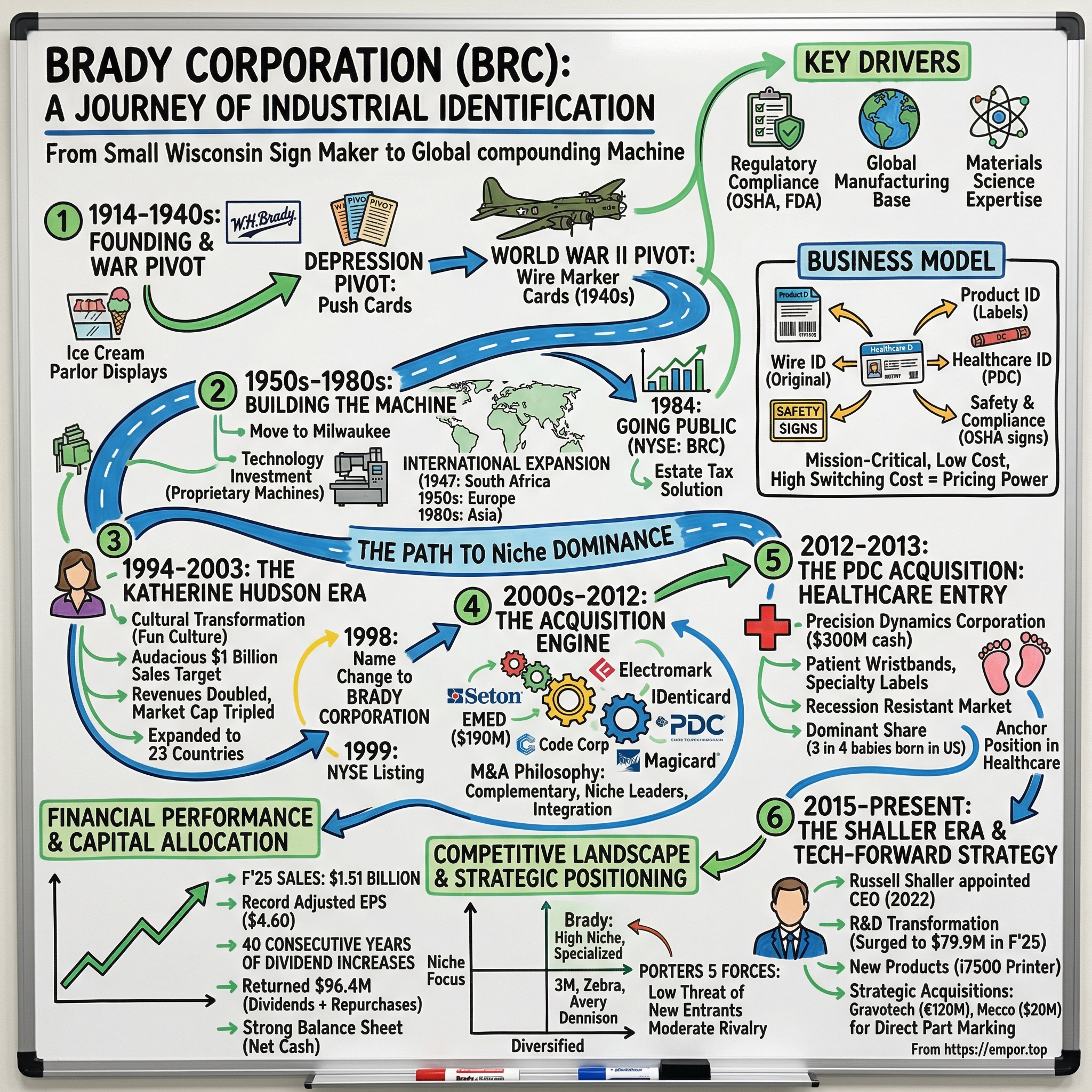

Brady Corporation: The Quiet Giant of Industrial Identification

I. Introduction: The Invisible Backbone of Modern Industry

In the basement of a Dallas hospital, a nurse scans a patient's wristband before administering medication. Inside a Boeing assembly plant in Seattle, a technician traces a wire marker to identify a critical electrical connection. At a construction site in Munich, a safety inspector photographs a pipe marker to verify compliance with local regulations. On the floor of a Foxconn facility in Shenzhen, a quality control manager scans a precision label to track a smartphone component through its journey from raw material to finished product.

These seemingly mundane moments share a common thread: they all depend on products manufactured by a company most investors have never heard of. Brady Corporation is an American developer and manufacturer of specialty products, technical equipment, and services for identifying components used in workplaces. Headquartered in Milwaukee, Wisconsin, Brady employs 6,600 people in North and South America, Europe, Asia, and Australia and serves customers and markets globally.

The hook for investors is deceptively simple: How did a company that started making painted signs and promotional calendars in 1914 become the invisible backbone of modern industrial safety and identification, serving everyone from NASA to hospital delivery rooms?

The answer lies in a story of transformation, disciplined execution, and the rare ability to compound value in decidedly unglamorous markets. Brady Corporation reported record adjusted earnings per share of $4.60 in fiscal year 2025, marking a 9.0% increase over the previous year and the fifth consecutive year of record adjusted EPS results. Total revenue reached $1,514 million, representing a 12.9% increase from F'24, with organic growth contributing 2.6% and acquisitions adding 10.5%.

This episode explores the themes that define Brady's century-long journey: the power of boring businesses, niche dominance through deep specialization, M&A as a disciplined growth engine, and the art of compounding in industrial B2B markets where customer relationships can span generations.

II. The Sign Painter's Vision: Founding & Origins (1914–1940s)

Picture Eau Claire, Wisconsin in 1914—a small city of perhaps 25,000 nestled in the timber country along the Chippewa River. The nation was industrializing rapidly, and advertising was evolving from hand-painted signs to more sophisticated promotional materials. It was in this environment that a young salesman named William Henry Brady made a fateful decision.

W. H. (Will) Brady's early career as a salesman for an Ohio remembrance advertising firm that manufactured calendars, yardsticks, and other promotional items on which advertising messages were printed. After turning down a promotion to the company's New York office, in 1914 Brady founded the W. H. Brady Company in Eau Claire, Wisconsin, Brady's hometown.

The decision to reject New York and return home speaks to a particular strain of Midwestern pragmatism that would come to define the company. Rather than chase the bright lights of Madison Avenue, Brady saw opportunity in serving local businesses with something tangible—visual aids that could draw customers through the door.

The company, originally named W. H. Brady Co., began with modest operations, creating colorful displays for ice cream parlors, printed glass beer signs, and roadside advertising materials to support local businesses. His first product was promotional photographic calendars sold to offices and stores, but he soon followed with elaborate color displays for ice cream parlors, printed glass beer signs, point-of-purchase displays, and pre-billboard roadside advertising.

The business grew steadily through the 1920s, riding the wave of American consumer culture. Then came October 1929.

Surviving the Depression Through Innovation

The stock market crash devastated Brady's customer base. Small retailers and local businesses—the very establishments buying his colorful displays and promotional calendars—shuttered by the thousands. After a decade and a half of growth, the stock market crash of 1929 and the depression that followed drove many of Brady's customers out of business, forcing him to sell his home and, with his parents' support, enroll in college. In the midst of this crisis, an unusual promotional gimmick saved the firm.

What saved Brady was an obscure product that seems almost quaint today: push cards. The company survived the Great Depression by producing push cards: small paperboard cards with rows of perforated circles concealing numbers. These were essentially low-tech lottery tickets used for candy promotions and small retail games of chance. The margins were thin, but the volumes were steady—people needed small pleasures during hard times.

During the 1920s and 1930s, the company transitioned from manual signage production to more industrialized products amid economic challenges. By the 1930s, Brady had become the largest U.S. producer of push cards.

This Depression-era pivot reveals something essential about Brady's DNA: the willingness to abandon pride for pragmatism. Will Brady had built a business creating beautiful promotional displays for prospering retailers. When that market collapsed, he didn't stubbornly cling to his original vision. He pivoted to whatever would keep the lights on.

The World War II Pivot: Finding a Permanent Niche

If push cards kept Brady alive during the Depression, World War II gave it a purpose that would define the company for the next eight decades.

Prior to the 1940s, electricians relied on primitive methods of identifying wires including marking them with color codes, tie-on tags, or actual notches. World War II brought an urgent need for a clear and easy way to identify the ever-more dense masses of wiring being installed in ships, planes, and other military equipment.

Modern warfare had created an identification problem. A single B-17 bomber contained miles of electrical wiring. A destroyer had even more. When something went wrong—and in combat, things went wrong constantly—technicians needed to trace specific wires through dense tangles of cables. The primitive methods that had served peacetime electricians were woefully inadequate for the chaos of wartime maintenance.

During World War II, Brady developed the wire marker card – numbered cloth strips on an adhesive card. This deceptively simple innovation—numbered cloth strips that could be wrapped around wires and would adhere despite heat, moisture, and fuel exposure—became standard equipment across the U.S. military.

The strategic decision during World War II to move away from promotional goods towards specialized industrial identification products, like wire markers for naval ships, set the foundation for the company's long-term niche focus.

Brady markers identified every pipe in the Manhattan Project's weapons plant in the 1940s. Brady Contract Services was used on North Slope during construction of the Alaska gas pipeline.

The wartime experience taught Brady's leadership several crucial lessons. First, industrial customers were more stable than retail customers—factories don't close during recessions the way ice cream parlors do. Second, compliance and safety requirements created reliable demand—when the Navy mandated wire identification, it wasn't optional. Third, specialty products with high switching costs could command premium prices—once technicians learned Brady's system, they weren't eager to switch.

By 1945, W. H. Brady Company had transformed from a promotional products business into an industrial identification specialist. The colorful ice cream parlor displays were gone. In their place was a growing catalog of wire markers, pipe markers, and industrial labels that would form the foundation of a billion-dollar enterprise.

III. The Bill Brady Jr. Era: Building the Machine (1950s–1980s)

William Henry Brady passed away in 1953, but by then his son had already begun shaping what would become the modern company. Bill Brady Jr. took the company from its humble origins with the advent of wire marker cards for industrial identification, to going public (NYSE: BRC) in 1984.

Bill Brady Jr. inherited a small but profitable niche business. What he built was something more ambitious: a self-sustaining growth machine with proprietary technology, international reach, and a disciplined acquisition strategy.

The Milwaukee Relocation and Technology Investment

In the 1950s and 1960s, Brady moved to Milwaukee. The company developed proprietary machines that could laminate, die cut, print and cut to length in a single operation.

The move to Milwaukee was more than geographic convenience. Wisconsin's largest city offered access to a deeper labor pool, better transportation links, and proximity to the industrial customers concentrated in the Great Lakes manufacturing belt. It also signaled ambition—Brady was no longer a small-town operation content with regional success.

More importantly, Brady Jr. recognized that the company's competitive advantage would ultimately depend on manufacturing capabilities that competitors couldn't easily replicate. The proprietary machines that could laminate, die cut, print, and cut in a single operation weren't just efficiency improvements—they created barriers to entry. A competitor would need years and significant capital investment to match Brady's manufacturing sophistication.

International Expansion: Thinking Globally Before It Was Fashionable

1947: Brady began selling its products internationally, to South Africa. 1950s: First European sales office in U.K., and operations in Canada. 1960s and 1970s: Expansion throughout Europe with operations in Belgium, Germany, France and Sweden. 1980s: Entered Asia, Australia, Hong Kong, Japan and Singapore.

The international expansion is remarkable for its timing. In 1947, when Brady made its first international sale to South Africa, most American manufacturers were focused entirely on the booming domestic market. The war was over, consumer demand was exploding, and the concept of "globalization" wouldn't enter the business vocabulary for decades.

Brady Jr.'s foresight in pursuing international sales created what would become a crucial competitive moat. By 1980, international subsidiaries accounted for 20 percent of sales.

Now operating six domestic divisions and eight international subsidiaries, Brady's annual sales grew 350 percent through the 1980s to $175 million, and profits soared past the $10 million mark.

Strategic Failures That Shaped Discipline

Not every initiative succeeded. The 1970s brought both innovation and expensive failure.

It had to abandon the product in 1972, however, when DuPont's competing brand won the battle for market share and Brady's engineers were unable to overcome Phodar's poor shelf life limitations. The same year Brady unveiled Kalograph, an instant, one-step label maker that promised to enable customers to create their own custom industrial labels. The product's high cost, however, combined with its inability to create black lettering and its labels' tendency to fade in sunlight, undermined Kalograph's early promise, and in 1979 Bill Jr. finally pulled it from the marketplace, making it the most expensive failure in Brady's history.

The Kalograph failure was painful but instructive. It taught Brady's leadership that innovation for its own sake wasn't enough—products needed to solve real customer problems at prices customers would actually pay. The experience also demonstrated discipline: rather than continuing to pour resources into a failing product, Bill Jr. cut his losses and moved on.

The Acquisition Machine Begins

In 1981, Brady acquired Seton Identification Products, a direct marketing business that sold nearly identical products.

The Seton acquisition established a template that Brady would follow for the next four decades. Rather than trying to build competing sales channels organically, Brady bought an established player with complementary distribution capabilities. Seton's catalog operation brought different customers—those who preferred browsing printed catalogs and ordering by phone rather than working through Brady's industrial sales force.

Seton's catalog mailings rose from 1 million in 1981 to 8 million in 1988 and 1985. Subsidiaries were established in England, Canada and Germany by 1988.

By the mid-1980s, Brady had grown from a small Wisconsin manufacturer into an international enterprise with diversified distribution channels, proprietary manufacturing technology, and a track record of profitable growth. Bill Brady Jr. had taken his father's post-war identification business and built something much larger: a platform ready for the next phase of expansion.

IV. Going Public: The IPO Catalyst (1984)

The decision to take Brady public in 1984 was driven by a reality that affects many successful family businesses: mortality and estate taxes.

In 1984 Brady became a private/public hybrid when it sold 500,000 shares of nonvoting stock to avoid the estate taxes due when Bill Brady Jr.'s heirs inherited his stake in the company.

This is a story as old as American capitalism. A founder builds something valuable over decades. As death approaches, the family faces a brutal choice: sell the business entirely, or find a way to create liquidity without surrendering control. The creation of nonvoting Class A shares allowed the Brady family to monetize a portion of their stake while maintaining governance control through Class B voting shares.

In 1984, the company went public and began trading on the NASDAQ market. Brady Corporation went public in 1984, listing on the NASDAQ under the ticker symbol BRC, which provided capital for expansion and subsequent acquisitions. The company later transitioned its trading to the New York Stock Exchange in 1999, maintaining the BRC ticker.

The 1984 IPO was a pivotal moment, unlocking access to capital markets which enabled Brady to pursue aggressive growth strategies, particularly through mergers and acquisitions, that would have been difficult as a private entity.

This initial public offering marked a pivotal shift, enabling Brady to diversify beyond its core industrial identification products into broader markets.

The Transition After Bill Brady Jr.

That moment came in 1988 when Bill Jr., the Brady Company's second founder, died, and a longtime Brady insider, Paul Gengler, took over direction of the company.

Bill Brady Jr.'s death in 1988 marked the end of the founding era. He had taken a small Depression-era survivor and built it into an international industrial enterprise with public shareholders. The question now was whether Brady could continue to thrive under professional management rather than family leadership.

Paul Gengler's tenure as a transitional figure prepared the company for what would come next: the arrival of an outsider who would transform Brady's culture, ambition, and trajectory.

V. The Katherine Hudson Era: Transformation (1994–2003)

By 1993, Brady faced a strategic crossroads. The company was profitable but stagnating—a well-managed industrial business that seemed content with modest growth. The board made a bold decision: hire an outsider with no industry experience to shake things up.

Brady retired its family-run reputation permanently in 1994 by hiring Katherine M. Hudson, a vice-president at Eastman Kodak, to lead it into the 21st century.

Katherine M. Hudson becomes the first non-family member to run the company.

In 1993, Hudson joined W. H. Brady and became its first female President and CEO in January 1994. The company was renamed the Brady Corporation in August 1998 and Hudson became its chairperson on April 1, 2003.

The Outsider's Perspective

Ms. Hudson is the retired Chairman of the Board of Directors, President and Chief Executive Officer of Brady Corporation, a global manufacturer of identification solutions and specialty industrial products. Ms. Hudson became President and CEO of Brady in 1994 after spending twenty-four years with Eastman Kodak Company. Her career at Kodak included positions in systems analysis, supply chain, finance, corporate communications, investor relations, information technology, litigation operations and general management.

Hudson brought an outsider's willingness to challenge assumptions that insiders take for granted. Her Kodak experience had exposed her to sophisticated marketing, global operations, and the urgency of technological change. She looked at Brady and saw not a finished company but raw material waiting to be shaped.

An aggressive, hands-on executive with a ready sense of humor, Hudson announced her intention to quadruple annual sales to $1 billion, improve earnings, and exploit new opportunities for joint ventures, acquisitions, and geographic expansion, particularly in such new markets as Italy, Brazil.

The billion-dollar target seemed audacious for a company with sales in the $250 million range. Hudson's ambition signaled that the comfortable growth rates of the past wouldn't satisfy the new management.

Cultural Transformation: From Stodgy to Spirited

You wouldn't think of Brady Corporation as an obvious place in which to find a fun culture. This traditional Midwestern company, a manufacturer of industrial signs and other identification products, didn't even allow employees to have coffee at their desks until 1989.

But when Katherine Hudson became CEO in 1994, she and her executive team determined that injecting some fun into the company's serious culture could create positive effects within the organization and contribute to increased performance and sales.

The coffee anecdote captures something essential about pre-Hudson Brady. This was a company so buttoned-up that it prohibited one of the most basic office rituals. Such rigidity might produce consistent execution, but it doesn't foster the creativity and initiative needed for aggressive growth.

At Brady, getting people to loosen up and enjoy themselves has fostered a company esprit de corps and greater team camaraderie. It has started conversations that have sparked innovation, helped to memorably convey corporate messages to employees, and increased productivity by reducing stress, among other benefits. And the company has doubled its sales and almost tripled its net income and market capitalization over the past seven years.

Results: The Transformation Quantified

From 1994 until her retirement in 2004, Brady expanded from 8 countries to 23 and its revenues doubled and market capitalization tripled.

In joining Brady as its leader, Katherine became the first female president and chief executive officer of a major public company in Wisconsin.

Hudson's tenure at Brady coincided with her serving on other prestigious boards, including Apple Computer's board of directors—a testament to her standing in corporate America. Hudson joined the board of directors of Apple Computer in 1994. However, she resigned in 1997 following the return of Apple co-founder Steve Jobs.

The Name Change: From W.H. Brady to Brady Corporation

As Brady prepared to enter the new millennium, the company opted to change its name to Brady Corporation. Hudson gave reasoning for the change in a July 1998 company press release stating, "As a company that's operating on a global stage to provide high-performance products and services, Brady needs a strong identity which communicates the quality, innovation and global reach we represent." She continued, "W.H. Brady Co. was named after the company founder, William H. Brady. While the name has served us well through the years, the name Brady Corporation reflects our growth from a private, small company founded in 1914 to a publicly traded, international business."

In 1998, W.H. Brady Co. became Brady Corporation and in 1999, the company began trading on the New York Stock Exchange under the ticker symbol BRC.

The NYSE listing was both practical and symbolic. The New York exchange offered greater visibility, analyst coverage, and prestige than NASDAQ. For a company with global ambitions, it was the appropriate venue.

Navigating the Asian Financial Crisis

Not everything went smoothly during Hudson's tenure. Exposure to international markets however, proved costly as the Asian financial crisis cut into the company's bottom line. Sales in Asia faltered and the company was forced to trim costs and cut 200 jobs.

The 1997-1998 Asian crisis was Hudson's first major test. Her response—cost-cutting and job reductions—demonstrated that she wouldn't let sentiment override financial discipline. The experience also validated Brady's geographic diversification strategy: when Asia stumbled, other regions picked up the slack.

By the time Hudson stepped down as CEO in 2003 and chairman in 2004, she had transformed Brady from a comfortable regional manufacturer into an aggressive global competitor. The company she inherited had been content with single-digit growth; the company she left behind was hungry for more.

VI. The Acquisition Engine: Building an Empire (2000s–2012)

If Hudson planted the seeds of aggressive growth, her successor Frank Jaehnert would harvest them through the most prolific acquisition period in Brady's history.

Beginning significantly in the late 1990s, the company embarked on a deliberate strategy of acquiring complementary businesses worldwide. This approach rapidly scaled operations, diversified revenue streams, and cemented its position in the workplace safety and identification markets, shaping its current structure and operational footprint.

In the 2000s, more than 35 acquisitions led to a tripling in size between 2003 and 2010.

The M&A Philosophy

Brady's acquisition strategy was characterized by several consistent principles. First, targets needed to be complementary—either bringing new products to existing customers or existing products to new customers. Second, they should have defensible market positions, preferably as niche leaders. Third, integration needed to be achievable without destroying what made the target valuable.

1990s: Began operating in Mexico, Italy, and Brazil with further expansion in Asia to China, Malaysia, Philippines, South Korea, and Taiwan.

Frank Jaehnert Takes the Helm

EMED Company is acquired for $190 million.

The EMED acquisition in 2004 represented Brady's largest deal to that point—a sign that the company was ready to pursue transformational acquisitions rather than just bolt-on deals.

Building the Brand Portfolio

As a result of acquisitions, Brady products are traded under a variety of names and brands, including Code Corporation, Nordic ID, Magicard, IDenticard, Seton, Electromark, PDC, Emedco, Scafftag, Clement Communications, ID Warehouse, Securimed, Signals, Precision Dynamics Corporation, Accidental Health & Safety, Safety Signs & Service, Trafalgar Australia, Carroll, SPC, and Transposafe.

This proliferation of brands reflected a deliberate strategy. Rather than forcing acquired companies to adopt the Brady name—potentially alienating loyal customers—Brady allowed successful brands to maintain their identities while integrating back-office operations. This approach preserved customer relationships while capturing synergies.

Brady serves over 300,000 customers in a wide variety of industries including general manufacturing, maintenance and safety, construction, electrical, telecommunications, electronics, laboratory/healthcare, airline/transportation, security/brand education, governmental, and public utility industries. Its more prominent customers have included NASA, Boeing, Hollywood's film industry, IBM, PepsiCo, General Electric, and the Alaskan oil pipeline.

VII. The PDC Acquisition: Healthcare Entry (2012–2013)

If there was a single acquisition that most dramatically expanded Brady's addressable market, it was the 2012 purchase of Precision Dynamics Corporation.

Brady Corporation (NYSE:BRC), a world leader in identification solutions, announced today that it has acquired Precision Dynamics Corporation (PDC) from Water Street Healthcare Partners, a strategic private equity firm focused exclusively on the health care industry, in a cash transaction for $300 million, subject to customary working capital and post-close adjustments. PDC, with annual sales of approximately $173 million, is a leader in identification products primarily for the healthcare market, specializing in patient wristbands, specialty labels and identification systems used in hospitals to reduce medical errors and integrate and share patient data.

The Strategic Rationale

"The acquisition of PDC, a leader in the U.S. healthcare identification space, provides an important anchor position for Brady in the attractive healthcare market and fits well with our mission to identify and protect premises, products and people, and our vision to be the market leader in all of our businesses," said Brady President and Chief Executive Officer Frank M. Jaehnert.

The healthcare market represented something Brady's traditional industrial markets couldn't match: recession resistance. Hospitals don't stop admitting patients during economic downturns. If anything, healthcare demand tends to be countercyclical. By acquiring PDC, Brady was diversifying away from the industrial cycle that had historically driven its results.

PDC's Market Position

In fact, three out of four babies born in the US wear PDC wristbands within minutes of birth. No other company can match our extensive portfolio of medical grade patient identification wristbands, labels, medical products, visitor and employee identification solutions, and more.

More than 80% of U.S. hospitals already use PDC hospital wristbands.

This market position was exactly what Brady sought: a dominant share in a mission-critical application where switching costs are high and regulatory requirements create barriers to entry.

PDC, founded in 1956, is based in Valencia, Cal., and employs approximately 1,000 people globally. The company has manufacturing facilities in Tijuana, Mexico and Port Orange, Fla., and a European sales office with light manufacturing in Nivelles, Belgium.

PDC co-founder Dr. Walter W. Mosher was 22 years old and focused on his engineering studies at UCLA when he started Precision Dynamics Corporation with three investors in 1956. The company developed what was then a revolutionary innovation: a single-piece wristband, no parts, no tools necessary. It sold immediately and became the system of choice for hospitals worldwide. With steady growth, PDC blazed new trails and set new standards, developing identification solutions for multiple markets, including healthcare, entertainment/recreation, law enforcement, and more.

VIII. The Shaller Era: Tech-Forward Strategy (2015–Present)

The most recent chapter in Brady's evolution began with the appointment of Russell Shaller as CEO in April 2022.

Shaller was appointed Brady's President and CEO and to the Company's Board of Directors in April, 2022 after serving seven years as president of Brady's Identification Solutions business.

Shaller was appointed Brady's President and CEO and to the Company's Board of Directors in April, 2022 after serving seven years as president of Brady's Identification Solutions business. Mr. Shaller places a strong emphasis on new product development, having helped to transform Brady's new product pipeline. Prior to joining Brady, from 2008-2015, he served as President of Teledyne Microwave Solutions, with responsibility for advanced microwave products sold in the aerospace and communications industry.

Mr. Richardson added, "We are fortunate to have Russell step in to serve as our President and CEO. With nearly 7 years of experience at Brady and over 30 years in the industrial manufacturing industry, Russell's leadership has been essential to both Brady's organic growth and inorganic expansion through the recent acquisition of companies in the high-growth industrial track and trace market."

The R&D Transformation

Shaller's most distinctive contribution has been dramatically increasing Brady's investment in research and development.

The Company incurred $79.9 million, $67.7 million, and $61.4 million of expense on its R&D activities during the years ended July 31, 2025, 2024, and 2023, respectively. The majority of R&D spend supports the Company's identification products.

In Q4 2025, R&D spending surged 31% to $23.1 million (5.8% of sales), funding innovations like the i7500 industrial label printer.

These acquisitions are designed to expand Brady's offerings in direct part marking and inkjet technologies, crucial for enhancing barcode verification and compliance systems. Furthermore, increased investment in R&D, with nearly $80 million spent in fiscal 2025 and plans for continued growth, underscores a commitment to organic innovation in identification products, coatings, adhesives, and printing systems, which is vital for long-term competitive advantage.

Strategic Acquisitions Under Shaller

Brady Corporation (NYSE: BRC) ("Brady") today announced that it has completed its acquisition of Gravotech Holding ("Gravotech"), a leader in specialized marking and engraving solutions, in a transaction valued at EUR 120 million (approximately USD 130 million). "We are pleased to welcome the Gravotech team to Brady," said Brady's President and Chief Executive Officer, Russell R. Shaller. "Gravotech offers specialty laser and mechanical engraving capabilities intended for direct part marking within a variety of industries and applications. The addition of Gravotech expands our product offering into precision direct part marking and engraving, directly aligning with Brady's market leading position in product identification solutions and specialty adhesive materials. We intend to expand Gravotech's addressable market by utilizing Brady's global footprint throughout Europe, Asia and the Americas."

Brady Corporation (NYSE: BRC) ("Brady," "our," "we") announced today that it has acquired Mecco Partners, LLC ("Mecco") for approximately $20 million, and for the fiscal year ending July 31, 2026, Brady expects revenue of approximately $20 million. Brady funded the acquisition with cash on hand. Mecco specializes in industrial product marking and identification systems designed for a variety of applications and industries. Its laser marking and pin marking technologies are custom designed and incorporate software for laser marking systems, laser marking workstations and custom and configured laser marking solutions. The acquisition of Mecco complements Brady's existing offering of direct part marking solutions acquired with Gravotech in fiscal year 2025, and advances Brady's strategy to provide customers with a variety of end-to-end direct part marking and specialty identification products.

Completed three strategic acquisitions (Gravotech, AB&R, Microfluidic Solutions) to expand product offerings and R&D capabilities. During the year ended July 31, 2025, Brady completed the acquisitions of three companies: Gravotech Holding ("Gravotech"), American Barcode and RFID Incorporated ("AB&R"), and the Microfluidic Solutions business unit of Funai Electric Co., Ltd. ("Microfluidic Solutions"). The acquired companies strengthen Brady's position in faster-growing markets, enabling us to accelerate growth while expanding our product offerings and research and development capabilities.

Product Innovation Focus

"Our investments in research and development continue to drive the introduction of new products such as our i7500 high-speed printer, which was launched this quarter."

Our engineered products, all things being equal, are probably 60% gross margin versus our more commodity products are 40%. The more we have engineered products, the more our gross margin will expand.

This margin differential between engineered and commodity products explains Shaller's strategic emphasis. Every dollar invested in developing proprietary, differentiated products generates far more profit than competing in commodity markets. The R&D investment is essentially margin expansion through product portfolio improvement.

IX. Business Model Deep Dive

Understanding Brady requires understanding how the company actually makes money—and why its business model is more defensible than it might appear.

Brady Corporation, founded in 1914 and headquartered in Milwaukee, manufactures and supplies identification solutions, specialty materials, and workplace safety products globally. The company operates through two main segments: Identification Solutions and Workplace Safety. The Identification Solutions segment provides safety signs, pipe markers, labeling systems, spill control products, lockout/tagout devices, printing systems for product identification, and hand-held printers for wire identification.

Product Categories Explained

Product Identification: This includes labels, tags, and marking systems that help companies track products through manufacturing, distribution, and end-use. Think of the barcode on a manufactured component that allows a technician to scan it and immediately see its specifications, origin, and compliance certifications.

Wire Identification: Brady's original wartime business remains relevant. Modern electrical systems are even more complex than World War II aircraft, and the need for reliable wire identification has only grown.

Healthcare Identification: Through PDC, Brady provides the wristbands that identify hospital patients, the labels that track laboratory specimens, and the badges that control facility access.

Safety and Compliance: Signs, labels, and marking systems that help companies comply with OSHA, ANSI, and other regulatory requirements. This is essentially a regulatory-driven business—when compliance is mandatory, customers don't have the option of not buying.

Customer Economics

Brady Corporation makes a diversified array of industrial identification and workplace safety products. The company's ID products include label printing systems, lockout/tagout devices, wire markers and tags, hospital and entertainment wristbands, ID badges, and safety compliance software and services. Other products include safety and compliance signs, tags, and labels; informational signage; compliance posters; asset tracking labels; and first aid products.

The key insight is that Brady's products represent a tiny fraction of its customers' total spending but are mission-critical for operations. A hospital might spend millions on medical equipment but only thousands on patient wristbands—yet without proper identification, the entire operation faces catastrophic risk. This asymmetry between cost and criticality is the foundation of Brady's pricing power.

Geographic Footprint

Brady's Americas & Asia segment, which accounted for approximately 66% of total sales in Q4 F'25, delivered sales of $260.8 million, up 14.1% from the prior year.

The Americas and Asia segment has been the growth engine, while Europe and Australia have faced more challenging conditions. This geographic mix provides diversification while concentrating resources in faster-growing markets.

X. Financial Performance & Capital Allocation

Brady's financial profile reflects its business model: steady, reliable, and increasingly profitable.

"Our investments in new products once again led to strong results in the Americas & Asia region, with 4.3 percent organic sales growth in the fourth quarter and 4.8 percent organic sales growth in fiscal 2025. The result was a new all-time company record quarter and record year of adjusted earnings per share," said Brady's President and Chief Executive Officer, Russell R. Shaller.

Brady's fiscal 2025 sales were approximately $1.51 billion.

Gross margin rose to $760.8 million but declined as a percentage of sales to 50.3%. Operating income fell to $236.6 million (15.6% of sales) from $243.4 million the prior year, driven by acquisition-related inventory fair value adjustments, facility closure and reorganization costs, and incremental amortization.

Shareholder Returns

This dividend represents the 40th consecutive annual increase in dividends.

Brady Corporation increased its annual dividend to $0.98 per share, reflecting 40 years of consecutive dividend growth. Brady Corporation announced an increase in its annual dividend for Class A Common Stock from $0.96 to $0.98 per share, marking the 40th consecutive year of dividend increases.

Returned $96.4 million to shareholders in fiscal 2025 in the form of dividends and share repurchases.

The 40-year dividend growth streak places Brady in elite company. This consistency reflects both the stability of the underlying business and management's commitment to shareholder returns.

Balance Sheet Strength

The company maintained its strong financial position with a net cash balance as of July 31, 2025, while returning $96.4 million to shareholders through dividends and share buybacks.

Cash and cash equivalents were $174.3 million with available credit of $198.1 million (expandable by conditions), totaling $1,267.4 million of liquidity.

Net cash position ($152.2M cash vs $102.8M debt) and 201.2% debt-to-cash-flow coverage reinforce resilience amid global economic uncertainty.

A net cash balance sheet is unusual for a company pursuing active M&A. Most serial acquirers carry significant debt. Brady's approach—using cash flow to fund acquisitions while maintaining balance sheet strength—reflects the conservative financial philosophy that has characterized the company throughout its history.

Forward Guidance

Looking ahead to fiscal 2026, Brady provided optimistic guidance, projecting GAAP diluted EPS of $4.55 to $4.85, representing growth of 15.5% to 23.1% compared to fiscal 2025. Adjusted diluted EPS is expected to range from $4.85 to $5.15, an increase of 5.4% to 12.0%.

The low end of Adjusted Diluted EPS* guidance was raised for the full year ending July 31, 2026 from the previous range of $4.85 to $5.15 per share to the new range of $4.90 to $5.15 per share.

XI. Competitive Landscape & Strategic Positioning

Who Brady Competes Against

Competitors in the industrial identification and safety solutions market, including players like Markem-Imaje, Zebra (NASDAQ: ZBRA), and Domino Printing, might face increased competitive pressure.

However, the company must navigate challenges such as macroeconomic headwinds, including tariffs, inflation, and currency fluctuations, alongside intense competition from major players like 3M (NYSE: MMM) and Avery Dennison (NYSE: AVY).

One of Brady Corp's most formidable competitors, 3M operates across diverse segments that include safety, industrial, health care, and consumer products. Specifically, in the safety and industrial segments, 3M offers a variety of products that directly compete with Brady's offerings. These include personal protective equipment, safety signs, and labeling solutions.

Market Opportunity

This sector, projected to grow significantly from USD 6.52 billion in 2025 to USD 8.12 billion by 2030, is characterized by several overarching trends that Brady's strategic decisions align with.

Market opportunities are significant, driven by the projected growth of the global workplace safety market (expected to reach $93.6 billion by 2027) and the industrial automation market (expected to grow to $326.1 billion by 2027). The increasing adoption of IoT in industrial settings, growing at over 15% through 2028, creates substantial demand for Brady's identification and safety solutions.

XII. Porter's Five Forces & Hamilton's Seven Powers Analysis

Porter's Five Forces Analysis

1. Threat of New Entrants: LOW

The company developed proprietary machines that could laminate, die cut, print and cut to length in a single operation.

Brady's barriers to entry include: - Proprietary manufacturing technology developed over decades - Deep regulatory expertise across FDA, OSHA, HIPAA, and international compliance frameworks - Established relationships with thousands of customers built over 110 years - Materials science capabilities in adhesives, coatings, and substrates that require specialized knowledge - High switching costs for customers with integrated labeling systems

A potential competitor would need years and hundreds of millions of dollars to replicate Brady's capabilities—and would face price competition from an entrenched incumbent with scale advantages.

2. Bargaining Power of Suppliers: LOW to MODERATE

Brady has vertical integration in key materials science areas and multiple sourcing options for commodity inputs. Specialized adhesives and substrates create some dependencies, but Brady's purchasing scale gives it leverage in negotiations.

3. Bargaining Power of Buyers: LOW to MODERATE

Brady has more than 1 million customers with fiscal net sales for 2013/14 of US$1.225 billion.

The fragmented customer base is a crucial advantage. No single customer represents a significant portion of Brady's revenue, eliminating the concentration risk that plagues many industrial suppliers. Additionally, Brady's products are mission-critical but represent a small portion of customers' total costs—the classic "low-cost of failure, high cost of switching" dynamic that supports pricing power.

4. Threat of Substitutes: LOW

Industrial identification and safety products are regulated necessities. Digital alternatives require physical implementation—a digital facility management system still needs physical labels, signs, and markers. Healthcare identification has no practical substitute—patients must be physically identified.

5. Industry Rivalry: MODERATE

Brady Corporation, a renowned player in the field of identification and safety solutions, faces competition from various companies across multiple sectors. These competitors range from large multinational corporations to specialized firms focusing on specific niches within the broader market that Brady Corp operates in. Understanding its competitive landscape is crucial for grasping Brady Corp's position in the market and its strategies for growth and innovation. Here, we highlight some of the notable competitors that Brady Corp contends with in its industry.

While Brady faces competition from giants like 3M and Avery Dennison, its niche focus provides defensible positions in specialized markets where scale advantages matter less than expertise and customer relationships.

Hamilton Helmer's Seven Powers Framework

1. Scale Economies: Moderate. Brady's manufacturing scale provides cost advantages, but these are less dramatic than in commodity manufacturing.

2. Network Effects: Limited. Unlike software platforms, identification products don't become more valuable as more people use them.

3. Counter-Positioning: Strong. Brady's focus on specialty identification makes it difficult for diversified competitors to match its depth of expertise without cannibalizing their broader businesses.

4. Switching Costs: High. Customers invest in Brady's printing systems, train personnel on Brady's products, and integrate Brady's identification systems into their operations. Switching requires time, money, and operational risk.

5. Branding: Moderate to Strong. The PDC brand's dominance in hospital wristbands and Brady's reputation for quality in industrial identification create preference that supports pricing power.

6. Cornered Resource: Brady's proprietary manufacturing technology and 110 years of materials science expertise qualify as cornered resources that competitors cannot easily replicate.

7. Process Power: Strong. Brady's ability to develop, manufacture, and distribute specialized identification products efficiently has been refined over a century. This institutional knowledge is embedded in processes that competitors cannot quickly copy.

XIII. Investment Considerations

The Bull Case

Regulatory Tailwinds: Safety and compliance requirements continue to expand globally. Every new OSHA regulation, FDA guideline, or international compliance standard creates demand for Brady's products. The company profits from complexity.

Healthcare Exposure: Through PDC, Brady has significant exposure to healthcare—a sector with demographic tailwinds (aging populations) and regulatory requirements that drive identification product demand.

Innovation Pipeline: The increased R&D investment under Shaller is beginning to produce higher-margin engineered products that can command premium prices.

Capital Allocation Discipline: The combination of dividends, buybacks, and strategic acquisitions demonstrates management's ability to deploy capital effectively. The 40-year dividend growth streak speaks for itself.

Acquisition Integration Track Record: Brady has successfully integrated dozens of acquisitions without the write-offs and disappointments that plague many serial acquirers.

The Bear Case

Organic Growth Challenges: Organic sales growth has been in the low single digits. The company's growth has increasingly depended on acquisitions, raising questions about the sustainability of its expansion.

European Weakness: The Europe and Australia segment has faced declining organic sales, requiring restructuring and facility closures. Geographic concentration risk remains a concern.

Integration Risks: Recent acquisitions like Gravotech and Mecco need to be successfully integrated. While Brady has a good track record, execution risk exists with any M&A strategy.

Tariff and Currency Exposure: As a global manufacturer with supply chains spanning multiple countries, Brady faces exposure to trade policy uncertainty and currency fluctuations.

Technology Disruption: While digital transformation has created opportunities, it also poses risks. New identification technologies could potentially disrupt Brady's traditional product lines.

Key Metrics to Monitor

For investors tracking Brady's ongoing performance, two KPIs stand out as the most critical:

1. Organic Revenue Growth Rate: This metric strips out the effects of acquisitions and currency to show how Brady's existing business is performing. Consistent low-single-digit organic growth indicates healthy market share maintenance; acceleration would signal the R&D investments are paying off; deceleration would raise concerns about competitive positioning.

2. R&D as a Percentage of Sales: Shaller has made R&D investment central to Brady's strategy. Tracking this ratio reveals whether management is maintaining its commitment to innovation. The FY2025 level of approximately 5.3% of sales represents a meaningful increase from historical levels; sustained or increased investment suggests continued focus on higher-margin engineered products.

XIV. Conclusion: The Compounding Machine

Brady Corporation's 110-year journey from a small Wisconsin sign painter to a global identification solutions leader illustrates the power of compounding in boring businesses. The company has never dominated headlines, never disrupted industries, never achieved the kind of explosive growth that creates venture capital legends. Instead, it has done something arguably more difficult: steadily build value through disciplined execution across more than a century of economic cycles, technological changes, and competitive pressures.

The company that Will Brady founded to sell photographic calendars to small-town businesses now provides products that identify patients in hospitals, components in aircraft, and chemicals in laboratories. Its wire markers still serve the same fundamental purpose they did during World War II—preventing catastrophic failures by ensuring people can identify what they're working with—but they now incorporate materials science, printing technology, and software integration that Brady's founder could never have imagined.

For investors, Brady represents a particular kind of opportunity: not the chance for explosive returns, but the potential for steady compounding supported by defensible market positions, consistent cash generation, and disciplined capital allocation. The 40 consecutive years of dividend increases tell the story better than any analysis: this is a company that has figured out how to grow while returning capital to shareholders, a combination that many companies promise but few achieve.

The question for prospective investors is whether Brady's past performance can continue. The bull case rests on regulatory tailwinds, healthcare demographics, and R&D-driven margin expansion. The bear case points to organic growth challenges, geographic weakness, and the inherent risks of acquisition-dependent growth. Both perspectives have merit.

What seems indisputable is that Brady has built something durable. In a market often obsessed with disruption and rapid growth, there's something to be said for a company that has been identifying and protecting premises, products, and people for 110 years—and seems positioned to continue doing so for decades to come.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube