Caplin Point Laboratories: The Untold Story of India's Pharmaceutical Maverick

I. Introduction & Episode Roadmap

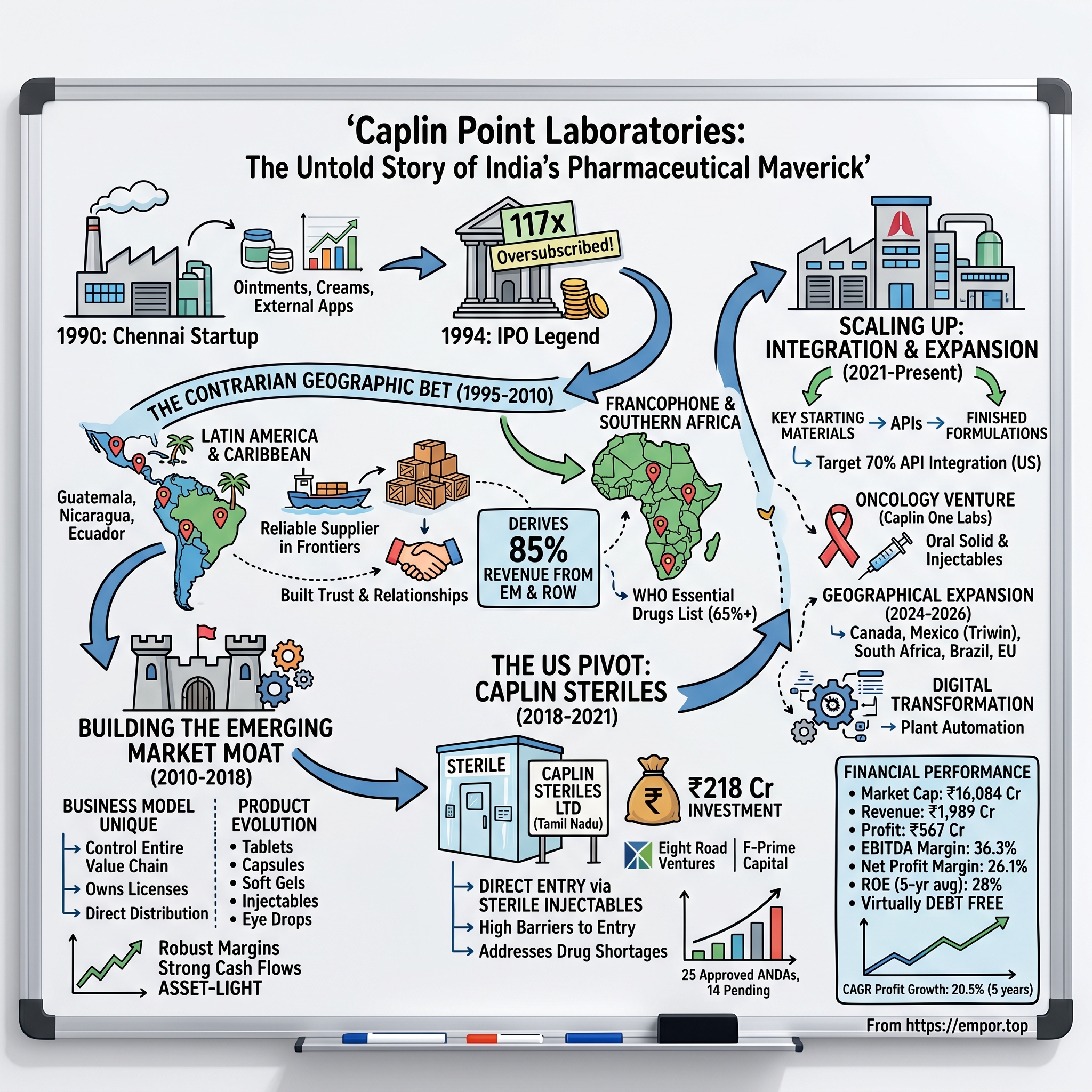

Picture this: It's 2010, and while every ambitious Indian pharmaceutical company is fighting tooth and nail for a slice of the lucrative US generics market, a Chennai-based company is quietly shipping containers full of medicines to Nicaragua, Guatemala, and the Ivory Coast. Their peers scoff—"Why waste time in these markets when the real money is in America?" Fast forward to 2024, and that same company, Caplin Point Laboratories, commands a ₹16,084 crore market capitalization, delivering 28% average return on equity over the past five years while maintaining virtually zero debt.

This is not your typical Indian pharma success story. Founded in 1990 as a modest manufacturer of ointments and creams, Caplin Point's journey defies every conventional playbook. When its 1994 IPO was oversubscribed 117 times—a phenomenon even by India's frothy IPO standards—few could have predicted that this topicals manufacturer would eventually become a pharmaceutical powerhouse dominating Latin American markets and pioneering injectable drugs for the United States.

The question that frames our entire exploration is deceptively simple: How did a small Chennai topicals manufacturer transform into a pharmaceutical force that controls significant market share across 23 countries, particularly in regions most Indian companies wouldn't dare to enter? The answer lies in a series of contrarian bets, each more audacious than the last—from choosing Latin America over the US in the 1990s, to building distribution networks in war-torn African nations, to eventually entering the US market through the backdoor of sterile injectables rather than the crowded oral solids space.

What unfolds is a masterclass in geographical arbitrage, regulatory navigation, and the art of building moats in markets others ignore. It's a story of how Caplin Point turned the pharmaceutical industry's conventional wisdom on its head, proving that sometimes the road less traveled isn't just different—it's devastatingly profitable.

Our journey will take us from the humid factory floors of Chennai in 1990 to the gleaming sterile facilities producing oncology drugs today. We'll explore how a company with 4,000+ registered licenses across 36 therapeutic areas built its empire not by following the herd to developed markets, but by becoming indispensable to healthcare systems in emerging economies. Along the way, we'll unpack the asset-light model that delivers 36% EBITDA margins, the backward integration strategy now encompassing 90+ molecules, and the calculated risks that transformed a regional player into a global contender.

Three themes will emerge repeatedly: First, the power of emerging market dominance when executed with operational excellence. Second, how an asset-light model combined with strategic vertical integration creates a unique competitive position. And third, the art of regulatory arbitrage—moving from semi-regulated to regulated markets with surgical precision.

This isn't just another pharmaceutical growth story. It's a blueprint for building a global business by zigging when everyone else zags, a testament to the power of patient capital allocation, and perhaps most importantly, a case study in how to build lasting competitive advantages in markets that Wall Street barely understands.

II. Origins: The Chennai Startup Story (1990–1994)

The year was 1990, and Chennai's pharmaceutical landscape was a battlefield of established players and ambitious upstarts. Into this arena stepped C.C. Paarthipan, an entrepreneur with a vision that seemed almost quaint by industry standards—he wanted to manufacture ointments, creams, and external applications. No blockbuster drugs, no complex molecules, just simple topical formulations that most pharma companies considered beneath their ambitions.

Paarthipan wasn't a typical pharma entrepreneur. While others obsessed over replicating Western blockbusters, he saw opportunity in the mundane—the everyday medicines that formed the backbone of primary healthcare. His initial factory in Chennai was modest, focusing on dermatological preparations and topical applications. The equipment was basic, the formulations straightforward, but the execution was meticulous. Every batch, every tube, every jar reflected an obsession with quality that would later become Caplin Point's calling card.

The early days were marked by a peculiar contradiction. Here was a company manufacturing the simplest of pharmaceutical products, yet Paarthipan was already thinking globally. While selling antifungal creams to local distributors, he was studying regulatory frameworks in Latin America. While perfecting ointment formulations, he was mapping healthcare systems in Francophone Africa. This wasn't hubris—it was calculated preparation for a game plan that wouldn't fully reveal itself for years. The 1994 IPO became the stuff of legend in Indian capital markets. When Caplin Point went public, the issue was oversubscribed 117 times—a staggering vote of confidence for a four-year-old company manufacturing basic pharmaceutical products. This wasn't the dot-com era with its irrational exuberance; this was 1994, when Indian investors were still learning to navigate post-liberalization markets. The overwhelming response spoke to something investors saw in Paarthipan's vision that perhaps even he hadn't fully articulated yet.

The IPO proceeds were immediately deployed to set up a manufacturing facility in Pondicherry, a strategic choice that would prove prescient. Pondicherry offered tax advantages, proximity to Chennai's port, and most importantly, the space to build a facility designed for future expansion rather than current needs. The new plant wasn't just about capacity—it was about capability. While the initial focus remained on topicals, the facility was designed with the flexibility to accommodate diverse dosage forms.

What made Caplin Point different in these formative years wasn't what they made but how they thought. While competitors rushed to copy Western blockbusters or flood the domestic market with me-too products, Paarthipan was methodically building something else entirely. He understood that in pharmaceuticals, distribution is destiny. You could have the best products, the lowest costs, the highest quality—but without reliable distribution, especially in emerging markets, you had nothing.

The product portfolio in these early years reads like a pharmacy's back shelf—antifungal creams, antibacterial ointments, wound healing gels. Nothing glamorous, nothing that would make headlines in pharmaceutical journals. But each product was chosen carefully, targeting high-volume, essential medicines that formed the foundation of primary healthcare. This wasn't about innovation; it was about execution. Every product had to meet international quality standards, even if it was destined for a small clinic in rural Tamil Nadu.

By 1994, Caplin Point had quietly assembled all the pieces for its next move. A state-of-the-art facility in Pondicherry, a growing portfolio of essential medicines, a war chest from the IPO, and most importantly, a leadership team that saw opportunity where others saw only risk. The Indian pharmaceutical market was booming, domestic consumption was rising, and any sensible company would have doubled down on the home market.

But Paarthipan wasn't interested in being sensible. While his peers fought over market share in Mumbai and Delhi, he was studying Spanish and Portuguese pharmaceutical regulations. While they invested in sales teams for Indian metros, he was mapping distribution networks in Central America. The Chennai startup phase was ending, but it had served its purpose—creating a launching pad for one of the most audacious geographical pivots in Indian pharmaceutical history.

III. The Contrarian Geographic Bet: Latin America & Africa (1995–2010)

The boardroom was skeptical. It was 1995, and C.C. Paarthipan had just proposed that Caplin Point essentially ignore the booming Indian market and the lucrative US opportunity to instead focus on Latin America and Africa. "You want us to ship medicines to Honduras? To Burkina Faso?" The questions weren't just skeptical—they were incredulous. At a time when every ambitious Indian pharma company was either consolidating domestically or preparing for US FDA inspections, Paarthipan was pointing at a map of markets most executives couldn't even pronounce correctly.

His logic was counterintuitive but compelling. The US generic market was already becoming a bloodbath of price competition, with established players like Ranbaxy and Dr. Reddy's spending millions on regulatory compliance and legal battles. Europe was even more complex, with its maze of country-specific regulations. But Latin America, the Caribbean, Francophone Africa, and Southern Africa? These were pharmaceutical frontiers—markets with massive unmet medical needs, minimal competition from multinational giants, and regulatory frameworks that, while challenging, were navigable for a nimble player.

The company focused on the emerging markets of Latin America, Caribbean, Francophone and Southern Africa, regions that presented a unique combination of opportunity and challenge. These weren't just developing markets; they were markets with geographical isolation, political instability, currency volatility, and infrastructure challenges that would make most pharmaceutical executives run in the opposite direction. For Paarthipan, these challenges weren't bugs—they were features. Every obstacle that deterred his competitors was a moat in the making.

The early forays were anything but smooth. Picture this: a Caplin Point business development manager landing in Guatemala City in 1996, armed with product samples and broken Spanish, trying to explain why a hospital should trust medicines from a company they'd never heard of, from a country better known for software than pharmaceuticals. The first shipments were tiny—a few thousand dollars worth of antibiotics here, some antifungals there. But each successful delivery built trust, each quality audit passed built credibility. The strategy was methodical and ruthless in its execution. Rather than competing on price in commoditized markets, Caplin Point focused on becoming the most reliable supplier in markets where reliability was scarce. In Nicaragua, where political upheavals could shut down supply chains overnight, Caplin maintained buffer stocks. In Ecuador, where currency devaluations could wipe out profits, they developed sophisticated hedging mechanisms. In West African nations where banking systems were primitive, they pioneered creative payment solutions.

Caplin Point derives 85% of its revenue from Latin America and Africa, a concentration that would terrify most risk committees. But this wasn't reckless concentration—it was calculated dominance. By 2010, the company had built 4,000+ registered licenses and 650 formulations across 36 therapeutic areas, with its product line including more than 65% of the drugs on the WHO essential drug list. This wasn't just a product portfolio; it was a comprehensive pharmaceutical armory designed to serve every level of the healthcare pyramid.

The "Bottom of the Pyramid" strategy was more than a business model—it was a philosophy. While multinational giants focused on expensive specialty drugs for urban hospitals, Caplin Point ensured that a clinic in rural Guatemala had the same quality antibiotics as a hospital in Guatemala City. They didn't just ship products; they built relationships. Local distributors weren't just customers; they were partners who understood that Caplin's success was their success.

Consider the product evolution during this period. The company expanded from its original topicals into tablets, capsules, injections, eye drops, oral liquids, soft gel capsules, ointments, creams, gels, injectable powders, suppositories, ovules, pre-mix bag formulations, inhalers, sprays, and IV infusions. Each addition was strategic—products chosen not for their complexity or profit margins, but for their essentiality in primary healthcare delivery.

The approach to distribution was revolutionary for an Indian pharmaceutical company. Instead of the typical model of appointing distributors and hoping for the best, Caplin Point invested in understanding each market's unique dynamics. They studied prescription patterns, mapped hospital procurement processes, understood tender mechanisms, and most importantly, built trust through consistent quality and reliable supply. In markets where a delayed shipment could mean the difference between life and death, Caplin Point became known as the company that always delivered.

One particular anecdote captures the essence of this period. In 2008, when a hurricane devastated Honduras, destroying much of the country's pharmaceutical supply chain, Caplin Point was among the first to restore supplies, airlifting essential medicines at their own cost. This wasn't charity—it was relationship building. When the market recovered, guess which company had preferential access to government tenders?

The financial discipline during this expansion was remarkable. Despite operating in markets known for payment delays and currency volatility, the company maintained positive cash flows. They learned to price in local currencies while hedging exposure, to maintain inventory buffers without tying up working capital, and most importantly, to grow without debt. This wasn't growth at any cost; it was profitable growth in the most challenging markets on earth.

By 2010, Caplin Point had achieved something extraordinary. The company had secured top positions in markets like Guatemala, El Salvador, Nicaragua, Ecuador, and Honduras. These weren't large markets by global standards, but Caplin Point wasn't trying to be a global giant. They were building an empire in markets others ignored, creating competitive moats through operational excellence rather than patent protection or regulatory barriers.

The lessons from this period would prove invaluable. First, that geographical diversification doesn't require entering every market—it requires dominating the markets you choose. Second, that in pharmaceuticals, distribution and reliability can be as powerful as innovation. And third, that the road less traveled isn't just less crowded—it can be incredibly profitable when navigated with skill and patience.

IV. Building the Emerging Market Moat (2010–2018)

The numbers told a story that Wall Street analysts struggled to comprehend. By 2015, Latin America and Rest of World accounted for 82-83% of Caplin Point's revenues, with the US contributing just 15-17%. In an era when every Indian pharmaceutical company's investor presentation led with their US pipeline, Caplin Point was doubling down on markets that most investors couldn't locate on a map. Yet the company was delivering returns that made their US-focused peers envious.

This wasn't stubborn adherence to a dated strategy—it was the systematic construction of an emerging market fortress. Caplin claimed top 3 spots amongst players in core markets, led by product launches, well-spread distribution networks and expanding into neighboring geographies. The company had evolved from being a supplier to becoming an integral part of the healthcare infrastructure in these regions.

The business model that emerged during this period was unique in the pharmaceutical industry. Rather than the typical approach of licensing products to local distributors, Caplin Point maintained control over the entire value chain. They owned the regulatory licenses, managed inventory at local warehouses, and in many cases, handled last-mile delivery to hospitals and pharmacies. This wasn't just vertical integration—it was geographical embedding.

After achieving strong success and creating their base over plain vanilla products like oral solids, capsules, powders, they were now going up the value chain and focusing on complex products like soft gels, injectables and ophthalmics. This product evolution wasn't driven by the desire to match competitors but by the specific needs of their markets. In regions where cold chain infrastructure was unreliable, they developed heat-stable formulations. Where injection administration was challenging, they created pre-filled syringes.

The approach to managing currency volatility and political instability became a masterclass in risk management. The company developed a natural hedge by maintaining costs in dollars (procurement from India and China) while earning in local currencies, with careful calibration of inventory levels to buffer against devaluations. As of Q2FY25, inventories stood at Rs 327 crore - 50% stock at warehouses close to customers, 20% in transit, and 30% in India. This wasn't just inventory management—it was strategic positioning.

During this period, Caplin Point also perfected what they called the "semi-regulated market advantage." These markets—not as stringent as the US FDA but not completely unregulated either—offered a sweet spot. The regulatory requirements were sufficient to keep out low-quality competitors but not so onerous as to make business unviable. The company became expert at navigating these regulatory frameworks, often being among the first to register new products.

The financial performance during this period validated the strategy. Despite operating in challenging markets, the company maintained robust margins and generated strong cash flows. The asset-light model, where significant manufacturing was outsourced while maintaining quality control, allowed for capital efficiency that would become crucial for their next phase of growth.

One critical innovation was their approach to market expansion. After strengthening smaller LatAm markets, Caplin focused on core LatAm markets like Brazil, Mexico, Colombia and Chile through distributors and tender-based contracts. This wasn't random expansion—it was methodical market adjacency. Success in Guatemala provided credibility in El Salvador. Dominance in Nicaragua opened doors in Honduras. Each market victory became a stepping stone to the next.

The company also pioneered what could be called "pharmaceutical micro-segmentation." In each market, they identified specific therapeutic areas where local competition was weak or multinational companies had withdrawn. They would then flood these segments with a comprehensive product range, making it uneconomical for competitors to challenge their position. A hospital that sourced its antibiotics from Caplin would find it convenient to source antifungals, analgesics, and vitamins from them as well.

The transformation of Caplin Point from a product supplier to a healthcare partner was complete by 2018. In many Central American countries, Caplin Point wasn't just another pharmaceutical company—they were the pharmaceutical company for essential medicines. Government health ministries knew them by name, hospital pharmacists trusted their quality implicitly, and importantly, patients—though they might never know the company's name—relied on their medicines for basic healthcare needs.

V. The US Pivot: Caplin Steriles & PE Investment (2018–2021)

The announcement caught the Indian pharmaceutical industry off guard. In 2018, when every generic company was struggling with US FDA warnings and price erosion in oral solids, Caplin Point declared they would enter the US market—not with tablets or capsules like everyone else, but with sterile injectables. It was like watching someone choose to climb Everest for their first mountain when everyone else was struggling with the local hills.

Caplin entered the US market directly through the injectables segment via its subsidiary Caplin Steriles Ltd with its manufacturing facility at Tamil Nadu. It attracted investments into Caplin Steriles to the tune of Rs. 218 crores from Eight Road Ventures and F-Prime Capital Partners, indicating a valuation of ~Rs. 817 crores for Caplin Steriles. This wasn't just capital raising—it was validation from two of the most sophisticated healthcare investors in the world.

The logic behind choosing injectables was counterintuitive but brilliant. While the oral solid generics market in the US was a race to the bottom with Indian companies undercutting each other, the sterile injectables market had significant barriers to entry. The technical complexity, stringent FDA requirements for sterile manufacturing, and high capital requirements kept competition limited. More importantly, the shortage of injectable drugs in the US had become a public health issue, creating both opportunity and purpose.

Building a sterile injectable facility from scratch is a pharmaceutical engineering marvel. Every surface must be pristine, every particle of air filtered, every drop of water purified to molecular perfection. The facility Caplin built wasn't just FDA-compliant—it was designed to exceed standards. Clean rooms with positive pressure gradients, automated filling lines to minimize human intervention, real-time environmental monitoring—this was pharmaceutical manufacturing at its most sophisticated.

The FDA approval journey for Caplin Steriles reads like a thriller. The first inspection, the observations, the responses, the remediation—each step fraught with risk. A single failed inspection could derail years of investment. But Caplin's experience in navigating complex regulatory environments in Latin America had prepared them well. They understood that regulatory compliance wasn't about meeting minimum standards—it was about building a culture of quality that permeated every aspect of operations.

What made the US strategy particularly clever was its integration with the Latin American business. The same products approved for the US could be registered in Brazil and Mexico, markets that often accepted US FDA approval as a gold standard. The ANVISA Brazil approval became a watershed moment, opening the largest Latin American pharmaceutical market to Caplin's injectable products.

By 2021, the numbers were validating the strategy. The company had 25 approved ANDAs with 14 pending and plans for 15 more filings. But these weren't random products—each was carefully selected based on market dynamics, competitive landscape, and Caplin's manufacturing capabilities. The focus was on products with limited competition, complex manufacturing requirements, or supply shortages.

Eight Road Ventures, the investment arm of Fidelity International Ltd, had vast experience and sizable investments in the healthcare sector (~50%). Their investment wasn't just about capital—it brought credibility, connections, and expertise. F-Prime Capital's involvement signaled to the US market that Caplin Steriles was a serious player, not just another Indian generic company trying to grab market share.

The PE investment also brought discipline and ambition. The company expected revenues for the US business to be $100M (~Rs 750 crores) over the next five years. This wasn't wishful thinking—it was a carefully constructed business plan based on approved products, pipeline visibility, and market dynamics.

The company targeted being backward integrated with own APIs for 70% of all US filings by 2024, a critical differentiator for generic injectables. This vertical integration strategy addressed one of the biggest risks in the injectable business—API supply security. By controlling their API supply, Caplin could ensure consistent quality, reliable supply, and better margins.

The transformation of Caplin Point during this period was remarkable. From a company that had built its reputation in emerging markets, it was now playing in the most sophisticated pharmaceutical market in the world. But unlike their peers who abandoned their core markets to chase US opportunities, Caplin maintained and strengthened their Latin American and African operations. The US wasn't a pivot away from emerging markets—it was an addition to an already strong portfolio.

VI. Scaling Up: Integration & Expansion (2021–Present)

The boardroom presentation in 2021 outlined an ambition that would have seemed fantastical just a decade earlier. Caplin earmarked Rs. 275-300 crores over 24-30 months for: an oncology facility for oral solid dosages and injectables, an API plant including US injectable API, OSD API and oncology API, and general category OSD/hormones/Penems plants for regulated & ROW markets. The company targeted complete backward integration from KSM to intermediates and API by 2024, meeting ~70% API requirements.

This wasn't just capacity expansion—it was a fundamental reimagining of what Caplin Point could become. The oncology venture through Caplin One Labs was particularly audacious. Oncology drugs represent the pinnacle of pharmaceutical complexity, requiring specialized facilities, handling protocols, and regulatory expertise. Yet by H1 FY25, the oncology business was already generating ₹12 crores in revenue, proving that Caplin could execute even in the most demanding therapeutic areas.

The geographical expansion strategy for 2024-2026 read like a pharmaceutical risk-taker's wishlist: entry into Canada, Mexico, South Africa, Brazil, and the EU. Each market represented different challenges—Canada's stringent regulatory requirements, Mexico's tender-based system, South Africa's unique disease burden, Brazil's complex approval process, and the EU's harmonized yet demanding standards. Yet Caplin approached each with the same methodical preparation that had served them in Latin America.

The acquisition of Triwin Pharma in Mexico deserves special attention. This wasn't just about buying a company—it was about acquiring a platform for government tenders and establishing a stock-and-sale model in one of Latin America's largest pharmaceutical markets. The acquisition provided immediate market access, local regulatory expertise, and most importantly, credibility with Mexican government procurement agencies. The R&D transformation has been particularly impressive. With an R&D team of 390 members working on backward integration for 90+ molecules, Caplin Point has evolved from a formulations company to a fully integrated pharmaceutical manufacturer. This isn't just about cost savings—it's about supply chain security, quality control, and the ability to respond quickly to market opportunities.

The backward integration strategy deserves deeper analysis. Starting from finished formulations, moving to APIs, then to intermediates, and finally to Key Starting Materials (KSMs)—each step represents increasing complexity and capital intensity. Yet Caplin has approached this systematically, focusing first on high-volume products where API availability was a constraint, then gradually expanding to more complex molecules.

The capacity expansion numbers tell their own story. Post-expansion capacities include: Liquid Vials: 105 million units; PreFilled Syringes: 18 million units; Pre-Mixed Bags: 11 million units; Lyophilised Vials: 15 million units. These aren't just production lines—they're platforms for entering new therapeutic areas and serving new markets.

The digital transformation initiative, though less visible, may prove equally important. Advancing plant automation to ensure compliance, particularly for regulated markets, represents the evolution from a manufacturing company to a technology-enabled pharmaceutical enterprise. In an industry where a single quality deviation can shut down a facility, automation isn't just efficiency—it's risk mitigation.

The oncology business via Caplin One Labs generating ₹12 Cr in H1 FY25 may seem modest compared to overall revenues, but it represents something far more significant—the ability to compete in the most sophisticated segment of the pharmaceutical market. Oncology drugs require specialized handling, complex manufacturing processes, and stringent quality controls. Success here validates Caplin's evolution from a basic generics manufacturer to a full-spectrum pharmaceutical company.

The partnership strategy for biologics and biosimilars with Chinese firms represents another calculated bet. Rather than attempting to build biosimilar capabilities from scratch—a multi-billion dollar endeavor—Caplin is leveraging partnerships to enter this high-growth segment. This capital-efficient approach to new market entry has become a Caplin signature.

What's remarkable about this expansion phase is its funding. Ongoing capital expenditures of ₹700+ Cr, funded via internal accruals, demonstrate the cash-generative nature of the core business. While peers leverage heavily for expansion, Caplin maintains its debt-free status, providing flexibility to pivot if market conditions change.

The integration of all these initiatives—backward integration, new market entry, capacity expansion, digital transformation—creates a flywheel effect. Each success provides resources and credibility for the next initiative. The company that once struggled to convince Latin American hospitals to buy its products now has the capability to manufacture everything from simple tablets to complex oncology injectables, from APIs to finished formulations, serving markets from Nicaragua to the United States.

VII. Financial Performance & Unit Economics

The numbers tell a story that defies conventional pharmaceutical economics. With a market cap of ₹16,084 crores, revenue of ₹1,989 crores, and profit of ₹567 crores, Caplin Point delivers profitability metrics that would make even specialty pharma companies envious. The 28.5% net profit margin isn't a one-time anomaly—it's the result of a business model engineered for capital efficiency from day one.

The company has delivered good profit growth of 20.5% CAGR over the last 5 years, but the consistency of this growth is what's truly remarkable. This isn't the volatile performance typical of companies dependent on product launches or patent cliffs—it's steady, predictable expansion driven by market share gains and operational excellence.

The H1 FY25 performance provides a window into the current momentum. Revenue growth of 17% YoY to ₹942 crores came with EBITDA margins at 36.3% and PAT margins at 26.1%. These aren't the margins of a commodity generics player—they're the margins of a company with significant competitive advantages. The ability to maintain such margins while growing at double digits challenges the typical trade-off between growth and profitability.

The company is almost debt free, a remarkable achievement for a capital-intensive pharmaceutical manufacturer. This isn't just financial conservatism—it's strategic flexibility. Without the burden of interest payments or debt covenants, Caplin can make long-term investment decisions that debt-laden competitors cannot afford.

The asset-light model deserves special attention. While maintaining manufacturing facilities in Tamil Nadu, Pondicherry, and Andhra Pradesh, the company outsources strategically, with 65% in-house manufacturing and 35% sourced from quality partners in India and China. This hybrid approach provides the quality control of owned facilities with the flexibility of outsourcing, optimizing capital deployment while maintaining product quality.

Working capital management has been transformed into a competitive advantage. With receivables at 118 days—reasonable for emerging markets—and strategic inventory positioning (50% at warehouses close to customers, 20% in transit, 30% in India), the company balances service levels with capital efficiency. The negative working capital in some quarters, achieved through favorable payment terms with suppliers, essentially means the business is funded by its supply chain.

The 5-year average ROE of 28% and ROCE of 32% place Caplin Point in the top tier of Indian pharmaceutical companies. These returns aren't achieved through financial engineering or aggressive accounting—they're the result of operational excellence and strategic positioning. When you dominate markets that others ignore, when you own the distribution that others outsource, when you backward integrate while maintaining capital discipline, these are the returns possible.

Free cash reserves of ₹1,039 crores and total liquid assets of ₹1,984 crores as of Q2FY25 provide both security and opportunity. This war chest enables the company to pursue acquisitions, fund capacity expansion, or weather any storms in their emerging markets—all without diluting shareholders or taking on debt.

Comparing Caplin Point's financials with Indian pharma peers reveals the uniqueness of their model:

| Metric | Caplin Point | Industry Average |

|---|---|---|

| EBITDA Margin | 36.3% | 18-22% |

| PAT Margin | 26.1% | 8-12% |

| ROE | 28% | 12-15% |

| ROCE | 32% | 15-18% |

| Debt/Equity | ~0 | 0.3-0.5 |

The geographic revenue composition—with Latin America and Rest of World contributing 82% and US contributing 18%—might concern investors focused on market risk. But this concentration is also the source of Caplin's superior economics. By dominating markets where they face limited competition, they achieve pricing power impossible in commoditized developed markets.

The evolution of US business economics is particularly interesting. Caplin Steriles' revenue composition demonstrates a balanced mix of product supply (75%) and milestone profit share (25%), providing both current cash flows and future upside. As the US business scales, it's approaching breakeven despite continued R&D investments, validating the injectable strategy.

What these numbers ultimately reveal is a business model that generates exceptional returns not through financial leverage or accounting gymnastics, but through operational excellence and strategic positioning. It's proof that in pharmaceuticals, as in many industries, where you compete can be more important than how you compete.

VIII. Playbook: Business & Investing Lessons

The Caplin Point story offers a masterclass in contrarian business strategy, but the lessons extend far beyond pharmaceuticals. This is ultimately a story about how to build competitive advantages in markets others ignore, how to scale without debt, and how to transform geographical disadvantage into strategic moat.

Geographic Arbitrage: The Art of Competing Where Others Won't

The decision to focus on Latin America and Africa wasn't just about avoiding competition—it was about recognizing that market attractiveness isn't always correlated with market size or GDP per capita. Caplin understood that in markets with underdeveloped healthcare infrastructure, being the reliable supplier of essential medicines created switching costs that no amount of price competition could overcome. When you're the only company that consistently delivers antibiotics to Honduras during the rainy season, you're not just a supplier—you're critical infrastructure.

Building Distribution as Competitive Advantage

While most pharmaceutical companies view distribution as a necessary cost, Caplin transformed it into their primary moat. By controlling the last mile in markets where logistics are challenging, they created barriers to entry that even larger competitors couldn't easily overcome. A multinational might have better products or lower costs, but without the relationships, local knowledge, and logistical capabilities Caplin built over decades, they couldn't effectively serve these markets.

The Power of Sequential Market Entry

Caplin's expansion wasn't random—it was methodical adjacency expansion. Success in Guatemala provided credibility for El Salvador. Dominance in Central America opened doors in South America. FDA approval in the US simplified entry into Brazil and Mexico. Each market victory wasn't just revenue—it was a credential for the next conquest. This sequential approach reduced risk while compounding advantages.

Managing Complexity Across 23+ Countries

Operating across multiple countries with different regulations, currencies, and business cultures requires organizational capabilities that can't be easily replicated. Caplin built systems to manage this complexity—from regulatory filing protocols that could be adapted across markets to financial hedging strategies that protected against currency volatility. This operational excellence in complexity management became a barrier to entry as formidable as any patent portfolio.

The Integration Paradox

Caplin's approach to vertical integration challenges conventional wisdom. They integrated backward (into APIs and intermediates) while maintaining an asset-light model through strategic outsourcing. They integrated forward (into distribution) while keeping capital requirements manageable. This selective integration—controlling what matters while outsourcing what doesn't—maximized returns while minimizing capital intensity.

Regulatory Strategy: The Semi-Regulated Sweet Spot

The progression from semi-regulated to regulated markets wasn't just growth strategy—it was risk management. By building capabilities in markets with moderate regulatory requirements, Caplin developed quality systems and compliance culture without the crushing costs of immediate FDA compliance. When they eventually entered the US market, they were prepared, having learned expensive lessons in cheaper markets.

Capital Allocation Without Debt

Perhaps the most remarkable aspect of Caplin's story is achieving all this growth while remaining virtually debt-free. This wasn't financial timidity—it was strategic discipline. By funding growth through cash flows rather than leverage, Caplin maintained flexibility to pivot when markets changed, to invest when opportunities arose, and to survive when crisis hit. In volatile emerging markets, this financial resilience became a competitive advantage.

The Emerging Market Pharmaceutical Playbook

For investors and entrepreneurs, Caplin Point offers a replicable playbook:

- Identify underserved markets with structural barriers to entry - not just regulatory or capital barriers, but operational complexity that deters competitors

- Build capabilities incrementally - start with simple products and basic markets, then systematically increase complexity

- Control critical points in the value chain - you don't need to own everything, just the parts that create competitive advantage

- Use success in one market as currency for the next - reputation and relationships compound

- Maintain financial discipline - in volatile markets, survival trumps growth

- Transform operational excellence into competitive moat - in markets where others struggle to operate, excellence becomes monopoly

The meta-lesson is that competitive advantage doesn't always come from innovation or scale—sometimes it comes from doing difficult things exceptionally well. Caplin Point didn't invent new drugs or discover new markets. They simply chose to excel where others chose not to compete.

IX. Analysis & Bear vs. Bull Case

The investment case for Caplin Point presents a fascinating study in risk-reward dynamics. Here's a company delivering software-like margins in a manufacturing business, dominating markets that most investors can't properly evaluate, all while preparing for a dramatic expansion into regulated markets. The bull and bear cases aren't just different—they're looking at entirely different companies.

Bull Case: The Emerging Market Pharmaceutical Monopoly

The optimists see Caplin Point as essentially owning a pharmaceutical monopoly across multiple emerging markets, with massive runway for growth as healthcare access expands in these regions. Latin America and Africa represent over 1.5 billion people with rapidly growing middle classes and increasing healthcare spending. Caplin's dominant position in these markets—built over three decades—creates switching costs and relationship moats that would take competitors decades to replicate.

The US injectable business is just beginning to show its potential. With 25 approved ANDAs and 14 pending, targeting markets with limited competition, the US could transform from 15% of revenues to 30-40% over the next five years while maintaining superior margins. The injectable focus avoids the commoditized oral solids bloodbath while addressing critical drug shortages—a combination of good business and good karma.

Backward integration is approaching an inflection point. Targeting being backward integrated with own APIs for 70% of all filings in US by 2024 creates cost advantages and supply security that few mid-sized players possess. This vertical integration, combined with the existing distribution network, creates an end-to-end pharmaceutical platform that's incredibly difficult to replicate.

The entry into new regulated markets—Canada, EU, Australia—leverages existing US approvals and manufacturing capabilities. These aren't speculative ventures but calculated expansions using proven products and established quality systems. Each new market adds diversification without proportional risk.

Financial strength provides optionality. With virtually no debt and substantial cash reserves, Caplin can pursue acquisitions, accelerate expansion, or weather any crisis. In a capital-intensive industry, this financial flexibility is a strategic weapon.

The valuation remains reasonable despite recent appreciation. Trading at a P/E that's in line with slower-growing domestic pharma companies, Caplin offers superior growth, higher margins, and better return ratios. As the US business scales and new markets contribute, multiple expansion seems probable.

Bear Case: The Concentration Conundrum

The pessimists focus on an uncomfortable truth: 85% of revenue from Latin America and Africa poses significant risk, as any economic downturn, regulatory changes, or geopolitical instability in these regions could significantly impact financial performance. This isn't diversification—it's concentration in the world's most volatile markets.

Currency volatility remains a persistent threat. While Caplin has managed this historically, a coordinated emerging market currency crisis—not uncommon in these regions—could devastate earnings despite operational excellence. The company's natural hedging only partially mitigates this risk.

Political and regulatory risks in core markets are real and unpredictable. A change in government in Guatemala, new pharmaceutical regulations in Nigeria, or social unrest in Ecuador—any of these could disrupt operations overnight. Unlike developed markets with stable regulatory frameworks, emerging markets can change rules retroactively.

Competition from Chinese and Indian peers is intensifying. As these markets become more attractive, larger players with deeper pockets are entering. Chinese companies, in particular, with their government backing and cost advantages, pose a significant threat to Caplin's market position.

The US injectable business, while promising, faces its own challenges. Any delays in approvals or launches in this highly competitive market may affect growth. Higher-than-expected erosion in the US market could lead to margin decline and profitability challenges. The injectable market, while less commoditized than oral solids, isn't immune to price competition.

Execution risk in new market entries is substantial. Entering Canada, EU, and other regulated markets requires different capabilities than emerging markets. Regulatory requirements are stricter, competition is more sophisticated, and customer expectations are higher. Success in Honduras doesn't guarantee success in Hamburg.

Supply chain vulnerabilities persist. Sourcing 35% of products from China and India means any supply disruptions from these countries, particularly due to geopolitical tensions or unforeseen events, could impact the company's overall growth and operational efficiency.

The Verdict: Asymmetric Risk-Reward

The investment case ultimately hinges on whether you believe Caplin Point's emerging market dominance is a sustainable competitive advantage or a risky concentration. The bulls see a company that has turned geographical disadvantage into a moat, building capabilities that would take competitors decades to replicate. The bears see exposure to volatile markets that could unravel quickly if conditions change.

The truth likely lies somewhere in between. Caplin Point has built something genuinely difficult to replicate—deep market presence in dozens of emerging markets, manufacturing capabilities spanning simple to complex products, and a financial profile that provides resilience. But the concentration risk is real, and the company's future depends on successfully diversifying into regulated markets while maintaining their emerging market fortress.

For investors, this presents an asymmetric opportunity. If Caplin executes their regulated market entry while maintaining emerging market dominance, the company could double or triple in value. If they stumble, the downside is cushioned by their debt-free balance sheet and cash generation. It's a bet on execution in an industry where execution is everything.

X. Epilogue & "What's Next"

As we sit in 2024, Caplin Point stands at an inflection point that will define its next decade. The company that built its fortune in the pharmaceutical backwaters of Latin America and Africa now has the capabilities, capital, and credibility to compete anywhere. The question isn't whether they can—it's whether they should, and more importantly, how they'll balance their emerging market heritage with regulated market ambitions.

The Biologics and Biosimilars Frontier

Partnering with Chinese firms for entry into the biologics/biosimilars segment represents perhaps the most ambitious pivot in Caplin's history. Biosimilars are to small molecule generics what smartphones are to rotary phones—exponentially more complex, requiring different capabilities, and offering different economics. Yet Caplin's approach—partnerships rather than ground-up development—shows the same capital discipline that has characterized their entire journey.

The biologics opportunity in emerging markets is particularly intriguing. While developed markets focus on cutting-edge monoclonal antibodies and gene therapies, emerging markets desperately need affordable versions of first-generation biologics—insulin, growth hormones, interferons. Caplin's distribution network and market knowledge position them perfectly to bring these life-saving biologics to markets where they're currently unaffordable.

The Oncology Opportunity: Serving the Underserved

The oncology venture isn't just about entering a high-margin therapeutic area—it's about addressing one of the greatest healthcare disparities in emerging markets. Cancer treatment in Latin America and Africa lags developed markets by decades, not because the disease is less prevalent, but because the drugs are unaffordable and unavailable.

Caplin's approach—starting with simple oral oncology drugs before moving to complex injectables—mirrors their original strategy. Build capabilities incrementally, establish trust with oncologists and hospitals, then expand the portfolio. The ₹12 crore revenue in H1 FY25 is just the beginning of what could become a significant franchise.

Digital Transformation: The Hidden Revolution

Advancing plant automation to ensure compliance, particularly for regulated markets understates the digital transformation underway. This isn't just about automation—it's about building a data-driven pharmaceutical company where every batch, every shipment, every customer interaction generates insights that improve operations.

Imagine predictive analytics that anticipate drug shortages in specific markets, AI-driven quality systems that prevent deviations before they occur, or blockchain-based supply chain tracking that ensures product authenticity. These aren't futuristic concepts—they're initiatives already underway, transforming Caplin from a traditional manufacturer into a technology-enabled pharmaceutical platform.

Can Caplin Become the "Sun Pharma of Emerging Markets"?

This comparison is both flattering and limiting. Sun Pharma built its empire through acquisitions and complex generics in developed markets. Caplin is building something different—a pharmaceutical company designed for the next billion patients, those in emerging markets who are just beginning to access modern healthcare.

The vision is more ambitious than replicating Sun Pharma's success. It's about creating a new model for pharmaceutical companies—one that prioritizes access over innovation, reliability over complexity, and sustainable growth over quarterly earnings. In a world where healthcare inequality is widening, Caplin's model of bringing quality medicines to underserved markets isn't just good business—it's necessary business.

Lessons for Indian Pharma Companies

Caplin Point's journey offers crucial lessons for Indian pharmaceutical companies caught in the US generics rat race:

- Market selection matters more than market size - A dominant position in Guatemala is worth more than a marginal position in Germany

- Distribution is destiny - In emerging markets, controlling distribution creates more value than developing products

- Patient capital wins - Building without debt provides flexibility that leveraged competitors lack

- Complexity is a moat - Operating successfully in difficult markets creates barriers competitors can't easily overcome

- Purpose drives performance - Serving underserved markets creates mission-driven organizations that outperform

Final Reflections on the Road Less Traveled

The Caplin Point story is ultimately about the courage to be different. In an industry obsessed with following the leader—everyone chasing the US market, everyone copying the same business model, everyone fighting for the same customers—Caplin chose a different path. They went where others wouldn't, served customers others ignored, and built capabilities others didn't value.

As we look forward, the question isn't whether Caplin's strategy was right—the results speak for themselves. The question is whether they can maintain their emerging market soul while embracing regulated market opportunities. Can they remain the company that airlifts medicines to hurricane-hit Honduras while also competing in the sterile halls of US hospitals?

The answer will determine whether Caplin Point becomes just another successful pharmaceutical company or something more significant—a new archetype for how pharmaceutical companies can create value by creating access, build moats by building relationships, and generate returns by generating impact.

The road less traveled has made all the difference. The question now is: what new roads will Caplin Point choose to travel, and who will have the courage to follow?

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube