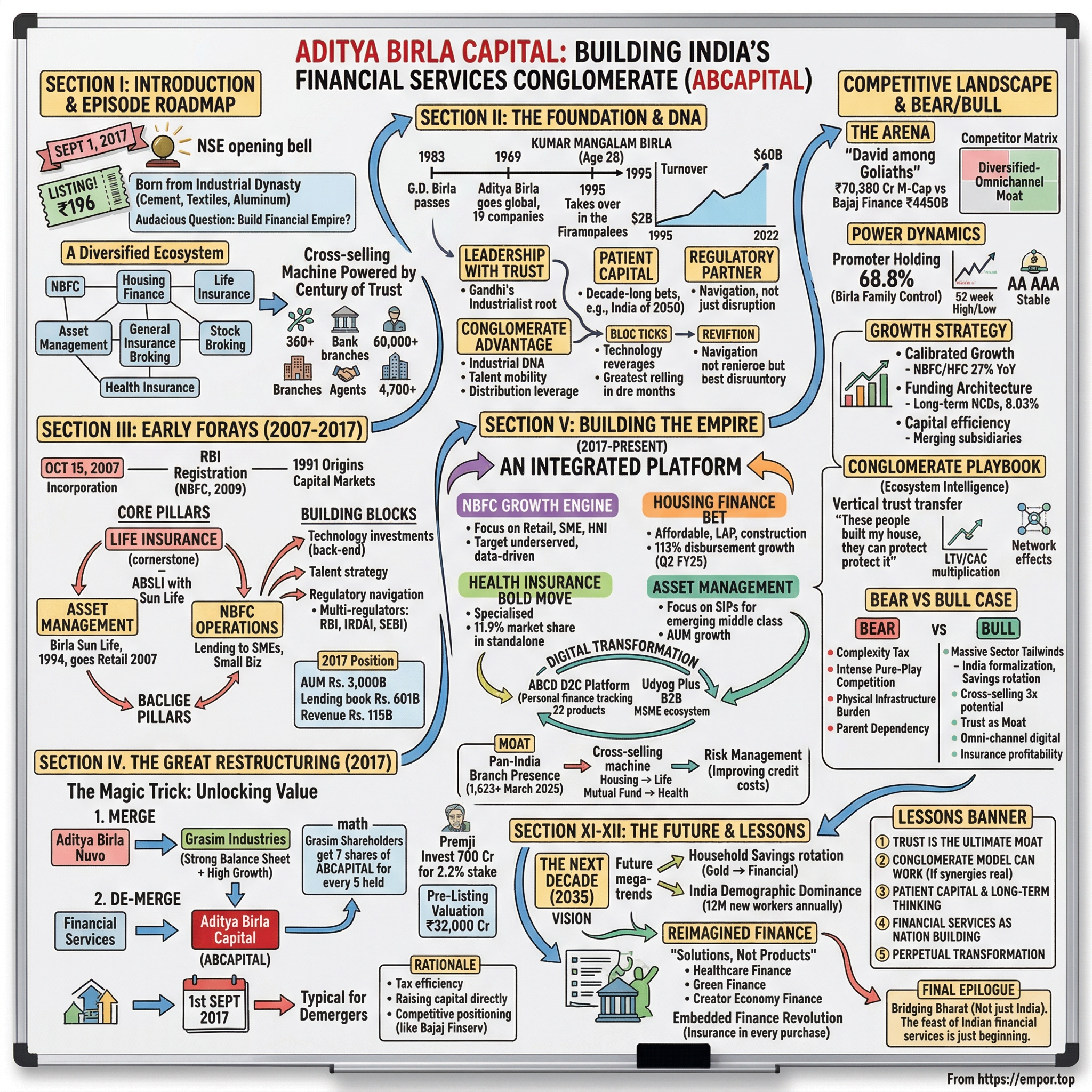

Aditya Birla Capital: From Holding Company to Operating Giant

I. Introduction & Episode Roadmap

On the afternoon of August 10, 2026, a share of Aditya Birla Capital changed hands on the National Stock Exchange at ₹407.75, valuing the company at roughly ₹1.12 lakh crore.1 Twelve months earlier, the same share had traded as low as ₹267.1 The stock has gained about 50% over that stretch, and it now sits within striking distance of its 52-week high of ₹430.70 on a trailing earnings multiple of roughly 26 times.1

Numbers like that usually mean one of two things in Indian financial services. Either a company has discovered a new growth engine, or the market has decided it was structurally mispriced and has corrected the error. Aditya Birla Capital is an unusual case, because both happened at once — and the second one happened because a regulator forced it.

Start with what the company actually is today, because it is not what it was two years ago. Aditya Birla Capital Limited — ABCL to the filings, ABC in conversation — is a listed, systemically important, non-deposit-taking NBFC.2 Not a holding company that owns an NBFC. The lending business is the parent. As of June 30, 2026, its own balance sheet carried a lending portfolio of ₹2,19,289 crore, up 32% year on year, split between a diversified NBFC book of ₹1,67,456 crore and a housing finance subsidiary at ₹51,833 crore.3 Bolted onto that lender are stakes in a listed asset manager, a life insurance joint venture with a Canadian partner, a health insurance joint venture with a South African partner and an Abu Dhabi sovereign fund alongside, a stockbroker, and an insurance brokerage. Combined assets under management across asset management, life insurance and health insurance reached ₹7,52,745 crore in the June 2026 quarter, up 36%.3 The company employs over 66,500 people across more than 1,740 branches.2

The transformation that produced this shape was not the product of a bold strategic vision presented at an investor day. It was the product of RBI Master Directions. In 2023 the Reserve Bank classified Aditya Birla Finance Limited — the group's core lending entity — as an "upper layer" NBFC under its Scale Based Regulation framework, which carried a hard obligation: list on a stock exchange by September 30, 2025.4 The group had two options. Float Aditya Birla Finance separately, creating yet another listed entity inside an already-complicated structure. Or merge it upward into the already-listed parent and let the parent become the lender.

They chose the merger. It took effect on April 1, 2025.5 And in one legal stroke, the holding-company discount that had shadowed the stock since its 2017 listing largely stopped applying, because there was no longer a holding company to discount.

That is the central question this story has to answer honestly. A re-rating driven by structural simplification is real but finite — you can only delete a holdco once. What comes after has to be earned operationally. So: has Aditya Birla Capital actually become a better lender, or just a more legible one? Can a mid-scale, multi-license financial conglomerate out-execute Bajaj Finance, the newly listed Tata Capital, and a banking system that is aggressively pushing into the same retail and MSME credit pools?

The arc runs like this. A financial services arm assembled quietly inside a textiles-and-telecom conglomerate through the 2000s. A 2017 demerger that set it free and immediately taught it a lesson about how markets price conglomerates. A 2021 asset management IPO that proved the parts were worth more than the whole. A 2022 leadership reset under a career ICICI banker. A 2025 regulatory merger that changed the company's legal identity. And now, a growth sprint funded, notably, by repeated infusions of outside capital rather than by retained earnings.

That last detail is where the skeptics live. Let's get to it properly.

II. The Aditya Birla Group Scaffolding

Every Indian business group has a founding myth, and most of them are about a patriarch. The Aditya Birla Group's most consequential moment was about a son who did not expect the job.

Kumar Mangalam Birla was 28 years old in 1995 when his father Aditya Vikram Birla died, and he inherited the chairmanship of a sprawling commodity-heavy conglomerate. He was a chartered accountant with a London Business School MBA — trained in numbers, not in the deal-making swagger of the licence-raj generation. What followed over the next three decades was a systematic reshaping: aggressive consolidation in cement, a leap into telecom, a retreat from businesses that could not earn their cost of capital, and — quietly, without much fanfare — the assembly of a financial services platform.

The group's stated operating philosophy is "Leadership with Trust," and in most conglomerate contexts that phrase would be corporate wallpaper. In financial services it is closer to an actual input. When a customer buys a 20-year life insurance policy or hands over retirement savings to a mutual fund, they are making a bet that the institution will still exist and still behave well in 2046. A 150-year-old industrial name is a genuine, if unquantifiable, asset in that transaction. Birla himself framed the sector in those terms at the 2017 listing: "The financial services sector is a key driver for the India growth story and is core to the Group's strategy."6

The mechanically important entity in this story, though, is not the group. It is Grasim Industries.

Grasim is the promoter vehicle that holds Aditya Birla Capital, and it is itself listed. That creates a specific and unusual capital structure: a listed company (Grasim) whose largest single asset by some measures is its controlling stake in another listed company (ABC), which in turn controls a third listed company (Aditya Birla Sun Life AMC). Three layers of public market pricing stacked on top of each other. If that sounds like exactly the kind of arrangement that produces valuation leakage, it is — and much of the last decade of corporate action at ABC has been about managing that leakage.

But the structure has a compensating benefit that showed up vividly in 2026. When Aditya Birla Capital needed growth equity to fund its lending sprint, it did not have to go to the open market and take whatever price was on offer. It went to Grasim. In a preferential allotment completed on June 23, 2026, Grasim subscribed to 8,08,94,331 equity shares at ₹356.02 apiece for ₹2,879.99 crore.7 The promoter effectively underwrote the company's growth capital.

Whether an investor reads that as patient strategic capital or as a captive backstop that lets management avoid market discipline is one of the genuine forks in this story. It is a real advantage — very few Indian NBFCs of this size can call a parent and get ₹2,880 crore. It is also a mechanism by which a company can keep growing its balance sheet without ever proving it can fund that growth from its own profits. Both readings are defensible on the current evidence, and the article will return to the question with numbers attached.

For now, hold one thought: the group scaffolding gave Aditya Birla Capital brand permission and a capital backstop. What it could not give was scale in lending. That had to be built.

III. Founding to Demerger: Building the Financial Supermarket (2007–2017)

The company that trades today as ABCAPITAL was incorporated on October 15, 2007 under a name almost nobody remembers: Aditya Birla Financial Services Private Limited.8 It was a corporate wrapper, not a business — a place to park the group's growing collection of financial licences.

The licences came in a burst characteristic of Indian financial services in the 2000s, when the sector was still opening up and partnering with a foreign institution was the standard route to expertise. The asset management and life insurance businesses were built as joint ventures with Sun Life Financial of Canada, an insurer with roots going back to the 1860s and no meaningful India presence of its own. The trade was legible on both sides: Sun Life brought actuarial and investment discipline, the Birlas brought distribution, brand, and the ability to navigate Indian regulation. Neither could have done it alone at that point.

On May 19, 2009, the entity received its certificate of registration from the Reserve Bank of India to operate as a non-deposit-taking NBFC.8 That is the legal birthday of the lending business. On December 4, 2014, it converted from a private to a public limited company and was renamed Aditya Birla Financial Services Limited — a step frequently misremembered as a stock market listing.8 It was not. The company remained wholly inside the group, sitting under Aditya Birla Nuvo, the conglomerate's designated incubator for new businesses.

And that placement was the problem.

Aditya Birla Nuvo was one of the strangest listed entities in India: a company that simultaneously made textiles and viscose filament yarn, manufactured fertilisers and insulators, sold branded apparel, ran a telecom stake, and — increasingly — housed a fast-growing financial services platform. Public market investors do not know how to price that. A viscose yarn business deserves a mid-single-digit multiple in a cyclical trough. A life insurance business compounding embedded value deserves something entirely different. Put them in one entity and the market splits the difference badly, usually to the disadvantage of the growth asset.

The resolution came in 2017 and it was structurally elegant. Aditya Birla Nuvo was amalgamated into Grasim Industries, the group's larger and more stable industrial vehicle, with the combined entity carrying proforma FY2015-16 turnover of ₹59,766 crore, EBITDA of ₹11,961 crore and net profit of ₹4,245 crore.9 Birla's framing at the time was about balance sheet strength meeting growth potential.9 But the financial services business was not folded in. It was carved out and demerged into a separately listed company, rechristened Aditya Birla Capital Limited in June 2017.8

On September 1, 2017, ABCL's shares opened for trading at ₹250, implying a market capitalisation of over ₹55,000 crore.6 It was, at that moment, a genuinely substantial financial services platform: aggregate assets under management of ₹2.6 lakh crore, a lending book of over ₹41,000 crore, 12,500 employees, more than 1,300 points of presence, over 150,000 agents and channel partners, and 13.5 million customers.6 Ajay Srinivasan, the CEO who had built much of it, described the ambition as providing "Universal Financial Solutions to meet our customers' money needs for life."6

The strategic logic was clean. Escape the conglomerate discount buried inside Nuvo. Give the market a pure-play financial services vehicle it could price on its own merits. Unlock value.

Here is the uncomfortable postscript, and it matters for everything that follows: it did not work. The market cap at listing — over ₹55,000 crore — was not exceeded on a durable basis for years. Investors had traded one discount for another. Instead of "financial services trapped inside a textiles company," they now owned "an operating-lender-plus-insurance-plus-AMC portfolio trapped inside a Core Investment Company that could not itself deploy capital efficiently."

The 2017 demerger solved the wrong problem. It took the group eight more years, and a regulatory mandate, to solve the right one. In the meantime, management found a different lever entirely: if the market would not pay up for the whole, perhaps it would pay up for the parts.

IV. Unlocking Value Inside the Group: Selling Down the Subsidiaries (2017–2022)

In late September 2021, Indian equity markets were in the middle of one of the great retail participation booms in the country's history. Demat accounts were opening at a pace nobody had modelled. Mutual fund SIPs were becoming a middle-class default. And into that window, Aditya Birla Capital walked its asset management business onto the exchanges.

The Aditya Birla Sun Life AMC IPO opened on September 29, 2021 and closed on October 1, priced in a band of ₹695–712 per share and raising ₹2,768.26 crore.10 It was subscribed 5.25 times.10 Critically, the entire issue was an offer for sale — 3.88 crore shares sold by the existing shareholders, with the overwhelming majority coming from Sun Life's holding rather than ABC's.10 No new money went into the asset manager. The shares listed on October 11, 2021 at ₹715, a whisper above the offer price.10

The muted listing pop obscured what actually happened. For the first time, a piece of Aditya Birla Capital had a public price of its own. And that price told a story the parent's own multiple had been suppressing: asset management, being a capital-light annuity on India's savings pool, deserved a materially richer valuation than a lending-heavy conglomerate. Aditya Birla Sun Life AMC today carries a market capitalisation of roughly ₹29,000 crore as a standalone listed entity — a discrete, market-priced line item that any analyst can drop into a sum-of-the-parts model without argument.11

Ten months later, the group ran a variation of the same play, this time in private markets and this time for cash into the business.

In August 2022, the Abu Dhabi Investment Authority — one of the world's largest sovereign wealth funds, and an institution with a long history of quiet, patient minority positions in Indian financial services — agreed to invest ₹665 crore in Aditya Birla Health Insurance for a 9.99% stake.12 The transaction valued the health insurer at ₹6,650 crore. Post-deal, Aditya Birla Capital's holding stood at 45.91% and joint venture partner Momentum Metropolitan of South Africa held 44.1%.12 The capital was earmarked for growth in what was then a small but fast-scaling business.

Look at these two transactions side by side and a repeatable corporate playbook emerges. Aditya Birla Capital does not typically fund the growth of a subsidiary entirely from the parent balance sheet. It brings in a partner — Sun Life in asset management and life insurance, Momentum Metropolitan and then ADIA in health, and later Advent International in housing finance and the International Finance Corporation at the parent. Each transaction does three things simultaneously: it injects growth capital, it establishes an external valuation benchmark for an asset the market was previously valuing at zero or a discount, and it transfers some execution risk to a co-investor with skin in the game.

That is genuinely sophisticated capital recycling, and it is the single most consistent behaviour management has displayed across two decades.

But the same pattern supports a much less flattering reading, and an honest analysis has to hold both. A business that must repeatedly sell equity in its best assets to fund their growth is telling you something about its own internal capital generation. Bajaj Finance did not sell down stakes in its subsidiaries to fund a decade of compounding; it funded growth from retained earnings and a return on equity high enough to self-sustain. Aditya Birla Capital's willingness to dilute is either discipline — recycling capital to its highest-return use — or necessity dressed as discipline.

By 2022, that question had become urgent. The lending business was sub-scale relative to its ambitions. The insurance businesses were consuming capital. The digital front-end barely existed. And the group brought in someone from outside to fix it.

V. The Vishakha Mulye Reset: "One ABC, One P&L"

Vishakha Mulye spent most of her career inside one institution, and it was the institution that essentially invented modern Indian private-sector banking. At the ICICI Group she served as Executive Director on the board of ICICI Bank, as Group Chief Financial Officer, and as Managing Director and CEO of ICICI Venture Funds Management.13 That is an unusually complete résumé: she has run a P&L, sat on the balance sheet side as CFO, and managed third-party capital in private equity. She has been named Economic Times Businesswoman of the Year and has appeared on Forbes Asia's Power Businesswomen list.13

When Mulye joined Aditya Birla Capital in 2022 as Executive Director, she inherited an organisation that looked, from the customer's side, like a collection of separate companies that happened to share a logo. A person with an Aditya Birla Sun Life mutual fund, an Aditya Birla home loan, and an Aditya Birla health policy was, internally, three unrelated customers sitting in three unconnected systems, each contributing to a business-unit P&L that a different executive was measured on. Every siloed conglomerate in the world looks like this. Very few fix it, because fixing it requires taking revenue attribution away from the people who currently own it.

Mulye's answer was branded "One ABC, One P&L," built on three stated principles: One Customer, One Experience, One Team.13 Stripped of the slogan, it is a plan to make the group's most plausible competitive advantage — owning multiple financial products the same household needs — actually show up as economics rather than as an org chart.

Two products carry the operational weight of that idea.

The first is ABCD, a direct-to-consumer omnichannel app that aggregates the group's offerings in one place. By the June 2026 quarter, ABCD had accumulated about 1.2 crore customer acquisitions and carried 26-plus products.3 For context on the trajectory, the same platform reported roughly 64 lakh customer acquisitions a year earlier.14 Roughly doubling a customer base in twelve months is real traction; what remains undisclosed is the thing that would actually validate the thesis — what those customers cost to acquire, how many hold more than one product, and what they contribute in revenue.

The second is Udyog Plus, a B2B digital platform for MSME credit. It reached over 24 lakh registrations and ₹6,229 crore of AUM by the June 2026 quarter, having nearly doubled in scale over FY26 and crossed ₹5,000 crore during that year.3 Rakesh Singh, the NBFC chief executive, told analysts that the platform now supports a full suite of digitally powered trade credit solutions and ranks among the top non-bank financiers on India's TReDS invoice discounting exchanges.15 This is the more interesting of the two, because MSME credit is where distribution and underwriting skill actually compound, and where a digital origination channel meaningfully lowers the cost of finding borrowers.

Mulye was elevated to Managing Director and CEO effective September 1, 2025, for a five-year term running through August 31, 2030.13 Alongside her, Rakesh Singh was appointed Executive Director and CEO of the NBFC business — the executive with direct accountability for the lending growth target that now defines the equity story.5

The early operating evidence is genuinely favourable, with one important caveat about what the numbers mean. The housing finance business improved its return on assets by 63 basis points year on year to 2.07% in the fourth quarter of FY26, and the NBFC business reached a return on assets of 2.31%.15 Both are respectable for their categories. Neither is yet at the level of the scaled leaders in Indian non-bank lending.

The AI narrative deserves more scrutiny than it usually receives. Mulye told the FY26 fourth-quarter call that "AI is now becoming a core operating layer for us," scaling across underwriting, sales, voice calling, audit and compliance, customer service and operations.15 Her business heads then supplied unusually specific evidence rather than the customary vagueness: roughly 65% of contact-centre calls and 71% of service emails were straight-through processed by the end of FY26; the health insurance business processes more than 25% of pre-authorisation requests with no human involvement and reported a 35–40% productivity improvement in underwriting from generative AI; the housing finance business cut turnaround times from 21 days to 12.15

Specific claims are more falsifiable than vague ones, which is a point in management's favour. But note carefully what none of these disclosures include: a rupee figure for cost saved. When an analyst on that call asked directly whether AI would moderate operating expenses further, Rakesh Singh's answer stayed on qualitative ground — turnaround times, Net Promoter Scores, self-cure rates in collections — before landing on "we will see what efficiency we can draw on this line as well."15 That is not evasion, exactly. It is a leader declining to promise a number he cannot yet defend. Investors should treat the AI efficiency thesis as plausible and unproven, and should watch operating expense growth against AUM growth as the actual test.

Because on that specific test, the recent record is not clean — and it became the sharpest exchange of the year on an earnings call. First, though, the event that reset the whole company.

VI. The 2025 Structural Reset: Merging Away the Holding Company

Regulatory frameworks rarely produce good business stories. This one did, because it forced a decision the group had been deferring for years.

In October 2021, the Reserve Bank of India introduced Scale Based Regulation for non-banking financial companies — a framework that sorted NBFCs into base, middle, upper and top layers according to size, complexity and systemic interconnectedness. The logic was straightforward and, after the IL&FS and DHFL failures, uncontroversial: an NBFC with a lending book the size of a mid-tier bank should face something closer to bank-like scrutiny. Entities placed in the upper layer picked up a specific obligation — mandatory listing on a stock exchange within three years of designation.4

Aditya Birla Finance Limited was named to the upper layer in September 2023, which set its listing deadline at September 30, 2025.16 Tata Capital, designated a year earlier, faced the same requirement.17

Now consider the board's actual choice set. Option one: take ABFL public through an IPO, exactly as Tata Capital ultimately did. This satisfies the regulator and crystallises a market value for the lending business. It also creates a listed operating company sitting beneath a listed holding company sitting beneath a listed industrial parent — three tiers of public equity, minority shareholders at two levels, and a permanent structural discount at the top.

Option two: merge ABFL upward into the already-listed parent. The parent is already on the exchanges, so the listing obligation is satisfied by definition. And in the process, the holding company simply ceases to exist as a separate layer.

They took option two, and the mechanics of the approval process show why these things take years. The Reserve Bank granted its no-objection to the scheme of amalgamation in September 2024.18 SEBI and the stock exchanges signed off. Shareholders and creditors approved. The National Company Law Tribunal's Ahmedabad bench issued its order on March 24, 2025, and the amalgamation became effective on April 1, 2025.5

What changed on that date was the company's legal identity. Aditya Birla Capital had been a Core Investment Company — a regulatory category for entities whose business is holding stakes in group companies. A CIC cannot lend meaningfully on its own account; it is a passive vehicle with severe constraints on how it deploys its balance sheet. After April 1, 2025, ABCL was an operating NBFC that lends directly.5

The financial consequence was concrete rather than cosmetic. On a pre-merger basis, ABCL's structure implied leverage of roughly 5.9 times; consolidating the lender into the parent brought projected leverage to approximately 4.15 times, a meaningful improvement in capital adequacy headroom.19 In plain terms: capital that had been sitting at the holding-company level, doing nothing except being counted twice in a sum-of-the-parts calculation, became capital the lending business could actually leverage. The transaction issued no new shares and changed no shareholder's proportionate ownership.19 Existing owners simply woke up owning a different kind of company.

At the time of the merger, the combined entity had aggregate AUM of over ₹5.03 lakh crore, a consolidated lending book of over ₹1.46 lakh crore, and a distribution network of 1,482 branches with more than 200,000 agents and channel partners.5 For the first nine months of FY25 it had recorded consolidated revenue of ₹28,376 crore and profit after tax of ₹2,468 crore.5 Birla's framing was about acceleration and financial inclusion; Mulye's was more precise and more revealing — the unified entity, she said, "now has better capital access to drive synergies and stakeholder value creation."5 Capital access was the point.

Myth vs reality: did the merger create value, or just relabel it?

The consensus narrative on this transaction is that it "unlocked" value by removing the holding company discount. That is half right, and the half that is wrong matters.

Nothing about the underlying businesses changed on April 1, 2025. The same loans, the same insurance policies, the same mutual funds. What changed was the packaging and the leverage capacity. So the re-rating is best understood as two distinct components: a one-time, non-repeatable elimination of a structural discount, and a durable improvement in the company's ability to deploy capital into lending. The first is finished and cannot happen twice. The second is real but only converts into shareholder value if the incremental lending earns a return above its cost of capital.

The useful benchmark arrived six months later, when Tata Capital took the road not travelled. Its IPO ran October 6–8, 2025, raising approximately ₹15,500 crore at ₹326 per share, with listing on October 13.17 Tata Capital entered public markets with an FY25 loan book of ₹2,21,950 crore, net profit of ₹3,655 crore, gross NPAs of 1.9% and a return on equity of 12.6%.17 That is a loan book almost identical in size to Aditya Birla Capital's today — which makes it the cleanest possible read-across for anyone trying to judge whether ABC's operating-company multiple is generous or conservative. Two comparable-scale Indian NBFCs, both pushed onto the exchanges by the same rule, arriving via opposite routes.

The structural work is done. From here the story stops being about corporate architecture and starts being about credit.

VII. Segment Deep Dive: Lending — NBFC & Housing Finance, the Core Profit Engine

Somewhere in the second half of the June 2026 quarter, Aditya Birla Capital's lending book crossed a threshold that would have seemed implausible a decade ago, when the entire platform lent ₹41,000 crore. The combined NBFC and housing finance portfolio reached ₹2,19,289 crore, up 32% year on year and 6% sequentially.3 The housing finance book crossed ₹50,000 crore for the first time.3

This is now the engine. Everything else in the group is either a minority-owned stake, a capital-consuming growth bet, or a distribution accessory. The lending business is where the profit and the risk both live.

The NBFC book: MSME-led, mostly secured, and priced accordingly

Rakesh Singh's franchise ended FY26 with AUM of ₹1,59,916 crore, up 27%, having crossed ₹1.5 lakh crore in February 2026 with retail and MSME assets alone passing ₹1 lakh crore.15 Full-year disbursements grew 25%, with retail and MSME accounting for 68% of the total and growing 33%.15 The MSME book specifically reached ₹91,451 crore, up 31%, and now represents 57% of overall AUM — 81% of it secured.15

That mix is the whole argument. About 72% of the NBFC book is secured, and Singh was explicit on the FY26 fourth-quarter call about the nature of that security: collateral "which is not depreciating in nature, which is appreciating in nature, majority backed by real estate collateral, primarily the MSME owners, self-occupied residences, offices."15 Lending against an owner-occupied property to a business owner who has a cash-flow reason to protect it is a structurally different risk from unsecured consumption credit, and it is the reason the book's credit costs have behaved well.

And they have behaved well. Full-year FY26 credit cost came in at 1.18%, thirteen basis points better than the prior year and below the guided range of 1.2–1.3%.15 Fourth-quarter credit cost of 1.04% was, by Singh's account, the lowest in five years. Combined Stage 2 and Stage 3 assets stood at 2.4%, improving 136 basis points year on year, with provision coverage of 47.8%.15 By the June 2026 quarter, gross Stage 3 had fallen to 1.30%, a 97-basis-point improvement.3

Delivering better than guided credit cost while growing 27% is not a trivial achievement, and it deserves to be stated plainly: on asset quality, this management team has under-promised and over-delivered across FY26. That is the single strongest piece of evidence in their favour.

Profitability follows. Net interest income rose 18% to ₹8,170 crore in FY26, net interest margin including fees ran at 6.08% in the fourth quarter, and full-year profit grew 20% to ₹3,001 crore.15 In the June 2026 quarter, NBFC profit before tax reached ₹1,222 crore, up 32%, with return on assets of 2.39%.3

Where the analysts pushed back

Earnings calls are useful precisely because the prepared remarks and the Q&A tell different stories. On the FY26 fourth-quarter call, three separate analysts pressed on the same soft spot from different angles.

Chintan Shah of ICICI Securities opened by noting that NBFC margins had compressed about four basis points sequentially despite strong growth in higher-yielding unsecured lending — a combination that ought to have pushed margins up, not down.15 Singh's response was that quarter-four margin was affected by mark-to-market losses on government securities, and that the real lever is mix: unsecured business loans plus personal and consumer lending together sit at 23.4% of the portfolio, and every 200 basis points of increase in that mix should add 25–30 basis points to margin.15 Pressed on where that leads, he committed to a specific number: "We are looking at 2.5% ROA by the end of this year."15

Then Arun Antony of JM Financial asked the question that actually matters. Operating expense growth, he observed, had "sharply outpaced the AUM growth and this is for the last three quarters as well." Why?15

Singh's answer, in full, was that the company has been investing in retail and MSME businesses over the last few years and quarters, that "there will be some normalization which will happen," and — the phrase worth writing down — "There's no specific reason for sharp rise in this quarter."15

That is a thin answer to a well-constructed question, and it stands in noticeable contrast to the granularity management brought to every asset-quality question on the same call. It is not a scandal. Operating expenses running ahead of AUM during a branch-and-technology build-out is a defensible pattern, and the absolute level is respectable — opex to AUM was 1.93% for FY26.15 But three consecutive quarters of a trend that management cannot attribute to a specific driver is the kind of thing that becomes a problem in reverse, when growth slows and the cost base does not. Investors should hold management to the promised normalisation.

Housing finance: the fastest-growing and the least seasoned

Aditya Birla Housing Finance, run by Pankaj Gadgil, had the more dramatic year. FY26 disbursements hit a record ₹25,332 crore, up 44%, and AUM reached ₹47,452 crore, up 53% — with profit before tax nearly doubling to ₹832 crore.15 Return on assets of 1.88% and return on equity of 14.27% for the year, with combined Stage 2 and 3 at 0.76%, improving 63 basis points.15 By the June 2026 quarter, AUM had reached ₹51,833 crore, up 50%, with profit before tax up 95% and gross Stage 3 at a remarkable 0.41%.3

Gadgil's operating story is a digital transformation begun in FY23 that he says delivered four times the processing capacity, a 96% productivity improvement, turnaround time down from 21 days to 12, and Stage 2 plus 3 improving from 4.99% in FY23 to 0.76% in FY26.15 He also delivered ahead of his own guidance: the target set at the start of FY26 was a return on assets of 2.0–2.2% "over the next 6–8 quarters," and the business hit 2.07% in the fourth quarter of FY26.15

Here is the analytical caution, and it is not a criticism of anyone's underwriting. A loan book growing at 50% is, by definition, a book in which the majority of loans are young. Mortgages do not default in year one; they default in years three through seven, typically after a job loss, a business reversal, or a property price correction. A 0.41% gross Stage 3 ratio on a book that has more than doubled in two years tells you far less about credit quality than the same ratio on a static book would. This is arithmetic, not skepticism — and Gadgil's own Stage 2 disclosure is the honest tell: of the 76 basis points of Stage 2 plus 3, 44 basis points is Stage 3 and 32 basis points is Stage 2, which he cited as giving "a lot of confidence that the credit cost will be normalized."15 The seasoning test arrives in FY28 and FY29, not now.

Management is planning to grow straight through it. The plan for FY27 includes opening 100-plus branches, concentrated in Tier 2 and Tier 3 markets, in service of a target of ₹1 lakh crore of housing AUM within 24 to 30 months.15 Guidance for FY27 is a return on assets of 2.10–2.15%, with return on equity temporarily depressed to 11.5–12% because of the new capital, before crossing 15% over 12 to 24 months as leverage rebuilds.15

That new capital came from a familiar playbook. On February 3, 2026, Advent International agreed to invest ₹2,750 crore into Aditya Birla Housing Finance for approximately 14.3%, valuing the business at ₹19,250 crore post-money, with Aditya Birla Capital retaining about 85.7%.20 Advent's Shweta Jalan pointed to structural tailwinds in India's mortgage market; Mulye described a "full-stack housing finance franchise with a strong focus on prime and affordable segments."20 The deal closed in April 2026 after regulatory approvals.15

The AMC precedent hangs over this transaction. Bring in a partner, establish a valuation, scale the business, then list it. Nothing has been announced, and investors should not assume it. But a private equity firm that has bought 14.3% of a housing finance company at ₹19,250 crore has an exit to think about, and there are only so many ways to get one.

The competitive reality

Aditya Birla Capital's ₹1.12 lakh crore market capitalisation sits against Bajaj Finance at roughly ₹6.7–6.9 lakh crore and Bajaj Finserv at approximately ₹3.2 lakh crore.121 Bajaj Finance alone is valued at six times ABC. That gap is not a mispricing to be arbitraged; it reflects two decades of compounding at returns on equity that Aditya Birla Capital has not yet demonstrated, on a deposit and distribution franchise built earlier.

The more instructive comparison remains Tata Capital, at almost identical loan book scale with an FY25 return on equity of 12.6%.17 And behind both sit the banks — which fund themselves with current and savings account deposits at a structurally lower cost than any wholesale-funded NBFC can achieve, and which have spent the last three years pushing hard into exactly the retail and MSME segments where ABC is growing fastest.

So where does Aditya Birla Capital actually win? Two places, on current evidence. First, secured MSME lending against appreciating collateral, where the credit cost data genuinely supports the claim of superior underwriting — Singh's assertion that "our credit costs have been one of the lowest among diversified NBFCs" is backed by a 1.18% full-year number against a 1.2–1.3% guide.15 Second, funding cost: Singh described the company as having "one of the best cost of borrowing," a direct benefit of the Aditya Birla name and the group's credit standing.15

Where it loses is on scale-driven operating leverage, on deposit access it does not have, and on the fact that it is still buying growth with equity rather than generating it.

Lending is where the money is made. Protection is where the optionality — and the ongoing capital consumption — sits.

VIII. Segment Deep Dive: Protection — Life & Health Insurance

The insurance sector spent FY26 absorbing more regulatory change than it had in a decade. Mayank Bathwal, who runs the health insurance business, listed them for analysts almost as a weather report: "reduction of GST to nil rate, new Insurance Act, new Labour Code, and the latest being transition to IFRS reporting from FY27."15 His verdict — supportive of long-term growth, messy in the short term — is the correct frame for reading both insurance businesses right now.

Life insurance: a margin story finally working

Aditya Birla Sun Life Insurance, the joint venture with Sun Life Financial, is run by Kamlesh Rao, and FY26 was the year its economics turned.

The headline is value of new business margin — the metric that measures how much economic value a life insurer creates on each rupee of new premium, and the closest thing the industry has to a gross margin. ABSLI's expanded 260 basis points year on year to 20.6% in FY26.15 Rao attributed the improvement to a deliberate shift in product mix: traditional business including protection rose to 67% of individual sales while ULIPs fell to 33%, alongside healthy rider attachment and a favourable interest rate environment.15

The mechanism is worth explaining in plain terms. A unit-linked insurance plan is essentially a mutual fund in an insurance wrapper — the customer takes the investment risk and the insurer earns a thin fee. A traditional protection or guaranteed-return product is a genuine risk transfer, where the insurer earns a spread for taking mortality and interest rate risk. Protection is more profitable and far more capital-intensive. Shifting mix toward it is the single most reliable way for an Indian life insurer to expand margin, and it requires distribution partners willing to sell harder products.

Which brings up the real asset. ABSLI now has 12 bancassurance tie-ups, and partnership business grew 23% in FY26 across every one of them.15 The Axis Bank relationship is the standout: the insurer started FY26 with access to roughly 20–25% of the bank's insurance business and expects to reach "close to about 50%" — the kind of shelf-space expansion that is nearly impossible to buy and difficult for a competitor to reverse.15

Supporting metrics: total premium of ₹24,779 crore in FY26, up 20%; 13th-month persistency of 86.1%; embedded value of ₹15,447 crore growing 12% with a 13.2% return on embedded value; solvency at 178%; customer NPS improving from 59 to 66; total AUM of ₹1,10,505 crore.15 Rao's guidance is 20%-plus individual first-year premium CAGR over three years, VNB margins held in the 18–20% band, and absolute net VNB doubled in three years.15

In the June 2026 quarter, individual first-year premium grew 20% to ₹952 crore, group new business jumped 74% to ₹1,281 crore, and absolute VNB rose 153% to ₹167 crore on a quarterly VNB margin of 15.1%.3 The lower quarterly margin against the 20.6% full-year figure reflects the pronounced seasonality of Indian life insurance, where the fourth quarter carries the profitable tax-season business — but it is worth watching whether the group business surge, which grew far faster than individual, dilutes the mix.

One accounting judgment deserves flagging. Asked about a negative operating variance and assumption change in the embedded value bridge, Rao explained that the company is preparing to shift from Indian GAAP to IFRS and has "revisited some of our assumptions," including on reduced paid-up benefits — and disclosed that ABSLI has "asked for a forbearance to say we will go to IFRS in financial year 2027."15 Voluntarily building in conservatism ahead of an accounting regime change is defensible, arguably prudent. It also means reported embedded value movements over the next several quarters will contain a component that is about accounting policy rather than business performance, and investors should read the bridges carefully rather than the headline.

Health insurance: growth is proven, profitability is not

Aditya Birla Health Insurance is the fastest-growing thing in the group and the one that most clearly has not yet earned its keep.

FY26 gross written premium reached ₹7,292 crore under the previous accounting convention, up 39%, lifting the company's share of the standalone health insurer market from 12.6% to 13.7%.15 Retail grew 43%, corporate 35%, on an agent base of over 1.86 lakh.15 In the June 2026 quarter, gross written premium rose 50% to ₹2,196 crore with market share reaching 16.2%.3

Now the profitability picture, which requires care because the accounting changed. Under the old convention, FY26 net profit was ₹85 crore; under the new 1/n framework — which spreads multi-year premium recognition — it was ₹39 crore, including a ₹36 crore GST impact and ₹5 crore from the new labour code.15 The combined ratio, the industry's core underwriting metric, was 102% under old accounting and 103% under the new framework, against 105% on a comparable basis the prior year.15

The combined ratio is the number that decides whether this business is worth anything. It measures claims plus expenses as a percentage of premium. Above 100%, the insurer loses money on underwriting and depends on investment income on float to reach profitability. Below 100%, underwriting itself is profitable and investment income is pure upside. ABHI has moved from 105% to 103% — real, directional progress, and still on the wrong side of the line. In the June 2026 quarter it printed 106%, which is not alarming on its own given seasonality and the growth rate, but does illustrate that the trend is not yet monotonic.3

Bathwal's differentiation claim is a "Health First" model that pays customers for staying healthy, and here the disclosure is better than most. He reported that 11.25% of eligible customers earned Health Returns incentives in FY26, up from 9%, and that these customers exhibit "8%+ lower loss ratios and 11%+ better persistency."15 Separately, targeted interventions with more than 270,000 high-risk lives improved their loss ratios by more than 9%.15

That is the single most credible unit-economics disclosure anywhere in the group's materials, because it links a specific behavioural programme to a specific claims outcome. It is exactly the kind of evidence the "One ABC" cross-sell thesis lacks elsewhere. Bathwal's argument that the model "needs a large investment commitment and persistent efforts over many years to mature" is a reasonable description of a barrier to entry — competitors can copy the marketing, but not five years of claims data on incentivised cohorts.

The caution is that 8% lower loss ratios on 11% of customers moves the aggregate combined ratio by a fraction of a point. It is a real edge operating at a scale too small to be decisive yet. FY27 marks the business's tenth year of operations, and Bathwal has committed to working "towards 100% combined ratio."15

In both insurance businesses, Aditya Birla Capital is a fast-growing mid-tier challenger, not an incumbent. Life competes against HDFC Life, ICICI Prudential Life, SBI Life and Max Life; health against Star Health, Care Health and Niva Bupa. The gap is illustrated by market values: HDFC Life alone carries a market capitalisation of roughly ₹1.17 lakh crore — more than all of Aditya Birla Capital.21 Challengers can win share, and ABHI clearly is. They usually do so by pricing below incumbents, which is precisely why the combined ratio, not the growth rate, is the metric that matters.

The third pillar of the group is the one that needs no capital at all — and is growing the slowest.

IX. Segment Deep Dive: Asset Management, Wealth & Broking

Asset management is the business every financial conglomerate wishes it had more of. It requires almost no balance sheet, it earns a recurring fee on someone else's assets, and its costs are largely fixed while its revenues scale with markets. Aditya Birla Sun Life AMC generated FY26 revenue from operations of ₹1,845 crore against ₹1,685 crore the prior year, operating profit of ₹1,051 crore, and profit after tax of ₹975 crore versus ₹931 crore.15

Read those numbers again. Operating profit is 57% of revenue. Nothing else in the group comes close.

A. Balasubramanian, who has run the asset manager for years, reported overall average AUM including alternates of ₹4.74 lakh crore in FY26, up 17%, with mutual fund quarterly average AUM at ₹4.36 lakh crore, up 14%, and equity AUM at ₹1.97 lakh crore, up 17%.15 SIP contribution reached ₹1,204 crore in March 2026 across 40 lakh contributing accounts, with total investor folios at 1.1 crore.15 Over 75% of equity AUM sat in the top two quartiles for one-year returns.15

The more interesting developments were at the edges. The PMS and AIF business grew from ₹11,300 crore to ₹32,570 crore over the year — though the headline tripling is largely one mandate, with the ESIC allocation accounting for approximately ₹28,400 crore; excluding it, the underlying business grew 14%.15 Management disclosed this decomposition unprompted, which is a small but genuine mark of disclosure quality. A comparable EPFO mandate has been signed and is operationally ready.15 Passive AUM reached ₹41,200 crore, up 25%, with ETF AUM up 68%, and the company incorporated a GIFT City subsidiary with a retail licence.15

Two things temper the enthusiasm.

First, the growth rate is decelerating. Mutual fund AUM grew 14% in FY26; in the June 2026 quarter, quarterly average AUM grew only 6% year on year and individual monthly average AUM grew 3%, with profit up 12% to ₹309 crore.3 Some of that is market-driven, but in a country where the mutual fund industry has been compounding faster, low-single-digit growth in individual AUM is a share loss signal. Aditya Birla Sun Life AMC remains meaningfully behind HDFC AMC, SBI Mutual Fund and ICICI Prudential AMC in industry AUM share, and the June quarter did not narrow that gap.

Second, the ownership structure means Aditya Birla Capital does not capture all of this. Following the 2021 offer for sale, Aditya Birla Capital and Sun Life together retain the large majority of the asset manager, with a public float of roughly 13% created at the IPO.10 The AMC's own market capitalisation of about ₹29,000 crore is separately priced, which is convenient for sum-of-the-parts analysis and inconvenient for anyone hoping ABC's consolidated earnings capture the full economics.11

Stockbroking through Aditya Birla Money and the general insurance broking arm round out the platform. Both are best understood as distribution synergies and customer touchpoints rather than growth pillars — they contribute to the "One ABC" product shelf without moving consolidated earnings materially. Sizing them as anything more would misrepresent the business.

The number that best captures the group's aggregate scale is neither a lending figure nor a fund figure but the combination: total AUM across asset management, life insurance and health insurance reached ₹7,52,745 crore as of June 30, 2026, up 36% year on year.3 Add the ₹2,19,289 crore lending book and Aditya Birla Capital touches close to ₹10 lakh crore of Indian household and corporate financial assets.

Scale of that order raises an obvious question: who is paying for the growth, and on what terms?

X. Capital Allocation, Ownership & Management Credibility

Aditya Birla Capital's shareholder register is one of the most concentrated among large Indian financial companies. As of August 2026, promoter holding stood at 68.81%, with foreign institutional investors at 7.94%, domestic institutions at 4.3% and public shareholders at 9.13%.22 Grasim Industries alone accounts for roughly 52.3% of the company after its June 2026 subscription.7

That concentration cuts both ways, and investors should be clear-eyed about which way it is cutting at any given moment. With less than a third of the equity in public hands, the free float is thin, which amplifies price moves in both directions and makes the stock unusually sensitive to foreign institutional flows. It also means the promoter's preferences, not the market's, determine strategy. When those preferences are good — as the merger decision arguably was — concentration is an asset. When they are not, minority holders have limited recourse.

The 2026 capital raise, examined closely

In the June 2026 quarter, Aditya Birla Capital raised ₹4,000 crore through a preferential allotment. Grasim contributed ₹2,880 crore, the International Finance Corporation — the World Bank's private sector arm — put in ₹920 crore, and Suryaja Investment Pte Limited added ₹200 crore.3 Management allocated 87.5% of the proceeds to NBFC growth and 12.5% to general corporate purposes.323

Grasim's tranche priced at ₹356.02 per share.7 The stock traded at ₹407.75 on August 10, 2026.1 Preferential allotments in India price off a regulated formula based on trailing volume-weighted averages, so a below-market price is normal and not evidence of anything improper. But the arithmetic still matters to a minority shareholder: new equity was issued at a discount to the prevailing market price, and existing holders were diluted at that price. The promoter's proportionate stake moved from 52.27% to 52.30% — essentially unchanged, meaning Grasim participated to hold its position rather than to increase it.7

The IFC participation is the more interesting signal. A multilateral development institution conducting its own due diligence before writing a ₹920 crore cheque is a form of third-party validation that no management presentation can substitute for. It is also, characteristically, another partner brought in rather than capital generated internally.

The credibility scorecard

Assessing a management team means checking what they said against what they delivered, and the FY26 record is genuinely mixed in an informative way.

Delivered ahead of guidance. NBFC credit cost came in at 1.18% for FY26 against a guided range of 1.2–1.3%.15 Housing finance return on assets reached 2.07% in the fourth quarter against guidance given at the start of the year of 2.0–2.2% "over the next 6–8 quarters" — arriving early.15 Housing finance operating expenses to average loan book fell from 2.94% to 2.40%, and management immediately guided to approximately 2.10% for FY27 while simultaneously opening 100-plus branches.15 Setting a tighter target while absorbing an expansion cost is a confident, falsifiable commitment.

Missed or unexplained. NBFC net interest margin did not expand as management had signalled it would; it compressed four basis points sequentially, attributed to mark-to-market losses on government securities.15 More significantly, operating expense growth outpaced AUM growth for three consecutive quarters with no specific driver offered.15 That answer stands out precisely because everything else on that call was answered with granularity.

Narrative consistency. Comparing the FY26 fourth-quarter call against the prior year's materials, the strategic story has been notably stable: retail and MSME focus, secured collateral, digital origination, and — added more recently — AI as an operating layer. There has been no strategy pivot, no quiet abandonment of a prior target, and no rebranding of a failed initiative. In a sector where management narratives often rotate with the credit cycle, that consistency is worth something.

Incentive alignment. The board approved an employee stock option scheme in August 2025.24 Whether it aligns management with shareholders depends on vesting conditions and performance hurdles that are not usefully disclosed in summary form; investors should read the scheme documents rather than the headline.

The activist stress test

What would a skeptical investor attack?

Start with the capital. Over roughly four years, Aditya Birla Capital and its subsidiaries have taken in ₹665 crore from ADIA, ₹2,750 crore from Advent, and ₹4,000 crore in the parent-level preferential issue, alongside the AMC offer for sale. That is a company whose growth has been substantially externally funded. Management would call it capital recycling at attractive valuations. An activist would ask a blunter question: if the lending business genuinely earns a 2.3–2.4% return on assets at 4-times leverage, why can't it fund 25% growth from retained earnings? The honest answer is arithmetic — a book growing at 32% cannot be funded by an ROE in the mid-teens without leverage rising — which means the equity raises are a mathematical consequence of the growth target, not a discretionary choice. The activist's follow-up is therefore the right one: is 25% growth actually the value-maximising choice, or is it growth pursued for its own sake?

Second, portfolio complexity. Aditya Birla Capital still runs lending, life insurance, health insurance, asset management, broking, and insurance broking under one roof, across multiple regulators and multiple joint venture partners with their own agendas. Every one of those partnerships is a negotiation waiting to happen. The 2025 merger simplified the structure meaningfully but did not make it simple.

Third, disclosure gaps. The strategic centrepiece — "One ABC, One P&L" and its cross-sell logic — has been running since 2022 without a single published cross-sell unit economic. No customer acquisition cost. No products-per-customer disclosure. No cross-sell revenue attribution. The housing finance business does disclose that the Aditya Birla Group ecosystem contributed 17.4% of retail disbursements in FY26, which is the closest thing to hard evidence available and is genuinely meaningful.15 One data point in one segment is not a validated thesis.

Fourth, related-party dynamics. Grasim's repeated capital infusions are supportive, but they mean the controlling shareholder is also the marginal price-setter for new equity. Minority shareholders should watch the pricing of future raises carefully.

None of these are red flags. All of them are the questions a serious owner should be asking at every quarterly result.

XI. Competitive & Structural Analysis

Strip away the branding and Indian lending is a commodity business wearing a suit. Money is fungible. A borrower comparing a secured business loan across four lenders is comparing rate, tenure, and how fast the money arrives. That is the structural reality any competitive analysis of Aditya Birla Capital has to start from.

Porter's Five Forces, applied honestly

Rivalry: intense and intensifying. Bajaj Finance operates at roughly six times ABC's market value.121 Tata Capital arrived on the exchanges in October 2025 at almost identical loan-book scale.17 Banks — funded by low-cost deposits ABC cannot access — have spent three years pushing into retail and MSME credit. And a cohort of digital-native lenders competes on origination speed. There is no segment where Aditya Birla Capital faces a weak competitive set.

Buyer power: high and rising. Switching costs in retail lending are close to zero. A borrower who finds 40 basis points cheaper elsewhere refinances. India's digital public infrastructure — the account aggregator framework, UPI, the credit bureau ecosystem — has made comparison shopping trivial. Pankaj Gadgil's disclosure that balance transfer outflows are "very consistent" quarter to quarter is a quiet confirmation that customers do leave, routinely, in a predictable stream.15

Supplier power: this is the one that matters. For a wholesale-funded NBFC, the supplier is the capital market, and the price it charges is cost of funds. This is the input that determines everything downstream. Singh's claim of "one of the best cost of borrowing" is the group's most economically valuable inherited asset — it flows from the Aditya Birla name and credit standing rather than from anything the lending team built.15 It is also entirely outside management's control. A credit rating action or a systemic funding squeeze resets the business model overnight, as every Indian NBFC learned in 2018.

Threat of new entrants: moderate, and asymmetric. Regulatory licences and capital requirements deter casual entry. But adjacent incumbents — banks, large fintechs, other conglomerates — face low barriers to entering ABC's segments, which is precisely what is happening.

Substitutes: structurally growing. Corporate bond markets, embedded finance at point of sale, and peer-to-peer channels all nibble at traditional NBFC lending. None is decisive yet.

Net assessment: this is a structurally competitive industry with one genuine choke point — funding cost — where Aditya Birla Capital happens to be advantaged.

Seven Powers, and where the claims break down

Hamilton Helmer's framework asks which durable advantages actually exist. Applied to Aditya Birla Capital:

Scale economies — partially present, insufficient. Fixed costs across technology, compliance and brand spread over a larger book. But the reference class matters: ABC's opex-to-AUM of 1.93% is good, and it is being compared against competitors with two to four times the book over which to amortise. The company is building scale economies; it does not yet possess them relative to the leaders.

Branding — present and real. This is the strongest of the seven. In insurance and asset management, where the customer buys a promise redeemable decades later, an established industrial name reduces perceived counterparty risk. It shows up in the 12 bancassurance partnerships, the 200,000-plus agent network, and the funding cost advantage. Branding is real but bounded: it does not let ABC charge more for a secured MSME loan, as Singh confirmed when he told analysts the company prices "quite well compared to the industry" at yields of 12.2–12.2%.15 Price parity, not premium.

Cornered resource — absent. No proprietary asset competitors cannot acquire. The joint venture partnerships are valuable but replicable; every large Indian insurer has a foreign partner.

Network economies — absent. A borrower gains nothing from other borrowers existing.

Counter-positioning — absent. ABC's model is a conventional diversified financial services platform. Nothing about it is structurally painful for an incumbent to copy.

Switching costs — weak. As established.

Process power — the central claim, still unproven. This is where "One ABC" lives. The argument is that owning multiple products for one household produces lower acquisition cost, higher lifetime value, and better credit information — advantages that accrue slowly through organisational learning and cannot be bought.

The evidence for and against is now clear enough to state. In favour: ABCD reached 1.2 crore customer acquisitions carrying 26-plus products;3 Udyog Plus scaled from under ₹3,700 crore to ₹6,229 crore in AUM in a year;314 the group ecosystem drove 17.4% of housing finance retail disbursements;15 life insurance credit-life business now sources 33% from the captive NBFC and housing finance channels;15 and the health insurance Health Returns programme demonstrably lowers loss ratios in the participating cohort.15 Against: the company has never published a customer acquisition cost, a products-per-customer figure, or a cross-sell margin.

A skeptical reading is that "One ABC" is currently a distribution efficiency programme — real, useful, worth doing — rather than a compounding process advantage. It would be converted into the latter by disclosure of unit economics showing that a multi-product ABC customer costs less to acquire and defaults less often than a single-product one. That disclosure has not appeared, and its absence after four years is itself information.

The honest conclusion: Aditya Birla Capital's durable advantages are brand and funding cost. Everything else is either being built or being asserted.

XII. Bull vs. Bear Case

The bull case

India's financialisation runway is not a slogan. Credit-to-GDP, insurance penetration, and mutual fund assets per capita all remain far below comparable emerging markets. A company positioned across lending, protection and savings compounds with the entire category, not just with share gains. Growing a lending book 32% while improving asset quality is only possible in a market where demand exceeds well-underwritten supply.3

The structural re-rating has a durable component. The elimination of a Core Investment Company layer improved deployable capital capacity, not just optics, taking implied leverage from roughly 5.9x to 4.15x.19 That headroom converts into earnings if the incremental book earns its cost of capital.

Asset quality has been delivered, not just promised. Credit cost beat guidance in FY26. Stage 2 plus 3 improved across both lending businesses. Gross Stage 3 in the NBFC book fell 97 basis points year on year to 1.30%.315 For a lender growing this fast, that combination is unusual and is the strongest evidence for underwriting competence.

Multiple engines are firing simultaneously. Lending up 32%, health insurance premium up 50%, life insurance absolute VNB up 153%, combined AUM up 36% — in the same quarter.3 Diversification is often a euphemism for mediocrity; here, several segments are compounding at once.

Insurance profitability is inflecting. Life VNB margin at 20.6% and the health combined ratio moving from 105% to 103% mean two businesses that consumed capital for a decade are approaching the point of contributing it.15

Promoter support is demonstrated, not theoretical. Grasim has repeatedly written cheques, most recently ₹2,880 crore.7 Very few Indian NBFCs have that backstop.

The bear case

Sub-scale against every relevant comparison. Six times smaller than Bajaj Finance by market value, without deposit funding, against banks with a permanent cost-of-funds advantage.121 Scale in lending is not vanity; it determines whether fixed technology and compliance costs are absorbed or dilutive.

The opex trend is unexplained. Three consecutive quarters of operating expense growth outpacing AUM growth, with management's own account offering "no specific reason."15 If AI-driven efficiency is the core forward thesis, this is the metric that falsifies it, and it is currently pointing the wrong way.

The housing finance book is young. A portfolio growing at 50% annually has a gross Stage 3 ratio of 0.41% partly because most loans have not had time to go bad.3 The real credit test arrives in FY28–FY29. Management is planning to grow to ₹1 lakh crore before that test occurs.15

Recurring dilution. ₹4,000 crore raised at the parent, ₹2,750 crore into housing finance, ₹665 crore into health insurance.31220 The pattern is consistent enough to be structural: this business does not currently self-fund its growth ambition.

Health insurance still loses money on underwriting. At a 103% full-year and 106% quarterly combined ratio, growth is being bought.315 Fast-growing health insurers that never reach 100% eventually discover that share bought below cost is not an asset.

Integration and execution risk stack up. Absorbing ABFL into the parent, chasing 25% loan CAGR,25 opening 100-plus housing branches, transitioning life insurance to IFRS, and absorbing a new health insurance accounting framework — simultaneously.

Ownership concentration and flow sensitivity. With a free float under a third of the equity and foreign institutions at 7.94%, this is a stock whose price is set at the margin by a small pool of shares.22

Margin expansion depends on a riskier mix. Singh's path to 2.5% ROA runs through increasing the unsecured and personal-consumer share from 23.4% of the book.15 That is a deliberate trade of asset quality for yield — coherent, and the opposite of the secured-collateral story that produced the current credit performance.

XIII. Risk Radar

Credit seasoning in housing finance. The mechanism is specific: mortgages default in years three through seven. A book that grew 53% in FY26 to ₹47,452 crore and is targeted at ₹1 lakh crore within 30 months will have the majority of its exposure in loans originated after 2025.15 Stage 2 at 32 basis points is a genuinely encouraging leading indicator, and it is a leading indicator on an immature book.15

Funding cost and refinancing. An NBFC borrows wholesale and lends retail; it lives on the spread. Its liabilities reprice on market conditions it does not control. Aditya Birla Capital's current advantage — best-in-class cost of borrowing — is inherited from group credit standing, which means the risk is also inherited. A rating action against any part of the group, or a systemic risk-off event in Indian credit markets, compresses the spread from the liability side without warning. The FY26 fourth-quarter mark-to-market hit from rising government securities yields was a small preview of the sensitivity.15

Margin dilution from the mix shift. Deliberately raising the unsecured share to expand margin means the credit cost guidance of 1.1–1.2% for FY27 is being made on a portfolio that will look different from the one that produced 1.18%.15 Management is aware and has guided accordingly; the risk is that the deterioration outruns the yield gain.

Regulatory change across three regulators. Scale Based Regulation has already reshaped the company once; further tightening on upper-layer NBFCs — capital, disclosure, governance — remains a live possibility. IRDAI capital and solvency requirements bind the insurance businesses independently. The nil-rate GST change on insurance cost the health business ₹36 crore in FY26 alone.15 Three regulators means three independent sources of unhedgeable policy risk.

Accounting transitions creating comparability breaks. Life insurance is moving to IFRS in FY27 under a forbearance, and health insurance has already shifted to a 1/n premium recognition framework that reduced reported FY26 profit from ₹85 crore to ₹39 crore.15 Neither change alters cash economics. Both will make year-on-year comparison genuinely difficult, and both create room for reported results to be flattered or depressed by assumption choices. This is the accounting judgment area investors should watch most closely.

Execution risk in the transformation itself. The merger simplified structure; it did not simplify operations. Integrating systems, cultures and risk frameworks while growing 32% is where operating expense overruns and underwriting slippage typically originate.

Competitive compression from digital-native lenders and banks. Origination speed is now a competitive weapon, which is why ABC has invested so heavily in cutting turnaround times. The risk is that speed becomes table stakes rather than differentiation, and the competition returns to price — where banks win.

What is not a material risk here. Geopolitical and supply chain exposure is minimal for a domestically-focused Indian lender; management noted no material portfolio impact from West Asia tensions.15 Currency exposure is limited. The risks that matter are credit, funding, regulation and execution — in that order.

XIV. Playbook: Lessons from the Restructuring

Every good business story leaves behind transferable lessons. This one leaves four.

Regulation can force the strategic decision management has been deferring. The most valuable structural change in Aditya Birla Capital's history was not a strategic choice. RBI's Scale Based Regulation created a listing obligation, and the obligation forced a decision the board had been circling for years.416 The 2017 demerger — a genuinely discretionary strategic action — solved the wrong problem and left a holding company discount in place for eight years. The 2025 merger, undertaken because a regulator required something, actually simplified the structure. The lesson for investors watching conglomerates: external forcing functions often produce cleaner outcomes than internal strategy processes, because they remove the option of doing nothing.

Subsidiary stake sales are a repeatable tool with an honest cost. Sun Life, Momentum Metropolitan, ADIA, Advent, IFC — the pattern is consistent and it works mechanically. Each transaction supplies capital, establishes an external valuation for an asset the market was under-pricing, and shares execution risk. The cost is equally real: the parent owns less of everything it built, and each sale is an admission that growth exceeded internal capital generation. Judge such a strategy not by whether stakes were sold, but by whether the capital raised earned more than it diluted. On Aditya Birla Capital's evidence, that verdict is still pending.

Multi-license conglomerates carry a permanent efficiency tax. Running lending, life insurance, health insurance, asset management and broking simultaneously means five regulators, five capital regimes, five technology stacks, and — in the insurance businesses — joint venture partners whose interests only partially align. The offsetting benefit is cross-sell, and the evidence for it remains thinner than the evidence for the cost. Focused competitors do not pay this tax.

Brand transfers across industries, but only so far. The Aditya Birla name genuinely lowers the cost of trust in insurance and asset management, and it demonstrably lowers the cost of borrowing.15 It does not permit premium pricing on a secured business loan — management confirmed price parity with the industry.15 Brand is a real advantage in this business, operating on the liability side of the balance sheet and on the promise-based products. On the asset side, in commodity credit, it is worth very little.

XV. The Road Ahead & Epilogue

Three questions will determine how this story reads in five years.

Does housing finance follow the AMC's path? Advent International owns approximately 14.3% of Aditya Birla Housing Finance at a ₹19,250 crore post-money valuation.20 The business is targeting ₹1 lakh crore of AUM within 24 to 30 months and a return on equity above 15% within 12 to 24 months.15 Nothing has been announced about a listing, and investors should not assume one. But the group has run this sequence before — bring in a partner, scale, list — and private equity investors are not permanent holders. If ABHFL hits ₹1 lakh crore with a 15%-plus return on equity and a still-clean book, a listing becomes the obvious next move. If asset quality deteriorates as the book seasons, it becomes a much harder conversation.

Does AI-driven efficiency actually compress the cost base? This is the most plausible next re-rating trigger and the most plausible next disappointment. The qualitative evidence is real: 65% of contact-centre calls straight-through processed, turnaround times down 30%-plus in retail and MSME journeys, 35–40% underwriting productivity gains in health insurance.15 The financial evidence is absent, and the one hard trend — three quarters of opex growing faster than AUM — currently contradicts the story.15 Management has effectively pre-committed by guiding housing finance opex to average loan book down to approximately 2.10% while opening 100-plus branches.15 That is a checkable promise. Check it.

Can 25% compound growth be executed without an underwriting misstep? Management has committed to a 25% loan CAGR over three years alongside its AI-led strategy.25 India's credit history is unkind to lenders who compound at that rate through a full cycle. The particular tension is that the margin expansion path runs through increasing the unsecured share, while the asset quality record was built on secured collateral. Those two objectives pull in opposite directions, and the FY28 and FY29 numbers will reveal which one won.

The three numbers to track

Skip the headline growth rates. Three metrics carry the analytical weight.

First: NBFC return on assets, and specifically the operating expense line beneath it. Rakesh Singh has publicly committed to 2.5% by the end of FY27, from 2.31% in the fourth quarter of FY26.15 That single number integrates margin, credit cost and efficiency. Watch operating expense growth against AUM growth as the leading indicator — if opex keeps outrunning AUM, the ROA target does not arrive regardless of what happens to margin.

Second: the health insurance combined ratio. It sat at 103% for FY26 and 106% in the June 2026 quarter, with management targeting 100%.315 This is the cleanest binary in the entire group. Below 100% and Aditya Birla Health Insurance becomes a genuine profit pool with a standalone valuation. Above it, growth continues to consume capital, and every point of market share gained has a cost attached.

Third: housing finance Stage 2 plus Stage 3 as the book ages. Currently 0.76%, with 32 basis points in Stage 2.15 Stage 2 is the early warning — accounts showing significant increase in credit risk before they default. Because the book is young and growing at 50%, the denominator is expanding fast enough to flatter the ratio. The signal to watch is Stage 2 rising while growth decelerates, which is what a seasoning problem looks like before it becomes a Stage 3 problem.

Epilogue

Three corporate actions define Aditya Birla Capital's public life, and together they teach a coherent lesson about unlocking value inside a regulated financial conglomerate.

The 2017 demerger separated financial services from an industrial conglomerate and produced a listed company worth over ₹55,000 crore on day one6 — then watched the market apply a fresh discount, because a holding company of financial subsidiaries is only marginally more legible than a textiles company that owns an insurer.

The 2021 asset management IPO proved the parts could be priced richly when separated, which was informative and, for the parent's own multiple, largely irrelevant. Selling a piece of the best business at a good price does not re-rate what remains.

The 2025 merger did what neither of the others managed: it eliminated a structural layer entirely and turned the listed entity into the operating business itself.5 The market's response — a stock up roughly 50% over the following twelve months1 — suggests investors agreed that the previous discount had been a real cost rather than a fair assessment.

The lesson is not that restructuring creates value. It is that structure only matters when it changes what a company can actually do with its capital. The 2017 demerger changed the wrapper. The 2021 IPO changed the price of one asset. The 2025 merger changed the balance sheet — and it took a regulator, not a strategy offsite, to make it happen.

What follows from here is no longer a structural story. Aditya Birla Capital is now a mid-scale operating lender with insurance and asset management stakes attached, competing against larger, better-funded, and in some cases better-run rivals, funding its growth substantially with outside equity, and asking the market to believe that a decade of cross-sell ambition is finally about to show up in unit economics. The credit data says the underwriting is currently good. The operating expense data says the efficiency thesis is unproven. The capital raises say the growth is not yet self-funding.

Those three facts have to be reconciled by FY28. The seasoning cycle will do the reconciling whether management is ready or not.

References

-

Aditya Birla Capital (NSE: ABCAPITAL) — Stock Quote, Market Cap, 52-Week Range, 2026-08-10 ↩↩↩↩↩↩↩↩

-

Aditya Birla Capital Q1 FY27 Results: Strong Earnings Growth Across Businesses — Aditya Birla Group press release, 2026-07-31 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

High Stakes, Smart Moves: Upper Layer NBFCs and the Mandatory Listing Requirement — Lexology ↩↩↩

-

Aditya Birla Capital Limited completes amalgamation of Aditya Birla Finance Limited, creates a unified larger operating NBFC — Aditya Birla Group press release, 2025-04-01 ↩↩↩↩↩↩↩↩

-

Aditya Birla Capital Limited lists on Stock Exchanges — Aditya Birla Group press release, 2017-09-01 ↩↩↩↩↩

-

Grasim Industries acquires additional stake in Aditya Birla Capital for Rs 2,880 crore — Business Upturn, 2026-06-23 ↩↩↩↩↩

-

Information Memorandum dated August 16, 2017 — Aditya Birla Capital Limited ↩↩↩↩

-

Amalgamation of Aditya Birla Nuvo with Grasim Industries — Aditya Birla Group press release, 2017 ↩↩

-

Aditya Birla AMC eyes Rs 20,500 cr valuation in Rs 2,768 cr IPO — Business Standard, 2021-09-24 ↩↩↩↩↩

-

Aditya Birla Sun Life AMC — Shareholder and Annual Report Information ↩↩

-

ADIA to invest Rs 665 crore in Aditya Birla Health Insurance for 9.99% stake — Business Standard, 2022-08-12 ↩↩↩

-

Aditya Birla Capital Q1 FY26 financial results: Consolidated PAT and Revenues up 10% — Aditya Birla Group press release, 2025-08-04 ↩↩

-

Aditya Birla Capital Ltd. — Q4 FY26 Earnings Conference Call Transcript, 2026-05-04 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Aditya Birla Capital merger: Reasons and perceived benefits — ICICIdirect Research ↩↩

-

Tata Capital IPO 2025: Dates, Price Band, Issue Size & Details — m.Stock ↩↩↩↩↩

-

RBI gives approval for Aditya Birla Finance's merger with parent — Business Standard, 2024-09-18 ↩

-

Aditya Birla Capital & Finance Merger Details — Ventura Securities ↩↩↩

-

Aditya Birla Housing Finance raises Rs 2,750 crore of growth capital from Advent International — Advent International, 2026-02-03 ↩↩↩↩

-

Bajaj Finance (NSE: BAJFINANCE) — Stock Quote and Market Cap, 2026-08-10 ↩↩↩↩

-

Aditya Birla Capital Ltd — Shareholding Pattern, Choice India, 2026-08-08 ↩↩

-

Aditya Birla Capital posts 40% rise in Q1 profit, raises ₹4,000 crore — Business Standard, 2026-07-31 ↩

-

Aditya Birla Capital Q1 result: Net profit up 10%, board approves ESOPs — Business Standard, 2025-08-04 ↩

-

Aditya Birla Capital bets on AI-led growth, aims 25% loan CAGR in 3 years — Business Standard, 2026-07-20 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube