AerCap: How Ireland's Aviation Upstart Became the 800-Pound Gorilla of Aircraft Leasing

I. Introduction & Episode Roadmap

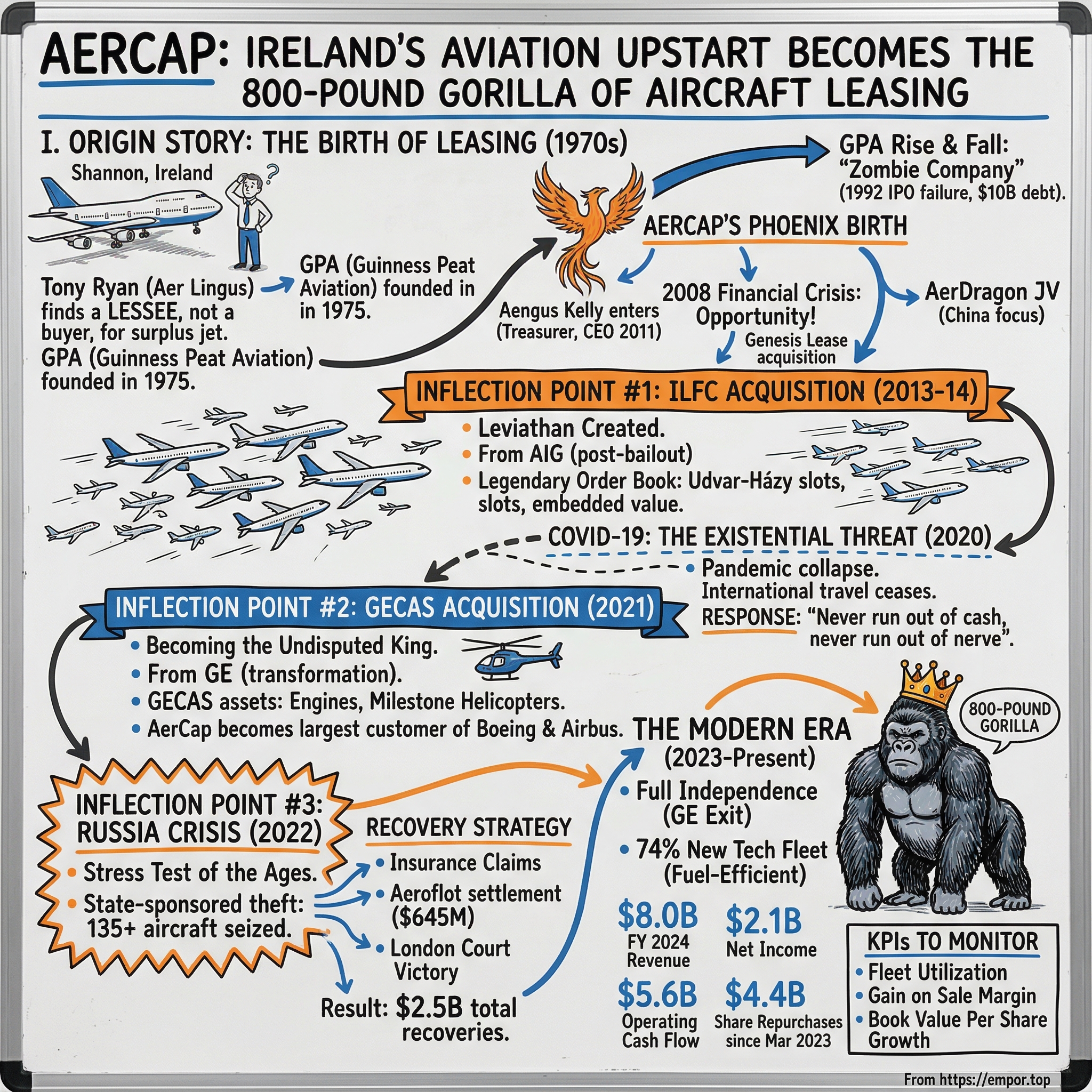

Picture a single Boeing 747 parked on the tarmac at Shannon Airport in the early 1970s—a gleaming jetliner that Aer Lingus, Ireland's flag carrier, no longer needs. The plane sits idle, bleeding cash, a monument to the brutal economics of aviation. A young executive named Tony Ryan receives an unusual assignment: find someone, anyone, willing to take this aircraft off their hands. Ryan doesn't find a buyer—he does something far more radical. He finds a lessee.

That improvised solution to a parking problem sparked an industry that would fundamentally reshape global aviation. Fifty years later, approximately half of all commercial aircraft worldwide fly under lease agreements, and the company that traces its lineage directly to Ryan's innovation—AerCap Holdings N.V.—stands as the undisputed emperor of this $200+ billion domain.

AerCap Holdings N.V. is the industry leader across all areas of aviation leasing. As of September 30, 2024, AerCap owns $74 billion in total assets, working with approximately 300 customers in countries across the world. Their portfolio includes 1,700 aircraft, more than 1,000 engines and more than 300 helicopters.

The hook is irresistible: How did a small Irish aviation firm, operating from a free-trade zone in the Atlantic mist, become the 800-pound gorilla of aircraft leasing through two of the largest transactions in aviation history? The answer involves a cast of visionary founders, financial engineering of Olympic caliber, existential crises survived, and geopolitical shocks that would have destroyed lesser companies.

The acquisitions of ILFC (the "ILFC Transaction") and GECAS (the "GECAS Transaction") are the two largest transactions in the history of aviation leasing. These weren't merely corporate transactions—they were acts of industry consolidation so decisive that they permanently altered the competitive landscape.

In the fourth quarter of 2024, AerCap reported net income of $671 million, or $3.56 per share, and $2.1 billion, or $10.79 per share, for the full year 2024. Full year 2024 revenue reached US$8.00 billion, up 5.6% from fiscal year 2023.

This is a story about scale economics in their purest form, about M&A execution that borders on artistry, about capital allocation discipline that would make Warren Buffett nod approvingly, and about surviving geopolitical earthquakes that saw billions in assets effectively confiscated by a hostile government. Let's trace the arc from a surplus jumbo jet in Shannon to global dominion.

II. The Birth of Aircraft Leasing: Ireland's Unlikely Gift to Aviation

The mist hangs low over Shannon Airport on a January morning in 1975. In a modest office building within the Shannon Free Trade Zone, a handful of employees—six, including a secretary—prepare to launch an enterprise that will eventually control assets worth more than the GDP of most countries. They don't know this yet. What they know is that their boss, Tony Ryan, has identified something the rest of the aviation industry has missed.

2025 marks a significant milestone for the aircraft leasing industry and for AerCap, as we celebrate 50 years since the industry was founded here in Ireland in 1975. Today, approximately 50% of the world's commercial aircraft fleet is leased, and Irish lessors own and manage ~$150 billion of assets.

To understand how Ireland became aviation's financial capital, you must understand the man who saw possibilities where others saw liabilities.

The Tony Ryan Origin Story

Thomas Anthony Ryan (2 February 1936 – 3 October 2007) was an Irish billionaire businessman and philanthropist who co-founded Ryanair in 1984 along with cofounders Christopher Ryan and Liam Lonergan. But before the famous budget airline, there was his first aviation revolution.

Ryan was born at Limerick Junction, County Tipperary on 2 February 1936; his father was a train driver. Around 1945 the family moved to Thurles in the same county, and he attended the Christian Brothers school there. This son of a railway stationmaster possessed neither family wealth nor Oxbridge connections—just relentless ambition and an uncanny instinct for the mechanics of money.

Ryan joined Aer Lingus as a dispatch clerk and climbed steadily. Tony Ryan, born Thomas Anthony Ryan on 2 February 1936 in Thurles, County Tipperary, Ireland, to a family where his father worked as a train driver, began his aviation career early in life. He joined Aer Lingus, Ireland's national airline, in 1955 as a dispatcher at Shannon Airport. Over the next two decades, Ryan demonstrated strong managerial skills, advancing through various positions in cargo handling and leasing.

The pivotal moment arrived in the early 1970s. Aer Lingus had acquired a Boeing 747 that proved redundant for its route network. His experience negotiating deals, such as leasing a surplus Boeing 747 to Air Siam (predecessor to Thai Airways International), convinced him of the potential for an independent leasing firm to bridge this gap by providing flexible financing options.

This wasn't merely a transaction—it was an epiphany. Ryan recognized that aviation's capital intensity created structural opportunities. Airlines needed flexibility; they couldn't predict demand years in advance. Aircraft manufacturers needed volume buyers who could place massive orders. Between these two needs lay an enormous gap that a well-capitalized, expertly managed intermediary could fill.

Founding Guinness Peat Aviation

Guinness Peat Aviation (GPA) was an aircraft leasing company set up in 1975 by Aer Lingus, the Guinness Peat Group (a London-based financial services company) and Tony Ryan, then an Aer Lingus executive. GPA was based in Shannon, Ireland.

In May he became chief executive of Guinness Peat Aviation (GPA), which brokered the sale and leasing of aircraft and was capitalised at £30,000, with Aer Lingus and London merchant bank Guinness Peat each having a 45 per cent shareholding. Extracting an equity holding, profit-sharing entitlements, and a guarantee that his stake could not be diluted, Ryan remortgaged his house to raise the £3,000 needed for his 10 per cent shareholding.

The symbolism is striking: Ryan bet his family home on an industry that didn't yet exist. The £3,000 stake—approximately $50,000 in today's currency—would eventually make him a billionaire.

By basing his small operation in the Shannon industrial zone, Co. Clare, Ryan gained tax exemptions on profits and dividends and also offices at subsidised rents. Conversely, this bleak backwater hampered recruitment and suffered from unreliable telecommunications and unsatisfactory services at the adjoining airport.

Shannon's location proved both blessing and curse. The tax advantages were substantial—Ireland's favorable treatment of aviation finance remains a cornerstone of the industry's Irish dominance—but the remote western Ireland location made attracting talent genuinely difficult. Ryan compensated by paying extraordinarily well and by cultivating a meritocratic culture that rewarded results over pedigree.

The Parallel Titan: ILFC in California

Across the Atlantic, in Southern California, another aviation visionary was simultaneously inventing the same business.

Steven Udvar-Házy founded ILFC with fellow Hungarian Leslie Gonda and his son Louis Gonda in 1973, leasing a single used Douglas DC-8 to Aeroméxico. He left ILFC in February 2010 and founded Air Lease Corporation.

ILFC introduced the world to a simple concept, now known as the "operating lease." No longer did airlines have to buy their planes with bank financing or long-term tax leverage leases.

The near-simultaneous emergence of GPA and ILFC—neither aware of the other's existence initially—demonstrates that aircraft leasing was an idea whose time had come. Rising fuel costs, economic volatility, and the massive capital requirements of the jet age created conditions that demanded a new financial structure.

He flew airplanes at age 14 and invented the aircraft leasing industry in his 20s. Udvar-Házy brought a refugee's hunger to succeed—his family had fled Communist Hungary in 1958—combined with an obsessive knowledge of aircraft specifications that bordered on savant-level.

Why Ireland Won

Other factors have contributed to the growth and success of the industry, including Ireland's rich aviation heritage, a highly skilled talent pool, a comprehensive double tax treaty network and pro-enterprise policies, along with a stable political and legal system and regulatory framework.

Ireland is the leading centre for aircraft leasing worldwide, with a 65 per cent share of the global market. More than 50 aircraft leasing companies are based here, including 14 of the world's top 15 lessors. It is estimated that an Irish-leased aircraft takes off somewhere in the world every two seconds.

Ireland's dominance stemmed from multiple reinforcing advantages: a 12.5% corporate tax rate, an extensive double taxation treaty network that eliminated withholding taxes on cross-border lease payments, common law legal traditions familiar to international investors, and English-language documentation. But most critically, Ireland possessed the human capital—generations of professionals trained at GPA and its successors who understood aviation finance's complexities.

Why Airlines Lease

The economics are compelling. An Airbus A320neo lists at approximately $110 million; a Boeing 787 approaches $250 million. For airlines operating dozens or hundreds of aircraft, the capital requirements are staggering. Leasing transforms this capex burden into operating expenditure, preserving capital for route development, marketing, and operational improvements.

Leasing is now the preferred option for airlines over buying, having risen from roughly 10 per cent of the total fleet in the 1970s to 58 per cent at the end of 2023. The most spectacular increase occurred between 1980 and 2010, and the share first crossed the 50 per cent mark in 2004, according to the International Air Transport Association (IATA).

Beyond balance sheet management, leasing provides fleet flexibility impossible for owners to achieve. An airline expanding into new markets can lease aircraft for the attempt without committing to purchases that might prove disastrous if the routes fail. Conversely, airlines facing downturns can return leased aircraft at lease-end rather than owning depreciating assets they cannot profitably deploy.

The industry that Ryan and Udvar-Házy invented had solved a genuine market failure. What followed was a fifty-year story of growth, crisis, consolidation, and ultimately, AerCap's emergence as the undisputed champion.

III. The GPA Rise and Fall, and AerCap's Phoenix Birth (1975-2006)

The GPA Empire Ascends

During the 1980s it became the world's largest commercial aircraft lessor.

In 1990 GPA reported profits of $242 million (up from $9 million in 1983), leased 240 planes (up from twenty in 1983) to sixty-eight airlines in forty-one countries, and claimed 10 per cent of all aircraft to be manufactured until 2000.

The growth was exponential. From a standing start with borrowed premises and a handful of staff, GPA expanded into a global powerhouse. Ryan himself became spectacularly wealthy. Benefiting from performance-related share bonuses, Ryan held an 8 per cent shareholding worth $304 million in 1990, and reaped $84.5 million in dividends during 1985–92.

The business soared, and by 1991 they had a turnover of more than $2bn and at its peak it was valued at $4bn and was reportedly buying a plane a week.

GPA's culture was famously demanding. Ryan drove his people hard, compensated them extraordinarily, and built loyalty through shared success. Headquartered at a tax-free base in Shannon, the initial staff consisted of six people, including a secretary. They worked hard under the very demanding Ryan and were compensated extremely well.

The company developed deep relationships with aircraft manufacturers, negotiating bulk orders at prices unavailable to airlines purchasing individually. This procurement advantage became a structural moat—GPA could offer aircraft at lease rates no competitor could match because no competitor had such favorable acquisition costs.

The 1992 Disaster

Then came the catastrophe.

The decision to float the company on the stock market in 1992, during an aviation industry downturn following the 1991 Gulf War, proved disastrous, as international financial institutions refused to buy shares. Unable to raise the capital it needed to continue its ambitious operations, the company plunged into crisis, with some $10 billion in debts.

It all came a cropper for GPA and Ryan in 1992 when its plans for an IPO on the stock market, offering $850 million worth of shares, collapsed at the last minute. Confidence in the company evaporated and it was effectively a zombie company. At a stroke, employee shares, which had soared in the years leading up to the flotation attempt, were worthless, leaving many GPA staff to nurse massive bank loans that had been taken to buy stock.

The timing could not have been worse. The First Gulf War had triggered aviation demand collapse; the industry was reeling. GPA's aggressive ordering strategy—brilliant in good times—became a millstone when airlines couldn't absorb new aircraft. The company had committed to billions in aircraft purchases it couldn't deploy or finance.

The failed IPO laid bare the business's vulnerabilities. GPA had grown too fast, ordered too aggressively, and financed itself too precariously. When confidence evaporated, so did GPA's access to capital markets.

The GE Rescue and Transformation

In a subsequent restructuring completed in November 1993, GPA avoided default on its debts by selling some of its aircraft to GE Capital Aviation Services (GECAS), a subsidiary of General Electric, which also took over the operational management of GPA's fleet and most of GPA's technical and marketing staff. GE Capital also acquired an option to purchase 90% of GPA's ordinary shares at a low price. GPA used the cash from this transaction to repay all its unsecured debt.

The GE intervention saved the company from liquidation but left it severely diminished. It was eventually sold in 2000 to Debis AirFinance, a unit of Daimler Chrysler, with Tony Ryan reportedly making $50 million from the sale.

AerCap's Formation

The corporate genealogy now grows complex, but it is essential to understanding AerCap's DNA.

In November 2006, the company became a public company via an initial public offering.

In March 2010, the company acquired Genesis Lease at a discount to book value as a result of the financial crisis, following this transaction Paul Dacier and Michael Gradon joined the AerCap board. By 2013, the affiliates of Cerberus sold substantially all of their shares in the company.

The company that emerged from this corporate restructuring carried GPA's institutional knowledge, its relationships, its Shannon heritage—but shed the excessive leverage and overcommitment that had destroyed the original enterprise. AerCap was, in essence, GPA reborn: leaner, more disciplined, and determined to avoid the mistakes that had brought its predecessor low.

The Ryanair Connection

One final element of the origin story demands attention. GPA's founder, Tony Ryan, set up his own airline, Ryanair, that was Europe's biggest in 2014, carrying over 83.8 million passengers annually.

The relationship between aircraft leasing and low-cost aviation proved symbiotic. Ryanair's aggressive growth strategy depended heavily on leased aircraft; conversely, the budget carrier model—high utilization rates, rapid turnaround times, strong credit quality—made low-cost airlines ideal lessees. Many of the directors and staff of GPA subsequently went on to found or work for other aircraft lessors, such as GECAS (now merged into AerCap), Genesis Lease, CIT, AerCap (a successor to Guinness Peat), ILFC (now merged into AerCap), and others.

The talent diaspora from GPA seeded the entire industry. Nearly every major aircraft lessor operating today can trace its leadership lineage back to Shannon.

IV. Aengus Kelly and the Genesis Acquisition (2006-2013)

Enter Aengus Kelly

The man who would transform AerCap from a mid-sized player into an industry colossus arrived not as a brash outsider but as a company lifer who understood the business from the ground up.

Mr. Kelly was appointed Executive Director and Chief Executive Officer of AerCap on May 18, 2011. Previously he served as Chief Executive Officer of AerCap's U.S. operations from January 2008 to May 2011. Mr. Kelly served as AerCap's Group Treasurer from 2005 through December 31, 2007. He started his career in the aviation leasing and financing business with Guinness Peat Aviation (GPA) in 1998 and continued working with its successors AerFi in Ireland and debis AirFinance and AerCap in Amsterdam. Prior to joining GPA in 1998, he spent three years with KPMG in Dublin. Mr. Kelly is a Chartered Accountant and holds a Bachelor's degree in Commerce and a Master's degree in Accounting from University College, Dublin.

Kelly's background—accountant, treasurer, operational executive—produced a CEO with comprehensive understanding of leasing economics. He knew how aircraft values behaved across economic cycles, how financing costs affected returns, and how airline credit quality varied by region and business model. This wasn't MBA theorizing; this was practical knowledge earned over a decade of deal-making.

Aengus Kelly, a chartered accountant with a degree in Commerce and a master's in Accounting from UCD, was appointed Executive Director and CEO of AerCap, the world's largest aviation leasing company, in 2011. Under his leadership, the Dublin-based, New York-listed company acquired GE Capital Aviation Services (GECAS) in a landmark €25bn deal in 2021.

Aengus Kelly's exceptional leadership was recognised at the Aviation 100 Awards 2024, where he was named Global CEO & Industry Leader of the Year.

The 2008 Financial Crisis Opportunity

The global financial crisis created conditions that would prove transformational. Banks retrenched from aircraft lending; weaker lessors faced financing pressures; asset prices declined. For a company with access to capital and the courage to deploy it, opportunities abounded.

In March 2010, the company acquired Genesis Lease at a discount to book value as a result of the financial crisis.

The Genesis acquisition demonstrated Kelly's approach: identify quality assets held by distressed sellers, acquire at attractive valuations, integrate efficiently, and wait for markets to normalize. The playbook was straightforward in concept, difficult in execution, and enormously lucrative when successful.

Building AerDragon and Expanding Horizons

Simultaneously, AerCap expanded geographically, recognizing that Asia's aviation growth would drive global demand.

From 2007 to 2013, AerCap expanded its fleet via new aircraft orders, secondary market acquisitions, and strategic partnerships. The company formed AerDragon Aviation Leasing in 2009 as a joint venture with Industrial and Commercial Bank of China to tap Asian markets.

China's aviation growth was—and remains—the industry's most important structural tailwind. Chinese middle-class expansion drives air travel demand; Chinese airlines need aircraft; Western lessors provide capital and fleet solutions that Chinese carriers increasingly embrace. AerCap's early positioning in this market proved prescient.

Setting the Stage

By 2013, AerCap had demonstrated the model worked at mid-tier scale. The company possessed: - A young, desirable fleet concentrated in fuel-efficient narrow-body aircraft - Strong relationships with Boeing and Airbus - Investment-grade credit ratings enabling efficient funding - Experienced leadership with deep industry knowledge - Geographic diversification across major aviation markets

What AerCap lacked was scale sufficient to dominate. In aircraft leasing, scale matters enormously. Larger lessors command better pricing from manufacturers, access cheaper financing, maintain deeper customer relationships, and generate higher returns on their fixed cost base.

The solution would arrive in the form of the industry's largest transaction ever.

V. INFLECTION POINT #1: The ILFC Acquisition – Creating a Leviathan (2013-2015)

The Strategic Context

The 2008 financial crisis had left profound scars on American International Group (AIG), the insurance giant that had acquired ILFC in 1990 for $1.3 billion. AIG's near-collapse required massive government intervention, and regulators demanded the company simplify its structure and divest non-core assets.

The divestiture of ILFC completes a series of sales that AIG began in 2008 to repay its government bailout.

ILFC was a crown jewel—the company Udvar-Házy had built into an industry powerhouse—but it sat awkwardly within a restructuring insurance company. AIG's agreement to sell ILFC to AerCap replaced a failed transaction with a group of Chinese investors. Earlier sale attempts had collapsed, leaving AIG increasingly motivated to transact.

The Legendary Order Book

ILFC possessed something beyond aircraft—it held production slots that represented billions in embedded value.

AerCap gains ILFC's $21 billion order backlog, stocked with highly sought-after production slots nabbed by Udvar-Hazy for Boeing Co. 787 Dreamliners and Airbus Group NV A350s at "unambiguously below-market prices." Wells Fargo estimates there is $2 billion or more of "embedded value" in ILFC's order book because of its early bulk orders for the jets.

Udvar-Házy had ordered aircraft years before competitors recognized their value, locking in prices that subsequent demand increases had rendered spectacularly favorable. These production slots couldn't be replicated—Boeing and Airbus production was sold out years in advance.

The Deal

On December 16, 2013, AerCap announced the transaction that would transform it from an industry participant into the industry leader.

AerCap today announced that it has entered into a definitive agreement with American International Group, Inc. ("AIG") under which AerCap will acquire 100% of the common stock of International Lease Finance Corporation ("ILFC"), a wholly-owned subsidiary of AIG. Under the terms of the agreement, AIG will receive $3.0 billion in cash and 97,560,976 AerCap shares.

Based on the closing stock price of AerCap's shares on Friday, December 13, 2013, the total consideration has a value of approximately $26 billion including the assumption of the outstanding ILFC net debt of $21 billion. Upon closing of the transaction, AIG will own approximately 46% of the combined company.

The structure was elegant. Rather than burdening AerCap with massive debt to fund an all-cash acquisition, the transaction used AerCap equity as currency. AIG became a substantial AerCap shareholder—aligned with the combined company's success—while receiving sufficient cash to satisfy regulatory requirements.

The Transformation

In May 2014, the company acquired International Lease Finance Corporation from American International Group (AIG) for $3.0 billion of cash and $4.6 billion in stock. The deal gave AerCap $43 billion in total assets and a fleet of over 1,300 aircraft, making it the largest in the world by fleet value, and second to competitor GE Capital Aviation Services by fleet count.

AerCap's CEO Aengus Kelly commented on the completion of the acquisition: "With approximately $45 billion of assets coupled with a diverse fleet of 1,300 aircraft and an attractive forward order book, AerCap will be a driving force in the industry. As such, we are well positioned to offer our customers on a global basis an unprecedented portfolio of best-in-class aircraft, while providing our shareholders tremendous growth prospects in the coming years."

Integration Excellence

The integration challenge was substantial. ILFC's Los Angeles headquarters, ILFC's culture (shaped by decades under Udvar-Házy's distinctive leadership), ILFC's systems—all required careful handling. But Kelly approached integration with the accountant's precision that characterized his leadership style.

In January 2015, the company moved its assets and headquarters to Ireland.

The headquarters relocation to Dublin consolidated AerCap's Irish identity while capturing tax efficiencies that the Irish jurisdiction provided. More importantly, it signaled that this was an AerCap-led integration, not a merger of equals.

The ILFC acquisition established a pattern that would define AerCap's strategy: identify transformational opportunities, structure transactions to preserve financial flexibility, integrate acquired operations efficiently, and emerge stronger than either predecessor company. Seven years later, Kelly would execute the playbook again—at even larger scale.

VI. The Integration Years & Building for the Next Leap (2015-2020)

Post-ILFC Integration

The years following the ILFC acquisition were ones of digestion and optimization. AerCap systematically rationalized the combined fleet, disposing of older aircraft while acquiring modern, fuel-efficient replacements.

By the end of 2015, AerCap's portfolio consisted of 1,697 aircraft that were owned, on order, under contract or managed. The average age of the owned fleet as of 31 December 2015 was 7.7 years and the average remaining contracted lease term was 5.9 years.

Fleet age matters enormously in aircraft leasing. Younger aircraft command higher lease rates, require less maintenance, consume less fuel, and depreciate more slowly. AerCap's disciplined focus on fleet youth—disposing of older aircraft before they became problematic—protected asset values and strengthened customer relationships.

In June 2015, AerCap signed an agreement with Boeing for an order of 100 Boeing 737 MAX 8 aircraft with deliveries starting in 2019.

In February 2016, AerCap reported record 2015 financial results and authorized a share repurchase program of $400 million.

The share repurchase announcement signaled confidence in the business and capital allocation discipline. Rather than empire-building through endless acquisitions or hoarding cash unnecessarily, AerCap returned capital to shareholders when attractive opportunities to deploy it were unavailable.

The Boeing 737 MAX Crisis

Then came an unexpected crisis—not from AerCap's operations but from one of its key suppliers.

The Boeing 737 MAX grounding from 2019 to 2020 disrupted delivery schedules across the industry. Airlines waiting for new aircraft faced delays; lessors with MAX orders confronted uncertainty about when—or whether—those aircraft would deliver.

AerCap navigated this disruption better than most. The company's diversified fleet included Airbus A320neo family aircraft—the MAX's direct competitor—allowing continued placements. Strong relationships with both manufacturers provided optionality unavailable to smaller lessors committed to single supplier strategies.

COVID-19: The Existential Threat

Nothing in AerCap's fifty-year corporate history compared to 2020. The COVID-19 pandemic triggered the most severe collapse in aviation demand ever recorded. International air travel essentially ceased; domestic markets plummeted; airlines faced existential liquidity crises.

For lessors, the pandemic presented dual threats: airlines unable to pay lease rents, and aircraft values potentially collapsing if demand didn't recover. AerCap's response demonstrated the resilience its leadership had spent decades building.

The company negotiated rent deferrals with struggling airlines—preserving relationships while supporting customers through unprecedented stress. It husbanded liquidity obsessively, ensuring it could meet obligations regardless of how long the crisis persisted. And it watched for opportunities, recognizing that aviation's fundamental drivers—growing global middle classes, irrepressible human desire to travel—remained intact.

"Never run out of cash, never run out of nerve" could have been the company's pandemic motto. AerCap did neither.

VII. INFLECTION POINT #2: The GECAS Acquisition – Becoming the Undisputed King (2021)

GE's Strategic Pivot

As AerCap navigated the pandemic's depths, General Electric was executing its own corporate restructuring. CEO Larry Culp, brought in to revive the struggling conglomerate, had concluded that GE's future lay in industrial businesses—aviation engines, power generation, healthcare equipment—not financial services.

GE Chairman and CEO H. Lawrence Culp, Jr. said, "Today marks GE's transformation to a more focused, simpler, and stronger industrial company. Coupled with our continuing efforts to strengthen GE's performance, operations, and culture, this deal brings GE closer to our future—delivering value for the long term and leading the energy transition, precision health, and the future of flight."

GECAS—General Electric Capital Aviation Services—was aviation leasing's second-largest player, tracing its lineage to GE's 1993 GPA bailout. The business was substantial, profitable, and strategically valuable. But it wasn't core to GE's future, and Culp was willing to sell.

The Deal Structure

In March 2021, AerCap announced they had reached a deal to acquire GE Capital Aviation Services (GECAS) from General Electric for US$24 billion in cash, US$1 billion of AerCap notes and approximately 46% of the combined business in shares. The acquisition was approved by AerCap shareholders in May 2021. In November, the company completed the acquisition for 111.5 million AerCap shares, approximately $23 billion of cash and $1 billion of AerCap notes.

Under the terms of the transaction agreement, GE received consideration valued at more than $30 billion, including approximately $24 billion in cash, 111.5 million ordinary shares. GE transferred $34 billion of GECAS' net assets, including its engine leasing and Milestone helicopter leasing businesses, to AerCap.

The acquisition's timing was audacious. AerCap announced it during the pandemic's grip, when aviation's future remained uncertain. But Kelly recognized what others missed: the pandemic was temporary; aviation's structural growth trajectory was permanent. Acquiring GECAS at distressed valuations—using cheap debt and equity that had declined from pre-pandemic levels—represented generational opportunity.

The Combined Company

The acquisition positions AerCap as the worldwide industry leader across all areas of aviation leasing: aircraft, engines and helicopters. The combined company will serve approximately 300 customers around the world and will be the largest customer of Airbus and Boeing. AerCap now has a portfolio of over 2,000 aircraft, over 900 engines and over 300 helicopters, as well as an order book of approximately 450 of the most fuel-efficient and technologically advanced aircraft in the world.

GECAS brought capabilities AerCap had lacked. Most significantly, GECAS operated a leading engine leasing business—engines represent an enormous pool of assets that aircraft lessors had largely neglected—and Milestone Aviation, the world's largest helicopter lessor. AerCap's addressable market expanded dramatically.

"Completion of this transaction represents an important milestone for AerCap that will generate benefits for our customers, partners, employees and investors for many years to come," said Aengus Kelly, Chief Executive Officer of AerCap. "In GECAS, AerCap has acquired the right business, for the right price, at the right time, as air travel continues to recover from the pandemic and demand for aircraft leasing continues to accelerate."

Financing Prowess

The GECAS acquisition required raising approximately $24 billion in new debt—an enormous sum under any circumstances, and extraordinary during a pandemic-induced credit crunch.

Aengus Kelly stated: "I am delighted that we successfully completed the acquisition of the GECAS business during the fourth quarter. Our ability to raise $24 billion of long-term funding for the acquisition at very attractive rates illustrates the depth of investor interest in aircraft leasing."

AerCap's investment-grade credit ratings—painstakingly earned over years of disciplined financial management—proved essential. The company accessed debt markets at rates unavailable to lower-rated competitors, locking in long-term funding that would prove valuable as interest rates subsequently rose.

VIII. INFLECTION POINT #3: The Russia Crisis – Stress Test for the Ages (2022-2025)

The Shock

Just months after completing the GECAS acquisition, AerCap faced a crisis without precedent in aviation leasing history.

The company was negatively affected by the 2022 Russian invasion of Ukraine and the international sanctions that followed. At the beginning of the invasion, it had 152 aircraft valued at $2.5 billion in Russia and Ukraine, which foreign companies were unable to recover or service. In May 2022, the company reported a net loss of $2 billion due to the seizure of its planes and engines by the Russian authorities.

Following the invasion of Ukraine on 24 February 2022, Western sanctions forced lessors to cancel all of these leasing contracts. However, Moscow refused to allow the planes to leave and passed somewhat legally dubious legislation which stated that any leased aircraft re-registered on the Russian civil aircraft register became the outright property of the operating Russian airline.

Russia's response was, in effect, state-sponsored theft. The country simply seized hundreds of Western-owned aircraft, re-registered them under Russian civil aviation authority, and claimed ownership had transferred. The legal basis was laughable; the practical effect was devastating.

AerCap had 135 aircraft on lease to Russian carriers at the time, along with 14 engines. Monthly lease rents had been running approximately $33 million. The company managed to recover only 22 aircraft and three engines before Russian authorities locked down the remainder.

The Recovery Strategy

AerCap's response combined legal action, insurance claims, and pragmatic settlement negotiations.

Aircraft leasing company AerCap said it received a cash settlement of $645 million for 17 aircraft and five engines leased to Aeroflot, including its subsidiary Rossiya Airlines. In a United States (US) Securities and Exchange Commission (SEC) filing on September 5, 2023, AerCap said it "received cash insurance settlement proceeds in the total amount of approximately US$645 million in full settlement of our insurance claims."

The Aeroflot settlement established a template: Russian airlines and their insurers would pay compensation—less than full value, but meaningful recovery—in exchange for AerCap releasing claims and transferring formal ownership to Russian entities.

"During the fourth quarter of 2023, we recognized recoveries related to the Ukraine Conflict of $614 million, primarily consisting of cash insurance settlement proceeds received from four Russian airlines and their Russian insurers in settlement of our insurance claims in respect of 50 aircraft and five spare engines on lease to these airlines at the time of Russia's invasion of Ukraine in February 2022."

The Insurance Litigation Victory

AerCap simultaneously pursued its Western insurers through London's Commercial Court, arguing that insurance policies should cover the losses Russia had inflicted.

The world's largest aircraft lessor AerCap can recover more than $1 billion in relation to jets stuck in Russia since the invasion of Ukraine, London's High Court ruled, though that is less than the roughly $2 billion it sought. The court ruled broadly in favor of leasing companies in a multi-billion-dollar legal dispute with insurers.

Following recoveries of $1.3 billion in 2023 and $195 million in 2024, this indemnity award will bring AerCap's total pre-tax recoveries relating to the Ukraine conflict to approximately $2.5 billion. In 2022, we recognized a pre-tax net charge of $2.7 billion to our earnings, which included a total loss write-off with respect to the assets which remained in Russia and Ukraine.

The recovery of approximately $2.5 billion against a $2.7 billion write-down represents remarkable success. While AerCap certainly suffered losses—the time value of money, the management distraction, the operational disruption—the company demonstrated resilience that validated decades of conservative risk management.

The Russia crisis also transformed industry practices. Lessors now examine geopolitical risk more carefully, diversify country exposures more deliberately, and structure leases with enhanced recovery provisions. AerCap emerged from the crisis with hard-won expertise that competitors will spend years developing.

IX. The Modern Era: Scale, Returns & Capital Allocation (2023-Present)

GE's Exit and Full Independence

Following a successful secondary offering of 30.7 million shares in the fourth quarter of 2023, GE has now sold all of its AerCap shares.

GE's complete divestiture marked AerCap's transition to full public ownership. The company no longer had a dominant shareholder with potentially divergent interests; management reported solely to public shareholders whose interests aligned entirely with long-term value creation.

The Current Portfolio

Since 2014, AerCap has transformed its fleet from approximately 6% new technology aircraft measured by net book value to approximately 74% new technology aircraft at the end of 2024, among the highest percentages of all major aircraft lessors. New technology aircraft include Airbus A220 Family, Airbus A320neo Family, Airbus A330neo Family, Airbus A350, Boeing 737 MAX, Boeing 787 and Embraer E2 aircraft.

This fleet transformation represents strategic execution at its finest. In 2014, AerCap owned primarily older-generation aircraft; by 2024, three-quarters of the fleet consisted of the newest, most fuel-efficient aircraft available. Airlines crave these aircraft—they reduce fuel costs, meet environmental regulations, and improve passenger experience. AerCap's ability to offer them at scale creates sustainable competitive advantage.

With a fleet utilization rate of 99% and strong lease revenue projections, AerCap maintains its leadership in the aircraft leasing industry.

The 99% utilization rate—meaning virtually every aircraft in the fleet is on lease and generating revenue—demonstrates the quality of both the aircraft and the customer relationships.

Financial Performance

Net income of $671 million, or $3.56 per share, for the fourth quarter of 2024 and $2.1 billion, or $10.79 per share, for the full year 2024. Adjusted net income of $624 million, or $3.31 per share, for the fourth quarter of 2024 and $2.3 billion, or $12.01 per share, for the full year 2024.

Record $5.6 billion operating cash flow for the last twelve months.

The operating cash flow figure deserves particular attention. Aircraft leasing generates enormous cash flows—lease payments arrive monthly, creating predictable revenue streams that exceed reported earnings due to non-cash depreciation charges. This cash generation provides capital for new aircraft purchases, debt repayment, and shareholder returns.

Capital Return Program

AerCap has deployed substantial capital to share repurchases—a signal that management believes the stock trades below intrinsic value.

Share repurchase authorizations total $4.4 billion since March 2023, continuing AerCap's strong track record of capital return.

AerCap returned $2.6 billion to shareholders through the repurchase of 44.3 million shares during 2023, at an average price of $59.09 per share.

New $1 billion share repurchase program announced. Quarterly dividend increased to $0.27 per share.

The repurchase program reflects both financial strength and value discipline. When aircraft opportunities arise at attractive prices, AerCap deploys capital to fleet growth; when equity appears undervalued, the company buys back shares. This flexible capital allocation creates value regardless of market conditions.

X. Business Model Deep Dive: How Aircraft Leasing Actually Works

The Operating Lease Structure

AerCap operates primarily through operating leases—arrangements where the lessor (AerCap) retains ownership while the lessee (airline) uses the aircraft for a specified period. At lease end, the aircraft returns to AerCap for re-lease or sale.

The distinction from finance leases matters enormously. Finance leases transfer substantially all risks and rewards of ownership to the lessee; they're essentially installment purchases. Operating leases keep ownership risks with the lessor—which sounds disadvantageous until you recognize that these "risks" include residual value that well-managed lessors capture profitably.

Revenue Streams

Basic Lease Rents: The monthly payments airlines make for aircraft use. These represent the majority of revenue and provide predictable cash flows.

Maintenance Reserves: Airlines pay monthly amounts into maintenance reserves that accumulate toward major maintenance events (engine overhauls, structural checks). When maintenance occurs, these reserves fund the work.

Asset Sales: Best-in-class trading platform with deep market insight and relationships: over the past four years AerCap and GECAS have sold on average over $5 billion of assets per year. AerCap actively trades aircraft, selling older or less desirable aircraft while acquiring newer models. The gains on these sales contribute meaningfully to earnings.

Engine Leasing: The GECAS acquisition brought a substantial engine leasing business. Engines can be leased separately from aircraft, providing flexibility for airlines facing maintenance events or capacity constraints.

The Order Book Advantage

AerCap's relationship with Boeing and Airbus provides structural advantages impossible for smaller competitors to replicate.

The combined company will be the largest customer of Airbus and Boeing.

As the largest customer, AerCap commands pricing unavailable to smaller buyers. Production slots—the right to take delivery of aircraft at specified future dates—represent locked-in cost bases when aircraft prices subsequently rise. The order book isn't merely future revenue; it's embedded value that generates returns for years.

Active Portfolio Management

AerCap doesn't simply hold aircraft passively—it actively manages the portfolio, selling aircraft when prices are favorable, redeploying capital to higher-returning opportunities, and constantly optimizing the fleet's composition.

Net gain on sale of assets for the fourth quarter of 2024 was $260 million, relating to 40 assets sold for $869 million. The increase was primarily due to the volume and composition of asset sales in the current strong sales market.

The $260 million quarterly gain on $869 million in sales represents a 30% margin—extraordinary for asset disposition and reflective of aircraft acquired at favorable prices years earlier.

Financing Strategy

AerCap funds its fleet through diverse sources: unsecured bonds, secured loans, bank facilities, and equity. Investment-grade credit ratings from Moody's (Baa1) and S&P (BBB+) enable efficient unsecured borrowing—critical because unsecured debt provides operational flexibility that secured financing lacks.

AerCap received credit rating upgrades from Moody's and S&P reflecting the company's best-in-class performance.

The rating upgrades lower borrowing costs industry-wide. A few basis points of interest expense reduction on $40+ billion of debt translates to tens of millions in annual savings.

Narrow-body vs. Wide-body Strategy

Narrowbody aircraft represent approximately 60% of the combined aircraft fleet.

The narrow-body focus reflects both customer demand and risk management. Single-aisle aircraft like the A320neo and 737 MAX serve the largest, fastest-growing segment of aviation: short-to-medium-haul routes. They're easier to place with multiple airlines, hold values more predictably, and generate higher returns than wide-body aircraft whose markets are more cyclical and concentrated.

XI. Competitive Landscape & Strategic Analysis

Industry Structure

The aviation asset management market exhibits moderate concentration. The top five lessors—AerCap, Avolon, SMBC Aviation Capital, Air Lease Corporation, and BOC Aviation—control about 55% of the global leased fleet, yet consolidation continues as scale proves critical to winning mega-orders and securing low-cost funding.

With a total fleet size of 1,676, AerCap has over 900 more aircraft than its next nearest competitor, SMBC. Japanese by ownership but based in Ireland, SMBC has a sizable fleet of 761 aircraft with a strong focus on the narrowbody side.

AerCap's scale advantage is enormous—more than double the next competitor by fleet size. This gap creates structural advantages in purchasing power, financing costs, and customer relationships that competitors cannot easily close.

Porter's Five Forces Analysis

1. Threat of New Entrants: LOW

The barriers to entry in aircraft leasing are formidable. New entrants would require: - Billions of dollars in capital - Decades of OEM relationships to access favorable order book positions - Credit ratings that take years to earn - Airline relationships built through economic cycles - Technical expertise in aircraft valuation and maintenance

Chinese lessors like ICBC Leasing and CDB Aviation have made inroads, backed by state capital. But even they struggle to replicate the institutional knowledge that AerCap has accumulated over fifty years.

2. Bargaining Power of Suppliers (Boeing/Airbus): MODERATE-HIGH

The commercial aircraft manufacturing duopoly—Boeing and Airbus control essentially the entire market—would seem to give suppliers enormous power. However, AerCap's position as their largest customer provides countervailing leverage. The combined company will be the largest customer of Airbus and Boeing.

Production constraints have shifted leverage toward those holding existing order book positions. AerCap's backlog of hundreds of aircraft represents locked-in access that cannot be replicated at any price.

3. Bargaining Power of Buyers (Airlines): MODERATE

Airlines need fleet flexibility, particularly post-COVID as demand patterns remain uncertain. Many airlines are capital-constrained and prefer leasing to ownership. However, large flag carriers can negotiate hard, and the lease market remains competitive enough that airlines have alternatives.

4. Threat of Substitutes: LOW

Aircraft ownership is the only substitute for leasing, and the trend has moved decisively toward leasing for fifty years. Leasing is now the preferred option for airlines over buying, having risen from roughly 10 per cent of the total fleet in the 1970s to 58 per cent at the end of 2023.

Airlines increasingly recognize that aircraft ownership ties up capital better deployed in route development and customer experience.

5. Competitive Rivalry: MODERATE

Competition among lessors is real but rational. The industry's history of consolidation has reduced the number of meaningful competitors, and remaining players generally avoid value-destructive pricing wars. AerCap's scale advantages in procurement and financing create sustainable margin advantages.

Hamilton Helmer's 7 Powers Framework

Scale Economies: AerCap exhibits classic scale economies. Fixed costs (management, systems, regulatory compliance) spread over a larger fleet create cost advantages. Purchasing power with manufacturers amplifies these advantages.

Network Effects: Limited. Airlines don't choose lessors because other airlines use them.

Counter-Positioning: AerCap's acquisition-driven consolidation strategy represents counter-positioning—incumbent lessors couldn't easily replicate the ILFC and GECAS acquisitions without transforming their own business models.

Switching Costs: Moderate. Airlines face costs switching lessors mid-lease but can choose different lessors for new aircraft.

Branding: Limited consumer impact, but AerCap's reputation among airlines and capital markets provides meaningful advantage in deal-making.

Cornered Resource: AerCap's order book positions represent cornered resources. The production slots for A320neos and 737 MAXs were secured years ago at prices no competitor can match.

Process Power: AerCap's decades of institutional knowledge in aircraft trading, maintenance management, and airline credit assessment create process advantages difficult to replicate.

XII. Bull Case & Bear Case

The Bull Case

Structural Demand Growth: Global air traffic has grown 5%+ annually for decades, interrupted only by wars, pandemics, and financial crises—all of which proved temporary. Rising middle classes in Asia, Latin America, and Africa will drive continued growth. More passengers mean more aircraft; more aircraft mean more leasing revenue.

Supply Constraints: Boeing's production challenges and Airbus's backlog constraints have created aircraft shortages that benefit lessors holding existing inventory. Airlines cannot simply buy aircraft; they must lease from companies that ordered years ago. This supply/demand imbalance drives lease rates higher and extends fleet values.

Fleet Modernization Advantage: AerCap has transformed its fleet from approximately 6% new technology aircraft to approximately 74% new technology aircraft at the end of 2024. This positions AerCap perfectly for airlines seeking fuel-efficient aircraft to meet environmental regulations and reduce operating costs.

Capital Return: Management's aggressive share repurchase program creates value as the stock trades below intrinsic value. Buying shares at 5-6x earnings while returns on equity exceed 15% is mathematically accretive.

Insurance Recovery Upside: Ongoing litigation against insurers could yield additional recoveries beyond the $2.5 billion already collected.

The Bear Case

Interest Rate Sensitivity: Aircraft leasing is fundamentally a spread business—borrow at one rate, lease at another. Rising interest rates compress margins unless lease rates rise correspondingly.

Geopolitical Risk: Russia demonstrated that aircraft can be seized by hostile governments. Similar events in China (where AerCap has substantial exposure) or elsewhere could inflict significant losses.

Cycle Risk: Aviation is cyclical. Recessions reduce travel demand, weakening airline credit quality and aircraft values simultaneously.

Boeing Dependency: AerCap's order book includes substantial Boeing commitments. Boeing's ongoing production and quality challenges create delivery uncertainty and potential value impairment.

Concentration Risk: While diversified across airlines, AerCap remains concentrated in commercial aviation. Alternative transportation technologies (high-speed rail, remote work reducing business travel) could dampen long-term demand growth.

XIII. Key Performance Indicators to Monitor

For investors tracking AerCap's ongoing performance, three KPIs matter most:

1. Fleet Utilization Rate

Currently at 99%, fleet utilization measures the percentage of aircraft on lease. Declining utilization signals either aircraft oversupply, deteriorating airline credit quality, or fleet age/composition problems. Sustained high utilization confirms demand for AerCap's aircraft remains robust.

2. Gain on Sale Margin

The margin on aircraft sales reflects both historical purchase pricing and current market conditions. Net gain on sale of assets for the fourth quarter of 2024 was $260 million on $869 million in sales—a 30% margin indicating strong market conditions and favorable cost basis. Declining margins would suggest either aircraft oversupply or earlier purchases at unfavorable prices.

3. Book Value Per Share Growth

Book value per share of $83.81 as of December 31, 2023, an increase of approximately 25% from December 31, 2022. Book value growth reflects the accumulation of retained earnings plus any unrealized gains in aircraft values. Combined with share repurchases reducing share count, book value per share growth captures AerCap's fundamental value creation.

XIV. Looking Forward

AerCap enters 2025 from a position of remarkable strength. The company has transformed itself from GPA's remains into the industry's undisputed leader through two of the largest transactions in aviation history. It has navigated a pandemic that threatened aviation's existence and a geopolitical crisis that saw billions in assets seized. Through it all, AerCap has delivered growing earnings, record cash flows, and substantial shareholder returns.

The industry continues to plan for a lower for longer supply environment, evidenced by continued increases in lease rates, lease extension demand and strong gain on sale. 2024 was the third year in a row of increased extension activity reflective of this ongoing demand for aircraft.

The structural tailwinds—aircraft supply shortages, growing global air travel demand, airline preference for leasing over ownership—remain firmly in place. AerCap's competitive advantages—scale, fleet quality, financing efficiency, institutional knowledge—remain intact.

Yet questions persist. Can AerCap maintain discipline as it becomes ever larger? Will geopolitical fragmentation create new Russia-style risks? How will the company navigate the aviation industry's eventual decarbonization transition?

What remains clear is that AerCap has earned its position as aviation leasing's 800-pound gorilla—not through luck or timing but through fifty years of accumulated expertise, disciplined capital allocation, and strategic vision that repeatedly saw opportunities others missed. The Shannon office where Tony Ryan mortgaged his house to buy a 10% stake in an industry that didn't yet exist has become something he could scarcely have imagined: the epicenter of an industry worth hundreds of billions, managed from Dublin by professionals who trace their intellectual lineage directly back to that single Boeing 747 that Aer Lingus couldn't use.

The story continues—but the first fifty years have been remarkable indeed.

Key Financial Summary (FY 2024)

| Metric | Value |

|---|---|

| Total Revenue | $8.0 billion |

| Net Income | $2.1 billion |

| Adjusted EPS | $12.01 |

| Operating Cash Flow | $5.6 billion |

| Fleet Utilization | 99% |

| Book Value Per Share | ~$95 (estimated) |

| Share Repurchases (2023-24) | ~$4 billion |

| Total Assets | $74+ billion |

| Aircraft Owned | 1,543 |

| Engines Owned | 900+ |

| Helicopters Owned | 300+ |

This analysis is for informational purposes only and does not constitute investment advice. Investors should conduct their own due diligence before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube