Saudi Aramco: The World's Most Valuable Company

I. Introduction & Episode Roadmap

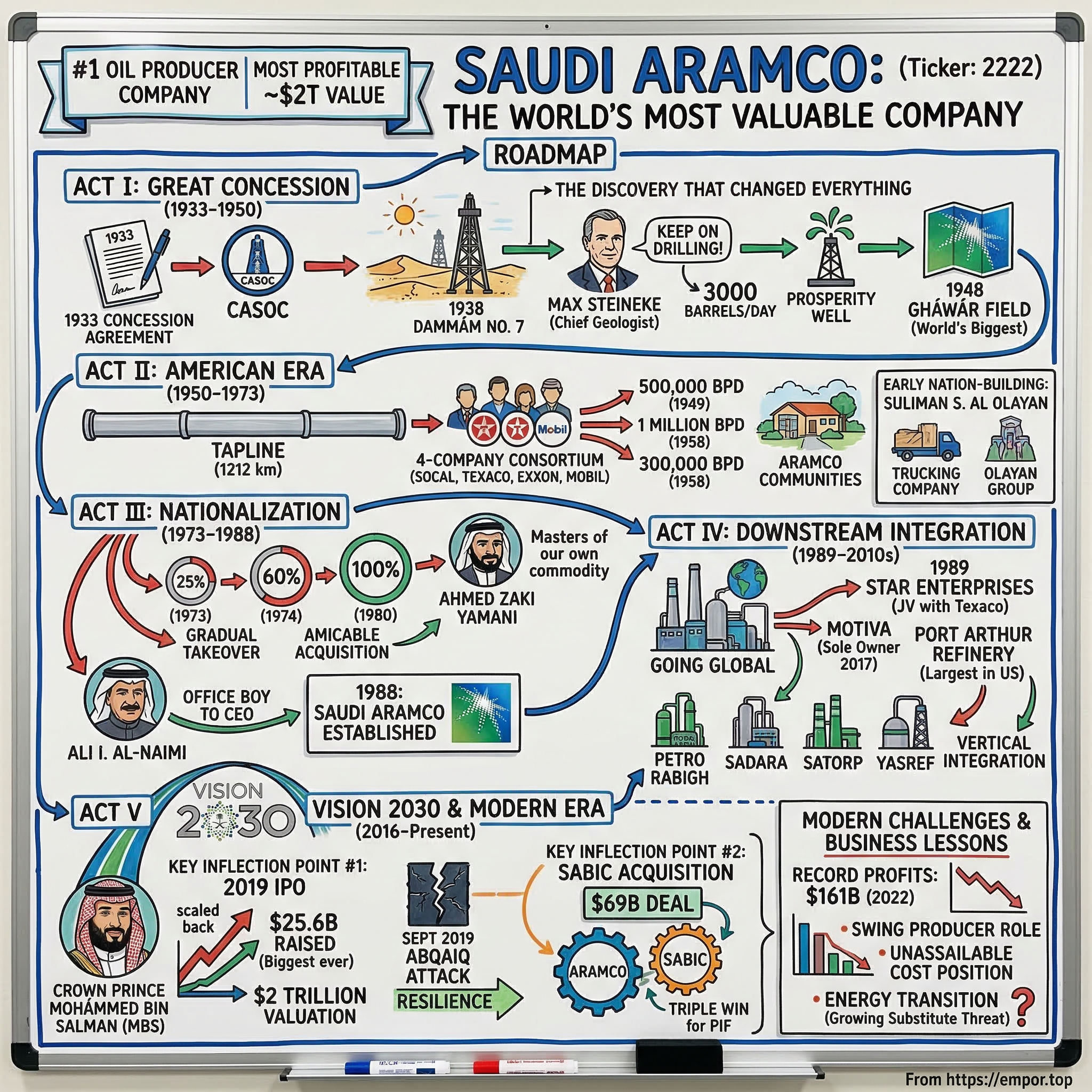

Picture this: an endless expanse of golden sand stretching toward the horizon, punctuated only by the occasional rocky outcrop. The year is 1938, and a team of exhausted American geologists is about to make a discovery that would reshape not just the Middle East, but the entire global order. At Dammam No. 7, after years of disappointment and near-abandonment, crude oil begins flowing from the Arabian desert in commercial quantities—a moment that would transform a largely agrarian kingdom into one of the world's most influential nations.

How did a concession signed in the Saudi desert in 1933 create a company worth nearly $2 trillion? That's the central question of this story, and it's one that encompasses American ambition, Saudi sovereignty, technological marvels, geopolitical intrigue, and the fundamental question of whether the world's quintessential oil company can survive—and thrive—in an era of energy transition.

Saudi Arabian Oil Company, or Saudi Aramco, is a state-owned energy giant based in Dhahran, Saudi Arabia. It is the world's largest oil producer and, as of 2024, the most profitable company in any industry and among the most valuable. The numbers are staggering: Aramco's low production costs and vast reserves have helped it consistently rank among the world's most profitable companies. It holds more than 250 billion barrels of proven reserves, the largest total of any company in the world. From 2016 to 2024, it generated about $800 billion in net income, outperforming every other corporation globally over that period.

Aramco is evolving far beyond its traditional role, now positioning itself at the forefront of economic diversification, technological innovation, and sustainability, aligning with the broader vision set forth by Crown Prince Mohammed bin Salman to transform the Saudi economy and reduce its dependence on oil. This shift has turned Aramco into a key player in reshaping the kingdom's energy landscape and broader strategic interests.

The story unfolds in five distinct acts: the American origins and discovery of Arabian oil, the gradual nationalization that transformed Aramco from an American company to a Saudi one, the downstream integration that made it a global energy giant, the dramatic IPO that crystallized Vision 2030's ambitions, and the modern era of record profits confronting existential challenges. Along the way, we'll meet the visionary geologists who defied conventional wisdom, the Saudi leaders who negotiated the largest amicable corporate acquisition in American history, and the strategists now betting billions on a post-oil future.

For investors, the Aramco story raises profound questions about resource advantages, state ownership, and the durability of competitive moats in a world grappling with climate change. Can a company whose fortunes are inextricably linked to fossil fuels maintain its position as one of the world's most valuable enterprises? The answer will shape not just Saudi Arabia's future, but the global energy landscape for decades to come.

II. The Great Concession: Origins & Discovery (1933–1950)

The Deal That Built a Nation

In the early 1930s, Saudi Arabia was a young kingdom struggling to survive. Founded by Ibn Saud in 1932 through the unification of disparate tribal territories, the nation lacked almost every modern convenience. There were no paved roads, no electricity grids, and no obvious path to prosperity. The royal coffers depended largely on revenues from the Hajj pilgrimage and modest customs duties. But across the Persian Gulf, in neighboring Bahrain, something remarkable had happened: on 31 May 1932, the SOCAL subsidiary, the Bahrain Petroleum Company (BAPCO) struck oil in Bahrain.

That discovery transformed American thinking about the Arabian Peninsula. The discovery brought fresh impetus to the search for oil on the Arabian peninsula. Standard Oil Company of California (SoCal, now Chevron) had been shut out of the Middle East by the British-dominated Iraq Petroleum Company, and the Bahrain success suggested that similar riches might lie beneath Saudi soil.

Negotiations for an oil concession for al-Hasa province opened at Jeddah in March, 1933. Twitchell attended with lawyer Lloyd Hamilton on behalf of SOCAL. The Iraq Petroleum Company represented by Stephen Longrigg competed in the bidding, but SOCAL was granted the concession on 23 May 1933. The terms were remarkably generous to the Americans: "exploration rights to some 930,000 square kilometers of land for 60 years."

Aramco traces its beginnings to 1933 when a Concession Agreement was signed between Saudi Arabia and the Standard Oil Company of California (SOCAL). A subsidiary company, the California Arabian Standard Oil Company (CASOC), was created to manage the agreement.

Years of Searching

What followed were years of frustration that would test even the most determined explorer. After surveying the Saudi desert for oil, drilling began in 1935. The geologists faced conditions unlike anything they had encountered in California or Texas: scorching temperatures exceeding 120°F, sandstorms that buried equipment, and a landscape that offered few surface indicators of what lay beneath.

It brought in Texaco as a partner in 1936, but the team didn't find commercially viable oil until 1938. By late 1937, after multiple dry wells at the Dammam dome, SoCal's management was losing patience. The Arabian venture was hemorrhaging money with nothing to show for it.

Enter Max Steineke, a man whose stubbornness would change history. Max Steineke was a prominent American petroleum geologist. He was chief geologist at California-Arabian Standard Oil Co. (CASOC) from 1936 until 1950. Born in 1898 to German immigrant parents in Brookings, Oregon, Steineke spent his early years on a homestead near Brookings, Oregon, one of nine children of German immigrants. At the age of twelve, he left home for nearby Crescent City, California, where he found employment at a lumber mill.

Steineke was a character from central casting—burly, profane, and absolutely relentless. Steineke had arrived for the first time in Saudi Arabia in 1934, and was appointed chief geologist of CASOC in 1936. In 1937 he made a round trip of geological reconnaissance across the Saudi Arabian Peninsula with a small party of other geologists.

Meanwhile, a series of test wells had been drilled at Dammam. Through 1936 none of the wells had demonstrated the presence of oil in commercial quantities. In December 1936, a "deep test", No. 7, was begun at the urging of Steineke, who wished to test the deeper porous limestone "Arab Zone" underlying impervious anhydrite.

All through 1937, No. 7 experienced a series of expensive accidents and delays, and SoCal management became increasingly impatient. The Arabian venture was costing a lot of money, and so far there wasn't much encouragement. In early 1938, Steineke was called back to San Francisco. SoCal had reportedly decided to "pull the plug" on Saudi Arabian exploration.

The Discovery That Changed Everything

Following years of effort with little to show for it, in 1937 SOCAL executives sought advice from their chief geologist, Max Steineke. Drawing on years of fieldwork, Steineke told them to keep on drilling. Steineke, now the chief geologist of the venture, convinced his managers to at least wait for the results from Dammam #7, which was still drilling at a slow pace.

Then, in March 1938, everything changed. During the first week of March 1938, at a depth of 1440 meters, Dammam No. 7 started producing at commercial quantities, reaching more than 3000 barrels per day by the end of the month.

The perseverance of the company's chief geologist paid off that year when CASOC struck oil at its Dammam No. 7 site (named after a nearby village) after a series of drilling setbacks. The success at No. 7 quickly led to further positive results, and by 1940, the Dammam field was producing more than 12,000 barrels per day. King Abdulaziz later named the well the "Prosperity Well"—an apt description given what would follow.

His efforts, and persistence through repeated setbacks, led to the first discovery of oil in commercial quantities in Saudi Arabia, which took place at the well known as "Dammam No. 7" in March 1938. The American Association of Petroleum Geologists would later honor Steineke with its highest recognition, noting: "The methods he [Steineke] developed in the area probably resulted in the discovery of greater reserves than any other geologist."

But Dammam No. 7 was merely the prologue. Steineke's innovations in structural drilling led to a series of even more spectacular discoveries. Steineke had found clues to oil at a site 30 miles from Dammam, where, in November 1940, the first well flowed at nearly 10,000 barrels per day. What Steineke had discovered was the huge Abqaiq field.

In 1943, the name of the company in control in Saudi Arabia was changed to Arabian American Oil Company (ARAMCO). In 1948, the partnership discovered something that would cement Saudi Arabia's position as the world's energy superpower: The Ghawar oilfield, located about 100km southwest of Dhahran in the Al Hasa Province of Saudi Arabia, is the world's biggest conventional oil field both by oil reserves and production. The giant oil field, discovered in 1948 and brought on-stream in 1951, currently holds more than a quarter of Saudi Arabia's total proven oil reserves and accounts for about half of the country's oil output.

In 1951, the company discovered the Safaniya Oil Field, the world's largest offshore field. In 1957, the discovery of smaller connected oil fields confirmed the Ghawar Field as the world's largest onshore field. The oil field was discovered in 1951. It is considered the largest offshore oil field in the world.

In the span of just 13 years, a team of American geologists had transformed Saudi Arabia from a desert backwater into a nation sitting atop the world's most valuable hydrocarbon reserves—a geological inheritance that would shape global politics for the next century.

III. The American Era: Growth & Scale (1950–1973)

Building an Oil Empire

By the late 1940s, Aramco had evolved from a scrappy exploration outfit into an industrial colossus. Now named Aramco (the Arabian American Oil Company), crude oil production hit 500,000 barrels per day in 1949. The challenge now was getting that oil to market.

In 1950, we completed the 1,212-kilometer Trans-Arabian Pipeline (Tapline) — the longest in the world. The Tapline was an engineering marvel, stretching from eastern Saudi Arabia to the Mediterranean coast of Lebanon, slashing transit times and costs for exporting oil to Europe. It represented the kind of infrastructure investment that only a well-capitalized consortium could undertake.

That consortium was a peculiar entity. Under his leadership, Aramco's ownership structure was secured, with control remaining among the four partner companies – Standard Oil of California, Texaco, Socony-Vacuum Oil (later ExxonMobil), and Standard Oil of New Jersey (later Chevron). This four-company consortium represented an alliance of convenience—American companies united in their desire to tap Arabian oil while hedging the risks inherent in such a distant and unfamiliar venture.

The Unique Four-Company Consortium

By 1958, the scale of operations had grown dramatically. Production exceeded 1 million barrels per day—an achievement that would have seemed fantastical just two decades earlier. By 1962, cumulative crude oil production reached 5 billion barrels. And by 1971, average daily production had ramped up to 4.49 million barrels, cementing Saudi Arabia's position as a global energy superpower.

The operational model was distinctly American in character. Aramco imported not just drilling technology and managerial expertise, but entire systems of corporate governance, employee development, and community relations. The company built schools, hospitals, and housing for its workers—creating self-contained communities that resembled miniature American suburbs transplanted into the Arabian desert.

But this structure also created inherent tensions. The Saudi government collected royalties and taxes but had limited visibility into Aramco's operations. The company's American executives made decisions about production levels, pricing, and investment with minimal Saudi input. It was a colonial-era arrangement dressed in corporate clothing—and everyone understood it couldn't last forever.

Early Nation-Building

One of Aramco's most enduring legacies was inadvertent: the creation of a Saudi entrepreneurial class. The company's massive operations required suppliers, contractors, and service providers—and Aramco actively cultivated relationships with promising Saudi businessmen.

Suliman Saleh Al Olayan (5 November 1918 – 4 July 2006) was among Saudi Arabia's wealthiest businessmen. He is the founder of the Olayan Group. Orphaned at the age of six, Olayan had more humble beginnings than most of his business counterparts from the Kingdom. Olayan's rise to great wealth reflected his connections to the Al-Saud royal family and his fronting for them, his acumen, the ability to cross cultural barriers, as well as extraordinary timing. Initially working for ARAMCO from 1937 to 1947, he left to start his own trucking company, the first of over 50 companies he would create or own.

The Olayan story exemplifies the spillover effects of Aramco's operations. GCC's first customer was Bechtel, which was under contract to Aramco to manage the construction of the Trans-Arabian Pipe Line (Tapline), a mammoth project linking the oil wells in Saudi Arabia's Eastern Province to a terminal in Lebanon on the Mediterranean Sea. GCC handled essential trucking and supply services for the historic project.

He played a key role in developing Saudi Arabia's earliest electrical power companies ultimately founding the country's first public utility, the National Gas Company. In 1954, he launched General Trading Company (GTC), a food and consumer products distribution business. That same year Suliman became instrumental in introducing commercial insurance to Saudi Arabia.

Olayan would eventually build a global business empire spanning banking, real estate, and manufacturing—a trajectory that traced directly back to his decade at Aramco. Similar stories unfolded across the Eastern Province, as Aramco's operations seeded an entire ecosystem of Saudi enterprises that would diversify the kingdom's economy.

The American era established patterns that would endure for decades: operational excellence, technological innovation, and a corporate culture that prized meritocracy. But it also laid the groundwork for the nationalization that would follow, as Saudi leaders increasingly questioned why foreigners should control their nation's most valuable asset.

IV. Nationalization: From American to Saudi (1973–1988)

The Gradual Takeover

The 1970s transformed global energy markets—and with them, the relationship between Aramco and its Saudi hosts. The 1970s was the decade in which, in the words of one of the leading policymakers of the era, Saudi Arabia became "masters of our own commodity" — the owner and operator of its gigantic oil industry, with all that meant for the economic development of the Kingdom and the wellbeing of its citizens. The decade began with the Arabian American Oil Co. — a consortium of four US oil giants, holding an exclusive concession to develop Saudi Arabia's most precious resource; it ended with an agreement to create Saudi Aramco, owned and operated by the Saudi government.

The catalyst was the 1973 Arab-Israeli War and the ensuing oil embargo. Arab producers, led by Saudi Arabia, wielded oil as a weapon against Western supporters of Israel—and in doing so, demonstrated their leverage over the global economy. Oil prices quadrupled, and the balance of power between producers and consumers shifted irrevocably.

Throughout the 1970s, we not only proved ourselves as an economic force for Saudi Arabia, but we also returned to our Saudi Arabian heritage. In 1973, the Saudi government bought a 25% interest in Aramco, increasing that interest to 60% the following year.

A Peaceful Transition

But — and this is crucial to understanding the events of the 1970s — the process by which the Kingdom acquired ownership of Aramco was unlike many of the fractious confrontations in the Middle East oil industry in that era. Whereas countries such as Libya, Iraq and Iran had simply confiscated American assets without compensation, leading to instability in global energy and geopolitics, Saudi Arabia negotiated the purchase of shares from the US owners in a gradual process that ensured good relations between the two countries. In the case of the Kingdom, the process was called "participation" rather than "nationalization."

This distinction mattered enormously. The move from US-owned Aramco to Saudi-owned Saudi Aramco was the largest amicable acquisition of corporate assets in American history, notable both for what did happen and for what didn't happen: no forcible takeover, no expropriation, no diplomatic chaos (or worse). Beginning in 1973, Saudi Arabia negotiated ever-larger interests in the company, and by 1980 the Saudi buyout was complete.

The man orchestrating the Saudi side of negotiations was Ahmed Zaki Yamani, the legendary petroleum minister. Yamani — author of the "masters of our own commodity" quote — was petroleum minister in 1968 when he told an oil conference in Beirut that it was the Kingdom's ambition to acquire 50 percent of Aramco from its American owners. The number would change as the decade wore on, but the ambition remained the same: To get control of Aramco.

At a meeting in Panama that year, Yamani was in no mood to delay any longer. The Kingdom wanted a commitment from the Americans to sell all their remaining shares. By mid-March the deal was done, effective 1980, and Saudi Aramco was officially renamed eight years later.

Birth of Saudi Aramco

In 1980, the Saudi government increased its interest in Aramco to 100%. Eight years later, the Saudi Arabian Oil Company (Saudi Aramco) was officially established — a new company to take over all the responsibilities of Aramco, with His Excellency Ali I. Al-Naimi becoming our first Saudi president in 1984, and the first Saudi president and CEO in 1988.

The choice of Al-Naimi was deeply symbolic. Naimi was born in Ar-Rakah in Saudi Arabia's Eastern Province. Born to Ibrahim, a pearl diver of the Al-Naimi tribe, and Fatima, a Bedouin of the Ajman, his parents became divorced during the pregnancy. As a consequence, Naimi was born into and lived the first eight years of his nomadic life with his mother's and stepfather's tribe. From the age of four, he tended the family's flock of lambs.

Former Saudi oil minister Ali al-Naimi joined Aramco as an office boy in 1947, replacing an older brother who died of pneumonia. He was 12 and had previously herded sheep. After Aramco sent him to Lebanon and the US to be educated, he rose through the ranks to become the first Saudi president of the firm in 1984 and its first Saudi CEO in 1988.

Al-Naimi's trajectory—from illiterate Bedouin shepherd to the most powerful figure in global oil—embodied Aramco's transformation. He represented a generation of Saudis who had literally grown up with the company, absorbing its technical expertise and corporate culture while maintaining deep roots in Saudi society.

"The real reason Aramco was able to become the successful company it is today is that once it became a Saudi firm, the oilmen continued to control it and its money, as opposed to government bureaucrats. This was unique among national oil companies."

This was Aramco's crucial distinction from other national oil companies. When Venezuela, Mexico, or Nigeria nationalized their oil industries, political appointees typically replaced technical professionals, leading to operational decline. Saudi Arabia preserved Aramco's meritocratic culture even as it transferred ownership—a decision that would pay enormous dividends in the decades ahead.

V. Downstream Integration: Going Global (1989–2010s)

Becoming an Integrated Major

The following year, Saudi Aramco began its transformation from an oil-producing and exporting company to an integrated petroleum enterprise, with the formation of Star Enterprises in 1989 — a joint venture with Texaco in the United States. This would evolve to become Motiva, initially a partnership with Texaco and Shell, which in 2017 progressed to Saudi Aramco being the sole owner of North America's largest single-site crude oil refinery at Port Arthur, Texas.

The strategic logic was compelling. As a pure upstream producer, Aramco was hostage to volatile commodity prices. When oil fell, revenues collapsed. By moving downstream into refining and marketing, the company could capture more of the value chain while securing guaranteed outlets for its crude.

Founded in the 1930s and taken over by the state in the 1980s, Aramco witnessed a significant increase in its worldwide reach in the 1990s. The business strategically diversified outside its upstream activities by establishing downstream joint ventures in the US and South Korea, thereby securing its position as a major participant in the global energy markets.

The company began as a 50–50 joint venture between Shell Oil Company (the wholly owned US subsidiary of Royal Dutch Shell) and Saudi Aramco (which had previously partnered with Texaco) in 1997. In 1988, Texaco and Saudi Refining agreed to form a joint venture known as "Star Enterprises" in which Saudi Refining would own a 50 percent share of Texaco's refining and marketing operations in the eastern United States and Gulf Coast.

Global Expansion

The opening of Petro Rabigh, Aramco's first petrochemical plant, in 2009, the establishment of Sadara Chemical Co. in 2011, and the inauguration of the SATORP and YASREF refineries in 2014 were significant turning points.

Each of these investments served multiple purposes. Petro Rabigh, a joint venture with Sumitomo Chemical, gave Aramco exposure to petrochemicals—the fastest-growing segment of oil demand. Sadara, a partnership with Dow Chemical, created the world's largest integrated chemical complex ever built in a single phase. SATORP and YASREF expanded domestic refining capacity while creating high-skilled jobs for Saudi workers.

The crown jewel of downstream expansion, however, was Port Arthur. Headquartered in Houston, Texas, Motiva refines, distributes, and markets petroleum products throughout the Americas. Our Port Arthur Manufacturing Complex in Port Arthur, Texas is comprised of North America's largest refinery with a total throughput of 720,000 barrels a day, the country's largest base oil plant, and an integrated chemical plant.

Saudi Arabia's state-owned oil company took full control of the sprawling Port Arthur refinery on Monday that is the largest refinery in the US. Aramco's deal allows the oil giant to shore up one of its best customers -- the US -- ahead of next year's planned IPO. Now that it controls the largest American refinery, Aramco can send more Saudi crude into the US for refining to sell to North American drivers.

Strategic Logic: Locking in Demand

Why does vertical integration matter? Consider Aramco's position. The company produces approximately 9 million barrels per day—but that crude is worthless unless refineries buy it. By owning refineries, Aramco guarantees demand for its own crude regardless of market conditions. It's the petroleum equivalent of Apple selling both iPhones and the chips that power them.

The petrochemical expansion serves a similar purpose. SABIC is a good strategic fit and a solid platform to support our continued investment for future growth in petrochemicals – the fastest growing sector of oil demand. Even as transportation demand potentially peaks due to electric vehicles, petrochemical demand continues growing—driven by plastics, fertilizers, and countless other products that modern civilization depends upon.

These investments transformed Aramco from a mere oil producer into a fully integrated energy company—one capable of capturing value at every stage from wellhead to gas pump. The transformation was complete by the mid-2010s, setting the stage for the next phase: going public.

VI. KEY INFLECTION POINT #1: Vision 2030 & The IPO (2016–2019)

The Crown Prince's Gambit

Saudi Vision 2030 is a government program launched by Saudi Arabia which aims to achieve the goal of increased diversification economically, socially, and culturally, in line with the vision of Crown Prince Mohammed bin Salman. It was first announced on 25 April 2016 by the Saudi government.

The vision was breathtakingly ambitious. Despite efforts to reduce Saudi dependence on oil, as of 2022, Saudi Arabia remains heavily dependent on oil revenue, as measured by its contribution to gross domestic product (GDP), fiscal revenue, and exports. Oil accounted for approximately 40% of Saudi GDP and 75% of its fiscal revenue. Mohammed bin Salman—universally known as MBS—proposed nothing less than rewiring the entire Saudi economy within 15 years.

And at the center of this transformation was Aramco. The initial goals of the stock float were to list 5 percent of the company on an international exchange, with a valuation at $2 trillion—thus raising $100 billion. Saudi Crown Prince Mohammed bin Salman (MBS) planned to use the revenue to diversify the Saudi economy.

The logic was elegant: sell a small stake in Aramco at an astronomical valuation, use the proceeds to fund investments in tourism, technology, and entertainment, and gradually wean the kingdom off its hydrocarbon dependence. He expected to raise $100 billion from the sale, valuing Aramco at $2 trillion.

The IPO Drama

But from the beginning, many investors balked at the $2 trillion valuation and the company flinched at the requirements for listing on the world's most important stock exchanges. The Saudis postponed the IPO a number of times, but a management shake-up in September 2019 was the first step in getting the process moving again.

The challenges were manifold. International investors worried about corporate governance—how could shareholders influence a company controlled by an absolute monarchy? They questioned the valuation—was $2 trillion justified for a company entirely dependent on a single commodity? And they fretted about transparency—Aramco's financial disclosures had historically been minimal.

Since around 2018, Saudi Arabia had been considering to put a portion of Saudi Aramco's ownership, up to 5%, onto public trading via a staged initial public offering (IPO), as to reduce the cost to the government of running the company. While the IPO had been vetted by major banks, the IPO was delayed over concerns of Aramco's corporate structure through 2018 into 2019.

The Abqaiq Crisis (September 2019)

Just as the IPO preparations were gaining momentum, catastrophe struck. On 14 September 2019, drones were used to attack oil processing facilities at Abqaiq and Khurais in eastern Saudi Arabia. The facilities were operated by Saudi Aramco, the country's state-owned oil company.

The Abqaiq–Khurais attack occurred on September 14, 2019, when drones and cruise missiles struck Saudi Aramco's Abqaiq oil processing facility and Khurais oil field in eastern Saudi Arabia, temporarily halting approximately 5.7 million barrels per day of crude oil production—equivalent to over half of Saudi Arabia's output and about 5% of global supply.

The attack was devastating in its precision and embarrassing in what it revealed about Saudi vulnerabilities. The Abqaiq oil facility was protected by three Skyguard short-range air defense batteries. Neither the Skyguards nor the other Saudi air-defense weapons — MIM-104 Patriot and Shahine (Crotale) — are known to have brought down any of the attacking weapons.

The September attacks were sophisticated and precise, clearly meant to send the message that the facilities are vulnerable. Spare capacity and a rapid repair program minimized the attacks' impact on global oil supply.

The September 2019 drone attacks on Aramco's facilities also delayed the onset of the IPO. Yet Aramco's response demonstrated something equally important: operational resilience. During the news conference, it was disclosed that production at Khurais resumed 24 hours after the attack. Meanwhile, Mr. Nasser stated that production at Abqaiq is currently 2 million barrels per day and its entire output is expected to be restored to prior rates by the end of September.

The Historic IPO

Despite the setbacks, the IPO proceeded—albeit in scaled-back form. However, the push for progress on the IPO was derailed in mid-October, when bankers informed Aramco management and Saudi officials that international investors were expected to value the company at between $1.1 and $1.7 trillion, far below the $2 trillion goal set by Crown Prince Mohammad bin Salman. Consequently, the Saudis decided to go with a scaled-back IPO on the Saudi stock exchange instead.

The Saudi state oil company listed 1.5 percent of shares in an IPO that raised $25.6 billion Wednesday, making it the biggest IPO of all time. On 11 December 2019, the company's shares commenced trading on the Saudi Exchange. The shares rose to 35.2 Saudi riyals, giving it a market capitalization of about US$1.88 trillion, and surpassed the US$2 trillion mark on the second day of trading.

Saudi Aramco shares zoomed higher on Thursday, turning the massive state oil producer into the world's first $2 trillion company and achieving the valuation long sought by Crown Prince Mohammed bin Salman. The stock gained 10% for a second consecutive day, reaching 38.70 riyals ($10.32) per share before giving up some of its gains. Saudi Aramco has gained roughly $300 billion in value since its shares debuted on the Riyadh stock exchange on Monday in the biggest initial public offering on record.

MBS had achieved his goal—albeit through a domestic-only listing rather than the international offering originally envisioned. The IPO crystallized Aramco's status as the world's most valuable company while providing capital for Vision 2030's ambitious projects. But it also exposed the company to a new constituency: public shareholders whose interests might not always align with those of the Saudi state.

VII. KEY INFLECTION POINT #2: The SABIC Acquisition (2019–2020)

The $69 Billion Deal

Even as the IPO drama unfolded, Aramco was executing another transformational move. Saudi Aramco today announced the signing of a share purchase agreement to acquire a 70% majority stake in Saudi Basic Industries Corporation (SABIC) from the Public Investment Fund of Saudi Arabia, in a private transaction for SAR 259.125 billion (or SAR 123.39 per share), which is equivalent to USD $69.1 billion. The remaining 30% publicly traded shares in SABIC are not part of the transaction.

Saudi Basic Industries Corporation, known as SABIC, is a Saudi chemical manufacturing company. 70% of SABIC's shares are owned by Saudi Aramco. It is active in petrochemicals, chemicals, industrial polymers and fertilizers. It is the second largest public company in the Middle East and Saudi Arabia as listed in Tadawul.

Strategic Rationale

The completion of the transaction enhances Aramco's presence in the global petrochemicals industry, a sector expected to record the fastest growth in oil demand in the years ahead.

The acquisition of the SABIC stake is consistent with Aramco's long-term Downstream strategy to grow its integrated refining and petrochemicals capacity and create value from integration across the hydrocarbon chain.

It specifically enhances Aramco's chemicals strategy by transforming Aramco into one of the major global petrochemicals players; integrating upstream production with SABIC feedstock; expanding capabilities in procurement, supply chain, manufacturing, marketing and sales; complementing geographic presence, projects and partners; and increasing the resilience of cash flow generation with synergistic opportunities.

The merger combined two Saudi champions into a single entity with unprecedented scale. Currently, Saudi Aramco and SABIC have petrochemicals production capacity of 17 and 62 million tons per annum respectively. Combined, in 2019 Aramco and SABIC recorded petrochemicals production volume of nearly 90 million tonnes, including agri-nutrient and specialty products.

Triple Win Structure

The deal's architecture was elegant in its complexity. Yasir Othman Al-Rumayyan, Managing Director, Public Investment Fund of Saudi Arabia said: "This is a win-win-win transaction and a transformational deal for three of Saudi Arabia's most important economic entities. It will unlock significant capital for PIF's continued long-term investment strategy, underpinning sectoral and revenue diversification for Saudi Arabia."

For Aramco, the deal accelerated its downstream diversification strategy. For SABIC, it provided access to Aramco's massive feedstock production and investment capabilities. For the Public Investment Fund—Saudi Arabia's sovereign wealth fund—it unlocked $69 billion in capital for Vision 2030 investments.

The transaction was completed in June 2020. Despite closing during the depths of the COVID-19 pandemic, Aramco pressed ahead. "Despite the COVID-19 pandemic forcing many companies to rethink or revise their long term strategies, our long-term focus, financial strength and resilience have enabled us to complete this historic deal. It marks the beginning of a new chapter in the history of both companies and is an important marker in delivering our long term Downstream strategy."

The Aramco-SABIC merger has delivered key strategic benefits. By acquiring a 70% stake in SABIC, Aramco expanded its global petrochemical footprint to over 50 countries and strengthened its integration across the hydrocarbon value chain. This has strengthened Aramco's position in the chemicals sector, diversifying its operations beyond crude oil and boosting resilience to market fluctuations.

VIII. Modern Era: Peak Profits & New Challenges (2020–Present)

Record Profitability

The years following the IPO brought both triumph and turbulence. From 2016 to 2024, it generated about $800 billion in net income, outperforming every other corporation globally over that period. In 2022, it posted a record net income of $161.1 billion, the highest annual profit ever disclosed by a publicly traded company. Earnings fell to $121.3 billion in 2023 and $106.2 billion in 2024, largely due to lower crude prices and reduced refining margins.

For 2024, the Company recorded strong earnings and cash flows and posted net income of ﷼398.4 billion ($106.2 billion) for the full year. According to the results, the net income reached $106.2 billion in 2024, compared to $121.3 billion in 2023. Cash flow from operating activities amounted to $135.7 billion compared to $143.4 billion in 2023.

Chairman's message: Dear shareholders, In the five years since our IPO, Aramco has provided exceptional dividend distributions and robust earnings, consistently delivering value to our shareholders. We have delivered ﷼1,656.4 billion ($441.7 billion) in dividends during this period.

Ownership & Governance Today

Aramco operates as a publicly traded company under Saudi law despite remaining majority-owned by the government. As of 2025, the Saudi government holds more than 81% of Aramco, with another 16% held by the Public Investment Fund, the kingdom's sovereign wealth fund. Only about 2.4% is available for public trading on the Saudi Exchange, or Tadawul.

In a strategic move in March, Saudi Arabia transferred 8% of Aramco's shares to the PIF – valued at around $163.6 billion, reflecting Aramco's market worth – aiming to bolster the fund as the kingdom prepares for a possible IPO of the company. This transaction could provide additional financing for Vision 2030. The transaction raised the combined stake of the PIF and its affiliates in Saudi Aramco to 16%, equating to $327 billion in value.

Diversification Initiatives

Capital investment of $53.3 billion in 2024, including $50.4 billion organic capex. 2025 capital investment guidance of $52.0 billion to $58.0 billion, excluding around $4.0 billion of project financing. Progress on track to deliver growth strategy across Upstream and Downstream, with potential additional operating cash flows of $9.0 billion to $10.0 billion from growth in Aramco's Upstream gas business, and $8.0 billion to $10.0 billion from growth in its Downstream business, by 2030.

To this end, the firm has created a special $1.5bn fund to invest in technology that can reduce the use of fossil fuels. Furthermore, Aramco Ventures, the firm's venture capital arm, has received a $4bn fund to invest in the development of disruptive technologies.

Aramco is working to secure downstream deals in Asia, particularly bolstering its presence in China, as it aims to lock in long-term crude demand and tap into the growing petrochemicals market.

Value Decline & Challenges

Yet for all its profitability, Aramco faces headwinds. As of November 2025 the stock trades at 25.8, giving it a market capitalisation of US$1.68 trillion. This represents an US$800bn fall in value since 2022, one of the largest decreases in corporate history.

The decline reflects multiple concerns: lower oil prices, the energy transition's uncertain timeline, and questions about whether state-controlled companies can deliver the kind of shareholder returns that global investors demand. Aramco remains enormously profitable, but its valuation increasingly reflects investor skepticism about long-term oil demand rather than its undeniable near-term earnings power.

IX. Playbook: Business & Investing Lessons

The Unassailable Cost Position

Aramco's low production costs and vast reserves have helped it consistently rank among the world's most profitable companies. It holds more than 250 billion barrels of proven reserves, the largest total of any company in the world.

This cost advantage is structural, not circumstantial. Saudi Arabia's geology produces oil with minimal effort—many wells flow under natural pressure, requiring none of the expensive fracking or deepwater drilling that characterizes production elsewhere. The result is a lifting cost measured in single digits per barrel while competitors struggle with costs several times higher.

The Swing Producer Role

Saudi Arabia is the primary swing producer in the Organization of the Petroleum Exporting Countries (OPEC), cutting oil production to prop up prices and balance markets when needed.

If called upon, utilizing one million barrels per day of existing spare capacity could generate an additional $12.0 billion in operating cash flow, based on 2024's average price.

This flexibility is invaluable. When competitors struggle with fixed costs and inflexible production schedules, Aramco can raise or lower output with remarkable agility. It's the ultimate insurance policy against market volatility—and a source of geopolitical leverage that few corporations possess.

Lessons for Investors and Operators

Several principles emerge from Aramco's nine-decade journey:

-

Resource advantages can be durable for decades when combined with operational excellence. Aramco didn't just inherit favorable geology—it invested relentlessly in technology, talent, and infrastructure to maximize that advantage.

-

Vertical integration (upstream → refining → petrochemicals) reduces cyclicality. When oil prices fall, refining margins often improve as feedstock costs decline. The integrated model provides natural hedges that pure-play producers lack.

-

State ownership creates both stability and governance concerns. Aramco benefits from patient, long-term-oriented ownership that doesn't panic during downturns. But investors rightly question whether their interests align with those of a government seeking to fund ambitious social programs.

-

The "too big to fail" dynamic: Aramco is the Saudi economy. With oil revenues still comprising 75% of government income, Aramco will receive support that private companies could never expect—but it also faces political constraints that competitors don't.

-

IPO timing and structure matter enormously. The decision to list domestically rather than internationally shaped Aramco's investor base, valuation dynamics, and governance requirements in ways that still reverberate.

X. Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Porter's 5 Forces Analysis

1. Threat of New Entrants: VERY LOW

The barriers to competing with Aramco are nearly insurmountable. It holds more than 250 billion barrels of proven reserves, the largest total of any company in the world. Accumulating comparable reserves would require either discovering new geological provinces (increasingly rare) or acquiring existing producers at enormous cost.

Beyond reserves, the technical expertise accumulated over 90 years creates formidable advantages. Aramco's geologists, engineers, and managers have institutional knowledge that cannot be replicated quickly. The capital requirements are staggering—exploration and development programs measured in billions annually. And geopolitical barriers mean that accessing comparable reserves requires sovereign agreements that take years or decades to negotiate.

2. Bargaining Power of Suppliers: LOW

Aramco owns its reserves outright—eliminating the most important "supplier" in the upstream oil business. Its significant in-house capabilities and vertical integration reduce dependence on external providers. Scale allows favorable terms with oilfield service companies like Schlumberger and Halliburton, who compete aggressively for Aramco contracts.

3. Bargaining Power of Buyers: MODERATE

Oil remains a commodity where buyers can theoretically choose among suppliers. However, several factors mitigate buyer power: Aramco's reliability and scale command premiums in a market where supply disruptions are common. Long-term supply agreements with refineries globally lock in demand for years. And Aramco's downstream integration—owning refineries that must buy its crude—reduces dependence on external customers.

4. Threat of Substitutes: GROWING (Long-term threat)

This is Aramco's existential challenge. Electric vehicles, renewable energy, and hydrogen all represent potential substitutes for petroleum products. However, the timeline remains uncertain, and petrochemicals provide ongoing demand even in an EV-dominated world. Petrochemicals – the fastest growing sector of oil demand—require crude oil feedstock regardless of what powers cars.

5. Competitive Rivalry: MODERATE

Aramco competes with ExxonMobil, Shell, Chevron, BP, and TotalEnergies—but from a position of structural advantage. Its production costs are a fraction of competitors', its reserves dwarf theirs, and its integration across the value chain provides resilience they lack.

Hamilton's 7 Powers Analysis

Scale Economies: Aramco exhibits enormous scale economies across exploration, production, refining, and petrochemicals. Fixed costs spread across billions of barrels create cost advantages that smaller producers cannot match.

Network Economies: Limited applicability—oil is not a network business in the traditional sense.

Counter-positioning: Aramco's willingness to maintain spare capacity represents a form of counter-positioning. Competitors cannot profitably adopt this strategy because they lack the financial resources to idle productive capacity.

Switching Costs: Moderate—refineries configured for Saudi crude grades face costs in switching to alternatives, but these are surmountable.

Branding: Minimal relevance in commodity markets, though Aramco's reputation for reliability commands premiums.

Cornered Resource: This is Aramco's defining power. The main areas of Saudi Arabia's oil reserves include the Ghawar Field (the world's largest onshore oil field) and the Safaniya Field (the world's largest offshore oil field). Both of these fields are operated by Saudi Arabia's state-owned oil company, Saudi Aramco, the world's largest oil-producing company. No competitor can access these resources.

Process Power: Aramco has developed proprietary technologies in reservoir management, enhanced oil recovery, and crude-to-chemicals conversion that provide sustainable advantages.

Key Performance Indicators for Ongoing Tracking

For investors monitoring Aramco's ongoing performance, three metrics matter most:

-

Production Cost Per Barrel: The foundation of Aramco's competitive advantage. Any material increase would signal deteriorating well productivity or rising operational complexity.

-

Downstream Integration Margin Capture: Track the spread between crude prices and refined/petrochemical product prices, multiplied by processing volumes. This reveals whether vertical integration is delivering promised value creation.

-

Free Cash Flow Conversion Rate: Net income is impressive, but free cash flow after capital expenditures and dividends determines actual value creation for shareholders. With the government extracting substantial dividends, investors should monitor whether sustainable reinvestment occurs.

Myth vs. Reality

Myth: "Aramco will be worthless when the world transitions away from oil."

Reality: The energy transition will unfold over decades, not years. Even aggressive scenarios see oil demand persisting well into the 2040s. More importantly, Aramco's cost position means it will be the last producer standing—profitably pumping crude long after higher-cost competitors have exited. The question isn't whether Aramco will survive the transition, but whether its valuation adequately reflects the uncertainty about timing.

Myth: "State ownership means Aramco operates like a government bureaucracy."

Reality: Aramco's preservation of meritocratic culture through nationalization distinguishes it from most national oil companies. Its operational performance—measured by uptime, safety records, and technological innovation—rivals or exceeds private-sector peers.

Myth: "The IPO transformed Aramco into a normal public company."

Reality: With 97%+ government ownership and production decisions subject to OPEC+ coordination, Aramco remains fundamentally different from publicly traded peers. Minority shareholders have limited influence over major decisions.

Regulatory and Legal Overhangs

Investors should monitor several areas of regulatory and accounting uncertainty:

Climate Liability Risk: According to environmentalists Aramco is responsible for more than 4% of global greenhouse gas emissions since 1965. Most of this is from the use of the oil they sold, for example burning gasoline in car engines. Aramco has no plan to limit scope 3 emissions. Climate litigation is accelerating globally, and Aramco's massive production makes it a potential target.

Reserve Estimation: Oil and gas reserves involve significant judgment in estimation. Aramco's reserves have never been independently audited to international standards, creating uncertainty about their precise magnitude.

Transfer Pricing: Transactions between Aramco and related government entities—including the SABIC acquisition—involve prices that cannot be verified against market benchmarks. Investors must trust that these are conducted at arm's length.

Conclusion

From Max Steineke's stubborn insistence on drilling deeper at Dammam No. 7 to Amin Nasser's navigation of drone attacks and pandemic disruptions, Saudi Aramco's story is one of remarkable continuity punctuated by transformational moments. The company that began as an American concession in an impoverished desert kingdom became the world's most profitable enterprise—and now confronts questions about its role in a warming world.

The bull case is straightforward: unmatched reserves, industry-leading costs, strategic integration across the value chain, and patient government ownership create a business that will generate profits for decades regardless of transition timelines.

The bear case is equally clear: state control creates governance concerns, transition uncertainty makes long-duration assets inherently risky, and declining demand growth may compress valuations even as profits remain robust.

What seems certain is that Aramco will remain central to global energy markets for the foreseeable future. The company that grew from Steineke's geological intuitions and Olayan's trucking contracts now supplies roughly 10% of the world's oil. Its decisions ripple through gasoline prices in Tokyo, petrochemical plants in Houston, and sovereign budgets in Riyadh.

For investors, the question is not whether Aramco is a good company—by any operational measure, it clearly is. The question is whether its current valuation adequately compensates for the uncertainty of demand trajectories, governance structures, and geopolitical risks that make this asset unlike any other in public markets. That judgment requires weighing decades of demonstrated excellence against an unknowable future—exactly the kind of analysis that separates genuine investment insight from mere financial calculation.

The story of Saudi Aramco is, in many ways, the story of the 20th century's most transformative industry. Where that story goes from here will shape not just one company's fate, but the trajectory of global energy for generations to come.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube