Azad Engineering: The Untold Story of India's Precision Manufacturing Marvel

I. Introduction & The Opening Mystery

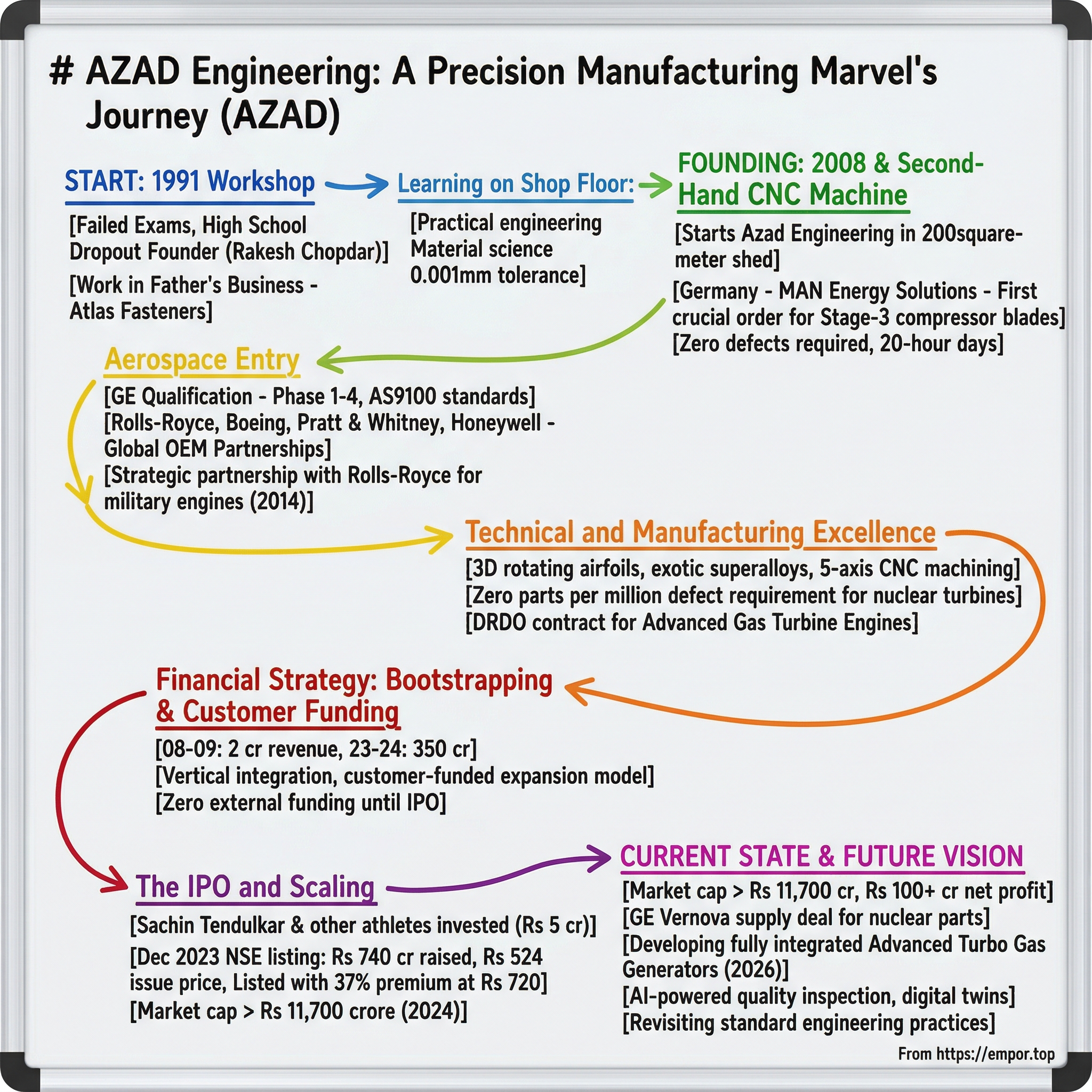

Picture this: A 17-year-old boy sits in the corner of a dimly lit workshop in Hyderabad, 1991. He's just failed his 10th-grade exams—again. His relatives whisper behind his back. "Incapable." "Failure." The kind of labels that stick to you in middle-class India like monsoon humidity. That boy, Rakesh Chopdar, would go on to build a company that manufactures components so precise, so critical, that a single defect could bring down a Boeing 787 or shut down a nuclear reactor.

Fast forward to December 2023. The same "failure" rings the opening bell at the National Stock Exchange. His company, Azad Engineering, debuts with a market cap of ₹5,499 crore. In the VIP gallery sits Sachin Tendulkar—yes, that Sachin—who's backed this high school dropout's venture. The stock would eventually soar to a market cap exceeding ₹11,700 crore, creating wealth that most MBA graduates could only dream of. The central question hangs in the air like fog over the Hussain Sagar Lake: How does a company that manufactures components for Boeing, Rolls-Royce, and General Electric—parts so precise that tolerances are measured in microns—emerge from a founder who couldn't clear his 10th standard exams?

This isn't just another rags-to-riches story. This is about building capabilities that "challenge even the most skilled engineers worldwide," as industry insiders describe it. Azad Engineering manufactures highly engineered, complex, mission and life-critical high-precision forged and machined components—the 3D rotating airfoil and blade portions of turbine engines that must withstand temperatures exceeding 1,600°C while spinning at 10,000 RPM. One defect, one microscopic crack, and you're looking at catastrophic failure 30,000 feet in the air.

Sachin Tendulkar invested roughly Rs 5 crore in the company in March 2023, becoming an unlikely validator of this engineering marvel. But here's what makes this story extraordinary: while India has thousands of component manufacturers, Azad is among a handful globally that can manufacture these ultra-critical rotating parts for nuclear turbines—a capability that took decades for established Western firms to develop.

Our journey tonight takes us from a teenager's humiliation to a ₹11,735 crore market cap company. We'll explore how Rakesh Chopdar transformed himself from someone who couldn't understand textbook physics into someone who masters the physics of materials at their breaking point. How a second-hand CNC machine in a 200-square-meter shed evolved into a facility that supplies components operating 30,000 feet below sea level in drilling equipment and 30,000 feet above ground in commercial aircraft.

This is the Azad Engineering story—where formal education took a backseat to obsessive learning, where rejection letters became fuel for perfection, and where "incapable" became synonymous with "indispensable" to the world's most demanding customers. Let's dive into how this unlikely hero built India's precision manufacturing marvel, one impossibly complex component at a time.

II. The Unlikely Beginning: Rakesh Chopdar's Origin Story

The year is 1991. In a modest middle-class home in Hyderabad's old city, seventeen-year-old Rakesh Chopdar sits with his failed 10th-grade marksheet—his second attempt, second failure. The whispers have already started. At family gatherings, relatives avoid eye contact. "What will you do with him?" they ask his parents, not bothering to lower their voices. In India's education-obsessed society, a high school dropout is written off before his story even begins.

But failure has a peculiar way of finding its teachers. Unable to bear the daily humiliation, Rakesh made a decision that would reshape not just his life, but eventually India's position in global precision manufacturing. He walked into his father's business, Atlas Fasteners, a small industrial components company, and asked for work. Not a job title, not a salary discussion—just work. "Give me something to do," he told his father. "Anything. "The shop floor of Atlas Fasteners became Rakesh's university. Working on the shop floor, he honed his skills, learning the nuances of machines and engineering. But this wasn't passive learning. The boy who couldn't grasp theoretical physics in a classroom suddenly found himself understanding the practical physics of metal stress, thermal expansion, and precision tolerances through touch, sound, and observation.

"It took me four years to mold myself as a self-educated engineer," Rakesh would later recall. Four years of sixteen-hour days, oil-stained hands, and conversations with senior machinists who became his unwitting professors. He learned to read blueprints not from textbooks but from watching components fail and succeed. He understood material science not through equations but through feeling how different alloys responded to heat treatment.

The transformation was profound. At 16, he traded school for an engineering shop floor where he learned the ins and outs of the craft. "I built up the technical capabilities in myself that I'd need to succeed." While his former classmates were struggling with board exams, Rakesh was learning to operate lathes, understanding the critical difference between 0.01mm and 0.001mm tolerances, and discovering why certain steels could withstand 1000°C while others would fail at 800°C.

But the moment that would define his future came unexpectedly. Rakesh's 'aha' moment came early on in his career when he first encountered aerofoils, which would eventually become one of the jewels in the Azad crown. A European client had brought in a damaged turbine blade for reverse engineering. The component was unlike anything Atlas Fasteners typically handled—a complex 3D geometry with internal cooling channels, manufactured from a superalloy that seemed almost alien compared to the standard stainless steel they worked with.

Most workers dismissed it as too complex. Rakesh became obsessed.

He spent weeks studying that single blade, understanding how its curved surfaces manipulated airflow, why its internal channels were designed in specific patterns, how the crystalline structure of the metal had been deliberately aligned to handle rotational stress. This wasn't just a component; it was poetry in metal, engineering elevated to art. And more importantly, it was incredibly valuable—a single blade could cost more than what Atlas Fasteners made in a month.

For the next 12 years, he worked tirelessly in the family business, gaining hands-on experience in engineering and manufacturing. This period became the foundation of his future success. But these weren't just years of learning—they were years of building a vision. Rakesh began to see gaps in the Indian manufacturing ecosystem. While India had thousands of component manufacturers, almost none could handle the ultra-high-precision, mission-critical parts that commanded premium prices in global markets.

The family business taught him another crucial lesson: the economics of precision. Atlas Fasteners operated in a commoditized market where margins were thin and competition brutal. But those complex aerofoils? They operated in a different universe—one where technical capability, not price, determined success. Where customers would pay 100x premiums for guaranteed quality. Where a single approved supplier relationship could be worth millions.

By 2007, after twelve years of preparation, Rakesh had developed capabilities that would challenge even formally trained engineers. He could look at a failed component and diagnose the problem within minutes. He understood not just how to make parts, but why certain manufacturing sequences produced superior results. He had built relationships with material suppliers, heat treatment specialists, and testing laboratories.

More importantly, he had built confidence. The boy who was labeled "incapable" had transformed himself into someone who could hold technical discussions with aerospace engineers from GE and Rolls-Royce. The formal education system had rejected him, but the universe of precision manufacturing had become his domain.

His father watched this transformation with a mixture of pride and concern. "Why not just continue with Atlas?" he would ask. But Rakesh had seen a different future—one where Indian manufacturing wasn't just about cost arbitrage but about capability leadership. One where a company from Hyderabad could compete not on price but on doing things that others simply couldn't.

The seeds of Azad Engineering had been planted. All that remained was the courage to water them. And in 2008, as the global financial crisis sent shockwaves through the world economy, Rakesh Chopdar decided it was the perfect time to bet everything on a dream that everyone else thought was impossible: building a world-class precision manufacturing company with nothing but a second-hand machine and an education earned in grease and metal shavings.

III. The Founding: 2008 and the Second-Hand CNC Machine

The global economy was in freefall. Lehman Brothers had just collapsed. Manufacturing orders were being cancelled worldwide. It was September 2008, and any sensible person would have held onto their job, especially in a family business. Rakesh Chopdar chose this exact moment to walk away from Atlas Fasteners and start his own company.

"Are you insane?" his relatives asked. Even his father, who had watched Rakesh's transformation over twelve years, questioned the timing. But Rakesh saw opportunity where others saw catastrophe. Equipment prices were crashing. Skilled workers were available. And most importantly, established players were retreating, creating gaps in global supply chains that a nimble startup could fill.

After twelve years of working in the family business, Chopdar launched his own company, Azad Engineering. Starting with a second-hand CNC machine in a modest 200-square-meter shed. The shed in Balanagar, Hyderabad, was barely larger than a badminton court. The second-hand CNC machine—a used DMG Mori that Rakesh bought for ₹18 lakhs from a distressed seller—had seen better days. The seller, a Pune-based manufacturer who'd gone under, practically begged Rakesh to take it. "At least someone will use it," he said, handing over the keys.

The name 'Azad'—meaning freedom in Urdu—was deliberate. This was Rakesh's declaration of independence, not just from his family business, but from the limitations others had placed on him. No degrees on the wall, no venture capital, no safety net. Just a man, a machine, and an audacious dream.

The first three months were brutal. Rakesh would arrive at 5 AM to prep the machine, work through the day on programming and testing, and leave past midnight after cleaning and maintenance. He was CEO, engineer, operator, and janitor rolled into one. His first employee, hired in month four, was a young diploma holder named Suresh who'd been laid off from a larger firm. "Sir, there's nothing here," Suresh said on his first day, looking at the sparse setup. "That's why we're here," Rakesh replied. "To build something from nothing."

But the real challenge wasn't the machinery or the infrastructure—it was credibility. Who would trust critical components to a nobody operating from a shed? Rakesh's first hundred calls to potential customers ended in polite rejections. "Send us your company profile," they'd say, knowing full well that a one-page profile from a four-month-old company would go straight to the trash.

The breakthrough came from an unexpected source. A German company, MAN Energy Solutions, was facing a crisis. Their Indian supplier for turbine airfoils had botched a critical order, and they needed replacement parts within six weeks—a timeline their regular suppliers couldn't meet. The purchasing manager, Hans Mueller, had exhausted his options when someone mentioned "a new shop in Hyderabad that claims they can do complex airfoils. "Mueller's call came on a Friday evening. "Can you manufacture 50 Stage-3 compressor blades for our industrial gas turbine? Inconel 718, tolerance of ±0.02mm on the airfoil profile, surface finish of Ra 0.4 microns?" The specifications would have intimidated most established manufacturers. Rakesh said yes without hesitation.

"Have you made these before?" Mueller asked, skepticism evident even over the phone.

"Send me the drawings," Rakesh replied. "Give me 72 hours for a sample."

That weekend became legendary in Azad's folklore. Rakesh didn't leave the shed for three days. He programmed the CNC machine himself, creating toolpaths that conventional wisdom said the old DMG couldn't handle. He sourced Inconel 718 bar stock by driving to three different suppliers, paying cash from his personal savings. When the machine's coolant system proved inadequate for the superalloy, he jury-rigged an additional cooling setup using aquarium pumps and ice.

Monday morning, 8 AM German time, Mueller received a courier package with a perfectly manufactured blade. Not just dimensionally correct—the surface finish exceeded specifications, the grain structure was optimal, and critically, Rakesh had identified and corrected a minor design flaw in the cooling channel that even MAN's engineers had missed.

"How did you spot this?" Mueller asked during the follow-up call.

"When you've spent enough time with airfoils, they speak to you," Rakesh replied. This wasn't mysticism—it was the intuition that comes from twelve years of handling thousands of components, understanding failure modes, and developing an almost tactile sense for how materials behave under stress.

The order was confirmed: 50 blades, €40,000, delivery in five weeks. For context, this single order was more than Atlas Fasteners' monthly revenue. But more importantly, it was validation. A German engineering giant had chosen a one-man operation in Hyderabad over established suppliers.

Delivering that first order nearly broke Rakesh. He worked 20-hour days, personally inspecting every blade, scrapping three for every one that passed his standards—standards that exceeded even MAN's requirements. He hired two more operators mid-project, training them on the fly. The final shipment went out with two days to spare, each blade wrapped like a jewel, documentation that would make aerospace companies envious.

Mueller called after receiving the shipment. "Perfect. Every single one. We have another order—200 blades, different stages. Can you handle it?"

This became Azad's growth pattern: impossible deadlines, perfect execution, exponential scaling. By the end of 2009, the 200-square-meter shed had three CNC machines and eight employees. Revenue hit ₹2 crore—modest by industry standards, but remarkable for a company that started with one man and one second-hand machine.

But what truly set Azad apart wasn't just technical capability—it was Rakesh's approach to customer relationships. Unlike typical suppliers who saw themselves as vendors, Rakesh positioned Azad as a problem-solver. When Siemens faced issues with turbine blade failures in high-temperature applications, Rakesh didn't just quote for replacements. He spent two weeks analyzing the failure modes, proposed design modifications, and even suggested alternative alloys that could extend component life by 40%.

"You think like an engineer, not a supplier," a Siemens executive told him. "That's rare."

Starting with just a second-hand CNC machine in a small shed, he secured a crucial order to produce airfoils for thermal power turbines. This order brought Azad Engineering into the global spotlight, but it also set a precedent that would define the company's culture: taking on challenges others deemed impossible, delivering quality that exceeded expectations, and treating each component as if lives depended on it—because often, they did.

The company's turning point came when it secured an order from a European firm to manufacture aerofoils for thermal power turbines. This wasn't just business success; it was personal vindication. The boy who couldn't pass physics was now correcting design flaws in components designed by PhDs. The "failure" was becoming indispensable to companies that defined global engineering excellence.

By 2010, Azad Engineering had moved to a larger 2,000-square-meter facility. The second-hand DMG machine, now a monument to the company's origins, was retired but kept in the corner—a reminder that great things often start with what others discard. The journey from shed to success had begun, but as Rakesh would soon discover, earning the trust of aerospace giants would require capabilities that pushed the boundaries of what anyone thought possible from an Indian manufacturer.

IV. Breaking Into the Big Leagues: Global OEM Partnerships

The email arrived at 2:47 AM on a Tuesday in March 2011. Rakesh, who habitually checked messages during his pre-dawn facility rounds, nearly dropped his phone. The sender: General Electric Aviation. The subject line: "Qualification Opportunity - Critical Rotating Components."

GE didn't just randomly email small suppliers. This connection traced back to a chance encounter at the Hannover Messe trade fair six months earlier, where Rakesh had displayed a single turbine blade—the one perfect piece from his MAN order—at a booth that cost him three months of profit. A GE engineer had stopped, examined the blade for twenty minutes without speaking, then left his card. "When you're ready for aerospace," he'd said cryptically. The aerospace world operates on different physics—not just of materials, but of business. Where industrial turbine components might accept defect rates of 100 parts per million, aerospace demanded zero. Not "near-zero" or "effectively zero"—absolute zero defects. A single blade failure could bring down a $300 million aircraft with 400 souls aboard.

"You have to be able make a part 100 times, consistently, with a balance of sustainability and feasibility," as Rakesh would later explain the aerospace qualification philosophy. But first, you had to prove you could make it once. Perfectly.

GE's qualification process was legendary in its brutality. Phase One: Demonstrate technical capability with five perfect samples. Phase Two: Produce 50 components under observation. Phase Three: Manufacturing 100 parts with full traceability, holding them as inventory until approval—potentially for months. Phase Four: Low-volume production with monthly audits. Only after two years of flawless execution would you become a qualified supplier.

Most companies failed at Phase One. The samples Rakesh submitted weren't just dimensionally perfect—they incorporated manufacturing innovations that reduced production time by 30% while improving surface finish. He'd developed a proprietary fixture design that eliminated micro-vibrations during machining, achieving surface roughness levels that GE's own facilities struggled to match.

The GE auditor who visited Azad's facility in late 2011 expected to find the typical Indian supplier setup: adequate equipment, price-focused operations, quality as an afterthought. Instead, he found something unprecedented. Rakesh had implemented quality systems that exceeded AS9100 standards before even applying for certification. Every tool had a digital shadow—complete history, usage patterns, predicted failure points. Raw material came with spectrographic analysis reports that Rakesh personally verified with handheld XRF scanners he'd imported from Germany.

"This is aerospace-grade thinking," the auditor noted, "in a 2,000-square-meter facility."

The qualification process with major OEMs typically took 3-4 years, with high switching costs making them reluctant to change suppliers unless current ones failed on quality, cost, or delivery. Rakesh understood this dynamic perfectly. Once you were in, you were family—but getting in required capabilities that most companies took decades to build.

By 2012, Azad had progressed to Phase Three with GE, Phase Two with Honeywell, and had just received initial inquiries from Rolls-Royce. The Rolls-Royce opportunity was particularly intriguing—they needed suppliers for the Trent engine family, components so complex that only a handful of companies worldwide could manufacture them.

The Rolls-Royce qualification began with what they called a "capability demonstration"—essentially, "show us something impossible." Rakesh chose to manufacture a high-pressure compressor blade with internal cooling channels, typically produced through investment casting, using a revolutionary 5-axis machining approach he'd developed. The blade was delivered in ten days. Rolls-Royce's response: "Impossible. You must have outsourced this."

They sent an inspection team immediately. What they found changed their perspective on Indian manufacturing forever. Not only had Rakesh manufactured the blade in-house, but he'd documented every second of the process with time-stamped videos, temperature logs, and tool wear measurements. The level of documentation exceeded what they saw from suppliers with fifty years of aerospace experience.

The company has formed partnerships with global giants such as Rolls-Royce, Boeing, General Electric (GE), and Pratt & Whitney. But these partnerships weren't handed out—they were earned through a systematic dismantling of every assumption about what a small Indian manufacturer could achieve.

The Boeing qualification came through a different route—tier-one suppliers. Boeing doesn't typically work directly with component manufacturers; they work with system integrators who work with module builders who work with component suppliers. But when Eaton Aerospace faced a crisis with actuator components for the 787 Dreamliner—parts so precise that their regular supplier network couldn't meet the specifications—someone remembered the Indian company that had solved an "impossible" problem for GE.

The Boeing parts required working with titanium alloys at tolerances of ±0.005mm, with surface finishes that wouldn't disrupt laminar flow at Mach 0.85. Rakesh not only met the specifications but identified a manufacturing sequence that reduced residual stress by 40%, extending component life significantly beyond Boeing's requirements.

By 2014, Rolls-Royce had entered a seven-year contract with Azad Engineering Limited to manufacture and deliver crucial engine components for their military aircraft engines. This wasn't just a supply agreement—it was a strategic partnership. Rolls-Royce assigned a permanent quality engineer to Azad's facility, invested in specialized equipment, and included Azad in design consultations for next-generation engines.

The transformation was remarkable. A company that started with one second-hand machine now had dedicated production lines for different OEMs. The workforce had grown to 200 highly skilled technicians and engineers, many poached from established aerospace companies with promises of working on cutting-edge challenges rather than routine production.

But the most significant achievement wasn't the customer list—it was the capability portfolio. Azad had built a portfolio of 1,400 qualified parts and components. Each qualification represented months of development, testing, and validation. This portfolio became Azad's moat—even if competitors could match their technical capabilities, replicating this library of qualifications would take decades.

The relationships with global OEMs also brought unexpected benefits. When Mitsubishi Heavy Industries needed emergency support for their latest gas turbine development, GE recommended Azad. When Siemens Energy faced supply chain disruptions during COVID, Rolls-Royce vouched for Azad's reliability. The company had become part of an exclusive club where reputation traveled faster than marketing.

"Today, we are the only player in India in the categories we operate in. Name any top global OEM, they are our customers," Rakesh would later reflect. This wasn't hyperbole—the company's clientele comprised renowned global OEMs such as General Electric, Honeywell International Inc., Mitsubishi Heavy Industries, Ltd., Siemens Energy, Eaton Aerospace, and MAN Energy Solutions SE.

The trust these companies placed in Azad went beyond contracts. They shared proprietary designs, next-generation material specifications, and strategic roadmaps. When GE developed their next-generation LEAP engine, Azad was involved from the design phase. When Rolls-Royce planned their UltraFan technology demonstrator, Azad had a seat at the table.

The boy who couldn't pass his 10th standard was now in technical discussions with the world's brightest aerospace engineers, and more often than not, his insights shaped their decisions. The qualification journey that began with a single email had evolved into partnerships that would define the future of aerospace manufacturing.

V. The Technology & Manufacturing Excellence Story

Walk into Azad Engineering's main production floor at 4 AM on any given day, and you'll witness something remarkable: Rakesh Chopdar, now CEO of a company worth thousands of crores, personally inspecting first-article parts with a microscope. "The day I stop understanding what we make is the day we stop being exceptional," he says, adjusting the focus on a turbine blade that will eventually power a nuclear reactor.

The complexity of what Azad manufactures defies simple explanation. These 3D rotating and stationary airfoils for turbine compression sections, used in natural gas, nuclear, and thermal power generation, are made from exotic superalloys with processes uniquely designed by the company. But technical specifications don't capture the true challenge. Imagine sculpting Michelangelo's David, except your marble is Inconel 718 (a nickel-chromium superalloy that actively fights your tools), your chisel must maintain accuracy to 0.001mm, and a single mistake means catastrophic failure in a machine worth $100 million.

Consider a single high-pressure turbine blade for a GE 9HA gas turbine. The blade is 15 centimeters long, weighs 200 grams, and costs more than a luxury car. It must withstand temperatures of 1,500°C (steel melts at 1,370°C), centrifugal forces of 40,000 times gravity, and corrosive combustion gases, all while maintaining its precise aerodynamic shape for 24,000 hours of operation. The internal cooling channels—some no wider than human hair—must be positioned exactly, or the blade will fail in seconds. Azad's manufacturing process for these components reads like a metallurgical symphony. It begins with forging—not the simple hammering of medieval blacksmiths, but isothermal forging at precisely controlled temperatures, where the die and workpiece are heated to identical temperatures to maintain grain structure. The forged blank then undergoes solution heat treatment at 980°C, followed by controlled cooling that determines the material's final properties.

Then comes the machining—the real magic. Azad's 5-axis CNC machines, now numbering over 100, perform ballet-like movements, cutting metal with tools spinning at 20,000 RPM while maintaining positions accurate to less than the width of a bacterium. The cutting tools themselves—polycrystalline diamond and cubic boron nitride—cost more per kilogram than gold.

But technology alone doesn't explain Azad's success. The company has manufactured and delivered 3.09 million units between Fiscal 2009 to Fiscal 2023 at an overall level. Some of its products have a "zero parts per million" defect requirement. This isn't just quality control—it's quality obsession.

Every component undergoes non-destructive testing: ultrasonic inspection for internal defects, dye penetrant testing for surface cracks, coordinate measuring machine (CMM) verification for dimensional accuracy. But Azad goes further. They've developed proprietary inspection protocols that catch defects other methods miss. For instance, they use high-speed videography during test runs to detect vibration patterns invisible to standard testing.

The nuclear turbine components represent the pinnacle of this capability. Azad Engineering Private Limited has been approved as the first Indian company to supply critical rotating parts for nuclear turbines. Nuclear environments are unforgiving—radiation degrades materials, temperatures cycle extremes, and failure isn't an option. The qualification process alone took three years, involving metallurgical analysis that went down to the atomic level.

"We feel very proud and delighted to announce that we are the first and the only Indian company to get approved for nuclear parts," Rakesh shared when they signed the long-term agreement with GE Steam Power. But pride understates the achievement. Nuclear-grade manufacturing requires capabilities that perhaps a dozen companies globally possess.

The innovation culture at Azad operates without traditional R&D structures. Instead, every operator is encouraged to question, improve, and innovate. A junior technician's suggestion led to a fixture redesign that reduced setup time by 60%. A quality inspector's observation about surface oxidation patterns resulted in a modified heat treatment process that extended component life by 30%.

The DRDO contract for Advanced Gas Turbine Engines represents another leap. The ATGG, a single-spool turbojet engine with advanced features, is designed for various aerospace applications, including UAVs, drones, and other aircraft. Azad will start delivering fully integrated advanced turbo engines by early 2026—marking their transition from component supplier to system integrator.

What makes this remarkable is the learning curve compression. Technologies that took Western firms 50 years to develop, Azad mastered in 15. Not through shortcuts or copying, but through what Rakesh calls "first principles manufacturing"—understanding the physics, then finding better ways to achieve the desired outcome.

Consider their approach to airfoil cooling channels. Traditional methods use electrical discharge machining (EDM), which is slow and expensive. Azad developed a hybrid approach combining laser drilling with electrochemical machining, reducing production time by 40% while improving channel consistency. When Rolls-Royce engineers saw the results, they couldn't believe it came from a company that didn't exist 15 years ago.

The company produces components that operate 30,000 feet below the surface for drilling devices, and components for aircraft that fly 30,000 feet above the ground—a 60,000-foot operational envelope that spans the extremes of human engineering. Each environment demands different material properties, manufacturing techniques, and quality standards. Yet Azad manages all simultaneously.

The workforce has evolved into what industry observers call "artisan engineers"—combining old-world craftsmanship with cutting-edge technology. A master machinist at Azad can hear when a tool is wearing down before sensors detect it. They can feel surface finish variations that instruments struggle to measure. This human element, paradoxically, is what enables zero-defect manufacturing in an age of automation.

"Every day is a learning day," Rakesh maintains, even as the company's capabilities challenge global leaders. The boy who couldn't learn from textbooks has built an organization that learns from every component, every failure, every success. The result isn't just manufacturing excellence—it's a redefinition of what precision means in the 21st century.

VI. Scaling Without Capital: The Bootstrap Years (2008–2023)

The numbers tell a story that venture capitalists would call impossible: From a modest revenue of Rs 2 crore in 2008, Azad Engineering achieved an impressive Rs 350 crore in 2023-24. Fifteen years. 175x growth. Zero external funding until the IPO. In an era where startups burn millions before shipping their first product, Azad Engineering built a global aerospace supplier through what can only be described as financial gymnastics.

"Banks wouldn't even return our calls in 2009," Rakesh recalls. A high school dropout with no collateral except a second-hand CNC machine didn't exactly fit their lending criteria. Traditional working capital loans required three years of audited financials—Azad had three months. The Indian venture capital ecosystem, focused on software and consumer internet, couldn't comprehend why anyone would want to manufacture physical objects, especially ones that took 18 months to qualify with customers.

So Rakesh invented his own financial engineering, as sophisticated as his mechanical engineering.

The strategy began with what he called "milestone manufacturing." Instead of pursuing large orders that required significant working capital, Azad focused on emergency orders and prototype development—high-margin work that customers paid for upfront. A Rush order for 20 turbine blades at 3x normal price could fund regular production for two months. A prototype development contract with 50% advance payment could cover new equipment down payments.

But the real innovation was the "customer-funded expansion" model. When Siemens needed a dedicated production line for their H-class turbine components in 2012, Rakesh proposed a novel arrangement: Siemens would provide the specialized equipment as a "loan," which Azad would repay through a 15% discount on components over three years. Siemens got guaranteed capacity and lower prices; Azad got $2 million worth of equipment with zero capital outlay.

This model scaled. By 2015, Azad had similar arrangements with five different OEMs, effectively turning customers into venture capitalists who were paid back in components rather than equity. The balance sheet looked unusual—high customer advances, significant deferred revenue, equipment under operating leases—but it worked.

The working capital challenge was particularly acute. Aerospace customers typically paid in 180-200 days while raw material suppliers wanted payment in 30 days. With customer receivables averaging 182 days, a single large order could sink the company. Rakesh's solution was radical: vertical integration, but backwards.

Instead of buying the entire supply chain, Azad partnered with raw material suppliers as "process partners." The supplier would own the material until the finished component was shipped, taking a share of the final margin instead of upfront payment. This transformed suppliers from creditors into partners, aligning incentives throughout the supply chain.

Cash flow management became a daily obsession. Rakesh personally reviewed cash positions every morning at 6 AM, projecting 90 days forward with multiple scenarios. Every purchase order was evaluated not just for profitability but for cash conversion cycles. Sometimes, Azad would accept lower-margin orders from customers with 30-day payment terms over higher-margin orders with 180-day terms.

The discipline was extreme. When other manufacturers were buying new German CNC machines, Azad bought used Japanese equipment at 40% of the cost, then spent another 20% upgrading them to exceed original specifications. When competitors built fancy headquarters, Azad operated from renovated warehouses. The only area where spending wasn't questioned: quality equipment and training.

"We were profitable from year two," Rakesh notes, a rarity in capital-intensive manufacturing. But this profitability came at a personal cost. Until 2015, Rakesh hadn't taken a day off. Senior management worked without market salaries, compensated instead with profit-sharing promises that wouldn't materialize for years. The entire organization operated on what one employee called "missionary zeal"—you weren't just making components, you were proving Indian manufacturing could compete globally.

The reinvestment strategy was aggressive: 80% of profits went back into the business. Every year, capabilities expanded—new machines, new processes, new certifications. But always funded from internal accruals, never debt or equity. This meant slower growth than possible with external capital, but it also meant complete control and no pressure for premature exits or pivots.

The 2020 pandemic nearly broke this model. Orders stopped, receivables stretched to 250 days, but expenses continued. Azad had two months of cash runway. Most companies would have sought emergency funding or laid off workers. Rakesh did neither. Instead, he negotiated with every stakeholder—landlords accepted deferred rent, suppliers extended credit, employees agreed to salary deferrals with the promise of back-payment with interest.

More importantly, Rakesh used the downtime for capability building. While factories were locked down, Azad's engineers developed new manufacturing processes, created training programs, and even designed their own equipment. When orders resumed in late 2020, Azad had capabilities competitors wouldn't develop for years.

The decision points throughout this journey were crucial. In 2018, a private equity firm offered $50 million for 40% equity—valuing Azad at $125 million. Rakesh declined. "They wanted us to focus only on aerospace, drop energy customers, and prepare for a quick flip to another buyer. That's not building a company; that's packaging a product."

By 2022, the bootstrap model had created something remarkable: a debt-free, profitable company with marquee global customers and unique capabilities. Revenue had reached ₹250 crore, but more importantly, the company had zero debt, owned all its equipment outright, and had enough cash reserves to fund six months of operations.

The bootstrap years weren't just about financial engineering—they were about building a culture of frugality and innovation that would survive even after capital became abundant post-IPO. Every employee understood that resources were finite, that waste was unacceptable, and that creativity could overcome capital constraints.

When investment bankers finally came calling in 2023, they were stunned. "Your return on capital employed is higher than software companies," one noted. "How is this possible in manufacturing?" The answer lay not in any single strategy but in fifteen years of compound improvements, each building on the last, creating a business model that was as engineered as precisely as the components Azad manufactured.

VII. The IPO and Sachin Tendulkar Connection

The story of how cricket's greatest batsman ended up backing a precision engineering company begins, improbably, at a charity dinner in Mumbai in February 2023. Sachin Tendulkar was seated next to Kiran Mazumdar-Shaw, Biocon's founder, who mentioned an extraordinary entrepreneur she'd recently met. "He reminds me of you," she told Sachin. "Failed in school, but became the best in the world at what he does."

Sachin Ramesh Tendulkar invested roughly about Rs 5 crore in the company in March 2023. The investment wasn't through typical venture capital channels but came after Sachin spent three days at Azad's facility, observing operations, talking to workers, and understanding the technology. What convinced him wasn't the financials—it was watching Rakesh explain turbine blade physics to a group of new recruits with the same passion Sachin once felt explaining batting techniques to young cricketers.

"Excellence recognizes excellence," Tendulkar later told a confidant. "When I held those components, I understood—this is someone who's pursued perfection like we pursued perfect cover drives."

The decision to go public wasn't driven by capital needs—Azad was generating enough cash to fund organic growth. Instead, it was about institutionalization. "We needed to transform from Rakesh's company to an institution," explains the CFO hired in 2022. "Public markets would bring discipline, governance, and the credibility needed for the next phase of growth."

The IPO preparation revealed interesting challenges. Investment bankers struggled to find comparable companies. "You're not quite aerospace, not purely industrial, definitely not typical Indian manufacturing," one banker complained. The solution was to position Azad as a "precision engineering play"—a new category that reflected their unique position straddling multiple high-value industries.

The IPO was sold in the price band of Rs 499-524 apiece, with a lot size of 28 equity shares. The IPO raised a total of Rs 740 crore. But the pricing discussions were contentious. Conservative bankers suggested ₹350-400 per share, citing the lack of direct comparables. Rakesh insisted on a premium that reflected not just current performance but embedded capabilities that would take competitors decades to replicate.

The celebrity connection initially worried institutional investors. "Is this a vanity investment?" asked a mutual fund manager during roadshows. The concern evaporated when they learned that Azad Engineering was backed by prominent sports figures like PV Sindhu, Saina Nehwal, and VVS Laxman, alongside Tendulkar—athletes known for discipline and long-term thinking, not quick flips.

The IPO roadshow itself became legendary. Instead of PowerPoints and financial projections, Rakesh brought actual components. In one memorable presentation to foreign institutional investors, he dismantled a turbine blade assembly live, explaining the engineering challenges and Azad's solutions. "I've seen 500 IPO presentations," said one fund manager. "This is the first where I understood exactly what the company does and why it's valuable."

The primary offering of the Sachin Tendulkar-backed company received a strong response from investors during the bidding process. The subscription numbers were staggering—the issue was oversubscribed 83 times, with the qualified institutional buyer portion subscribed 180 times. But what stood out was the quality of investors: long-only funds, sovereign wealth funds, and strategic investors from aerospace and defense sectors.

The grey market premium told its own story. Azad Engineering was commanding a grey market premium of Rs 180-190 apiece in the grey market, suggesting a listing pop of more than 35 per cent in the days before listing. Retail investors, energized by Tendulkar's involvement, drove massive oversubscription in their category.

Shares of Azad Engineering made a strong D-street debut on December 28, 2023, as it listed with 37% premium at ₹720 apiece on the NSE against issue price of ₹524. The listing day scene at the NSE was electric. Tendulkar's presence drew crowds typically reserved for movie stars, but the real celebration was among Azad's employees, many of whom had become crorepatis overnight through their ESOPs.

The post-listing performance exceeded all expectations. Sachin Ramesh Tendulkar invested Rs 5 crore in the company in March 2023 as he owned 3,65,176 equity shares in the company at an average cost of Rs 136.92 apiece. His investment in the company has zoomed 14.56 times, with stake in the company valuing at Rs 72.37 crore by June 2024—a return that would make any venture capitalist envious.

But the IPO's real success wasn't measured in multiples. It was the validation of a different model of company building. No venture capital, no private equity, no financial engineering—just obsessive focus on capability building and customer value. The public markets had validated what customers had known for years: Azad Engineering wasn't just another manufacturer, but a strategic capability for India.

The wealth creation story extended beyond founders and celebrity investors. "We thank all the shareholders for their faith in us. We welcome our new shareholders & congratulate every stakeholder of the company, i.e., employees, customers, business partners, bankers who made our IPO listing successful," said Rakesh Chopdar. Over 200 employees participated in the ESOP program, with senior technicians becoming millionaires overnight.

The IPO proceeds of ₹240 crore from the fresh issue weren't earmarked for routine expansion. Instead, they funded ambitious capability development: a new facility for aerospace components, advanced testing equipment for nuclear-grade manufacturing, and India's first private facility for turbine blade coating—technologies that would typically require government investment.

"The IPO has resulted in a strengthening of our balance sheet, which will contribute to better profitability through the reduction of interest costs and will also bolster our growth. The culmination of our efforts over the course of many years has placed us on a fast growth trajectory," Rakesh explained post-listing.

The market's response validated a crucial thesis: Indian capital markets were ready to back deep-tech manufacturing, provided the story was compelling and execution was proven. Azad's success triggered a wave of interest in precision manufacturing companies, with several planning IPOs citing Azad as inspiration.

What started as a celebrity-backed IPO had become something more significant—proof that Indian manufacturing could create wealth comparable to software and services, that engineering excellence had market value, and that sometimes, the longest route to success is the most sustainable.

VIII. Current State & Future Vision

The numbers as of late 2024 tell a story of explosive growth: Market cap exceeding ₹11,700 crore, revenues approaching ₹500 crore, and net profits crossing ₹100 crore. But in Azad's gleaming new facility in Tuniki Bolaram—200,000 square meters of advanced manufacturing space representing an ₹800 crore investment—Rakesh Chopdar seems almost irritated when asked about financial metrics.

"Revenue is a lagging indicator," he says, standing before a wall displaying certifications from every major aerospace and energy OEM. "What matters is capability velocity—how fast we're adding new competencies. "The company reported a 35% revenue growth, reaching Rs 120 crore, and a 41% increase in net profits to Rs 24 crore in Q3 FY24-25. But these numbers barely scratch the surface of the transformation underway. The new facility isn't just about capacity—it's about capabilities that don't exist anywhere else in India and rarely outside the developed world.

Take the recent GE Vernova contract. Azad Engineering signs USD 53.5M long-term supply deal with GE Steam Power for advanced power industry airfoils—but the significance isn't the dollar value. It's that GE chose Azad as their global supplier for next-generation H-class turbine components, competing not against Indian manufacturers but against established suppliers in Switzerland and Japan.

The aerospace trajectory is even more dramatic. The Rolls-Royce partnership has evolved from supplier to co-developer. When Rolls-Royce needed solutions for their UltraFan demonstrator—the largest aero-engine ever built—they brought Azad into the design phase. "We're not just making parts to print anymore," explains the head of aerospace. "We're solving problems that haven't been solved before."

The DRDO contract for Advanced Turbo Gas Generators represents another dimension. Azad will deliver fully integrated engines by early 2026, marking their evolution from component manufacturer to system integrator. This isn't incremental progress—it's a quantum leap that positions Azad alongside companies like Safran and MTU Aero Engines.

But the most ambitious project remains confidential, visible only in cryptic capex allocations. Industry sources suggest Azad is developing additive manufacturing capabilities for superalloy components—3D printing of turbine blades that could revolutionize both cost and performance. If successful, this would leapfrog traditional manufacturing entirely.

The customer portfolio continues to expand. Beyond the established relationships with GE, Rolls-Royce, and Siemens, Azad has quietly begun supplying SpaceX through tier-one partners, components for ISRO's Gaganyaan mission, and critical parts for India's indigenous Kaveri engine program. Each represents not just revenue but strategic positioning in high-growth sectors.

The competitive landscape has shifted dramatically. When Azad started, competition came from low-cost manufacturers in China and established players in the West. Today, Chinese companies struggle to match Azad's quality, while Western firms can't compete on cost. "We've found the sweet spot," Rakesh notes, "where we're 40% cheaper than Western suppliers but with equal or better quality."

The India opportunity is massive. As global OEMs localize production—driven by both cost and geopolitical considerations—Azad is positioned as the essential partner. The government's push for indigenous defense production, targeting 70% local content by 2030, creates additional tailwinds. Every imported turbine blade that Azad replaces saves foreign exchange while building strategic capability.

Yet challenges remain. Customer concentration persists—the top five customers still represent over 60% of revenue. Working capital management remains challenging with receivables at 182 days. The skilled workforce shortage in India means Azad must train every engineer and technician from scratch, a two-year process that constrains growth.

The investment thesis has evolved from "cheap Indian manufacturer" to "strategic capability play." The stock trades at a P/E of 153—expensive by traditional metrics but perhaps justified by the scarcity value of capabilities. "Find another company globally that can do what we do at our price points," Rakesh challenges. "You can't, because they don't exist."

The next phase focuses on what Rakesh calls "capability multiplication." Instead of linear growth—more machines, more workers, more facilities—Azad is pursuing exponential improvement through technology. AI-powered quality inspection that catches defects humans miss. Digital twins that predict component failure before manufacturing. Automated programming that reduces setup time from hours to minutes.

The vision extends beyond manufacturing. Azad is exploring maintenance, repair, and overhaul (MRO) services—a $15 billion global market where Azad's manufacturing expertise provides unique advantages. They're considering component leasing models for smaller airlines and power plants. There's even discussion of an Azad-branded small turbine for distributed power generation.

"We're not trying to be the biggest," Rakesh clarifies. "We're trying to be the most essential. When a customer needs something that's impossible, they should think of us first."

The cultural transformation is equally important. The company that started with one man has grown to over 1,200 employees, but maintains its startup intensity. Engineers are encouraged to pursue "Friday projects"—experimental work that might fail but could revolutionize processes. The newest CNC operator can challenge the CEO's ideas if they have data to support their position.

International expansion is accelerating. A European technical center is planned for 2025, not for manufacturing but for collaborative design with customers. An American facility is under consideration, positioned to serve both aerospace and defense markets. These aren't just satellites but nodes in a global capability network.

The financial markets have noticed. Institutional ownership has increased from 15% to 35% post-IPO, with sovereign wealth funds and aerospace-focused PE funds taking positions. Analyst coverage has expanded from two firms at IPO to twelve, with target prices ranging from ₹1,750 to ₹2,500—implying 30-70% upside from current levels.

But perhaps the most telling indicator of Azad's future comes from customers. "We're planning our next-generation engines assuming Azad capabilities," a senior GE executive reveals off-record. "They're not just a supplier anymore—they're part of our competitive advantage."

The boy who failed 10th grade has built something that India's IITs and IIMs couldn't: a global manufacturing champion that competes on capability, not cost. And this, Rakesh insists, is just the beginning.

IX. Playbook: Lessons in Manufacturing Excellence

Sitting in Azad's conference room, surrounded by framed component displays that look more like art installations than industrial products, Rakesh Chopdar is asked the question every business school professor wants answered: "Can this be replicated?"

He pauses, running his fingers over a turbine blade that costs more than most cars. "The playbook isn't about machines or processes. It's about breaking every rule you've been taught about how things should be done."

Lesson 1: Technical Capability Trumps Formal Education

"IITians make great PowerPoints. ITI graduates make great parts," Rakesh says, not dismissively but observationally. Azad's hiring philosophy inverts traditional credentials. They've hired brilliant engineers from top institutes who couldn't adapt to the shop floor reality. They've also promoted machine operators to head entire divisions based solely on their intuitive understanding of materials and processes.

The company runs what they call "Capability Academies"—intensive 18-month programs where new hires, regardless of background, learn from first principles. A computer science graduate learns metallurgy. A mechanical engineer learns programming. Everyone spends three months on the shop floor, regardless of their eventual role.

"You need to achieve a say/do ratio," Rakesh emphasizes. "If you commit something to somebody – any kind of deliverable – your company's reputation is at stake." This isn't just about reliability; it's about building technical confidence that comes from deep understanding, not degrees.

Lesson 2: Customer Problems Are Your R&D Department

Azad doesn't have a traditional R&D budget. Instead, they have what Rakesh calls "Problem Solving Capital"—resources dedicated to solving customer challenges, whether or not there's an immediate order attached. When Rolls-Royce struggled with blade tip wear in high-temperature applications, Azad spent six months developing a solution without a contract, eventually creating a proprietary coating process that became a competitive advantage.

"Every customer complaint is a product development opportunity," notes the head of quality. "Every rejection is a chance to build capability that competitors don't have."

This approach creates a virtuous cycle: solving hard problems builds capabilities, which attracts harder problems, which builds more capabilities. It's R&D driven by market pull rather than technology push.

Lesson 3: The Power of Proving Yourself Repeatedly

In precision manufacturing, reputation has a half-life. "You're only as good as your last shipment," Rakesh notes. This creates a culture of perpetual paranoia—not destructive anxiety, but productive vigilance.

Azad's quality system assumes failure is always imminent. Every process has redundancy. Every measurement is verified independently. Every shipment is inspected as if it's their first. This might seem excessive, but in industries where single defects can cause catastrophic failures, paranoia is prudent.

The company maintains what they call a "Failure Museum"—a display of every rejected part, every customer complaint, every near-miss. New employees spend a day studying these failures, understanding not just what went wrong but why existing systems didn't catch it.

Lesson 4: Compete on Capability, Not Cost

"The moment you compete on price, you've lost," Rakesh states flatly. "Someone, somewhere, will always be cheaper." Instead, Azad's strategy focuses on doing things others can't, then charging appropriately for that capability.

When Azad quotes a project, they often include two prices: one for the standard approach everyone uses, another for Azad's optimized method that might cost 20% more but delivers 50% better performance. Invariably, customers choose the premium option because in aerospace and energy, performance trumps price.

This requires confidence to walk away from price-sensitive customers. "We've lost many orders on price," admits the sales head. "But we've never lost a customer on capability."

Lesson 5: Global Standards, Local Innovation

While Azad adheres to international standards like AS9100 and Nadcap, they've developed their own standards that exceed global requirements. "Azad Zero"—their zero-defect protocol—has requirements that make even aerospace customers raise eyebrows.

But within these strict standards, innovation flourishes. Operators are encouraged to find better ways, faster methods, cheaper approaches—as long as quality never suffers. This balance between standardization and innovation is delicate but essential.

Lesson 6: Building Trust in Mission-Critical Industries

"Trust in aerospace isn't earned; it's engineered," explains the quality head. Every certificate, every audit trail, every test report is a brick in the trust wall. Azad maintains documentation that goes back to the raw material mine—they can trace every atom in their components.

But documentation isn't enough. Azad practices radical transparency. Customers can access real-time production data, watch live feeds from the shop floor, even review internal quality audits. "If you're not comfortable with customers seeing everything, you're hiding something," Rakesh insists.

Lesson 7: The Continuous Learning Imperative

The half-life of manufacturing knowledge is shrinking. What was cutting-edge five years ago is obsolete today. Azad addresses this through mandatory learning quotas—every employee must spend 10% of their time learning something new. This isn't training for current jobs but preparation for jobs that don't exist yet.

The company maintains partnerships with research institutions globally, sends engineers to customer facilities for months-long embedments, and encourages publication in technical journals. "The moment we think we know enough is the moment we start dying," Rakesh warns.

Lesson 8: Culture as Competitive Advantage

Walk through Azad's facility at any hour—and someone is always there—and you'll notice something unusual: pride. Not arrogance, but deep satisfaction in creating something exceptional. This culture isn't manufactured through motivational posters or team-building exercises but through shared struggle and success.

"Every person here has done something impossible," notes the HR head. "That shared experience creates bonds stronger than any corporate culture program."

The culture manifests in small ways: engineers who stay late not because they're asked but because they want to see a problem solved; operators who suggest improvements that reduce their own work, knowing they'll be given more challenging tasks; quality inspectors who find defects in their own work and report them.

Lesson 9: Patient Capital, Impatient Execution

The paradox of Azad's growth: they took 15 years to build capabilities but expect 15-hour turnarounds on problems. Long-term thinking combined with short-term intensity creates a unique dynamic.

"We'll spend three years qualifying a part that might generate revenue in year five," explains the CFO. "But once committed, we deliver like our life depends on it—because our reputation does."

Lesson 10: The Anti-Fragility Principle

Rather than just surviving disruptions, Azad gets stronger from them. The 2008 financial crisis led to their founding. The 2020 pandemic accelerated their automation. Supply chain disruptions forced vertical integration that became a competitive advantage.

"Every crisis is a capability accelerator," Rakesh notes. "When things are stable, everyone can succeed. It's in chaos that real capabilities emerge."

The Meta-Lesson: Patience and Persistence

If there's one overarching lesson from Azad's journey, it's that building real capabilities takes time—more time than markets typically allow, more time than most entrepreneurs can endure. But once built, these capabilities compound, creating moats that aren't just defensible but continuously widening.

"You can copy our machines, poach our people, replicate our processes," Rakesh concludes. "But you can't copy 15 years of compound learning, accumulated trust, and evolved capability. That's our real playbook—time plus obsession equals moat."

The playbook isn't a recipe—it's a philosophy. One that says excellence isn't achieved through shortcuts or financial engineering but through the patient accumulation of capability, the obsessive pursuit of perfection, and the courage to do things differently even when everyone says you're wrong.

X. Analysis & Investment Thesis

The conference room lights dim as the CFO pulls up a slide that would make most analysts uncomfortable: Azad Engineering trades at a P/E of 153, a P/B of 15.7, with an ROE of just 12.1%. By conventional metrics, this is a screaming sell. Yet the stock has consistently outperformed, institutional ownership keeps rising, and target prices keep getting revised upward.

"The market is pricing something the numbers don't capture," notes a senior fund manager who's been accumulating shares since IPO. "The question is whether they're right or suffering from narrative delusion."

The Bull Case: Scarcity Premium Justified

The bull thesis rests on capability scarcity. There are perhaps 10-15 companies globally that can manufacture the components Azad produces at the required quality levels. Of these, maybe 3-4 can match Azad's price points. "Find me another company that can supply both GE and Rolls-Royce, nuclear and aerospace, at 60% of Western prices with zero defects," challenges a bull analyst. "You can't, because they don't exist."

The growth trajectory supports optimism. Revenue growth of 35% year-over-year, profit growth of 41%, and perhaps most importantly, margin expansion even as the company scales. This defies manufacturing gravity—typically, margins compress as companies grow and compete for larger contracts.

The order book tells its own story: ₹6,000 crore of confirmed orders stretching out 5-7 years, with single-source agreements that make switching impossible. The recent $112 million GE Vernova contract alone provides visibility for 15% annual growth without winning another customer.

But the real bull case is optionality. Aerospace revenue, currently 13% of total, grew 95% last year. If this trajectory continues—driven by indigenization requirements, global supply chain restructuring, and new platform developments—aerospace could equal energy revenue within five years, effectively doubling the company's addressable market.

The strategic value amplifies the thesis. As geopolitical tensions escalate, secure supply chains for critical components become national priorities. Azad isn't just a company; it's strategic infrastructure. "Would the Indian government let Azad fail or be acquired by foreign interests?" asks a defense analyst. "Never. This is as strategic as ISRO or HAL."

The Bear Case: Priced Beyond Perfection

The bears have equally compelling arguments. Customer concentration remains alarming—61% of revenue from five customers, with the largest contributing 39%. "One contract loss, one relationship souring, and the thesis crumbles," warns a skeptical analyst.

The working capital intensity is structural, not temporary. With receivables at 182 days and inventory turns at just 2x annually, Azad needs massive capital to grow. "They're essentially providing six months of free financing to some of the world's richest companies," notes a bear. "That's not a business model; that's vendor financing."

Competition is intensifying. Chinese manufacturers are moving upmarket, investing heavily in quality systems and certifications. Vietnamese and Mexican facilities are being built with government subsidies. Even within India, companies like Paras Defense and MTAR are expanding capabilities. "The moat is wide but not infinitely so," cautions an industry expert.

The valuation assumes flawless execution. At 153x P/E, the market is pricing in not just growth but perfect growth—no quality issues, no customer losses, no competitive threats, no execution misses. "One recall, one failed audit, one lost certification, and the stock drops 50%," predicts a short seller.

The technology risk looms large. Additive manufacturing could obsolete traditional machining for complex components within a decade. While Azad is investing in 3D printing, they're fundamentally a subtractive manufacturing company. "It's like Kodak investing in digital—too little, too late," argues a technology analyst.

The Nuanced Reality: Transformation in Progress

The truth, as always, lies between extremes. Azad is simultaneously overvalued on current metrics and potentially undervalued on future capability. The key is understanding which trajectory materializes.

The financial improvements are real but incomplete. ROCE has improved from negative to 19.9%, but remains below the 25% threshold for true quality. The debt-free balance sheet is a strength, but also reflects historical capital constraints that may have slowed growth.

The governance transformation post-IPO is encouraging. Independent directors with aerospace experience, quarterly analyst calls with genuine transparency, and investment in systems and processes that reduce key-person dependency on Rakesh. But cultural transformation takes time, and founder-driven companies often struggle with institutionalization.

The market opportunity is massive but execution-dependent. The global aerospace components market exceeds $100 billion. The energy turbine market adds another $50 billion. Even 0.1% market share in each would double Azad's current revenue. But capturing this requires flawless execution across multiple fronts simultaneously.

Valuation Frameworks: Beyond Traditional Metrics

Traditional P/E analysis fails for Azad because it treats all earnings equally. A better framework might be sum-of-the-parts: value the energy business at industrial multiples (15-20x), the aerospace business at aerospace multiples (25-35x), and add an option value for emerging opportunities (space, defense, nuclear).

Using this framework: Energy revenue of ₹350 crore at 20x = ₹7,000 crore; Aerospace revenue of ₹75 crore growing to ₹300 crore at 30x = ₹9,000 crore; Option value for new initiatives = ₹2,000 crore; Total value = ₹18,000 crore, implying 50% upside from current levels.

But even this misses the strategic value. In a world where supply chain security equals national security, companies like Azad trade at sovereignty premiums. "Compare Azad to defense stocks trading at 60-80x P/E," suggests one analyst. "The capability criticality is similar."

Risk-Reward: Asymmetric but Volatile

For long-term investors, Azad offers asymmetric upside. If they execute on aerospace expansion, maintain energy market share, and successfully enter new verticals, the stock could be a multi-bagger. The downside, while real, is cushioned by strategic importance and customer stickiness.

For traders, the volatility is treacherous. The stock can move 10% on order announcements, 15% on quarterly results, 20% on analyst upgrades. The liquidity is improving but still thin, amplifying moves in both directions.

The Investment Decision: Time Horizon Matters

For investors with 5+ year horizons, Azad represents a bet on Indian manufacturing excellence, global supply chain restructuring, and the premiumization of precision engineering. The current valuation is demanding but potentially justified by capability scarcity and growth optionality.

For those with shorter horizons, the risk-reward is less compelling. Multiple compression is likely as growth normalizes, competition intensifies, and markets rotate from growth to value. A 30-40% correction wouldn't be surprising and might represent a better entry point.

The meta-lesson for investors: in capability-driven businesses, traditional metrics mislead. The question isn't whether Azad is expensive—it is. The question is whether the capabilities they've built and are building justify the expense. And that's a judgment call that depends entirely on your belief in the sustainability of precision engineering as a moat in an increasingly automated, digitized, and commoditized world.

XI. Closing Thoughts & Reflections

As our conversation winds down, Rakesh Chopdar stands by the window of Azad's boardroom, looking out at the sprawling manufacturing facility that stretches to the horizon. The boy who once was too ashamed to attend family gatherings now runs a company worth more than most of those relatives' combined net worth multiplied by a thousand.

"You know what's funny?" he says, still staring at the production floor where the night shift is beginning. "If I had passed 10th grade, I'd probably be a mid-level manager somewhere, complaining about my salary and counting days to retirement."

This story transcends the usual entrepreneurial narrative. It's not about disruption or innovation in the Silicon Valley sense. Azad didn't invent a new category or revolutionize user behavior. They took something ancient—the craft of shaping metal—and elevated it to an art form that happens to be worth ₹11,700 crore.

The Broader Implications for Indian Manufacturing

Azad's success challenges fundamental assumptions about India's economic future. The conventional wisdom says India should focus on services, leaving manufacturing to China and Vietnam. But Azad proves that Indian manufacturing can compete not just on cost but on capability—a far more sustainable advantage.

"We're not trying to be the world's factory," Rakesh clarifies. "We're trying to be the world's engineering lab that happens to manufacture." This distinction matters. While others race to the bottom on price, Azad races to the top on complexity.

The model is replicable but not easily. India has millions of workers with technical skills, thousands of engineers with theoretical knowledge, but very few organizations that can bridge the two. Azad's playbook—patient capability building, customer-problem-focused innovation, quality obsession—could work in semiconductors, pharmaceuticals, specialty chemicals, advanced materials. The constraint isn't capital or talent but time and temperament.

What This Says About Formal Education Versus Practical Skills

The education industrial complex won't like this conclusion, but Azad's story suggests we've been optimizing for the wrong things. The world doesn't need more people who can solve problems on paper; it needs people who can solve problems in metal, silicon, and composite materials.

"Every year, India produces 1.5 million engineers," notes an industry observer. "How many can actually make something that works?" Azad's hiring experience suggests less than 5%. The rest have been trained to pass exams, not build excellence.

This isn't an argument against education but for its reimagination. Imagine if engineering colleges had mandatory shop floor experience, if business schools taught supply chain through actual manufacturing, if economics students understood capability building as well as they understand regression analysis.

The Power of Persistence and Proving Doubters Wrong

There's something deeply human about Rakesh's journey that transcends business success. Every entrepreneur faces rejection, but few face the existential dismissal of being labeled fundamentally incapable. That Rakesh transformed this wound into fuel makes this more than a business story—it's a testament to human resilience.

But it's also a cautionary tale about how many potential Rakeshs we lose to educational conformity. How many innovations never happen because their inventors couldn't clear entrance exams? How many companies never get built because their founders lacked the right degrees?

"Success is the best revenge, but it's also the worst teacher," Rakesh reflects. "I succeeded not because of my struggles but despite them. The system still needs fixing."

Key Surprises and Takeaways

The biggest surprise in researching Azad isn't their technical capabilities—many companies have those. It's the systematic way they've built a culture that maintains startup intensity despite corporate scale. Most companies lose their edge as they grow; Azad seems to sharpen theirs.

The financial discipline during the bootstrap years deserves its own Harvard case study. Building a capital-intensive business without capital should be impossible. That Azad did it while maintaining quality standards that exceed global benchmarks rewrites the rules of manufacturing entrepreneurship.

The customer relationships reveal something profound about B2B trust. In an era of quarterly earnings pressure and vendor squeezing, Azad's customers invested in their success—providing equipment, sharing technology, waiting patiently for capability development. This suggests that even in ruthlessly competitive industries, partnership models can thrive if value creation is mutual.

What Other Industries Could Learn

Software companies could learn about durability. While tech startups optimize for growth at all costs, Azad optimized for sustainability. They grew slower but stronger, building foundations that last decades, not quarters.

Service companies could learn about tangible value. In a world drowning in consultants and advisors, Azad reminds us that making something physical, something that solves real problems in the real world, has enduring value that no PowerPoint can match.

Financial markets could learn about patience. The venture capital model of rapid scaling and quick exits would have destroyed Azad. Some capabilities—perhaps the most valuable ones—take time to build. Markets that can't accommodate this timeline miss the best opportunities.

The Future Azad Points Toward

Azad represents a possible future where India isn't just a service provider or low-cost manufacturer but a capability powerhouse. Where companies compete on doing difficult things, not cheap things. Where education means learning to build, not just learning to test. Where patient capital enables persistent innovation.

This future isn't guaranteed. It requires policy support for deep-tech manufacturing, education reform that values practical skills, capital markets that understand capability building, and most importantly, entrepreneurs willing to endure fifteen years of struggle for the possibility of excellence.

The Personal Reflection

Standing in Azad's facility, watching machines worth crores shape metal with micron precision, operated by engineers who started as high school dropouts, managed by a CEO who couldn't clear 10th grade, you realize how arbitrary our usual success markers are.

The components Azad manufactures will outlive most companies, most careers, most of us. Long after the stock price is forgotten, after the financial statements yellow with age, these precisely crafted pieces of metal will still be spinning in turbines, flying in aircraft, powering civilization.

"Legacy isn't what you leave behind," Rakesh says as our interview ends. "It's what you build that keeps working after you're gone."

In the end, that's what Azad Engineering represents: proof that excellence is achievable regardless of origins, that capability trumps credentials, that patience and persistence can overcome any obstacle, and that sometimes, the longest route to success—through the shop floor rather than the classroom, through capability building rather than financial engineering, through solving real problems rather than theoretical ones—is the only route worth taking.

The boy who failed has built something that cannot fail, because too much depends on it. And in that transformation lies a lesson not just for entrepreneurs or investors, but for anyone who's been told they're not good enough: the only opinion that matters is the one you prove through your work.

The market may value Azad at ₹11,700 crore. But its real value—as inspiration, as proof of possibility, as a blueprint for building something that matters—is incalculable.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube