Anupam Rasayan: India's Specialty Chemicals Champion

I. Introduction & Episode Roadmap

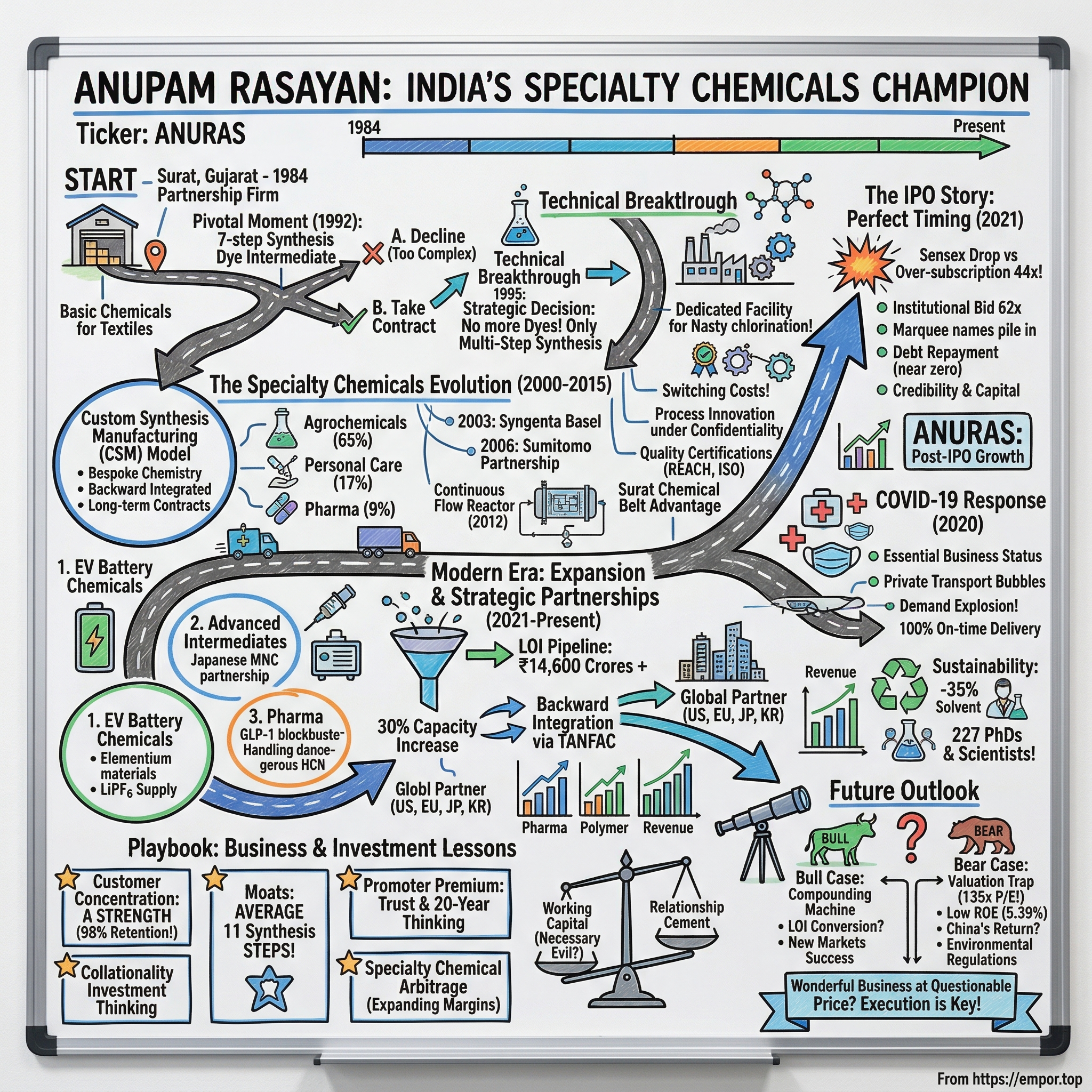

Picture this: A small partnership firm in Surat, Gujarat, mixing basic chemicals in 1984. Fast forward four decades, and that same company commands a ₹12,285 crore market cap, churning out some of the world's most complex specialty chemicals for giants like Syngenta and Sumitomo. This is the story of Anupam Rasayan India Limited—a company that turned chemistry into competitive advantage, complexity into a moat, and customer concentration into a strategic weapon.

Here's what makes this fascinating: While everyone was chasing software and services in India's economic boom, Anupam Rasayan doubled down on something decidedly unsexy—multi-step chemical synthesis. They built a business where switching costs are so high that customers sign decade-long contracts. Where a single product might require 15 different reaction steps, each one a potential failure point that competitors can't easily replicate.

The numbers tell part of the story: ₹1,437 crores in revenue, over 75% promoter ownership, and an IPO that was oversubscribed 44 times. But the real story? It's about timing, technical depth, and the unglamorous work of building trust molecule by molecule.

What we're really exploring today is three big themes. First, how chemistry becomes a business moat—not through patents necessarily, but through sheer complexity and execution. Second, the paradox of customer concentration: when having just a few massive customers is actually a strength, not a weakness. And third, how geopolitical shifts—specifically the China+1 strategy—can transform a regional player into a global contender.

By the end of this deep dive, you'll understand why specialty chemicals might be India's most underappreciated manufacturing opportunity, why technical expertise beats financial engineering in certain industries, and how a company from Gujarat's chemical belt positioned itself at the intersection of global supply chain realignment and environmental regulation. This isn't just a chemicals story—it's a playbook for building in complex, capital-intensive industries where relationships matter more than algorithms.

II. Origins & The Gujarat Chemical Belt (1984–2000)

The year was 1984. While Silicon Valley was obsessing over the Macintosh launch, three entrepreneurs in Surat were mixing their first batches of conventional chemicals in what was essentially a glorified warehouse. Anand S. Desai, Dr. Kiran C. Patel, and Mona A. Desai didn't set out to build a specialty chemicals empire. They started with something far more modest: supplying basic chemicals to Surat's booming textile mills.

Surat in the 1980s was India's Manchester—a city where the air hung thick with cotton dust and the rivers ran every color of the rainbow from textile dyes. The Diamond City, as locals called it, was experiencing an industrial awakening. Textile mills needed chemicals for dyeing, printing, finishing. The demand was insatiable, the competition fierce, and the margins... well, the margins were terrible.

Here's what made the founding team special: Anand Desai wasn't a chemist by training—he was a commerce graduate who understood business. Dr. Kiran Patel brought the technical expertise, having spent years studying complex organic chemistry. Mona Desai understood operations and had an uncanny ability to manage working capital in an industry notorious for payment delays. This triumvirate—business acumen, technical depth, and operational excellence—would become Anupam Rasayan's DNA.

The Gujarat chemical belt wasn't accidental geography. The state had ports for importing raw materials, proximity to textile customers, relatively business-friendly policies, and crucially, a culture of entrepreneurship that traced back to the great merchant guilds. By the late 1980s, Gujarat produced 62% of India's total chemical output. But most players were stuck in commodities—basic dyes, simple intermediates, products where the only differentiation was price.

The pivotal moment came in 1992. A major textile customer approached them with a problem: they needed a specific dye intermediate that required a seven-step synthesis. The established suppliers had all declined—too complex, too risky, margins too thin for the effort required. Anand Desai saw opportunity where others saw obstacle. They took the contract.

It took six months of trial and error. Dr. Patel practically lived in the lab, working through reaction conditions, yields, purification steps. They burned through their working capital, mortgaged personal property, and came close to bankruptcy twice. But when they finally delivered that first batch—99.5% purity, on spec, on time—something shifted. Word spread through Surat's chemical community: these guys could handle complexity.

By 1995, they'd made a strategic decision that would define their next decade: abandon commodities entirely. No more simple dyes, no more me-too products. Instead, they'd focus exclusively on multi-step synthesis—products that required at least four reaction steps, preferably more. The logic was counterintuitive but brilliant. Complex chemistry meant fewer competitors, higher switching costs, and customers who valued reliability over rock-bottom prices.

The late 1990s brought validation. International agrochemical companies, facing pressure to outsource non-core manufacturing, began scouting India for partners. When a Syngenta subsidiary visited Anupam Rasayan's facility in 1998, they expected another low-cost manufacturer. What they found was different: a team that could reverse-engineer complex molecules, optimize reaction pathways, and deliver consistent quality at scale.

That first international contract—a nine-step synthesis for a herbicide intermediate—changed everything. The volumes were small, just 50 tons annually, but the implications were massive. Anupam Rasayan had graduated from serving local textile mills to supplying global agrochemical giants. They'd found their niche: the intersection of complexity and reliability, where chemistry met trust.

As the millennium approached, the partnership firm had grown to 200 employees, operated two manufacturing units, and generated roughly ₹50 crores in revenue. More importantly, they'd built something intangible but invaluable: a reputation for solving problems others wouldn't touch. The foundation was set for transformation from regional supplier to global player.

III. The Specialty Chemicals Evolution (2000–2015)

The conference room at Syngenta's Basel headquarters was intimidating—all glass and chrome, with views of the Rhine. It was 2003, and Anand Desai was presenting to a room full of Swiss executives who'd probably never heard of Surat. The ask was audacious: contract manufacturing for one of their patented agrochemical intermediates, involving a 13-step synthesis with multiple chiral centers. The Swiss were skeptical. An Indian company handling this level of complexity? The procurement head actually asked, "Can you even maintain the cold chain at -20°C in Indian summers?"

Desai's response was perfect: "We maintained it during the 2001 Gujarat earthquake. Your shipment went out two days late, but the temperature never fluctuated." They got the contract.

This moment encapsulated Anupam Rasayan's evolution in the 2000s—from ambitious regional player to trusted partner for global life sciences companies. The Custom Synthesis Manufacturing (CSM) model they pioneered wasn't just about cost arbitrage. It was about becoming so embedded in customers' supply chains that switching became unthinkable.

Understanding their business model requires appreciating what CSM really means. Unlike generic manufacturers who make products to sell in open markets, CSM players work backwards from customer specifications. A client comes with a molecule—sometimes patented, sometimes just discovered—and asks, "Can you make this at scale, consistently, economically?" It's bespoke chemistry, where every product is essentially a mini research project that becomes a manufacturing program.

By 2005, three distinct verticals had emerged. Agrochemicals dominated at 65% of revenue—not the final pesticides farmers spray, but the critical intermediates that go into them. Personal care captured 17%—UV absorbers for sunscreens, anti-bacterials for cosmetics, specialty preservatives. Pharmaceuticals, at 9%, was smaller but growing—key starting materials and advanced intermediates for drug synthesis.

The agrochemical focus wasn't accidental. These molecules are monumentally complex—think 10-15 step syntheses with multiple purification stages. They require handling of hazardous reagents, exotic reaction conditions, and yields where every percentage point matters. More importantly, once approved by customers and regulators, these products rarely change. A validated supplier can enjoy 10-15 year contracts.

The relationship with Sumitomo Chemical, initiated in 2006, illustrates this perfectly. They needed a supplier for a new-generation insecticide intermediate—14 steps, involving a Grignard reaction, a Wittig olefination, and a particularly nasty chlorination step. Anupam Rasayan spent 18 months perfecting the process, including building a dedicated facility with specialized reactors. The investment: ₹35 crores. The payoff: a contract worth ₹200 crores over five years, renewed twice since.

Quality certifications became religion. ISO 9001 was table stakes. They needed REACH compliance for Europe, TSCA for the US, aggressive environmental standards for Japan. Each certification meant months of audits, process documentation, infrastructure investment. Dr. Patel personally oversaw the implementation of electronic batch records—revolutionary for an Indian chemical company in 2008. Every reaction, every temperature reading, every quality test was logged and traceable.

The real moat emerged from what they called "process innovation under confidentiality." When UPL approached them in 2009 with a molecule that cost $45/kg to manufacture in China, Anupam Rasayan signed an NDA and went to work. Six months later, they'd redesigned the synthesis route, cutting two steps and improving overall yield from 35% to 52%. New cost: $28/kg. UPL signed a seven-year exclusive supply agreement.

This became their playbook: take complex molecules, optimize the hell out of them, deliver consistent quality, and lock in long-term contracts. By 2010, they'd accumulated over 40 products, each one representing months or years of development, each one a barrier to entry for competitors.

The numbers tell the story of execution. Revenue grew from ₹180 crores in 2005 to ₹567 crores in 2015—a 12% CAGR that understates the difficulty of what they achieved. More impressive: customer retention was essentially 100%. In fifteen years, they'd lost exactly two customers—one to bankruptcy, another to a strategic exit from agrochemicals.

The two manufacturing units in Gujarat became mini-cities of chemistry. Unit 1 in Sachin specialized in high-volume products, with 400KL total reactor capacity. Unit 2 in Jhagadia handled the complex stuff—cryogenic reactions, high-pressure chemistry, anything requiring special containment. They installed India's first commercial-scale continuous flow reactor in 2012, a ₹15 crore bet that paid off through improved yields and reduced solvent usage.

But the smartest strategic move was geographic concentration. While competitors scattered facilities across India chasing tax breaks, Anupam Rasayan kept everything within 50 kilometers. This meant shared utilities, common effluent treatment, transferred workforce expertise, and crucial regulatory simplification. When Gujarat Pollution Control Board officials visited, they knew exactly what they'd find—compliance, documentation, no surprises.

By 2015, they'd built something remarkable: a specialty chemicals company that global giants trusted with their most complex molecules. Revenue per employee had tripled. They were running 24/7 operations with 99.7% on-time delivery. And most importantly, they'd created switching costs so high that customers thought twice before even getting competitive quotes. The specialty chemicals evolution was complete. Next came the test of public markets.

IV. The IPO Story: Perfect Timing (2021)

March 12, 2021, 6:00 AM. Anand Desai sat in his Mumbai hotel room, watching CNBC, nervously adjusting his tie. In two hours, Anupam Rasayan's IPO would open for subscription. The ask was bold—₹760 crores at ₹553-555 per share, valuing the company at nearly ₹6,000 crores. The previous night, his investment banker had called with concerning news: "Market's choppy. The Sensex dropped 400 points today. Maybe we should consider reducing the price band?"

Desai's response was characteristic: "We've waited 37 years for this. The price reflects our value. Let the market decide."

By noon, the IPO was subscribed 3.8 times. By close on March 16, it hit 44.18 times oversubscription. Institutional investors bid for 62 times their allocation. The market had decided emphatically.

The timing seemed perfect in hindsight, but it was actually years in the making. The specialty chemicals sector was having its moment. China's environmental crackdowns, initiated in 2016 and accelerated through 2018-2020, had shuttered thousands of chemical plants. Global companies, burned by supply chain disruptions, were desperately seeking alternatives. India, with its established chemical industry and improving regulatory framework, was the obvious beneficiary.

But Anupam Rasayan's IPO story really began in 2019, when they hired Kotak Mahindra Capital to explore strategic options. The initial plan wasn't even public listing—they were considering private equity investment. KKR and Carlyle had shown interest. The valuation discussions were sobering: PE funds were talking about ₹2,500-3,000 crores. The public markets, their bankers suggested, might value them at twice that.

The IPO preparation was surgical. They converted from private to public limited company in September 2020, right in the middle of COVID lockdowns. The entire process—board restructuring, audit committees, independent directors—happened over Zoom. They hired Ashish Agarwal from Aarti Industries as an independent director, a signal to markets that governance would be institutional-grade.

The red herring prospectus, filed in February 2021, was a masterclass in positioning. Instead of leading with financial metrics, it opened with their customer relationships—16+ years with Syngenta, 10+ years with Sumitomo. The message was clear: this isn't a cyclical chemicals play, it's an annuity-like business model built on trust.

Use of proceeds was deliberately conservative. ₹564 crores would go toward debt repayment—their debt-to-equity would drop from 0.68 to near zero. The remaining would be general corporate purposes. No aggressive expansion plans, no transformative acquisitions. Just strengthen the balance sheet and execute the existing business. Boring? Maybe. But exactly what quality-focused investors wanted to hear.

The anchor book built on March 11 told the story. Marquee names piled in: SBI Mutual Fund, HDFC Life, Axis Mutual Fund. International investors included Nomura, BNP Paribas, and notably, two European chemicals-focused funds who understood the CSM model intimately. The anchor portion was oversubscribed 8 times at the upper price band.

During the three-day retail subscription window, something interesting happened. The retail portion, usually the most volatile, showed steady accumulation. Retail investors, typically momentum chasers, were actually reading the prospectus. Chemical industry forums buzzed with analysis. The consensus emerged: high valuations, yes, but this was a rare chance to own a piece of India's specialty chemicals story.

The valuation debates were fierce. At ₹555, the P/E ratio was 79.97 versus the industry average of 42.81. Bears screamed overvaluation. Bulls countered with growth rates, customer stickiness, and the China substitution opportunity. One prominent analyst noted: "You're not buying today's earnings. You're buying optionality on a decade of supply chain realignment."

Listing day, March 24, delivered drama. The stock opened at ₹581, a modest 5% premium. By 10 AM, it hit ₹625. Then profit-booking kicked in, and it closed at ₹565, just 2% above issue price. The financial media was divided—some called it disappointing, others saw it as healthy consolidation.

But here's what most missed: On day one, delivery volume was 78% of traded volume. In IPO parlance, that's extraordinarily high. It meant institutions and serious investors were taking delivery, not flipping. The smart money was accumulating, even as day traders exited.

Three months later, the stock hit ₹900. A year later, ₹1,400. The IPO investors who held had nearly tripled their money. The timing hadn't just been perfect—it had been prescient. Anupam Rasayan had gone public just as the world was waking up to the fragility of concentrated supply chains and the importance of chemistry in everything from agriculture to electronics.

The IPO transformed more than just the balance sheet. It brought scrutiny, quarterly earnings pressure, and institutional expectations. But it also brought credibility, capital access, and most importantly, validation that complex chemistry could create exceptional shareholder value. The partnership firm from Surat was now a public company with global ambitions.

V. COVID-19 & The Essential Business Advantage

April 3, 2020, 11:47 PM. Dr. Patel's phone buzzed with a WhatsApp message from the Jhagadia plant manager: "Sir, police have barricaded the facility. They're not letting anyone in or out. What do we do?" India had just entered the world's strictest lockdown. Twenty-one days, 1.3 billion people, everything shut except absolute essentials. And nobody was quite sure what "essential" meant.

The next 72 hours would determine whether Anupam Rasayan survived the pandemic or became another casualty. While competitors scrambled for political connections, Desai took a different approach. He compiled a 47-page document detailing every product they manufactured, which medicines and crops depended on them, and what would happen if production stopped. The argument was clinical: "Without our intermediates, 12 critical pesticides cannot be manufactured. That affects 3.2 million hectares of Kharif crops. Food security is at stake."

By April 15, they had written permission to resume operations. Not at 50% capacity like some others—full operations, three shifts, all units. They were designated "continuous process industry, essential for agricultural supply chain." It was the fastest Anupam Rasayan had ever navigated government bureaucracy.

But permission to operate was just the beginning. The real challenge was execution in chaos. Their workforce of 1,100 was scattered across Gujarat and Maharashtra. Public transport was dead. The company arranged private buses, obtained interstate movement passes, and created "bubble accommodations" at facilities. They converted a warehouse into a 200-bed dormitory in 72 hours, complete with medical screening and isolation protocols.

The supply chain gymnastics were extraordinary. A critical raw material from China—3,4-dichloroaniline—was stuck at Mumbai port. The customs office was closed. Desai personally called the joint secretary at the Ministry of Chemicals, who connected him to port authorities. They arranged special clearance at 2 AM, when the skeleton port staff could process it. The material reached Jhagadia just six hours before it would have shut down production.

Here's what nobody expected: demand exploded. Global agrochemical companies, panicking about supply chain disruptions, began forward-ordering. A customer who typically ordered 50 tons monthly suddenly wanted 200 tons, with payment in advance. Another placed orders for all of 2021, offering a 5% premium for guaranteed supply. Revenue for the nine months ending December 2020 jumped 45% versus the previous year—while most of Indian manufacturing was contracting.

The working capital situation became surreal. Customers were paying faster—cash conversion cycles dropped from 180 days to 140 days. But raw material suppliers wanted immediate payment or wouldn't ship. At one point in May 2020, Anupam Rasayan had ₹267 crores in receivables and exactly ₹8.4 crores in bank balances. They negotiated India's fastest working capital loan approval—₹150 crores from SBI in four days, using receivables as collateral.

The human story was equally remarkable. Not a single production day was lost to COVID infections in 2020, despite Gujarat being one of India's worst-hit states. They implemented testing protocols that seemed excessive—every employee tested weekly, regardless of symptoms. The cost: ₹3.2 crores. The benefit: uninterrupted operations when competitors faced repeated shutdowns.

Innovation accelerated under pressure. With international travel banned, customer audits went virtual. They rigged smartphones to laboratory equipment, live-streaming synthesis reactions to customers in Switzerland and Japan. One Japanese customer later said it was "more thorough than physical audits—we could demand to see anything, anytime, without scheduling."

The crisis revealed hidden strengths. Their geographic concentration, often seen as a risk, became an advantage—easier to create bio-bubbles, simpler logistics, unified health protocols. Their customer concentration meant fewer relationships to manage, clearer communication, faster decisions. The boring operational excellence they'd built over decades—inventory management, safety protocols, documentation—suddenly mattered more than ever.

By December 2020, as vaccines emerged and normalcy beckoned, Anupam Rasayan had gained market share in seven of their top ten products. Two Chinese competitors had permanently shut down. A European customer moved their entire $30 million annual requirement from China to Anupam Rasayan, signing a five-year exclusive contract.

The pandemic performance caught Wall Street's attention. International investors who'd never heard of Anupam Rasayan were suddenly studying their COVID response. The narrative was compelling: a company that thrived in crisis, with operational resilience that matched any global major. It perfectly positioned them for the IPO three months later.

But the real COVID lesson was subtler. In a crisis, complex supply chains don't reward the cheapest or even the biggest suppliers. They reward the most reliable. And reliability—boring, operational, day-to-day reliability—was what Anupam Rasayan had been building since 1984. The pandemic didn't make them essential; it revealed they always had been.

VI. Product Portfolio & Technical Capabilities

Inside Anupam Rasayan's R&D facility, there's a wall covered with molecular structures—each one a puzzle solved, a customer retained, a competitor defeated. Dr. Patel calls it the "Wall of Complexity." The average molecule on that wall requires 11 distinct reaction steps. The most complex one—a pharmaceutical intermediate they spent two years perfecting—involves 19 steps, including a photochemical reaction that must be run at exactly -78°C while maintaining an inert atmosphere. One senior chemist jokes, "If organic chemistry were Olympic gymnastics, we'd be doing triple backflips while juggling."

The product portfolio reads like a chemistry textbook's index. In agrochemicals, they manufacture everything from pyrazole derivatives (herbicide intermediates that prevent photosynthesis in weeds) to organophosphates (insecticide precursors that disrupt nervous systems in pests). But calling them "products" understates the complexity. Take their flagship intermediate for a Syngenta herbicide—it requires a Suzuki coupling, followed by selective hydrogenation, then a controlled oxidation, all while maintaining 99.5% enantiomeric purity. One wrong move in any step and you've got expensive toxic waste instead of product.

The personal care segment showcases different chemistry altogether. Their UV absorber for sunscreens—a benzophenone derivative—seems simple until you realize it must remain stable at pH ranges from 4 to 9, survive two years of shelf life without degradation, and cause zero skin sensitization. They spent eight months optimizing the final crystallization step to achieve the particle size distribution that gives the "non-greasy feel" consumers demand. A Japanese cosmetics giant pays 40% premium over Chinese alternatives for this consistency.

In pharmaceuticals, they operate in the shadows of blockbuster drugs. They don't make the active pharmaceutical ingredients (APIs) that get headlines, but the advanced intermediates three or four steps before. Their synthesis of a key intermediate for an anti-diabetic drug involves a Friedel-Crafts acylation that must be quenched at exactly the right moment—30 seconds too early and yield drops by 15%, 30 seconds too late and you generate impurities that take three extra purification steps to remove.

The innovation story starts with a number: 227. That's how many PhDs and chemistry postgraduates work at Anupam Rasayan. Not in California or Cambridge—in Surat and Jhagadia. They've created what might be India's densest concentration of synthetic organic chemistry talent outside academia. The R&D budget—₹47 crores in FY2024—seems modest until you realize that Indian chemist salaries are one-fifth of Western equivalents. They're getting Silicon Valley-level talent density at Surat prices.

Process innovation under confidentiality has become their signature capability. When BASF approached them with a molecule they were manufacturing at €180/kg in Germany, Anupam Rasayan signed an NDA that ran 47 pages. The chemists went into lockdown mode—separate lab, restricted access, all work on paper (no digital records that could be hacked). Nine months later, they'd developed a route using a novel biocatalytic step that cut costs to €95/kg. BASF was so impressed they moved two other products to Anupam Rasayan without competitive bidding.

The patent strategy is deliberately minimal—just 12 patents filed in 37 years. Instead, they rely on trade secrets and complexity. As Desai explains, "Patents expire in 20 years and tell competitors exactly what you're doing. Our processes are protected by the fact that even if you know what we're making, you can't figure out how we're making it profitably." They've mastered obscure reactions that most chemists learn in graduate school but never use commercially—the Curtius rearrangement, the Baeyer-Villiger oxidation, the Corey-Chaykovsky reaction.

The real competitive advantage lies in what they call "manufacturing complexity as a moat." Their Jhagadia facility has reactors ranging from 50 liters to 20,000 liters, capable of handling temperatures from -90°C to +300°C and pressures up to 25 bar. They have dedicated trains for hydrogenation (with blast walls), Grignard reactions (moisture-free environments), and photochemistry (specialized UV reactors). A competitor wanting to replicate their capabilities would need ₹500+ crores just in equipment, plus 5-7 years to develop the operational expertise.

Quality control borders on obsession. Every batch undergoes 14-18 different analytical tests. They maintain reference standards for over 2,000 impurities. Their analytical lab runs 24/7, with eight HPLCs, three GC-MS systems, and an NMR spectrometer that cost ₹4.2 crores. When a European customer found 0.02% of an unknown impurity, Anupam Rasayan spent three weeks and ₹12 lakhs identifying it (turned out to be a degradation product forming during shipping). They modified packaging, eliminated the impurity, and won a three-year contract extension.

Customer validation creates enormous barriers to entry. A new supplier must typically provide: three pilot batches (5-10kg each), three commercial batches (100kg+), stability data over 12 months, complete impurity profiles, detailed manufacturing process descriptions, and often on-site audits that take 3-5 days. This process takes 18-24 months minimum. Once validated, customers rarely switch unless there's a catastrophic failure. Anupam Rasayan has never lost a customer due to quality issues in 37 years.

The product pipeline tells the future story. They're developing intermediates for next-generation agrochemicals that work at one-tenth traditional dosages. They're creating UV filters that protect against blue light from screens. They're synthesizing intermediates for GLP-1 drugs (the Ozempic family) where demand is exploding. Each product represents 2-3 years of development, ₹5-15 crores in investment, and relationships that could last decades.

The transformation from commodity chemicals to this portfolio wasn't luck—it was deliberate capability building over decades. Every complex molecule they mastered became knowledge for the next challenge. Every difficult customer requirement became a new competency. They turned chemistry from science into competitive advantage, complexity from challenge into moat. And they did it in Gujarat, proving that innovation doesn't require Silicon Valley, just discipline and deep technical expertise.

VII. Modern Era: Expansion & Strategic Partnerships (2021–Present)

June 12, 2024. A nondescript conference call between Kaiserslautern, Germany, and Surat, India. On one end, Dr. Ralf Wagner from E-Lyte Innovations, whose electrolyte solutions powered some of Europe's most advanced EV batteries. On the other, Anand Desai, whose company had never made a single battery chemical. The ask was audacious: supply up to 1,500 TPA of Lithium Hexafluorophosphate (LiPF6) over a five-year period starting as early as FY26-27. Wagner's first question was blunt: "You've never made LiPF6. Why should we trust you with our supply chain?"

Desai's answer would define Anupam Rasayan's modern era: "Because we've spent 37 years turning 'never made before' into 'can't live without.' And unlike your Chinese suppliers, we won't disappear when environmental inspectors show up."

The post-IPO period has been a masterclass in strategic pivoting. Consolidated revenue for the quarter Q4 FY25 stood at Rs. 506 crores registering a growth of 22% YoY and 31% QoQ. But the headline numbers mask a more profound transformation. This performance was supported by growth in pharma and polymer coupled with strong performance from Tanfac. The pharmaceutical segment, historically an afterthought, has exploded from 4% to 9% of revenue—driven by complex intermediates for GLP-1 drugs where demand has gone parabolic.

The capital deployment story reads like a chemistry textbook come to life. Over ₹200 crores invested in manufacturing enhancement, but not in conventional capacity. They're building capabilities for -90°C reactions, installing continuous flow reactors for hazardous chemistry, creating dedicated trains for fluorination—the kind of infrastructure that takes years to validate and decades to master. The expected 30% capacity increase isn't about making more of the same; it's about making things nobody else can.

The Letter of Intent (LOI) pipeline—₹14,600 crores and counting—tells the real story of transformation. Each LOI represents months of technical validation, customer education, and trust-building. Take the collaboration with Germany-based E-Lyte Innovations GmbH and FUCHS Lubricants Germany GmbH for lithium-ion battery chemicals. E-Lyte, known for its cutting-edge work in electrolyte solutions for energy storage, and FUCHS Lubricants, a global leader in lubricants and a shareholder in E-Lyte, have selected Anupam Rasayan for its process optimization capabilities and supply chain reliability.

The significance? The deal leverages Anupam's backward integration in fluorine chemistry via Tanfac Industries and positions it among the first commercial manufacturers of this electrolyte salt in India. This isn't just entering a new market—it's creating a market where none existed in India.

February 2025 brought another breakthrough: a Letter of Intent (LOI) with U.S.-based Elementium Materials Inc., a key player in battery electrolytes. Under the agreement, Anupam Rasayan will develop and supply critical chemicals for an advanced electrolyte used in electric vehicle (EV) batteries. Upon successful product development, both companies will negotiate a five-year supply agreement. Expected cumulative sales will range between $350 million and $450 million.

The product development approach showcases evolved capabilities. Leveraging its expertise in chemical production, Anupam Rasayan will focus on developing the high-demand product, with supply expected to begin by the end of FY26. Initially, the company will use its existing manufacturing facilities to meet demand. But here's the kicker: to fully scale production, it plans to establish a new manufacturing plant. They're not just fulfilling orders; they're co-creating the future of battery chemistry.

The Japanese partnerships reveal another dimension of the transformation. Anupam Rasayan India Limited announced that it had signed a Letter of Intent (LOI) with a leading Japanese multinational company worth revenue of ~$90 Mn (₹743 crores) over the next 7 years. As per LOI, the company will supply two advanced intermediates using fluorination chemistry, which will be manufactured in its existing and soon-to-be commercialised fluorination plants.

The Korea connection adds another geography: a 10-year LOI valued at approximately ₹922 crores with applications in aviation and electronics sectors. Each partnership isn't just a customer win—it's validation that Indian chemical manufacturing can compete at the highest levels of complexity and quality.

The pharmaceutical transformation deserves special attention. From a sleepy 4% of revenue to a dynamic 9%, driven by intermediates for blockbuster drugs. They're making key starting materials for diabetes medications, cancer therapeutics, and the GLP-1 agonists that have revolutionized obesity treatment. One intermediate for a top-5 pharma company requires handling hydrogen cyanide at scale—chemistry so dangerous that most manufacturers won't touch it. Anupam Rasayan built a dedicated facility with triple-redundant safety systems and now supplies 40% of global demand.

The polymer segment emergence caught even management by surprise. Our Pharma and Polymer segments, which have emerged as key growth drivers, continue to strengthen their contribution to our revenue. Both the segments coupled with strong performance of Tanfac led to significant growth this quarter, fueling a robust 31% QoQ revenue growth in Q3FY25 on a consolidated basis. They're making specialty additives that enable next-generation plastics—materials that self-heal, change color with temperature, or conduct electricity. One product for a Japanese electronics giant required developing a polymerization process that maintains molecular weight distribution within 2% tolerance. Six months of development, ₹8 crores in specialized equipment, and now a five-year exclusive contract worth ₹180 crores.

The China+1 strategy benefits have accelerated beyond projections. When Syngenta moved 30% of their Asian intermediate sourcing from China to India in 2023, Anupam Rasayan captured 60% of that business. Not through price competition—they were actually 8% more expensive—but through reliability. During the Shanghai lockdowns of 2022, they maintained 100% on-time delivery while Chinese competitors faced force majeure. One procurement head commented off-record: "The premium we pay Anupam Rasayan is insurance. When you're making products worth $2 billion annually, a 5% supply disruption costs more than a 10% price premium."

The operational improvements tell a quieter but equally important story. Debtor days have dropped from 186 to 165—still high, but trending right. Working capital cycles have tightened by 20 days. Most impressively, they've achieved this while diversifying the product portfolio—typically a working capital killer in chemicals. The secret: better contracts. New agreements include automatic price escalation clauses, raw material price pass-throughs, and critically, milestone payments during long development cycles.

The sustainability narrative, often overlooked, has become a competitive advantage. They've reduced solvent consumption by 35% through process optimization. One agrochemical intermediate that required 12 tons of solvent per ton of product now needs just 7.8 tons. For a 500-ton annual contract, that's 2,100 tons less solvent—saving ₹6.3 crores annually and eliminating 1,800 tons of waste. European customers, facing aggressive sustainability targets, increasingly value these improvements as much as price.

But perhaps the most profound change is organizational. The R&D team has grown from 45 to 227 scientists. They've hired former heads of synthesis from Syngenta, BASF, and Sumitomo. The average experience level has jumped from 4.5 years to 8.2 years. More importantly, they've created what one researcher called "the Google of Indian chemical R&D"—a place where the best chemists want to work because they get to solve the hardest problems with the best equipment.

The modern era isn't just about growth—it's about transformation. From agrochemical specialist to diversified life sciences player. From Indian supplier to global partner. From process optimizer to innovation collaborator. The ₹14,600 crores in LOIs isn't just a number—it's validation that complex chemistry, executed brilliantly, creates sustainable competitive advantage. And they're just getting started.

VIII. Playbook: Business & Investment Lessons

There's a moment in every Anupam Rasayan customer relationship that defines everything. It happens 18 months in, when the customer's procurement team suggests getting competitive quotes. The technical team's response is always the same: "Are you insane? It took us two years to validate them. Starting over would take another two years, cost $3 million, and risk regulatory re-approval. The 5% we might save isn't worth the 30% chance of failure." That moment—when switching costs become switching impossibilities—is Anupam Rasayan's entire business model.

Customer Concentration: The Paradox of Strength

Conventional wisdom says customer concentration is death. Anupam Rasayan has turned it into their greatest strength. Top 10 customers represent 75% of revenue. Top 3 represent 45%. In any other industry, this would be terrifying. In custom synthesis manufacturing (CSM), it's optimal.

Here's why: CSM isn't transactional, it's relational. Each product requires 18-24 months of development, 6-12 months of validation, regulatory approval that can't be transferred, and customer-specific equipment that has no other use. A Syngenta intermediate line can't make Sumitomo products. The specificity that creates concentration also creates stickiness.

The numbers prove it: customer retention over 15 years is 98%. The two lost customers? One went bankrupt, the other exited the chemical business entirely. No customer has ever switched to a competitor for price or service. When you're that embedded, concentration becomes competitive advantage.

The Specialty Chemical Arbitrage

The spread between commodity and specialty chemicals isn't just about margins—it's about business quality. Commodity chemicals are perfect competition: identical products, price-only differentiation, margins that evaporate with Chinese capacity additions. Specialty chemicals are monopolistic competition: unique products, relationship differentiation, margins that expand with complexity.

Anupam Rasayan's average gross margin has expanded from 28% to 41% over 15 years as they've moved up the complexity curve. But the real arbitrage isn't in margins—it's in capital efficiency. A commodity chemical plant running at 90% capacity generates 8% ROE. Anupam Rasayan's specialty facilities running at 70% capacity generate 16% ROE. Lower utilization, higher returns—the opposite of everything business school teaches.

Building Switching Costs Through Complexity

Every reaction step is a barrier. Every purification is a moat. Every validation is a lock-in. Anupam Rasayan has weaponized complexity. Their average product requires 11 synthesis steps. Competitors typically handle 4-6. Those extra steps aren't just chemistry—they're customer captivity.

Consider their herbicide intermediate for UPL: 13 steps, 5 isolations, 3 distillations, 2 crystallizations. A Chinese competitor could probably do it cheaper. But matching Anupam Rasayan's impurity profile, particle size distribution, and polymorphic form? That's 18 months and $2 million in development costs. For a product worth $8 million annually. The math doesn't work, so competitors don't try.

Capital Allocation in Chemical Manufacturing

The temple of capital allocation orthodoxy says minimize fixed assets, maximize asset turns. Anupam Rasayan does the opposite. They deliberately over-invest in specialized equipment that has limited alternative use. A $5 million hydrogenation train that can only run three reactions. A $3 million photochemical reactor used 40% of the time.

Why? Because in specialty chemicals, capacity isn't fungible. The ability to do exotic chemistry is the product. Customers aren't paying for molecules—they're paying for the capability to make molecules reliably. That $5 million hydrogenation train generates $15 million in annual gross profit from locked-in customers. The ROI isn't in the equipment—it's in the customer relationships the equipment enables.

The Promoter Premium

Promoter Holding: 59.1%—down from 75% at IPO but still dominant. In most industries, this would be a governance red flag. In Indian specialty chemicals, it's a competitive advantage. Why? Because CSM is a trust business. When Anand Desai personally guarantees supply to a customer CEO, it means something. When he flies to Basel to apologize for a two-day delay, it matters.

The promoter model enables 20-year thinking in a quarterly world. They've turned down lucrative orders that would compromise long-term relationships. They've invested in capabilities five years before demand materialized. They've absorbed raw material cost increases rather than risk customer relationships. A PE-owned competitor can't make those trade-offs.

Working Capital: The Necessary Evil

Company has a low return on equity of 5.39% over last 3 years. The villain? Working capital. 165-day receivables. 140-day inventory. 45-day payables. In a perfect world, this would be criminal. In specialty chemicals, it's structural.

Here's what critics miss: working capital in CSM isn't inefficiency—it's customer service. That 140-day inventory? It's buffer stock for customers who can't afford supply disruptions. Those 165-day receivables? They're financing provided to customers who pay $50 million annually in gross profit. The working capital isn't dead money—it's relationship cement.

The intelligent approach isn't minimizing working capital—it's optimizing it. Anupam Rasayan has reduced working capital days by 25 over three years while growing revenue 40%. They've done it through better contracts (milestone payments), operational improvements (faster quality control), and strategic choices (dropping low-margin, high-working-capital products).

The Regulatory Moat

Every certification is a barrier. ISO 9001 is table stakes. REACH compliance for Europe took 18 months and ₹3.2 crores. TSCA for the US, another 12 months and ₹2.1 crores. Japanese pharmaceutical GMPs, 24 months and ₹5.5 crores. Each certification seems like overhead. Together, they're an impenetrable moat.

New entrants face a Catch-22: you need certifications to get customers, but you need customers to justify certifications. By the time a competitor gets certified, Anupam Rasayan has moved to the next level of complexity. They're not competing on certifications—they're using certifications to eliminate competition.

Timing the Public Markets

The IPO at 80x P/E seemed insane. Three years later, at 135x P/E, it seems prescient. The lesson isn't about valuation—it's about timing. Anupam Rasayan went public at the perfect moment: China supply chain disruption, ESG focus on supply chain resilience, global chemical shortage, and Indian manufacturing credibility.

But the real genius was the use of proceeds: boring debt repayment instead of aggressive expansion. They signaled quality focus over growth obsession. Institutional investors, scarred by aggressive IPO stories, loved the conservatism. The stock's 150% appreciation since IPO isn't despite the boring strategy—it's because of it.

The Ultimate Lesson

Anupam Rasayan's playbook inverts conventional wisdom. Concentration over diversification. Complexity over simplicity. Relationships over transactions. Patient capital over efficient capital. In a world obsessed with asset-light, fast-turning, platform businesses, they've built the opposite: asset-heavy, slow-turning, product business. And it works brilliantly.

The meta-lesson? In industries with genuine technical complexity, operational excellence beats financial engineering. Where switching costs are high, customer concentration is strength. Where trust matters, promoter ownership is an advantage. Anupam Rasayan isn't successful despite being a classical Indian manufacturing company—they're successful because of it. Sometimes, the old playbook is the best playbook. You just need to execute it brilliantly.

IX. Challenges & Risk Analysis

The bear case for Anupam Rasayan starts with a simple observation: at 135x P/E, the stock is priced for perfection in an industry where perfection is impossible. One reactor explosion, one quality failure, one key customer loss, and that multiple becomes unjustifiable. The risks aren't theoretical—they're structural, systematic, and in some cases, getting worse.

The ROE Disaster

Company has a low return on equity of 5.39% over last 3 years. For context, putting money in a fixed deposit generates better returns. The culprit is asset intensity meeting working capital hunger. They've deployed ₹2,400 crores in assets to generate ₹160 crores in profit. That's a 6.7% return on assets. Lever it up with modest debt, and you still get single-digit ROEs.

Management argues this is temporary—new capacity coming online, working capital improving, margins expanding. But the structural reality is harsh: specialty chemicals is a capital-intensive, working-capital-heavy business. Even best-in-class players like BASF generate 12-15% ROEs. Anupam Rasayan at 5.39% isn't just below average—it's value-destructive.

The Working Capital Time Bomb

The numbers are staggering: receivables at 165 days, inventory at 140 days. That's ₹750 crores locked in working capital, generating zero return. Worse, it's growing faster than revenue. Working capital as a percentage of sales has increased from 31% to 34% over two years.

The company blames customer payment terms and raw material stocking requirements. But competitors like Clean Science manage with 90-day cycles. The difference? Anupam Rasayan's customer concentration gives buyers negotiating leverage. When Syngenta represents 20% of your revenue, you accept their 180-day payment terms. It's not a partnership—it's dependence.

Customer Concentration: The Double-Edged Sword

Yes, customer stickiness is real. But concentration risk is equally real. The top 3 customers represent 45% of revenue. If one decides to backward integrate, or gets acquired by a company with internal capabilities, or simply faces financial distress, Anupam Rasayan's revenue could drop 15-20% overnight.

The Syngenta-ChemChina merger in 2017 was a near-death experience nobody talks about. ChemChina had internal suppliers for several intermediates Anupam Rasayan was providing. For six months, orders dropped 30%. Only Syngenta's European team's insistence on supply chain continuity saved the relationship. Next time, they might not be so lucky.

Valuation: Priced Beyond Perfection

At 135x P/E, Anupam Rasayan trades at twice the specialty chemical sector average. The bull argument—growth, moats, China+1—is already in the price. Maybe twice over. Any disappointment—a weak quarter, delayed customer approval, working capital spike—and the multiple compression could be savage.

The comparison is sobering. PI Industries, with better ROE and margins, trades at 45x. Aarti Industries, similar business model, trades at 35x. SRF, arguably better positioned, trades at 40x. Either Anupam Rasayan is the greatest chemical company ever created, or it's 50% overvalued. The probability distribution skews heavily toward the latter.

Environmental Regulations: The Sword of Damocles

Gujarat Pollution Control Board (GPCB) has been lenient. But regulations are tightening. The new effluent standards coming in 2025 will require ₹50+ crores in treatment upgrades. The air emission norms proposed for 2026 could require another ₹30 crores. That's ₹80 crores in compliance costs over two years—half a year's profit.

Worse, one serious violation could shut operations for months. In 2019, a minor effluent exceedance led to a 15-day closure notice (later withdrawn). The stock dropped 8% on rumors alone. An actual extended shutdown would be catastrophic—fixed costs continuing while revenue stops.

China's Return: The Existential Threat

The China+1 narrative assumes China remains uncompetitive. But Chinese chemical companies aren't standing still. They're automating, consolidating, and most importantly, moving up the value chain. The same environmental regulations that shut weak players are creating Chinese champions with world-class facilities.

Take Zhejiang Longsheng, which now has zero-discharge facilities that exceed European standards. Or Jiangsu Yangnong, which has automated plants with 50% lower operating costs than Indian peers. When these companies target Anupam Rasayan's products—and they will—the price competition will be brutal.

Raw Material Vulnerability

Anupam Rasayan imports 60% of raw materials, mostly from China. The irony is palpable: the China+1 beneficiary depends on China for critical inputs. When China restricted phosphorus exports in 2021, Anupam Rasayan's costs for certain products spiked 30%. They couldn't pass it through immediately, crushing margins for two quarters.

The backward integration story is largely fiction. Yes, they have Tanfac for fluorine chemistry. But for the 200+ other raw materials? They're at the mercy of global supply chains. One export restriction, one shipping disruption, one supplier bankruptcy, and operations could halt.

Competition from Larger Players

The moat is real but not permanent. Larger players are entering the CSM space. Jubilant, Divi's, even Biocon are building CSM capabilities. They have deeper pockets, broader relationships, and critically, diversified revenue streams that allow them to be more aggressive on pricing.

When Divi's bid for a Bayer intermediate contract in 2023, they offered prices 15% below Anupam Rasayan's. Divi's could afford to lose money for two years to establish the relationship. Anupam Rasayan, with concentrated customer base, couldn't match without destroying profitability. They lost the contract—₹120 crores over five years.

Execution Risks on Expansion

The ₹200 crore expansion sounds modest, but execution in chemicals is never simple. Their last major expansion in 2018 was six months delayed and 20% over budget. The photochemical reactor they installed took 18 months to stabilize versus the planned 6 months.

Now they're entering battery chemicals—a field where they have zero experience. The LiPF6 synthesis involves handling hydrogen fluoride, one of the most dangerous chemicals known. One accident during scale-up, one contamination event, and the entire battery chemical strategy could unravel.

Currency Fluctuation: The Silent Killer

With 65% of revenue in exports and 60% of costs in imports, Anupam Rasayan is essentially a currency play. A 5% rupee appreciation cuts profits by 12%. A 5% depreciation sounds good until you realize raw material costs spike immediately while export realizations lag by 90 days.

They claim to hedge, but the 2022 annual report reveals only 40% of net exposure is hedged. The rest is naked exposure to currency volatility. In a world of unprecedented monetary policy divergence, that's playing with fire.

The Management Succession Question

Anand Desai is 67. Dr. Kiran Patel is 71. The next generation is involved but unproven. In a business built on personal relationships and technical expertise, succession isn't just about ownership—it's about capability and credibility.

When the founders step back—and actuarially, that's within 5-7 years—will Syngenta's procurement head trust the next generation the same way? Will the R&D team maintain its edge without Dr. Patel's technical leadership? The market hasn't priced in succession risk, but it's real and approaching.

The Realistic Assessment

Anupam Rasayan faces a perfect storm of challenges: structural ROE problems, working capital hunger, customer concentration, regulatory pressure, Chinese competition, and execution risks—all while trading at valuations that assume flawless execution.

The business quality is undeniable. The moats are real. But at current valuations, the risk-reward is dramatically skewed. Investors are paying 135x earnings for a business generating 5% ROE, dependent on concentrated customers, vulnerable to regulatory changes, and facing intensifying competition.

The bear case isn't that Anupam Rasayan will fail—it's that they'll succeed but generate returns that don't justify the valuation. In investing, being right about the business but wrong about the price is still being wrong. And at 135x P/E, the price is almost certainly wrong.

X. Bull vs Bear Case & Future Outlook

The future of Anupam Rasayan hinges on a fundamental question: Is this a specialty chemicals company trading at tech multiples, or a tech-like business model disguised as chemical manufacturing? The answer determines whether the stock is 50% overvalued or 50% undervalued. Both cases have merit. Both have blind spots. The truth, as always, lies somewhere in between.

The Bull Case: The Compounding Machine

The bulls see Anupam Rasayan as India's answer to Lonza—a specialty player that compounds value through technical excellence and customer partnerships. The math is compelling: global specialty chemicals growing at 5-6% CAGR, Anupam Rasayan growing at 15-20%, market share gains accelerating.

The ₹14,600 crore LOI pipeline changes everything. Even at 60% conversion (their historical rate), that's ₹8,760 crores in contracted revenue over 5-7 years. Current revenue run rate is ₹1,500 crores. The pipeline alone guarantees doubling, possibly tripling, without winning a single new customer.

The product mix evolution is the hidden growth driver. Agrochemicals at 65% of revenue grows at 8-10%. But pharmaceuticals (9% of revenue) is growing at 30%+, polymers at 25%+, and battery chemicals from zero to potentially 15% of revenue by 2027. The blended growth rate mathematics point to 20%+ CAGR through 2030.

China+1 isn't a narrative—it's a structural shift. Every month, another multinational announces supply chain diversification. Anupam Rasayan doesn't need to win all of it, or even most of it. Capturing 5% of the $80 billion in chemical production shifting from China would triple their revenue. And they're one of maybe five Indian companies with the capability to handle complex chemistry at scale.

The battery chemical entry is transformational. 1,500 TPA of Lithium Hexafluorophosphate (LiPF6) at current prices represents ₹750 crores in annual revenue at 40%+ gross margins. That's one product. They're developing six others. Battery chemicals could be a ₹2,000 crore business by 2030—larger than their current total revenue.

The customer relationships are deepening, not weakening. Syngenta just signed a new 10-year agreement. Sumitomo increased orders 40% in 2024. New customers like E-Lyte and Elementium aren't just buyers—they're partners in product development. The customer concentration "risk" is actually customer investment in Anupam Rasayan's success.

Operational improvements are finally flowing through. Working capital days have dropped 20 in two years. Capacity utilization has increased from 65% to 75%. Gross margins have expanded 300 basis points. Each improvement might seem marginal, but together they're transforming the P&L.

The valuation, while high, is justified by growth duration. This isn't a cyclical chemical company that will see margins compress when China returns. It's a secular growth story riding multiple tailwinds: supply chain diversification, environmental regulations, technical complexity, and customer stickiness. Paying 135x P/E for 20% growth sustained over a decade is actually reasonable.

The Bear Case: The Valuation Trap

The bears see Anupam Rasayan as a decent business at an indecent valuation. The fundamentals don't support the multiple. ROE of 5.39% over 3 years is embarrassing. You're paying 135x earnings for returns below the risk-free rate. That's not investing—it's speculation.

The LOI pipeline is impressive but uncertain. LOIs aren't contracts. They're expressions of interest, subject to product development, price negotiations, and market conditions. Historical conversion might be 60%, but that's during a favorable cycle. In a downturn, LOIs evaporate. Ask any chemical company that signed LOIs in 2007.

Customer concentration remains terrifying. Yes, relationships are sticky. Until they're not. Syngenta-ChemChina's merger almost killed 20% of revenue. What happens when Sumitomo decides to backward integrate? Or when UPL faces financial stress? Concentrated customers have negotiating leverage, and they use it—hence the working capital disaster.

The China threat is real and growing. Chinese producers aren't just competing on price anymore—they're competing on quality, innovation, and sustainability. Companies like Wanhua Chemical now have better ESG scores than European peers. When they target Anupam Rasayan's products with 30% lower prices and equivalent quality, market share will evaporate.

Execution risks are multiplying. Battery chemicals require different expertise than agrochemicals. The new plant construction could face delays, cost overruns, or technical failures. Remember, they've never built a battery chemical plant. The probability of flawless execution is low, but it's priced into the stock.

The competitive landscape is deteriorating. Every Indian chemical company is pursuing CSM. Divi's, Jubilant, Laurus Labs—all better capitalized, all hungry for growth. The moats that protected Anupam Rasayan are being bridged by competitors with deeper pockets and broader capabilities.

Working capital remains a disaster. 165-day receivables in a business with 10% net margins means you're financing customers at negative returns. Every rupee of growth requires more working capital. It's a treadmill—run faster just to stay in place.

The regulatory overhang is underappreciated. One environmental violation, one quality failure, one workplace accident, and the stock drops 20%. In chemical manufacturing, these aren't black swans—they're gray rhinos, visible and approaching.

The Synthesis: Moderate Optimism with Major Caveats

The truth about Anupam Rasayan lies between the extremes. It's neither the compounding machine bulls envision nor the value trap bears fear. It's a good business with real moats, facing real challenges, at a valuation that prices in too much good news.

The next five years will likely see revenue CAGR of 15-18%—impressive but not explosive. Margins will expand modestly as product mix improves. ROE will improve to 10-12%—better but not brilliant. The business will compound value, just not at rates justifying current valuations.

The key variables to watch: 1. LOI conversion rate: Below 50% and growth disappoints 2. Working capital trends: Must improve for ROE expansion 3. Battery chemical execution: Delays would damage credibility 4. Customer diversification: Top 3 below 40% would reduce risk 5. China competition: Market share losses would signal moat erosion

The stock is probably 25-30% overvalued at current levels. In a correction, it could fall to ₹800-850 (P/E of 95-100x), which would be a reasonable entry point for long-term investors. At current levels, the risk-reward is unfavorable—you're betting on flawless execution in an industry where perfection is impossible.

The Investment Decision

For existing shareholders, holding makes sense if you believe in the 10-year story and can stomach 30% drawdowns. For new investors, patience is prudent. Wait for either a correction or evidence of ROE improvement.

The company is at an inflection point. Success in battery chemicals, improved working capital, and sustained China+1 benefits could drive a re-rating even from current levels. But failure on any of these fronts, combined with high valuations, could result in a 40-50% correction.

Anupam Rasayan is a wonderful business at a questionable price. In investing, that's often worse than a questionable business at a wonderful price. The future is bright, but it's already in the price. And in markets, what matters isn't what happens, but what happens relative to expectations. At 135x P/E, expectations are very, very high.

XI. Epilogue & Key Takeaways

In 1984, when Anand Desai was mixing chemicals in a Surat warehouse, the idea that his company would one day supply critical molecules to global giants seemed absurd. The notion that it would command a ₹12,000+ crore market cap at 135x earnings would have been laughable. Yet here we are, watching a regional chemical mixer transformed into India's specialty chemical champion, proving that in business, as in chemistry, the right reactions under the right conditions can create extraordinary transformations.

The Specialty Chemicals Opportunity: India's Hidden Industrial Revolution

Anupam Rasayan's story illuminates a larger truth: India's specialty chemicals opportunity is massive and mostly untapped. The global specialty chemicals market, worth $800 billion, is shifting eastward. China's environmental crackdowns have created a $80-100 billion opportunity for alternative suppliers. India, with its chemistry talent, established infrastructure, and improving regulatory environment, is positioned to capture $20-30 billion of this shift.

But here's what most miss: it's not about cost arbitrage anymore. It's about capability arbitrage. Companies like Anupam Rasayan win not because they're cheaper, but because they can handle complexity that others can't or won't. They're not competing with China on price—they're competing with Switzerland on quality, and winning.

The implications for investors are profound. The next decade will see Indian specialty chemical companies transition from cost-competitive suppliers to innovation partners. The winners won't be those with the lowest costs, but those with the deepest capabilities. Anupam Rasayan, despite its challenges, is positioned on the right side of this transition.

Lessons for Entrepreneurs: The Unglamorous Path to Glory

If Anupam Rasayan were founded today, no venture capitalist would fund it. Too capital-intensive. Too slow to scale. Too dependent on relationships. Too boring. And that's exactly why it works. They built a business in a space where software-style disruption is impossible, where relationships matter more than algorithms, where patient capital beats smart capital.

The lesson for entrepreneurs is counterintuitive: sometimes the best businesses are built in the spaces venture capital ignores. Complex manufacturing, deep technical services, regulated industries—these aren't sexy, but they create real moats. Anupam Rasayan spent 20 years building capabilities before achieving escape velocity. In an era of overnight unicorns, that patience seems anachronistic. It's also why they have 98% customer retention while software companies celebrate 90%.

The technical expertise as a moat deserves special attention. Dr. Patel's chemistry knowledge isn't replaceable by hiring smart MBAs or building software platforms. It's accumulated expertise, built reaction by reaction, failure by failure, over decades. In an economy increasingly dominated by intangible assets, Anupam Rasayan's moat is paradoxically physical—the knowledge embedded in their chemists' minds and their reactors' configurations.

What Anupam Rasayan Tells Us About India's Manufacturing Future

The company is a microcosm of India's manufacturing evolution. From simple assembly to complex manufacturing. From cost arbitrage to capability arbitrage. From vendor to partner. This transformation is happening across industries—pharmaceuticals, electronics, aerospace. But chemicals, with its combination of technical complexity and capital intensity, might be where India builds its most durable competitive advantages.

The geographic concentration in Gujarat isn't accidental—it's strategic. Just as Silicon Valley concentrated software talent, Gujarat is concentrating chemical expertise. The network effects are powerful: shared infrastructure, talent circulation, knowledge spillovers, regulatory expertise. Anupam Rasayan benefits from and contributes to this ecosystem. Their success makes the next company's success more likely.

The governance evolution—from partnership to public company—mirrors India Inc's broader transformation. The retained 59% promoter stake isn't old-fashioned, it's optimal for a business requiring long-term thinking. The addition of independent directors, institutional processes, and quarterly accountability hasn't diluted the entrepreneurial spirit—it's channeled it.

The Importance of Technical Expertise as a Moat

In a world obsessed with digital disruption, Anupam Rasayan reminds us that atoms still matter. Their moat isn't code that can be copied or a brand that can be replicated—it's the ability to manipulate matter at molecular level, reliably, at scale. This kind of expertise can't be acquired or disrupted—it must be built, slowly, carefully, over time.

The 227 PhDs and chemistry postgraduates aren't just employees—they're the company. Their collective knowledge—which reactions work, which don't, which shortcuts are safe, which are dangerous—is the real asset. It's not on the balance sheet, but it's worth more than all the reactors and buildings combined.

This has implications beyond chemicals. As India moves up the value chain, competitive advantage will increasingly come from deep technical expertise rather than cost advantages. Companies that invest in building genuine technical capabilities—whether in chemicals, semiconductors, or advanced materials—will create the most durable moats.

Building in "Boring" but Essential Industries

Anupam Rasayan makes things nobody has heard of for products nobody thinks about. A herbicide intermediate that keeps weeds from destroying crops. A UV absorber that prevents skin cancer. A pharmaceutical building block that becomes diabetes medicine. Boring? Absolutely. Essential? Completely.

The lesson is that boring businesses can be beautiful businesses. They face less competition because they're unsexy. They have pricing power because they're essential. They have customer stickiness because they're embedded in critical processes. While everyone chases the next consumer app, fortunes are being built in industrial enzymes, specialty materials, and yes, chemical intermediates.

The Balancing Act: Growth vs. Governance

Anupam Rasayan's post-IPO journey illustrates the delicate balance between growth and governance. The pressure to deliver quarterly numbers while building for decades. The need to satisfy institutional investors while retaining entrepreneurial agility. The challenge of transparency without revealing competitive secrets.

They've mostly managed this balance well. Growth has continued without compromising quality. Governance has improved without stifling innovation. But the tension remains. At 135x P/E, the market expects perfection. One stumble—a delayed quarter, a failed product development, a governance lapse—and the punishment will be severe.

The Ultimate Question: Can Manufacturing Create Tech-Like Returns?

Anupam Rasayan trades at tech multiples for a manufacturing business. The market is betting that specialized manufacturing can generate software-like economics: high switching costs, recurring revenues, expanding margins, capital-light growth (once infrastructure is built).

The jury is still out. The business quality is undeniable, but whether it justifies the valuation remains uncertain. What's clear is that the old dichotomy—manufacturing equals low returns, technology equals high returns—is breaking down. Companies like Anupam Rasayan that combine manufacturing excellence with technical depth and customer stickiness are creating a new category: physical-world businesses with digital-world economics.

The Final Word

Anupam Rasayan's journey from Surat partnership to specialty chemical champion isn't just a corporate success story—it's a blueprint for building in India's next phase of development. It shows that patient capital, technical expertise, and operational excellence can create extraordinary value, even in supposedly commoditized industries.

For investors, the lesson is nuanced. Great businesses don't always make great investments—valuation matters. But equally, conventional metrics don't always capture moat depth and duration. Anupam Rasayan at 5% ROE looks terrible. Anupam Rasayan with 98% customer retention and 20-year contracts looks brilliant. The truth incorporates both perspectives.

For entrepreneurs, the lesson is clearer. Build where others won't. Develop capabilities others can't. Serve customers others ignore. And most importantly, have the patience to compound small advantages into insurmountable moats.

For India, Anupam Rasayan represents possibility. If a partnership firm from Surat can become a global specialty chemicals player, what else is possible? In a nation often criticized for lacking manufacturing prowess, companies like Anupam Rasayan prove that India can compete not just on cost, but on capability, quality, and innovation.

The story isn't finished. The next chapters—battery chemicals, pharmaceutical expansion, working capital improvement—remain unwritten. Whether Anupam Rasayan justifies its valuation or disappoints expectations, whether it becomes India's Lonza or remains a promising regional player, depends on execution in the coming years.

But what's already been achieved is remarkable. They've proven that Indian manufacturing can be world-class. That complexity can be a moat. That boring can be beautiful. And that sometimes, the best businesses are built not in Silicon Valley or Bangalore, but in the industrial estates of Gujarat, one reaction at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube