CRRC Corporation: The World's Rail Giant

How a Fragmented Network of State-Owned Railway Factories Became the Dominant Force in Global Rail Manufacturing

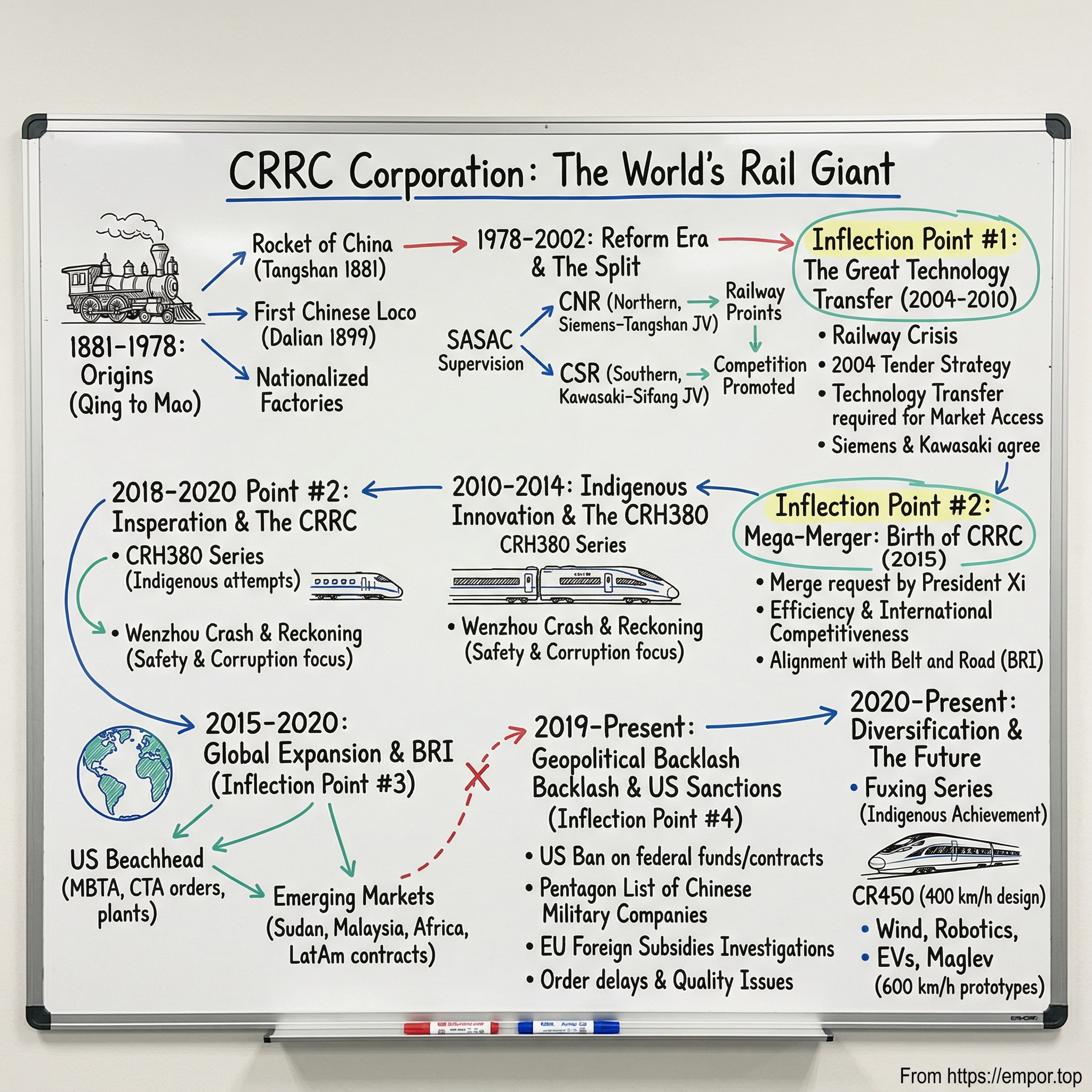

I. Introduction: The Track to Dominance

In the gleaming control rooms of Qingdao Sifang's high-speed train assembly facility, engineers monitor the final production stages of the CR400AF—nicknamed the "Red Dragon." The sleek trainsets, designed to cruise at 350 km/h, roll off production lines destined for routes spanning Tibet's frozen plateaus to the subtropical deltas of the Pearl River. Each train represents the culmination of a decades-long national project to master advanced rail technology—a project that began with borrowed designs and ended with China building more high-speed track than the rest of the world combined.

CRRC Corporation Limited is a Chinese state-owned and publicly traded rolling stock manufacturer. It is the world's largest rolling stock manufacturer in terms of revenue, eclipsing its major competitors of Alstom and Siemens. The company commands a dominant position in the global rail market that would have seemed impossible just two decades ago, when China's trains averaged barely 48 km/h and its domestic rail manufacturers were decades behind their Western and Japanese counterparts.

China's high-speed railway network is by far the longest in the world. The HSR network reached 48,000 km in total length by the end of 2024, with plans to expand to 60,000 km by 2030. CRRC supplies virtually all of this rolling stock, positioning it at the heart of an infrastructure build-out unprecedented in human history.

The central question that emerges from CRRC's story cuts to the heart of industrial competition in the 21st century: How did a fragmented network of state-owned railway factories, some dating to the Qing dynasty, become the dominant force in global rail manufacturing—and what does this tell us about China's industrial strategy?

The answer involves technology transfer deals that foreign executives later regretted, a massive domestic market that served as an unassailable fortress, strategic mergers orchestrated from Beijing, and an export push that has now triggered geopolitical backlash from Washington to Brussels. CRRC's trajectory offers a roadmap—or perhaps a warning—for how state capitalism, when combined with strategic patience and a captive home market, can reshape entire industries.

II. Origins: The Qing Dynasty to Mao's China (1881–1978)

On a humid summer day in 1881, in the coal-mining town of Tangshan in Hebei province, China's first steam locomotive chugged along newly laid tracks. CRRC Tangshan Co., Ltd. is a prominent Chinese state-owned manufacturer of rail transit equipment, founded in 1881 as the nation's first railway vehicle producer during the late Qing Dynasty's Westernization Movement. Workers nicknamed it the "Rocket of China"—an ambitious moniker that captured both the locomotive's modest power and the grand aspirations of late imperial reformers who saw railways as China's path to modernization.

Built in 1881, CRRC Tangshan Co., Ltd. has not only produced the first Chinese locomotive "Rocket of China", the first Chinese passenger train "Palace Car", the first Chinese freight wagon, the first railway inspection train, the first special vehicle and first high-class official train. These pioneering achievements came during the Self-Strengthening Movement, when Qing officials sought to adopt Western technology to preserve Chinese sovereignty—a goal that would prove elusive as foreign powers carved up China's coastline into spheres of influence.

The history of CRRC's constituent factories mirrors China's tumultuous 20th century. The factory was established in 1899 during the period of construction of the Chinese Eastern Railway, as the Shahekou works, and was under Japanese control from 1905, and later part of the Manchukuo state. After the end of the Second World War the railway was under joint Chinese and Russian control until the 1950s when the Chinese Eastern Railroad and the city of Dalian were transferred to sole Chinese control.

CRRC Dalian Co., Ltd. originally founded in 1899 as the Eastern Railway Locomotive Manufacturing Plant during the construction of the Chinese Eastern Railway, it holds the distinction of being China's oldest locomotive production facility. The Dalian works passed through Russian, Japanese, Soviet, and finally Chinese hands—each transition leaving its mark on the facility's equipment, processes, and institutional memory.

In 1934 the factory together with Kawasaki Heavy Industries, manufactured the Asia Express high speed steam train for the South Manchuria Railway. This early collaboration with Kawasaki would echo decades later when Chinese officials negotiated technology transfer agreements with the same Japanese company for bullet train technology.

After the Communist revolution in 1949, these scattered works were nationalized and brought under the Ministry of Railways. Its origins can be traced back to the Qing dynasty in the late 1800s. After the establishment of the People's Republic of China in 1949, CRRC made rail cars as a state-owned train maker under the former Ministry of Railways.

In September, 1956 the company successfully designed and manufactured China's first main line steam locomotive. In September, 1958 the Company successfully self-designed and manufactured China's first mainline diesel locomotive. In 1965 the Company realized a historic transition, turned into China's first diesel locomotive manufacturer rather than a steam locomotive manufacturer. In September 1969 the Company successfully designed and manufactured DF4 mainline diesel locomotive, from then on, DF4 locomotive has become the main type diesel traction locomotive for Chinese railways.

While Datong built mainline steam locomotives until 1988, Tangshan built steam for industrial use until 1999, becoming the last works in the world to build steam for non-tourist use. This remarkable fact—that a company now producing 350 km/h bullet trains was still manufacturing steam engines just 26 years ago—captures the speed of China's industrial transformation.

The fragmented nature of these factory systems under socialist planning would later prove consequential. Different regions maintained their own production facilities, creating redundancy and regional competition that would shape the industry's post-reform structure. When Deng Xiaoping opened China to market reforms, these competing factory systems would need to be rationalized—but the question of how, and by whom, remained unresolved.

III. Reform Era & The Split: Creating Competition (1978–2002)

Deng Xiaoping's economic reforms transformed China's state-owned enterprises from instruments of central planning into entities that needed to grapple with market forces. For the railway equipment sector, this meant a fundamental rethinking of how factories should be organized and governed.

The origins of CRRC date back to the establishment of China National Railway Locomotive & Rolling Stock Industry Corporation (LORIC) in 1986, which initially operated as a state-owned railway equipment manufacturer. In 2000, LORIC was detached from the Ministry of Railways (MOR) and split into two companies, China CNR Corporation Limited (CNR) and CSR Group Corporation (CSR), to promote competition but remained under the supervision of SASAC.

The logic behind the split reflected the reformist thinking of the era: competition, even among state-owned enterprises, would drive efficiency gains that monopoly control could never achieve. CNR Group and CSR Group, were once one company, China National Railway Locomotive & Rolling Stock Industry Corporation (LORIC). The company was split up in 2002.

China's central government gave up control, but maintained ownership, of the two companies during state-owned enterprise restructuring in 2000. CNR and CSR were then free to pursue competitive agendas to the benefit of China's domestic railway industry, and flourished in China's push to connect the country by rail.

The newly formed competitors inherited geographic portfolios: CNR ("Northern") took factories in the northern provinces including Tangshan and Dalian, while CSR ("Southern") received facilities like the Qingdao Sifang works and Zhuzhou Locomotive. The key high-speed rail joint ventures that would later emerge reflected this division: The key high-speed rail JVs were Bombardier-Sifang (a CSR subsidiary), Kawasaki-Sifang (CSR), Siemens-Tangshan (a CNR subsidiary), and Alstom-Changchun (CNR).

Both companies fell under the supervision of SASAC (State-owned Assets Supervision and Administration Commission), the powerful agency that manages China's central state-owned enterprises. This arrangement meant that while CNR and CSR competed domestically, they remained ultimately accountable to the same government apparatus—a structure that would later facilitate their re-merger.

The split created a duopoly that would dominate China's locomotive and rolling stock manufacturing for over a decade. But even as these twin giants competed domestically, a transformational force was gathering: China's leadership had decided that the country needed high-speed rail, and it needed to acquire the technology by any means necessary.

IV. The Great Technology Transfer (2004–2010): Inflection Point #1

In meeting rooms in Beijing, Tokyo, Munich, and Paris, one of the most consequential technology acquisitions in industrial history was being negotiated. The stakes were immense: access to the world's largest potential high-speed rail market in exchange for the technological crown jewels of companies that had spent decades perfecting bullet train technology.

The Setup: A Railway System in Crisis

China's railways in the early 2000s were a national embarrassment. Commercial train service averaged only 48 km/h—slower than intercity buses on the expanding highway network. Airlines and road transport were steadily capturing market share from a rail system that seemed frozen in time.

Despite setting speed records on test tracks, the DJJ2, DJF2 and other domestically produced high-speed trains were insufficiently reliable for commercial operation. The State Council turned to advanced technology abroad but made it clear in directives that China's HSR expansion could not solely benefit foreign economies and should also be used to develop its own high-speed train building capacity through technology transfers.

China had attempted indigenous high-speed rail development, but the results were discouraging. Domestically designed trains lacked the reliability required for commercial operation, and years of research had consumed resources without producing viable results. The leadership faced a choice: continue the slow path of indigenous development, or take a shortcut by acquiring foreign technology.

The 2004 Tender Strategy: The Game Changes

In 2004, MOR Minister Liu Zhijun launched 3 tenders to make some 200 high-speed trains, with each one stipulating that foreign companies had to collaborate with domestic partners and transfer key technologies to achieve localization.

The strategy was as brilliant as it was ruthless. Criteria imposed by the MoR included competitive pricing and that companies awarded contracts be legally registered in the PRC, comprehensively transfer key technology to Chinese enterprises and use a Chinese trademark on the finished product. While foreign partners might provide technical services and training, Chinese companies must ultimately be able to function without the partnership.

Each tender included two key conditions: (1) to win, the bidder had to transfer technology to China; and (2) the final products had to be marketed under the Chinese SOE rail car brand.

This was not merely a procurement exercise—it was industrial policy dressed up as a tender. By requiring technology transfer as a precondition for market access, China was leveraging its massive domestic market to extract know-how that foreign companies had spent billions developing.

The Bidding Drama: Siemens Blinks

In June 2004, the MOR solicited bids to make 200 high-speed train sets that can run 200 km/h. Alstom of France, Siemens of Germany, Bombardier Transportation based in Germany and a Japanese consortium led by Kawasaki all submitted bids. With the exception of Siemens, which refused to lower its demand of CN¥350 million per train set and €390 million for the technology transfer, the other three were all awarded portions of the contract.

Siemens' initial refusal to play by China's rules became a cautionary tale. According to the People's Daily, the elimination of Siemens from the first bidding round (allegedly) led to the collapse of the company's share price and the firing of its negotiating team in China.

In 2005, Siemens returned to tender for 350 km/h+ train contracts subject to more severe conditions, agreeing to lower its prices and comprehensively transfer technology. In November 2005, Siemens reached an agreement with the MoR, entering into joint ventures with Changchun Railway Vehicles and Tangshan Railway Vehicle Co, (both CNR subsidiaries) and was awarded sixty 300 km/h train orders. It supplied the technology for the CRH3C, based on the ICE3 design, to CNR's Tangshan.

Meanwhile, the Japanese consortium led by Kawasaki had already signed on, believing the Chinese market was worth the risk. Kawasaki won an order for 60 train sets based on its E2 Series Shinkansen for ¥9.3 billion. Of the 60 train sets, three were directly delivered from Nagoya, Japan, six were kits assembled at CSR Sifang Locomotive & Rolling Stock, and the remaining 51 were made in China using transferred technology with domestic and imported parts.

The Execution: Technology Flows East

The technology transfer was structured to maximize knowledge absorption. Examples of technology transfer include Mitsubishi Electric's MT205 traction motor and ATM9 transformer to CSR Zhuzhou Electric, Hitachi's YJ92A traction motor and Alstom's YJ87A Traction motor to CNR Yongji Electric, Siemens' TSG series pantograph to Zhuzhou Gofront Electric. For foreign train manufacturers, technology transfer was a crucial part of gaining market access in China.

In October 2004, Kawasaki and the MoR signed an export and technology transfer agreement with China ordering 60 high-speed train sets from Kawasaki based on its E2 Series Shinkansen for a total of 9.3 billion RMB ($1.5 billion). The contract provisions also stipulated that a certain number of key technologies would be transferred to China. Kawasaki evidently believed that this technology would be used only in the domestic market. Three of the train sets would be completed in Japan and delivered completed, another six would be handed over and assembled by the Chinese party. A further 51 would be manufactured by Qingdao Sifang with transferred technology.

The Aftermath: Foreign Partner Frustration

The speed of Chinese absorption stunned foreign partners. Six years after licensing the Shinkansen E2 design from Kawasaki, CRRC Sifang was able to produce the CRH2A without Japanese input.

In 2008 (two years into the partnership), CSR ended its cooperation with Kawasaki and began independently building CRH2B, CRH2C and CRH2E models at its Sifang plant and designated the technology for export.

In a 2011 interview with the Financial Times, Alstom chief executive Patrick Kron accused Siemens of inadvertently allowing key technical know-how to leak out to Chinese companies through a HSR partnership. Kron asserted that Alstom, unlike Siemens or Kawasaki, had been careful not to engage in Chinese joint ventures or collaborations that involved giving up key technology. "You should ask Mr. [Peter] Löscher [Siemens chief executive] whether he is satisfied…"

Within three years, Chinese firms started producing high-speed trains based on the foreign technology.

The technology transfer episode reveals a fundamental asymmetry in the global technology marketplace. Foreign companies, competing against each other for access to China's vast market, found themselves trapped in a prisoner's dilemma. Each feared that if they refused to transfer technology, a competitor would step in and reap the benefits. The result was a collective technology giveaway that no individual company would have chosen in isolation.

V. Indigenous Innovation & The CRH380 (2010–2014)

The technology transfer agreements of 2004-2005 were supposed to be the beginning, not the end, of foreign involvement in China's high-speed rail program. Instead, they proved to be the beginning of the end. Within five years, Chinese engineers had not only absorbed foreign designs but were pushing beyond them.

The CRH380 series marked China's first serious attempt to develop "indigenous" high-speed trains operating at speeds that exceeded the designs they had licensed. The goal was ambitious: trains capable of sustained operation at 380 km/h, faster than anything then running in Europe or Japan.

CSR Qingdao Sifang developed the CRH380A using the CRH2 (Kawasaki-derived) platform as a foundation. CRH380A; Maximum operating speed of 380 km/h. Developed by CSR based on CRH2 and manufactured by Sifang Locomotive and Rolling Stock; entered service in 2010. CRH380B: upgraded version of CRH3; maximum operating speed of 380 km/h, manufactured by Tangshan Railway Vehicle and CRRC Changchun Railway Vehicles; entered service in 2011.

The CRH380A achieved a world operational speed record during testing, demonstrating that Chinese engineers had mastered not only manufacturing but design optimization. The trains incorporated improvements to aerodynamics, traction systems, and bogies that pushed beyond the original licensed specifications.

The Wenzhou Crash: Tragedy and Reckoning

On the evening of July 23, 2011, a lightning strike disabled signaling equipment along the Yongtaiwen railway near Wenzhou. The Wenzhou train collision was a railway accident that occurred on 23 July 2011, when a high-speed train travelling on the Yong-Tai-Wen railway line collided into the rear of another stationary train on a viaduct in Lucheng District, Wenzhou, Zhejiang province, China. The two trains derailed, and four carriages fell off the viaduct. 40 people were killed, and at least 192 were injured, 12 severely. This disaster was caused by both defects in railway signal design and poor management by the railway company.

"The disastrous crash was caused by serious design flaws in the train control system, inadequate safety procedure implemented by the authority and poor emergency response to system failure," says the report.

The Chinese government had sacked railways minister Liu Zhijun in February 2011, for allegedly taking over 800 million yuan in kickbacks connected with contracts for high-speed rail expansion. Liu Zhijun—the same minister who had orchestrated the technology transfer strategy—had been arrested on corruption charges just months before the crash.

The Wenzhou train collision had an immediate and major effect on China's high-speed rail program. On 10 August 2011 the Chinese government announced that it was suspending approvals of any new high-speed rail lines pending the outcome of the investigation. The Minister of Railways announced further cuts in the speed of Chinese high-speed trains, with the speed of the second-tier 'D' trains reduced from 250 to 200 km/h.

The crash exposed the dark side of China's high-speed rail expansion: the rush to build had compromised safety systems, and the political pressure to show results had overridden engineering caution. The most senior official implicated in the report is former minister Liu Zhijun, who had been detained on corruption charges before the accident, but nonetheless is accused of improperly raising the operating speed of the Ningbo-Taizhou-Wenzhou Railway and compressing the construction schedule.

High-speed railway construction virtually came to a halt in China after the July crash. The sector has been hit hard as the government tightened liquidity and the fatal Wenzhou accident eroded investors' confidence affecting the ministry's ability to borrow money or sell bonds. Total railway infrastructure investment shrank to only Yuan 469bn ($US 74.4bn) in 2011, a 33% drop from the more than Yuan 700bn invested in 2010.

Yet the pause proved temporary. The State Council meeting says high-speed railway development is "the right direction" as it helps to improve public transport and boosts economic growth. As long as China strengthens the quality of its railway management, improves safety, and puts more effort into technical innovation, the Chinese high-speed rail sector will advance in a scientific, safe and sustainable manner.

The Wenzhou crash forced a reckoning with the costs of breakneck expansion, but it did not halt the program. By 2015, the network would resume its growth trajectory—and CNR and CSR would be merged into a single national champion.

VI. The Mega-Merger: Birth of CRRC (2015): Inflection Point #2

The marble corridors of Beijing's government offices had witnessed many consequential decisions, but the one that emerged in late 2014 would reshape the global rail industry. China's two largest rolling stock manufacturers—competitors for over a decade—would become one.

CRRC was split into CSR and CNR in 2000 following state-owned company reforms. However, it merged again as a gigantic train maker at the request of President Xi Jinping's administration, a proponent for Chinese companies expanding overseas.

State-owned China CNR Corporation Limited (CNR) and China South Locomotive & Rolling Stock Corporation Limited (CSR) announced in a joint statement on December 30, 2014 that they will merge to form a single company—China Railway Stock Corp. (CRRC)—valued at $26 billion. CSR will purchase shares from CNR shareholders on the Shanghai and Hong Kong stock exchanges at a rate of 1.1 CSR shares for each CNR share and then delist the CNR shares in order to complete the merger. CNR's shares jumped 45 percent in light of the deal, while CSR's shares jumped 32 percent.

Why Re-Merge? The Strategic Calculus

The rationales given for the merger were increased efficiency, and the ability to better compete internationally. The merger came into effect 1 June 2015, with each CNR share exchanged for 1.1 CSR shares - the combined company became the largest railway rolling stock manufacturer in the world, and held over 90% of the Chinese market.

The official rationale—efficiency and international competitiveness—obscured a more complex picture. In 2012 CNR and CSR both submitted bids by a public call for tenders of the Argentine government and fiercely competed with low prices. Cut-throat competition on international markets is believed to have resulted in a significant loss of financial resources for both companies. Recognizing the need to address these coordination problems, SASAC finally pushed a merger of CSR and CNR.

The Argentine fiasco had exposed an embarrassing reality: China's two rail giants were undercutting each other abroad, destroying value for both companies while enriching foreign buyers. From Beijing's perspective, this was a coordination failure that only central intervention could solve.

The merger has created a giant with an annual revenue greater than Siemens, Alstom and Bombardier combined, and a 30 percent share of the global rail market.

The Merger Mechanics

The CRRC board of directors held its first meeting on June 1, chaired by Mr Cui Dianguo, the former CNR chairman while CNR's president, Mr Xi Guohua, becomes president of CRRC. Former CSR chairman Mr Zheng Changhong and president Mr Liu Hualong become vice-chairmen of CRRC. CRRC was granted its business license on June 1, and inherited all the businesses and assets of both CNR and CSR which now cease to exist as legal entities.

The total value of the combined assets of CNR and CSR in 2014 was Yuan 299.7bn ($US 48.3bn), and the two companies had a combined turnover of Yuan 224bn last year. CNR made a net profit of Yuan 4.49bn in 2014 compared with CSR's net profit of Yuan 5.31bn. CRRC is headquartered in Beijing, and has 175,700 employees.

Belt and Road Alignment

The merger timing was not accidental. China's Belt and Road Initiative (BRI) is one of the most ambitious infrastructure projects ever conceived. Launched in 2013 by President Xi Jinping, the vast collection of development and investment initiatives was originally devised to link East Asia and Europe through physical infrastructure.

A handful of state firms operate most projects. These firms are funded by and report directly to the central government, and include China Harbor, CRRC, State Grid, China Three Gorges, and COSCO.

CRRC was now positioned to be the rail equipment supplier for the world's largest infrastructure initiative. A fragmented domestic industry would have complicated this role; a unified national champion could negotiate with a single voice and avoid the self-defeating price competition that had plagued CNR and CSR abroad.

CRRC will remain state-owned and supported by the Chinese government, which plans to invest $1.2 trillion in overseas projects over the next ten years.

The merger was the culmination of a fifteen-year journey: from the 2000 split designed to introduce domestic competition, through the 2004 technology transfer that rapidly upgraded Chinese capabilities, to the 2015 consolidation that created a world-beating national champion. Each phase served its purpose in an industrial strategy of extraordinary patience and sophistication.

VII. Global Expansion & Belt and Road (2015–2020): Inflection Point #3

With the merger complete, CRRC turned its attention abroad. The newly formed giant had already demonstrated its appetite for international markets through the contracts won by its predecessor companies. Now, with unified management and government backing, CRRC pursued a global expansion strategy that would test the limits of welcome in markets from Boston to Berlin.

After being awarded a 284 vehicle order (later expanded to 404 vehicles) for metro cars for Massachusetts Bay Transportation Authority's Red and Orange lines with a US$556.6 million bid in October 2014, the company started constructing a 13,900 square metres assembly plant in Springfield, Massachusetts, at a former Westinghouse plant beginning in September 2015. Manufacturing work began in April 2018.

In mid-2015, production began at a rolling stock plant in Batu Gajah, Perak, Malaysia—a satellite of CRRC Zhuzhou Locomotive, and the corporation's first plant outside China. Additionally the former CSR had acquired Emprendimientos Ferroviarios in Argentina in 2014.

The American Beachhead

In March 2016, CRRC Qingdao Sifang was awarded a contract to build 400 7000-series cars for the Chicago Transit Authority (CTA), with an option for another 446 cars. The cost of the contract was US$632 million up to US$1.3 billion with options.

More than $100 million was invested in the site. CRRC carries out the final assembly of cars at the enterprise, the components for which are supplied by 24 companies, and 19 of them are based in the USA.

CRRC's entry into the American market followed a familiar playbook: aggressive pricing to win contracts, followed by local assembly operations that generated American jobs and created local political constituencies. The Springfield and Chicago plants were not merely production facilities—they were political insurance policies.

Competing manufacturers criticized the deal because of the degree to which CRRC was able to underbid them and the foothold it allowed CRRC to gain in the American transit market, a strategy that company officials acknowledged.

Belt and Road: The Global Push

The Sudan Railways Authority is receiving 21 new locomotives from the Chinese company CRRC Ziyang, which departed from the Chinese port in mid-June 2022 and is expected to arrive in Port Sudan in the first week of August. Out of the 34 locomotives agreed on in a contract signed between the Sudan Railways Authority and CRRC Ziyang in September 2020, these 21 new locomotives would be the first batch received. As an important achievement of the authority, this project has received great attention from the governments of Sudan and China. With the arrival of new locomotives, the rail transport capacity is expected to significantly improve.

Rail: Total rail engagement (including light rail and subway) was worth USD5.7 billion, where particularly the expansion of the Standard Gauge Railway in Tanzania stands out. In Mexico, China Railway Rolling Stock Corporation (CRRC) won the bid to supply 17 electric units for a light rail in Mexico City.

CRRC engaged through rail construction contracts with engagements in Africa, Latin America and East Asia, such as the Kinshasa urban railway in the Democratic Republic of Congo. Also, China engaged through its CRRC to manufacture rail wagons and wheels in Saudi Arabia.

The global expansion was not without controversy. In June 2016 a predecessor company of CRRC, CSR Corporation Limited, was implicated in allegations of bribery to obtain a 2012 US$6 billion tender to deliver 600 locomotives to the state owned Passenger Rail Agency of South Africa (PRASA). By 2020 it was reported that funds allocated to pay for an adjusted contract to deliver the locomotives produced by CSR Corporation, now reformed into CRRC, had been frozen by the South African Revenue Service due to possible instances of corruption.

By 2020, CRRC had established a truly global footprint. But the same scale and state backing that enabled this expansion was beginning to trigger a backlash from governments increasingly wary of Chinese industrial ambitions.

VIII. The Geopolitical Backlash & US Sanctions (2019–Present): Inflection Point #4

The conference room at the U.S. Department of Defense was not accustomed to discussions of subway cars. But in the increasingly fraught world of U.S.-China competition, even mundane rolling stock had become a matter of national security.

Counterworks against CRRC have been continuing in the US for several years. Thus, in July 2019, the US Senate approved a one-year ban on signing state contracts for the supply of rolling stock with companies that are owned or subsidized by the Chinese government.

Congress passed legislation in 2019 that prevents federal dollars from being used to buy rail cars or buses built by Chinese state-owned firms, effectively banning CRRC from government-funded transit contracts.

The legislation reflected growing concerns about cybersecurity, supply chain dependence, and the strategic implications of allowing a Chinese state-owned enterprise to build critical transportation infrastructure. Transit railcars contain sensors to ensure safety, GPS systems, surveillance cameras, Wi-Fi, and more. Allowing a Chinese SOE to manufacture those technologies with potential backdoor visibility and monitoring capabilities presents a clear threat.

The Pentagon List

In October 2022, the United States Department of Defense added CRRC to a list of "Chinese military companies" operating in the U.S.

The ban on investing in the CRRC was already introduced in June last year. The corresponding document, signed by US President Joe Biden, prohibits American citizens and companies from trading in CRRC's securities.

In November 2020, Donald Trump issued an executive order prohibiting any American company or individual from owning shares in companies that the United States Department of Defense has listed as having links to the People's Liberation Army, which included CRRC.

Quality and Delivery Problems

The geopolitical headwinds coincided with operational difficulties that undermined CRRC's reputation for value. In 2020, the delivery schedule was postponed: a new deadline was approved for the Orange Line in April 2023, and for the Red Line in September 2024. In October, CRRC asked to delay deliveries again due to concerns related to the COVID-19 pandemic: for the Orange Line until the summer of 2023, and for the Red Line until 2025. MBTA representatives are not ready to confirm the new schedule and threaten the manufacturer with fines of $500 for each day of one train delivery delay.

In April 2024, SEPTA terminated their order of bi-level rail cars, citing delays and poor build quality. They have stated "The authority is assessing its options for recouping funds that have been spent on the project" after spending $50 million on the project.

The European Front

In February 2024, the European Union launched an investigation into CRRC for allegedly using state subsidies to undercut European suppliers.

The investigation relates to a public procurement procedure by the Bulgarian Ministry of Transport and Communications for 20 electronic "push-pull" trains and their maintenance with a contract valued at EUR 610 million. CRRC Qingdao Sifang Locomotive ("CRRC"), a subsidiary of the Chinese state-owned company CRRC Corporation Limited, had submitted a tender in the public procurement procedure.

In December Talgo submitted a bid of 1·22bn leva, while the bid from CRRC Qingdao Sifang Locomotive was much lower at just 607m leva. CRRC's bid was roughly half the price of its European competitor—a differential that the European Commission found suspicious enough to warrant formal investigation.

Brussels had alleged that CRRC had received almost US$2 billion in state subsidies.

CRRC Qingdao Sifang Locomotive has withdrawn its bid for a contract to supply 20 push-pull trainsets, after the European Commission launched an investigation into whether the Chinese state-owned company might have benefited from an unfair subsidy.

'In just a few weeks, our first investigation under the Foreign Subsidies Regulation has already yielded results', commented Commissioner for Internal Market Thierry Breton on March 26. 'Our single market is open for firms that are truly competitive and play fair.'

The Bulgarian withdrawal signaled that CRRC's global expansion would face increasing resistance in developed markets. The company remains dominant in China and maintains strong positions in developing countries, but the U.S. and EU have effectively closed their doors to new contracts.

IX. Diversification & The Future (2020–Present)

In Qingdao's coastal industrial zone, CRRC engineers are testing the CR450—a next-generation high-speed train designed to operate at 400 km/h, further cementing China's technological lead in high-speed rail. The CR450 bullet train prototypes made their debut in Beijing on Dec 29. They are designed to have a maximum speed of 450 kilometers per hour. On Dec 29, China unveiled two CR450 high-speed train prototypes, which are capable of reaching a test speed of 450 km/h and an operational speed of 400 km/h. They will be the fastest high-speed trains in the world once they enter commercial service.

The Fuxing Series: Indigenous Achievement

Fuxing, also known as the CR series EMU (or as the Fuxing Hao), is a series of high-speed and higher-speed EMU trains operated by China Railway High-speed (CRH) and developed by CRRC. They are the first successful high-speed trains to be designed and manufactured in China.

Initially known as the China Standardized EMU, development on the project started in 2012, and the design plan was finished in September 2014. The first EMU rolled off the production line on 30 June 2015. The series received its current designation of Fuxing in June 2017, with nicknames such as "Red Dragon" (CR400AF) and "Golden Phoenix" (CR400BF) for certain units. It is among the world's fastest conventional high-speed trains in regular service, with an operating speed of 350 km/h for the CR400AF and CR400BF models.

The Fuxing Hao high-speed train stands as a testament to China's ingenuity, being exclusively developed within its borders. Notably, China retains complete ownership of its intellectual property rights.

Presently, more than 4,000 Fuxing Hao trains are operational across 32 provinces in China. These trains boast an impressive average speed of 350 kilometers per hour.

The Network Continues to Grow

As of the end of last year, China's railway network had stretched to 162,000 kilometers, with 48,000 km dedicated to high-speed rail, further pressing its advantage as the global leader in high-speed rail.

China aims to expand the length of its operating high-speed rail tracks to around 60,000 km by 2030, up from 48,000 km at the end of 2024.

The length of China's high-speed network will surpass 50,000km by the end of this year. Song also revealed that CR is aiming to expand the network to more than 70,000km by the end of 2035, and increase the maximum speed to 400km/h from 350km/h today.

Diversification Beyond Rail

CRRC is increasingly positioning itself as more than a rolling stock manufacturer. The company is expanding into wind power equipment, industrial robots, polymer composite materials, new energy automobiles, environmental protection, photovoltaic power generation, and maritime engineering equipment.

In October 2016, CRRC announced research and development of a 600 km/h maglev train, the CRRC 600, and the construction of a 5 kilometres test track. In June 2020, a prototype trial run was conducted at Tongji University. In July 2021, China's first high-speed maglev train with a designed top speed of 600 km/h rolled off the production line in Qingdao, Shandong. Developed by CRRC Qingdao Sifang, the train underwent testing on dedicated maglev tracks. On 17 July 2025, CRRC officially unveiled the 600 km/h high-speed maglev train at the 12th UIC World Congress on High-Speed Rail in Beijing.

2024 Financial Performance

Rail equipment revenue reached RMB 110.461 billion, up 12.5% year-on-year, while new industry revenue rose to RMB 86.375 billion, up 7.13%.

Total new orders for the year reached approximately RMB 322.2 billion, including RMB 47.2 billion in international orders.

In 2024 the company made a revenue of $34.19 Billion USD an increase over the revenue in the year 2023 that were of $32.98 Billion USD.

X. Playbook: Business & Investing Lessons

CRRC's trajectory offers a masterclass in industrial strategy—though the lessons may be as cautionary as they are instructive.

Technology Acquisition Strategy: Market Access as Leverage

China has used an extensive and coordinated set of mercantilist tools to gain high-speed rail technology and market share. It refined and ratcheted up the restrictiveness of these tools over time as its firms became larger and more competitive.

The playbook was brutally effective: leverage access to the world's largest market to extract technology that foreign companies had spent decades developing. By dividing contracts among multiple foreign suppliers, China avoided dependence on any single source while maximizing the breadth of technology absorbed.

Most government tenders were awarded to domestic companies, resulting in a continuous decline in market share for foreign corporations like Alstom, Kawasaki, and Siemens since the late 2000s.

Scale as Destiny

China's high-speed network reached 48,000km at the end of 2024, accounting for 70% of the world's total high-speed lines.

CRRC's domestic monopoly provides an unassailable foundation. No foreign competitor can match the volume-based cost advantages that come from supplying 70% of the world's high-speed rail network. This scale enables R&D investments that would be impossible for smaller players.

The Chinese railway market is now dominated by CRRC Corporation Limited. CRRC holds a market share of over 90% in railway and urban rail vehicles on the Chinese market.

The State Capitalism Model

In 2023, CRRC received the equivalent of US$214 million in state subsidies.

Large state-backed loans and subsidies were granted to CNR and CSR. The debt owed to state-owned banks by both companies 'surged over sevenfold from $70 billion in 2005 to over $558 billion in 2017.'

The state capitalism model provides patient capital, guaranteed domestic demand, and strategic coordination that private companies cannot replicate. The government can orchestrate mergers, coordinate R&D across institutions, and subsidize export expansion—all in service of long-term industrial goals.

Lessons for Foreign Partners

Chinese high-speed rail firm CRRC is less innovative than European and Japanese firms, but mercantilist policies help it dominate in China and expand globally. This starves superior firms of revenue, reduces their R&D, and slows the pace of global innovation.

The technology transfer episode offers a sobering lesson for companies contemplating partnerships with Chinese state-backed enterprises. Short-term market access may come at the cost of long-term competitive position.

XI. Analysis: Competitive Position & Investment Considerations

Porter's Five Forces Analysis

| Force | Assessment | Details |

|---|---|---|

| Threat of New Entrants | Very Low | High-speed rail manufacturing requires decades of accumulated expertise, massive capital investment, and established track records for safety certification. Regulatory barriers in most markets further limit entry. CRRC's scale economies make the unit economics prohibitive for new entrants. |

| Bargaining Power of Suppliers | Moderate | CRRC has vertically integrated many critical components, but still relies on some specialized technology suppliers. The company's scale gives it negotiating leverage, but high-technology components from specialized suppliers retain some pricing power. |

| Bargaining Power of Buyers | Low (Domestic), Moderate (International) | In China, CRRC faces essentially captive demand from China Railway, the state-owned rail operator. Internationally, buyers have more options but face limited alternatives for certain product categories. |

| Threat of Substitutes | Low | For high-speed rail, no practical substitute exists for the combination of speed, capacity, and energy efficiency. Air travel competes on longer routes but faces capacity and environmental constraints. |

| Competitive Rivalry | Low (Domestic), Moderate (International) | CRRC holds over 90% of China's domestic market. Internationally, it competes with Alstom, Siemens, Hitachi, and Hyundai Rotem, but geopolitical restrictions increasingly segment markets. |

Hamilton's 7 Powers Framework

Scale Economies: CRRC's dominant position derives primarily from unmatched scale. Supplying 70% of world high-speed rail kilometers generates cost advantages in manufacturing, R&D amortization, and supplier negotiations that no competitor can approach.

Network Effects: Limited direct network effects, but significant ecosystem effects through China's standardized rail infrastructure, training programs, and component suppliers optimized for CRRC products.

Counter-Positioning: CRRC's state-backed model represents counter-positioning versus Western competitors who cannot access equivalent government support. This is a structural advantage in markets where state financing is acceptable, but a liability where it triggers sanctions.

Switching Costs: High for installed base—rail operators standardize on equipment families for maintenance efficiency, spare parts inventory, and crew training. This creates durable advantages in markets where CRRC has established presence.

Cornered Resource: CRRC's access to China's domestic market represents a cornered resource—no competitor can access equivalent scale without a comparable captive market.

Process Power: Decades of high-volume production have embedded learning curve advantages in manufacturing processes, though quality issues suggest this power may be less developed than scale advantages.

Branding: Weak internationally, where CRRC carries negative associations with state subsidies and geopolitical tensions. Strong domestically, where Fuxing trains are symbols of national achievement.

Key Metrics to Watch

For investors tracking CRRC's ongoing performance, three KPIs warrant particular attention:

-

International Order Value as Percentage of Total Backlog: This metric captures CRRC's success in diversifying beyond its captive domestic market. A declining percentage would signal intensifying geopolitical headwinds, while growth would indicate successful navigation of trade barriers.

-

Contract Execution Rate (On-Time Delivery): The SEPTA cancellation and MBTA delays damaged CRRC's reputation. Consistent on-time delivery is essential for winning future international contracts and maintaining pricing power.

-

R&D Intensity (R&D Spending/Revenue): CRRC's long-term competitive position depends on maintaining technological leadership through the Fuxing platform and next-generation products like CR450. Declining R&D intensity would signal reduced innovation ambition.

Bull Case vs. Bear Case

Bull Case: - Domestic demand remains robust with plans to expand high-speed network to 70,000km by 2035 - CR450 platform positions CRRC at technological frontier with 400 km/h operation - Belt and Road Initiative provides durable pipeline of emerging market opportunities - Diversification into wind, EVs, and automation provides growth optionality - State backing ensures access to patient capital for long-term investments

Bear Case: - U.S. and EU market access effectively closed, limiting addressable market - Quality and delivery issues undermine reputation and pricing power - Emerging market contracts carry higher execution risk and lower margins - Geopolitical tensions may spread to additional markets (e.g., Five Eyes countries) - Overcapacity in Chinese domestic market as network completion approaches

Myth vs. Reality

| Myth | Reality |

|---|---|

| "CRRC is simply a low-cost competitor" | CRRC's Fuxing trains represent genuine technological achievement, operating at speeds no Western operator has matched commercially. The company has moved beyond mere cost competition to technological leadership in high-speed rail. |

| "Chinese technology transfer was 'theft'" | Technology transfer was contractually agreed—foreign companies accepted terms in exchange for market access. The wisdom of those deals is debatable, but they were legal commercial transactions. |

| "CRRC cannot compete without subsidies" | While subsidies provide advantages, CRRC's scale-based cost structure would make it competitive in many markets regardless. The subsidy question is most relevant for premium pricing in developed markets. |

Material Risks and Regulatory Considerations

Geopolitical Risk: CRRC is named on the U.S. Department of Defense list of Chinese military companies, subject to investment restrictions, and faces regulatory scrutiny in multiple Western jurisdictions. These designations could expand to additional countries.

Subsidy Investigations: The EU's Foreign Subsidies Regulation investigation, though resolved through CRRC's withdrawal, established a template for challenging CRRC bids in future European tenders.

Debt Levels: As of 2022, the China State Railway Group carries debt of approximately US$900 billion, with the system operating at a daily loss of US$24 million. While this debt sits with CRRC's customer rather than CRRC itself, sustained losses at China Railway could eventually constrain domestic demand.

Accounting Considerations: State subsidies flow through CRRC's financials in complex ways, including direct grants, preferential loan terms, and advantageous land access. Investors should scrutinize the "other income" line items and government grant disclosures for a complete picture of economic performance.

XII. Conclusion: The View from the Platform

At Shanghai Hongqiao Station, one of the world's busiest rail hubs, CR400AF "Red Dragon" trainsets depart every few minutes for cities across China. The station itself—a soaring architectural statement covering 1.3 million square meters—stands as testament to the scale of China's railway ambitions. On any given day, more than 20 million passengers ride Chinese high-speed trains, a number that would have seemed fantastical when the technology transfer negotiations concluded in 2005.

CRRC's story is, in many ways, the story of China's industrial rise: patient strategy, state coordination, market leverage, technology absorption, and ultimately, indigenous capability. The company today operates at a scale that no competitor can match, supplying equipment for a high-speed network that accounts for 70% of the world's total.

Yet the story is also one of gathering constraints. The markets that CRRC most wants to conquer—the United States, the European Union, Japan—have largely closed their doors. Quality issues have undermined the value proposition that won early contracts. And the geopolitical climate shows no sign of warming.

For investors evaluating CRRC, the fundamental question is whether the massive scale of the captive Chinese market can sustain growth and profitability as international expansion stalls. With plans to expand domestic high-speed track from 48,000km to 70,000km by 2035, the runway remains substantial—but the steepest growth phase may be past.

The CR450 prototypes represent CRRC's bet on continued technological leadership. If the company can successfully commercialize 400 km/h operation—faster than any service anywhere in the world—it will have demonstrated capabilities that even its detractors cannot dismiss. The maglev program, though more speculative, positions CRRC for potential step-change advances in ground transportation.

What emerges from the CRRC story is a picture of industrial strategy at its most sophisticated—and also at its most contested. The playbook that worked spectacularly from 2004 to 2015 is encountering resistance in an era of great power competition. Whether CRRC can adapt to this new environment, or whether its growth will increasingly be confined to the developing world and China's massive domestic market, remains the central question for the company's next decade.

As the Fuxing trains accelerate out of Hongqiao Station, reaching 350 km/h within minutes, they carry with them the aspirations of a nation that has, in a single generation, transformed itself from a technology borrower into a technology leader. CRRC's journey—from Qing dynasty workshops to world's largest rail manufacturer—encapsulates both the achievements and the tensions that will define industrial competition in the century ahead.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube