Archean Chemical Industries: The Salt to Semiconductors Story

I. Introduction & The Archean Mystery

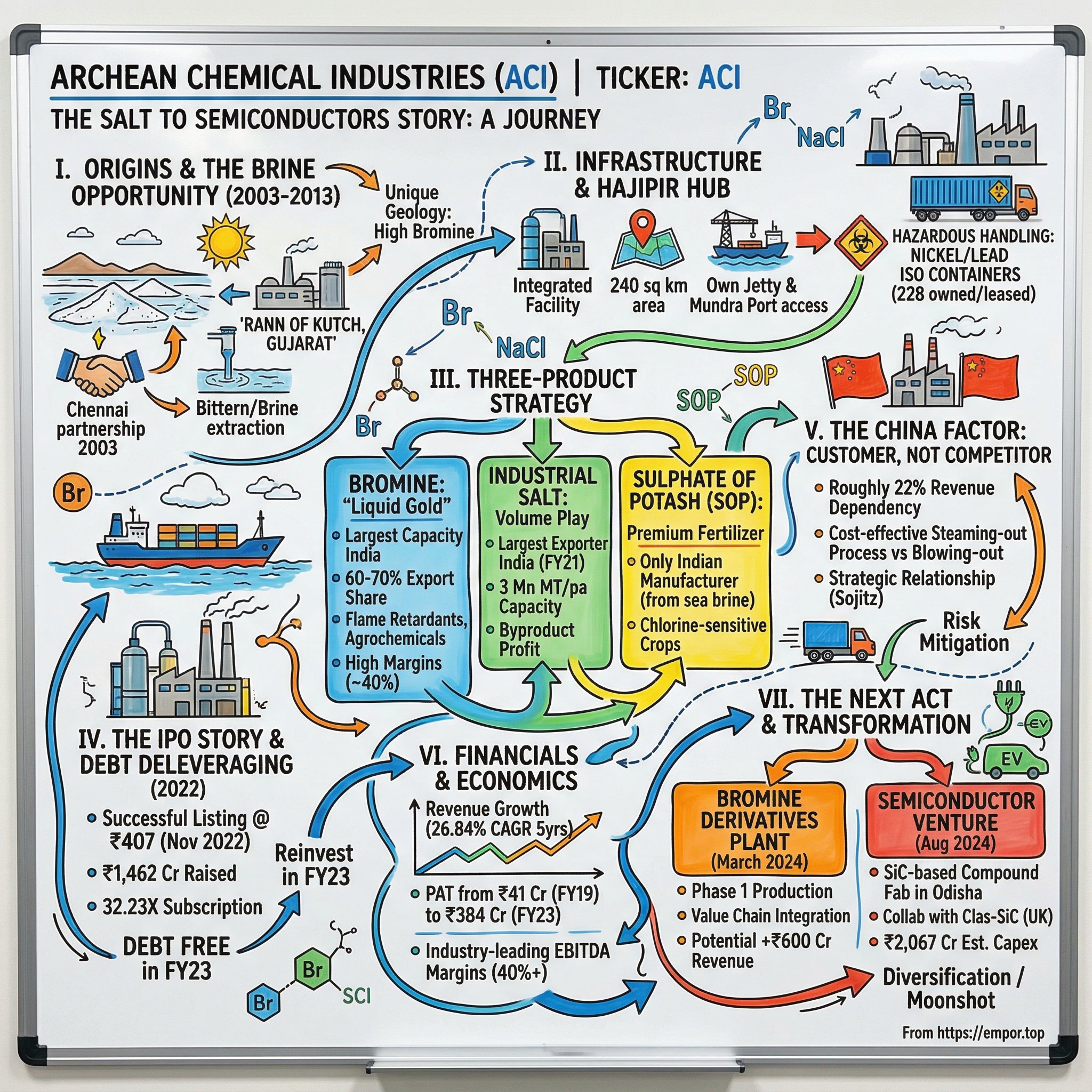

Picture the vast white expanse of the Rann of Kutch in Gujarat—a 7,500 square kilometer salt marsh that transforms from desert to shallow sea with the monsoons. Here, where temperatures soar to 50°C in summer and ancient seawater has concentrated minerals over millennia, lies one of nature's most peculiar chemical treasuries. It's 2003, and while most see only desolate salt flats, a partnership firm in Chennai sees liquid gold beneath the crystalline surface.

The mystery isn't just geographical—it's chemical. How does a region that looks like a lunar landscape hold the key to everything from flame-proofing your smartphone to purifying oil wells halfway across the world? And how does a company that started as a simple partnership extracting salt transform into India's largest exporter of bromine and industrial salt in Fiscal 2021. The company is the leading specialty marine chemical manufacturer in India and is focused on producing and exporting bromine, industrial salt, and sulphate of potash to customers around the world.

This is the story of Archean Chemical Industries Limited (ACI)—a company that has mastered the alchemy of turning brine into business, leveraging one of the world's most unique geological formations into a global chemical powerhouse. The Rann of Kutch isn't just any salt marsh; it's one of the largest salt marshes in the world, and its brine holds concentrations of bromine second only to the Dead Sea.

Today, as you read this on your device—likely containing brominated flame retardants—or sit in an office with fire-safety compliant materials, you're surrounded by the invisible presence of marine chemicals. The global bromine market alone exceeds $3.6 billion, and India has emerged as a critical player. But the real intrigue lies in how a company mining ancient seas is now positioning itself in cutting-edge semiconductor manufacturing with a Rs.2067 crore SiC semiconductor fab approved by the Union Cabinet for its subsidiary in Odisha.

The themes we'll explore are as layered as the geological strata of the Rann itself: How resource monopolies are built in the 21st century. Why chemistry creates moats deeper than Warren Buffett's castle. The paradox of China as both largest customer and potential competitor. And perhaps most fascinating—how a commodity chemicals company is making the leap to semiconductors, bridging ancient geology with silicon-age technology.

II. Origins & The Brine Opportunity (2003-2013)

The year 2003 wasn't particularly auspicious for starting a chemical venture in India. The global economy was still recovering from the dot-com bust, and specialty chemicals weren't exactly the darling of investors. Yet on November 20, 2003, Archean Chemical Industries was originally formed as a Partnership Firm under the name of Archean Chemical Industries at Chennai pursuant to a Partnership Deed dated November 20 2003 which was registered under the Indian Partnership Act 1932 with the Registrar of Firms Chennai.

The founding vision wasn't born in a boardroom but from recognizing what others had overlooked. The Rann of Kutch, straddling the India-Pakistan border, had been exploited for common salt for centuries. But the real treasure lay deeper—in the concentrated brine that contained bromine at levels that made extraction economically viable. The company sources its brine reserves from the Rann of Kutch, located on the Gujarat coast, and manufactures its products at its state-of-the-art facility near Hajipir in Gujarat.

Understanding the resource requires a chemistry lesson most MBAs never get. Seawater contains about 65 parts per million of bromine. Through solar evaporation in the Rann's natural pans, this concentration increases dramatically. When seawater evaporates under the scorching Gujarat sun, it leaves behind not just salt, but a complex cocktail of minerals. The art lies in the sequence of extraction—first comes sodium chloride (common salt), then other salts precipitate, and finally, you're left with bittern, the mother liquor rich in bromine, magnesium, and potassium.

But having a resource and extracting it profitably are two different games entirely. The early years from 2003 to 2009 were about solving fundamental challenges. How do you build infrastructure in a region where the nearest proper road is kilometers away? Where summer temperatures make equipment malfunction and monsoons can flood everything? Where skilled labor thinks you're crazy for wanting to work in such conditions?

Subsequently, the Partnership Firm converted into Private Limited Company under the Companies Act, 1956 with the name 'Archean Chemical Industries Private Limited' and a Certificate of Incorporation dated July 14, 2009 was issued by the Registrar of Companies, at Chennai. This transformation wasn't just legal restructuring—it marked the shift from experimental venture to serious industrial operation.

The chemistry lesson that changed everything was understanding why bromine matters. It's the only non-metallic element that's liquid at room temperature—a reddish-brown, fuming liquid that's highly corrosive and toxic. Bromine, a naturally occurring halogen element, manifests as a reddish-brown liquid with a distinct odor that can cause irritation to the eyes, skin, and respiratory system. Even brief exposure to concentrated bromine vapor can prove fatal. Yet this dangerous element is crucial for modern life. It's the key ingredient in flame retardants that keep our electronics from catching fire, in compounds that help extract oil from deep wells, in pharmaceuticals that treat everything from seizures to sedation, and in agrochemicals that protect crops.

The Hajipir facility, built on the northern edge of the Rann, wasn't just another chemical plant. The company has an integrated production facility for the bromine, industrial salt, and sulphate of potash operations, located at Hajipir, Gujarat, located on the northern edge of the Rann of Kutch brine fields. The location was strategic—close enough to the brine fields to minimize raw material transport, yet accessible enough to connect to ports for export. The facility would eventually span approximately 240 square kilometers, including the salt fields and brine reservoirs.

By 2013, the foundation was set. In 2013, it commenced the operations of industrial salt to Japan and South Korea. In 2014, it commenced operations on production of bromine in China. The company had cracked the code of extraction, built the infrastructure, and begun to establish its market presence. But this was just the beginning of a much larger story.

III. The Three-Product Strategy: Bromine, Salt & SOP

In the commodity chemicals business, diversification isn't just about risk management—it's about extracting every molecule of value from your raw material. Archean's three-product strategy reads like a masterclass in resource optimization, turning what nature provides into three distinct revenue streams, each with its own market dynamics, pricing power, and growth trajectory.

Let's start with bromine—the liquid gold. At current capacity of 28,500 MT per annum, Archean has built one of the leading players in the bromine with largest capacity in India. Company further holds ~60-70% of the market share in exports of bromine. But what makes bromine so valuable? It's not just scarcity—it's the complexity of handling it. The transportation of bromine is also dangerous and requires nickel and lead lined ISO containers, of which they had 228 such containers (owned and leased) for the export business as of June 30, 2022. This isn't a product you can just load onto any truck. The specialized handling requirements create a natural barrier to entry that protects margins.

The economics of bromine are fascinating. It enjoys healthy operating efficiency with profitability of over ~40% in fiscals 2022 and 2023, driven by low cost of production due to fully integrated facility and quality of sea brine available in the Great Rann of Kutch region. Due to the quality and nature of the available sea brine, the steaming out process is used to extract bromine, which is more cost-effective than the blowing out process used in China and Japan. This process advantage isn't replicable—it's a gift from geology that translates directly to the bottom line.

Industrial salt, with its 3 million MT annual capacity, might seem pedestrian compared to bromine, but it's the volume play that provides stability. The beauty lies in the integration—salt is the first product extracted from seawater evaporation, making it essentially a byproduct that becomes a profit center. The company was the largest exporter of industrial salt in India with exports of 2.7 million MT in Fiscal 2021. Every ton of salt sold improves the economics of bromine extraction, creating a virtuous cycle of profitability.

Then there's Sulphate of Potash (SOP)—the specialty fertilizer that commands premium prices. Archean is also the only manufacturer of SOP from natural sea brine in India. With 130,000 MT per annum capacity, it's the smallest by volume but highest by value-add. SOP is crucial for chlorine-sensitive crops like tobacco, fruits, and vegetables—markets where farmers pay premiums for quality. It's extracted from the bittern left after salt crystallization, meaning Archean squeezes value from what others might consider waste.

The integrated production model is where the magic happens. One brine reservoir, one facility, three products—each supporting the economics of the others. The salt pans that concentrate brine for bromine extraction also produce industrial salt. The bittern that remains after salt crystallization yields both bromine and SOP. It's circular economy before the term became fashionable.

But integration without customers is just efficient isolation. Here's where things get interesting—and concerning. It derives ~25% of revenues from its top customer, Sojitz and also about ~70% of revenues from its top 10 customers exposing the company to customer concentration risk. Sojitz Corporation, the Japanese trading giant, isn't just a customer—they're also a shareholder, creating an interesting dynamic of aligned interests but also dependency.

The customer concentration story reveals both strength and vulnerability. The key geographies to which it exports products include China, Japan, South Korea, Qatar, Belgium and the Netherlands. Some of its major customers include Sojitz Corporation, which is also a shareholder in the Company, Shandong Tianyi Chemical Corporation, Unibrom Corporation, Wanhau Chemicals and Qatar Vinyl Company Limited. These aren't spot market transactions—they're long-term relationships with global giants who need reliable supply of specification-grade chemicals.

The margin story across products tells us about competitive positioning. While bromine commands the highest margins due to complexity and scarcity, industrial salt provides the volume that absorbs fixed costs, and SOP delivers premium realization in agricultural markets. Together, they create a margin profile that's the envy of the commodity chemicals industry—40%+ EBITDA margins in an industry where 15-20% is considered healthy.

IV. The IPO Story & Market Debut (2022)

November 2022 wasn't the most auspicious time for an IPO. Global markets were jittery with inflation concerns, the Russia-Ukraine conflict had disrupted supply chains, and tech IPOs globally were getting hammered. Yet here was a specialty chemicals company from Gujarat, preparing to test public markets with a ₹1,462 crore offering. The pre-IPO journey itself was a transformation story—from debt-laden struggler to profitable powerhouse.

The IPO construct was interesting: Archean Chemical IPO is a main-board IPO of 3,59,28,869 equity shares of the face value of ₹2 aggregating up to ₹1,462.30 Crores. The issue is priced at ₹407 per share. This wasn't just founders cashing out—₹805 crores was fresh capital for growth, while ₹657 crores was an offer for sale. The pricing at ₹407 per share valued the company at roughly ₹5,000 crores at the upper band, aggressive for a commodity chemicals player but perhaps justified by those 40% margins.

Archean Chemical IPO bidding started from November 9, 2022 and ended on November 11, 2022. The allotment for Archean Chemical IPO was finalized on Wednesday, November 16, 2022. The shares got listed on BSE, NSE on November 21, 2022. Those twelve days from opening to listing would prove eventful.

The subscription numbers told the real story: With subscription of 32.23X overall and QIB subscription at 48.91X, the listing was expected to be healthy, at the very least. When institutional investors oversubscribe nearly 49 times, they're seeing something beyond the numbers. The retail portion at 9.96X was healthy but not overwhelming—perhaps the complexity of marine chemicals didn't resonate with individual investors the way a consumer company might.

Then came November 21, 2022—listing day. On 21st November 2022, the stock of Archean Chemical Industries Ltd listed on the NSE at a price of Rs.450, a premium of 10.57% over the issue price of Rs.407. In a market where many IPOs were listing flat or at discounts, a 10%+ premium was validation. The stock touched ₹476 during the day, suggesting demand beyond the initial pop.

The use of proceeds revealed strategic thinking. This wasn't growth for growth's sake—it was balance sheet repair first. The company had explicitly stated its intention to redeem NCDs (non-convertible debentures), essentially using public money to replace expensive debt. It's not the sexiest use of IPO proceeds, but for a capital-intensive business with cyclical cash flows, deleveraging at the right time can be the difference between thriving and merely surviving.

What's fascinating is the investor mix that emerged. Chemikas Speciality LLP, Ravi Pendurthi and Ranjit Pendurthi are the company promoters. Post-IPO, promoters retained 53.4% stake—enough to control but not so much as to concern minority investors about governance. The presence of Sojitz Corporation as both customer and shareholder added an interesting dimension—a strategic investor who understood the business intimately.

The post-IPO performance validated the pricing. Archean made its debut on the NSE and BSE on November 22, 2022, via a successful IPO at INR 407 per share. The shares opened at INR 450 on the NSE, representing a ~11% premium over the IPO price, and closed at INR 458. The current share is ~40% higher than the IPO price. For early investors, this wasn't just a successful listing—it was the beginning of a rerating story.

But the real validation came from the fundamentals post-listing. Company has grown its revenue at 26.84% in past 5 years, while PAT grew from Rs 41 Cr in FY19 to Rs 384 Cr in FY23. Moreover, company now become a debt free in FY23. From ₹41 crores profit to ₹384 crores in four years—that's not just growth, it's transformation. And achieving debt-free status within months of listing? That's execution.

The IPO marked a turning point—from private company managing stakeholders to public company managing expectations. The quarterly scrutiny, the analyst calls, the constant comparison with peers—all new challenges. But it also brought currency for acquisitions, credibility for expansion, and capital for the next phase of growth. The market had validated the Archean story. Now came the harder part—delivering on the promise.

V. The China Factor: Customer or Competitor?

In the global chemicals game, China is usually the disruptor—massive scale, lower costs, and government support creating unbeatable competition. But in bromine, Archean has found a sweet paradox: China is its biggest customer, not its competitor. Almost 50% of revenue comes from Bromine and 44% of that goes to China. This means roughly 22% of Archean's total revenue depends on Chinese demand—a concentration that would make risk managers nervous, yet has proven remarkably stable.

Understanding why requires grasping China's bromine predicament. Despite being the world's largest chemical producer, China's bromine resources are limited and extraction costs are high. In the competitive landscape of the chemical industry, China often emerges as a formidable competitor. However, in the case of Bromine, China plays a different role – that of a significant consumer. Archean benefits from this dynamic, as China stands as one of the largest consumers of Indian Bromine.

The technical advantage is profound. Chinese producers primarily use the "blowing out" process for bromine extraction—passing air through brine to volatilize bromine, then capturing it. It works, but it's energy-intensive and less efficient. Archean's "steaming out" process, enabled by the unique chemistry of Rann of Kutch brine, delivers significantly lower costs. It's a geological gift that no amount of Chinese industrial policy can replicate.

Post-COVID, the supply chain dynamics shifted dramatically. The world learned the risks of single-source dependency, and "China Plus One" became corporate strategy across industries. For Archean, this presented opportunity on multiple fronts. Companies seeking to diversify from Chinese suppliers looked to India. Meanwhile, Chinese companies, facing their own supply constraints, increased purchases from India. And while it is currently lagging behind on innovation—especially in more complex fine chemicals—all signs suggest it will catch up with the global leaders within the next decade or two.

The competitive positioning versus other global players adds another layer. The Dead Sea producers—Israel's ICL and Jordan's Arab Potash—have similar geological advantages but face different challenges. ICL deals with environmental concerns about Dead Sea depletion. Jordan faces regional instability issues. American producers in Arkansas have deep brine wells but higher extraction costs. India's cost-competitive position in Bromine production is highlighted, with Archean among the top five global producers, surpassing China and Japan in cost efficiency.

But customer concentration remains the elephant in the room. During FY23, Sojitz Corporation (A Japanese trading conglomerate, largest customer & equity shareholder), contributed to 23% of revenue. Furthermore, the top 10 customers of the company contributed to 64% of revenue. This isn't unusual in specialty chemicals—long-term contracts with major players provide stability—but it does mean Archean's fortunes are tied to a handful of relationships.

The nature of these relationships matters. These aren't commodity trades on a mercantile exchange. Some of their major customers include Sojitz Corporation, which is also a shareholder in their Company, Shandong Tianyi Chemical Corporation, Unibrom Corporation, Wanhau Chemicals and Qatar Vinyl Company Limited. Each represents multi-year contracts, technical specifications, quality audits, and deep integration into customer supply chains. Switching costs are high on both sides.

China's domestic bromine market tells another story. The enormous base that China's chemical industry now constitutes—around $1.5 trillion of sales in 2017, amounting to nearly 40 percent of global chemical-industry revenue—means that, even at lower overall growth rates, the growth of absolute volume is still very large. To get a sense of that potential, consider that, at 5 percent growth per year, China will be adding the equivalent of the annual sales of Brazil's or Spain's chemical industries. This isn't a market that's going away.

The application mix in China reveals strategic dependency. Chinese demand for brominated flame retardants—driven by its massive electronics manufacturing sector—creates structural demand. Every smartphone, laptop, television needs flame retardants. As long as China remains the world's electronics factory, it needs bromine. And increasingly stringent fire safety regulations only increase this demand.

Risk mitigation has become strategic priority. Geographic diversification beyond China, development of bromine derivatives to capture more value, and the surprising semiconductor pivot—all represent attempts to reduce Chinese customer concentration while maintaining the relationship value. It's a delicate balance: embrace the Chinese opportunity while building alternatives.

VI. Infrastructure & Operations: The Hajipir Hub

Drive 270 kilometers northwest from Ahmedabad, past the last proper towns, through increasingly desolate landscape where the horizon shimmers with heat mirages, and you'll reach Hajipir—a name that means nothing to most Indians but everything to global bromine markets. Here, where the Little Rann of Kutch meets industrial ambition, sits one of the most integrated chemical operations in Asia.

The integrated facility isn't just large—at 240 square kilometers including brine fields, it's a small city dedicated to chemical extraction. Their production plant is close to the captive Jakhau Jetty and Mundra Port, from which they deliver their products to foreign consumers. Their complex, as well as the adjacent salt flats and brine reservoirs, covers an area of about 240 square kilometres. Their production plant has an installed capacity of 28,500 MT per annum of bromine, 3,000,000 MT per annum of industrial salt, and 130,000 MT per annum of sulphate of potash as of September 30, 2021.

The logistics advantage can't be overstated. The manufacturing facility is located in close proximity to the Jakhau Jetty and Mundra Port. Jakhau Jetty, though operational only 7-8 months due to monsoons, handles 5 million MT annually with twin conveyor systems. When Jakhau closes, Mundra Port—one of India's largest private ports—takes over. This dual-port strategy ensures year-round export capability, crucial for maintaining customer commitments.

But it's the hazardous materials challenge that truly defines operations. Bromine isn't just dangerous—it's viciously corrosive, attacking most materials, toxic enough that a few breaths of concentrated vapor can be fatal. Bromine is a very caustic, dangerous, and toxic chemical, and handling it necessitates a high level of specialist knowledge, which they have acquired. Bromine transportation is also hazardous, necessitating the use of nickel and lead coated ISO containers, of which they had 226 (owned and rented) for their export operations.

The specialized ISO containers tell a story of capital intensity and expertise. Each nickel-and-lead-lined container costs lakhs of rupees. You can't just rent these anywhere—there's a global shortage. Owning 228 containers isn't just about having transport capacity; it's about controlling a critical bottleneck in the supply chain. Competitors can't simply decide to enter the bromine export business—where would they get the containers?

Environmental management at Hajipir is a constant battle against nature and regulation. The facility must handle everything from bittern disposal to air emissions, all while operating in an ecologically sensitive area. The brine fields themselves are a delicate balance—too much extraction and salinity drops, too little and economics suffer. It's industrial ecology where chemistry, biology, and business intersect.

The land lease complexity adds another dimension. Archean manages a manufacturing facility and brine reserves on land that was leased by the Government of Gujarat. These aren't perpetual freeholds—they're government leases that need renewal, renegotiation, and constant political management. In a state where land is political, maintaining good relationships with successive governments becomes a core competency.

Sustainability isn't just corporate speak here—it's operational necessity. The solar evaporation process that concentrates brine is carbon-neutral by design. The integrated production means minimal waste—what's bittern for one process becomes raw material for another. Even the water used is recycled multiple times before discharge. It's sustainability driven by economics, the best kind.

The workforce challenge in such remote, harsh conditions is real. Convincing engineers to live in Hajipir, where summer temperatures hit 48°C and the nearest entertainment is hours away, requires more than money. The company has built colonies, schools, medical facilities—infrastructure that makes life possible if not comfortable. It's the hidden cost of operating at the edge of civilization.

Maintenance in this environment is relentless. Salt corrodes everything. Heat degrades equipment. Monsoons flood areas. The facility runs 24/7, 365 days—bromine doesn't wait. Preventive maintenance isn't just good practice; it's survival. A major equipment failure could mean weeks of lost production and millions in contract penalties.

The recent capacity expansions show confidence in the model. Adding bromine derivatives production means more complexity but also more value capture. Each expansion isn't just about adding equipment—it's about maintaining the delicate balance of integrated production while scaling up. It's industrial orchestration at its most complex.

VII. Financial Deep Dive & Unit Economics

The numbers tell a story of transformation that would make any private equity firm jealous. Revenue grew from Rs 617 Crores in FY20 to Rs 1142 Crores in FY22, but revenue growth alone doesn't capture the real story. It's the margin expansion that reveals the operational leverage at work.

Starting with the headline margins: healthy operating efficiency with profitability of over ~40% in fiscals 2022 and 2023. In commodity chemicals, where 15% EBITDA margins are respectable and 20% is excellent, Archean operates in a different league. This isn't financial engineering—it's the compound effect of geological advantage, process efficiency, and integrated operations.

The unit economics of bromine reveal why these margins are sustainable. With production costs among the lowest globally thanks to the steaming-out process, Archean enjoys a cost advantage that's structural, not temporary. When global bromine prices are $3,000 per MT, and your production cost is under $1,500, the math becomes compelling. Even in down cycles, when prices might fall to $2,000, the business remains solidly profitable.

Company has grown its revenue at 26.84% in past 5 years, while PAT grew from Rs 41 Cr in FY19 to Rs 384 Cr in FY23. Moreover, company now become a debt free in FY23. The PAT growth from ₹41 crores to ₹384 crores—an 837% increase—shows operational leverage at its finest. Fixed costs spread over growing volumes, efficiency improvements, and better product mix all contributed.

The working capital dynamics deserve attention. Debtor days have increased from 43.5 to 57.7 days. Working capital days have increased from 59.5 days to 83.8 days. This deterioration might concern some, but in specialty chemicals with large customers, extending credit is often the price of maintaining relationships. When your customer is Sojitz or a major Chinese importer, you accept their payment terms.

The cash conversion story post-debt reduction is where things get interesting. With no debt servicing burden, almost all operating cash flow becomes available for growth or distribution. The company generated enough cash not only to fund operations but also to embark on the ambitious bromine derivatives expansion without significantly leveraging the balance sheet again.

Comparing with global peers illuminates competitive position. Israel's ICL, despite Dead Sea advantages, operates at 25-30% EBITDA margins. Jordan Bromine Company achieves similar levels. Albemarle's bromine division in Arkansas reports margins in the 20-25% range. Archean's 40%+ margins aren't just good—they're industry-leading, suggesting either superior operations or under-pricing that could correct upward.

The cyclical nature requires understanding. Bromine prices have historically shown 3-5 year cycles, driven by capacity additions and demand fluctuations. In up cycles, prices can double; in down cycles, they might fall 40%. But with Archean's cost position, even trough pricing maintains profitability. It's not about avoiding cycles—it's about surviving them better than competitors.

The capital allocation framework emerging post-IPO shows maturity. First priority: maintain the base business with sustenance capex of ₹50-70 crores annually. Second: growth investments in derivatives and new products, budgeted at ₹250 crores for the derivatives plant. Third: the surprising semiconductor venture, suggesting management's appetite for adjacency expansion. No dividends yet, but with this cash generation, it's likely coming.

The recent quarters show some volatility—volumes affected by Chinese destocking, prices under pressure from global slowdown. But the cost position remains intact. When your production costs are half of global averages, temporary price weakness is manageable. It's structural advantage versus cyclical headwinds, and structure usually wins over time.

VIII. The Next Act: Derivatives & Semiconductors

The bromine derivatives plant marks Archean's evolution from commodity producer to specialty chemicals player. In March 2024, Archean Chemical Industries started production facility of bromine derivative products. Unit commissioned phase1 of production facility of bromine derivative products. This isn't just capacity addition—it's value chain integration that could double the revenue per MT of bromine processed.

The product portfolio being developed reads like a who's who of specialty chemicals. Flame Retardants, Clear Brine Fluids, and PTA Synthesis Catalysts. With a focus on Flame Retardants, Clear Brine Fluids, and Bromine Catalysts, Archean aims to tap into diverse markets and increase its annual revenue potential by 600 Cr. Each serves different industries—flame retardants for electronics and construction, clear brine fluids for oil drilling, PTA catalysts for polyester production. It's diversification within specialization.

The economics of derivatives are compelling. While liquid bromine might sell for $2,500-3,000 per MT, brominated flame retardants can command $5,000-8,000 per MT. Clear brine fluids for deep-well drilling, where performance is critical, can exceed $10,000 per MT. The value addition is substantial, and margins expand accordingly.

But the real surprise came in August 2024: SiCSem Pvt. Ltd., a subsidiary of Archean Chemicals, which will establish a Silicon Carbide-based compound semiconductor fab in Info Valley, Bhubaneshwar, Odisha. This will be the first commercial compound fab in India, boasting an annual capacity of 60,000 wafers and a packaging capability of 96 million units. The ambitious project will be realised with an estimated capital expenditure of ₹2,067 crore.

Silicon Carbide semiconductors? From a bromine company? The logic requires understanding that SiC devices are crucial for electric vehicles, renewable energy systems, and high-efficiency power electronics. They operate at higher temperatures, voltages, and frequencies than silicon. As India pushes for EVs and renewable energy, domestic SiC production becomes strategic.

The partnership structure reveals sophistication. SiCSem Pvt. Ltd. is set to collaborate with Clas-SiC Wafer Fab Ltd., a UK-based company, to establish this integrated facility. Technology transfer from an established player, government support under the India Semiconductor Mission, and Archean's execution capabilities—it's a combination that might just work.

Ranjit Pendurthi is a highly accomplished 49-year-old Promoter and Managing Director of Archean Chemical Industries Limited. With over two decades of experience, he has successfully created and led multiple successful organizations, driving value for stakeholders at every step. Ranjit's leadership is characterized by a strategic vision, operational excellence, and a relentless commitment to sustainable growth. Under his leadership, this diversification isn't random—it's strategic.

The execution risks are real. Semiconductor manufacturing is orders of magnitude more complex than chemical production. Clean rooms, nanometer precision, yield management—these are different capabilities entirely. The capital intensity is enormous, and the learning curve steep. Many have tried to enter semiconductors and failed. But the government support and technology partnership de-risk the venture somewhat.

The timeline is ambitious but realistic. The Indian company plans to build a silicon carbide manufacturing facility in Odisha within the next 24-36 months, positioning itself to cater to domestic and international markets. This isn't a 5-10 year dream—it's a near-term reality with concrete milestones and committed capital.

Market timing appears favorable. The proposed products will have applications in Missiles, Defence equipment, Electric Vehicles (EVs), Railway, Fast Chargers, Data Centre racks, Consumer Appliances, and Solar Power Inverters. Given the growing demand of semiconductors in telecom, automotive, datacentres, consumer electronics and industrial electronics, these four new approved semiconductors projects would significantly contribute to making Atmanirbhar Bharat. The India semiconductor mission provides subsidies, the EV transition drives demand, and geopolitical tensions make supply chain diversification critical.

The capital allocation for these ventures shows confidence. ₹250 crores for bromine derivatives, ₹2,067 crores for semiconductors—this is betting the company on transformation. But with strong cash generation from the base business and no debt, Archean can afford calculated risks. The derivatives plant is already generating revenue; the semiconductor venture is the moonshot.

IX. Playbook: Lessons in Resource-Based Businesses

Building moats with natural resources isn't just about having the resource—it's about creating barriers that compound over time. Archean's playbook offers lessons that extend beyond chemicals to any resource-based business.

First, location isn't just important—it's everything. The Rann of Kutch isn't replaceable. You can't create another one, move it closer to markets, or replicate its chemistry elsewhere. This geological monopoly is the foundation upon which everything else builds. But having a resource means nothing without the ability to extract it economically, and here the integration with logistics infrastructure—the proximity to ports, the owned jetty capacity—transforms potential into profit.

The importance of process innovation in commodities cannot be overstated. The steaming-out versus blowing-out process difference might seem like technical minutiae, but it's the difference between 40% margins and 20% margins. In commodities, where you can't differentiate the product, you must differentiate the process. Every percentage point of efficiency improvement drops straight to the bottom line.

Managing customer concentration in B2B markets requires a delicate balance. Archean's relationship with Sojitz—customer, shareholder, and strategic partner—shows how concentration can be strength if managed correctly. The key is making yourself indispensable not through lock-in but through reliability, quality, and continuous improvement. When switching costs are high on both sides, partnerships become sticky.

The timing of public markets entry matters enormously. Going public in 2022, after achieving profitability and cleaning up the balance sheet, was masterful timing. The market rewarded the transformation story. Had they gone public earlier, during the struggling years, the valuation would have been a fraction. Patience in capital markets entry can mean billions in market cap difference.

Capital allocation in cyclical industries requires counter-cyclical thinking. Expanding during downturns, when equipment is cheap and competitors are retrenching, positions you for the upturn. Archean's derivatives expansion during a bromine price downturn shows this thinking. By the time the plant is operational, the cycle might have turned, and they'll capture the full margin expansion.

The value of vertical integration depends on market structure. In fragmented markets, integration might not pay off. But in concentrated markets with few players and high switching costs, integration creates competitive advantage. Archean's move into derivatives isn't just about margin capture—it's about controlling more of the value chain when customers have few alternatives.

Managing government relations in resource businesses is non-negotiable. Land leases, environmental permits, export licenses—government touches everything. Archean's ability to maintain operations through multiple political changes in Gujarat shows institutional relationship management beyond any single individual or party.

The unexpected value of adjacencies appears when you look beyond the obvious. Who would have thought a bromine company could enter semiconductors? But the competencies—managing complex projects, handling hazardous materials, operating in difficult environments, maintaining quality standards—transfer more than you'd expect. Core competencies are often broader than they appear.

Technology adoption in traditional industries can be transformative. While Archean appears to be a basic chemicals company, the process optimization, quality control systems, and now semiconductor venture show technological sophistication. The companies that survive in commodities are often technology leaders disguised as traditional players.

The importance of patient capital cannot be overstated. From 2003 to 2022—nineteen years from founding to IPO. Building resource businesses takes time. The infrastructure, the processes, the relationships—none of this happens quickly. Investors seeking quick returns need not apply. But for those with patience, the returns can be extraordinary.

X. Bull vs. Bear Case & Valuation

The Bull Case:

Start with the resource monopoly. The Rann of Kutch isn't making more of itself. With limited global bromine resources and growing demand from electronics, EVs, and flame retardancy regulations, supply-demand dynamics favor producers. Archean's position as lowest-cost producer globally means they win in any pricing environment—making outsized profits in good times, taking market share in bad times.

The derivatives expansion could be transformative. FY25 will see scaling up of this facility with potential sales of Rs2-3bn (at 60-70% utilisation). Adding ₹200-300 crores of high-margin revenue from derivatives could push EBITDA margins even higher. If flame retardants achieve anticipated penetration, revenue could double without adding bromine capacity.

India's chemical export opportunity is real and growing. Global companies seeking China+1 alternatives find India attractive—similar cost structure, better IP protection, democratic governance. Archean, as India's leading marine chemicals exporter, captures this trend naturally. The government's focus on chemical manufacturing through PLI schemes and infrastructure development only helps.

The semiconductor diversification, if successful, transforms the company's multiple. Semiconductor companies trade at 25-30x earnings; chemical companies at 12-15x. Even partial success in SiC semiconductors could rerate the entire company. The ₹2,067 crore investment, backed by government support, could create ₹5,000+ crores of value.

The debt-free balance sheet provides flexibility. No interest burden, no covenant restrictions, no refinancing risks. In a rising rate environment, this is particularly valuable. The company can pursue growth opportunities, weather downturns, or return capital to shareholders as conditions warrant.

ESG tailwinds are underappreciated. Solar evaporation for brine concentration is carbon-neutral. The integrated production minimizes waste. As ESG mandates tighten globally, clean producers command premiums. Archean's sustainable production could become a differentiator beyond just cost.

The Bear Case:

Customer concentration is the obvious risk. The reliance on a single customer, Sojitz, for a significant portion of industrial salt revenues exposes the company to customer concentration risk. Losing Sojitz or even one major Chinese customer could crater earnings. In B2B chemicals, customer relationships can change suddenly due to factors beyond company control.

Commodity price volatility is structural. Bromine prices can halve in bad cycles. While Archean's cost position provides cushion, the operating leverage works both ways. A 30% price decline could cut profits by 50% or more. The market tends to overreact to commodity price movements, creating stock volatility.

China dependency cuts both ways. Today China is a customer; tomorrow it could be a competitor. Chinese companies are investing heavily in bromine extraction technology. If they crack the code on cost-effective extraction, Archean's largest market could evaporate. The geopolitical risks of India-China tensions add another layer of uncertainty.

Execution risk in semiconductors is enormous. Chemical companies entering semiconductors have a poor track record. The capital intensity, technological complexity, and competitive dynamics are completely different. The ₹2,067 crore could be a massive capital sink with no returns. Management attention diverted to semiconductors could hurt the core business.

Environmental and regulatory risks are rising. The Rann of Kutch is ecologically sensitive. One environmental accident, one regulatory change, one PIL challenging operations could disrupt everything. As climate activism intensifies, resource extraction businesses face increasing scrutiny. The social license to operate isn't guaranteed.

The lease renewal uncertainty hangs over everything. Government leases aren't perpetual. Terms could change, costs could rise, or renewals could be denied. In Indian politics, where populism often trumps economics, assuming continued favorable treatment is risky. A change in state government could change everything.

Technology disruption is possible. Flame retardants face pressure from non-halogenated alternatives. If technology develops that makes brominated flame retardants obsolete, a major demand driver disappears. In chemicals, technology shifts happen slowly—until they happen fast.

Valuation Perspective:

At current levels around ₹630, the market cap stands at approximately ₹7,800 crores. With TTM earnings of ₹380 crores, the P/E is roughly 20x. For a commodity chemicals company, this seems full. For a specialty chemicals company with 40% margins, it's reasonable. For a potential semiconductor play, it might be cheap.

The EV/EBITDA multiple around 11-12x compares favorably to global peers. ICL trades at 8-10x, but with lower margins. Indian specialty chemical companies trade at 15-20x, but with less defensive positions. The valuation seems to price the base business fairly with limited credit for growth options.

The derivatives expansion and semiconductor venture provide free optionality at current valuations. If either succeeds, significant rerating is possible. If both fail, the core business still justifies current valuation. It's asymmetric risk-reward—limited downside, significant upside.

XI. Epilogue: From Ancient Seas to Modern Industry

The story of Archean Chemical Industries is fundamentally about transformation—of ancient seawater into modern materials, of a partnership firm into a public company, of commodity producer into potential technology player. It's a narrative that speaks to larger themes about India's industrial evolution and the unexpected paths to value creation.

Standing at the Hajipir facility, watching the endless white expanse of salt pans shimmer under the Gujarat sun, you see the physical manifestation of geological time meeting human ambition. The bromine being extracted today was concentrated over millions of years, yet serves industries that didn't exist a generation ago. It's temporal arbitrage at its most elegant.

India's role in global chemical supply chains is evolving rapidly. The country offers not just cost advantages but increasingly sophisticated capabilities. Archean exemplifies this evolution—from basic extraction to complex derivatives to cutting-edge semiconductors. It's a progression that mirrors India's own industrial journey.

The sustainability questions facing resource extraction businesses are real and intensifying. How do you balance economic development with environmental protection? How do you ensure resource extraction benefits local communities? Archean's solar evaporation process and integrated production offer partial answers, but the questions will only grow more pressing.

ESG considerations are reshaping how markets value resource companies. The old model of extract-and-export is giving way to more nuanced approaches that consider total impact. Companies that can demonstrate sustainable practices, circular economy principles, and positive community impact will command valuation premiums. Archean's story here is still being written.

If we were management, the strategic priorities would be clear. First, maintain the core business moat through continuous operational improvement. Second, execute flawlessly on the derivatives expansion—this is the near-term value driver. Third, approach semiconductors with milestone-based investment, preserving the option to pivot if needed. Fourth, diversify the customer base gradually without sacrificing economics. Fifth, prepare for the next cycle—both up and down.

The key takeaways for investors and entrepreneurs are multilayered. Resource advantages are real but must be paired with operational excellence to create value. Customer concentration in B2B markets is manageable if relationships are deep and switching costs are high. Diversification should leverage core competencies rather than abandon them. Patient capital and long-term thinking remain competitive advantages in an increasingly short-term world.

The unexpected journey from salt marshes to semiconductors reminds us that corporate evolution is rarely linear. Companies, like the elements they work with, can transform under the right conditions. Archean's story—still being written—suggests that in the intersection of ancient resources and modern technology lies opportunity for those willing to see it.

As global supply chains reconfigure, as technology advances, as new applications for old materials emerge, companies like Archean will play crucial but often invisible roles. The bromine in your electronics, the salt in industrial processes, perhaps someday the silicon carbide in your electric vehicle—all connecting ancient seas to modern life.

The next chapter of this story depends on execution, market conditions, and some luck. But the foundation—geological advantage, operational excellence, strategic vision—appears solid. For investors, entrepreneurs, and students of business, Archean offers lessons in building lasting value from finite resources. In a world increasingly concerned with sustainability and supply chain resilience, these lessons matter more than ever.

The transformation continues. From ancient seas to modern industry, from commodity to specialty, from chemicals to semiconductors—Archean's journey reflects broader transitions in global industry. Where it goes from here will depend on how well it navigates the tensions between stability and growth, between focus and diversification, between serving today's customers and creating tomorrow's markets.

In the end, Archean Chemical Industries is more than a company extracting minerals from salt marshes. It's a case study in industrial evolution, a testament to the value of patient capital, and a reminder that competitive advantage often lies not in what you do but in how and where you do it. The white expanse of the Rann of Kutch holds more than just chemicals—it holds lessons for anyone seeking to build enduring value in an ever-changing world.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube