Capri Global Capital: From Financial Advisory to India's NBFC Powerhouse

I. Introduction & Setting the Stage

Picture this: It's March 2023, and the Women's Premier League is making headlines across India. Among the franchise owners sits an unlikely name—not a Bollywood star, not a tech billionaire, but Capri Global Capital Limited, a non-banking financial company that most cricket fans have never heard of. The UP Warriorz, decked in orange and gold, take the field while their corporate parent quietly processes thousands of MSME loans across tier-2 and tier-3 cities. It's a paradox that defines modern Indian business: a company built on unglamorous lending to small businesses and affordable housing suddenly thrust into the spotlight of India's newest sporting spectacle.

This is the story of how a company that changed its name four times, pivoted its business model repeatedly, and nearly disappeared into obscurity became a ₹17,800 crore market cap powerhouse. Today, CGCL generates ₹3,534 crores in revenue and ₹578 crores in profit, operating through 800+ branches across 12 states. But the numbers only tell part of the story.

The real narrative is about timing, transformation, and the relentless pursuit of India's underserved millions. It's about recognizing that between the traditional banks that won't lend to small businesses and the predatory moneylenders charging usurious rates, there existed a massive opportunity. An opportunity that required patient capital, deep local relationships, and the willingness to build infrastructure where others saw only risk.

What makes CGCL fascinating isn't just its financial performance—though a 34% revenue growth and 71% earnings surge in 2024 certainly catches attention. It's how the company navigated India's complex regulatory landscape, survived multiple economic cycles, and emerged as a diversified lender when most NBFCs either failed or got acquired. The company that started as Daiwa Securities in 1994, morphed through Dover Securities and Money Matters Financial Services, before finally settling on Capri Global Capital in 2013, has become a case study in institutional resilience.

The big question isn't just how they did it—it's whether their playbook can sustain them through India's next economic chapter. As we dive into this multi-decade saga, we'll explore the strategic pivots, the near-death experiences, and the calculated bets that transformed a wandering financial advisory firm into one of India's most intriguing NBFC stories. Along the way, we'll uncover why owning a cricket team might be more than just a vanity project, how co-lending became their secret weapon, and what the next decade might hold for this unlikely financial services champion.

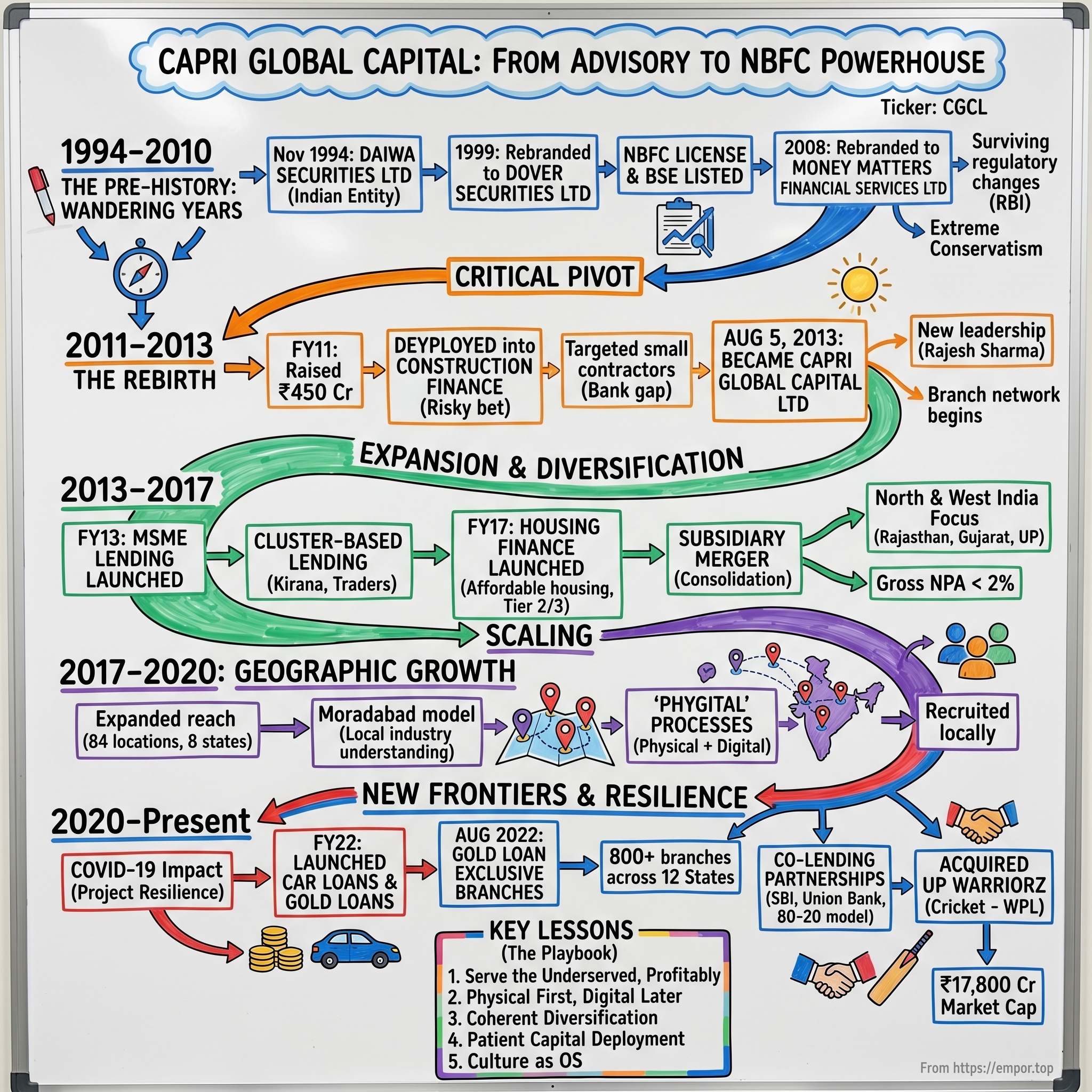

II. The Pre-History & Early Incarnations (1994-2010)

The Mumbai of 1994 was a city in transition. The Bombay Stock Exchange had just witnessed the Harshad Mehta scam two years prior, foreign institutional investors were tentatively entering Indian markets post-liberalization, and trust in financial intermediaries was at an all-time low. Into this environment came Daiwa Securities Limited—not the Japanese giant, but an Indian entity that would eventually become Capri Global Capital.

The company's early years read like a corporate identity crisis. Incorporated in November 1994 as Daiwa Securities Limited, it operated in the shadows of India's nascent capital markets. The name itself was curious—leveraging the credibility of a Japanese-sounding moniker in an era when foreign partnerships signaled sophistication. But by 1999, reality set in. The company shed its international pretensions and became Dover Securities Limited, a more honest reflection of its modest domestic operations.

These were the wandering years, characterized by false starts and strategic pivots. The company dabbled in financial advisory services, tried its hand at debt syndication, and eventually registered as a BSE-listed non-deposit taking NBFC. Think of it as a financial services firm searching for its soul—offering advisory to companies that couldn't afford the big investment banks, trading in debt securities when opportunities arose, and essentially surviving on the margins of India's formal financial system.

The regulatory environment was particularly challenging. The Reserve Bank of India, still carrying scars from various NBFC crises of the 1990s, had tightened regulations significantly. Capital requirements were increasing, operational guidelines were becoming more stringent, and the space for small, undifferentiated players was shrinking rapidly. Dover Securities found itself in a classic squeeze—too small to compete with banks, too regulated to be nimble, and lacking a clear value proposition that resonated with either borrowers or investors.

By 2008, another transformation was underway. Dover Securities became Money Matters Financial Services Limited—a name that sounds like it was chosen by a committee trying too hard to be consumer-friendly. The rebranding reflected a shift in ambition, moving from pure financial intermediation toward more direct lending activities. But the timing couldn't have been worse. The global financial crisis was unfolding, credit markets were freezing, and Indian NBFCs were facing their worst liquidity crisis in a decade.

What's remarkable about this period isn't what the company achieved—it's what it survived. While larger NBFCs collapsed or merged, while foreign players retreated from India, this small entity persisted. The management, whose names are lost to corporate history during this period, made a crucial decision: instead of chasing growth at any cost, they would preserve capital and wait for the right opportunity.

The company's balance sheet during these years tells a story of extreme conservatism. Limited leverage, minimal asset growth, and a focus on fee-based income rather than balance sheet expansion. It was unglamorous, even boring. But in hindsight, this conservatism created the foundation for what would come next. By staying alive when others died, by maintaining their NBFC license when others surrendered it, they positioned themselves perfectly for the transformation that would begin in 2011.

The lesson from these early years is counterintuitive: sometimes the best strategy is simply to survive. In a country where thousands of financial services companies have come and gone, where regulatory changes can destroy business models overnight, mere persistence becomes a competitive advantage. The company that would become Capri Global understood this implicitly. They weren't trying to be heroes; they were trying to be survivors. And in the Indian NBFC sector, survivors eventually get their chance to thrive.

III. The Rebirth as Capri Global (2011-2013)

The boardroom at Money Matters Financial Services in early 2011 must have felt electric. After years of treading water, the company was about to make its biggest bet yet. The decision wasn't just to raise capital—plenty of NBFCs did that. It was to raise ₹450 crores and immediately deploy it into construction finance, one of the riskiest segments in Indian lending. For a company that had survived by being conservative, this was the equivalent of a chess player suddenly sacrificing their queen to open up the board.

The timing seemed almost suicidal. Real estate markets were overheated, land acquisition controversies were making headlines, and everyone remembered the 2008 property crash. But the new leadership saw something others missed: India's infrastructure boom was creating a massive funding gap. Banks were happy to fund large developers but ignored small and medium contractors. These contractors—building everything from affordable housing to commercial complexes—were borrowing from local moneylenders at rates that would make a loan shark blush.

The transformation accelerated in 2013 when the company finally shed its awkward Money Matters moniker and became Capri Global Capital Limited. The name change on August 5, 2013, wasn't just cosmetic. It signaled a complete strategic overhaul. "Capri" evoked sophistication and aspiration, while "Global Capital" suggested scale and ambition. More importantly, it marked a psychological break from the company's meandering past.

But names don't build businesses—people do. The leadership team that orchestrated this transformation understood a fundamental truth about Indian lending: the opportunity wasn't in competing with banks for prime customers, but in serving the vast universe of borrowers that banks wouldn't touch. This wasn't about financial inclusion as charity; it was financial inclusion as a business model.

The construction finance business became their laboratory for innovation. Unlike banks that demanded extensive documentation and collateral that small contractors couldn't provide, Capri developed a different approach. They sent relationship managers to construction sites, understood cash flow patterns, and structured loans around project milestones rather than traditional metrics. A contractor building a school in Lucknow didn't need to provide three years of audited financials; they needed someone who understood that government payments came in lumps and construction happened in phases. The numbers tell one story, but the human element tells another. Rajesh Sharma, a first-generation entrepreneur, emerged as the driving force behind this transformation. Unlike the typical NBFC promoter who came from banking or old money, Sharma brought an outsider's perspective. He understood that India's formal financial system was failing millions of small businesses not because they were uncreditworthy, but because the system wasn't designed for them.

The ₹450 crore raised in FY11 wasn't just capital—it was a war chest that allowed Capri to build capabilities others couldn't afford. They hired teams from failed NBFCs, invested in technology when others were cutting costs, and most importantly, began building a branch network in markets where established players feared to tread. By 2013, when the company officially became Capri Global Capital Limited, they had already laid the groundwork for what would become their signature move: serving the underserved profitably.

The real innovation wasn't in the products they offered—construction finance had existed for decades. It was in how they underwrote and serviced these loans. Traditional lenders looked at balance sheets; Capri looked at cash flows. Banks demanded collateral worth 200% of the loan; Capri structured deals based on project viability. While others waited for borrowers to come to them, Capri's relationship managers went to construction sites, mandis, and industrial clusters.

This period also saw the beginning of what would become a defining characteristic of Capri's strategy: patience. Unlike the venture-funded fintech companies that would emerge later, Capri wasn't in a hurry to show hockey-stick growth. They were building infrastructure—not just physical branches, but trust networks, underwriting expertise, and operational capabilities that would take years to mature. The construction finance business, which many saw as their risky bet, was actually their training ground for everything that would follow.

IV. The Great Expansion: Product Diversification (2013-2017)

The conference room walls at Capri's Mumbai headquarters in 2013 must have been covered with maps and charts. The question wasn't whether to expand, but how fast and into which segments. The construction finance business was generating healthy returns, but relying on a single product line in Indian lending was like sailing with one sail—functional but vulnerable. The decision to launch MSME lending that year would prove to be the inflection point that transformed Capri from a niche player into a diversified NBFC.

The MSME lending launch in FY13 wasn't just adding another product—it was entering India's most competitive yet underserved lending segment. Every bank claimed to serve MSMEs, yet millions of small businesses still borrowed from informal sources at rates exceeding 36% annually. The disconnect was glaring: banks wanted two years of ITR filings, but most MSMEs barely maintained proper books. Banks demanded collateral, but MSMEs' biggest assets were often their business relationships and cash flows.

Capri's approach was radically different. They built what they called "cluster-based lending"—identifying geographic or trade clusters where similar businesses operated, understanding their unique cash flow patterns, and designing products specifically for them. A kirana store owner in Jaipur had different financing needs than a textile trader in Surat. Instead of force-fitting them into standard products, Capri created variations—working capital loans timed to inventory cycles, term loans for shop expansion, and even emergency credit lines for seasonal disruptions.

By FY17, they added Housing Finance to their portfolio, targeting the affordable housing segment that mainstream housing finance companies ignored. This wasn't the ₹50 lakh home loans that HDFC or LIC Housing Finance competed for. These were ₹10-15 lakh loans to first-time homebuyers in tier-2 and tier-3 cities, often self-employed individuals whose income documentation was patchy at best. The same underwriting philosophy that worked for MSMEs—look beyond paperwork to actual repayment capacity—proved equally effective in affordable housing.

But the most dramatic transformation during this period happened in 2015-2016, hidden in the corporate actions that most investors ignored. Capri Global Distribution Company Private Limited, Capri Global Finance Private Limited, Capri Global Investment Advisors Private Limited, and Capri Global Research Private Limited all merged with the parent company. This wasn't just corporate cleanup—it was strategic consolidation. By bringing all subsidiaries under one roof, Capri eliminated redundancies, improved capital efficiency, and most importantly, created a unified platform for cross-selling.

The merger revealed something profound about Capri's evolution. They weren't building separate businesses; they were creating an ecosystem. The same customer who took a construction finance loan might need MSME lending for their suppliers. The small business owner who started with a working capital loan might graduate to a home loan. This wasn't theoretical—by 2016, over 30% of new business was coming from existing customers or their referrals.

The company's focus on North and West India during this period was deliberate. These markets had several advantages: large MSME clusters, growing real estate markets, and relatively less competition from established NBFCs. States like Rajasthan, Gujarat, and Uttar Pradesh became their laboratories for innovation. What worked in Jodhpur's marble trading cluster could be replicated in Morbi's ceramic industry. Lessons from financing small developers in Ahmedabad informed their approach in Lucknow.

The numbers from this period tell a story of disciplined execution. Assets under management grew from ₹500 crores to over ₹2,000 crores, but more importantly, the portfolio quality remained robust. Their gross NPA stayed below 2%—remarkable for a company lending to segments considered "high risk" by traditional metrics. The secret wasn't better customers; it was better understanding of customers. While banks relied on credit scores and financial statements, Capri's field officers knew their borrowers' businesses intimately—their suppliers, their customers, their seasonal patterns, even their family situations.

Technology adoption during this phase was pragmatic rather than revolutionary. They didn't try to build a "digital-first" NBFC like the fintech players who would emerge later. Instead, they digitized specific pain points—loan origination systems for faster processing, mobile apps for field officers to upload documents, automated credit scoring for standard products. The goal wasn't to eliminate human judgment but to augment it with data and efficiency.

By 2017, Capri had transformed from a single-product construction finance company into a diversified lender with multiple revenue streams. But more than products, they had built capabilities—underwriting expertise in informal sectors, a distribution network in underserved markets, and most crucially, a reputation for being a lender that understood its customers' realities rather than forcing them into predetermined boxes. This foundation would prove invaluable as they entered their next phase of geographic expansion.

V. Geographic Expansion & Scaling (2017-2020)

The dusty roads connecting Kanpur to Agra, Udaipur to Ajmer, and Surat to Vadodara became Capri's highways to growth. While Mumbai's financial district debated digital disruption and fintech revolution, Capri's expansion team was setting up branches in places where bank branches had closed down years ago. By 2018-19, they had expanded their reach to 84 locations spread over 8 states, but each new pin on the map represented months of groundwork, relationship building, and careful calibration of risk and opportunity.

The expansion strategy was counterintuitive in an era obsessed with digital reach. While fintech startups boasted about their app downloads and digital onboarding, Capri was investing in physical infrastructure. Each branch opening followed a meticulous playbook: scout the location for six months, understand local business dynamics, hire relationship managers from the community, and slowly build trust through small-ticket loans before scaling up. A branch in Bikaner wasn't just a Capri outpost; it became part of the local business ecosystem.

Consider the Moradabad expansion in 2018. Known as "Brass City," Moradabad's handicraft exporters had been struggling with working capital for years. Banks found their business too volatile—orders from foreign buyers were erratic, payment cycles were long, and most transactions happened in cash. Capri's team spent three months just understanding the brass manufacturing process, export cycles, and payment patterns. They discovered that these businesses were actually less risky than they appeared—export orders, even if delayed, almost always got paid, and the community had strong internal mechanisms for dispute resolution.

The Moradabad model became a template for entering new markets: understand the dominant local industry, design products around their specific needs, and build trust through consistent presence. In Panipat's textile clusters, they financed power loom operators. In Jodhpur, they backed furniture manufacturers. In Ludhiana, they supported sports goods exporters. Each market required different underwriting criteria, different relationship management approaches, and different risk mitigation strategies.

Technology during this expansion played a supporting rather than leading role. The company developed what they called "phygital" processes—physical presence enhanced by digital tools. Loan applications started with face-to-face meetings but were processed through tablet-based systems. Documents were collected in person but verified digitally. Repayments could happen through multiple channels—cash at branches, digital transfers, or even through local collection agents. This hybrid model proved perfect for customers transitioning from informal to formal credit.

The competition landscape during this period was particularly interesting. Public sector banks were retreating from smaller markets due to NPA pressures. Private banks cherry-picked only the best customers. Traditional NBFCs were struggling with liquidity issues post the IL&FS crisis. Fintech lenders hadn't yet figured out how to serve customers without smartphones or digital footprints. Capri found itself in a sweet spot—organized enough to scale efficiently, local enough to understand customer needs, and patient enough to build sustainable portfolios.

One of the most underappreciated aspects of this expansion was talent management. Capri couldn't parachute Mumbai-trained bankers into Muzaffarnagar and expect them to succeed. Instead, they recruited locally—the branch manager in Bikaner was someone who had grown up there, understood local business families, and could navigate the complex social dynamics that determined creditworthiness in these markets. Training programs focused not just on financial analysis but on cultural sensitivity, relationship building, and ethical lending practices.

The housing finance subsidiary's expansion followed a similar pattern but with unique twists. They targeted affordable housing in the same geographies where they had MSME presence. This created powerful synergies—the small business owner who took an MSME loan often needed a home loan within a few years. The contractor who borrowed for working capital might later need construction finance. The cross-selling opportunities were natural and trust-based rather than forced.

Risk management during this rapid expansion required constant vigilance. Each new market brought new challenges—different local regulations, varying customer behaviors, unique competitive dynamics. The company developed what they called "market risk scorecards"—detailed assessments of local economic conditions, competitive intensity, regulatory environment, and portfolio performance metrics. Branches that showed early signs of stress received additional support or modified product offerings.

By early 2020, just before COVID-19 struck, Capri had built something remarkable—a network that reached deep into India's economic hinterland while maintaining portfolio quality that matched or exceeded many larger players. Their presence in 8 states wasn't just about geographic diversification; it was about building multiple engines of growth, each calibrated to local conditions but operating within a unified risk and governance framework. This distributed resilience would prove invaluable when the pandemic tested every assumption about lending and credit risk.

VI. The New Frontiers: Gold Loans & Beyond (2020-Present)

March 2020. The nation goes into lockdown. MSMEs shut their shutters, construction sites fall silent, and the entire lending industry holds its breath. For Capri Global, the pandemic could have been catastrophic—their customers were exactly the segments hit hardest by COVID-19. Yet what followed wasn't collapse but transformation. The crisis became a catalyst for their most ambitious expansion yet.

The immediate response was triage. Collections dropped to 60% in April 2020 as customers struggled with the sudden economic stop. But instead of aggressive recovery tactics, Capri activated what they called "Project Resilience." Relationship managers called every single customer—not to demand payment but to understand their situation. Moratoriums were offered proactively. Restructuring happened before defaults. The message was clear: we're in this together. By September 2020, collections had recovered to 92%, and more importantly, customer trust had deepened.

But the real story of this period isn't crisis management—it's opportunity recognition. In FY22, even as the economy was recovering, Capri launched two new products: Car Loans and Gold Loans. The timing seemed odd, but the logic was impeccable. The pandemic had created new financial behaviors. Families were liquidating gold to meet emergencies. First-time car buyers emerged as public transport became risky. Traditional lenders were still risk-averse, creating gaps that Capri could fill.

The gold loan business, launched with 108 exclusive branches in August 2022, became their most aggressive expansion ever. Within 18 months, they added 188 more branches, creating a network that rivaled established players like Muthoot and Manappuram in select geographies. But Capri's gold loan wasn't just another me-too product. They targeted a specific segment—small business owners who needed quick liquidity but didn't want to visit traditional gold loan companies due to social stigma.

The branches themselves were different—located in commercial areas rather than residential neighborhoods, designed to look like bank branches rather than pawnshops, staffed with relationship managers who understood business cycles rather than just gold valuation. The average ticket size was higher, the customer profile more sophisticated, and the use cases more diverse—working capital for businesses rather than just emergency personal needs.

The network expanded to 800+ branches across 12 States and Union Territories, but the real transformation was in operational capability. Each gold loan branch required specialized infrastructure—strong rooms, valuation equipment, trained appraisers, insurance arrangements. Building this while maintaining their core MSME and housing finance businesses required exceptional execution. They didn't just add products; they built parallel organizations within the company.

The car loan business took a different approach—asset-light and partnership-driven. Instead of competing with established auto financiers, Capri became a distribution partner, originating loans for banks and earning fee income. This required minimal capital deployment but leveraged their branch network and customer relationships. A small business owner walking in for an MSME loan might walk out with a car loan approval—processed by Capri but funded by a partner bank.

Digital transformation accelerated but remained pragmatic. The company launched WhatsApp-based customer service, mobile apps for loan applications, and digital payment collections. But they didn't abandon their physical-first approach. The co-lending business launched in FY24 used digital platforms to partner with banks, expanding to include gold loans in addition to MSME and home loans. This hybrid model—digital for efficiency, physical for trust—proved perfect for their customer base.

Perhaps the most unexpected move was acquiring UP Warriorz, a Women's Premier League cricket team. Critics called it a vanity project, a distraction from core business. But the strategic logic was subtle and powerful. Cricket gave Capri instant brand recognition in markets where financial services advertising struggled to cut through. Every UP Warriorz match was watched by millions of potential customers in Capri's core markets. The association with women's cricket aligned with their women entrepreneur loan programs. Marketing genius or expensive folly? Time will tell, but early indicators suggest the brand value impact exceeded traditional advertising ROI.

The COVID period also saw important strategic partnerships. Capri tied up with State Bank of India and Union Bank for co-lending, allowing them to originate loans that were largely funded by these banks. The 80-20 model (bank funds 80%, Capri funds 20%) dramatically improved capital efficiency. The firm estimated that ROE of around 25% would be generated through this arrangement—transforming their economics without increasing risk.

Technology infrastructure investments during this period focused on three areas: risk management systems using alternative data, customer service platforms enabling omnichannel engagement, and operational efficiency tools reducing turnaround times. They partnered with fintech companies for specific capabilities rather than trying to build everything in-house—a pragmatic approach that delivered results without massive technology spending.

By 2024, Capri had emerged from the pandemic stronger than ever. Revenue reached ₹3,534 Cr with profit of ₹578 Cr, but more importantly, they had proven their model's resilience. They had successfully added new products, expanded geographically, embraced digital tools, and even ventured into sports ownership—all while maintaining asset quality and customer trust. The company that had wandered for years had found not just its path but multiple highways to growth.

VII. Business Model Deep Dive

The genius of Capri Global's business model lies not in any single innovation but in the orchestration of multiple revenue streams, each reinforcing the others. Think of it as a financial services symphony where MSME loans provide the baseline, housing finance adds melody, gold loans bring rhythm, and fee income from distribution creates harmonics. The result is a business that's both diversified and integrated, resilient yet dynamic.

The firm's AUM composition reflects this diversity: MSME lending forms the core, complemented by Housing Finance, Construction Finance, and Indirect Retail Lending. Gold loans represent the newest addition, while car loan distribution generates fee income without balance sheet deployment. Each segment serves different customer needs, operates on different cycles, and provides different margin profiles—creating natural hedges against sector-specific downturns.

The MSME lending business, their largest segment, operates on a relationship model that's expensive to build but difficult to replicate. Average ticket sizes range from ₹5 lakhs to ₹50 lakhs, with tenures between 12 to 84 months. The interest rates, typically 14-18%, might seem high compared to bank rates, but they're transformational for customers previously paying 24-36% to informal lenders. The unit economics work because customer acquisition costs are amortized over multiple products and loan cycles—a customer acquired for a ₹10 lakh working capital loan might take a ₹30 lakh term loan two years later and a ₹50 lakh home loan after that.

Housing finance, operated through their subsidiary, targets a sweet spot ignored by both banks and large HFCs. These are ₹10-25 lakh loans to customers in tier-2 and tier-3 cities, often self-employed individuals with irregular income documentation. The superior asset quality of the Housing Finance segment provides an additional advantage—Capri earns better margins due to low-cost fund availability from NHB. The National Housing Bank refinancing, available at rates 200-300 basis points below market, creates a structural margin advantage that pure MSME lenders can't match.

Construction finance, their original business, has evolved into a sophisticated operation targeting small and medium real estate developers. These aren't the DLFs or Godrejs of the world but local developers building 20-50 unit projects in suburban markets. Loan sizes range from ₹5 crores to ₹50 crores, with interest rates of 13-16%. The key differentiator is speed—while banks take 3-6 months for approval, Capri can move in 3-4 weeks. This speed premium justifies the higher rates, especially when developers calculate the opportunity cost of delayed projects.

The gold loan segment, despite being newest, has been identified as high-margin with minor delinquency costs. Working with Boston Consulting Group and credit bureaus, Capri identified specific opportunities in North and Western India. Despite high operational expenses requiring extensive branch networks, they planned 1,500 branches to profitably reach their customer base. The average loan-to-value ratio of 75% provides a significant safety buffer, while the ability to liquidate collateral quickly reduces recovery risks.

But the real innovation in Capri's model is the co-lending arrangement. The 80-20 co-lending model with banks allows leverage up to 25 times and generates higher ROI. Here's how it works: Capri originates and services the loan but only funds 20% from their balance sheet. The partner bank funds 80% but relies on Capri's underwriting and collection capabilities. Capri earns fee income for origination and servicing plus interest margin on their 20% share. This transforms their capital efficiency—instead of deploying ₹100 to earn ₹15 in interest, they deploy ₹20 to earn ₹8 (₹3 interest plus ₹5 fees), improving ROE from 15% to 40% on that capital.

The indirect retail lending business adds another layer—providing wholesale funding to smaller NBFCs and microfinance institutions. This allows Capri to participate in segments like microfinance or consumer durables without building direct distribution. The margins are lower (2-3% spread) but the operational costs are minimal, and it provides portfolio diversification.

Risk management underpins everything. The low proportion of Gross Non-Performing Assets reveals superior underwriting, with collection efficiency around 98% for the last five quarters. This isn't achieved through aggressive recovery but through careful origination. Their "Five C" framework—Character, Capacity, Capital, Collateral, and Conditions—sounds conventional but the execution is nuanced. "Character" isn't just credit history but includes community standing, business relationships, and family involvement. "Capacity" looks beyond financial statements to actual business operations, customer relationships, and market position.

The funding mix has evolved from purely equity and term loans to a sophisticated structure including NCDs, bank borrowings, NHB refinancing, and co-lending arrangements. The average cost of funds has declined from 11% in 2015 to around 8.5% in 2024, even as the portfolio risk profile has improved. This is the virtuous cycle of NBFC maturation—better asset quality leads to better credit ratings, which reduces funding costs, which improves margins, which attracts more capital.

Fee income streams—from insurance distribution, co-lending origination, and car loan sourcing—now contribute 15% of total revenues but require minimal capital. This capital-light revenue stream improves overall ROE while providing cushion during interest rate cycles. The insurance distribution license allows them to earn commissions on life, general, and health insurance products sold to their loan customers—a natural cross-sell that requires minimal additional effort.

The technology stack, while not cutting-edge, is fit for purpose. Loan origination systems reduce turnaround time from 15 days to 3 days for standard products. Mobile apps allow field officers to capture documents and process applications remotely. Automated credit scoring handles 60% of renewal decisions without manual intervention. But human judgment remains central for new customer acquisition and large ticket loans—technology augments rather than replaces relationship management.

VIII. Financial Performance & Market Position

The numbers tell a story of exceptional execution in challenging times. 2024 revenue of ₹17.92 billion marked a 34.18% increase, while earnings of ₹4.79 billion represented a 71.27% surge. But raw growth numbers only scratch the surface. The real story lies in the improving unit economics, expanding margins, and strengthening market position that these numbers represent.

With a market cap hovering around ₹17,761-17,819 Crore, Capri trades at a P/E of 30.9 times and book value of ₹52.2. The valuations might seem rich compared to traditional NBFCs, but they reflect market recognition of several unique factors: the quality of their growth, the sustainability of their model, and the optionality embedded in their new initiatives. Compare this to established players like Bajaj Finance (P/E of 35-40x) or newer entrants like Poonawalla Fincorp (P/E of 45-50x), and Capri's valuations seem reasonable for its growth profile.

The return metrics reveal both strengths and areas for improvement. The current ROE of 11.8% appears modest, but this needs context. The three-year average ROE of 9.15% includes the pandemic period when the company prioritized stability over profitability. More importantly, the ROE is improving quarter by quarter as newer initiatives like gold loans and co-lending start contributing. Management's target of 18-20% ROE by FY26 seems achievable given current trajectories.

Asset quality metrics paint a picture of conservative growth. While gross NPAs have remained below 2%, the provision coverage ratio exceeds 70%, creating a buffer for potential stress. Net NPAs for Construction Finance and Housing Finance were actually negative, meaning provisions exceeded actual bad loans—a sign of conservative accounting rather than aggressive growth. The MSME portfolio, despite being perceived as risky, has shown remarkable resilience with NPAs below 2.5% even post-pandemic.

The margin story is particularly compelling. Net interest margins have expanded from 6.5% in FY20 to 8.2% in FY24, driven by three factors: declining cost of funds as credit ratings improved, better pricing power in underserved segments, and increasing contribution from high-margin products like gold loans. Operating expenses as a percentage of average assets have declined from 4.5% to 3.8%, showing operational leverage kicking in as the branch network matures.

Competitive positioning reveals Capri's unique niche. Unlike Bajaj Finance, which dominates consumer finance, or Cholamandalam, which focuses on vehicle finance, Capri has carved out leadership in the MSME plus affordable housing space. In their core markets of Rajasthan, Uttar Pradesh, and Gujarat, they're often among the top 3 NBFCs by presence and market share. In specific segments like small ticket construction finance or cluster-based MSME lending, they're often the market leader.

The funding profile has strengthened considerably. Credit ratings have improved from BBB+ to A+ over five years, reducing borrowing costs by 150-200 basis points. The debt-equity ratio of 4.5x is conservative by NBFC standards (peers operate at 6-8x), providing room for leverage expansion. More importantly, funding sources have diversified—from primarily term loans in 2015 to a mix including NCDs (30%), bank borrowings (40%), NHB refinancing (20%), and co-lending (10%) today.

Capital raising has been strategic rather than desperate. The recent ₹2,000 crore QIP wasn't about survival but growth acceleration. The ₹1,200 crore rights issue showed promoter confidence, with existing shareholders participating fully. LIC increasing its stake by 7% provided institutional validation. The capital adequacy ratio of 22% is well above regulatory requirements of 15%, providing a buffer for 30-40% AUM growth without additional capital raising.

Quarter-on-quarter performance shows remarkable consistency. Even during volatile periods like demonetization, IL&FS crisis, and COVID-19, Capri never reported a quarterly loss. Disbursements have grown for 16 consecutive quarters. The loan book has compounded at 35% annually over five years while maintaining asset quality. This consistency in execution has earned market credibility, reflected in the stock's outperformance—up 300% over three years versus the Nifty Financial Services index's 80% gain.

Recent analyst coverage has been increasingly positive. Most brokerages have buy ratings with target prices 15-20% above current levels. The bull case centers on underpenetrated markets, improving ROEs, and successful new initiatives. The bear case focuses on low interest coverage ratios, the recent 9.92% decrease in promoter holding, and potential asset quality stress in an economic downturn. On balance, the street sees more upside than downside, reflected in increasing institutional ownership.

The competitive moat is strengthening. While new fintech lenders can replicate their technology, they can't easily replicate Capri's 800+ branch network, deep local relationships, and detailed understanding of informal sector credit. While banks have the capital, they lack the risk appetite and operational flexibility to serve Capri's customer segments profitably. This positioning in the "middle space"—too complex for fintech, too risky for banks—creates a sustainable competitive advantage.

IX. The Playbook: Key Strategic Moves

Every successful company has a playbook—a set of strategic principles that guide decisions and create competitive advantage. Capri Global's playbook isn't written in any manual, but it's visible in every major decision they've made over the past decade. Understanding these principles helps explain not just what they did, but why it worked.

Principle 1: Serve the Underserved, Profitably The foundation of Capri's strategy is a seeming paradox—making money by serving customers others reject. This isn't corporate social responsibility masquerading as business; it's hard-nosed capitalism recognizing market failure. When banks demand 24 months of ITR filings, Capri asks for 6 months of bank statements. When others see a small contractor as risky, Capri sees a business with government contracts and steady cash flows. The key insight: underserved doesn't mean unprofitable; it means differently profitable.

Principle 2: Physical First, Digital Later In an era obsessed with digital disruption, Capri's insistence on physical branches seems anachronistic. But their logic is compelling: trust in financial services, especially in tier-2/3 markets, is built through presence, not apps. The branch manager who attends local business association meetings, who knows the family that runs the local textile mill, who can be reached when there's a problem—that's irreplaceable. Digital tools enhance this relationship; they don't replace it. The branch generates the customer; technology serves them efficiently.

Principle 3: Diversification Through Adjacent Expansion Capri never made random pivots. Each new product or market was adjacent to existing capabilities. Construction finance customers needed MSME loans for their suppliers. MSME borrowers eventually needed home loans. Gold loans served the same customers during emergencies. This adjacency strategy reduced execution risk while maximizing cross-sell opportunities. They weren't building multiple businesses; they were building one integrated financial services platform.

Principle 4: Patient Capital Deployment Unlike venture-funded NBFCs chasing growth at any cost, Capri has been remarkably patient. New branches take 12-18 months to break even. New products take 2-3 years to achieve scale. Market entry requires 6-12 months of preparation. This patience—enabled by patient promoter capital and supportive institutional investors—allows them to build sustainable advantages rather than chase quick wins. The gold loan business, for instance, required two years of planning before the first branch opened.

Principle 5: Risk Management Through Diversification Traditional risk management focuses on credit underwriting. Capri's approach is more holistic—diversify across products (MSME, housing, gold), geographies (12 states), customer segments (retail and wholesale), and funding sources (banks, NCDs, NHB). This diversification isn't just about reducing concentration risk; it's about creating multiple growth engines that can compensate for temporary weakness in any single area. When construction finance slowed during COVID, gold loans picked up the slack.

Principle 6: Leverage Partnerships, Don't Fight Them The co-lending model exemplifies this principle. Instead of competing with banks for funding, Capri partners with them. Banks get access to customers they can't serve directly; Capri gets cheap funding and fee income. The car loan distribution business follows similar logic—why compete with established auto financiers when you can earn fees distributing their products? This partnership approach multiplies their reach without multiplying their capital requirements.

Principle 7: Build Trust Through Transparency In an industry plagued by hidden charges and aggressive recovery practices, Capri differentiated through transparency. Loan terms are clearly explained. Processing fees are upfront. Recovery follows regulatory guidelines. This might reduce short-term profits but builds long-term relationships. The 98% collection efficiency isn't achieved through coercion but through customer selection and relationship management.

Principle 8: Invest Counter-Cyclically Capri's major expansions often came during industry stress. They raised capital in 2011 when NBFCs were struggling. They expanded branches during the IL&FS crisis when others were retrenching. They launched gold loans during COVID when the industry was defensive. This counter-cyclical approach allowed them to acquire talent, enter markets, and build capabilities at attractive costs. When the cycle turned, they were positioned to capture disproportionate gains.

Principle 9: Culture as Competitive Advantage The company culture, shaped by founder Rajesh Sharma's first-generation entrepreneur background, emphasizes empathy with customers who are themselves entrepreneurs. Loan officers are trained to understand business operations, not just financial statements. Performance metrics balance growth with quality. Incentive structures reward long-term relationship building over short-term disbursements. This cultural alignment ensures strategic consistency across 800+ branches.

Principle 10: Maintain Strategic Flexibility Despite clear principles, Capri has shown remarkable flexibility in execution. When co-lending opportunities emerged, they quickly pivoted to asset-light models. When gold loans showed promise, they rapidly scaled despite it being operationally different from their core business. This combination of strategic clarity and tactical flexibility allows them to capitalize on opportunities without losing focus.

The playbook's effectiveness is evident in the results. But more importantly, it's created a business model that's difficult to replicate. New entrants can copy products but not relationships. They can match interest rates but not local knowledge. They can build technology but not trust. This soft moat, built through consistent execution of these principles, might prove more durable than any regulatory license or capital advantage.

X. Bear vs Bull Case & Future Outlook

The investment community remains divided on Capri Global. Bulls see an undervalued compounder riding India's formalization wave. Bears worry about asset quality in a downturn and increasing competition. Both sides make compelling arguments, and understanding these perspectives is crucial for assessing Capri's future trajectory.

The Bull Case: Massive Runway in Underserved Markets

The optimists start with market size. India's MSME credit gap exceeds $400 billion. Affordable housing requires $1 trillion in financing over the next decade. Gold loan penetration is below 35% despite Indians holding 25,000 tonnes of gold. Even capturing 1% of these markets would triple Capri's AUM. The addressable market isn't just large; it's growing faster than GDP as formalization accelerates and credit penetration deepens.

Execution track record provides confidence. Management has successfully navigated multiple crises—IL&FS, COVID, demonetization—while maintaining growth and asset quality. They've launched new products successfully, entered new markets profitably, and scaled operations efficiently. The consistent positive performance has had significant positive effects on the bottom line. This isn't a company promising future execution; they've demonstrated it repeatedly.

The co-lending model could be transformational. If Capri can scale this to 30-40% of originations, ROEs could expand to 25%+ without additional risk. Banks need their origination capabilities; Capri needs their funding. It's a symbiotic relationship that could dramatically improve economics. Early results are promising, with multiple bank partnerships already operational.

Technology adoption, while gradual, is reducing costs and improving efficiency. Operating expenses have declined 70 basis points over two years even while expanding branches. As digital adoption increases among their customer base, further efficiency gains are likely. The company doesn't need to become a fintech; even modest technology leverage could expand margins significantly.

Regulatory tailwinds favor organized players. Recent RBI guidelines on microfinance, co-lending, and priority sector lending benefit companies like Capri. As regulatory oversight increases, informal lenders and weaker NBFCs will exit, leaving market share for stronger players. Capri's strong compliance record positions them to benefit from this consolidation.

The valuation remains reasonable despite recent gains. At 3.5x book value, Capri trades at a discount to high-quality NBFCs like Bajaj Finance (6x) or Poonawalla Fincorp (8x). As ROEs improve toward management's 18-20% target, valuations could re-rate higher. The market hasn't fully appreciated the transformation from a traditional NBFC to a diversified financial services platform.

The Bear Case: Multiple Headwinds Converging

Skeptics point to troubling indicators. The low interest coverage ratio suggests thin margins for error. In a rising rate environment, funding costs could spike faster than lending rates adjust, squeezing margins. The recent 200 basis point rate increase has already impacted margins; further tightening could be painful.

Promoter holding decreased 9.92% in the last quarter, raising questions about insider confidence. While this might be portfolio rebalancing or regulatory compliance, large promoter sales often signal caution. The timing—after a strong run-up—suggests profit booking rather than long-term conviction.

Competition is intensifying from multiple directions. Banks are becoming more aggressive in MSME lending as corporate credit demand weakens. Fintech lenders are moving downstream, offering instant loans to small businesses. Large NBFCs are entering tier-2/3 markets as tier-1 markets saturate. Capri's comfortable niche is becoming increasingly crowded.

Asset quality concerns loom large. The low average ROE of 9.15% over three years suggests structural challenges beyond pandemic impact. MSME lending is inherently volatile; the next economic downturn could reveal hidden weaknesses. The rapid expansion into gold loans and new markets increases operational risk. One bad monsoon, one economic shock, or one regulatory change could trigger widespread defaults.

The gold loan business faces specific challenges. Established players like Muthoot and Manappuram have decades of experience and operational advantages. Gold prices are volatile; a sharp correction could impact recovery values. Regulatory scrutiny on gold loans is increasing, with RBI expressing concerns about aggressive lending practices. Capri's late entry might mean they're picking up customers rejected by established players.

Execution risk in rapid expansion is significant. Managing 800+ branches requires exceptional operational capabilities. Each new product adds complexity. Technology integration remains a work in progress. Cultural dilution as the organization scales could impact the relationship-based model that's been their differentiator. History is littered with NBFCs that grew too fast and imploded.

The Balanced View: Cautious Optimism

Reality likely lies between these extremes. Capri has built a solid franchise in underserved markets with demonstrated execution capabilities. The business model is sound, the market opportunity is real, and management has proven competent. However, challenges are mounting—competition is increasing, margins are under pressure, and execution complexity is rising.

The next 24 months will be crucial. If Capri can successfully scale co-lending, establish gold loans profitably, and maintain asset quality through any economic turbulence, the bull case strengthens considerably. ROEs approaching 15-18% would justify premium valuations. However, any significant deterioration in asset quality, funding stress, or execution missteps could trigger a sharp correction.

For long-term investors, Capri represents a play on India's financial inclusion story with both significant upside and meaningful risks. The key monitorables are clear: asset quality trends, margin trajectory, co-lending scale, and competitive dynamics. The company has earned the benefit of doubt through past performance, but future success isn't guaranteed. As always in financial services, the difference between hero and zero is often just a few percentage points of bad loans.

XI. Key Lessons & Takeaways

After examining Capri Global's two-decade journey from a wandering financial advisory firm to a ₹17,800 crore NBFC powerhouse, several profound lessons emerge. These insights transcend the specifics of Indian financial services, offering wisdom for building businesses in regulated industries, serving underserved markets, and creating sustainable competitive advantages.

Lesson 1: Survival Precedes Success The most underappreciated phase of Capri's journey was the "lost decade" from 1994 to 2010. While seemingly unproductive, this period of survival created the foundation for everything that followed. In highly regulated industries with significant barriers to entry, simply maintaining licenses, preserving capital, and staying operational creates optionality. The company that renamed itself four times wasn't confused; it was adaptive. Sometimes the best strategy is patient persistence until the right opportunity emerges.

Lesson 2: Underserved Doesn't Mean Unprofitable Capri's core insight—that millions of creditworthy borrowers were being ignored by traditional lenders—seems obvious in hindsight but required courage to execute. The gap between the 36% charged by moneylenders and the 8% offered by banks to prime customers created a massive profitable middle ground. By charging 14-18%, Capri could be simultaneously cheaper than informal credit and more profitable than traditional banks. The lesson: market failures create opportunities for those willing to understand and serve neglected segments.

Lesson 3: Trust Scales Slowly but Compounds Powerfully In financial services, especially in markets with low financial literacy and high skepticism, trust is the ultimate moat. Capri's investment in physical branches, local hiring, and transparent practices seemed inefficient compared to digital-first models. But trust, once established, creates compounding advantages—lower acquisition costs, higher retention, better recovery rates, and powerful word-of-mouth marketing. The branch manager who attended a customer's daughter's wedding created more value than any algorithm could.

Lesson 4: Diversification and Focus Aren't Contradictory Capri managed to be both diversified (multiple products, geographies, customer segments) and focused (serving the underserved profitably). The key was expanding through adjacencies rather than random pivots. Each new product served existing customers' additional needs. Each new market applied proven playbooks. This "coherent diversification" reduced risk while maintaining operational synergies. The lesson: diversification works when it builds on existing capabilities rather than requiring entirely new ones.

Lesson 5: Capital Structure Is Strategy The evolution from equity-funded growth to co-lending partnerships demonstrates how capital structure innovations can transform business models. The 80-20 co-lending arrangement didn't just improve ROE; it aligned interests between banks and NBFCs, creating sustainable competitive advantage. Smart capital structure—not just having capital but structuring it optimally—can be as important as operational excellence.

Lesson 6: Timing Matters More Than Speed Capri's major moves—raising capital in 2011, launching gold loans in 2022, acquiring a cricket team in 2023—often seemed contrarian. But timing these initiatives when competitors were distracted, markets were dislocated, or opportunities were emerging proved more valuable than being first or fastest. The patient approach to market entry, product launches, and expansion created better outcomes than aggressive land-grabs would have.

Lesson 7: Culture Is Operating System, Not Window Dressing The first-generation entrepreneur culture instilled by founder Rajesh Sharma created empathy with customers who were themselves entrepreneurs. This wasn't just cultural nice-to-have; it translated into better underwriting (understanding business realities), better collections (working with customers through difficulties), and better product design (addressing actual pain points). Culture, when aligned with strategy, becomes a powerful execution enabler.

Lesson 8: Regulatory Arbitrage Is Temporary, Regulatory Alignment Is Permanent Rather than exploiting regulatory loopholes or operating in grey areas, Capri chose to be a model corporate citizen. This meant lower short-term profits but created long-term advantages—better credit ratings, regulatory support for new initiatives, and survival when regulations tightened. In regulated industries, working with regulators rather than around them creates sustainable competitive advantage.

Lesson 9: Technology Should Augment, Not Replace, Human Judgment In an era of AI-driven lending and automated underwriting, Capri's approach seems quaint. But their selective use of technology—digitizing processes while maintaining human decision-making for complex cases—proved optimal for their market. Technology reduced costs and improved efficiency, but relationship managers who understood local business dynamics made the credit decisions. The lesson: technology is a tool, not a strategy.

Lesson 10: Building in India Requires India-Specific Solutions Capri succeeded by recognizing that India isn't a monolithic market but thousands of micro-markets with unique characteristics. What worked in Moradabad's brass cluster wouldn't work in Panipat's textile hub. This hyperlocal approach—understanding specific industries, communities, and economic dynamics—created advantages that neither global best practices nor one-size-fits-all solutions could match.

The Meta-Lesson: Compound Advantages Perhaps the most important takeaway is how these elements compound. Trust enables customer acquisition, which generates data, which improves underwriting, which enhances profitability, which attracts capital, which funds expansion, which builds brand, which reinforces trust. This virtuous cycle, once established, becomes increasingly difficult for competitors to disrupt. Capri didn't build a business; they built a system where each component reinforces the others.

For investors, these lessons suggest looking beyond financial metrics to understand the underlying business system. For entrepreneurs, they demonstrate that serving underserved markets profitably requires more than just capital and good intentions—it requires patient building of capabilities, trust, and sustainable advantages. For policymakers, Capri's journey shows how financial inclusion can be achieved through market mechanisms rather than just subsidies or mandates.

The story of Capri Global Capital isn't finished. The next chapters—scaling co-lending, establishing gold loan leadership, navigating economic cycles—remain unwritten. But the lessons from their journey so far provide a masterclass in building financial services businesses in complex, regulated, emerging markets. Whether they ultimately succeed or stumble, the playbook they've developed deserves study and respect.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube