Campus Activewear: India's Homegrown Sports Shoe Revolution

Introduction & Episode Roadmap

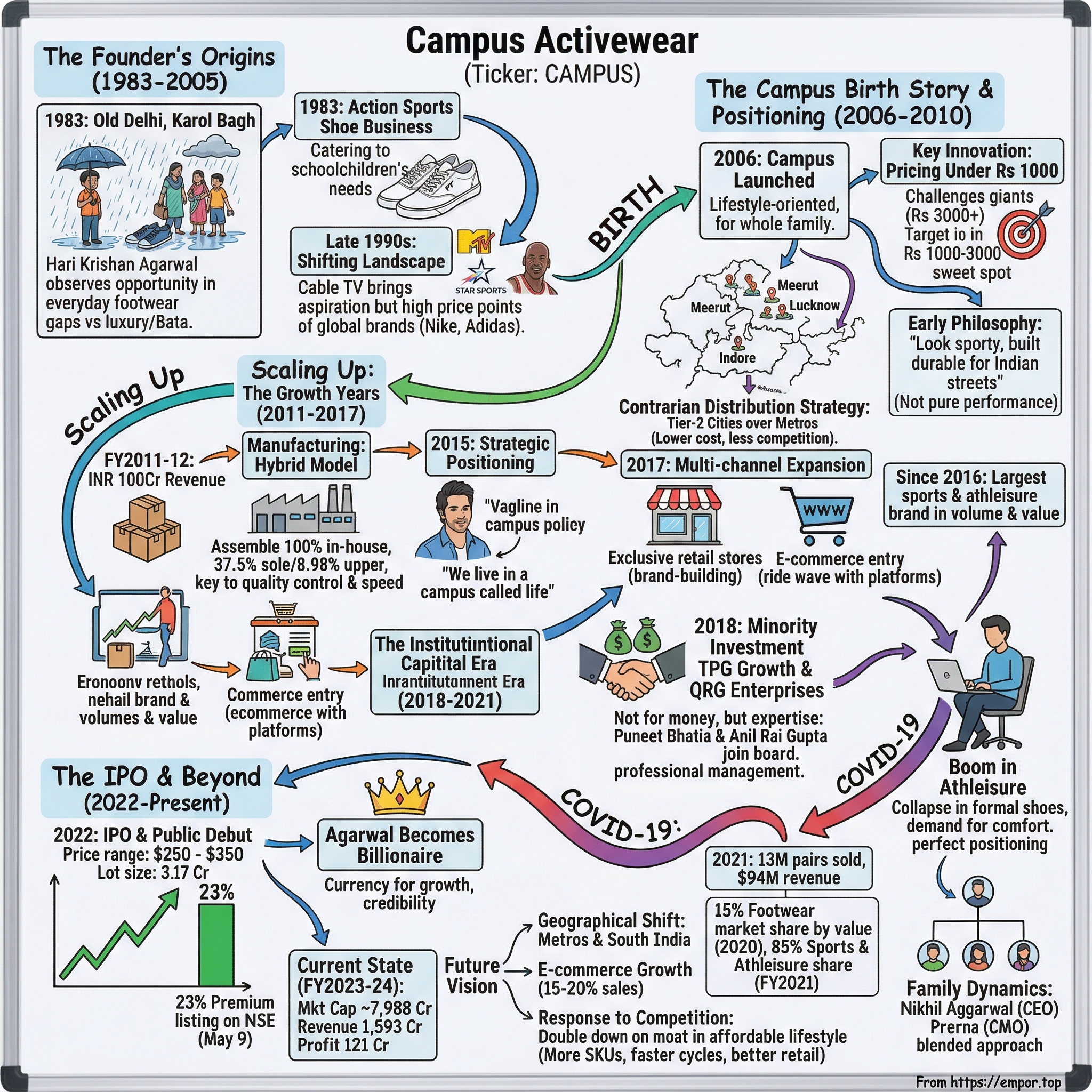

Picture this: A monsoon evening in Old Delhi's Karol Bagh market, 1983. The narrow lanes are packed with traders hawking everything from textiles to electronics. Among the chaos, a young entrepreneur named Hari Krishan Agarwal watches families navigate puddle-strewn streets, children clutching their parents' hands, their worn canvas shoes soaked through. He sees opportunity where others see only commerce—not in luxury, but in the everyday footwear needs of millions of Indians who couldn't afford Bata's premium lines, let alone dream of Nike or Adidas.

Four decades later, that observation has transformed into a company valued at around 1.5 Billion Dollars, with revenue of 1,593 Cr and profit of 121 Cr. Campus Activewear stands as the largest sports and athleisure brand in India, commanding 17% market share in the scaled sports and athleisure footwear market.

The question that drives our exploration today isn't just how a local Delhi shoe seller built a brand that competes with global giants. It's something more fundamental: In a market where international brands carried aspirational value and local meant compromise, how did Campus flip that script? How did they convince millions of Indians that homegrown could mean both affordable and desirable?

This is a story about timing market gaps with surgical precision, about family businesses navigating institutional capital, about choosing Tier-2 cities over metros when everyone else was doing the opposite. It's about understanding that in India, the real market isn't the top of the pyramid—it's the vast middle that international brands consistently overlook.

The Founder's Origins & Early Years (1983-2005)

Agarwal's entrepreneurial journey began in 1983 when he created the "Action" sports shoe business. But this wasn't some grand vision from day one. Agarwal was simply another trader in Delhi's sprawling unorganized footwear market, which in the 1980s operated more like a medieval bazaar than a modern industry. No brands, no marketing, just relationships and razor-thin margins.

The Indian footwear landscape of the 1980s was peculiar. Close to 75 per cent production came from the unorganised sector, which included micro, small, and medium enterprises (MSMEs). International brands were virtually absent. Bata ruled the organized sector with an iron grip, but even they focused on formal shoes and school footwear. Sports shoes? That was a luxury product, imported and unaffordable.

Action gained recognition, particularly among schoolchildren. This wasn't accident—it was insight. Agarwal noticed that parents bought sports shoes for their children not for sports, but as durable everyday footwear that could survive the punishment of Indian streets and playgrounds. The white canvas PT shoes that every Indian schoolchild wore? That was his market.

By the late 1990s, something fundamental was shifting. Cable television brought MTV and Star Sports into middle-class homes. Suddenly, Indian kids weren't just watching cricket—they were watching NBA, Premier League, extreme sports. They saw Michael Jordan in Nikes, David Beckham in Adidas. The aspiration was there, but the price points were galaxies apart.

Mr. HK Agarwal founded the "Action" brand in 1983, which became a household name in the casual and sports footwear segment in India. Inheriting the rich legacy of the brand and drawing on his deep insight pertaining to the Indian footwear industry, Mr. Agarwal curated the "Campus" brand in 1997.

The Action brand had given Agarwal something invaluable: four decades of experience in the footwear industry in India. He understood the supply chains, knew every component supplier from Agra to Ambur, had relationships with thousands of retailers. But more importantly, he understood Indian consumer psychology—the complex dance between aspiration and affordability, between wanting global and buying local.

The Campus Birth Story & Market Positioning (2006-2010)

It was launched in 2006 as a lifestyle-oriented sports and athleisure brand with an extensive product line for the whole family. The timing was deliberate. India's GDP was growing at 8-9% annually. The IT boom had created a new middle class with disposable income. Shopping malls were sprouting in Tier-2 cities. And crucially, international brands were still focusing on the top 10% of the market.

In 2006, he launched "Campus" athletic sneakers priced under Rs 1000, challenging global giants like Nike, Adidas, and Puma. Think about that price point for a moment. Nike's entry-level shoes were Rs 3,000-plus. Campus came in at one-third the price. But here's what's counterintuitive: they didn't position themselves as the "cheap alternative." The marketing spoke to aspiration, the designs mimicked global trends, the quality punched above its weight.

H K Agarwal took advantage of a significant gap in the Indian sports shoe market—in the price range of Rs 1000 to Rs 3000. This wasn't the bottom of the market—that was unbranded footwear selling for Rs 200-500. This wasn't the top either. This was the sweet spot: affordable for the aspiring middle class, but expensive enough to carry status.

The distribution strategy was pure contrarian genius. While Reebok and Adidas fought for prime real estate in Delhi's Select City Walk and Mumbai's Phoenix Mills, Campus went to Meerut, Lucknow, Indore, Nagpur. Agarwal founded Campus with smaller cities as its primary markets. The logic was beautiful: lower rental costs, less competition, and customers who were even more value-conscious than metro consumers.

The early product philosophy revealed deep market understanding. Campus didn't try to make performance sports shoes—Indians weren't actually playing that much sport. They made shoes that looked sporty but were built for walking to work, standing in buses, navigating broken footpaths. The cushioning was designed not for basketball courts but for concrete streets. The materials chosen not for breathability during exercise but for durability during monsoons.

By 2010, Campus had quietly built something remarkable: a brand that small-town India actually preferred over international names they couldn't afford anyway. The company was profitable from Day 1, growing organically without external capital, reinvesting everything back into the business.

Scaling Up: The Growth Years (2011-2017)

The company reached the INR 100 crore revenue milestone in the fiscal year 2011-2012. In the FMCG world, 100 crores is pocket change. In footwear, with average selling prices under Rs 800, it meant moving serious volume—over 15 lakh pairs annually.

The manufacturing strategy during this period deserves attention. Unlike apparel, footwear manufacturing is technically complex—it requires molds, lasts, specialized machinery. Most Indian brands simply imported from China or outsourced to clusters in Agra and Chennai. Campus took a hybrid approach: Through its manufacturing facilities, the company can manufacture 37.5% of its requirement of soles and 8.98% of shoe uppers in-house while it assembles 100% of its products in-house.

This gave them quality control without massive capital expenditure. They could respond to market trends in weeks, not months. When neon colors suddenly became popular in 2013, Campus had them in stores before international brands had even placed orders with their Asian suppliers.

Improving its marketing game in 2015, the company hired Varun Dhawan as its brand ambassador. This wasn't just celebrity endorsement—it was strategic positioning. Dhawan represented the young, urban Indian who was confident in his choices, who didn't need foreign validation. The tagline evolved: "We live in a campus called life."

In 2017, the company opened 16 exclusive retail stores and entered the E-commerce industry. The exclusive stores served a different purpose than sales—they were brand-building exercises, letting Campus control the narrative, display the full range, create an experience that multi-brand outlets couldn't.

The e-commerce entry timing was perfect. Flipkart and Amazon were in a cash-burning customer acquisition phase, subsidizing logistics, offering deep discounts. Campus rode this wave without bearing the costs. Online sales also gave them data—which styles sold in which cities, what price points worked, how customers searched for shoes.

Since 2016, the flagship brand "Campus", has been the largest sports and athleisure footwear brand in India, in both volume and value terms. Think about that achievement: beating Reebok, Puma, Fila—brands with decades of global heritage—in their own category, in volume AND value.

The family dynamics during this growth phase were fascinating. His son, Nikhil Aggarwal is the CEO of the company. His daughter-in-law, Prerna, is the chief marketing officer of Campus Activewear. Agarwal's wife was on the company's board until September 2021, where used to drive supply chain efforts and a fabricator network. Unlike many family businesses where second generation means conflict, here it meant complementary skills.

The Institutional Capital Era (2018-2021)

TPG Growth, the middle market and growth equity platform of alternative asset firm TPG, and QRG Enterprises Limited, the family office of the promoters of Havells Group, have made an undisclosed minority investment in Campus Activewear. The 2018 investment wasn't about needing money—Campus was highly profitable. It was about what came next.

TPG brought more than capital. Puneet Bhatia, partner and country head of India for TPG and Anil Rai Gupta, from Havells Group, will join the company's board. Gupta's experience was particularly valuable—he'd built Havells from an industrial brand into a consumer powerhouse. He understood the journey Campus was embarking on.

The institutionalization process was delicate. TPG pushed for professional management, better systems, governance structures. But they were smart enough not to disrupt what worked. The family retained operational control. Nikhil Aggarwal, who holds a degree in industrial engineering from Purdue University, serves as the CEO of Campus Activewear. Nikhil's leadership has brought a fresh perspective to the company, blending modern technological approaches with the traditional business values.

COVID-19 should have been a disaster. Footwear sales collapsed in Q1 2020. Retailers cancelled orders. But something unexpected happened: the work-from-home economy created an athleisure boom. People weren't buying formal shoes, but they were buying comfortable, casual footwear for their limited outings. Campus's positioning at the casual-sports intersection was suddenly perfect.

Selling 13 million pairs and generating $94 million in revenue in 2021. The company also used the pandemic to clean up operations—inventory management, supply chain digitization, direct-to-consumer capabilities. They emerged stronger.

Achieving a 15% market share in the footwear industry by value in 2020. Dominating the sports and athleisure market with over 85% share by the financial year 2021. These numbers need context: in a market with Nike, Adidas, Puma, Reebok, Skechers, plus Indian brands like Relaxo and Liberty, Campus had become the default choice for value-conscious consumers.

The IPO Story & Public Market Debut (2022)

IPO date 26th – 28th Apr 2022, Listing date 09 May 2022, Price range ₹278 – ₹292, Lot size 51 — ₹14892. The timing seemed awful. Global markets were correcting post-COVID excesses. The Russia-Ukraine war had started. Tech IPOs were failing globally.

But Agarwal understood something others missed: Indian retail investors were hungry for consumption stories they could understand. Campus wasn't some complicated SaaS business or loss-making unicorn. It was shoes. Everyone understood shoes.

Initial public offering of 47,950,000 equity shares of face value of Rs. 5 each of Campus Activewear Limited for cash at a price of Rs. 292 per equity share (including a premium of Rs. 287 per equity share) aggregating to Rs. 1399.60 crores.

The IPO was entirely an Offer for Sale—no fresh capital raise. This sent a signal: Campus didn't need money, they were giving investors a chance to participate in a proven business model. The selling shareholders were taking partial exits, not full ones, showing continued confidence.

Campus Activewear made its stock market debut on May 9, 2022, with its shares listing at ₹360 per share on the NSE, around a 23% premium over its issue price of ₹292. During the trading session, the stock surged to ₹418 despite global issues and a bearish trend in the broader market.

Agarwal became a billionaire when Campus shoes' stock was floated in 2022 at a 23% premium to the IPO price. But this wasn't about personal wealth. The listing gave Campus currency for acquisitions, stock options for talent retention, and most importantly, the credibility that comes with public market scrutiny.

Post-IPO, the shareholding structure was telling. Promoter Holding: 72.1%—the family retained firm control. TPG made a partial exit but retained a stake. The public float was enough for liquidity but not so much that the company became vulnerable to hostile takeovers.

Business Model & Competitive Advantages

Let's dissect why Campus works where others fail. Campus Activewear has five factories across India, strategically located to balance labor costs, logistics, and raw material access. But it's not just about owning factories.

The manufacturing philosophy is nuanced. Approximately 85% of the company's raw materials are sourced locally in India. The remainder of the raw materials is sourced from China, South Korea, and other South-East Asian countries. This balance gives them cost advantages while maintaining quality and reducing forex risk.

The capacity utilization story is impressive: starting with 28.8 million pairs annual capacity with ability to scale to 35.5 million without major capex. They're not building for today's demand but tomorrow's opportunity.

The company has a pan-India presence with a network of over 425 distributors in 28 states and 664 cities. But here's the clever part: Campus doesn't just distribute; they finance. They extend credit to distributors, who extend credit to retailers. In India's relationship-driven market, this creates stickiness that no amount of advertising can buy.

The product portfolio strategy reveals sophisticated thinking. The company manufactures and distributes a variety of footwear like Running Shoes, Walking Shoes, Casual Shoes, Floaters, Slippers, Flip Flops, and Sandals. They're not trying to be Nike in performance sports. They're being everything in affordable lifestyle footwear.

Price architecture is their moat. With ASPs (Average Selling Prices) around Rs 620-650, they're 70% cheaper than international brands but 50% more expensive than unbranded products. This positioning is nearly impossible for others to attack—go lower, and you can't maintain quality; go higher, and you lose the value proposition.

The Current State & Future Vision (2023-Present)

Mkt Cap: 7,988 Crore, Revenue: 1,593 Cr, Profit: 121 Cr. The market cap multiple of 66x earnings might seem expensive, but consider the growth trajectory and market opportunity.

From just INR 100 crore in revenue back in FY 2011-12, we have soared to INR 1,448 crore in FY 2023-24. That's a 14x growth in 12 years—a CAGR of nearly 25%. More importantly, this growth came with profitability, not the burn-now-profit-later model of new-age companies.

The geographical expansion strategy is shifting. Having dominated Tier-2/3 cities, Campus is now attacking metros and South India—traditionally weak markets. But they're not changing their positioning. Instead, they're betting that metro consumers are becoming more value-conscious post-COVID.

E-commerce now contributes 15-20% of sales, growing at 40% annually. But Campus isn't dependent on it. They use online as a marketing channel as much as a sales channel—product discovery happens online even if purchase happens offline.

Competition is intensifying from unexpected quarters. Direct-to-consumer brands like Solethreads and Yoho are attacking from below with online-only models. International brands are launching sub-brands for the Indian market. Chinese players are dumping products at impossible prices.

Campus's response? Double down on what works. They're not trying to go premium or performance. They're deepening the moat in affordable lifestyle footwear. More SKUs, faster fashion cycles, better retail experience, but same price-value equation.

With a B.Sc. degree in Industrial Engineering from Purdue University, Nikhil is effectively channelizing his skills and knowledge to help Campus achieve its objectives. In 2007, he attended the Summer School Programme at the London School of Economics. The second generation isn't just inheriting; they're reimagining. Digital transformation, sustainability initiatives, international expansion—all while maintaining the core DNA.

Playbook: Lessons & Investment Insights

What can we extract from Campus's journey that's applicable beyond footwear, beyond India even?

First, the power of unglamorous markets. While everyone chased the top of the pyramid, Campus built a fortress in the middle. The middle market is harder—lower margins, more price sensitivity, need for scale. But once you win, the moat is deeper because competitors find it hard to come down-market.

Second, timing market transitions. Campus didn't create the athleisure trend or the aspiring middle class. They recognized these shifts early and positioned accordingly. They were ready when the market turned their way.

Third, the hybrid model advantage. Not fully integrated like Bata, not fully outsourced like most brands. This balance gave them flexibility and control without massive capital requirements.

Fourth, family businesses can professionalize without losing soul. The Agarwal family brought in institutional capital, professional management, and modern systems while retaining what made them successful—entrepreneurial speed, relationship focus, and long-term thinking.

Fifth, IPO as strategic tool, not exit. The public listing wasn't about cashing out but about currency for growth, credibility for partnerships, and discipline from market scrutiny.

Capital allocation lessons: Campus never raised equity capital until they were already successful. They grew organically, reinvested profits, and only brought in external capital for strategic value, not operational needs. Post-IPO, they're not splurging on acquisitions or vanity projects but continuing measured expansion.

Bear vs Bull Case Analysis

The Bull Case:

The India opportunity is massive. Footwear per capita consumption in India is 1.7 pairs versus 7+ in developed markets. As income rises, this gap will close. Campus is perfectly positioned to capture this growth.

The brand has achieved something rare—moving from functional to aspirational while maintaining affordability. Young India doesn't see Campus as compromise anymore; they see it as smart choice.

Manufacturing and distribution advantages create real moats. The India footwear industry is dominated by key players like Bata India, Relaxo Footwears, Metro Brands, Campus Activewear, and Liberty Shoes, and Campus has emerged as a leader through execution, not just strategy.

The athleisure megatrend has decades to run. Casual Friday became casual everyday. Sports shoes aren't for sports anymore—they're daily wear. Campus owns this intersection.

The Bear Case:

Competition is intensifying from every direction. D2C brands are gaining traction with younger consumers. Chinese imports are destroying price points. International brands are finally taking the mass market seriously.

Margin pressure is real. Raw material costs are volatile. Retail rentals are rising. E-commerce means constant discounting. The sweet spot of pricing power Campus enjoyed might be narrowing.

Fashion risk cannot be ignored. Footwear is becoming like apparel—trend-driven, fast-changing. Campus's product development cycle might be too slow for Instagram-speed fashion.

Geographic concentration remains concerning. Despite expansion efforts, North and Central India still drive majority revenues. Success in South India and metros isn't guaranteed.

The promoter dependence question: What happens post-Agarwal? Yes, Nikhil is capable, but founder transitions are always risky in family businesses.

Epilogue & Reflections

Step back and consider what Campus really represents. This isn't just another business success story. It's a template for how Indian companies can win in categories dominated by global giants.

The conventional wisdom was that Indian consumers would eventually "graduate" to international brands as incomes rose. Campus proved that with the right product-market fit, Indian brands could be the destination, not the stepping stone.

The story challenges our assumptions about value chains. Campus didn't innovate in technology like Nike's Air cushioning or Adidas's Boost foam. They innovated in business model—finding the exact intersection of price, quality, and aspiration that resonated with Indian consumers.

What's most counterintuitive is how Campus won by not trying to be global. While Titan tried to take watches worldwide and Café Coffee Day dreamed of challenging Starbucks internationally, Campus focused relentlessly on India. Sometimes the biggest opportunity is in your backyard.

The family business angle deserves reflection. In an era where professional management is gospel, Campus shows that family ownership—when combined with professional discipline—can be a competitive advantage. The long-term orientation, the patience to build slowly, the ability to make quick decisions—these are features, not bugs.

Looking forward, Campus faces an interesting inflection point. Do they stay focused on India or chase international markets? Do they move upmarket as their consumers become affluent or stay true to affordable positioning? Do they expand into adjacent categories like apparel or remain footwear specialists?

What would different strategic choices have meant?

If Campus had raised venture capital early, they might have grown faster but lost control. If they'd positioned as premium from the start, they might have better margins but smaller market. If they'd gone international early, they might have lost focus on India.

The path not taken is always unknowable. But the path Campus chose—patient, profitable, purposeful—created something remarkable: an Indian brand that doesn't apologize for being Indian, doesn't aspire to be global, and doesn't need foreign validation to succeed.

In the end, Campus Activewear's story is really about understanding your customer better than they understand themselves. Hari Krishan Agarwal saw that Indians didn't actually want cheap shoes—they wanted affordable dignity. They didn't need performance technology—they needed everyday reliability. They didn't require global brands—they wanted brands that understood their reality.

That insight, executed over four decades with discipline and focus, built a billion-dollar business. It's a reminder that in business, like in life, the biggest opportunities often hide in plain sight. You just need to look at them differently.

The Campus story isn't finished. With India's demographic dividend playing out, urbanization accelerating, and lifestyle changes permanent post-COVID, the next decade could be even more transformative than the last four. Whether Campus can maintain its edge while scaling further, whether the second generation can build on the founder's legacy, whether the public market's quarterly pressures conflict with long-term building—these questions remain open.

But one thing is certain: Campus has earned its place in India's corporate history as the company that proved you don't need to be Nike to win in sports shoes. You just need to be yourself, executed brilliantly.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube