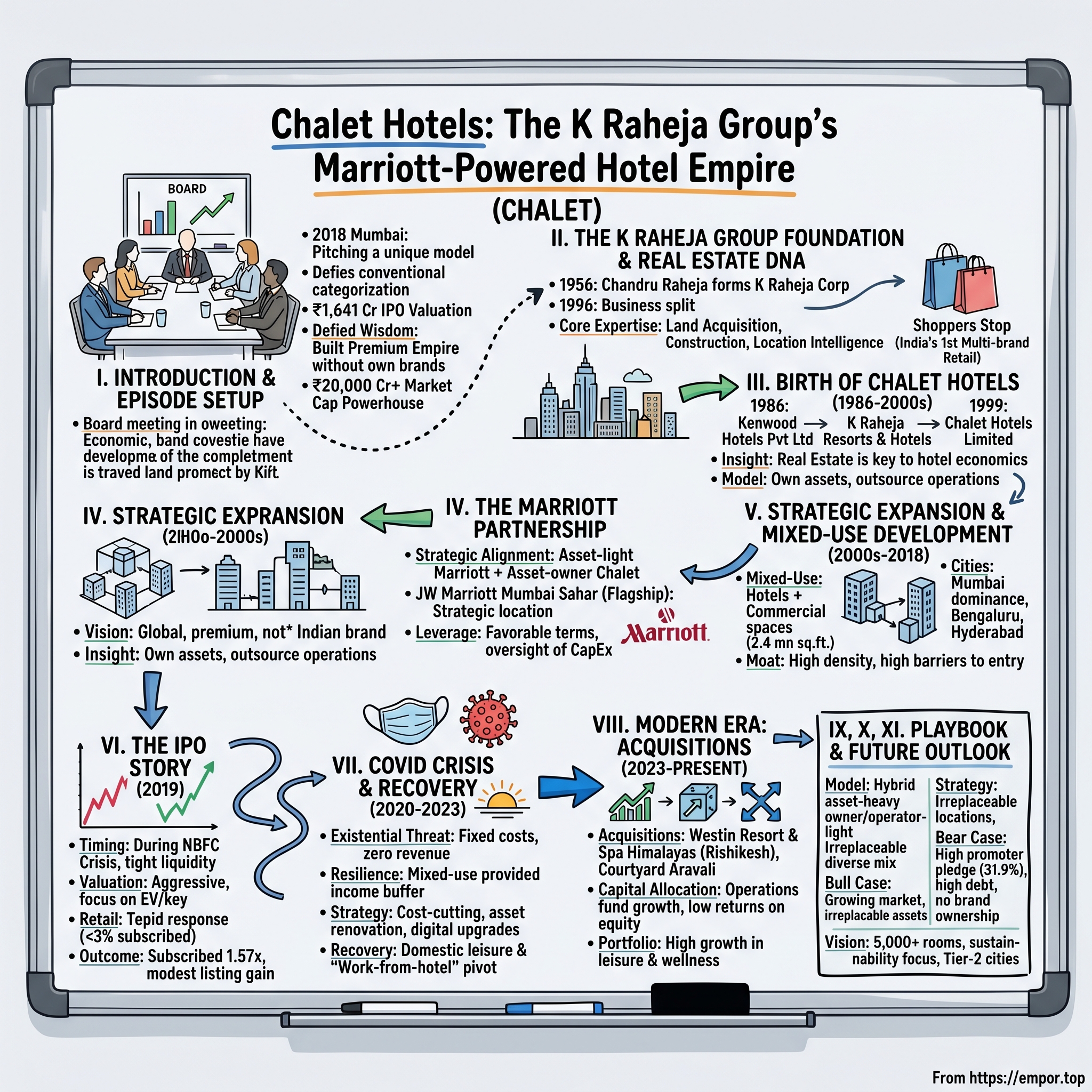

Chalet Hotels: The K Raheja Group's Marriott-Powered Hotel Empire

I. Introduction & Episode Setup

Picture this: It's 2018, and in the gleaming boardrooms of Mumbai's business district, a unique proposition is being pitched to investors. A hotel company that owns prime real estate worth thousands of crores, operates luxury properties under Marriott and Accor flags, but doesn't actually run the hotels themselves. The bankers are trying to explain why Chalet Hotels—a company that seems to defy conventional categorization—deserves a ₹1,641 crore IPO valuation. The question wasn't just about valuation—it was about identity. Is Chalet Hotels a real estate company that happens to own hotels? A hospitality operator without brands? Or something entirely different?

Welcome to the story of Chalet Hotels—a company that defied conventional wisdom by building India's premium hotel empire without creating a single hotel brand. It's a tale of strategic opportunism, where a real estate dynasty leveraged their land expertise to partner with global hospitality giants, creating a unique business model that would weather economic storms and emerge as a ₹20,000 crore market cap powerhouse.

The IPO bidding started from January 29, 2019 and ended on January 31, 2019, with allotment finalized on February 5, 2019. The shares got listed on BSE, NSE on February 7, 2019. The Rs. 1,641 crore IPO was split as Rs. 950 crore via fresh issue and an offer for sale (OFS) of 2.47 crore shares, with Rs. 691 crore OFS making up 41% of the total size.

This isn't just another hotel company story. It's about how the K Raheja Group—one of India's most successful real estate conglomerates—saw an opportunity where others saw complexity. While competitors built brands from scratch, Chalet built relationships. While others fought for operational control, Chalet mastered the art of strategic delegation. And while the industry obsessed over occupancy rates, Chalet focused on something more fundamental: location, location, location.

The roadmap ahead takes us through a seven-decade journey—from post-independence real estate dreams to modern hospitality innovation. We'll explore how a company incorporated as "Kenwood Hotels" in 1986 transformed into a Marriott-powered empire. We'll dissect the partnership model that lets them operate JW Marriotts without the brand burden. And we'll analyze how they turned the COVID crisis into an expansion opportunity, emerging stronger while competitors struggled.

But most intriguingly, we'll examine the paradox at the heart of their model: How do you maintain control when someone else runs your hotels? How do you build competitive advantages without owning brands? And in an industry obsessed with asset-light models, why did Chalet choose to own billions in real estate?

II. The K Raheja Group Foundation & Real Estate DNA

The year was 1956. As India was finding its feet as a newly independent nation, a young entrepreneur named Chandru Raheja saw opportunity where others saw chaos. The partition had created massive urban migration, cities were expanding rapidly, and India desperately needed modern infrastructure. Founded in 1956 by Chandru Raheja, K Raheja Corp was formed after a split between Raheja brothers as a separate group.

But the K Raheja story didn't begin in isolation. Chandru's father, Lachmandas Raheja, had founded the original K. Raheja Group in 1956, planting the seeds for what would become one of India's most powerful real estate dynasties. The family's entrepreneurial DNA ran deep, but it was the 1996 split that would truly unleash Chandru's vision.

The business was divided into three groups between Gopal Raheja, chairman of K Raheja Constructions, Suresh Raheja, chairman of K Raheja Universal and Chandru Raheja, the chairman of K Raheja Corp. While his brothers took their portions of the empire, Chandru had something different in mind—not just building structures, but creating ecosystems.

What emerged from this split wasn't just another real estate company. K Raheja Corp became India's leading Real Estate conglomerate, a success story spanning over four decades, with business diversified across office spaces, hospitality, malls, residential offerings, retail, and power. The group didn't just build buildings; they pioneered concepts that would reshape Indian urban life.

Consider their revolutionary approach to commercial spaces. K Raheja Corp was the first to initiate the concept of self contained township and commercial business districts which comprehend all the facilities like residential apartment, offices, malls, virtually making it a mini city. This wasn't just real estate development—it was urban planning on a private scale, creating integrated ecosystems where people could live, work, shop, and play without leaving the compound.

The Mindspace brand, launched in the late 1990s, exemplified this philosophy. These weren't just office parks; they were complete business ecosystems with integrated amenities, green spaces, and infrastructure that rivaled anything in Singapore or Hong Kong. By the time competitors caught on, K Raheja had already locked up prime land parcels in Mumbai, Hyderabad, and Pune.

But perhaps the most intriguing diversification came in retail. In 1991, K Raheja launched India's first multi-brand retail showroom, Shoppers Stop in Andheri, Mumbai. This wasn't just opportunistic expansion—it was strategic genius. By owning both the retail brands and the malls they operated in, K Raheja controlled the entire value chain. Multi-brand lifestyle store Shoppers Stop and its subsidiary bookstore company Crosswords are part of K Raheja Corp. The ₹5,113 crore company Shoppers Stop would eventually list on Indian stock exchanges, creating massive value for the group.

The retail empire didn't stop there. HyperCity Retail India Ltd. was part of the K Raheja Corp, which also owns Shoppers Stop. In 2017, Future Group acquired HyperCity for ₹655 crore. Even exits were profitable—the group had mastered the art of building value and monetizing at the right time.

By the early 2000s, K Raheja Corp had evolved far beyond its construction roots. It owns the brands Mindspace, Commerzone, Crossword Bookstores and Shoppers Stop, and is the second largest commercial developer in India. The company had built formidable expertise across the entire real estate value chain—from land acquisition and development to asset management and eventual monetization.

This multi-decade success wasn't accidental. The group's real estate DNA provided three critical advantages that would prove invaluable when they entered hospitality:

First, land acquisition expertise. In India's complex regulatory environment, knowing how to identify, acquire, and develop prime land parcels was a superpower. K Raheja had spent decades building relationships with landowners, understanding zoning laws, and navigating government approvals.

Second, construction and project management capabilities. While hotel operators worried about service standards, K Raheja could build properties at costs that made competitors weep. They controlled the entire construction value chain, from sourcing materials to managing contractors.

Third, location intelligence. Four decades of real estate development had given them an unmatched understanding of micro-markets. They knew which areas would boom before the boom happened, where infrastructure would improve, and how urban growth patterns evolved.

This real estate DNA would become the secret weapon in their hospitality journey. While traditional hotel companies struggled with high capital costs and long development cycles, K Raheja could leverage their existing capabilities to build hotels faster, cheaper, and in better locations than anyone else.

The stage was set. By the late 1990s, K Raheja Corp wasn't just a real estate company—it was an urban infrastructure powerhouse with tentacles in commercial, residential, retail, and mall development. The question wasn't whether to enter hospitality, but how to do it in a way that leveraged all their accumulated advantages while avoiding the pitfalls that had trapped traditional hotel companies.

III. Birth of Chalet Hotels: From Kenwood to Premium Hospitality (1986–2000s)

The story begins not with fanfare, but with a curious name: Kenwood. Chalet Hotels Limited was incorporated as a Private Limited Company with the name 'Kenwood Hotels Private Limited' on January 6 1986. Why would a Mumbai-based real estate group choose such an Anglo-Saxon name for their hospitality venture? The answer lies in the K Raheja Group's approach—they weren't trying to create an Indian hotel brand. From day one, they were thinking globally.

The evolution of the company's identity tells its own story. On July 19 1997 the Company was converted into a Public Company and the name was changed to 'Kenwood Hotels Limited'. On April 6 1998 the name of Company was further changed to 'K. Raheja Resorts & Hotels Limited'. Each name change reflected a strategic shift—from private ambitions to public aspirations, from generic hospitality to family-branded resorts.

But the most significant transformation came on May 4, 1999, when the company finally became "Chalet Hotels Limited." The name "Chalet"—evoking images of Alpine luxury and European sophistication—was deliberate. This wasn't going to be another Indian hotel chain competing on price. This would be about premium experiences, international standards, and global partnerships.

The company is part of the larger K. Raheja Corp Group, which has been in operation since 1956. The company was originally incorporated in 1986 and has focused on the development and management of high-end hotels in key metropolitan areas. But why did K Raheja Corp, already successful in real estate and retail, venture into hotels in 1986?

The timing was prescient. India was on the cusp of economic liberalization. Business travel was increasing. Mumbai was transforming from a manufacturing hub to a services powerhouse. And crucially, international hotel chains were beginning to eye India seriously. The Rahejas saw an opportunity that others missed: you didn't need to build a hotel brand to succeed in hospitality. You needed to own the right properties in the right locations.

This insight—that real estate, not branding, was the key to hotel economics—would define Chalet's entire strategy. While competitors like Indian Hotels (Taj) and EIH (Oberoi) invested heavily in brand building, marketing, and operational training, Chalet focused on what they knew best: identifying prime locations, acquiring land at favorable terms, and developing properties efficiently.

The early years were about learning and experimentation. The company's first properties were modest—business hotels in Mumbai's emerging commercial districts. But each project taught valuable lessons. How to optimize room configurations for maximum revenue. How to integrate commercial spaces with hospitality assets. How to negotiate with international operators.

The critical decision that would shape Chalet's future came in the mid-1990s. Should they create their own hotel brand or partner with established international chains? The traditional wisdom said own your brand—that's where the value lies. But the Rahejas saw it differently.

Building a hotel brand from scratch would require massive investments in marketing, training, technology, and systems. It would take decades to achieve the recognition that Marriott or Hilton enjoyed. And even then, success wasn't guaranteed. The graveyard of failed hotel brands was littered with well-funded attempts.

Instead, Chalet chose a different path: they would own the assets but outsource the operations. They would provide the hardware—the buildings, the locations, the capital. International operators would provide the software—the brand, the systems, the expertise.

This model had several advantages. First, it allowed Chalet to leverage world-class operational expertise without the learning curve. Second, it gave them access to global distribution systems and loyalty programs. Third, it reduced operational risk—if an operator underperformed, they could be replaced.

But most importantly, it allowed Chalet to focus on what they did best: real estate development and asset management. They could use their expertise to identify locations, their relationships to acquire land, and their construction capabilities to build efficiently. The actual running of hotels—the hiring, training, daily operations—could be left to specialists.

By the late 1990s, the strategy was crystallizing. Chalet would become India's premier owner of luxury hotel assets, operated by the world's best brands. They wouldn't compete with Taj or Oberoi on brand. They would compete on location, quality, and financial returns.

The transformation from Kenwood to Chalet wasn't just a name change—it was a strategic metamorphosis. The company had found its unique positioning in India's hospitality landscape. Now it needed the right partner to execute its vision.

IV. The Marriott Partnership: Building Without Branding

The year was 2000, and Chalet Hotels faced a defining moment. They had prime land near Mumbai's soon-to-be-expanded international airport. They had the capital. They had the construction expertise. What they needed was a brand partner who understood luxury, had global distribution, and most importantly, would work with them as asset owners rather than operators.

Enter Marriott International—the world's largest hotel company, with a portfolio spanning from limited-service to ultra-luxury. But it wasn't Marriott's size that attracted Chalet. It was their business model. Unlike Hilton or Hyatt, which still owned significant real estate, Marriott had fully embraced the asset-light model. They wanted to manage hotels, not own them. This alignment of interests would prove crucial.

The brand's portfolio includes hotels under the brands of Marriott and Renaissance, which have gained recognition for their service quality and luxury offerings. But this wasn't just about slapping a Marriott flag on a building. The partnership represented a fundamental reimagining of how hotels could be developed and operated in India.

The first major project under this partnership would set the template: JW Marriott Mumbai Sahar. Located strategically near Mumbai's international airport, this would be Chalet's flagship—588 spacious rooms with pillowtop beds, marble bathrooms and high-speed Wi-Fi, as well as generous work desks and 24-hour room service. The property wasn't just a hotel; it was a statement of intent.

The negotiations for this first partnership revealed the genius of Chalet's approach. Traditional hotel management contracts heavily favored the operator—long terms (often 20-30 years), significant fees (3-6% of revenue plus incentives), and limited owner oversight. But Chalet had leverage that most hotel owners lacked: they understood construction, they controlled prime locations, and they had patient capital from the K Raheja Group.

This leverage allowed them to negotiate terms that were unusually favorable for an owner. Shorter initial terms with renewal options. Performance-based incentive structures. Greater oversight of capital expenditure. And crucially, the ability to co-develop commercial spaces adjacent to the hotels, creating additional revenue streams that Marriott couldn't touch.

The asset management model Chalet developed was sophisticated. Unlike passive real estate investors who simply collected rent, Chalet remained deeply involved in their properties' performance. They closely monitored operations, benchmarked against competitors, and weren't afraid to push back on operator decisions that didn't align with ownership interests.

The group's hospitality business is focused on hotels and convention centres for business and leisure needs. K Raheja Corp promotes Chalet Hotels – a high end hotel chain in India with established global brands such as Sheraton (Starwood Hotels and Resorts), Westin and JW Marriott.

The relationship expanded rapidly. After JW Marriott Sahar came The Westin Mumbai Powai Lake—another strategic location overlooking one of Mumbai's few lakes, in the heart of the city's emerging IT corridor. Then Four Points by Sheraton in Navi Mumbai, capturing the overflow from Mumbai's congested business districts. Each property was carefully chosen, meticulously developed, and strategically positioned.

But why did Marriott agree to these terms? The answer lies in India's hotel market dynamics circa 2000-2010. International operators desperately wanted Indian exposure but faced significant challenges. Land acquisition was complex and expensive. Construction quality was inconsistent. Local partners often lacked sophistication or capital. Chalet solved all these problems.

For Marriott, Chalet represented the ideal partner: professionally managed, well-capitalized, with proven execution capabilities. They could deliver hotels on time, at quality standards Marriott demanded, in locations Marriott wanted. The trade-off—more owner-friendly terms—was worth it for guaranteed expansion in India's most important markets.

The financial model that emerged from these partnerships was compelling. Chalet would invest roughly ₹300-400 crores to develop a 300-room luxury hotel. Marriott would manage it, taking their fees but also driving occupancy through their global distribution system. Chalet would retain the real estate upside, collect the majority of operating profits, and control adjacent commercial developments.

This model had another crucial advantage: risk mitigation. If a hotel underperformed, Marriott bore reputational risk and could lose the management contract. But Chalet still owned a prime piece of real estate in a growing city. If the location appreciated—as Mumbai real estate inevitably did—Chalet won regardless of hotel performance.

The partnership also brought intangible benefits. Marriott's training programs elevated service standards. Their technology platforms improved operational efficiency. Their loyalty program—Marriott Bonvoy—drove high-value repeat customers. Chalet got all these benefits without the massive investments required to build them independently.

By 2010, the Chalet-Marriott partnership had become a template for hotel development in India. Other developers tried to replicate it, but few had Chalet's unique combination of real estate expertise, patient capital, and sophisticated asset management capabilities.

The success of this model attracted other operators too. Accor, the French hospitality giant, partnered with Chalet for properties where Marriott wasn't the right fit. This multi-brand strategy gave Chalet flexibility to match brands to specific markets and customer segments while maintaining their asset ownership model.

Looking back, the decision to partner rather than build brands seems obvious. But in 2000, it was contrarian. The conventional wisdom said brands created value. Chalet proved that in hospitality, like in real estate, location and execution could create more value than branding ever could.

V. Strategic Expansion & Mixed-Use Development (2000s–2018)

By 2005, Chalet Hotels had mastered the art of luxury hotel development. But a casual observation during a board meeting would transform their entire strategy. Someone noted that their hotels attracted not just guests, but also office workers from nearby buildings who used their restaurants, meeting rooms, and facilities. Why not capture that entire ecosystem?

The insight was brilliant in its simplicity. Chalet has also developed commercial spaces in proximity to the hotels, giving it a competitive lead in key metro cities, due to its first-mover advantage in large, mixed-use developments in specific micro-markets. This wasn't just about adding office buildings next to hotels. It was about creating self-contained business districts where the hotel became the social and commercial hub.

The numbers told the story. By the pre-IPO period, The Company's portfolio comprises 11 fully operational hotels representing 3351 keys, across mainstream and luxury segments, and commercial spaces, representing ~2.4 mn sq.ft. in close proximity to the hospitality assets. That 2.4 million square feet of commercial space wasn't an afterthought—it was generating predictable, high-margin rental income that smoothed out the cyclical nature of hotel revenues.

The Mumbai dominance was deliberate and strategic. The city represented India's commercial capital, with the highest room rates, strongest corporate demand, and most severe real estate constraints. Chalet's Mumbai portfolio read like a masterclass in location selection:

- JW Marriott Sahar: 588 keys positioned perfectly near the international airport

- The Westin Mumbai Powai Lake: 604 keys overlooking one of Mumbai's rare natural features

- Lakeside Chalet, Marriott Executive Apartments: 173 serviced apartments for long-stay executives

- Four Points by Sheraton, Navi Mumbai: 152 keys capturing the satellite city overflow

Each property wasn't just a hotel—it was an ecosystem. The JW Marriott Sahar, for instance, included significant commercial space that housed airline offices, travel companies, and businesses that needed airport proximity. The synergy was perfect: office tenants provided weekday hotel demand, while the hotel provided dining and meeting facilities for the offices.

The Powai property exemplified this mixed-use mastery. Located in Mumbai's emerging IT corridor, The Westin wasn't just competing for hotel guests—it was the social hub for the entire business district. Tech workers came for lunch meetings, companies booked conference facilities, and the property's restaurants became the default venue for corporate celebrations.

But Chalet's ambitions extended beyond Mumbai. The tech boom was creating new opportunities in Bengaluru and Hyderabad—cities with growing international business, increasing room rates, and less saturated hotel markets. The expansion strategy was surgical: target emerging business districts before they fully matured, lock in land at reasonable prices, and develop mixed-use properties that would benefit from the area's growth.

The Bengaluru Marriott Hotel Whitefield captured this perfectly. Whitefield was transforming from a sleepy suburb to Bengaluru's IT epicenter. By entering early with a premium property, Chalet locked in a dominant position that would become increasingly valuable as the area developed.

Similarly, The Westin Hyderabad Mindspace targeted the city's premier IT district. But Chalet went further—they didn't just build one Westin in Hyderabad, they built two, with The Westin Hyderabad Hitec City capturing another strategic node. This concentration strategy created operational efficiencies while dominating key micro-markets.

The Company's strength lies in identifying strategic locations and efficient design & development of properties focusing on gross built-up area and development cost per key. Majority of the assets are located in high-density business districts of metro cities with high barriers to entry. This "high barriers to entry" point was crucial—once Chalet secured prime locations in congested business districts, competitors couldn't easily replicate their position.

The pre-IPO portfolio of 2,328 keys across 6 hotels represented just the visible part of the iceberg. The real value lay in the integrated ecosystems they had created. A typical Chalet property might generate 60% of revenue from rooms, 20% from food and beverage, and 20% from commercial rentals—a far more balanced and resilient model than pure-play hotels.

The financial engineering was equally sophisticated. Commercial properties were often held in separate entities, allowing different financing structures and potential monetization options. Hotel properties could be leveraged for expansion, while commercial assets provided stable cash flows for debt service.

This period also saw Chalet refine their development philosophy. Rather than maximize the number of rooms, they optimized total revenue per square foot. This might mean allocating more space to high-margin restaurants, adding premium commercial space, or including serviced apartments that commanded higher rates than standard rooms.

The asset management model had evolved too. Chalet Hotels has also strategically streamlined operations by partnering with leading hospitality chains such as Marriott and Accor. It adheres to an active asset management model for hotels operated by third parties, closely monitoring and exercising a robust review mechanism driving operational and financial excellence.

By 2018, on the eve of their IPO, Chalet had built something unique in Indian hospitality. They weren't just a hotel company with some real estate, or a real estate company with some hotels. They were an integrated mixed-use developer that happened to specialize in hospitality-anchored projects. The distinction mattered—it meant higher margins, more stable cash flows, and most importantly, a competitive moat that pure hotel operators couldn't cross.

VI. The IPO Story: Timing, Valuation & Market Reception (2019)

January 29, 2019. The timing couldn't have been worse. The NBFC (Non-Banking Finance Companies) crisis which erupted in September-October of 2018 led to drying up of funds. This in turn drove companies away from the IPO markets. Ending this hiatus, Chalet Hotels have come up with the first IPO of 2019. The market was nervous, liquidity was tight, and investors were skittish about anything remotely connected to real estate.

But the Rahejas had waited long enough. Chalet Hotels is entering the primary market on Tuesday 29th January 2019 with a Rs. 1,641 crore IPO – split as Rs. 950 crore via fresh issue of equity shares of Rs.10 each and an offer for sale (OFS) of 2.47 crore share, both in the price band of Rs. 275 to Rs. 280 per share.

The structure was telling. Issue represents 28.59% of the post issue paid-up share capital (at upper end) with Rs. 691 crore OFS making up 41% of the total size. The promoters weren't just raising growth capital—they were also partially cashing out, a move that raised eyebrows among analysts.

The valuation debate dominated pre-IPO discussions. Since PAT is negative, PE based valuation is not possible. On cash profit basis, FY18 multiple stands at 38x, while EV/sales and EV/EBITDA multiples are 9x and 23x respectively. These were aggressive multiples for a capital-intensive business in a cyclical industry.

The most telling metric was EV per key. Another popular matrix used in the hospitality sector is EV/key, which is Rs. 3.3 crore for Chalet, as against Rs. 1.4 crore/key development cost (including land) incurred by the company in 2015 for 585 key JW Marriott Sahar. Investors were being asked to pay more than double the replacement cost.

The investment bankers—Axis Capital Limited, Jm Financial Limited, Morgan Stanley India Company Pvt Ltd—had their work cut out. They pitched Chalet not as a hotel company but as a unique play on India's premium real estate with operational upside. The mixed-use model, they argued, deserved a premium valuation.

But the market wasn't buying it. As the IPO opened on January 29, the response was tepid. The Chalet Hotels Limited IPO is subscribed 1.5706 times by Jan 31, 2019 18:00. Retail category of Chalet Hotels Limited IPO subscribed 0.0282 times. The retail investors—usually the most enthusiastic participants in IPOs—practically stayed away, subscribing less than 3% of their reserved portion.

The institutional response was marginally better, but hardly enthusiastic. The overall subscription of 1.57 times was barely enough to ensure the IPO went through. For context, successful IPOs in India typically see subscriptions of 5-10 times or more.

The analyst community was divided. Key positive for the company is its industry-leading EBITDA margin due to: promoter's real estate expertise coming in handy to keep capex low · property manager Marriott controlled opex (e.g. low employee cost vs industry). But the negatives were hard to ignore.

However, few negatives must also be highlighted here: High debt pressurising margins and denting debt-equity ratio, even on post listing. The debt burden was substantial—Total debt (Pre IPO) - Rs 2,689 crores Total debt (Post IPO) - Rs 1,969 crores. Even after using IPO proceeds for debt reduction, leverage remained high.

The timing issue went beyond just market conditions. In the current conditions, when bluechips are finding the going tough, it will not be a comfortable walk for this company. While hospitality industry believes to be at an inflection point as average daily rates may rise given average occupancy achieving critical mass, a macro economic slowdown, which has affected other consumption sectors like cars, cement etc. may not hold this premise true, especially in the near term.

SP Tulsian, one of India's most respected IPO analysts, was blunt: "Check-in not recommended." His verdict carried weight. While company's portfolio of asset and operating profit is strong, the risk-reward is not favourable, given the negatives highlighted above. In such uncertain times, one is better-off avoiding aggressively priced midcaps and instead look to accumulate large caps in the secondary market.

The company's recent financial performance didn't help. This company has shown loss for first half that raises concern. In a market looking for profitable growth stories, Chalet's losses—even if temporary—were a red flag.

Listing day, February 7, 2019, brought modest relief. Chalet Hotels IPO listed at a listing price of 290.40 against the offer price of 280.00. The 3.7% premium was respectable but hardly spectacular. It suggested the IPO was fairly priced but not a bargain.

The post-listing journey would prove the skeptics wrong, but that's a story for later. What mattered in February 2019 was that Chalet had crossed the rubicon. They were now a public company, with all the scrutiny, expectations, and opportunities that entailed.

The IPO raised important questions about Chalet's model. Was it too capital-intensive for public markets that preferred asset-light businesses? Was the dependence on Marriott a strength or vulnerability? Could a company without its own brands command premium valuations?

The lukewarm reception also reflected broader market concerns. The IL&FS crisis had shaken confidence in anything connected to real estate. The economic slowdown was becoming apparent. And the hotel industry's historically poor return ratios made investors wary.

But beneath the skepticism lay opportunity. At ₹280 per share, Chalet was valued at roughly ₹5,700 crores. The same company would be worth over ₹20,000 crores just five years later. Sometimes, the best investments are made when nobody else is interested.

VII. COVID Crisis & Recovery: The Resilience Test (2020–2023)

March 2020. The world stopped. For Chalet Hotels, with their concentration in Mumbai—India's COVID epicenter—and dependence on business travel, the pandemic represented an existential threat. Occupancy rates show what's happening. In early May, occupancy was less than 15% for luxury hotels. The math was brutal: fixed costs remained while revenues evaporated overnight.

The first quarter of fiscal 2021 told the story in numbers. Occupancy collapsed from 70%+ to single digits. Revenue per available room (RevPAR) fell by over 80%. But unlike standalone hotel operators, Chalet had a crucial advantage: their mixed-use model. While hotel revenues disappeared, commercial rentals continued, providing a financial lifeline when others were drowning.

The immediate response was textbook crisis management, but executed with unusual sophistication. Cost-cutting wasn't just about survival—it was strategic. Rather than blanket layoffs, Chalet negotiated with Marriott to reduce management fees, renegotiated vendor contracts, and implemented variable cost structures that could scale with recovery.

The debt burden—Rs 1,969 crores post-IPO—suddenly looked crushing. But here, the K Raheja Group's relationships proved invaluable. Banks, knowing the group's track record and asset quality, provided moratoriums and restructuring that wouldn't have been available to standalone operators.

What set Chalet apart during the crisis was their ability to think beyond survival. While competitors hibernated, Chalet used the downtime for strategic initiatives. Properties underwent renovations that would have been impossible with normal occupancy. Technology upgrades—contactless check-ins, digital room keys, enhanced air filtration—were accelerated.

The company also reimagined their customer mix. With international travel dead and corporate travel moribund, they pivoted to domestic leisure, staycations, and an unexpected segment: work-from-hotel packages. The Westin Powai, with its lake views and proximity to residential areas, became a refuge for Mumbai's affluent seeking escape from lockdown monotony.

As of 2023, Chalet Hotels Limited operates more than 3,200 rooms across various locations in India, including major cities like Mumbai, Bangalore, and Hyderabad. This expansion during the pandemic—when asset prices were depressed and competition was weakened—exemplified contrarian thinking at its best.

The recovery strategy was multi-pronged. First, capture the revenge travel boom as restrictions eased. Indians, unable to travel internationally, splurged on domestic luxury. Chalet's properties, with their international brands and prime locations, were perfectly positioned.

Second, reimagine the business mix. The traditional 70% corporate, 30% leisure split was dead. The new reality was 50% leisure, 30% corporate, 20% new segments (long stays, work-from-hotel, quarantine stays). This diversification made the business more resilient.

Third, accelerate the mixed-use strategy. With commercial real estate in flux and hotels recovering slowly, Chalet doubled down on creating integrated ecosystems. Hotels would anchor mixed-use developments that included co-working spaces, serviced apartments, and retail—creating multiple revenue streams from single properties.

In FY 2023, Chalet Hotels reported revenue of ₹1,117 crore, substantial growth from ₹970 crore in FY 2022, marking increase of approximately 15.16%. Growth attributed to resurgence in travel following lifting of pandemic restrictions. But this wasn't just recovery—it was transformation.

The pandemic had changed customer expectations permanently. Hygiene became paramount. Technology was no longer optional. Flexibility—in bookings, cancellations, services—became table stakes. Chalet's response wasn't just to meet these expectations but to exceed them, using the crisis to leapfrog competitors who were slower to adapt.

The financial recovery was remarkable. From near-zero occupancy in April 2020, properties returned to 60%+ by early 2023. Average room rates not only recovered but exceeded pre-pandemic levels as supply constraints and pent-up demand created pricing power.

But perhaps the most important outcome was strategic. The pandemic validated Chalet's model. While pure-play hotel companies struggled with fixed costs and no revenue, Chalet's mixed-use approach provided resilience. While brand-dependent operators had limited flexibility, Chalet could negotiate with partners and adapt quickly.

The crisis also accelerated industry consolidation. Weaker players exited or sold distressed assets. Chalet, with its strong balance sheet and patient capital, was a buyer, not a seller. Properties that would have been unaffordable in 2019 became available at attractive valuations in 2021-2022.

Looking back, COVID-19 was both Chalet's darkest hour and finest moment. They didn't just survive—they used the crisis to strengthen their competitive position, expand their portfolio, and validate their business model. Recovery to pre-COVID-19 levels could take until 2023—or later, the experts had warned. Chalet beat that timeline and emerged stronger than before.

VIII. Modern Era: Expansion, Acquisitions & Capital Allocation (2023–Present)

The post-pandemic world presented Chalet Hotels with a generational opportunity. While competitors struggled with debt and diminished valuations, Chalet emerged from COVID with a war chest and an appetite for growth. The Company's portfolio comprises 11 fully operational hotels representing 3314 keys as of May 2025, across mainstream and luxury segments, and commercial spaces representing ~2.4 mn sq.ft—but this was just the beginning.

The acquisition strategy that unfolded in 2023-2025 wasn't random opportunism—it was deliberate portfolio construction. Each deal filled a strategic gap, expanded geographic presence, or captured a new demand segment.

The most significant acquisition came in February 2025: Acquisition of 100% stake in Mahananda Spa and Resorts, owning The Westin Resort & Spa, Himalayas, a 141 room hotel at Rishikesh. Acquisition at enterprise value of Rs 530 crore. This wasn't just another hotel—it was Chalet's entry into the high-growth wellness and spiritual tourism segment.

Rishikesh, the "Yoga Capital of the World," represented a different kind of luxury—experiential rather than just material. The 141-key luxury resort boasts more than 10,000 sq ft of sophisticated event spaces, making it a sought-after destination for upscale gatherings. But more importantly, it tapped into the global wellness tourism boom, estimated to be growing at 20% annually.

The acquisition from Mankind Pharma's founders was telling. Even successful entrepreneurs from other industries were finding hospitality challenging. Managing Director and CEO Sanjay Sethi called the acquisition a "key milestone" in Chalet's growth strategy, reinforcing its presence in the high-growth luxury and leisure segment.

But the Rishikesh deal was part of a broader expansion spree. Last year, the company also acquired Courtyard by Marriott Aravali from Mankind Pharma's founders, highlighting its ongoing expansion through acquisitions. The Aravali property, launched in July 2022 with average daily rates exceeding ₹15,000 per night, gave Chalet its second property in North India.

The company has been expanding aggressively, acquiring an 11-acre site near Varca Beach in Goa, The Dukes Retreat in Khandala, and Courtyard by Marriott Aravali Resort in Delhi-NCR. Each acquisition followed a pattern: distressed sellers or first-time hospitality investors looking to exit, prime locations with high barriers to entry, and properties that could be enhanced through Chalet's operational expertise.

The capital allocation strategy was sophisticated. In Q3 FY25, Chalet Hotels reported a 22% revenue growth, reaching Rs 4.57 billion, with a net profit of Rs 963 million. This operational cash generation funded growth without excessive leverage—a lesson learned from the pre-IPO era.

But Chalet wasn't just buying hotels. The mixed-use development strategy accelerated. New projects integrated hotels with commercial spaces, co-working facilities, and even residential components. The company has about 70 per cent of its office spaces leased out across India and office rentals contribute about 13 to 14 per cent of its overall revenue and the rest from the hospitality business.

This diversification provided stability. While hotel revenues could be volatile—affected by everything from monsoons to geopolitical tensions—commercial rentals provided predictable cash flows. It also created synergies: business travelers staying at hotels often worked in adjacent office buildings.

The company intends to have about 5,000 rooms in the next three to four years in its entire portfolio. This represents nearly 50% growth from current levels—ambitious but achievable given their track record and capital access.

The leisure pivot was particularly strategic. India's domestic tourism was booming, driven by rising disposable incomes, improved infrastructure, and a growing preference for experiences over possessions. Properties like The Westin Rishikesh and Courtyard Aravali targeted this demand perfectly—close enough to major cities for weekend getaways, luxurious enough to command premium rates.

Market Cap: 19,469 Crore, Revenue: 2,251 Cr, Profit: 285 Cr—these numbers tell only part of the story. The real value lies in Chalet's transformation from a Mumbai-centric business hotel operator to a pan-Indian hospitality platform spanning business, leisure, wellness, and mixed-use developments.

The operational improvements were equally impressive. There is a lot happening because some of the assets that we have added in the last few quarters are still maturing, as they mature, the margins will improve in those assets. This maturation process—where newly acquired properties are integrated, renovated, and optimized—typically takes 12-18 months but can double profitability.

Progressive policies benchmarked at par with global standards. Certified Great Place to work for 6th time in a row in 2025, secured 11th Rank in India's Great Mid-Size Workplaces 2025. In an industry notorious for high turnover and poor working conditions, Chalet's employee-friendly approach created a competitive advantage in talent retention.

The capital markets rewarded this execution. From the IPO price of ₹280 in 2019, the stock had more than tripled by 2025. But Stock trading at 6.41 times book value, Company has low return on equity of 10.3% over last 3 years—the valuation premium reflected expectations of continued growth rather than current profitability.

Looking ahead, Chalet Hotels is positioning for the next phase of India's economic development. As GDP per capita rises, domestic tourism explodes, and international arrivals recover, the demand for quality hospitality will only grow. With their unique model—asset ownership with operational flexibility, mixed-use development capabilities, and strategic brand partnerships—Chalet is perfectly positioned to capture this growth.

IX. Playbook: The Chalet Hotels Operating System

The Chalet Hotels model is deceptively simple on the surface: own the real estate, partner for operations, maximize value per square foot. But the execution requires a sophisticated understanding of multiple industries—real estate development, hotel operations, commercial leasing, and capital markets. It's this multi-disciplinary expertise that creates Chalet's competitive moat.

Asset-Light but Asset-Owned: The Unique Model

The paradox at the heart of Chalet's model deserves examination. In an era where asset-light is gospel—from Uber to Airbnb—Chalet deliberately chose to own billions in real estate. But unlike traditional hotel companies that also own and operate, Chalet separated ownership from operations.

This hybrid model captures the best of both worlds. Asset ownership provides long-term value appreciation, control over strategic decisions, and the ability to capture multiple revenue streams from single properties. But outsourcing operations to Marriott and Accor eliminates the complexity of managing thousands of employees, maintaining brand standards, and keeping up with technological changes.

Company focusses on driving business efficiencies and sustainable growth right from pre-development stage, through entire lifecycle of assets, while maximising returns on every square foot owned and operated. This lifecycle approach means Chalet is involved from land acquisition through development, operations, and eventual monetization—but only in areas where they add unique value.

Location Strategy: High Barriers to Entry as Competitive Moat

Majority of the assets are located in high-density business districts of metro cities with high barriers to entry. This isn't accidental. Chalet's location strategy follows three principles:

First, density creates demand. Hotels in Mumbai's Bandra Kurla Complex or Hyderabad's Mindspace benefit from thousands of offices, millions of square feet of commercial space, and captive demand that doesn't depend on tourism cycles.

Second, scarcity creates pricing power. Once prime locations are developed, competitors can't replicate them. You can't build another hotel next to Mumbai airport—the land doesn't exist. This scarcity allows premium pricing even during downturns.

Third, mixed-use creates resilience. By developing commercial spaces alongside hotels, Chalet creates mini-ecosystems. The JW Marriott Sahar isn't just a hotel—it's a business hub with offices, restaurants, and meeting facilities that generate revenue independent of room occupancy.

Brand Partnerships vs. Ownership: The Trade-offs

The decision to partner with Marriott and Accor rather than build proprietary brands was controversial but ultimately vindicated. The trade-offs are clear:

Advantages of partnerships: - Immediate brand recognition and global distribution - Access to loyalty programs with millions of members - Operational expertise and standardized systems - Technology platforms that would cost hundreds of crores to develop - Reduced operational risk and complexity

Disadvantages: - Management fees (typically 3-6% of revenue) - Less control over operations and customer experience - Dependence on operator performance - No brand value creation

For Chalet, the math favored partnerships. Building a luxury hotel brand comparable to JW Marriott would take decades and billions in investment with uncertain returns. By partnering, they could focus capital and management attention on their core competency: real estate development and asset management.

Mixed-Use Development: Maximizing Land Value

Chalet has also developed commercial spaces in proximity to the hotels, giving it a competitive lead in key metro cities, due to its first-mover advantage in large, mixed-use developments in specific micro-markets. This strategy transforms simple hotel projects into complex real estate developments.

Consider a typical Chalet project: A 10-acre parcel might include a 300-room hotel, 200,000 sq ft of office space, 50 serviced apartments, and retail facilities. Each component supports the others. Office workers dine at hotel restaurants. Business travelers prefer hotels near their meetings. Serviced apartments cater to long-term corporate stays.

The financial impact is substantial. While a standalone hotel might generate ₹100 crores in annual revenue, the mixed-use development could generate ₹150 crores—with the additional ₹50 crores from commercial leases being far more stable and profitable than hotel revenues.

Capital Efficiency Metrics and Benchmarking

Chalet's capital efficiency can be measured through several metrics:

- Development cost per key: Chalet develops hotels at ₹1.5-2 crores per key versus industry average of ₹2.5-3 crores

- Revenue per square foot: Mixed-use properties generate ₹2,000-3,000 per sq ft versus ₹1,500 for standalone hotels

- Asset turnover: 0.4x, lower than pure operators but higher than pure real estate companies

- EBITDA margins: 35-40% versus 25-30% for traditional hotel companies

These metrics reflect the efficiency of Chalet's model. By controlling development costs through in-house expertise, maximizing revenue through mixed-use, and maintaining lean operations through outsourcing, they achieve returns superior to both traditional hotel companies and pure real estate players.

The Operating System in Practice

A typical Chalet project follows a well-defined playbook:

-

Land Acquisition: Leverage K Raheja relationships and market knowledge to identify and acquire prime parcels before full value is recognized

-

Development Planning: Design mixed-use projects that maximize revenue per square foot while maintaining luxury positioning

-

Partner Selection: Choose appropriate brand (JW Marriott for ultra-luxury, Courtyard for business hotels) and negotiate favorable terms

-

Construction Management: Use in-house expertise to control costs and timelines

-

Pre-Opening: Work with operator on hiring, training, and marketing while simultaneously leasing commercial spaces

-

Asset Management: Continuously monitor performance, benchmark against competition, and push for operational improvements

-

Value Enhancement: Regular renovations, rebranding if necessary, and optimization of commercial spaces

-

Capital Recycling: Selectively sell mature assets to fund new development

This systematic approach—refined over decades—is difficult for competitors to replicate. It requires patient capital, real estate expertise, operational knowledge, and relationship networks that take years to build.

X. Competition, Market Dynamics & Future Outlook

The Indian hospitality landscape presents a study in contrasts. Legacy players like Indian Hotels (Taj) and EIH (Oberoi) built their empires on brand prestige. New entrants like OYO disrupted with technology and scale. International chains expanded through franchising. Amidst this competitive chaos, Chalet carved out a unique position—neither a brand owner nor a pure franchise play, but something distinctively different.

The Competitive Landscape

Indian Hotels Company (IHCL), with its iconic Taj brand, represents the traditional approach—own the brand, own some assets, manage others. With over 200 hotels and market cap exceeding ₹70,000 crores, IHCL dwarfs Chalet in scale. But size doesn't always mean superior returns. IHCL's asset-heavy model and brand-building costs result in lower margins despite premium positioning.

EIH Limited (Oberoi) takes luxury to another level, but with only 35 properties, lacks scale. Their strategy of ultra-luxury in select markets creates pricing power but limits growth. Lemon Tree targets the budget-to-midscale segment—the opposite of Chalet's premium focus—proving that different strategies can coexist in India's diverse market.

The real disruption came from OYO, which applied Silicon Valley playbook to Indian hospitality—aggregate supply, standardize through technology, and scale rapidly. But OYO's struggles with quality control and partner relations validate Chalet's premium, controlled-growth approach.

International Chains: Threat or Opportunity?

Marriott, Hilton, Hyatt, and Accor are aggressively expanding in India, but primarily through franchise and management contracts. This expansion actually benefits Chalet—more brands seeking local partners with development capabilities and prime locations. Chalet's proven track record makes them a preferred partner.

The international chains face their own challenges. Direct ownership requires massive capital in India's expensive real estate markets. Franchise models depend on finding capable local partners. Management contracts need owners willing to invest hundreds of crores while ceding operational control. Chalet solves these problems, making them valuable to international brands rather than competitors.

The OYO and Airbnb Disruption

OYO's budget hotel aggregation and Airbnb's alternative accommodation model initially seemed like existential threats. But their impact on premium segment has been limited. Business travelers, Chalet's core customers, still prefer branded hotels with consistent service, corporate agreements, and proper invoicing.

If anything, OYO and Airbnb educated consumers about online booking and price transparency, trends that benefit all players. They also absorbed budget-conscious demand, allowing premium hotels to maintain pricing discipline rather than dropping rates to fill rooms.

India's Hospitality Boom Thesis

The macro story remains compelling. India's hotel room supply per capita is among the lowest globally—0.9 rooms per 1,000 people versus 4.5 in China and 16 in the US. As GDP per capita rises from $2,500 to $5,000 over the next decade, domestic travel will explode.

Business travel is recovering post-pandemic, but with a twist. Companies are consolidating vendors, preferring quality over price, and demanding flexibility. Chalet's premium properties in business hubs capture this demand perfectly.

The infrastructure boom—new airports, highways, high-speed rail—makes travel easier and more frequent. Mumbai's new airport, Bengaluru's expanded terminal, and Delhi's aerocity development all create demand for quality accommodation.

International tourism, while recovering slowly, presents massive potential. India received 10 million foreign tourists in 2019, compared to 65 million for Thailand. Even doubling foreign arrivals would transform the hospitality industry.

ESG and Sustainability Initiatives

Environmental consciousness is reshaping hospitality. Chalet's response has been substantive rather than cosmetic. New properties incorporate renewable energy, water recycling, and sustainable materials. Existing hotels undergo green retrofits that reduce operating costs while meeting corporate clients' ESG requirements.

But sustainability goes beyond environment. Certified Great Place to work for 6th time in a row in 2025 reflects social sustainability—treating employees well in an industry known for exploitation. This translates to lower turnover, better service, and ultimately, superior returns.

Technology and Digital Transformation

While Chalet doesn't own customer-facing technology, they benefit from partners' investments. Marriott's Bonvoy app, contactless check-in, and digital concierge services required billions in development—costs Chalet didn't bear but benefits from.

Chalet's technology focus is operational—using data analytics for revenue management, predictive maintenance for facilities, and automation for back-office functions. These less visible investments improve margins without the risk of consumer-facing technology bets.

Future Market Dynamics

Several trends will shape the industry's future:

Consolidation: Smaller players lacking scale or capital will exit or merge. Chalet, with its strong balance sheet and operational expertise, will be a consolidator rather than consolidated.

Premiumization: As Indians become wealthier, they'll trade up from budget to mid-scale, mid-scale to premium. Chalet's premium positioning captures this secular trend.

Experiential Travel: Post-pandemic, travelers seek experiences over simple accommodation. Properties like The Westin Rishikesh offering wellness, spirituality, and nature align perfectly with this trend.

Bleisure Travel: The blending of business and leisure travel benefits hotels that offer both corporate facilities and leisure amenities—exactly Chalet's sweet spot.

Domestic Tourism: International travel restrictions taught Indians to explore their own country. This structural shift toward domestic tourism provides sustained demand for quality hotels.

The competitive dynamics favor Chalet's model. Pure brand owners face rising customer acquisition costs. Pure operators face margin pressure from OTAs and competition. Real estate owners without operational expertise struggle with low returns. Chalet's hybrid model—owning strategic assets while leveraging others' operational expertise—navigates these challenges effectively.

XI. Bear vs. Bull Case Analysis

Every investment thesis has two sides. For Chalet Hotels, the bull case seems compelling—premium assets, proven execution, structural tailwinds. But the bear case deserves equal attention. Let's examine both with the rigor of institutional investors.

Bull Case: The Platform for India's Hospitality Future

India's Under-Penetrated Hospitality Market

The numbers are staggering. India has 0.9 hotel rooms per 1,000 people. China has 4.5. The US has 16. Even reaching China's penetration would require tripling India's room inventory. This isn't speculation—it's math.

But penetration rates tell only part of the story. Quality supply is even scarcer. Branded hotels represent less than 10% of India's total inventory versus 70% in the US. As Indian consumers become more discerning, demand for quality accommodation will outpace supply for years.

The GDP multiplier effect is proven globally—hotel demand grows at 1.5-2x GDP growth. With India targeting 7-8% GDP growth, hotel demand should grow at 10-15% annually. Even accounting for new supply, this creates sustained pricing power for existing hotels.

Strategic Locations with High Barriers to Entry

Chalet's properties aren't just well-located—they're irreplaceable. You cannot build another hotel next to Mumbai airport. The land doesn't exist. Powai Lake cannot be replicated. These locations become more valuable as cities grow around them.

The regulatory moat is equally important. Getting permits for hotel development in Indian metros takes years. Environmental clearances, traffic studies, height restrictions—each hurdle reduces competition. Chalet's existing properties bypassed these barriers when regulations were simpler.

Mixed-use development creates additional barriers. Competitors would need to match not just the hotel but also millions of square feet of commercial space. The capital requirements and execution complexity eliminate most potential competitors.

Asset Ownership Provides Downside Protection

Unlike asset-light models that can go to zero in downturns, Chalet owns real estate worth thousands of crores. Mumbai real estate has appreciated at 12% annually over the past two decades. Even if the hotel business struggles, the land value provides downside protection.

This isn't theoretical. During COVID, when hotel operations generated losses, the real estate still had value. Banks extended credit against property, not cash flows. Asset ownership provided resilience that pure operators lacked.

Real estate also provides optionality. Properties can be redeveloped, repurposed, or partially sold. A struggling hotel sitting on prime land can be converted to mixed-use, unlocking value impossible for operators without ownership.

K Raheja Group Backing and Synergies

The K Raheja connection provides advantages beyond capital. Knowledge of infrastructure development, land acquisition expertise, construction capabilities, vendor relationships—these create cost advantages competitors cannot match.

Group synergies extend to demand generation. Shoppers Stop customers become hotel guests. Office tenants in Mindspace properties use Chalet hotels for corporate events. Mall visitors dine at hotel restaurants. These internal synergies create a revenue base independent of market conditions.

The patient capital mentality matters. Public companies face quarterly earnings pressure. Chalet, with 67% promoter holding, can make long-term decisions—acquiring distressed assets, investing through downturns, waiting for locations to mature.

Recovery Momentum and Pricing Power

Post-COVID recovery isn't just about returning to 2019 levels—structural changes favor premium hotels. Corporate travel budgets concentrate on fewer, quality suppliers. Safety concerns drive preference for branded hotels. Revenge travel creates willingness to pay premium prices.

Chalet's average room rates already exceed pre-pandemic levels. Occupancy is recovering. The combination—higher rates and recovering occupancy—creates operational leverage that drops directly to the bottom line.

Bear Case: The Structural Challenges

Promoters Have Pledged 31.9% of Their Holding

This is concerning. Promoters have pledged or encumbered 31.9% of their holding. In market downturns, pledged shares can trigger forced selling, creating price pressure independent of fundamentals.

The pledge suggests promoters needed liquidity despite the company's apparent success. Are there hidden stresses? Undisclosed related-party obligations? The pledge creates uncertainty that sophisticated investors dislike.

High Debt Levels and Interest Burden

Despite post-IPO deleveraging, debt remains substantial. Interest coverage ratios are adequate but not comfortable. In a rising rate environment, interest costs could pressure profitability.

The capital-intensive model requires continuous investment. New properties, renovations, commercial development—all require capital. This creates a perpetual funding need that either dilutes equity or increases debt.

Debt also reduces flexibility. In downturns, high fixed costs (interest and operations) create losses quickly. Unlike asset-light models that can scale down, Chalet faces structural rigidity that amplifies cyclical risks.

No Brand Ownership Unlike Peers

Company does not own the brands (unlike bigger peers Indian Hotels, EIH and even Lemon Tree). This is a fundamental strategic weakness. Brands create customer loyalty, pricing power, and enterprise value beyond physical assets.

Management contracts with Marriott and Accor typically run 15-30 years, but they're not permanent. If relationships sour or terms become unfavorable at renewal, Chalet faces rebranding costs and customer confusion.

Without brands, Chalet cannot expand through asset-light franchising or management contracts. Every expansion requires capital investment. Peers can grow by licensing their brands—a higher-return, scalable model unavailable to Chalet.

Concentration Risk in Mumbai Market

Mumbai generates the majority of revenue. This concentration creates vulnerability to local shocks—flooding, infrastructure failures, terrorism, or economic downturns affecting India's financial capital.

Mumbai's hotel market is also the most competitive, with every major brand present. New supply from competitors could pressure occupancy and rates. The new airport might shift demand patterns, affecting properties positioned for the old airport.

Regulatory risks in Mumbai are significant. Coastal zone regulations, height restrictions, property taxes—all could adversely impact operations. The recent draft Development Control Regulations suggest tightening rather than loosening of rules.

Capital Intensive Growth Model

Unlike technology companies that scale with minimal incremental capital, every Chalet expansion requires hundreds of crores. This limits growth rate and return on equity.

Company has a low return on equity of 10.3% over last 3 years. For a company trading at 6.41 times book value, these returns don't justify the premium valuation. Investors paying 6x book value for 10% ROE are betting on dramatic improvement.

The capital intensity also creates execution risk. Construction delays, cost overruns, lower-than-expected returns—each project carries risks that compound with expansion.

The Balanced View

Neither bull nor bear case exists in isolation. The truth incorporates elements of both. Chalet's premium assets and strategic locations provide genuine competitive advantages. But high debt, lack of brand ownership, and capital intensity create structural limitations.

The investment decision depends on time horizon and risk tolerance. Short-term investors face uncertainty from debt levels and economic cycles. Long-term investors might see through-the-cycle value creation from irreplaceable assets and India's structural hospitality growth.

Valuation matters. At ₹280 (IPO price), the risk-reward was attractive. At current levels above ₹900, much of the good news appears priced in. Future returns depend on execution—successful acquisitions, margin expansion, and navigating the next downturn.

XII. If We Were CEOs: Strategic Choices

Sitting in Chalet's corner office overlooking Mumbai's skyline, what strategic decisions would maximize long-term value? The answer isn't obvious. The current model works, but success creates its own challenges—complacency, competition, and the complexity of scale.

Brand Creation vs. Partnership Debate

The elephant in the room: should Chalet create its own brand? The arguments for are compelling. Brands create enterprise value beyond physical assets. They enable asset-light expansion through franchising. They provide control over customer experience.

But building a luxury hotel brand in 2025 isn't like 1903 when the Taj was founded. The market is saturated with brands. Customer acquisition costs are astronomical. The investment—probably ₹1,000+ crores over a decade—might generate negative returns.

The smarter play might be acquiring a distressed but salvageable brand. Imagine buying a regional luxury brand with heritage properties but weak finances. Chalet's operational expertise and capital could revive it while gaining brand IP.

Alternatively, create a hybrid—white-label luxury where Chalet controls operations but doesn't build consumer brand. Focus on B2B—corporate contracts, travel agents, OTAs—where brand matters less than location and service quality.

Geographic Expansion Priorities

The current portfolio concentrates in Mumbai, Bengaluru, Hyderabad, and NCR. The next wave of expansion should target:

Tier-2 Tech Cities: Pune, Chennai, Kochi—cities with growing IT sectors but less hotel supply. These markets offer better entry valuations and faster growth.

Leisure Destinations: Goa, Kerala, Rajasthan, Northeast—capture the domestic tourism boom. The Rishikesh acquisition shows this works, but needs acceleration.

Religious Circuits: Varanasi, Amritsar, Tirupati—massive domestic demand, limited quality supply. A premium offering in religious cities could generate exceptional returns.

International: This is controversial, but consider Sri Lanka, Nepal, Bhutan—markets where Indian expertise translates and Marriott partnerships extend. Small bets could provide learnings for larger expansion.

Technology and Digital Transformation

Chalet's technology strategy has been passive—rely on partners' investments. This needs evolution. Not competing with Marriott's consumer technology, but building proprietary capabilities in:

Revenue Management AI: Dynamic pricing across rooms, commercial spaces, and services based on demand patterns, events, and competition.

Predictive Maintenance: IoT sensors and analytics to prevent equipment failures, reduce maintenance costs, and improve guest experience.

Customer Intelligence: Even without owning brands, Chalet can build databases of guests, preferences, and patterns to drive direct bookings and reduce OTA dependence.

Virtual Hospitality: The metaverse sounds ridiculous, but virtual hotel tours, digital concierge services, and online experiences could generate revenue without physical capacity constraints.

Capital Allocation: Growth vs. Dividends

Though the company is reporting repeated profits, it is not paying out dividend. This is controversial. Growth companies reinvest profits, but at some point, shareholders deserve returns.

The optimal strategy might be variable dividends—pay out excess cash after funding identified growth opportunities. This maintains flexibility while rewarding shareholders. A 2-3% dividend yield would attract income investors without constraining growth.

Buybacks could be better than dividends given the tax efficiency. When stock trades below intrinsic value, buybacks create more value than acquisitions. The promoter stake makes this complex but not impossible.

The Next 5-Year Vision

By 2030, Chalet should be:

Scale: 5,000+ keys across 15+ cities, making it India's largest premium hotel owner

Diversification: 40% Mumbai, 30% other metros, 30% leisure destinations—reducing concentration risk

Revenue Mix: 60% hotels, 25% commercial, 15% new ventures (co-working, serviced apartments, senior living)

Technology Integration: Direct bookings at 30%+ of revenue, reducing OTA dependence

Sustainability Leadership: Net-zero operations by 2030, creating premium from ESG-focused investors

Capital Structure: Debt-to-equity below 1x, investment-grade rating, regular dividends

Brand Option: Either acquired brand or proven white-label model, enabling asset-light growth

This vision requires bold moves—larger acquisitions, international expansion, technology investments. But the alternative—incremental growth in existing markets—risks competitive disadvantage as the industry evolves.

The CEO's job isn't just executing today's model but building tomorrow's. Chalet's current success creates the platform and credibility for transformation. The question is whether management has the vision and courage to evolve before circumstances force change.

The Chalet Hotels story is far from over. From its origins as Kenwood Hotels in 1986 to its current position as a ₹20,000 crore hospitality powerhouse, the company has consistently defied conventional wisdom. While others built brands, Chalet built assets. While others chased scale, Chalet focused on quality. While others went asset-light, Chalet doubled down on ownership.

The model isn't perfect. High debt, lack of brand ownership, and capital intensity create structural challenges. Promoters have pledged or encumbered 31.9% of their holding. Company has a low return on equity of 10.3% over last 3 years. These aren't minor issues—they're fundamental questions about sustainability and value creation.

Yet the bull case remains compelling. India's hospitality market will double or triple over the next decade. Premium hotels in prime locations will capture disproportionate value. Mixed-use development provides resilience and returns superior to pure plays. The K Raheja backing provides patient capital and expertise competitors lack.

For investors, Chalet represents a bet on India's consumption story, real estate appreciation, and the premiumization of travel. It's not without risks—no investment is—but the asymmetry favors the upside. The assets are real, the locations irreplaceable, and the market opportunity enormous.

The strategic choices ahead—brand creation, geographic expansion, technology adoption—will determine whether Chalet becomes India's hospitality champion or remains a successful but subscale player. Management's track record suggests they'll make the right calls, but execution in an evolving industry is never guaranteed.

What makes Chalet fascinating isn't just what it is, but what it represents—a uniquely Indian solution to hospitality, blending real estate expertise with operational partnerships, patient capital with public market discipline, local knowledge with global standards. It's a model that shouldn't work in theory but does in practice.

As India stands on the cusp of explosive growth in travel and tourism, Chalet Hotels is positioned to capture this opportunity. Whether they fully capitalize depends on strategic choices made today. The story continues, and the best chapters may be yet unwritten.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube