Fast Retailing: The Uniqlo Empire and Japan's Answer to Fast Fashion

I. Introduction & Episode Roadmap

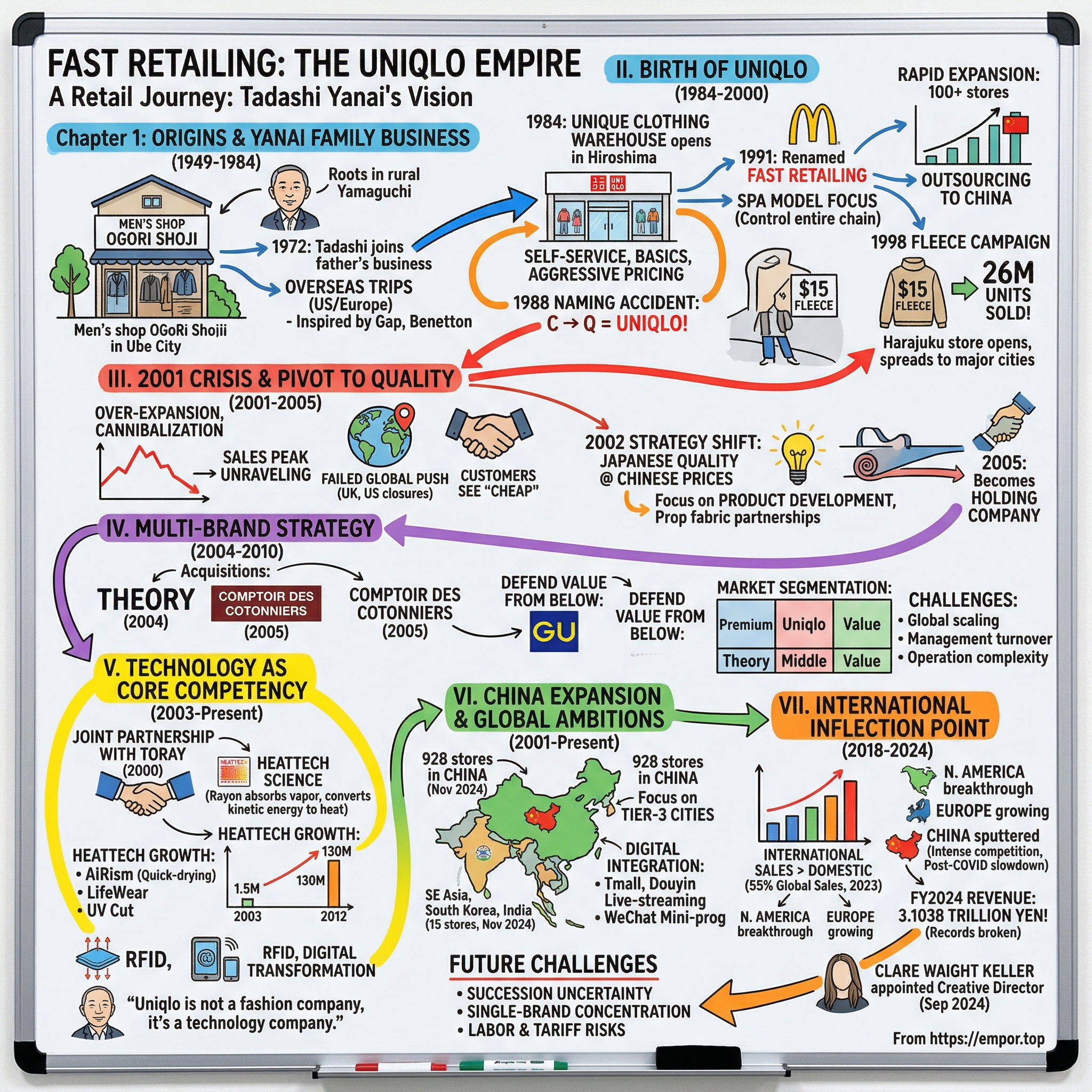

Picture this: A modest 22-store menswear chain tucked away in rural Yamaguchi Prefecture, Japan—the kind of provincial business that typically serves local salarymen and stays local forever. Now fast-forward four decades. That same company commands a market capitalization of approximately $120 billion, operates over 2,500 stores globally, and has fundamentally redefined what affordable quality means in apparel. This is the story of Fast Retailing, parent company of Uniqlo, and its founder Tadashi Yanai—Japan's richest person and perhaps the most underestimated retail visionary of our time.

The central paradox of Fast Retailing's success lies in how it conquered fast fashion by explicitly rejecting everything fast fashion represents. While Zara and H&M chase runway trends with 52 micro-seasons per year, Uniqlo perfected timeless basics. While competitors race to be first, Uniqlo obsesses over being best. While others sell fashion, Yanai insists he sells technology wrapped in fabric.

This transformation didn't happen overnight. It required multiple near-death experiences, radical pivots, and a willingness to completely reimagine what a clothing company could be. From a naming accident that became destiny to betting the company on heat-generating underwear, from acquiring Jil Sander to watching China become both the company's greatest opportunity and biggest challenge—every chapter reveals how an outsider from Japan's countryside built Asia's answer to the global apparel giants.

What makes this story particularly relevant today is timing. Fast Retailing has just crossed a historic inflection point: international sales now exceed domestic Japanese revenue for the first time. The company targets 3 trillion yen in revenue by fiscal 2024 and has set its sights on 10 trillion yen long-term—numbers that would make it the world's largest apparel retailer. But can a company built on Japanese sensibilities and quality truly win globally? Can Yanai's successor—whoever that might be—maintain the founder's paradoxical blend of patience and ambition?

Over the next few hours, we'll trace this journey from a tailor shop above which young Tadashi lived, through the bubble economy boom and bust, into China's shopping malls, and onto Fifth Avenue. We'll examine why Uniqlo works, why the other brands don't, and what it all means for the future of retail. This isn't just a story about selling clothes—it's about how technology, culture, and contrarian thinking can transform an industry. Let's begin where all great business stories do: with a son reluctantly joining his father's struggling shop.

II. Origins & The Yanai Family Business (1949–1984)

The year was 1949, and Japan lay in ruins. Among the entrepreneurs emerging from the postwar devastation was Hitoshi Yanai, who opened a small tailoring shop called Men's Shop Ogori Shoji in Ube City, Yamaguchi Prefecture. Ube wasn't Tokyo or Osaka—it was a modest industrial town known for coal mining and chemical plants, about as far from fashion's cutting edge as you could get. But Hitoshi saw opportunity in providing working men with affordable, practical clothing as Japan rebuilt.

By 1963, Hitoshi had incorporated the business as Ogōri Shōji Co., Ltd., expanding from tailoring into ready-to-wear men's clothing. The shop occupied the ground floor of the family building, with the Yanai family living in the cramped quarters above. This was where young Tadashi Yanai grew up—literally above the store, watching his father work sixteen-hour days, hearing the cash register ring (or not ring) through the floorboards, absorbing the rhythms of retail through osmosis.

Tadashi initially wanted nothing to do with the family business. After graduating from Waseda University with a degree in economics and political science in 1971, he joined Jusco (now Aeon), a major Japanese supermarket chain. The contrast was stark: from his father's single shop to a modern corporation with systems, processes, and scale. But the prodigal son's corporate career lasted just nine months. Whether from family pressure or entrepreneurial restlessness, Tadashi returned to Ube in 1972 to join his father's business.

The homecoming wasn't triumphant. The younger Yanai found the business stagnant, the merchandise boring, the entire operation crying out for modernization. Father and son clashed constantly. Hitoshi believed in traditional Japanese retail values—relationships, service, knowing every customer by name. Tadashi saw inefficiency and missed opportunities. Their first major conflict came when Tadashi wanted to open a new store in Hiroshima, about 100 kilometers from Ube. Hitoshi thought it was too risky, too far from their base. Tadashi persisted. The year was 1972. Yanai was handed the keys to his father's shop in 1972, but it was far from a smooth handover. The young manager brought radical ideas and Western management techniques that clashed violently with the traditional Japanese retail culture. Within two years, all the staff bar one had walked out because of frictions over his management style—six of seven employees quit in what amounted to a mass revolt against the heir apparent. The sole remaining employee, remarkably, still works with him today, over five decades later.

What drove employees away wasn't just strictness but a fundamental reimagining of how retail could work. Yanai had observed something crucial during his brief stint at Jusco: modern retail was about systems, efficiency, and scale. His father's business was about relationships. The younger Yanai believed relationships were important but insufficient. You needed data, processes, and most importantly, a vision beyond your immediate geography.

The transformative moment came during Yanai's buying trips to Europe and the United States in the late 1970s and early 1980s. He took frequent overseas buying trips to the US and Europe—and inspired by brands such as Espirit, Benetton, Gap and Next, Tadashi spotted a gap in the Japanese retail market for a casualwear concept. These weren't luxury brands but democratic ones—fashion for everyone, not just elites. He was particularly struck by how these chains controlled their entire value chain, from design to retail, a model completely foreign to Japanese apparel retail at the time.

Gap, especially, became his North Star. Here was a company that had taken the most basic of garments—jeans, t-shirts, khakis—and built an empire by perfecting fit, quality, and presentation. No seasonal fashion risks, no chasing trends, just relentless optimization of classics. Benetton showed him how a European company could build a global brand through franchising and distinctive marketing. The Limited demonstrated the power of fast inventory turns and data-driven merchandising.

But Yanai didn't just want to copy these Western retailers. He saw an opportunity to combine their operational excellence with Japanese attention to quality and detail. "I wanted to create stores where people could shop for clothes much like they shopped for books or records," he later explained—browsing, self-service, no pressure from sales staff hovering nearby. This was revolutionary in Japan, where personal service was considered sacred.

By 1984, after years of preparation and family negotiations, Yanai was ready to launch his vision. He had convinced his father to let him take full control as CEO, though Hitoshi remained skeptical of his son's grandiose plans. The family business had grown to 22 stores, all operating under various names, all serving local markets, all profitable but unremarkable. Yanai was about to change everything, starting with a single store in Hiroshima that would either vindicate his decade of preparation or prove his father right about the dangers of thinking too big.

III. The Birth of Uniqlo & Early Expansion (1984–2000)

On June 2, 1984, Yanai opened a unisex casual wear store in Fukuro-machi, Naka-ku, Hiroshima, named Unique Clothing Warehouse. The name itself told a story—this wasn't a boutique or a traditional clothing store, but a warehouse, suggesting volume, value, and a certain anti-fashion utility. The store looked nothing like his father's shops. Products were stacked high on industrial shelving. Customers served themselves. Prices were clearly marked—no negotiation, no special deals for regular customers, just transparent, aggressive pricing.

The Hiroshima location was strategic. It was urban enough to attract young consumers but not so expensive that the economics wouldn't work. Yanai had calculated everything: the optimal store size (larger than traditional Japanese shops but smaller than American big boxes), the product mix (70% basics, 30% seasonal items), even the height of the shelving (high enough to create a warehouse feel but not so high as to intimidate Japanese shoppers used to intimate retail spaces).

Then came the accident that became destiny. In 1988, during administration work in Hong Kong for registering the brand, the staff misread the "C" as "Q," leading to the current spelling of Uniqlo. Rather than correct the error, Yanai embraced it. "Uniqlo" had a certain ring to it—modern, memorable, and completely unlike any other Japanese retail brand. It was a happy accident that would prove prophetic: the company's greatest successes would often come from turning apparent mistakes into advantages.

The timing couldn't have been better. Japan in the late 1980s was experiencing the height of its bubble economy. Consumers had money and wanted to express their individuality, but not everyone could afford designer brands. Uniqlo positioned itself perfectly in the middle—better than discount stores, more affordable than department stores, and crucially, free from the stuffy formality that characterized much of Japanese retail.

In 1991, Yanai renamed his father's business from Ogori Shoji to the more globally identifiable Fast Retailing, a nod to the fast-food prototype. The name change signaled ambition far beyond Japan. Yanai had studied McDonald's and saw parallels: standardized products, consistent quality, efficient operations, and most importantly, the ability to scale globally. If Ray Kroc could turn hamburgers into a worldwide empire, why couldn't someone do the same with basic clothing?

The real breakthrough in expansion came from an insight about Japanese consumers that seems obvious in retrospect but was revolutionary at the time. Japanese shoppers, Yanai realized, were tired of being told what to wear each season. They wanted quality basics they could mix and match, layer and personalize. While other retailers pushed fashion trends, Uniqlo would perfect the white shirt, the selvedge jean, the cashmere sweater—items that never went out of style.

This philosophy drove rapid expansion through the 1990s. He grew the company to over 100 stores within three years of the Fast Retailing rebrand. Each new store followed the same template: large format, self-service, clear pricing, and a product mix heavy on basics. But Yanai learned quickly that physical expansion alone wouldn't be enough. He needed to control the entire value chain.

The SPA (Specialty store retailer of Private label Apparel) model, pioneered by Gap, became Yanai's obsession. Instead of buying from wholesalers who bought from manufacturers who bought from fabric mills, Fast Retailing would control everything from design to retail. This meant massive capital requirements and operational complexity, but also the ability to maintain quality while driving down costs.

Uniqlo outsourced their clothing manufacturing to factories in China, where labour was cheap. But this wasn't just about cost arbitrage. Yanai personally visited factories, worked with them to improve quality, and established long-term partnerships rather than constantly switching to the lowest bidder. He applied Japanese manufacturing principles—kaizen, just-in-time inventory, total quality management—to Chinese textile production.

The approach paid off spectacularly when Japan's bubble economy burst in 1991. Japan was in the depths of a recession at the time, and the low-cost goods proved popular. While department stores struggled with excess inventory of expensive designer goods, Uniqlo's $15 fleece jackets flew off the shelves. The recession, paradoxically, accelerated Uniqlo's growth. Consumers who once shopped at department stores traded down to Uniqlo and discovered that lower prices didn't mean sacrificing quality.

In November 1998, it opened their first urban Uniqlo store in Tokyo's Harajuku district, and outlets soon spread to major cities throughout Japan. The Harajuku store was a statement of intent. This trendy district was the heart of Japanese youth culture, home to luxury brands and cutting-edge fashion. For Uniqlo to open there was audacious—like Walmart opening on Fifth Avenue. But Yanai knew that to become a national brand, he needed to win in Tokyo.

The Tokyo expansion coincided with Uniqlo's most successful product launch ever: the fleece campaign of 1998. Its debut campaign was a lightweight fleece for just $15, which caused a sensation amid the cost-conscious post-bubble economy. The company sold 2 million units in the first year, then 8.5 million the next, then 26 million. The fleece became a phenomenon—everyone from students to CEOs owned one. It proved that Uniqlo could create products that transcended class and age, that utility and style weren't mutually exclusive.

By 2000, Uniqlo operated over 400 stores across Japan with sales approaching 300 billion yen. The company had gone public in 1994 on the Hiroshima Stock Exchange, then moved to the Tokyo Stock Exchange in 1997. Yanai was being hailed as a retail genius, Japan's answer to Sam Walton or Leslie Wexner. But success was breeding complacency, and the very strategies that had driven growth were about to become liabilities. The company was heading for its first major crisis.

IV. The 2001 Crisis & Pivot to Quality (2001-2005)

The year 2001 marked a stunning reversal. In 2001, sales turnover and gross profit reached a peak, with over 500 retail stores in Japan, but the very next year, everything began unraveling. The problem wasn't a single crisis but a cascade of failures that exposed fundamental flaws in Uniqlo's rapid expansion model.

Yanai had become intoxicated by growth. The company was opening stores at a breakneck pace—sometimes multiple locations per week—without considering cannibalization or market saturation. Quality control slipped as the company prioritized volume over everything else. Customers began complaining that Uniqlo had become "cheap" in the worst sense—shoddy materials, poor construction, uninspiring designs. The brand that had once stood for value was becoming synonymous with disposable.

The international expansion turned into a disaster. In 2001, Uniqlo opened 21 stores in the U.K. only to shut 16 of them within two years after miserable results. The UK venture hemorrhaged money—360 million yen in losses by 2002. In 2005, Uniqlo opened its first three U.S. stores in New Jersey, but all were closed by the following year. "We were nobody," Yanai says of that period.

The root cause of the international failures went deeper than mere execution problems. As President Yanai subsequently remarked regarding the failure in UK that "There is absolutely no familiarity with UNIQLO (overseas). You can't expect a brand to sell if people don't know it. This was not a matter of good or bad products, the problem was one step before". Uniqlo had assumed its Japanese success would translate automatically to Western markets, but British and American consumers saw the brand as generic Asian discount wear—if they saw it at all.

Back in Japan, the situation was equally dire. Same-store sales plummeted. The stock price crashed from over 12,000 yen in 2000 to below 3,000 yen by 2002. Analysts who had celebrated Yanai as a visionary now questioned whether Uniqlo was just another bubble-era phenomenon that couldn't survive in the harsh light of recession. Some predicted the company would need to close half its stores to survive.

But the crisis forced Yanai to confront uncomfortable truths about his business model. During a company retreat in 2002, he shocked executives by announcing that Uniqlo would completely pivot its strategy. No more chasing volume. No more competing on price alone. Instead, the company would focus on what Yanai called "Japanese quality at Chinese prices"—a seemingly impossible equation that would require reimagining every aspect of the business.

The transformation began with product development. Yanai created teams of designers and technical specialists who would spend months perfecting a single item—the perfect white shirt, the ideal pair of jeans, the ultimate winter coat. He established partnerships with textile manufacturers to develop proprietary fabrics. Most radically, he decided that Uniqlo would carry fewer SKUs but ensure that each item was best-in-class for its price point.

When Uniqlo decided to expand overseas, it separated Uniqlo from the parent company, and established Fast Retailing (Jiangsu) Apparel Co., Ltd. in China. In 2002, their first Chinese Uniqlo outlet was opened in Shanghai, marking a strategic shift from failed Western expansion to focusing on Asia where the brand's value proposition resonated more naturally.

The company also underwent a crucial corporate restructuring. On 1 November 2005, Fast Retailing transferred the business related to clothing manufacturing and retailing to Sun Road Co., Ltd., a wholly owned subsidiary that operated golf courses through a company split (absorption-type split), and became a holding company. This transformation into a holding company structure would prove essential for Fast Retailing's next phase—building a portfolio of brands rather than relying solely on Uniqlo.

The pivot to quality over quantity was painful. Revenues initially declined as the company closed underperforming stores and reduced inventory. But gradually, customers began noticing the difference. The fleece was softer. The t-shirts held their shape after washing. The down jackets were as warm as those costing three times more. Word spread that Uniqlo had changed, that it was no longer just cheap but genuinely good value.

By 2005, the company had stabilized and was ready to attempt international expansion again, but this time with hard-won wisdom. 2005 saw more overseas expansion, with stores opening in the United States (New York City), Hong Kong (Tsim Sha Tsui) and South Korea (Seoul). The approach was completely different—flagship stores in premium locations to build brand awareness first, then gradual expansion once the market understood what Uniqlo represented.

The crisis of 2001-2005 could have destroyed Fast Retailing. Instead, it became the crucible in which the modern Uniqlo was forged—a brand that would never again mistake growth for success or confuse cheap with value. The lessons learned during these dark years would guide every major decision for the next two decades.

V. The Multi-Brand Strategy: Theory, Comptoir des Cotonniers & GU (2004-2010)

Even as Yanai was rescuing Uniqlo from its crisis, he understood a fundamental problem: relying on a single brand, no matter how successful, was dangerous. The world's great apparel companies—LVMH, Kering, VF Corporation—all operated portfolios. They could weather the cyclical nature of fashion, capture different market segments, and cross-pollinate ideas between brands. In 2004, with Uniqlo stabilized, Yanai embarked on his most ambitious strategy yet: transforming Fast Retailing into a multi-brand powerhouse.

The first major move came in January 2004 when Fast Retailing acquired "an equity stake in Link Theory Holdings Co., Ltd., the marketer of the Theory and Helmut Lang apparel brands". Theory represented everything Uniqlo wasn't—premium pricing, fashion-forward design, and a sophisticated urban customer base. Founded by Andrew Rosen in 1997, Theory had revolutionized contemporary fashion with its concept of the "urban uniform"—impeccably tailored pieces in luxurious fabrics that could transition seamlessly from boardroom to dinner.

The Theory acquisition wasn't just about diversification; it was strategic education. Fast Retailing had held a 32.32% stake in LTH since 2004. In spring 2009, Fast Retailing acquired the remaining stock and LTH became a fully owned subsidiary of Fast Retailing. The total investment approached 240 million euros, a massive bet for a company that had nearly collapsed just years earlier. But Yanai saw Theory as a laboratory for understanding premium retail—how to command higher prices, how to work with luxury fabrics, how to appeal to fashion-conscious consumers without chasing trends.

Theory also brought an unexpected bonus: Helmut Lang, the Austrian designer's eponymous brand that had defined minimalist cool in the 1990s. Though the brand had lost its founder and much of its cachet, owning Helmut Lang gave Fast Retailing credibility in fashion circles that no amount of marketing could have bought. It was like a tech company acquiring a prestigious research lab—the immediate revenue mattered less than the knowledge and reputation gained.

While Theory elevated Fast Retailing's fashion credentials, Yanai recognized he also needed to defend Uniqlo's value position from below. Enter GU (initially pronounced "jee-you"), launched in 2006 as Fast Retailing's answer to ultra-fast fashion. If Uniqlo was about timeless basics at reasonable prices, GU would be about trend-driven fashion at rock-bottom prices. The brand's motto was simple: "Fashion for everyone, every day."

Successful acquisition of the Comptoir des Cotonniers brand, founded in Paris in 1995, with boutiques in Belgium, Germany, the United Kingdom, South Korea, the United States and Japan. Comptoir des Cotonniers Japan Co, Ltd. was established shortly thereafter. This French brand, specializing in feminine, romantic clothing for mothers and daughters, gave Fast Retailing a foothold in European fashion sensibility. Unlike the Theory acquisition, which was about learning premium retail, Comptoir des Cotonniers was about understanding European taste and expanding Fast Retailing's geographic and demographic reach.

The multi-brand strategy revealed Yanai's sophisticated understanding of market segmentation. Theory would capture the premium contemporary market ($200 t-shirts), Uniqlo would dominate the middle ($20 t-shirts), and GU would own the value segment ($5 t-shirts). Comptoir des Cotonniers and Princesse Tam. Tam (lingerie) would provide specialized offerings for specific demographics. In theory, this portfolio approach was brilliant—Fast Retailing could capture a customer at GU in their twenties, graduate them to Uniqlo in their thirties, and Theory in their forties.

But execution proved far more challenging than strategy. Theory struggled to expand beyond its American base, with cultural differences making global scaling difficult. The brand's New York sophistication didn't translate easily to Tokyo or Paris. Management turnover was constant, with creative directors and CEOs cycling through regularly. While Theory maintained its quality and reputation, it never achieved the explosive growth Yanai had envisioned.

GU faced different challenges. The 999 yen jeans of the G.U. brand become a bestseller in Japan, proving the concept could work. But competing at the very bottom of the market meant razor-thin margins and constant pressure to cut costs. Quality inevitably suffered, and GU developed a reputation as "Uniqlo's cheaper cousin"—not exactly a compelling brand proposition. The cannibalization Yanai had hoped to avoid became reality, with GU stealing price-conscious customers from Uniqlo rather than bringing in new ones.

The portfolio strategy also created operational complexity that Fast Retailing struggled to manage. Each brand needed its own design team, marketing strategy, supply chain, and store operations. The synergies Yanai had expected—shared factories, cross-brand innovation, management expertise—proved elusive. Theory's designers didn't want to work with Uniqlo's technical teams. GU's fast-fashion model conflicted with Uniqlo's quality-first approach. Comptoir des Cotonniers' French management resisted Japanese efficiency initiatives.

By 2010, the verdict on Fast Retailing's multi-brand strategy was mixed at best. Theory remained profitable but niche. GU was growing but diluting the parent company's reputation for quality. The European brands were beautiful but subscale. Most tellingly, Uniqlo still generated over 80% of Fast Retailing's revenue and an even higher percentage of profits. The portfolio hadn't failed, but it hadn't transformed Fast Retailing into the Japanese LVMH either.

Yet the multi-brand years weren't wasted. Each acquisition taught Fast Retailing valuable lessons. Theory showed how to elevate product and price. GU revealed the limits of competing on price alone. The European brands demonstrated the importance of cultural authenticity. Most importantly, the struggles of managing multiple brands convinced Yanai that Uniqlo's true competitive advantage lay not in portfolio diversification but in doing one thing extraordinarily well. The stage was set for Uniqlo's next evolution: from clothing retailer to technology company.

VI. The Jil Sander Partnership & Premium Push (2009-2011, 2020-2021)

The morning of March 23, 2009, fashion insiders around the world did a collective double-take. Fast Retailing signed a design consulting contract for Uniqlo products with fashion designer Jil Sander in March 2009. Sander was appointed creative director of the brand's menswear and womenswear. This wasn't just any designer—Sander was the "Queen of Less," the woman who had defined minimalism in fashion, whose uncompromising vision had made her a legend. And she was partnering with. Uniqlo?

The collaboration seemed impossible on paper. Sander's mainline collections sold $2,000 coats to fashion's elite. Uniqlo sold $50 jackets to everyone. She was famous for walking away from her own brand twice rather than compromise her vision. Yanai was famous for relentless optimization and mass production. Yet both shared an obsession with perfection, a belief that good design should be democratic, and most importantly, a conviction that fashion had lost its way in pursuit of novelty over quality.

In 2009, UNIQLO and legendary fashion designer Jil Sander launched "+J". The name itself was elegantly simple—a plus sign suggesting addition, collaboration, something extra, followed by J for Jil. It challenged conventions in its mission to improve life with thoughtfulness, accessibility, and high-quality pieces.

The first +J collection launched in October 2009 to scenes of near-pandemonium. At Uniqlo's flagship stores in Tokyo, Paris, and New York, lines formed before dawn. The collection sold out within hours—not days, hours. Fashion editors who normally wouldn't be caught dead in Uniqlo were photographing themselves in +J trenches and cashmere knits. The pieces looked like Jil Sander mainline but cost 95% less. A navy wool coat that would have been $3,000 at Barneys was $150 at Uniqlo.

But +J wasn't just Jil Sander designs at Uniqlo prices—it was a philosophical merger. "I set out to define the global modern uniform with this in mind: Clothes should be longlasting and enduring," Sander said in a statement. She brought her perfectionist approach to every detail: the weight of a button, the angle of a lapel, the precise shade of navy. Uniqlo's technical teams, accustomed to iterating products based on data, found themselves in lengthy debates about the metaphysical properties of a perfect white shirt.

The collaboration elevated both partners. For Uniqlo, +J provided instant fashion credibility, proving the brand could attract the world's most respected designers. For Sander, who had been without a platform since leaving her namesake brand, it offered the chance to realize her democratic vision of design—beautiful clothes for everyone, not just the wealthy. The German designer, known for her meticulous attention to detail, designed the +J range for Uniqlo from 2009 to 2011.

Each +J collection became an event. Fashion bloggers dissected lookbooks like religious texts. Resellers bought armfuls to flip on eBay at multiples of retail price. Most remarkably, +J items held their value—a $200 +J coat from 2010 might sell for $400 on the secondary market years later, unheard of for fast fashion. The collaboration had achieved something thought impossible: it made Uniqlo collectible.

In 2011, Uniqlo discontinued its cult-favorite collaboration with Jil Sander after a short two-year run. Save for a "greatest hits" drop in 2014, the +J line came and went in what seemed like a flash of a second. She left the Japanese company and briefly resurfaced at her eponymous label for three seasons before effectively retiring from fashion. The departure was amicable but left a void. Uniqlo had tasted high fashion success, and customers wanted more.

For nearly a decade, +J remained a legend, a high-water mark for designer collaborations. Uniqlo continued working with other designers—Christophe Lemaire, Alexander Wang, JW Anderson—but none captured the magic of +J. The collaborations felt either too commercial or too niche, lacking the perfect balance Sander had achieved. Meanwhile, fashion had continued its acceleration toward disposability, with ultra-fast fashion brands like Shein making Zara look slow.

Then came 2020 and COVID-19. The pandemic forced a global reconsideration of consumption, quality, and what really mattered in clothing. Suddenly, Sander's philosophy of "longlasting and enduring" pieces felt prophetic. People stuck at home didn't need party dresses; they needed perfect basics that would last. In this context, Uniqlo made a bold move: bringing back +J.

"+J" made its return in Fall/Winter 2020 to the excitement of fans worldwide. On Friday, Uniqlo will begin selling a new collection that revives a popular tie-up with German minimalist designer Jil Sander, with looks and prices beyond the store's usual lineup. The 2020 revival during COVID wasn't just nostalgia—it was strategic timing. Fashion designer Jil Sander returns to Uniqlo with her signature modern style.

The new +J was both familiar and evolved. The collection features many of Sander's minimalist tendencies and pared down design signatures, from understated tailoring to sculptural silhouettes in a neutral color palette. Outerwear designs include hybrid down styles, military jackets and cashmere blend coats. But there were concessions to the new reality—more comfortable fits for working from home, technical fabrics that could transition from video calls to outdoor walks, prices slightly higher than 2009 but still revolutionary for the quality offered.

The 2020 launch was even more successful than the original. Despite pandemic restrictions, socially distanced lines formed at stores. The online allocation crashed Uniqlo's website in multiple countries. The collection that was supposed to last through the season sold out in days. +J had proven that the appetite for democratic luxury hadn't diminished—if anything, it had grown stronger.

The +J partnership represented something larger than successful product launches. It proved that the binary between "fast fashion" and "luxury" was false. Quality, design, and accessibility weren't mutually exclusive. Most importantly for Fast Retailing, it established Uniqlo not as a fashion brand chasing trends, but as a platform where the world's best designers could realize democratic visions. This positioning would prove crucial as Uniqlo prepared for its most ambitious expansion yet: conquering China and the rest of Asia.

VII. The China Expansion & Global Ambitions (2001-2020)

By 2001, it had ventured into the Chinese market, opening its first store in Shanghai—a decision that would prove to be the most consequential in Fast Retailing's history. While Western expansion had failed spectacularly, China represented something different: a massive population discovering middle-class consumption, a culture that valued quality and durability, and crucially, geographic and cultural proximity to Japan that made operations manageable.

Uniqlo entered the Chinese mainland in 2002. As of November 2024, there are 928 stores in China. But the path from one store to nearly a thousand wasn't linear. The early years were about learning—understanding Chinese sizing preferences (generally smaller than Western but different from Japanese), navigating complex regulations, building relationships with local partners, and most importantly, positioning Uniqlo not as a foreign luxury brand but as accessible quality for China's emerging middle class.

The 2008 Financial Crisis became an unexpected accelerator. While Western retailers retreated from international expansion, Yanai saw opportunity in crisis—a philosophy ingrained from Japan's own economic struggles. Chinese consumers, suddenly more price-conscious but still aspirational, found Uniqlo's value proposition perfect. The company aggressively expanded while real estate costs plummeted and competitors pulled back.

On 2 September 2009, Fast Retailing announced that the company would target annual group sales of 5 trillion yen (approx. US$61.2 billion) and pretax profit from operations of 1 trillion yen (approx. US$12.2 billion) by 2020. This meant that the company was aiming to be the world's biggest specialty retailer of private label apparel. The company also aimed for a growth rate of 20% per year. The company's international business target included one trillion yen in China, one trillion in other Asian countries, and one trillion in Europe and the United States.

These weren't just ambitious targets—they were a complete reimagining of what Fast Retailing could become. The "trillion yen" framework forced the company to think beyond incremental growth. China alone would need to become as large as the entire Japanese operation. This required not just more stores but a fundamental rethinking of how Uniqlo operated internationally.

The China strategy evolved through distinct phases. First came the coastal megacities—Shanghai, Beijing, Guangzhou—where international brands were expected and purchasing power was highest. At present, the majority of Uniqlo stores are located in Tier-1 cities in China. Meanwhile, the company is focusing significantly on expanding its presence in Tier-3 cities where there is potential for rapid growth. Recognizing the sinking market phenomenon in China, the company has been strategically opening new stores in these lower-tier cities as part of a broader expansion plan to tap into less saturated markets. As of Summer 2023, nearly half of the newly opened Uniqlo stores in China are located in third-tier and fourth-tier cities.

But Uniqlo's real breakthrough in China came from understanding that Chinese consumers weren't just looking for cheap clothes—they wanted quality that lasted, designs that were versatile, and increasingly, technology that solved real problems. HeatTech became a phenomenon in northern China's harsh winters. AIRism found devoted followers in the humid south. The minimalist aesthetic that had seemed too plain for Western consumers resonated with Chinese millennials who valued subtlety over logos.

Digital integration proved crucial. Moreover, the success of Uniqlo in China is significantly fueled by its strong e-commerce presence. With 84% of internet users in China shopping online, platforms like Tmall, Douyin Shop, and WeChat Mini Programs are vital to reaching consumers. Uniqlo's strategic utilization of these platforms has paid off handsomely. It was evidenced by its top-10 sales ranking on Tmall for three consecutive months as of February 2024. Furthermore, Uniqlo has clinched the Tmall Double Eleven championship for six years in a row. The brand also saw a remarkable 25% year-on-year increase in live broadcast sales during the first half of fiscal year 2024. As such, it amounted to RMB 390 million and accounted for 20% of total e-commerce sales.

The company didn't just sell through Chinese platforms—it integrated into the Chinese digital ecosystem. WeChat mini-programs allowed customers to check inventory, reserve items, and even get styling advice. Live-streaming events on Douyin (TikTok's Chinese version) turned product launches into entertainment. Uniqlo became one of the first international retailers to truly understand that in China, online and offline weren't separate channels but parts of an integrated experience.

Uniqlo started to have a bigger focus on countries outside of Japan, as you can see by the number of stores in Japan decreasing from 853 at their highest point down to 800 stores, while stores in China skyrocketed from 178 to 1031 stores. This wasn't just expansion—it was a fundamental shift in Fast Retailing's center of gravity. By 2018, Greater China (including Hong Kong and Taiwan) had become Uniqlo's largest market by store count.

Meanwhile, the company continued pushing into other Asian markets. 2005 saw more overseas expansion, with stores opening in the United States (New York City), Hong Kong (Tsim Sha Tsui) and South Korea (Seoul), their South Korean expansion being part of a joint venture with Lotte. Each market required unique adaptations—smaller sizes in Southeast Asia, more colorful designs in India, weather-appropriate materials in tropical climates—but the core value proposition remained consistent.

The global financial performance reflected this Asian-centric strategy. Uniqlo in China is contributing for more than a quarter of Fast Retailing's revenue, with a year-to-year growth of 15.2%. But success brought new challenges. The U.S.-China trade war created uncertainty. Competition from Chinese domestic brands intensified. Most recently, the China growth engine began sputtering.

By 2020, Fast Retailing had largely achieved its geographic expansion goals, with over 2,000 stores internationally. But the question was no longer about presence—it was about purpose. Could a Japanese company truly become global? Could it maintain quality while operating at massive scale? And most pressingly, what would happen when China, the growth engine of two decades, began to slow? The pandemic was about to provide unexpected answers.

VIII. Technology as Core Competency: HeatTech, AIRism & Digital Transformation (2003–Present)

Yanai's famous quote captures everything: "Uniqlo is not a fashion company, it's a technology company." This wasn't marketing spin—it was a fundamental reconceptualization of what a clothing company could be. While competitors chased runway trends, Uniqlo invested in molecular engineering. While others focused on design, Uniqlo obsessed over functionality. The result would transform not just the company but the entire concept of performance apparel.

The story began in 2000 at a management meeting between Fast Retailing and Toray Industries, Japan's leading chemical and fiber company. The story began at a management meeting between the two companies that took place back in 2000. Yanai had just achieved his fleece triumph and was looking for the next breakthrough. HEATTECH is an innovative new material that UNIQLO developed jointly with global textile maker Toray. To achieve the ultimate in warmth and comfort, we created more than 10,000 prototypes.

It started in 2003, when we received a request from UNIQLO asking us: "Can you develop a thin and warm material that could be worn under denim?" The request seemed simple but was technically audacious. Traditional thermal underwear was bulky, uncomfortable, and unfashionable. Yanai wanted something that generated heat, felt like a second skin, and could be worn invisibly under regular clothes.

A joint partnership between UNIQLO and textile manufacturers Toray brought about this clothing that is an epitome of comfort and warmth during winters. The HEATTECH is made with special blends of products that wick the moisture from the human body and convert the kinetic energy into heat. The very fibers of this clothing absorb the heat and keep the body warm. The science was elegant: "The first is that it absorbs moisture and generates heat," Onishi explains. "Our bodies produce water vapour without us realising it, and the rayon inside HEATTECH® fabric absorbs that vapour. When that happens, the moisture molecules try to move around, converting that kinetic energy into heat energy. The material traps the generated heat in air pockets and maintains warmth."

But developing the technology was only half the challenge. HEATTECH cannot be made with ordinary equipment. The fabric is made on dedicated production lines. Uniqlo had to convince factories to invest in specialized equipment, train workers in new techniques, and maintain quality standards that were unprecedented for what was essentially underwear. The investment was massive—hundreds of millions of dollars before a single product was sold.

This clothing has been in the market since 2003 and since then they have constantly been improving based upon the customer reviews. The first generation of HeatTech was good but not revolutionary. It generated some warmth but pilled easily and lost shape after washing. Rather than rush to market, Yanai insisted on continuous improvement. Much of the development comes out of a dedicated weather simulation chamber at Uniqlo's Tokyo head office: a large laboratory equipped to replicate various climate and humidity conditions, including plunging negative temperatures that would have any Scandinavian feeling right at home.

The breakthrough came with version 2.0 in 2006. In 2003, 1.5 million HeatTech products were sold while in 2012 over 130 million units were sold across 250 items. The exponential growth wasn't just about improved technology—it was about creating a new category. HeatTech wasn't competing with other thermal underwear; it was replacing the need for heavy winter clothing entirely.

HEATTECH – the Japan technology wear from UNIQLO that sold 28 million units worldwide last year. HEATTECH, jointly developed by UNIQLO and world leading textile manufacturer TORAY INDUSTRIES, has gone from strength to strength since its launch in 2003. Sales reached 28 million units last winter as many customers purchased HEATTECH items. By 2009, HeatTech had become a phenomenon, with dedicated marketing campaigns and customers lining up to buy multiple pieces.

But Yanai wasn't satisfied with one innovation. Besides HeatTech, Uniqlo has also created AIRism (a soft fabric with quick-drying inner fabric), LifeWear (a blend between casual and sportswear) and UV Cut (material designed to prevent 90% of ultraviolet rays from reaching the wearer) technologies. Each technology addressed a specific problem: AIRism for hot, humid weather; UV Cut for sun protection; LifeWear for the athleisure trend.

The technology push extended beyond fabrics to retail operations. Uniqlo became one of the first fashion retailers to fully embrace RFID (Radio Frequency Identification) tags, allowing instant inventory tracking and self-checkout. Digital mirrors in fitting rooms could suggest complementary items. The Uniqlo app integrated with stores to check inventory, reserve items, and even navigate to specific products in-store.

For example, they launched the "fast-moving images" campaign for HEATTECH. They put up digital billboards in busy Australian spots and ran online ads with images flashing so fast you couldn't read them—unless you took a photo. Each photo revealed a code that unlocked product videos, discounts, and gifts. The campaign reached 4M people and brought in 35,000 new customers, earning UNIQLO a Shorty Award for Best in Retail and E-Commerce in Social Media.

The pandemic accelerated Uniqlo's digital transformation. While competitors struggled with store closures, Uniqlo's integrated online-offline model thrived. Customers could buy online and pick up in store, try in store and have items delivered, or use the app to access virtual styling sessions. The company's e-commerce sales doubled in many markets during 2020-2021.

But the real innovation wasn't any single technology—it was the systematic approach to innovation itself. Ishii: We have a cycle where we create new prototypes of materials in discussion with UNIQLO, then remake them, discuss again, then do it again—particularly when it comes to developing technologies for the medium to long term future. The end result of this collaborative process is innovative LifeWear like HEATTECH, AIRism, and Ultra Light Down, which UNIQLO sells around the world today.

This technology-first approach fundamentally changed Uniqlo's economics. While fashion brands typically achieve 50-60% gross margins through high markups on trend-driven items, Uniqlo achieved similar margins through technical innovation and scale. A HeatTech shirt might cost only marginally more to produce than a regular shirt, but customers willingly paid premium prices for the functionality.

More importantly, technology created defensibility. Anyone could copy a design, but recreating HeatTech required years of R&D, specialized equipment, and deep partnerships. One of Uniqlo's signature innovations is HeatTech, a fabric developed in conjunction with Toray Industries (a Japanese chemical company) that turns moisture into heat and has air pockets in the fabric to retain that heat. Competitors could sell thermal underwear, but they couldn't sell HeatTech.

The technology strategy also changed how customers thought about Uniqlo. No longer was it just affordable basics—it was innovative solutions to everyday problems. Customers didn't just buy Uniqlo clothes; they bought HeatTech for winter, AIRism for summer, UV Cut for outdoor activities. The brand had successfully created a functional wardrobe ecosystem, with technology as the differentiator. This positioning would prove crucial as Uniqlo entered its most challenging phase yet: becoming a truly global brand.

IX. The International Inflection Point (2018–2024)

The year 2023 marked a watershed moment in Fast Retailing's history. By 2023, Uniqlo's international revenue accounted for 55% of its global sales, surpassing domestic sales for the first time. This wasn't just a statistical milestone—it represented the culmination of two decades of international expansion and the birth of Fast Retailing as a truly global company. The Japanese retailer from rural Yamaguchi had officially become more international than domestic.

The transformation was driven by explosive growth across multiple markets. UNIQLO North America and UNIQLO Europe both generated large increases in revenue and profit on the back of growing customer support for LifeWear and strong sales. Uniqlo had a large revenue increase of 32.8% in North America to JPY217.7bn and its operating profit rose 65.1% to JPY34.8bn. North America, long considered Uniqlo's white whale, was finally delivering meaningful profits. The strategy of flagship stores in major cities, combined with improved e-commerce and better understanding of American sizing and preferences, had finally clicked.

Europe told an even more dramatic story. It was a similar positive story in Europe with a large revenue increase of 44.5% to JPY276.5bn and a 70.1% operating profit climb to JPY46.5bn. European consumers, traditionally skeptical of non-European fashion brands, had embraced Uniqlo's quality-first approach. The success was particularly pronounced in markets like France and Germany, where Uniqlo's understated aesthetic and technical fabrics resonated with local preferences for functional elegance.

But the international success story had a notable exception: China. The market that had driven Uniqlo's growth for two decades was suddenly sputtering. For China, where sales and profit declines extended into the latest quarter, the company is closing under-performing stores and revamping bigger and better-located outlets to drive sales. Revenue in the mainland fell 5%, and profits dropped 3% in the third quarter from March to May, marking a 10% decline in Greater China profit for the full business year.

The China challenges were multifaceted. Competition from domestic brands like Anta and Li-Ning had intensified, offering similar quality at lower prices with designs more attuned to local tastes. The post-COVID economic slowdown dampened consumer spending. Most critically, Chinese consumers, once enamored with foreign brands, were increasingly embracing domestic alternatives in a wave of cultural nationalism. Uniqlo, despite two decades of success, was discovering that past performance didn't guarantee future results.

Yet even as China struggled, other Asian markets compensated. Internationally, Uniqlo saw revenue up and a slight rise in profit in the greater China region, while South Korea, South East Asia, India and Australia enjoyed large revenue and profit gains. Southeast Asia proved particularly promising, with young populations embracing Uniqlo's affordable quality. In 2023, Uniqlo accelerated its global expansion, opening its first store in Mumbai, India, and announcing its entry into the Brazilian market. On October 2019, Uniqlo opened its first Indian store in New Delhi. As of November 2024, there are 15 stores in India.

The India entry was strategic beyond mere expansion. With China slowing, India represented the next great growth market—a massive population entering middle-class consumption, a young demographic open to international brands, and a climate perfectly suited for Uniqlo's technical fabrics. The Mumbai flagship store opening drew crowds reminiscent of Uniqlo's early days in China, suggesting the potential for another two-decade growth story.

Financial performance reflected this global rebalancing. FY2024 revenue: 3.1038 trillion yen (+12.2% year-on-year), operating profit: 500.9 billion yen (+31.4%), and profit attributable to owners of the parent: 371.9 billion yen (+25.6%). Revenue topped 3 trillion yen and operating profit surpassed 500 billion yen for the first time. These weren't just records—they represented Fast Retailing achieving the scale Yanai had targeted fifteen years earlier.

The international success was also changing Uniqlo's product development. Product development and communications were once centered on Japan, but the more global they are, the bigger the impact. Indeed, products such as Washable Knit Rib Pants, Bra Tops, and Sports Utility Wear, developed based on European and American feedback, have sold well globally. Uniqlo was no longer exporting Japanese products globally but creating global products informed by diverse markets.

Digital transformation accelerated during this period. The pandemic had forced rapid adoption of online-to-offline integration, and Uniqlo emerged with one of retail's most sophisticated omnichannel operations. Customers could browse online, try in store, buy via app, and receive same-day delivery in major cities. RFID tags enabled real-time inventory tracking across channels. The distinction between online and offline had effectively disappeared.

But the international inflection point also revealed structural challenges. UNIQLO is Fast Retailing's core business, generating 84 percent of group revenue in 2023. Owned by Fast-retailing, one of the leading retailers in Japan, Uniqlo generated around 84 percent of the retail groups' revenue in fiscal year 2023. Despite decades of trying to build a portfolio, Fast Retailing remained essentially a single-brand company. Theory, GU, and other brands contributed less than 20% of revenue and even less of profits.

Management challenges loomed as well. Yanai, now 75, had built a global empire but struggled with succession planning. Several potential successors had left the company over the years. The company's culture remained intensely Japanese despite its global footprint, creating tensions in international markets. The question wasn't whether Fast Retailing could continue growing, but whether it could survive the eventual transition from its founder.

In FY2025, UNIQLO North America plans to open 25 new large-format, flagship-class, and other stores, pushing our total stores over 100. In 2024, in addition to urban store openings on the continent's east and west coasts, we also expanded into Texas, which we saw as having significant latent demand, ranking third in e-commerce sales after New York and California. Our first store opened in Houston in October 2024, and during the fall we opened four more stores in Houston and Dallas. All generated stronger-than-expected sales, confirming consumer anticipation.

The geographic diversification continued at pace. But unlike the scattered approach of earlier years, expansion now followed clear strategic logic: dense urban markets with young, fashion-conscious consumers and strong digital infrastructure. The company was no longer just opening stores—it was building ecosystems where physical stores, e-commerce, and social media created reinforcing loops of brand awareness and sales.

As 2024 progressed, Fast Retailing stood at a crossroads. It had achieved its dream of becoming a global retailer, with international sales exceeding domestic for the first time. But with China slowing, succession uncertain, and competition intensifying from both ultra-fast fashion and premium brands, the next chapter remained unwritten. The company that had redefined affordable quality now needed to redefine itself for a world where consumers had infinite choices and decreasing loyalty.

X. Playbook: Business & Strategic Lessons

The Fast Retailing story offers a masterclass in building a global retail empire from an unlikely starting point. The playbook that emerged from four decades of evolution contains lessons that transcend industry boundaries, revealing fundamental principles about scale, quality, and the delicate balance between global ambition and local authenticity.

The "LifeWear" Philosophy vs. Fast Fashion

Uniqlo's greatest strategic insight was recognizing that competing directly with Zara or H&M was a losing game. While competitors raced through 52 micro-seasons annually, Uniqlo perfected timeless pieces. The LifeWear concept—clothing designed to make life better—sounds like marketing fluff until you understand its operational implications. Every product decision flows from a simple question: Will this improve someone's daily life?

This philosophy drove seemingly irrational decisions that proved brilliant. Why spend three years perfecting a white shirt? Because millions of people wear white shirts every day, and making the perfect one creates lifetime customers. Why invest hundreds of millions in developing HeatTech? Because solving the problem of winter bulk versus warmth affects billions of people. The discipline to resist trend-chasing while competitors grabbed headlines required extraordinary conviction.

The approach created a different customer relationship. Zara customers visit stores frequently to see what's new. Uniqlo customers return because they know exactly what they'll find—the same excellent basics, perhaps with subtle improvements. It's the difference between entertainment and utility, between fashion and function. Paradoxically, by ignoring fashion, Uniqlo became fashionable among consumers tired of constant novelty.

Vertical Integration and the SPA Model Mastery

Tadashi Yanai also discovered that many foreign fashion chains were vertically integrated, taking control of the entire business process from design to production to retail. But Uniqlo didn't just adopt the SPA (Specialty store retailer of Private label Apparel) model—it perfected it through a uniquely Japanese lens.

While Gap and others used vertical integration primarily for cost control, Uniqlo used it for quality improvement. Controlling the entire chain meant Uniqlo could spend months working with fabric mills to develop new materials. It could maintain relationships with factories for decades, investing in their capabilities rather than constantly seeking lower costs. It could ensure that the thread used in Bangladesh matched exactly the specifications developed in Tokyo.

The company's approach to manufacturing partnerships exemplified this difference. Where competitors typically worked with hundreds of factories, constantly switching based on price, Uniqlo concentrated production among a smaller number of long-term partners. These weren't just suppliers but extensions of Uniqlo's operations, with Uniqlo engineers permanently stationed at major facilities, sharing technology and expertise.

This depth of integration enabled innovations impossible in traditional retail. When developing AIRism, Uniqlo could work directly with yarn producers, fabric mills, and garment factories to create an entirely new category of clothing. Competitors could copy the concept but not the execution, because they lacked the integrated infrastructure to innovate at the molecular level.

Technology-Driven Product Development

The masterstroke was positioning Uniqlo as a technology company that happens to make clothes. This wasn't just clever positioning—it reflected a fundamental difference in how the company approached product development. While fashion brands started with aesthetics and worked backward to production, Uniqlo started with problems and engineered solutions.

Consider the development process for any Uniqlo innovation. HeatTech began with a technical challenge: create warmth without bulk. AIRism started with humidity management. UV Cut addressed sun protection. Each product emerged from years of R&D, thousands of prototypes, and millions in investment—approaches more common in electronics or automobiles than apparel.

This technical approach created powerful moats. A competitor could copy a design in weeks, but recreating HeatTech's heat-generation properties required years of materials science research. More importantly, it changed how consumers evaluated products. Customers didn't compare Uniqlo's $40 jacket to another brand's $40 jacket—they compared HeatTech's warmth-to-weight ratio, AIRism's moisture management, or Ultra Light Down's packability.

Long-term Thinking in a Short-term Industry

Fashion retail typically operates on seasonal cycles, with success measured quarterly. Uniqlo operates on decade-long horizons. This long-term orientation manifested in countless ways: spending years perfecting products before launch, maintaining factory relationships through economic cycles, investing in markets that wouldn't be profitable for years.

The 2001 crisis exemplified this approach. While conventional wisdom suggested closing stores and cutting costs, Yanai used the crisis to fundamentally restructure the business. He accepted short-term pain—declining revenues, closing stores, disappointing investors—to build a stronger foundation. This pattern repeated throughout Uniqlo's history: using crises as opportunities for transformation rather than mere survival.

Long-term thinking also enabled counter-cyclical investments. Uniqlo expanded aggressively during the 2008 financial crisis when real estate was cheap and competitors were retrenching. It invested in digital infrastructure years before e-commerce became essential. It developed sustainable materials and processes before ESG became a boardroom priority. By the time trends became obvious, Uniqlo had already built commanding positions.

The Portfolio Problem

Despite its successes, Fast Retailing never solved the portfolio challenge. Theory remained niche, GU cannibalized Uniqlo, and European acquisitions like Comptoir des Cotonniers and Princesse Tam. Tam never achieved meaningful scale. The company that had disrupted retail with Uniqlo couldn't replicate that success with other brands.

The failure wasn't from lack of trying or resources. Fast Retailing applied the same operational excellence, invested comparable capital, and deployed talented management. But each brand faced a fundamental tension: operate independently and lose Uniqlo's operational advantages, or integrate with Uniqlo and lose brand authenticity.

Theory exemplified this challenge. As a premium contemporary brand, it needed different supply chains, design processes, and retail experiences than Uniqlo. But maintaining completely separate operations sacrificed the economies of scale that made Uniqlo successful. Attempts to share back-office functions or manufacturing relationships created conflicts. Theory designers didn't want to work with Uniqlo's factories, and Uniqlo's factories weren't optimized for Theory's small runs of fashion-forward designs.

The portfolio struggles revealed an uncomfortable truth: Uniqlo's success might be unrepeatable, even by its own parent company. The unique combination of Japanese quality obsession, technical innovation, and democratic pricing that defined Uniqlo couldn't simply be replicated with different positioning. Fast Retailing was learning what Procter & Gamble, Unilever, and other multi-brand companies knew: managing a portfolio requires different capabilities than building a single great brand.

Yet the portfolio challenges also highlighted Uniqlo's strengths. By generating 84% of Fast Retailing's revenue and an even higher percentage of profits, Uniqlo proved that in retail, focus could triumph over diversification. While competitors like Inditex managed multiple successful brands, Fast Retailing's concentration on a single powerful brand created advantages in operational efficiency, marketing effectiveness, and strategic clarity.

The lesson for other companies was nuanced. Diversification wasn't inherently wrong, but it required capabilities beyond operational excellence. Success in one category didn't guarantee success in others. And sometimes, the pursuit of portfolio diversification could distract from maximizing the potential of a core business. For Fast Retailing, the failed portfolio strategy ironically validated its core approach: do one thing extraordinarily well rather than many things adequately.

XI. Analysis & Bear vs. Bull Case

Bull Case: The Unstoppable Force of Accessible Quality

The optimistic case for Fast Retailing rests on structural advantages that only deepen with scale. After a subsequent period of decreased revenue and profits, business recovered, being spurred by an increase in women's products, and with consolidated sales of 2,290.5 billion yen and operating profits of 257.6 billion yen in 2019, they came to represent one of Japan's top companies. The recovery from past crises demonstrates resilience, but the current position is far stronger.

First, Uniqlo has solved retail's fundamental challenge: providing genuine value. In an era of inflation and economic uncertainty, consumers globally are reconsidering their relationship with consumption. Uniqlo's positioning—better quality than fast fashion, more affordable than premium brands—becomes increasingly relevant. The brand doesn't require consumers to choose between quality and price, a proposition that resonates across economic cycles.

The technology moat continues widening. While competitors struggle to match Uniqlo's fabric innovations from a decade ago, Uniqlo pushes further ahead. The R&D infrastructure—partnerships with Toray, testing laboratories, decades of accumulated knowledge—cannot be replicated quickly. Each year of innovation compounds, making catch-up increasingly difficult for competitors. When Shein or H&M tries to create their version of HeatTech, they're competing against twenty years of refinement.

Geographic diversification is finally paying dividends. In FY2025, UNIQLO North America plans to open 25 new large-format, flagship-class, and other stores, pushing our total stores over 100. UNIQLO North America is targeting ¥300 billion in sales and a 20% operating profit margin in FY2027, with the possibility of ¥1 trillion sales on the horizon. The U.S. market, which defeated Uniqlo twice before, now represents its fastest-growing major market. Success in America would transform Fast Retailing from an Asian retailer with global presence to a truly global powerhouse.

Digital capabilities provide another advantage. Uniqlo's integrated online-offline model, refined through COVID, gives it flexibility competitors lack. Pure e-commerce players can't match Uniqlo's physical presence for brand building and customer experience. Traditional retailers can't match Uniqlo's digital sophistication. The company operates in the sweet spot, leveraging both channels for maximum effect.

The sustainability transition favors Uniqlo's model. As consumers become more conscious of fashion's environmental impact, Uniqlo's emphasis on durability and timeless design gains relevance. Buying fewer, better pieces aligns with emerging consumer values. The RE.UNIQLO recycling program and sustainable material initiatives position the company for stricter environmental regulations and changing consumer preferences.

Most importantly, Uniqlo has achieved something rare in retail: brand permission to expand categories. Customers who trust Uniqlo for shirts now buy Uniqlo underwear, outerwear, even furniture through collaborations. Each successful category expansion strengthens the ecosystem, making Uniqlo not just a clothing store but a lifestyle solution. This expansion potential remains largely untapped, especially in newer markets.

Bear Case: The Limits of Growth and Structural Headwinds

The pessimistic view starts with Fast Retailing's most obvious vulnerability: extreme concentration risk. With Uniqlo generating ~84% of revenue and over 90% of profits, Fast Retailing is essentially a single-brand company masquerading as a conglomerate. Any significant damage to the Uniqlo brand—whether from quality issues, labor scandals, or shifting consumer preferences—would devastate the entire company.

China's slowdown represents an existential challenge. For China, where sales and profit declines extended into the latest quarter, the company is closing under-performing stores and revamping bigger and better-located outlets to drive sales. Revenue in the mainland fell 5%, and profits dropped 3% in the third quarter from March to May, marking a 10% decline in Greater China profit for the full business year. This isn't a temporary blip but potentially a structural shift. Chinese consumers are embracing domestic brands with increasing fervor. The market that drove growth for two decades may have permanently changed.

Competition is intensifying from both ends. At the low end, Shein's ultra-fast fashion model makes Uniqlo look expensive and slow. Shein can design, produce, and deliver new products in days, not months, at prices that undercut even Uniqlo. At the high end, the premiumization trend sees consumers buying fewer, more expensive pieces from luxury brands. Uniqlo's middle positioning—neither the cheapest nor the most prestigious—becomes precarious.

Fast Retailing's Gu brand saw its revenue rise and a sharp profit increase, which was roughly in line with its plan. Its revenue was up 8.1% to JPY319.1bn. and operating profit was 28.9% up to JPY33.7bn. GU brand meanwhile reported a rise in revenue but a contraction in profit in some quarters. The supposed growth driver increasingly looks like a distraction, cannibalizing Uniqlo sales without generating meaningful independent growth. Theory and other premium brands remain subscale despite years of investment.

Succession represents perhaps the greatest long-term risk. Tadashi Yanai, at 75, has built Fast Retailing around his vision and personality. Multiple potential successors have left the company. The deep bench of talent that characterizes companies like P&G or Unilever doesn't exist at Fast Retailing. When Yanai eventually steps down, the company faces an identity crisis alongside a leadership transition.

Labor challenges are mounting globally. Rising wages in manufacturing countries pressure margins. Retail labor shortages in developed markets increase costs and reduce service quality. The company's reputation, while strong, faces constant scrutiny over supply chain practices. One major scandal could trigger the kind of consumer boycott that has damaged other fashion brands.

Market saturation looms in key markets. Japan is fully penetrated with little room for growth. China's tier-1 and tier-2 cities are approaching saturation. While expansion opportunities exist in India, Southeast Asia, and other emerging markets, these come with execution risks and typically lower margins than established markets.

The macro environment poses additional challenges. A global recession would hit discretionary spending, and even Uniqlo's "affordable" positioning might not provide immunity. Currency fluctuations—particularly yen strength—could devastate profitability given the company's global operations. Trade tensions and potential tariffs threaten the integrated supply chain model that enables Uniqlo's value proposition.

The Verdict: Navigating Between Excellence and Exhaustion

Fast Retailing stands at an inflection point where its greatest strengths could become weaknesses. The operational excellence that built Uniqlo might prevent successful diversification. The focus on basics that differentiated the brand might limit growth as markets saturate. The founder-led culture that drove innovation might prevent successful succession.

The bull case remains compelling: Uniqlo has built a unique position in global retail with structural advantages that deepen over time. The brand resonates with contemporary values around sustainability, quality, and conscious consumption. Geographic expansion provides runway for growth, and operational excellence ensures profitable growth.

But the bear case cannot be dismissed. Concentration risk, succession challenges, and competitive pressures are real and mounting. The China slowdown demonstrates that past success doesn't guarantee future performance. The failed portfolio strategy suggests limits to Fast Retailing's expansion potential.

The most likely scenario lies between extremes. Fast Retailing will probably continue growing, but at moderating rates. Uniqlo will remain dominant in Asia while slowly building presence in Western markets. The company will muddle through succession, losing some dynamism but maintaining operational excellence. Competition will erode margins but not destroy the business model.

For investors and observers, Fast Retailing represents a fascinating study in retail evolution. Can a company built on Japanese perfectionism and long-term thinking survive in an increasingly fast, global, and digital marketplace? Can operational excellence overcome strategic limitations? Can a founder's vision outlive the founder? The answers will shape not just Fast Retailing's future but offer lessons for global retail's evolution.

XII. Epilogue & Recent Developments

As autumn 2024 unfolds, Tadashi Yanai, now 75, still arrives at Uniqlo's Tokyo headquarters before sunrise most days. The wood-paneled office from which he orchestrates a global empire feels both monument to achievement and reminder of unfinished business. The company is on track to meet its goal of achieving 3 trillion yen (US$20bn) in fiscal 2024, 5 trillion yen (US$33bn) in revenue in the year ending in August 2028, and 10 trillion yen in the long term. These aren't just numbers—they represent Yanai's vision of Uniqlo as the world's largest apparel retailer, a goal that once seemed impossible for a company from rural Japan.

The succession question hangs over everything like morning fog over Mount Fuji—visible, persistent, unavoidable. Yanai has promised to retire multiple times, only to return when successors departed or strategies faltered. The latest plan involves a collective leadership model, with different executives managing different regions and functions. But everyone knows Fast Retailing has been Yanai's company for four decades. Whether it can survive without him remains the existential question. Recent developments suggest Fast Retailing is preparing for its post-Yanai future while the founder still controls the transition. The Clare Waight Keller appointment as Creative Director represents a significant evolution. In September 2024, Waight Keller was appointed at the helm of Uniqlo design as creative director of the brand. She will also lead the UNIQLO mainline collection, including menswear, from 2024 Fall/Winter. Clare Waight Keller is the creative director of Uniqlo and was Givenchy's first female artistic director. The British designer previously served as creative director at LVMH-owned Givenchy and Richemont's Chloé.

The appointment signals Uniqlo's continuing evolution from basic retailer to design-conscious brand. Waight Keller brings luxury credibility—she designed Meghan Markle's wedding dress—but also understands commercial reality. "I have been thinking about where fashion will go in the next 10 to 15 years," says Waight Keller. Her vision aligns perfectly with Uniqlo's positioning: democratic luxury, accessible quality, timeless design with contemporary relevance.

The sustainability pivot represents another crucial evolution. The RE.UNIQLO recycling program has expanded globally, with stores accepting used Uniqlo items for recycling into new products. "Our biggest issue is actually people not donating enough, if you can believe it. So anyone who has any extra nylons or downs, please bring them to a Uniqlo shop and we'll make you a new one," Waight Keller notes. This isn't just environmental consciousness—it's building a circular economy that reinforces customer loyalty and brand values.

Geographic expansion continues but with notable strategic shifts. The company is targeting annual group sales of 5 trillion yen (approx. US$33bn) in revenue in the year ending in August 2028, and 10 trillion yen in the long term. But growth increasingly comes from depth rather than breadth—more sales per store, higher customer lifetime value, greater share of closet rather than simply more locations.

The North American breakthrough represents the most significant recent development. UNIQLO North America is targeting ¥300 billion in sales and a 20% operating profit margin in FY2027, with the possibility of ¥1 trillion sales on the horizon. After decades of false starts, Uniqlo has finally cracked the American market by accepting that U.S. consumers aren't Japanese consumers who happen to live in America. Larger sizes, different color preferences, distinct shopping patterns—success required genuine localization, not just translation.

Technology integration accelerates. The company now uses AI for demand forecasting, reducing overproduction and markdowns. Virtual fitting rooms allow customers to see how clothes look without trying them on. RFID tags enable instant checkout and real-time inventory management. But technology serves the mission rather than driving it—each innovation must demonstrably improve the customer experience or operational efficiency.

The competitive landscape continues evolving in ways that both threaten and validate Uniqlo's model. Shein's ultra-fast fashion makes Uniqlo look slow and expensive to some consumers. But sustainability concerns and quality issues also make Uniqlo's approach look prescient to others. The question isn't whether Uniqlo can compete with Shein on speed or price—it can't and shouldn't try—but whether enough consumers value quality and sustainability over instant gratification and rock-bottom prices.

Management succession remains the elephant in every boardroom. Yanai has promised various transition timelines, none fulfilled. The latest plan involves distributed leadership—regional CEOs with significant autonomy, functional leaders with global responsibility, a gradual transition of power rather than sudden handover. But everyone knows Fast Retailing has been Yanai's company for four decades. Whether its culture, strategy, and dynamism can survive his departure remains unknowable.

The China question looms largest. With revenue declining and competition intensifying, the market that drove two decades of growth has become a source of concern rather than comfort. Fast Retailing is adapting—closing underperforming stores, localizing product mix, investing in digital channels—but the golden age of easy growth in China has clearly ended. The company must find new growth engines while managing decline in its most important international market.

Current market cap: ~$120B, making it one of world's most valuable apparel companies. This valuation reflects both achievement and expectation—recognition of what Fast Retailing has built and belief in what it might become. But it also creates pressure. The market expects continued growth, successful succession, and navigation of geopolitical tensions. Any significant stumble could trigger a painful revaluation.

As 2024 winds down, Fast Retailing stands as both triumph and question mark. It has achieved what seemed impossible: building a global apparel empire from rural Japan, redefining value in fashion, creating technical innovations that competitors still struggle to match. But whether this success can survive its founder, transcend its origins, and adapt to a rapidly changing world remains uncertain.

The story of Fast Retailing ultimately asks a fundamental question: Can operational excellence and long-term thinking survive in an increasingly fast, disposable, and short-term world? Can quality win against quantity? Can a company built on Japanese values succeed globally while maintaining its soul? The answers will shape not just Fast Retailing's future but offer lessons for any company trying to build something lasting in an ephemeral age.

Yanai, still arriving before dawn at 75, continues to believe the answer is yes. The company is on track for its 5 trillion yen target. International expansion accelerates. New leaders emerge, even if none yet match the founder's vision and drive. The machine Yanai built over four decades continues to hum, producing millions of perfectly designed, reasonably priced, technically innovative garments for customers worldwide.