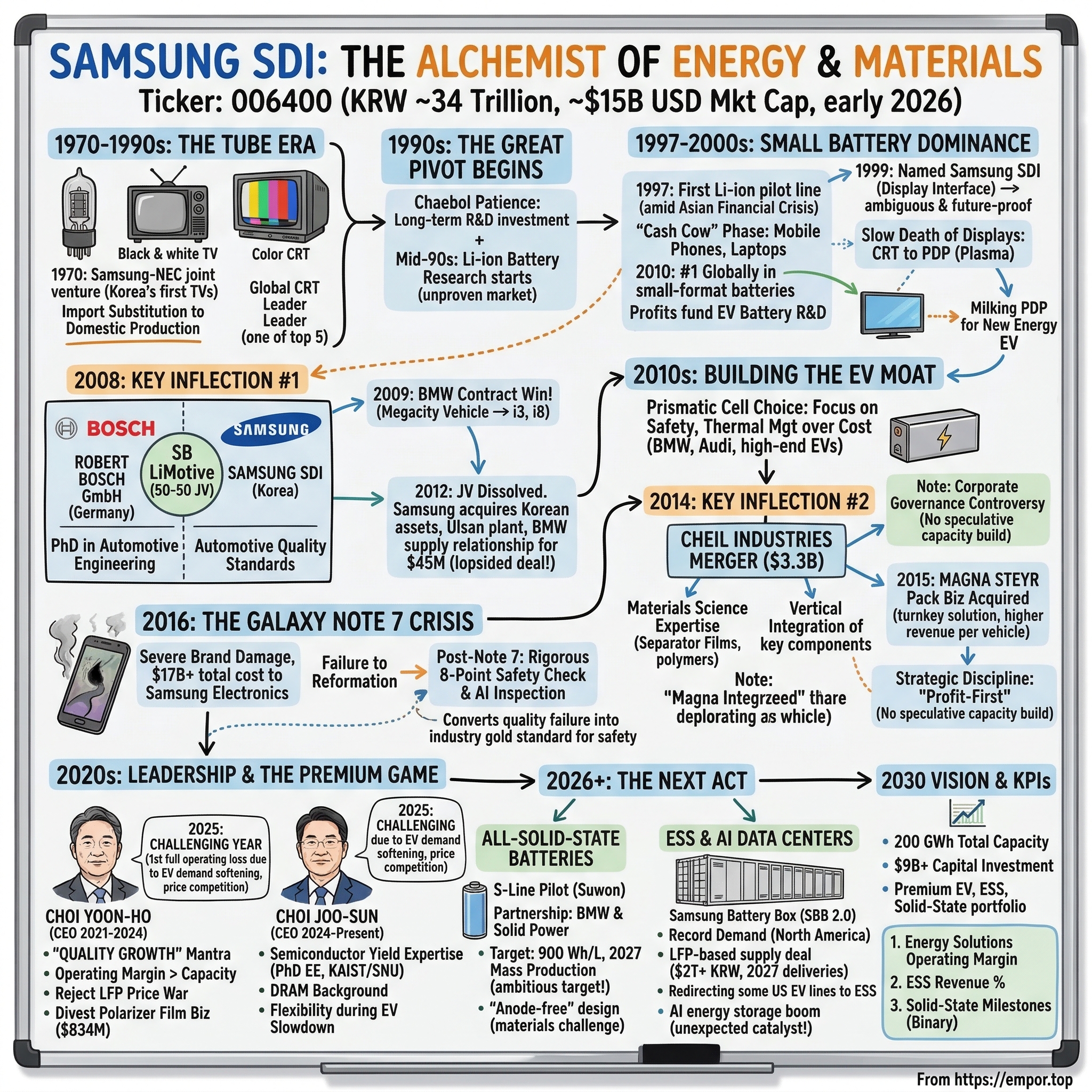

Samsung SDI: The Alchemist of Energy and Materials

I. Introduction: The Suwon to Solid-State Roadmap

Walk into the showroom of a BMW i7 at any dealership in Munich, and you will find one of the most luxurious electric sedans ever manufactured. Lift the floor, peer beneath the exquisite leather and hand-stitched wood trim, and there sits the beating heart of a one-hundred-and-five-kilowatt-hour battery pack. Every cell stamped with the name of a company that most western investors have never heard of: Samsung SDI.

Now zoom out. Travel halfway across the world to a sprawling semiconductor fabrication plant in Taiwan or Arizona. Inside the cleanroom, robotic arms polish silicon wafers to a near-atomic smoothness using a chemical-mechanical planarization slurry—a gritty liquid that functions like the world's most precise sandpaper. That slurry was also made by Samsung SDI.

This is a company that lives at the strange intersection of batteries and semiconductor materials, two of the most consequential supply chains on the planet. In early 2026, it trades at a market capitalization of roughly thirty-four trillion Korean won—about fifteen billion US dollars. That is a fraction of what CATL commands in Shenzhen or what LG Energy Solution fetches in Seoul. And yet, by certain measures, Samsung SDI has been the most profitable EV battery company on Earth for much of the past decade.

The central question is worth asking slowly: how did a company that started by making vacuum tubes for black-and-white televisions in 1970 survive the death of the cathode ray tube, the collapse of the plasma display panel, the global inferno of the Galaxy Note 7, and a savage EV demand slowdown—to remain standing as a credible contender for the solid-state battery crown?

The thesis is simple but counterintuitive. While its Korean rival LG Energy Solution pursued volume and its Chinese nemesis CATL pursued total domination, Samsung SDI pursued what its former leadership called "Quality Growth"—a conservative, engineering-first approach that prioritizes margins over market share.

Think of it as the difference between Walmart and Hermès. Both are wildly successful. But only one of them sleeps well when the economy softens.

To appreciate just how unusual this strategy is in the battery world, consider the competitive landscape. CATL, the Chinese juggernaut, held a staggering 45.2 percent of the global EV battery market in January 2026. BYD, another Chinese giant, held 13.8 percent. The three major Korean players—LG Energy Solution, SK On, and Samsung SDI—collectively held just twelve percent.

Samsung SDI alone ranked approximately tenth by installed capacity, shipping about 1.6 gigawatt-hours in January 2026, with its battery usage declining 24.4 percent year-on-year. These are not the numbers of a market leader. They are the numbers of a company that has made a deliberate, calculated choice about which game it wants to play.

This is a story that begins in a factory making cathode ray tubes for Korea's first televisions, passes through the Asian Financial Crisis, a transformative joint venture with Robert Bosch, the most expensive product recall in consumer electronics history, and a high-stakes merger that rewired the company's DNA.

It ends—or rather pauses—in a six-thousand-five-hundred-square-meter pilot line in Suwon, South Korea, where engineers are producing prototype all-solid-state battery cells that could leapfrog every lithium-ion chemistry on the market.

Along the way, we will unpack how Samsung SDI built a hidden cash machine in semiconductor materials, why it sold its polarizer film business for nearly a billion dollars, and what the AI data center boom means for a battery company that most people still associate with exploding smartphones.

Let us start at the beginning.

II. The Samsung Ecosystem: Why SDI Exists

To understand Samsung SDI, you first have to understand the Samsung Group itself. Samsung is not a company. It is an ecosystem—a constellation of interlocking entities that share a founding family, a corporate culture, and a borderline-obsessive commitment to vertical integration.

Samsung Electronics makes the chips and the phones. Samsung Display makes the screens. Samsung Electro-Mechanics makes the components. Samsung C&T builds the buildings they all work in. Samsung SDS runs the IT infrastructure. And Samsung SDI? It was created to make the parts that light up the screens.

This kind of structure has a name: the chaebol, Korea's distinctive form of family-controlled conglomerate. The chaebols—Samsung, Hyundai, SK, LG—were the engines of Korea's postwar economic miracle. They share certain characteristics: sprawling, diversified, vertically integrated, and governed by a founding family that wields influence far beyond its formal equity stake.

The Samsung Group is controlled by the Lee family, now in its third generation. Every major affiliate, including Samsung SDI, operates within a web of cross-shareholdings, shared R&D resources, and informal coordination that Western corporate governance experts view with a mixture of fascination and horror.

But for capital-intensive, long-cycle businesses like batteries, the chaebol structure has a specific and powerful advantage: patient capital. The willingness to invest for ten or fifteen years before seeing a return. The ability to absorb losses in one division because another division is printing money. The institutional stamina to maintain R&D spending through economic downturns when every instinct says to cut.

On January 20, 1970, Samsung-NEC Co., Ltd. was born as a joint venture between the Samsung Group and Japan's NEC Corporation. The strategic logic was pure import substitution. South Korea was in the early stages of its industrial miracle. Televisions were becoming a consumer staple, and every single cathode ray tube inside those TVs was being imported from Japan. The Korean government wanted domestic production. Samsung wanted vertical integration. NEC wanted a manufacturing partner in a lower-cost country. It was a marriage of convenience that worked brilliantly for decades.

The company's first factory produced vacuum tubes for black-and-white TV sets. By 1975, it had graduated to full color cathode ray tubes, and by the 1980s it was one of the largest CRT producers in Asia. In 1974 it was renamed Samsung Electron Device Inc., a title that better reflected its expanding portfolio.

For a quarter century, this was a perfectly fine business. Samsung's television division needed tubes. Samsung's monitor division needed tubes. And the world could not get enough of both. At its peak in the mid-1990s, Samsung SDI was one of the five largest CRT manufacturers on the planet, supplying not only Samsung's own consumer electronics divisions but also exporting to television and monitor makers across Asia, Europe, and the Americas.

In 1999, the company was renamed yet again—this time to Samsung SDI. The acronym originally stood for Samsung Display Interface, but it was deliberately chosen to be ambiguous enough to accommodate whatever the company might become next. That ambiguity was intentional. The Samsung Group has always treated its affiliates as platforms that can be repurposed, not as fixed businesses tied to a single product category.

Samsung SDI's name was designed to outlive its current identity. And that is exactly what happened.

The critical advantage—the one that made everything else possible—was chaebol patience. When Samsung SDI began investing in lithium-ion battery research in the mid-1990s, the technology was unproven. The market was nonexistent. The returns were a decade away.

No venture capitalist would have funded that timeline. No private equity firm would have tolerated a ten-year R&D burn before the first dollar of revenue. But the Samsung Group could afford to think in ten-year increments, because it was building an integrated supply chain where batteries would eventually complement semiconductors, displays, and consumer electronics. The losses in the battery division were, in a sense, an R&D expense for the entire Samsung ecosystem.

That patient capital would prove to be the single most important asset in Samsung SDI's history. Without it, there would have been no battery pilot line in 1997, no BMW contract in 2009, and no solid-state prototype in 2023.

The chaebol structure has its critics, and rightly so—particularly around governance, transparency, and the concentration of economic power. But for the specific challenge of incubating a battery business over two decades, it was the perfect incubator. And it set the stage for what was about to become the most consequential corporate pivot in Korean industrial history.

III. The Great Pivot: 1995 to 2010

Picture Seoul in the autumn of 1996. The Korean economy is booming. Samsung Electronics has just become the world's largest memory chip manufacturer. Samsung SDI's CRT business is printing money. Inside the executive suites, however, a small group of engineers and strategists is staring at something deeply unsettling: a flat panel display.

The cathode ray tube—that bulky glass bottle that had powered every television and computer monitor since the 1950s—was about to become obsolete. LCD technology was advancing faster than anyone had predicted, and every major display maker was racing to scale flat panels. For Samsung SDI, which had built its entire business around CRTs, this was not a gradual decline. It was an existential threat.

The question was not whether CRTs would die, but how fast—and what Samsung SDI would become when they did.

The answer arrived in November 1997, at precisely the worst possible moment. As the Asian Financial Crisis tore through South Korea, as the Korean won collapsed by nearly half, as the International Monetary Fund imposed brutal austerity conditions and the country's largest chaebols were forced into humiliating restructurings, Samsung SDI broke ground on its first lithium-ion battery pilot line at its factory in Cheonan—about ninety kilometers south of Seoul.

The timing seemed insane. The entire country was in a financial emergency. Companies were going bankrupt by the dozen. Banks were failing. Unemployment was skyrocketing. And here was Samsung SDI, pouring money into a technology that had no proven market demand outside of a few niche applications in camcorders and early laptops.

But the logic was impeccable, if you squinted hard enough. Samsung Electronics was about to explode in the mobile phone market. Every one of those phones needed a battery. Every one of those laptops needed a battery. If Samsung SDI could master lithium-ion chemistry, it would have a captive customer in its own corporate family and a potential global market that would dwarf anything CRTs had ever produced.

The pilot line was a bet that the future of Samsung SDI was not glass tubes but electrochemistry. And the crisis, paradoxically, made the bet easier: with the won cratered, labor costs in Korea were at historic lows, making it the cheapest possible moment to build a factory.

By July 2000, Samsung SDI had moved from pilot to mass production of lithium-ion cells. The timing was exquisite. The early 2000s saw an explosion in mobile devices—clamshell phones, MP3 players, digital cameras, and the first generation of slim laptops. Every one of those devices needed a small, high-energy-density rechargeable battery. Samsung SDI was ready to supply them.

By 2005, the company was one of the top three small-format battery makers in the world, competing neck-and-neck with Sony and Sanyo. By 2010, it was number one globally in batteries for laptops and mobile phones.

This was the "cash cow" phase—and it is worth dwelling on because it funded everything that came after. Small batteries are not glamorous. Nobody writes breathless articles about the battery inside a Dell laptop. But they are enormously profitable when you have scale and a captive customer base.

The margins on small-format lithium-ion cells were substantially higher than what EV batteries would later command, because the customers—consumer electronics companies—were less price-sensitive than automakers. Samsung SDI used the cash flows from its small battery business to fund something far more ambitious: electric vehicle batteries. Every quarter, money flowed from the small battery division into R&D labs where engineers were experimenting with larger-format cells, higher energy densities, and the kind of safety testing that automotive applications would demand.

Meanwhile, the company was also managing the slow death of its display businesses. After CRTs came Plasma Display Panels, or PDPs, which Samsung SDI invested in heavily during the early 2000s.

Plasma was a gorgeous technology—rich colors, deep blacks, excellent motion handling—and for a few years it looked like it might become the dominant flat-panel technology. But it was power-hungry and expensive compared to LCD. Samsung Display, SDI's sibling, was simultaneously scaling LCD technology at breathtaking speed. By 2008, it was clear that LCD had won the war. Samsung SDI found itself on the wrong side of an intra-Samsung technology battle.

What the company did next was disciplined and unsentimental. It extracted every last dollar of cash flow from its PDP operations—squeezing margins, reducing capital expenditure to maintenance levels only, and reinvesting every won of free cash flow into what it was now calling its "New Energy" division. The PDP business was formally wound down by 2014, but by then, the batteries had already taken over.

The PDP division did not die a sudden death. It was harvested—methodically and deliberately—to feed the next growth engine.

The lesson here is one that investors encounter repeatedly in the Samsung universe. These companies do not panic when a technology cycle turns against them. They manage the decline with surgical precision, milking the old business while funding the new one, and they do it with a time horizon that would give most Western fund managers an anxiety attack.

Samsung SDI spent fifteen years pivoting from tubes to batteries, and it did so profitably in almost every single quarter. That is the chaebol advantage in action: not just patient capital, but patient management.

There is a myth in the investment world that pivots are sudden. That companies "reinvent themselves overnight." The reality is far more mundane and far more instructive. Great pivots are managed over decades, funded by the very businesses they are designed to replace. Samsung SDI did not leap from CRTs to batteries. It built a bridge, one cash flow statement at a time, and walked across it at a deliberate pace. By the time the CRT and PDP businesses were fully wound down, the battery business was already self-sustaining.

It was this institutional stamina that gave them the confidence to enter the most demanding customer relationship in the automotive world.

IV. Key Inflection Number One: The Bosch Joint Venture and the BMW Marriage

In June 2008, two companies from opposite sides of the planet sat down to sign one of the most consequential joint ventures in the history of the automotive battery industry. One was Robert Bosch GmbH—the 130-year-old German engineering titan, the world's largest automotive supplier, a company so deeply embedded in the European car industry that practically every vehicle on the Autobahn contained dozens of its components.

The other was Samsung SDI—a Korean company that was very good at making laptop batteries but had never shipped a single cell for an electric vehicle.

The joint venture was called SB LiMotive. The deal was fifty-fifty. Headquarters in Suwon, with operations spanning Korea, Germany, and the United States. The stated goal was to develop, manufacture, and sell lithium-ion batteries for hybrid and electric vehicles.

For Samsung SDI, this was not just a business deal. It was a PhD program in automotive engineering.

To appreciate why this mattered so much, you have to understand the chasm between making a battery for a laptop and making a battery for a car. A laptop battery needs to last two to four years, power a device that sits on a desk, and survive being charged maybe five hundred times.

An automotive battery needs to last ten to fifteen years. It must operate in temperatures ranging from minus thirty to plus fifty degrees Celsius. It must survive thousands of charge-discharge cycles. It must withstand vibration and shock from road surfaces. And it absolutely, categorically, under no circumstances can catch fire in a vehicle traveling at highway speed with four passengers inside.

The testing regimes are different. The qualification timelines are different. The documentation requirements are different. The liability exposure is on an entirely different planet.

Bosch brought something that Samsung SDI could not have acquired any other way: intimate knowledge of what the European automotive industry actually requires from a battery supplier. Not just the chemistry, but the testing protocols, the quality certifications, the Failure Mode and Effects Analysis, the fourteen-month qualification cycles, the automotive quality management standards, the expectation that every single cell would perform identically across a ten-year, two-hundred-thousand-kilometer lifecycle.

Samsung SDI learned all of this inside the Bosch partnership, and the knowledge became permanently embedded in its engineering culture.

SB LiMotive formally started operations on September 1, 2008. Within a year, it achieved the most important customer win in Samsung SDI's history. In 2009, SB LiMotive won the contract to supply lithium-ion battery cells for BMW's "Megacity Vehicle" project—which would eventually become the BMW i3 and i8.

This was not just any contract. BMW was the most prestigious electric vehicle program in Europe, and it chose a Korean-German battery supplier over every Japanese and Chinese alternative. The Japanese incumbents—Panasonic and AESC—had deeper experience in automotive batteries. The Chinese manufacturers were cheaper. But BMW chose SB LiMotive because it offered Samsung's cell chemistry expertise combined with Bosch's automotive integration knowledge, wrapped in a quality management system that met German automotive standards.

For Samsung SDI, the BMW relationship would define its entire automotive battery strategy for the next fifteen years and counting.

Then, in September 2012, the joint venture was dissolved. Bosch and Samsung had grown in different strategic directions—Bosch increasingly skeptical about the near-term economics of EV batteries, and Samsung eager to control its own destiny. When SB LiMotive was disbanded, the assets were split. Bosch took the US and German operations. Samsung SDI took the Korean operations, including the manufacturing plant in Ulsan, and—crucially—retained the BMW supply relationship.

The reported buyout price was approximately forty-five million dollars. That number bears repeating. Forty-five million dollars. For context, that is roughly what it costs to build a single battery module assembly line today.

Samsung SDI walked away with four years of automotive-grade engineering knowledge, a fully operational manufacturing plant, and the BMW supply contract—all for what amounts to a rounding error in the battery industry's capital expenditure budgets. In hindsight, this was one of the most lopsided technology acquisitions of the decade.

The Bosch partnership also crystallized a critical strategic choice that would shape Samsung SDI's competitive identity for the next decade: cell format.

There are three main formats for automotive battery cells. Cylindrical cells—the kind Tesla uses—look like oversized AA batteries and are produced in enormous quantities at high speed. Pouch cells—favored by LG Energy Solution and SK Innovation—are flat and flexible, like metallic pillows, and can be shaped to fit irregular spaces. And prismatic cells are hard-cased rectangular blocks, like small metal bricks, with rigid aluminum or steel housings.

Samsung SDI chose prismatic. The reasoning was rooted in safety and thermal management. Prismatic cells have rigid metal casings that provide structural integrity and consistent pressure on the electrode stack. They are easier to cool uniformly because their flat surfaces allow efficient contact with cooling plates. They are harder to puncture, swell less during charging, and are simpler to assemble into modules because of their uniform, rigid shape.

They are also more expensive to manufacture than pouch cells—which is precisely why LG and SK chose pouch instead.

But Samsung SDI was not optimizing for cost. It was optimizing for the kind of customer that would pay a premium for safety and reliability. Customers like BMW. Customers like Audi. Customers who sell six-figure luxury vehicles and cannot tolerate a single battery-related recall.

BMW remained the anchor customer throughout this period—from the i3 in 2013 to the iX and i4 in the early 2020s to the electric 7 Series and the broader "Neue Klasse" platform. That kind of longevity in the automotive supply chain is rare and extraordinarily valuable.

Switching battery suppliers is not like switching paper clip vendors. It requires a complete redesign of the battery pack architecture, new crash testing, new thermal simulation, new integration with the battery management system, and new validation of the vehicle's entire safety certification. Once an automaker designs a platform around a specific cell format and supplier, they are locked in for a vehicle cycle of seven to ten years.

Samsung SDI understood this from the very beginning.

It is worth pausing here to reflect on what this relationship actually looks like in practice. Samsung SDI does not simply ship cells to BMW and wait for a purchase order. Its engineers are embedded in BMW's development process from the earliest stages of platform design. They collaborate on cell specifications, thermal management requirements, crash simulation parameters, and battery management system integration. The relationship is less like a supplier-customer transaction and more like a technology partnership—which is precisely why it endures.

This is the foundation of the company's most important competitive moat—one that would soon be reinforced by a marriage of a very different kind.

V. Key Inflection Number Two: The Cheil Industries Merger and Strategic M&A

If the Bosch joint venture was Samsung SDI's education in automotive engineering, the Cheil Industries merger was its graduate thesis in materials science.

On March 31, 2014, Samsung SDI announced it would acquire Cheil Industries through a stock swap valued at approximately three and a half trillion Korean won—roughly three point three billion dollars.

Cheil Industries was, to put it mildly, a strange company. It was the Samsung Group's chemical and materials arm, but its portfolio read like a corporate identity crisis: flame-retardant plastics, engineering polymers, semiconductor materials, artificial marble, golf course turf, and a fashion retail business that included the Bean Pole and 8 Seconds clothing brands.

On the surface, merging a battery company with a fashion conglomerate seemed bizarre—like combining a Formula One team with a perfume house. Which, come to think of it, is exactly what Ferrari does.

Beneath the surface, however, the logic was compelling. Batteries are ultimately a materials science game. The performance of a lithium-ion cell—its energy density, its cycle life, its safety profile—is determined by the quality of four critical components: the cathode material, the anode material, the electrolyte, and the separator.

To put this in layman's terms: a battery cell is like a sandwich. The cathode and anode are the bread. The electrolyte is the filling. And the separator is the thinnest, most critical layer—the one that prevents the entire thing from collapsing into a short circuit. The separator is often just twelve to twenty microns thick, about a fifth the width of a human hair.

Improving any one of these layers requires deep expertise in polymer chemistry, ceramic processing, and materials engineering. Cheil Industries had exactly that expertise. It produced separator films for batteries. It had R&D capabilities in specialty polymers and synthetic resins that were directly applicable to cathode and electrolyte development.

By absorbing Cheil's chemical expertise, Samsung SDI was vertically integrating the most critical upstream components of its battery business. The merger was completed on July 1, 2014, following shareholder approval.

Think of it as a winemaker acquiring its own vineyard. You cannot make great wine without great grapes, and you cannot make great batteries without great cathode materials.

It is worth noting that this merger also had a corporate governance dimension that investors should understand. The Cheil Industries–Samsung SDI merger was part of a broader restructuring of the Samsung Group's ownership structure, which included the subsequent merger of Cheil Industries with Samsung C&T in 2015. These transactions were controversial, with minority shareholders and activist investors arguing that the merger ratios undervalued certain entities to benefit the Lee family's control.

The controversy eventually contributed to the impeachment of South Korean President Park Geun-hye and the imprisonment of Samsung's de facto leader, Lee Jae-yong. These governance issues represent a material risk factor for any investor in Samsung-affiliated companies, and they have not been fully resolved to this day.

Setting aside the governance drama, the industrial logic of the merger proved sound. One year later, in February 2015, Samsung SDI made another surgical acquisition—purchasing the entire battery pack business from Magna Steyr, the Austrian operating unit of Magna International. The deal included all 264 employees, production and development sites in Austria, and existing contracts with European automakers. Exact financial terms were not publicly disclosed.

This was strategically significant because it transformed Samsung SDI's sales proposition. Until that point, SDI sold battery cells and modules—but automakers had to find someone else to assemble those cells into complete battery packs.

A battery pack is far more than cells stacked together. It includes the structural housing, the thermal management system with cooling plates and heating elements, the battery management system electronics, the high-voltage wiring harness, and the integration with the vehicle's crash structure. Many automakers prefer to buy this as a turnkey solution from a single supplier.

By acquiring Magna's pack business, Samsung SDI could walk into a meeting with Stellantis or BMW and say: "We will design, build, and deliver the complete battery system for your next EV platform." That is a fundamentally different sales proposition than "we make cells, and you figure out the rest." It also dramatically increased the revenue per vehicle, since a complete pack commands a much higher price than the cells alone. And it deepened the customer relationship, because pack-level integration creates even more switching costs than cell-level supply.

What is equally notable about Samsung SDI's capital deployment during this period is what it did not do. While the rest of the battery industry was caught up in what might be called "Gigafactory Mania"—with CATL, LG, SK, and Tesla racing to announce ever-larger manufacturing commitments—Samsung SDI was conspicuously restrained.

The company adopted what it internally called the "Profit-First" mandate: it would only build new capacity when it had a firm customer contract to fill that capacity. No speculative construction. No building-it-and-hoping-they-will-come. Every gigawatt-hour of new capacity had a customer's name attached to it before the first concrete was poured.

This approach meant Samsung SDI grew more slowly than its competitors. By 2025, CATL's annual capacity exceeded 800 gigawatt-hours. LG Energy Solution's exceeded 200. Samsung SDI's was a fraction of that.

But it also meant the company avoided the write-downs, the idle factory costs, and the margin-destroying price cuts that would later plague companies that had overbuilt in anticipation of an EV demand curve that arrived more slowly than the hockey-stick projections suggested.

By the time the global EV market hit its soft patch through 2024 and 2025, Samsung SDI's conservative approach looked less like timidity—and more like prescience. But before the market slowdown, there was a crisis of a very different kind to survive.

VI. The Note 7 Crisis and the Quality Reformation

No account of Samsung SDI would be complete without addressing the single most damaging event in its corporate history: the Galaxy Note 7.

In August 2016, Samsung Electronics launched the Galaxy Note 7 to rapturous reviews. It was the most advanced smartphone Samsung had ever produced—a flagship device designed to compete head-to-head with the iPhone 7. Reviewers praised its curved display, its iris scanner, its water resistance, and its sleek design.

Within weeks, that praise turned to alarm as reports began surfacing of Note 7 handsets catching fire.

Batteries were overheating, swelling, and in some cases igniting—in users' pockets, on nightstands, and in airplane cabins. Airlines began banning the device. Videos of burning phones went viral on social media. It was a public relations catastrophe of the highest order.

The culprit was a design flaw in the battery cells supplied by Samsung SDI. The electrodes in the upper-right corner of the cell were susceptible to bending, which weakened the separation between the positive and negative terminals. When this separation failed, it caused thermal runaway—an uncontrolled chain reaction in which the battery's internal temperature spikes, the electrolyte ignites, and the cell vents hot gases and flames.

The root cause was traced to aggressive dimensional targets. Samsung Electronics had pushed for a battery that packed maximum energy into a minimally thin form factor, and Samsung SDI had delivered a cell that was too tightly wound, with insufficient tolerances for the natural swelling that occurs during charge-discharge cycling.

Samsung Electronics initially recalled the devices and replaced them with units containing batteries from an alternative supplier, Amperex Technology Limited. When those replacement devices also caught fire—due to a different manufacturing defect—Samsung did something unprecedented: on October 10, 2016, it permanently discontinued the Galaxy Note 7 entirely.

The total cost to Samsung Electronics was estimated at over seventeen billion dollars, encompassing the recall, replacement devices, lost sales, and brand damage. It remains one of the most expensive product recalls in history.

For Samsung SDI specifically, the impact was severe. The stock lost roughly a fifth of its market value. Clients across the industry, including Apple, began demanding detailed safety assurances about batteries used in their own products. The company's reputation—painstakingly built over two decades of small-format battery leadership—was suddenly and dramatically in question.

What happened next reveals something important about the institutional DNA of Samsung SDI.

Rather than deflect blame, minimize the incident, or retreat into corporate double-speak, the company launched an exhaustive post-mortem that fundamentally redesigned its quality control infrastructure. It created what it called an eight-point battery safety check—a multi-layered testing protocol that subjects every cell to X-ray inspection of internal structure, charge-discharge cycling under extreme conditions, accelerated-use testing designed to simulate years of real-world wear in weeks, puncture and crush testing, overcharge testing, and visual and disassembly analysis.

Samsung SDI invested in AI-powered inspection systems that could detect microscopic defects invisible to the human eye. It redesigned its manufacturing processes to include wider tolerances and additional internal safeguards.

The Note 7 crisis became, paradoxically, a competitive advantage. Samsung SDI emerged from the disaster with arguably the most rigorous battery safety testing regime in the industry. When the company sat down with BMW or Stellantis and pitched its cells, it could point to the Note 7 as evidence that it had been through the absolute worst-case scenario, had investigated it with ruthless transparency, and had rebuilt its entire quality infrastructure from the ground up.

You cannot buy that kind of credibility. You can only earn it through failure and reformation. In boardrooms across Munich, Stuttgart, and Detroit, the Note 7 story has been retold not as a cautionary tale about Samsung, but as a case study in how a great supplier responds to catastrophe. The answer—total transparency, massive investment, and a refusal to cut corners on the fix—is exactly what automakers want to hear from a partner they are trusting with the safety of their vehicles.

The episode illustrates a broader pattern: Samsung SDI's ability to absorb catastrophic setbacks and convert them into institutional learning. The CRT-to-battery pivot was a response to technological obsolescence. The Bosch dissolution extracted maximum value from a partnership that had run its course. And the Note 7 reformation converted a quality failure into the industry's gold standard for safety testing.

Each time, Samsung SDI did not merely survive the crisis but extracted something structurally valuable from it. That is a rare organizational capability, and it is worth a lot more than it shows up on any balance sheet. The question, heading into 2021, was who would lead this transformed company into the EV age.

VII. Management: From Choi Yoon-ho to Choi Joo-sun

In December 2021, Samsung SDI appointed Choi Yoon-ho as President and CEO. Choi was a Samsung Electronics veteran and former CFO, and his appointment sent a clear signal: the era of pure engineering leadership was being supplemented with financial discipline.

Under Choi Yoon-ho, Samsung SDI adopted what became its defining mantra—"Quality Growth"—a philosophy that prioritized operating margin and return on equity over raw gigawatt-hour capacity.

Choi was blunt with the market in a way that Korean corporate leaders rarely are. He told investors and analysts that Samsung SDI would not engage in a price war for low-end lithium iron phosphate batteries—the commodity chemistry that CATL was using to dominate the Chinese market. Instead, SDI would focus on premium nickel-rich chemistries for high-end EVs and, eventually, solid-state.

The message was unmistakable: let CATL have the volume. We want the profit.

In a 2024 earnings call, he was characteristically direct: "The difficult situation persisting in the second half may turn into a critical opportunity for the company when tackled with well-prepared countermeasures. The company will continue to gain a differentiated competitive edge in a bid to be the first to capture new opportunities when the market turns around."

Under Choi Yoon-ho's watch, Samsung SDI navigated the pandemic, the semiconductor shortage, and the supply chain chaos of 2021 and 2022. Revenue grew. Margins held. The company secured landmark customer wins with GM and Hyundai Motor while deepening its relationship with BMW. He also oversaw the divestiture of the polarizer film business and the completion of next-generation technology development, including the all-solid-state battery program.

Then, in November 2024, Samsung SDI announced a leadership transition. Choi Yoon-ho was reassigned to head a newly established business consultation division at Samsung Global Research, and the CEO role passed to Choi Joo-sun. The appointment of yet another semiconductor-background CEO tells you something important about how the Samsung Group thinks about battery manufacturing.

The new CEO's profile is revealing. Born in 1963, Choi Joo-sun holds a PhD in electronic engineering from KAIST—Korea's premier science and technology university—and an undergraduate degree in electrical engineering from Seoul National University, the country's most prestigious.

His early career was spent in DRAM design—first at Hynix Semiconductor (now SK Hynix) and then at Micron Technology in the United States. He joined Samsung Electronics in 2004 and rose through a series of senior roles spanning both the technical and commercial sides of the semiconductor business: head of DRAM Development Center, head of Sales and Marketing in the Memory Business, vice president overseeing strategic marketing, and leader of Samsung's US operations. Most recently, he served as President and CEO of Samsung Display since 2020, where he managed the transition from LCD to OLED at one of the world's largest display manufacturers.

The Samsung Group views battery manufacturing and semiconductor manufacturing as fundamentally similar disciplines. Both require extreme precision in chemical and physical processes. Both demand massive, front-loaded capital investment with long payback periods. Both involve long customer qualification cycles where a single defect can be catastrophic.

And both are driven by yield rates—the percentage of production that meets specification—as the primary determinant of profitability. A leader who has managed the economics of a DRAM fabrication plant, where the difference between a ninety percent yield and a ninety-five percent yield can mean hundreds of millions of dollars in annual profit, understands at an intuitive level the challenges of scaling battery production while maintaining quality.

Choi Joo-sun inherited a difficult situation. The full-year 2025 results were sobering: revenue of 13.27 trillion won—down from 16.59 trillion in 2024—and an operating loss of 1.72 trillion won. This was the first full-year operating loss in the company's modern history. The culprits were the global slowdown in EV demand, aggressive price competition from Chinese manufacturers, and the costs associated with ramping new capacity.

The fourth quarter of 2025 showed some improvement, with revenue of 3.86 trillion won rising 26.4 percent quarter-on-quarter and 2.8 percent year-on-year, suggesting the bottom may have been reached. But the road to recovery is long.

Like most professional managers within the Samsung Group, neither Choi holds significant personal equity in the company. Their incentive structures are tied to long-term performance metrics set by Samsung's corporate office, rather than stock-option-driven short-termism.

This creates an interesting governance dynamic: management optimizes for multi-year strategic goals rather than quarterly stock price movements. The downside is that minority shareholders have limited ability to influence management decisions. The upside is that management can make decisions like "do not chase low-margin LFP volume" without worrying about activist investors demanding immediate revenue growth.

The test of this leadership will be whether Samsung SDI can navigate the current trough while executing on its most ambitious technology bet. But first, it helps to understand the quiet engine that has been generating cash through every downturn.

VIII. The Hidden Engine: Electronic Materials

Every analyst covering Samsung SDI spends ninety percent of their time talking about batteries. This is understandable—the Energy Solutions segment accounts for roughly eighty-seven percent of revenue. But the remaining thirteen percent, the Electronic Materials division, is where some of the most interesting economics in the company live.

This is Samsung SDI's original business—the descendant of its display technology heritage, repurposed for the semiconductor and OLED age. The division produces three primary product categories that are worth understanding in detail, because they reveal the kind of "picks-and-shovels" businesses that often generate the best risk-adjusted returns in technology supply chains.

CMP Slurry. CMP stands for chemical-mechanical planarization, and it refers to the process of polishing semiconductor wafers to the atomically flat surfaces required for advanced chip manufacturing. Think of it this way: a silicon wafer goes through dozens of processing steps, each adding a thin layer of material—a metal circuit, an insulating layer, a transistor gate. After each step, the wafer surface is uneven, like a landscape of tiny hills and valleys. Before the next layer can be deposited, the surface needs to be made perfectly flat, to within a few nanometers. CMP slurry is the abrasive liquid—a mix of tiny particles and chemical agents—that achieves this. It is, literally, the world's most precise sandpaper.

Samsung SDI's CMP portfolio includes oxide slurry for polishing insulating layers, metal slurries for tungsten and copper interconnects, and ceria slurry for advanced planarization steps. These are not commodity products. Each formulation is tailored to specific manufacturing processes at specific chip fabrication plants. Qualifying a new slurry supplier typically takes twelve to eighteen months of testing. Once qualified, customers rarely switch—the risk of introducing defects into a multi-billion-dollar fab line far outweighs any potential cost savings.

OLED Materials. These are the organic compounds that emit light in OLED displays. Unlike LCDs, which use a backlight and liquid crystals to create images, OLED displays use organic molecules that emit their own light when an electric current passes through them. The quality of these materials—color purity, brightness, efficiency, and longevity—directly determines the quality of the display. Samsung SDI supplies OLED materials to Samsung Display and other manufacturers.

The Polarizer Divestiture. The third product line, until September 2024, was polarizer films—thin films that polarize light and are essential components in display panels. Samsung SDI sold this business to Wuxi Hengxin Optoelectronic Materials, a Chinese competitor, for 1.12 trillion won (approximately 834 million dollars), transferring manufacturing facilities in Cheongju and Suwon, Korea, plus a wholly owned Chinese operation.

The logic was classic portfolio management: polarizer film was a mature, lower-margin product line in an increasingly commoditized market. The proceeds—nearly a billion dollars—were earmarked for investment in the areas where Samsung SDI has genuine competitive advantages: battery materials and solid-state R&D. Shed the legacy, fund the future. It is the same playbook the company ran when it wound down CRTs to fund small batteries, and when it wound down plasma TVs to fund EV batteries.

To understand why Electronic Materials matters for the investment thesis, consider margins. The battery business, even in good years, operates at single-digit operating margins—typically five to eight percent. It is capital-intensive and commodity-leaning, where customers are large automakers with enormous bargaining power.

Electronic Materials, by contrast, routinely generates operating margins in the fifteen-to-twenty-percent range. The products are specialty chemicals sold into the semiconductor and display industries, where switching costs are extremely high, volumes are smaller but unit economics are much richer, and the competitive landscape is dominated by a handful of qualified suppliers.

The AI boom has made this segment even more valuable. The insatiable demand for advanced semiconductors—from the Nvidia GPUs that train large language models to the high-bandwidth memory chips that store AI model weights—translates directly into demand for CMP slurry. More chips means more wafers, means more polishing steps, means more slurry.

For investors, Electronic Materials serves as a natural hedge against the cyclicality of the battery business. When EV demand softens and battery margins compress—as they did through 2025—the Electronic Materials division continues to generate healthy cash flows. It is the steady, high-margin utility sitting inside a high-growth, high-volatility battery company. Ignoring it when analyzing Samsung SDI is like analyzing Apple and forgetting about the Services segment.

IX. The Next Act: Solid-State Batteries and the AI Energy Storage Boom

In March 2022, Samsung SDI inaugurated the "S-Line"—a six-thousand-five-hundred-square-meter pilot production line for all-solid-state batteries at its R&D Center in Suwon. By the end of 2023, the line was producing working prototype cells. By October 2025, Samsung SDI had entered a trilateral partnership with BMW and Solid Power, the Colorado-based solid electrolyte specialist, to collaboratively develop and validate all-solid-state battery technology for next-generation electric vehicles.

To understand why solid-state is considered the holy grail of battery technology, a brief chemistry lesson is in order.

A conventional lithium-ion battery contains a liquid electrolyte—the medium through which lithium ions shuttle between the cathode and anode during charging and discharging. Think of the electrolyte as a highway connecting two cities: ions travel along it, carrying energy from one electrode to the other.

This liquid highway works well, but it has two fundamental problems. First, it is flammable. The organic solvents used in liquid electrolytes are volatile, and if the cell is damaged, overcharged, or manufactured with a defect that allows the electrodes to touch, the electrolyte can ignite. Every battery fire traces back to this fundamental vulnerability. Second, it limits energy density. The liquid electrolyte occupies space inside the cell and constrains the types of electrode materials that can be used safely.

An all-solid-state battery replaces the liquid highway with a solid one—typically a ceramic or sulfide-based compound. This eliminates the fire risk almost entirely, because solid electrolytes do not contain flammable solvents. And because solid electrolytes are thinner, more chemically stable, and compatible with higher-energy electrode materials like lithium metal, they allow for significantly higher energy density.

Samsung SDI is targeting 900 watt-hours per liter—a massive improvement over the roughly 600 to 700 watt-hours per liter that the best conventional lithium-ion cells achieve today. In practical terms, this means an electric vehicle with a solid-state battery could offer thirty to fifty percent more range in the same physical space, or the same range with a smaller, lighter, cheaper battery pack. Some demonstrations have shown the potential for charging to eighty percent in as little as nine minutes.

Samsung SDI is pursuing what is known as an "anode-free" design. In a conventional cell, the anode is made of graphite or silicon that stores lithium ions during charging. In an anode-free design, there is no pre-formed anode at all. Instead, pure lithium metal deposits directly onto a bare current collector during charging and dissolves back during discharging. This eliminates the weight and volume of the graphite anode entirely, further boosting energy density. It is an elegant concept—but manufacturing it reliably at scale is one of the most difficult challenges in materials science.

Samsung SDI holds one of the largest patent portfolios in all-solid-state battery technology globally. The company has stated publicly that it aims to begin mass production in 2027. The BMW–Solid Power partnership adds credibility: under the arrangement, Solid Power supplies sulfide-based solid electrolyte material to Samsung SDI, which integrates the material into separator and catholyte layers and builds complete cells. These cells are then evaluated by BMW against automotive-grade performance requirements.

The fact that BMW—one of the most demanding and quality-obsessed automakers on the planet—is willing to put its name on this collaboration suggests that the technology has moved beyond the laboratory curiosity stage.

However, skepticism is warranted. The history of solid-state battery promises is littered with missed deadlines and overhyped demonstrations. Manufacturing solid electrolytes at scale without defects, maintaining intimate contact between the solid layers during thousands of charge-discharge cycles, and achieving cost parity with conventional lithium-ion are all unsolved challenges. Toyota has been working on solid-state for over a decade and has repeatedly pushed back its timeline. QuantumScape has produced test cells but has not demonstrated mass manufacturing capability.

Samsung SDI has the R&D resources and the manufacturing expertise to have a serious shot. But 2027 mass production is a target, not a guarantee.

Meanwhile, a second growth vector has emerged that almost no one in the battery investment community was talking about three years ago: energy storage systems for AI data centers.

The explosion in artificial intelligence workloads has created a voracious, almost insatiable demand for electricity. Training a single large language model can consume as much electricity as a small city uses in a month. Running inference—the process of actually using those models—consumes even more on an ongoing basis. Hyperscale data center operators are building new facilities at a pace that is straining electrical grids worldwide.

Battery energy storage systems, or BESS, are the answer. Grid operators and data center operators need them to manage peak electricity loads, provide backup power during outages, smooth the integration of renewable energy, and provide the instantaneous power response that AI workloads demand.

Samsung SDI's "Samsung Battery Box" has seen record demand in North America. In early 2026, the company clinched an LFP-based ESS supply deal with a US customer valued at well over two trillion won, with deliveries starting in 2027. The company also debuted its SBB 2.0 product, powered by LFP cells in its proprietary prismatic form factor, designed specifically for grid-scale and data center applications.

Notably, Samsung SDI is actively shifting some of its US EV battery production lines to ESS output—a pragmatic recognition that near-term demand for grid storage is stronger and more predictable than demand for electric vehicle batteries. This flexibility is itself a competitive advantage. Companies that built single-purpose EV battery factories are stuck waiting for automotive demand to recover. Samsung SDI can redirect production to wherever demand is hottest—and right now, that is the data center.

US ESS demand alone is projected to more than double from 59 gigawatt-hours in 2025 to 142 gigawatt-hours by 2030, driven by renewable energy buildout and AI data center capacity. Samsung SDI does not need to beat CATL in electric vehicles if it can establish a strong position in grid-scale energy storage. The ESS opportunity could turn out to be the unexpected catalyst that rerates the stock, because the market is currently pricing Samsung SDI almost exclusively as an EV battery company—and the ESS tailwind has barely been factored in.

X. Hamilton's Seven Powers and Porter's Five Forces

No serious analysis of a company's competitive position is complete without examining the structural advantages that protect it from erosion. Samsung SDI's moat is not a single fortification but a layered defense system.

Switching Costs: Very High. This is Samsung SDI's most formidable power. When BMW or Stellantis designs a vehicle platform around SDI's prismatic P6 cells, they commit to that architecture for the platform's entire lifecycle—typically seven to ten years. The battery pack is integrated into the chassis structure, the thermal management system, the battery management software, and the crash safety architecture. Changing suppliers mid-cycle would require a complete redesign and recertification costing hundreds of millions of dollars. Once you are in, you are in for a decade.

Cornered Resource: High. The patent portfolio in solid-state electrolytes represents a genuine cornered resource. Battery chemistry patents are grounded in specific material compositions and manufacturing processes that are extraordinarily difficult to design around. If Samsung SDI's sulfide-based formulations prove to be the winning chemistry for mass production, competitors will either license the technology or spend years and billions developing alternatives.

Scale Economies: Moderate. Samsung SDI is at a disadvantage relative to CATL, which produces roughly ten times as many cells annually. However, the StarPlus Energy joint venture with Stellantis in Kokomo, Indiana—with a combined planned capacity of 67 gigawatt-hours across two plants—and the planned GM joint venture are closing the gap in North America specifically. Samsung SDI does not need global scale parity with CATL. It needs sufficient scale in the regions where its target customers manufacture vehicles and where trade policy increasingly favors domestic production.

Brand: High. The "Samsung" brand carries significant weight in B2B negotiations. It signals financial stability, R&D depth, and the implicit backing of one of Asia's largest conglomerates. Automakers making twenty-billion-dollar platform bets need to know their battery supplier will still be solvent and technologically competitive in 2035.

Process Power: High. The post-Note 7 quality control infrastructure, proprietary electrode coating techniques, formation cycling protocols, and AI-powered defect detection systems represent genuine process power—institutional knowledge embedded in the manufacturing line that competitors cannot replicate by simply buying the same equipment.

Now, turning to the competitive landscape through Porter's framework, the picture becomes more nuanced.

Bargaining Power of Buyers: High. Samsung SDI's customers are among the world's largest automakers, and they negotiate with the subtlety of a sledgehammer. BMW, Stellantis, and GM actively play battery suppliers against each other, maintain relationships with multiple cell manufacturers, and are increasingly developing in-house battery capabilities. This structural pressure limits pricing power and explains why margins remain compressed across the industry—even for premium suppliers.

Bargaining Power of Suppliers: Moderate, but Managed. The critical input for SDI's nickel-rich batteries is cathode material. The company has mitigated this through its landmark deal with EcoPro BM—a five-year supply agreement valued at approximately thirty-four billion dollars covering high-nickel NCA cathode materials from 2024 to 2028. Samsung SDI also has a joint venture with EcoPro EM for precursor materials, and EcoPro is building a factory in Debrecen, Hungary, to supply SDI's European operations. These contracts lock in supply and reduce spot-market exposure—though they also create concentration risk.

Threat of Substitutes: Real, but Segmented. In the low-end and mid-market EV segments, lithium iron phosphate chemistry from Chinese manufacturers is rapidly gaining share. LFP is cheaper, safer, and good enough for vehicles with moderate range requirements. Sodium-ion, an even cheaper chemistry using abundant raw materials, is emerging as a potential threat at the very bottom of the market. Samsung SDI has wisely avoided competing in these segments—but if LFP and sodium-ion move upmarket faster than expected, the "premium" segment could shrink.

Threat of New Entrants: Low. Building a battery cell manufacturing line requires billions in capital, years of qualification with automakers, and deep expertise in electrochemistry and high-volume manufacturing. The recent wave of battery startup failures—from Britishvolt to Northvolt's restructuring—underscores just how difficult it is to enter this industry. This high barrier protects incumbents like Samsung SDI.

Competitive Rivalry: Intense, but Bifurcating. The battery market is increasingly splitting into two arenas: a commodity market dominated by CATL and BYD where competition is primarily on price, and a premium market where Samsung SDI, LG Energy Solution, and Panasonic compete on technology, safety, and customer relationships. Samsung SDI's global EV battery market share by volume has been declining—but volume share is a misleading metric for a company that has explicitly chosen margin over share. The relevant question is not "how many cells do you ship?" but "how much profit do you earn per cell shipped?"

When you layer all of these forces together, a clear picture emerges. Samsung SDI operates in a brutally competitive industry with powerful buyers and aggressive rivals. But it has built structural defenses—switching costs, patents, process knowledge, and brand credibility—that insulate it from the worst of the pricing pressure. The question is whether those defenses are thick enough to withstand a prolonged downturn in which Chinese competitors continue to gain share. The answer depends, more than anything else, on whether the premium end of the battery market grows fast enough—and whether solid-state arrives in time.

XI. Bear Case versus Bull Case

The Bear Case.

The pessimistic view of Samsung SDI starts with the financial trajectory. Revenue declined from 16.59 trillion won in 2024 to 13.27 trillion in 2025—a drop of twenty percent. The company swung from a modest operating profit of 363 billion won to a 1.72 trillion won operating loss. That is not a speed bump. It is a crater.

The bears argue that SDI's "premium" strategy is a luxury it can no longer afford. Chinese competitors, led by CATL, are expanding aggressively into Europe and Southeast Asia with LFP batteries that are thirty to forty percent cheaper than Samsung SDI's nickel-rich cells—and are increasingly good enough for mainstream applications. If the battery market commoditizes faster than expected, Samsung SDI's positioning could become a euphemism for "expensive and shrinking."

The solid-state bet is also a source of risk. If the 2027 mass production target slips—as many industry observers expect based on the history of solid-state development—Samsung SDI would have invested billions in a technology not yet generating revenue while its conventional battery business faces intensifying price pressure. The company's relatively small scale compared to CATL means it has less capacity to absorb losses during a prolonged downturn.

There is also the US policy question. Samsung SDI has made massive bets on American manufacturing through the StarPlus Energy and GM joint ventures. But US EV policy has been volatile, with subsidies and mandates subject to political cycles. If demand for EVs in North America stalls, SDI could face underutilized factories in Indiana—exactly the stranded-asset scenario it spent two decades trying to avoid.

And the leadership transition—with a new CEO taking the helm during the most challenging period in the company's modern history—introduces execution risk at exactly the wrong moment.

The Bull Case.

The optimistic view begins with the balance sheet. Samsung SDI entered the downturn with one of the strongest financial positions in the battery industry, bolstered by the 834 million dollar polarizer divestiture and the implicit backing of the Samsung Group.

Companies go bankrupt during downturns not because their products are bad, but because they run out of cash. Samsung SDI is in no danger of running out of cash. It has the financial resilience to weather a multi-year trough that could force weaker competitors to exit or consolidate—potentially improving SDI's competitive position once the cycle turns.

The solid-state opportunity is the most electrifying element of the bull case. If Samsung SDI can deliver on its 2027 timeline—even with a one-to-two-year delay—it would be the first company to mass-produce an automotive-grade solid-state battery. That would represent a genuine paradigm shift, comparable to Samsung Electronics' move from DRAM to NAND flash or Apple's introduction of the iPhone. It would not just improve SDI's existing product lineup; it would create an entirely new product category that commands premium pricing and resets the competitive landscape.

The AI-driven ESS boom is what bulls describe as an "unpriced call option." If data center power demand continues to grow at current rates, the market for grid-scale energy storage could approach the size of the EV battery market within a decade. Samsung SDI's early pivot to ESS production—including the two-trillion-won-plus US supply deal—positions it to capture a meaningful share of a market that virtually no sell-side analyst has fully modeled.

The EcoPro cathode supply agreement, the vertical integration from the Cheil Industries merger, and the diversified revenue stream from Electronic Materials provide layers of resilience not immediately obvious from headline financial numbers. In a world where Western governments are actively seeking to reduce dependence on Chinese battery supply chains, Samsung SDI's position as a non-Chinese supplier with advanced technology and US manufacturing partnerships is a strategic asset whose value is only beginning to be recognized.

The Playbook Lessons.

Three enduring principles emerge from Samsung SDI's fifty-six-year history. First, the "Quality over Volume" play: the willingness to sacrifice market share to protect margins creates a fundamentally different risk profile than the volume-at-all-costs approach—one that proves its worth precisely when the market turns down.

Second, how to manage a "Sunset" business to fund a "Sunrise" business: from CRTs to small batteries to EV batteries, Samsung SDI has demonstrated a rare institutional discipline in harvesting declining businesses to finance emerging ones—without ever cutting the R&D lifeline to the future.

Third, the importance of "Relational Capital": the fifteen-year BMW relationship, the EcoPro supply partnership, the Stellantis joint venture—these are not transactions but ecosystems of trust built over decades. In an industry where qualification cycles run for years and switching costs are measured in hundreds of millions, relational capital may be the most durable competitive advantage of all.

XII. The KPIs That Matter

For investors tracking Samsung SDI's ongoing performance, three metrics cut through the noise.

First, Energy Solutions operating margin. This is the single most important indicator of whether the "Quality Growth" strategy is working. Samsung SDI has historically maintained higher margins than its Korean peers, and the ability to return to positive operating margins in the battery segment will be the clearest signal that the 2025 trough is behind it. A return to mid-single-digit margins would confirm the thesis. A sustained period at zero or below would raise serious questions about positioning.

Second, ESS revenue as a percentage of total Energy Solutions revenue. The pivot from EV-only to EV-plus-ESS is the most important strategic shift at Samsung SDI right now. If ESS revenue grows to twenty or thirty percent of the Energy Solutions segment over the next two to three years, it would meaningfully diversify the customer base, reduce dependence on the cyclical auto industry, and tap into a market with potentially better unit economics. This ratio will show how fast the pivot is actually happening.

Third, solid-state battery milestone achievement. This is a binary, event-driven metric: is the company hitting its publicly stated milestones on the path to mass production? Watch for automotive-grade cell deliveries to BMW evaluation programs, expansion of the S-Line pilot facility, formal selection as the solid-state cell supplier for a specific OEM production vehicle, and groundbreaking on a dedicated production line. Every milestone hit on schedule increases the probability that Samsung SDI will be the first mover in what could ultimately become a hundred-billion-dollar market.

XIII. Epilogue: The 2030 Vision

In a brightly lit conference room in Suwon, Samsung SDI's leadership has laid out a vision for 2030: two hundred gigawatt-hours of total battery manufacturing capacity, over nine billion dollars in fresh capital investment, and a product portfolio spanning everything from premium EV cells to grid-scale energy storage systems to the industry's first mass-produced solid-state battery.

It is an ambitious target for a company that just reported its first full-year operating loss. The path from here to there runs through unfinished factories in Indiana, a pilot line in Suwon that needs to become a full-scale production facility, a global EV market that remains stubbornly uncertain, and a competitive landscape where the largest player has ten times the capacity and is willing to sell at razor-thin margins.

But Samsung SDI has been here before. It stared down the death of the cathode ray tube and pivoted to batteries. It weathered the Asian Financial Crisis and built a pilot line when the entire country was in financial emergency. It survived the Note 7 and emerged with the industry's most rigorous quality protocols. It watched competitors overextend and collapse while quietly accumulating the patents, the partnerships, and the manufacturing know-how to be ready when the moment arrives.

Samsung SDI is not trying to win the most headlines. It is not trying to ship the most cells. It is trying to win the most profit per cell, in the most demanding applications, for the most discerning customers. In a battery industry littered with broken promises, bankrupt startups, and overcapacity crises, that might just be the most radical strategy of all.

The company that started making vacuum tubes for Korean televisions fifty-six years ago is now arguably closer than anyone on Earth to cracking the solid-state code. It has survived technological obsolescence, financial crises, product recalls, and market downturns. Each time, it emerged stronger, more disciplined, and better positioned than before.

Whether it gets there by 2027 or 2029, whether the AI-driven ESS boom lives up to its extraordinary promise, and whether the market ultimately rewards patient discipline or punishes conservative caution—these are the questions that will determine whether Samsung SDI's next chapter is its greatest. The alchemist has spent fifty-six years perfecting the art of transformation. The next transmutation is the most ambitious yet.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube