Birkenstock: From German Cobbler to Global Luxury Footwear Empire

I. Introduction: The 250-Year-Old Startup

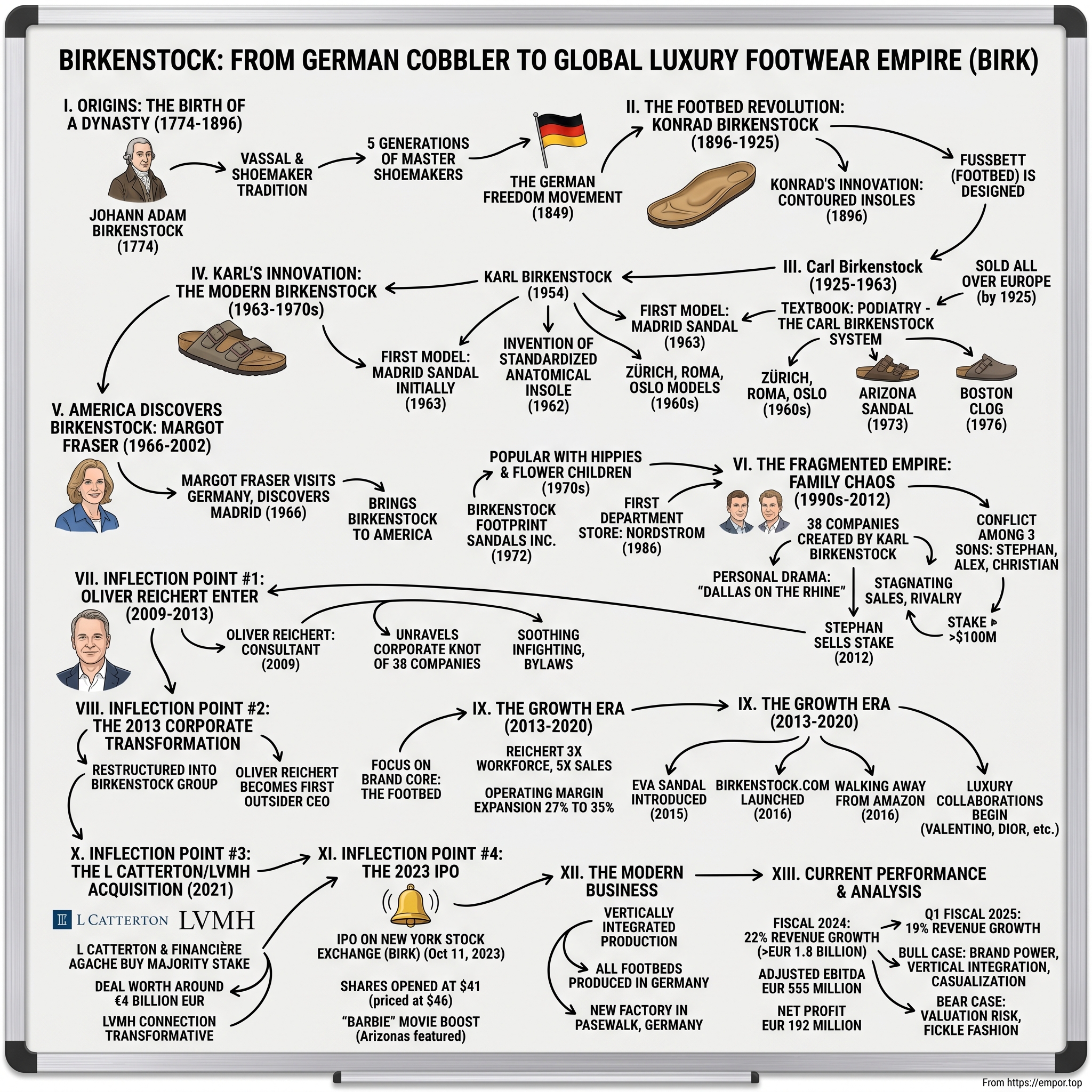

In 1774, as American colonists were preparing to declare independence from Britain, a cobbler named Johann Adam Birkenstock registered his trade in a small Hessian village in Germany. No one could have imagined that this humble shoemaker's lineage would, two and a half centuries later, ring the opening bell at the New York Stock Exchange, backed by the world's wealthiest luxury mogul.

Birkenstock Holding plc is a German shoe manufacturer known for its sandals and other shoes notable for contoured cork footbeds made with layers of suede and jute. Founded in 1774 by Johann Adam Birkenstock and headquartered in Neustadt (Wied), Rhineland-Palatinate, Germany, the company's original purpose was to create shoes that support and contour the foot.

Today, Birkenstock's share price hovers around $43.51 per share, with a market capitalization of approximately $8 billion. The company closed fiscal 2024 with 22% revenue growth, reaching over EUR 1.8 billion, continuing a decade-long track record of 20%+ revenue growth.

The central question confronting investors and business strategists alike is this: How did a 250-year-old German orthopedic shoe company—long associated with hippies, granola, and "crunchy" counterculture—transform into a luxury fashion icon backed by LVMH's Bernard Arnault? The answer involves multi-generational family drama worthy of a German soap opera, a professional CEO with an astonishing resume, vertical integration that would make Henry Ford proud, and the peculiar phenomenon of "ugly fashion" becoming aspirational.

This is a story about what happens when craft meets capital, when authenticity becomes strategy, and when the world's most powerful luxury investor decides that comfort can indeed be sexy.

II. Origins: The Birkenstock Shoemaking Dynasty (1774–1896)

The history of the Birkenstock "shoemaking dynasty" can be traced back to the first documented mention of Johannes Birkenstock (1749–1812), registered on March 25, 1774, as a "vassal and shoemaker" in local church archives in the small Hessian village of Langen-Bergheim.

Picture the Holy Roman Empire in its twilight years—a patchwork of German principalities where craft guilds still determined a man's station in life. In this context, becoming a master shoemaker was no small achievement. Johannes Birkenstock, laboring in a village about 40 kilometers northeast of Frankfurt, likely had no grand ambitions beyond serving his local community. Yet he established something that would prove far more durable than any political boundary: a craft tradition.

Since that time, there have been five generations of master shoemakers or part-time shoemakers, several lines of the Birkenstock family working in the shoemaking trade, and finally three generations of shoe manufacturers.

The next critical chapter came with Johannes Junior (1790-1866), nephew of the founder, who continued the shoemaking tradition. What's fascinating about this period is how the Birkenstock family's craft intersected with history's great upheavals. The family's continued poverty caused Johannes Junior and his son Johann Conrad (1819-1888) to join the German freedom movement, participating in the revolution of 1849—an early indicator that Birkenstocks would always carry the DNA of rebellion against convention.

The real breakthrough came when Konrad Birkenstock, the descendant who would reshape the family business, left the countryside for Frankfurt am Main. In the late nineteenth century, Konrad Birkenstock owned two specialist footwear stores in Frankfurt. He made shoes, not sandals. At the time, the insoles of shoes were typically flat; Konrad's innovation was to make shoes with insoles that were contoured to fit and support the foot. He was one of the world's first shoemakers to experiment with insoles molded to the shape of the foot rather than the traditional flat footbed back in 1896.

This was the philosophical foundation—German craftsmanship married to health-consciousness—that would eventually power a multi-billion dollar empire. Konrad wasn't chasing fashion; he was chasing function. In an era of industrialization and mass production, he zagged toward personalization and biomechanics. This contrarian positioning would prove prophetic.

III. The Footbed Revolution: Konrad & Carl Birkenstock (1896–1963)

In 1896, the Fussbett (footbed) was designed, and by 1925, Birkenstocks were sold all over Europe.

The word Fussbett—literally "foot bed"—captures perfectly what Konrad Birkenstock invented. Rather than treating the foot as a passive platform to be molded by fashion, he designed an insole that would cradle and support the foot's natural contours. In an age when most footwear was essentially flat slabs of leather, this was revolutionary thinking.

Konrad's son Carl took the innovation further, transforming it from craft knowledge into systematized methodology. Carl Birkenstock started the Birkenstock training courses, which went on to become famous. In the following years, he trained more than 5,000 specialists during his one-week foot service courses. Leading physicians supported the courses and the "Carl Birkenstock System."

Carl published a textbook, "Podiatry - the Carl Birkenstock System," with a print run of 14,000 copies—remarkable for specialized literature. He was building something more valuable than a product; he was building an ecosystem of believers, a network of professionals who understood and could articulate why the Birkenstock approach mattered.

After 1945, Carl Birkenstock continued to pursue his idea of handmade healthy footwear at his new headquarters in Bad Honnef near Bonn. He wanted to make this "ideal shoe" suitable for mass production, which he tried to realize together with shoe manufacturers until 1961, when he abandoned this idea and retired to writing books on foot health. During this time, the still very small company earned money through the successful sale of the "Blue Footbed" orthopaedic insole.

Here's a crucial insight for understanding Birkenstock's DNA: the company spent nearly two centuries not making sandals. They made insoles. The footbed—that contoured cork-and-latex platform—was the product. Everything else was just a delivery mechanism. This focus on the hidden, functional core rather than the visible, fashionable shell would define the brand's identity for generations to come.

The "Blue Footbed" became a staple in orthopedic circles. Physicians prescribed them. Patients sought them out. The Birkenstock name became synonymous with foot health—a positioning that would prove invaluable when the company finally pivoted to finished footwear.

IV. Karl's Innovation: The Birth of the Modern Birkenstock (1963–1970s)

In 1954, Carl's only son, Karl, joined his father's company. While his grandfather Konrad and father Carl Birkenstock worked all their lives on producing orthopaedic insoles that were as individualized as possible for the wearer, the young Karl Birkenstock succeeded in making healthy footwear mass-produced in 1962 with the invention of a standardized, permanently installed, anatomically shaped insole.

This was Karl's genius: he recognized that individualization was a barrier to scale. His father and grandfather had created bespoke solutions; Karl figured out how to standardize them. By developing a footbed that could work for the "average" foot—still anatomically correct, still supportive, but producible at scale—he cracked the code that had eluded Carl for decades.

In 1963, Karl Birkenstock released his first model, the "Original Birkenstock Footbed Sandal," an athletic sandal with a flexible footbed, which has been called "Madrid" since 1979, laying the foundation for the company's expansion since the 1970s. The shoe was constructed so that the wearer would have to grip their toes to keep the sandals on; this resulted in toning the calf muscle, which became quite useful to athletes, especially among gymnasts. However, the market launch in 1963 was a disaster. No shoe retailer wanted to offer the gender-neutral sandal, which was diametrically opposed to the shoe fashion trend of the time—Italian stilettos—and consequently, orders failed to materialize. The first sales were made through direct marketing in the medical sector.

Imagine the scene: it's 1963, and women's shoes are heading toward ever-higher heels, ever-narrower toes. Into this environment, Karl Birkenstock introduces a flat, chunky, gender-neutral sandal that prioritizes toe-grip exercise over aesthetics. Shoe retailers literally refused to carry it.

Birkenstock Orthopädie GmbH, as the company was now called, was run jointly by Karl and his wife Gisela. The number of employees in 1970 was 57.

Those 57 employees in 1970 were building something far larger than they knew. The product DNA established in this era—function over fashion, health over style, authenticity over trends—would become the brand's greatest asset half a century later.

Although derided at the shoe trade fair in 1963, Karl Birkenstock developed the closed sandal "Zürich" the following year, followed by the strappy sandal "Roma" in 1965, the low shoe "Oslo" and the boot "Athen" in the second half of the 1960s. A first plastic model—the "Noppy" massage sandal—saw the light of day in the new decade. In 1973, Birkenstock's most popular sandal, Arizona, was introduced. This was followed in 1976 by the first cork clog, the "Boston", and finally in 1983 by the range of thong sandals, including the "Gizeh".

The Arizona two-strap sandal, introduced in November 1973, would become the company's signature product—eventually featuring in one of the most talked-about movie scenes of 2023. The Boston clog, launched in 1976, would experience its own viral moment nearly five decades later. Karl was building an arsenal of classic silhouettes that could transcend any single fashion cycle.

V. America Discovers Birkenstock: The Margot Fraser Story (1966–2002)

In 1966, Margot Fraser, a German-American dressmaker who resided in Santa Cruz, California, decided to travel back to Germany to visit a spa in Bavaria, where she was recommended Madrids to help with a foot ailment caused by tight shoes.

This is the entrepreneurial creation myth that business school professors dream about. A woman travels to Germany, discovers a product that solves her personal problem, and decides—against all odds—to bring it to America.

"I didn't realize what it would take or how I would do it, but I thought that this had great potential right from the beginning," Fraser told Footwear Plus magazine in 1998.

"Women thought they had to be uncomfortable, that it was part of being alive and being a woman," Fraser later reflected. This insight—that American women had internalized foot pain as normal—revealed a massive unmet need.

Many shoe stores rejected the sandals due to their appearance, leading Fraser to health stores near the granola section. The 1970s brought a spike in sales. In the United States, Birkenstocks were first popular among young men and later on among flower children, a group traditionally associated with American liberalism. The shoe became popular with hippies and others who had a "back to nature" philosophy and appreciated the natural foot shape and foot-friendly comfort of Birkenstocks. Hippies and representatives of the tech movement in California discovered the shoes as an expression of the unconventional.

Fraser didn't fight the hippie association; she leaned into it. The health food stores that would carry her sandals attracted exactly the kind of customer who cared about natural materials, foot health, and authenticity. What might have been a brand liability became, accidentally, an authentic identity.

In 1972, she founds BIRKENSTOCK Footprint Sandals Inc., the nucleus of today's BIRKENSTOCK USA, which became a rapid success thanks to the reform movements and hippies.

Fraser was the one who first suggested adding color to the shoes, much to the dismay of the Swiss distributor who thought that since the shoes were orthopedic, they didn't need to be fashionable. However, Fraser pressed on and, in 1989, hired the first full-time sales representatives for the company. At that time, the company offered 28 styles.

Fraser understood something the German headquarters initially resisted: in America, even functional products need to be aspirational. Colors didn't compromise the orthopedic mission; they made it more accessible. Fraser's growing sales record impressed Karl Birkenstock who, in 1974, signed an import agreement making Fraser the sole US importer of the sandals. A year later, her business broke the sales record of one million US dollars for the first time.

In 1986 Nordstrom became the first department store to sell Birkenstock sandals—a watershed moment signaling that the brand could exist beyond health food stores and hippie enclaves.

In 2002, Margot Fraser retires from her company, but returns briefly in 2004 before Christian Birkenstock acquires a majority stake in Birkenstock Footprint Sandals Inc. Fraser's retirement would mark the beginning of a turbulent period for the American business—and for the Birkenstock family itself.

VI. The Fragmented Empire: 38 Companies and Family Chaos (1990s–2012)

The company had always been 100% owned by the same family and managed by a single descendant, a tradition upended in 2002 when Carl Birkenstock, the CEO and owner, handed over his shares and job to his three sons.

When Karl Birkenstock—that's Karl, not Carl, across two generations the names blur—decided to retire, he made a fateful choice: rather than designate a single successor, he split the empire among his three sons. Karl Birkenstock created 38 companies under the Birkenstock umbrella and divided them amongst his three sons.

With his retirement approaching, Karl carved up the family business into a constellation of entities that he parceled out to his sons. That made it harder for employees to organize, since technically they worked for smaller companies. But it also made it more difficult for the brothers to forge a shared vision for the future.

The three brothers—Stephan (the oldest), Alex (the middle child), and Christian (the youngest)—had very different visions. Instead, they began cooking up a bunch of separate brands that used the family footbed, which they expected distributors, including Fraser's company in the US, to market. Stephan, the oldest brother, hewed closest to Karl's conservative approach and focused on a line of cheaper plastic clogs called Birkis. Alex, the middle child, was more interested in exploring fashion-forward styles and created other brands such as the lacquered, shiny sandals he called Tatami and closed-toe shoes known as Footprints.

Meanwhile, the American business was adrift. Back in the US, Fraser's old staff had struggled since her retirement in 2002. She'd sold her distribution company to employees, but the workers-turned-owners couldn't decide on a strategy. Meanwhile, the Birkenstock brothers' escalating rivalry over the company's direction was coming to a head.

When Christian Birkenstock hired Reichert in 2009, the family business was in disarray, with stagnating sales and no coherent plan for the future. After their domineering father, Karl, stepped back years earlier, Christian and Alex—then in their late 30s and early 40s, respectively—began fighting with their older brother, Stephan, for creative control. It had been more than a decade since the public had fawned over Birkenstocks, and suddenly upstarts such as Crocs were jolting a category long relegated to stoners, geriatrics and German tourists.

The situation deteriorated further with personal drama. The Birkenstock brothers were mired in internal conflicts including a lawsuit against an ex-wife. After separating from Christian, Susanne launched her own line called Beautystep, which purported to help women fight off cellulite. Before long, Susanne was appearing in ads saying she stood behind the sandals with her name, which remained Birkenstock even years after the divorce. Journalists dubbed the ongoing drama "Dallas on the Rhine," and a German court eventually put a restriction on Susanne's use of the Birkenstock name. (Her business went broke.)

For investors trying to understand Birkenstock's current trajectory, this period matters profoundly. The chaos of the 38-company structure, the family conflicts, the lack of strategic direction—all of it created the conditions for the transformation that would follow. A smoothly-running family business might never have opened the door to an outsider CEO or, eventually, to private equity.

VII. INFLECTION POINT #1: Enter Oliver Reichert—The Professional CEO (2009–2013)

If you were casting a CEO for a turnaround story, you probably wouldn't pick a former techno club owner, war correspondent, and sports television executive. Yet that's exactly who Christian Birkenstock found sipping a beer early one morning at a posh Austrian Alpine resort.

When chief executive officer Oliver Reichert first came on the scene as a consultant to Birkenstock's founding family in 2009, the earlier techno club owner, war correspondent and sports TV executive had to unravel a corporate knot of 38 feuding companies, labels and family members.

The origin story is almost too good: Christian Birkenstock, "smoldering away one morning in the posh Austrian Alpine resort of Kitzbühel," had a chance encounter with Reichert—"a towering, brusque unemployed TV executive who'd recently been fired from his job at a German station." Reichert was a crisis reporter in Africa and an exec at a German sports TV station. He was introduced to the Birkenstock family in 2009 via an art dealer friend and became an external consultant.

Enter Reichert, a former war correspondent and sports television executive who hails from the Bavarian countryside. First taking a position as a consultant for Birkenstock in 2009, he attempted to soothe over the infighting and introduced bylaws on how the brothers would handle each other during business deals. Four years later, he was named CEO when the family took a step back from the company.

"Probably I'm not the average CEO," Reichert said. "I never tried to be average in anything."

Reichert's first task was essentially family therapy with a business license. He needed to get the brothers to stop fighting long enough to make any coherent decisions. But he also saw what none of them could see: the 38-company structure was a disaster, and one brother needed to go.

Reichert concluded that in trying to reconcile the brothers, the sticking point was Stephan, a homebody who wanted to play it safe with basics, which clashed with Christian and Alex's desire to experiment. One of Reichert's first accomplishments: persuading Stephan to sell his stake to his younger brothers in 2012 for more than $100 million, according to a German magazine.

Reichert told Christian and Alex that each of them owning 50% of the company couldn't work for long; there was simply too much baggage. Eventually, they'd need either to sell the business to a more organized owner or to prepare it for an IPO.

He sets the new age of Birkenstock in 2013, when a comprehensible structure was in place that could actually accommodate a CEO. This is the key insight: Reichert spent four years creating the conditions for his own success. He couldn't lead the company until the company was leadable.

At the helm of Birkenstock is CEO Oliver Reichert, the German brand's first leader from outside the founding family. Since assuming the role in 2009, Reichert has been on a mission to transform Birkenstock into a global lifestyle brand.

VIII. INFLECTION POINT #2: The 2013 Corporate Transformation

In 2013, the company, which had previously consisted of 38 individual companies since the 1990s, was fundamentally restructured to form a single group of companies, the Birkenstock Group.

Think about what this means: for two decades, Birkenstock had operated as 38 separate legal entities. Imagine trying to implement a coherent pricing strategy, a unified marketing message, or a consistent supply chain across 38 different companies, each with its own P&L, its own management, its own agenda. It was organizational chaos.

In 2013, Stephan sold his stake to the two brothers; they recruited Oliver Reichert, an outsider, to consolidate various subsidiaries into Birkenstock Group and lead the company.

Familial disagreements contributed to leadership passing to Reichert, who in 2013 became the first outsider to head Birkenstock in a nearly 250-year history that can be traced back to the cobbler Johannes Birkenstock.

This cannot be overstated: for 239 years, Birkenstock had been run by a Birkenstock. The willingness to bring in an outsider represented a fundamental break with nearly a quarter-millennium of tradition. It was an admission that the family model had failed—and, paradoxically, the only way to save the family legacy.

Producing 95 percent of its range in Germany, Birkenstock has doubled its domestic workforce to about 3,800 since 2013. While many companies were offshoring production to cut costs, Reichert doubled down on German manufacturing. This wasn't sentimentality; it was strategy. The executive has focused on expanding its production in Germany, where 95 percent of Birkenstock's products are assembled.

Oliver Reichert: "It was the rebirth, the wake-up call. But basically it was a release—in terms of creativity. To concentrate the energy on what is Birkenstock and somehow define the core of the brand, which is the footbed. It meant being aware of tradition but not being afraid."

Reichert understood something essential: the footbed was the brand. Everything else—the styles, the colors, the collaborations—could evolve, but the orthopedic core had to remain inviolate. "It's about real creativity, about filling a white wall, and our wall is not purely white. It's the footbed. You cannot touch the orthopedic thinking behind it and just crucify it for your own benefit."

IX. The Growth Era: 2013–2020

Once the organizational chaos was resolved, growth followed with almost mechanical precision. The company has been growing at an annual rate of 20% from fiscal 2014 to last year.

Reichert 3x'd the workforce to 4k+ and—even as sales grew 5x—expanded operating margin from 27% to 35%. This is the dream scenario for any turnaround: revenue quintuples while profitability improves. Usually, rapid growth comes at the expense of margins as companies scramble to build infrastructure. Reichert managed both simultaneously.

Most of the brand's popular pairs are upwards of $100, but in the spring of 2015, the company released a style that was nearly half the price thanks to an innovative material named EVA. EVA—which is an acronym for ethylene, vinyl and acetate—is a lightweight elastic material that feels a bit like dense foam. It's flexible, smooth and provides cushioning that makes shoes comfortable from the very first wear.

The EVA sandal was a master stroke of market expansion. At roughly $50-60, it opened Birkenstock to customers who might balk at $120+ for a traditional cork sandal. It was waterproof, perfect for beach and pool. And critically, it introduced the brand to younger consumers who might later trade up to premium styles.

The company also executed a sophisticated e-commerce transformation. The website Birkenstock.com launched in 2016, and the online channel has gone from 0% to 38% of sales in 7 years. In an era when many heritage brands were struggling to adapt to digital, Birkenstock built a direct-to-consumer machine.

But perhaps the most consequential decision was what Birkenstock refused to do. Plagued by counterfeits and unauthorized selling on the online shopping site, the sandals company will no longer supply products to Amazon in the U.S. starting Jan. 1, 2016. Additionally, Birkenstock won't authorize third-party merchants to sell on the site.

"The Amazon marketplace, which operates as an 'open market,' creates an environment where we experience unacceptable business practices which we believe jeopardize our brand," Birkenstock USA CEO David Kahan wrote. "Policing this activity internally and in partnership with Amazon.com has proven impossible."

Walking away from Amazon—the world's largest online marketplace—was audacious. But it signaled that Birkenstock valued brand control over short-term revenue. How hard was pulling out of Amazon? "For us, nothing," said Reichert. "Maybe, but not a good one. I think at the beginning Amazon was a pioneer in online trading. You have to kill monsters when they are small. They're getting too big? You can't kill them, okay? They will eat you."

The luxury fashion world took notice. Since 2021, they've partnered with six major fashion houses including Proenza Schouler, Rick Owens, Valentino, Dior, and Manolo Blahnik. Before teaming up with Dior, Birkenstock had cemented its place in luxury fashion through high-profile collaborations with Valentino, Rick Owens, and Proenza Schouler. Valentino's 2019 red leather Arizona sandals marked the first high-fashion interpretation of the classic silhouette.

These weren't typical licensing deals where a fashion house slaps its name on a commodity product. Each collaboration started with the footbed and built outward, maintaining Birkenstock's orthopedic integrity while allowing designers creative expression.

X. INFLECTION POINT #3: The L Catterton/LVMH Acquisition (2021)

German footwear brand Birkenstock is selling a majority stake to L Catterton, a private equity firm backed by Bernard Arnault's LVMH. The company said in a statement on Friday that L Catterton affiliates including Arnault's family investment company, Financière Agache, will also invest in the maker of the iconic flat sandals.

The deal is believed to be worth around €4 billion EUR (approximately $4.8 billion USD) and will see owners Christian and Alex Birkenstock maintain a minority stake.

The backstory of how this deal came together reads like a business thriller. In the early hours of December 24, Alexander Dibelius struck a gentleman's agreement with Oliver Reichert, the chief executive of Birkenstock. CVC Capital Partners, the buyout firm where Dibelius is a managing partner, was set to buy the iconic German sandal-maker for more than €3.5 billion.

But Reichert had bigger ambitions. Besides, Reichert had long dreamed of selling to the House of LVMH rather than a faceless financier.

In 2021, he convinced the Birkenstock family to sell for ~$5B to PE firm L Catterton (backed by the family office of LVMH's Bernard Arnault). Reichert says "I called Bernard Arnault. And he welcomed me to his Paris offices in the middle of the pandemic. The deal was in place six weeks later."

By August of last year, Birkenstock had quietly signed on Goldman Sachs as adviser, and the US bank set up a meeting at an upmarket hotel in London's Mayfair district between Reichert and Mike Chu, L Catterton's co-CEO. Chu purchased a pair of Birkenstocks before the meeting, though he didn't wear them to see Reichert. The encounter turned from a one-hour introduction into a four-hour meeting of the minds. Whatever unspoken animosity might have existed between the two alpha males Reichert and Dibelius, the chemistry between the Birkenstock CEO and the down-to-earth Chu was positive from the get-go. The secret Mayfair meeting was followed by more discreet conversations later in the year.

Instead, Reichert switched over to L Catterton, a private equity firm that flies under the radar but boasts a powerful backer: LVMH CEO Bernard Arnault, who became Europe's richest man thanks to a nose for brands he can supercharge in the engine room of his French luxury emporium. In a matter of weeks, L Catterton sealed the deal to buy Birkenstock for more than 4 billion euros.

"In L Catterton and Financière Agache we have found not just shareholders, but also partners for achieving our global growth ambitions," said CEO Oliver Reichert.

The LVMH connection was transformative. When L Catterton, LVMH's private equity arm, acquired Birkenstock in 2021, they weren't just buying a sandal company. They were acquiring a heritage brand with all the raw materials needed for luxury transformation: European craftsmanship, cultural credibility spanning counterculture to high fashion, and premium pricing tolerance.

Christian and Alex Birkenstock retained minority ownership and remained responsible for production in Germany. The family didn't entirely exit—they remained connected to the manufacturing heritage. But the strategic direction was now in new hands.

XI. INFLECTION POINT #4: The 2023 IPO

Shares opened at $41 after the company priced its IPO at $46 per share, near the midpoint of its expected range of $44 to $49. Birkenstock raised about $495 million in the offering and plans to use the proceeds to pay off loans.

Birkenstock's IPO was priced at $46 per share, within its projected range of $44 to $49, raising $1.48 billion and valuing the company at approximately $8.64 billion. This valuation indicates a multiple of 6.9 times its annual sales and a price-to-earnings ratio of over 45, suggesting a premium compared to industry peers like Nike, Adidas, and others who trade between 1.0x to 3.0x sales with lower earnings multiples.

The ordinary shares began trading on the New York Stock Exchange under the symbol "BIRK" on October 11, 2023.

The timing was fortunate. Birkenstock scored a major boost to its profile this summer when a pair of its sandals was featured in the wildly successful "Barbie" movie.

In one of the most memed moments of the summer zeitgeist film, the character Weird Barbie, played by Kate McKinnon, offers her in one hand a pale pink high-heel pump and in the other a basic brown Birkenstock Arizona sandal.

This movie moment sparked a 110 percent increase on searches for Birkenstock Arizonas following its release, according to Lyst. The scene—comparing Birkenstocks to high heels as a choice between fantasy and reality—was free advertising worth millions.

The IPO itself, however, was rocky. Despite these expectations, the market response was lukewarm, with shares opening at $41 and closing down at $40.20, a 12.6% decrease, reflecting skepticism about the ambitious valuation.

In the past ten years, Birkenstock's IPO opening day performance ranks as the sixth worst of 95 IPOs to have raised over $1 billion.

"The best thing for this brand would be staying family-owned," Reichert told CNBC. "But within the family, there was so many problems—so we go for the second-best option."

"Some say 'Birkenstock is having a moment.' I always reply then 'this movement has lasted for 250 years, and it will continue to last,'" Reichert told shareholders. "Birkenstock is more than a shoe. It's a way of thinking, a way of living."

XII. The Modern Business: Vertical Integration & Manufacturing Strategy

To ensure each product meets rigorous quality standards, the company operates a vertically integrated manufacturing base and produces all footbeds in Germany. In addition, it assembles the vast majority of products in Germany and produces the remainder elsewhere in the EU.

In an era of global supply chains and Chinese manufacturing, Birkenstock's commitment to German production is unusual—and strategic. All footwear is made in the EU, adhering to some of the world's strictest regulatory frameworks, and raw materials are predominantly sourced from Europe in compliance with rigorous social, environmental, and quality standards. Vertical integration enhances strategic control while ensuring operational continuity through diversified supplier relationships.

With around 6,200 employees, the long-standing business is also the German footwear industry's largest employer. BIRKENSTOCK operates a vertically integrated production and manufactures all of its footbeds in Germany.

With global headquarters, production, and logistics based throughout Germany, Birkenstock footwear is sold in approximately 90 countries worldwide.

The four-layer footbed technology represents the proprietary core. The original footbed possesses four different layers: a shock-absorbent sole, followed by a layer of jute fibers, a firm cork footbed, and another layer of jute. The final layer is the footbed lining—a soft suede that molds to the wearer's foot over time. This architecture is nearly impossible to counterfeit perfectly, creating a natural moat against knockoffs.

The company recently broke ground on a new production factory in Pasewalk, Germany, which will increase productivity to more than 40 million pairs of shoes a year and is the single largest investment in company history at 110 million euros.

XIII. Current Performance & Financial Analysis

The company closed fiscal 2024 with 22% revenue growth, reaching over EUR 1.8 billion in its first year as a public company, continuing a decade-long track record of 20%+ revenue growth. The Company reports fiscal 2024 revenue growth of 21% on a reported and 22% on a constant currency basis, ahead of the Company's guidance of 20%.

Key financial highlights include: Adjusted EBITDA of EUR 555 million (+15% YoY) with a margin of 30.8%, net profit of EUR 192 million (+155% YoY), and EPS of EUR 1.02 (+149% YoY).

The company achieved double-digit growth across all segments: Americas (19%), Europe (21%), and APMA (42%).

For the first quarter of fiscal 2025, the Company reports first quarter revenue growth of 19% on a reported and constant currency basis, ahead of the Company's annual guidance of 15-17%, driven by strong holiday demand. Financial highlights include: Revenue of EUR 362 million, an increase of 19% on a reported and constant currency basis; Strong double-digit revenue growth across all segments including 16% in the Americas, 17% in EMEA and 47% in APAC.

The company confirms FY2025 guidance with expected revenue growth of 15-17% in constant currency and Adjusted EBITDA margin of 30.8-31.3%. The company maintains strong liquidity with EUR 299 million in cash and cash equivalents, with net leverage at 1.9x as of December 31, 2024.

Management remains confident in medium to long-term objectives for mid-to-high teens revenue growth, gross profit margin of around 60% and Adjusted EBITDA margin of over 30%.

XIV. Bull & Bear Cases: A Framework for Analysis

The Bull Case:

The bull case rests on several pillars. First, Birkenstock benefits from what Hamilton Helmer might call "brand power"—a deep reservoir of accumulated goodwill and authenticity that competitors cannot replicate. You cannot manufacture 250 years of heritage overnight. The brand's association with foot health, German craftsmanship, and countercultural authenticity creates customer affinity that translates into pricing power.

Two years later, Birkenstock achieves nearly 60% gross margins rivaling Louis Vuitton, generates over €1 billion in revenue, and their hand-braided Kith partnership sells out instantly at luxury price points.

Second, vertical integration creates what Helmer would term "cornered resource" advantages. All footbeds are engineered and produced in Germany, and final assembly is conducted exclusively within the EU, reflecting a heritage of enduring craftsmanship and precision. This manufacturing control is increasingly valuable in a world of supply chain disruptions and rising consumer concern about product authenticity.

Third, the "casualization" of fashion is a secular tailwind. The pandemic accelerated trends toward comfort-first footwear, and those habits have proven sticky. While at first glance Birkenstocks may seem incongruous with luxury, the brand has become a magnet for high fashion labels—even more so since the beginning of the pandemic, when consumer appetites shifted toward extreme comfort. Birkenstocks are no longer just a symbol of the counterculture; they have become a footwear icon thanks to successful collaborations.

Fourth, geographic expansion offers substantial runway. APMA growth of 42% on a constant currency basis suggests that Asia represents a massive opportunity barely penetrated.

The Bear Case:

The bear case centers on valuation and fashion risk. The company trades at premium multiples compared to most footwear peers. If growth decelerates—or if the brand falls out of fashion favor—multiple compression could be painful.

Fashion is notoriously fickle. While the classic clog has been around for ages, it's had a particular resurgence over the past year. Blame it on the trail of collaborations with luxury designers like Valentino, Manolo Blahnik, Proenza Schouler, and Rick Owens, or the need for all things comfort in a post-pandemic world. What happens when the pendulum swings back toward heels and fashion-forward footwear?

From a Porter's Five Forces perspective:

- Supplier Power: Moderate. Birkenstock's vertical integration mitigates this risk, but it remains dependent on cork, leather, and other natural materials.

- Buyer Power: Low for now, given brand loyalty and pricing power. But luxury positioning raises expectations that must be continuously met.

- Competitive Rivalry: Increasing. Crocs has shown that "ugly" footwear can scale, and numerous brands are attempting to replicate Birkenstock's formula.

- Threat of New Entrants: Low in premium segment (brand heritage matters), higher in mass market.

- Threat of Substitutes: Moderate. Sneakers, other comfort footwear, and traditional dress shoes all compete for foot share.

Critical KPIs to Monitor:

-

Average Selling Price (ASP) Growth: This reveals whether the company maintains pricing power—a key indicator of brand strength and luxury positioning. Mid-single-digit ASP growth suggests health; declining ASP would signal competitive pressure.

-

DTC Mix / Owned Retail Performance: Direct-to-consumer sales carry higher margins and provide richer customer data. The trajectory from 18% DTC (2018) to 38% (2022) needs to continue.

XV. Conclusion: The Paradox of Comfortable Luxury

Birkenstock's story defies easy categorization. It's a 250-year-old family business that became a startup. It's an orthopedic product that became a fashion icon. It's a hippie sandal backed by the world's largest luxury conglomerate. It's ugly—and that's the point.

"Birkenstock is more than a brand; it's rather like a religion," Reichert has said.

The company's trajectory from German cobbler to global luxury empire offers several lessons. First, authenticity cannot be manufactured—but it can be stewarded. The Birkenstock family spent generations building craft credibility; Reichert's genius was recognizing that credibility's value and positioning it for a new era.

Second, vertical integration matters more than ever. In a world of counterfeits and supply chain disruptions, owning your manufacturing creates both quality control and strategic optionality.

Third, saying "no" can be more valuable than saying "yes." Walking away from Amazon, rejecting most collaboration requests, and refusing to discount—these negative choices preserved the brand equity that now commands premium pricing.

"If you have such a tradition and such a history, the threat is to wake up in your own museum," Reichert observed. "And I don't want to have this."

The coming years will test whether Birkenstock can sustain its remarkable trajectory. The L Catterton/LVMH backing provides capital and luxury expertise. The global shift toward comfort-first fashion provides tailwinds. The brand's authenticity provides differentiation.

But fashion is fickle. Premium valuations must be earned quarter after quarter. And the very qualities that made Birkenstock cool—its outsider status, its rejection of trends, its unglamorous practicality—become harder to maintain as the company scales into a multi-billion dollar public enterprise.

"We're the only 'fashion' brand that is not defined by fashion," Reichert told Glossy. "We do not chase trends."

For investors, the question is simple but profound: can a 250-year-old orthopedic shoe company keep outrunning fashion's tendency to move on? History suggests that true classics—those products that solve real problems rather than merely satisfying transient desires—can indeed endure.

The footbed, after all, hasn't changed much since Konrad Birkenstock first contoured it in 1896. Perhaps some things don't need to change. Perhaps that's precisely the point.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube