APL Apollo Tubes: India's Steel Revolution

I. Introduction & Episode Roadmap

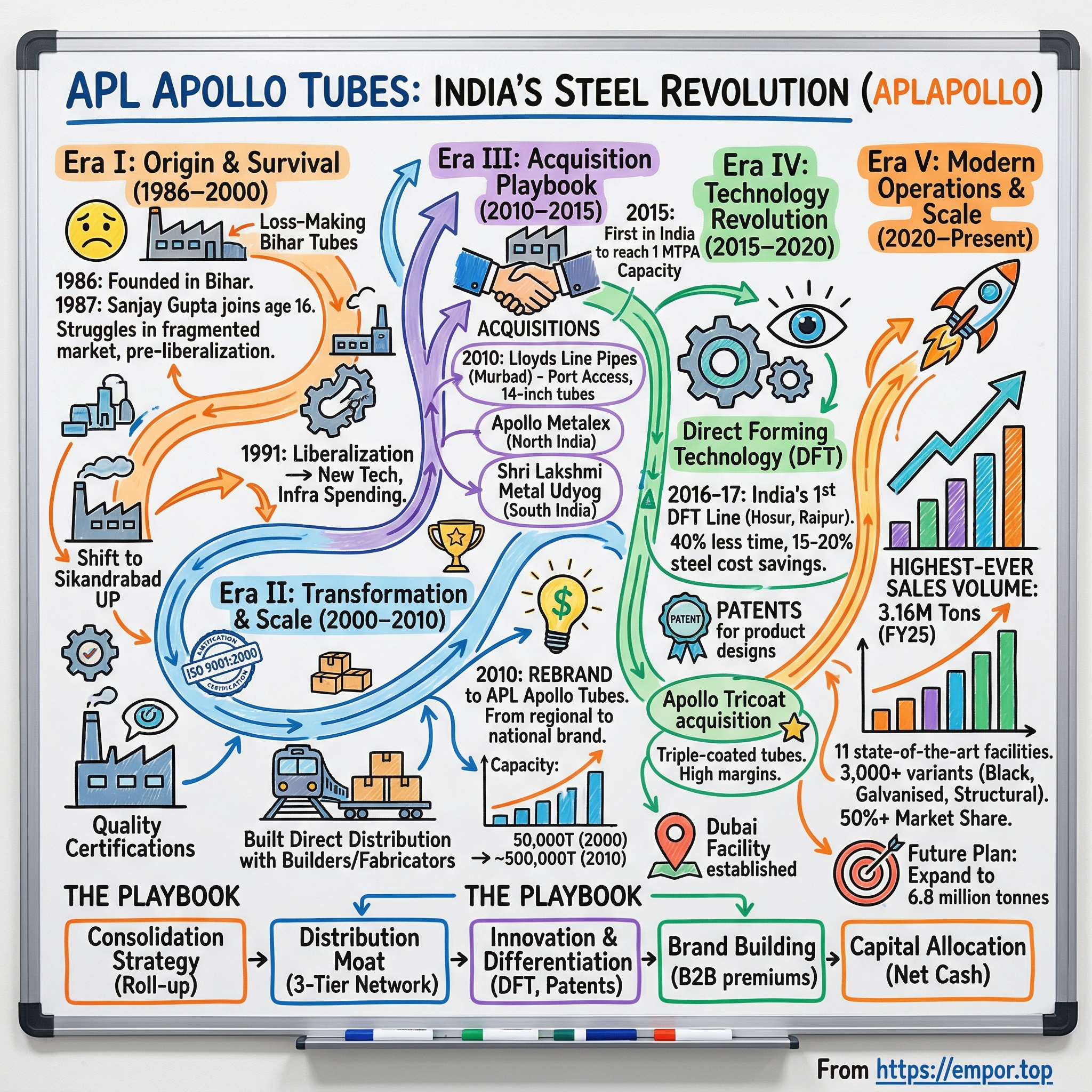

Picture this: A dusty industrial estate in Bihar, 1986. The clatter of old machinery echoes through a loss-making tube factory that most investors wouldn't touch with a ten-foot pole. Fast forward to 2024—that same company commands a ₹44,000+ crore market capitalization, dominates India's structural steel market with over 50% share, and runs ten state-of-the-art manufacturing facilities producing 1,500+ product varieties. This is the story of APL Apollo Tubes, and more importantly, the story of how Sanjay Gupta transformed his father's failing venture into India's structural steel giant.

The company today manufactures everything from the steel bones that hold up India's infrastructure to the tubes that form furniture in millions of homes. But APL Apollo isn't just another commodity player in a crowded market. It's a masterclass in turning a fragmented, unorganized sector into a branded, consolidated powerhouse. While Tata Steel and JSW duke it out in primary steel, APL Apollo quietly built a distribution moat spanning 500+ cities with 800+ dealers, introduced cutting-edge Direct Forming Technology when competitors were still using decades-old methods, and somehow convinced customers to pay premiums for branded tubes in a market that traditionally bought on price alone.

The transformation from Bihar Tubes to APL Apollo reads like a business school case study in strategic pivots. How does a company go from hemorrhaging cash in Bihar to generating ₹20,690 crore in revenue? How do you build brand loyalty in structural steel—a product most people never see once it's inside a building? And perhaps most intriguingly, how did Sanjay Gupta execute a roll-up strategy in one of India's most fragmented industries while maintaining family control and professionalizing management simultaneously?

This episode traces that journey through five distinct eras: the survival years in Bihar, the transformation decade that saw the crucial rebrand, the acquisition playbook that consolidated the market, the technology revolution that differentiated commodity products, and the current scale-up phase targeting global markets. Along the way, we'll decode the strategic decisions, examine the financial engineering, and extract the playbook that turned a regional tube manufacturer into India's structural steel champion.

II. The Origin Story: Bihar to Apollo (1986–2000)

The year is 1986, and India's economy is still years away from liberalization. In Bihar—not exactly known as India's industrial powerhouse—a small tube manufacturing company begins operations at what can generously be called a modest scale. The founder, Sanjay Gupta's father, had ventured into the steel tubes business with typical first-generation entrepreneur optimism. The reality was brutal. Bihar Tubes Limited, as it was then known, was bleeding money from day one. When young Sanjay Gupta looked at the balance sheet, the numbers told a story of defeat. The company formed by his father in Bihar was completely loss-making, hemorrhaging cash in an industry dominated by unorganized players who competed purely on price. Sanjay joined his father in 1987, as soon as he was out of school, barely 16-years-old. The confines of their plant would become college for him since he didn't pursue formal education thereafter.

Sanjay's father had shifted his pipe-trading business from Bihar to Delhi in 1986, with their main plant manufacturing GI and black pipes in Sikandrabad, in the Bulandshahr district of Uttar Pradesh. The industrial landscape of pre-liberalization India wasn't kind to small manufacturers. Steel was controlled by giants like SAIL and Tata Steel, credit was scarce, and the market for structural tubes was virtually non-existent—Indians built with concrete and rebar, not hollow steel sections.

Sanjay Gupta used to think constantly about converting the loss-making company into profit-making. This became possible only due to the confidence, courage, and conviction that Sanjay Gupta possessed. But conviction alone doesn't pay suppliers or keep machinery running. The early years were about survival, learning the trade from the shop floor up, understanding why certain tube mills in Meerut thrived while others in Bihar struggled.

"At that time, this industry was totally lala type," an unorganised industry not run professionally. But it also meant an opportunity for transformation. While competitors focused on churning out standard pipes at the lowest possible cost, young Sanjay began observing patterns—which construction sites demanded consistent quality, which dealers had the best networks, why imported tubes commanded premiums despite higher prices.

The 1991 economic liberalization changed everything. Suddenly, foreign technology was accessible, infrastructure spending increased, and a new class of builders emerged who cared about specifications and delivery schedules. Bihar Tubes pivoted from pure survival mode to strategic growth. The company began investing in quality certifications—unusual for a small tube manufacturer in the 1990s—and started building relationships with institutional buyers who valued reliability over rock-bottom prices.

By the late 1990s, the groundwork was laid. The loss-making Bihar venture had stabilized, found its niche in North India's construction boom, and most importantly, developed a vision beyond just making tubes. Sanjay's father passed away in 2002. "I had worked with him for 16 years, gaining a lot of experience". The baton passed to a 31-year-old who had spent half his life in steel plants, and the real transformation was about to begin.

III. The Transformation Years: Building Scale (2000–2010)

The morning after his father's funeral, Sanjay Gupta stood in the Sikandrabad plant watching molten steel flow through the mills. The business he inherited was profitable but pedestrian—a regional player in a fragmented market where hundreds of small manufacturers competed on price alone. His first major decision would set the tone for everything that followed: instead of mourning, he flew to Japan.

In 2002, APL partnered with a Japanese company to make pre-galvanised tubes in India. The Rs.50-million investment in technology helped them make 150 metre pipe per minute, against the earlier 20 metre pipe per minute, reducing cost and improving productivity. This wasn't just a technology upgrade—it was a philosophical shift. While Indian competitors bought second-hand European mills, Gupta invested in cutting-edge Japanese precision engineering. Between 2000–2002, the company commissioned a new tube mill and modern Galium mill, receiving ISO 9001:2000 certification—a credential that set them apart from the "lala" manufacturers still operating without formal quality systems. But certifications were just table stakes. The real game-changer came in 2003-04 when APL developed in-house hollow sections across a wide range of sizes and became the first in India to launch pre-galvanized pipes.

The period between 2007-2008 was significant as the company expanded and acquired Apollo Metalex Private Limited and Shri Lakshmi Metal Udyog Limited (Bangalore). These weren't distressed asset purchases but strategic consolidations. Apollo Metalex brought distribution strength in North India, while Shri Lakshmi provided a manufacturing foothold in the South—crucial for a business where transportation costs could kill margins.

The 2008 financial crisis that crushed global markets became APL's opportunity. While competitors pulled back, Gupta accelerated. In 2009, the company commissioned a plant in Hosur, Tamil Nadu, started a greenfield venture with state-of-the-art mills, and set up multiple warehouses across India. The Hosur facility wasn't just another plant—it was South India's largest steel tube manufacturing unit, strategically positioned to serve the booming construction markets of Bangalore, Chennai, and Hyderabad.

But perhaps the boldest move came in 2010. After 24 years as Bihar Tubes—a name that screamed commodity player from a backward state—the company rebranded as APL Apollo Tubes Limited. The name change wasn't cosmetic. It signaled a transformation from regional manufacturer to national brand, from commodity producer to value-added player, from family business to professional enterprise.

The numbers validated the strategy. From a single plant in Sikandrabad producing 50,000 tonnes annually in 2000, APL Apollo had grown to multiple facilities with combined capacity approaching 500,000 tonnes by 2010. Revenue had multiplied ten-fold. More importantly, the company had cracked the distribution code—instead of selling through traders who squeezed margins, APL built direct relationships with fabricators and builders, creating a moat that pure manufacturing couldn't match.

The transformation decade ended with APL Apollo positioned as India's largest ERW steel tube manufacturer. But Sanjay Gupta was just getting started. The next phase would involve an acquisition that would define the company's trajectory for the next decade.

IV. The Acquisition Playbook: Lloyds & Beyond (2010–2015)

The call came on a Sunday evening in 2010. Lloyds Line Pipes, a Maharashtra-based manufacturer with a prime location near Mumbai port, was hemorrhaging cash and looking for a buyer. Within 48 hours, Sanjay Gupta was walking through their Murbad facility, mentally calculating not what the company was worth today, but what it could become under APL Apollo's umbrella.

APL Apollo completed the acquisition of Lloyds Line Pipes for Rs 40 crore in an all-cash deal. For context, this was a company with facilities that could manufacture up to 14-inch tubes—a capability APL Apollo desperately needed to compete in infrastructure projects. The location near ports ensured logistics savings and opened up export markets that had been economically unviable from landlocked Sikandrabad.

The Lloyds acquisition became the template for APL Apollo's consolidation strategy. Don't just buy capacity—buy capabilities, geography, and customer relationships. Within months of the acquisition, the company modernized and enhanced capacity at the Murbad facility, transforming a loss-making unit into a profit center that strengthened total capacity from 400,000 tonnes to 490,000 tonnes per annum.

The years 2011-2012 marked a technological renaissance. APL Apollo introduced Rotary Sizing Mill (RSM) technology for the first time in India at the Hosur plant, commissioned sheet galvanizing facilities in South India, and began a modernization drive across all manufacturing locations. The company was no longer playing catch-up with global standards—it was setting them for the Indian market.

During 2013-14, APL procured CRFH coils from JSW Steel to expand the product range and launched door sections, window sections, and railing tubes. This wasn't random product proliferation. Each new SKU targeted a specific pain point in construction. Door frames, for instance, traditionally used wood or solid steel—both expensive and cumbersome. APL's hollow-section steel frames cost 50% less than wooden alternatives while offering superior durability.

By 2015, APL Apollo achieved a milestone that had seemed impossible a decade earlier: becoming the first company in India to achieve 1 MTPA capacity in steel pipes. This wasn't just about bragging rights. The million-tonne mark brought economies of scale that fundamentally changed the unit economics. Fixed costs spread across larger volumes, procurement leverage increased, and most importantly, APL Apollo could now serve pan-India demand without capacity constraints.

The distribution network had evolved into a competitive weapon. With 500+ touchpoints across India, APL Apollo wasn't just selling tubes—it was providing same-day delivery, technical support, and customization that smaller players couldn't match. The company's tagline "Desh Ki Badhti Taqat" (The Nation's Growing Strength) wasn't mere marketing—it reflected a business that had become synonymous with India's infrastructure boom.

But even as APL Apollo celebrated crossing the million-tonne mark, Sanjay Gupta was already obsessing over the next frontier. During his annual technology-scouting trips to Germany and Japan, he had discovered something that would revolutionize the Indian structural steel market: Direct Forming Technology.

V. The Technology Revolution: DFT & Innovation (2015–2020)

The German engineer at the trade show in Düsseldorf looked skeptical when Sanjay Gupta asked about implementing Direct Forming Technology in India. "Your market isn't ready for this level of sophistication," he said, pointing to the gleaming DFT machine that could produce structural steel tubes with tolerances measured in fractions of millimeters. Gupta smiled and placed the order anyway.

In 2016-17, APL Apollo established India's first-ever Direct Forming Technology line in Hosur and commissioned a greenfield facility at Raipur with DFT. While traditional tube manufacturing involved multiple steps—forming, welding, sizing—DFT accomplished everything in a single pass, reducing manufacturing time by 40% and improving structural integrity by 25%. The technology allowed APL to produce larger sections with thinner walls, saving 15-20% in steel costs while maintaining strength specifications.

The same year, APL Apollo received patents for six product designs—unusual for a company in what most considered a commodity business. These weren't incremental improvements but fundamental reimaginings of structural steel applications. The patented door frame design Gupta had been evangelizing could support the same load as traditional frames while using 40% less steel. "We are selling three million a year today. Two years back, this market didn't exist," Gupta noted. During FY 2019, APL undertook de-bottlenecking initiatives at DFT lines, leading to capacity enhancement of 1 lakh MTPA, taking DFT capacity to 6 lakh MTPA and total capacity to 2.1 million MTPA. The efficiency gains were staggering—what used to take three shifts could now be done in two, energy consumption dropped by 30%, and rejection rates fell below 1%.

The real masterstroke came through the Apollo Tricoat acquisition. In early 2018, Rahul Gupta (Sanjay's son), in his personal capacity, acquired controlling stake in Best Steel Logistics and changed its name to Apollo TriCoat. He introduced a new business of manufacturing of TriCoat Tubes in three variants – SureCoat, DuraCoat and SuperCoat, with the advanced Galvant technology. This technology and the products have been introduced for the first time in India.

In October 2018, SLMUL, a WoS (Wholly Owned Subsidiary) of APL Apollo, entered into a Share Purchase Agreement with Mr. Rahul Gupta for acquisition of 80,30,030 Equity shares of Rupees 120/- each and Options attached to 43,00,000 warrants at a price of Rupees 120/- per option of Apollo TriCoat Tubes Limited. The open offer has been made at ₹ 135 per share.

The Tricoat products weren't just incrementally better—they operated in a different universe of margins. Tricoat's products enjoy 2x of APL Apollo's operating margins. These triple-coated tubes could replace PVC electrical conduits, enter premium home improvement segments, and command prices that traditional steel tubes could never achieve.

By 2020, APL Apollo's product portfolio had exploded to 1,500+ varieties. The company wasn't just making tubes anymore—it was providing solutions. Need a steel frame that looks like wood for premium homes? APL had it. Want corrosion-resistant tubes for coastal construction? Available in three grades. Require custom sizes for architectural applications? Delivered in 48 hours.

The distribution network had evolved into a three-tier system spanning 800+ dealers and reaching 50,000+ retailers. "Half of the market for hollow section of 3 MT and GP of 1 MT today has been created by APL Apollo," industry analysts noted. The company hadn't just captured market share—it had created markets that didn't exist before.

Innovation wasn't limited to products. APL Apollo pioneered branding in a B2B commodity business. The "Apollo" brand became synonymous with quality in structural steel, allowing the company to command 5-10% premiums over unbranded competitors. Marketing campaigns targeted not just builders but architects, engineers, and even end consumers—unprecedented for a steel tube manufacturer.

As 2020 dawned, APL Apollo stood transformed. From a single-product, single-location manufacturer, it had become India's structural steel giant with 50%+ market share, technological leadership, and a brand that resonated across the construction ecosystem. But the biggest transformation was yet to come.

VI. Modern Operations & Scale (2020–Present)

The pandemic should have been a disaster for APL Apollo. Construction sites shut down, migrant workers fled cities, and steel demand collapsed 50% in April 2020. Instead, Sanjay Gupta saw opportunity where others saw catastrophe. While competitors furloughed workers and mothballed capacity, APL Apollo accelerated its automation drive, launched direct-to-consumer initiatives, and prepared for the post-COVID infrastructure boom that Gupta was certain would follow. By 2024, the transformation was complete. The company runs 10 manufacturing facilities churning out over 1,500 varieties of MS Black Pipes, Galvanised Tubes, Pre-Galvanised Tubes, Structural ERW Steel Tubes and Hollow Sections. APL Apollo manufactures multiple products with capacity to produce 4.3 MT metric tonnes per annum—a scale that would have seemed fantastical even five years earlier.

The product portfolio had evolved into three distinct segments. As of FY24, Apollo structural comprises 68% of revenues, Apollo Z contributes 28%, and Apollo Galv represents 4%. Each segment targeted different customer needs—structural for construction, Z for rust-proof applications, and Galv for agricultural and industrial uses.

The Q4FY25 numbers tell the story of dominance. APL Apollo Tubes Limited, the world's largest branded structural steel tube manufacturer, has reported its highest-ever quarterly sales volume of 850,447 tons in Q4FY25. This marks a 25% year-on-year (YoY) increase and a 3% growth quarter-on-quarter (QoQ), up from 828,200 tons in Q3FY25 and 678,556 tons in Q4FY24. For the full financial year FY25, the company recorded a total sales volume of 3,157,978 tons, registering a robust 21% YoY growth compared to 2,618,477 tons in FY24.

The granular segment performance reveals strategic execution. Heavy structural tubes grew from 71,608 tons in Q4FY24 to 81,583 tons in Q4FY25. Light segments jumped from 102,411 tons to 142,797 tons. General category expanded from 271,677 tons to 353,293 tons. The rust-proof segment reached 184,636 tons, while coated products hit 55,174 tons—each representing markets that APL Apollo had essentially created through innovation.

APL Apollo's product portfolio now includes over 3,000 structural steel tube variants used across urban infrastructure, real estate, commercial construction, greenhouses, engineering, and rural housing sectors. With 11 state-of-the-art manufacturing facilities and a total production capacity of 4.5 million tons, APL Apollo operates across key locations in India and the UAE, including Hyderabad, Sikandrabad, Raipur, Hosur, Malur, Murbad, and Umm Al Quwain.

The UAE facility represents APL Apollo's international ambitions. Established to serve Middle Eastern markets, it demonstrates the company's evolution from regional player to global aspirant. The facility doesn't just export Indian tubes—it manufactures locally to meet specific regional requirements, avoiding import duties and reducing delivery times.

The company's extensive three-tier distribution network of over 800 distributors spans more than 300 towns and cities across India, reinforcing its position as a one-stop shop for building material solutions. This network isn't just about reach—it's about relationships. Each distributor receives technical training, marketing support, and exclusive territory rights, creating aligned incentives that competitors struggle to replicate.

The digital transformation accelerated during COVID has continued. APL Apollo launched dealer apps for real-time ordering, introduced QR codes for product authentication (addressing the counterfeit problem that plagues the industry), and created virtual reality showrooms where architects can visualize structural applications. The company even started direct-to-consumer sales for home improvement products—unheard of for a B2B steel manufacturer.

As we speak, APL Apollo operates at a scale that positions it uniquely in the global structural steel market. The company that started with a single loss-making plant now runs a manufacturing empire that would take competitors decades to replicate—if they could at all.

VII. Financial Performance & Market Position

Walk into any equity research firm's conference room discussing Indian manufacturing, and APL Apollo's financials will inevitably spark debate. How does a steel tube company maintain 20%+ ROE when steel giants like Tata Steel fluctuate between 5-15%? Why does it trade at 50+ P/E when peers languish at single digits? The numbers tell a story that challenges conventional wisdom about commodity businesses. In 2024, revenue was ₹20,690 crore, an increase of 14.15% compared to the previous year's ₹18,124 crore. Earnings were ₹757 crore, an increase of 3.36%. But these headline numbers mask the real story. Consolidated net profit of ₹293 crore for Q4 ended March 31, 2025, a solid improvement from ₹171 crore reported in same quarter last year—a 72% jump that would make software companies envious.

The stock trades at P/E 54.8, Book Value ₹152, Dividend Yield 0.36%, ROCE 22.8%, ROE 19.4%. These aren't commodity company metrics—they're premium valuations that reflect APL Apollo's transformation from tube manufacturer to branded building materials provider. The market values the distribution moat, the innovation pipeline, and most importantly, the ability to generate consistent returns despite steel price volatility.

Market dominance tells another story. With 50%+ market share in structural steel tubes, APL Apollo has achieved something rare in Indian manufacturing—consolidation in a fragmented market. The next largest player has less than 10% share. This isn't accidental. Every acquisition, every new plant location, every product innovation was designed to create insurmountable scale advantages.

Capital efficiency deserves special attention. The key milestone was to achieve a net cash balance sheet as on 31 March 2024. This is after the fact that the company invested Rs 23.7bn in last 4 years in its capacity expansion program. Think about that—APL Apollo expanded capacity by 2 million tonnes while becoming net cash positive. Most steel companies leverage heavily during expansion phases.

Working capital management has become a competitive weapon. The company operates with negative working capital in many quarters—customers pay before APL Apollo pays suppliers. This is unheard of in steel manufacturing where 60-90 day credit cycles are standard. How? Brand power allows APL to demand better terms, while scale provides leverage with suppliers.

In a strategic move to boost production, the board approved a capital expenditure of Rs 1,500 crore to expand manufacturing capacity from 4.5 million tonnes to 6.8 million tonnes. This isn't just capacity addition—it's a bet on India's infrastructure super-cycle. With government spending on highways, railways, airports, and urban infrastructure accelerating, structural steel demand could double by 2030.

The comparison with steel giants reveals APL Apollo's unique positioning. Tata Steel produces 20+ million tonnes but operates in the commodity primary steel market with single-digit EBITDA margins. JSW Steel has massive scale but limited pricing power. Jindal Steel focuses on long products with volatile margins. APL Apollo, at 4.3 million tonnes capacity, generates higher returns on capital than all of them.

International investors have taken notice. FII holding has increased from 5% in 2015 to over 20% today. Marquee funds like Aberdeen, Fidelity, and Norges Bank hold significant positions. Their investment thesis: APL Apollo isn't a steel company—it's a play on India's construction boom with characteristics more similar to building materials companies like Asian Paints than commodity steel producers.

The financial resilience was tested during COVID and passed with flying colors. While revenue dipped briefly in Q1FY21, margins actually expanded as APL Apollo used the disruption to eliminate inefficient SKUs, optimize product mix toward higher-margin items, and negotiate better terms with suppliers facing demand destruction elsewhere. By Q3FY21, the company was posting record profits while competitors were still recovering.

One metric captures the transformation: In 2010, APL Apollo generated ₹2,000 EBITDA per tonne. APL Apollo Tubes demonstrated strong Q4FY25 performance with a 25% volume increase and EBITDA per ton of ₹4,864. The company aims for over 20% volume growth in FY26E, targeting ₹5,000 EBITDA per ton. That's a 2.5x improvement in unit economics—achieved not through price increases but through mix improvement, value addition, and operational excellence.

VIII. Playbook: Business & Strategic Lessons

If you gathered India's top business strategists in a room and asked them to design a playbook for consolidating a fragmented commodity market, they'd probably recreate APL Apollo's strategy—though likely without the audacity to actually execute it. The playbook reads like a masterclass in turning conventional business wisdom on its head.

The Consolidation Strategy: Roll-up in a Fragmented Market

The Indian steel tubes market in 2000 had over 500 manufacturers. By 2024, APL Apollo controls over 50% market share. This wasn't achieved through price wars or hostile takeovers but through a nuanced consolidation strategy. Each acquisition targeted specific gaps—Lloyds for port access and large-diameter capabilities, Apollo Metalex for North India distribution, Shri Lakshmi for South India manufacturing, Tricoat for high-margin specialty products.

The genius lay in integration. Most roll-ups fail because acquirers can't integrate operations effectively. APL Apollo developed a playbook: Keep the entrepreneurial management for 12-18 months, standardize IT systems immediately, integrate procurement within six months, and gradually migrate customers to the Apollo brand. The company retained the best of acquired companies—customer relationships, local knowledge, specialized capabilities—while eliminating redundancies.

Distribution as Competitive Advantage: The 3-Tier Network

While competitors focused on manufacturing, APL Apollo built India's most extensive steel distribution network. The three-tier structure—company depots, exclusive dealers, and sub-dealers—created multiple defensive moats. Dealers received exclusive territories, ensuring they pushed Apollo products over competitors. Sub-dealers got credit support and technical training, creating loyalty at the last mile.

The network effect is powerful. A fabricator in Tier-3 town needs 10 tonnes of tubes urgently. APL Apollo can deliver tomorrow from the nearest depot. Competitors might take a week. That fabricator becomes an Apollo customer for life. Multiply this by thousands of touch points, and you understand why new entrants can't compete despite having similar manufacturing capabilities.

Innovation in a Commodity Business: Product Differentiation

"You can't differentiate steel tubes"—every expert said this in 2010. APL Apollo proved them wrong by creating 1,500+ SKUs, each targeting specific applications. The innovation wasn't just in products but in identifying unmet needs. Door frames were dominated by wood and aluminum—APL created hollow steel sections that were cheaper, stronger, and termite-proof. Greenhouse structures used bamboo or basic pipes—APL developed specialized tubes with optimal strength-to-weight ratios.

The patent portfolio—unusual for a tubes company—creates legal moats around high-margin products. Competitors can copy the concept but not the specific design, giving APL Apollo 18-24 month head starts in new categories. By the time competitors catch up, APL has moved to the next innovation.

Brand Building in B2B: "Desh Ki Badhti Taqat"

APL Apollo spends more on marketing than the rest of the industry combined. The "Desh Ki Badhti Taqat" (The Nation's Growing Strength) campaign positioned APL Apollo as nation-building infrastructure, not just tubes. Television commercials during IPL matches, billboards at construction sites, technical seminars for engineers—APL Apollo built a consumer brand in a B2B market.

The brand premium is real. In blind quality tests, APL Apollo tubes perform similarly to competitors. Yet customers pay 5-10% premiums for the Apollo brand. Why? Trust, availability, and the intangible comfort of buying from the market leader. This pricing power drops straight to the bottom line.

Family Business Modernization: Professional Management Integration

Many Indian family businesses struggle with professionalization. APL Apollo cracked the code. The Gupta family maintains strategic control while bringing in professional managers for operational roles. The CFO comes from Vedanta, the manufacturing head from Tata Steel, the CMO from Asian Paints. This blend of entrepreneurial vision and professional execution created a culture that's both aggressive and disciplined.

Succession planning started early. Rahul Gupta didn't join as heir apparent but proved himself by independently acquiring and turning around Apollo Tricoat. This merit-based approach ensures family members earn their positions while attracting top external talent who see clear career paths.

Capital Allocation: Balancing Growth vs Dividends

APL Apollo's capital allocation reflects sophisticated financial thinking. During high-growth phases (2010-2020), virtually all cash flow was reinvested. As the business matured and generated surplus cash, the company initiated dividends while maintaining growth capex. The recent ₹1,500 crore expansion announcement shows the company hasn't lost its growth appetite despite achieving market leadership.

The balance sheet philosophy—maintaining net cash while growing rapidly—seems contradictory but makes strategic sense. In a cyclical industry, financial strength becomes a competitive advantage during downturns. Competitors leveraged during good times struggle when demand drops. APL Apollo can acquire distressed assets, gain market share, and emerge stronger from cycles.

The working capital optimization deserves its own Harvard case study. Through a combination of brand power (allowing cash sales), supplier financing programs, and inventory management, APL Apollo generates cash while growing. The company essentially uses supplier capital to fund growth—a beautiful business model when executed well.

IX. Analysis & Investment Case

The investment community remains split on APL Apollo. Bulls see India's Nucor—a nimble, innovative steel company riding a multi-decade infrastructure boom. Bears see a cyclical commodity business trading at tech-like valuations, vulnerable to Chinese imports and raw material volatility. Both sides make compelling arguments.

Bull Case: Infrastructure Boom, Market Leadership, Capacity Expansion

India's infrastructure spending is accelerating. The government allocated ₹10 lakh crore for infrastructure in FY24, up from ₹5 lakh crore in FY20. Every kilometer of highway needs structural steel. Every airport expansion requires hollow sections. Every metro project consumes thousands of tonnes of tubes. APL Apollo supplies them all.

The shift from unorganized to organized is a multi-decade tailwind. Currently, 60% of the structural steel market remains unorganized—small manufacturers producing unbranded tubes with inconsistent quality. As construction becomes more sophisticated, builders increasingly prefer branded products with guaranteed specifications. APL Apollo captures this shift disproportionately.

Structural steel penetration in India is 35 kg per capita versus 150 kg in China and 250 kg in developed markets. As India urbanizes and construction methods modernize, structural steel usage could triple. APL Apollo, with 50%+ market share, captures this growth multiplicatively—market growth plus market share gains plus pricing power equals explosive earnings growth.

The capacity expansion to 6.8 million tonnes positions APL Apollo for the next leg of growth. With competitors struggling to fund expansion and new entrants facing distribution barriers, APL Apollo could reach 60-70% market share by 2030. In a ₹50,000 crore market growing at 15% annually, that's a ₹35,000 crore revenue opportunity.

Bear Case: Commodity Price Volatility, Competition from Imports, Capital Intensity

Steel prices doubled during COVID then crashed 40%. While APL Apollo claims to pass through raw material costs, reality is more nuanced. During rapid price increases, customers resist price hikes. During price declines, competition intensifies. This volatility compresses margins unpredictably, making earnings forecasting difficult.

Chinese steel overcapacity poses existential risks. If China dumps structural steel tubes in India, APL Apollo's pricing power evaporates overnight. While anti-dumping duties provide protection, trade policies can change. The company's premium valuations assume continued protection—a political variable outside management control.

Capital intensity remains concerning. The ₹1,500 crore expansion represents 2x annual profits. While returns on capital have been excellent historically, they assume continued market dominance. If competition intensifies or demand disappoints, these investments could destroy value. The steel industry is littered with companies that over-expanded during booms.

Intrinsic Value and Market Pricing

Current market price of ₹1,701.8 INR. Analyst estimates vary widely—from ₹1,200 (assuming margin compression) to ₹2,200 (assuming successful expansion and market share gains). The wide range reflects fundamental uncertainty about whether APL Apollo is a structural growth story or a cyclical play at peak margins.

Competitive Positioning vs Tata Steel, JSW, Jindal Steel

APL Apollo operates in a different league than primary steel producers. Tata Steel's integrated plants require billions in maintenance capex. JSW's blast furnaces face environmental pressures. Jindal's long products compete directly with Chinese imports. APL Apollo's asset-light model (relatively speaking), downstream focus, and brand moat provide structural advantages.

The real competition comes from potential new entrants. If Tata Steel or JSW decided to seriously enter structural tubes, they have the balance sheet strength to build capacity and distribution. So far, they've focused on primary steel where scale advantages are greater. But strategic priorities can change.

ESG Considerations and Sustainability Initiatives

ESG increasingly matters for institutional investors. APL Apollo's record is mixed. Positives include lower emissions than primary steel (as they process, not produce steel), water recycling at newer plants, and solar installations at facilities. Negatives include limited disclosure on Scope 3 emissions and absence from major sustainability indices.

The circular economy presents opportunities. As buildings get demolished, structural steel can be recycled. APL Apollo could vertically integrate into scrap processing, securing raw material supply while improving environmental credentials. Management has hinted at this possibility but provided no concrete plans.

X. The Future & Epilogue

Standing at APL Apollo's newest Raipur facility, you see the future of Indian manufacturing. Robots move steel coils weighing tonnes with millimeter precision. Artificial intelligence optimizes cutting patterns to minimize waste. Digital twins simulate production scenarios before physical manufacturing begins. This isn't your grandfather's tube factory—it's a glimpse into Industry 4.0.

Infrastructure Super-cycle Thesis in India

India stands at an inflection point. The country needs to build infrastructure equivalent to what currently exists—double the highways, triple the airports, quadruple the metro networks—over the next two decades. This isn't political rhetoric but mathematical necessity. India's urban population will reach 600 million by 2040. They need places to live, work, and commute.

Structural steel becomes critical in this narrative. Traditional construction using concrete and rebar takes too long. Pre-fabricated structures using steel tubes can be assembled in weeks, not months. As construction labor becomes scarcer and more expensive, the economics increasingly favor steel. APL Apollo isn't just riding this trend—it's enabling it.

The company's vision extends beyond tubes. Management speaks of becoming a "complete building materials solution provider." This could mean adjacent products like roofing sheets, wall panels, or even pre-fabricated housing modules. The distribution network and brand equity create optionality for category expansion.

International Expansion Opportunities

The UAE facility marks the beginning, not end, of international ambitions. Middle Eastern construction booms as countries diversify from oil. African infrastructure needs are massive. Southeast Asian markets are graduating from bamboo to steel. APL Apollo's cost-competitive manufacturing and proven execution capabilities position it well for international expansion.

But international expansion requires nuance. Every market has local competitors, different specifications, and unique distribution channels. APL Apollo must decide whether to export from India, set up local manufacturing, or acquire existing players. Each strategy has trade-offs. Early indications suggest a hybrid approach—exports for specialized products, local manufacturing for volume items.

Technology Disruptions: Green Steel, Alternative Materials

The steel industry faces disruption. Green steel, produced using hydrogen instead of coal, could revolutionize manufacturing. While APL Apollo doesn't produce primary steel, green steel adoption would affect input costs and potentially create marketing advantages for early adopters. The company must navigate this transition carefully.

Alternative materials pose longer-term threats. Carbon fiber composites, engineered wood products, and even 3D-printed structures could substitute structural steel in specific applications. APL Apollo's innovation capabilities and customer relationships provide early warning systems for these threats, but vigilance is essential.

Next Generation Leadership and Succession Planning

Sanjay Gupta turned 53 this year. While he shows no signs of slowing down, succession planning has begun. Rahul Gupta's successful Apollo Tricoat turnaround proved his capabilities. Other family members are being groomed in different divisions. The challenge is maintaining entrepreneurial culture while professionalizing operations.

The next generation faces different challenges. Market share gains become harder from 50% base. International expansion requires different skills than domestic consolidation. Technology disruption accelerates. Success will require combining Sanjay's entrepreneurial instincts with sophisticated global management capabilities.

Key Takeaways for Entrepreneurs and Investors

APL Apollo's journey offers lessons extending beyond steel tubes. First, operational excellence beats financial engineering. While peers leveraged balance sheets, APL Apollo focused on operations, ultimately generating superior returns. Second, brand building works even in B2B commodities. The Apollo brand commands premiums that drop straight to bottom lines.

Third, distribution often matters more than manufacturing. APL Apollo's moat isn't its factories—Chinese companies have better equipment. The moat is thousands of dealer relationships built over decades. Fourth, consolidating fragmented markets requires patience and capital. Quick flips don't work. Integration takes years.

Finally, family businesses can professionalize without losing entrepreneurial edge. The Gupta family's willingness to bring in outside talent while maintaining strategic control created a unique culture combining aggression with discipline.

For investors, APL Apollo represents a fascinating case study in value creation. A ₹100 investment in 2010 is worth ₹5,000+ today—a 50x return beating most venture capital investments. The question is whether the next decade offers similar opportunities. Bulls believe we're still early in India's infrastructure story. Bears see a maturing business at peak valuations.

The truth, as always, lies somewhere in between. APL Apollo has transformed from struggling regional manufacturer to national champion. The company created a category, built a brand, and generated exceptional returns. Whether it can maintain this trajectory depends on execution, competition, and India's economic trajectory—variables that make investing equal parts analysis and faith.

As our story concludes where it began—in that loss-making Bihar factory—the transformation seems almost mythical. Yet every milestone was achieved through countless small decisions, incremental improvements, and relentless execution. APL Apollo's story isn't about dramatic pivots or brilliant strategies. It's about doing ordinary things extraordinarily well, consistently, over decades.

The company that couldn't pay suppliers in 1986 now shapes India's skyline. The teenager who joined his father's struggling business now runs a ₹44,000 crore enterprise. The commodity that "couldn't be branded" now commands premium prices. Sometimes, the most extraordinary transformations come from the most ordinary beginnings.

That's the APL Apollo story—and perhaps, the India story itself.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube