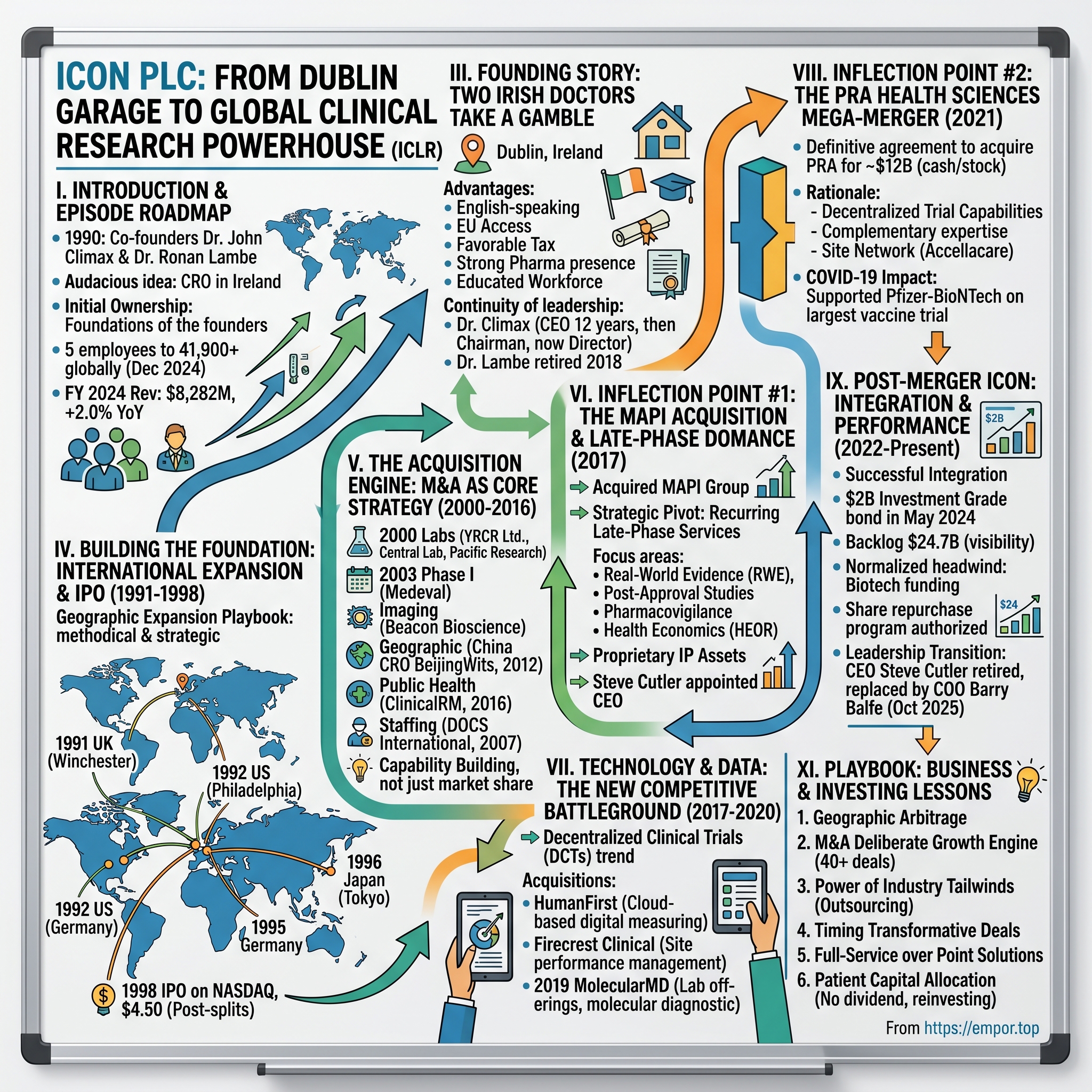

ICON plc: From Dublin Garage to Global Clinical Research Powerhouse

I. Introduction & Episode Roadmap

Picture this: It's 1990, and two Irish doctors are sitting in a cramped Dublin office, surrounded by case files and the persistent rain that defines Irish winters. Dr. John Climax and Dr. Ronan Lambe have just quit their stable positions to launch something audacious—a contract research organization in a country better known for sheep farming than pharmaceutical innovation. The early days of ICON plc were characterized by the foundational ownership of its two co-founders, Dr. John Climax and Dr. Ronan Lambe. Their personal investment and strategic direction were paramount in navigating the nascent stages of the company.

ICON plc was founded in 1990 by Dr. John Climax and Dr. Ronan Lambe in Dublin, Ireland. The company began as a small contract research organization with just five employees, focusing primarily on providing clinical research services to pharmaceutical companies.

Fast forward thirty-five years, and the numbers tell an extraordinary story. Full year revenue reached $8,282 million, representing a year on year increase of 2.0%. With headquarters in Dublin, Ireland, ICON employed approximately 41,900 employees in 106 locations in 55 countries as at December 31, 2024.

But raw numbers don't capture what makes ICON's journey so compelling for students of business strategy. This is a story about contrarian positioning, relentless M&A execution, and the ability to ride one of healthcare's most powerful secular trends—the outsourcing revolution in pharmaceutical development.

Here's what we'll explore: How did two doctors with no venture capital backing build one of the world's largest clinical trial companies? Why did Ireland—a country with more livestock than people—become a springboard for global expansion? What strategic moves transformed ICON from a regional player into the company that helped deliver the world's first COVID-19 vaccine? And critically, what does the $12 billion PRA Health Sciences merger tell us about where this industry is heading?

The global contract research organization (CRO) services market, valued at US$79.10 billion in 2024, stood at US$84.61 billion in 2025 and is projected to advance at a resilient CAGR of 8.3% from 2025 to 2030, culminating in a forecasted valuation of US$125.95 billion by the end of the period.

ICON sits at the center of this massive industry transformation. Whether you're an investor trying to understand pharmaceutical supply chains, an entrepreneur studying M&A-driven growth strategies, or simply curious about how medicines actually get developed and tested, ICON's story offers a masterclass in building a global services business from scratch.

II. The CRO Industry Primer: Why This Business Exists

Before diving into ICON's story, we need to understand why contract research organizations exist at all. The answer lies in one of the most challenging economics problems in modern business: drug development.

In 2001, researchers from the Center estimated that the cost of doing so was $802 million, and in 2014, they released a study estimating that this amount had risen to nearly $2.6 billion. The process from ideation to market introduction takes about 10 to 15 years. That's 10-15 years and billions of dollars before a company knows whether its drug will work—let alone whether regulators will approve it.

The attrition is brutal. The 9.6% success rate is not just a number—it's a reality check for businesses entering this space. For every drug that reaches patients, roughly ten others failed somewhere along the 10-15 year journey.

This creates a classic "make vs. buy" decision for pharmaceutical companies. Should Pfizer, Novartis, or AstraZeneca maintain massive internal clinical trial organizations capable of running studies across dozens of countries, in multiple therapeutic areas, with varying regulatory requirements? Or should they outsource this incredibly complex work to specialists who do nothing else?

The answer has shifted decisively toward outsourcing. Across the global pharma market, the overall CRO outsourcing penetration rate ranges from 45%-50%, depending on the service type. Currently, big pharma is outsourcing nearly half of all its R&D activities, while the share can even increase to 100 percent for smaller companies.

The logic is compelling. CROs offer:

Flexibility: Pharma companies can scale clinical trial capacity up or down without maintaining expensive fixed infrastructure. When a drug program fails, they don't have thousands of clinical researchers on permanent payroll.

Specialized Expertise: Shaped by the demand for clinical trials in specific therapeutic areas, CROs recognize the need to adapt to R&D pipeline trends and hone resources and expertise accordingly. Key therapeutic focuses are oncology, immunology, neurology and cardiovascular, which represent 71% of the 5,318 clinical trials started in 2024.

Global Reach: A modern clinical trial might enroll patients across 50+ countries simultaneously. Building that infrastructure independently would take years and billions of dollars.

Cost Efficiency: CROs achieve economies of scale and scope that individual pharma companies cannot match. They maintain relationships with tens of thousands of clinical trial sites worldwide, have established regulatory relationships in every major market, and possess proprietary technologies for trial design and execution.

"EBPs, mostly pre-commercial, are responsible for 63% of trial starts, up from 56% in 2019," according to industry analysis. "It can be a make-or-break time for EBPs heavily focused on one or two key assets."

This last point matters enormously. The pharmaceutical industry has bifurcated. Large pharma companies focus increasingly on late-stage development, commercialization, and manufacturing, while emerging biotech companies (EBPs) drive most early-stage innovation. These smaller companies have neither the capability nor the desire to build in-house clinical trial operations—they need CRO partners.

The implications for investors are profound. CROs aren't just service providers; they're essential infrastructure for the entire pharmaceutical innovation ecosystem. As drug development grows more complex—more specialized therapeutic areas, more stringent regulatory requirements, more global trials—the value of CRO expertise compounds.

III. Founding Story: Two Irish Doctors Take a Gamble

The founding of ICON represents one of the great contrarian bets in healthcare services. Ireland in 1990 was not Silicon Valley. It wasn't even a pharmaceutical hub. The country was still emerging from economic stagnation, and the idea of building a global clinical research business there seemed almost absurd.

"Having co-founded ICON in 1990, I have had the pleasure of seeing the company grow from humble beginnings to become one of the world's leading clinical research organisations," said Dr. Climax.

Dr. John Climax brought an unusual combination of credentials to the venture. Dr. Climax received his primary degree in pharmacy in 1977 from the University of Singapore, his Masters in Applied Pharmacology in 1979 from the University of Wales and his PhD in Pharmacology from the National University of Ireland in 1982. This international background would prove crucial for a company that needed to operate globally from day one.

In 1990, Dr. John Climax and Dr. Ronan Lambe founded ICON Clinical Research in Dublin with just five staff.

But why Ireland? The country's advantages weren't immediately obvious, but they were real and durable:

English-speaking: Unlike other European countries, Ireland offered native English capability essential for regulatory submissions and global client communication.

EU membership: Ireland provided access to the European market while maintaining distinct regulatory relationships.

Favorable corporate tax regime: Ireland's business-friendly tax policies were already attracting pharmaceutical manufacturing investment.

Strong pharmaceutical presence: Major pharma companies had already established manufacturing operations in Ireland, creating local relationships and industry familiarity.

Educated workforce: Ireland's strong university system produced science graduates who could staff clinical research operations.

The cultural positioning was equally strategic. Ireland's neutral global standing opened doors that might remain closed to British or American firms. This wasn't just about avoiding political baggage—it created genuine commercial advantages in regions emerging as important for clinical trial recruitment.

John Climax, one of the ICON's co-founders, served as Chairman of the Board of ICON plc from November 2002 to December 2009 and as Chief Executive Officer from June 1990 to October 2002. From January 2010 he has held a position as a non-executive director.

The founders' commitment has been remarkable. Dr. Climax led the company as CEO for its first twelve years, then served as Chairman for another seven years, and remains on the board today—35 years after founding the company. Dr. Ronan Lambe retired as a non-executive director at the Annual General Meeting (AGM) of the Company on the 24th July 2018. This follows the announcement in the 2018 AGM Notice that Dr. Lambe had decided to retire and not seek re-election at the AGM.

This continuity matters. ICON never experienced the founder-transition trauma that derails many young companies. The strategic vision remained consistent even as execution scaled globally.

IV. Building the Foundation: International Expansion & IPO (1991-1998)

The founders understood from the beginning that ICON could not succeed as an Irish company serving Irish clients. The pharmaceutical industry was global, and a CRO needed global reach to win significant contracts. The expansion playbook was methodical and strategic.

Between 1991 and 1996, ICON opened offices in the United Kingdom, United States, Germany, and Japan.

Consider the strategic logic of this sequence:

1991 - United Kingdom: The first overseas office in Winchester established a beachhead in Europe's largest pharmaceutical market and created proximity to London-based global pharma headquarters.

1992 - United States (Philadelphia): The U.S. represented then—and represents now—the world's largest pharmaceutical market. Philadelphia offered access to the dense concentration of pharmaceutical companies along the East Coast.

1995 - Germany: Continental Europe's largest pharmaceutical market and home to major companies like Bayer and Boehringer Ingelheim.

1996 - Japan (Tokyo): Asia's largest pharmaceutical market and a regulatory jurisdiction with distinct requirements that demanded local expertise.

ICON provides contract clinical research services to the pharmaceutical industry world-wide. It currently has nine offices in six countries and has approximately 500 employees world-wide. By 1998, the five-person Dublin startup had grown 100x in employee count.

The rapid growth required capital. In May 1998, ICON went public on NASDAQ. ICON (ICLR) went public in May 1998 at an initial price of $4.50 (Post splits).

"Fiscal 1998 has been a year of major progress for ICON", commented Chairman Dr. Ronan Lambe. "We developed our presence in the Asia Pacific region, which has enhanced our ability to win major, global projects and we grew revenues strongly world-wide, especially in the United States. On May 15, 1998 we successfully completed our IPO, which strengthens the Company financially and puts us in a good position to capitalise on our strengths, and to develop further areas of expertise and excellence."

The IPO timing proved fortuitous. The late 1990s saw pharmaceutical R&D spending accelerating, and the outsourcing trend was just beginning to take hold. ICON had positioned itself to capture this wave.

The company continued geographic expansion after the IPO, entering South America in 1998 and Africa in 2002. Each new region added capabilities for running truly global trials—essential for winning large pharma contracts.

For long-term investors, the IPO marked the beginning of an extraordinary compounding journey. From that initial listing price, ICON would grow to become one of the world's largest CROs, delivering returns that far exceeded most healthcare investments.

V. The Acquisition Engine: M&A as Core Strategy (2000-2016)

If ICON's founding was about vision and its international expansion about execution, the period from 2000 to 2016 was about acquisition-driven growth. The company developed what can only be described as an "M&A playbook"—a systematic approach to building capabilities through targeted deals.

Over the years, we have grown both organically and through strategic acquisitions, expanding our service portfolio and scaling our capabilities.

The acquisition pattern reveals deliberate strategic thinking. ICON wasn't buying competitors for market share—it was building a full-service platform through capability additions:

Laboratory Capabilities: 2000: ICON acquired UK-based regulatory consultancy, YRCR Ltd.; Central Laboratory in New York; and bioanalytical consultancy, Pacific Research. Central lab services are essential for processing and analyzing patient samples from clinical trials. Rather than building this capability organically—which would take years—ICON bought established operations.

Phase I Facilities: 2003: ICON acquired Medeval, a UK-based Phase I facility. Phase I trials (first-in-human studies) require specialized facilities with intensive patient monitoring. These early-phase capabilities positioned ICON to capture drug programs from their earliest stages.

Medical Imaging: ICON acquires medical imaging specialist, Beacon Bioscience Inc. As trials increasingly relied on imaging endpoints (tumor measurements, brain scans, etc.), ICON needed specialized expertise.

Geographic Expansion: 2012: ICON acquired PriceSpective and Chinese CRO, BeijingWits. China represented an enormous growth opportunity—both for recruiting patients and for serving the emerging Chinese pharmaceutical industry.

Government/Public Health: On 15 September 2016, a subsidiary of the Company acquired Clinical Research Management, Inc. ("ClinicalRM") which resulted in initial net cash outflows of $52.4 million. ClinicalRM is a full-service CRO specialising in preclinical through Phase IV support of clinical research and clinical trial services for biologics, drugs and devices.

Staffing and FSP: 2007: ICON acquired European staffing group, DOCS International. Functional Service Provider (FSP) contracts—where pharma companies outsource specific functions rather than entire programs—were becoming increasingly important. DOCS gave ICON a strong FSP platform.

The pattern is clear: systematic capability building to create a full-service offering. Each acquisition addressed a specific gap in ICON's ability to serve clients across the entire drug development lifecycle.

What's remarkable is that ICON maintained this acquisition discipline even during difficult periods. Even during Ireland's worst recession years in 2010, ICON posted its first-ever quarterly loss but still acquired Veeda Laboratories in the U.K. The company's commitment to long-term capability building trumped short-term financial concerns.

For investors, this M&A strategy creates both opportunity and risk. The opportunity lies in accelerated capability development and market positioning. The risk involves integration execution and capital allocation discipline. ICON's track record suggests the company has managed this balance effectively, but each deal requires careful evaluation.

VI. Inflection Point #1: The MAPI Acquisition & Late-Phase Dominance (2017)

While most of ICON's acquisitions were "bolt-on" deals adding specific capabilities, the 2017 MAPI acquisition represented a strategic pivot that fundamentally expanded the company's addressable market.

2017: ICON acquired MAPI Group, thereby becoming the world's second-largest provider of late-phase services.

DUBLIN--(BUSINESS WIRE)--July 27, 2017--ICON plc today announced that it has acquired the Mapi Group, a leading Patient-Centered Health Outcomes Research and Commercialisation company.

What are "late-phase" services and why do they matter?

Most CRO revenue historically came from Phase I-III clinical trials—the pre-approval studies required to demonstrate safety and efficacy. But once a drug is approved, pharmaceutical companies face ongoing requirements:

Post-Approval Studies (Phase IV): Regulators often require additional studies after approval to monitor long-term safety or efficacy in broader patient populations.

Real-World Evidence Generation: Payers (insurance companies, government health systems) increasingly demand evidence that drugs work in "real-world" settings, not just controlled clinical trials.

Pharmacovigilance: Companies must monitor and report adverse events for as long as their drugs remain on the market.

Health Economics and Outcomes Research: Demonstrating value to payers requires specialized expertise in health economics modeling and outcomes measurement.

"The late phase CRO market continues to grow as our customers face greater scrutiny from regulators and reimbursement bodies around real-world evidence of product value and safety," commented Dr. Steve Cutler, Chief Executive Officer, ICON plc. "The acquisition of Mapi extends the breadth and depth of ICON's late phase capabilities, creating an industry leading provider of post-approval research, spanning evidence generation, strategic regulatory services, scientific communications and commercial strategy."

The strategic logic was elegant. Traditional CRO work is inherently lumpy—companies win or lose large trial contracts, creating revenue volatility. Late-phase services tend to be more recurring, as drug companies require ongoing support for as long as their products remain on market.

The combined organisation will be a leader for real world evidence, post approval research, language services, consultancy services supporting clinical outcomes assessments, pricing and market access and scientific communications. The acquisition also enables ICON to have direct access to Mapi Research Trust, the industry's most subscribed library of Clinical Outcomes Assessments (COAs).

The MAPI deal also gave ICON intellectual property assets—validated questionnaires and assessment tools that drug companies license for their studies. This created a unique competitive moat: customers needed ICON not just for services, but for proprietary tools essential to regulatory submissions.

The timing coincided with Steve Cutler's tenure as CEO. In March 2017, Steve Cutler was appointed Chief Executive Officer of ICON. He had previously been with Quintiles South Africa, Sandoz AG, and Kendle Intl Inc, before joining ICON Clinical Research Services in 2011, and becoming Chief Operating Officer in 2014.

Cutler brought deep industry experience from multiple CRO competitors. Prior to joining the Company, Dr. Cutler held the position of Chief Executive Officer of Kendle, having previously served as Chief Operating Officer. Prior to Kendle, Dr. Cutler spent 14 years with Quintiles where he served as Senior Vice President, Global Project Management; Senior Vice President, Clinical, Medical and Regulatory; and Vice President, Oncology - Europe, as well as regional leadership positions in South Africa and Australia.

His operational expertise would prove essential for the company's next major transformation.

VII. Technology & Data: The New Competitive Battleground (2017-2020)

As ICON integrated MAPI and consolidated its late-phase position, a technology revolution was reshaping clinical research. The company recognized that future competitive advantage would depend on digital capabilities as much as operational excellence.

ICON acquires HumanFirst, a cloud-based technology company for life sciences supporting precision measurement in patient centered clinical research.

ICON acquires Firecrest Clinical, a technology provider specialising in site performance and study management.

2019: ICON acquired MolecularMD, to enhance its laboratory offerings in molecular diagnostic testing and immunohistochemistry.

These weren't random technology acquisitions. Each addressed specific operational pain points in clinical trial execution:

Site Performance Management (Firecrest): Clinical trials depend on hundreds of investigative sites (hospitals, clinics, physician offices) that recruit patients and conduct study visits. Managing site performance—enrollment rates, protocol compliance, data quality—determines trial success. Firecrest's technology enabled real-time visibility into site operations.

Digital Measurement Tools (HumanFirst): As trials incorporated more digital endpoints (wearable devices, smartphone apps, patient-reported outcomes), ICON needed expertise in validating these novel measurement approaches.

Precision Medicine Testing (MolecularMD): Increasingly, trials target specific patient populations defined by genetic markers. MolecularMD added capabilities in companion diagnostic development and molecular testing.

The strategic context was the emerging "decentralized clinical trial" (DCT) model. Traditional trials require patients to visit clinical sites repeatedly—for examinations, blood draws, drug administration, and monitoring. This creates patient burden (travel time, cost, missed work) and limits who can participate.

The Decentralized Clinical Trials (DCTs) Market was valued at USD 9.63 Billion in 2024, and is expected to reach USD 21.34 Billion by 2030, rising at a CAGR of 14.16%.

Decentralized trials use technology to bring the trial to the patient: telemedicine visits, home nursing, direct-to-patient drug shipments, and wearable devices for remote monitoring. This model promises faster enrollment, broader patient populations, reduced costs, and better patient retention.

Then COVID-19 arrived, and everything accelerated.

VIII. Inflection Point #2: The PRA Health Sciences Mega-Merger (2021)

The pandemic created unprecedented demand for clinical trial capabilities—vaccine development required trials enrolling tens of thousands of patients in months rather than years. ICON found itself at the center of this effort.

"We are proud to have supported Pfizer and BioNTech on one of the largest and most expeditious randomised clinical trials ever conducted, and to have helped accelerate their mission to develop the world's first safe and effective investigational vaccine for COVID-19."

Irish clinical trials group Icon has revealed that it carried out the late-stage trial of the Pfizer-BioNTech coronavirus vaccine. The trial, which involved 44,000 participants over a four-month period last year, was the largest trial of a Covid-19 vaccine.

ICON has provided clinical trial services to Pfizer over the past 30 years and formed a strategic relationship with the company in 2011, to provide global expertise in the planning, execution, management and conduct of clinical trials.

The vaccine trial demonstrated what ICON could accomplish when technology, global scale, and operational expertise converged. But it also revealed the industry's trajectory: decentralized trial elements weren't just nice-to-have; they were essential for modern clinical research.

This realization catalyzed the most transformative deal in ICON's history.

ICON today announced it has entered into a definitive agreement to acquire PRA Health Sciences, Inc. in a cash and stock transaction valued at approximately $12 billion, with the per share merger consideration consisting of $80 in cash and 0.4125 shares of ICON stock.

The consideration represents an approximately 30% premium to PRA's closing price as of February 23rd, 2021. The transaction brings together two high-quality, innovative and growing organisations with similar cultures and a shared focus on high quality and efficient clinical trial execution from Phase 1 to post-approval studies.

Why PRA specifically? The strategic rationale went beyond simple scale:

Decentralized Trial Capabilities: PRA had invested heavily in technology for conducting trials remotely, including its Health Harmony mobile platform for patient engagement and monitoring.

Complementary Therapeutic Expertise: PRA's strengths in certain therapeutic areas (CNS, vaccines) complemented ICON's existing capabilities.

Site Network: PRA's Accellacare network of proprietary clinical trial sites provided guaranteed capacity for patient recruitment—increasingly valuable as site competition intensified.

"The combined company will create a new paradigm for accelerating clinical research and bringing new medicines and devices to market. Both ICON and PRA have track records of robust growth and performance and we are ready to build on this unrivalled position of strength, utilising the outstanding talent in both organisations. With broader and deeper operational scale combined with innovative technology and real world data solutions, we will enable all customers to reduce their development time and cost."

The combined entity's scale was impressive:

The combined company will retain the name ICON and will bring together 38,000 employees across 47 countries, creating the world's most advanced healthcare intelligence and clinical research organisation.

The new ICON will have a renewed focus on leveraging data, applying technology and accessing diverse patient populations to speed up drug development.

The financing structure deserves attention. The transaction valued PRA at approximately $12 billion, with approximately $6.3 billion of debt financing. This was a significant leverage increase for ICON, transforming its balance sheet from essentially debt-free to meaningfully levered.

The July 2021 close came almost exactly on schedule. On July 1, 2021, ICON plc today announced the completion of its acquisition of PRA Health Sciences. The combined company will retain the name ICON and will bring together 38,000 employees across 47 countries.

IX. Post-Merger ICON: Integration & Recent Performance (2022-Present)

Large acquisitions are won or lost in integration. The PRA deal created a combined entity with tremendous potential but also significant execution risk. Could ICON realize the promised synergies while maintaining service quality for demanding pharmaceutical clients?

The early evidence suggests careful management. Successful issuance of $2 billion investment grade bond in May 2024. Achieving investment grade status represented a milestone—it signaled credit market confidence in the combined entity's stability and reduced interest costs significantly.

Financial performance has been solid if unspectacular in a challenging environment:

On a full year basis, we reported growth across key metrics, including revenue growth of 2% as well as adjusted diluted earnings per share growth of 9.5% year over year.

Adjusted EBITDA was $1,735.8 million or 21.0% of revenue, a year on year increase of 2.5%.

Closing backlog of $24.7 billion, an increase of 1.4% on quarter three 2024 and 8.3% on quarter four 2023.

The backlog figure—$24.7 billion in contracted future work—provides visibility into revenue sustainability. A book-to-bill ratio above 1.0 indicates growing demand.

Cash generation has been strong:

Cash management was strong in quarter four, bringing full year free cash flow in line with our targeted $1.1 billion.

$500.0 million worth of stock repurchased in full year 2024 at an average price of $229. Board of Directors authorized a new share repurchase program of up to $750 million to be opportunistically deployed.

The capital allocation philosophy shows discipline—debt reduction, share repurchases at reasonable valuations, and continued tuck-in acquisitions. ICON acquires KCR, a mid-size CRO, founded and headquartered in Poland, offering full service and functional service provision clinical trial services.

However, the post-pandemic normalization has created headwinds:

"ICON's performance in quarter one was impacted by the volatility and cautiousness that continues to be present in the broader clinical development market. Bookings were below expectations due to delays in customer decision making, careful capital allocation and continued elevated cancellations."

The biotech funding environment remains challenging. During the 2020-2021 period, unprecedented capital flowed into biotech companies, driving robust clinical trial spending. The subsequent market correction reduced available funding, leading to trial cancellations and delayed program starts.

A leadership transition adds another variable. On September 4, 2025, ICON announced that Steve Cutler will step down as CEO following his retirement on 1 October 2025 and is to be replaced by Chief Operating Officer Barry Balfe.

Mr. Barry Balfe was appointed Chief Executive Officer of ICON plc in October 2025 and appointed to the Board of ICON plc in September 2025. Mr. Balfe has been with ICON for over 20 years and has held a number of leadership roles across both full service and functional solutions at ICON where he has successfully grown business and has developed and led a number of new strategic partnerships with some of the world's largest pharmaceutical companies.

The internal promotion provides continuity—Balfe knows ICON's operations intimately. But new leadership always creates uncertainty about strategic direction.

X. Leadership & Culture: The ICON Way

ICON's culture reflects its Irish origins—pragmatic, relationship-focused, and long-term oriented. The leadership tenure speaks volumes: founder Dr. John Climax remains on the board after 35 years, providing continuity that's rare in the corporate world.

Dr. Climax has over 30 years of experience in the clinical research industry. He received his primary degree in pharmacy in 1977 from the University of Singapore, his masters in applied pharmacology in 1979 from the University of Wales and his Ph.D. in pharmacology from the National University of Ireland in 1982. He has authored a significant number of papers and presentations, and holds adjunct professorship at the Royal College of Surgeons of Ireland and an honorary professorship at the National University of Singapore. He is currently Executive Chairman of DS Biopharma and CEO of Afimmune, both of which are private companies.

The geographic distribution is striking for a company that retains its Dublin headquarters. Though Ireland remains home base, the workforce is overwhelmingly global—with less than 10% stationed in Ireland.

The capital allocation philosophy has remained remarkably consistent. To date our policy has been to re-invest profits, while we continuously review this policy we do not expect any change in the foreseeable future.

ICON has never paid a dividend. Every dollar of profit has been reinvested—in acquisitions, technology, geographic expansion, and capability development. This approach requires patient shareholders willing to forgo current income for future growth, but the track record suggests disciplined deployment.

Innovation focus centers on practical operational improvements rather than moonshot technology bets. The company's stated priority: reducing time to market, reducing cost, and increasing quality for clients. This customer-centric focus has built durable relationships—ICON's 30-year partnership with Pfizer exemplifies the long-term approach.

XI. Playbook: Business & Investing Lessons

ICON's journey from five-person Dublin startup to global CRO powerhouse offers several enduring lessons:

Lesson 1: Geographic arbitrage can be a founding advantage

Starting in Ireland seemed crazy in 1990, but it created differentiation. The "CRO from Ireland" novelty prompted curiosity from potential clients, opening doors that might have stayed closed for yet another American or British company. The neutral Irish positioning also created advantages in emerging markets.

Lesson 2: M&A as a deliberate growth engine

ICON has completed 40+ acquisitions since 2000, building capabilities systematically rather than opportunistically. Each deal addressed specific strategic gaps—laboratory services, imaging, late-phase capabilities, geographic reach, technology platforms. This requires discipline: knowing what to buy, what to pay, and how to integrate.

Lesson 3: The power of industry tailwinds

Across the global pharma market, the overall CRO outsourcing penetration rate ranges from 45%-50%. When ICON was founded, outsourcing penetration was perhaps 20-25%. The company built on solid ground as the entire market expanded. Riding secular tailwinds compounds advantages over decades.

Lesson 4: Timing transformative deals

The PRA merger during COVID-19 proved prescient. The pandemic accelerated decentralized trial adoption, and PRA's capabilities in this area enhanced the combined company's competitive position. Strategic deals timed to industry inflection points create outsized value.

Lesson 5: Full-service beats point solutions

ICON systematically built end-to-end capabilities—from early-phase development through post-approval studies. This creates client stickiness (easier to use one partner than coordinate multiple vendors) and switching costs (data, relationships, and institutional knowledge accumulate).

Lesson 6: Patient capital allocation

Never paying a dividend, always reinvesting, compounding over 35 years—this approach won't appeal to income-seeking investors, but it enabled ICON to compound capital at attractive rates through multiple cycles.

XII. Competitive Landscape & Industry Dynamics

The global CRO services market is competitive, with leading players contributing to a significant share, including IQVIA Inc. (US), ICON Plc. (Ireland), Thermo Fisher Scientific Inc. (US), Laboratory Corporation of America Holdings (LabCorp) (US), WuXi AppTec Co., Ltd. (China), Charles River Laboratories International, Inc. (US), Pharmaron Beijing Co., Ltd. (China), Medpace, Inc. (US), and Eurofins Scientific (Luxembourg), among others.

IQVIA stands as ICON's primary competitor. In 2024, IQVIA generated revenues of US$15,405 million, reflecting a 2.8% growth compared to the previous year. This nearly doubles ICON's revenue, though IQVIA's business model differs—incorporating data and technology services alongside clinical research.

In 2016, Quintiles and IMS Health merged and rebranded as IQVIA, becoming the largest CRO in the world. As a leading global provider of advanced analytics, technology solutions and clinical research services to the life sciences industry, IQVIA has solidified its position at the forefront of the CRO world through a series of strategic acquisitions.

The competitive landscape continues consolidating:

Syneos Health, a global contract research organization (CRO) headquartered in Morrisville, will likely be sold to a consortium of private investment firms in a deal valued at $7.1 billion. The publicly traded company has signed a definitive agreement to be taken private by Elliott Investment Management, Patient Square Capital and Veritas Capital for $43 per share in cash plus outstanding debt.

In 2021, Icon bought PRA Health Sciences for about $12 billion in cash and stock. That followed LabCorp's $6 billion acquisition of Covance in 2015, the $9 billion merger of IMS Health and Quintiles in 2016 and Thermo Fisher's more recent purchases of Patheon for $7.2 billion.

Why consolidation? Several factors favor scale:

Global Reach Requirements: Modern trials span 50+ countries. Only large CROs can maintain the infrastructure, regulatory expertise, and site relationships required.

Technology Investment: Building competitive technology platforms (electronic data capture, remote monitoring, AI-enabled analytics) requires scale to amortize development costs.

Customer Concentration: Large pharma companies prefer working with CROs capable of handling their entire portfolio across therapeutic areas and geographies.

Data Advantages: Larger CROs accumulate more data on site performance, patient populations, and trial design—creating informational advantages for future work.

In 2024, ICON generated full-year revenues of $8,282 million, a year-on-year increase of 2.0%. In 2024, ICON embarked on a series of strategic acquisitions to expand its capabilities and market presence.

Medpace represents an interesting counterpoint. The mid-sized CRO has grown rapidly through organic expansion and a focus on close client relationships. Its success suggests the "bigger is always better" thesis isn't absolute—specialized positioning and superior execution can win against scale.

XIII. Porter's Five Forces & Strategic Analysis

Threat of New Entrants: LOW-MODERATE

Barriers to entry are substantial:

- Regulatory expertise: Building relationships with FDA, EMA, and other regulatory bodies takes years

- Global infrastructure: Establishing site networks across 50+ countries requires massive investment

- Technology platforms: Developing competitive clinical trial technology costs hundreds of millions

- Track record: Pharma companies prefer CROs with proven execution histories

However, specialty CROs can enter specific therapeutic areas or geographies. A CNS-focused CRO might compete effectively in that niche without matching ICON's global scale.

Bargaining Power of Suppliers: LOW-MODERATE

Key "suppliers" include: - Clinical investigators and sites: Fragmented supply with thousands of potential sites globally - Technology vendors: Competitive market with multiple alternatives - Skilled labor: This is the constraint—experienced clinical research professionals are scarce and mobile

The talent bottleneck deserves emphasis. The clinical research industry confronts an acute talent crisis, with 95% of cancer research centers reporting staffing issues that compromise trial quality and delay therapy development. Unfilled positions inflate labor budgets and delay site-initiation milestones.

Bargaining Power of Buyers: MODERATE-HIGH

Pharmaceutical companies are sophisticated, concentrated buyers. The top 20 pharma companies represent a disproportionate share of industry R&D spending. They can (and do) negotiate aggressively on pricing, play CROs against each other in competitive bids, and maintain multiple CRO relationships to ensure competition.

However, switching costs exist. Once a CRO is running trials, changing partners mid-stream is expensive and risky. Long-term relationships create stickiness.

Threat of Substitutes: LOW

The primary "substitute" is in-house clinical development. But the long-term trend runs strongly toward outsourcing—pharma companies are divesting internal capabilities, not building them. Currently, big pharma is outsourcing nearly half of all its R&D activities, while the share can even increase to 100 percent for smaller companies.

Competitive Rivalry: HIGH

Competition among established CROs is intense. ICON, IQVIA, Thermo Fisher (PPD), LabCorp, and others compete aggressively for major contracts. Differentiation is difficult—most large CROs offer similar services with comparable global reach.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Moderate. Larger CROs can amortize technology investments and maintain broader site networks, but the business remains fundamentally labor-intensive.

Network Effects: Limited. CRO value doesn't increase proportionally with more customers.

Counter-Positioning: ICON's PRA acquisition positioned it in decentralized trials ahead of competitors, though others are investing heavily to catch up.

Switching Costs: Moderate. Once embedded in a client's operations through FSP contracts or multi-study partnerships, displacement becomes difficult.

Branding: Limited in B2B context. Pharma companies select CROs based on capabilities and track record, not brand perception.

Cornered Resource: ICON's proprietary site networks (Accellacare) and MAPI's Clinical Outcomes Assessment library represent defensible assets.

Process Power: The accumulated institutional knowledge from running thousands of trials—knowing which sites perform, how to design protocols, where to recruit patients—creates advantages that are difficult to replicate.

XIV. Bull and Bear Case Analysis

Bull Case

-

Secular Tailwind Continuation: The outsourcing trend has decades to run. CRO outsourcing penetration ranges from 45%-50%—suggesting significant expansion potential as pharma companies continue divesting internal capabilities.

-

Decentralized Trial Leadership: COVID-19 accelerated hybrid/decentralized trial adoption permanently. The DCT market is expected to reach USD 21.34 Billion by 2030, rising at a CAGR of 14.16%. ICON's investments position it well for this shift.

-

Synergy Realization: The PRA integration appears successful. Investment grade credit rating achieved, free cash flow targets met, and margin expansion continuing.

-

Biotech Funding Recovery: The current biotech funding drought won't last forever. When capital returns to emerging pharma, trial volumes will increase.

-

AI/Technology Upside: Machine learning applications in trial design, patient recruitment, and monitoring could dramatically improve efficiency. Large CROs with data advantages may capture disproportionate benefits.

Bear Case

-

Biotech Funding Headwinds Persist: Bookings were below expectations due to delays in customer decision making, careful capital allocation and continued elevated cancellations. Extended biotech capital constraints would pressure growth and margins.

-

Customer Concentration Risk: Large pharma companies represent significant revenue concentration. Losing a major strategic relationship would materially impact results.

-

Integration Execution: Large acquisitions frequently underperform expectations. While PRA integration appears on track, realization of full synergies remains uncertain.

-

Competitive Pressure: IQVIA, Thermo Fisher (PPD), and others continue investing heavily. Pricing pressure may compress margins.

-

Geopolitical Risks: While U.S.-based companies continued to account for most trial starts in 2024, there has been a noteworthy increase in trials from China-headquartered companies, predominantly EBPs. U.S.-China tensions could disrupt trial operations and client relationships.

-

Leadership Transition: New CEO Barry Balfe takes the helm in October 2025. While internal promotion provides continuity, leadership changes introduce uncertainty.

XV. Key Metrics for Ongoing Monitoring

For investors tracking ICON's ongoing performance, three metrics deserve primary attention:

1. Book-to-Bill Ratio

This ratio—new bookings divided by revenue recognized—indicates demand trajectory. Consistently above 1.0 suggests growing backlog and future revenue visibility. Below 1.0 for extended periods signals demand weakness.

Gross business wins in the fourth quarter were $3,064 million and cancellations were $651 million. This resulted in net business wins of $2,413 million and a book to bill of 1.18.

Watch for: Trend direction, cancellation rates as percentage of gross wins, and comparison to peer metrics.

2. Adjusted EBITDA Margin

Margin trends reveal operating leverage and competitive positioning. Expanding margins suggest synergy capture and pricing power; compressing margins indicate competitive pressure or cost inflation.

Full year adjusted EBITDA of $1,735.8 million or 21.0% of revenue, representing a year on year increase of 2.5%.

Watch for: Year-over-year margin change, performance relative to guidance, and comparison to competitors.

3. Free Cash Flow Conversion

Strong free cash flow generation enables debt paydown, share repurchases, and continued M&A. Conversion rate (FCF as percentage of EBITDA) indicates capital intensity and working capital efficiency.

Cash management was strong in quarter four, bringing full year free cash flow in line with our targeted $1.1 billion.

Watch for: FCF versus net income relationship, capital intensity trends, and working capital movements.

XVI. Conclusion: What Kind of Company is ICON?

ICON represents a particular archetype: the disciplined consolidator in a secularly growing industry. The company doesn't invent drugs or breakthrough technologies. Instead, it builds operational capabilities—through acquisition, investment, and execution—that pharmaceutical companies increasingly need but don't want to own.

The business model is services at its core: recruiting ICON means renting access to global infrastructure, regulatory expertise, technology platforms, and thousands of skilled professionals. This creates both opportunity (recurring relationships, high switching costs) and limitation (labor intensity, competitive bidding pressure).

For investors, ICON offers exposure to pharmaceutical innovation without the binary outcomes of individual drug bets. As long as R&D spending continues—and demographic trends suggest it will—CROs will remain essential infrastructure. The question is whether ICON can maintain competitive position and earn attractive returns on capital as the industry continues consolidating.

The founders' original insight remains valid: clinical trial execution is complex enough that specialization creates value. Pharmaceutical companies face ever-more-demanding requirements—faster timelines, global reach, diverse patient populations, technology integration, regulatory expertise—that favor partners with scale and capabilities.

From five employees in a Dublin office to 42,000 employees across 55 countries, ICON has built something durable. Whether the next 35 years prove as successful as the first depends on execution—integrating PRA successfully, navigating the biotech funding cycle, maintaining innovation in trial technology, and sustaining the culture that enabled this improbable journey.

The sheep and cows still outnumber people in Ireland. But from that unlikely starting point, two doctors built a global powerhouse that helped deliver the world's first COVID-19 vaccine. That story—of vision, execution, and patient capital allocation—offers lessons for builders and investors alike.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube