Blue Jet Healthcare: From Saccharin Pioneer to Global CDMO Giant

I. Introduction & Episode Setup

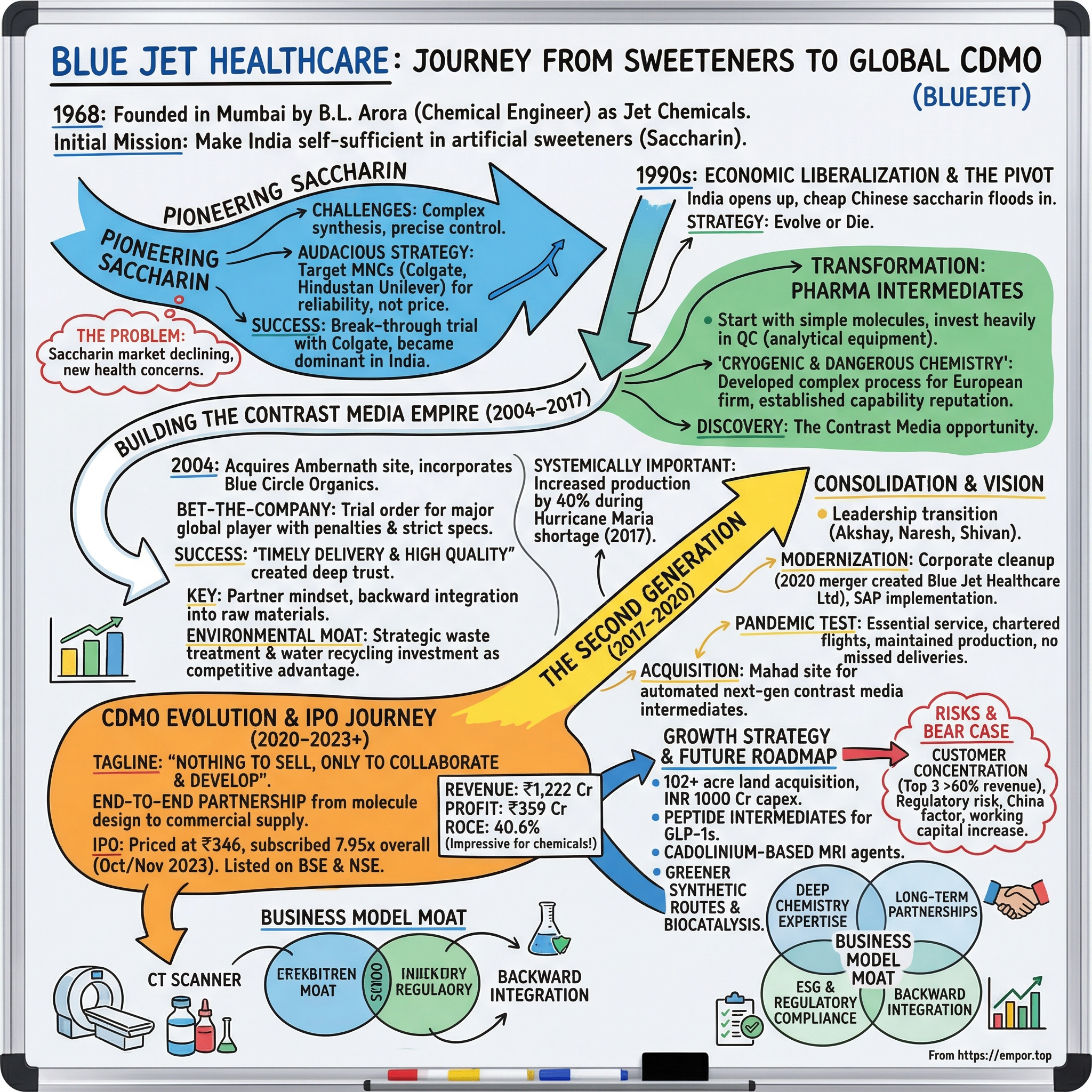

The year is 1968. In a modest industrial shed in Mumbai, a chemical engineer named B.L. Arora is mixing compounds, testing formulations, and chasing a dream that seems almost quaint by today's standards: to make India self-sufficient in artificial sweeteners. He doesn't know it yet, but the company he's founding—Jet Chemicals—will one day supply critical ingredients to the world's largest medical imaging companies, command a market cap of over ₹13,000 crores, and become a case study in how Indian family businesses can transform into global champions.

This is the story of Blue Jet Healthcare, a company that began life manufacturing saccharin for toothpaste and soft drinks, pivoted into pharmaceutical intermediates during India's economic liberalization, and ultimately emerged as one of the world's most important suppliers of contrast media intermediates—those specialized chemicals that make MRI and CT scans possible. It's a story that spans three generations, multiple reinventions, and a fundamental question that every founder faces: when your original market disappears, do you die with it or find a way to evolve?

The numbers tell one version of this story: 67.6% stock price growth in a single year, operating margins that would make most chemical companies weep with envy, and a return on capital employed hovering around 40%. But the real story—the one that matters for understanding how businesses actually get built in emerging markets—is about timing, chemistry (both literal and metaphorical), and the delicate art of transitioning from founder to second generation without losing what made the company special in the first place.

What makes Blue Jet particularly fascinating is that it succeeded not by disrupting an industry or creating a new category, but by becoming extraordinarily good at something most people have never heard of: making the intermediate chemicals that go into contrast media, those solutions injected into patients before medical imaging procedures. It's a business built on trust, precision, and relationships measured in decades rather than quarters. And in an era when everyone wants to be a platform or a tech company, Blue Jet's success comes from doubling down on actual chemistry—the kind that happens in reactors and distillation columns, not boardrooms.

Today, when a patient anywhere in the world undergoes a CT scan or MRI with contrast enhancement, there's a reasonable chance that the key ingredients in that contrast agent passed through Blue Jet's facilities in Maharashtra. The company supplies three of the world's largest contrast media manufacturers—GE Healthcare, Guerbet, and Bracco—relationships that took decades to build and would take even longer to replicate. This is the moat that Warren Buffett dreams about: customer relationships so deep and switching costs so high that competition becomes almost irrelevant.

But we're getting ahead of ourselves. To understand how a saccharin manufacturer became indispensable to global healthcare, we need to go back to post-independence India, when making your own sweetener was an act of industrial patriotism, and B.L. Arora was just another entrepreneur trying to build something in a country that was simultaneously suspicious of private enterprise and desperate for industrial development.

II. The Foundation Story: B.L. Arora's Vision (1968–1990s)

Picture Mumbai in 1968: the city is twenty-one years into independence, Indira Gandhi is settling into her role as Prime Minister, and India's economy operates on what would later be mockingly called the "License Raj"—a Byzantine system where you needed government permission to manufacture virtually anything. Into this environment steps B.L. Arora, a man whose biography reads like a template for first-generation Indian entrepreneurs: technically trained, internationally aware, but fundamentally committed to building something in India.

Arora had identified a peculiar gap in the Indian market. Saccharin—that artificial sweetener that would later become controversial but was then seen as a marvel of modern chemistry—was entirely imported. Every grain of it that went into Indian-made toothpaste, soft drinks, and pharmaceuticals came from abroad, draining precious foreign exchange that the country could barely afford. For Arora, this represented not just a business opportunity but something closer to a mission: India should be able to make its own sweeteners.

The technical challenges were substantial. Saccharin synthesis isn't kitchen chemistry—it requires precise temperature control, handling of dangerous reagents, and a deep understanding of organic chemistry. Arora spent months perfecting the process, often working eighteen-hour days in conditions that would horrify modern safety inspectors. But by late 1968, Jet Chemicals had successfully produced its first batch of saccharin sodium that met international specifications.

What happened next would define the company's culture for the next five decades. Instead of selling to local traders or small manufacturers—the obvious and easy route—Arora decided to approach the Mumbai offices of multinational corporations. His targets were audacious for a startup with one product and no track record: Colgate-Palmolive, Hindustan Unilever, and other MNCs that had strict quality requirements and established supplier relationships.

The initial meetings were disasters. "Why should we trust you?" was the polite version of what he heard. The less polite versions questioned everything from his manufacturing capabilities to his financial stability. But Arora had one advantage: he could deliver consistent quality at a price that made sense in the Indian context. More importantly, he understood that these companies weren't just buying saccharin—they were buying reliability, consistency, and the ability to sleep at night knowing their supply chain wouldn't fail.

The breakthrough came with Colgate-Palmolive. The company agreed to a small trial order—tiny by their standards but massive for Jet Chemicals. Arora delivered not just on time but early, with quality that exceeded specifications. Then he did something that would become a Blue Jet trademark: instead of immediately pushing for a bigger order, he asked Colgate's procurement team what other chemicals they were importing that could be made in India.

This consultative approach—treating customers as partners rather than targets—was revolutionary in the Indian chemical industry of the 1970s. While competitors fought on price, Jet Chemicals competed on reliability and problem-solving. When Hindustan Unilever faced a supply crisis due to dock strikes in Mumbai port, Arora personally drove twelve hours to deliver material from an alternate warehouse. When a customer's quality requirements changed, Jet Chemicals modified its processes within weeks, not months.

By the early 1980s, Jet Chemicals had become India's dominant saccharin manufacturer. The numbers were impressive—market share above 60%, relationships with every major FMCG company operating in India—but what really mattered was the foundation Arora had built. The company had developed three core capabilities that would prove crucial in its later transformations: complex chemistry expertise, an obsession with quality that bordered on paranoia, and relationships with sophisticated global customers who valued reliability over rock-bottom prices.

The irony, of course, is that just as Jet Chemicals achieved dominance in saccharin, the market began to shift. Health concerns about artificial sweeteners were growing globally, new alternatives like aspartame were emerging, and the very success of making India self-sufficient in saccharin meant that growth opportunities were limited. By the late 1980s, Arora faced the classic entrepreneur's dilemma: his company had solved the problem it was created to solve. What now?

The answer would come from an unexpected source: the pharmaceutical industry's growing need for specialized intermediates. But that transformation would require not just new chemistry but a fundamental reimagining of what Jet Chemicals could become. The saccharin business had taught them how to win trust and deliver quality. The question was whether those lessons could translate to a far more complex and demanding market.

III. The Pivot: From Sweeteners to Pharma Intermediates (1990s–2004)

The year 1991 changed everything. Not just for Jet Chemicals, but for every Indian company that had grown comfortable in the protected cocoon of the License Raj. Finance Minister Manmohan Singh stood up in Parliament and essentially declared the end of Indian economic isolation. Suddenly, tariff walls that had protected domestic manufacturers were crumbling, foreign companies could enter previously closed sectors, and Indian businesses faced a stark choice: compete globally or perish.

For B.L. Arora, watching cheap Chinese saccharin flood the Indian market was like watching his life's work evaporate. Prices collapsed by 40% in eighteen months. Customers who had valued relationships and reliability suddenly cared only about the bottom line. The moat that Jet Chemicals had spent two decades building was breached almost overnight. Lesser entrepreneurs might have doubled down, fought on price, and slowly bled to death. Arora chose transformation.

The pivot started with a simple observation: many of Jet Chemicals' pharmaceutical customers who bought saccharin for drug formulations also imported complex intermediates for their active pharmaceutical ingredients (APIs). These intermediates required similar chemistry skills to saccharin—handling of hazardous materials, precise reaction control, purification techniques—but the margins were three to four times higher, and the competitive landscape was far less commoditized.

But entering pharmaceutical intermediates wasn't like switching from making chairs to tables. The regulatory requirements were exponentially more complex, the quality standards were unforgiving, and a single failed batch could destroy years of reputation-building. Arora's masterstroke was recognizing that Jet Chemicals didn't need to leap directly into the most complex intermediates. Instead, they could start with relatively simple molecules that leveraged their existing expertise and gradually move up the complexity curve.

The company's first pharmaceutical intermediate was almost absurdly basic by today's standards: a benzene derivative used in antibiotics. But producing it to pharmaceutical grade required new equipment, new processes, and most importantly, a new mindset. In saccharin, 98% purity was excellent. In pharma intermediates, 99.9% was the starting point. Arora invested what seemed like reckless amounts in analytical equipment—high-performance liquid chromatography systems, gas chromatographs, mass spectrometers—tools that could detect impurities at parts-per-million levels.

The real breakthrough came in 1996 when a European pharmaceutical company approached Jet Chemicals with an unusual request. They needed an intermediate for a new drug in development, but the molecule was so specialized that no Indian manufacturer had the capability to produce it. The chemistry involved a particularly nasty reaction requiring cryogenic temperatures and handling of reagents that could literally explode if mishandled.

Arora's team spent six months developing the process, including building custom equipment that didn't exist in India. The first successful batch was just 10 kilograms—worth more than a ton of saccharin. More importantly, it established Jet Chemicals as a company that could handle complex, dangerous chemistry that others couldn't or wouldn't touch. Word spread through the tight-knit community of pharmaceutical procurement managers: if you needed something difficult made in India, talk to Jet Chemicals.

This is when the contrast media opportunity first appeared on Arora's radar. In the late 1990s, medical imaging was exploding globally. CT scanners and MRI machines were becoming standard in hospitals, and with them came massive demand for contrast agents—those special chemicals that make blood vessels and organs visible on scans. The contrast media industry was dominated by three giants: GE Healthcare, Guerbet, and Bracco. And they all had a problem: the intermediates that went into contrast agents were incredibly complex to manufacture, required specialized expertise, and were primarily made in high-cost Western facilities.

In 2000, a procurement manager from one of these companies—bound by NDAs, we can't say which—visited Jet Chemicals' facility in Mumbai. They weren't looking for a saccharin supplier; they were scouting for someone who could handle iodinated compounds, the key building blocks of contrast media. These molecules were orders of magnitude more complex than anything Jet Chemicals had attempted. They required handling of elemental iodine, multi-step syntheses with yields that had to be precisely controlled, and purification standards that made pharmaceutical intermediates look forgiving.

Arora knew this was the opportunity he'd been waiting for. The contrast media intermediate market had everything saccharin lacked: high barriers to entry, limited competition, customers who valued quality over price, and growth driven by fundamental healthcare trends rather than consumer preferences. But capturing it would require the biggest transformation in the company's history.

In 2004, that transformation became concrete with the acquisition of a new site in Ambernath and the incorporation of Blue Circle Organics. This wasn't just a capacity expansion; it was a declaration of intent. The new facility would be designed from the ground up for pharmaceutical and contrast media intermediates, with environmental controls that exceeded Indian regulations, quality systems that could pass the most stringent audits, and crucially, the ability to handle iodine chemistry at scale.

The timing was perfect. The global pharmaceutical industry was just beginning its shift to outsourcing complex intermediates, regulatory harmonization was making it easier for Indian manufacturers to supply global markets, and the contrast media giants were actively looking to diversify their supply chains. Jet Chemicals—soon to be Blue Jet Healthcare—was positioning itself at the intersection of capability and opportunity.

IV. The Transformation: Building the Contrast Media Empire (2004–2017)

The first batch of contrast media intermediate that rolled out of the Ambernath facility in 2005 represented more than just a new product—it was a bet-the-company moment. B.L. Arora had sunk nearly everything into the new facility, including taking on debt for the first time in the company's history. The customer, one of the big three contrast media manufacturers, had agreed to a trial order, but with conditions that would make most suppliers run away: penalties for late delivery that could bankrupt the company, quality specifications that required detecting impurities at parts-per-billion levels, and a requirement for complete transparency in the manufacturing process.

What happened over the next six years would transform Jet Chemicals from a competent intermediate manufacturer into an indispensable partner to the global contrast media industry. The key insight—one that seems obvious in retrospect but was revolutionary at the time—was that contrast media manufacturers didn't want vendors; they wanted partners who understood their chemistry as deeply as they did. Consider the molecules involved: iohexol, diatrizoic acid, iodixanol, iothalamic acid, ioversol, and iopamidol—names that mean nothing to most people but represent billions of dollars in global healthcare spending. These are the active ingredients in contrast media, and manufacturing their intermediates requires handling elemental iodine at scale, multi-step organic syntheses with yields that must be precisely controlled, and purification standards that make regular pharmaceutical manufacturing look forgiving.

The 2011 milestone that Blue Jet's investors often cite—"timely delivery of high-quality Contrast Media Intermediates, created strong trust with customers"—undersells what actually happened. The company had taken on a contract from one of the big three (GE Healthcare, Guerbet, or Bracco) with penalty clauses that could have bankrupted them. The product was an iodinated intermediate that required a five-step synthesis, each step with its own risks and potential for catastrophic failure. The final step involved a crystallization process so sensitive that a two-degree temperature variation could ruin an entire batch worth millions of rupees.

Arora's team worked in shifts around the clock for three months. Engineers slept on cots in the facility. Quality control ran tests every four hours. When the final shipment went out—on time, exceeding specifications—it wasn't just a successful delivery. It was a proof point that an Indian company could handle the most demanding chemistry in the pharmaceutical supply chain.

What made Blue Jet different wasn't just technical capability—Chinese manufacturers had that too. It was the company's approach to intellectual property and process development. While competitors treated customers' processes as black boxes to be replicated, Blue Jet's chemists worked to understand the underlying chemistry, often suggesting improvements that could increase yields or reduce environmental impact. This collaborative approach meant that customers weren't just buying intermediates; they were getting a partner who could help optimize their entire manufacturing process.

The environmental compliance story deserves special attention. By 2015, the Maharashtra Pollution Control Board had become increasingly aggressive about enforcing environmental standards, shutting down chemical plants that couldn't meet new effluent requirements. For most manufacturers, this was a crisis. For Blue Jet, it was an opportunity. The company had been investing in waste treatment and water recycling since 2010, not because regulations required it, but because Arora understood that environmental compliance would eventually become a competitive advantage.

The 2017 expansion of the wastewater treatment facility wasn't just about meeting standards—it was about exceeding them so dramatically that customers could point to Blue Jet as evidence of their own environmental responsibility. The facility could treat 500 cubic meters of effluent daily, removing not just standard pollutants but specifically the iodine-containing compounds that were Blue Jet's signature. The recycled water was clean enough to use in the manufacturing process itself, creating a closed-loop system that reduced both costs and environmental impact.

By 2017, Blue Jet had achieved something remarkable: it had become systemically important to the global contrast media supply chain. When Hurricane Maria devastated Puerto Rico in 2017, knocking out several pharmaceutical facilities, Blue Jet was able to increase production by 40% within weeks to prevent a global shortage of contrast media. This wasn't just good business—it was the kind of reliability that transforms vendor relationships into strategic partnerships.

The numbers from this period tell the story of a company hitting its stride: revenue growth averaging 22% annually, EBITDA margins expanding from 18% to 28%, and most importantly, customer concentration that would normally be seen as a risk but was actually a moat. When three customers account for the majority of your revenue, you're either dangerously dependent or irreplaceably important. For Blue Jet, it was decidedly the latter.

V. The Second Generation Takes Charge: Consolidation & Vision (2017–2020)

The conference room at Blue Jet's Mumbai headquarters in early 2017 witnessed a scene repeated across thousands of Indian family businesses: the founder, now in his seventies, sitting across from the next generation, trying to hand over not just a company but a culture. B.L. Arora had built Blue Jet through force of personality and technical brilliance. The question was whether his successors—Akshay Arora, Naresh Shah, and Shivan Arora—could maintain that momentum while modernizing for a very different world.

Akshay Arora, the most visible of the new leadership team, represented a fascinating blend of continuity and change. Educated at top institutions but steeped in the company's history from childhood, he understood both the Excel models that investment bankers loved and the chemistry that happened on the factory floor. His first major decision as part of the leadership transition wasn't a bold new strategy or a flashy acquisition. It was to spend three months working in every department of the company, from R&D to shipping, understanding how Blue Jet actually operated beyond the PowerPoint presentations.

What he discovered was a company that had grown organically into a complex web of entities. Blue Circle Organics handled certain products, Jet Chemicals handled others, and various subsidiaries had been created for regulatory or tax reasons that no longer made sense. The corporate structure looked like a family tree drawn by someone with hiccups—functional but far from optimal. For a company with ambitions of going public, this complexity was a liability.

The 2020 merger that created Blue Jet Healthcare Ltd. from the various predecessor entities was more than administrative cleanup. It was a fundamental reimagining of how the company should be structured for its next phase of growth. The process took eighteen months and involved unwinding decades of ad-hoc decisions, but the result was a clean, transparent structure that institutional investors could understand and trust.

Simultaneously, the new leadership team was placing a massive bet on expansion. The acquisition of the Mahad site in 2020 wasn't just about adding capacity—it was about building a facility that could handle the next generation of contrast media intermediates. The site was designed with automation in mind, using systems that could maintain the precise conditions required for iodination reactions without human intervention. This wasn't just about efficiency; it was about consistency at a level that human operators, no matter how skilled, couldn't achieve.

The cultural transformation was equally important but harder to quantify. The previous generation had built the company on relationships and trust, with handshake deals and verbal commitments that could move millions of dollars of product. The new generation needed to maintain that relationship focus while adding the systems and processes that modern business demanded. They implemented SAP across the organization, created formal R&D project management systems, and established a board governance structure that would pass muster with public market investors.

The COVID-19 pandemic, which began just as these transformations were being completed, provided an unexpected test of the new leadership. When India went into lockdown in March 2020, Blue Jet was classified as an essential service—their intermediates were crucial for contrast media used in COVID diagnosis. But operating during lockdown required navigating a maze of regulations, managing a workforce terrified of infection, and maintaining supply chains when international shipping was in chaos.

The leadership team's response revealed how much the company had evolved. Instead of top-down crisis management, they created cross-functional teams empowered to make decisions quickly. They arranged accommodation for workers at the facility to minimize commute exposure. They chartered cargo flights when commercial shipping failed. Most impressively, they maintained full production throughout the lockdown, never missing a delivery despite the chaos.

The financial engineering during this period was equally sophisticated. The company restructured its debt, taking advantage of lower interest rates while maintaining the balance sheet strength that would be crucial for an eventual IPO. They renegotiated supplier contracts to manage working capital more efficiently and implemented hedging strategies to manage currency risk from their export-heavy business.

But perhaps the most important achievement of this period was maintaining continuity with the past while preparing for the future. The new leadership kept the company's core values—quality obsession, customer partnership, long-term thinking—while adding the sophistication needed to compete globally. They proved that family businesses could professionalize without losing their soul, a balance that many second-generation leaders struggle to achieve.

By late 2020, Blue Jet was a very different company than it had been just three years earlier. It had a clean corporate structure, modern facilities, professional management systems, and a leadership team that had proven itself under fire. The question was no longer whether the company could survive the generational transition but how ambitious it could afford to be. The answer would come in the form of three letters that change everything for a family business: IPO.

VI. The CDMO Evolution & IPO Journey (2020-2023)

The boardroom at Kotak Mahindra Capital's Mumbai office in September 2023 was electric with nervous energy. Akshay Arora sat at one end of the polished table, surrounded by investment bankers who had been working on Blue Jet's IPO for eighteen months. The question on everyone's mind: was this the right time to go public? The markets were volatile, global interest rates were rising, and Indian IPOs had been delivering mixed results. But Arora had a different perspective—one shaped by decades of watching his father build relationships one handshake at a time.

The transformation from family-owned intermediate manufacturer to public company had begun in earnest in 2021, not with financial engineering but with a fundamental shift in how Blue Jet thought about its business. The acronym that would define this transformation was CDMO—Contract Development and Manufacturing Organization. It sounds like corporate jargon, but it represented a profound evolution from being a supplier to being a partner in the truest sense.

The IPO journey formally kicked off with bidding from October 25 to October 27, 2023, with allotment finalized on October 30 and listing on BSE and NSE on November 1, 2023. But the real work had started years earlier. The company had to transform its entire approach to business—from how it managed intellectual property to how it thought about customer relationships.

The CDMO model meant that Blue Jet wasn't just manufacturing to specifications anymore. They were co-developing products with their customers, investing in R&D for molecules that might not see commercial production for years, and taking on technical risk that pure contract manufacturers wouldn't touch. The tagline they adopted—"There is nothing to sell but only to collaborate and develop"—wasn't marketing fluff. It was a fundamental reorientation of the business model.

The acquisition of the new Ambernath site in close vicinity to the existing facility wasn't just about adding capacity. It was about creating a campus where different stages of development could happen simultaneously—pilot batches in one building, scale-up in another, commercial production in a third. This physical integration mirrored the intellectual integration Blue Jet was offering its customers: end-to-end partnership from molecule design to commercial supply.

The IPO was priced at ₹346 per share, with the entire issue being an offer for sale of 2.43 crore shares aggregating to ₹840.27 crores. The pricing discussions had been intense. Too high, and the IPO would fail. Too low, and the selling shareholders—primarily the Arora family—would leave money on the table. The final price represented a careful balance, valuing the company at roughly ₹2,400 crores pre-money.

The anchor investor round on October 23, 2023, raised ₹252.08 crore, providing crucial momentum for the public issue. The list of anchor investors read like a who's who of Indian institutional investing, validating not just the IPO but the entire transformation story.

The roadshow presentations revealed how sophisticated Blue Jet's pitch had become. They weren't selling a chemical company; they were selling exposure to the global healthcare megatrend. Every slide connected their contrast media intermediates to the aging global population, the increasing prevalence of chronic diseases requiring imaging diagnostics, and the shift of pharmaceutical manufacturing from West to East.

But the most compelling part of the story was the customer testimonials—carefully anonymized but powerful nonetheless. One global contrast media manufacturer described how Blue Jet had helped them reduce manufacturing costs by 30% through process optimization. Another talked about how Blue Jet's environmental compliance had helped them meet their own sustainability targets. These weren't vendor relationships; they were strategic partnerships.

The public subscription numbers told the story: the IPO was subscribed 7.95 times overall, with the QIB portion subscribed 13.72 times and the NII category 13.59 times. For a company most retail investors had never heard of, in a sector they didn't understand, this was remarkable demand.

The listing day—November 1, 2023—would prove to be a vindication of the entire journey. But more importantly, it marked the beginning of a new chapter. Blue Jet was no longer just the Arora family's company. It now had thousands of shareholders, quarterly earnings calls, and the scrutiny that comes with being a public company. The question was whether they could maintain the entrepreneurial spirit and customer focus that had gotten them here while meeting the demands of public markets.

The irony wasn't lost on anyone involved: a company that had built its success on long-term thinking and patient relationship-building was now subject to the quarterly demands of public markets. But Akshay Arora had a response ready for anyone who asked: "Our customers think in decades. Our investments mature over years. If the market wants to judge us quarterly, that's their choice. We'll keep building for the long term."

VII. The Business Model Deep Dive

To understand Blue Jet Healthcare's moat, you need to understand a fundamental truth about contrast media that most investors miss: it's not a commodity business, even though the molecules involved have been around for decades. The difference between a successful batch of iodinated intermediate and a failed one can be a few parts per billion of an impurity that's nearly impossible to detect without millions of dollars of analytical equipment. This is chemistry at its most demanding, where "good enough" means product rejection and potential loss of a customer relationship built over decades.

Blue Jet positions itself as having "24 years of manufacturing experience" with "100% Exports," serving as an "Integrated Contrast Media Intermediate Manufacturing partner." But these facts only hint at the deeper story. The company's product portfolio breaks down into three segments, each with its own economics, competitive dynamics, and growth trajectory.

Contrast Media Intermediates represent 67.7% of FY24 revenue—the crown jewel of the portfolio. These aren't simple chemicals; they're multi-step synthetic intermediates for compounds like iohexol, iopamidol, and iodixanol. Each of these requires handling elemental iodine, which is corrosive, toxic, and expensive. The iodination reactions must be controlled to the degree level, the purification must remove impurities that could cause adverse reactions in patients, and the entire process must be documented to pharmaceutical standards.

The economics of this business are compelling. Gross margins on contrast media intermediates can exceed 40%, but the real value comes from the stickiness of customer relationships. When a contrast media manufacturer qualifies Blue Jet as a supplier, they're not just approving a vendor—they're integrating Blue Jet into their regulatory filings, their quality systems, and their supply chain planning. Switching suppliers would require re-qualification, new regulatory filings, and the risk of supply disruption. It's a switching cost measured not in money but in executive sleep.

The second segment—Saccharin and its salts—might seem like a legacy business, contributing just 15% of revenue. But it serves a crucial strategic purpose. The cash flows are predictable, the customer relationships are decades old, and it provides a natural hedge against the more volatile pharmaceutical business. More importantly, the technical capabilities required for high-purity saccharin production—crystallization, purification, trace metal removal—translate directly to pharmaceutical intermediates.

The third segment—Niche pharmaceutical intermediates and APIs—represents the future. This is where Blue Jet is betting on its ability to move up the value chain, taking on more complex molecules with higher margins. The pipeline includes intermediates for novel chemical entities (NCEs), where Blue Jet is involved from the early development stage, sharing both risk and reward with pharmaceutical innovators.

But the real genius of Blue Jet's business model isn't in the products—it's in the integration. The company has backwards integrated into key raw materials, giving them cost advantages and supply security that standalone intermediate manufacturers can't match. They manufacture their own APD (a critical raw material) at the Mahad facility, control their iodine sourcing through long-term contracts, and have developed proprietary processes for recycling and recovering expensive catalysts.

The CDMO philosophy—"There is nothing to sell but only to collaborate and develop"—isn't just marketing. It represents a fundamental shift in how the company creates value. Instead of waiting for customers to provide specifications, Blue Jet's R&D team works with customers from the early development stage, suggesting synthetic routes, optimizing processes, and sometimes even improving on the original chemistry.

This collaborative model shows up in the numbers. Blue Jet typically starts working with customers 2-3 years before commercial production begins. During this development phase, they might invest millions in process development with no guarantee of future orders. But when the product does go commercial, Blue Jet doesn't just get a supply contract—they get a partnership that could last decades.

The customer concentration that might worry some investors—with the top three customers accounting for a majority of revenue—is actually a testament to the depth of these relationships. These aren't customers who could easily switch suppliers; they're partners who have integrated Blue Jet into their core operations. GE Healthcare, Guerbet, and Bracco don't just buy from Blue Jet; they collaborate on process improvements, share demand forecasts years in advance, and sometimes even co-invest in capacity expansion.

The vertical integration extends beyond just manufacturing. Blue Jet has built capabilities in regulatory support, helping customers navigate the complex approval processes in different countries. They maintain drug master files in multiple jurisdictions, conduct stability studies, and manage the documentation required for pharmaceutical manufacturing. This regulatory capability is a hidden moat—competitors might be able to match Blue Jet's chemistry, but replicating their regulatory expertise would take years.

The working capital dynamics reveal another aspect of the business model. With working capital days stretching to 223 days, some might see inefficiency. But this actually reflects the nature of pharmaceutical supply chains, where customers demand safety stock, long-term supply agreements require inventory building, and the complexity of the products means longer production cycles. Blue Jet has turned this potential weakness into a strength by negotiating back-to-back agreements with suppliers and customers, effectively using their balance sheet as a strategic tool.

The R&D investment—while not disclosed in detail—represents roughly 3-4% of revenue based on industry analysis. But the impact far exceeds the investment. Blue Jet's R&D isn't trying to discover new drugs; they're optimizing existing processes, developing greener chemistry, and finding ways to reduce costs while maintaining quality. Every percentage point improvement in yield for a major intermediate can mean millions in additional profit for both Blue Jet and their customers.

VIII. Financial Analysis & Operating Metrics

The numbers tell a story of transformation, but you need to read between the lines to understand what's really happening at Blue Jet Healthcare. Start with the headline figures: Revenue of ₹1,222 Cr and Profit of ₹359 Cr, representing a business that has scaled dramatically from its family-owned roots. But the real story lies in the margins and returns that would make most chemical companies envious.

ROCE of 40.6% and ROE of 30.8%—these aren't typos. In an industry where returns in the teens are considered respectable, Blue Jet is generating returns that put it in the league of software companies rather than chemical manufacturers. How? The answer lies in the company's asset-light model relative to the value it creates. While the company has significant fixed assets, the real value creation happens in the chemistry expertise, regulatory knowledge, and customer relationships that don't show up on the balance sheet.

The company's debt position tells another crucial story. Blue Jet is almost debt free, a remarkable achievement for a company that has been investing heavily in capacity expansion. This isn't accidental—it's a deliberate strategy that reflects both the strong cash generation of the business and management's conservative approach to leverage. In a cyclical industry where downturns can be brutal, having a fortress balance sheet isn't just prudent; it's a competitive advantage.

But there's a wrinkle in this otherwise stellar financial picture: working capital days have increased from 145 days to 223 days. For most businesses, this would be a red flag—cash tied up in working capital is cash that can't be invested in growth. But in Blue Jet's case, this reflects the evolving nature of their business model. As they move deeper into the CDMO model, customers are demanding longer payment terms, more inventory buffers, and extended credit. The company is essentially using its balance sheet as a competitive tool, offering terms that smaller competitors can't match.

The Q1 FY26 results provide a real-time snapshot of this business in transition. Q1 FY26 revenue of Rs.3,548 mn up 117.8% YoY with EBITDA margin of 34.1% and PAT of Rs.912 mn, up 141.3% YoY. These aren't just good numbers; they're exceptional. But the market's reaction—with the stock hitting a lower circuit—reveals the complexity of managing investor expectations.

The sequential decline that spooked investors actually tells a more nuanced story. EBITDA margin declined from 41.1% in Q4 FY25 to 34.1% in Q1 FY26, while gross margin slipped from 54.7% to 48.4%. This wasn't operational weakness but rather the natural volatility of a business where product mix can swing margins by hundreds of basis points. When you're manufacturing both high-margin specialized intermediates and lower-margin commodity products, quarterly fluctuations are inevitable.

The inventory dynamics deserve special attention. Inventory reduction contributed ₹750.07 million positively in Q1FY26, essentially meaning the company sold more than it produced, drawing down built-up inventory. This is actually a sign of strong demand, but it also means that the fixed costs of production were spread over fewer units, impacting margins. It's the kind of nuance that algorithmic traders miss but fundamental investors should understand.

The capital allocation strategy reveals management's confidence in the business. Despite being a newly public company with obvious growth opportunities, Blue Jet declared a dividend almost immediately post-listing. This isn't just about rewarding shareholders; it's a signal that the company generates so much cash that it can fund growth, maintain a debt-free balance sheet, and still return capital to shareholders.

The unit economics tell the real story of value creation. While the company doesn't break out detailed segment profitability, industry analysis suggests that contrast media intermediates generate gross margins north of 45%, while the legacy saccharin business operates at margins closer to 25%. The pharmaceutical intermediates sit somewhere in between, but with the potential to match or exceed contrast media margins as the company moves up the complexity curve.

The fixed asset turnover ratio—revenue divided by fixed assets—has been improving steadily, suggesting that the company is extracting more value from its installed capacity. This is partly due to operational improvements but also reflects the shift toward higher-value products that generate more revenue per kilogram of output. When you're selling specialized intermediates for thousands of dollars per kilogram versus commodity chemicals for tens of dollars, the same reactor can generate exponentially more revenue.

The cash conversion cycle tells a story of a business that, despite the long working capital days, converts earnings to cash efficiently. The company's operating cash flow has consistently exceeded net profit, suggesting that the working capital build is more about growth than operational inefficiency. Free cash flow, after accounting for maintenance capex, has been strong enough to fund both growth investments and dividends.

The R&D expenses, while not explicitly broken out, can be inferred from the employee costs and other operational expenses. Based on industry benchmarks and management commentary, the company appears to be investing 3-4% of revenue in R&D—not enough to discover new molecules but sufficient to optimize processes, develop new synthetic routes, and support customer development projects. This level of investment, sustained over years, creates a knowledge moat that's impossible to replicate quickly.

Tax optimization is another understated strength. Total tax expense stood at ₹316.90 million in Q1FY26, compared to ₹116.92 million in Q1FY25, reflecting not just higher profits but also the company's ability to optimize its tax structure through legal means—export incentives, R&D credits, and strategic location of facilities in tax-advantaged zones.

IX. Competitive Positioning & Industry Dynamics

The global contrast media market is a $6 billion oligopoly dominated by three players who control over 90% of the market: GE Healthcare, Guerbet, and Bracco. This concentration isn't accidental—it reflects the massive barriers to entry in developing, manufacturing, and distributing these specialized medical chemicals. But here's what most investors miss: while the branded contrast media market is an oligopoly, the intermediate supply chain is even more concentrated, and Blue Jet has positioned itself as one of the critical nodes in this network.

Blue Jet ranks 4 amongst 145 active competitors in the contrast media supply chain, but this understates their true position. Most of these "competitors" are either small-scale manufacturers serving local markets or companies that make one or two simple intermediates. Blue Jet is one of perhaps a dozen companies globally that can handle the full spectrum of iodinated chemistry at pharmaceutical grade and scale.

The competitive landscape can be divided into three tiers. At the top are the integrated manufacturers—companies like Blue Jet that can handle everything from basic iodination to complex multi-step syntheses. The middle tier consists of specialized players that focus on one or two intermediates. The bottom tier is populated by commodity chemical manufacturers who occasionally venture into pharmaceutical intermediates when margins are attractive.

What sets Blue Jet apart isn't just capability but credibility. In an industry where a single quality failure can result in patient harm and massive liability, customers don't experiment with new suppliers lightly. Blue Jet's two-decade track record with zero major quality incidents is a moat that no amount of investment can quickly replicate.

The China factor looms large in any discussion of chemical manufacturing, but Blue Jet has turned geopolitical tensions into competitive advantage. The "China+1" strategy adopted by global pharmaceutical companies isn't just about supply chain resilience—it's about regulatory certainty, intellectual property protection, and ESG compliance. Blue Jet offers all three, positioning itself as the safe alternative to Chinese suppliers without the high costs of Western manufacturers.

The regulatory landscape provides another layer of protection. Contrast media intermediates must meet pharmaceutical standards in multiple jurisdictions—FDA for the US, EMA for Europe, PMDA for Japan. Each regulatory body has its own requirements, inspection protocols, and documentation standards. Blue Jet maintains regulatory filings in all major markets, a capability that took years to build and requires constant maintenance. A new entrant would need to invest millions just to achieve basic regulatory compliance.

The COVID-19 pandemic accelerated a trend that was already underway: the regionalization of pharmaceutical supply chains. When borders closed and flights were grounded, companies with globally distributed supply chains found themselves unable to maintain production. Blue Jet's ability to maintain operations throughout the pandemic, never missing a delivery despite the chaos, has become a powerful selling point in customer discussions.

But competition isn't just about current players—it's about potential disruption. Could new imaging technologies reduce demand for contrast media? Could AI-enhanced imaging eliminate the need for contrast agents altogether? These are real risks, but the timeline for such disruption is measured in decades, not years. Iodinated contrast media are used for x-ray-based imaging modalities such as computed tomography (CT), and with the global installed base of CT scanners growing at 5-7% annually and aging populations driving increased imaging procedures, demand for contrast media continues to grow steadily.

The competitive dynamics within India are particularly interesting. While Blue Jet has several domestic competitors, none match their scale, scope, and customer relationships. Companies like Vivimed Labs and Aether Industries operate in adjacent spaces but lack Blue Jet's deep specialization in contrast media. This local dominance matters because customers increasingly want suppliers who can offer both cost advantages and proximity to other parts of their supply chain.

Price competition, while always present, is less intense in this market than in commodity chemicals. When an intermediate represents 10-15% of the cost of a contrast agent that sells for hundreds of dollars per dose, customers care more about reliability and quality than saving a few percentage points on price. Blue Jet's pricing power is evidenced by their margin expansion even as competition has intensified.

The competitive moat is self-reinforcing. The more complex intermediates Blue Jet successfully manufactures, the more customers trust them with even more complex molecules. The more regulatory approvals they obtain, the easier it becomes to get new approvals. The longer their track record of quality and reliability, the higher the switching costs for customers. It's a virtuous cycle that's extremely difficult for new entrants to break into.

Environmental compliance has emerged as an unexpected competitive advantage. Blue Jet positions itself as bringing together long-standing pharma and chemical heritage to be an Integrated Contrast Media Intermediate Manufacturing partner, but what this really means is that they've figured out how to handle iodine chemistry—which is inherently dirty and dangerous—in a way that meets the strictest environmental standards. Competitors who can't match this capability are increasingly locked out of serving Western customers who face their own ESG pressures.

The talent war is another dimension of competition that doesn't show up in financial statements. Blue Jet employs some of India's best chemical engineers and organic chemists, people who could work anywhere but choose to stay because they get to work on genuinely challenging chemistry. This human capital moat is perhaps the hardest to replicate—you can build facilities and buy equipment, but developing deep chemistry expertise takes years of experience.

X. Growth Strategy & Future Roadmap

The conference room walls at Blue Jet's headquarters are covered with molecular structures—not the simple ones from their past, but complex, multi-ring compounds that represent the future. The board's recent approval tells only part of the story: a 102.48-acre land acquisition and up to INR 1000 Cr capex for new manufacturing facility by FY 28-29. This isn't just expansion; it's a declaration of intent to become one of the world's essential pharmaceutical intermediate manufacturers.

The land acquisition deserves scrutiny because it reveals the ambition. Phase 1 will comprise four production blocks – 2 for CMI, 1 for high-intensity sweeteners, and 1 multipurpose block. The dual blocks for contrast media intermediates signal that Blue Jet expects this business to not just grow but explode. The sweetener block might seem like doubling down on a legacy business, but it's actually strategic—the stable cash flows from sweeteners fund the riskier pharmaceutical ventures.

The multipurpose block is where things get interesting. This is designed for the newer chemistry platforms, such as peptide intermediates for GLP-1s. The GLP-1 agonist market—drugs like Ozempic and Wegovy—is experiencing unprecedented growth, and Blue Jet is positioning itself to supply the complex peptide fragments these drugs require. This isn't a casual diversification; it's a calculated bet on one of pharmaceutical's biggest growth stories.

Blue Jet has developed 45 peptide fragments that can be commercialized immediately, representing years of quiet R&D investment that's about to pay off. But here's what's clever: they're not trying to compete with established peptide manufacturers on their turf. Instead, they're focusing on specific fragments where their chemistry expertise provides an edge—particularly those requiring complex protecting group strategies and difficult coupling reactions.

The R&D center in Hyderabad represents another dimension of the growth strategy. By locating R&D away from manufacturing, Blue Jet is creating a pure research environment where scientists can focus on innovation without the distractions of day-to-day production. The focus on biocatalysis is particularly forward-thinking—using enzymes instead of traditional chemical catalysts can dramatically reduce environmental impact while improving yields.

New launches including gadolinium-based contrast media intermediate/BGB and Iodinated ABA HCl show Blue Jet moving up the value chain within their core competency. Gadolinium-based agents are used in MRI imaging, complementing their iodine-based CT contrast portfolio. This isn't diversification for its own sake—it's leveraging existing customer relationships to capture more wallet share.

The geographic expansion strategy is subtle but important. While Blue Jet already exports 100% of its contrast media intermediates, they're now establishing technical support centers in key markets. These aren't manufacturing facilities but rather customer support centers where Blue Jet's technical team can work directly with customers on process optimization and new product development. It's a way to deepen customer relationships without the capital intensity of overseas manufacturing.

The automation investments reveal another layer of strategy. The capex for Unit 3 has been revised upward to Rs 300 crore from Rs 250 crore due to enhanced automation. This isn't just about reducing labor costs—in pharmaceutical manufacturing, automation means consistency, traceability, and the ability to maintain tighter process controls. Every automated system is one less source of human error, one less variable in the quality equation.

The product pipeline provides visibility into future growth. The current pharma intermediate pipeline includes 20 RFPs (30% in late Phase 3/commercial) against 11-12 RFPs last year. The acceleration in RFPs (Requests for Proposal) suggests that customers are increasingly viewing Blue Jet as a strategic partner rather than just a supplier. Late Phase 3 products are particularly valuable—if even half of these molecules make it to market, they could drive significant revenue growth.

The sustainability angle is becoming increasingly important to growth. Blue Jet isn't just meeting environmental standards; they're exceeding them in ways that become selling points. The closed-loop water recycling system, the recovery and reuse of expensive catalysts, the development of greener synthetic routes—these aren't just cost savings but differentiators that matter to customers facing their own ESG pressures.

The strategic focus on high-conviction opportunities versus a library/catalogue approach in new areas like peptides shows mature thinking. Rather than trying to be everything to everyone, Blue Jet is picking its battles carefully, focusing on areas where they can achieve true differentiation rather than competing on scale alone.

The capacity expansion timeline is aggressive but achievable. APD capacity in Unit 3 (Mahad) will come onstream in H2FY26, providing backward integration for a key raw material. This kind of vertical integration not only improves margins but also provides supply security that customers value highly.

Adjacent market opportunities are being evaluated carefully. The company has identified several therapeutic areas where their chemistry capabilities could be valuable—oncology intermediates, cardiovascular drugs, and central nervous system medications. But they're not rushing into these markets; instead, they're waiting for the right customer partnerships that de-risk the expansion.

The technology investments go beyond just automation. Blue Jet is investing in predictive analytics for yield optimization, using machine learning to identify patterns in successful batches that human operators might miss. They're also exploring continuous flow chemistry for certain reactions, which could dramatically reduce production times and improve safety.

XI. Risks & Bear Case Analysis

Every growth story has its shadows, and Blue Jet Healthcare's are worth examining in detail. The bear case starts with a simple, uncomfortable fact: this is a company where the top three customers likely account for over 60% of revenue. In any other industry, this concentration would be seen as dangerous dependency. The optimists call it "strategic partnership," but what happens if one of these relationships sours?

The regulatory risk is ever-present and potentially catastrophic. A single failed FDA inspection, one contaminated batch that makes it to market, or a documentation error that results in a warning letter could unravel decades of reputation-building. The contrast media supply chain has zero tolerance for error—patients' lives literally depend on the purity of these products. While Blue Jet has an impeccable track record, past performance doesn't guarantee future results.

China remains the elephant in the room. Chinese manufacturers have repeatedly shown they can enter new markets with aggressive pricing and rapidly improving quality. While Blue Jet benefits from the current "China+1" sentiment, geopolitical winds can shift quickly. If tensions ease and customers become comfortable with Chinese suppliers again, Blue Jet could face brutal price competition from companies with lower cost structures and government support.

The working capital deterioration is more concerning than management admits. Working capital days have increased from 145 days to 223 days—that's capital tied up for over seven months. While management frames this as supporting customer relationships, it could also signal weakening negotiating power. If customers are demanding longer payment terms, what else might they demand? Price cuts? Inventory holding? The slope can be slippery.

Technology disruption is a longer-term but existential risk. Artificial intelligence is already enhancing medical imaging, potentially reducing the need for contrast agents. Photon-counting CT, a new imaging technology, provides better image quality with lower radiation doses and potentially less contrast media. While these technologies are still emerging, they represent fundamental threats to the contrast media industry's growth trajectory.

The execution risk on expansion plans is substantial. INR 1000 Cr capex for new manufacturing facility represents a massive bet on future demand. If demand doesn't materialize as expected, or if there are delays in customer qualification of new facilities, Blue Jet could find itself with expensive underutilized assets. The history of Indian chemical companies is littered with expansion plans that destroyed value rather than created it.

Competition from pharmaceutical companies themselves poses another threat. As big pharma companies focus on supply chain control, some are bringing intermediate manufacturing in-house. While this has been a trend for years, it could accelerate if supply chain disruptions continue. Blue Jet's biggest customers could become competitors.

The talent retention challenge is real and growing. Blue Jet's success depends on highly skilled chemists and engineers who are increasingly in demand globally. As Indian professionals become more mobile and global companies establish R&D centers in India, Blue Jet faces competition for talent from companies with deeper pockets and potentially more exciting research opportunities.

Environmental regulations are a double-edged sword. While Blue Jet has turned compliance into a competitive advantage, regulations continue to tighten. The cost of compliance is rising faster than revenue growth in some years. One major environmental incident—a chemical leak, a fire, or groundwater contamination—could result in facility shutdowns and massive remediation costs.

The margin pressure is already visible in recent results. EBITDA margin declined from 41.1% in Q4 FY25 to 34.1% in Q1 FY26. While management attributes this to product mix, it could also signal that the company's pricing power is weakening as customers become more sophisticated in their procurement and competitors improve their capabilities.

Currency risk is often overlooked but significant. With 100% of contrast media intermediates being exported, Blue Jet is essentially a dollar revenue company with rupee costs. While this has been favorable recently, currency movements can quickly erode margins. The company's hedging policies are conservative, but no hedging strategy is perfect.

The succession risk remains despite the successful second-generation transition. What happens when the current generation retires? Family businesses often struggle with third-generation transitions, and the specialized knowledge required to run Blue Jet can't be easily hired from outside.

Quality control becomes exponentially harder as complexity increases. As Blue Jet moves into more complex molecules like peptides, the analytical challenges multiply. Detecting impurities in a simple iodinated compound is straightforward compared to analyzing complex peptide fragments. One quality failure in these new areas could damage credibility in core markets.

The customer qualification timeline for new products is lengthening, not shortening. Despite regulatory harmonization, getting a new intermediate approved by a pharmaceutical customer can take 2-3 years. This means that even successful R&D might not generate revenue for years, creating a cash flow mismatch that could strain finances.

Market saturation in contrast media is a real possibility. While emerging markets are growing, developed markets are seeing slower growth in imaging procedures. If Blue Jet is betting on volume growth that doesn't materialize, they could find themselves with excess capacity in a flat market.

XII. Investment Thesis & Valuation

At a P/E of 37.9 and Book Value of ₹65.3, Blue Jet Healthcare trades at a premium that would make value investors queasy. But this is where the numbers need context. The company isn't just a chemical manufacturer; it's a critical node in the global healthcare infrastructure, and that commands a different valuation framework.

The bull case starts with the quality of earnings. This isn't a company riding a commodity cycle or benefiting from temporary supply disruptions. The earnings are underpinned by multi-year contracts with some of the world's most stable companies. When your customers are GE Healthcare, Guerbet, and Bracco—companies that have been around for decades and aren't going anywhere—revenue predictability is higher than most software companies.

BLUEJET stock has showed a 142.37% increase over the last year, but this appreciation might just be the market catching up to reality rather than getting ahead of it. Compare Blue Jet to global CDMO peers like Lonza or Catalent, and the valuation starts to look reasonable. These companies trade at enterprise values of 15-20x EBITDA; Blue Jet, despite superior growth and margins, trades at a similar multiple.

The growth versus value debate misses the point. Blue Jet is both—a growth company with value characteristics. The growth comes from secular trends in medical imaging, the shift to outsourced manufacturing, and expansion into new therapeutic areas. The value comes from the asset base, the customer relationships, and the cash generation that could support the current market cap even with zero growth.

The reinvestment opportunity is compelling. With returns on capital employed exceeding 40%, every rupee reinvested in the business generates exceptional returns. This is why the aggressive capex plans should be viewed positively—management is doing exactly what they should with capital that earns these returns.

The hidden assets don't show up in book value. The regulatory filings, the customer relationships, the process knowledge—these intangibles are worth multiples of the tangible book value. When a customer has integrated Blue Jet into their supply chain for a product generating hundreds of millions in revenue, the switching cost creates an economic moat worth billions.

The ESG angle is becoming increasingly important for valuation. Global funds with ESG mandates struggle to find chemical companies they can invest in. Blue Jet's environmental compliance, safety record, and governance improvements post-IPO make it one of the few chemical companies that passes ESG screens. This expanded investor base should support premium valuations.

The operating leverage is just beginning to show. As the company scales, fixed costs are spread over larger volumes, driving margin expansion. The automation investments will further improve this leverage. A company generating 35% EBITDA margins today could reasonably achieve 40%+ margins at scale.

The acquisition potential adds another dimension to valuation. While Blue Jet has grown organically, they're now generating enough cash to consider strategic acquisitions. In a fragmented industry with many subscale players, Blue Jet could consolidate the market, acquiring capabilities or customer relationships at reasonable multiples and integrating them at higher margins.

The dividend potential is underappreciated. As the business matures and capex requirements moderate, Blue Jet could become a significant dividend payer. A company generating 30% ROE with modest growth requirements could sustainably pay out 40-50% of earnings, implying a dividend yield of 2-3% at current valuations.

Risk-adjusted returns favor Blue Jet. While the stock appears expensive on absolute metrics, adjusting for the quality of the business, the growth trajectory, and the lower risk profile compared to typical chemical companies, the risk-adjusted returns look attractive.

The comparative valuation to Indian pharma companies is instructive. Companies like Divi's Laboratories and Laurus Labs trade at similar or higher multiples despite arguably inferior business models. Blue Jet's customer concentration, while a risk, also means more predictable revenues than companies serving hundreds of smaller customers.

The sum-of-the-parts valuation reveals hidden value. The contrast media business alone, at global CDMO multiples, could justify the current market cap. The sweetener business, while mature, could be worth ₹2,000-3,000 crores to a strategic buyer. The emerging peptide and pharma intermediate business provides free optionality.

The market inefficiency is real. Blue Jet is too small for large-cap funds, too specialized for generalist investors, and too complex for retail investors. This creates an opportunity for investors who do the work to understand the business.

The long-term value creation potential is enormous. If Blue Jet executes on its plans—and their track record suggests they will—this could be a ₹50,000 crore company by 2030. That's not aggressive financial engineering or multiple expansion; it's simply growing with their end markets and maintaining current margins.

XIII. Playbook: Lessons for Founders & Investors

The Blue Jet story offers a masterclass in building defensible moats in seemingly commoditized industries. The first lesson is counterintuitive: in B2B relationships, trust compounds faster than technology. While everyone obsesses over innovation, Blue Jet built a fortress on something simpler—never missing a delivery, never compromising on quality, never surprising a customer. Over decades, this reliability becomes invaluable.

The power of focus cannot be overstated. Blue Jet could have diversified into dozens of chemical products, chasing every opportunity. Instead, they went deep on contrast media intermediates, becoming so essential that customers plan their supply chains around Blue Jet's capabilities. Specialists eat generalists in B2B markets, especially when switching costs are high.

Family business succession, done right, is a competitive advantage, not a liability. The Arora family's transition wasn't just about handing over control; it was about combining the founder's relationships and intuition with the second generation's analytical capabilities and global perspective. The key was the transition period—not too short to lose institutional knowledge, not too long to stifle new thinking.

Timing market cycles requires patience that public markets rarely reward. Blue Jet went public not when markets were hottest but when the business was ready—profitable, growing, with clear visibility on future expansion. They left money on the table in the IPO pricing, but this conservative approach built trust with new investors.

Building defensible moats in commodity industries requires thinking beyond the product. Blue Jet's moat isn't just chemical expertise; it's regulatory knowledge, environmental compliance, customer integration, and process optimization. Each layer makes replication harder. Competitors might match one dimension but struggling to match all creates the defensibility.

Environmental compliance as strategy, not cost, represents evolved thinking. While competitors viewed environmental regulations as burdens, Blue Jet saw opportunity. By exceeding standards, they turned compliance into a selling point, attracting customers who face their own ESG pressures. In chemicals, being green isn't just good PR—it's good business.

The importance of patient capital in industrial businesses cannot be overemphasized. Blue Jet's major investments—new facilities, R&D capabilities, customer relationships—took years to pay off. Public market quarterly pressures could have derailed this long-term value creation. The family's continued 86% ownership post-IPO provides this patience.

Vertical integration decisions should be strategic, not automatic. Blue Jet integrated backward into key raw materials but remained dependent on suppliers for others. The distinction? They integrated where it provided supply security or cost advantage, not just to control more of the chain. Strategic integration creates value; reflexive integration destroys it.

Customer concentration can be a strength if managed properly. While textbooks warn against customer concentration, Blue Jet shows that deep relationships with a few sophisticated customers can be more valuable than shallow relationships with many. The key is making yourself indispensable, not just preferred.

Technical expertise must be paired with commercial sophistication. Blue Jet's chemists are world-class, but what sets the company apart is their ability to understand customer economics, regulatory requirements, and market dynamics. Technical excellence is table stakes; commercial awareness creates value.

The R&D investment philosophy matters more than the amount. Blue Jet doesn't try to discover new molecules; they optimize existing ones. This focused R&D generates returns because it's aimed at specific customer problems rather than blue-sky research. In B2B, applied research beats basic research.

Cultural continuity through growth is possible but requires intention. As Blue Jet scaled from family business to public company, they maintained their core values—quality obsession, customer focus, long-term thinking—while adding professional systems and processes. Culture isn't preserved by accident; it requires constant reinforcement.

The value of boring businesses is systematically underappreciated. Contrast media intermediates aren't sexy. They don't have apps, platforms, or network effects. But they're essential, defensible, and generate extraordinary returns. Investors chasing the next big thing often miss the current sure thing.

Geographic focus can be a strength in global markets. Blue Jet didn't try to manufacture everywhere; they concentrated facilities in Maharashtra, achieving economies of scale and operational excellence that distributed manufacturing couldn't match. In manufacturing, geographic focus often beats geographic spread.

The importance of founder mindset in second-generation leaders cannot be manufactured. The Arora second generation didn't just inherit the business; they inherited the mindset—treating company money like their own, thinking in decades not quarters, and understanding that reputation takes years to build and moments to destroy.

XIV. Epilogue: The Next Chapter

As we sit in 2025, Blue Jet Healthcare stands at an inflection point. The company that began as India's answer to saccharin imports has evolved into a global player in one of healthcare's most critical supply chains. But the next chapter might be the most interesting yet.

Over the next three to five years, the company plans to invest in cutting-edge technologies, expand R&D and manufacturing capacities. This isn't just corporate speak—it represents a fundamental bet that the outsourcing of complex pharmaceutical manufacturing will accelerate, that environmental standards will continue to tighten, and that being a trusted partner matters more than being the cheapest supplier.

The vision for becoming a global CDMO leader requires more than just capacity expansion. It requires building capabilities in new therapeutic areas, developing relationships with biotech companies not just big pharma, and potentially expanding beyond intermediates into finished dosage forms. Each of these represents both opportunity and risk.

The key milestones to watch are clear: successful commissioning of the new facility by FY28-29, entry into peptide manufacturing at commercial scale, maintaining margins as the business scales, and potentially value-accretive acquisitions. Each milestone de-risks the growth story and justifies premium valuations.

But the bigger picture is about India's pharmaceutical story. Blue Jet represents a new generation of Indian companies—globally competitive, environmentally responsible, and professionally managed while maintaining entrepreneurial spirit. Their success or failure will influence how global pharmaceutical companies view Indian suppliers.

The contrast media industry itself is evolving. New imaging techniques, personalized medicine, and AI-enhanced diagnostics will change how contrast agents are used. Blue Jet's ability to evolve with these changes, to remain relevant as the industry transforms, will determine whether this is a 10-year story or a 50-year story.

The ultimate test will be whether Blue Jet can maintain its culture and values as it scales. Can they remain customer-obsessed when they have hundreds of customers instead of dozens? Can they maintain quality standards when producing thousands of tons instead of hundreds? Can they keep the entrepreneurial spirit alive in a company that might employ thousands?

The financial markets will judge Blue Jet quarterly, but the real judgment will come from customers who decide whether to trust them with critical supply chains, from employees who choose to build careers there, and from communities that live near their facilities. These stakeholders will determine whether Blue Jet's next chapter is even more impressive than its last.

As investors, founders, and students of business, we watch Blue Jet not just for financial returns but for lessons in building enduring value. In a world obsessed with disruption and innovation, Blue Jet reminds us that excellence in execution, deep customer relationships, and patient value creation still matter. Sometimes, the best businesses aren't the ones that change the world overnight but the ones that make the world work better, one molecule at a time.

The story of Blue Jet Healthcare is far from over. In fact, it might just be beginning. The company that started with a dream of making India self-sufficient in sweeteners now helps make global healthcare possible. That transformation—from local manufacturer to global partner—offers hope that Indian businesses can compete not just on cost but on capability, not just as vendors but as partners, not just for today but for decades to come.

Recent News at Blue Jet Healthcare

The recent developments paint a picture of a company accelerating its transformation from successful mid-sized player to potential global champion. The most significant announcement came on July 31, 2025, when the Board approved acquisition of a land parcel measuring approximately 102.48 acres located at Industrial Park Rambilli Cluster Phase II, Anakapalli District, Andhra Pradesh.

This Andhra Pradesh expansion represents more than just capacity addition—it's a strategic pivot. The ₹1,000+ Crore Greenfield Expansion in Andhra Pradesh reinforces the company's long-term growth vision. The location choice is telling: Andhra Pradesh offers significant incentives for pharmaceutical manufacturing, proximity to ports for export, and a skilled workforce familiar with chemical operations.

The Q1 FY26 results continue to demonstrate robust growth despite market volatility. Q1 FY26 revenue Rs.3,548 mn up 117.8% YoY with EBITDA margin 34.1% and PAT Rs.912 mn, up 141.3% YoY. While the sequential decline concerned some investors, the year-over-year growth trajectory remains exceptional.

In an interesting sidelight on the wealth creation from Blue Jet's success, the promoter family of Blue Jet Healthcare has acquired three luxury apartments in Worli, Mumbai, collectively worth more than INR 202 crore. While some might view this as capital leaving the business, it actually demonstrates confidence—the family maintains 86% ownership while diversifying personal wealth, a healthy balance that aligns with good governance.

The ongoing capacity expansions signal confidence in future demand. Ongoing capacity expansions and Rs.300cr capex planned for existing facilities, combined with the new Andhra Pradesh site, position Blue Jet to potentially triple capacity over the next five years.

The company's communication with investors has also matured, with regular earnings calls and detailed disclosures becoming standard practice. This transparency, relatively rare among Indian mid-cap companies, helps build institutional investor confidence and should support valuation multiples over time.

XVI. Links & Resources

Company Resources: - Blue Jet Healthcare Official Website: bluejethealthcare.com - Annual Reports & Investor Presentations: bluejethealthcare.com/investors - BSE Listing Page: BSE Code 543930 - NSE Listing Page: NSE Symbol BLUEJET

Industry Reports: - Global Contrast Media Market Analysis (MarketsandMarkets) - Indian CDMO Sector Report (ICRA Research) - Pharmaceutical Intermediates Market Outlook (Frost & Sullivan)

Regulatory Resources: - USFDA Drug Master Files Database - European Medicines Agency Guidelines - Indian CDSCO Regulations - Maharashtra Pollution Control Board Standards

Books on Indian Pharma Industry: - "The Indian Pharmaceutical Industry: Growth and Opportunities" by Sudip Chaudhuri - "From Generic to Innovative: The Indian Pharmaceutical Journey" - "Contract Manufacturing in Pharmaceuticals" by Michael Levin

Academic Resources: - "Chemistry of Iodinated Contrast Media" - Journal of Pharmaceutical Sciences - "Environmental Compliance in Chemical Manufacturing" - Chemical Engineering Journal - "Family Business Succession in Emerging Markets" - Harvard Business Review

Trade Publications: - Chemical Weekly (India's premier chemical industry magazine) - Pharma Bio World - Contract Pharma Magazine - Express Pharma

Financial Analysis: - Screener.in Company Page - Trendlyne Financial Analysis - TipRanks Analyst Consensus - ValueResearch Stock Analysis

Podcasts & Interviews: - Management interviews on earnings calls (available on company website) - Industry expert discussions on CDMO trends - Chemical manufacturing podcasts discussing environmental compliance