Adani Power: From Trading House to India's Power Giant

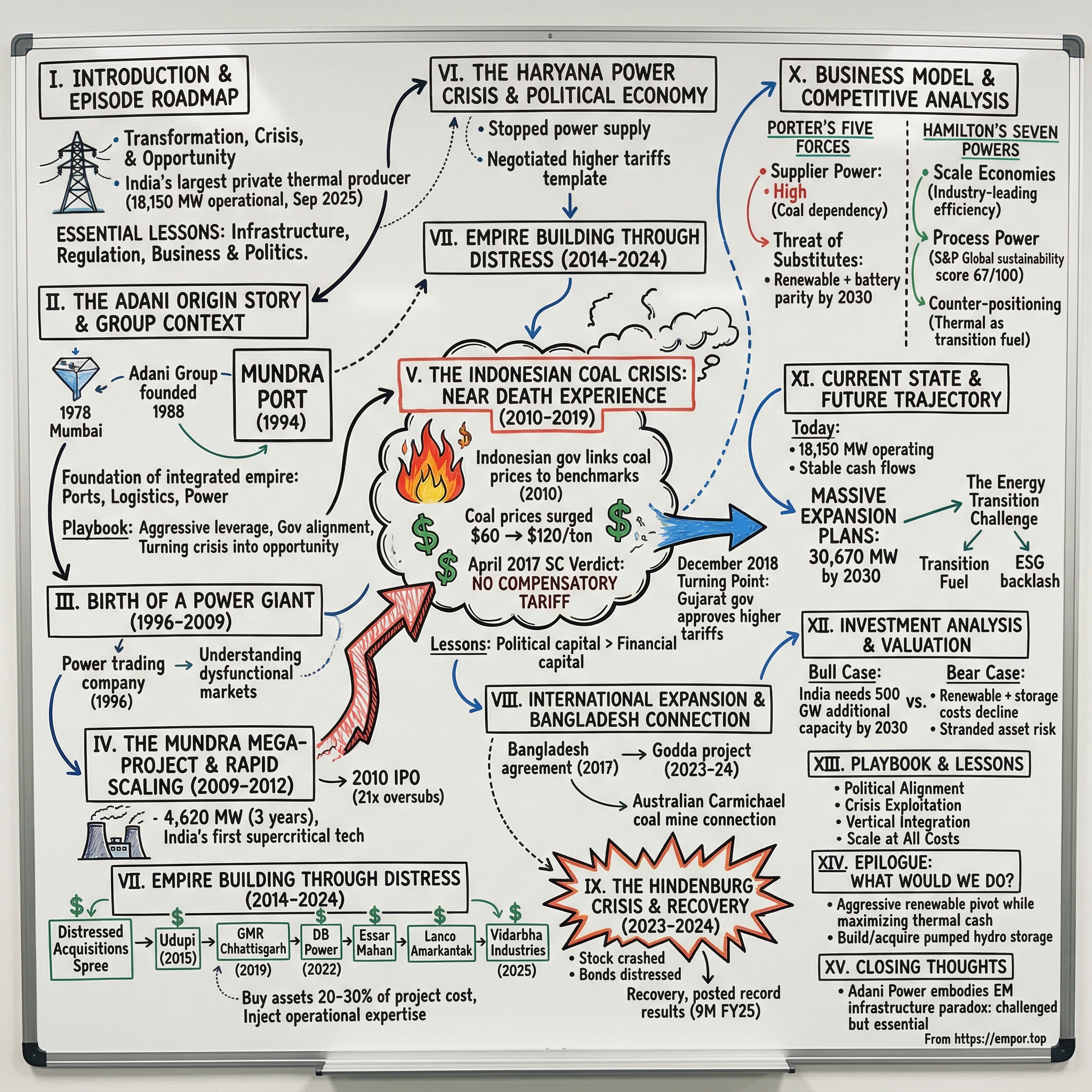

I. Introduction & Episode Roadmap

India's power sector tells a story of transformation, crisis, and opportunity. At the heart of this narrative stands Adani Power, which has emerged from near-bankruptcy in 2018 to become India's largest private thermal power producer with 18,150 MW operational capacity as of September 2025. The company's journey from a commodity trading business to a power behemoth reveals essential lessons about building infrastructure in emerging markets, navigating regulatory minefields, and the intersection of business and politics in developing economies.

This deep dive explores how Adani Power survived existential crises that destroyed competitors, executed distressed acquisitions at fraction of replacement costs, and positioned itself at the center of India's energy future despite mounting ESG concerns. The story provides a masterclass in political economy, infrastructure nationalism, and surviving commodity cycles in one of the world's most complex business environments.

II. The Adani Origin Story & Group Context

The Adani story begins not in boardrooms but in Mumbai's diamond markets. In 1978, Gautam Adani arrived in Mumbai as a diamond sorter, learning the fundamentals of commodity trading that would define his business philosophy. By 1988, with just ₹5 lakh in initial capital, he founded what would become the Adani Group as a commodity trading business, focusing on agricultural and polymer imports.

The watershed moment came in 1994 when the Gujarat government invited Adani to develop Mundra Port. This wasn't just an infrastructure project - it was the foundation of a vertically integrated empire. Adani seized the opportunity, understanding that controlling ports meant controlling the gateway to India's economy. From ports came logistics, from logistics came the need for power, and from power came the transformation into infrastructure.

The Gujarat business ecosystem provided fertile ground. The state's pro-business policies and Adani's alignment with political priorities created a symbiotic relationship that would define the group's trajectory. The playbook was established early: aggressive leverage, government alignment, infrastructure focus, and turning every crisis into an opportunity for expansion.

III. Birth of a Power Giant (1996-2009)

Adani Power's genesis in 1996 as a power trading company was strategic. Before generating a single megawatt, the company spent years understanding India's dysfunctional power markets. State electricity boards were bleeding money, chronic shortages plagued industrial growth, and the gap between demand and supply widened each year.

The Mundra project conception revealed Adani's contrarian thinking. While others focused on domestic coal, Adani bet on imported coal from Indonesia. The logic was compelling: Indonesian coal was cheaper, cleaner, and more reliable than domestic supplies. The proximity to Mundra port created a natural advantage - ships could dock directly at Adani's own port, eliminating intermediaries.

Building relationships with state governments became an art form. Adani didn't just sell power; the company sold reliability to states desperate for solutions. By July 2009, when the first 330 MW unit was commissioned at Mundra, Adani had already secured power purchase agreements that would define its future.

IV. The Mundra Mega-Project & Rapid Scaling (2009-2012)

The Mundra power project represented audacious ambition. Between 2009 and 2012, Adani commissioned 4,620 MW in just three years, creating India's largest single-location coal-based power project. This wasn't just about scale - it was about technology leadership. Mundra deployed India's first supercritical technology, operating at higher temperatures and pressures for better efficiency.

Financing this $2 billion-plus project required financial engineering at scale. Adani leveraged everything - the group's balance sheet, project finance from banks, and most crucially, long-term PPAs that guaranteed revenue streams. The 2010 IPO was a defining moment, oversubscribed 21 times, validating market confidence in the aggressive expansion.

The competitive bidding era brought both opportunity and peril. Adani bid aggressively low tariffs of ₹2.35 per unit to win contracts, betting that volumes and efficiency would compensate for thin margins. This strategy would soon face its greatest test.

V. The Indonesian Coal Crisis: Near Death Experience (2010-2019)

The Crisis Unfolds

The Indonesian government's decision in 2010 to link coal export prices to international benchmarks triggered Adani Power's existential crisis. Coal prices surged from $60 to over $120 per ton, destroying the economics of projects built on assumptions of stable fuel costs.

The revelation that Adani Enterprises held 74% of the Indonesian coal mining company Bunyu added complexity. While Adani Power bled money buying expensive coal, the group's trading arm profited from high prices - a conflict of interest that regulators and courts would scrutinize for years.

The Fight for Survival

April 2017 brought the Supreme Court's devastating verdict: no compensatory tariff for Adani despite changed circumstances. The judgment pushed Adani Power to the brink. Internal assessments showed the company would be bankrupt within two years without intervention.

December 2018 marked the turning point. The Gujarat government, facing its own power crisis, approved higher tariffs for Adani despite the Supreme Court ruling. This wasn't just regulatory relief - it was political intervention to save a strategic asset. By April 2019, after seven years of legal battles, the Central Electricity Regulatory Commission finally approved revised PPAs.

Lessons from the Crisis

The Indonesian coal crisis revealed fundamental truths about infrastructure investing in India. Political capital proved more valuable than financial capital. While competitors like Tata Power's Coastal Gujarat project struggled with similar issues, Adani emerged stronger through a combination of political alignment, financial resilience, and strategic patience.

VI. The Haryana Power Crisis & Political Economy

The Haryana episode in 2017-2018 demonstrated Adani's willingness to play hardball. When the state disputed tariffs, Adani stopped power supply during peak summer, creating a political crisis. The allegation that Adani diverted Haryana's contracted power to Gujarat during heat waves highlighted the leverage private generators wielded over states.

The resolution came through negotiated higher tariffs - effectively, Haryana capitulated. This template would be replicated across states: create dependency, exploit crisis moments, and extract favorable terms. It was ruthless but effective, establishing Adani as a player states couldn't ignore.

VII. Empire Building Through Distress (2014-2024)

The Acquisition Spree

Adani's transformation into India's largest private power producer came through distressed acquisitions. The 2015 Udupi Power acquisition for ₹6,000 crores established the template: buy assets at 20-30% of project cost, inject operational expertise, and generate outsized returns.

The acquisition momentum accelerated: GMR Chhattisgarh for ₹3,530 crores in 2019, DB Power for ₹7,017 crores in 2022, and Essar's Mahan project for ₹4,250 crores through the insolvency process. Each deal followed the same playbook - acquire through NCLT/IBC proceedings for clean titles, implement operational improvements, and leverage existing infrastructure.

The 2024 completion of the Lanco Amarkantak acquisition and July 2025 completion of Vidarbha Industries Power Limited acquisition for 600 MW added to this empire built on others' failures. By acquiring distressed assets, Adani assembled 15,250 MW of capacity while competitors struggled with stranded investments.

The Strategy

The brilliance lay in timing and execution. The Insolvency and Bankruptcy Code created a mechanism for clean acquisitions. Banks, desperate to recover loans, accepted massive haircuts. Adani provided the operational expertise to revive dead assets, generating returns that new projects could never achieve.

VIII. International Expansion & Bangladesh Connection

The 2017 Bangladesh agreement for 1,600 MW from the Godda project represented Adani's international ambitions. This wasn't just about power exports - it was about India's neighborhood diplomacy. The project, commissioned in 2023-24, created a 25-year revenue stream while establishing Adani as a regional player.

The Australian Carmichael coal mine connection completed the vertical integration. Despite global environmental opposition, Adani persisted, creating a coal-to-power supply chain spanning continents. The controversy only strengthened political support domestically, positioning Adani as a champion of India's energy security.

IX. The Hindenburg Crisis & Recovery (2023-2024)

January 2023's Hindenburg report alleged market manipulation, overleveraging, and corporate governance failures. The stock crashed, bonds traded at distressed levels, and questions about the group's viability dominated headlines. Yet by late 2024, Adani Power had recovered, posting record results.

The company reported a 33% YoY rise in PBT to ₹10,679 crore and a 22% increase in EBITDA to ₹16,478 crore for 9M FY25. The operational performance - higher volumes, improved efficiency, and successful commissioning of new capacity - trumped financial engineering concerns. Markets ultimately valued cash flows over controversy.

X. Business Model & Competitive Analysis

Porter's Five Forces Analysis

Supplier Power: High dependency on coal creates vulnerability. Indonesian coal price volatility nearly destroyed the company once. Domestic coal allocation remains politically controlled.

Buyer Power: Moderate but changing. State DISCOMs are locked into long-term PPAs, but their financial weakness creates payment risks. Industrial customers provide better margins but demand flexibility.

Competitive Rivalry: Intensifying as NTPC modernizes, Tata Power expands, and JSW Energy enters new markets. The era of easy growth has ended.

Threat of Substitutes: Renewable energy plus battery storage approaches grid parity. Solar-wind hybrid projects with storage threaten baseload economics by 2030.

Barriers to Entry: Extremely high. Land acquisition, environmental clearances, and capital requirements of ₹6-7 crores per MW deter new entrants.

Hamilton's Seven Powers Framework

Scale Economies: With net debt per MW of Rs. 1.77 Crore as of 31st March 2025, Adani operates at industry-leading capital efficiency. The 18,150 MW operational capacity provides unmatched economies of scale.

Network Effects: Limited but emerging in fuel procurement and power trading. The company's size enables better coal sourcing terms and trading opportunities.

Switching Costs: 25-year PPAs create lock-in, but state governments can default or renegotiate during distress, as history shows.

Branding: Weak in a commodity business. The Adani name carries political baggage internationally, limiting ESG-focused funding access.

Cornered Resource: Strategic coastal locations for imported coal plants and established coal linkages provide advantages competitors cannot replicate.

Process Power: APL scored 67/100 in Corporate Sustainability Assessment by S&P Global in November 2024, placing it in the 86th percentile, better than World Electric Utilities' average score of 42/100.

Counter-positioning: Positioning thermal as essential "transition fuel" while others exit creates opportunity for consolidation.

XI. Current State & Future Trajectory

Today's Position

Adani Power's consolidated operating capacity increased to 18,150 MW as of September 30, 2025, with 40 MW of solar capacity. The company operates with 9,153 MW under long-term PPAs across six states, providing stable cash flows. All-India power demand grew by 3.5% to 415 BU in Q4 FY25, with full year FY25 demand growing 4.2% to 1,695 BU, though March 2025 registered stronger growth of 6.6%.

Massive Expansion Plans

APL has undertaken expansion of its existing capacities from 17,550 MW to 30,670 MW by 2030. The company secured major wins recently, including Bihar's 2,400 MW Bhagalpur project with the lowest bid of Rs 6.075 per kWh, representing around ₹30,000 crore investment.

Execution of three ultra-supercritical power plants of 1,600 MW each is in full swing at Mahan, Raipur, and Rajgarh. The Kawai plant expansion will add 3,200 MW in two phases, increasing capacity from 1,320 MW to 4,520 MW.

Recent developments include securing 4.5 GW of new long-term PPAs under the SHAKTI scheme, including 2,400 MW from Bihar, 1,600 MW from Madhya Pradesh, and 570 MW from Karnataka. The company has also made strategic land acquisitions, including a December 2024 environmental approval application for a 2,400 MW project in Odisha.

The Energy Transition Challenge

India's power demand growth creates opportunity despite global energy transition trends. With the Government estimating peak power demand reaching 270 GW in summer 2025 from 250 GW in 2024, thermal power remains essential for grid stability.

Adani frames thermal as "transition fuel" necessary until renewable plus storage achieves true grid-scale reliability. The company invests in efficiency improvements, with ultra-supercritical technology reducing emissions per unit of power generated. Carbon capture investments and "clean coal" narratives attempt to address ESG concerns, though international investors remain skeptical.

Strategic options include pivoting to renewable-thermal hybrid models, developing pumped hydro storage for grid services, focusing on industrial captive power with better payment profiles, and expanding into Southeast Asian markets before developed markets close doors.

XII. Investment Analysis & Valuation

Bull Case

India requires 500 GW additional capacity by 2030 to support economic growth. Thermal power provides essential grid stability until at least 2040, especially during renewable intermittency. Net Total Debt increased to Rs. 31,023 Crore as of 31st March 2025, though this includes acquisition debt for KPL and higher working capital borrowings in line with increased scale.

Replacement cost of existing assets exceeds ₹100,000 crores, while market capitalization provides discount to book value. Operating leverage increases with capacity utilization improvement from current 60% to targeted 75%.

Bear Case

Renewable plus storage costs decline 10-15% annually, reaching grid parity by 2027-2028. Stranded asset risk escalates post-2030 as countries implement carbon pricing. Regulatory overhang persists with state governments' weak finances threatening PPA sanctity.

ESG-focused funds permanently exclude coal-exposed companies, limiting capital access. Debt refinancing needs of ₹31,000 crores create vulnerability to interest rate cycles.

Key Metrics to Track

Plant Load Factor trends indicate demand-supply dynamics. Merchant versus PPA mix reveals pricing power. Coal cost pass-through effectiveness determines margin stability. Regulated returns versus market returns highlight regulatory risk.

XIII. Playbook & Lessons

The Adani Power Playbook

Political Alignment: Success requires working with, not against, government priorities. Every major milestone coincided with political support.

Crisis Exploitation: Distressed markets provide best opportunities. Adani built its empire buying assets at 20-30% of replacement cost.

Vertical Integration: Controlling coal sourcing through captive mines and imports reduces supply risk.

Regulatory Arbitrage: Mastering complex regulations creates competitive advantage. Understanding loopholes matters more than operational excellence.

Patient Capital: Infrastructure returns require decade-long horizons. Surviving short-term pain enables long-term value creation.

Scale at All Costs: Size provides resilience and negotiating leverage with governments, banks, and suppliers.

Key Business Lessons

Infrastructure investing in emerging markets requires political capital equal to financial capital. The real customer in regulated businesses is the regulator, not the end consumer. Commodity cycles create 50% price swings - only the prepared survive.

Distressed M&A in infrastructure can generate 5-10x returns if assets are operated well. ESG backlash is real but may be premature in emerging markets where development trumps environmental concerns.

XIV. Epilogue: What Would We Do?

If We Were Running Adani Power

Execute aggressive renewable pivot while maximizing thermal cash generation over next 5-7 years. Focus on industrial customers and bilateral PPAs avoiding state DISCOM payment risks. Build or acquire pumped hydro storage assets for grid stability services commanding premium pricing.

Accelerate Southeast Asia expansion before carbon regulations close markets. Prepare for carbon pricing through technology investments and financial hedges. Develop transition finance narrative for ESG investors focusing on grid stability role.

The Bigger Picture

India faces an energy trilemma: Affordable, Reliable, Clean - currently, only two are achievable simultaneously. This may be the last thermal power cycle before renewable dominance, making timing critical.

The Adani question transcends business - it's about development models. Is this crony capitalism or nation building? The answer depends on whether India achieves energy security and economic development.

XV. Closing Thoughts

Adani Power embodies the paradox of emerging market infrastructure - environmentally challenged but economically essential. The company's journey from trader to titan reveals how business works in the "real" economy where politics, regulation, and operations intersect.

The story teaches that infrastructure development in emerging markets follows different rules than Silicon Valley startups or developed market utilities. Success requires navigating political economy, surviving commodity cycles, and maintaining operational excellence while managing massive capital requirements.

Whether Adani Power transforms into a sustainable energy company or becomes this generation's stranded coal asset will define not just the company's future but India's energy transition. The next decade will determine if thermal power was a necessary bridge to clean energy or an expensive detour that delayed inevitable change.

Power remains the foundation of economic development. Adani Power's story, controversial as it may be, provides essential lessons about building critical infrastructure in complex emerging markets where perfect solutions don't exist - only pragmatic ones that balance competing priorities while serving immediate needs.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube