Choice International: The Story of India's Financial Services Consolidator

I. Introduction & Episode Roadmap

Picture this: A company worth ₹14,789 crore that most Indians have never heard of. No celebrity endorsements, no unicorn valuations splashed across newspapers, no venture capital fanfare. Yet Choice International has quietly assembled one of India's most ambitious financial services empires through sheer acquisition hunger and operational discipline. In the last year alone, the stock has surged 87.7%—all while refusing to pay a single rupee in dividends despite posting consistent profits.

The enigma deepens when you dig into the numbers. Here's a company that started as a modest NBFC in 1993, navigating India's pre-liberalization financial maze, and has somehow transformed into a multi-vertical behemoth spanning broking, wealth management, insurance, and now mutual funds. The promoters still hold 56.4% of the company—a rarity in today's dilution-happy markets—suggesting they're playing a much longer game than quarterly earnings calls would suggest. The central question driving this story: Can you build India's Charles Schwab through aggressive M&A? While American financial services giants grew organically over decades, Choice International is attempting something audacious—rolling up India's fragmented financial services landscape at breakneck speed. The company's material subsidiary Choice Equity Broking recently entered into an agreement for acquiring entire stake in Arete Capital Services which is in the distribution of wealth products, with the cost of acquisition at Rs 36 crore.

This isn't just another financial services company. It's a case study in contrarian capital allocation, aggressive consolidation, and the peculiar dynamics of India's wealth creation boom. As we'll see, the story of Choice International is really three stories: the patient foundation-building of the 1990s, the strategic positioning of the 2010s, and the explosive M&A-driven expansion of the 2020s. Each phase reveals different lessons about building in regulated markets, timing entry into new verticals, and the delicate balance between growth and governance.

What makes this particularly fascinating is the timing. India's financialization is accelerating—mutual fund folios have doubled in five years, demat accounts have tripled, and yet household savings in financial assets remain below 10% of GDP. Choice International isn't just riding this wave; it's positioning itself as the consolidator of consolidators, buying up smaller players who themselves were regional aggregators. It's financial services inception—acquisitions within acquisitions.

II. The Foundation Story (1993–2010)

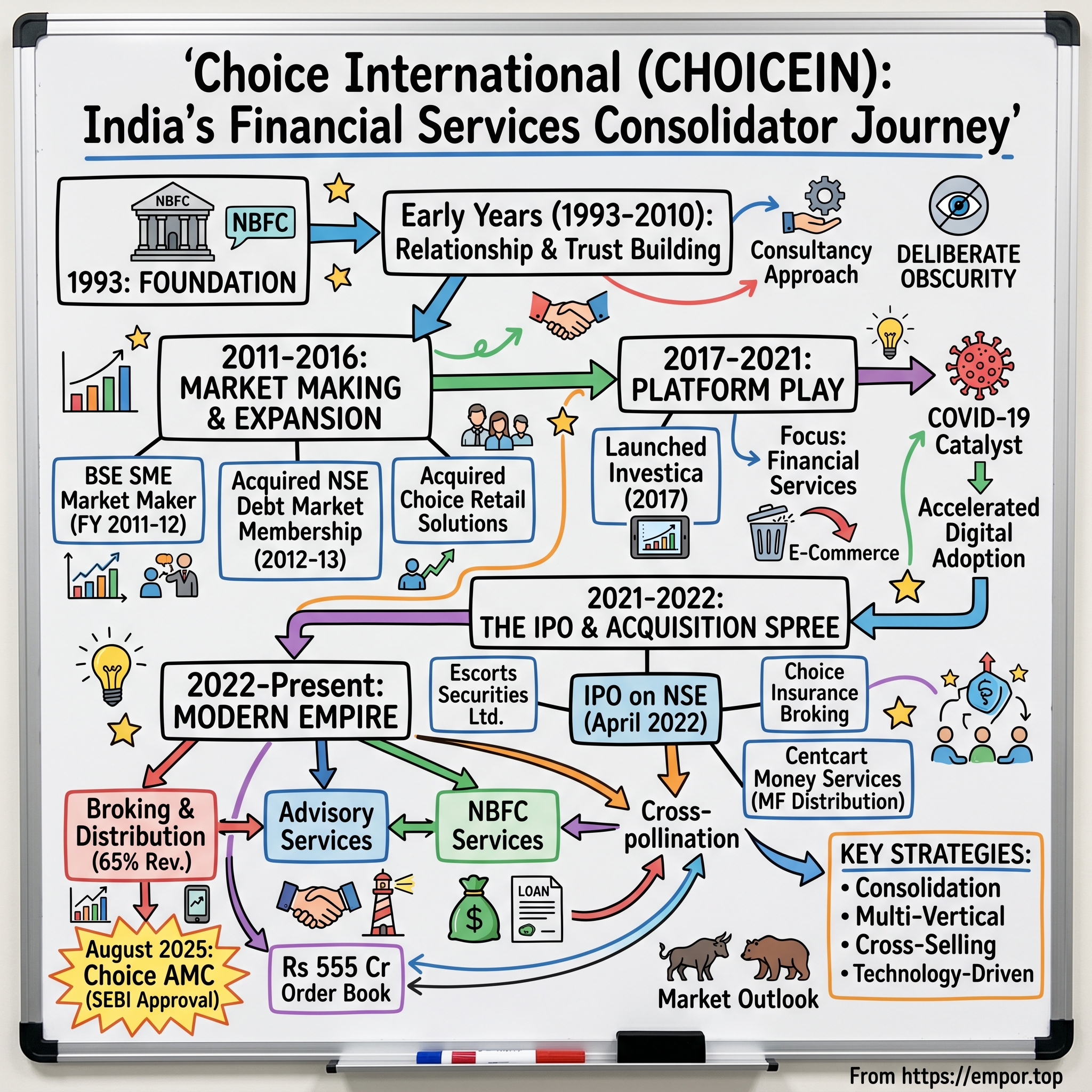

The year was 1993. India had just emerged from its balance of payments crisis. Manmohan Singh's liberalization was barely two years old. The Bombay Stock Exchange still operated with an open outcry system—traders literally shouting orders across a crowded floor. Into this chaos stepped Choice International, incorporated on March 12, 1993, as an RBI-registered Non-Banking Financial Company.

The founder, Kamal Poddar, wasn't your typical financial services entrepreneur. He didn't come from the established business houses of Mumbai or the trading communities of Gujarat. Instead, he built Choice Wealth Management Private Limited with a consultancy-first approach—a radical departure in an era when NBFCs were primarily seen as quasi-banks for those who couldn't get banking licenses.

The early Choice wasn't trying to be a financial supermarket. It was, in many ways, a solutions shop—helping businesses navigate India's byzantine regulatory environment, arranging project finance when banks wouldn't lend, structuring deals that required creativity more than capital. This consultancy DNA would prove crucial decades later when the company began its acquisition spree. They understood deal-making because they'd been in the deal-making business from day one.

Mumbai in the 1990s was a peculiar place for financial services. The city was simultaneously the epicenter of Indian finance and remarkably provincial in its practices. Relationship banking ruled. Trust was earned over decades, often generations. For a new NBFC without established family connections or community ties, every client was a battle.

Choice's strategy during these wilderness years was deliberate obscurity. While peers chased growth through aggressive lending or played regulatory arbitrage games, Choice built what would later be described as "a strong reputation worldwide as a provider of business consultative solutions." The "worldwide" might have been aspirational, but the consultative approach was real. They weren't just lending money; they were solving problems.

The 2000s brought new challenges. The dot-com bust, the 2008 financial crisis, regulatory tightening after various NBFC scandals—each crisis culled the weak players. Choice survived not through brilliance but through conservatism. They didn't blow up because they didn't take the big swings. In hindsight, this looks like strategic patience. At the time, it probably felt like treading water.

What's remarkable about this period is what didn't happen. No venture capital, no rapid expansion, no headlines. Just slow, steady relationship building in Mumbai's Nariman Point and Bandra-Kurla Complex offices. The company was essentially building trust equity—an intangible asset that doesn't show up on balance sheets but would prove invaluable when they eventually needed to integrate acquired companies.

By 2010, Choice International had spent 17 years doing something that seemed almost quaint: building a reputation for reliability in Indian financial services. They hadn't scaled dramatically. They hadn't disrupted anything. But they had survived, and in Indian financial services, survival itself was an achievement. The foundation was set, though few could have predicted what would come next.

III. The Transformation Begins: Market Making & Expansion (2011–2016)

Something shifted in 2011. After nearly two decades of patient foundation-building, Choice International suddenly began moving with the urgency of a startup. The transformation started with an seemingly mundane regulatory approval: in FY 2011-12, they registered as a Market Maker in the SME segment of BSE and converted their Trading Membership into Clearing Membership of BSE's F&O Segment.

To understand why this mattered, you need to understand the economics of Indian capital markets in 2011. The SME segment was the unloved stepchild of Indian exchanges—illiquid, risky, and largely ignored by established brokers. But for Choice, it represented something else: a beachhead into capital markets without competing directly with entrenched players. Being a market maker meant providing liquidity where none existed, earning spreads that larger players wouldn't bother chasing.

The real strategic insight came in 2012-13 when Choice acquired Debt Market membership in NSE Limited. Debt markets in India were (and remain) institutionally dominated, with retail participation nearly non-existent. But Choice wasn't thinking retail. They were building capabilities—accumulating licenses like a collector accumulates rare stamps, each one opening new revenue possibilities, each one a potential moat.

Then came the MCX-SX licenses for cash and F&O segments. MCX-SX would eventually fail as an exchange, but Choice's willingness to bet on it revealed their strategy: be everywhere, even in places that might not work out. The cost of these licenses was minimal. The optionality they provided was enormous.

The masterstroke of this period was the acquisition of 100% stake in Choice Retail Solutions Private Limited. The name was misleading—this wasn't about retail in the shopping sense. It was about distribution. Choice Retail Solutions gave them boots on the ground, a network of sub-brokers and franchisees who could push products into tier-2 and tier-3 cities where digital penetration was still a dream.

Consider the timing: 2011-2016 was when India's smartphone revolution was just beginning. Jio hadn't launched yet. Digital payments were nascent. Yet Choice was building both digital capabilities (through exchange memberships) and physical distribution (through retail solutions). They were preparing for a hybrid future that wouldn't fully materialize for another decade.

The numbers from this period don't tell the whole story, but they hint at it. Revenue grew modestly, profits remained thin, but the company was accumulating something more valuable than immediate returns: operating leverage. Each new license, each new capability, was a fixed cost that could support exponentially more revenue without proportional cost increases.

What's fascinating is what Choice didn't do during this period. They didn't raise significant external capital. They didn't launch a flashy trading app. They didn't chase the discount broking model that was beginning to disrupt the industry. Instead, they built infrastructure—boring, essential infrastructure that would allow them to plug in acquisitions seamlessly later.

By 2016, Choice International had transformed from a consultancy-focused NBFC into a multi-licensed financial services player. They had memberships across exchanges, segments across asset classes, and distribution reaching into India's hinterlands. The platform was ready. All they needed was the right moment to deploy it.

IV. The Platform Play: Technology & Consolidation (2017–2021)

The launch of Investica in 2017 marked Choice's belated entry into the digital age. By startup standards, they were laughably late—Zerodha had already conquered discount broking, and Groww was gaining momentum. But Choice wasn't trying to out-innovate the innovators. Investica was infrastructure, not innovation—a digital backbone that could absorb and integrate future acquisitions.

The platform itself was unremarkable. No gamification, no social features, no viral growth mechanics. Just functional trading and investment capabilities wrapped in a competent interface. The technology press ignored it. Fintech Twitter mocked it. But Investica wasn't built for them. It was built as a universal adapter—a system that could talk to legacy banking protocols and modern APIs with equal fluency.

The real tell came with a corporate action that seemed like retreat: Choice disposed of its holding in Choice E-Commerce Private Limited. E-commerce was booming, everyone was chasing the next Flipkart, yet Choice walked away. This wasn't failure; it was focus. They were pruning the portfolio, concentrating resources on financial services. Every rupee not spent on e-commerce experiments could be deployed into their core consolidation thesis.

Then COVID hit. March 2020 should have been catastrophic for a company with significant physical distribution. Instead, it accelerated their digital transformation by necessity. Branches closed, but trading volumes exploded. Customers who would never have downloaded an app were suddenly digital-first by default. The pandemic did what no amount of marketing could: it forced behavioral change. While specific data about Choice International's digital transformation during COVID isn't publicly available, the broader context is instructive. As a result of the COVID-19 crisis, there was a rise in online banking activity such as increased digital transactions and a decline in trips to brick-and-mortar branches. The current pandemic forced individual consumers as well as corporates who once resisted online banking to adopt digital banking apps as their new default. For Choice, with its established physical distribution network, this could have been catastrophic. Instead, it became catalytic.

The company's strategic positioning during this period was masterful. While competitors were cutting costs and hunkering down, Choice was quietly preparing for what would become India's most ambitious financial services IPO of 2022. They understood that post-pandemic markets would reward platforms over products, ecosystems over individual services.

What's particularly clever about Choice's approach was their refusal to compete on the same battlefield as digital-first players. They weren't trying to build the next Zerodha. They were building something different—a full-stack financial services platform that could serve everyone from day traders to corporate treasuries, from insurance buyers to mutual fund investors. The technology was the enabler, not the differentiator.

By early 2021, Choice had assembled all the pieces. Multiple licenses across exchanges. A functional digital platform. A distribution network spanning urban and rural India. Strong balance sheet despite the pandemic. The stage was set for their most audacious move yet—going public in the midst of market uncertainty and embarking on an acquisition spree that would transform them from a mid-sized player to a financial services powerhouse.

V. The IPO & Acquisition Spree (2021–2022)

April 8, 2021, marked the beginning of Choice International's transformation from opportunistic acquirer to systematic consolidator. The agreement to acquire Escorts Securities Limited from its existing shareholders wasn't just another deal—it was a statement of intent. Escorts brought with it not just clients and revenues, but decades of market credibility and a broking infrastructure that would have taken years to build organically.

The timing seemed counterintuitive. Indian markets were still reeling from the second COVID wave. Retail participation, which had surged during the lockdowns, was showing signs of fatigue. Yet Choice pressed ahead, structuring the deal in a way that would become their signature: cash-heavy, integration-focused, with immediate revenue synergies.

Six months later, on October 29, 2021, came the next move: acquiring 50% stake in Choice Insurance Broking India Private Limited for Rs. 59,40,000. The amount seems almost trivial—less than Rs. 60 lakhs for half an insurance broking business. But this wasn't about the price; it was about the license. Insurance broking in India requires IRDAI approval, a process that can take years. Choice had just bought their way into the insurance distribution game for the price of a luxury apartment in Mumbai.

The real sophistication showed in how they layered acquisitions. While the parent company was acquiring Escorts Securities, Choice Wealth Private Limited—a subsidiary—was simultaneously acquiring the mutual fund distribution business of Centcart Money Services Private Limited during 2021-22. This wasn't just expansion; it was orchestrated multiplication. Each entity within the Choice ecosystem was hunting for complementary acquisitions, creating a fractal pattern of growth.

Then came April 8, 2022—exactly one year after the Escorts agreement—when Choice International's equity shares listed on NSE's Main Board platform. The timing was either brilliant or lucky, possibly both. They hit the market just before the global tech rout truly began, raising capital when valuations were still generous but not quite at their frothy peaks.

The IPO prospectus revealed the true scale of Choice's ambition. This wasn't a company going public to give exits to early investors—remember, there were no VCs to satisfy. This was about war chest building. Every rupee raised was earmarked for growth: technology upgrades, working capital for the expanded broking business, and most importantly, more acquisitions.

The Escorts Securities integration became the template for future deals. Instead of the typical post-merger chaos—system migrations, client defections, cultural clashes—Choice executed with almost boring efficiency. Escorts clients were migrated to Choice platforms within quarters, not years. Cross-selling began immediately. The combined entity's operating metrics improved rather than deteriorated, defying the usual M&A playbook.

What made this period remarkable wasn't just the pace of acquisitions but their strategic coherence. Each deal filled a specific gap: Escorts for institutional broking credibility, Choice Insurance Broking for distribution licenses, Centcart for mutual fund clientele. This wasn't the scatter-shot approach of a conglomerate building for the sake of size. It was targeted capability acquisition, each piece fitting into a larger puzzle.

The market initially struggled to value this transformation. Was Choice a broking company? An NBFC? A wealth manager? The answer was yes to all, and that was precisely the point. In India's traditionally siloed financial services industry, Choice was building something unprecedented—a true one-stop shop for financial services, backed not by flashy technology but by old-fashioned execution excellence.

VI. The Modern Empire: Business Lines & Strategy (2022–Present)

Today's Choice International operates across three core verticals that would seem schizophrenic if not for their underlying logic. Its key offerings include Broking & Distribution, NBFC Services, and Advisory, covering Government Infrastructure Consultancy, Government Advisory, and Investment Banking. On paper, these look like completely different businesses. In practice, they're a masterclass in cross-pollination.

The broking and distribution business, accounting for 65% of total revenues, forms the gravitational center. The broking and distribution business, which accounts for 65% of our total revenues, recorded a YoY growth of 9%, generating Rs 135 crore in revenue for Q3FY25. This isn't just about executing trades—it's about controlling the customer relationship at the point of transaction. Every trade, every mutual fund purchase, every insurance policy sold generates data, relationships, and cross-selling opportunities. The August 2025 milestone cannot be understated: Choice AMC received final approval from SEBI to commence operations as an Asset Management Company, with the regulatory clearance in place, Choice is set to commence operations of its AMC, initiating a strategic and phased rollout beginning with passive investment products such as index funds and exchange traded funds (ETFs). This wasn't just another license—it was the crown jewel. India's mutual fund industry manages over Rs 68 trillion in assets, and Choice had just gained entry to the most lucrative segment of Indian financial services.

The 2024 acquisition spree revealed the acceleration of their consolidation thesis. They acquired the business of Sernet Financial Services Pvt Ltd, Berkeley Securities Ltd, and RK Stock Holdings Pvt Ltd—three acquisitions in a single year. Each brought specific capabilities: Sernet for its technology infrastructure, Berkeley for its institutional relationships, RK Stock for its retail distribution network.

The Choice FinX trading app, while not revolutionary in features, serves a different purpose entirely. It's not competing with Zerodha on pricing or Groww on user experience. Instead, it's a retention tool—keeping acquired customers within the Choice ecosystem while cross-selling higher-margin products. A customer might come for the trading, but Choice wants them to stay for the wealth management, insurance, and now mutual funds.

The government advisory business seems incongruous until you understand the strategic logic. Advisory segment Order book stood at Rs 555 crore. This isn't about the revenues—it's about relationships. Working with government entities on infrastructure projects gives Choice unparalleled access to decision-makers, regulatory insights, and most importantly, credibility when bidding for government-linked financial services mandates.

The numbers tell the integration story: 4,096 total employees across all entities. That's a small army by Indian financial services standards, but it's precisely calibrated. Each acquisition brings its own workforce, already trained, already productive. Choice isn't hiring; it's acquiring human capital along with licenses and customers.

What's emerging is something unique in Indian financial services—a platform company that owns the entire value chain. When a customer trades, Choice earns brokerage. When they buy mutual funds, Choice earns distribution fees and now AMC management fees. When they need insurance, Choice earns broking commissions. When they need loans, Choice's NBFC provides them. It's vertical integration meeting horizontal expansion, creating a web of interdependencies that makes customer churn increasingly unlikely.

VII. Financial Performance & Market Position

The numbers are compelling and confounding in equal measure. Revenue of 944 Crore, Profit of 179 Crore—solid but not spectacular. Yet the market values Choice at a P/E of 87.8, trading at 14.4 times book value. This isn't just expensive; it's priced for perfection. The question is whether the market sees something the numbers don't yet show, or if this is another case of India's eternal optimism about financial services.

The 65.9% CAGR profit growth over the last five years tells the real story. This isn't linear growth; it's exponential. Annual revenue growth of 21% might seem pedestrian compared to the profit trajectory, but the 24% pre-tax margin reveals the operating leverage at work. Each incremental rupee of revenue drops increasingly more to the bottom line—the beauty of platform economics in financial services.

Net profit of Choice International rose 34.22% to Rs 51.69 crore in the quarter ended March 2025 as against Rs 38.51 crore during the previous quarter ended March 2024. Sales rose 17.92% to Rs 253.00 crore in the quarter ended March 2025 as against Rs 214.55 crore during the previous quarter ended March 2024. For the full year, net profit rose 21.48% to Rs 156.54 crore in the year ended March 2025 as against Rs 128.86 crore during the previous year ended March 2024. Sales rose 21.27% to Rs 910.38 crore in the year ended March 2025 as against Rs 750.68 crore during the previous year ended March 2024.

The ROE of 15% seems modest until you realize this is achieved without leverage. Most financial services companies juice returns through borrowing. Choice is generating these returns through operational efficiency and acquisition synergies. The balance sheet remains remarkably clean—a rarity in Indian NBFCs where asset quality is often a concern.

The promoter holding of 56.4% is both a strength and a question mark. On one hand, it signals skin in the game—the Poddar family's wealth is tied to Choice's success. On the other, it limits float, potentially explaining some of the valuation premium. With limited shares available for trading, even modest buying interest can drive significant price movements.

The no-dividend policy despite repeated profits is the elephant in the room. Though the company is reporting repeated profits, it is not paying out dividend. This isn't capital starvation—it's capital accumulation. Every rupee retained is a rupee available for the next acquisition. In a consolidating industry, cash is ammunition, and Choice is building an arsenal.

The quarterly volatility tells another story. Net profit of Choice International declined 25.42% to Rs 29.40 crore in the quarter ended December 2024 as against Rs 39.42 crore during the previous quarter ended December 2023. Sales rose 0.99% to Rs 209.34 crore in the quarter ended December 2024 as against Rs 207.28 crore during the previous quarter ended December 2023. This December 2024 performance reveals the inherent volatility in transaction-based revenues. When markets correct, broking revenues suffer immediately. But the diversification strategy is already paying dividends—notice how revenues remained flat while profits declined, suggesting the more stable advisory and NBFC businesses provided cushion.

The comparison to intrinsic value is sobering. Currently trading at 553.15 INR versus an intrinsic value of 379.06 INR suggests overvaluation by 31% according to DCF models. But DCF models struggle with roll-up strategies. How do you value future acquisitions that haven't been announced? How do you price in the network effects of an integrated financial services platform?

What's particularly interesting is the capital efficiency. Unlike banks that need regulatory capital for every rupee lent, or insurance companies that need solvency margins, Choice's broking and distribution businesses are capital-light. The NBFC requires capital, yes, but it's a small portion of overall revenues. This creates a flywheel effect—profits from capital-light businesses fund expansion into capital-intensive ones, which in turn generate more customers for the capital-light segments.

VIII. Playbook: The Indian Financial Services Roll-up Strategy

The Choice playbook is deceptively simple: buy established players at reasonable valuations, integrate them rapidly, and cross-sell aggressively. But execution is everything, and Choice has developed a systematic approach that turns conventional M&A wisdom on its head.

First, the targeting. Choice doesn't buy distressed assets hoping for turnarounds. They buy profitable, established businesses with specific assets—licenses, customer relationships, or distribution networks. The price paid often seems high relative to the book value, but Choice isn't buying books; they're buying capabilities that would take years to build organically.

The integration philosophy is counterintuitive. Instead of immediate consolidation, Choice often maintains separate brands and entities initially. Choice Insurance Broking, Choice Wealth, Choice Equity Broking—each maintains its identity while being progressively integrated at the backend. Customers don't experience disruption; employees don't face immediate redundancies. This patient integration reduces the typical M&A failure points.

Technology becomes the binding glue. Rather than forcing acquired companies onto a single platform immediately, Choice builds APIs and middleware that allow different systems to communicate. The Choice FinX app isn't replacing legacy systems; it's sitting on top of them, providing a unified interface while the messy work of system consolidation happens gradually in the background.

The regulatory arbitrage is masterful. In India's licensed financial services landscape, approvals can take years. By acquiring companies with existing licenses, Choice bypasses the queue. In accordance with Sebi's approval, Choice International will set up an asset management company (AMC) and a trustee company, adhering to all applicable regulations and legal requirements. But even with acquisitions, new licenses like the mutual fund approval show Choice isn't purely dependent on M&A for regulatory permissions.

Cross-selling synergies, often promised but rarely delivered in financial services M&A, actually materialize at Choice. A broking client becomes a wealth management prospect. A wealth management client needs insurance. An insurance client might need a loan. Each touchpoint creates data, and data creates opportunities for the next product. It's not aggressive selling; it's systematic relationship deepening.

The no-dividend policy isn't stubbornness—it's strategy. In India's fragmented financial services market, consolidation opportunities abound. Every rupee paid as dividend is a rupee not available for the next acquisition. Shareholders seeking income are implicitly in the wrong stock; Choice is for those believing in the consolidation thesis.

The comparison with global consolidators is instructive. Charles Schwab built through innovation and organic growth, occasionally making transformative acquisitions like TD Ameritrade. Interactive Brokers grew through technology superiority. Choice is following neither playbook exactly—it's creating an Indian version where execution excellence and regulatory navigation matter more than technological innovation or scale economies.

The lesson from global markets is that financial services consolidation accelerates during two periods: regulatory change and technological disruption. India is experiencing both simultaneously. Digital payments have exploded, regulatory frameworks are modernizing, and customer expectations are shifting. Choice isn't causing these changes; it's positioning to benefit from them.

What's particularly clever is the portfolio approach to risk. Broking is volatile but capital-light. NBFC lending is stable but capital-intensive. Insurance distribution is recurring but slow-growing. Government advisory is lumpy but high-margin. The combination creates a more resilient whole than any individual part.

The human capital strategy deserves attention. This quarter we have onboarded 2,500 Choice Business Associates which takes our total headcount to 28K associates. This isn't just about employees—it's about building a distribution army. In India, relationships still matter more than apps. While competitors focus on digital-only strategies, Choice is building both digital capabilities and physical presence.

IX. Competition & Market Dynamics

The competitive landscape reveals why Choice's strategy might work precisely because it's so unfashionable. While Zerodha conquered discount broking with zero-brokerage models and Groww captured millennials with gamified investing, Choice is playing an entirely different game—consolidating the consolidators in India's fragmented financial services market.

The established competitors—IIFL Capital Service, Share India Securities, Geojit Financial Service—follow similar full-service models but lack Choice's acquisition appetite. They're growing organically, adding services incrementally, competing for the same high-net-worth individuals and corporate clients. Choice isn't trying to out-execute them at their own game; it's buying market share and capabilities they've spent decades building.

The discount brokers have fundamentally changed the economics of retail broking. Zerodha's zero-brokerage model on equity delivery trades has conditioned an entire generation to expect free trading. But here's what the market misses: Zerodha's 2 crore clients generate an average revenue per user (ARPU) of less than Rs 1,000 annually. Choice's strategy targets customers worth 10-50 times that amount—the ones who need advice, not just execution.

Groww's pivot from mutual funds to broking, raising unicorn valuations along the way, represents the VC-funded disruption playbook. But Groww burns cash to acquire customers, hoping to monetize them eventually. Choice acquires profitable businesses with existing customer relationships. One is betting on future monetization; the other is buying current cash flows.

The traditional players—Motilal Oswal, HDFC Securities, ICICI Securities—have parent company advantages Choice can't match. Bank-led brokers have captive customer bases and cost-of-capital advantages. But they also have bureaucracies, legacy systems, and innovation antibodies that make rapid transformation difficult. Choice's entrepreneurial culture and acquisition-led growth allow it to move faster than these elephants can dance.

Choice International major competitors are IIFL Capital Service, Angel One, Share India Sec., Monarch Networth Cap, Geojit Finl. Service, ICICI Securities, Master Trust. Among these, Angel One represents an interesting parallel—another company growing through acquisition and platform building, now entering mutual funds. The difference? Angel One is VC-backed, growth-at-all-costs focused. Choice is promoter-driven, profitability-obsessed.

The regulatory environment is both headwind and tailwind. SEBI's increasing compliance requirements raise the cost of being a financial services provider, driving smaller players to sell. But the same regulations also protect established players from fly-by-night competition. Every new circular, every additional compliance requirement, makes Choice's licensed platform more valuable.

The macro tailwinds are undeniable. India's household savings in financial assets are still below 10% of GDP compared to 30%+ in developed markets. The equity cult is just beginning—demat accounts have grown from 4 crore in 2020 to over 15 crore today. But this isn't just about more investors; it's about more sophisticated investors who need wealth management, not just trading apps.

The technology disruption narrative misses a crucial point about India. Yes, digital adoption is accelerating, but India isn't Silicon Valley. Relationships, trust, and physical presence still matter, especially for high-value financial decisions. Choice's hybrid model—digital capabilities with human touchpoints—might be better suited to India's reality than pure digital plays.

What's emerging is a barbell market structure. At one end, digital-first discount brokers serving price-conscious retail traders. At the other end, relationship-driven wealth managers serving HNIs and institutions. The middle—full-service brokers charging full-service prices to middle-class clients—is getting squeezed. Choice is trying to own both ends through different brands and acquisitions.

The international context matters too. As global brokers like Interactive Brokers and Charles Schwab expand internationally, Indian players need scale to compete. But regulatory restrictions limit foreign ownership in Indian financial services. This creates a window for domestic consolidators like Choice to build scale before international competition fully arrives.

X. Bear vs Bull Case & Valuation

The Bull Case rests on three pillars, each compelling in isolation, potentially transformative in combination. First, India's financialization story has barely begun. With household financial savings at less than 10% of GDP and growing at 15-20% annually, the addressable market is expanding faster than any single player can capture. Choice doesn't need to win market share; it just needs to participate in the growth.

Second, the M&A track record speaks for itself. Every acquisition has been integrated successfully, synergies have materialized, and the combined entity is growing faster than the sum of its parts. This isn't financial engineering; it's operational excellence. The recent agreement for acquiring entire stake in Arete Capital Services which is in the distribution of wealth products with the cost of acquisition is Rs 36 crore shows they're still finding accretive deals despite the elevated valuations in the market.

Third, the platform economics are just beginning to show. With the mutual fund license now operational, Choice can capture the entire value chain—distribution fees, management fees, and transaction charges. A customer acquired for broking can be monetized across five different verticals. The lifetime value of customers is multiples higher than pure-play brokers or wealth managers.

The strong promoter backing with 56.4% ownership ensures aligned interests and patient capital. Unlike VC-backed competitors racing to exit, the Poddar family is building for generations. This long-term orientation allows for decisions that might hurt quarterly earnings but build lasting competitive advantages.

The Bear Case is equally persuasive. The valuation is stretched by any conventional metric. Trading at 87.8 times earnings and 14.4 times book value prices in perfect execution for years. Any stumble—a failed acquisition, regulatory issues, market downturn—could trigger a violent re-rating. The current valuation of 553.15 INR against an intrinsic value of 379.06 INR suggests 31% downside just to reach fair value.

Integration risks multiply with each acquisition. While Choice has been successful so far, the law of large numbers suggests a failed integration is inevitable. As they acquire larger, more complex businesses, the integration challenges grow exponentially. One bad acquisition could unwind years of patient building.

The no-dividend policy raises governance questions. While reinvestment for growth makes sense, the complete absence of shareholder returns despite consistent profitability suggests either extreme confidence or disregard for minority shareholders. The company seems to be paying a very low dividend. Investors need to see where the company is allocating its profits. Choice International latest dividend payout ratio is 0% and 3yr average dividend payout ratio is 0%.

Regulatory risks loom large in financial services. One adverse SEBI ruling, one RBI circular, one tax change could fundamentally alter the business model. The recent emphasis on compliance and customer protection, while good for the industry, increases operational costs and reduces margins.

The competitive dynamics are intensifying. A host of new mutual fund (MF) players are set to enter the Rs 68-trillion industry in 2025 as the Securities and Exchange Board of India (Sebi) has issued several partial and final approvals in the past few months. There are now at least six applicants either holding a licence or having in-principle approval. While Angel One and Unifi Capital have obtained the final licence, four applicants — Jio BlackRock, Capitalmind, Choice International, and Cosmea Financial Holdings — have received in-principle approvals. The entry of Jio BlackRock, backed by Reliance's distribution might and BlackRock's global expertise, could fundamentally disrupt the wealth management space.

The Valuation Conundrum comes down to how you model a roll-up strategy. Traditional DCF models fail because they can't capture the optionality of future acquisitions. Comparable company analysis struggles because Choice's hybrid model doesn't fit neatly into any category. Is it a broker? An NBFC? A wealth manager? The answer is yes, which makes it either undervalued relative to the sum of its parts or overvalued because it lacks focus.

The market is clearly betting on the bull case, but the risk-reward seems asymmetric. Limited upside if everything goes perfectly, significant downside if anything goes wrong. For fundamental investors, this suggests waiting for a better entry point. For momentum traders, the trend remains favorable until it isn't.

XI. What Would We Do If We Were Running Choice?

The strategic crossroads facing Choice International demands bold decisions. The consolidation strategy has worked brilliantly, but the easy acquisitions are done. Future targets will be more expensive, integration will be more complex, and synergies harder to extract. The playbook needs evolution, not revolution.

First priority: accelerate the digital transformation, but not in the obvious way. Instead of competing with Zerodha on features or Groww on user experience, build the best B2B2C platform in India. License the technology to smaller brokers and wealth managers who can't afford their own tech development. Become the AWS of Indian financial services—invisible to end customers but essential to the ecosystem.

The wealth management opportunity deserves singular focus. India is creating millionaires at an unprecedented pace—2,000 new ones every day by some estimates. These aren't traders looking for the cheapest brokerage; they're individuals needing sophisticated financial planning, estate planning, tax optimization. Build or acquire a premium wealth brand, separate from the Choice umbrella, targeting just this segment.

International expansion isn't about planting flags globally. It's about serving the global Indian. NRIs manage over $100 billion in assets, much of it poorly served by foreign banks who don't understand Indian regulations or Indian banks who don't understand foreign markets. Create a dedicated NRI platform that bridges this gap.

The dividend question needs resolution. The current zero-dividend policy made sense during the land-grab phase, but as the company matures, it needs to reward patient shareholders. Implement a progressive dividend policy—start with a token 10% payout ratio, increasing by 5% annually until reaching 30%. This signals confidence while retaining capital for growth.

Capital allocation must become more disciplined. Set clear hurdle rates for acquisitions—minimum 20% IRR, maximum 2-year payback on synergies. Walk away from deals that don't meet these criteria, regardless of strategic fit. The temptation to overpay for the "last piece of the puzzle" has destroyed more value than any other M&A mistake.

The technology infrastructure needs modernization, not for customer-facing features but for risk management and compliance. As the business becomes more complex, the ability to monitor risk across entities in real-time becomes critical. Invest in building a unified risk platform that can aggregate exposures across broking, lending, and advisory businesses.

Build versus buy decisions should tilt toward building in areas of core competence. The mutual fund business should be built organically, leveraging the distribution network but creating distinct investment capabilities. Passive products are the right starting point, but the real opportunity is in creating India-specific factor-based strategies that neither global giants nor local players are offering.

The governance structure needs evolution. The 56.4% promoter holding provides stability but limits institutional ownership. Consider a gradual dilution through strategic stakes to global financial services players who bring expertise, not just capital. A 10% stake to a global wealth manager could transform the private banking business overnight.

Regulatory engagement should shift from compliance to shaping. As one of the few integrated financial services platforms, Choice has unique insights into regulatory gaps and overlaps. Actively engage with SEBI, RBI, and IRDAI to shape regulations that favor integrated players over single-product providers.

The human capital strategy needs rethinking. 4,096 total employees seems light for the ambition. But instead of mass hiring, implement an acqui-hire strategy—buy small firms primarily for their talent, not their customers. The best wealth managers, the smartest traders, the most connected investment bankers—acquire their firms to acquire them.

Finally, the communication strategy needs sophistication. The market doesn't understand Choice because Choice doesn't explain itself well. Regular investor calls, detailed segment reporting, clear guidance on acquisition criteria—these aren't just good governance; they're value creation tools. A properly understood story trades at a premium to a mysterious one.

XII. Epilogue & Lessons

The Choice International story offers profound lessons about building in regulated markets, timing transformations, and the peculiar dynamics of Indian capitalism. It's a story that challenges Silicon Valley orthodoxies about growth, disruption, and capital allocation, while validating older truths about patience, relationships, and execution.

The power of patient capital emerges as perhaps the most important lesson. In an era of quarterly earnings obsession and venture capital impatience, Choice spent nearly two decades building foundation before accelerating. This wasn't wasted time—it was trust accumulation, capability building, relationship deepening. The companies that survived 2008 without scars had credibility to lead consolidation in 2020.

Timing markets versus time in market takes on new meaning in Choice's journey. They didn't time their entry into broking or wealth management perfectly. They entered early, suffered through lean years, but were positioned perfectly when the market exploded. The lesson isn't about perfect timing; it's about being present when timing becomes perfect.

Building in regulated industries requires a different playbook than building in open markets. Every license is a moat, every compliance requirement a barrier to entry. While tech entrepreneurs celebrate disruption, Choice celebrates integration. While startups chase regulatory arbitrage, Choice accumulates regulatory permissions. It's not sexy, but it's sustainable.

The India opportunity deserves special consideration. Western investors often misunderstand India, seeing it as either the next China (it's not) or a permanently chaotic market (also wrong). India is creating wealth at an unprecedented pace, but capturing that wealth requires understanding Indian psychology, sociology, and relationships. Choice's hybrid model—digital capability with human touch—might be the template for success in India.

The consolidation thesis playing out in Indian financial services mirrors global trends but with Indian characteristics. Unlike the US where consolidation was driven by technology and scale economics, Indian consolidation is driven by regulatory complexity and distribution challenges. The winners won't necessarily be the most innovative; they'll be the best integrators.

For entrepreneurs, Choice offers a masterclass in building without venture capital. No dilution, no growth-at-all-costs pressure, no forced exits. Just steady building, reinvestment, and compound growth. In an era where every startup seeks venture funding, Choice proves that bootstrapping to billions remains possible.

For investors, the lessons are more complex. Choice demonstrates that understanding business quality requires looking beyond financial metrics to execution capability, regulatory positioning, and integration excellence. It also shows that valuation discipline matters—great companies at ridiculous prices are still bad investments.

The broader lesson about financial services evolution is that distribution still matters more than product. Zerodha won discount broking not through superior technology but superior word-of-mouth. Choice is winning consolidation not through innovation but through execution. In financial services, trust scales slower than technology but lasts longer.

Looking ahead, Choice International represents a bet on India's financial maturation. If India follows the path of developed markets, financial services will consolidate, margins will compress, but scale players will thrive. If India charts its own path, the winners will be those who understand India's unique dynamics. Choice is positioned for either scenario.

The ultimate test will be whether Choice can transform from successful acquirer to successful operator. Rolling up is the easy part; creating lasting value from the rolled-up entity is where most consolidators fail. The next five years will determine whether Choice International becomes India's Charles Schwab or just another ambitious idea that couldn't scale.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube