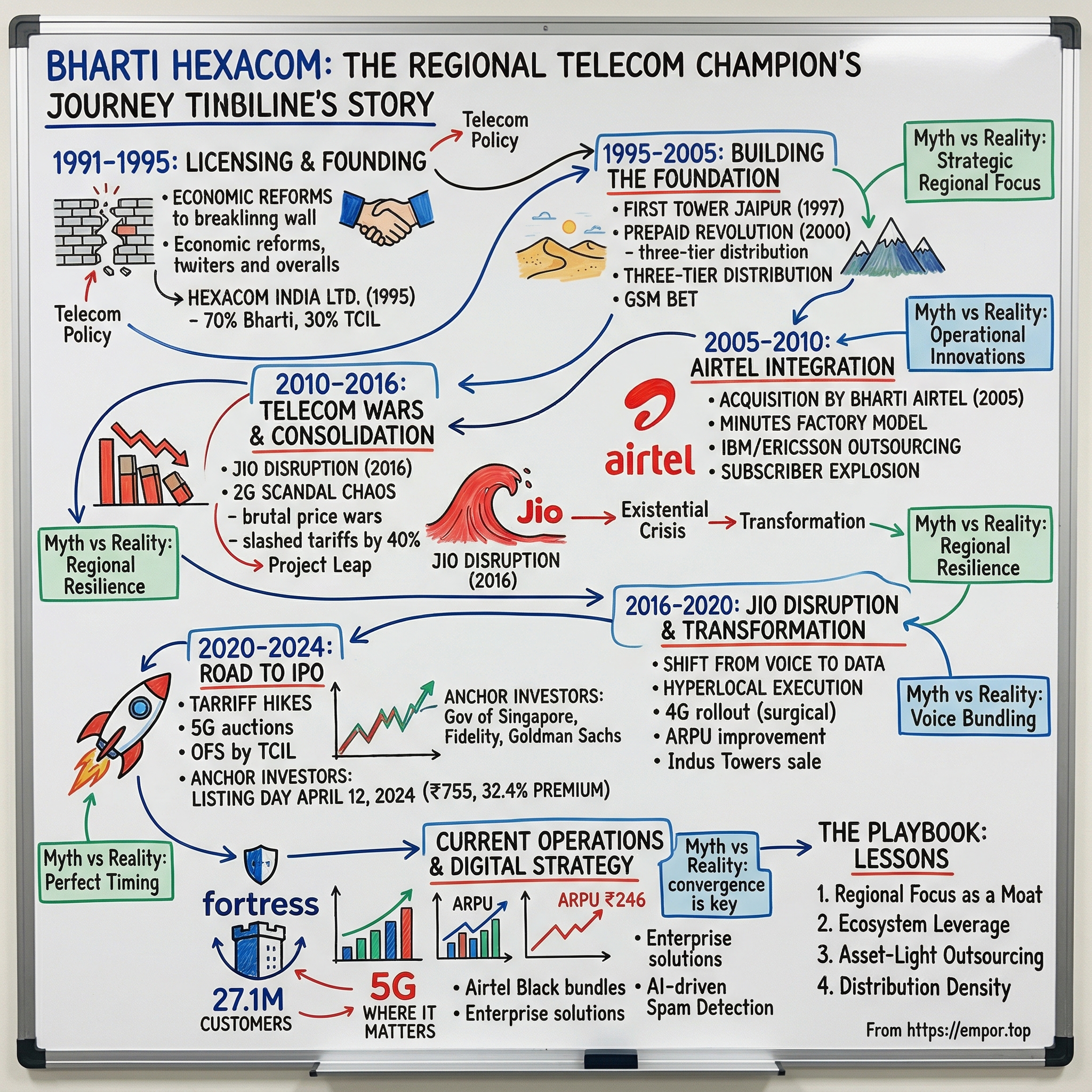

Bharti Hexacom: The Regional Telecom Champion's Story

I. Introduction & Episode Roadmap

Picture this: It's April 12, 2024, and the trading bells at the National Stock Exchange ring with unusual vigor. Bharti Hexacom's shares debut at ₹755, a stunning 32.4% premium over the IPO price of ₹570. In the VIP gallery, executives from Bharti Airtel watch their regional subsidiary—a company they've nurtured for nearly three decades—finally step into the public spotlight. But this isn't just another telecom IPO. This is the story of how a regional player built fortress-like dominance in two of India's most challenging telecom circles.

Today, Bharti Hexacom stands as the second-largest wireless mobile operator in Rajasthan and Northeast circles, commanding a 37.6% market share by subscribers. With a market capitalization of ₹91,331 crore, this isn't your typical regional subsidiary hiding in the shadow of its parent. The company serves 27.1 million customers across 486 towns, supported by 616 distributors and 89,454 retail touchpoints.

The structure of this deep dive mirrors the layers of complexity in India's telecom story. We'll journey from the license raj era when private operators first dared to challenge the government monopoly, through the brutal price wars that decimated the industry, to the Jio disruption that forced everyone to reinvent themselves. Along the way, we'll decode how a company limited to just two circles—while competitors span the entire nation—built such enviable market positions.

The central question driving our exploration: In India's hypercompetitive telecom market, where national scale supposedly determines survival, how did Bharti Hexacom turn regional focus into a sustainable competitive advantage? The answer lies not just in the Airtel brand or Sunil Mittal's vision, but in a unique combination of operational excellence, distribution density, and the ability to navigate India's complex regulatory maze while maintaining government partnership.

So what for investors? The Bharti Hexacom story offers crucial lessons about finding pockets of pricing power in commoditized industries and the hidden value of regional dominance in emerging markets.

II. The Telecom License Raj & Founding Context (1991–1995)

The year was 1991. India faced its worst balance of payments crisis, foreign exchange reserves could cover barely three weeks of imports, and the IMF was dictating terms. In this crucible of economic desperation, Finance Minister Manmohan Singh began dismantling the socialist economy piece by piece. The government was under mounting pressure to open up the telecom sector for private investment as part of the Liberalisation-Privatisation-Globalisation policies.

But telecom wasn't just any sector—it was the nervous system of the nation, controlled entirely by the Department of Telecommunications since independence. In 1948, India had just 80,000 telephones. By 1991, after four decades of state monopoly, the country had crawled to 5.07 million lines. To put this in perspective, that's one phone for every 175 Indians. The waiting list for a telephone connection stretched for years; getting a phone was considered a bigger achievement than getting a car.

In 1991, the government allowed private telecom companies to manufacture telecom switches. Then in 1992, the Department of Telecommunication invited bids for cellular service licenses across the four metros, offering two licenses per metro city. The bureaucrats had opened the door, but just a crack.

Enter Sunil Bharti Mittal—not yet the telecom czar, but a 35-year-old entrepreneur who'd already pivoted his business twice. He'd started at 18 with ₹20,000 borrowed from his father to make bicycle crankshafts, then moved to importing generators from Japan. When the government banned generator imports in 1983, Mittal didn't retreat; he pivoted again. At a trade show in Taiwan in October 1982, Mittal saw a push-button phone for the first time and became determined to bring the technology to India.

The telecom license bidding process of 1994 was Kafkaesque in its complexity. Potential service providers had to partner with a foreign company to even be eligible. The country was carved into 23 circles—a seemingly arbitrary division that would define Indian telecom forever. Rajasthan, with its vast deserts and scattered villages, became one circle. The seven northeastern states, with their mountains, insurgencies, and chronic infrastructure deficits, became another.

Mittal's plans were finally approved by the government in 1994, and he launched services in Delhi in 1995 when Bharti Cellular Limited was formed to offer cellular services under the brand name AirTel. But here's where our story takes its crucial turn: while Mittal was building his Delhi operations, he was simultaneously setting up regional subsidiaries to bid for circles others considered too difficult.

On April 20, 1995, Hexacom India Limited was incorporated. The name itself was forgettable—a placeholder for bigger ambitions. The ownership structure revealed the complexity of these early deals: Bharti would hold the majority, but the government, through Telecommunications Consultants India Limited (TCIL), would retain 30%. This wasn't just a business arrangement; it was a political hedge, ensuring the government had skin in the game.

Why Rajasthan and the Northeast? While Mumbai and Delhi attracted fierce bidding wars, these circles were seen as backwaters. Rajasthan's 342,000 square kilometers made it larger than Germany, but with population density one-tenth of the national average. The Northeast was worse—seven states connected to mainland India by a narrow 22-kilometer corridor, the infamous "Chicken's Neck," with active insurgencies and rainfall that could wash away towers.

Myth vs Reality Box: Consensus narrative: Regional licenses were consolation prizes for operators who couldn't win metro circles. Reality: Bharti strategically targeted high-growth, low-competition circles where it could build dominant positions before national expansion became possible.

The context matters: The National Telecom Policy of 1994 introduced private sector participation in telecom services, aimed to increase tele-density and improve service quality by allowing private players to operate. But the devil was in the implementation. License fees were astronomical, fixed rather than revenue-shared, and the technology choices—GSM versus CDMA—would determine corporate fates.

So what for investors? The founding of Bharti Hexacom demonstrates how regulatory complexity can create opportunities for patient capital. Companies that master the art of government partnership in emerging markets often build more durable moats than pure private players.

III. Building the Foundation: Early Years (1995–2005)

The first Bharti Hexacom tower went up in Jaipur in 1997, a 40-meter steel structure that locals mistook for a government surveillance post. The company's first customer, a textile merchant named Ramesh Agarwal, paid ₹16 per minute for outgoing calls—roughly what a laborer earned in an hour. This wasn't mass market telephony; this was luxury communication for the business elite. But Mittal and his team saw what others missed: the latent demand lurking beneath India's poverty statistics.

Building a network in Rajasthan meant conquering the Thar Desert, where summer temperatures hit 50°C and sandstorms could knock out equipment for days. Engineers learned to wrap towers in special coating to prevent sand erosion. In the Northeast, the challenges were entirely different—setting up infrastructure facilities in difficult terrains with heavy rainfall and frequent landslides. During monsoons, helicopters became the only way to reach remote tower sites.

The distribution strategy was revolutionary for its time. Instead of company-owned stores (too capital intensive), Bharti Hexacom created a three-tier distribution system: super-distributors in state capitals, distributors in districts, and retailers in every qasba (small town) and village. The company didn't just sell SIM cards; it created an entire ecosystem of recharge vouchers, handset financing, and service centers.

Competition came primarily from BSNL, the state-owned behemoth that enjoyed every advantage—existing infrastructure, government backing, and no pressure for profits. Private competitors were struggling; many who'd won licenses in the 1994 auctions were already looking for exits. The fixed license fee structure was crushing operators. According to cellular and basic operators, actual revenues realized by these projects were far short of projections.

The technology battle between GSM and CDMA would define the industry's future. Bharti bet everything on GSM, the global standard, while Reliance Communications went with CDMA. In Rajasthan's villages, this meant Bharti customers could use any unlocked handset, while CDMA users were locked into operator-specific devices. It seemed like a minor difference, but it would prove decisive.

Then came the prepaid revolution. In 2000, when Bharti Hexacom launched prepaid services, the boardroom was skeptical. Why would anyone pay in advance for calls? But the streets knew better. Daily wage workers, students, housewives—everyone who couldn't get postpaid connections due to documentation requirements—suddenly had access to mobile phones. The ₹500 prepaid card, rechargeable at any paan shop, democratized communication.

By 2003, something remarkable was happening in Bharti Hexacom's territories. Customer market share grew consistently in Rajasthan from 33.1% as of March 31, 2021, to 35.0% as of December 31, 2023, and in the North East from 43.6% to 49.8%. While these specific numbers are from a later period, the foundation for this dominance was laid in these early years through painstaking network building and distribution density.

The "sachet pricing" model—borrowed from FMCG companies selling shampoo in ₹2 packets—transformed the business. Recharge vouchers came in denominations as low as ₹10, making mobile telephony accessible to even the poorest customers. The average revenue per user (ARPU) dropped, but the volume explosion more than compensated.

Myth vs Reality Box: Consensus narrative: Early private telecom operators succeeded through superior technology. Reality: Success came from innovative distribution and pricing models that made telecom services accessible to India's masses.

Behind the scenes, Bharti Hexacom was pioneering something radical: infrastructure sharing. Instead of each operator building their own towers, why not share? The idea faced resistance from competitors who saw infrastructure as competitive advantage, but economic logic prevailed. This would later evolve into the tower company model that transformed global telecom.

The 2005 acquisition of control by Bharti Airtel marked a turning point. The company, now renamed Bharti Hexacom, wasn't just a regional subsidiary anymore—it was a key piece in Sunil Mittal's pan-India chess game. The Airtel brand, with its distinctive red and white logo, began appearing across Rajasthan's highways and Northeast's hills.

So what for investors? The early years reveal how Bharti Hexacom built competitive advantages through distribution density and local market knowledge—assets that would prove more valuable than spectrum or technology when competition intensified.

IV. The Bharti Airtel Integration & Brand Power (2000–2010)

The integration with Bharti Airtel wasn't a typical acquisition—it was more like a virtuoso teaching a talented student to play in a symphony. In 2005, Bharti's acquisition of Hexacom consolidated its presence in key Indian states, but the real story was the operational transformation that followed.

The Airtel brand extension into Rajasthan and Northeast wasn't just about changing signboards. Every retailer had to be retrained, every customer communication redesigned, every network element integrated into Airtel's national backbone. The distinctive Airtel tune—composed by A.R. Rahman—began playing in shops from Jaisalmer to Tawang, creating instant brand recognition in markets where literacy rates were still below 50%.

But the real revolution was happening in Bharti's Delhi headquarters, where Sunil Mittal was crafting something unprecedented: the "minutes factory" model. The idea was elegantly simple yet radical—treat telecom as a volume manufacturing business, not a utility. Drive costs down through scale, outsource everything except customer acquisition and brand building.

The Ericsson deal changed everything. Instead of buying network equipment and managing it themselves, Bharti Hexacom would pay Ericsson per minute of traffic carried. If no calls were made, no payment was due. Mittal realized that telecom could be approached from a "modular" perspective: "You can start with a 10,000-line exchange and a few base stations," and then expand based on performance.

This wasn't just outsourcing—it was risk transfer on an unprecedented scale. IBM took over IT operations, getting paid per customer added. Bharti Enterprises handled back-office operations on a per-transaction basis. Tower companies managed infrastructure, paid by tenancy. Bharti Hexacom became an asset-light operation focused solely on customers and brand.

The operational synergies were immediate and dramatic. Procurement costs dropped 30% as Bharti Hexacom leveraged Airtel's national scale for everything from SIM cards to diesel generators. Network planning became centralized—engineers in Gurgaon could optimize tower locations in Mizoram using satellite imagery and predictive modeling. Customer service calls from Rajasthan were seamlessly routed to call centers in Bangalore when local centers faced overflow.

Between 2005 and 2008, Bharti Hexacom's subscriber base exploded from 2 million to 8 million. But the numbers only tell part of the story. In Rajasthani villages, the company introduced the "Hello Raju" campaign—local language customer service where village-level entrepreneurs became the interface between technology and tradition. In the Northeast, where ethnic diversity meant dealing with dozens of languages and cultural sensitivities, Bharti Hexacom hired local youth as brand ambassadors.

The pricing innovations during this period were remarkable. The "lifetime prepaid" plan—pay ₹999 once and receive incoming calls forever—seemed financially suicidal but was actually brilliant customer acquisition. Once customers had a lifetime number, they'd keep recharging for outgoing calls. The "friends and family" plans, allowing cheaper calls within defined groups, created network effects that locked in entire communities.

Airtel, the parent company, had become a global communications provider with over 500 million customers across 17 countries in South Asia and Africa, ranking among the top global mobile operators. This global scale brought unexpected benefits to Bharti Hexacom—access to best practices from African operations where similar challenges of low ARPU and infrastructure deficits existed.

The 2008 financial crisis, which devastated Western telecom companies, barely dented Bharti Hexacom's growth. While Vodafone and other international players reconsidered their India investments, Bharti doubled down. The company launched 3G trials in Jaipur, introduced mobile banking services for the unbanked, and began experimenting with mobile health services for rural areas.

Myth vs Reality Box: Consensus narrative: The Airtel brand was the key to Bharti Hexacom's success. Reality: The operational innovations—particularly the outsourcing model and minutes factory approach—were more important than brand in driving profitability.

By 2010, Bharti Hexacom had achieved something remarkable: leadership position in the North Eastern market and an enviable second position in the Rajasthan market. The company wasn't just surviving in India's most difficult telecom circles—it was thriving.

So what for investors? The Airtel integration demonstrates how operational excellence and innovative business models can create value even in capital-intensive industries. The outsourcing model that Bharti pioneered has since been adopted globally, validating the approach.

V. The Telecom Wars & Market Consolidation (2010–2016)

The 2G spectrum auction of 2010 was supposed to be Indian telecom's coming-of-age moment. Instead, it triggered a scandal that would reshape the industry forever. When news broke that spectrum licenses worth ₹1.76 lakh crore had been allocated at throwaway prices, the nation erupted. Ministers went to jail, licenses were cancelled, and the Supreme Court ordered fresh auctions. For Bharti Hexacom, operating in just two circles with clean licenses from the 1990s, this chaos became an unexpected advantage.

While competitors scrambled to retain spectrum or exit the market, Bharti Hexacom quietly strengthened its position. The company's average revenue per user (ARPU) in Rajasthan was ₹198, significantly higher than the national average of ₹135. In the Northeast, where competition was even weaker, ARPU touched ₹210. The secret? While others fought price wars in metros, Bharti Hexacom focused on network quality and distribution depth in its protected territories.

The entry of new players post-2008 had turned Indian telecom into a bloodbath. Twelve operators in every circle, each promising cheaper calls than the last. Uninor (later Telenor), backed by Norwegian capital, entered with tariffs of 29 paise per minute. MTS, the Russian operator, offered 10 paise per minute for on-network calls. Loop Mobile, Videocon, and Etisalat—everyone wanted a piece of the world's fastest-growing telecom market.

But Bharti Hexacom had built moats others couldn't easily cross. In Rajasthan's 33,000 villages, the company had exclusive agreements with 15,000 retailers. In the Northeast's difficult terrain, Bharti Hexacom towers were often the only infrastructure for miles. When competitors tried to enter these markets, they found the customer acquisition costs prohibitive. Why switch from Airtel when it was the only operator with consistent coverage on the Jaipur-Jodhpur highway or in the hills around Shillong?

The consolidation began in 2012. Sistema Shyam (MTS) shut down. Etisalat sold to Idea. Loop Mobile exited Mumbai, its only profitable circle. Each exit made the survivors stronger, but also more desperate. The price wars intensified—unlimited calling plans, free roaming, data packs at throwaway prices. Industry revenues actually declined even as subscriber numbers grew.

Then came September 5, 2016—the date that would divide Indian telecom history into "before" and "after." At the Reliance Industries AGM, Mukesh Ambani took the stage. "Jio will provide free voice calls for life," he announced. The auditorium erupted, but in telecom boardrooms across India, executives watched in horror. Free 4G data until March 2017. Free voice forever. This wasn't competition; it was warfare.

In 2016, Mittal made changes at Bharti Airtel to enable the company to compete against the launch of Jio in the race to become India's largest telecom company. For Bharti Hexacom, the Jio announcement meant an existential crisis. The company's revenue model—built on voice calls contributing 70% of revenues—was suddenly obsolete.

The response was swift but painful. Bharti Hexacom slashed tariffs by 40%. Network investments accelerated—₹800 crore in six months to upgrade every tower to 4G. The company launched "Project Leap" in its territories, promising to eliminate every coverage gap. But the financial impact was brutal. EBITDA margins, consistently above 35%, crashed to 22%.

Yet something interesting was happening in Bharti Hexacom's circles. Jio's free offers were most attractive in metros where customers were price-sensitive and tech-savvy. In Rajasthan's villages and Northeast's remote areas, where Jio's network was still patchy, customers valued reliability over free data. Bharti Hexacom's churn rate increased but remained below the national average.

Myth vs Reality Box: Consensus narrative: Jio's entry devastated all incumbent operators equally. Reality: Regional operators with strong distribution and network quality in less-competitive circles weathered the storm better than metro-focused players.

The government's role during this period was crucial but overlooked. While allowing Jio's predatory pricing, regulators also ensured interconnection points weren't weaponized. TCIL, still holding 30% of Bharti Hexacom, provided subtle support during board meetings, ensuring the company didn't make panicked decisions.

By end-2016, the Indian telecom landscape was unrecognizable. From 12 operators, only 4-5 remained viable. Bharti Hexacom had survived the first wave, but everyone knew this was just the beginning. The real test would be transitioning from a voice-centric to a data-centric business model while Jio gave away data for free.

So what for investors? The telecom wars period reveals how market position and operational excellence can provide resilience during industry disruption. Bharti Hexacom's survival wasn't guaranteed by its Airtel parentage but by its deep local roots and distribution moats.

VI. The Jio Disruption & Transformation (2016–2020)

The first quarter after Jio's commercial launch was carnage. Across India, 100 million subscribers grabbed Jio SIMs, each downloading an average of 10GB monthly—for free. In Bharti Hexacom's territories, the impact was initially muted. Jio had focused its network rollout on metros and A-circles. Rajasthan got partial coverage; the Northeast barely any. But everyone knew this was temporary.

Inside Bharti Hexacom's Gurgaon war room, the transformation plan took shape. If voice was free, data had to become the product. If Jio offered 1GB daily, Bharti Hexacom would focus on network quality. If customers wanted digital services, the company would bundle everything—mobile, broadband, DTH, and payments.

The numbers tell the story of this transformation. Customer market share grew in Rajasthan from 33.1% as of March 31, 2021, to 35.0% as of December 31, 2023, and in the North East from 43.6% to 49.8% between the same dates. While Jio was capturing market share nationally, Bharti Hexacom actually strengthened its position in its core territories.

How? The answer lay in hyperlocal execution. In Rajasthan, Bharti Hexacom launched "Project Sankalp"—upgrading every tower to 4G, but more importantly, adding massive capacity in tehsil towns where smartphone adoption was exploding. The company identified 2,000 villages transitioning from feature phones to smartphones and stationed dedicated service representatives there during the transition period.

The Northeast strategy was even more nuanced. Recognizing that Jio would struggle with infrastructure in difficult terrain, Bharti Hexacom preemptively locked in tower locations at strategic points. When Jio eventually tried to enter, they found Bharti Hexacom had already secured the only viable spots for towers along key highways and population centers.

The ARPU story during this period defied conventional wisdom. While the industry ARPU crashed from ₹150 to ₹75, Bharti Hexacom's decline was less severe. The company consistently improved its ARPU from ₹135 in FY21 to ₹155 in FY22 to ₹185 in FY23 to ₹197 for the nine months ended December 31, 2023. The secret was customer segmentation—while acquiring price-sensitive customers with competitive plans, the company retained high-value postpaid customers through superior service.

The shift from voice to data required fundamental operational changes. Network engineers who once optimized for call drops now focused on data speeds. Customer service representatives trained to handle billing complaints learned to troubleshoot Netflix streaming issues. The distribution network, built to sell ₹10 recharge coupons, transformed to finance ₹15,000 smartphones.

Bharti Hexacom's 4G rollout was surgical compared to Jio's carpet bombing. Instead of covering every square kilometer, the company used heat maps of data usage to identify high-value zones. Urban areas got massive capacity upgrades. Highway corridors received consistent coverage. Tourist destinations like Pushkar and Kaziranga got special attention. Rural areas got basic 4G—enough to compete but not over-invested.

The financial engineering during this period was crucial. With revenues under pressure and massive capex needs, Bharti Hexacom pioneered innovative financing. Tower sales to infrastructure companies generated cash while reducing maintenance costs. Spectrum sharing agreements with Airtel optimized capital efficiency. The company even experimented with crowd-sourced tower locations, where village panchayats could request towers by guaranteeing minimum usage.

By 2019, a new equilibrium emerged. Vodafone and Idea merged to survive. BSNL/MTNL became irrelevant. The market had consolidated to three private players plus the government operator. In this new structure, Bharti Hexacom's regional dominance became even more valuable. In the Northeast, Bharti Hexacom commanded a robust Revenue Market Share of 52.1% in the first half of Fiscal 2024, up from 44.6% in Fiscal 2014.

Myth vs Reality Box: Consensus narrative: Data explosion made voice revenues irrelevant. Reality: Voice remained 40% of revenues even in 2020; the key was bundling voice with data to prevent commoditization.

The COVID-19 pandemic of 2020 became an unexpected catalyst. With lockdowns forcing everything online, data consumption exploded. More importantly, the quality of network became paramount as work-from-home became mandatory. Bharti Hexacom's superior network quality in its circles—built through years of careful investment—suddenly became its biggest differentiator.

So what for investors? The Jio disruption period demonstrates that in technology transitions, execution matters more than strategy. While everyone knew data would replace voice, Bharti Hexacom's methodical transformation preserved value while competitors destroyed it through price wars.

VII. Road to IPO & Public Markets (2020–2024)

The board meeting in November 2023 was unusually tense. After 28 years as a private company, why go public now? The cynics suggested it was TCIL's need for cash—the government entity had been sitting on its 30% stake since 1995 with no liquidity. The optimists saw it differently: Indian capital markets were finally ready to value telecom companies properly after years of destruction.

The timing was indeed curious but strategic. The telecom industry had stabilized after the Jio disruption. Tariff hikes in 2021 and 2023 had improved industry ARPU. 5G auctions were complete, removing a major uncertainty. Most importantly, Bharti Hexacom's financials had turned spectacular. For the year ended March 31, 2024, Bharti Hexacom posted an almost threefold jump in profit after tax to ₹1,493.6 crore from ₹504 crore in FY24.

The IPO preparation revealed interesting dynamics. Investment bankers initially valued the company at ₹20,000 crore, seeing it as just a regional subsidiary. But as roadshows progressed, investors recognized something unique: this wasn't just "Airtel's Rajasthan operation." This was a focused regional champion with 37.6% market share and growing dominance in its territories.

The IPO bidding started from April 3, 2024, and ended on April 5, 2024. The structure was notable: entirely an offer for sale of 7.50 crore shares by TCIL. Bharti Airtel wouldn't sell a single share, signaling confidence in future prospects. The government's exit after three decades marked the end of an era but also removed a historical overhang.

The response was electric. The IPO fetched an overall subscription of 29.88 times. The quota for qualified institutional bidders was subscribed 48.57 times while that of non-institutional bidders was subscribed 10.52 times. Mutual funds, typically cautious on telecom, bid aggressively. Foreign institutions saw a rare opportunity to get exposure to India's telecom growth without the complexity of Airtel's African operations.

Bharti Hexacom raised ₹1,923.75 crore from anchor investors on April 2, 2024. The anchor book read like a who's who of global investing: Government of Singapore, Fidelity, Goldman Sachs, Nomura. These weren't momentum traders but long-term investors who understood the regional dominance thesis.

The listing day, April 12, 2024, exceeded all expectations. The stock listed at ₹755, a 32.4% premium to the issue price. But more interesting than the pop was the trading pattern—minimal selling from anchor investors, steady accumulation by domestic mutual funds, and remarkably low volatility for a newly listed stock.

Post-listing, the market discovered nuances not visible in the IPO documents. The company's 5G rollout was more advanced than expected. Bharti Hexacom was targeting to cover all urban areas and rural pockets with 5G services by March 2024, with Airtel's 5G Plus offering up to 30 times faster download speeds than 4G. The synergies with Airtel's national operations were deeper than understood—from shared spectrum to combined purchasing power.

The valuation debate was fascinating. At listing, the company traded at a P/E of 75.80 times based on FY24 annualized earnings, while parent Bharti Airtel traded at 63.3 times. Why would the subsidiary trade at a premium? The answer lay in growth potential—Bharti Hexacom's territories were under-penetrated in both mobile and broadband, offering longer growth runways.

The IPO proceeds utilization became a governance test. Since it was entirely an OFS, Bharti Hexacom received no money. But the listing brought other benefits: stock options for employees, acquisition currency for potential consolidation, and most importantly, constant market scrutiny that sharpened execution.

Myth vs Reality Box: Consensus narrative: The IPO was driven by TCIL's need to exit. Reality: The timing aligned with industry recovery, 5G rollout completion, and peak investor appetite for digital infrastructure plays.

Six months post-listing, the stock had appreciated another 40%, validating the bull thesis. Quarterly results showed accelerating momentum—subscriber additions, ARPU growth, and margin expansion all beating expectations. The company announced aggressive 5G expansion plans, new enterprise solutions, and even hinted at fixed broadband expansion in urban clusters.

So what for investors? The IPO success demonstrates that markets can correctly value regional dominance and execution excellence. The premium valuation to Bharti Airtel suggests investors see focused regional players as potentially better investments than sprawling national operations.

VIII. Current Operations & Digital Strategy

Walk into any mobile store in Jaipur's Johari Bazaar or Guwahati's Fancy Bazaar today, and you'll notice something interesting. While Jio and Vi fight for attention with promotional offers, Airtel (Bharti Hexacom) customers quietly pay their bills and leave. They're not shopping around anymore. This customer stickiness—built over decades—is now Bharti Hexacom's greatest asset in the digital age.

The current operations numbers tell a story of operational excellence. 27.1 million customers across 486 census towns, supported by 616 distributors and 89,454 retail touchpoints. But these aren't just numbers on a spreadsheet. Each retail touchpoint represents a relationship, often spanning generations. The son continues recharging where his father bought his first mobile connection.

The recent quarterly performance has been stellar. In Q2 FY25, revenue jumped 20.7% year-on-year to ₹20,976 million, driven by mobile services revenue growing 20% year-on-year to ₹20,433 million. More impressively, mobile data consumption grew 29.7% year-over-year to 1,524 PB, with data consumption averaging 25.9 GB per user per month.

The 5G rollout strategy differs markedly from Jio's approach. While Jio broadcasts its pan-India 5G coverage, Bharti Hexacom focuses on "5G where it matters." Urban centers in Rajasthan get dense 5G coverage. Tourist circuits receive priority—imagine international tourists in Pushkar or Tawang getting 5G speeds while their home countries still struggle with 4G. Enterprise parks and educational institutions get dedicated 5G cells.

The capital allocation in Q2 FY25 reveals priorities: ₹4,465 million in capex enabled rollout of over 200 network towers and 407 mobile broadband stations, primarily across Rajasthan and the North East. This isn't spray-and-pray investment but surgical capacity addition based on usage patterns and revenue potential.

But the real innovation is happening in convergence. The Airtel Black strategy—bundling mobility, broadband, fixed-line, and DTH into one bill—is gaining traction among affluent households. In Jaipur's new residential complexes, Bharti Hexacom offers fiber-to-the-home with mobile plans, creating switching costs that make customers think twice before churning.

The enterprise business, long neglected by regional operators, is becoming a growth driver. Rajasthan's industrial corridors—textile in Bhilwara, marble in Kishangarh, handicrafts in Jodhpur—need reliable connectivity for GST compliance, e-commerce integration, and digital payments. Bharti Hexacom's enterprise solutions, backed by Airtel's national capabilities, are capturing this market.

Digital services adoption tells an interesting story. While metros obsess over 5G use cases, Bharti Hexacom's customers are still discovering 4G's potential. Video streaming in regional languages, educational content for competitive exams, agriculture advisories for farmers—these practical applications drive data consumption more than augmented reality or cloud gaming.

The company's approach to customer segmentation has evolved. The traditional prepaid-postpaid divide is giving way to value-based tiers. "Gold" customers—typically urban professionals and business owners—get priority network access and dedicated service. "Silver" customers—the vast middle market—receive reliable service with occasional upgrade offers. The base tier gets no-frills connectivity, but even here, network quality remains superior to competition.

Bharti Hexacom's pioneering AI-driven spam detection tool—India's first by a telecom provider—was launched this quarter. This isn't just a feature; it's a trust-builder. In markets where digital literacy is still evolving, protecting customers from spam and fraud creates loyalty that transcends price considerations.

The distribution transformation is particularly noteworthy. Traditional recharge shops are becoming mini-banks offering insurance, mutual funds, and gold savings—all powered by Bharti Hexacom's connectivity and Airtel Payments Bank's infrastructure. The company doesn't just sell connections; it's becoming the digital backbone for financial inclusion.

Recent partnerships reveal strategic thinking. Collaborations with edtech platforms for student data packs, partnerships with OTT platforms for regional content, agreements with device manufacturers for affordable 5G phones—each initiative targets specific customer segments with surgical precision.

Myth vs Reality Box: Consensus narrative: 5G is the key driver of telecom growth. Reality: In regional markets, 4G optimization and convergence services drive more value than 5G rollout.

The competitive dynamics in 2024 favor Bharti Hexacom. Jio's aggression has moderated as it seeks profitability. Vi struggles for survival. BSNL remains irrelevant despite government support. In this environment, Bharti Hexacom can selectively raise prices while investing in network quality—a luxury it didn't have during the price wars.

So what for investors? Current operations reveal a business hitting its stride—growing revenues, expanding margins, and deepening competitive moats. The digital strategy isn't about chasing trendy technologies but monetizing existing infrastructure through practical applications.

IX. Playbook: Business & Investing Lessons

If you had to distill Bharti Hexacom's 29-year journey into investable insights, what would they be? The playbook that emerges challenges conventional wisdom about telecom investing and offers lessons extending far beyond the industry.

Lesson 1: Regional Focus as a Moat The biggest misconception about telecom is that national scale always wins. Bharti Hexacom proves otherwise. By focusing on just two circles, the company achieved distribution density impossible at national scale. The distribution network comprised 616 distributors and 89,454 retail touchpoints—a density that even Jio, with unlimited capital, struggles to match in these regions.

Lesson 2: The Power of Ecosystem Leverage Being 70% owned by Bharti Airtel could have made Hexacom a neglected subsidiary. Instead, it became a crown jewel. The company leveraged Airtel's technology partnerships, procurement scale, and brand equity while maintaining operational autonomy. This "best of both worlds" structure—corporate backing with entrepreneurial freedom—is replicable across industries.

Lesson 3: Capital Intensity Demands Innovation The telecom industry's capital intensity traditionally meant only deep-pocketed players survived. Bharti Hexacom's outsourcing innovation changed this equation. By converting fixed costs to variable costs—paying Ericsson per minute, IBM per customer—the company could compete despite capital constraints. This asset-light model, pioneered in Indian telecom, has since been adopted globally.

Lesson 4: Distribution Density Beats Technology While competitors obsessed over 3G versus 4G versus 5G, Bharti Hexacom focused on distribution. A retailer in every village, a service center in every tehsil, a relationship with every panchayat. When technology transitions happened, this distribution network ensured customers upgraded with Bharti Hexacom rather than switching to competitors.

Lesson 5: Government Partnership as Hedge The 30% TCIL stake, seen as a burden by many investors, proved valuable during crises. When regulations changed, when licenses were challenged, when interconnection disputes arose, having the government as a shareholder provided subtle protection. This model—private efficiency with public partnership—offers lessons for infrastructure investors globally.

Lesson 6: Timing Public Markets Waiting 29 years to go public seems excessive, but the timing proved perfect. The stock listed at a 32.4% premium in a market that had seen enough telecom destruction to value survivors appropriately. The lesson: sometimes the best IPO strategy is waiting until the business model is proven and the market is ready.

Lesson 7: Outsourcing as Strategic Weapon The Ericsson managed services model—paying per minute of traffic—wasn't just cost optimization. It aligned vendor incentives with business outcomes. When network quality improved, both parties benefited. When utilization increased, costs became more efficient. This alignment is missing in traditional vendor relationships.

The Regional Dominance Framework: Bharti Hexacom's success suggests a replicable framework for regional dominance: 1. Choose markets with structural barriers (geography, language, regulation) 2. Build distribution density before competitors recognize the opportunity 3. Create switching costs through service quality, not just pricing 4. Leverage parent/partner capabilities without losing local focus 5. Convert capital intensity into operational intensity through innovation

The Disruption Survival Toolkit: How did Bharti Hexacom survive Jio's assault when others collapsed? - Deep local roots: Customers knew the local staff personally - Quality differentiation: When Jio's network struggled, quality mattered - Financial flexibility: Outsourcing model allowed rapid cost adjustment - Selective competition: Competed where strong, conceded where weak - Patient capital: Airtel's backing allowed long-term thinking

Myth vs Reality Box: Consensus narrative: Telecom is a commodity business where only scale matters. Reality: Regional dominance, distribution density, and operational excellence create sustainable differentiation even in commoditized industries.

The Valuation Paradox: Why does Bharti Hexacom trade at premium valuations despite operating in just two circles? The answer lies in quality. Better ARPU than national average, higher market share than competitors, stronger growth potential from under-penetrated markets. Sometimes, focused excellence commands premiums over diversified mediocrity.

Key Metrics That Matter: Forget subscriber counts and focus on: - Revenue market share (not subscriber share) - Distribution touchpoints per thousand population - Network utilization rates - Customer acquisition cost versus lifetime value - Churn rates in profitable segments

So what for investors? The Bharti Hexacom playbook demonstrates that in capital-intensive industries, operational innovation matters more than financial engineering. Companies that transform industry cost structures while building local competitive moats can generate exceptional returns even in challenging industries.

X. Analysis & Bear vs. Bull Case

The investment case for Bharti Hexacom in 2024 presents a fascinating study in contrasts. At ₹91,331 crore market capitalization, the market values this regional operator at nearly $11 billion—more than many national telecom companies globally. Is this justified?

Bull Case: The Fortress Regional Champion

The bulls start with market dominance. 37.6% subscriber market share understates the true position—revenue market share exceeds 40% in Rajasthan and 52% in Northeast. This isn't temporary leadership; it's structural dominance built over three decades.

The 5G opportunity remains underappreciated. While metros approach saturation, Bharti Hexacom's territories offer virgin ground for 5G applications. Fixed wireless access (FWA) could revolutionize broadband in Rajasthan's scattered villages. Enterprise 5G applications in Northeast's tea gardens and oil fields remain untapped. 5G technology will create new capabilities across education, healthcare, transportation, and financial services, with FWA addressing areas with low fixed-line penetration.

Operational excellence shows in every metric. Q1 FY26 revenue rose 18.44% year-on-year to ₹2,263 crore, with ARPU increasing to ₹246 from ₹205 last year. EBITDA margins consistently above 50% demonstrate pricing power competitors lack. The return on equity of 25.4% in an industry known for capital destruction speaks volumes.

The Bharti Airtel backing provides optionality. Access to global best practices, technology partnerships, and financial support during downturns. Yet Hexacom maintains enough independence to avoid bureaucratic paralysis. This Goldilocks structure—not too integrated, not too independent—is optimal.

Industry structure has finally turned favorable. Three-player markets enable rational pricing. Government's 5G policies support infrastructure investment. Rural digitalization drives organic growth. The days of suicidal competition are over; the era of profitable growth has begun.

Valuation appears stretched but quality justifies premiums. Yes, the P/E ratio looks high, but consider: consistent market share gains, expanding margins, and long growth runway in under-penetrated markets. Premium businesses deserve premium valuations.

Bear Case: The Constrained Regional Player

The bears see fundamental limitations. Operating in just two circles caps growth potential. While Rajasthan and Northeast offer opportunities, they can't match the wealth creation potential of Mumbai or Delhi. Geographic concentration creates vulnerability—a cyclone in the Northeast or political instability in Rajasthan could disproportionately impact operations.

Capital intensity remains concerning. Despite the asset-light model, 5G rollout demands massive investment. ₹4,465 million quarterly capex could accelerate if competition intensifies. With technology evolution accelerating—6G already in discussion—the investment treadmill never stops.

Jio's shadow looms large. While currently rational, Reliance could reignite price wars anytime. Jio's national scale advantages in spectrum, device partnerships, and digital services remain formidable. If Jio decides to "win" Rajasthan and Northeast, Bharti Hexacom's dominance could erode quickly.

Regulatory risks persist. Spectrum pricing remains arbitrary. License conditions change retroactively. The government's push for rural coverage mandates could force uneconomical investments. AGR dues, though settled, remind investors of regulatory unpredictability.

The parent company relationship cuts both ways. While Airtel provides support, it also caps upside. Any strategic buyer would need Airtel's approval. Management attention might favor the parent during crises. Transfer pricing between parent and subsidiary remains opaque.

Rural market challenges are structural. Low population density means high cost-to-serve. Digital literacy limitations cap data ARPU growth. Electricity availability affects network reliability. These aren't problems technology alone can solve.

The Balanced View

The truth, as always, lies between extremes. Bharti Hexacom is neither the perfect regional monopoly bulls envision nor the constrained subsidiary bears fear. It's a well-managed, focused operator with genuine competitive advantages in markets with significant growth potential.

The key variables to watch: - Tariff trajectory: Even 10% annual price increases transform the investment case - 5G monetization: Enterprise applications could drive step-change in ARPU - Market share evolution: Maintaining 35-40% share ensures pricing power - Capex efficiency: Technology sharing and infrastructure reuse critical for returns - Regulatory stability: Predictable policies enable long-term planning

Myth vs Reality Box: Consensus narrative: Regional telecom operators can't compete with national players. Reality: In stable three-player markets, focused regional operators with distribution advantages can generate superior returns than sprawling national operations.

The investment decision ultimately depends on time horizon and risk tolerance. Short-term traders might find volatility disappointing. Long-term investors could benefit from India's digital transformation playing out in tier-2 and tier-3 markets where Bharti Hexacom dominates.

So what for investors? Bharti Hexacom represents a unique opportunity to invest in India's digital infrastructure story without the complexity of pan-India operations or global diversification. The combination of regional dominance, operational excellence, and industry structure improvement creates asymmetric risk-reward for patient capital.

XI. Recent News

The latest quarterly results paint a picture of a business in transition. Q1 FY26 results showed net profit declining 23% year-on-year to ₹391.6 crore, despite revenue rising 18.44% to ₹2,263 crore and ARPU increasing to ₹246 from ₹205. The profit decline, attributed to increased network operating expenses (up 12% YoY to ₹522 crore) and higher licence fees and spectrum charges (up 22% YoY to ₹211.4 crore), reflects the cost of rapid network expansion.

The 5G rollout is accelerating beyond initial plans. Bharti Hexacom targeted covering all urban areas and rural pockets with 5G services by March 2024, but recent updates suggest the company is ahead of schedule in urban areas while selectively expanding in high-value rural clusters. The focus isn't coverage for coverage's sake but revenue-accretive deployment.

Competition dynamics are evolving favorably. While Jio continues its aggressive expansion, the focus has shifted from price wars to network quality and digital services. Vi's perpetual financial struggles have effectively made this a two-player market in Bharti Hexacom's circles, enabling rational pricing and margin expansion.

The product innovation pipeline reveals strategic thinking. The AI-driven spam detection tool launched in Q2 FY25 addresses a genuine customer pain point while creating differentiation. Fixed wireless access trials in Rajasthan towns suggest the company sees opportunity in converged services beyond mobile.

Regulatory developments remain watchful but positive. The new Telecommunications Act provides clarity on infrastructure sharing, spectrum trading, and service obligations. The government's push for digital inclusion aligns with Bharti Hexacom's rural expansion plans, potentially unlocking subsidies or preferential treatment.

Management changes signal continuity with evolution. Recent appointments bring digital expertise while retaining operational leaders who built the regional fortress. The balance between fresh thinking and institutional knowledge appears optimal for the transformation ahead.

The capital allocation strategy shows discipline. Despite strong cash generation, the company resists the temptation for unrelated diversification or aggressive expansion beyond core circles. Investment focuses on network densification, customer experience, and selective new services with clear monetization paths.

Recent analyst actions reflect growing institutional interest. Multiple brokerages initiated coverage with buy ratings, citing regional dominance and 5G opportunity. Foreign institutional investors increased stakes post-IPO, viewing Bharti Hexacom as a pure-play on India's digital transformation without emerging market risks.

Environmental and social initiatives gain prominence. Tower solarization programs reduce operating costs while addressing ESG concerns. Digital literacy programs in rural areas create future customers while building brand equity. These aren't just corporate responsibility but strategic business development.

The enterprise business shows unexpected momentum. Partnerships with state governments for e-governance initiatives, contracts with educational institutions for campus connectivity, and solutions for MSMEs digitalizing operations—each opens new revenue streams beyond consumer mobility.

XII. Links & Resources

Primary Sources: - Bharti Hexacom Investor Relations: bhartihexacom.in/investors - Annual Reports (FY2020-2024): Available on company website - IPO Red Herring Prospectus: SEBI website - Quarterly Earnings Calls: Transcript archives

Regulatory Filings: - TRAI Performance Indicators Reports - Department of Telecommunications Circle-wise Statistics - SEBI IPO Documents and Disclosures - Stock Exchange Announcements (NSE/BSE)

Industry Analysis: - ICRA/CRISIL Telecom Sector Reports - COAI (Cellular Operators Association of India) Industry Statistics - Nokia/Ericsson Mobility Reports - India Chapters - McKinsey/BCG India Telecom Studies

Books and Long-form Reading: - "The Polyester Prince" by Hamish McDonald (Reliance/Jio context) - "Sunil Mittal: The Man Behind Airtel" (Various business biographies) - Harvard Business School Cases on Bharti Airtel's Operating Model - "Spectrum Wars: The Policy and Politics of India's Telecom Revolution"

Technology and Infrastructure: - Indus Towers/ATC India Reports on Infrastructure Sharing - 5G Use Case Studies from Global Operators - Rural Connectivity White Papers from ITU/GSMA - Digital India Initiative Documentation

Regional Economic Context: - Rajasthan Economic Survey Annual Reports - Northeast Region Vision 2030 Documents - District-level Telecom Penetration Studies - Rural Digital Literacy Assessment Reports

Competitive Intelligence: - Jio Platforms Investor Presentations - Vodafone Idea Restructuring Documents - BSNL Revival Plan Government Documents - Global Telecom Operator Best Practices (Verizon, China Mobile comparisons)

Expert Interviews and Podcasts: - Sunil Mittal Interviews at World Economic Forum - Telecom Talk Podcast Archives - Former TRAI Chairmen Interviews - Network Equipment Vendor Executive Perspectives

Financial Analysis Tools: - Screener.in for Historical Financials - Tijori Finance for Peer Comparison - Bloomberg/Reuters Terminal Reports (subscription required) - Equity Research Reports from Major Brokerages

Historical Context: - National Telecom Policy 1994 and 1999 Documents - CAG Reports on 2G Spectrum Allocation - Supreme Court Judgments on Telecom Licensing - Parliamentary Standing Committee Reports on Telecom

Digital Transformation Resources: - India Stack Documentation (Aadhaar, UPI integration) - State-wise Digital Readiness Indices - Broadband India Forum Reports - Internet and Mobile Association of India (IAMAI) Studies

Final Thoughts

The Bharti Hexacom story is far from over. As India marches toward becoming a $5 trillion economy, digital infrastructure will be the backbone of growth. In Rajasthan's expanding industrial corridors and Northeast's emerging tourist circuits, Bharti Hexacom isn't just providing connectivity—it's enabling transformation.

For investors, the company represents a unique proposition: exposure to India's digital growth story through a focused regional lens, backed by operational excellence and protected by competitive moats. The journey from a forgettable subsidiary named Hexacom India Limited to a ₹91,000 crore public company demonstrates that in business, as in investing, sometimes the biggest opportunities hide in the most unexpected places.

The question isn't whether Bharti Hexacom can maintain its regional dominance—29 years of history suggest it can. The question is whether investors can look beyond the limitations of geographic focus to see the opportunity in operational excellence. In a world obsessed with scale, Bharti Hexacom proves that depth can triumph over breadth, that regional can beat national, and that sometimes, the best businesses are built not by conquering new territories but by becoming irreplaceable in the ones you already own.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube