Acerinox: The Quiet Spanish Champion of Global Stainless Steel

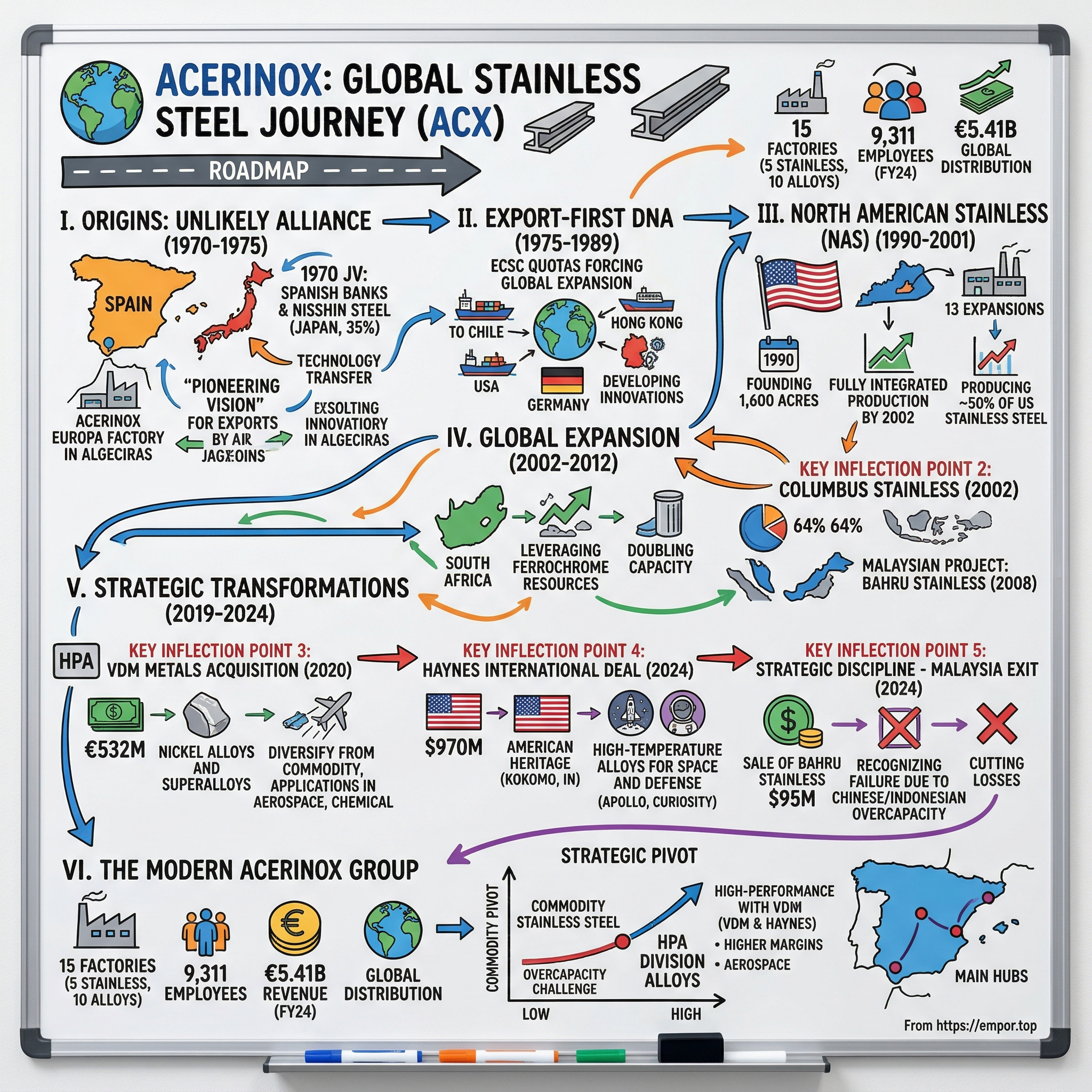

I. Introduction & Episode Roadmap

Picture the southernmost tip of Spain in 1970—the Campo de Gibraltar, where the Mediterranean meets the Atlantic, and Franco's Spain was cautiously opening its industrial doors to foreign investment. In this unlikely setting, a small group of Spanish engineers and bankers was about to forge a partnership that would quietly reshape the global stainless steel industry for the next five decades.

Acerinox was established on September 30, 1970, in Madrid, Spain, through a joint venture between Spanish banking and industrial groups—primarily led by Banco Español de Crédito (Banesto)—and Japan's Nisshin Steel Co., which provided 35% of the initial capital alongside 65% Spanish investment. What began as a technology transfer arrangement in a peripheral European economy has evolved into something far more consequential: the Acerinox Group is now the global leader in the manufacture of stainless steel and high-performance alloys, with a melting shop capacity of 3.5 million tons.

The numbers tell a remarkable story. As of 2024, Acerinox employs approximately 9,311 people and reported annual revenue of €5.41 billion for the fiscal year. The firm manages 15 factories globally, with five focused on stainless steel and ten on high-performance alloys, complemented by service centers and warehouses to support distribution.

The central question of this analysis is deceptively simple: How did a Spanish-Japanese joint venture built during the Franco era become a global stainless steel powerhouse, and—more critically—is the company's strategic pivot toward high-performance alloys positioning it for the next fifty years of leadership?

The answer lies in understanding five key inflection points in Acerinox's history: the American beachhead through North American Stainless (NAS), the four-continent strategy via Columbus Stainless in South Africa, the transformational VDM Metals acquisition in 2020, the 2024 Haynes International deal that completed the high-performance alloys platform, and—perhaps most instructive—the disciplined exit from Malaysia that demonstrated management's willingness to cut losses when a strategic thesis proves wrong.

These episodes reveal a company with a distinctive strategic playbook: technology transfer mastery, regional production to avoid trade barriers, ruthless capital discipline, and a willingness to transform its business model when commodity dynamics shift against it.

II. Origins: The Unlikely Spanish-Japanese Alliance (1970-1975)

The story of Acerinox begins not in a boardroom, but on a commercial airline somewhere between Tokyo and Madrid in the late 1960s. Internationalization has long formed an essential part of the seed which ultimately grew into Acerinox. In the late 1960s, a small group of engineers and entrepreneurs entered into discussion with the Japanese Nisshin Steel and Nissho Iwai companies to negotiate the founding contracts of the Spanish Stainless Steel Manufacturing Company, based in Spain and currently known as Acerinox.

To understand why this partnership mattered, one must grasp the state of stainless steel production in 1960s Spain: it barely existed. In the mid 1960s, in the peripheral and backward country of Southern Europe which was then Spain, there were a few industrial engineers willing to participate in entrepreneurial projects. Production of this special type of steels had started in Germany, France, Italy, Japan, and above all the United States, before World War II, but it was only after the war when other countries in the world started rapid consumption, and production. Machinery in the food industry, the chemical industry, or the construction and carmaking industries, increasingly appreciated this kind of steels that resisted the erosion produced by chemical elements.

The partnership agreement was formalized on April 21, 1970, in Tokyo, aiming to leverage Japanese technical expertise in stainless steel production to meet growing European demand amid Spain's economic liberalization under the Franco regime. This collaboration addressed Spain's prior reliance on imports for stainless steel, introducing advanced melting and rolling technologies previously absent in the domestic market.

The site selection was equally strategic. The company's inaugural facility, Acerinox Europa, was constructed in Palmones near Algeciras in Cádiz province, with groundbreaking in 1970; this site was selected for its proximity to the Strait of Gibraltar, facilitating raw material imports and exports. This wasn't merely geographic convenience—it was a statement of intent about where the company's future customers would be located.

What made this partnership extraordinary was its ambition. In 1970 the first stone was laid of what, within a few years, was to become the first Acerinox Europa factory, in Palmones, Algeciras. It was designed to produce ten times more stainless steel than the total amount consumed in Spain that year. The above clearly shows to what extent Acerinox was founded with an eye cast on foreign markets, with a focus predominantly on exports.

Think about that for a moment: building capacity ten times larger than domestic consumption in a country that had never produced stainless steel at scale. At that time, a business plan so dependent on other markets and such a distinctive vision as a global company were not just ground-breaking concepts; they also entailed a great risk in a field such as the steel industry, which requires significant investments of time and money and whose returns are almost always visible only in the long term. Acerinox remains a pioneering company in our country, a pacesetter in the internationalization process.

This corporation has been the only successful joint venture with Japanese investors in the steel industries in Europe. Why did it succeed where others failed? The academic literature points to three factors: genuine technology transfer from Nisshin, not just licensing; cultural exchange that allowed Spanish engineers to spend extended periods at Nisshin's Shunan facility in Japan; and patient capital from Banesto that didn't demand immediate returns.

Nisshin Steel has been a shareholder in Acerinox, an integrated Spanish stainless steel maker with production bases in the U.S. and South Africa, since 1970. The Japanese partner's commitment has never wavered. In 2009, Nisshin increased its ownership in the company from 11.3% to 15.0%.

This origin story matters because it established the DNA that would guide Acerinox for the next half-century: export orientation from day one, technology acquisition through partnership rather than acquisition, and a willingness to bet big on distant markets.

III. Building the Machine: Early Expansion & Export-First DNA (1975-1989)

Adversity, it turns out, was the making of Acerinox. Just as the Campo de Gibraltar factory was ramping production, Europe slammed the door on exactly the kind of export-driven strategy the company had envisioned.

Acerinox managed to adapt to survive while it was still in the making. In the early 1970s, when Acerinox Europa began increasing its production capacity, the European Coal and Steel Community (ECSC) imposed severe export quotas on European producers. These were limits which could not be exceeded, at the risk of significant fines. Since there were considerable drawbacks for selling its product in Europe, the company looked to other markets to find outlets for its steel.

What seems like a crisis in retrospect became the foundation of Acerinox's competitive advantage. Rather than lobby for quota relief or scale back ambitions, management did something counterintuitive: they went further afield, faster. Thus, by 1980 Acerinox was already operating in five countries on three continents (Spain, France, Chile, Argentina and Hong Kong), from which it supplied customers in more than 20 countries. The offices in Germany and the United States were added shortly afterwards.

This was export-first DNA hardwired into the company's operating system before many competitors had even considered international markets. The ECSC quotas, designed to protect European producers from each other, inadvertently created a Spanish company with the most globally diversified customer base of any European stainless steel manufacturer.

From its constitution, Acerinox has carried out a continuous program of investments, with development of own technological innovations that, in some cases, has constituted a true landmark in the technology of stainless steel. The company wasn't merely distributing product—it was developing proprietary processes that would give it cost advantages for decades.

By the late 1980s, the office in New Jersey that served U.S. customers would prove particularly consequential. American customers were experiencing firsthand the quality and reliability of Acerinox product. Management saw an opportunity: why ship steel across the Atlantic when you could make it in America, for Americans, at American prices?

IV. The American Beachhead: North American Stainless (1990-2001)

KEY INFLECTION POINT #1

In the rolling hills of rural Kentucky, about an hour northeast of Louisville, sits one of the most consequential industrial investments any Spanish company has ever made in the United States. Founded in 1990, North American Stainless (NAS) has undertaken several phases of expansion to become the largest, fully integrated stainless steel producer in the U.S.

NAS is situated on 1,600 acres in Carroll County. Founded in 1990, NAS has become the largest, fully integrated stainless steel producer in the United States and remains focused on being the leading producer of high-quality stainless steel in the Western Hemisphere.

The strategic logic was elegant: the New Jersey sales office had given Acerinox intimate knowledge of American demand patterns, but shipping steel from Spain to the U.S. meant vulnerability to trade barriers, currency fluctuations, and logistics costs. Building a world-class facility on American soil eliminated all three problems.

The site selection criteria reveal management's long-term thinking. Carroll County offered proximity to the Ohio River for waterborne transport, access to steel scrap markets for electric arc furnace operations, a workforce with manufacturing heritage, and—critically—state and local governments eager for industrial investment.

Carroll County Judge/Executive David Wilhoite spoke on the economic impact NAS has had on the county: "Investing over $3 billion in the local community and creating over 1,500 jobs for the region, North American Stainless is a cornerstone of Carroll County and the Commonwealth of Kentucky."

Since opening in 1990, this is NAS' 13th major expansion. That statistic alone tells the story of Acerinox's American commitment—not a one-time investment, but a continuous program of capacity additions that has transformed a greenfield site into the dominant player in the world's largest economy.

Acerinox is one of the world's largest companies, with a 6% share of production, and it owns three factories with an integrated process for the production of flat products: Campo de Gibraltar (Spain, 1970), the first to exceed one million tonnes per year (2001), North American Stainless, N.A.S. (Kentucky, USA, 1990), also fully integrated since February 2002.

The investment thesis proved prophetic. Acerinox CEO Bernardo Velázquez says, adding that the decision "reinforces our leadership in the American market and our commitment to this factory, one of the most efficient in the world. We are proud to produce in NAS about 50% of the country's stainless steel."

Half of all stainless steel cast in the United States comes from a Spanish-owned facility in rural Kentucky. That's not just market share—it's strategic dominance in the world's most important steel market.

The NAS investment also created something invaluable: options. Having a fully integrated American facility meant that regardless of trade policy—Section 232 tariffs, anti-dumping duties, whatever Brussels and Washington might negotiate—Acerinox would have American capacity serving American customers with American labor.

V. Going Global: Columbus Stainless & The Four-Continent Strategy (2002-2012)

KEY INFLECTION POINT #2

If NAS represented mastering the world's largest developed market, Columbus Stainless represented something different: controlling a strategic position in an emerging continent with unique raw material advantages.

Columbus Stainless, part of the Acerinox Group, a global player in the stainless and high performance alloys market, has been a trusted manufacturer and provider since 1964. But it wasn't until Acerinox arrived that Columbus reached its potential.

On 1 January 2002 Acerinox, SA (Spain) acquired a 64% shareholding in Columbus Stainless (Pty) Ltd. The South-African company to which has been transferred the assets related to the production of stainless steel flat products of the old Joint Venture Columbus, was acquired by Acerinox for 232 million €. The Acerinox Group, with this operation, became the third worldwide producer of stainless steel with a production capacity of 2.5 million tons.

The strategic logic went beyond scale. The acquisition enabled Acerinox to leverage South Africa's ferrochrome resources for cost advantages in raw material sourcing while expanding market access to emerging African and export-oriented demand. Stainless steel requires chromium, and South Africa has some of the world's richest chrome deposits.

Acerinox, S.A. has acquired the 12% shareholding of Highveld Steel & Vanadium Corp. Ltd. in the South African company Columbus Stainless. After said transaction, Acerinox, S.A. shareholding in Columbus Stainless rises to 76%. After Columbus melt-shop revamping, carried out last month of April, its annual capacity has risen to one million tons, which means twice the production achieved in 2001, the year before to Acerinox entry in Columbus.

Doubling capacity within a few years of acquisition—that's the Acerinox operational playbook in action. Not financial engineering, but industrial transformation.

With the Malaysian project announcement in 2008, the four-continent strategy was complete: Long-time venture partners Acerinox SA and Nisshin Steel announce they will build a new integrated stainless steel production plant in Malaysia. Acerinox SA and Nisshin Steel announced they will build a new stainless steel production plant in Malaysia. Their decision follows a full-scale feasibility study and consideration of various alternatives.

It will have a melting capacity of 1 million tonnes/year and 600,000 tonnes/year of cold rolled production. The estimated total investment amounts to $1,500 million USD. The facility is to be located in Johor Bahru, Malaysia, which is close to the sea.

It was agreed to develop it in phases with a constant process of implementation of production lines and, following a thorough feasibility study in which other alternatives were included, the construction of an integrated production plant took place in Johor Bahru (Malaysia). The land acquired, covering 140 hectares, has direct access to the sea and is situated in the Straits of Johor (one of the busiest routes in the world), opposite Singapore and a strategic location of enormous value for distribution and commercial work.

The thesis seemed unassailable: Asia was consuming an ever-larger share of global stainless steel, and proximity to Indonesia, China, India, and Southeast Asia would provide cost and service advantages. What management couldn't foresee was just how dramatically Chinese and Indonesian overcapacity would reshape global stainless steel economics—a lesson that would prove expensive.

VI. The High-Performance Alloys Pivot: VDM Metals Acquisition (2019-2020)

KEY INFLECTION POINT #3 – STRATEGIC TRANSFORMATION

By 2019, Acerinox management had arrived at an uncomfortable truth: the stainless steel business they had spent five decades building was structurally challenged. Chinese overcapacity wasn't a cyclical phenomenon—it was a permanent feature of the global market. Indonesian production, subsidized and sitting atop the world's largest nickel reserves, was flooding Asian markets. The commodity stainless steel business faced chronic oversupply.

The answer wasn't retreat. It was transformation.

Acerinox, S.A., a global leading stainless steel manufacturer with headquarters in Spain, has reached an agreement for the acquisition from Lindsay Goldberg Vogel GmbH and Falcon Metals BV of VDM Metals Holding GmbH ("VDM Metals"), with headquarters in Germany and leader producer of specialty alloys. With this deal, the Acerinox Group is looking to diversify into higher value added sectors. VDM Metals represents a great opportunity for Acerinox to grow into new markets and growing sectors such as aerospace, chemical industry, medical industry, oil and gas and renewable energies, water treatment and emissions control.

The deal concluded in the acquisition agreement valued at €532 million. Acerinox will pay €310 million and will assume debt for an amount of €57 million and pension plans and other liabilities for an amount of €165 million.

The valuation metrics tell the story of disciplined acquisition: The transaction is valued at €532 million, of which Acerinox disbursed €310 million yesterday, assuming debts of €57 million, giving rise to a valuation of 5.5 times EBITDA before synergies.

VDM Metals brought something Acerinox had never possessed: deep expertise in nickel-based superalloys and high-alloyed special stainless steels for the most demanding applications. VDM Metals Group based in Werdohl, Germany, is a manufacturer of corrosion-resistant, heat-resistant and high-temperature nickel alloys, cobalt and zirconium alloys as well as high-alloyed special stainless steels. These materials are used in the chemical process industry, the oil and gas industry, aerospace, automotive and electronics / electrical engineering. VDM Metals operates production sites in Germany (Altena, Siegen, Unna and Werdohl) and the United States (Florham Park, NJ, and Reno, NV).

The history of VDM is itself remarkable. The original Vereinigte Deutsche Metallwerke AG (VDM) was founded in 1930 by the takeover of Heddernheimer Kupferwerk and Süddeutsche Kabelwerk AG in Frankfurt by Berg-Heckmann-Selve AG in Altena. The merger took place on the initiative of Metallgesellschaft, which was the main shareholder of Heddernheimer Kupferwerke since 1893 and also took over the majority of the new corporate group.

The nickel alloys segment proved to be an exception. Since the mid-seventies, VDM has successfully focused on the development and production of these alloys. From the outset, Metallgesellschaft had its own very successful metal laboratory for materials research and product development. In 1972, the melting shop for nickel alloys and special alloys opened its doors in Unna, where it still operates today. For VDM, developing its own nickel alloys and concentrating on its core competence of melting and casting provided the opportunity to grow into a leading specialised supplier selling worldwide.

The incorporation of VDM Metals into the Acerinox Group will increase net sales and EBITDA by more than 20 percent.

The timing proved fortuitous. "In the circumstances we are currently living, this acquisition makes more sense than ever, since it diversifies our risk, adds a business line and establishes a strategy that we believe will be successful, in addition to strengthening the group's competitiveness and robustness. Furthermore, the cash generation and decrease in debt recognised last year leaves us in an optimal situation for taking on this challenge," stated Bernardo Velázquez, CEO of Acerinox.

The deal closed in March 2020—just as COVID-19 was reshaping global supply chains. In March 2020, it acquired VDM Metals for €532 million. What looked like unfortunate timing proved strategic: the pandemic accelerated reshoring trends and highlighted supply chain vulnerabilities in specialty materials, both of which favored VDM's positioning.

VII. The Haynes Deal & Full Transformation (2024)

KEY INFLECTION POINT #4 – COMPLETING THE HPA PLATFORM

If VDM Metals was the opening move in Acerinox's high-performance alloys strategy, Haynes International was the move that completed the transformation.

Acerinox, a leading global company in the manufacturing and distribution of stainless steel and high-performance alloys, has completed today, through its wholly owned U.S. subsidiary – North American Stainless ("NAS") – the acquisition of Haynes International ("Haynes"), a U.S. leading manufacturer and marketer of technologically advanced high-performance alloys.

Under the terms of the agreement, Acerinox will acquire all the outstanding shares of Haynes for $61.00 per share in cash, which represents a fully diluted equity value of $798 million, and a premium of approximately 22% to Haynes's six-month volume-weighted average share price for the period ending February 2, 2024. The all-cash transaction values Haynes at an enterprise value of approximately $970 million.

Haynes brought something VDM couldn't: over a century of American heritage in the most advanced alloys. Formed in Kokomo, Indiana in October 1912, the more than 100-year history of Haynes' continuous operation also captures the historic growth of many well-known nickel- and cobalt-base superalloy families.

Haynes International, Inc., a subsidiary of Acerinox headquartered in Kokomo, Indiana, is one of the largest producers of corrosion-resistant and high-temperature alloys. In addition to Kokomo, Haynes has manufacturing facilities in Arcadia, Louisiana, Laporte, Indiana, and Mountain Home, North Carolina. The Kokomo facility specializes in flat products, the Arcadia facility in tubular products, and the Mountain Home facility in wire products.

The founder's story adds color. Elwood Haynes moved to Kokomo in December of 1892 and found time to work on his horseless carriage. His first automobile, the "Pioneer," was successfully tested on July 4, 1894. While there is some dispute as to whom the honor of the first automobile in the United States should go, the success of the Pioneer led Haynes to form an automobile company. A tireless inventor, Haynes was in search of a material that would resist tarnishing and be suitable for cutlery. After several years of unsuccessful experiments, he developed viable alloys in 1907.

Alloys invented and produced throughout our history have flown on every Apollo and space shuttle flight and can be found in most rocket parts used in satellite launches today, as well as the "Curiosity" Mission to Mars and the latest Mars 2020 Perseverance Mission.

The investment commitment signals Acerinox's conviction: Acerinox will invest approximately $200 million over the next four years in the newly combined U.S. business, mostly in Haynes's operations in Kokomo, to create an integrated high-performance alloy and stainless-steel platform.

Additional transaction highlights, as previously announced during February of this year: Offers estimated annual synergies of $71 million.

Together, Haynes and VDM Metals will form Acerinox's High-Performance Alloys (HPA) Division. The integration of Haynes will support Acerinox's strategic priorities, including the company's focus on enhancing its operations in the U.S. market, high-performance alloys, and the aerospace sector.

"For over 113 years, Haynes has been at the forefront of the high-performance alloy industry, and today's announcement sets the foundation for our future, ensuring that we will be able to better serve our customers through increased capacity and an even broader portfolio of products, applications and services," said Michael L. Shor, President and Chief Executive Officer of Haynes. "We are excited to officially join the Acerinox family and know that the investment in our operations will drive growth for not just the Group, but our local communities."

The combined HPA Division now represents a formidable platform: The seven production centres (five in Germany and two in the US) combine the manufacture of high performance alloy products and solutions with a strong value added and a high R&D&I component, making it world leader in its sector.

VIII. The Malaysia Exit: Strategic Discipline (2024)

KEY INFLECTION POINT #5 – KNOWING WHEN TO FOLD

The Malaysia story offers perhaps the most instructive lesson in Acerinox's history—not because it succeeded, but because management recognized failure and acted decisively.

In 2024, the Group acquired Haynes International, a leading company in the high-performance alloys sector in the U.S. Additionally, a new organizational model has been implemented at the Campo de Gibraltar plant (Acerinox Europa), and the Group has ceased operations in Malaysia with the sale of Bahru Stainless. The Acerinox Group described the year 2024 as "transformational", marked by strategic decisions such as the sale of the Bahru Stainless plant, a difficult but necessary decision that responded to the overproduction in China and Indonesia and its impact on prices and profitability in Southeast Asia.

Bahru Stainless is Malaysia's sole producer of cold-rolled stainless steel and had ceased operations in May 2024. Worldwide Stainless Sdn Bhd has reached an agreement with Spain-based stainless steel leader Acerinox SA to acquire Bahru Stainless Sdn Bhd for a total consideration of US$95 million.

The original thesis made sense in 2008. Thus began the process to build the factory, from which Acerinox can supply one of the most populated areas in the world, whose countries have the highest current-day rates of growth. Malaysia, Indonesia, Vietnam, Mainland China, Korea, Laos, the Philippines, Thailand, Singapore and India are the major markets to which the Bahru products are sold.

USD 370 million has been invested so far. But Asian stainless steel economics shifted dramatically. Indonesian producers, backed by Chinese investment and sitting on the world's largest nickel reserves, flooded the market with product that Bahru couldn't match on cost.

Bahru Stainless, the Group's factory located in Johor (Malaysia), announced to its customers in May 2024 that it would cease operations. Strong Asian competition, some of it unfair, and market shifts hindered the development and profitability of this asset, which ceased to be strategic for the Group.

The sale proceeds were modest relative to the original investment: for a total sum of USD 95 million. But the decision freed capital and management attention for the Haynes acquisition, which offered far more attractive returns.

The sale of Bahru Stainless has resulted in an EBITDA income of EUR 146 million. This accounting gain—recognizing impairment losses already taken—allowed the transaction to actually contribute positively to 2024 results while removing a structurally challenged asset from the portfolio.

This is capital discipline in action. Many companies would have thrown good money after bad, hoping for a cyclical recovery. Acerinox recognized that the problem was structural, not cyclical, and redeployed resources toward higher-return opportunities.

IX. The NAS Expansion: Doubling Down on America (2023-2025)

While exiting Malaysia, Acerinox was simultaneously making its largest-ever commitment to its most profitable market.

North American Stainless will increase its production capacity by 200,000 tonnes, up by 20%. With this expansion, North American Stainless (NAS), the largest integrated stainless steel factory in the United States, will strengthen its position in the market for higher value-added products.

The new equipment planned with this $244 million investment will be aimed at increasing the volume of flat products, with a special focus on upping the production of those with greater value-added, such as BA (Bright Annealing) and special composition steels. NAS will have a new cold rolling mill, upgrade its annealing and pickling lines, and enlarge the melt shop to include a 400 metric tonne crane, among other equipment.

These investments will create 70 new jobs in addition to the factory's 1,600 employees and 500 local suppliers.

The timing relates directly to reshoring trends and concerns about supply chain resilience. The continued importation of subsidized stainless steel—and the accompanying national security threats—made the NAS expansion a pressing priority.

Acerinox CEO Bernardo Velázquez explained that this is "a strategic decision with which Acerinox will increase its positioning in the United States to accompany the expected growth in the American market." Mr Velázquez added that this decision "reinforces our leadership in the American market and our commitment to this factory, one of the most efficient in the world. We are proud to produce in NAS about 50% of the country's stainless steel".

NAS expects to complete the expansion by the end of 2025. The NAS expansion project is in its second year of implementation on time and budget: The melting shop expansion phase includes an extension of the building structure; this has already been delivered, pending installation. The components needed to modernize the annealing and pickling line have also been received. Regarding the new rolling and Skin-Pass mills, foundation and installation works are currently in progress.

The investment addresses not just capacity but product mix—shifting toward higher-margin specialty grades that command premium prices and face less competition from Asian imports.

X. The Chinese Overcapacity Challenge

No analysis of Acerinox's strategic positioning is complete without understanding the structural challenge that has reshaped global stainless steel economics.

China exported 110.7 million tons of steel in 2024, a 22.7% jump from the prior year and the highest number ever recorded. With weak demand at home, China's domestic steel consumption fell to a six-year low in 2024, pushing the steel industry to aggressively court foreign buyers with low-priced steel.

China's stainless steel exports totaled 5.04 million tonnes in 2024, according to data released by the General Administration of Customs (GACC) on January 20, higher by a huge 25.6% year-on-year and marking an all time high for China's exports of stainless steel. In December alone, the export volume reached 465,700 tonnes, up 6% from November and by a remarkable 38.8% compared with December 2023.

Despite the bottlenecks in shipping routes and container shortages, the United States sits on a large warehouse of subsidized imports of specific stainless steel grades from China and Southeast Asia. Overcapacity in those regions has been the main reason for several Asian countries targeting export destinations. Cold rolled overcapacity could exceed 4 million metric tonnes this year in China and 12 million metric tonnes globally, increasing by 2 million metric tonnes compared to 2023.

The Indonesian phenomenon is particularly relevant to Acerinox's Malaysia decision: The stainless steel industry has been particularly affected by the expansion of Chinese-owned steel production into Indonesia, which has the world's largest mining reserves of nickel, a key component in the production of stainless steel. In return for heavily subsidized Chinese steel investment into that country, the Indonesian government has banned the export of nickel ore, requiring that it be processed domestically in Indonesia. This Indonesian steel capacity is almost entirely intended for export, as stainless steelmaking capacity in Indonesia is currently nearly 27 times more than Indonesia's domestic demand for this product. Indeed, Indonesian exports of stainless steel have grown rapidly in recent years, from less than 70,000 metric tons in 2015 to over 4.7 million metric tons in 2022.

So far, Beijing has ordered the closure of 50 million tons of steel capacity this year to curb oversupply, with more cuts planned through 2030. Still, even if exports ease, they'll remain enormous by historical standards. Analysts at S&P Global expect China will ship on the order of 100 million tons of steel by the end of 2025.

This structural reality explains Acerinox's strategic pivot. In commodity stainless steel, competing with Chinese and Indonesian producers on cost is a losing proposition. The winners will be those who either enjoy tariff protection (hence NAS expansion) or who escape the commodity trap entirely (hence VDM and Haynes).

XI. Financial Performance & Current State

The numbers tell the story of a company in transition.

In this challenging geopolitical context, alongside supply chain incidents that affected trade routes, Acerinox achieved an EBITDA of 703 million in 2023. Net profit was 228 million euros and the revenue stood at 6,608 million.

EBITDA, 703 million euros, was the fourth best in our history. We reached a new profitability level, with a sales margin of 11%.

The 2024 results reflect the transition year: "EBITDA, EUR 500 million, was 29% lower than that of 2023, with a sales margin of 9%, and profit after tax and non-controlling interests amounted to EUR 225 million, just 1% lower than in 2023. The Group's revenue during the fiscal year amounted to EUR 5,413 million (18% lower than that of 2023)."

The decline requires context. After 2023, a year in which demand fell by around 20%, neither of the two markets experienced the expected recovery during 2024. Amid this situation, Acerinox managed to reaffirm its strong position and the success of its strategy.

The debt position reflects the Haynes acquisition: Net financial debt, at December 31, 2024, stood at EUR 1,120 million, an increase of EUR 779 million (EUR 341 million at December 31, 2023) due to the acquisition of Haynes International (EUR 841 million) and the debt payment prior to the sale of Bahru Stainless (EUR 60 million). Without these transactions, net financial debt would have been EUR 219 million.

The dividend commitment signals confidence: Shareholder remuneration has amounted to EUR 155 million in ordinary dividends. The interim dividend has been effected by way of a cash payment of EUR 0.62 per share, representing a 69% payout.

Looking at segment performance, the HPA division provides stability: EBITDA of the high-performance alloys division, EUR 117 million, was 33% lower than that of last year. The major differences with respect to 2023 were mainly due to the effect of raw materials, which were very positive last year and not so this year. The sales margin was 9% (12% in 2023).

XII. Competitive Positioning & Industry Structure

Porter's Five Forces Analysis

Threat of New Entrants: Low to Moderate Stainless steel manufacturing requires billion-dollar capital investments, specialized technical expertise, and decades of customer relationship development. The high-performance alloys segment is even more protected—customers require years of testing and certification before approving new suppliers for aerospace or chemical processing applications.

Supplier Power: Moderate Nickel, chromium, and molybdenum are traded commodities with multiple sources. However, Indonesia's nickel ore export ban has concentrated certain supply chains, and scrap availability varies by region. Acerinox's South African position provides some ferrochrome self-sufficiency.

Buyer Power: Moderate to High Large automotive, aerospace, and construction customers have significant negotiating leverage in commodity grades. However, specification lock-in and switching costs in high-performance alloys reduce buyer power in those segments.

Threat of Substitutes: Low For most applications, stainless steel and nickel alloys have no practical substitutes. Aluminum competes in some weight-sensitive applications, but corrosion resistance and temperature tolerance create durable demand.

Industry Rivalry: Intense in Commodity, Moderate in Specialty Chinese and Indonesian overcapacity has made commodity stainless steel brutally competitive. After Outokumpu acquired Inoxum, there were basically only three major players in Europe – Outokumpu, Acerinox and Aperam. High-performance alloys face less intense competition due to technical barriers and customer certification requirements.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Acerinox benefits from scale economies across its integrated facilities. NAS's 50% U.S. market share creates significant cost advantages.

Network Effects: Limited direct network effects, though the global service center network creates distribution advantages.

Counter-Positioning: The HPA pivot represents classic counter-positioning—moving toward segments where established competitors (Outokumpu, Aperam) have limited presence.

Switching Costs: Very high in aerospace and chemical processing applications where customer qualification processes take years.

Branding: Industrial commodities have limited branding power, but the HASTELLOY® and HAYNES® brands carry real value in specialty applications.

Cornered Resource: According to the 2011 South African Steel Producers Handbook, Acerinox Columbus Stainless sources most of their raw materials (including steel scrap, ferrochrome, and nickel) from South Africa. This ferrochrome access represents a modest cornered resource.

Process Power: Acerinox's manufacturing efficiency and operational expertise represent genuine process power, developed over 50+ years of continuous improvement.

XIII. Leadership & Governance

The current leadership team reflects Acerinox's promote-from-within culture.

Mr. Bernardo Velázquez Herreros, a Spanish citizen, and an Industrial Engineer from the Comillas Pontifical University (ICAI), is the CEO of Acerinox and has been a member of the company's Executive Committee since 2010. Since he joined Acerinox's Marketing Department in 1990, Mr. Velázquez has risen through successive positions of increasing responsibility within the company, gaining in-depth experience in the international stainless steel business. On his return to Spain after a tenure in Mexico and Australia, he held the positions of Assistant Managing Director, Chief Information Officer, and Head of Strategic Planning. In 2007, he was appointed as Managing Director, a position that he held until his appointment as CEO in July 2010.

Prior to this, he served as the managing Director of the company since 2007. Previously, he served as the Chairman of Bahru Stainless in Malaysia. He also served as the Chairman of the Stainless Steel Eurofer's Group. Currently he is serving as Chairman of North American Stainless (USA) and UNESID.

Velázquez's 35-year tenure within Acerinox provides deep institutional knowledge but also raises succession questions that long-tenured CEO arrangements inevitably create.

XIV. Bull & Bear Cases

The Bull Case

HPA Transformation Delivering Superior Returns: The combined VDM-Haynes platform creates the world's leading high-performance alloys division outside China. Aerospace supply chains are prioritizing Western suppliers, and decarbonization drives demand for specialized alloys in hydrogen, nuclear, and renewable energy applications. The ~$71 million in annual synergies from Haynes alone represents substantial value creation.

U.S. Market Dominance Provides Shelter: With 50% U.S. stainless steel market share and insulation from trade policy volatility, NAS generates consistent cash flows regardless of global commodity dynamics. The ongoing $244 million expansion positions NAS for share gains as reshoring accelerates.

Capital Discipline Proven: The Malaysia exit demonstrates management willingness to cut losses. The combination of HPA pivot, U.S. focus, and Malaysia disposal represents coherent capital allocation that deserves investor confidence.

Valuation Attractive: At current market capitalization, the company trades at modest multiples relative to the quality of assets and strategic positioning.

The Bear Case

Cyclical Exposure Remains: Despite the HPA pivot, stainless steel still represents the majority of revenues. A global recession would pressure volumes and margins across both segments simultaneously.

Chinese Overcapacity Structural: The 100+ million tons of Chinese steel exports annually may be permanent, not temporary. Acerinox's European operations face chronic pressure from Asian imports despite trade remedies.

Debt Elevated Post-Haynes: EUR 1.12 billion in net debt requires disciplined cash generation for deleveraging. A prolonged downturn could stress the balance sheet.

Concentration Risk in Leadership: CEO Velázquez has been with Acerinox since 1990 and CEO since 2010. Succession planning is a legitimate concern for a company of this scale and complexity.

Integration Execution Risk: Haynes integration is ongoing, and realizing $71 million in synergies requires flawless execution across different corporate cultures.

XV. Key Metrics to Watch

For investors tracking Acerinox, three KPIs matter most:

1. HPA Division EBITDA Margin This segment represents the strategic future. Tracking margin evolution—which stood at 9% in 2024 versus 12% in 2023—reveals whether the high-value strategy is translating to superior profitability. Look for margin expansion as Haynes synergies realize and product mix optimization progresses.

2. NAS Capacity Utilization and Market Share NAS is the cash cow. Monitoring U.S. market share (currently ~50%) and capacity utilization rates reveals whether the American franchise is defending its dominant position against import competition. The 200,000-ton capacity expansion completing in 2025 makes this metric particularly important going forward.

3. Net Debt / EBITDA Ratio With EUR 1.12 billion in net debt post-Haynes, deleveraging progress is critical. Management's target trajectory and actual performance against it will signal whether the capital allocation strategy is sustainable. Any material deviation warrants attention.

XVI. Conclusion: The Quiet Champion Thesis

Acerinox has spent fifty-five years building one of the world's most efficient stainless steel operations while staying largely under the radar of global investors. The company's Japanese-Spanish heritage, regional production strategy, and disciplined capital allocation have created a business uniquely positioned for the next era of industrial supply chains.

The strategic pivot toward high-performance alloys represents the most significant transformation in company history. If successful, Acerinox emerges as a leader in materials essential for aerospace, energy transition, and advanced manufacturing—segments with durable demand and pricing power that commodity stainless steel cannot offer.

The Malaysia exit demonstrates that management can recognize strategic mistakes and act decisively. The NAS expansion shows conviction in doubling down on winning positions. The Haynes acquisition completes the HPA platform with American heritage and aerospace certification that would take decades to replicate organically.

What remains is execution: integrating Haynes successfully, completing the NAS expansion on schedule, and navigating a global economy where Chinese overcapacity remains a permanent feature of commodity steel markets.

For investors seeking exposure to industrial transformation, supply chain resilience, and the materials enabling energy transition, Acerinox merits serious consideration. The quiet Spanish champion has built something durable—and the next chapter may be its most valuable yet.

Investment considerations should account for currency exposure (EUR-denominated company with USD and ZAR revenue streams), cyclical industry dynamics, and ongoing strategic execution requirements. The information presented reflects publicly available data and company disclosures through November 2025.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube