ALK-Abelló: The Century-Old Danish Company Quietly Treating the World's Allergies

I. Introduction: A Hidden Champion in Plain Sight

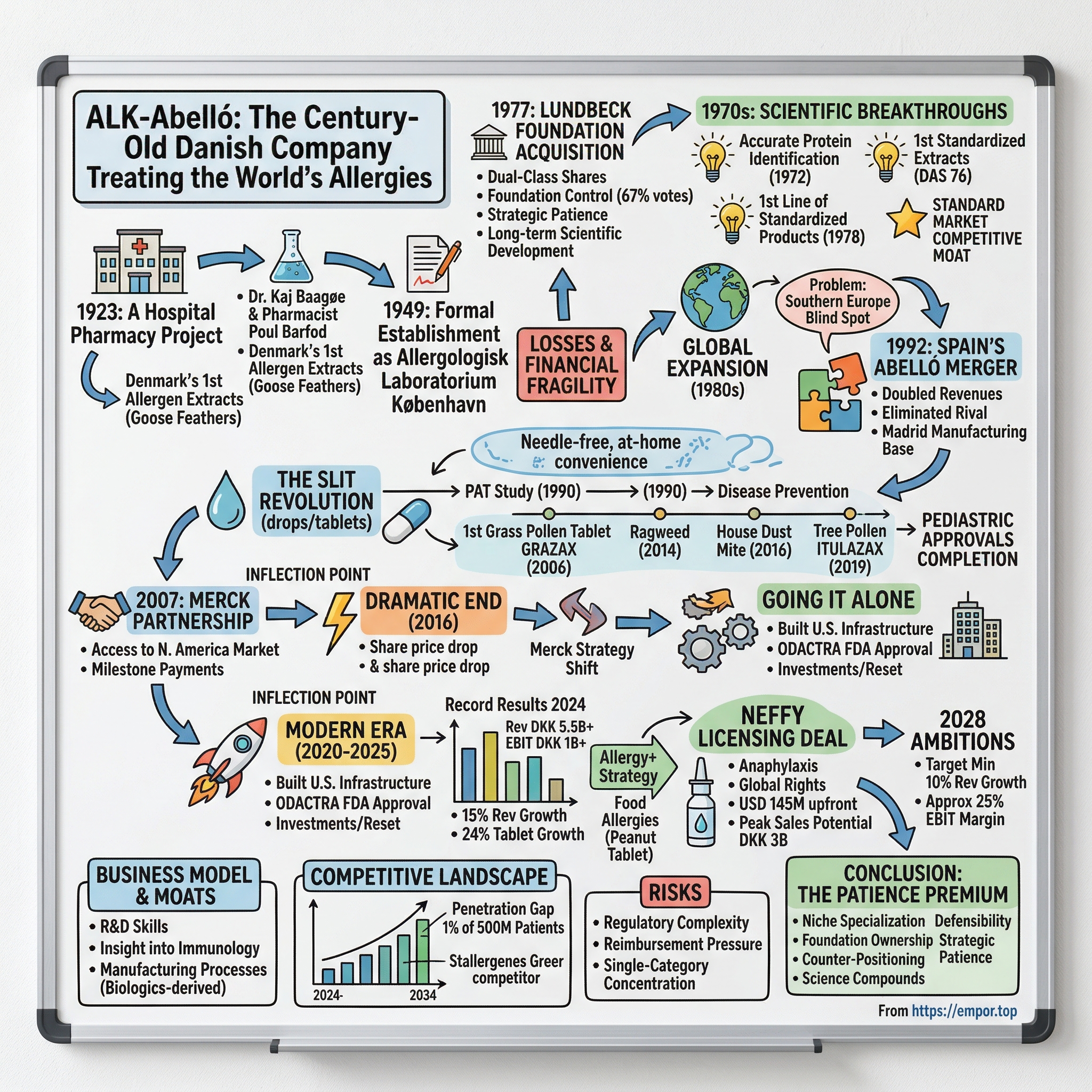

Picture Copenhagen in 1923. A young doctor named Kaj Hedemann Baagøe stands in the sterile corridors of Rigshospitalet—Copenhagen University Hospital—watching children struggle to breathe during asthma attacks. These weren't the dramatic emergency room scenes of today; medicine had few answers for allergies beyond vague advice to "avoid triggers." But Baagøe saw something others didn't: a pattern in how certain substances provoked these attacks, and perhaps, a way to train the body to fight back.

From that hospital pharmacy, where Baagøe's pharmacist partner Poul Barfod recorded Denmark's first allergen extract—goose feathers, ironically not even a significant allergen—emerged a company that would quietly become one of the most durable, specialized pharmaceutical businesses on the planet. ALK-Abelló dates back to 1923, when Denmark's first allergen extracts were produced at the pharmacy of the Copenhagen University Hospital. The company was subsequently established as Allergologisk Laboratorium København.

Today, ALK-Abelló commands a 35% global market share in immunotherapies for allergies. It is one of the world's largest makers of allergy immunotherapy products with 67% of its revenue coming from sales in Europe. The company employs 2,900 people globally and operates across 46 countries, generating over DKK 5.5 billion in annual revenue. Yet most investors have never heard of it.

The central question driving this analysis: How did a university hospital pharmacy project become the unchallenged world leader in a $2 billion market that most pharmaceutical giants walked away from? And what does ALK-Abelló's trajectory tell us about the power of niche specialization, foundation ownership, and the courage to go it alone when your largest partner abandons you?

Allergies are a 500 million patient market, but only 1% of patients are using immunotherapies. If that penetration rate shifts even modestly, ALK sits at the epicenter of a massive opportunity. But penetration has remained stubbornly low for decades—why? Is this a value trap or a coiled spring?

The story of ALK-Abelló is one of those rare business narratives that spans the entire arc of modern pharmaceutical development—from artisanal hospital pharmacy concoctions to FDA-approved biologics, from European family-owned roots to the world's most sophisticated clinical trial machinery. It's a story of patience measured in decades, of regulatory moats built allergen by allergen, and of the strategic resilience required when your biggest bet suddenly gets handed back to you.

II. The Founding Story: From Hospital Pharmacy to Allergy Pioneer (1923-1977)

The origin of ALK-Abelló involves a partnership as unlikely as it was consequential. In 1923, Doctor Kaj Baagøe and pharmacist Peter Barfod produced Denmark's first pharmaceutically manufactured allergen extract at Copenhagen University Hospital (Rigshospitalet). Dr. Baagøe had been researching asthma in children, particularly its relationship to allergic reactions, while Barfod worked on the practical chemistry of allergen preparations in the hospital pharmacy.

Their first recorded extract was goose feathers—and here's the irony that underscores how nascent allergy science was at the time: goose feathers weren't actually a significant allergen source. The real culprits were the dust mites living in duvets and pillows. But imperfect as that first extract was, it set a train of thought in motion that would define ALK's mission for the next century.

The concept behind allergy immunotherapy (AIT) was both counterintuitive and elegant: expose patients to tiny, gradually increasing doses of the substances triggering their allergic reactions. Over time, this "desensitization" could train the immune system to tolerate what it once attacked. Unlike antihistamines or corticosteroids—which merely masked symptoms—AIT addressed the root cause. This disease-modifying approach offered something no other allergy treatment could: the possibility of long-term remission.

In 1949, production of allergy vaccines and diagnostics was centered at an independent unit called Allergologisk Laboratorium (Allergology Laboratory). This marked ALK's formal establishment as a standalone entity, though it remained closely tied to the academic research community in Copenhagen.

The scientific breakthroughs came in rapid succession during the 1970s. In 1972, the technique to accurately identify the proteins that provoke allergies in individual patients was developed. In 1976, the first standardized process for allergen extracts (DAS 76) was developed. Then came the watershed moment: In 1978, ALK released the first standardized line of products for the treatment of allergies. The world's first standardized allergy immunotherapy product had arrived.

Why did standardization matter so much? Before DAS 76, allergen extracts were essentially artisanal products—each batch potentially varying in potency and composition. Standardization transformed allergy treatment from craft to science, enabling reproducible clinical outcomes, rigorous testing, and eventually, regulatory approval pathways that would become ALK's competitive moat.

But scientific progress couldn't mask the company's financial fragility. After more than four decades as an independent company, in the mid-1970s Allergologisk Laboratorium København posted consecutive years of losses and saw its finances stretched. The pioneering allergy lab was running out of money. It needed a savior—and found one in an unlikely corner of the Danish pharmaceutical establishment.

III. The Lundbeck Foundation Era & Spanish Merger (1977-2005)

The Lundbeck Foundation's 1977 acquisition of ALK would prove transformative—not just for providing capital, but for establishing a governance structure that would define the company's strategic patience for the next half-century.

The Lundbeck Foundation became the major shareholder of ALK. The foundation awards research grants primarily to support research in the biomedical sciences. The Foundation's model prioritized long-term scientific development over quarterly earnings pressure—exactly what a company developing therapies with multi-year treatment protocols and decade-long clinical development timelines needed.

Although traded on the NASDAQ Copenhagen, ALK boasts an unusually stable ownership, with two shareholders having notified shareholdings of 5% or more. The Lundbeck Foundation, one of Denmark's largest enterprise foundations, is the controlling shareholder of ALK, holding 67% of the votes and 40% of the capital.

This dual-class share structure deserves attention. A- and AA-shares are almost all in the hands of the Lundbeck Foundation, which also owns approximately 35% of the B-shares and thus controls ALK with 40% of capital and 67% of the votes. The Foundation's control insulates ALK from activist pressure and hostile takeovers, enabling management to pursue strategies that might take a decade to bear fruit.

The Foundation grants a minimum of DKK 500 million each year to public biomedical and health science research. Its business activities encompass majority shareholdings in two other healthcare companies, H. Lundbeck and Falck, a significant shareholding in Ferrosan Medical Devices and Ellab, and an international portfolio of early-stage biotech companies.

Under Foundation ownership, ALK expanded globally throughout the 1980s. In 1984, ALK began a period of global expansion by establishing a presence in several new markets and through strategic acquisitions. But by the early 1990s, a geographical blind spot had become impossible to ignore.

In the early 1990s, ALK occupied a strong position in the USA and was the market leader in Scandinavia and Central Europe. Yet its presence was almost non-existent in Southern Europe, despite collaboration with local distributors. One of the many reasons was the dominance of the Spanish company Alergia e Inmunología Abelló S.A: with its headquarters in Madrid and subsidiaries in Italy and Germany, the company was ALK's strongest competitor in the European market, with sales at the time higher than ALK's.

The opportunity to transform this competitive landscape came from an unexpected source: corporate scandal.

But thanks to the financial troubles and corruption scandals embroiling Abelló's Italian owner (the Ferruzzi Group), the Spanish company was acquired in 1992 for DKK 305 million, immediately doubling ALK's revenues.

The ALK-Abelló merger was a masterstroke of opportunistic M&A. A landmark in ALK-Abelló's history was the 1992 merger with a Spanish competitor, Abello Pharmaceuticals. The company's current name is a combination of the three initial letters of its original name and the name of its Spanish merger partner. In one transaction, ALK eliminated its fiercest European rival, gained critical manufacturing capabilities in Madrid, and established the Southern European beachhead that had eluded it for decades. In 1992, ALK and Abello merged.

The Foundation's role in enabling this acquisition cannot be overstated. A publicly-traded company without patient controlling shareholders might have hesitated to deploy capital for a transformational but risky acquisition during uncertain times. The Lundbeck Foundation's long-term orientation gave ALK's management the freedom to act decisively.

IV. The SLIT Revolution: From Injections to Tablets (1990s-2006)

The problem with traditional allergy immunotherapy was simple but commercially devastating: no one wanted to do it. Subcutaneous immunotherapy (SCIT) required patients to receive injections at a doctor's office—typically weekly during the initial buildup phase, then monthly for three to five years. Each visit took time. Each injection hurt. Many patients dropped out before experiencing full benefits.

ALK recognized that the needle was killing the market. In the 1990s, ALK was the first company to launch sublingual immunotherapy drops (allergy immunotherapy administered as droplets under the tongue).

ALK-Abelló was the first company to offer allergy sufferers the option of administering immunotherapies that were delivered as drops placed under the tongue—"sublingual immunotherapy" in industry lingo, or "SLIT." These drops were first offered for grass pollen, then for other allergens such as ragweed pollen and house dust mites.

Sublingual delivery wasn't just more convenient—it fundamentally changed where and how patients could receive treatment. Instead of weekly clinic visits, patients could administer drops at home. The implications for patient compliance, healthcare costs, and ultimately, market penetration were profound.

But ALK's innovation ambitions went further. In the 1990s, the company initiated one of the most important studies in allergy immunotherapy history.

In 1990, the PAT (Preventative Allergy Treatment) study was initiated in collaboration with leading European allergy specialists. The PAT study wasn't just measuring symptom relief—it was testing whether allergy immunotherapy could actually prevent disease progression. Specifically: could treating hay fever prevent it from developing into asthma?

When the 10-year follow-up results were published in 2007, they delivered landmark evidence: allergy vaccination could indeed prevent hay fever from developing into asthma. This finding transformed how physicians and patients thought about AIT—not just as symptom management, but as disease prevention.

The next leap came with tablets. The world's first sublingual allergy immunotherapy tablet (SLIT-tablet) was approved in Europe in 2006. GRAZAX, the grass pollen tablet, offered even greater convenience than drops. The tablet dissolved under the tongue in seconds, required no refrigeration, and could be self-administered with minimal training.

In recent years, ALK's research and development strategy has been focused on introducing a range of sublingual immunotherapy tablets. The first, for grass pollen allergy, was launched in 2006, and was followed by SLIT-tablets for ragweed pollen allergy in 2014, and house dust mite allergy in 2016.

This was paradigm-shifting for market accessibility. The tablets made home-based treatment practical for millions of patients who would never have tolerated weekly injection visits. ALK had spent decades building scientific expertise in allergen extraction and standardization—now it had a delivery mechanism that could finally unlock the market's potential.

Understanding why this matters requires grasping what makes AIT fundamentally different from other allergy treatments. Unlike antihistamines and corticosteroids that mask symptoms, AIT addresses the underlying cause of allergic diseases. It gradually desensitizes the immune system to specific allergens, offering the possibility of long-term remission even after treatment ends. This disease-modifying approach is why patients who complete AIT treatment can experience benefits that persist for years—or decades.

V. The Merck Partnership & Its Dramatic End (2007-2016): A Key Inflection Point

By the mid-2000s, ALK faced a strategic dilemma. The company had developed revolutionary tablet-based immunotherapies with compelling clinical data. Europe was adopting them enthusiastically. But North America—the world's largest pharmaceutical market—remained essentially untapped.

The U.S. market presented unique challenges. American allergists were comfortable with existing treatment paradigms. The healthcare system's structure meant that office-based injections (SCIT) were often economically attractive for allergy practices. And the FDA's biologics approval pathway for allergen products was notoriously complex.

ALK decided it needed a partner with deep U.S. commercial capabilities—and found one in pharmaceutical giant Schering-Plough (which later merged with Merck).

In 2007, ALK entered into a strategic partnership with MSD (then Schering Plough), known as Merck in the USA and Canada, to develop and commercialise a portfolio of sublingual allergy immunotherapy tablets against grass pollen (GRASTEK®), ragweed (RAGWITEK®) and house dust mite allergy in the USA, Canada and Mexico.

The deal was substantial. Under the agreement, ALK would receive up to DKK 1.6 billion (USD 290 million) in milestone payments from Merck. Merck was responsible for all costs of clinical development, registration, marketing and sales of the products on the North American markets.

For a mid-sized European pharma company, partnering with Merck seemed like hitting the jackpot. One of the world's largest pharmaceutical companies would shoulder the financial burden of U.S. clinical trials, navigate FDA approval, and deploy its formidable sales force to drive adoption.

The partnership delivered initial success. In 2014, the grass and ragweed SLIT-tablets were launched in the US. The FDA approvals for GRASTEK and RAGWITEK represented milestone achievements—the first sublingual allergy immunotherapy tablets approved in the United States.

Then came the shock.

In June 2016, U.S. pharma giant Merck & CO told Denmark's ALK-Abelló that it plans to end their partnership, causing the share price of the Denmark-based allergy specialist to drop by more than 18%.

Following a review of Merck & Co's strategic priorities and after partnership sales for the last two years fell below expectations, the New Jersey-based company informed its partner of the news. As a result, all rights to ALK's sublingual allergy immunotherapy tablets against grass, ragweed and house dust mite allergies for North America would revert to ALK from MSD at no fee to ALK.

The timing couldn't have been worse. The decision, which came partway through a clinical trial and regulatory approval process, left ALK without a partner in the U.S. and triggered an 18% drop in its share price.

Why did Merck walk away? Faced with healthcare professionals that are reticent to shift away from existing treatment options, Merck has struggled to gain ground. The U.S. market adoption had been slower than expected. For a pharmaceutical giant with blockbuster cancer drugs and vaccines, the allergy immunotherapy market's growth trajectory simply didn't move the needle enough.

Merck had paid out more than DKK 700 million ($100 million) to ALK as part of the deal, but its returns to date had been small. In the first half of 2016, ALK earned approximately $2 million through sales royalties, R&D services and product supply under the Merck deal.

The Merck exit was a defining moment—not just for ALK, but as a case study in big pharma's relationship with niche markets. The allergy immunotherapy market was growing, but not fast enough for a company measuring success in billions. This dynamic—where large pharmaceutical companies abandon markets that are perfectly viable for focused specialists—would prove to be ALK's strategic salvation.

North America still an important opportunity. Steen Riisgaard, Chairman of ALK's Board of Directors and acting Chief Executive, said: "The timing of this move is unexpected. However, we understand that MSD's decision was based on a prioritisation of resources. Our belief that North America represents an important opportunity for ALK's SLIT-tablets is unchanged."

VI. Going It Alone: Building a U.S. Presence (2017-2020)

The Merck departure forced ALK into an existential strategic decision: find another partner or build North American commercial capabilities from scratch. Many companies in this position would have sought a quick replacement deal, accepting unfavorable terms rather than risking going it alone in the world's largest pharmaceutical market.

ALK remains fully committed to the North American markets and will mobilise resources from its North American operations and headquarters in Denmark to ensure a smooth transition. At the same time, ALK will undertake a full strategic review of the North American markets to determine the best options for future commercialisation of the SLIT-tablets. Options include alternative partnerships and commercialisation by ALK's North American subsidiary.

ALK chose the harder path: building its own U.S. commercial infrastructure. This decision reflected both strategic conviction and realistic assessment of partnership alternatives. After watching Merck struggle to prioritize AIT within its vast portfolio, ALK's leadership concluded that only a company focused exclusively on allergy could summon the sustained commitment needed to develop the U.S. market.

The transition wasn't painless. ALK had to expand its North American subsidiary, hire commercial and medical affairs teams, and establish the physician education programs that would be crucial for market development. The company also needed to see through the FDA approval process for ODACTRA, its house dust mite tablet—work that Merck had been leading.

In March 2017, the FDA approved ODACTRA®, the first allergen extract to be administered under the tongue (sublingually) to treat house dust mite-induced allergic rhinitis in adults. In 2016, ALK expanded its partnership with Abbott to cover seven markets in South-East Asia and terminated its partnerships with Merck and EddingPharm.

The FDA approval of ODACTRA was particularly significant because house dust mite allergy is a year-round condition—unlike seasonal grass or ragweed allergies, it affects patients continuously. This expanded the potential treatment window and patient population.

ALK also strengthened its North American manufacturing base through acquisitions. North American production facilities in Port Washington, New York, in Post Falls, Idaho, in Luther, Iowa, and in Oklahoma City, Oklahoma. This geographic diversification provided supply chain resilience and enabled ALK to serve the U.S. market from local manufacturing facilities.

ALK-Abello's most recent deal was a Merger/Acquisition with Allerquest. The deal was made on 02-Jan-2024.

The strategic repositioning required investments that would pressure near-term results. The changes were clearly telegraphed—"Subdued earnings over the next three years"; "Total negative cash flow"; "greatest effect in the next two years"—but the market reaction was a roughly 20% decline in the stock price. Even though it was the right long-term decision, few companies would have done such a strategic reset without the support of a long-term oriented majority shareholder like the Lundbeck Foundation.

Here again, the Lundbeck Foundation's ownership structure proved crucial. A company facing public market pressure might have cut investment or sold North American rights at unfavorable terms. The Foundation's patient capital gave management the freedom to make decisions measured in decades, not quarters.

VII. Global Expansion & Partnership Strategy (2011-Present)

While navigating the Merck situation, ALK was simultaneously building a sophisticated partnership network to access markets where local expertise and regulatory knowledge were essential.

In 2011, an agreement with Torii Pharmaceutical Co., Ltd. to develop, register and commercialize a number of SLIT-tablet products in Japan was signed. The agreement covers selected existing ALK products and diagnostics against house dust mite allergy. It also covers a research and development contract to develop a sublingual immunotherapy tablet against Japanese cedar pollen allergy.

The Japan partnership illustrates ALK's sophisticated approach to international expansion. Japanese cedar pollen allergy ("sugi") is one of the most prevalent allergic conditions in Japan, affecting roughly a quarter of the population. But the specific allergen differs from European and American pollen species. Rather than simply exporting existing products, ALK worked with Torii to develop a Japan-specific solution—CEDARCURE—that addresses the local disease burden.

In 2014, ALK signed collaboration agreements with Eddingpharm for China and Abbott for Russia and selected emerging markets. In 2015, ALK signed a collaboration agreement with bioCSL (now Seqirus) covering Australia and New Zealand. In 2016, ALK expanded its partnership with Abbott to cover seven markets in South-East Asia.

The company is present in 46 countries, either directly or via partnerships.

This partnership strategy reflects a nuanced understanding of the allergy immunotherapy market's peculiarities. Unlike pills that can be manufactured centrally and shipped globally, AIT products often require local regulatory approval based on regionally-specific allergen sources. The regulatory, medical affairs, and commercial knowledge needed to navigate these markets is difficult to build from headquarters in Denmark.

The partnership model allows ALK to access these markets with relatively modest capital deployment while leveraging local partners' existing physician relationships and regulatory expertise. Partners handle downstream commercial activities; ALK provides the science, the products, and increasingly, the global brand.

VIII. The Modern Era: Allergy+ Strategy & Record Results (2020-2025): A Key Inflection Point

The COVID-19 pandemic initially disrupted allergy treatment patterns—clinic visits declined, and some patients deferred treatment initiation. But the post-pandemic period has seen ALK accelerate into what management calls its strongest performance in company history.

In June 2024, ALK announced that the Board of Directors has adopted a new corporate strategy (Allergy+) and 2028 financial ambitions. Allergy+ aims to further strengthen ALK's leadership in allergy immunotherapy, establishing a leading position in food allergy and anaphylaxis, as well as pursuing new innovations to address adjacent allergic conditions with high unmet needs. The strategy targets average revenue growth of minimum 10% in local currencies (5-year CAGR) until 2028.

Average revenue growth of minimum 10% in local currencies (5-year CAGR) until 2028. An EBIT margin of approximately 25% in 2025 after which ALK will aim for annual profitability improvements in line with revenue growth implying a projected EBIT margin of around 25% until 2028.

The 2024 results validated the strategy's execution. Revenue increased by 15% to DKK 5,537 million (4,824) on growth in all product lines. Tablet sales increased by 24% to DKK 2,851 million (2,296) on growth in all sales regions. European tablet sales sustained momentum with 31% growth, driven by higher volumes and improved pricing.

The profitability improvement was equally striking. EBIT was DKK 1,091 million (666) on higher sales, gross margin improvements, and modest cost increases. The margin was 20% (14).

The year 2024 was a milestone for ALK, achieving record revenue with a 15% increase, largely driven by European tablet sales. The company's earnings improved by 65% in local currencies, and the EBIT result surpassed DKK 1 billion for the first time, setting a new benchmark for the company.

ALK's CEO Peter Halling says: "2024 was a remarkable year in which we delivered considerably better results than we originally anticipated. We established a new strategic framework for ALK's long-term development and are expanding our addressable markets in respiratory allergy by adding new patient groups – especially children – and new markets. Efforts are also well underway to build new revenue streams in anaphylaxis, food allergies, and other allergic conditions with high unmet needs."

For 2025, management guidance reflects continued momentum. Revenue is expected to grow by 9-13% primarily on volume-driven growth across sales regions and product groups. Tablets remain key to growth. The EBIT margin is expected to improve by 5 percentage points to around 25%.

The neffy® Licensing Deal

In November 2024, ALK made its largest strategic move in years. ALK entered into a strategic license agreement with US-based ARS Pharmaceuticals, Inc. The agreement grants ALK exclusive global rights to the neffy® adrenaline (epinephrine) nasal spray, with exception of the USA, Australia, New Zealand, Japan and China.

Needle-free, nasal delivery of adrenaline has the potential to become an important treatment option in anaphylaxis. For patients at risk of severe allergic reactions—from food allergies, insect stings, or other triggers—the current standard of care requires injecting epinephrine via auto-injector devices like EpiPen. Many patients are needle-averse or hesitate during emergencies.

Under the agreement, ARS Pharma is entitled to receive an upfront payment of USD 145 million (DKK 1 billion) from ALK. Furthermore, ARS Pharma may receive up to USD 320 million (DKK 2.2 billion) related to regulatory and commercial milestones, potentially over the next 15+ years as well as tiered royalties in the teens on future sales.

ALK estimates that neffy® holds a long-term annual peak sales potential in anaphylaxis of up to DKK 3 billion in the licensed territories.

The strategic logic is compelling. ALK already sells Jext®, its adrenaline auto-injector, and has established relationships with allergists who manage patients at risk of anaphylaxis. Adding neffy creates a portfolio approach: patients can choose between needle-based and needle-free options based on their preferences and circumstances. The deal expands ALK's addressable market beyond chronic allergy treatment into emergency medicine.

In May 2025, ALK announced a 4-year agreement with US-based ARS Pharmaceuticals to co-promote the neffy® adrenaline (epinephrine) nasal spray to up to 9,000 named paediatricians in the USA. These paediatricians currently account for close to 10% of all adrenaline auto-injector prescriptions in the USA. The agreement is expected to give ALK improved access to US paediatricians, providing attractive synergies to ALK's existing product portfolio.

Paediatric Expansion: Completing the Portfolio

The recent approval of ITULAZAX for pediatric use marks a decade-long development effort's completion. ALK's European regulatory filing for ITULAZAX® (tree pollen sublingual allergy immunotherapy tablet) for treatment of young children and adolescents aged five to 17 has been approved by the health authorities in 17 EU countries via a type II variation procedure. First market introductions are expected to follow in the coming months ahead of the 2025/2026 initiation season.

The approval of ITULAZAX® for paediatric use marks the completion of ALK's decade-long development efforts, ensuring that five of the most common respiratory allergies (grass pollen, house dust mite, ragweed pollen, Japanese cedar pollen, and now tree pollen) are all covered by allergy immunotherapy tablets approved for children, adolescents, and adults in relevant markets.

This is strategically crucial. Children represent the population most likely to benefit from early intervention—treating allergies before they progress to asthma, before the disease burden compounds over decades. The pediatric approvals essentially complete ALK's addressable market expansion in respiratory allergies.

IX. Product Portfolio Deep Dive

Understanding ALK requires understanding its products. Allergy immunotherapy products account for 88% of ALK's revenues and comprise three types of product: Sublingual immunotherapy tablets (SLIT-tablets) covering grass pollen, ragweed pollen and house dust mite allergies. Sublingual immunotherapy drops (SLIT-drops)—a droplet-based allergy vaccine marketed under various brand names and covering approximately 40 different allergens and combinations of allergens, including pollens, molds, mites and pets.

The product lineup includes:

GRAZAX/GRASTEK (grass pollen): The original breakthrough tablet, approved in Europe in 2006 and the U.S. in 2014. Treats grass pollen-induced allergic rhinitis, one of the most common seasonal allergies globally.

RAGWITEK/RAGWIZAX (ragweed): Particularly important in North America, where ragweed causes severe seasonal allergies. Approved in the U.S. in 2014.

ACARIZAX/ODACTRA (house dust mite): Year-round treatment for dust mite allergies, approved in Europe in 2015 and the U.S. in 2017. Particularly significant because dust mite allergy persists throughout the year.

ITULAZAX/ITULATEK (tree pollen): Treats allergies to birch and related tree pollens, approved in Europe in 2019 and now expanded to pediatric populations.

CEDARCURE/MITICURE (Japanese cedar/house dust mite in Japan): Developed specifically for the Japanese market through the Torii partnership.

Jext®: ALK's adrenaline auto-injector for emergency treatment of anaphylaxis. While not an immunotherapy product, it serves the same allergist customer base and addresses acute allergic emergencies.

neffy®: The newly licensed epinephrine nasal spray for anaphylaxis, expected to launch in European markets in 2025.

Emerging Pipeline: Food Allergies

ALK is developing a peanut allergy SLIT-tablet using the same technology platform as its respiratory tablets. In December 2024, ALK announced positive interim results from its phase I/II clinical trial (ALLIANCE) for its investigational peanut SLIT tablet. This part of the trial, which involved approximately 30 patients, investigated safety and tolerability of multiple doses. For all dose levels, the tablet was shown to be safe and tolerable.

The phase II part is expected to involve approximately 125 patients (aged four to 65) in the USA and Canada and is scheduled to complete in 2026. Provided a successful phase II outcome, ALK intends to advance the peanut SLIT-tablet into phase III development after which it can be submitted for regulatory approval, expectedly towards the late 2020s.

In the USA, peanut allergy affects up to 1.5 million children and adolescents aged 4-17, while in Europe, around 1 million children and adolescents are affected by this potentially life-threatening condition. The disease often presents in early childhood, and can last a lifetime.

The food allergy market represents a substantial expansion opportunity. In food allergy, ALK's objective is to build a portfolio of treatments that addresses the unmet medical need among the approximately 200 million people worldwide affected, particularly among children. This portfolio will be spearheaded by the peanut SLIT tablet, currently in clinical Phase I/II development.

X. Business Model & Competitive Moats

ALK's business model is centred around strong R&D skills, insight into immunology and unique manufacturing processes: as AIT treatments are classified as biologics because they are produced from living cells rather than being synthesised by chemists, intricate manufacturing processes present significant barriers to entry and ensure a sustained market exclusivity.

This biologics classification is crucial. Unlike small-molecule drugs that can be synthesized chemically, allergen extracts are derived from natural sources—pollens, dust mites, animal dander. The complexity of sourcing, processing, and standardizing these biological materials creates barriers that go far beyond patent protection.

ALK invests annually approximately 20% of revenue in research that aims to develop new, evidence-based allergy immunotherapy. This R&D intensity—remarkably consistent over decades—has built a compounding knowledge advantage in allergen characterization, extraction, and standardization.

Manufacturing Complexity: European production facilities in Hørsholm, Denmark, in Vanduille and Varennes, France, and in Madrid, Spain. North American production facilities in Port Washington, New York, in Post Falls, Idaho, in Luther, Iowa, and in Oklahoma City, Oklahoma. This global manufacturing footprint represents decades of investment and regulatory approval.

Geographic Revenue Mix: 67% of its revenue comes from sales in Europe. Europe remains ALK's stronghold, with North America and International markets (including Japan and emerging markets) representing growth opportunities.

XI. Porter's Five Forces & Hamilton's 7 Powers Analysis

Porter's Five Forces

1. Threat of New Entrants: LOW

The barriers to entering allergy immunotherapy are formidable. AIT treatments are classified as biologics because they are produced from living cells rather than being synthesised by chemists, intricate manufacturing processes present significant barriers to entry.

New entrants would need to: - Build decade-long clinical trial databases demonstrating safety and efficacy - Master allergen sourcing, extraction, and standardization - Navigate complex FDA/EMA approval pathways for biologics - Establish relationships with thousands of allergists globally - Develop manufacturing capabilities for biological products

The regulatory and scientific barriers effectively protect established players. Even well-capitalized pharmaceutical companies have struggled—as Merck's exit demonstrates.

2. Bargaining Power of Suppliers: MODERATE

Natural allergen sources (pollens, dust mites) require specialized cultivation and sourcing. ALK has vertically integrated much of its supply chain through decades of investment, reducing supplier power. The company's proprietary standardization processes add another layer of control over input quality.

3. Bargaining Power of Buyers: MODERATE

Physicians (allergists) are key decision-makers with limited alternatives. Most allergists work with just one or two immunotherapy providers due to training, familiarity, and formulary constraints. However, healthcare systems and payers increasingly exert pressure on pricing and reimbursement, particularly in Europe.

Patient adherence challenges with multi-year treatment protocols create some leverage—if patients drop out, neither the company nor the physician benefits.

4. Threat of Substitutes: MODERATE-HIGH

Symptomatic treatments (antihistamines, corticosteroids, nasal sprays) remain the first-line option for most allergy sufferers. These are cheaper, require no prescription in many cases, and provide immediate relief. However, they only mask symptoms rather than treating root cause—creating an ongoing treatment burden rather than potential remission.

Biologics like omalizumab (Xolair) represent emerging alternatives for severe cases, particularly allergic asthma. These high-cost injectables target different patient populations but could compete for some severe allergy patients.

5. Industry Rivalry: MODERATE

Leading players in Allergy Immunotherapy Market are Stallergenes Greer, ALK-Abello A/S, Allergy Therapeutics, Allergopharma, HAL Allergy Group.

ALK-Abelló's closest competitor is Stallergenes Greer, a Swiss firm that has about one-third the annual sales of its Danish peer. It's privately held. The UK's Allergy Therapeutics is publicly listed, but it has annual sales of just a sixth of what ALK-Abelló achieves.

In 2022, Stallergenes recorded €360 million in sales, roughly 60% of ALK's revenues in that year.

The market has consolidated over time. Stallergenes Greer announced in February 2023 that it had completed the acquisition of Allergy Therapeutics. This acquisition is expected to strengthen Stallergenes Greer's position in the global allergy immunotherapy market.

Hamilton's 7 Powers Analysis

1. Scale Economies: STRONG

ALK's global manufacturing network provides significant fixed-cost leverage. R&D investments amortized across larger revenue base than competitors. Clinical trial costs for new indications (pediatrics, new allergens) can be spread across global markets.

2. Network Effects: WEAK

Limited network effects in pharmaceutical business. Some benefit from physician education and referral patterns—once an allergist is trained on ALK products, they tend to stay loyal—but this isn't a true network effect.

3. Counter-Positioning: STRONG

This is perhaps ALK's most underappreciated advantage. Big Pharma walked away (Merck exit) because AIT market growth didn't meet their return thresholds. ALK's focused strategy wouldn't make sense for diversified pharma giants managing billion-dollar franchises. The allergy immunotherapy market is "too small to matter" for companies like Pfizer or Merck, but represents a sustainable growth runway for a focused specialist.

4. Switching Costs: MODERATE

Patients on multi-year treatment protocols face high switching costs—they've invested months or years in building tolerance. Physicians trained on specific products tend to stay loyal due to familiarity with dosing protocols and patient management.

5. Branding: MODERATE

Strong reputation among allergists globally. Trust built over 100 years of specialization. However, this is B2B2C branding—the allergist makes the recommendation, and patients typically follow. Consumer awareness of ALK is minimal.

6. Cornered Resource: STRONG

ALK's century of accumulated expertise in allergen characterization, extraction, and standardization represents a cornered resource that competitors cannot replicate quickly. The clinical database from landmark studies like PAT provides unique evidence supporting disease-modification claims. Proprietary manufacturing processes and standardization methods developed over decades.

7. Process Power: STRONG

In 1978, ALK released the first standardized line of products for the treatment of allergies. The standardized allergen extraction processes developed over decades represent embedded organizational capabilities that competitors cannot easily replicate. Manufacturing know-how for biologics from natural sources requires years of refinement.

XII. Competitive Landscape & Market Dynamics

The global allergy immunotherapy market size is expected to be worth around US$ 4.4 billion by 2034 from US$ 1.9 billion in 2024, growing at a CAGR of 8.8% during the forecast period 2025 to 2034.

The market is expanding steadily, but the real story is the penetration gap. According to Stallergenes, approximately 30% of the world population is affected by one or more allergic conditions and it is expected that by 2050 several billion people will suffer from allergies. Allergic rhinitis affects approximately 10% to 30% of adults and 40% of children. But only 12% of them are treated with allergen immunotherapy products due to low awareness among physicians and patients, a complex treatment pathway and a market that is dominated by lower cost symptomatic treatments.

This penetration gap is both the bull case and the question mark for ALK. If even a modest share of the 500 million people with respiratory allergies shifted from symptomatic treatment to disease-modifying immunotherapy, market size could expand dramatically. But this shift has been slow—raising questions about whether it will ever accelerate meaningfully.

In 2024, Europe led the allergy immunotherapy market share of 68%, with subcutaneous immunotherapy dominating treatment types. Europe's dominance reflects both ALK's historical strength and more favorable reimbursement structures for immunotherapy.

Regionally, North America maintained its dominant position in 2024, securing a 39.5% share of the global market, attributed to advanced healthcare systems, high awareness levels, and favorable reimbursement frameworks for allergy treatments. Note: There's some variation in market share data depending on how "allergy treatment" vs. "allergy immunotherapy" is defined.

The broader allergy treatment market (including antihistamines, corticosteroids, and biologics) is substantially larger—The Allergy Treatment Market is expected to reach USD 22.76 billion in 2025 and grow at a CAGR of 8.10% to reach USD 33.59 billion by 2030.

XIII. Leadership & Governance

In June 2023, ALK announced that Carsten Hellmann would step down as President & CEO at the end of 2023. He was succeeded by Peter Halling no later than 1 January 2024.

Peter Halling is currently CEO of Fertin Pharma, a leading specialist contract development and manufacturing organisation in innovative oral and intra-oral delivery technologies, which he, together with private-equity firm EQT, led through a successful sale in 2021. Before joining Fertin Pharma in 2020, he held several international executive roles at Novozymes A/S, Ingredion Inc. and Doehler Group GmbH.

Peter Halling has a successful track record of driving cultural and digital transformation and growing, transforming and managing global companies, business units and partnerships. Peter Halling is a Danish citizen, born in 1977.

Hellmann, 59, was replaced by the comparatively youthful 45-year-old Peter Halling at the end of the year, which ALK Board Chairman Anders Hedegaard said would help future-proof the company. Halling is currently the CEO of Fertin Pharma, the global market leader in medicated chewing gum, and a veteran of Novozymes, Ingredion, and Doehler Group. Speaking to MedWatch about what Halling can bring to the position, Hedegaard said, "Being in my over-sixties, I'll allow myself to say that Peter is a young and dynamic 45-year-old. He's always been very successful in his past jobs, and has the right integrity as a person. He's a winner."

The leadership transition was significant. The mandate of the new CEO, Peter Halling, officially appointed on 1 January 2024, is to grow as fast as possible while improving operating margins and cash flows.

Under Halling's leadership, ALK launched the Allergy+ strategy and delivered record financial results in 2024. The early returns suggest the transition has been successful, though the strategic direction largely continues the path established under Hellmann—with added emphasis on adjacent markets like anaphylaxis and food allergy.

XIV. Bull & Bear Case Analysis

The Bull Case

Market Penetration Opportunity: The fundamental bull case rests on the penetration gap. Only ~1% of the 500 million people with respiratory allergies currently use immunotherapy. If awareness increases, tablet convenience drives adoption, and healthcare systems recognize the cost-effectiveness of disease-modification versus decades of symptomatic treatment, market size could expand dramatically. ALK is positioned to capture disproportionate share of any market expansion.

Complete Portfolio Coverage: With pediatric approvals now covering all major respiratory allergens, ALK has removed a significant barrier to physician adoption. Parents increasingly seek disease-modifying treatment for children before allergies progress to asthma—exactly the demographic that ALK can now fully serve.

Adjacent Market Expansion: The neffy licensing deal and peanut allergy development represent optionality beyond the core respiratory allergy business. Anaphylaxis emergency treatment and food allergies are high-unmet-need markets with clear commercial synergies to ALK's existing allergist relationships.

Foundation Ownership Advantage: The Lundbeck Foundation's controlling stake enables patient capital allocation and strategic decisions measured in decades. This governance structure is particularly valuable in a market requiring sustained investment through slow adoption curves.

Financial Momentum: Record 2024 results with 15% revenue growth and 65% earnings improvement demonstrate operational leverage. The path to 25% EBIT margins is credible based on current trajectory.

The Bear Case

Structural Adoption Barriers: The 1% penetration rate has persisted for decades despite ALK's innovations. Symptomatic treatments are cheaper, more convenient (no multi-year commitment), and immediately effective. Many patients and physicians may simply prefer managing symptoms over pursuing disease modification. If this dynamic doesn't change, market growth will remain modest.

Competition Intensifying: Stallergenes Greer's acquisition of Allergy Therapeutics creates a larger, better-capitalized competitor. Big pharma biologics (omalizumab and newer anti-IgE therapies) represent emerging competition for severe allergy patients.

North American Execution Risk: Despite years of investment, ALK's U.S. market penetration remains challenging. American allergist practice economics often favor in-office injections (SCIT) over take-home tablets. If U.S. growth disappoints, a key pillar of the bull case weakens.

China and Emerging Markets Uncertainty: Despite overall strong performance, ALK faced stagnation in North America with unchanged revenue, and only a modest 4% increase in international markets. The renewal of ALK's import license in China posed significant challenges, impacting revenue in that region. China proved to be a challenging market for ALK, with revenue from SCIT products declining significantly due to no shipments being made during the import license renewal process. Regulatory and market access challenges in emerging markets could limit geographic expansion.

Pipeline Execution Risk: Food allergy development is early-stage. The peanut tablet won't reach market until late 2020s at earliest. If clinical trials disappoint, a key growth driver evaporates.

Valuation: The stock trades at approximately 45x TTM earnings with a market cap of DKK 41+ billion. This valuation implies significant expectations for sustained growth and margin expansion. If market penetration doesn't accelerate, multiple compression could offset earnings growth.

XV. Key Performance Indicators for Monitoring

For investors following ALK-Abelló, three KPIs deserve particular attention:

1. European Tablet Sales Growth Rate — This metric captures the core business momentum. European tablet sales have been the primary growth driver, with 31% growth in 2024. Sustained double-digit growth would confirm the market penetration thesis; deceleration below high-single-digits would raise concerns about structural adoption ceilings.

2. EBIT Margin Trajectory — The path from 20% (2024) toward management's 25% target reflects operating leverage. Margin improvement demonstrates that investments in commercial infrastructure and R&D are generating returns. Any margin pressure would signal execution challenges or market headwinds.

3. U.S. Tablet Sales/Revenue — North America represents both ALK's largest market opportunity and greatest execution challenge. Progress in U.S. tablet adoption would validate the decision to go it alone after Merck's departure. Stagnation would confirm structural barriers to American market penetration.

XVI. Material Risks & Considerations

Regulatory Complexity: Allergen products face complex regulatory pathways across jurisdictions. The FDA's CBER (Center for Biologics) oversight means longer review timelines and more stringent requirements than typical pharmaceuticals. European regulations continue evolving. Regulatory delays or unexpected requirements could slow market access.

Reimbursement Pressure: Healthcare systems increasingly scrutinize specialty pharmaceutical pricing. While immunotherapy may offer long-term cost savings versus decades of symptomatic treatment, demonstrating this value to payers requires substantial real-world evidence.

Manufacturing Disruption: As biological products derived from natural sources, ALK's products face supply chain vulnerabilities that synthetic drugs don't encounter. Climate change could affect pollen sources; quality issues at manufacturing facilities could disrupt supply.

Single-Category Concentration: Unlike diversified pharmaceutical companies, ALK's entire business depends on allergy. A breakthrough alternative treatment (gene therapy, novel biologics) could disrupt the market. This concentration creates both operational leverage and strategic vulnerability.

Currency Exposure: With 67% of revenue from Europe but substantial costs in Danish kroner and other currencies, ALK faces meaningful FX exposure. Currency fluctuations can impact reported results and cross-border competitive positioning.

XVII. Conclusion: The Patience Premium

ALK-Abelló represents something increasingly rare in modern markets: a century-old company that has maintained focus on a single therapeutic area, building compounding advantages in scientific knowledge, manufacturing capability, and physician relationships that would be nearly impossible to replicate.

The company's journey illustrates several enduring business principles:

Niche Specialization Creates Defensibility: ALK's 100-year focus on allergy has generated expertise that broad pharmaceutical companies cannot match. When Merck walked away, it wasn't because the market lacked potential—it was because a $2 billion market couldn't move the needle for a $200 billion company. For ALK, that same market represents its entire reason for being.

Foundation Ownership Enables Strategic Patience: The Lundbeck Foundation's controlling stake has allowed ALK to make decisions with decade-long time horizons. The strategic repositioning after Merck's departure required accepting near-term financial pressure for long-term independence. Few publicly-traded companies could execute such a reset without shareholder revolt.

Counter-Positioning Against Giants: ALK's very DNA—deep specialization, patient-focused innovation, multi-decade clinical development—makes it unattractive for big pharma to compete directly. This "too small to matter" dynamic for large pharmaceutical companies is precisely why the market remains attractive for focused specialists.

Science Compounds Over Time: The standardization breakthroughs of the 1970s, the SLIT innovation of the 1990s, and the tablet development of the 2000s each built on prior knowledge. This compounding expertise creates barriers that competitors measuring time horizons in quarters simply cannot overcome.

The central question remains: will the penetration rate finally inflect upward? If millions more allergy sufferers shift from symptom management to disease modification, ALK sits at the center of a market expansion that could exceed current expectations. If adoption remains stubbornly low, the company remains a solid, growing business—but not the transformation story the bull case implies.

What seems clear is that ALK-Abelló has built a business designed to compound value over decades rather than quarters. The Lundbeck Foundation's patient capital, century-accumulated expertise, and complete portfolio of disease-modifying therapies create a foundation that should prove resilient through market cycles.

For long-term investors willing to accept the pace of healthcare market development, ALK-Abelló offers exposure to an underappreciated secular trend—the shift toward disease-modifying therapies that address root causes rather than masking symptoms. Whether that shift accelerates in the coming decade remains the key variable that will determine whether ALK is a hidden champion finally ready for recognition or a perpetual "tomorrow story" that never quite arrives.

In the allergy immunotherapy market, as in allergy treatment itself, the theme is patience: patient capital, patient physicians, and patients willing to commit to multi-year treatment protocols for the promise of lasting relief. ALK-Abelló has built a business that rewards precisely that virtue.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube