Carl Zeiss Meditec: The Precision Empire of the Eye

How a 19th-Century German Optics Workshop Became the World's Most Dominant Force in Eye Surgery Technology

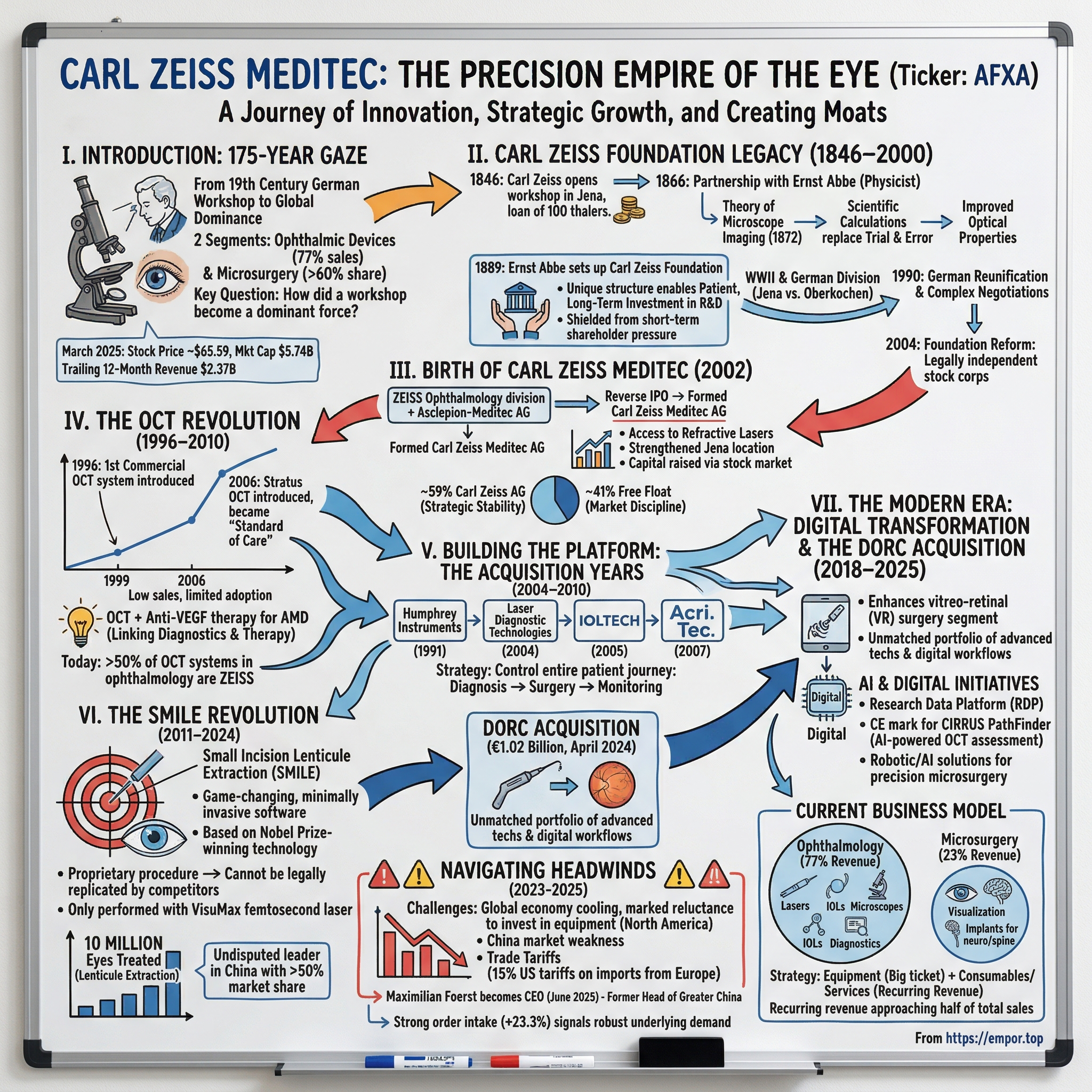

I. Introduction: The 175-Year Gaze

In a gleaming surgical suite somewhere in Shanghai, a patient lies still as a femtosecond laser—firing pulses timed to the quintillionth of a second—carves a microscopic disc within her cornea. In less than ten seconds, the procedure is complete. No blade, no flap, no pain. The technology enabling this moment traces its roots not to Silicon Valley or a modern biotech campus, but to a cramped workshop in Jena, Germany, where in 1846 a 30-year-old optician named Carl Zeiss began grinding lenses by hand.

Carl Zeiss Meditec is one of the largest medical technology companies in the world, operating in two segments: ophthalmic devices and microsurgery. The Ophthalmic Devices segment made up roughly 77% of sales, including refractive lasers, surgical ophthalmic devices, equipment for ophthalmic diagnostics, as well as a portfolio of intraocular lenses and disposable medical instruments. With a low-teens share of the overall ophthalmology market, Zeiss is the second-largest player in the space. The Microsurgery segment is composed of implants, surgical instruments, and visualization devices used during neurosurgery, spine surgery, and otolaryngology surgery. With over 60% market share, Zeiss is the clear leader in the microsurgery space.

The core question animating this story is deceptively simple: How did a 19th-century German optics workshop, born when microscopes were still built by trial and error, evolve into the dominant force in eye surgery technology—a company whose proprietary laser procedure, SMILE, cannot legally be replicated by any competitor on Earth?

As of March 2025, Carl Zeiss Meditec's stock price stood at approximately $65.59, with a market capitalization of $5.74 billion and 87.5 million shares outstanding. Trailing 12-month revenue reached $2.37 billion.

The answer lies in three threads woven through nearly two centuries of innovation: a unique foundation structure that enabled patient, long-term investment in science; a series of strategic acquisitions that built an integrated diagnostic-and-treatment ecosystem; and the development of proprietary technologies—most notably OCT imaging and SMILE laser correction—that created insurmountable moats around core business segments.

II. The Carl Zeiss Foundation Legacy (1846–2000): A Social Experiment Becomes an Innovation Engine

The story begins not with venture capital or IPO roadshows, but with a loan of 100 thalers—roughly the cost of a decent horse—from Eduard Zeiss to his younger brother Carl. With that starting capital, Carl began the official operation of his "Werkstätte für Feinmechanik und Optik" on November 17, 1846, in Jena. A historic date. Zeiss first worked without any employees, constructing, repairing and optimizing different instruments by himself.

Carl Zeiss opened an optics workshop in Jena in 1846. By 1847, he was making microscopes full-time. But what distinguished Zeiss from the many craftsmen grinding lenses across Europe was his refusal to accept the status quo. Zeiss was not satisfied and continued to further improve his microscope technology over the years. In particular, the "trial and error" production methods common at the time struck him as outdated. Confronted with an inefficient system of trial and error, Zeiss ignored standard practice and developed the idea of using calculations to produce his microscope lenses. Thus the precision engineer ultimately chose one particular employee to make his conception of an ideal production process a reality in 1866. From this time on, he worked on his great goal with the physicist Ernst Abbe: to develop a microscope which would exceed the optical properties of all his competitors' devices. Zeiss was 50, Abbe had just turned 26.

The partnership between Zeiss the craftsman and Abbe the physicist proved transformative. Already as a young scientist, Abbe placed his knowledge at the disposal of Carl Zeiss. He was hired as a scientist in 1866. From 1870, Abbe was a professor at the University of Jena. His theory of microscope imaging made him the founder of scientific optics and gave Carl Zeiss an important technological boost: While microscopes had previously been built only by using the trial-and-error method, from 1872 on they were designed on the foundation of sound scientific calculations, thereby exhibiting vastly improved optical properties. This in turn allowed for pioneering research in biology and medicine, such as that by Robert Koch and Paul Ehrlich.

The scientific revolution Abbe enabled was matched by his social vision. Abbe was concerned that future owners of Zeiss and Schott would be tempted to enrich themselves at the companies' and employees' expense, so in 1889 he set up and endowed the Carl Zeiss Foundation to run the two companies. The foundation became the sole owner of Zeiss and of Abbe's share of Schott in 1891. (Schott transferred his shares to the foundation after his death in 1935.) Abbe published in 1896 the foundation statute, which reorganized the two companies, with management, workmen, and the University of Jena sharing in the profits. The statute instituted many reforms that later became commonplace in Germany such as overtime and sick pay, disability assistance, a minimum wage, and at Zeiss a nine-hour day (which was shortened to eight hours in 1900).

This foundation structure, established in 1889 and still governing the company today, represents perhaps the most consequential decision in Zeiss's 175-year history. The Carl Zeiss Foundation was founded in 1889 by the physicist and entrepreneur Ernst Abbe in Jena, Germany, with the support of Otto Schott, founder of SCHOTT. The Carl Zeiss Foundation is the owner of Carl Zeiss AG and SCHOTT AG. Its overarching aim is to ensure responsible management of the foundation companies.

Why does ownership structure matter for investors evaluating Zeiss today? Because it explains the company's ability to maintain consistently high R&D spending through economic cycles—a commitment that most publicly traded competitors struggle to match. With the founding of the Carl-Zeiss-Stiftung, Ernst Abbe pursued two overarching goals, which still determine the funding purpose in the Foundation Statute to this day. On the one hand, he was concerned with the long-term securing of the foundation companies and the well-being of his employees, which in his opinion could only be guaranteed by depersonalization of the owners.

The 20th century tested this structure severely. World War II and the subsequent division of Germany split Zeiss in two—Jena was initially occupied by American forces who took the leading employees to the American Zone before Thuringia was handed over to the Soviet Union. These employees established a new company in Oberkochen, which later also carries the name Carl Zeiss.

For four decades, two companies bearing the Zeiss name competed head-to-head across the Iron Curtain. The company in Jena was nationalized in 1948. In 1965 it was reshaped to form the leading combine in the optics industry, and in 1989 it employed over 70,000 people. German reunification in 1990 required complex negotiations to reunite the competing entities, culminating in a 2004 foundation reform. As part of a comprehensive foundation reform, the companies ZEISS and SCHOTT were converted into legally independent stock corporations with the Carl Zeiss Foundation as the sole shareholder in 2004.

Through it all, the foundation's fundamental promise held: profits would be reinvested into science, employees would be protected, and short-term shareholder pressure would never dictate strategy. That legacy directly enabled the patient, decade-long investments in OCT imaging and SMILE laser technology that would later define Carl Zeiss Meditec's competitive moats.

III. The Birth of Carl Zeiss Meditec (2002): The Reverse IPO That Built an Empire

By the 1990s, Zeiss leadership saw the future with unusual clarity. Fast forward to the 1990s when Carl Zeiss looked ahead to an increasingly aging world population and made the strategic decision to place a higher priority on developing and expanding its eyecare business. The acquisition of Humphrey Instruments in 1991 was followed by a combination with Ascepion-Meditec in 2002, leading directly to the formation of Carl Zeiss Meditec AG and its spin-off from Carl Zeiss as an independent, publicly traded company in that same year. In Carl Zeiss Meditec, a forward-looking management brought together the optical leadership of Zeiss, the perimetry leadership of Humphrey and the laser expertise of Ascepion-Meditec in a single entity. The company had the ability to provide a wide range of eyecare capabilities in diagnosis, treatment and follow-up.

In 2002, Carl Zeiss Meditec AG, as it is known today, was created from the merger of the ZEISS Ophthalmology division with Asclepion-Meditec AG, a medical lasers specialist. On 22 July 2002, the Carl Zeiss Meditec AG shares were traded on the Neuer Markt for the first time, making it publicly traded.

This was no ordinary IPO. The formation of this company as a reverse IPO (the acquisition of a company already listed on the stock exchange) solved several problems at once: It gave Carl Zeiss access to business with refractive lasers (hitherto the sole domain of Asclepion), strengthened the Jena location, enabled extra capital to be raised on the stock market, and placed all the medical technology activities dispersed among the various sites under one umbrella. The process was completed with the reform of the Carl Zeiss Foundation in 2004 and the new opportunity for Carl Zeiss Meditec AG to acquire the Oberkochen OPMI business. However, this was just the beginning of implementing the actual strategy of complete diagnostic and treatment solutions. Through the acquisition of IOLTECH (2005) and Acri. Tec (2007), Carl Zeiss Meditec AG expanded its portfolio, offering products such as intraocular lenses and consumables for eye surgery.

The ownership structure that emerged from this transaction remains in place today. Around 41 percent of Carl Zeiss Meditec AG's shares are in free float. The remaining approx. 59 percent are held by Carl Zeiss AG, one of the world's leading groups in the optical and optoelectronic industries.

For investors, this parent-subsidiary relationship carries critical implications. The foundation's 59% stake provides strategic stability and shields management from activist pressure, while the 41% free float ensures market discipline and capital access. This hybrid structure enables long-term R&D investment while maintaining public-market accountability—a balance few medical technology companies achieve.

IV. The OCT Revolution: Creating the Standard of Care (1996–2010)

In ophthalmology circles, certain technologies achieve the status of "standard of care"—procedures so essential that no competent practitioner can operate without them. Optical coherence tomography (OCT) represents the most dramatic example in modern eye care, and Zeiss played the central role in its commercialization.

Optical coherence tomography was first introduced commercially by Carl Zeiss in 1996. The first commercially available OCT was based on time-domain technology.

The technology's origins trace to academic research at MIT. Optical coherence tomography was developed by researchers at the Massachusetts Institute of Technology and collaborators and was first reported in Science in 1991. Because ocular media are transparent, the retina provided an ideal tissue for OCT imaging. The first in vivo studies of the human retina were published in 1993, and these were soon followed by clinical studies. Although OCT was originally commercialized through a startup company, Advanced Ophthalmic Devices, in 1994 the technology was transferred to Humphrey Instruments, a subsidiary of Carl Zeiss.

In collaboration with MIT's leading researchers, clinical scientists and engineering experts, ZEISS played a key role in bringing this groundbreaking technology to eye care by building the first commercially available OCT device in 1996.

But commercialization was neither immediate nor inevitable. By 1996, just 2 years after acquiring AOD, Zeiss released its first regulatory cleared commercial OCT unit. Although the first OCT instruments became commercially available in 1996, clinical adoption was slow and in 1999 only a total of ~180 units were sold. Humphrey (Zeiss) introduced the first OCT instrument in 1996. Optical coherence tomography 2 was introduced in 2000, but limited sales almost caused OCT to be abandoned. After the introduction of the Stratus OCT in 2006, OCT became a standard of care in ophthalmology. The volume of published clinical data, coupled with technological improvements and reimbursement helped drive the clinical adoption of OCT.

What saved OCT from abandonment? A convergence of clinical need and pharmaceutical innovation. A powerful factor in OCT adoption was the development of anti-VEGF therapy for exudative AMD. Anti-VEGF therapy revolutionized the treatment of AMD, but patients had varying responses and OCT became important for identifying markers of treatment response. The concept of linking diagnostics and therapy remains a key point in business development to this day.

Today, Zeiss's persistence has paid extraordinary dividends. In 1996, ZEISS introduced the first OCT system in eye care and since then OCT has become the standard of care in eye clinics. Today, more than half of all Optical Coherence Tomography Systems in ophthalmological practices are ZEISS OCTs.

The OCT story illustrates a pattern that would repeat throughout Zeiss's history: patient investment in promising but unproven technology, followed by relentless iteration until market adoption reached critical mass. For investors, this suggests that Zeiss's current R&D investments—particularly in AI-powered diagnostics—may follow similar multi-year adoption curves.

V. Building the Platform: The Acquisition Years (2004–2010)

With the foundation reform complete in 2004, Carl Zeiss Meditec embarked on an acquisition strategy designed to transform the company from a diagnostics specialist into a comprehensive eye care platform.

In the past 2 years, Carl Zeiss Meditec has further broadened its portfolio by acquiring IOLTech, a French-based company best known for its IOLs and associated cataract surgery and refractive products, and Laser Diagnostic Technologies, a pioneer in glaucoma detection with its GDx technology and Variable Cornea Compensation (VCC) enhancement, which measures changes in the tissue characteristics of the retinal nerve fiber layer. Along with these acquisitions, CZM has continued to develop new and improved products internally, allocating approximately 10% of overall revenues to R&D. This impressive commitment to R&D has resulted in the recent launch of the Visante OCT, which expands the company's expertise in optical coherence tomography to anterior segment applications, and the Visucam Pro NM non-mydriatic fundus camera.

The strategic logic was straightforward but ambitious: Zeiss sought to control the entire patient journey, from initial diagnosis through surgical intervention to post-operative monitoring. Each acquisition filled a specific gap:

- Humphrey Instruments (1991): Perimetry and visual field testing

- IOLTECH (2005): Intraocular lenses and cataract consumables

- Laser Diagnostic Technologies (2004): Glaucoma detection technology

- Acri. Tec (2007): Advanced IOL designs and surgical consumables

This portfolio approach created powerful cross-selling opportunities. An ophthalmologist who purchased Zeiss diagnostic equipment would naturally consider Zeiss surgical systems, creating an integrated workflow that competitors struggled to match.

The strategy proved remarkably resilient during the 2008-2009 financial crisis. While capital equipment purchases slowed across healthcare, Zeiss's growing consumables business provided revenue stability—a pattern that would intensify in subsequent years as recurring revenue became central to company strategy.

VI. The SMILE Revolution: Creating a Proprietary Technology Moat (2011–2024)

If OCT represented Zeiss's first major technology platform, SMILE (Small Incision Lenticule Extraction) represented something more audacious: a proprietary surgical procedure that competitors could not legally perform.

SMILE from ZEISS enables the first Small Incision Lenticule Extraction procedure for minimally invasive laser vision correction. It offers a potentially lower incidence of transient dry eye syndrome and a wider preservation of biomechanical stability. ZEISS SMILE is a game-changing software for laser vision correction that goes beyond PRK and LASIK and redefines refractive surgery. It is exclusively performed with the VisuMax femtosecond laser from ZEISS. Based on Nobel Prize-winning technology (Nobel Prize in Physics 2018).

The technology's connection to Nobel Prize-winning research deserves emphasis. In granting the award, the Royal Swedish Academy of Sciences noted Dr. Mourou and Strickland developed laser chirped pulse amplification, a technology which allowed laser energy to be compressed into incredibly short time intervals, increasing the intensity of the laser in each ultra short pulse. The Academy emphasized this laser technology's "benefit to humankind." In particular, ultra short pulse laser technology led to the development of femtosecond lasers. Femtosecond lasers are used in LASIK to create the LASIK flap and also are used in a different corneal refractive laser eye surgery technique known as "SMILE". Femtosecond lasers are now also being used in cataract surgery as well.

The commercial trajectory of SMILE demonstrates Zeiss's patient capital deployment. The procedure launched internationally in 2011, but FDA approval for the U.S. market—the world's largest refractive surgery market—came only in 2016, followed by expanded indications over subsequent years.

In October 2018, Carl Zeiss Meditec won FDA premarket approval for its ReLEx Smile laser system. Also in October 2018, Carl Zeiss Meditec announced the acquisition of Reno, Nevada-based IanTech for an undisclosed sum.

The next-generation system, VISUMAX 800 with SMILE pro software, received FDA approval in January 2024. ZEISS Milestone: Celebrating more than 10 million eyes treated with lenticule extraction solutions utilizing ZEISS SMILE and ZEISS SMILE pro. ZEISS marked its 25th year of leadership in defining optical biometry, with ZEISS IOLMaster biometers becoming the most commonly used biometers in the ophthalmic world.

Carl Zeiss Meditec AG announced that ZEISS is celebrating its latest refractive milestone of surpassing the 10 million mark for lenticule extraction procedures performed with ZEISS SMILE and ZEISS SMILE pro. ZEISS leads the industry as the first medical device manufacturer to offer treatment for hyperopia with lenticule extraction using SMILE pro in the CE markets.

The competitive moat created by SMILE is substantial. Unlike LASIK, which can be performed using various manufacturers' equipment, SMILE requires Zeiss's proprietary VisuMax system. Zeiss makes money in the classic med-tech way: big-ticket equipment (think the VISUMAX 800 refractive laser), consumables like intraocular lenses, and a steady stream of service contracts and digital workflow tools. The landscape is crowded, with Zeiss butting heads against bigger diversified firms like Alcon, Johnson & Johnson Vision, Bausch & Lomb, and Topcon, as well as optical specialists like Leica and Nikon. Zeiss holds about 40% of the global refractive surgery market and a hefty 60% of microsurgery.

ZEISS maintains a competitive edge in broader applications due to its extensive track record and safety profile, with over 10 million SMILE procedures performed globally. ZEISS maintains a competitive edge in broader applications due to its extensive track record and safety profile. Strategic Positioning: ZEISS is poised to strengthen its competitive edge with the upcoming rollout of the VisuMax 800, a more advanced platform designed to enhance procedure speed, precision, and patient outcomes.

In China, the SMILE competitive advantage is particularly pronounced. Despite short-term challenges such as anti-corruption reforms, post-COVID consumer sentiment softness, and volume-based procurement (VBP) schemes, Carl Zeiss Meditec has remained resilient. ZEISS is the undisputed market leader in China with an estimated >50% market share, over 1,200 installed VISUMAX femtosecond lasers with more than 15% due for replacement, new platforms VISUMAX 800 and PRESBYOND launched for high-growth refractive and presbyopia treatments, and SMILE procedure accounts for 70% of volume, significantly ahead of LASIK at 30%.

VII. The Modern Era: Digital Transformation & The DORC Acquisition (2018–2025)

The period from 2018 to 2025 marked Carl Zeiss Meditec's most aggressive strategic transformation since its founding. Two parallel shifts defined this era: the pivot toward recurring revenue streams and the transformational acquisition of Dutch Ophthalmic Research Center (DORC).

The Recurring Revenue Transformation

Recurring revenue amounted to 47% in the 2023/24 fiscal year (prior year: 43%), with the DORC acquisition making a significant contribution.

This shift from equipment-centric revenue to consumables and services represents a fundamental business model evolution. The growth plan: deploy new VISUMAX 800 refractive lasers, ramp up premium intraocular lens launches, keep building recurring revenue (consumables and services now make up 47% of sales), and tap deeper into Asia-Pacific (already 26% of revenue).

The DORC Acquisition

In December 2023, Carl Zeiss Meditec announced its largest acquisition in company history. The acquisition is valued at approximately EUR 985 million and is expected to close in the first half of calendar year 2024. The transaction remains subject to applicable regulatory and antitrust approvals. Carl Zeiss Meditec AG announced today that it has entered into an agreement to acquire 100% of the shares in Dutch Ophthalmic Research Center (International) B.V. (D.O.R.C.) from the investment firm Eurazeo SE, Paris, France. The acquisition will enhance and complement ZEISS Medical Technology's broad ophthalmic portfolio and range of digitally connected workflow solutions for addressing a wide variety of eye conditions, including retinal disorders, cataracts, glaucoma and refractive errors. D.O.R.C., a leading player in the retinal surgical devices market, will be a key contributor to ZEISS Medical Technology's long-term strategy and success going forward. With the acquisition, ZEISS will expand its position in the vitreo-retinal (VR) surgery segment.

The deal closed in April 2024. Jena/Deutschland | Dublin/USA | April 4, 2024 | Carl Zeiss Meditec AG announced today that, after securing all required regulatory approvals, it has completed the acquisition of 100% of D.O.R.C. (Dutch Ophthalmic Research Center) from the investment firm Eurazeo SE, Paris, France. The acquisition enhances and complements ZEISS Medical Technology's broad ophthalmic portfolio and range of digitally connected workflow solutions for addressing a wide variety of eye conditions, spanning retina and cornea disorders, cataract, glaucoma, and refractive errors.

This acquisition extends and expands the Carl Zeiss Meditec Group's broad ophthalmic product portfolio and its offering of digitally networked workflow solutions for the treatment of a wide range of eye diseases by adding a solution for vitrectomy (VR). The purchase price amounts to €1,023.7m, and was paid on 3 April 2024.

Strategic rationale for the DORC acquisition extended beyond simple portfolio expansion. "Together we can offer an unmatched portfolio of advanced technologies and digital workflows. With D.O.R.C., we have an incredible opportunity to serve ophthalmologists around the world with more complete workflows and solutions than ever before," says Euan S. Thomson, Ph.D., President of Ophthalmology and Head of the Digital Business Unit for ZEISS Medical Technology. "We've set our sights high to become the top player in the world for ophthalmology by leveraging our workflow solutions, enhancing our portfolio offerings and market position in the anterior surgery segment, and by significantly expanding our presence in the posterior surgery segment."

AI and Digital Initiatives

At the ARVO 2025 conference, ZEISS unveiled the Research Data Platform (RDP), a cloud-based AI-driven tool that integrates clinical and research data to accelerate ophthalmic studies and enable personalized eye care through collaborations like one with Boehringer Ingelheim. In August 2025, ZEISS received CE mark approval for CIRRUS PathFinder, an AI-powered optical coherence tomography (OCT) assessment tool integrated into the CIRRUS 6000 system, which automates pathology detection and supports informed clinical decisions using deep learning algorithms.

Building on the 2022 acquisition of Preceyes B.V., Carl Zeiss Meditec has expanded robotic and AI-enhanced solutions for precision microsurgery, emphasizing applications in ophthalmology to improve surgical accuracy beyond 20 micrometers.

VIII. Current Business Model & Segment Deep Dive

Carl Zeiss Meditec operates through two primary segments, with ophthalmology representing the dominant revenue contributor.

Ophthalmology Segment (77% of Revenue)

The Ophthalmic Devices segment offers optical biometers, ophthalmic surgical microscopes, phacoemulsification/vitrectomy devices, intraocular lenses, and ophthalmic viscoelastic products for the diagnosis and treatment of ophthalmic diseases in the field of cataract and retinal surgery. This segment also offers optical coherence tomography devices, perimeters, fundus cameras, slit lamps, and therapeutic and refractive lasers for the diagnosis and treatment of various eye diseases, such as refraction, glaucoma, and other retinal diseases, as well as FORUM, an eye care data management system.

In the 2023/24 fiscal year, the Ophthalmology Strategic Business Unit (SBU) recorded slight growth of +0.8% (adjusted for currency effects: +1.8%, adjusted for currency and acquisition effects: -4.5%) with revenue of €1,589.2m (prior year: €1,576.5m). The initial contribution from the acquisition of the company DORC, specialized in retinal surgery, amounted to €99.9m.

The segment encompasses four major product categories:

- Refractive Surgery: VISUMAX femtosecond lasers, SMILE technology

- Cataract Surgery: Phacoemulsification systems, intraocular lenses, surgical microscopes

- Diagnostics: OCT systems, optical biometry, visual field analyzers

- Retinal Surgery: DORC vitrectomy platforms, surgical instruments, consumables

Microsurgery Segment (23% of Revenue)

MCS is composed of implants, surgical instruments, and visualization devices used during neurosurgery, spine surgery, and otolaryngology surgery.

The Microsurgery segment leverages Zeiss's optical heritage in non-ophthalmic applications. Core products include:

- KINEVO surgical microscopes for neurosurgery

- Visualization systems for ENT procedures

- Spine surgery instruments and navigation systems

With over 60% market share, Zeiss is the clear leader in the microsurgery space.

Revenue Mix and Recurring Revenue Growth

The shift toward recurring revenue represents a strategic priority. Zeiss makes money in the classic med-tech way: big-ticket equipment (think the VISUMAX 800 refractive laser), consumables like intraocular lenses, and a steady stream of service contracts and digital workflow tools.

With consumables and services now approaching half of total sales, Zeiss has substantially reduced its dependence on capital equipment cycles—a transformation that should provide greater earnings stability through economic downturns.

IX. Geographic Expansion & The China Factor

Carl Zeiss Meditec's geographic footprint reflects both its German heritage and its global ambitions.

The Group's head office is located in Jena, Germany, and it has subsidiaries in Germany and abroad; more than 50 percent of its employees are based in the USA, Japan, Spain and France. The Center for Application and Research (CARIn) in Bangalore, India and the Carl Zeiss Innovations Center for Research and Development in Shanghai, China, strengthen the Company's presence in these rapidly developing economies.

The China Opportunity—and Challenge

The region Greater China is the largest single market for Carl Zeiss Meditec AG with a revenue share of 26% in fiscal year 2023/24.

China's importance to Zeiss extends beyond current revenue. The myopia epidemic affecting Asian populations creates structural demand for refractive surgery solutions. The prevalence of myopia and HM in young adults in urban area of East Asian countries has risen to 80–90% and around 20%, respectively.

According to a myopia prevalence survey conducted in 2024 among adolescents aged 12–15 in Shandong Province, the overall prevalence of myopia was found to be 71.34%. When analyzed by gender, the data revealed a slightly higher incidence in girls at 72.26%, compared to 70.45% in boys. Age also appeared to be a contributing factor. The highest myopia prevalence was observed in 15-year-olds at 73.12%, followed by 14-year-olds at 72.10%, 13-year-olds at 70.46%, and 12-year-olds at 68.97%.

In China, the myopic population reached 750 million in 2020, accounting for about 47% of the total Chinese population. Among them, the overall prevalence of myopia in children and adolescents was 53.6%, and the overall prevalence of myopia in college students exceeded 90%.

This demographic tsunami creates enormous long-term demand for refractive correction. But China also presents significant near-term challenges.

China saw a decline due to a subdued peak season for refractive laser surgery in the summer months of 2024 compared to the previous year, following the normalization of refractive consumables inventories. The decline is mainly due to the weak revenue performance and a significantly less favorable product mix compared to the previous year, primarily as a result of the reduction in inventories of surgical consumables in the Chinese distribution channel and the weaker than expected demand for refractive treatments in China in the peak season summer months.

There is a strong market position in China, with a market share of over 50% in refractive procedures. There are ongoing pressures in the Chinese market, with a decline in consumer confidence and a shift towards more price-sensitive procedures.

X. Navigating Headwinds: 2023-2025 Challenges

Fiscal year 2023/24 tested Carl Zeiss Meditec's resilience. Dr. Markus Weber, President and CEO of Carl Zeiss Meditec AG commented on the results for the fiscal year: "2023/24 was a challenging fiscal year for us – we had to contend with significant cooling of the global economy and the consumer climate as well as a marked reluctance to invest in the equipment business in several core markets – particularly in North America. However, the tighter resilience measures that were imposed over the course of the fiscal year proved effective, ensuring that the lowered forecast for adjusted EBIT in June could be securely achieved. The general conditions are not expected to improve in 2024/25 – the current weakness of the Chinese market in particular has prompted us to take a cautious view."

Carl Zeiss Meditec generated revenue of €2,066.1m in fiscal year 2023/24 (prior year: €2,089.3m), corresponding to a decline of -1.1% (adjusted for currency and acquisition effects: -4.8%). Adjusted earnings before interest and taxes (EBIT) fell to €245.9m (prior year: €362.9m) and were therefore comfortably within the guidance after 9M 2023/24 of €225 – 275m. The adjusted EBIT margin, based on revenue excluding the contribution from the DORC acquisition, amounted to 12.5% (prior year: 17.4%).

Trade Tariff Impact

The introduction of 15% trade tariffs by the US on imports from Europe will have a negative impact on earnings in the current fiscal year. The effects will, to a large extent, be passed on to the market through a targeted pricing policy. Further devaluation of the US and Asian (CNY, KRW, JPY) currencies, in particular, has not been included in the forecast and represents an additional risk.

Leadership Transition

Starting 1 June 2025, the new President and CEO will be Maximilian Foerst, who is currently Head of ZEISS Greater China. Speaking about his appointment as President and CEO of Carl Zeiss Meditec AG, Maximilian Foerst said: "I am very much looking forward to this new position at Carl Zeiss Meditec AG. In challenging times, Carl Zeiss Meditec AG is very well positioned and aligned. The long-term potential of innovative medical technology is based on megatrends such as demographic change, the increasing importance of health and digitalization. Now, we have to leverage this with a keen eye to the diverse requirements of our global markets." Thus, starting 1 June 2025, the Management Board of Carl Zeiss Meditec AG will consist of Maximilian Foerst (President and CEO) and Justus Wehmer (Chief Financial Officer).

He then took on his current role as Head of ZEISS Greater China. Since then, he has overseen all business activities in China, Hong Kong and Taiwan (region). Under his leadership, these grew from 60 million euros in revenue to around two billion euros in annual revenue today. During this time, Maximilian Foerst established three strategic fields of business with global development and revenue responsibility and initiated a variety of acquisitions.

The appointment of Foerst—a leader who built Zeiss's China business from €60 million to €2 billion—signals strategic priorities: navigating the critical Asia-Pacific market and accelerating the digital transformation already underway.

Recovery Signs

Carl Zeiss Meditec generated revenue of €1,600.1m in the first nine months of fiscal year 2024/25 (prior year: €1,486.5m), including the DORC consolidation, corresponding to growth of +7.6% (adjusted for currency effects: +8.0%). Adjusted for currency and acquisition effects, revenue, at +1.1%, was slightly above the prior year's figure. Order intake rose significantly by +23.3%. Maximilian Foerst comments: "Overall, we are satisfied with the level of growth. We had to contend with headwinds in the third quarter, in particular in the form of negative currency effects and the introduction of US trade tariffs, but were nevertheless able to achieve both organic growth and earnings growth."

Order entry rose significantly by +33.4%.

The surge in order intake—up more than 23% in the nine-month period—suggests that underlying demand remains robust despite macro headwinds. This order book strength provides visibility into future revenue and supports management's moderate growth outlook.

XI. Playbook: Business & Strategy Lessons

Carl Zeiss Meditec's 175-year journey offers enduring lessons for investors analyzing medical technology companies.

Lesson 1: Foundation Ownership Enables Long-Term Thinking

The Carl Zeiss Foundation's perpetual ownership structure shields management from short-term shareholder pressure, enabling multi-decade technology bets like OCT and SMILE. Companies with patient capital often outperform in industries requiring sustained R&D investment.

The company's R&D intensity—approximately 16-18% of revenue—exceeds most publicly traded medical device peers. In spite of the slight decline in revenue in the first six months of fiscal year 2023/24, the R&D ratio increased from 17.0% in the prior year to 18.4%.

Lesson 2: Proprietary Technology Creates Durable Moats

SMILE represents perhaps the purest example of a technology moat in medical devices. Because the procedure requires Zeiss's proprietary VisuMax system, competitors cannot legally offer SMILE regardless of their manufacturing capabilities or financial resources.

Lesson 3: Platform Building Through Acquisitions Requires Patience

From Humphrey Instruments (1991) to DORC (2024), Zeiss has methodically assembled an integrated diagnostic-and-treatment ecosystem. Each acquisition filled specific gaps while creating cross-selling opportunities that competitors struggle to match.

Lesson 4: Recurring Revenue Transformation Requires Discipline

The shift from equipment-centric revenue (volatile, cyclical) to consumables and services (predictable, recurring) has taken two decades. With recurring revenue now approaching 47% of sales, Zeiss has materially reduced earnings volatility.

Lesson 5: Geographic Concentration Creates Both Opportunity and Risk

China's 26% revenue share exposes Zeiss to regulatory, geopolitical, and economic risks in that market. However, the structural myopia epidemic in Asia creates demand tailwinds that should persist for decades.

XII. Porter's Five Forces & Competitive Analysis

1. Threat of New Entrants: LOW

The barriers to entering ophthalmic medical devices are formidable: - Massive R&D requirements (16-18% of revenue for established players) - Regulatory approval timelines of 5-10 years for novel devices - Deep clinical relationships built over decades - Proprietary technologies (like SMILE) protected by patents and trade secrets

2. Bargaining Power of Suppliers: MODERATE

While Zeiss sources specialized optical components and precision instruments, vertical integration (through the parent Carl Zeiss AG and Schott glass) reduces supplier dependency. However, semiconductor shortages demonstrated supply chain vulnerabilities.

3. Bargaining Power of Buyers: MODERATE TO HIGH

Large hospital systems and purchasing groups can negotiate volume discounts. However, for premium procedures like SMILE—where Zeiss holds a monopoly—buyer power is limited. The shift to consumables increases switching costs.

4. Threat of Substitutes: LOW TO MODERATE

For diagnostic imaging (OCT), substitution is minimal—the technology has become standard of care. For refractive surgery, alternatives include glasses, contact lenses, and implantable collamer lenses (ICLs). However, surgical correction addresses underlying conditions rather than merely compensating for them.

5. Competitive Rivalry: HIGH

The landscape is crowded, with Zeiss butting heads against bigger diversified firms like Alcon, Johnson & Johnson Vision, Bausch & Lomb, and Topcon, as well as optical specialists like Leica and Nikon. Competitive threats: Deep-pocketed rivals like Alcon and J&J Vision are pushing hard on both research and pricing, which could eat into Zeiss's share in its core business areas.

The top players in this market are Carl Zeiss Meditec AG (Germany), EssilorLuxottica (France), Alcon (Switzerland), Topcon Corporation (Japan) and Bausch Health Companies Inc. (Canada). Due to their broad geographic reach and vast product portfolios, these companies dominate the market.

Hamilton Helmer's 7 Powers Analysis

- Scale Economies: Present but limited—medical devices do not exhibit the same scale effects as semiconductors or software

- Network Effects: Weak—device adoption is not self-reinforcing

- Counter-Positioning: Strong—Foundation ownership enables long-term R&D investment that public competitors cannot match

- Switching Costs: High for integrated workflows; surgeons trained on Zeiss systems face retraining costs

- Branding: Strong—175-year heritage commands premium pricing

- Cornered Resource: SMILE technology represents a genuine cornered resource

- Process Power: Moderate—precision manufacturing excellence provides quality advantages

XIII. Investment Considerations: Bulls, Bears, and Key Metrics

Bull Case

-

Structural Growth Tailwinds: The global ophthalmology market is projected to grow from approximately $63.71 billion in 2024 to $67.85 billion in 2025, continuing at a CAGR of 6.76%, reaching $94.36 billion by 2030.

-

Myopia Epidemic: Rising myopia prevalence, particularly in Asia, creates multi-decade demand for refractive correction. Researchers estimated the current global prevalence of myopia among children and young people to be 30.47%. The scientists predict that global prevalence will reach 39.80% by 2050.

-

SMILE Monopoly: Proprietary technology moat prevents direct competition

-

Recurring Revenue Growth: 47% recurring revenue reduces cyclicality

-

DORC Integration: Vitreoretinal surgery expansion opens new growth vectors

-

AI/Digital Transformation: Cloud platforms and AI diagnostics create new monetization opportunities

Bear Case

-

China Concentration: 26% revenue exposure to a single market with regulatory uncertainty

-

Tariff Headwinds: 15% US tariffs on European imports compress margins

-

Capital Equipment Cycles: Hospital spending remains sensitive to interest rates and economic conditions

-

Competition Intensifying: Alcon, J&J Vision investing heavily in refractive and cataract segments

-

DORC Integration Risk: €1 billion acquisition requires successful operational integration

-

Leadership Transition: New CEO during challenging market conditions

Key Metrics to Track

For investors monitoring Carl Zeiss Meditec, three KPIs deserve primary attention:

-

Recurring Revenue as % of Total Revenue: Currently 47%; trajectory toward 50%+ would signal successful business model transformation

-

Order Intake Growth: Leading indicator of future revenue; recent +23.3% growth signals demand recovery

-

China Segment Performance: Quarterly revenue and margin trends in Greater China region indicate both market position and macro exposure

XIV. Conclusion: The Patient Capital Advantage

Carl Zeiss Meditec represents an unusual case study in medical technology: a company whose competitive advantages derive as much from its 19th-century ownership structure as from its 21st-century technology portfolio.

The foundation model—Ernst Abbe's social experiment from 1889—continues to enable patient R&D investment that publicly traded competitors struggle to match. This structural advantage produced OCT imaging (standard of care since 2006) and SMILE laser correction (proprietary monopoly since 2011).

Today's challenges—China market weakness, tariff headwinds, capital equipment cycles—are real but likely cyclical. The structural tailwinds—global myopia epidemic, aging populations, healthcare digitalization—appear durable.

For long-term investors, Carl Zeiss Meditec offers exposure to a company with genuine technology moats, increasing recurring revenue, and patient capital backing. The 175-year track record suggests that short-term headwinds rarely derail long-term value creation when ownership prioritizes science over quarterly earnings.

The optician's workshop Carl Zeiss opened in 1846 has become the precision empire of the eye—and the foundation structure Ernst Abbe created in 1889 remains its most enduring competitive advantage.

Material Risks and Disclosures: Carl Zeiss Meditec faces regulatory risks in all operating jurisdictions, particularly regarding FDA and CE mark approvals. China exposure creates geopolitical and regulatory uncertainty. The company's fiscal year ends September 30, and currency translation effects can materially impact reported results. The 59% stake held by Carl Zeiss AG limits public shareholder influence on strategic decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube