SignatureGlobal: The Affordable Housing Revolution in India's Capital

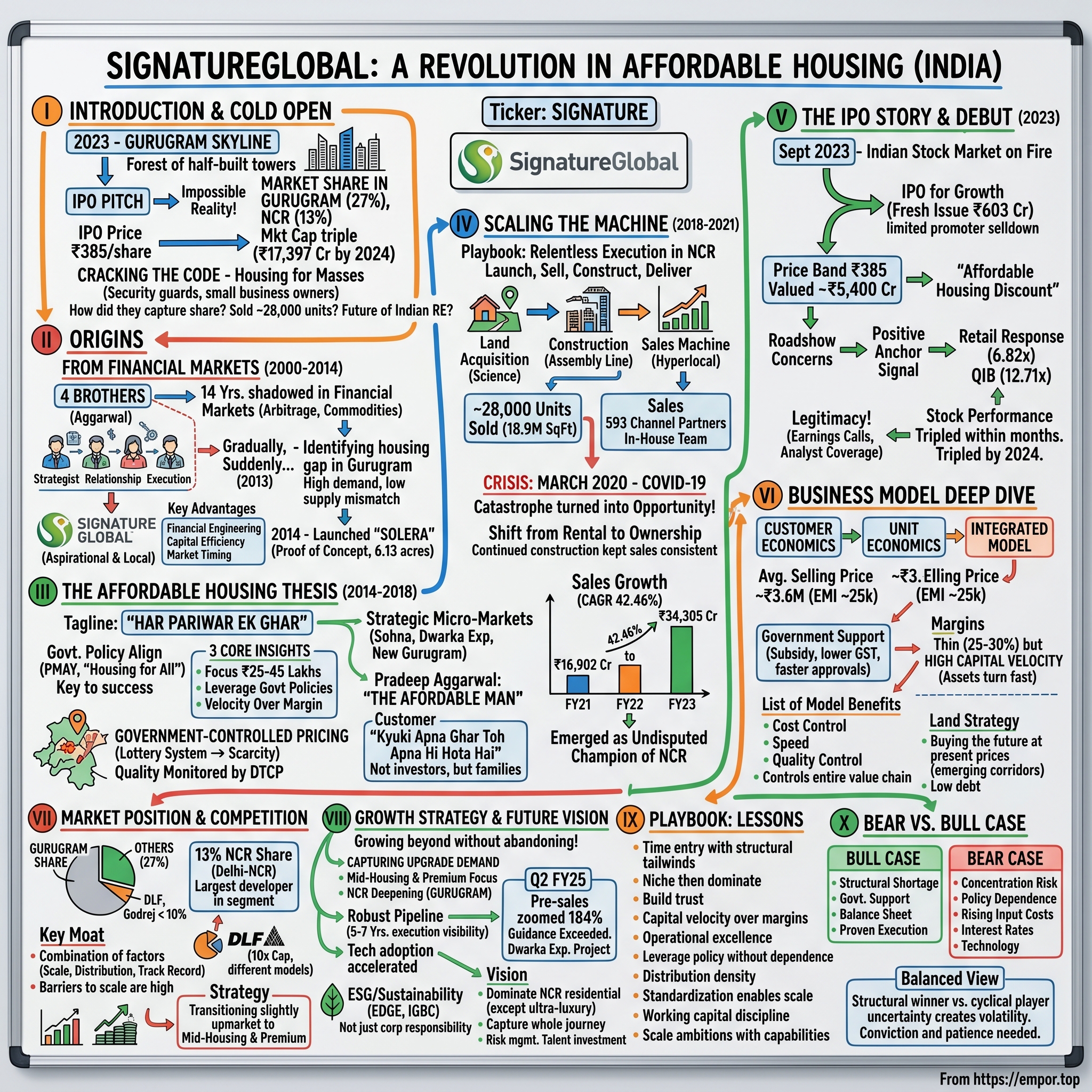

I. Introduction & Cold Open

The year is 2023. In a gleaming conference room overlooking Gurugram's skyline—a forest of half-built towers and construction cranes—investment bankers are pitching what seems impossible: a real estate company with 27% market share in India's most competitive property market. Not DLF, not Godrej, not Sobha. A company most people outside Delhi NCR have never heard of: SignatureGlobal.

The numbers defy logic. In Gurugram's affordable housing segment, they control nearly one in three sales. Across the entire National Capital Region, their market share hits 13%. The IPO prospectus reveals something even more remarkable: they've sold 27,965 residential and commercial units—all within a single geographic market. Every. Single. One. When the bankers arrive at the IPO price—₹385 per share—the math seems conservative. Market cap at listing: ₹5,409.66 crores. Within months, that number would triple. By 2024, SignatureGlobal's market cap would reach ₹17,397 crores, making early investors look prescient and late arrivals wonder what they missed.

But the real story isn't the stock price multiplication. It's how four brothers from a financial services background cracked the code to India's most intractable problem: housing for the masses. While giants like DLF built glass towers for multinationals and Godrej crafted luxury apartments for India's elite, SignatureGlobal went the opposite direction. They built homes for families earning ₹6-8 lakhs annually—the security guards, junior executives, and small business owners who form the backbone of India's economic miracle.

The central question that drives our story today: How did a company that didn't exist in real estate until 2014 capture 27% market share in Gurugram and 13% market share in NCR in less than a decade? How did they sell nearly 28,000 units when established players struggled to move inventory? And perhaps most importantly—what does SignatureGlobal's rise tell us about the future of Indian real estate?

This is the story of SignatureGlobal—a company that turned government policy into profit, transformed affordable housing from charity to capitalism, and built an empire one ₹35-lakh apartment at a time. It's about timing, execution, and the radical idea that you could build a premium business by serving India's non-premium customers.

Let's begin where all great business stories begin: with founders who saw opportunity where others saw only obstacles.

II. Origins: From Financial Markets to Real Estate (2000-2014)

March 28, 2000. The dot-com bubble is about to burst. Y2K fears have just subsided. In this moment of global financial uncertainty, four brothers—Pradeep Kumar Aggarwal, Lalit Kumar Aggarwal, Ravi Aggarwal, and Devender Aggarwal—register a company that would spend its first fourteen years doing everything except what would eventually make it famous.

Pradeep Aggarwal brought two decades of experience in financial capital markets and commodity markets, with deep knowledge of securities markets and financial services that would later lead him to diversify the arbitrage business. Think of him as the strategist—the one who could read market cycles and spot arbitrage opportunities others missed. His brothers complemented him: Lalit with operational excellence, Ravi with relationship management, Devender with execution focus.

For fourteen years, SignatureGlobal operated in the shadows of India's financial markets. Arbitrage trading, commodity dealing, financial services—profitable but unglamorous work. They were making money, but they weren't building anything tangible. No monuments to their success. No physical manifestation of their ambitions.

The pivot moment came gradually, then suddenly. By 2013, Pradeep Aggarwal was studying a different kind of arbitrage opportunity. Not between stock prices or commodity futures, but between housing demand and supply in India's fastest-growing city. Gurugram—once called Gurgaon, once just farmland—had transformed into India's Millennium City. Glass towers housed Fortune 500 companies. Malls sprouted like mushrooms after monsoon. But there was a glaring gap: where would the millions of workers powering this economic engine live?

The numbers were staggering. A software engineer earning ₹8 lakhs annually would need to spend 15-20 years of salary to buy a decent apartment in Gurugram. The mismatch was unsustainable. Either salaries had to rise dramatically, or housing prices had to fall. Pradeep bet on a third option: create a new category of housing that traditional developers ignored.

With a keen desire to do more, he ventured into the real estate business under the brand name 'Signature Global', focusing on Affordable Housing which was key to the growth of housing in India. The name itself was aspirational—"Signature" suggesting premium quality, "Global" indicating ambitions beyond local markets. The irony wasn't lost on industry observers: a global brand for local affordable housing.

The transformation from financial services to real estate wasn't random. Real estate is, at its core, a financial engineering business. You acquire land (working capital), develop it (value addition), sell units (revenue realization), and manage cash flows across multi-year project cycles. The Aggarwal brothers' financial markets background gave them three critical advantages:

First, they understood leverage and capital efficiency in ways traditional real estate families didn't. They knew how to structure deals, manage debt, and optimize returns on capital employed.

Second, they had relationships with financial institutions. While other developers struggled to raise capital, SignatureGlobal could tap into their decades-old relationships with banks and NBFCs.

Third, and most importantly, they understood market timing. Financial traders live and die by timing. Buy too early, you're stuck with dead capital. Buy too late, you miss the move. This timing instinct would prove crucial in 2014.

The company commenced operations in 2014 through its Subsidiary, Signature Builders Private Limited, with the launch of Solera project on 6.13 acres of land in Gurugram, Haryana. Solera wasn't just their first project—it was their proof of concept. Six acres might seem small, but in Gurugram's land-scarce market, it was enough to test their hypothesis: could you build quality affordable housing profitably?

The Solera project revealed something profound about Indian real estate. Traditional developers avoided affordable housing for three reasons: lower margins per unit, perceived reputational risk (affordable meant "cheap" in industry parlance), and execution complexity (selling 500 affordable units required different capabilities than selling 50 luxury units).

SignatureGlobal flipped each constraint into competitive advantage. Lower margins per unit? They'd make it up in volume and velocity. Reputational risk? They'd build a separate brand identity focused exclusively on affordable housing. Execution complexity? They'd build systems and processes optimized for high-volume sales and construction.

By late 2014, as Solera's foundation was being laid, something else was taking shape in New Delhi's power corridors. A new government had taken office with a mandate for development. Among its ambitious promises: Housing for All by 2022. SignatureGlobal had spent fourteen years preparing for a moment they didn't know was coming. The arbitrage traders had found their ultimate arbitrage: between government policy and market reality, between political promises and profitable execution.

The brothers didn't know it yet, but they had just entered the right market at the right time with the right model. The next phase would test whether their financial market instincts could translate into real estate success.

III. The Affordable Housing Thesis (2014-2018)

"Har Pariwar Ek Ghar"—a house for every family. When Pradeep Aggarwal unveiled this tagline in 2015, industry veterans smirked. It sounded like a government slogan, not a business strategy. But Aggarwal wasn't trying to impress real estate moguls. He was speaking directly to millions of Indians who'd given up on owning homes.

Affordable housing received greater prominence in 2015, when the Modi government made a grand announcement of providing 'Housing for All by 2022'—India's 75th year of independence. The Prime Minister's vision aligned perfectly with SignatureGlobal's business model, creating a rare moment when private profit and public policy converged.

The Affordable Housing Policy of 2013 had already laid groundwork, but it was the Pradhan Mantri Awas Yojana (PMAY) that transformed affordable housing from niche to necessity. Interest subsidies, tax benefits, infrastructure status for affordable housing—suddenly, building homes for the masses wasn't just socially responsible; it was financially lucrative.

Pradeep Aggarwal earned a moniker that would define his legacy: "The Affordable Man." Not the most glamorous title in real estate—no one was calling him a "visionary" or "mogul"—but it captured something essential. While others built for the classes, he built for the masses. While others sold dreams, he sold reality. The business model crystallized around three core insights. First, focus on the price band between ₹25-45 lakhs—affordable enough for middle-income families but profitable enough to scale. Second, leverage government policies that provided infrastructure status, tax benefits, and streamlined approvals. Third, build in bulk and sell fast—velocity over margin per unit.

The company successfully launched 18 Affordable Housing projects, all in prime locations which include Gurugram, Sohna and Karnal in Haryana. Each project followed a similar template: acquire land in emerging micro-markets, design standardized floor plans, launch pre-sales quickly, and deliver on time.

The strategic location choices were counterintuitive. While luxury developers fought over Golf Course Road and MG Road, SignatureGlobal targeted Sohna, sectors along the Dwarka Expressway, and parts of New Gurugram that traditional developers ignored. These weren't prime locations yet, but they had three advantages: lower land costs, proximity to employment hubs (a 30-45 minute commute), and government infrastructure investments planned for the next decade.

The Gurugram micro-market became their laboratory. Unlike Mumbai or Bangalore where multiple city centers existed, Gurugram's growth was linear—expanding outward from the Cyber City core. SignatureGlobal positioned itself along these growth corridors, buying land just ahead of infrastructure development. When the Southern Peripheral Road was announced, they were already there. When Dwarka Expressway plans materialized, they had locked in land parcels.

By 2016, something remarkable was happening. Projects were being governed by Haryana Affordable Housing Policy, 2013 as amended, which meant government-controlled pricing but also guaranteed demand through lottery systems. The lottery mechanism was brilliant—it created scarcity psychology even for affordable housing. Thousands would apply for hundreds of units, making each project launch an event.

The operational machine they built was equally impressive. The entire construction of projects was monitored by DTCP with developers mandated to use predefined materials approved by the government, ensuring superior quality construction. This wasn't just regulatory compliance—it was brand building. In a market where "affordable" often meant "substandard," SignatureGlobal's government-monitored quality became a differentiator.

The numbers started compounding. From a single project in 2014, they expanded to multiple launches annually. Each successful delivery built credibility, which drove more sales, which funded more land acquisition. The flywheel was spinning.

But the real masterstroke was understanding their customer psyche. These weren't investors looking for appreciation or NRIs parking money. These were families making the biggest financial decision of their lives—often liquidating ancestral gold, taking loans from relatives, stretching their finances to the breaking point. For them, owning a home wasn't just financial security; it was social arrival. SignatureGlobal's tagline resonated: "Kyuki Apna Ghar Toh Apna Hi Hota Hai" (Because your own home is truly your own).

By 2018, the company had achieved what seemed impossible four years earlier. They weren't just participants in affordable housing; they were defining it. The "Affordable Man" had built an affordable empire. But success in real estate is never permanent—it must be defended project by project, sale by sale. The next phase would test whether SignatureGlobal could scale without losing its edge.

IV. Scaling the Machine (2018-2021)

2018 opened with SignatureGlobal at an inflection point. They had proven the model worked. Now came the harder challenge: could they scale without breaking what made them successful?

The expansion strategy was methodical, almost boring in its consistency. No dramatic pivots to commercial real estate. No ventures into Mumbai or Bangalore. Just relentless execution in Delhi NCR—launch, sell, construct, deliver, repeat. By this point, they had refined their playbook to near-algorithmic precision.

Land acquisition became a science. The team identified parcels 18-24 months before launch, negotiating with farmers and land aggregators while infrastructure plans were still on drawing boards. They avoided land banking—tying up capital in undeveloped land for years. Instead, they practiced just-in-time acquisition: buy, develop, launch, sell. Capital velocity was everything. The construction methodology evolved into an assembly line. Standardized floor plans—450 square feet for 1BHK, 650 for 2BHK, 850 for 3BHK—enabled bulk procurement and faster construction. They weren't building architectural marvels; they were manufacturing homes. Think Henry Ford, but for apartments.

By March 31, 2023, they had sold 27,965 residential and commercial units, all within the Delhi NCR region, with an aggregate Saleable Area of 18.90 million square feet. These weren't just numbers—each unit represented a family's dream realized, a vote of confidence in SignatureGlobal's ability to deliver.

The sales machine was equally sophisticated. An extensive distribution network focused on customer segments with 593 channel partners and an in-house team of 41 employees engaged in direct sales and 100 employees supporting the sales infrastructure. This wasn't the typical real estate sales model of relationship managers in luxury showrooms. This was feet-on-the-street, hyperlocal distribution—channel partners who knew every society, every employer, every community in their territory.

Operating through Real Estate, NBFC, and Others segments gave them multiple revenue streams and financial flexibility. The NBFC arm could provide financing to customers who couldn't get traditional bank loans quickly enough. The construction materials supply business ensured quality control while capturing additional margin. Real estate consultancy and construction services to other developers generated cash flow during lean periods.

Then came March 2020. COVID-19 hit India, and the real estate sector froze. Construction sites shut down. Sales offices closed. Migrant workers fled cities. For most developers, it was catastrophe. For SignatureGlobal, it became opportunity.

The company's track record in execution and continued construction was instrumental in maintaining consistent sales and performance, even amid challenging market conditions during the COVID-19 pandemic. While luxury developers saw projects stall and buyers disappear, affordable housing demand remained resilient. Why? Because SignatureGlobal's customers weren't buying investment properties or second homes. They were buying primary residences—essential, not discretionary purchases.

The pandemic accelerated a trend that benefited SignatureGlobal: the shift from rental to ownership. Locked in small rental apartments during lockdowns, thousands of families decided they needed their own homes. Work-from-home meant they could move to peripheral areas where SignatureGlobal dominated. The government's liquidity measures and low interest rates made mortgages more affordable.

SignatureGlobal's response was textbook crisis management. They kept construction going wherever permitted, ensuring project timelines didn't slip catastrophically. They pivoted sales online—virtual tours, digital documentation, online bookings. Most importantly, they maintained trust by continuing to deliver projects when competitors couldn't.

Sales (net of cancellation) grew at CAGR of 42.46%, from ₹16,902.74 million in Fiscal 2021 to ₹34,305.84 million in Fiscal 2023. While the world was melting down, SignatureGlobal was melting up. The pandemic that should have killed them made them stronger.

The standardization that seemed like a limitation became their salvation. Because every project followed similar blueprints, they could shift resources between sites as lockdowns lifted in different areas. Because their supply chain was concentrated on fewer materials, they could negotiate better when supplies tightened. Because their customers were local, not NRI investors, demand stayed robust.

By early 2021, as India emerged from its second COVID wave, SignatureGlobal's position had strengthened dramatically. Weaker competitors had exited or slowed expansion. Land prices had corrected, creating acquisition opportunities. The company that entered the pandemic as a strong regional player would exit it as the undisputed affordable housing champion of NCR. The stage was set for their next act: going public.

V. The IPO Story & Public Market Debut (2023)

September 2023. The Indian stock market is on fire. The Sensex has crossed 67,000. IPO mania grips retail investors. In this frothy environment, SignatureGlobal's bankers are pitching a different story: not a tech unicorn or a consumer brand, but a nuts-and-bolts real estate developer from Gurugram. The timing was deliberate. India's real estate sector had finally recovered from the twin shocks of demonetization and GST implementation. Interest rates were stable. The affordable housing segment was seeing unprecedented demand. And crucially, SignatureGlobal had numbers to show: they were profitable, growing, and dominant in their niche.

The IPO aimed to raise ₹730 crores, with the fresh issue portion comprising 1,56,62,338 shares, translating into a fresh issue size of ₹603 crore. The offer for sale (OFS) portion comprised 32,98,701 shares. The structure was telling—mostly fresh capital for growth, with limited promoter selldown. The founders weren't cashing out; they were raising ammunition for the next phase.

The price band was set at ₹385 per share, valuing the company at approximately ₹5,400 crores at the upper band. For context, this was less than one-tenth of DLF's market cap, despite SignatureGlobal having higher market share in affordable housing than DLF had in luxury. The valuation discount was the "affordable housing discount"—investors systematically valued affordable housing developers lower than luxury players.

The roadshow revealed investor concerns. Could they maintain margins as land prices rose? Would government support for affordable housing continue? How would they handle competition from larger players entering their segment? The management team had answers, but ultimately, the market would decide.

SignatureGlobal raised ₹318.50 crore from anchor investors on September 18, 2023—a positive signal. The anchor book included marquee names, suggesting institutional confidence. When the IPO opened for retail subscription on September 20, the response was immediate.

The IPO was subscribed 11.88 times on September 22, 2023. The public issue subscribed 6.82 times in the retail category, 12.71 times in the QIB category, and 13.54 times in the NII category. The oversubscription wasn't spectacular by 2023 IPO standards—some tech IPOs were seeing 100x oversubscription—but it was solid, especially for a real estate company.

The retail response—6.82 times—was particularly interesting. These were individual investors betting on a company that built homes for people like them. The QIB oversubscription of 12.71 times showed institutional interest, while the highest oversubscription in the NII category (13.54 times) suggested wealthy individuals saw value.

The shares got listed on BSE, NSE on September 27, 2023. The listing day was anticlimatic—no massive pop, no dramatic crash. The stock opened near the issue price, traded in a narrow range, and closed marginally higher. The real story would unfold over the coming months.

The use of proceeds revealed the company's priorities. Repayment or pre-payment of certain borrowings availed by the Company and to reimburse or prepay certain borrowings its subsidiaries had taken out. This wasn't growth capital for aggressive expansion—it was balance sheet strengthening, reducing leverage before the next growth phase.

What the IPO really achieved was legitimacy. SignatureGlobal was no longer a private company operating in opacity. They now had quarterly earnings calls, analyst coverage, and institutional shareholders. The scrutiny would be intense, but so would the access to capital.

Post-IPO, the stock's performance would surprise everyone. From ₹385 at listing to over ₹1,000 within a year—a nearly 3x return while the broader market rose 20%. The market was rerating affordable housing, and SignatureGlobal was the primary beneficiary.

But success in public markets brings its own challenges. Quarterly earnings pressure, analyst expectations, and the constant need to communicate strategy to thousands of shareholders. The company that had operated like a tight-knit family business now had to perform on the public stage.

VI. Business Model Deep Dive

To understand SignatureGlobal's dominance, you need to understand the unit economics of affordable housing in India. It's a business of millimeters—thin margins multiplied by massive volume, where a 2% cost overrun can destroy profitability and a 2% efficiency gain can double it.

Start with the customer. A typical SignatureGlobal buyer is a household earning ₹6-10 lakhs annually—a junior manager at an IT company, a small business owner, a government employee. As of March 31, 2023, they sold 25,089 residential units with an average selling price of ₹3.60 million per unit. At ₹36 lakhs, with a 20% down payment and a 20-year loan at 8.5% interest, the EMI comes to roughly ₹25,000—about 35-40% of household income. Just within the boundary of affordability.

The economics work because of government support. Under the Pradhan Mantri Awas Yojana, buyers get interest subsidies of up to 2.67% for loans up to ₹6 lakhs. GST on affordable housing is 1% versus 5% for other residential projects. Developers get faster approvals, lower development charges, and additional FSI (Floor Space Index). Each incentive might seem small, but together they transform the economics.

SignatureGlobal's gross margins hover around 25-30%—lower than the 40-50% luxury developers target, but the asset turnover is completely different. A luxury project might take 5-7 years from land acquisition to completion. SignatureGlobal's projects typically complete in 3-4 years. When you're turning capital twice as fast, you can accept lower margins per turn.

Sales (net of cancellation) grew at a compounded annual growth rate of 42.46%, from Rs. 1690.27 cr. in Fiscal 2021 to Rs. 3430.58 cr in Fiscal 2023. This wasn't just market growth—SignatureGlobal was taking share. How? Through what they call the "integrated model."

SignatureGlobal adopted an integrated real estate development model, with in-house capabilities and resources to execute projects from inception to completion. Unlike competitors who outsource construction, sales, or design, SignatureGlobal controls the entire value chain. This vertical integration has three benefits:

First, cost control. When you're building at ₹1,800 per square foot and selling at ₹4,500, every ₹100 saved in construction costs directly impacts margins. By controlling procurement, construction, and project management, they squeeze out inefficiencies that layered outsourcing creates.

Second, speed. Among its core strengths is the Company's ability to efficiently turnaround projects on land that it ties-up and it typically launched projects within a period of 18 months from the date of acquisition of the land. In real estate, time is literally money—every month of delay means additional interest costs, opportunity costs, and market risk.

Third, quality control. When subcontractors have different standards and incentives, quality suffers. SignatureGlobal's integrated model ensures consistency—critical when your brand promise is "affordable doesn't mean compromise."

The land acquisition strategy is particularly clever. Unlike luxury developers who compete for prime locations, SignatureGlobal targets land in emerging corridors—areas that will be prime in 5-10 years. They're not buying the present; they're buying the future at present prices.

The capital structure reveals another advantage. While real estate is typically a leveraged business, SignatureGlobal maintains surprisingly low debt levels. This isn't conservatism—it's strategy. In affordable housing, presales fund construction. Customers pay 20-30% upfront, then instalments linked to construction milestones. By the time construction completes, 80-90% of the project is already paid for.

The NBFC subsidiary adds another dimension. Many affordable housing buyers don't qualify for bank loans immediately—documentation issues, informal income, credit history gaps. SignatureGlobal's NBFC can bridge this gap, providing short-term financing until buyers qualify for bank loans. It's not a major profit center, but it removes a crucial bottleneck in the sales process.

Distribution is where SignatureGlobal truly differs from luxury developers. The Company has an extensive distribution network focused on the customer segments it targets, with 593 channel partners and an in-house team of 41 employees engaged in direct sales. These aren't relationship managers in air-conditioned offices—they're feet-on-the-street salespeople who understand local markets intimately.

The technology stack, while not cutting-edge, is fit for purpose. CRM systems track thousands of leads. Construction management software monitors multiple projects simultaneously. Digital marketing generates leads at a fraction of traditional advertising costs. Nothing revolutionary, but in affordable housing, competent execution beats innovation.

What's remarkable is what SignatureGlobal doesn't do. No land banking—tying up capital for years. No diversification into commercial or retail—different economics, different capabilities needed. No geographic expansion beyond NCR—better to dominate one market than be subscale in many. This focus might seem limiting, but it's actually liberating. When you know exactly what you are, decisions become clearer.

The numbers tell the story. Till Q1FY24-25, Signature Global has delivered over 11 million square feet of projects and currently has ongoing projects covering 16.4 million square feet, along with a robust pipeline of 29.6 million square feet of saleable area. This pipeline visibility—essentially 5-7 years of execution already locked in—provides revenue predictability rare in real estate.

The business model's true test came during COVID-19. While luxury developers saw projects stall and buyers disappear, SignatureGlobal's affordable housing demand remained resilient. Their customers weren't buying investment properties—they were buying homes to live in. This demand stability, combined with operational efficiency, explains why they emerged from the pandemic stronger than they entered it.

VII. Market Position & Competition

In real estate, market share numbers can lie. A developer might claim 10% market share by including all segments, all geographies, all price points. SignatureGlobal's market share claims are different—they're specific, verifiable, and dominant within their defined niche.

Signature Global is the largest real estate development company in the National Capital Region of Delhi in affordable and lower mid-segment housing in terms of units supplied with a 27% Market share in Gurguam and 13% Market share in NCR. These aren't marketing claims—they're from ANAROCK, India's leading real estate research firm.

To understand what 27% market share in Gurugram means, consider the competition. DLF, India's largest real estate company by market cap, has less than 10% share in Gurugram's overall residential market. Godrej Properties, backed by one of India's most trusted conglomerates, has single-digit share. M3M, Vatika, Ireo—all established players, all with smaller shares than SignatureGlobal in affordable housing.

How did a company that started in 2014 achieve what established players couldn't? The answer lies in focus and timing. While others were building luxury towers for the top 1%, SignatureGlobal targeted the next 10%—a market ten times larger but historically ignored.

The competitive landscape in affordable housing is fundamentally different from luxury real estate. In luxury, brand matters enormously. Buyers pay premiums for a DLF or Godrej address. In affordable housing, brand matters less than location, price, and delivery certainty. SignatureGlobal understood this and built capabilities accordingly.

Take DLF, the obvious comparison. With a market cap over ₹1,50,000 crores versus SignatureGlobal's ₹17,000 crores, DLF is nearly 10 times larger. But DLF's business model is fundamentally different. They're asset-heavy, owning commercial properties that generate rental income. They build luxury residential projects with 50%+ margins but multi-year execution cycles. They have diversified across India's major cities.

SignatureGlobal is DLF's opposite—asset-light (no commercial properties), focused on quick-turnover residential projects, concentrated in one geography. It's not that one model is better; they're playing different games. DLF is building a real estate empire; SignatureGlobal is running a housing factory.

Godrej Properties presents a different challenge. Backed by the 125-year-old Godrej Group, they have brand trust SignatureGlobal can't match. They've entered affordable housing aggressively, leveraging their brand to attract buyers. But they're spread across Mumbai, Bangalore, Pune, and NCR. In each market, they're subscale compared to local specialists like SignatureGlobal in NCR.

The local competition is more direct. Signature's real competitors are companies like ATS, Pareena, ROF, and dozens of smaller developers building in the same micro-markets. These players know the local approval processes, have relationships with landowners, understand the customer. But most lack SignatureGlobal's scale, execution capability, and capital access.

Signature Global holds a market share of 13% in the Delhi NCR region and 27% in the micro markets of Gurugram within these segments. The micro-market focus is crucial. Gurugram isn't one market—it's multiple micro-markets with different dynamics. Old Gurugram near the Cyber City is saturated and expensive. New Gurugram along Dwarka Expressway is emerging. Sohna Road is transforming from peripheral to prime. SignatureGlobal dominates the emerging micro-markets where affordable housing demand concentrates.

The barriers to entry in affordable housing seem low—land is available, construction is standardized, customers are plentiful. But the barriers to scale are high. You need relationships with hundreds of channel partners. You need credibility with banks for project financing. You need track record for customer trust. Most importantly, you need operational excellence to make money at these price points.

SignatureGlobal's competitive moat isn't any single factor—it's the combination. Scale economies in procurement. Distribution network density. Execution track record. Government relationships. Brand recognition in the target segment. Each reinforces the others, creating a flywheel effect that's hard for competitors to replicate.

The competitive dynamics are changing, though. As affordable housing becomes more attractive, larger players are entering. DLF has announced affordable housing projects. Godrej is scaling up. Private equity funds are backing new developers. The easy market share gains are over; future growth will require taking share from established players.

SignatureGlobal's response has been to move slightly upmarket. Initially established as a key player in affordable and mid-housing, the company successfully transitioned to the premium housing segment in 2024, marked by the successful launch of two group housing projects with record sales value. The company now focuses on the mid-housing and premium segments.

This isn't abandoning affordable housing—it's expanding the addressable market. As their original customers' incomes grow, they want to upgrade. By offering mid-segment and premium options, SignatureGlobal can capture this upgrade demand while using their execution capabilities in higher-margin segments.

The Delhi NCR market itself provides structural advantages. Unlike Mumbai where land is scarce or Bangalore where development is scattered, NCR has vast land banks awaiting development. The government's infrastructure investments—new metro lines, expressways, airports—constantly create new micro-markets. For a developer with SignatureGlobal's capabilities, it's a target-rich environment.

The real competition might come from an unexpected source: organized rental housing. As work-from-home normalizes and job mobility increases, young professionals might prefer renting to buying. Companies like Nestaway and NoBroker are making rental more organized and attractive. If rental becomes a viable alternative to ownership, it could impact affordable housing demand.

But for now, SignatureGlobal's market position seems secure. They have scale advantages over smaller players, focus advantages over diversified players, and execution advantages over new entrants. The question isn't whether they'll maintain market share—it's whether they can replicate this dominance as they expand into new segments and potentially new geographies.

VIII. Growth Strategy & Future Vision

December 2024. SignatureGlobal's senior management gathers for their annual strategy session. The agenda seems paradoxical: how to grow beyond affordable housing without abandoning what made them successful. The answer would reshape the company's next decade. Initially established as a key player in affordable and mid-housing, the company successfully transitioned to the premium housing segment in 2024, marked by the successful launch of two group housing projects with record sales value. The pivot wasn't abandonment—it was evolution.

The logic was compelling. SignatureGlobal's original customers from 2014-2018 had seen their incomes grow. The IT professional earning ₹6 lakhs in 2014 might be earning ₹15 lakhs by 2024. They wanted to upgrade, but didn't trust new developers. SignatureGlobal could capture this upgrade demand while maintaining customer relationships.

The company now focuses on the mid-housing and premium segments, emphasizing quality execution, value creation, reliability, and adherence to global standards. This wasn't just changing price points—it required fundamental capability building. Premium buyers expect different amenities, finishes, and service levels. The sales process changes from mass marketing to relationship building.

As of H1FY25, the company has sold over 30,000 residential and commercial units. The scale had reached a point where they could support multiple product lines without losing focus. Think of it like Toyota—they started with affordable Corollas but eventually built Lexus. Same operational excellence, different market positioning.

The geographic expansion strategy remains notably conservative. While competitors rush to enter Mumbai, Bangalore, or Pune, SignatureGlobal continues to deepen its presence in NCR. The company has replicated its business model across micro-markets in Delhi NCR, with a particular focus on Gurugram, Haryana, and has consistently grown its operations by leveraging its strong brand presence.

This NCR focus isn't stubbornness—it's strategy. Every new micro-market within NCR leverages existing relationships, brand recognition, and operational infrastructure. Expanding to Mumbai would mean starting from scratch—new approval processes, new channel partners, new customer preferences. Better to be the big fish in one pond than a minnow in many.

The land acquisition strategy has evolved with the market. Recent land acquisition in Sohna, with Chairman emphasizing strong project launches and customer focus, shows they're still betting on emerging corridors. But now they're also looking at land in more established areas for premium projects. The ability to play across the spectrum—from emerging to established locations—provides flexibility as market dynamics shift.

Till Q1FY24-25, Signature Global has delivered over 11 million square feet of projects and currently has ongoing projects covering 16.4 million square feet, along with a robust pipeline of 29.6 million square feet of saleable area. This pipeline—essentially 5-7 years of execution visibility—provides remarkable revenue predictability for a real estate company.

Technology adoption has accelerated post-IPO. Digital marketing capabilities that were adequate for affordable housing need upgrading for premium segments. Virtual reality tours, AI-powered lead scoring, automated customer relationship management—investments that seemed unnecessary in affordable housing become essential in premium segments where customer acquisition costs are higher.

The company's pre sales zoomed 184% to Rs 2,780 crore in Q2 FY25 from Rs 980 crore recorded in Q2 FY24. This explosive growth came primarily from the premium segment launches, validating the strategy pivot. On half year basis, companys sales realization for first half of FY25 was at Rs 13,379 per sq. ft. as compared with Rs 11,762 per sq. ft. posted in same period a year ago. The 14% increase in realization per square foot shows successful upmarket movement.

The company is expected to reach Rs 10,000 crore in pre-sales by 2024-25, driven by the launch of three new projects spread across 8-10 million square feet. They have already exceeded their guidance of Rs 4,500 crore for the current financial year, generating Rs 3,600 crore from their latest premium housing residential development project on Dwarka Expressway.

The sustainable development focus isn't just corporate responsibility—it's becoming a differentiator. Most of the company's projects are either EDGE or IGBC certified. In premium segments, environmental certification can command price premiums. What started as compliance in affordable housing becomes a selling point in premium segments.

Signature Global has attracted support from prominent investors like Nomura, HDFC, IFC, Standard Chartered, Bandhan MF, and Kotak. This institutional backing provides not just capital but credibility—crucial when entering premium segments where brand perception matters more.

The vertical integration strategy continues to evolve. Beyond construction and sales, they're exploring property management, rental housing, and even co-working spaces. Each adjacent business leverages existing capabilities while providing new revenue streams and customer touchpoints.

The organizational challenge is maintaining culture while scaling. The scrappy, entrepreneurial culture that built the affordable housing business might not fit the premium segment's demands. SignatureGlobal is investing heavily in talent—hiring from luxury developers, bringing in design consultants, upgrading customer service capabilities.

Risk management has become more sophisticated post-IPO. Net debt stood at Rs 1,020 crore as on 30 September 2024. For a company with their scale and pipeline, this debt level is conservative—showing they're growing without overleveraging.

The future vision is becoming clearer: SignatureGlobal wants to be NCR's dominant residential developer across all segments except ultra-luxury. From ₹35 lakh affordable homes to ₹3 crore premium apartments, they want to capture the entire middle-class housing journey. It's ambitious but logical—leveraging their execution capabilities across wider price points while maintaining geographic focus.

The international opportunity remains unexplored. Indian developers like Lodha and Prestige have successfully entered Dubai and London markets. SignatureGlobal hasn't shown international ambitions yet, preferring to consolidate their NCR dominance. But with their execution capabilities and capital access, international expansion could be the next frontier.

What's remarkable is what they're not doing. No massive commercial real estate projects. No township developments requiring decades-long execution. No speculative land banking. The discipline that defined their affordable housing success continues even as they expand into new segments. They're growing, but growing carefully.

IX. Playbook: Lessons for Founders & Investors

SignatureGlobal's journey from financial services firm to NCR's affordable housing champion offers a masterclass in market entry, scaling, and category creation. The lessons aren't just for real estate—they apply to any founder trying to build in traditional industries with entrenched incumbents.

Lesson 1: Time Your Entry with Structural Tailwinds

SignatureGlobal didn't enter real estate randomly in 2014. They identified three converging factors: government policy support (Affordable Housing Policy 2013), demographic demand (millions entering middle class), and competitive void (established players ignoring affordable segment). When structural forces align, even new entrants can win against incumbents.

The timing wasn't luck—it was pattern recognition. The Aggarwal brothers' financial markets background taught them to identify when multiple factors converge to create opportunity. In markets, this creates price dislocations. In business, it creates market dislocations that new entrants can exploit.

Lesson 2: Pick Your Niche and Dominate Before Expanding

Between 2014-2023, SignatureGlobal resisted every temptation to diversify. No commercial real estate when it was booming. No luxury housing when margins looked attractive. No geographic expansion when other markets beckoned. They picked affordable housing in NCR and became undisputed champions before expanding to adjacent segments.

This focus seems limiting but it's actually liberating. When you know exactly what you are, every decision becomes clearer. Should we enter Mumbai? No, we're NCR-focused. Should we build a mall? No, we're residential specialists. Should we try luxury? Not until we've dominated affordable.

Lesson 3: Build Trust in Trust-Deficit Industries

Indian real estate in 2014 was synonymous with delays, quality issues, and developer bankruptcies. Buyers, especially in affordable segments, were skeptical. SignatureGlobal's response wasn't marketing—it was execution. Deliver projects on time. Build quality even at low price points. Honor commitments even when costly.

Trust compounds faster than capital in trust-deficit industries. Every delivered project became a reference. Every satisfied customer became a salesperson. By year 5, SignatureGlobal didn't need to convince buyers they were trustworthy—their track record spoke for itself.

Lesson 4: Design for Capital Velocity, Not Margin Maximization

Traditional real estate optimizes for margin per project. SignatureGlobal optimized for capital velocity—how fast they could turn invested capital into returned capital. Lower margins (25-30%) but faster turns (3-4 years) generated better returns than higher margins (40-50%) with slower turns (5-7 years).

This velocity focus shaped everything: standardized designs to speed construction, presales to fund development, quick launch cycles to maintain momentum. They thought like traders (their original business) not builders—maximizing portfolio returns, not individual project returns.

Lesson 5: Operational Excellence Beats Strategic Brilliance

SignatureGlobal's strategy wasn't revolutionary—build affordable homes in growing markets. Dozens of developers had the same strategy. The difference was execution. Their 18-month land-to-launch cycle, 593-partner distribution network, standardized construction processes—these operational capabilities created the moat.

In commodity businesses (and affordable housing is ultimately a commodity), operational excellence is the only sustainable differentiation. You can't compete on product features—everyone builds similar apartments. You compete on who can deliver those apartments faster, cheaper, more reliably.

Lesson 6: Leverage Government Policy, Don't Depend on It

SignatureGlobal brilliantly leveraged government support for affordable housing—interest subsidies, tax benefits, faster approvals. But they didn't become dependent. Their business model worked even without subsidies; government support just improved the economics.

This balance is crucial. Too little engagement with policy and you miss opportunities. Too much dependence and you're vulnerable to policy changes. SignatureGlobal found the sweet spot—aligned with government objectives while building a business that could survive policy shifts.

Lesson 7: Distribution Density Beats Brand Building

While luxury developers invested in brand advertising, SignatureGlobal invested in distribution density. Their 593 channel partners and 100-person sales team created presence in every relevant micro-market. In affordable housing, being present where customers are beats having a premium brand they see in advertisements.

This ground-level distribution also provided market intelligence. Channel partners knew which projects were selling, what customers wanted, where infrastructure was developing. This information advantage helped SignatureGlobal make better land acquisition and project design decisions.

Lesson 8: Standardization Enables Scale

SignatureGlobal's standardized floor plans—450/650/850 square feet—seemed limiting but enabled massive operational advantages. Bulk procurement, faster approvals, construction efficiency, reduced errors. Standardization in affordable housing is like McDonald's in fast food—consistency enables scale.

But standardization doesn't mean rigidity. SignatureGlobal adapted amenities, facades, and configurations to local preferences while maintaining core standardization. They found the balance between efficiency and customization.

Lesson 9: Manage Working Capital Like a Trader

The Aggarwal brothers' trading background showed in how they managed working capital. Quick land acquisition decisions (but with 18-month development cycles). Aggressive presales to generate cash. Minimal land banking to avoid dead capital. They ran a real estate company with a trader's capital discipline.

This discipline became crucial during COVID-19. While overleveraged developers struggled, SignatureGlobal's conservative balance sheet and positive cash flows allowed them to continue operations and even acquire distressed assets.

Lesson 10: Scale Your Ambitions with Your Capabilities

SignatureGlobal's evolution from affordable to premium housing wasn't premature ambition—it matched their capability development. Only after dominating affordable housing, building execution credibility, and accessing public markets did they attempt premium segments. They scaled ambitions with capabilities, not ahead of them.

For Investors: What to Look For

SignatureGlobal's journey offers lessons for investors evaluating similar businesses:

- Market position in growing niches beats subscale presence in large markets

- Execution track record matters more than strategic vision in operational businesses

- Capital efficiency (high velocity, low leverage) provides downside protection

- Management's background often predicts operational DNA (traders → capital discipline)

- Regulatory alignment without dependence provides upside with limited downside

The Meta-Lesson

SignatureGlobal's biggest lesson might be that traditional industries aren't impenetrable. With proper timing, focused execution, and operational excellence, new entrants can disrupt established players. The key isn't revolutionary innovation—it's evolutionary execution, doing basics better than incumbents who've become complacent.

X. Bear vs. Bull Case Analysis

Every investment thesis has two sides. For SignatureGlobal, the bull case seems compelling—dominant market position, structural tailwinds, proven execution. But the bear case has merit too. Let's examine both with the objectivity that fundamental investors require.

Bull Case: The Unstoppable Force

Structural Housing Shortage India needs 40+ million additional housing units by 2030. The deficit isn't shrinking—urbanization adds 10 million people annually to cities. At current construction rates, the shortage will persist for decades. SignatureGlobal operates in a market where demand exceeds supply by multiples, not percentages.

Government Support Continuing Housing for All isn't just policy—it's political necessity. Every major party supports affordable housing. The benefits—interest subsidies, tax breaks, infrastructure status—have survived multiple budgets and political changes. This isn't discretionary spending; it's core to India's development agenda.

Proven Execution Machine As of H1FY25, the company has sold over 30,000 residential and commercial units. This isn't promise—it's performance. Their ability to deliver projects on time, at scale, profitably, has been proven through cycles. In real estate, execution track record is everything.

Balance Sheet Strength Net debt stood at Rs 1,020 crore as on 30 September 2024. For a company with ₹17,000+ crore market cap and massive pipeline, this leverage is minimal. They can weather downturns, acquire distressed assets, and fund growth without dilution.

Successful Premium Pivot Sales realization for first half of FY25 was at Rs 13,379 per sq. ft. as compared with Rs 11,762 per sq. ft. posted in same period a year ago. The 14% realization increase proves they can move upmarket successfully. Premium housing offers higher margins, better working capital cycles, and less dependence on government policy.

NCR's Continued Growth Delhi NCR adds 500,000 people annually. New infrastructure—metros, expressways, airports—constantly creates new micro-markets. Unlike Mumbai (land-constrained) or Bangalore (infrastructure-challenged), NCR has room to grow for decades.

Operational Leverage Kicking In The fixed costs—management, systems, brand—are largely built. Incremental projects require minimal additional overhead. As they scale from 30,000 to 50,000 units, margins should expand significantly.

Second-Generation Demand SignatureGlobal's customers from 2014-2018 are now looking to upgrade. Their children need homes. This creates natural, recurring demand from a customer base that already trusts the brand.

Valuation Discount to Peers At ₹17,000 crore market cap versus DLF's ₹150,000+ crore, SignatureGlobal trades at massive discount despite higher growth and market share in their segment. As institutional ownership increases, this valuation gap should narrow.

Bear Case: The Immovable Objects

Geographic Concentration Risk 100% revenue from NCR is dangerous. A regional slowdown, regulatory change, or infrastructure failure could devastate the business. No geographic diversification means no risk mitigation.

Policy Dependence Despite claims of independence, affordable housing economics depend on government support. Remove interest subsidies or tax benefits, and the addressable market shrinks dramatically. Policy support that created the business could also destroy it.

Rising Input Costs Land prices in NCR are rising faster than income growth. Construction costs—cement, steel, labor—face structural inflation. If input costs rise faster than selling prices, margins will compress regardless of execution efficiency.

Competition Intensifying DLF, Godrej, and other established players are entering affordable housing. They bring brand recognition, capital access, and government relationships SignatureGlobal took years to build. The easy market share gains are over.

Interest Rate Sensitivity SignatureGlobal's customers are extremely rate-sensitive. A 2% rate increase might price out 30% of potential buyers. India's interest rate cycle has been benign for years—that could change quickly.

Execution Risk at Scale Managing 30,000 units is different from managing 50,000. Systems that work at current scale might break at larger scale. Real estate is notorious for successful companies failing when they grow too fast.

Technology Disruption Proptech companies are reimagining real estate—from purchase processes to construction methods. SignatureGlobal's traditional model might be disrupted by technology-first competitors.

Working Class Vulnerability SignatureGlobal's target customers—earning ₹6-15 lakhs—are vulnerable to economic shocks. Job losses, wage cuts, or inflation could dramatically impact their home-buying capacity. This customer segment has less financial resilience than luxury buyers.

Reputation Risk One major project failure—quality issues, delays, legal problems—could destroy decades of trust-building. In affordable housing where buyers have limited recourse, reputation is fragile.

Market Saturation NCR's affordable housing market isn't infinite. At current construction rates, supply might catch up with demand within 5-7 years. When it does, pricing power evaporates and competition intensifies.

The Balanced View

The truth likely lies between extremes. SignatureGlobal operates in a structurally attractive market with proven execution capabilities, but faces real risks from concentration, competition, and cyclicality.

For long-term investors, the key questions are: - Can they maintain execution quality while scaling? - Will government support persist through political cycles? - Can they successfully expand beyond NCR when needed? - Will the premium pivot reduce their policy dependence? - Can they build technological capabilities before disruption arrives?

The bull case rests on continued execution in a growing market. The bear case warns of concentration risk and competitive threats. Neither is wrong—both could be right at different times.

Smart investors might see SignatureGlobal as a play on India's urbanization with embedded options on premium housing and geographic expansion. The affordable housing business provides base case value; successful expansion provides upside optionality.

The stock's volatility reflects this uncertainty. From ₹385 IPO price to over ₹1,000, back to ₹800, now around ₹1,000—the market can't decide if SignatureGlobal is a structural winner or a cyclical player. This volatility creates opportunity for investors with conviction and patience.

XI. Epilogue & Final Thoughts

As we close this deep dive into SignatureGlobal, it's worth zooming out to see what their story represents in India's larger economic narrative. This isn't just about one company's success—it's about how India's economic transformation creates opportunities for those who can execute at the intersection of policy, demographics, and ambition.

SignatureGlobal embodies a uniquely Indian business model: solving social problems profitably. While Silicon Valley startups chase unicorn valuations by creating needs, SignatureGlobal addresses existing, desperate need—shelter for millions of Indian families. They've proven you can build a ₹17,000 crore company by serving customers that luxury-focused competitors ignored.

The India growth story isn't abstract GDP numbers or stock indices—it's millions of families moving from rental to ownership, from informal to formal housing, from aspiration to achievement. SignatureGlobal captures this transition perfectly. Every apartment they deliver represents a family's arrival into India's middle class, complete with property rights, formal credit history, and generational wealth creation.

The urbanization megatrend will define India's next three decades. By 2050, 600 million Indians will live in cities—double today's urban population. These new urbanites need housing, and not the luxury towers dotting Mumbai's skyline. They need what SignatureGlobal builds—functional, affordable, aspirational homes. The company sits at the center of India's largest demographic shift.

What's particularly instructive is how SignatureGlobal navigated the tension between social impact and profit maximization. They didn't choose one or the other—they found synthesis. By keeping prices affordable, they expanded their addressable market. By maintaining quality despite low prices, they built trust and repeat business. By aligning with government objectives, they accessed benefits that improved economics. Social impact became competitive advantage.

The entrepreneurial lesson is profound: in emerging markets, the biggest opportunities often lie in serving the masses, not the classes. While competitors fought over the luxury segment's 1-2% of buyers, SignatureGlobal dominated the next 15-20%. The math is simple but the execution is complex—which is exactly the kind of moat that sustains competitive advantage.

For international investors trying to understand India, SignatureGlobal offers a window into how Indian businesses actually work. The importance of government relations (but not dependence). The value of operational excellence over strategic brilliance. The power of solving real problems for real people. These aren't lessons from business school—they're lessons from building in India's complex, competitive markets.

The company's evolution from affordable to premium housing reflects India's own economic evolution. As incomes rise, aspirations expand. The customer buying a ₹35 lakh apartment today wants a ₹75 lakh apartment tomorrow. SignatureGlobal is positioning to capture this upgrade cycle—growing with their customers rather than constantly finding new ones.

There's also a sobering lesson about the limits of financial engineering in real businesses. The Aggarwal brothers' financial markets background helped with capital allocation and risk management, but ultimately, SignatureGlobal succeeded through operational execution. You can't trade your way to success in real estate—you have to build, literally and figuratively.

Looking forward, SignatureGlobal faces choices that will define its next decade. Geographic expansion beyond NCR seems inevitable but risky. International expansion could provide growth but requires new capabilities. Technology integration is necessary but expensive. Each choice involves trade-offs between growth and focus, ambition and execution.

The biggest risk might be success itself. As SignatureGlobal becomes larger, wealthier, more institutional, will it maintain the hunger that drove its first decade? Can a ₹17,000 crore public company maintain the agility of a startup? History suggests it's difficult but not impossible—companies like HDFC Bank and Asian Paints have maintained execution excellence despite scale.

For India's real estate sector, SignatureGlobal represents hope that the industry can evolve beyond its reputation for delays, defaults, and disappointments. By delivering what they promise, when they promise it, at the price they promise, they've shown that real estate can be a professional, trustworthy business.

The macro picture remains compelling. India needs millions of homes. The government supports affordable housing. Urbanization continues accelerating. Income growth, while volatile, trends upward. SignatureGlobal is positioned at the intersection of these trends, with proven ability to execute at scale.

Yet nothing is guaranteed. Real estate is cyclical. Government policies change. Competition intensifies. Technology disrupts. SignatureGlobal's next decade will test whether they can navigate these challenges while maintaining their execution edge.

What makes SignatureGlobal fascinating isn't just their past success but their potential future. Could they become India's largest residential developer? Could they replicate their model internationally? Could they redefine what affordable housing means in India? These questions remain open, their answers being written quarter by quarter, project by project.

As we conclude, it's worth remembering that every SignatureGlobal apartment represents a dream realized. Behind the financial metrics and market share statistics are millions of Indians who now own homes because SignatureGlobal figured out how to make housing affordable and profitable simultaneously.

That's perhaps SignatureGlobal's greatest achievement—proving that in India's vast, complex, opportunity-rich markets, solving real problems for real people isn't just good business; it's great business. The company that started as arbitrage traders became builders of dreams, one affordable apartment at a time.

The SignatureGlobal story is still being written. Whether it becomes a case study in sustained excellence or a cautionary tale of overreach remains to be seen. But what's already clear is that they've changed India's real estate industry, created enormous value for stakeholders, and helped millions of Indians achieve their dream of homeownership.

In a world obsessed with disruption and innovation, SignatureGlobal reminds us that sometimes the biggest opportunities lie not in creating the future but in delivering the present—professionally, profitably, and at scale. That's a lesson worth remembering, whether you're an entrepreneur, investor, or simply someone trying to understand how business really works in the world's most populous nation.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube