Hong Kong Exchanges and Clearing: The Gateway to China

The Bridge Between Two Worlds

On a crisp autumn morning in November 2014, something unprecedented happened in the world of global finance. At precisely 9:30 AM Hong Kong time, Chinese retail investors in Shanghai clicked their trading terminals and, for the first time in history, bought shares in companies listed on the Hong Kong Stock Exchange. Simultaneously, international fund managers in New York, London, and Singapore accessed mainland China's A-share market through Hong Kong's infrastructure. This was the launch of Shanghai-Hong Kong Stock Connect—a scheme that would fundamentally reshape how the world's second-largest economy interfaces with global capital.

Hong Kong Exchanges and Clearing Limited (HKEX) operates a range of equity, commodity, fixed income and currency markets through its wholly owned subsidiaries The Stock Exchange of Hong Kong Limited (SEHK), Hong Kong Futures Exchange Limited (HKFE) and London Metal Exchange (LME). As of December 2024, HKEX has a market capitalization of approximately US$35 trillion and 2,631 listed companies, making it the 8th largest stock exchange globally.

But what makes HKEX truly remarkable isn't just its size—it's its unique position as the world's premier "super-connector" between China and international capital markets. The stock exchange is owned by Hong Kong Exchanges and Clearing Limited, a holding company that in 2021 became the world's largest bourse operator in terms of market capitalization, surpassing Chicago-based CME.

The story of how a colonial-era trading house transformed into this gateway is one of the most fascinating narratives in financial history—a tale spanning opium traders and Qing Dynasty ports, British colonial governance, Beijing's grand opening strategy, and the digital revolution that's reshaping finance. It involves visionary leaders who saw China's integration into global markets before almost anyone else, catastrophic market crashes that forced reform, and billion-dollar bets that sometimes paid off spectacularly—and sometimes didn't.

This is that story.

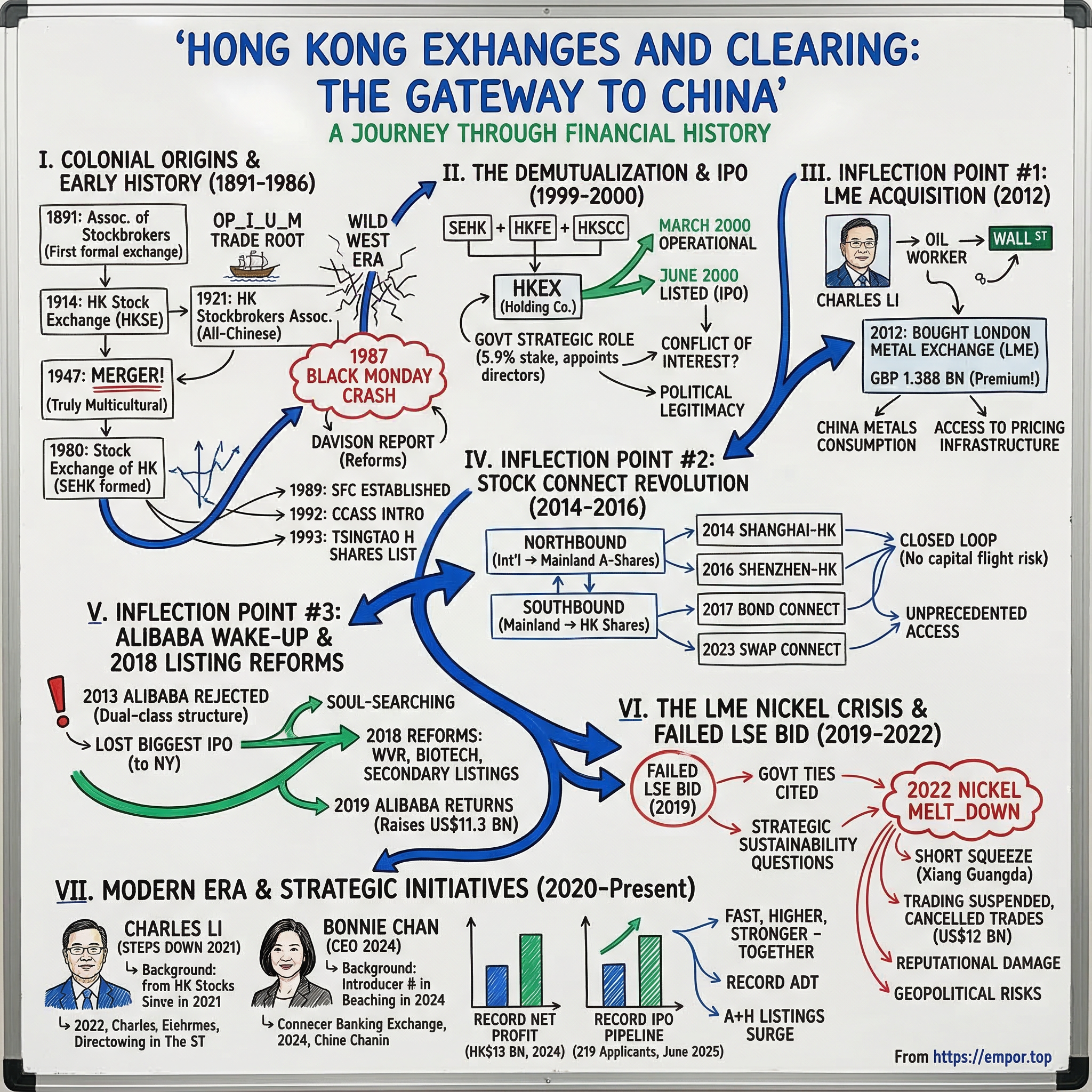

I. Colonial Origins & Early History (1891-1986)

The Opium-Era Roots

Picture Hong Kong in the late 19th century: a British colonial outpost built on the opium trade, its harbor crowded with trading vessels carrying tea, silk, and—more controversially—narcotics bound for the Chinese mainland. In the narrow streets of Central, British merchants and Chinese compradors conducted business in pidgin English, signing contracts over cups of congee and afternoon tea.

The Hong Kong securities market can be traced back to 1869, but the stock market was formally set up in 1891, when the Association of Stockbrokers in Hong Kong was established. It was established in response to the Share Bill which was proposing much needed regulation to stop speculation in the market.

The Hong Kong Stock Exchange can be traced back to 1891 when the Association of Stockbrokers in Hong Kong was established as the first formal stock exchange. In 1914, its name was changed to the Hong Kong Stock Exchange (HKSE).

The early market was an entirely British affair. Trading happened on the streets and in teahouses—informal, gentlemanly, and completely lacking the infrastructure we'd recognize today. The Association's founding chairman, Mr. Vernon, led a cohort of British traders who saw an opportunity to formalize capital markets in this emerging Asian entrepôt.

Non-Chinese membership characterized the exchange until 1921, when the Hong Kong Stockbrokers' Association was formed, which was an all-Chinese stock exchange. After the end of World War II, the two exchanges merged to form the new Hong Kong Stock Exchange.

This merger in 1947 was more than administrative convenience—it represented Hong Kong's emergence as a truly multicultural financial center, where British capital and Chinese entrepreneurship could coexist.

The Wild West Era

The next two decades saw Hong Kong transform from a sleepy colonial port into an industrial powerhouse. Refugees fleeing communist China brought capital, skills, and an entrepreneurial drive that would define the territory. The rapid growth of Hong Kong's economy triggered the emergence of other exchanges – i.e., the Kam Ngan Stock Exchange, the Far East Exchange, and the Kowloon Stock Exchange. The three exchanges unified their activities in 1980, with the formation of the Stock Exchange of Hong Kong.

Due to rapid economic growth in Hong Kong, three other exchanges were later opened in the late 1960s and early 1970s. First, there was the Far East Exchange, which opened its doors in 1969. Then, Kam Ngan Stock Exchange launched in 1971, and it was soon followed by Kowloon Stock Exchange, which opened in 1972. Following pressure to increase the regulation of the various markets, those three exchanges and Hong Kong were consolidated into the Stock Exchange of Hong Kong (SEHK) in 1980, which began trading on 2 April 1986.

By the early 1970s, Hong Kong had four competing stock exchanges—a situation that created chaos and opportunity in equal measure. Different exchanges quoted different prices for the same shares. Investors could arbitrage between venues. Regulation was minimal. It was, in the words of one contemporary observer, the "Wild West of Asian finance."

The 1987 Crash and Its Aftermath

In October 1987, the Stock Exchange was closed for four days in an attempt to stop losses during Black Monday global equities market crash. In May 1988, the Ian Hay Davison Report, commissioned to investigate practices on the exchange in the lead-up to its closure, is released, resulting in significant market reforms - although many took years to finally implement.

Often referred to as "Black Monday," this crash occurred on October 19, 1987, and was part of a global stock market crash. Hong Kong's Hang Seng Index plummeted by over 45% in a single day.

The 1987 crash exposed fundamental weaknesses in Hong Kong's market infrastructure. While other global exchanges struggled and then recovered, Hong Kong's decision to close for four days was widely criticized as panicky and amateurish. The Davison Report that followed was scathing: the exchange lacked proper risk management, clearing systems, and regulatory oversight.

The market crash of 1987 showed that further reforms were needed. These reforms led to the creation of a central exchange system and the establishment of the Securities and Futures Commission (SFC) in 1989.

The crisis became the catalyst for modernization. On 24 June 1992, the Central Clearing and Settlement System (CCASS) was introduced. On 15 July 1993, the Tsingtao Brewery became the first Chinese enterprise to list its H shares on the exchange.

That Tsingtao Brewery listing was a harbinger of things to come. For the first time, a mainland Chinese company was raising capital in Hong Kong. It was a small step, but one that pointed toward HKEX's eventual destiny as the primary offshore fundraising platform for China Inc.

So what for investors: The 1987 crash established a pattern that would repeat throughout HKEX's history: crisis as catalyst for reform. Each major shock—whether market collapse, regulatory failure, or competitive threat—ultimately strengthened the institution. This crisis-response muscle would prove essential in the decades ahead.

II. The Demutualization & IPO (1999-2000)

The Reform Imperative

By the late 1990s, Hong Kong faced an existential question: How could it remain relevant as a financial center in the new millennium? The handover to China in 1997 had raised questions about the territory's future. The Asian Financial Crisis of 1997-98 had battered confidence. And the global exchange industry was consolidating rapidly.

Following the October 1987 stock market crash, Hong Kong authorities instituted in 1989 a comprehensive reform of the city's various securities and commodities exchanges in order to "enhance the competitiveness of the Hong Kong stock exchange and to meet the challenge of an increasingly globalised market." "The reforms included the establishment of a more widely representative Council and a strong, professional executive management team, to safeguard the interests of all participants and to operate and develop the market effectively." Under the reform, the Stock Exchange of Hong Kong (SEHK), the Hong Kong Futures Exchange (HKFE) and the Hong Kong Securities Clearing Company (HKSCC) were merged under a single holding company, HKEX. The merger took operational effect on 6 March 2000.

The solution was bold: demutualize the exchanges, merge them into a single holding company, and take that company public. Under the reform, SEHK and Hong Kong Futures Exchange Limited (HKFE) were demutualised, the two exchanges and their respective clearing houses were merged with the Hong Kong Securities Clearing Company Limited (HKSCC) to form a single holding company - Hong Kong Exchanges and Clearing Limited (HKEx). In accordance with the Schemes of Arrangements of the exchanges and the Exchanges and Clearing Houses (Merger) Ordinance which took effect on 6th March 2000, SEHK became a wholly-owned subsidiary of HKEx together with HKFE and HKSCC.

On 6 March 2000, The Stock Exchange, Futures Exchange, and Hong Kong Securities Clearing Company all became wholly owned subsidiaries of HKEx, which was in turn listed on 27 June 2000.

The IPO was a milestone. HKEX became a publicly-traded company—a rarity among major exchanges at the time. This created powerful incentives for innovation and efficiency. The exchange was no longer a sleepy club run by its members; it was now a competitive enterprise answerable to shareholders.

The Government's Strategic Role

The Hong Kong Government is the single largest shareholder in HKEX, and has the right to appoint six of the thirteen directors to the board.

This governance structure was—and remains—controversial. In September 2007, the government revealed that it had increased its stake in HKEX from 4.41 percent to 5.88 percent. According to market sources, the Government spent HK$2.44 billion to buy 15.72 million shares in the company. The stake would be held by the Exchange Fund as a "strategic asset".

The largest shareholder is the Hong Kong Special Administrative Region Government, which holds a direct 5.9% stake. Citigroup, now the second-largest shareholder with a 5% stake, has surpassed JPMorgan, which reduced its shareholding.

The government's stake created what some critics called an inherent conflict of interest. Financial commentator Jake van der Kamp noted the Financial Secretary's conundrum: The government is faced with a conflict of interest, as its desire for an efficient marketplace is contrary to its desire as a shareholder, who would prefer to maximise returns.

Activist investor David Webb said that HKEX's desire to delist stemmed from these companies generating very little revenue for the exchange but taking up a disproportionate amount of staff resources. Webb decried the conflict of interest between its role as operator and regulator, and called on the regulatory role to be passed to the SFC.

Yet the government stake also provided something invaluable: political legitimacy and a direct line to Beijing's priorities. As Hong Kong positioned itself as China's offshore financial center, having government involvement meant HKEX's interests were closely aligned with broader policy objectives—including China's desire to open its capital markets on its own terms.

So what for investors: HKEX's governance structure—government stake, right to appoint directors, public listing—creates a unique hybrid: commercial incentives tempered by strategic policy considerations. This structure has enabled bold moves (like the LME acquisition) that a purely commercial entity might shy away from, while also exposing the exchange to political risks that concern some investors.

III. Inflection Point #1: The LME Acquisition (2012)

Charles Li's Vision

Charles Li Xiaojia (born 25 March 1961) is a Chinese banker. He was the Chief Executive of the Hong Kong Exchanges and Clearing Limited (HKEX) from 2010 to 2021.

Charles Li's biography reads like a parable of China's opening to the world. Li was born in 1961 and was an offshore oil worker in the north China sea prior to college. He became a newspaper editor-reporter for the China Daily from 1984 to 1986 and obtained a bachelor's degree in journalism from the Xiamen University in 1984 before he studied at the University of Alabama in which he was graduated with a master's degree in 1988. In 1991, he obtained a Juris Doctor degree from Columbia Law School. After graduation, Li practiced law in New York with Davis Polk & Wardwell and Brown & Wood. He also began to work in the financial services sector, including in corporate and securities law practices, corporate finance and advisory services in New York, mainland China and New York, and joined Merrill Lynch in 1994 and became president of Merrill Lynch China in 1999.

From oil worker in the North China Sea to J.D. at Columbia Law to Wall Street dealmaker—Li embodied the bridge between China and the West that he would later help HKEX become. The China Chairman of JPMorgan Chase & Co. before being hired to head the HKEX, Li is best known as the architect of the Connect programme, a series of cross-border investment channels that allow global investors to tap China's yuan-denominated A shares and bonds, while letting Chinese institutions and individuals invest in shares and financial instruments listed in Hong Kong and London.

The Audacious Bid

In June 2012, HKEX announced its cash offer to acquire the London Metal Exchange (LME), the world's premier metal exchange since its founding in 1877, for GBP1.388 billion. The acquisition was completed in December 2012.

The LME was a peculiar target. Founded in 1877 above a London hat shop, it was the world's oldest and most important commodities exchange for base metals—copper, aluminum, zinc, nickel, lead, and tin. Its "Ring" trading floor, where red-coated dealers shouted orders in a centuries-old open outcry system, seemed like a relic of a bygone era.

On July 25, 2012, London Metal Exchange shareholders approved a $2.2 billion takeover offer from Hong Kong Exchanges & Clearing Ltd. The vote was more than 99 percent in favor of the deal. HKEX's proposal won out over offers from its rivals CME Group, Intercontinental Exchange and NYSE Euronext.

HKEX acquired the London Metal Exchange in the summer of 2012. HKEX agreed in June to pay 1.39 billion British pounds ($2.15 billion) for the exchange, outbidding Intercontinental Exchange. The transaction was the exchange's first overseas acquisition and gave the exchange its first commodities contracts.

At nearly 180 times the LME's 2011 earnings, the price raised eyebrows. But Li saw something others didn't: China was consuming half the world's base metals, yet Chinese companies lacked proper hedging tools. The LME wasn't just a commodities exchange; it was the infrastructure for global metals pricing, and China desperately needed access to that infrastructure.

LME continues to be based in London and to be regulated by the U.K. Financial Conduct Authority. HKEX said the deal would help grow the number of clients in China and help disperse LME data across Asia. In addition, HKEX said it would "keep the LME's existing warehousing network, help the bourse develop its own clearing house and freeze trading fees until at least the start of 2015."

The integration commitments reflected shrewd political navigation. By promising to keep the LME in London under UK regulation, HKEX defused nationalist concerns. By committing to fee freezes and infrastructure investments, it won over the LME's traditional members.

So what for investors: The LME acquisition demonstrated HKEX's willingness to make transformative bets on China's growth trajectory. It also revealed the exchange's tolerance for paying premium prices for strategic assets—a pattern that would repeat with other initiatives.

IV. Inflection Point #2: Stock Connect Revolution (2014-2016)

A New Architecture for Capital

If the LME acquisition was about commodities, Stock Connect was about reshaping how the world's capital flows to and from China. He was also the architect of the groundbreaking Shanghai-Hong Kong Stock Connect cross-border trading scheme in 2014, which was expanded to include Shenzhen-Hong Kong Stock Connect in 2016 and Bond Connect in 2017.

He also helped cement Hong Kong's role as a conduit for the outside world to invest in China with the launch in 2014 of the Stock Connect trading link between the Hong Kong and Shanghai stock exchanges. This created a new opening for international investors to gain exposure to China's domestic market.

The genius of Stock Connect lay in its structure. Rather than requiring investors to open accounts in unfamiliar jurisdictions, navigate foreign regulations, or convert currencies, the system allowed them to trade through their existing brokers. During his tenure Li orchestrated some of the most significant strategic initiatives in HKEX's history, including the 2012 acquisition of the London Metal Exchange, which provided it with its first commodities contracts, and the launch of central counterparty OTC Clear in 2013. He also helped cement Hong Kong's role as a conduit for the outside world to invest in China with the launch in 2014 of the Stock Connect trading link between the Hong Kong and Shanghai stock exchanges. This created a new opening for international investors to gain exposure to China's domestic market. It was followed by a similar link with the Shenzhen stock exchange, as well as a bond market equivalent.

The program was scalable, controllable, and—crucially—operated within a closed loop that satisfied Beijing's concerns about capital flight while giving international investors unprecedented access.

Shenzhen Connect and Beyond

Bond Connect is an innovative mutual market access scheme that enables investors from Mainland China and overseas to trade in each other's bond markets through connection between the related Mainland and Hong Kong financial infrastructure institutions. Northbound trading commenced on 3 July 2017, offering China Interbank Bond Market (CIBM) access to international investors, and Southbound trading was launched on 24 September 2021, providing a convenient and efficient channel for Mainland China institutional investors to invest in offshore bonds through the Hong Kong bond market.

The Connect franchise kept expanding. Each new program—Shenzhen Connect in 2016, Bond Connect in 2017, ETF Connect in 2022, and Swap Connect in 2023—added new asset classes and deepened the integration between Hong Kong and mainland markets.

Hong Kong Exchanges and Clearing Limited (HKEX) today celebrated the launch of Swap Connect, the new mutual access programme between Hong Kong and Mainland China's interbank interest rate swap markets, with a ceremony held at HKEX Connect Hall and in Beijing. HKEX, through its clearing subsidiary OTC Clear, has been working with China Foreign Exchange Trade System (CFETS) and Shanghai Clearing House (SHCH) to support the trading and clearing of Swap Connect, which is launching initially with a Northbound channel.

Following on from Stock Connect and Bond Connect, Swap Connect is another innovation of Hong Kong and Mainland China mutual access programme and is the world's first derivatives mutual market access programme. The launch of Swap Connect will help forge stronger ties between Hong Kong's and Mainland China's capital markets, encourage the sustainable development of common financial markets and enhance Hong Kong's role as an international financial centre.

For investors, the Connect schemes solved a problem that had bedeviled China allocation for decades: how to gain exposure to the world's second-largest economy without the regulatory and operational headaches of direct investment.

So what for investors: Stock Connect transformed HKEX from a regional exchange into genuinely irreplaceable infrastructure for accessing China. This "super-connector" position creates a moat that competitors cannot easily replicate—it took years of negotiation with Beijing to establish these schemes.

V. Inflection Point #3: The Alibaba Wake-Up Call & 2018 Listing Reforms

The Loss That Changed Everything

In late 2013, representatives from Alibaba Group sat across the table from Hong Kong exchange officials, negotiating terms for what would become the largest IPO in history. Alibaba had proposed a partnership structure that would allow Jack Ma and a small group of managers to control board appointments—effectively retaining control of the company while taking money from public shareholders.

For months Alibaba Group Holding Limited had tried to convince the Stock Exchange of Hong Kong Limited (SEHK) that they should open their doors to the internet giant. Alibaba had proposed a system through which a handpicked group of "partners" would nominate a majority of its board.

While Alibaba may have originally preferred to achieve this through a simple dual share class structure, knowing this is contrary to the SEHK's Rules Governing the Listing of Securities ("Listing Rules") they proposed a partnership structure which would enable a group of partners, comprised of founders and top managers "to set the company's strategic course without being influenced by the fluctuating attitudes of the capital markets". The partners, they believe, would enable the company to preserve its culture and safeguard the development of the company long after its original founders have gone. In essence, the partners would be entitled to nominate the majority of Alibaba's directors for a shareholder vote, and would nominate an alternative if shareholders reject a candidate. Investors would still have the right to elect independent directors, and vote on major and related party transactions. This proposal was rejected by Hong Kong regulators in late September 2013.

Hong Kong said no. The exchange's long-standing "one share, one vote" principle—established after problems with B shares in the 1980s—wouldn't bend.

Back in 2014, Hong Kong's stock exchange rejected Alibaba's application for an initial public offering because the company wanted to adopt a dual-class share structure. The decision meant losing the world's biggest IPO, as the Chinese company eventually went to New York and raised a record US$25 billion. It was a blow to executives at the exchange and led to a period of soul-searching that culminated this year in a belated U-turn on the issue.

Alibaba Group Holding held its record $25 billion public float in New York in 2014 after Hong Kong, its favoured venue, refused to accept its governance structure where a self-selecting group of senior managers control the majority of board appointments.

The aftermath was painful. Hong Kong had let the largest IPO in history slip through its fingers. Worse, it signaled to the emerging generation of Chinese tech entrepreneurs that Hong Kong wasn't a viable listing venue.

On March 17, 2014, Charles Li said in response to Alibaba's plans for an IPO in the United States that the SEHK needs "to find ways to make our market more responsive and competitive, particularly with respect to new economy or technology companies". In earlier comments, Charles Li had noted that, "losing one or two listing candidates is not a big deal for Hong Kong; but losing a generation of companies from China's new economy is."

The 2018 Reforms

It took four years, but Hong Kong eventually changed course. On April 30, 2018, HKEx introduced a series of reforms to encourage the listing of high-tech, new-economy companies with dual-class share structures and pre-revenue biotech companies.

"After a remarkable four-year journey of careful deliberation, HKEX's new listing regime is finally open for business," said HKEX Chief Executive Charles Li. "We are now at the dawn of an exciting new era for Hong Kong's capital markets."

The reforms came in three parts: weighted voting rights for innovative companies, Chapter 18A allowing pre-revenue biotech companies to list, and Chapter 19C facilitating secondary listings of overseas-listed companies.

The new rules subsequently published on April 24, 2018, represent the most significant changes to the Hong Kong listing regime in over 20 years. The new rules and corresponding amendments to the Main Board Listing Rules permit listings of high-growth and innovative companies with dual-class shares or "weighted voting rights" (WVR) structures; permit listings of preprofit/prerevenue biotech issuers.

Smartphone maker Xiaomi Corp was the first company to take advantage of Hong Kong's new rules and raised $4.72 billion in an IPO for a $54 billion valuation.

Alibaba's Return

Chapter 19C of the Main Board Listing Rules allows companies listed on an overseas qualifying exchange, with their "centre of gravity" in Greater China, to seek secondary listing on HKEx. Following the reforms, Chinese e-commerce giant Alibaba Group's secondary listing on HKEx debuted on 26 November 2019, raising at least US$ 11.3 billion, surpassing Uber Technologies' US$ 8.1 billion offering in May 2019 and representing the largest in Hong Kong since insurance group AIA's HK$ 159 billion was raised in 2010. By the end of its first session, Alibaba's shares closed at HK$ 187.60, 6.6 percent higher than the issue price of HK$ 176 per share.

Alibaba's return was a vindication—and a reminder of what Hong Kong had missed five years earlier. The secondary listing raised over $11 billion, but more importantly, it signaled that the new regime worked and that major tech companies would consider Hong Kong again.

So what for investors: The Alibaba saga demonstrates both HKEX's governance rigidity and its ultimate adaptability. The exchange's willingness to change course—even if belatedly—preserved its relevance. But investors should note the four-year delay: in fast-moving markets, such delays can be costly.

VI. The LME Nickel Crisis & Failed LSE Bid (2019-2022)

Overreach in London

On September 11, 2019, Charles Li made his boldest move yet: a surprise $39 billion offer to acquire the London Stock Exchange. Hong Kong's bourse on Tuesday dropped its unsolicited $39 billion bid for London Stock Exchange Group (LSE), conceding it hadn't won over LSE management for a move that could have transformed both global financial services businesses.

London Stock Exchange Group Plc has rejected a takeover proposal from Asian rival Hong Kong Exchanges & Clearing Ltd., saying the bid has "fundamental flaws." The board of the British bourse, which is working on its own deal to buy data provider Refinitiv, said HKEX's approach on Wednesday had problems in its "strategy, deliverability, form of consideration and value."

The rejection was swift and brutal. London Stock Exchange Group on Friday formally rejected a takeover bid by its Hong Kong rival, citing "fundamental" flaws and concerns over its ties to the Hong Kong government. In a statement, LSEG said management "unanimously rejects the conditional proposal" from Hong Kong Stock Exchange (HKEX) and "given its fundamental flaws, sees no merit in further engagement" regarding the offer worth almost 32 billion. "There is no doubt that your unusual board structure and your relationship with the Hong Kong government will complicate matters," LSEG told HKEX bosses in a letter published alongside the rejection statement.

Furthermore, we question the sustainability of HKEX's position as a strategic gateway in the longer term. The Hong Kong concentration and core characteristics of your business, together with your Hong Kong domicile and listing, present an additional set of difficulties.

The timing couldn't have been worse. Pro-democracy protests were roiling Hong Kong, raising questions about the territory's future autonomy. The LSE's rejection letter cited not just strategic concerns but explicitly raised issues about HKEX's government ties.

The LSE board unanimously rejected the offer, citing "fundamental flaws." HKEX dropped its bid in October 2019, after failing to secure support from LSE shareholders.

The 2022 Nickel Meltdown

If the failed LSE bid was embarrassing, the nickel crisis of March 2022 was existential. The L.M.E. suspended nickel market trading on 8 March 2022, halting trade in all nickel contract and canceling trades executed on or after midnight local time. The market reopened on 16 March, only to shutdown again when it quickly hit the price decline limit of 5 percent. It hit the expanded limit of 8 percent on 17 March, shutting down again for the day, and the larger expanded limit of 12% price decline on 18 March. The turmoil began two weeks after the Russian invasion of Ukraine and some analysts see Russia's large nickel exports as a related cause.

In the several months leading to March 2022, Xiang Guangda began taking a large short position in nickel through Tsingshan Group, in order to hedge against falling prices. Due to a rise in nickel prices by early March, Xiang was forced to purchase nickel contracts at the LME, creating a short squeeze. By the time trading had been suspended, Tsingshan had suffered US$8 billion in losses on paper.

However, nickel almost brought down the London Metal Exchange (LME), the world's largest and oldest trading venue for industrial metals, two years ago. Over the course of three days, the nickel price traded on the bourse surged by more than 270 per cent from US$27,080 per tonne to more than US$100,000 on 8 March 2022 before falling to around US$80,000 per tonne. The LME took action by suspending the trading and returning the price to the previous date, cancelling billions of US$ in transactions. The 147-year-old bourse saw it necessary to prevent a "death spiral" that could have led itself and its members to collapse. One of the members, a Chinese company and world leader in nickel production, Tsingshan, was saved from the verge of losing US$8 billion.

The decision to cancel $12 billion in trades was unprecedented. In the words of its chief risk officer, the situation carried "a significant risk of market collapse leaving the LME unable to function as a venue for the world's non-ferrous metals markets." Hedge fund Elliott Investment Management and trading firm Jane Street are seeking $472 million in damages in a judicial review, but the $12 billion of trades the LME cancelled on March 8 is more than 100 times its annual profit.

Its handling of the saga has been criticized by everyone from the International Monetary Fund to Citadel Securities' Ken Griffin.

The courts ultimately sided with the LME, but the reputational damage was severe. Critics argued that the cancellation protected Tsingshan—a major Chinese producer—at the expense of traders who had legitimately profited from the squeeze.

So what for investors: The failed LSE bid and nickel crisis exposed HKEX's vulnerabilities. The Hong Kong government connection that enables strategic flexibility also creates geopolitical risks. The LME, once seen as a crown jewel, became a source of legal liability and reputational damage.

VII. Modern Era & Strategic Initiatives (2020-Present)

Leadership Transition

He officially stepped down on 1 January 2021. Charles Li's departure marked the end of an era. He had transformed HKEX from a regional exchange into a global platform, but the failures of 2019-2022 cast a shadow over his final years.

Bonnie Y Chan is a Hong Kong-based attorney and exchange executive who is the CEO of Hong Kong Exchanges and Clearing Limited (HKEX). She assumed that role on March 1, 2024 and will serve a three-year term. Chan was previously the co-chief operating officer of HKEX.

Bonnie Chan Yiting made history when she was announced CEO of the city's stock exchange operator Hong Kong Exchanges and Clearing (HKEX) in March, being the first woman to serve in the role. Since her appointment—and the market's post-Covid recovery—Hong Kong has been climbing back up the ranks of global IPO markets.

Chan's career spans top-tier legal firms, international banks, and regulatory bodies. She began her journey at Deacons in Hong Kong, moving to Sullivan & Cromwell to gain experience in both the Hong Kong and U.S. markets. Her expertise in capital markets grew during her tenure at Morgan Stanley, where she served as executive director, overseeing Asia's capital markets legal function, from 2003 to 2007. Chan first joined HKEX in 2007 as Head of IPO Transactions, where she played a critical role in modernising Hong Kong's listing framework.

Chan's background—legal, regulatory, institutional—contrasts with Li's dealmaking persona. Her "Faster, Higher, Stronger – Together" strategy emphasizes collaboration over competition. Bonnie Chan, who took the helm as HKEX CEO on March 1, 2024, has swiftly moved to define a forward-looking strategy that redefines the role of a stock exchange in the 21st century. Her "Faster, Higher, Stronger – Together" mantra is not merely a slogan but a blueprint for operational and strategic transformation. The core of her argument posits that achieving greater market speed, higher standards, and stronger foundations necessitates collective action with all stakeholders, from market participants to other global exchanges. This collaborative philosophy is particularly pertinent as exchanges worldwide grapple with the demands for faster trading and quicker settlements, exemplified by the global push towards shorter settlement cycles like T+1, which HKEX is actively preparing for by the end of 2025. Central to Chan's vision is HKEX's role as a "super connector," leveraging its unique position to bridge China with global capital and opportunities.

Record Performance

Upon releasing its annual financial results on Thursday, the bourse operator revealed its net profit for 2024 rose 10 percent year on year to HK$13 billion, from the HK$11.9 billion registered a year earlier. The firm also maintained the payout ratio at 90 percent of earnings. "HKEX achieved significant progress and delivery in 2024, a year that featured greater connectivity and engagement with international markets, the launch of multi-year infrastructure enhancement programmes, and fresh trading records that underscore the market's vibrancy and resilience," said Bonnie Chan. "The improved macro backdrop supported renewed vibrancy and robustness of our markets, which was reflected in the largest IPO in Hong Kong since 2021 as well as an all-time record trading turnover," she noted.

The financial results for 2024 and 2025 have been impressive. Record quarterly high of $7.8 billion in Q3 2025, up 45 per cent compared with Q3 2024. With operating expenses effectively controlled, Q3 profit reached a record quarterly high of $4.9 billion, 56 per cent higher than Q3 2024.

EBITDA margin was 81 per cent, 7 percentage points higher than Q3 2024.

IPO Market Resurgence

Hong Kong is poised to regain the top spot in global IPO market rankings by the end of 2025, fuelled by an unprecedented wave of IPO applications. At the end of the third quarter, the Hong Kong market is setting new benchmarks, with historic number of almost 300 active IPO applications in the pipeline (not including confidential filings) as of 30 September 2025.

We regained our position as the world's No.1 IPO venue, with IPO and follow-on funds raised more than doubled, and enter 2H 2025 with a robust IPO pipeline of 207 active listing applicants as at 30 Jun 2025.

Hong Kong's IPO market rebounded sharply in the first half of 2025, raising HK$107.1 billion across 42 listings, representing a 700% increase in funds raised and a 40% rise in deal volume. The strong momentum is further reflected in the IPO pipeline, which now has 219 applicants, including a record breaking 210 Main Board applicants, and more than double the 86 applicants as at 31 December 2024. A record 7 A+H listings were completed during the period, accounting for 72% of total IPO fund raised. Notably, the world's largest EV battery manufacturer raised HK$41.0 billion in its A+H listing, making it the largest global IPO in the first half of 2025, and also the largest Hong Kong IPO since 2021. The A+H listing trend is expected to continue, as there were already 47 new A+H listing applications during the first six months of 2025, compared to only 5 during the entirety of 2024.

The A+H dual listing surge reflects Beijing's policy of encouraging quality mainland companies to tap Hong Kong's international investor base. "While other global IPO markets have slowed, Hong Kong is showing significant growth driven by A+H and high-tech listings," said Louis Lau, partner and head of Hong Kong Capital Markets Group at KPMG China. "We remain highly optimistic about the outlook for Hong Kong's IPO market for this year and beyond."

So what for investors: HKEX's recent performance suggests the turnaround is real. Record trading volumes, a revived IPO market, and expanding Connect programs all point to strong underlying demand for Hong Kong as a capital markets venue. The question is whether this represents a cyclical upturn or structural improvement.

VIII. Business Model Deep Dive

Revenue Streams

HKEX's business model is elegantly simple: it earns money every time securities trade, clear, or settle on its platforms. The exchange operates through five primary segments:

Cash Market (Equities): Trading and clearing fees from securities transactions on the Hong Kong Stock Exchange. This includes stocks, ETFs, REITs, and structured products. Revenue correlates directly with average daily turnover—when markets are active, HKEX profits.

Equity and Financial Derivatives: Trading and clearing for index futures, options, and other derivative products traded on HKEX and HKFE. Products like Hang Seng Index futures and USD/CNH currency futures generate both trading fees and clearing fees.

Commodities (LME): Base metals trading on the London Metal Exchange—copper, aluminum, zinc, nickel, lead, and tin. Revenue comes from trading fees, clearing fees, and data licensing.

Clearing: The backbone of HKEX's infrastructure. HKSCC, HKCC and SEOCH provide integrated clearing, settlement, depository and nominee activities to their participants, while OTC Clear provides OTC interest rate derivatives and non-deliverable forwards clearing and settlement services to its members.

Data and Connectivity: HKEX provides market data through its data dissemination entity, HKEX Information Services Limited. Market data licensing is a high-margin, recurring revenue stream that grows with the exchange's importance.

Operating Leverage

The financial profile of an exchange is unlike almost any other business. Once infrastructure is built, the marginal cost of an additional trade is essentially zero. This creates extraordinary operating leverage.

EBITDA margin was 81 per cent. An 81% EBITDA margin would be extraordinary in any industry—in financial services, it's almost unheard of. For context, major investment banks typically earn EBITDA margins of 20-35%. Asset managers might reach 40-50%. Exchanges, with their fixed-cost infrastructure and variable revenue, can reach 70-80% in good years.

This leverage works both ways. When volumes surge—as they did in 2025—profits soar. When volumes decline—as they did in 2023—profits fall disproportionately.

The "Super-Connector" Moat

HKEX is the world's leading IPO market and as Hong Kong's only securities and derivatives exchange and sole operator of its clearing houses, it is uniquely placed to offer regional and international investors access to Asia's most vibrant market.

HKEX's competitive position rests on three interlocking advantages:

-

Legal Monopoly: HKEX is Hong Kong's only securities and derivatives exchange. Unlike the US, where NYSE, Nasdaq, and multiple alternative trading systems compete for order flow, Hong Kong has a single venue. This eliminates price competition at the trading layer.

-

Connect Infrastructure: The Stock Connect, Bond Connect, Swap Connect, and ETF Connect programs took years to negotiate with Beijing and can't be replicated by competitors. Any international investor wanting China A-share exposure through a regulated, institutional-quality channel must use HKEX.

-

Network Effects: Liquidity begets liquidity. As more investors trade in Hong Kong, bid-ask spreads narrow, making the market more attractive to additional investors. As more companies list, the market offers better diversification, attracting more capital.

IX. Porter's Five Forces & Competitive Analysis

Threat of New Entrants: VERY LOW

Creating a competing exchange in Hong Kong would require regulatory approval from authorities who have a stake in HKEX's success. Even if approval were granted, a new entrant would face the chicken-and-egg problem: no liquidity attracts no listings, and no listings attract no liquidity. The Stock Connect infrastructure, built over a decade of negotiation with Beijing, cannot be replicated.

Bargaining Power of Suppliers: LOW

HKEX's primary suppliers are technology vendors and data providers. While trading system technology is sophisticated, multiple vendors compete for exchange contracts globally. HKEX has been investing in the Orion Derivatives Platform to reduce dependency on third-party technology.

Bargaining Power of Buyers: MODERATE

Buyers include listed companies (who pay listing fees), traders (who pay transaction fees), and data consumers (who pay for market data). Large institutional traders can negotiate fee discounts, and highly liquid securities often receive preferential treatment. However, for access to China, alternatives are limited.

Threat of Substitutes: MODERATE AND RISING

This is HKEX's most significant competitive concern. Chinese companies can now list on the A-share markets in Shanghai and Shenzhen, which have improved dramatically in quality and accessibility. US markets—particularly Nasdaq—continue to attract Chinese tech companies. ADRs allow non-Hong Kong investors to gain exposure to Hong Kong-listed companies.

This strategic redirection comes at a critical juncture for global financial markets, which are grappling with rapid technological advancements, the emergence of new non-traditional competitors like "big techs" and "digital natives."

Industry Rivalry: LOW (REGIONALLY), MODERATE (GLOBALLY)

Within Hong Kong, HKEX faces no direct competition. Globally, the exchange competes with NYSE, Nasdaq, LSE, and increasingly Shanghai and Shenzhen for major IPOs. The 2018 listing reforms were explicitly designed to compete more effectively for tech company listings.

Hamilton Helmer's 7 Powers Analysis

Network Effects: Strong. Liquidity attracts liquidity. The more investors trade Hong Kong stocks, the more attractive the market becomes for new listings.

Counter-Positioning: Moderate. HKEX's position as a "super-connector" between China and the world is a strategic role that mainland exchanges cannot easily replicate. However, if mainland markets fully open, this positioning weakens.

Switching Costs: High for issuers (delisting is expensive and disruptive), moderate for traders (who can redirect flow with some friction).

Scale Economies: Moderate. Technology and compliance costs are largely fixed, but HKEX is not dramatically larger than major competitors.

Captured Process Power: Low. Exchange operations are relatively standardized globally.

Branding: Strong. HKEX's reputation as a gateway to China is a genuine intangible asset.

Cornered Resource: The Stock Connect programs represent a cornered resource—HKEX has exclusive access to this infrastructure.

X. Bull and Bear Case

The Bull Case

China's Capital Markets Are Still Early: With China's capital markets projected to exceed US$100 trillion by 2030, HKEX's focus on facilitating two-way capital flows is a crucial enabler of this growth. If HKEX captures even a fraction of this growth, the revenue opportunity is immense.

A+H Dual Listing Wave: The exceptional performance was driven by a surge in A+H listings, including the listing of the world's largest manufacturer of batteries for electric vehicles, which collectively accounted for over 70% of total funds raised in Hong Kong during the period. This has positioned Hong Kong as the global IPO market leader in terms of funds raised for the first half of 2025.

Operating Leverage: At 81% EBITDA margins, every incremental dollar of revenue flows almost directly to profit. Even modest volume increases translate to disproportionate earnings growth.

Connect Expansion: Each new Connect program—ETFs, swaps, bonds—expands the revenue opportunity without proportional cost increases. The infrastructure is built; now it's about utilization.

ESG and Carbon Markets: Chan has also led HKEX's effort to eradicate all-male boards among its listed companies, the first major exchange to do so. HKEX is positioning for emerging carbon trading and sustainability products.

The Bear Case

Geopolitical Risk: The LSE's blunt rejection highlighted how HKEX's Hong Kong government ties create deal-blocking concerns. In a world of US-China tensions, HKEX sits uncomfortably in the middle.

Competition from Mainland Exchanges: Shanghai and Shenzhen exchanges are improving rapidly. If Beijing decides to prioritize onshore listings over Hong Kong, HKEX loses its franchise.

Volume Cyclicality: The business model that creates extraordinary operating leverage in good times works in reverse during downturns. The 2022-2023 period showed how quickly profits can compress.

LME Legacy Issues: The nickel crisis damaged the LME's reputation and triggered ongoing legal battles. The acquisition that was supposed to cement HKEX as a global commodities player instead became a liability.

Technology Disruption: Tokenization, decentralized finance, and alternative trading venues could theoretically disintermediate traditional exchanges—though this risk is more theoretical than imminent.

XI. Key Metrics for Investors

For investors tracking HKEX's performance, three metrics matter above all others:

1. Average Daily Turnover (ADT)

ADT in the securities market is the single most important driver of HKEX's revenue and profits. The exchange reports monthly statistics, allowing real-time tracking. When ADT rises, trading fees, clearing fees, and data revenue all increase. In H1 2025, record ADT drove record profits.

What to watch: Month-over-month and year-over-year ADT trends. Southbound and Northbound Stock Connect flows. Correlation between ADT and Hang Seng Index volatility.

2. IPO Fundraising and Pipeline

While IPOs are less frequent than daily trading, they represent HKEX's long-term competitiveness. A healthy IPO pipeline suggests continued relevance as a listing venue. Declining applications would signal structural problems.

What to watch: The strong momentum is further reflected in the IPO pipeline, which now has 219 applicants, including a record breaking 210 Main Board applicants. Monthly IPO filing data. Mix between A+H listings, Chapter 18A biotech, and Chapter 18C tech companies.

3. Stock Connect Trading Value

Stock Connect flows indicate the health of HKEX's core "super-connector" franchise. Growing Northbound flows suggest international appetite for China. Growing Southbound flows suggest mainland confidence in Hong Kong.

What to watch: Daily Northbound and Southbound quota utilization. ETF Connect and Bond Connect volumes. Swap Connect growth as the newest program matures.

XII. Conclusion: The Irreplaceable Middleman

What is HKEX's enduring value proposition? Strip away the historical narrative, the executive biographies, and the complex governance structure, and one insight remains: HKEX has made itself irreplaceable.

For international investors wanting China exposure through a developed-market legal framework, Hong Kong remains the only option. For mainland Chinese companies wanting international capital and global visibility, Hong Kong offers what Shanghai and Shenzhen cannot: a credible, transparent, internationally recognized market.

This positioning is both HKEX's greatest strength and its greatest vulnerability. If China fully opens its capital account, the "super-connector" becomes less essential. If geopolitical tensions sever connections between East and West, Hong Kong's intermediary role collapses. If mainland exchanges achieve global credibility, HKEX loses its unique value.

Hong Kong Exchanges and Clearing Limited is a publicly-traded company and one of the world's leading global exchange groups, offering a range of equity, derivative, commodity, fixed income and other financial markets, products and services, including the London Metal Exchange. As a superconnector and gateway between East and West, HKEX facilitates the two-way flow of capital, ideas and dialogue between China and the rest of world, through its pioneering Connect schemes, increasingly diversified product ecosystem and its deep, liquid and international markets.

But for now, HKEX sits at a point of maximum leverage. China is not opening its capital account. Geopolitical tensions, paradoxically, make the "closed-loop" Connect structure more attractive, not less—Beijing retains control, while international investors gain access. Mainland exchanges remain largely domestic. The super-connector is more essential than ever.

The question isn't whether HKEX is a good business—it clearly is, with 80%+ margins and recurring revenue from irreplaceable infrastructure. The question is whether that business faces secular growth or secular decline. The answer likely depends on China's own trajectory: a confident, outward-looking China needs HKEX; an isolated, inward-looking China does not.

For investors willing to bet on continued—even if imperfect—integration between China and global markets, HKEX offers something rare: a monopoly on the bridge between the world's two largest economies.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube