as lending becomes commoditized is perhaps the most fundamental. As credit bureau data improves, as digital KYC makes customer acquisition frictionless, as instant loans become the norm, what remains special about Cholamandalam's model? The answer might lie not in the lending itself but in the ecosystem—the value-added services, the community building, the transformation enablement that goes beyond mere financing.

International expansion possibilities deserve serious consideration. Indian NBFCs have historically been domestic-focused, but Cholamandalam's expertise in emerging market lending could travel. Southeast Asian and African markets have similar characteristics—large informal economies, underpenetrated vehicle finance markets, and growing SME sectors. The question is whether Cholamandalam has the organizational bandwidth and risk appetite for international ventures.

The evolution from vehicle finance to comprehensive SME banking represents the most ambitious possibility. SMEs need more than just loans—they need payment solutions, forex services, cash management, and advisory services. Could Cholamandalam leverage its deep SME relationships to become a full-service financial partner? This would require new licenses, capabilities, and possibly acquisitions, but the opportunity to serve the entire financial needs of millions of SMEs is tantalizing.

Technology infrastructure decisions will be critical. Should Cholamandalam build proprietary technology or rely on third-party solutions? The company has chosen a hybrid approach, building core lending systems internally while partnering for peripheral services. But as technology becomes more central to competitive advantage, this balance might need recalibration. The recent experiments with artificial intelligence for credit scoring and blockchain for supply chain financing suggest an appetite for innovation.

The regulatory landscape presents both constraints and opportunities. The Reserve Bank of India is gradually creating a more level playing field between banks and NBFCs, potentially allowing NBFCs to offer more products. Could Cholamandalam eventually become a small finance bank? The company has consistently maintained it's happy being an NBFC, but regulatory evolution might force reconsideration.

Talent acquisition and retention in a digital age pose new challenges. Cholamandalam's traditional strength has been relationship managers who understand local markets. But increasingly, the company needs data scientists, product managers, and technology architects. How does it attract such talent while maintaining its unique culture? The answer might lie in creating parallel career tracks—one for traditional banking skills, another for digital capabilities.

The sustainability and ESG (Environmental, Social, and Governance) agenda is becoming business-critical. Cholamandalam's role in financing commercial vehicles puts it at the center of India's carbon transition. Should the company actively discourage financing of polluting vehicles? How should it support customers in transitioning to cleaner alternatives? The company's recent green financing initiatives suggest recognition of this imperative, but execution remains nascent.

Customer segment evolution presents interesting strategic choices. Cholamandalam's traditional customer—the first-time buyer, the driver-turned-owner—remains important, but a new segment is emerging: the digital-native small business owner who values convenience over relationships. Should Cholamandalam create separate brands or channels for different segments? The risk is diluting focus; the opportunity is capturing a broader market.

Partnership strategies need refinement. The company has partnerships with OEMs, digital platforms, and corporate entities, but these remain largely transactional. Could Cholamandalam create deeper, more strategic partnerships—perhaps exclusive financing arrangements with EV manufacturers or integrated supply chain solutions with e-commerce platforms? The challenge is maintaining independence while deepening integration.

The capital allocation question becomes more complex with scale. As the company approaches Rs 2 lakh crore in AUM, growth requires increasingly large capital commitments. Should Cholamandalam prioritize growth, accepting lower returns in the short term? Or should it focus on profitability, potentially ceding market share? The recent performance suggests an attempt to balance both, but trade-offs will become sharper.

Data strategy might be the most underappreciated strategic question. Cholamandalam sits on a goldmine of data—decades of lending history across multiple products and segments. This data could be monetized through credit bureau services, risk analytics, or market intelligence. But it could also be the foundation for AI-driven lending models that dramatically improve risk assessment and customer service.

The organizational structure question looms large. As Cholamandalam becomes more complex—multiple products, channels, and customer segments—should it reorganize from a functional structure to business units? Should vehicle finance, SME lending, and housing finance be run as separate entities with their own P&Ls? The trade-off between focus and synergy is delicate.

Looking ahead, the next decade will likely see Cholamandalam attempting something unprecedented in Indian financial services: maintaining its relationship-based, high-touch model while building digital capabilities that match pure-play fintechs. Success would create a unique competitive position—the trust and distribution of a traditional lender with the efficiency and innovation of a digital player.

The ultimate question is whether Cholamandalam can maintain its soul—the commitment to enabling customers to enter a better life—while transforming into a modern financial services powerhouse. The track record suggests it can, but the challenges ahead are unlike anything the company has faced before. The decisions made in corporate boardrooms in Chennai will determine whether millions of Indians can access the capital they need to transform their lives. In that sense, Cholamandalam's strategic questions aren't just business decisions—they're choices about India's economic future.

XI. Key Takeaways & Lessons

After traversing nearly five decades of Cholamandalam's evolution, from a modest equipment financier to one of India's most formidable NBFCs, several profound lessons emerge. These aren't just insights for financial services professionals but fundamental principles about building enduring businesses in emerging markets, creating value through deep customer understanding, and maintaining institutional values while embracing change.

Distribution Still Matters in the Digital Age

Perhaps the most counterintuitive lesson from Cholamandalam's success is that physical distribution remains a powerful competitive advantage even as the world goes digital. While fintech evangelists proclaim the death of branches, Cholamandalam's 1,387 branches across the country generate value that no app can replicate. These branches aren't just transaction points—they're trust nodes in communities where a physical presence signals commitment and permanence.