Arvind Limited: India's Denim Revolution and the Lalbhai Legacy

I. Introduction & The Great Depression Opportunity

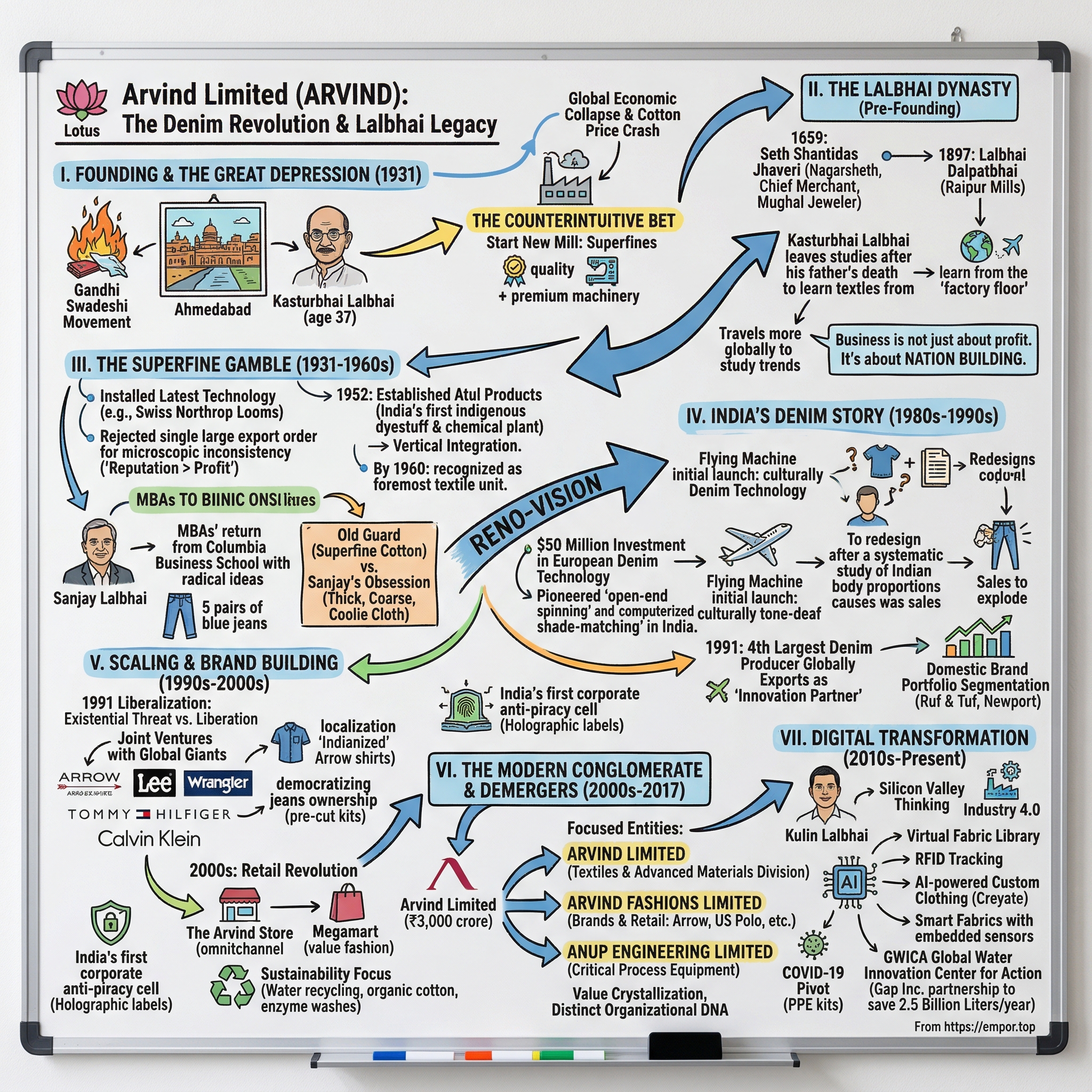

Picture Ahmedabad in 1931: The world economy lies in ruins. Banks have collapsed across continents. Cotton prices have cratered by 67% from their 1929 peaks. In America, breadlines stretch for blocks. In Britain, the pound has just crashed off the gold standard. And in this ancient textile city on the banks of the Sabarmati River, a 37-year-old mill owner named Kasturbhai Lalbhai is about to make the most counterintuitive business decision of the Great Depression.

While textile mills across India are shuttering—victims of both global economic collapse and Gandhi's Swadeshi movement that has Indians burning British cloth in the streets—Kasturbhai and his brother Narottam decide to start a new mill. Not just any mill, but one focused on superfine fabrics, the most technically demanding and capital-intensive segment of textiles. They scrape together ₹165,000 in share capital (roughly $2,500 in Depression-era dollars) and christen their venture Arvind Mills, after Kasturbhai's eldest son.

Today, Arvind Limited stands as India's largest denim manufacturer, producing over 100 million meters annually—enough fabric to wrap around the Earth two and a half times. The company that began making dhoties and sarees during economic catastrophe now supplies denim to global fashion houses, operates a portfolio of international brands from Tommy Hilfiger to Calvin Klein, and has expanded into everything from advanced materials for spacesuits to smart city water management systems. With a market cap of ₹7,519 Crore and annual revenue of ₹8,505 Crore, the company represents one of those rare Indian industrial stories that spans nearly a century—from colonial rule through independence, from the License Raj through liberalization, from family patriarchs to fourth-generation MBAs.

This is the story of how a Depression-era bet on quality became a global denim empire, how a family's commitment to nation-building created one of India's most enduring industrial houses, and how each generation found its own revolution to lead—whether superfine cotton, synthetic denim, international brands, or now, advanced materials and smart cities.

It's also a story of timing, transformation, and the peculiar Indian genius for managing complexity—running everything from fashion retail to water treatment plants, from automotive composites to real estate development, all while maintaining family control and navigating the treacherous waters of Indian capital markets.

Welcome to the Acquired-style deep dive into Arvind Limited—where we'll trace how a company named after a mill owner's son became synonymous with the jeans revolution in a country where, just decades earlier, wearing Western clothing was considered unpatriotic.

II. The Lalbhai Dynasty & Pre-Founding Context

The year is 1659. The Mughal Empire stretches across the subcontinent, Aurangzeb has just crowned himself emperor, and in the bustling trade city of Ahmedabad, a jeweler named Seth Shantidas Jhaveri sits in his haveli, weighing diamonds destined for the imperial treasury. Shantidas isn't just any merchant—he's the Nagarsheth (chief merchant) of Ahmedabad, banker to nobles, and trusted jeweler to three successive Mughal emperors. When the Dutch East India Company needs local intelligence, they come to him. When Persian armies threaten Gujarat, it's Shantidas who negotiates safe passage for the city's merchants.

This is where the Lalbhai story begins—not in some humble village but at the apex of Mughal commerce. The family traces its lineage directly to Shantidas, inheriting not just wealth but something more valuable: an understanding of how business and power intersect, how to survive regime changes, and how to build institutions that outlast individuals.

Fast forward two and a half centuries. It's 1911, and 17-year-old Kasturbhai Lalbhai has just received news that will alter his destiny: his father, Lalbhai Dalpatbhai, has died suddenly. Kasturbhai must abandon his studies and return to Ahmedabad to manage Raipur Mills, the family's textile venture established in 1897. The teenager who dreamed of becoming an engineer now finds himself learning the textile trade from the factory floor—literally working as a timekeeper, understanding every aspect of mill operations from yarn counts to worker psychology.

But Kasturbhai isn't content merely managing an inherited mill. By the 1920s, he's established multiple ventures including Asoka Mills, each more ambitious than the last. He studies global textile trends obsessively, traveling to Manchester and Osaka, observing how the world's textile capitals operate. What he sees both inspires and alarms him: India, which once clothed the world with its muslins and calicos, now imports 80% of its cloth from Lancashire mills.

The political context makes everything more complex. Gandhi has launched the Swadeshi movement, calling for Indians to boycott British goods and burn foreign cloth. Bonfires of Manchester textiles light up Indian cities. Mill owners face a paradox: there's massive demand for Indian-made cloth, but most Indian mills produce only coarse fabrics. The fine fabrics that India's growing middle class desires—for shirts, sarees, and formal wear—still come from Britain.

This is where Kasturbhai sees opportunity where others see impossibility. While his peers chase volume in coarse cloth, he envisions something different: an Indian mill that can match Manchester's superfines, fabrics so refined they feel like silk, so precisely woven they drape like liquid. It's a technical challenge that requires importing specialized machinery, training workers in new techniques, and convincing retailers that Indian mills can produce luxury-grade textiles.

The Lalbhai family philosophy crystallizes during these years—a blend of Jain business ethics, Gandhian nationalism, and surprisingly global ambition. Kasturbhai articulates it simply: "Business is not just about profit. It's about building the nation's capabilities." This isn't mere rhetoric. Even as he plans his superfine mill, he's establishing educational institutions (he'll later help found IIM Ahmedabad), building hospitals, and creating what would become standard practice for the Lalbhais: using business success to fund social infrastructure.

By 1930, the stage is set. Kasturbhai has spent years studying global textile technology, building relationships with machinery suppliers in Switzerland and England, and quietly recruiting the best textile engineers in India. He's watched Indian mills fail at superfines, analyzed why (usually cutting corners on machinery or training), and developed a different approach: spare no expense on quality, even if it means lower initial returns.

The timing seems insane. The Wall Street Crash of 1929 has triggered global economic collapse. Cotton prices have crashed from 44 cents per pound to under 10 cents. Mills across India are shuttering—over 30% will close by 1932. Credit has dried up. Even established businesses struggle to pay workers.

But Kasturbhai and his brother Narottam see what others miss: precisely because everyone else is retreating, this is the moment to build something extraordinary. Equipment prices have collapsed. Skilled workers, laid off from closing mills, are available. Land is cheap. And most importantly, there's a gap in the market—British imports are declining due to the Swadeshi movement, but no Indian mill has successfully filled the superfine segment.

In late 1930, the brothers begin pooling resources. They approach fellow merchants in Ahmedabad's tight-knit business community, many of whom think they're mad. Start a superfine mill during a depression? When Gandhi himself is calling for homespun khadi? But the Lalbhai name carries weight—generations of successful trading, a reputation for honoring contracts even when it hurts, and Kasturbhai's track record at Raipur Mills.

They name the venture after Kasturbhai's eldest son, Arvind—a Sanskrit name meaning "lotus," symbolizing purity emerging from muddy waters. It's an apt metaphor for starting a premium textile business during economic catastrophe. As 1930 ends and 1931 begins, construction starts on what will become one of India's most storied industrial enterprises, built on a contrarian bet that quality, not just quantity, will define India's industrial future.

The pre-founding context reveals something crucial about Arvind's DNA: this wasn't a startup in the modern sense but the culmination of three centuries of merchant evolution, from Mughal jewelers to colonial-era industrialists to independence-era nation-builders. That long view—thinking in generations, not quarters—would prove to be Arvind's secret weapon through every crisis and transformation that followed.

III. Founding & Early Years: The Superfine Gamble (1931–1960s)

The first loom at Arvind Mills begins operation on a sweltering May morning in 1931. Kasturbhai Lalbhai stands watching as superfine cotton yarn—40s count, twice as fine as what most Indian mills dare attempt—feeds into Swiss-made Northrop looms. The machinery alone cost more than some entire mills. Every component was handpicked: Platt Brothers carding machines from England, ring frames from Toyota Automatic Loom Works in Japan, humidification systems from Carrier Corporation. While other mills make do with second-hand equipment bought cheap from closing British factories, Arvind installs only the latest technology.

The product range seems almost delusional for a startup mill: dhoties and sarees, yes, but also mulls, dorias, crepes, shirtings, lingerie fabrics, coatings, printed lawns, voiles, cambrics, twills, and gaberdines. Each requires different technical specifications, different training, different quality control. Most mills master one, maybe two fabric types. Arvind attempts to master them all simultaneously.

The early months are brutal. Superfine yarn breaks constantly in Ahmedabad's dry heat—humidity control becomes an obsession, with workers manually spraying water every hour until proper systems are installed. The mill's first technical director, recruited from Manchester at enormous expense, quits after three months, declaring Indian workers incapable of handling superfine production. Local retailers refuse to stock Arvind fabrics, convinced Indian consumers won't pay premium prices for Indian-made superfines.

But Kasturbhai persists with almost mystical conviction. He personally supervises production for 14-hour days, teaching workers techniques he learned in Manchester. When retailers refuse to stock Arvind fabrics, he opens his own showrooms. When the British technical director quits, he promotes a young Indian engineer, Chimanlal Parikh, who becomes legendary for innovations like adjusting loom speeds for Indian climate conditions.

By 1934, something remarkable happens: Arvind Mills becomes recognized as one of the foremost textile units in the country. The transformation is so rapid it seems almost miraculous. What changed? The answer lies in a quality breakthrough that even surprised Kasturbhai. Arvind's superfine fabrics aren't just matching imported quality—in some categories, they're exceeding it. The combination of premium equipment, obsessive quality control, and unexpected innovations (like using longer-staple Indian cotton varieties previously considered unsuitable) creates fabrics with a distinctive hand-feel that becomes Arvind's signature.

The real validation comes in 1935. Swiss textile importers—from Switzerland, the global capital of luxury textiles—place orders for Arvind's butta voiles. These are intricate fabrics with woven patterns that require absolute precision. For Swiss buyers to import textiles from India reverses centuries of trade flow. By 1938, Arvind fabrics are being exported to the United Kingdom itself, the colonial power that had destroyed India's textile industry a century earlier. The symbolism isn't lost on anyone.

World War II transforms everything. British textile imports cease almost entirely. The colonial government, desperate for military supplies, places massive orders for tent fabrics, uniforms, and parachute cloth. Arvind, with its superfine capabilities, can produce fabrics other Indian mills cannot. Profits soar, but Kasturbhai makes a curious decision: instead of maximizing wartime profits like his competitors, he invests heavily in vertical integration.

In 1952, he establishes Atul Products Ltd, India's first indigenous dyestuff and chemical plant. This seems like dangerous diversification—chemicals and textiles require completely different expertise. But Kasturbhai sees what others miss: India imports nearly all its dyes from Germany and Britain. Every Indian textile mill is vulnerable to supply disruption. By controlling dye production, Arvind can guarantee consistent color quality while competitors struggle with irregular imported dyes.

The vertical integration philosophy deepens through the 1950s. Arvind builds its own sizing plants (for treating yarn before weaving), printing facilities (for fabric designs), and even machinery workshops (for maintaining imported equipment without foreign technicians). Each addition seems expensive and unnecessary to contemporary observers. Why not just outsource to specialists? But Kasturbhai is playing a longer game—building capabilities that will compound over decades.

The numbers tell the story: by 1960, Arvind operates 50,000 spindles and 1,500 looms, employing over 5,000 workers. But raw scale isn't what distinguishes Arvind—several mills are larger. It's the technical sophistication. Arvind can produce fabrics with thread counts that other mills consider impossible. Their quality control laboratory, established in 1955, rivals those in Manchester and Osaka. Foreign buyers often can't believe the fabrics come from India.

The human dimension deserves attention. Kasturbhai builds Arvind Township, providing housing, schools, and healthcare for workers—not unusual for Indian industrialists, but the quality is exceptional. The company establishes technical training institutes, sending promising workers to Japan and Europe for advanced training. This investment in human capital seems extravagant, but it creates fierce loyalty and institutional knowledge that becomes Arvind's real moat.

A telling episode from 1959 captures the Arvind ethos. A large export order for superfine voiles fails quality inspection—microscopic inconsistencies invisible to the naked eye but detected by laboratory testing. The financial hit of rejecting the entire production run would be severe. Every manager argues for shipping the order—the customer will never notice. Kasturbhai personally inspects the fabric, then orders the entire batch destroyed. "Our reputation is worth more than any single order," he declares. The story becomes legend within Arvind, establishing a quality culture that transcends procedures and manuals.

By the 1960s, Arvind has achieved something remarkable: it's simultaneously one of India's most technically advanced mills and one of its most profitable. The superfine gamble has paid off spectacularly. But success brings new challenges. The License Raj is tightening, making expansion difficult. New synthetic fibers are disrupting global textile markets. And Kasturbhai is aging, raising succession questions.

Most importantly, a new generation is coming of age—including Kasturbhai's son Sanjay, born in 1944, who will soon return from America with radical ideas about denim, branding, and transforming Arvind from a textile manufacturer into something unprecedented in Indian business: a fashion powerhouse. The superfine foundation is built, but the real revolution is about to begin.

IV. The "Reno-vision" Revolution: India's Denim Story (1980s–1990s)

Sanjay Lalbhai steps off the plane at Bombay Airport in 1973, fresh from his MBA at Columbia Business School, carrying something unusual in his luggage: five pairs of blue jeans. Not for himself—market research. He's spent two years in New York watching a fashion revolution unfold. Jeans, once workwear for cowboys and miners, have become the uniform of youth rebellion, worn by everyone from Columbia students to Wall Street bankers on weekends. In India, jeans are virtually unknown, imported only through smuggling or diplomatic pouches, selling for astronomical prices in black markets.

Sanjay's return to Arvind Mills isn't smooth. The old guard—men who've spent decades perfecting superfine cotton—can't understand his obsession with this thick, coarse, indigo-dyed fabric. "You want us to make coolie cloth?" one senior manager asks, using the derogatory term for laborer's clothing. The Indian market seems impossible: jeans require special washing, they're associated with Western decadence, and at projected price points, they'd cost more than most Indians earn in a month.

But Sanjay sees what others miss. India's demographic pyramid is inverting—by 1985, over 50% of Indians will be under 25. Liberalization is coming, however slowly. Indian cinema is beginning to show heroes in jeans. And crucially, he's identified a technical gap: denim production requires completely different capabilities from traditional textiles—rope dyeing, special weaving techniques, enzyme washing. No Indian mill has mastered this. If Arvind can crack denim, they'll have years of competitive advantage.

The "Reno-vision" program—Sanjay's modernization initiative—begins in 1980 with what seems like corporate madness. While other textile mills are cutting costs to survive recession, Arvind invests $50 million (massive for an Indian company then) in European denim technology. They import an entire production line from Switzerland's Sulzer Ruti, including India's first rope dyeing range. The equipment is so specialized that Arvind must send 30 engineers to Europe for six months of training.

The same year, Arvind launches Flying Machine—India's first indigenous denim brand. The name is deliberate, evoking freedom, modernity, and subtle rebellion. The logo, sketched by Sanjay himself, shows stylized wings. But the product launch is a disaster. The jeans are technically perfect but culturally tone-deaf. They're exact copies of American styles—too tight for Indian bodies, too long for average Indian height, with back pockets positioned for Western posteriors. First-year sales are abysmal.

The failure becomes a learning laboratory. Arvind conducts India's first systematic anthropometric study, measuring thousands of Indian bodies to understand proportions. They discover Indian men have shorter legs relative to torso length, different waist-to-hip ratios, and strong preferences for higher rises. The redesigned Flying Machine jeans, launched in 1982, fit Indian bodies perfectly. Sales explode.

But Sanjay isn't satisfied with just one brand. In 1985, Arvind makes a bizarre diversification, entering electronics with an EPABX (electronic private branch exchange) plant and marketing pharmaceutical products and television sets under the Pyramid brand. This seems like dangerous distraction, but there's method to the madness. The electronics venture gives Arvind experience with retail distribution and brand building outside textiles. The lessons learned—about dealer networks, consumer financing, advertising—will prove invaluable for the denim business.

1986 marks the turning point. Arvind becomes the first Indian company to bring globally accepted denim variations—not just basic blue but yarn-dyed shirting fabrics and wrinkle-free gaberdines. The technical achievement is staggering. Wrinkle-free treatment requires precise chemical application that most developed-country mills struggle with. Arvind masters it using equipment modified in-house, creating fabrics that return to shape even after crushing.

The modernization program accelerates in 1987 with an audacious goal: triple denim production within four years. This requires not just new machinery but revolutionizing every aspect of operations. Arvind pioneers "open-end spinning" in India, a technology that produces denim yarn 5-10 times faster than traditional ring spinning. They install India's first computerized shade-matching system, ensuring consistent indigo coloring across batches. Most radically, they create a dedicated denim research center, hiring textile PhDs to develop new washes, finishes, and fabric constructions.

By 1991, Arvind reaches a milestone that seemed impossible a decade earlier: 100 million meters of denim annually, making them the fourth-largest denim producer globally. Only Cone Mills (USA), Kurabo (Japan), and Swift Textiles (USA) produce more. But unlike these competitors focused on their domestic markets, Arvind has a unique position—they're simultaneously building Indian denim consumption and becoming a major exporter.

The export strategy is particularly clever. Rather than competing on price like other Asian mills, Arvind positions itself as the "innovation partner" for global brands. When Levi's wants a new wash technique, Arvind's lab develops it. When Gap needs sustainable denim, Arvind creates organic cotton variants. This technical collaboration creates switching costs—brands become dependent on Arvind's innovation capabilities, not just production capacity.

The domestic brand portfolio expands strategically through the late 1980s. Ruf & Tuf targets rural markets with durable, affordable jeans that can withstand Indian washing methods (beating on rocks, harsh detergents). Newport aims at urban professionals with formal-casual crossover styles. Each brand gets distinct positioning, distribution, and price points—sophisticated market segmentation that Indian companies rarely attempted then.

A pivotal moment comes in 1989. Levi's, the global denim giant, is evaluating Indian partners for local production. Every major textile company pitches aggressively. Arvind wins not through lowest pricing but through what Levi's executives later call "unprecedented technical depth." During factory visits, Arvind engineers explain not just how they make denim but why specific technical choices improve quality—from enzyme concentrations in stone-washing to optimal cotton blend ratios. Levi's signs an exclusive manufacturing agreement, validating Arvind's transformation from commodity producer to technical partner.

The numbers by decade-end are staggering: denim revenues have grown 50x since 1980, exports account for 40% of production, and Arvind controls nearly 60% of India's organized denim market. But the real achievement is cultural. Arvind has made jeans acceptable, even aspirational, for middle-class Indians. Flying Machine becomes the first Indian brand many consumers trust for Western wear. The company has created a category that didn't exist a decade earlier.

Yet success brings complexity. By 1991, Arvind is simultaneously a superfine cotton producer, denim manufacturer, electronics assembler, and brand owner. The organization struggles with focus. Different businesses require different capabilities, capital allocation becomes contentious, and management attention is scattered. These tensions will drive the strategic decisions of the next decade—whether to remain a diversified conglomerate or focus on core strengths, whether to prioritize manufacturing or brand building, whether to serve global giants or build indigenous brands.

As the 1990s begin, with India on the cusp of economic liberalization, Arvind stands at an inflection point. They've proven Indian companies can innovate, not just imitate. They've built global-scale manufacturing with local market understanding. Most importantly, they've shown that technical excellence and brand building aren't mutually exclusive. The question now is how to leverage these capabilities in an economy about to open to global competition. The answer will transform Arvind from a textile company into something unprecedented—a vertically integrated fashion-to-retail powerhouse that somehow also makes technical textiles for spacesuits and water treatment systems for smart cities.

V. Scaling the Denim Empire & Brand Building (1990s–2000s)

The year 1991 changes everything. India's foreign exchange reserves have dwindled to barely three weeks of imports. The IMF demands economic liberalization as a bailout condition. Finance Minister Manmohan Singh announces sweeping reforms—import licenses abolished, foreign investment welcomed, the License Raj dismantled. For Arvind, liberation and existential threat arrive simultaneously. Global brands can now enter India directly. Why would Levi's or Gap need an Indian partner when they can set up their own operations?

Sanjay Lalbhai's response is counterintuitive: instead of protecting manufacturing margins, he invites competition inside. In 1993, Arvind signs transformative joint ventures with VF Corporation (owner of Lee and Wrangler) and Cluett Peabody (Arrow shirts), creating VF Arvind Brands and Arrow Arvind Brands. The deals are structured brilliantly—Arvind provides manufacturing, distribution, and local knowledge while partners bring brands and global design capabilities. Rather than simple licensing, these are true partnerships with shared equity and aligned incentives.

The Arrow deal particularly showcases Arvind's evolution. Arrow, the inventor of the detachable collar, represents American professional fashion—crisp, conservative, aspirational. But directly importing American styles would fail, as Flying Machine's initial launch proved. Arvind's team spends months studying Indian office culture: the preference for full-sleeves even in summer (status signaling), the need for fabrics that survive harsh washing, the importance of pocket placement for pens (Indian professionals still handwrite extensively). The "Indianized" Arrow shirts, maintaining brand DNA while adapting to local needs, become instant hits.

1994 brings organizational revolution. Arvind divides operations into three focused divisions: textiles (manufacturing), telecom (the electronics experiment, now focused on telecommunications equipment), and garments (branded apparel and retail). Each gets separate P&L responsibility, capital allocation, and management teams. It's matrix organization before Indian companies typically attempt such complexity. The structure enables entrepreneurial speed while maintaining scale advantages.

The innovation pipeline accelerates remarkably. 1995 sees Arvind launch India's first "ready-to-stitch" jeans kit under Ruf & Tuf—pre-cut denim pieces with thread and instructions, targeting India's massive tailoring market. It's genius localization: most Indians still get clothes tailored rather than buying ready-made, but lack access to quality denim fabric. The kit democratizes jeans ownership for millions who can't afford branded ready-made versions.

But Arvind's smartest move is anticipating and solving a problem nobody else sees coming. As international brands flood India, counterfeit products explode. By 1996, fake Levi's and Arrow products probably outsell genuine ones. Most companies respond with legal action—ineffective in India's overburdened courts. Arvind takes a different approach. In 1997, they establish India's first corporate anti-piracy cell, not relying on law enforcement but using technology and distribution strategy.

The anti-piracy innovation is multifaceted. Arvind develops holographic labels, nearly impossible to counterfeit with 1990s technology. They create a telephone verification system—customers can call a number and input a code to verify authenticity. Most cleverly, they adopt a franchisee system for manufacturing and distribution, essentially co-opting potential counterfeiters. Small manufacturers who might produce fakes are instead given legitimate licenses to produce for local markets, with Arvind providing fabric and quality control. It's judo strategy—using opponents' strength against them.

By 1998, the strategy's success is undeniable: Arvind Mills emerges as the world's third-largest denim manufacturer, producing 110 million meters annually. Only Cone Mills and Swift Textiles produce more, but Arvind's trajectory is steeper. They're adding capacity faster than any competitor, with plans for 150 million meters by 2000. International customers now include virtually every major brand—Gap, Tommy Hilfiger, Polo Ralph Lauren, Diesel, Lee, Wrangler. Arvind has become the "Intel Inside" of denim—invisible to consumers but essential to brands.

The retail revolution begins in earnest in 1999 with "The Arvind Store" concept. These aren't just brand outlets but "solution stores" offering everything from fabrics to ready-made garments to customization services. A customer can buy Arrow shirts, get Flying Machine jeans altered, purchase fabric for tailoring, even design custom clothing. It's an omnichannel approach before the term exists, recognizing that Indian consumers don't shop in rigid categories.

The new millennium brings new ambitions. In 2000, Arvind launches Megamart, India's first value fashion retail chain. While competitors chase premium segments, Arvind recognizes a massive underserved market: middle-class consumers who want fashion but can't afford mall brands. Megamart offers private label clothing at 30-50% below branded equivalents, using Arvind's manufacturing scale to maintain quality while cutting costs. Within two years, Megamart operates 30 stores, pioneering organized value retail in India.

International expansion accelerates through technical partnerships rather than simple exports. Arvind establishes design studios in New York, Milan, and Tokyo, not for vanity but for collaboration. When Japanese brand Uniqlo wants to develop new selvage denim, Arvind's Tokyo studio works directly with their designers. When Italian luxury brands need organic cotton variants, the Milan studio coordinates with Arvind's agricultural programs. These studios become listening posts, identifying trends before they reach mass markets.

The brand portfolio strategy becomes increasingly sophisticated. By 2005, Arvind manages over 30 brands across price points and categories. Flying Machine targets youth, Arrow serves professionals, Newport offers casual Friday options, Excalibur provides premium European styling, Ruf & Tuf dominates rural markets. But this isn't random proliferation—each brand fills a specific gap, uses distinct distribution channels, and targets different consumer psychographics. The portfolio approach hedges risks while maximizing market coverage.

A critical innovation often overlooked: Arvind pioneers "market-making" in Indian fashion. When research shows Indian men don't understand "smart casual" dress codes, Arvind launches education campaigns—fashion shows in offices, style guides in newspapers, partnerships with Bollywood stylists. They're not just selling products but creating categories, teaching consumers how to dress for occasions that didn't exist in traditional Indian society.

The manufacturing backbone continues strengthening. By 2006, Arvind operates one of the world's most integrated denim facilities in Santej, Gujarat—spanning 500 acres, processing everything from cotton ginning to finished garments. The facility produces 130 million meters of denim annually, but capacity alone doesn't capture its sophistication. Arvind can produce 10,000 unique fabric variations, offers 50 different washing techniques, and maintains consistent quality whether producing 100 or 100,000 pieces.

Supply chain innovation becomes a competitive weapon. Arvind develops "speed to market" capabilities rivaling European fast fashion. Using advanced planning systems and modular manufacturing, they can move from design to retail in 45 days—remarkable for a company operating in India's infrastructure constraints. This speed enables them to serve both traditional wholesale (two seasons annually) and fast fashion (new products monthly) simultaneously.

But the most prescient move is sustainability investment, beginning in 2003 before ESG becomes fashionable. Arvind develops organic cotton supply chains, working directly with farmers to eliminate pesticides. They pioneer water recycling systems, reducing consumption by 40% per meter of fabric. They create enzyme-based washing techniques eliminating harmful chemicals. Initially, these seem like costly experiments. By decade's end, as global brands face sustainability pressure, Arvind's early investments become massive competitive advantages.

The 2008 financial crisis tests everything. Global demand collapses, brands cancel orders, and credit markets freeze. Many textile companies fail. Arvind survives through portfolio diversification—when exports crash, domestic brands cushion the blow. When premium segments shrink, value retail grows. The crisis validates Arvind's complex, multi-brand, multi-channel strategy that seemed inefficient during boom times.

As the decade ends, Arvind faces a strategic crossroads. They've built incredible complexity—manufacturing to retail, cotton to synthetics, India to global, value to luxury. The business has become unwieldy, with different segments requiring different strategies, capital structures, and management capabilities. The next chapter will involve difficult choices about focus, structure, and identity. Should Arvind remain an integrated conglomerate or split into focused entities? The answer will reshape not just Arvind but provide a template for how traditional Indian companies can evolve for the 21st century.

VI. The Modern Conglomerate & Demergers (2000s–2017)

The boardroom at Arvind's Ahmedabad headquarters, December 2007. Sanjay Lalbhai faces his most complex strategic decision yet. Arvind has grown into an unwieldy giant—₹3,000 crore in revenues, but spanning textiles, retail, real estate, engineering, and telecom. Investment analysts can't understand the company. The stock trades at a "conglomerate discount," valued less than the sum of its parts. Private equity firms circle, offering to buy individual divisions. Most critically, each business needs different capital structures, growth strategies, and management cultures. The textile manufacturing business requires steady capital investment and operational excellence. The retail business needs rapid expansion and brand building. Advanced materials demand R&D investment with long payoff periods. Trying to manage all simultaneously is like conducting three orchestras playing different symphonies.

The first move comes in 2008: Arvind Mills Limited officially becomes Arvind Limited. It's not mere rebranding but a declaration—we're no longer just a mills company but a diversified corporation. The same year brings painful restructuring. The telecom equipment business, never truly synergistic, is shut down. The electronics adventure that began in 1985 finally ends, with Arvind accepting that convergence has limits.

But even as they exit non-core ventures, Arvind doubles down on adjacencies that leverage textile expertise. 2011 marks a pivotal entry into technical textiles with the Advanced Materials Division (AMD). This isn't random diversification—it's applying five decades of fabric expertise to new problems. The division focuses on human protection fabrics (for firefighters, soldiers, industrial workers), industrial products (filtration, composites), and automotive textiles (seat fabrics, interior components). The same capabilities that produce premium denim—precision weaving, chemical treatment, quality control—translate into bulletproof fabrics and fire-resistant materials.

The AMD strategy reveals sophisticated thinking. While commodity textiles face margin pressure, technical textiles command premium pricing. A square meter of denim might sell for $3-5. The same area of ballistic fabric sells for $50-100. The customers—governments, aerospace companies, automotive manufacturers—value performance over price. It's a completely different game from fashion retail, but one where Arvind's technical capabilities provide genuine differentiation.

The real action comes in 2011 with the VF Arvind Brands transaction. VF Corporation, wanting greater control over Indian operations, offers to buy Arvind's 40% stake for ₹257 crore. Many see this as retreat—abandoning a successful joint venture. But Sanjay Lalbhai sees liberation. The partnership has served its purpose: Arvind learned brand building, VF established Indian presence. Now both need freedom to pursue different strategies. The sale provides capital while eliminating conflicts between manufacturing for partners versus building proprietary brands.

International joint ventures multiply, but with careful selection. A partnership with Japan's Epsilon creates Arvind-Epsilon Advanced Materials, targeting automotive composites. Another with Germany's A&E brings thread technology. Each partnership fills specific capability gaps rather than just providing market access. It's technology transfer disguised as joint ventures, systematically acquiring capabilities that would take decades to build independently.

The portfolio complexity reaches breaking point by 2015. Arvind now operates: - Textiles: Denim, woven, knits, with 200+ million meters capacity - Brands & Retail: 30+ brands, 1000+ stores (owned and franchised) - Advanced Materials: Technical textiles, composites, automotive fabrics - Real Estate: Developing residential and commercial projects on mill lands - Engineering: Precision engineering components through subsidiary operations

Each business has different economics. Textiles is capital-intensive with 15-20% ROCE. Brands generate 25-30% ROCE but need marketing investment. Real estate provides lumpy but high returns. Advanced materials require patient capital with J-curve returns. Managing these under one structure becomes impossible—capital allocation conflicts arise constantly, management attention fragments, and investors can't properly value the company.

The solution, announced in 2016 and executed in 2017, is radical: demerge into focused entities. It's India's most complex corporate restructuring, involving:

Arvind Fashions Limited: Takes the brands and retail business—Arrow, US Polo, Tommy Hilfiger, Calvin Klein, Flying Machine, plus retail operations. This becomes a pure-play fashion company, asset-light, focused on brand building and retail expansion. The equity story clarifies: a fashion house riding India's consumption boom.

Anup Engineering Limited: Separates the engineering business, manufacturing critical process equipment for fertilizer, petrochemical, and refinery sectors. This hidden gem, obscured within Arvind's complexity, can now pursue industrial customers without competing for capital with fashion businesses.

Arvind Limited (continuing entity): Retains textiles and advanced materials—the manufacturing DNA. This focuses on B2B relationships, technical innovation, and operational excellence. The story becomes India's technical textile champion, serving global brands while pioneering new materials.

The demerger execution is masterful. Shareholders receive proportional stakes in all three entities—no value destruction, just value crystallization. Each company gets appropriate capital structure: Arvind Fashions with higher debt for retail expansion, Anup Engineering with conservative balance sheet for cyclical industrial markets, Arvind Limited with moderate leverage for steady capacity expansion.

But the real genius is cultural. Each entity develops distinct organizational DNA: - Arvind Fashions becomes young, aggressive, marketing-driven—hiring from FMCG companies and startups - Anup Engineering remains engineering-focused, quality-obsessed—the culture of precision manufacturing - Arvind Limited balances innovation with operational excellence—technically sophisticated but commercially pragmatic

Post-demerger performance validates the strategy. Arvind Fashions' valuation multiples expand as investors appreciate the pure-play fashion story. Anup Engineering, previously invisible, gains institutional following. Arvind Limited attracts different investors—those seeking steady manufacturing businesses with technical moats.

The 2017 demerger represents more than corporate restructuring—it's a template for how Indian conglomerates can evolve. Rather than remaining sprawling empires with unclear focus (the Tata or Reliance model), Arvind shows how to create focused entities while maintaining family control. Each Lalbhai family member takes leadership of different entities, maintaining dynasty continuity while enabling professional management.

The restructuring also enables new growth vectors. Arvind Limited, freed from retail capital needs, accelerates advanced materials investment. They develop fabrics for Indian military modernization, materials for renewable energy infrastructure, and composites for aerospace applications. The company becomes a critical supplier for India's strategic programs—their fabrics protect soldiers in Siachen, their composites strengthen indigenous aircraft.

Meanwhile, Arvind Fashions pursues aggressive expansion, launching online-first brands, experimenting with subscription models, and building India's largest fashion retail portfolio. Unencumbered by manufacturing assets, they can pivot quickly—critical in fast-changing fashion markets. When COVID-19 arrives in 2020, Arvind Fashions rapidly shifts online while manufacturing-heavy competitors struggle.

The demerger saga teaches valuable lessons about corporate evolution. Sometimes the best way to preserve a legacy is to divide it thoughtfully. By splitting into focused entities, Arvind multiplies value creation potential while reducing execution complexity. It's financial engineering in service of operational excellence—using structure to enable strategy rather than constrain it.

As 2017 ends, the three Arvind entities begin independent journeys, each carrying different parts of the original DNA. But the story is far from over. The fourth generation of Lalbhais is taking charge, bringing Silicon Valley thinking to Ahmedabad mills, digital transformation to traditional businesses, and global ambitions to Indian companies. The next chapter will test whether the Lalbhai legacy of innovation and institution-building can survive generational transition and digital disruption.

VII. The Fourth Generation & Digital Transformation (2010s–Present)

Kulin Lalbhai returns to Ahmedabad in 2009, his Harvard MBA fresh, his mind buzzing with case studies of digital disruption. The 33-year-old faces a peculiar challenge: he's heir to a textile empire just as software begins eating the world. His classmates are joining Google and Goldman Sachs. He's joining a company that makes physical fabric in an increasingly digital economy. But Kulin sees what others miss—the intersection of atoms and bits, where physical products meet digital intelligence, might be the most interesting space in business.

His first move seems minor but proves transformative. In 2010, Kulin launches a "digital lab" within Arvind—just five engineers tasked with experimenting. No KPIs, no revenue targets, just exploration. They build India's first virtual fabric library, digitizing thousands of swatches so designers worldwide can browse Arvind's materials online. They experiment with RFID tags for inventory tracking. They prototype an app letting customers visualize how fabrics look as finished garments. Small experiments, but they begin shifting Arvind's culture from pure manufacturing to manufacturing-plus-intelligence.

The breakthrough comes in 2014 with Creyate (creative + create), India's first true custom clothing platform. While competitors offer basic customization (choosing collar styles or monograms), Creyate enables radical personalization. Customers design shirts from scratch—selecting fabrics, patterns, fits, and details through an AI-powered interface that ensures aesthetic coherence. The platform connects directly to Arvind's production systems, enabling single-piece manufacturing at near-mass production costs.

The technology stack behind Creyate is sophisticated. Machine learning algorithms predict fit based on a few measurements, reducing returns by 60%. Computer vision systems inspect finished garments, ensuring handmade quality at digital speed. Dynamic pricing algorithms balance demand across production capacity. It's Industry 4.0 implemented not in Germany or Japan but in Gujarat, proving Indian manufacturers can lead digital transformation.

But Kulin's ambitions extend beyond consumer-facing innovation. He recognizes that Arvind's B2B relationships—with Gap, H&M, Zara—are ripe for digital enhancement. In 2015, Arvind launches a supplier portal that seems mundane but revolutionizes operations. Brands can track orders in real-time, modify specifications mid-production, and collaborate on designs through virtual sampling. What once required weeks of physical samples and courier shipments now happens in hours through digital twins.

The advanced materials division becomes an unexpected digital frontier. When developing fabrics for automotive clients, Arvind creates simulation software predicting how materials perform under stress, heat, and wear. Instead of producing hundreds of physical prototypes, they test thousands of virtual variants, only manufacturing the most promising options. This reduces development time from months to weeks while improving success rates. German automotive giants, initially skeptical of Indian technical capabilities, become believers when Arvind's simulations prove more accurate than their own.

2018 brings the most ambitious technical venture: a joint venture with Adient for automotive fabrics. But this isn't just manufacturing—it's creating "smart fabrics" with embedded sensors. Seat fabrics that monitor driver alertness, detect occupant weight for airbag calibration, even measure vital signs for health monitoring. It sounds like science fiction, but prototypes are already in testing with major automakers. The convergence of textiles and electronics, attempted crudely in the 1980s, finally makes sense with modern technology.

The organizational transformation proves harder than technical innovation. Arvind's workforce—average age 45, many with decades of textile experience—initially resists digital tools. Kulin's approach is patient but persistent. Rather than forcing change, he creates "digital champions" in each department—respected veterans who embrace new tools and evangelize to peers. He establishes "Arvind University," an internal training program where workers learn everything from basic computer skills to advanced data analysis.

The investment in human capital pays unexpected dividends. Shop floor workers, empowered with tablets showing real-time production data, begin suggesting process improvements that engineers missed. Quality control inspectors, trained in statistical analysis, identify defect patterns that prevent future problems. The digital transformation becomes democratized, driven by thousands of small improvements rather than top-down mandates. Sustainability becomes not just compliance but competitive advantage. Having successfully implemented Zero Liquid Discharge and utilizing solely recycled water in manufacturing processes, Arvind transforms from water consumer to water steward. The 2019 partnership with Gap Inc. creates something unprecedented: a new innovation center designed around a wastewater treatment plant established in 2019. A first-of-its-kind initiative by Gap Inc. and Arvind Limited to save 8 million liters of fresh water per day, or 2.5 billion liters of water annually at Arvind's Denim manufacturing facility.

The sustainability journey that began as cost-cutting becomes market differentiation. Patagonia, one of the most reputed global brands that champions sustainable fashion, sources almost its entire denim requirements from Arvind. When European brands face pressure to reduce environmental impact, Arvind's decade-old investments in organic cotton, water recycling, and chemical-free processing become invaluable. The company that once competed on cost now wins contracts through environmental credentials. But Kulin's leadership reveals unexpected depth. The fifth-generation scion (as per LinkedIn, though some sources say fourth generation) doesn't just digitize existing processes—he reimagines what a textile company can be. Kulin, a fifth-generation family business leader and Vice Chairman of Arvind Limited oversees the new initiatives for the Arvind Group's consumer and digital businesses including Arvind Fashions, Arvind Smartspaces and Syntel Telecom. His Stanford electrical engineering degree and McKinsey experience bring Silicon Valley rigor to Santej mills.

The real estate venture, Arvind Smartspaces, exemplifies this evolution. Rather than simply selling surplus mill land, Arvind develops integrated townships, commercial complexes, and smart cities. He has also been closely involved in the Group's foray into real estate (Arvind Smartspaces), with over 15 Mn square feet of projects under execution. They're applying manufacturing precision to real estate development—standardized processes, quality metrics, predictable delivery. What began as monetizing excess land becomes a ₹1,000+ crore business.

The water management division represents perhaps the most audacious pivot. Arvind Envisol, established to manage the company's own wastewater, now provides solutions to other industries and municipalities. Launched in 2011, as part of Arvind Limited, the 1.3 billion USD global textile conglomerate, Arvind Envisol is a world-class water management company providing end-to-end solutions for water treatment, industrial wastewater treatment, sewage treatment and zero liquid discharge solutions at minimal costs. The patented polymeric film evaporation technology, developed for textile processing, finds applications in pharmaceuticals, chemicals, even food processing. A textile company has become a water technology company.

Arvind and Gap have cut the ribbon on a new innovation center designed around a wastewater treatment plant established in 2019. Arvind, Ltd. and Gap Inc. are doubling down on a longstanding partnership with the launch of the Global Water Innovation Center for Action (GWICA) at the Indian denim manufacturer's mill in Santej. The 18,000-square-foot facility will serve as a collaborative meeting point for manufacturers, brands, upstream suppliers, sustainability experts and environmental groups engaged in changing the way the apparel industry uses water and manages waste. The facility, inaugurated at a ceremony this week by Arvind vice chairman and executive director Punit Lalbhai and Richard Dickson, president and CEO of Gap Inc., aims to showcase technological advancements in water treatment and help the fashion sector establish best practices.

The COVID-19 pandemic becomes an unexpected accelerator. Within weeks of lockdown, Arvind pivots production to PPE kits, leveraging their human protection fabric expertise. The digital initiatives, once nice-to-have, become essential—virtual showrooms replace physical visits, AI-powered demand forecasting prevents inventory buildup, automated quality control reduces human contact. The crisis validates years of digital investment.

Current financial performance reflects this transformation's complexity. Mkt Cap: 7,519 Crore (down -29.3% in 1 year) · Revenue: 8,505 Cr · Profit: 378 Cr · The company has delivered a poor sales growth of 2.48% over past five years. · Company has a low return on equity of 10.1% over last 3 years. · Promoter Holding: 39.6% The numbers disappoint—growth has stalled, returns remain modest. But beneath aggregated financials, transformation continues. The advanced materials division grows at 20%+ annually. Digital initiatives improve margins even as revenues plateau. Sustainability investments, initially dilutive, now command premium pricing.

The generational handoff progresses smoothly. Punit Lalbhai, Vice Chairman & Executive Director and Kulin Lalbhai, Executive Director, Arvind Ltd had a courtesy meeting with Shri Yogi Adityanathji, Hon'ble Chief Minister of Uttar Pradesh to apprise him about the company's upcoming Garmenting unit in Varanasi, bringing approximately Rs 100 cr investment and direct employment for approximately 2000 women. The brothers divide responsibilities—Punit focusing on manufacturing and sustainability, Kulin on consumer businesses and digital transformation. It's collaborative leadership for a complex conglomerate.

Looking forward, Arvind faces fundamental questions. Can a 93-year-old textile company truly become a technology company? Can manufacturing excellence translate into brand power? Can family control survive professional management needs? The answers remain uncertain, but the trajectory is clear—from making fabric to creating solutions, from serving brands to building platforms, from industrial heritage to digital future.

The fourth (or fifth) generation hasn't abandoned textiles—they've expanded the definition of what a textile company can be. When your fabric protects astronauts, filters industrial emissions, and generates fashion trends, you're no longer just a mills company. You're an advanced materials innovator that happens to have textile heritage. It's a transformation that would make great-grandfather Kasturbhai proud—and probably confused.

VIII. Playbook: The Lalbhai Way

There's a photograph in Arvind's headquarters that captures everything: Kasturbhai Lalbhai presenting a check to Vikram Sarabhai for establishing IIM Ahmedabad in 1961. The amount—₹50 lakhs—was enormous for a textile company then. Kasturbhai's son Sanjay, barely 17, stands watching. The message was clear: business success without institution-building is hollow victory. Six decades later, that same philosophy drives Kulin Lalbhai as he builds innovation centers that competitors can visit, creating industry infrastructure rather than proprietary advantage.

This is the first principle of the Lalbhai playbook: Think in centuries, not quarters. When you trace your lineage to 1590, when your family has survived Mughal decline, British colonialism, Partition, and License Raj, you develop a particular relationship with time. The Lalbhais don't chase trends; they identify tectonic shifts and position decades ahead. Superfines during the Depression. Denim before liberalization. Sustainability before ESG. Advanced materials before Make in India. Each bet seems premature, even foolish, until suddenly it's obvious.

The long-term thinking manifests in capital allocation. While peers maximize current returns, Arvind consistently overinvests in capabilities that won't pay off for years. The 1952 dye plant—why backward integrate into chemicals? The 1987 R&D center—why does a mill need PhDs? The 2003 organic cotton program—who cares about pesticide-free fabric? The 2011 water recycling—isn't groundwater free? Each investment drags down contemporary returns but compounds into competitive moats.

The second principle: Timing transitions over optimization. The Lalbhais have an uncanny ability to sense inflection points and move decisively. Not first-mover advantage—that's for venture capitalists. Instead, "fast-second advantage"—letting pioneers establish categories, then entering with superior execution. They weren't India's first textile mill, but the first successful superfine mill. Not the first to import denim technology, but the first to localize it. Not the first in branded apparel, but the first to build portfolio scale.

Consider the 2017 demerger timing. Most conglomerates demerge during crisis, forced by debt or activism. Arvind demerged from strength, recognizing that complexity would eventually destroy value. They moved before markets forced them, maintaining control over structure and timing. It's proactive evolution rather than reactive restructuring.

The third principle: Build through partnerships, not alone. From Swiss machinery suppliers in 1931 to Gap Inc. in 2019, Arvind consistently partners for capability building. But these aren't passive licensing deals or financial investments. Each partnership involves deep technical collaboration, knowledge transfer, and capability development. The VF Corporation joint venture didn't just bring Lee jeans to India—it taught Arvind retail operations, brand management, and consumer marketing. The Japanese automotive partnerships don't just supply fabric—they embed Arvind engineers in Toyota plants, learning lean manufacturing and quality systems.

This partnership philosophy extends beyond business. Arvind's sustainability initiatives involve farmers, NGOs, competitors, even critics. We have collaborated with fellow Fashion for Good partners, Materra, Kering and PVH Corp, on a consortium project to grow climate-resilient cotton in a sustainable way wherein water and fertiliser usage is reduced by 80%, and it is completely free of insecticides. Our structured efforts on promoting sustainable cotton farming, which includes regenerative, organic, inconversion organic and better cotton initiatives, have resulted in a three-fold growth in the number of farmers as well as the area under sustainable agriculture during the reporting period. They share innovations openly—the GWICA water center invites competitors to learn. It seems naive, but creates ecosystem effects. When Arvind improves cotton farming, input quality improves for everyone. When they train workers, industry skill levels rise. Enlightened self-interest disguised as altruism.

The fourth principle: Vertical integration as capability platform. Unlike conglomerates that diversify randomly, Arvind's expansion follows capability logic. Textile manufacturing teaches chemical processing, leading to dyestuffs. Dyeing expertise enables technical textiles. Technical textiles create advanced materials. Advanced materials spawn automotive components. Each business builds on previous capabilities while adding new ones, creating compounding competencies.

But vertical integration at Arvind isn't about control—it's about learning. They integrate to understand, not to capture margins. Once learning is complete, they're willing to demerge, partner, or exit. The electronics venture failed financially but taught brand building. The telecom equipment business lost money but provided B2B experience. Failures become tuition for future success.

The fifth principle: Managing complexity through structure. As businesses multiply, most conglomerates become unwieldy. Arvind's solution is organizational innovation—creating structures that enable complexity without chaos. The 1994 divisional structure. The 2008 holding company reorganization. The 2017 demerger. Each restructuring isn't just financial engineering but operational enablement, allowing different businesses to develop appropriate cultures, metrics, and strategies.

The sixth principle: CSR as strategy, not charity. The Lalbhais don't do corporate social responsibility—they do societal institution building. Education (IIM, CEPT University), healthcare (multiple hospitals), urban development (slum rehabilitation), and environmental restoration (water conservation). But this isn't philanthropy seeking recognition. It's ecosystem development ensuring sustainable business environment. Healthy businesses require healthy societies.

Mr. Lalbhai believes that addressing societal concerns and creating a long-lasting benefit to society is integral to the business strategy and a duty of every business leader. He provides strategic leadership to Arvind's CSR initiatives as Trustee to SHARDA Trust ─ the CSR arm of the company. When Arvind trains farmers in organic cultivation, they're creating supply chains. When they educate workers' children, they're building future talent. When they develop water recycling, they're ensuring production sustainability. CSR and business strategy converge.

The seventh principle: Balance tradition with innovation. Each generation must prove itself, not through revolution but evolution. Kasturbhai didn't abandon trading for manufacturing—he industrialized trading relationships. Sanjay didn't abandon textiles for fashion—he fashionized textiles. Kulin isn't abandoning manufacturing for technology—he's digitizing manufacturing. Evolution preserves institutional knowledge while enabling advancement.

This balance manifests in governance. Family members must earn leadership through external validation—education at global universities, experience at consulting firms or other companies, proven competence before authority. But family control remains sacrosanct, ensuring long-term thinking survives market pressures. It's professional management with family oversight, combining stability with competence.

The eighth principle: Quality as identity, not just standard. From superfines in 1931 to technical textiles today, Arvind consistently chooses quality over volume. This isn't just operational preference but existential philosophy. In commodity businesses, quality is the only sustainable differentiation. When Chinese competitors can match costs and Vietnamese factories can match scale, technical superiority becomes survival necessity.

But quality at Arvind transcends products. Quality of relationships—suppliers retained for decades, customers served for generations. Quality of workplace—townships that become models, training that creates careers. Quality of governance—transparency before regulations require it, ethics when no one's watching. Quality becomes culture, not just metric.

The playbook's effectiveness shows in longevity. In Indian business, three-generation survival is exceptional. Four generations is remarkable. The Lalbhais are in their fifth generation, with the sixth already in training. This isn't inherited wealth but renewed entrepreneurship, each generation building something new while preserving what matters.

Yet the playbook faces modern challenges. Digital disruption moves faster than generational transitions. Global competition intensifies while family businesses naturally move slowly. Professional managers demand equity while families want control. ESG requirements codify what Lalbhais did instinctively, adding compliance costs without competitive advantage.

The real test comes next: Can the Lalbhai playbook survive when manufacturing moves to Bangladesh, brands shift online, and artificial intelligence designs fabrics? Can century-thinking work in millisecond markets? Can partnership philosophy survive platform economics? Can quality differentiation matter when algorithms determine purchases?

The answers will determine whether Arvind reaches its centenary in 2031 as a thriving institution or historical footnote. But if history guides, the Lalbhais will find a way. They've survived every disruption by embracing it, every crisis by preparing for it, every transition by leading it. The playbook isn't rigid rules but adaptive principles, evolving while enduring.

As one senior manager puts it: "The Lalbhais don't predict the future—they prepare for multiple futures, then help create the one they prefer." It's active adaptation, not passive survival. And in Indian business, where most companies don't survive their founders, that might be the greatest innovation of all.

IX. Analysis & Investment Case

The numbers tell a sobering story. Mkt Cap: 7,519 Crore (down -29.3% in 1 year) · Revenue: 8,505 Cr · Profit: 378 Cr. The company has delivered a poor sales growth of 2.48% over past five years. Company has a low return on equity of 10.1% over last 3 years. For a company with nine decades of history, global manufacturing leadership, and fourth-generation professional management, these metrics disappoint. The stock market has rendered its verdict: Arvind trades at historical discount to book value, ignored by growth investors, too complex for value investors.

But financial statements capture only part of reality. Arvind represents a fascinating study in industrial transformation—simultaneously a global manufacturing champion and a struggling public equity. Understanding this paradox requires examining multiple, often contradictory, narratives.

The Bear Case: Structural Decline

Pessimists see terminal decline masked by financial engineering. Textile manufacturing is migrating to Bangladesh, Vietnam, and Ethiopia—countries with lower wages, better trade agreements, and government support. India's cost advantages have evaporated while infrastructure disadvantages persist. Power costs remain high, logistics inefficient, labor regulations restrictive. Why manufacture in Gujarat when Dhaka offers everything cheaper?

The branded apparel business faces different but equally severe challenges. International brands increasingly go direct-to-consumer, bypassing partners like Arvind. Tommy Hilfiger and Calvin Klein build their own Indian operations once markets mature. Meanwhile, digital-native brands like Bewakoof and Souled Store capture young consumers without manufacturing assets or retail stores. Arvind seems trapped between disappearing manufacturing margins and evaporating brand franchises.

The advanced materials division, despite promise, remains subscale. Technical textiles require massive R&D investment with uncertain returns. Global competitors like DuPont and Teijin spend more on research annually than Arvind's entire market cap. Indian defense and aerospace markets, while growing, can't match Chinese scale or American sophistication. It's a nice story that doesn't move financial needles.

Corporate governance raises questions. The 2017 demerger was supposed to unlock value—instead, all three entities trade below pre-demerger valuations. Promoter Holding: 39.6%—enough for control but not enough for alignment. Related-party transactions between group companies create complexity. The conglomerate discount persists despite restructuring.

Most damning: execution disappointments. Five-year revenue CAGR of 2.48% during India's consumption boom. ROE of 10.1% despite manufacturing excellence. Working capital cycles elongating, inventory turns declining. The numbers suggest a company that's lost its edge, coasting on legacy while competitors accelerate.

The Bull Case: Hidden Value

Optimists see misunderstood transformation with multiple catalysts ahead. Start with manufacturing moats deeper than perceived. Arvind is a leading manufacturer of denim and woven fabrics, with capacities of 100 million meters per annum (MMPA) and 150 MMPA, respectively, as of March 31, 2023. This isn't commodity capacity but sophisticated capability. Arvind can produce fabric varieties that competitors can't replicate—from fire-resistant military textiles to graphene-enhanced denim. When Patagonia needs sustainable fabric innovation, they don't go to Bangladesh—they come to Santej.

The sustainability advantage is becoming decisive. The denim maker's production facilities have been equipped with Zero Liquid Discharge technology, resulting in a 93-percent reduction in wastewater discharge. Its major manufacturing facilities are now equipped with Zero Liquid Discharge (ZLD) systems, leading to a 93% reduction in wastewater discharge. As European regulations tighten and American brands face ESG pressure, Arvind's decade-old sustainability investments become competitive moats. Competitors must spend billions to match capabilities Arvind already possesses.

The real estate option is undervalued. Arvind sits on prime urban land in Ahmedabad, Mumbai, and Bangalore—legacy mill properties now surrounded by commercial development. Conservative estimates value this land at ₹2,000+ crore, nearly 30% of market cap. As Indian cities expand and land prices appreciate, this hidden asset becomes increasingly valuable.

Human capital represents intangible value. Arvind employs 25,000+ workers with irreplaceable skills—from handloom weavers preserving ancient techniques to engineers designing next-generation materials. This institutional knowledge, accumulated over generations, can't be replicated by competitors or automated by machines. It's a learning organization disguised as a manufacturing company.

The platform potential remains unrecognized. Arvind's B2B relationships span every major fashion brand globally. Their manufacturing facilities anchor supply chains. Their innovation capabilities solve industry problems. With minor pivots, Arvind could become a platform company—connecting brands with suppliers, offering manufacturing-as-a-service, monetizing decades of technical knowledge. The building blocks exist; only imagination limits possibilities.

The Investment Framework

Valuing Arvind requires sum-of-parts analysis, recognizing distinct businesses with different characteristics:

-

Textile Manufacturing (₹6,000 crore revenues): Mature, cyclical, but with technical differentiation. Deserves 0.5-0.7x sales multiple given margins and growth. Value: ₹3,000-4,200 crore.

-

Advanced Materials (₹1,000 crore revenues): High-growth, high-margin, strategic importance. Worth 2-3x sales given trajectory. Value: ₹2,000-3,000 crore.

-

Real Estate (hidden asset): Conservative land valuations plus development potential. Value: ₹2,000-2,500 crore.

-

Brand Relationships & IP: Difficult to value but substantial. Licensing arrangements, technical knowledge, customer relationships. Value: ₹1,000-1,500 crore.

Total value: ₹8,000-11,200 crore versus current market cap of ₹7,519 crore. The stock trades at discount to conservative sum-of-parts, with free options on transformation success.

Risk Factors

Multiple risks threaten the investment case:

-

Technology Disruption: 3D printing could eliminate textile manufacturing. Synthetic biology might create new materials. Digital fashion could reduce physical clothing demand.

-

Trade Wars: India's exclusion from RCEP limits Asian market access. Potential US-China decoupling might benefit competitors more than India. Brexit complications affect European exports.

-

Succession Risk: Fifth generation must prove competence. Professional managers might clash with family control. Governance structures could discourage institutional investment.

-

Capital Allocation: History of ventures outside core competence. Tendency toward empire-building over return optimization. CSR spending might prioritize social over financial returns.

-

ESG Backlash: Despite sustainability leadership, textile industry faces scrutiny. Fast fashion criticism might reduce demand. Water scarcity could limit production despite recycling.

The Verdict

Arvind represents a complex investment proposition—neither pure value nor growth, neither simple manufacturer nor brand house. It's a transformation story with uncertain ending, requiring patience most investors lack and faith markets rarely reward.

For long-term fundamental investors, Arvind offers asymmetric risk-reward. Downside seems limited given asset value and cash generation. Upside could be substantial if transformation succeeds. The margin of safety exists in hidden assets and unrecognized capabilities.

For traders and momentum investors, Arvind offers little. The stock will likely remain range-bound until catalysts emerge—major contract wins, successful new ventures, or strategic actions unlocking value. Without near-term triggers, dead money seems likely.

The investment case ultimately depends on belief—in Indian manufacturing renaissance, in sustainable fashion's premium pricing, in family businesses' evolutionary capability. Those who see only textile mills will find better opportunities elsewhere. Those who see industrial transformation might discover hidden value.

As one fund manager observed: "Arvind is priced like a declining textile mill but positioned like an advanced materials innovator. The market will eventually recognize reality—the question is whether you have patience to wait."

X. Epilogue & Future Horizons

The conference room at the new GWICA innovation center, January 2024. Kulin Lalbhai stands before a gathering of global fashion executives, sustainability experts, and technology entrepreneurs. Behind him, through floor-to-ceiling windows, the Santej complex stretches to the horizon—500 acres where cotton becomes denim, where wastewater becomes fresh water, where tradition meets innovation. His presentation slide reads: "We are a fashion powerhouse that is also building new age homes. We are a global leader in apparel manufacturing that is also transforming water management. A denim pioneer that is a trailblazer in advanced materials. A wearable technology manufacturer that is also delivering state-of-the-art engineering solutions."

To outside observers, this seems like corporate schizophrenia—too many identities, too many ambitions. But for the Lalbhais, it represents evolution's logical conclusion. When your great-great-grandfather sold jewels to Mughal emperors, when your great-grandfather built mills during the Depression, when your grandfather pioneered denim in socialist India, when your father transformed manufacturing into fashion—you don't see contradictions. You see continuity.

The next decade will test whether this continuity can survive discontinuous change. The challenges facing Arvind aren't cyclical downturns or competitive pressures—they're existential questions about manufacturing's future, fashion's sustainability, and family businesses' relevance.

Consider the technology frontier. Arvind's labs are experimenting with bio-fabricated materials—growing leather from mushrooms, creating silk from bacteria, developing cotton from captured carbon. It sounds fantastical, but prototypes exist. The same company that mastered mechanical looms now cultures materials in petri dishes. The question isn't technical feasibility but commercial viability. Can a textile manufacturer become a biotechnology company? More importantly, should it?

The sustainability imperative intensifies. Fashion contributes 10% of global carbon emissions, consumes more water than any industry except agriculture, and generates mountains of waste. Regulators are responding—the EU's textile strategy demands circular economy compliance by 2030. Consumers, especially Gen Z, increasingly reject fast fashion's disposability. Arvind, with its water recycling and organic cotton, seems well-positioned. But incremental improvement might not suffice when revolution is required.

The geopolitical landscape shifts rapidly. The China-Plus-One strategy should benefit India, but Bangladesh and Vietnam capture most relocated production. India's infrastructure improves but not fast enough. Trade agreements proliferate but exclude India. Arvind must navigate narrowing windows—competing globally while India struggles with competitiveness, building scale while automation eliminates jobs, pursuing growth while sustainability demands degrowth.

Digital transformation accelerates everything. When AI can design fabrics, when algorithms predict fashion trends, when virtual clothing exists only in metaverses—what happens to physical manufacturers? Arvind's digital initiatives seem progressive for a 93-year-old company but primitive compared to Silicon Valley standards. The company must somehow preserve manufacturing excellence while building software capabilities, maintain physical assets while creating digital value.

The succession question looms largest. The fifth generation has proven competent, but competence might not suffice for coming challenges. The sixth generation—Kulin and Punit's children—grow up in entirely different India: startup unicorns not textile mills, Instagram not industry journals, global aspirations not Gujarati traditions. Will they want to run manufacturing companies? Should they?

Yet reasons for optimism exist. India's demographic dividend remains real—300 million people entering middle class by 2030, demanding quality products Arvind can provide. The Make in India initiative, despite disappointments, gradually improves manufacturing competitiveness. Climate change makes local production increasingly attractive versus transcontinental shipping. The world might be deglobalizing just as Arvind perfects global capabilities.

The advanced materials opportunity could transform everything. As electric vehicles proliferate, automotive textiles demand explodes. As space exploration accelerates, technical fabrics for extreme environments become critical. As military modernization continues, protective materials gain strategic importance. Arvind's capabilities—developed for fashion—might find greatest value in completely different industries.

The water business represents another transformation vector. As water scarcity intensifies globally, Arvind's recycling technology becomes increasingly valuable. The company treating textile wastewater could treat municipal sewage, industrial effluent, even agricultural runoff. From textile manufacturer to water solutions provider—stranger pivots have succeeded.

Most intriguingly, Arvind might transcend traditional categories entirely. Imagine Arvind as a sustainable materials platform—designing, producing, and recycling materials across industries. Or as an innovation hub—the GWICA center expanded into a global R&D network solving fashion's sustainability crisis. Or as a circular economy enabler—collecting, processing, and regenerating textile waste into new products. The assets, capabilities, and relationships exist. Only imagination limits possibilities.

The financial trajectory remains uncertain. Bulls project ₹15,000 crore revenue by 2030, driven by advanced materials and sustainability premiums. Bears see continued stagnation as manufacturing shifts elsewhere and brands abandon partnerships. Reality likely lies between—moderate growth with margin improvement, transformation proceeding gradually not dramatically.

But focusing on financials misses the larger story. Arvind represents something beyond investment returns—it's a testament to industrial evolution, family enterprise, and institutional resilience. In a business environment that celebrates disruption and creative destruction, Arvind demonstrates creation through evolution, value through values, innovation within tradition.

As the presentation concludes, Kulin fields questions from the audience. A young entrepreneur asks the inevitable: "Why not just shut the mills and become a technology company?" Kulin smiles—he's heard this before. "Because making things matters," he responds. "Software scales infinitely but fabric clothes humanity. Algorithms optimize efficiency but looms create livelihoods. We're not choosing between atoms and bits—we're combining them."