Fresenius Medical Care: The Dialysis Giant Building Healthcare's Most Durable Moat

I. Introduction & Episode Roadmap

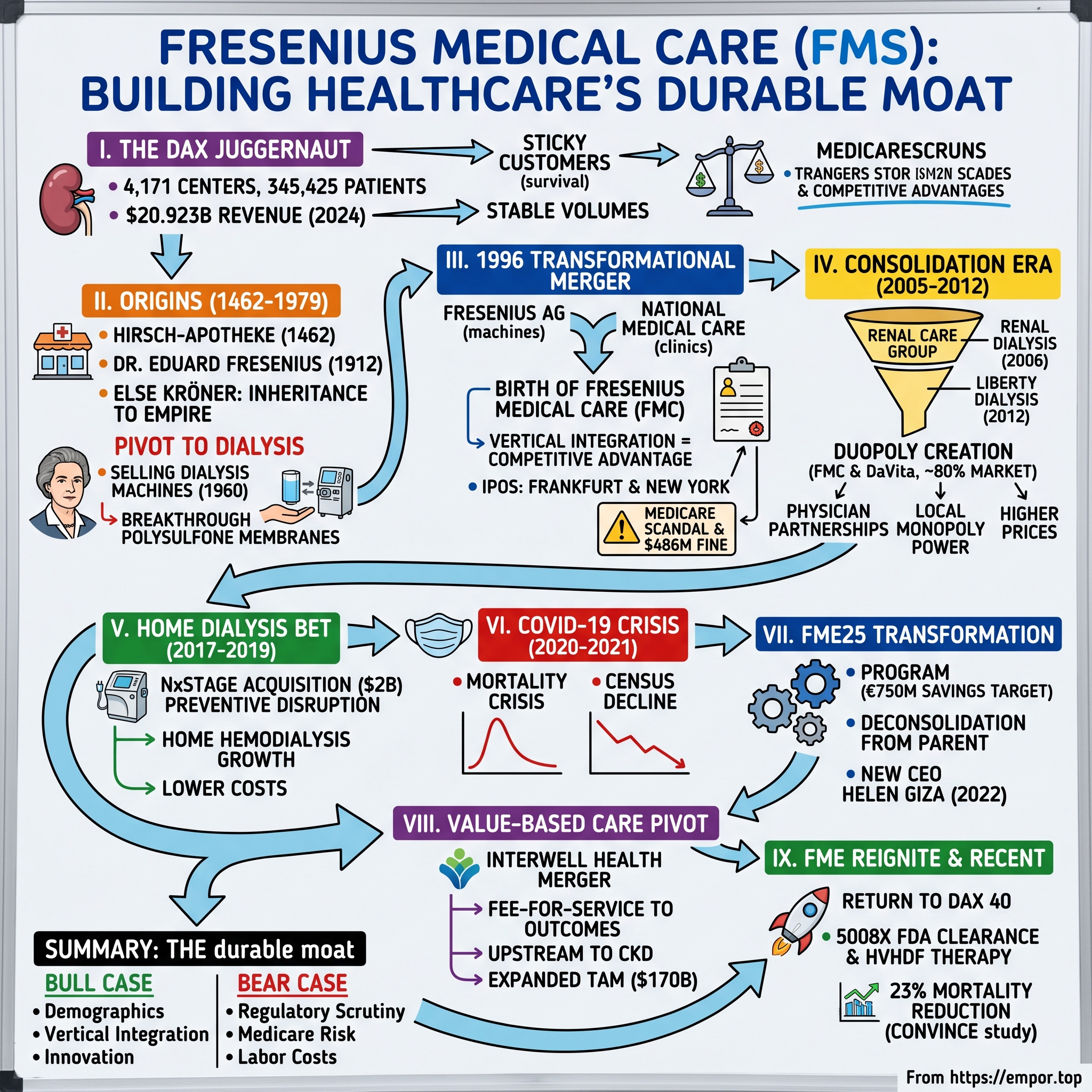

Picture a German healthcare company that has quietly constructed one of the most defensible business models in modern medicine. Fresenius Medical Care AG provides kidney dialysis services through a network of 4,171 outpatient dialysis centers, serving 345,425 patients. The company primarily treats end-stage renal disease (ESRD), which requires patients to undergo dialysis 3 times per week for the rest of their lives.

This is the ultimate "sticky customer" business—when your patients literally need you to survive, the calculus of customer retention takes on an entirely different dimension. Unlike a subscription software company worried about monthly churn or a retailer concerned with same-store sales, Fresenius operates in a realm where the switching costs are measured not in dollars but in life expectancy.

With a global headquarters in Bad Homburg vor der Höhe, Germany, and a North American headquarters in Waltham, Massachusetts, the company holds a 38% market share of the dialysis market in the United States. But how did a German pharmaceutical company become America's largest dialysis provider? The answer lies in a century-long story of technological innovation, audacious dealmaking, and an understanding that healthcare, at its core, is about building infrastructure that becomes indispensable.

This healthcare powerhouse generated $20.923 billion in revenue for 2024. That's not a small pharmaceutical company—it's a healthcare juggernaut that few outside the medical industry truly understand. Yet the company faces a fundamental question that investors must grapple with: Is this the most defensible healthcare business ever built, or a regulatory house of cards dependent on Medicare reimbursement rates and susceptible to technological disruption?

The story of Fresenius Medical Care encompasses five major strategic phases: the century-long evolution from a Frankfurt pharmacy to a dialysis pioneer; the transformational 1996 merger that created the modern company; the consolidation era that built an American duopoly; the COVID-19 crisis that threatened the business model's foundations; and the current transformation under CEO Helen Giza that is reshaping the company for a new era of value-based care and technological innovation.

II. Origins: From Pharmacy to Dialysis Pioneer (1462-1979)

The story begins not in a modern laboratory, but in the cobblestone streets of medieval Frankfurt. The world was quite a different place when the Hirsch Pharmacy in Frankfurt am Main opened its doors in 1462. That pharmacy, one of the oldest apothecaries in the city, would eventually become the seed from which a global healthcare empire grew—though it would take nearly five centuries for that transformation to begin in earnest.

The Hirsch Pharmacy has a long tradition: Its history can be traced back to the 15th Century. The Fresenius family becomes the owners in the 1870s. But the true founding moment came on October 1, 1912. The pharmacist Dr. Eduard Fresenius founded the pharmaceutical company Dr. E. Fresenius. The location of his business was the Hirsch Pharmacy. The date he chose to open his business had a special significance for him because on that same day, October 1, the Hirsch Pharmacy had celebrated its 450th anniversary.

Dr. Fresenius was a man ahead of his time—not just in pharmaceutical innovation, but in marketing. As a leading global healthcare group we are dedicated to medicine and human health - values we have upheld since our founding as a pharmacy lab in 1912. Operated by the Hirsch Pharmacy under Dr. Eduard Fresenius, a service for delivering products by automobile was something special at the time the company was founded in Frankfurt. In an age of horse-drawn carriages, Fresenius understood that speed of delivery could differentiate his pharmaceutical business.

The company's early decades were marked by modest but steady growth, interrupted by the chaos of world war. During the Second World War he loses contact with a lot of important business partners. He does not join the Nazi party. Supplying the German army with medications like the Freka frostbite cream helps for a time to maintain company production.

The war's end found Eduard Fresenius standing before ruins. The end of the war finds Eduard Fresenius standing before the rubble that was his existence: Allied bombs have completely destroyed the Hirsch Pharmacy. Raw material shortages make production in Bad Homburg impossible. In the midst of reorganizing the company, Dr. Fresenius dies suddenly in 1946. He names his foster daughter, Else Kröner, née Fernau, as benefactor of his estate. Just 26 years old, she inherits the Hirsch Pharmacy and the leadership of the company.

The Remarkable Story of Else Kröner

The inheritance that Else Kröner received was less a gift than a burden. Else Kröner was one of Germany's most successful entrepreneurs. Starting with the Hirsch-Apotheke pharmacy in Frankfurt and a small pharmaceutical business, she built up the Fresenius healthcare group that operates worldwide. Else Kröner (1925 – 1988) not only laid the foundations for...

Our founding benefactress is born on May 15, 1925 in Frankfurt am Main bearing the name Else Fernau. Her mother, Therese Fernau, is housekeeper at the home of pharmacist Dr. Eduard Fresenius, and lives there in an attic apartment with her husband and daughter, Else. The story of how a housekeeper's daughter came to inherit and rebuild a pharmaceutical empire is one of the most remarkable in German business history.

Disregarding advice that she should decline the legacy, Else Fernau assumed responsibility for the pharmacy and the company when she was only 21. The Fresenius company was heavily indebted, and all but 30 of the original 400 employees had to be let go. She succeeded in saving the company, and along with Dr. Hans Kröner, who later became her husband, rebuilt and significantly expanded Fresenius.

As a newly licensed pharmacist, Else Kröner knew her way around pharmaceutics, but when it comes to business management she soon reached her limits. She obtained the needed skills by attending evening classes at a private business school in Frankfurt. She spent nearly 12 hours a day in the company and doggedly worked to rebuild the firm during difficult years. Her efforts earned her a great deal of respect and admiration among the staff.

The Pivot to Dialysis

The decision that would define Fresenius's future came in 1960. Fresenius starts to sell dialysis machines and dialyzers manufactured by various foreign companies and gains substantial market shares. This was a pivotal moment—rather than trying to compete as a generic pharmaceutical manufacturer, Fresenius recognized that the emerging field of dialysis represented an enormous unmet medical need.

At the time, end-stage kidney disease was essentially a death sentence. Dialysis was a new technology, expensive and rare. But Else Kröner and her husband Dr. Hans Kröner saw something that others missed: this wasn't just a treatment—it was life support. And any company that could master the technology and scale its delivery would create something close to an indispensable franchise.

Production of the A2008 dialysis machine begins in a newly acquired factory in Schweinfurt. The machine is awarded a gold medal at the Leipzig Trade Fair that year. The A2008 wasn't just a product—it was a statement. Fresenius had transitioned from distributor to manufacturer, from middleman to innovator.

Fresenius begins producing synthetic polysulfone fiber membranes for blood purification. These membranes represented a quantum leap in dialysis technology. Polysulfone dialyzers are particularly effective at cleaning the patient's blood and still set the industry standard to this day. In the early 1980s, this breakthrough opened up a new era in the treatment of kidney disease.

By the time of her death in 1988, Else Kröner had transformed a near-bankrupt pharmacy into a growing healthcare company. In 1983, Else Kröner founds the Else Kröner-Fresenius Foundation (EKFS), dedicated to advancing medical research and supporting humanitarian projects. When she dies unexpectedly on June 5, 1988, her entire estate passes to the foundation – as per her testament.

For investors: The early Fresenius story illustrates a crucial strategic pattern—the company didn't try to win by being the biggest or cheapest. Instead, it identified an emerging market with enormous barriers to entry (medical devices require regulatory approval, clinical validation, and physician adoption) and invested in becoming the technological leader. This pattern of technical excellence combined with vertical integration would define the company's strategy for the next four decades.

III. The Transformational Merger: Birth of Fresenius Medical Care (1996)

In 1996, the dialysis industry stood at an inflection point. Fresenius had established itself as the premier dialysis equipment manufacturer in Europe, but its footprint in the world's largest healthcare market—the United States—remained modest. Meanwhile, across the Atlantic, W.R. Grace & Co., the American conglomerate known primarily for chemicals and packaging, operated a subsidiary called National Medical Care that had built something remarkable: a network of dialysis clinics serving tens of thousands of American patients.

The coming together of these two companies would create a new category of healthcare company—one that both made the machines and operated the clinics, captured value at every point in the dialysis value chain.

Everything begun with the merger of the dialysis business of Fresenius and the American dialysis services provider National Medical Care on September 30, 1996; directly followed by the initial public offering in Frankfurt and New York at the beginning of October. In 1996, the merger of Fresenius' dialysis business with the U.S. dialysis provider National Medical Care resulted in the creation of Fresenius Medical Care, the world's leading dialysis provider. Its shares are traded on the Frankfurt and New York stock exchanges. At the time of the acquisition, National Medical Care operated about 500 clinics, and treated some 40,000 patients.

The Deal Structure

The merger was structured with a sophistication that reflected both companies' tax and strategic considerations. Baxter International Inc. officials were left scratching their heads Monday after being jilted in their bid to acquire the National Medical Care division of W.R. Grace & Co. Grace announced Monday that it had agreed to combine its dialysis business with that of Fresenius AG of Germany, in a deal in which Grace would receive $2.3 billion.

Baxter, the American healthcare giant, had publicly offered $3.8 billion for National Medical Care. Baxter International Inc.'s $3.8 billion offer for National Medical Care, W.R. Grace & Co.'s kidney dialysis business, was rejected over the weekend as Grace chose instead to combine the unit with a third company. Grace's decision blew apart Baxter's strategy. The health care giant made its offer public last Friday in an effort to force the issue. Grace agreed to combine National Medical with the dialysis unit of Germany's Fresenius AG, a deal that will yield $2.3 billion for Grace and allow it to retain a stake in the business.

Why would Grace accept the lower offer? The Fresenius proposal calls for W. R. Grace to spin off National Medical and merge it into Fresenius Medical Care, a new company based in Germany. Grace shareholders would own 44.8 percent of the new company. The Fresenius structure allowed Grace shareholders to participate in the combined company's future upside while generating immediate liquidity—a tax-efficient outcome that pure cash couldn't match.

The Strategic Genius

The strategy of combining the two parts of the business – the product development side as well as the care provider side – proved highly successful lots of achievements were made in years that followed.

The combination was strategic brilliance: German engineering excellence in dialysis machines and consumables combined with American operational scale in service delivery. Fresenius brought technological superiority—its dialyzers and machines were the gold standard. National Medical Care brought patient relationships, clinic infrastructure, and deep expertise in navigating the American healthcare system, particularly Medicare reimbursement.

The asbestos plaintiffs have filed suit against companies that acquired businesses spun off by Grace in the late 1990s: Sealed Air Corp., a Saddle Brook, N.J., packaging-materials company that merged with former Grace unit Cryovac Inc. in 1998, and Fresenius Medical Care Holdings Inc., a subsidiary of Germany-based Fresenius Medical Care AG, which took over Grace's National Medical Care Inc. business in a $4.4 billion merger in 1996.

Early Challenges: The Medicare Scandal

In 1996, Fresenius SE & Co. KGaA merged its dialysis business into W.R. Grace's National Medical Care to form Fresenius Medical Care. In 2000, the company pleaded guilty to billing Medicare for unnecessary medical tests and to paying kickbacks for lab business and paid a $486 million fine.

The $486 million fine was a stark reminder that the dialysis business operates under intense regulatory scrutiny. The issues related to National Medical Care's pre-merger practices, but Fresenius Medical Care bore the consequences. The scandal underscored a fundamental truth about the dialysis business: operating in America means operating under Medicare's watchful eye, and any misstep can prove enormously costly.

For investors: The 1996 merger established the template for Fresenius Medical Care's competitive advantage: vertical integration. By controlling both products (machines, dialyzers, pharmaceuticals) and services (clinic operations), the company created multiple profit pools and operational synergies that pure-play competitors couldn't match. However, the early compliance issues also highlighted the regulatory risk inherent in a business so dependent on government reimbursement.

IV. The Consolidation Era: Building the Duopoly (2005-2012)

The years following the merger saw Fresenius Medical Care pursue an aggressive consolidation strategy that would reshape the American dialysis landscape. What emerged was not the fragmented market of small providers that had characterized dialysis in its early decades, but a concentrated duopoly dominated by just two players: Fresenius and its rival DaVita.

Between 2005 and 2019, the market share of DaVita and Fresenius increased from 59.1% to 77.1%, with 32.5% of the national population living in a hospital service area without access to a dialysis facility other than the... The combined share of DaVita and Fresenius increased from 59.1% in 2005 to 77.1% in 2019, while the share owned by independent facilities decreased from 20.4% to 10.6%.

The Renal Care Group Acquisition (2006)

Strategic Acquisitions: Key acquisitions, such as Renal Care Group in 2006, significantly expanded Fresenius Medical Care's market share and service capabilities in North America.

The Renal Care Group acquisition was transformational. Fresenius Medical Care takes over U.S. dialysis care provider Renal Care Group. Through its network of approximately 2,000 dialysis clinics in North America, Europe, Latin America, Asia-Pacific and Africa, Fresenius Medical Care provides dialysis treatment to approximately 157,000 patients around the globe.

The Liberty Dialysis Acquisition (2012)

In February 2012, the company acquired Liberty Dialysis Holding, which added 201 clinics, for $1.5 billion. In March 2012, Rice Powell was appointed CEO.

The Liberty Dialysis acquisition came just as Rice Powell took the helm. Powell had joined Fresenius Medical Care in 1997 and worked his way up through the organization. Rice Powell joined Fresenius Medical Care in 1997, and as CEO of Fresenius Medical Care North America was appointed to the Management Board of Fresenius Medical Care in 2004. He has been the company's CEO since January 1, 2013.

The Duopoly Takes Shape

During this era of outpatient growth, two dominant players emerged in the dialysis space: DaVita and Fresenius, which collectively control approximately 80% of the U.S. dialysis market with a combined 7,000 clinics in their global operations.

The economics of duopoly were compelling for both companies. During this period, markets with only 1 large chain had $495.08 higher commercial prices for outpatient hemodialysis and $564.56 higher medical director compensation per patient compared to markets without large chain facilities.

More recently, according to the study, the largest dialysis chains have enhanced their financial ties with doctors by offering ownership stakes in facilities and paying substantially higher salaries to serve as medical directors. Among the specific findings reported by corresponding author Ryan C. McDevitt, Ph.D., a professor at Duke University's Fuqua School of Business in Durham, North Carolina, and colleagues: Between 2005 and 2019, a period when both DaVita and Fresenius made several large acquisitions, their combined market share increased from 59.1% to 77.1%, while the share owned by independent facilities decreased from 20.4% to 10.6%.

In 2019, 32.5% of the national population lived in a hospital service area without access to a dialysis facility other than DaVita or Fresenius, including 99% in the state of Minnesota. The share of facilities with a physician owner increased from 11.4% to 29.1% over the study period.

The Physician Partnership Model

The consolidation wasn't just about buying clinics—it was about building relationships with the nephrologists who referred patients. The average owner of a DaVita facility owned 2.8 DaVita facilities and no others, while the average owner of a Fresenius center owned 4.19 Fresenius facilities and virtually no others. The portion of physician-owned facilities that are jointly owned by chains, referred to as joint ventures, increased from 4.6% in 2005 to 23.7% in 2019.

For investors: The consolidation era created extraordinary value for Fresenius shareholders by establishing what economists call "local monopoly power." In many markets, patients have limited alternatives to Fresenius or DaVita, creating pricing power with commercial insurers and stable volumes. However, this market structure has increasingly attracted regulatory scrutiny—a risk that would manifest more fully in subsequent years.

V. The Home Dialysis Bet: NxStage Acquisition (2017-2019)

By 2017, Fresenius Medical Care faced a strategic challenge: the in-center dialysis model that had built its empire might not be the future of kidney care. Home dialysis, long a niche modality, was gaining momentum—driven by patient preference, policy changes, and technological improvements that made home treatment safer and more practical.

Acquisition of NxStage Medical, Inc. would: position Fresenius Medical Care as a global leader in home dialysis, establish U.S. presence in the critical care space, further enhance clinical outcomes and patient empowerment, support strategic initiative of vertical integration and Care Coordination. Fresenius Medical Care, the world's largest provider of dialysis products and services, has signed an agreement to acquire NxStage Medical, Inc., (NxStage) (Nasdaq: NXTM) a U.S.-based medical technology and services company. NxStage, which just like Fresenius Medical Care North America, has its headquarters in the Boston, Massachusetts area, was founded in 1998 and has approximately 3,400 employees. It develops, produces and markets an innovative product portfolio of medical devices for use in home dialysis and in the critical care setting. In 2016, NxStage delivered USD 366 million in revenue.

The Strategic Rationale

"The combination of Fresenius Medical Care's industry leadership with NxStage's innovative products and employees has the potential to significantly advance the standard of care for patients around the world," said Jeff Burbank, Founder and CEO of NxStage Medical, Inc. "Fresenius Medical Care would like us to continue doing what we do best, and a lot more of it. I strongly believe our opportunities would be greater working together for the benefit of patients, customers and shareholders." "Home dialysis is a critical component of renal care, and this acquisition would help us accelerate growth and innovation in this important modality," said Bill Valle, CEO of Fresenius Medical Care North America.

Fresenius Medical Care announced Tuesday it has completed the $2 billion purchase of home dialysis devicemaker NxStage Medical.

The deal closed in February 2019 after extensive regulatory review. WALTHAM, MASS. – Feb. 26, 2019 – Fresenius Medical Care, the world's largest provider of dialysis products and services, has successfully completed the acquisition of NxStage Medical, Inc. (NxStage), following approval by antitrust authorities in the United States. NxStage develops, produces and markets an innovative product portfolio of medical devices for use in home dialysis and critical care. The acquisition will enable Fresenius Medical Care to leverage its manufacturing, supply chain and marketing competencies across the dialysis products, services and Care Coordination businesses in a less labor- and capital-intensive care setting.

The Home Dialysis Opportunity

The case for home dialysis is compelling: it's up to 5 times cheaper than in-clinic dialysis, is favored by most nephrologists, and is less stressful for patients. For Fresenius, the NxStage acquisition served multiple purposes: it neutralized a potential competitive threat, gave the company a leading position in a growing segment, and provided optionality if policy changes accelerated the shift to home-based care.

In September 2024, Fresenius Medical Care reported over 14,000 U.S. patients utilizing its NxStage systems for home hemodialysis, while launching the upgraded NxStage VersiHD with GuideMe Software to enhance user experience.

For investors: The NxStage acquisition illustrates Fresenius's strategic approach: identify potential disruptors and acquire them before they can erode the core business. Home dialysis remains a small percentage of total treatments, but the acquisition ensures Fresenius will participate in any shift toward home-based care rather than be disrupted by it.

VI. Key Inflection Point #1: The COVID-19 Crisis (2020-2021)

When COVID-19 swept across the world in early 2020, few patient populations faced greater risk than those on dialysis. These patients—older, immunocompromised, and required to gather in clinical settings three times weekly—were sitting ducks for a respiratory virus that spread through close contact.

I caught the last flight out of Frankfurt on a Friday in March. The airport was unnaturally quiet, the flight surprisingly calm. But as soon as we landed in Boston, my phone lit up. "Rice," a friend said, "get ready. There are decisions to be made." As the CEO of Fresenius Medical Care, I am responsible for 350,000 patients. They suffer from end-stage kidney disease, need regular dialysis to survive, and are generally older and less healthy than the average population. With COVID-19 spreading like wildfire, our patients needed to get tested quickly.

The Mortality Crisis

Among 41,257 patients receiving maintenance dialysis, all-cause hospitalization dropped abruptly in March/April 2020 and increased thereafter, albeit remaining below prepandemic rates. All-cause mortality exhibited typical seasonal variability during 2018-2019, subsequently increasing with onset of the COVID-19 pandemic in March 2020. Mortality peaked in January 2021 at 228 deaths per 1,000 person-years before declining to 151 deaths per 1,000 person-years in March 2021.

Studies in China, Italy, the United Kingdom, and the United States (New York and southern California) showed that maintenance dialysis patients with COVID-19 experience higher mortality and more severe disease than the general population.

Mortality was 22% among COVID-19 patients with odds ratios 219.8 to 342.7, compared to matched patients without COVID-19.

During the COVID-19 pandemic, around 25% of infected dialysis patients died, exceeding general population rates. This led to the first decline in the U.S. dialysis patient census due to excess deaths and treatment disruptions.

The Census Decline

For the first time in company history, Fresenius Medical Care faced a decline in patient census. Throughout 2020, the excess mortality trend significantly accelerated, particularly in the U.S. and in EMEA, especially in November and December 2020, accumulating to approximately 10,000 patients over the pre-pandemic baseline.

In early 2020, an excess mortality of 15% to 20% (corresponding to 7,000–10,000 deaths) was observed in the U.S. population on dialysis. This wasn't just a humanitarian tragedy—it was an existential threat to a business model predicated on a growing patient population.

The Home Dialysis Advantage

438 of 7948 (5.5%) maintenance dialysis patients developed COVID-19. Male sex, Black race, in-center dialysis (vs home dialysis), treatment at an urban clinic, residence in a congregate setting, and greater comorbidity were associated...

Relative to in-facility hemodialysis, home dialysis was associated with 36%–60% lower odds of all events during weeks 12–23 of 2020. The pandemic validated the strategic logic of the NxStage acquisition—home dialysis wasn't just a preference issue; it was a safety issue.

For investors: COVID-19 represented the most significant business disruption in Fresenius Medical Care's history. The patient census decline demonstrated that even the most "sticky" customer base can erode under extreme circumstances. However, the crisis also accelerated strategic initiatives (home dialysis, value-based care, operational efficiency) that would prove beneficial post-pandemic.

VII. Key Inflection Point #2: The FME25 Transformation & Deconsolidation (2021-2024)

As the pandemic's worst effects began to recede, Fresenius Medical Care embarked on the most ambitious transformation in its history. The FME25 program, launched in 2021, aimed to fundamentally restructure the company's operating model while achieving significant cost savings. But even more dramatic was the decision to deconsolidate from its parent company, creating an independent Fresenius Medical Care for the first time since 1996.

The FME25 Program

Fresenius Medical Care has increased the savings target for its FME25 transformation program from €500 million to €650 million by 2025 and now expects to invest up to €650 million in the same period. By the end of 2022, Fresenius Medical Care delivered €131 million (on EBIT level) of sustainable savings under the FME25 program, exceeding the original target of €40 to 70 million for the same period.

As part of the FME25 program, Fresenius Medical Care transformed its operating model into a simplified structure with two global operating segments—Care Enablement and Care Delivery—providing the basis for the acceleration of innovation and future sustainable profitable growth.

The FME25 transformation program reached annual sustainable savings of EUR 346 million, ahead of our initial plan for the year (EUR 250 to 300 million). Related one-time costs were EUR 153 million in 2023, adding up to EUR 420 million since... the start of the program in 2021. The FME25 transformation program reached annual sustainable savings of EUR 346 million, ahead of our initial plan for the year (EUR 250 to 300 million). Related one-time costs were EUR 153 million in 2023, adding up to EUR 420 million since the start of the program in 2021.

The Deconsolidation

Intention to deconsolidate Fresenius Medical Care The company plans to deconsolidate Fresenius Medical Care by changing Fresenius Medical Care's legal form to a German Stock Corporation ("Aktiengesellschaft"). Subject to the necessary shareholder approvals and the registration with the commercial register, the conversion is expected to become effective by the end of the 2023 financial year at the latest. Following the planned change in its legal form, Fresenius Medical Care will no longer be part of the fully consolidated subsidiaries of Fresenius. Fresenius' will continue to hold a 32 percent stake in the share capital of Fresenius Medical Care.

The shareholders of Fresenius Medical Care had already approved the change in legal form from a partnership limited by shares (KGaA) to a stock corporation (AG) by a majority of more than 99% at an Extraordinary General Meeting held on July 14, 2023. Following the change in legal form, Fresenius Medical Care is no longer part of the consolidated subsidiaries of Fresenius. Fresenius continues to hold 32 percent of Fresenius Medical Care's share capital and therefore remains the company's largest shareholder.

The change in legal form was entered in the commercial register on November 30, 2023.

Leadership Transition

The transformation required new leadership. Helen Giza (54) has been appointed Chief Executive Officer of Fresenius Medical Care, the world's leading provider of products and services for individuals with renal diseases, with immediate effect. Previously, she was Deputy CEO of Fresenius Medical Care. The Supervisory Board of Fresenius Medical Care Management AG unanimously appointed her to succeed Dr. Carla Kriwet (51), who will leave the company at her own request and by mutual agreement due to strategic differences.

Helen Giza was appointed Chief Executive Officer effective December 6, 2022. She continued to serve as acting Chief Financial Officer until September 30, 2023. Helen Giza joined Fresenius Medical Care in 2019 as Chief Financial Officer and took on the additional role of Chief Transformation Officer heading the FME25 transformation program in 2021. Previously, she has been Chief Integration and Divestiture Management Officer at Takeda Pharmaceuticals since 2018. Before joining the Takeda Corporate Executive Team, she served as Chief Financial Officer of Takeda's U.S. business unit since 2008. Prior to that she held a number of key international finance and controlling positions, amongst others at TAP Pharmaceuticals and Abbott Laboratories. Helen Giza is a U.K. Chartered Certified Accountant and holds a Master of Business Administration from the Kellogg School of Management at Northwestern University in Evanston, Illinois, USA.

Execution Results

Net financial leverage ratio reduced from 3.2x to 2.9x and dividend is planned to be raised by 21% High teens to high twenties percent earnings growth in 2025, translating into an 11 to 12% margin · Bad Homburg, Germany (February 25, 2025) – "Fresenius Medical Care has again delivered against its commitments and we met the top end of our 2024 target to profitably grow our business. We successfully executed against our strategic turnaround and transformation plan, advancing our legacy portfolio optimization and realizing significant FME25 savings ahead of plan. The momentum we have created enables us to further raise our FME25 savings target from EUR 650 million to EUR 750 million", said Helen Giza, Chief Executive Officer of Fresenius Medical Care AG. "Our continued focus on improving operational performance resulted in meaningful progress in the operating income margin towards our 2025 margin targets.

For investors: The FME25 transformation and deconsolidation represent the most significant structural changes since the 1996 merger. The program continues well on track to achieving the targeted €750 million of sustainable annual savings by year end 2025. The deconsolidation gives Fresenius Medical Care greater strategic flexibility and clearer accountability, while the cost savings are translating directly to improved margins.

VIII. Key Inflection Point #3: Value-Based Care Pivot (2022-Present)

Perhaps the most profound strategic shift in Fresenius Medical Care's recent history is its pivot toward value-based care—a fundamental reimagining of how the company creates and captures value in the kidney care ecosystem.

CAMBRIDGE, Mass., Aug. 24, 2022 /PRNewswire/ -- InterWell Health today announced it has completed a three-way merger between Fresenius Medical Care's value-based care division, Fresenius Health Partners; InterWell Health, a leading physician organization driving innovation in the kidney care industry; and Cricket Health, a provider of value-based kidney care with an industry-leading patient engagement and data platform. The new independent company, which will operate under the InterWell Health brand, will set the standard in value-based kidney care by partnering with a patient's nephrologist, improving their care delivery throughout the entire spectrum of their journey with kidney disease. With extraordinary capabilities, expertise, and reach, the new company expects to improve health outcomes for individuals with kidney disease and reduce costs to public and private payers, health systems, and all others that take risk for this vulnerable and complex patient population.

The InterWell Health Merger

The transformative deal brings together InterWell Health's strong network of more than 1,600 nephrologists, Cricket Health's technology-enabled care model and patient engagement platform, and the expertise in value based kidney care contracting of Fresenius Health Partners, the value based care division of Fresenius Medical Care North America, to create an innovative, stand-alone entity poised to transform kidney care. The new organization is valued at $2.4 billion and will operate under the InterWell Health brand. With a total addressable market of $170 billion, more than $6 billion of medical costs under management, and over 100,000 covered lives, the new company will accelerate growth in the mid- and late-stage chronic kidney disease value based care population and will build upon a strong foundation of success to accelerate the transformation of kidney care.

With the completion of the merger, the new company expects to engage and manage the care of more than 270,000 Americans living with kidney disease with more than USD 11 billion in costs under management by 2025, an increase from 100,000 covered lives and USD 6 billion currently under management. The strategic expansion along the Renal Care Continuum significantly expands InterWell Health's total addressable market in the U.S. from approximately USD 50 billion to USD 170 billion.

InterWell Health will be the premier value-based kidney care provider in the U.S., combining and leveraging innovative new tools, vast experience, and a deep nephrologist network. By further expanding into the strategically important chronic kidney disease stage-3-to-5-market, we will be able to support even more patients throughout the Renal Care Continuum, inc...

The Strategic Logic

The shift from fee-for-service to outcomes-based care represents both an opportunity and a necessity for Fresenius Medical Care. Under traditional fee-for-service, the company gets paid for each dialysis treatment delivered—an incentive structure that rewards volume over outcomes. Value-based care flips this model: the company takes on risk for patient outcomes and total cost of care, creating alignment between financial performance and clinical excellence.

IWH has emerged as the leader in the renal value-based care industry, partnering with over 2,200 nephrologists in the U.S. and experiencing revenue growth of 23.5% in the first half of 2024.

For investors: The value-based care pivot represents Fresenius Medical Care's answer to the fundamental question facing all dialysis providers: how do you grow in a market where your customers are chronically ill and your treatments, while life-sustaining, don't cure anyone? By expanding "upstream" into chronic kidney disease management, Fresenius can engage patients earlier, potentially slow disease progression, and capture value across the entire care continuum.

IX. The FME Reignite Strategy & Recent Developments (2024-2025)

Bad Homburg (December 20, 2024) - Fresenius Medical Care (FME), the world's leading provider of products and services for people with kidney disease, will return to the top tier of the German Stock Index, the DAX 40, as of December 27, 2024. The index represents the performance of the 40 largest... publicly traded companies listed on the Frankfurt Stock Exchange and accounts for around 80 percent of the market capitalization of listed stock corporations in Germany.

Fresenius Medical Care has been currently listed in the second-largest German stock market index, the Mid-Cap DAX (MDAX), which tracks the 50 largest companies below the DAX 40 since March 2023. Prior to this, the company had been a member of the DAX since September 1999.

The return to the DAX 40 symbolized the company's turnaround under Helen Giza's leadership. Helen Giza, CEO and Chair of the Management Board of Fresenius Medical Care AG, said: "We are delighted to return to the DAX 40. In Germany and worldwide, the index is synonymous with German innovative strength and entrepreneurial growth. This recognition underscores the continuous hard work of our employees for our patients and shareholders and is a strong testament of our performance. Our path had been defined always very clearly to return to the large-cap index by turning around the performance and by successfully executing...

The 5008X and HVHDF Revolution

Perhaps the most significant product development in years came with the FDA clearance of the 5008X dialysis system. Introducing the 5008X CAREsystem and hemodiafiltration kidney replacement therapy is a key pillar of the company's growth strategy · BAD HOMBURG, Germany, June 4, 2025 /PRNewswire/ -- Fresenius Medical Care (FME), the world's leading provider of products and services for individuals with renal diseases, today begins the second phase of the company's efforts to introduce high-volume hemodiafiltration (HVHDF) kidney replacement therapy across the United States. The company last week received FDA 510(k) clearance for the updated version of its new, hemodiafiltration-capable 5008X CAREsystem with additional features, a key benchmark enabling the next steps in the company's broader commercialization efforts across the U.S. later this year, followed by a full-scale commercial launch in 2026.

The results of the groundbreaking CONVINCE study demonstrated that patients treated with high-volume hemodiafiltration experienced a remarkable 23% decrease in mortality rates compared to those treated with the more commonly used high-flux hemodialysis. Funded by the European Union, the CONVINCE study was a multinational research study that compared these two types of hemodialysis techniques in a three-year trial performed at 61 dialysis centers in eight European countries.

By 2030, the Company expects to have replaced all existing 2008T dialysis machines in its own U.S. clinic network with the innovative 5008X machine, offering the new standard of care to all its eligible dialysis patients. Following an increasing penetration of HVHDF treatments, clinic operations are expected to benefit from reduced mortality rates, machine-related clinic labor and supply efficiencies and potential for reduced drug usage. As the manufacturer of the 5008X machine, the first and until today only FDA-cleared hemodiafiltration machine, Fresenius Medical Care expects to benefit from its strong U.S. market leader position in the currently installed machine base and to further increase its captive market share in disposable products.

2025 Performance

Bad Homburg, Germany (November 4, 2025) – "In Q3 of 2025, we continued the momentum and further accelerated revenue growth. Conversion into operating income growth increased as planned for the third consecutive quarter, underlining our continued operational and financial progress. Our Group operating income margin of 11.7% extended well into the implied full year 2025 range of 11% to 12%. This demonstrates important progress on our trajectory to deliver our full year 2025 financial outlook", said Helen Giza, Chief Executive Officer of Fresenius Medical Care AG. "All three operating segments contributed to the Group organic growth of 10%. U.S. same market treatment growth was slightly positive in Q3.

As of September 30, 2025, Fresenius Medical Care treated 293,620 patients in 3,628 dialysis clinics worldwide and had 109,916 employees (headcount) globally, compared to 112,445 employees as of June 30, 2025.

For investors: The combination of the 5008X launch, continued FME25 savings, and operational turnaround positions Fresenius Medical Care for sustainable profitable growth. The HVHDF technology represents a genuine clinical advancement that could differentiate Fresenius from competitors while improving patient outcomes—a rare alignment of clinical and commercial interests.

X. The Business Model Deep Dive

Vertical Integration

Fresenius Medical Care has constructed perhaps the most vertically integrated business model in healthcare. The company manufactures the machines, produces the dialyzers, operates the clinics, and increasingly manages the patient's entire care journey through value-based arrangements.

Today, every second dialyzer worldwide has been built by our company. Fresenius Medical Care has manufactured more than two billion dialyzers—a staggering number that reflects both the scale of the dialysis market and the company's dominance in it.

It also operates 42 production sites, the largest of which are in the U.S., Germany, and Japan.

Revenue Composition

In 2024 the company made a revenue of $20.80 Billion USD a decrease over the revenue in the year 2023 that were of $21.11 Billion USD.

The revenue breakdown reflects the company's integrated model: - Care Delivery (clinic services): approximately 75% of revenue - Care Enablement (products/equipment): approximately 25% of revenue - Geographic split: U.S. dominance (~70% of revenue)

The Medicare Dependency

The government is a substantial payer for dialysis under the End-Stage Renal Disease (ESRD) Program. Medicare covers virtually all ESRD patients regardless of age—unique in U.S. healthcare. This creates a stable, predictable revenue stream but also concentrates regulatory risk.

Moreover, the provision of dialysis services in the country is supported by government initiatives like Medicare and Medicaid. Medicare covers a substantial portion of dialysis costs for patients suffering from ESRD. This reimbursement framework provides financial security for the dialysis service providers and makes it easier for patients to avail these services.

XI. Porter's 5 Forces & Hamilton's 7 Powers Analysis

Porter's 5 Forces

1. Threat of New Entrants: LOW

The dialysis chains segment held the largest market share of 82.9% in 2024, owing to their extensive networks and operational efficiencies. Established chains, such as DaVita and Fresenius, deliver standardized quality of care across numerous locations, thereby ensuring both accessibility and efficiency for patients in need of dialysis services, ultimately enhancing patient experiences.

The barriers to entry in dialysis are formidable: massive capital requirements for clinics and equipment, complex regulatory compliance, Medicare certification requirements, and physician relationships that take decades to build. A new entrant would need to invest billions of dollars over many years to achieve meaningful scale.

2. Bargaining Power of Suppliers: MODERATE

Fresenius's vertical integration largely neutralizes supplier power—the company manufactures its own dialyzers and machines. Labor (nurses, technicians) represents the critical constrained input, and healthcare labor markets have tightened significantly in recent years.

3. Bargaining Power of Buyers: LOW-MODERATE

Medicare rates are set administratively—no negotiation possible. Commercial insurers have limited alternatives given the duopoly structure. Markets served only by one large chain had $495 higher average commercial prices for outpatient dialysis and $565 higher medical director compensation per patient than markets that did not have large chain facilities. Patients have limited choice due to geographic constraints—you can't easily switch dialysis providers when you need treatment three times weekly.

4. Threat of Substitutes: LOW (but evolving)

Kidney transplant is the only true substitute—but there is a massive organ shortage. No pharmaceutical alternative to dialysis exists for ESRD. Home dialysis is growing but still represents a small percentage of treatments. Long-term threats include artificial kidneys and xenotransplantation, but these remain years or decades away from commercial viability.

5. Competitive Rivalry: MODERATE

As of 2024, DaVita serves approximately 281,100 patients across 3,166 outpatient dialysis centers, with 2,657 of those located in the U.S., giving it about 37% market share domestically. The duopoly structure with rational competition characterizes the industry—competition mainly on quality metrics and geographic expansion rather than destructive price competition.

In 2024, the Federal Trade Commission began investigating Fresenius Medical Care along with DaVita under allegations they use illegal tactics to push smaller companies out of the market.

Hamilton's 7 Powers

1. Scale Economies: STRONG

Manufacturing scale (2+ billion dialyzers produced), purchasing power across 4,000+ clinics, and shared services spread across a massive base create significant cost advantages. The dialysis chains segment held the largest market share of 82.9% in 2024, owing to their extensive networks and operational efficiencies.

2. Network Effects: MODERATE

Limited direct network effects, but physician referral networks create indirect benefits. The more clinics in a geography, the more convenient for patients, creating a virtuous cycle.

3. Counter-Positioning: WEAK

The legacy business model (in-center dialysis) may be counter-positioned against home dialysis growth. The NxStage acquisition was a defensive response to this risk, ensuring Fresenius participates in any modality shift.

4. Switching Costs: VERY STRONG

Patients develop relationships with care teams, geographic convenience is critical (3x weekly visits), and medical records and treatment protocols create stickiness. For products, clinics invest in training, supplies, and workflows around specific equipment.

5. Branding: MODERATE

B2B brand recognition among nephrologists is strong; patient brand awareness is more limited. Quality reputation matters significantly for physician referrals.

6. Cornered Resource: MODERATE-STRONG

Polysulfone membrane technology leadership represents a genuine cornered resource. Real estate locations near patient populations and physician relationships/joint venture partnerships create additional advantages.

7. Process Power: STRONG

Decades of operational refinement, standardized clinical protocols across thousands of clinics, and manufacturing expertise create process advantages that would take years for competitors to replicate. Significant improvement in labor productivity in Care Delivery achieved a year earlier than targeted demonstrates this power.

XII. Competitive Landscape & Market Dynamics

The Duopoly Structure

As of 2024, DaVita serves approximately 281,100 patients across 3,166 outpatient dialysis centers, with 2,657 of those located in the U.S., giving it about 37% market share domestically. Fresenius Medical Care operates between 2,600–2,800 U.S. centers and holds roughly 38% of the domestic market share.

During this era of outpatient growth, two dominant players emerged in the dialysis space: DaVita and Fresenius, which collectively control approximately 80% of the U.S. dialysis market with a combined 7,000 clinics in their global operations.

Market Size and Growth

The U.S. dialysis centers market size was estimated at USD 29.51 billion in 2024 and is projected to grow at a CAGR of 5.4% from 2025 to 2030. Factors driving market growth include the high prevalence of renal diseases, particularly end-stage renal disease (ESRD) and chronic kidney disease (CKD). Currently, nearly 808,000 individuals are living with ESRD in the U.S., with approximately 69% undergoing hemodialysis and 31% receiving kidney transplants. The prevalence of CKD affects about 35.5 million U.S. adults, or 14% of the adult population, with age being a significant risk factor-34% of those affected are aged 65 and older.

As of March 31, 2025, there are 7,556 dialysis centers in the U.S., treating over 500,000 patients for dialysis and roughly 300,000 transplant patients. The breakdown of treatment methods shows that about 433,400 patients are treated in-center, 78,400 at home, and a smaller number in skilled nursing environments. The uptick in ESRD across the country is driven by increasing rates of diabetes and hypertension, the two primary causes of kidney failure.

Regulatory Scrutiny

The investigation involves DaVita and Fresenius Medical Care (FMC) and is still in its early stages, anonymous sources with knowledge of the inquiries told Politico. Both companies have confirmed to Fierce Healthcare that they are aware of and... The Federal Trade Commission (FTC) has opened a probe into the country's two largest dialysis care providers and the terms of their contracts with physicians, according to a weekend report that has been confirmed by the companies.

The Federal Trade Commission is expanding its scrutiny of the health care industry to the growing dialysis market and investigating whether dialysis giants DaVita and Fresenius Medical Care are squeezing out competitors by restricting kidney doctors from changing jobs. Why it matters: The antitrust probe is part of a wider FTC focus on noncompete agreements that are often used in the health care labor force but that the agency says stifle business innovation. The stakes are especially high in dialysis, where DaVita and Fresenius control at least 70% of a market expected to be worth more than $180 billion by the next decade.

XIII. Key KPIs for Monitoring Performance

For long-term fundamental investors, three metrics deserve close monitoring:

1. U.S. Same Market Treatment Growth This KPI captures organic patient volume growth independent of acquisitions or clinic openings. It reflects the underlying health of the core business—are new patients being referred at a rate that offsets natural attrition (deaths, transplants)? Post-COVID, this metric has been recovering, but sustained positive growth is essential for the investment thesis.

2. Operating Income Margin (Excluding Special Items) The FME25 program and operational turnaround are designed to improve profitability. The company targets 11-12% margins in 2025, advancing toward mid-teens by 2030. Progress on this metric validates execution on cost savings and pricing improvements.

3. Net Leverage Ratio (Net Debt/EBITDA) Total net debt and lease liabilities were further reduced to EUR 9,803 million (Q4 2023: EUR 10,760 million). The net leverage ratio (net debt/EBITDA) improved from 3.2x in Q4 2023 to 2.9x in Q4 2024. Balance sheet health is critical for a company that may need to invest in technology upgrades (5008X rollout), make acquisitions, or weather regulatory/reimbursement headwinds.

XIV. Bull Case and Bear Case

Bull Case

Fresenius Medical Care possesses one of the most durable competitive positions in healthcare. The combination of vertical integration, scale economics, switching costs, and regulatory barriers creates a business that would be nearly impossible to replicate from scratch.

The FME25 transformation has delivered ahead of schedule, with sustainable savings raised to €750 million by year-end 2025. Under Helen Giza's leadership, the company has returned to the DAX 40, demonstrating that the turnaround is working.

The 5008X machine and HVHDF therapy represent a genuine clinical breakthrough—a 23% reduction in mortality is meaningful for patients and creates competitive differentiation. As the only FDA-cleared HVHDF system, Fresenius has first-mover advantage in what could become the new standard of care.

The aging population and rising rates of diabetes virtually guarantee growth in the ESRD patient population. The prevalence of CKD affects about 35.5 million U.S. adults, or 14% of the adult population, with age being a significant risk factor—34% of those affected are aged 65 and older. This demographic tailwind provides visibility into demand for decades.

The value-based care pivot through InterWell Health expands the addressable market from ~$50 billion (dialysis services) to ~$170 billion (full kidney care continuum), creating new avenues for growth.

Bear Case

The regulatory environment poses significant risks. The ongoing FTC investigation into noncompete clauses could force structural changes to how Fresenius (and DaVita) engage with physicians. Any antitrust enforcement could disrupt the stable competitive dynamics that have supported industry profitability.

Medicare reimbursement risk is ever-present. The ESRD program represents a massive government expenditure, and any future administration could target dialysis reimbursement rates as part of cost containment efforts.

Labor costs remain elevated, and the healthcare worker shortage is structural rather than cyclical. Significant improvement in labor productivity has been achieved, but continued pressure on wages could offset savings from other efficiency initiatives.

Home dialysis growth, while captured partially through NxStage, could accelerate faster than expected. If home dialysis becomes the dominant modality, Fresenius's extensive in-center clinic infrastructure becomes a stranded asset.

In May 2025, the benefits fund of the United Food and Commercial Workers Local 1776 filed a proposed class-action lawsuit against Fresenius Medical Care and DaVita Inc., another dialysis provider, alleging that the two companies illegally conspired to inflate treatment costs for dialysis patients by billions of dollars. Litigation risk remains a wildcard.

XV. Conclusion: The Investment Case

Fresenius Medical Care represents a rare combination in public markets: a company with genuine structural advantages operating in a market with visible long-term growth. The business model—vertically integrated, deeply embedded in the healthcare system, serving patients who require treatment to survive—creates durability that few businesses can match.

The transformation under Helen Giza has been impressive. FME achieved important top- and bottom-line contributions, with 4% organic revenue growth and 18% operating income growth on an outlook base. The operational turnaround is translating into financial results.

Yet investors must weigh this durability against meaningful risks: regulatory scrutiny of the duopoly structure, Medicare reimbursement uncertainty, labor cost pressures, and the potential for technological disruption. The business model that served so well for two decades may require continued evolution to remain competitive.

For long-term fundamental investors, Fresenius Medical Care offers exposure to an essential healthcare service with structural growth drivers, operated by a management team that has demonstrated execution capability. The key question is whether the attractive competitive dynamics of the past will persist—or whether regulatory intervention, technological change, or competitive pressure will erode the moat that Fresenius has spent three decades building.

As with any investment, the price matters enormously. At the right valuation, Fresenius Medical Care's combination of durability, dividends, and growth potential makes it a compelling holding for patient investors willing to accept healthcare-sector volatility. The company has proven resilient through a global pandemic, management transitions, and major restructuring—evidence that the business model can weather significant storms.

The ultimate judge will be time. But for a company whose roots trace back to a 15th-century pharmacy, patience has always been part of the formula.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube