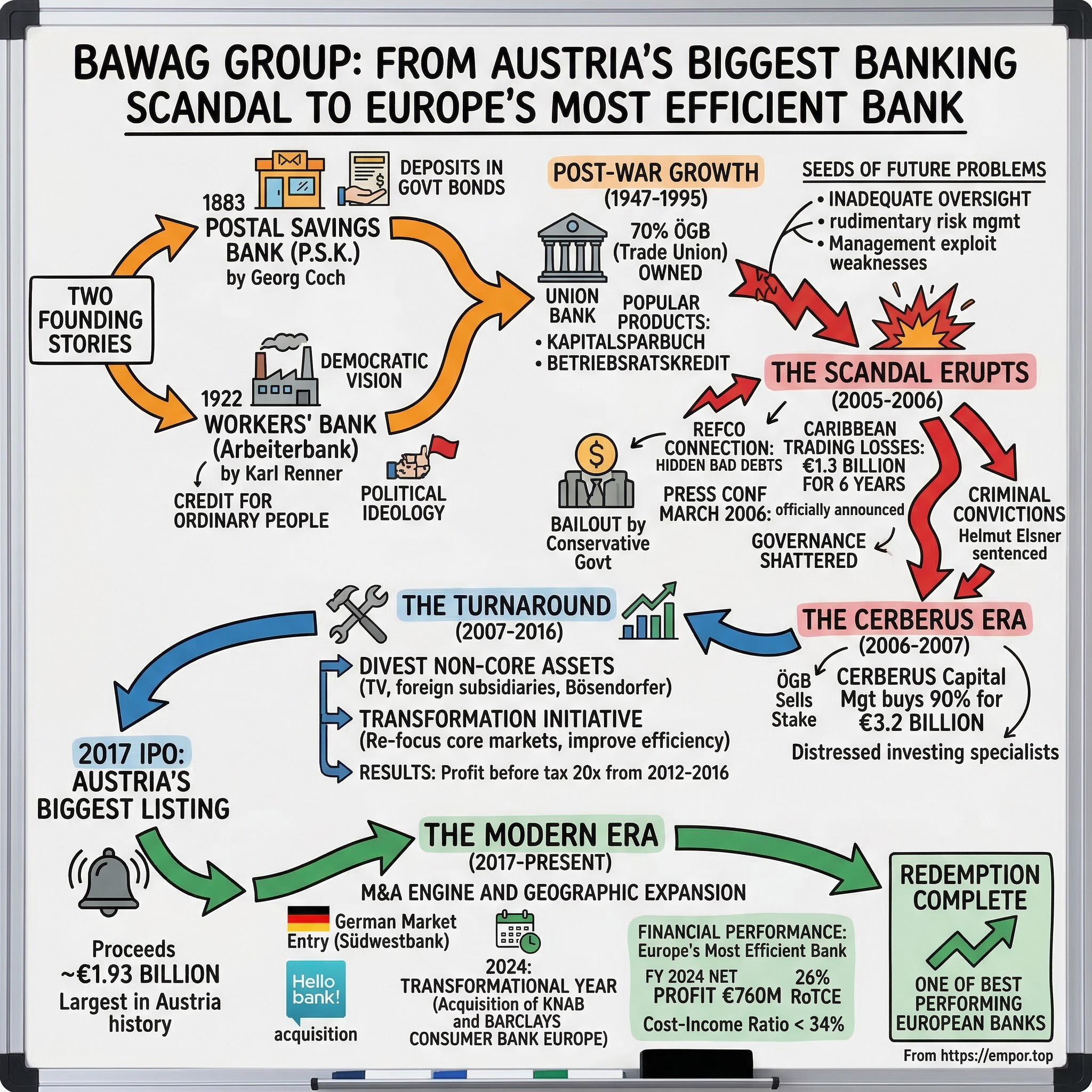

BAWAG Group: From Austria's Biggest Banking Scandal to Europe's Most Efficient Bank

Picture this: Vienna, March 2006. A press conference unlike any in Austrian financial history is about to unfold. Günter Weninger, Chair of BAWAG's Supervisory Board, steps forward to deliver news that will shake the foundations of the Austrian labor movement and trigger the biggest banking scandal the country has ever witnessed. At the press conference on March 24, 2006, Weninger officially announced the bank's accumulation of €1.3 billion in overall losses during a five-year period. He also stated that he had been informed of these losses by management at the end of 2000. However, at the time, he had decided to conceal the losses in derivatives trading for fear of triggering a bank run by customers and thus possible insolvency.

Fast forward nearly two decades, and the same institution that required government bailout now ranks among Europe's most profitable and efficient banks. For full year 2024, BAWAG Group reported a net profit of €760 million, earnings per share of €9.60, and a return on tangible common equity of 26%. The story of how a trade union bank that nearly collapsed transformed into a best-in-class financial institution is one of scandal, redemption, private equity intervention, and relentless operational excellence.

The Banker, an international industry magazine for banks published by the Financial Times, awarded BAWAG Group as "Bank of the Year 2024" in Austria during its traditional ceremony in London on December 4, 2024. This is a recognition of BAWAG's ongoing commitment to growth and innovation, following the bank's strategic acquisitions of the Dutch digital bank Knab and Barclays Consumer Bank Europe this year.

Today's BAWAG is a far cry from the institution that nearly brought down Austria's trade union movement. BAWAG Group AG is a publicly listed holding company headquartered in Vienna, Austria, serving over 4 million retail, small business, corporate, real estate and public sector customers across Austria, Germany, Switzerland, Netherlands, Western Europe and the United States. What follows is the remarkable tale of institutional failure, private equity turnaround, and disciplined execution that made this transformation possible.

Two Founding Stories: The Workers' Bank Meets Postal Savings (1883–1947)

The story of BAWAG actually begins with two distinct institutions, born nearly forty years apart, each reflecting a different vision of democratizing finance for ordinary Austrians.

The Postal Savings Bank: Georg Coch's Democratic Vision

P.S.K. was founded in 1883 as Austrian Postal Savings Bank by Georg Coch offering the idea of saving to broad sections of the population, to ensure the security of the deposits by investing in government bonds only as well as to provide funding for the state.

This was banking for the masses in an era when financial services remained the province of the wealthy. Coch's insight was brilliantly simple: leverage Austria's extensive postal network to create a savings institution that could reach every corner of the empire. By placing savings windows in post offices, the Postsparkasse eliminated the intimidation factor of grand bank buildings and brought financial services to villages and towns that had never seen a banker.

The philosophy was conservative by design. Deposits were invested exclusively in government bonds—no speculative ventures, no complex derivatives, just steady, reliable returns backed by the Austrian state. It was banking reduced to its purest form: accept deposits, pay modest interest, invest safely. This approach would stand in stark contrast to the culture that would later emerge at its eventual merger partner.

Karl Renner's Workers' Bank: Banking for the Proletariat

The second founding story is more overtly political, emerging from the tumult of post-World War I Austria. BAWAG was founded in 1922 by former Austrian Chancellor Karl Renner to extend favourable terms of credit to ordinary people, as the 'Austrian Worker's Bank'.

Karl Renner was no ordinary banker—he was the first Chancellor of the Austrian Republic and a leading figure in the Social Democratic Party. His vision for the Arbeiterbank was explicitly ideological: spare workers from having to resort to capitalist institutions for their banking needs. BAWAG was founded by Karl Renner as the Arbeiterbank not so much to extend favourable terms of credit to ordinary people, but to spare them having to resort to more capitalist institutions. Socialist trade unions and the Großeinkaufsgesellschaft für österreichische Consumvereine (Austrian consumer associations procurement company) each held a 40% stake in the bank.

The founding came at a particularly treacherous moment for ordinary Austrians. Hyperinflation had devastated savings, the empire had dissolved, and workers faced exploitation from traditional lenders. The Arbeiterbank positioned itself as an alternative—a bank owned by and for the working class.

But this political identity came with existential risk during Austria's turbulent interwar years. Because of close ties to the Social Democratic Party of Austria (SPÖ) and labour unions, BAWAG was forced to close in 1934 by the Austro-fascist government of Chancellor Engelbert Dollfuß. It resumed its operations after the end of World War II in 1947.

The bank's forced closure under fascism and resurrection after liberation established a pattern that would define BAWAG for decades: the institution's fate was inextricably tied to Austria's political currents. This wasn't simply a bank—it was a symbol of the Austrian labor movement, and that symbolic status would prove both blessing and curse in the decades ahead.

Post-War Growth and the Union Bank Model (1947–1995)

When BAWAG reopened its doors in 1947, Austria lay in ruins but was rebuilding with remarkable speed. The bank quickly resumed its position at the heart of the Austrian labor movement, though now with a more formal institutional structure.

In 1963, it took the name of Bank für Arbeit und Wirtschaft AG (BAWAG, translatable as "Bank for Labour and Business"). The bank continued to have close relations to social democratic party SPÖ and the unions.

The ownership structure cemented the institution's political identity. The Austrian Trade Union Federation (ÖGB) retained 70% of the shares, the other 30% were held by the Konsum retail cooperative chain. This arrangement created a uniquely insular governance structure—the bank was owned by institutions with deep political ties rather than dispersed shareholders demanding accountability.

The Golden Era: Products for Workers

In the 1970s, popular products were the Kapitalsparbuch (fixed-term savings passbook) and the Betriebsratskredit. At the same period, the bank actively used its finances to sponsor the promotion of Austrian contemporary art and culture. The BAWAG Foundation was established in 1974 with the goal of making art as accessible as possible to all people.

The Betriebsratskredit—essentially a works council loan—was emblematic of BAWAG's mission. These were loans facilitated through factory works councils, leveraging the trust relationship between workers and their union representatives. It was credit distribution through social networks rather than credit algorithms.

The BAWAG Foundation represented another dimension of the bank's identity. Rather than pure profit maximization, the institution saw itself as a patron of Austrian culture, channeling funds to make art accessible to ordinary people. This was banking as social mission—a far cry from the casino capitalism that would later bring the institution to its knees.

Branching Out: The 1979 Expansion

In 1979, parliament amended the Austrian Banking Act (Kreditwesengesetz or KWG), which now allowed the operation of branches. The BAWAG experienced rapid expansion throughout Austria, from an existing network of 26 offices to 120 by 1982.

This nearly five-fold expansion in just three years transformed BAWAG from a niche labor bank into a national retail player. But rapid growth brings complexity, and complexity breeds risk—particularly in an institution where oversight remained concentrated in the hands of trade union officials rather than independent directors.

Seeds of Future Problems

The cozy relationship between unions, politics, and banking created what governance experts would later recognize as a textbook case of inadequate oversight. Board members were typically union officials or SPÖ loyalists rather than banking professionals. Risk management was rudimentary. And the assumption that alignment with the labor movement meant alignment with workers' interests would prove tragically naive.

The institution that entered the 1990s was large, politically connected, and operating with governance structures fundamentally inadequate for a modern bank. All that was needed was management willing to exploit these weaknesses.

Cracks Appear: Konsum Collapse and New Shareholders (1995–2004)

The first tremors of the earthquake to come arrived in 1995, when Konsum—the retail cooperative holding 30% of BAWAG's shares—collapsed into bankruptcy.

The shareholder Konsum went bankrupt in 1995, which sent shockwaves through the political landscape in Austria, especially for the social democrats.

The Konsum failure was a blow to the entire ecosystem of Austrian social democracy. The consumer cooperative had been a pillar of the labor movement since the early twentieth century, and its collapse exposed the vulnerability of the interconnected network of unions, cooperatives, and financial institutions that had defined Austrian socialism.

Bayerische Landesbank's Investment

With Konsum gone, a new shareholder was needed. The Bayerische Landesbank sold its 46% share in 2004 to the other shareholder, the Austrian Trade Union Federation (ÖGB). With that deal, the ÖGB became sole owner of the BAWAG.

This transaction concentrated ownership even further. Instead of diversifying governance, the ÖGB chose to consolidate control—a decision that would prove catastrophic when hidden losses emerged.

Hidden Problems Accumulating

What the public didn't know—and wouldn't learn until 2006—was that massive losses were already accumulating in off-balance-sheet vehicles. In late March 2006, internal investigations within the bank revealed that additional losses of one billion euro had also been covered up. These resulted from derivatives trading in the Caribbean from 1995 to 2000.

The strategy of concealment persisted for nearly a decade, evading detection by Austrian financial authorities. The losses came from a series of failed bets using risky derivative investments held in off-balance-sheet vehicles. Though the bets go back as far as 1998, they surfaced only in 2006 during U.S. investigations into the bankruptcy of Refco.

During this period, senior management was engaged in precisely the kind of speculative activity that the original founders had wanted to spare workers from. The irony was bitter: a bank founded to protect workers from exploitative capitalist institutions had become a venue for casino-style gambling with depositors' money.

Building the Modern Platform: The P.S.K. Merger (2000–2005)

Even as hidden losses accumulated, BAWAG's management was pursuing aggressive expansion. The most significant move was acquiring the Österreichische Postsparkasse (P.S.K.)—the very postal savings bank that Georg Coch had founded over a century earlier.

In 2000, BAWAG successfully took over a majority of shares of the Österreichische Postsparkasse (P.S.K.) bank, buying 74.82% of the shares from the government. In November 2003, the remaining 25.18% were bought up as well. The merger, which was not finalized until 2005, created the country's third-largest bank group with a balance sheet total of nearly 45 billion euros, 5000 employees, some 2000 outlets and over one million private customers.

The merger brought together two institutions with fundamentally different cultures. P.S.K. had maintained its conservative, deposit-focused heritage—exactly the approach that BAWAG's aggressive traders had abandoned. But rather than allowing P.S.K.'s risk-averse culture to temper BAWAG's speculative tendencies, management continued pursuing high-risk strategies.

Eastern European Ambitions

The merger coincided with expansion into Central and Eastern Europe, as Austria's banks raced to capture newly opened markets following the fall of communism.

In 2002, the Slovakian bank Istrobanka was bought, a year later the Czech bank Interbanka. Both equities were owned 100% by the BAWAG. The new partners opened up opportunities to expand in retail banking and intended to open new branches throughout Europe. In 2004, BAWAG acquired 100% of the shares of Dresdner Bank CZ, integrating it into the Interbanka, now renamed as BAWAG Bank CZ.

Non-Core Diversification

In one of the more peculiar acquisitions in banking history, The piano manufacturer Bösendorfer was bought from the American company Kimball International in 2001.

Why would a retail bank own a piano manufacturer? The acquisition reflected the hubris of management that believed their expertise extended beyond banking—and a governance structure that failed to question such decisions.

The formal merger creating BAWAG P.S.K. closed on October 1, 2005—just weeks before the scandal erupted that would nearly destroy everything.

The Scandal Erupts: Refco, Caribbean Trading, and Near-Collapse (2005–2006)

The BAWAG scandal didn't erupt from internal whistleblowers or Austrian regulators. It emerged from an American bankruptcy—specifically, the collapse of commodities broker Refco in October 2005.

The Refco Connection

In October 2005, BAWAG approved a loan of 425 million euros to Phillip R. Bennett, then CEO of the commodities broker Refco, collateralized against Bennett's own holdings in the firm. However, the reason he required the money was that he had lent an undisclosed 430 million dollars of the broker's money to himself in an attempt to cover up the company's bad debts. The very day after BAWAG made Bennett the loan, the irregularities were made public, triggering a number of regulatory investigations. Refco has since declared chapter 11 bankruptcy, making BAWAG's collateral essentially worthless. Austria's central bank and Austria's Financial Market Authority have started investigations. In April 2006, creditors of Refco sued BAWAG for over $1.3 billion, alleging that the bank had colluded to hide Bennett's fraudulent transactions back to at least 2000, and that the bank owned far more of Refco than it had ever revealed in regulatory filings.

The timing was almost cinematically dramatic—BAWAG making a massive loan one day, and the borrower's fraud becoming public the next. But this wasn't merely bad luck. BAWAG's relationship with Refco ran far deeper than a single unfortunate loan.

Years of Complicity

In the early 2000s, BAWAG P.S.K. engaged in a series of year-end transactions with Refco Group Ltd. to help conceal Refco's approximately $430 million in uncollectible debt owed by its CEO, Phillip R. Bennett. These arrangements, initiated as early as February 2000 and continuing through 2005, involved BAWAG providing short-term loans to Refco—disguised as currency trades—that allowed Refco to offload the bad debt temporarily from its balance sheet at fiscal year-ends. BAWAG's participation earned it fees totaling around €23 million over the period, and the bank held a 10% equity stake in Refco acquired in 1999.

For €23 million in fees, BAWAG had made itself complicit in one of the largest broker frauds in American history. The SEC would later describe the arrangement in damning terms. The Commission's Complaint alleges that BAWAG helped Refco conceal hundreds of millions of dollars in debt owed to Refco by an entity controlled by Refco's Chief Executive Officer. Partly as a result of those connections, former BAWAG executives understood, from at least 2002 through 2004, that Refco had misstated its balance sheet.

The Caribbean Losses Emerge

As bad as the Refco connection was, it was merely the thread that unraveled a far larger scandal. Investigators probing BAWAG's Refco dealings discovered something worse: over a billion euros in hidden losses from speculative currency trading through Caribbean off-shore vehicles.

At the heart of these losses was Wolfgang Flöttl, son of former BAWAG CEO Walter Flöttl. According to prosecutors, Flöttl lost 639 million dollars in a single speculation against the Japanese yen in autumn 1998. Until 2000, money continued to be poured in, and the damage grew to 1.44 billion euros.

The Cover-Up Confessed

At the press conference on March 24, 2006, Weninger officially announced the bank's accumulation of €1.3 billion in overall losses. He also stated that he had been informed of these losses by management at the end of 2000. However, at the time, he had decided to conceal the losses in derivatives trading for fear of triggering a bank run by customers and thus possible insolvency. Moreover, he did not inform the rest of the supervisory board members nor BAWAG's former co-owner and major shareholder, the Bayerische Landesbank, which held 46% of its shares. The only trade union representative made aware of the crisis was ÖGB President, Fritz Verzetnitsch.

This admission was extraordinary. A supervisory board chairman publicly confessing that he had concealed billion-euro losses for six years, deliberately deceiving his fellow board members, a major shareholder, and financial regulators.

Government Rescue

Since the Refco scandal in October 2005, the bank almost defaulted on its obligations and had to be bailed out by the conservative government of Wolfgang Schüssel.

The irony wasn't lost on observers: a labor-movement bank owned by socialist unions was rescued by a conservative government. The political ramifications were severe.

SEC Enforcement and Criminal Prosecution

The U.S. Attorney's Office for the Southern District of New York entered into an agreement with BAWAG not to prosecute the bank for its role in assisting Bennett in his scheme to hide the RGHI receivables. BAWAG would forfeit $337.5 million and pay at least $675 million to settle its non-prosecution agreement and related claims against it by the Refco bankruptcy estate.

Nearly $700 million in settlements and forfeitures—on top of the billion-plus in trading losses. The financial damage was staggering.

Criminal Convictions

Several people were found guilty and convicted. Helmut Elsner, former chief executive of Bawag, was found guilty of breach of trust, fraud and false accounting and was sentenced to nine and a half years in prison. The judge also ordered him to repay Bawag €6.8 million in pension benefits.

Elsner was tried along with other top people at the bank and sentenced to nine and a half years in prison. Vienna Federal Court judge Claudia Bandion-Ortner wrote in her verdict: "He gambled with the bank's money as though in a casino."

Political Earthquake

A scandal involving the trade union-owned Labour and Economics Bank has revealed the true extent of the rottenness of the Austrian trade union movement. The Austrian trade union federation is currently experiencing the deepest crisis in its more-than-50-year history. The affair came to light with the announcement of billions in losses incurred by the Bawag following high-risk financial transactions in the Caribbean and through its involvement in the bankrupt US broker house Refco.

Due to increasing public pressure and calls from within the ÖGB for the resignations of the President, Mr Verzetnitsch, and the Secretary for Financial Affairs, Mr Weninger, they both stepped down on 27 March 2006.

The scandal was Austria's Enron moment—a revelation that shattered faith in institutions and led to fundamental questions about governance and accountability.

The Cerberus Era Begins: Private Equity Rescue (2006–2007)

With the scandal exposed and leadership decapitated, the Austrian Trade Union Federation faced an unpalatable choice: find a buyer or watch their bank collapse.

As BAWAG's shareholders were also facing financial trouble, ÖGB decided to sell its entire stake in March 2006. Cerberus was finally chosen in December 2006, beating competitors Bayerische Landesbank, Allianz and Lone Star Funds, and bought 90% of BAWAG for €3.2 billion.

Why Cerberus?

Cerberus Capital Management, the New York-based private equity firm known for distressed investing, was an unusual choice to rescue a labor-movement bank. Cerberus, based in New York, specializes in investing in distressed properties. A consortium led by Cerberus was one of four bidders for Bawag.

Cerberus acquired BAWAG in a highly contested government auction in 2006, paying €3.2 billion. As it turned out, Cerberus invested at a bad moment, thinking that Eastern Europe would grow "infinitely."

The timing was indeed unfortunate. Cerberus closed the acquisition just as the global financial crisis was beginning to gather force. The Eastern European growth thesis that had justified the valuation would collapse along with Lehman Brothers.

The Magnitude of the Challenge

The acquisition followed the bank's entanglement in trading scandals. Cerberus injected additional capital, estimated at over €600 million, to recapitalize the institution and enable divestitures of non-core international assets, such as U.S. brokerage operations, to refocus on domestic retail and commercial banking in Austria. This shift prioritized operational efficiency and risk reduction. Subsequent restructuring efforts from 2007 to 2016 emphasized cost discipline and portfolio streamlining.

Looking back, the condition of the bank they purchased was dire. The institution combined the worst of multiple worlds: hidden losses still emerging, complex off-balance-sheet structures, subscale international operations, undercapitalization, and a culture that had tolerated—even encouraged—speculative excess.

Transforming this mess into a functioning bank would require nearly a decade of painstaking work.

The Turnaround: Cleaning Up and Refocusing (2007–2016)

The Cerberus turnaround proceeded in distinct phases: first stabilization and divestiture, then strategic refocusing, and finally operational excellence.

Divesting Non-Core Assets

In order to transform the bank, the new management sold non-strategic assets, like a 43% stake in Austrian TV operator ATV, foreign subsidiaries Istrobanka to KBC Group in July 2008, BAWAG Bank CZ to Landesbank Baden-Württemberg in September 2008, piano producer Bösendorfer to Yamaha in January 2008 and Stiefelkönig (shoe retailer) in 2011.

Each divestiture represented a rejection of the previous management's empire-building mentality. The message was clear: BAWAG would be a focused retail and commercial bank, not a conglomerate owning piano makers and shoe retailers.

The Transformation Initiative

In 2012, BAWAG P.S.K. began executing a transformational initiative to improve and restructure its operations to improve its financial strength and efficiency. The key pillars of the transformation included re-focusing on core geographic markets and products, driving cost efficiency through disciplined cost management and simplified processes and deleveraging the balance sheet to increase capital and liquidity.

As part of BAWAG P.S.K.'s effort to reduce operating expenses, the bank implemented a new cost management approach, rationalized its business model and simplified its organizational structure. The bank also de-risked the balance sheet, which was achieved predominantly by reducing its exposure to Central and Eastern Europe, exiting proprietary trading, reducing the non-performing loans volume and introducing improved performance management tools.

The Results

As a result BAWAG P.S.K.'s profit before tax increased from €23 million in 2012 to €470 million in 2016, primarily resulting from stronger core revenues and reduced operating expenses.

A twenty-fold increase in profit before tax over four years—this was private equity turnaround execution at its finest.

Over the last 10 years, Cerberus has carried out extensive restructuring at BAWAG, which began making profits in 2014 and has seen strong growth since then. Its return on average equity jumped to 15.56% in 2016 from 7.91% in 2013, while its cost-to-income ratio dropped to 44.4% from 70.3% over the same period.

The cost-to-income improvement from 70% to 44% deserves particular attention. In retail banking, operational efficiency is everything—the bank that can serve customers at the lowest cost wins. This 26-percentage-point improvement represented a fundamental transformation in how the bank operated.

Anas Abuzaakouk: The Turnaround Architect

A critical factor in the transformation was the arrival of Anas Abuzaakouk, who would become one of European banking's most successful transformation leaders.

Anas Abuzaakouk has been the Chief Executive Officer of the bank since 2017. Prior to this, he served as the Chief Financial Officer of the bank from 2014 to 2017. Previously, he served as the Chief Restructuring Officer of the bank from 2012 to 2013. Earlier, he worked as Financial Services Senior Executive at Cerberus from 2007 to 2012.

Abuzaakouk holds a B.S in Finance & Accounting from University of Maryland - Robert H. Smith School of Business. He brings experience from previous roles at BAWAG Group, Cerberus Capital Management and General Electric.

The progression from Cerberus executive to restructuring officer to CFO to CEO tells the story of someone who understood the business from every angle. Abuzaakouk didn't arrive as an external savior—he had been in the trenches of the turnaround from the beginning.

The 2017 IPO: Austria's Biggest Listing

By 2017, the turnaround was complete enough that Cerberus could contemplate an exit. What followed was the largest initial public offering in Austrian history.

BAWAG Group AG's IPO on 25 October 2017 marked the largest IPO in Austrian history. At the event for the start of trading, BAWAG CEO Anas Abuzaakouk rang the opening bell jointly with Christoph Boschan, CEO of the Vienna Stock Exchange.

Scale of the Offering

The Austrian bank's initial public offering yielded proceeds of around EUR 1.93 billion including greenshoe, the largest initial public offering in the history of the Vienna Stock Exchange. Before the IPO of BAWAG Group AG, the ranking was led by Strabag SE (2007: EUR 1.3 bn) ahead of Raiffeisen International Bank AG (2005: EUR 1.1 bn). The initial public offering has been the largest bank IPO in the region of Germany, Austria and Switzerland (DACH) since 2000.

The transaction in 2017 was Europe's third-largest IPO and one of the top 10 IPOs worldwide, based on PWC's latest IPO ranking.

Symbolic Significance

The IPO carried symbolic weight beyond the financial transaction. Almost exactly a decade after the government bailout, BAWAG was returning to public markets—and to Austrian ownership.

The stocks got off to a good start and were added to the leading Austrian index, the ATX, on the second day of trading, 27 October 2017, under the fast-entry rule. At a weighting of more than 4%, it became one of the ATX heavyweights.

Cerberus's Gradual Exit

The IPO was the beginning, not the end, of Cerberus's exit. Cerberus Capital Management sold a 13.5% stake in BAWAG Group for €471 million via an accelerated bookbuilding process in November 2019.

The private equity playbook—buy distressed, fix operations, exit at a premium—had worked. But unlike many private equity stories, this wasn't a tale of financial engineering and leverage. The transformation was real: cost discipline, balance sheet repair, strategic focus. BAWAG had become a genuinely better bank.

The Modern Era: M&A Engine and Geographic Expansion (2017–Present)

With the IPO complete, BAWAG pivoted from turnaround to growth. But this wouldn't be the reckless expansion of the pre-crisis era. Every acquisition would need to meet strict return thresholds and strategic fit criteria.

German Market Entry

BAWAG acquired Südwestbank in December 2017 and completed the acquisition of Deutscher Ring Bausparkasse in September 2018.

Germany represented the natural expansion opportunity—culturally similar, economically stable, and underserved by digitally-focused retail banking.

2021-2022: Building Blocks

BAWAG Group acquired the Dutch digital bank Knab and Barclays Consumer Bank Europe in 2024.

Each acquisition added specific capabilities. The DEPFA Bank acquisition in November 2021 brought public-sector lending expertise. The Hello bank! acquisition in December 2021 added an online securities platform. The Idaho First Bank acquisition in February 2022 established a U.S. foothold.

2024: Transformational Year

The most significant transactions came in 2024, fundamentally reshaping BAWAG's geographic footprint.

BAWAG Group announced the signing of a transaction to acquire 100% of the shares in Knab from ASR Nederland N.V., for a consideration of €510 million payable at closing. This is a great strategic fit in terms of customers, product offering, market presence and team members. The bank was excited to build on the strong Knab brand and expand on the current offering of current accounts, mortgages, and savings products across a large and diverse customer base.

As of Q2 2024, Knab held €17.6 billion in total assets, primarily in Dutch mortgages, €12.3 billion in customer deposits, and €2.5 billion in covered bonds.

On November 1, 2024, BAWAG Group announced the successful completion of the acquisition of Knab, a bank based in the Netherlands.

The second major 2024 acquisition targeted Germany's consumer finance market.

On July 4, 2024, BAWAG Group announced the signing of a transaction to acquire Hamburg-based Barclays Consumer Bank Europe from Barclays Bank Ireland PLC.

Barclays Consumer Bank Europe has been operating successfully in Germany for more than 30 years and is one of the leading providers of credit cards with a genuine credit function. The company's other business areas include consumer loans, installment purchase financing via the online retailer Amazon and overnight money accounts.

On February 3, 2025, BAWAG Group announced the successful acquisition of the Hamburg-based Barclays Consumer Bank Europe from Barclays Bank Ireland PLC.

Financial Performance: The Numbers Tell the Story

The transformation from near-bankrupt union bank to European banking champion is visible in every financial metric.

FY 2024 net profit of €760 million (+11% vs. prior year), EPS of €9.60 and RoTCE of 26.0%. The operating performance was strong with pre-provision profits of €1,083 million and a cost-income ratio of 33.5%.

Core revenues increased by 5% to €1,621.7 million in 2024 versus the prior year. Net interest income was at €1,311.8 million, up by 5% versus 2023.

Capital Strength

At the end of 2024, the CET1 ratio was at 15.2%, an increase of 50 basis points compared to the prior year. The CET1 ratio considers the deduction of €432 million dividend accrual for 2024 as well as the self-funded acquisition of Knab.

Forward Guidance

By 2027, BAWAG plans to generate over €2.7 billion net profit from 2025 through 2027, with net profit of over €1 billion in 2027. The bank is targeting to deliver a return on tangible common equity greater than 20% across all cycles and plans to achieve a cost-income ratio of less than 33% by 2027.

For Q3 2025, the operating performance remained strong with a net profit of €219 million, earnings per share of €2.77, and a RoTCE of 27.8%. This resulted in a net profit of €630 million, €7.98 earnings per share and a RoTCE of 26.9% for the first nine months 2025. BAWAG expects to outperform its full year targets in 2025.

Competitive Positioning: BAWAG in the Austrian Banking Landscape

Understanding BAWAG requires context about Austrian banking more broadly.

Erste Group Bank AG is one of the largest financial service providers in Central and Eastern Europe serving more than 16 million clients in over 2,000 branches in seven countries. Erste Group is headquartered in Vienna and operates as a universal bank.

Raiffeisen Bank International is a key entity of the decentralized Raiffeisen Banking Group in Austria, acting both as the latter's domestic central financial entity and as the holding company for all the group's operations outside of Austria. The bank is listed on the Vienna Stock Exchange.

Major banks in Austria include Erste Group Bank AG (#1), UniCredit Bank Austria AG (#2), Raiffeisen Bank International AG (#3), and BAWAG P.S.K. (#4).

BAWAG's differentiation lies not in size—it's Austria's fourth-largest bank—but in efficiency and profitability. While Erste and Raiffeisen have pursued CEE expansion (with Raiffeisen now facing significant Russia-related complications), BAWAG has focused on developed Western European markets.

Strategic Analysis: What Makes BAWAG Work

The Operational Excellence Model

BAWAG's strategy rests on a few core principles that management has articulated consistently since the turnaround:

The strategy has been unchanged since the beginning of the transformation. The foundation is consistent execution, a continuous improvement mindset, and a "self-help" DNA. The value proposition is about "Providing simple, transparent and affordable financial products and services customers need." The core markets are Austria, Germany, Switzerland, Netherlands (DACH/NL region), Western Europe and the United States.

The Acquisition Playbook

BAWAG pursues earnings-accretive M&A meeting the Group RoTCE target of at least 20%.

This discipline—requiring every acquisition to meet the group's return threshold—prevents the empire-building that characterized pre-crisis BAWAG. Management doesn't do deals for scale or prestige; they do deals that make money.

Investment Considerations: Bull Case and Bear Case

The Bull Case

Operational Excellence as Moat: BAWAG's sub-34% cost-income ratio represents genuine competitive advantage. In a commoditized industry like retail banking, the lowest-cost operator wins. BAWAG has built systems, processes, and culture that consistently extract more efficiency from every revenue euro.

M&A as Growth Engine: Management has demonstrated the ability to acquire and integrate successfully. The Knab and Barclays Consumer Bank Europe acquisitions position BAWAG for continued growth without depending on organic expansion in mature home markets.

Attractive Capital Returns: BAWAG plans to generate over €1 billion in excess capital, after accounting for a 55% dividend payout ratio, which will be deployed towards incremental organic growth, further M&A, and/or capital distributions.

Management Continuity: The Supervisory Board has decided to extend the mandates of all six Management Board members through the end of December 2029. This reflects the long-term commitment of both the Supervisory Board and Management Board members to the long-term profitable growth and success of the Group.

The Bear Case

Interest Rate Sensitivity: Like all retail banks, BAWAG benefits from higher rates. As European rates potentially decline, net interest margin compression could pressure profitability.

Acquisition Integration Risk: The rapid pace of acquisitions—Knab and Barclays Consumer Bank Europe in quick succession—creates integration risk. Cultural mismatches, system integration challenges, or customer attrition could undermine deal economics.

Concentration Risk: BAWAG remains heavily dependent on the Austrian market. Economic downturns in Austria would impact a significant portion of the loan book.

Limited Scale: At roughly 4 million customers, BAWAG lacks the scale economies available to Europe's largest banks. Technology investments must be spread across a smaller revenue base.

Key Performance Indicators to Monitor

For investors tracking BAWAG's ongoing performance, three metrics deserve particular attention:

1. Cost-Income Ratio (CIR): This is the single most important metric for understanding BAWAG's competitive position. Management targets CIR below 33% by 2027, down from 33.5% in 2024. Sustained improvement here validates the operational excellence thesis; deterioration would signal trouble.

2. Return on Tangible Common Equity (RoTCE): At 26% for 2024, BAWAG's RoTCE places it among Europe's most profitable banks. The target of maintaining over 20% "across all cycles" acknowledges that returns will fluctuate with interest rates and credit conditions. Watch whether management actually delivers through-the-cycle returns at this level.

3. NPL Ratio: The NPL ratio remained at a historically low level of 0.8% at the end of the third quarter, reflecting consistently strong asset quality. This metric will be crucial as the acquisition-enlarged loan book seasons and as economic conditions potentially deteriorate.

Conclusion: The Redemption Complete

The BAWAG story is, at its core, a governance story. The pre-crisis bank suffered from precisely the weaknesses that academic literature identifies: concentrated ownership by stakeholders with non-financial objectives, boards populated by loyalists rather than experts, and a culture that prioritized political relationships over risk management.

The intervention of Cerberus—profit-motivated, unsentimental, expertise-focused—represented a governance revolution. Private equity's reputation for ruthless cost-cutting has negative connotations in many contexts, but for BAWAG it was exactly what was needed: discipline, accountability, and focus on economic outcomes rather than political symbolism.

This past year BAWAG delivered a return on tangible common equity of 26% and has averaged 18% over the last 13 years, which included 8 years of zero or negative rates during which the franchise underearned. After delivering a record year in 2024 and closing two transformative acquisitions, BAWAG Group stands as one of the best performing European banks.

The bank founded by Karl Renner to serve workers and oppose capitalist institutions was rescued by American private equity and transformed into a model of operational efficiency. The BAWAG Foundation that sponsored Austrian contemporary art was closed in 2013, replaced by a relentless focus on cost discipline and return metrics.

Is this a tragedy—the loss of a social mission in favor of cold profit maximization? Or is it a success story—the rescue of an institution that would have otherwise destroyed depositors' savings and union workers' pensions?

Perhaps it's both. The pre-crisis BAWAG clothed itself in the language of worker solidarity while its executives gambled with depositors' money in Caribbean tax havens. The post-crisis BAWAG makes no pretense of social mission but actually serves its customers well—with simple, transparent, affordable products delivered efficiently.

After over seven years as a public company, the bank is taking stock on what it has achieved and more importantly focusing on how it has positioned its franchise for growth. Following the transformation over the past decade, BAWAG Group today ranks among the most profitable and efficient banks in Europe, with the financial strength to support customers and local communities.

From Austria's biggest banking scandal to Europe's most efficient bank—the BAWAG redemption is complete.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube