Allegion: The Story of Security at the Doorway

I. Introduction & Episode Roadmap

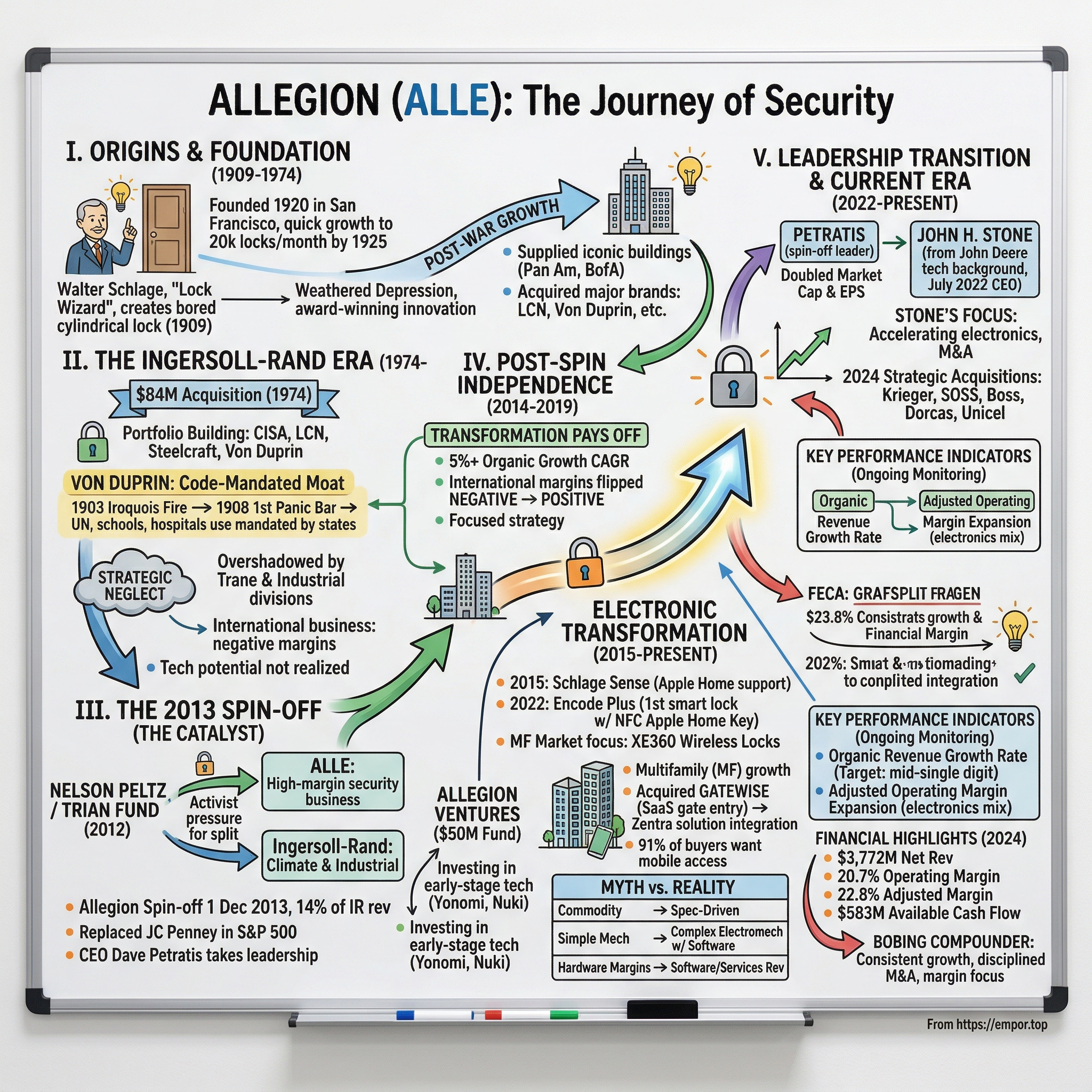

Picture a German-born engineer in turn-of-the-century San Francisco, working after-hours on an invention that would forever change how humanity secures its spaces. Walter Schlage wasn't trying to reinvent the wheel—he was trying to make opening a door turn on the lights. That simple insight, patented in 1909, would spark a century-long journey that created one of America's most valuable yet least understood industrial compounders.

Allegion plc is an American Irish-domiciled provider of security products for homes and businesses. Though it comprises thirty-one global brands, including CISA, Interflex, LCN, Schlage and Von Duprin, the company operates through two main sections: Allegion International and Allegion Americas. The company employs around 12,000 people, sells its products in more than 130 countries across the world and is part of the S&P 500. In 2024, Allegion reported full-year net revenues of $3,772.2 million.

The central question animating this story: How did a century-old lock business become a high-margin, S&P 500 compounder—and what happens when the ancient art of securing the doorway goes digital?

The answer lies in a 2013 corporate separation that liberated these security businesses from decades of conglomerate neglect. Allegion spun off from Ingersoll Rand Plc on 1 December 2013, and became a standalone, publicly traded company. This placed Allegion on the S&P 500, where it replaced JC Penney. That spin-off—driven by activist pressure and executed with precision—represents a textbook case in how strategic separations unlock hidden value.

This story weaves together several powerful threads that sophisticated investors should understand: legacy brands with hidden moats, the mechanical-to-electronic transition reshaping hardware businesses, the underappreciated power of specification-driven sales, and the durability of industrial compounders in seemingly "boring" categories. The humble lock on your front door represents more strategic complexity than most investors appreciate—and Allegion sits at the center of that complexity.

II. Origins: Walter Schlage and the Birth of Modern Lock Security (1909–1974)

In 1909, a young German immigrant named Walter Reinhold Schlage sat in his San Francisco apartment, frustrated by a common problem: fumbling in the dark for light switches after opening a door. Walter Reinhold Schlage (1882–1946) was a German-born American engineer and inventor. Known as the Lock Wizard of Thuringia, he is best known for the bored cylindrical lock and the lock company that bears his name, Schlage Lock Co.

Schlage's background made him uniquely suited for invention. Early on in his life, his father recognized his aptitude for mechanics and academics and worked on his behalf to have his son admitted to the Carl Zeiss Optical Works in Jena, Germany. During his apprenticeship, Schlage learned drafting, applied mechanics and engineering. After four years, he graduated with a special award of merit.

Walter developed a sense of adventure whetted by guests that stayed in his father's hotel, in Thuringia, Germany. Following his training he left Germany for London where he worked as an instrument maker for Hileger, Ltd. Lasting a year in England, he emigrated to the United States where he gained employment with the Western Electric Company.

Walter Schlage had already secured several patents dating back to 1909, when he patented a doorknob that would also complete an electrical circuit so that, for instance, the lights would turn on when the door was opened. This wasn't just an inventor's whimsy—it represented the first bridge between mechanical hardware and electrical systems, a theme that would define the company's trajectory more than a century later.

However, Schlage's key invention was the bored cylindrical lock, which evolved through several iterations, including a 1917 filing for a mortise mechanism which locked when the knob was tilted.

The bored cylindrical lock revolutionized construction. Unlike the mortise locks prevalent at the time—which required carpenters to chisel a large rectangular pocket into the door's edge—Schlage's design needed only two simple bored holes. Installation time dropped from hours to minutes. Construction costs fell. And builders loved the simplicity.

The Schlage Manufacturing Company was founded by inventor Walter Schlage (d. 1946) in 1920 with the help of three businessmen who each contributed $10 to become equal partners. Schlage's new company grew quickly and into larger facilities throughout the 1920s. The company was manufacturing 20,000 locks per month in 1925.

Despite the opening of the new plant, the company, now known as the Schlage Lock Company, was overextended and operating at a deficit in 1926. Beset with financial difficulties, Schlage urgently appealed to Charles Kendrick, a local businessman and manufacturer, who agreed to make a substantial investment in the company. By 1929, Kendrick wiped out the deficit of more than $80,000, and netted $108,330 in 1928 against $81,157 in 1927 and a net loss of $85,585 in 1926. The company was seeing considerable success marketing a new lock for households and offices.

Nevertheless, the Schlage Lock Company weathered the financial crisis of the Great Depression, emerging as a more profitable company in the 1940s. In 1940, Schlage was awarded the Modern Pioneer award given to outstanding American inventors.

In 1946, Walter Schlage died, leaving the company he founded in the hands of his successors, who steered the firm through more profitable times.

Post-war America presented explosive growth opportunities. After the war, the company supplied lock hardware to the Pan Am Building (1964) and the Bank of America Headquarters (1969) skyscrapers. The company was also busy post-war acquiring smaller hardware manufacturers, including the California Lock Company, Peabody Company, LCN Closers, the Von Duprin Factory, and the General Lock Company (Pontiac, Michigan).

In 1974, the year the company was acquired by Ingersoll Rand, Schlage employed 1,600 and was the largest manufacturer in San Francisco. Ingersoll-Rand Company acquired Schlage Lock Company for approximately $84 million.

That $84 million acquisition—roughly $500 million in today's dollars—would prove to be one of the great bargains in industrial history. Ingersoll Rand was buying not just a profitable lock company, but a specification-driven business with architect relationships, code-mandated products, and brand loyalty that would compound for decades.

III. The Ingersoll-Rand Era: Building a Security Portfolio (1974–2012)

For nearly four decades, Schlage and its sister security brands operated within the sprawling structure of Ingersoll-Rand, a diversified industrial conglomerate focused primarily on climate control systems and industrial equipment. The security businesses were a small but reliably profitable piece of a much larger puzzle.

During this period, Ingersoll-Rand assembled an impressive portfolio of security brands. The acquisitions included CISA, an Italian lock manufacturer acquired in 2005, along with door hardware from multiple countries and market segments. The Security Technology unit grew to include Schlage Commercial and Residential Door Hardware, LCN Door Closers, Von Duprin Exit Hardware, Steelcraft doors and frames, Falcon locks, Ives hinges and door accessory hardware, and Glynn-Johnson overhead stops and holders.

The Von Duprin story deserves particular attention for investors trying to understand the power of code-mandated products. Exit hardware has been providing users with a safe means of escape since the early 20th century. Following a string of high-profile disasters – including the infamous Iroquois Theatre Fire in Chicago in 1903 – the conditions of the world's built environment and its emergency exits were more closely inspected as crucial elements of public safety. This was in large part due to The National Fire Protection Association's Life Safety Code. Incidentally, this period was a catalyst for change in the exit device industry, with the world's first panic bar made available in an assortment of configurations in 1908, courtesy of Von Duprin.

Over a century ago, Von Duprin invented the first self-releasing fire exit device. Today we continue to push the envelope by delivering innovative solutions to challenging applications.

Prinzler and DuPont submitted patents for an "Emergency Exit Attachment for Knob Latches" in October 1908. They submitted a subsequent patent for an "Emergency Exit Lock" in November 1908. In 1910, Vonnegut Hardware Company began to sell the Von Duprin Safe Exit Device.

Local architect Oscar D. Bohlen implemented the panic bar as part of the design specifications for the Murat Theatre not only to make the building safer but to publicize the use of the new device. In March 1910, the Indiana state factory inspector confirmed the new theater exceeded Indiana theater safety law requirements. Most other public buildings in Indianapolis soon implemented the panic bar.

Within 45 seconds, every student escaped the building that equipped every door with Von Duprin devices. The United Nations headquarters in New York City (1947) and the Statler Center and Hotel were two of countless buildings across the United States designed with the Von Duprin device on all exit doors. Most states required its use in places of public assembly such as schools, hospitals, and theaters.

Vonnegut Hardware Company owned the Von Duprin exit hardware division until Schlage Lock Company purchased the business on June 1, 1966.

But while the security businesses grew steadily, they were often overshadowed by Ingersoll-Rand's larger divisions. The strategic logic of housing security within a diversified industrial conglomerate made less and less sense as the years passed. Climate control systems (Trane) and industrial equipment operated with fundamentally different dynamics than door hardware and access control.

After 73 years of operation, the Schlage Lock Co. Bayshore factory was closed in 1999. Manufacturing began shifting away from San Francisco, marking the end of an era for Schlage's historic presence in the city where Walter had founded the company.

Management's rationale for the separation at the time was to allow each company to execute their distinct strategies by deploying resources in a more focused way. In other words, there weren't significant synergies between the two businesses and parts of Allegion were being neglected as part of Ingersoll-Rand.

This neglect was most apparent in the International businesses, which operated at negative margins. The cutting-edge access control technology wasn't being appreciated by Ingersoll-Rand investors focused on larger industrial equipment markets. The security division represented high-margin, high-return-on-capital opportunities that simply weren't getting the attention they deserved within the conglomerate structure.

IV. The Spin-Off: Allegion is Born (2013)

The transformation began in May 2012, when activist investor Nelson Peltz's Trian Fund Management acquired a major stake in Ingersoll-Rand. In May 2012, Trian announced that in partnership with CalSTRS, it had a 7% stake in Ingersoll Rand. In August, Peltz joined its board. Trian and Peltz spearheaded a move to break up the company to improve profitability.

The spin-off, buybacks and dividend hikes are part of a strategic review undertaken by Ingersoll after investor Nelson Peltz's Trian Fund Management LP acquired a stake of about 7 per cent and proposed a break-up of the company. Peltz joined the company's board in August after three months of arguing for changes at the manufacturer.

Peltz's thesis was straightforward: Ingersoll-Rand's conglomerate structure obscured the value of its distinct businesses. Peltz has suggested separating Ingersoll's main business units into three separate publicly-listed companies focused on air conditioning and heating, security, and the remainder of its industrials businesses.

On December 10th, 2012 Ingersoll-Rand completed a strategic review and announced the spin-off their commercial and residential security business, Allegion, into a new public company. Activist investment firm Trian Partners had a large stake in the company and was pushing for a breakup. The total transaction took about a year to close but ultimately resulted in two separate companies, each with distinct business drivers, margin structures, and returns on capital. Allegion made up about 14% of the total Ingersoll-Rand revenue at the time of the transaction.

Reuters noted that "the spinoff removes some of the legacy company's best high-margin businesses, which account for about 14 percent of revenue."

As previously announced, Ingersoll Rand expects the spinoff, which is intended to be tax free to shareholders, to occur prior to year-end. Allegion is the name of the new $2.05 billion security company. The name represents the collaborative, long-term relationships the company forges with customers. It embodies the company's team of experts and their relentless commitment to safeguarding people and property.

Allegion ordinary shares were distributed on December 1, 2013, with Ingersoll Rand shareholders receiving one Allegion ordinary share for every three Ingersoll Rand ordinary shares held at the close of business on the record date of November 22, 2013.

David D. Petratis was announced chairman of the board, chief executive officer and president of the company, in August 2013. Petratis brought manufacturing leadership experience from Quanex Building Products and would guide the newly independent company through its formative years.

Allegion, a constituent of the S&P 500®, was a $2 billion business employing more than 7,600 people and offering products in more than 120 countries across the world.

"For more than a century, we have been pioneers in developing products that help keep people safe where they live, work and visit," said Dave Petratis, Allegion chairman, president and CEO. "This is an opportunity to carry forward the best of Allegion's heritage, expertise and entrepreneurial roots while becoming bolder at capitalizing on major trends in commercial and residential security."

"The future of our company and the entire security industry lies in addressing the needs of an increasingly connected world. That's why we intend to invest in the electronic side of our business moving forward, all while maintaining our same level of dedication to the continuous improvement and advancement of our mechanical products," Petratis added.

This wasn't just corporate platitude—it was a strategic declaration. From day one, Allegion's leadership recognized that the mechanical-to-electronic transition would define the company's next chapter.

V. Post-Spin Transformation: Independence Pays Off (2014–2019)

The benefits of independence became apparent almost immediately. Allegion is a 2013 spin-off from Ingersoll-Rand that has benefited significantly from the separation. As a stand-alone company removed from their former conglomerate parent, the business has received much more attention, particularly in their international segments where margins have flipped from negative to positive. Organic revenue growth has compounded at over 5% per year.

The business is deeply entrenched with customers and has strong brands in niche security access control markets. This all cumulates in a very attractive financial profile and return on invested capital.

The international margin improvement was particularly striking. Under Ingersoll-Rand's stewardship, the international security operations had languished with negative margins—essentially a value-destroying drag on the overall business. Freed from conglomerate neglect, Allegion's management could finally give these operations the attention they deserved. Cost structures were rationalized, pricing was improved, and within a few years, international margins had flipped from negative to solidly positive territory.

The acquisition strategy began taking shape. Management defined three key focus areas: product portfolio expansion, emerging technology and solutions, and growth of software and services. Each acquisition was evaluated through the lens of strategic fit rather than pure financial engineering.

On March 8, 2018, Allegion plc launched Allegion Ventures – a $50 million corporate venture fund formed to accelerate the growth of innovative technologies and products.

"Creating this corporate venture fund underscores Allegion's commitment to investment in growth companies, which is a part of our long-term strategy, as evidenced by our previous investments in Yonomi and Nuki," said Allegion Chairman, President and CEO David D. Petratis. Allegion Ventures will invest in early-stage companies that are poised for growth and going beyond traditional approaches to make security and access smarter, stronger, faster and less intrusive.

"We want to use our knowledge of how real people live and work to make security and access better in the future. With the addition of a venture fund, Allegion – already a pioneer in the industry – will help companies grow and scale faster as a result of our market expertise." Allegion's experience in residential and commercial markets, distribution and marketing presence in almost 130 countries, manufacturing capabilities and robust knowledge of IoT trends make it uniquely qualified to help portfolio companies reach their full potential.

The venture fund represented more than financial investment—it was a listening post for technological disruption and a pathway to accelerate emerging technologies into Allegion's product portfolio.

The 2017-2018 period proved particularly robust, with organic revenues growing at nearly 6%. The company was benefiting from an improving economic environment, but the fundamental thesis was playing out: a focused security company could execute more effectively than a division buried within a diversified conglomerate.

VI. The Electronic Transformation: Mechanical to Digital (2015–Present)

The transition from mechanical to electronic security represents one of the most significant technological shifts in Allegion's century-long history—and one of the most compelling value creation opportunities for shareholders.

The evolution began in earnest in 2015, when Schlage introduced the Sense deadbolt—a Bluetooth-enabled smart lock and its first to support Apple Home. This wasn't just a product launch; it was Allegion's first serious foray into the connected home ecosystem that was beginning to reshape residential security.

Back at CES 2022, Schlage introduced the Encode Plus deadbolt, the first smart lock in North America to support Apple's home key feature that lets you unlock your door via NFC just by using an iPhone or Apple Watch.

Debuting in 2022, the Encode Plus made history as the first smart lock compatible with Apple's NFC Home Key technology, enabling seamless door access using an iPhone or Apple Watch.

The Schlage Encode Plus went on sale on March 31, 2022, which is when we reviewed the lock; it costs $299, which is $50 more than the Schlage Encode, which will continue to be sold alongside the Encode Plus.

As first announced at WWDC 2021, iOS 15 evolves Apple Wallet to store keys for hotels, homes, and even cars. The Schlage Encode Plus is the first such consumer lock solution to take advantage of the NFC-powered Apple home key support. Schlage's smart lock is finally widely available at Home Depot.

The commercial side saw similar innovation. Allegion US has introduced the Schlage® XE360™ Series Wireless Locks, a new electronic lock portfolio designed with multifamily market needs – like style and technology – in mind, at an attractive price point. The XE360 Series is the next generation of innovative electronic locks from Schlage, outfitted with the options and features most looked for by multifamily properties and made to fit the needs of a wide range of common area openings. With in-demand finishes and modern lever styles, the XE360 Series was designed to complement a variety of design styles.

The trend of mobile access control is increasing in popularity for apartment selection. According to Allegion's 2023 Multifamily Living Trends Report, over 59% of survey respondents would select a future place of residence if they were able to access their unit using a mobile device.

At CES 2025, Allegion unveiled its latest breakthroughs. Schlage, a trusted leader in home security and access solutions for over a century, today announced its latest breakthroughs in smart lock technology at the 2025 Consumer Electronics Show (CES): the Schlage Sense Pro™ Smart Deadbolt and the Schlage Arrive™ Smart WiFi Deadbolt. Set to transform home access with its cutting-edge innovation, the Schlage Sense Pro™ Smart Deadbolt, which will feature Matter-over-Thread, delivers a hands-free unlocking experience that combines ultimate convenience with trusted security. The Schlage Sense Pro™ Smart Deadbolt introduces the brand's latest development of Schlage Converge™ technology. This feature uses Ultra Wideband and the user's paired and authorized personal device to intelligently calculate speed, trajectory and motion, ensuring seamless, intuitive entry.

"With the coming launches of the Schlage Sense Pro™ Smart Deadbolt and Schlage Arrive™ Smart WiFi Deadbolt, we are excited to continue our legacy of commitment to innovation in home security," said David Perozzi, general manager, Allegion Home. "As our first smart lock that will be Matter-over-Thread compatible, Schlage Sense Pro™ redefines home access."

The multifamily strategy has been particularly aggressive. Founded in 2017 and based in Houston, Texas, Gatewise is a software-as-a-service provider that offers a modern and retrofit-friendly gate entry system for multifamily communities. The Gatewise portfolio features a mobile app for residents and a cloud-based management portal for property managers. It is highly complementary to Allegion's electronic locks and Zentra multifamily access solution, bringing together expanded perimeter security with unit and common area security.

"This acquisition strengthens Allegion's position as a leader in smart, secure and scalable access solutions, especially for multifamily property owners and their residents," Allegion President and CEO John H. Stone said. "Together, Gatewise and Zentra will bring a more complete access and security solution to multifamily properties, delivering recurring value to our customers and end users with seamless, safe experiences."

The electronic transformation matters for investors because electronic products typically carry higher margins and stronger competitive moats than mechanical alternatives. A $50 mechanical deadbolt faces commoditization pressure; a $300 smart lock with proprietary software creates switching costs and potential recurring revenue streams through software updates and ecosystem integration.

VII. Leadership Transition & Strategic Evolution (2022–Present)

In May 2022, Allegion announced a pivotal leadership transition. Allegion plc announced that John H. Stone will succeed David D. Petratis as president and CEO, effective July 11, 2022.

Petratis has led Allegion since its spin-off from the former Ingersoll Rand in 2013, capping off a distinguished 40-year career. During his tenure, Allegion has achieved substantial financial and business success, doubling its market capitalization and annual adjusted earnings per share (EPS), delivering industry-leading profitability and completing more than 20 acquisitions and strategic investments.

Stone's background marked a departure from traditional lock industry executives. Most recently, he served as president of Deere & Company's Worldwide Construction, Forestry and Power Systems business, overseeing the nearly $11.4 billion segment. Under Stone's leadership, the segment has delivered impressive growth and profitability. He has also been influential in Deere & Company's rapid development of artificial intelligence (AI) and machine learning capabilities, better integration of precision-ag technology into each of its flagship products and in helping the company establish itself as a leader in technology. Prior to Deere & Company, Stone was a quality engineer at General Electric and an infantry officer in the U.S. Army.

In that role, he led the company's acquisition of tech startup Blue River Technology, in addition to the establishment of the San Francisco John Deere Labs office and the precision-ag headquarters in Urbandale, Iowa. John enjoyed a 20-year career at Deere & Company and held additional leadership positions, including: vice president, Corporate Strategy & Business Development; global director, Utility Tractor Product Line; and general manager, John Deere Ningbo (China) Works. Prior to Deere & Company, John worked for General Electric as a Six Sigma Black Belt quality engineer, and he served as an infantry officer in the U.S. Army. John holds a bachelor's degree in mechanical engineering from the U.S. Military Academy and an MBA from Harvard Business School.

"Allegion's leadership succession plan enables a smooth transition of the CEO role. John is an outstanding leader with a proven ability to formulate and deliver operating and business process excellence, and he possesses a deep understanding of the technological trends shaping our world."

Stone's technology background proved immediately relevant given the accelerating electronic transformation. The board recruited someone who had navigated the precision agriculture revolution at John Deere—a useful parallel for a lock company transitioning from mechanical to connected products.

Strategic decisions under the new leadership have included optimizing the geographic footprint. One more item of interest that I'd like to cover given the evolving headlines in recent weeks is tariffs. Our guidance includes the currently enacted tariffs on imports from China and at the enterprise level we import less than 5% of our cost of goods sold from China. We're taking a combination of pricing actions and sharing those costs with our suppliers to minimize the impact.

The 2024 acquisition activity accelerated under Stone's leadership. Mergers and acquisitions (M&A) play a key role in Allegion's growth strategy. In 2024, we acquired five businesses that will help us deliver innovative solutions, expand our capabilities and strengthen our position as a global leader in security and access solutions. The newest additions to the Allegion portfolio of brands enable us to build on our strengths while meeting more customer needs in the market.

In 2024, Allegion continued to expand its innovative portfolio and meet additional customer needs through strategic acquisitions. We invested in five bolt-on companies that leverage Allegion strengths, like our specification-writing capabilities, our deep customer relationships and our manufacturing and distribution scale.

Strategic Acquisitions: In 2024, Allegion executed several strategic acquisitions to enhance its product offerings and market presence, including the acquisition of Boss Door Controls, Dorcas, Krieger Specialty Products, Unicel Architectural Corp., and SOSS Door Hardware. These acquisitions are part of the company's strategy to expand its Allegion Americas and Allegion International segments.

Dorcas is a leading manufacturer of electro-mechanical access control solutions in Spain, specializing in the production of electric strikes, electro-mechanical and electro-magnetic locks, as well as complementary access control solutions and door control products. Dorcas solutions are distributed and sold internationally with a strong presence across European markets, including healthcare and education verticals. Boss Door Controls is a door solutions provider in the U.K. serving customers in the specified door hardware market and holding meaningful relationships with the local architectural channel. Its portfolio includes door closers and levers, automatic door operators and pocket door frames.

VIII. Current Financial Performance & Business Model

Allegion reported full-year 2024 net revenues of $3,772.2 million and net earnings of $597.5 million, or $6.82 per share.

"Allegion delivered a record year in 2024 – a year marked by consistent, strong execution, solid margin expansion and balanced capital deployment," said Allegion President and CEO John H. Stone.

Full-Year Financial Highlights include EPS of $6.82, up 11.4% compared with $6.12; Adjusted EPS of $7.53, up 8.2% compared with $6.96. Revenues of $3,772.2 million were up 3.3% on a reported basis and up 2.1% on an organic basis. Operating margin of 20.7%, compared with 19.4%; Adjusted operating margin of 22.8%, up 70 basis points compared with 22.1%.

Available cash flow, which is defined as net cash from operating activities minus capital expenditures, was $582.9 million for 2024, an increase of 12.9%.

The outlook for 2025 reflects continued steady execution. The company expects full-year 2025 revenues to increase 1% to 3% on a reported basis and increase 1.5% to 3.5% organically, when compared to 2024. Full-year 2025 reported EPS is expected to be in the range of $7.05 to $7.25, or $7.65 to $7.85 on an adjusted basis.

The Americas segment remains the engine of profitability. Allegion Americas is the largest segment, accounting for approximately 80% of sales and 90% of segment profitability.

On an organic basis, which excludes impacts of acquisitions, divestitures and foreign currency movements, net revenues increased 3.5%, led by the Americas region. The organic revenue increase was driven by price realization and volume growth.

Capital Management: The company amended and restated its Credit Facilities, increasing the total commitment on the Revolving Facility from $500 million to $750 million and extending its maturity to May 2029. It issued $400 million of 5.600% Senior Notes due 2034, using the proceeds to repay existing debt. In 2024, the company paid $167 million in dividends and repurchased approximately 1.6 million shares for $220 million.

InvestingPro analysis reveals the company has maintained dividend payments for 12 consecutive years, with a 13.3% dividend growth in the last twelve months.

Myth vs. Reality: "Allegion is Just a Lock Company"

| Myth | Reality |

|---|---|

| Simple mechanical products | Complex electromechanical systems with software components |

| Commodity competition | Specification-driven sales with 2-3 year specification cycles |

| Low technology content | Smart locks with NFC, WiFi, UWB, and Matter integration |

| Discretionary spending | Building code-mandated safety products |

| Pure hardware margins | Growing software and services revenue streams |

IX. Playbook: Business & Investing Lessons

The Specification Moat

The most underappreciated aspect of Allegion's business model is the specification-driven nature of commercial sales. When architects design buildings, they specify particular door hardware—often by brand name—in their drawings and construction documents. These specifications are typically made 12-36 months before construction begins and product is actually purchased.

Those brands have roots in businesses from as early as 1750, and many have since created their respective product categories, adding to the breadth of the company global heritage and pioneering spirit. Today, Allegion and its brands continue innovating and developing leading-edge solutions.

Codes such as NFPA 101 The Life Safety Code and International Building Code (IBC) include requirements pertaining to panic hardware. NFPA 101 and IBC are frequently used as the basis for many state building codes such as California Building Code (CBC), but adoptions may vary. The International Fire Code (IFC) is the base code for many state fire codes. Application of any code may vary depending on which publication and edition are being enforced in a particular jurisdiction.

This creates a powerful moat: once Schlage or Von Duprin is written into the specifications, switching becomes extremely difficult. Contractors purchasing hardware years later must either use the specified products or seek approval for substitutions—a time-consuming process most prefer to avoid.

The "Boring" Compounder Model

Overall, investors have the opportunity to purchase a competitively entrenched 'orphan' business with a very attractive ROIC and normalized operating profile of low-to-mid single digit revenue growth with operating leverage pushing margins up a bit over time. This is consistent with management's targets of mid-single digit organic growth, EBITDA margin expansion, EPS growth of ~10%, and ~100% cash flow conversion.

The consistency is remarkable: steady organic growth, margin expansion through operational focus, and disciplined capital allocation. This isn't a "growth stock" in the traditional sense, but it compounds value reliably.

The Spin-Off Playbook

As a stand-alone company removed from their former conglomerate parent, the business has received much more attention, particularly in their international segments where margins have flipped from negative to positive.

The fragmented market structure reflects regulatory requirements at the local level and niche customer needs. The industry has historically been disciplined, with companies able to pass through pricing increases to customers to at least keep up with raw material inflation.

The Electronic Transition

The ongoing shift toward higher-margin electronic products parallels transformations in other industrial businesses—think the shift from mechanical to electronic industrial controls. Electronic products carry higher ASPs, better margins, and create potential for recurring software and services revenue.

X. Porter's Five Forces & Hamilton's 7 Powers Analysis

Porter's Five Forces

1. Threat of New Entrants: LOW

The high market concentration creates significant entry barriers for new players, as success in this sector requires large capital investments, long-term reliability, and compliance with stringent security regulations.

Specification-driven sales create a 2-3 year lag between when products are designed into buildings and when revenue is recognized. New entrants would need to build architect and specifier relationships over many years before seeing meaningful commercial revenue.

2. Bargaining Power of Suppliers: MODERATE

Steel, brass, zinc, and electronic components are commodity inputs with multiple supply sources. The industry has historically maintained pricing discipline, passing through raw material inflation to customers.

3. Bargaining Power of Buyers: LOW-MODERATE

The customer base is highly fragmented—builders, contractors, building owners—with no single buyer representing significant revenue concentration. Once products are specified, switching costs are high due to keying systems and integrated access control. The aftermarket/replacement business provides recurring revenue with even lower buyer power.

4. Threat of Substitutes: LOW

Offshore private label competitors can reach market quickly through online channels, representing a real risk on the residential side—but that's only ~25% of Allegion's portfolio. Commercial security requires code compliance, installation expertise, and liability considerations that limit substitution.

5. Competitive Rivalry: MODERATE-HIGH

The access control market is consolidated, with the top five players (dormakaba Group, ASSA ABLOY, Johnson Controls, Honeywell International Inc., and Allegion Plc) collectively holding around 70–80% of the total market share in 2024. These companies leverage their extensive product portfolios, global distribution networks, and strong customer relationships to maintain leadership across commercial, government, residential, and other verticals. Their dominance enables them to set pricing structures, influence technology adoption, and establish performance benchmarks, while continuous investments in R&D and integration with digital solutions strengthen their competitive edge.

Allegion's main competitors include Assa Abloy, Stanley Black & Decker, Honeywell International, Johnson Controls, and Dorma+Kaba.

Hamilton's 7 Powers Analysis

1. Scale Economies: MODERATE

Manufacturing scale provides some cost advantage but isn't the dominant source of competitive advantage. The real economies come from specification relationship leverage and brand portfolio breadth.

2. Network Effects: WEAK (but emerging)

Traditional mechanical locks have essentially zero network effects. However, electronic access control systems are beginning to show network effects with integrated software platforms, mobile credentials, and building management systems. As Allegion builds its software ecosystem around Zentra, Gatewise, and other platforms, network effects may become more meaningful.

3. Counter-Positioning: STRONG (during electronic transition)

The shift towards smart lock manufacturers presents a notable competitive threat.

Allegion's integrated hardware + software approach is difficult for pure mechanical competitors to match quickly. Meanwhile, pure-play smart lock startups (August, Level) lack the specification relationships and commercial credibility that Allegion's century-old brands provide. This counter-positioning creates opportunities on both flanks.

4. Switching Costs: STRONG

Master keying systems across buildings create significant switching costs—if a university uses Schlage locks across 50 buildings, switching to a competitor would require replacing every lock or maintaining dual key systems indefinitely. Access control software integration with building systems adds another layer of switching costs.

5. Branding: STRONG

In 2024 — for the fifth year in a row — Schlage was recognized as the most trusted brand in the America's Most Trusted Door Locks & Hardware Study conducted by Lifestory Research.

The company benefits from a strong legacy of brands including CISA®, Interflex®, LCN®, Schlage®, SimonsVoss®, Von Duprin® and Zentra®.

6. Cornered Resource: MODERATE

The specification relationships developed over decades represent a form of cornered resource—these relationships can't be quickly replicated by competitors. The code-mandated nature of products like Von Duprin panic hardware provides another layer of protection.

7. Process Power: MODERATE

Manufacturing and distribution expertise built over a century provides some process advantage, though this is less distinctive than the relationship and brand-based powers.

Key Performance Indicators for Ongoing Monitoring

For investors tracking Allegion's ongoing performance, two KPIs warrant particular attention:

1. Organic Revenue Growth Rate This metric strips out acquisition, divestiture, and currency effects to reveal the underlying health of the business. Management targets mid-single digit organic growth; consistent achievement of 3-5% organic growth signals healthy specification wins and market share maintenance. Watch for any sustained deviation below this range, which might indicate competitive pressure or market share loss.

2. Adjusted Operating Margin Expansion With the electronic transformation underway, margin expansion reflects successful execution of the higher-ASP, higher-margin product transition. The 2024 adjusted operating margin of 22.8% (up 70 bps year-over-year) demonstrates continued improvement. Investors should monitor whether this trajectory continues as electronics mix increases.

Investment Considerations

Bull Case Factors: - Specification-driven sales create durable competitive moats - Electronic transformation offers higher margins and recurring revenue potential - Disciplined M&A strategy adds value without empire-building - Strong cash generation supports dividends, buybacks, and acquisitions - Institutional markets (healthcare, education, commercial) remain healthy - Post-spin-off management attention has dramatically improved international margins

Bear Case Factors: - Construction cycle exposure creates revenue volatility - Residential segment (~25% of sales) faces more commoditization pressure - ASSA ABLOY's scale (13% of global market) dwarfs Allegion's position - Smart lock startup competition could intensify - Tariff exposure on Mexican manufacturing (~20-25% of COGS) - Technology transitions carry execution risk

Key Risks to Monitor: - Construction spending trends, particularly non-residential - Competitive dynamics in smart/electronic locks - Trade policy developments affecting Mexico-sourced products - Integration success of acquired businesses - Cybersecurity vulnerabilities in connected products

Conclusion

Allegion's story illuminates a powerful pattern in industrial investing: the hidden value that can be unlocked when focused management attention replaces conglomerate neglect. What Ingersoll-Rand saw as a small, peripheral business—accounting for just 14% of revenue—has become a standalone S&P 500 company that has doubled earnings per share since independence.

The century-long journey from Walter Schlage's San Francisco workshop to today's connected lock ecosystem demonstrates remarkable strategic consistency: secure the doorway, build specification relationships, innovate within the category, and never compromise on quality. These principles have survived world wars, depressions, technology transitions, and corporate restructurings.

For investors, Allegion represents a specific type of opportunity: the "boring compounder" that consistently generates mid-single-digit organic growth, expands margins through operational focus, and compounds shareholder value through disciplined capital allocation. It won't appear on lists of the fastest-growing companies, but neither will it likely destroy capital through ill-conceived acquisitions or boom-bust revenue cycles.

The electronic transformation represents the most significant strategic inflection point since the company's founding. Success here—transitioning from purely mechanical products to connected, software-enabled solutions—would extend Allegion's competitive advantages into a new technological era. Failure could open doors (quite literally) to disruptive competitors.

For those who understand the specification moat, appreciate the durability of code-mandated products, and believe in the compounding power of steady execution, Allegion offers a window into how centuries-old businesses adapt and thrive. The lock on your front door has never been more interesting.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube