SMIC: China's Semiconductor Gambit and the New Cold War of Chips

I. Introduction: A Story Written in Rice Fields

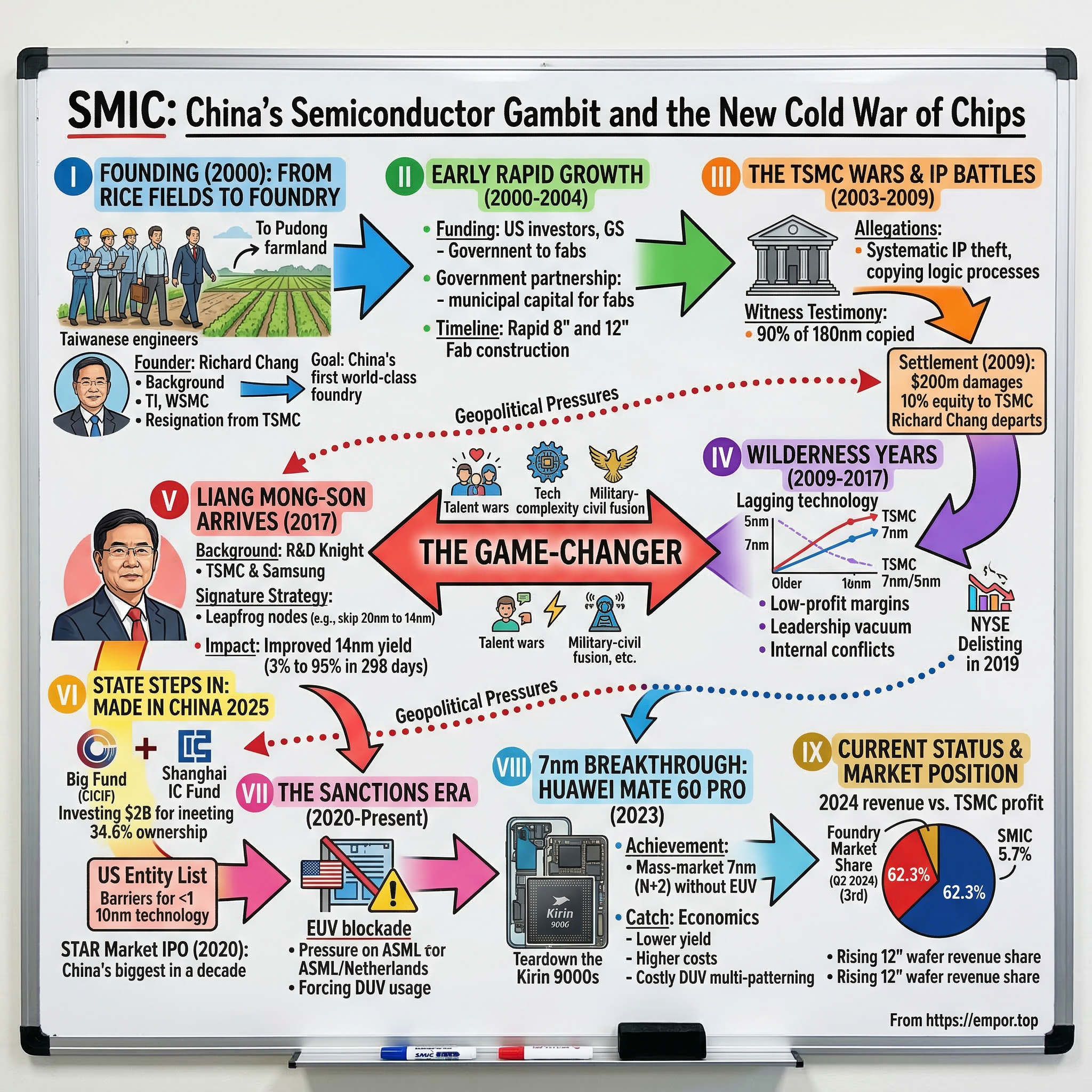

In the spring of 2000, a group of Taiwanese engineers stepped off planes in Shanghai's Pudong district. They carried with them suitcases, ambitions—and, allegedly, secrets worth billions. Their destination: a patch of rice paddies in Zhangjiang Hi-Tech Park, where they would attempt something that had eluded China for decades. These weren't ordinary engineers on an ordinary mission. They were about to build China's first world-class semiconductor foundry from nothing but farmland and sheer will.

The venture drew extraordinary attention given that its 73-year-old founder took a group of Taiwanese engineers across the Taiwan Strait 21 years ago to set up SMIC in the rice fields of Shanghai's suburbs.

Today, Semiconductor Manufacturing International Corporation (SMIC) stands as the centerpiece of the most consequential technology conflict of our time. As of 2024, it is the world's third largest contract chip maker. The company sits at the nexus of geopolitics, technology supremacy, and the multi-hundred-billion-dollar semiconductor industry that underpins everything from smartphones to weapons systems.

But how did we get here? How did a company founded in rice fields by a refugee's son become so strategically vital that it now appears on U.S. defense blacklists? How did it manage to produce 7nm chips despite being cut off from the world's most advanced manufacturing equipment?

Semiconductor Manufacturing International Corporation (SMIC) is a partially state-owned publicly listed Chinese pure-play semiconductor foundry company. It is the largest contract chip maker in mainland China. But that dry description barely scratches the surface of what makes SMIC one of the most fascinating—and consequential—business stories of the 21st century.

This is a story of talent wars, intellectual property theft accusations, crushing sanctions, and technological breakthroughs that shocked the world. It's a story that reveals the limits of export controls and the power of state-backed industrial policy. And at its center stand two remarkable figures—Richard Chang and Liang Mong-Song—whose personal ambitions, grievances, and genius reshaped entire industries.

Let's begin.

II. Context: The Oil of the 21st Century

Before understanding SMIC, one must understand why semiconductors matter so much—and why China found itself so desperately behind.

Semiconductors are the foundational technology of the modern world. They power our phones, our cars, our military systems, our medical devices. If oil was the strategic resource of the 20th century, chips are the oil of the 21st. Nations that control semiconductor manufacturing control the commanding heights of the digital economy. Those that don't face technological dependence with profound national security implications.

The challenge is that making advanced semiconductors is arguably the most complex manufacturing process ever devised. A modern chip factory represents a convergence of physics, chemistry, materials science, and precision engineering that pushes the boundaries of what's physically possible. The machines that make these chips cost hundreds of millions of dollars each, and only a handful of companies in the world can produce them.

Twenty years ago, the semiconductor industry in mainland China wasn't superior in the market and didn't have any international standards. This wasn't for lack of trying. China had made multiple attempts to build domestic chip manufacturing capability, but each had foundered on the rocks of technology complexity and talent scarcity.

The revolutionary business model that transformed semiconductor manufacturing emerged from Taiwan, not China. Taiwan Semiconductor Manufacturing Company (TSMC), founded by Morris Chang in 1987, pioneered the "pure-play foundry" concept: a company that manufactured chips designed by other companies but did no chip design of its own. This model separated chip design from chip fabrication, allowing fabless semiconductor companies to flourish. It was brilliant, and it gave Taiwan an outsized role in the global technology supply chain.

By the late 1990s, TSMC dominated global foundry production. Samsung in South Korea had significant manufacturing capability. The United States and Europe had Intel and a smattering of other manufacturers. But China—despite being the world's largest consumer of semiconductors—had essentially nothing. The world's manufacturing superpower couldn't make its own chips.

In 1996, leaders from a visiting delegation from the now-defunct Chinese Ministry of Electronics Industry approached Zhang in the United States and, noting China's twenty-year gap in semiconductor manufacture, encouraged Zhang to return to mainland China and help his birth nation establish their own chip fabrication industry.

That delegation had identified their man. Richard Chang, a Taiwanese-American engineer with two decades of experience building fabs around the world, might be the person who could finally close China's semiconductor gap. They just needed to convince him to come.

III. The Founder: Richard Chang's Remarkable Journey

Zhang Rujing (born 1948), alternatively known as Richard Chang Ru-gin, is a Taiwanese electrical engineer, businessman, and entrepreneur who founded Semiconductor Manufacturing International Corporation (SMIC), the largest contract chip manufacturer in mainland China. He is known as "the father of China's foundry industry" and China's "godfather of semiconductors".

To understand SMIC, you must understand Richard Chang. His life story reads like a historical novel spanning continents and ideological conflicts.

Zhang Rujing was born in 1948 in the city of Nanjing, Jiangsu Province to a steelworker and his wife. When he was less than a year old, Zhang and his family fled on a boat to Taiwan during the Great Retreat. They arrived in Kaohsiung on the southern coast of Taiwan in 1949.

This was the great exodus of 1949, when the Kuomintang government and millions of Chinese fled to Taiwan ahead of the advancing Communist forces. The infant Zhang and his family were among the refugees, their boat landing on Taiwan's southern coast as the Chinese Civil War concluded and the bamboo curtain fell between the mainland and the island.

Chang grew up in Taiwan, excelling academically. He graduated from National Taiwan University with a bachelor's degree in mechanical engineering in 1970, then completed graduate studies in the United States. He earned a master's from the University at Buffalo and a doctorate in electrical engineering from Southern Methodist University.

In 1977, at 29 years old, Zhang began working at the semi-conductor giant Texas Instruments alongside experts in integrated circuits with his first boss, Nobel Prize in Physics laureate Jack Kilby. Starting as a design engineer, Zhang would then develop under the mentorship of Shao Zifan, and help establish large-scale microchip factories including four in Texas, and others in Italy, Japan, Singapore, and Taiwan.

This is crucial context. Chang didn't just work at Texas Instruments—he became one of its most prolific fab builders, developing an almost unmatched expertise in the art and science of constructing semiconductor manufacturing facilities from the ground up. Chang worked for 20 years at Texas Instruments Inc, where he helped build chip plants in the US, Japan, Singapore, Italy and Taiwan.

By the late 1990s, Chang had left TI and was back in Taiwan, where he founded Worldwide Semiconductor Manufacturing Corp (WSMC) in 1997 as a foundry competitor to TSMC. But WSMC's independence was short-lived.

As TSMC expanded in Taiwan, its head, Zhang Zhongmou (Morris Chang), convinced TSMC shareholders in 2000 to acquire Shida Semiconductor for $5 billion USD. Zhang Zhongmou, reportedly appreciative of Zhang Rujing's talent and expertise, requested that Zhang Rujing continue to lead Shida Semiconductor, a deal Zhang Rujing accepted on the purported condition that a factory one day be built in mainland China. Learning that Zhang Zhongmou did not intend to establish a factory in mainland China, in 2000, Zhang Rujing resigned, gave up his shares of TSMC, and travelled to the PRC capital of Beijing.

This was the decisive break. Richard Chang forfeited his TSMC shares—worth a fortune—and headed to Beijing. The reason, by most accounts, was his belief that he could build something great in his birthplace. Some sources suggest religious motivations as well. He told people that he wasn't just thinking about making money, he wanted to: "Share God's love with the Chinese." Chang, a devout Christian, thought the communists of China needed some spiritual succour.

Whatever his motivations, Chang's arrival in Beijing in 2000 would reshape the global semiconductor industry.

IV. Founding & Early Years: Building in the Rice Fields (2000-2004)

When Richard Chang landed in Beijing in early 2000, he didn't find the reception he expected. Finding neither the city's mayor or vice mayor for science and technology who weren't in the city at that time, Zhang met with Deputy Directory of the Shanghai Economic Commission Jiang Shangzhou who brought Zhang south to Shanghai and introduced him to Zhangjiang Hi-Tech Park.

Shanghai, not Beijing, would become SMIC's home. SMIC was founded on April 3, 2000, and is headquartered in Shanghai.

The funding came together with remarkable speed. In 1999, Richard Chang raised $1.6bn from a group of US investors led by Goldman Sachs. He looked around for a suitable place to build another fab, and set up another foundry company, and was offered a good deal by the China government which had been trying, unsuccessfully, to spawn a semiconductor industry for a couple of decades.

The deal with China was simple but powerful: generous land grants, tax incentives, and government support in exchange for bringing world-class semiconductor manufacturing to the mainland. It was a template that would be repeated in the years ahead—state capital enabling private sector execution.

The Taiwanese government immediately swung into action, saying it was illegal for Chang to raise money in Taiwan, then spend it on a business in China. The Taiwanese government fined him NT$5m, and threatened Chang with confiscation of his assets in Taiwan if he went ahead with the plan to establish SMIC.

He founded SMIC in 2000 with funding and land from the Chinese government. His native Taiwan fined him NT$5 million (US$155,000) in 2005 for forming the company and ordered him to withdraw his investments from China.

Chang went ahead anyway. In 2000, however, Chang, went ahead. The fines and threats from Taiwan were a price he was willing to pay.

What followed was an expansion of staggering speed. It quickly built a fully owned plant in Shanghai, acquired a Motorola plant in Tianjin, and then began to build a fully owned plant in Beijing.

SMIC got to a rapid start, moving from equipment installation in August 2001 to qualified production in December 2001.

This timeline was unprecedented. In the semiconductor industry, it typically takes years to build and qualify a new fab. SMIC was producing chips within months. The speed raised eyebrows—and suspicions.

SMIC pioneered a novel government partnership model that would become a template for China's semiconductor industry. SMIC also became involved in two projects in Chengdu and Wuhan, which reversed a common pattern in Chinese development of government building, operating, then transferring industrial projects, such that SMIC operated the company, but the capital costs were borne by municipal government, relieving SMIC of the major cost of its fab plants.

This was ingenious. Municipal governments bore the massive capital costs of building fabs—often running into billions of dollars—while SMIC provided the expertise to operate them. It allowed SMIC to expand rapidly without the crushing debt that would typically accompany such growth.

Already experienced in the establishment of semiconductor factories, Zhang continued to expand SMIC by building three 8 inch wafer factories in Shanghai, two 12 inch factories in Beijing, and purchased an 8 inch factory in Tianjin from Motorola.

By 2003, SMIC was preparing for an IPO in Hong Kong. The company had gone from rice paddies to one of the world's largest foundries in just three years. The suits were filed amid SMIC's meteoric rise in the foundry business. The Chinese company came from no where to become the world's fourth largest pure-play foundry, behind only TSMC, UMC, and Chartered.

But TSMC wasn't about to let this stand without a fight.

V. The TSMC Wars: IP Theft Allegations & Legal Battle (2003-2009)

The lawsuits that TSMC brought against SMIC represent one of the most dramatic intellectual property battles in semiconductor history. They reveal uncomfortable truths about how technology transfers happen—and don't happen—in high-stakes industries.

The First Lawsuit (2003-2005)

In August 2003, as SMIC planned to launch an IPO in Hong Kong, TSMC sued SMIC in the United States courts for intellectual property theft and patent infringement.

The timing was strategic. SMIC was about to go public, and a lawsuit alleging systematic IP theft would cast a shadow over the offering. TSMC originally filed suit in December 2003, about three months before SMIC's initial public offering.

SMIC's progress was unusually fast given the complexities of foundry construction; SMIC had hired more than 100 employees from TSMC that had access to sensitive process information. TSMC consequently filed suit in December 2003 in California claiming IP theft against SMIC.

The evidence presented was damning. December 2003, TSMC filed suit alleging systematic intellectual-property (IP) theft and patent infringement by SMIC. Witness testimony indicated: An estimated 90% of SMIC's 180nm logic process was copied from TSMC.

The lawsuit alleged that SMIC had systematically recruited TSMC engineers and asked them to bring proprietary information with them. In 2003, TSMC filed a suit against SMIC over foundry patents and misappropriation of trade secrets. The original complaint stated that SMIC hired over 100 TSMC employees and asked some of them to provide SMIC with TSMC's trade secrets.

Not surprisingly, SMIC agreed to settle the case in February of 2005. Under terms of the settlement, SMIC is to pay TSMC $175 million over 6 years and the companies have agreed to cross license 180nm patent portfolios.

In 2005, SMIC was ordered to pay US$175 million to TSMC in damages, surrender TSMC documents, and halt the use of TSMC technology and processes in SMIC's fabrication.

The settlement seemed to close the matter. But TSMC didn't yet know the full extent of what had been taken.

The Second Lawsuit (2006-2009)

But at the time of the first settlement in 2005, TSMC did not know that SMIC actually had 15,000 TSMC documents, amounting to 500,000 pages of information. "Quite honestly, if we had known back in 2005 they had our stuff on 0.13 (micron), 90 nanometer, then, yeah, the dollar amount would have gone up in the original settlement."

After reviewing documents provided as part of the 2005 settlement, TSMC discovered the alleged theft went far deeper than originally understood. After poring over documents SMIC provided as part of the settlement agreement, the Taiwanese foundry also claims to have discovered that SMIC's alleged theft was greater than originally assumed and that the alleged illegal activity was the enabling factor behind the Chinese foundry's rapid ramp between 2001 and 2003. "SMIC achieved its lightning-fast ramp-up, at such little cost, by stealing and misusing TSMC's confidential semiconductor processing technology and related information, from soup to nuts," the suit states.

TSMC filed a second lawsuit in 2006. In 2009, a California jury ruled that SMIC had indeed breached the agreement and stolen trade secrets. This would put SMIC on the hook for a billion dollars in damages.

The verdict was devastating for SMIC. Along with a compensation of $200 million USD and 10% equity given by SMIC to TSMC in 2009, Zhang, then 61, was prohibited from operating in the chip industry for a period of three years.

Chang stepped down as CEO of SMIC in November 2009, three days after the company settled a years-long lawsuit with Taiwan Semiconductor Manufacturing Company.

The SMIC IPO in 2004, conducted amid the lawsuits, had not fared well. The Shanghai-based chipmaker's shares have declined 86 percent since the company sold stock at HK$2.72 in an initial public offering in March 2004.

What the Lawsuits Revealed

The TSMC-SMIC litigation revealed a pattern that would repeat across China's semiconductor ambitions: the difficulty of building advanced manufacturing capability from scratch, and the temptation to shortcut that process through technology transfer—whether authorized or not.

SMIC account managers told their prospective foundry customers that SMIC's fabrication processes were "TSMC compatible" and "just like TSMC's". One boasted that the two technologies were so similar that little design work would be needed on the customer's part so to make the switch.

For TSMC, the victory secured its intellectual property but also eliminated a potentially existential threat. On the contrary, TSMC was careful not to cause SMIC to bleed to death from compensation payments, because once SMIC went bankrupt and its fabs were sold off, TSMC's process technology would also be leaked to the competition. TSMC was anxious to prevent a worst-case scenario: whichever company took over a cash-strapped SMIC would fight a price war and destroy the market order.

Richard Chang's departure marked the end of SMIC's founding era. But the company—and China's semiconductor ambitions—would not die with his departure.

VI. The Wilderness Years: Post-Chang Struggles (2009-2017)

The departure of Richard Chang left SMIC in a leadership vacuum at a critical moment. The company was technologically wounded, financially strained, and reputationally damaged. What followed was nearly a decade of struggle.

SMIC trails bigger rivals including TSMC in technology for making more advanced products, which have higher profit margins.

The technology gap that had already existed widened into a chasm. While TSMC raced ahead toward ever-smaller process nodes—14nm, 10nm, 7nm—SMIC found itself stuck on older technologies. By 2017, SMIC lags behind TSMC at about two generations of process nodes. While TSMC's 7nm node techniques are commonly used in chips and 5nm will be mass-produced this year, SMIC just realized 14nm processing.

The company cycled through leadership. Internal conflicts plagued the organization. The co-CEO structure that emerged—with different executives overseeing different aspects of the business—reflected these divisions.

The profitability challenge was real. SMIC's technology trailed competitors, which meant it competed primarily on price in lower-margin product segments. Without access to the most advanced manufacturing processes, SMIC couldn't attract the highest-value customers.

On May 24, 2019, SMIC announced it would voluntarily delist from the New York Stock Exchange (NYSE), citing low trade volumes. Along with low US trading volumes, the company named the high administrative cost of maintaining the NYSE listing.

The NYSE delisting in 2019 marked the end of SMIC's American chapter. It was a precursor of the more dramatic breaks with the U.S. that would follow.

But something was changing beneath the surface. Richard Chang's three-year ban from the semiconductor industry had expired, and he returned to found new ventures. In 2014, having passed his three-year prohibition from the semiconductor industry, a 66-year-old Zhang founded Shanghai Xinsheng, the first 300 mm large silicon wafer company in mainland China.

More importantly, China's government was becoming increasingly serious about semiconductor self-sufficiency. The Made in China 2025 plan explicitly identified semiconductors as a strategic priority. State money began flowing into the industry at unprecedented scale.

And then, in 2017, a pivotal hire changed everything.

VII. The Game-Changer: Liang Mong-Song Arrives (2017)

Liang Mong Song is a Taiwanese electronic engineer. He is the co-chief executive officer of the Semiconductor Manufacturing International Corporation. He was previously an engineer at TSMC and Samsung Electronics. He is known as one of the "Six Knights of TSMC R&D".

If Richard Chang was SMIC's Moses—leading the company out of nothing into existence—Liang Mong-Song would be its Joshua, the warrior who would lead it into advanced territory against seemingly impossible odds.

After returning to Taiwan in 1992, Liang served as an engineer and senior R&D director of TSMC. He is credited with nearly 500 TSMC patents and was responsible for or participated in the most advanced development of each generation of TSMC's manufacturing processes.

Liang's credentials were extraordinary. 500 patents. Leadership of TSMC's most advanced process development. Recognition as one of the company's most brilliant technical minds. But like many brilliant technical people, Liang had ambitions that exceeded his opportunities within the organization.

In 2005, when Morris Chang named Rick Tsai to succeed him as CEO, Liang expected to be promoted to R&D Vice President. However he was passed over, leaving Liang furious.

In February 2009, Liang Mong Song left TSMC and joined National Tsing Hua University as a professor in the Department of Electrical Engineering and Institute of Electronics.

The Samsung Interlude

Under the conditions that Samsung Electronics offered Liang three years' salary equivalent to his ten years of service at TSMC, Liang agreed to join Samsung and at the same time took away more than 20 employees, including those from his old TSMC engineering department. To comply with the period stipulated in the non-compete clause, Liang began to work as a visiting professor at Sungkyunkwan University under Samsung in October 2010.

On 13 July 2011, Liang officially joined Samsung as the chief technology officer of Samsung's LSI department and was also the executive vice president of Samsung's wafer foundry. At that time, Samsung was at the R&D bottleneck of switching from the 28 nm process to the 20-nanometer process. Liang advocated that Samsung abandon the 20 nm process and directly upgrade from the 28 nm process to the 14 nm process.

This was Liang's signature move—the leap-frog strategy. Rather than incrementally advancing through each process node, he advocated skipping intermediate steps and jumping directly to more advanced technologies. It was risky, but it worked.

In the end, Samsung's 14 nm process was mass-produced about half a year earlier than TSMC. After Liang assisted Samsung in successfully developing the 14 nm process, Samsung won the first batch of orders for the Apple A9 and Qualcomm's order, which were originally exclusive to TSMC in the Apple processor-related market. This caused TSMC's stock price to fall for a time, losing 80% of Apple's orders and losing US$1 billion.

Liang had helped Samsung beat TSMC to the punch on 14nm, costing his former employer a billion dollars in lost business. The Taiwanese press was furious. Former TSMC R&D executive Liang Mong-song, dubbed the biggest traitor in Taiwan's semiconductor industry for leaking trade secrets to South Korean rival Samsung, has jumped ship again.

TSMC sued, and eventually won. TSMC's lawsuit against Mong-Song Liang for infringing business secrets was lost in the first instance but won in the second instance. In the end, the Supreme Court ruled that Mong-Song Liang could not continue to provide services to Samsung in any way.

Joining SMIC

When his Samsung contract ended, Liang had another destination in mind. In 2017 he was hired at Semiconductor Manufacturing International Corporation Co-CEO. After he joined, SMIC improved the yield of its mass production and shrank the size of its chips.

On October 16, SMIC announced in a press release that Liang had been appointed Co-CEO, alongside incumbent CEO Zhao Haijun, to take charge of process technology development.

The co-CEO arrangement was unusual but reflected SMIC's complex internal politics. Liang would focus on advanced process development—the bleeding edge—while Zhao Haijun handled the profitable trailing-edge business that generated SMIC's actual cash flows.

Mong-Song Liang significantly improved the 14nm process yield rate from 3% to more than 95% within 298 days, making SMIC the sixth largest manufacturer in the world after TSMC, UMC, Samsung, Global Foundry and Intel.

The impact was immediate and dramatic. SMIC, which also had difficulties with 28nm, solved the problem after Liang Mengsong joined and succeeded in mass-producing 14nm chips by skipping 20nm.

Once again, Liang employed his leapfrog strategy—jumping over the 20nm node that had given Samsung so much trouble and going directly to 14nm. The pattern that had worked at Samsung was now working at SMIC.

Liang Mong Song is responsible for pushing China to 7nm (close to the leading edge).

VIII. The State Steps In: Made in China 2025 & Massive Investment (2019-2020)

While Liang Mong-Song was transforming SMIC's technical capabilities, the Chinese government was transforming its financial foundation. The Made in China 2025 plan identified semiconductors as a critical industry for national self-sufficiency, and state money began flowing in unprecedented quantities.

In May 2020, in support of the country's Made in China 2025 program; the China Integrated Circuit Industry Investment Fund and the Shanghai Integrated Circuit Industry Investment Fund invested a combined US$2 billion, gaining, respectively, 23.08% and 11.54% ownership of SMIC.

This $2 billion injection was transformative, but it was just the beginning.

In July 2020 SMIC issued 1,685,620,000 shares at 27.46 yuan per share on the STAR Market of the Shanghai Stock Exchange, raising 46.28 billion yuan ($6.62 billion).

If the overallotment option was fully exercised, the total fund raised would amount to RMB 53.23 billion, setting a new record of fund raising in the STAR Market. This is the biggest A-share IPO by a semiconductor enterprise in terms of the financing scale in history, and the biggest A-share IPO in the past decade.

Semiconductor Manufacturing International Corp (SMIC) made its trading debut on Shanghai's Nasdaq-style STAR Market on Thursday, opening at 95 yuan (about 13.6 U.S. dollars), 246 percent higher than its offered price of 27.46 yuan. The chipmaker plans to inaugurate 1.9 billion shares at 27.46 yuan each, raising as much as 53.2 billion yuan, becoming China's biggest IPO in a decade.

The regulatory process was extraordinarily fast. After its IPO application was accepted, it took SMIC only 19 days to obtain CSRC approval and 29 days to obtain the registration approval, the fastest IPO review and approval in the STAR Market history.

The state's involvement went beyond just funding. State-owned civilian and military telecommunications equipment provider Datang Telecom Group as well as the China Integrated Circuit Industry Investment Fund are major shareholders of SMIC.

SMIC's largest shareholders are tied to the Chinese State, party, and military bureaucracies. SMIC also partners with and supplies PRC entities tied to the military, military-civil fusion, and government ecosystems.

This is the complex reality of SMIC: it is simultaneously a publicly traded company pursuing commercial objectives and a strategic national asset pursuing the Chinese government's industrial policy goals. These two identities are not always in harmony.

The structure of SMIC's ownership reflects the China Integrated Circuit Industry Investment Fund's approach. The China Integrated Circuit Industry Investment Fund, also known as the National Integrated Circuit Industry Investment Fund and the Big Fund, is a China Government Guidance Fund. The fund aims to help China reach its national goal of achieving self-sufficiency in the semiconductor industry by investing in domestic semiconductor companies. It has played a significant role with regards to the semiconductor industry in China by funding companies such as SMIC, Hua Hong Semiconductor, and YMTC.

Armed with billions in new capital, SMIC was positioned to make a major push toward advanced manufacturing capability. But American policymakers had other plans.

IX. The Sanctions Era: US Export Controls (2020-Present)

The Trump administration's December 2020 action against SMIC represented a dramatic escalation in the technology conflict between the United States and China.

The Bureau of Industry and Security (BIS) in the Department of Commerce (Commerce) added Semiconductor Manufacturing International Corporation (SMIC) of China to the Entity List. BIS is taking this action to protect U.S. national security. This action stems from China's military-civil fusion (MCF) doctrine and evidence of activities between SMIC and entities of concern in the Chinese military industrial complex.

The Entity List designation limits SMIC's ability to acquire certain U.S. technology by requiring U.S. exporters to apply for a license to sell to the company. Items uniquely required to produce semiconductors at advanced technology nodes—10 nanometers or below—will be subject to a presumption of denial.

The sanctions were severe but not absolute. SMIC could still acquire equipment for producing older-generation chips. But the path to advanced manufacturing—10nm and below—was now effectively blocked.

In December 2020, the United States Department of Defense named SMIC as a company owned and controlled by the People's Liberation Army, and prohibited any American company or individual from investing in SMIC.

The EUV Blockade

The most critical chokepoint was extreme ultraviolet (EUV) lithography equipment. Only one company in the world—ASML of the Netherlands—can produce these machines, which are essential for manufacturing the most advanced chips.

SMIC ordered an EUV step-and-scan system from ASML Holding for $120 million in 2018. The order was blocked after the US government pressured the Netherlands and ASML.

The current phase of escalated controls on China began in 2018, when the US started encouraging the Netherlands to restrict sales of the most advanced extreme ultraviolet (EUV) lithography tools to China's leading chipmaker, the partially state-owned Semiconductor Manufacturing International Corporation (SMIC). EUVs are produced by a single company — the Netherlands' ASML — and cost over $100 million each. Only a handful of companies have acquired these tools. Barring US pressure and the Dutch decision to block the sale, China would have acquired its first tool in 2019.

For several years, ASML has been barred from exporting this machine to China. To date, it has not yet shipped a single EUV machine to China.

Without EUV, conventional wisdom held that SMIC could not produce chips at the 7nm node or below. EUV uses extremely short wavelengths of light to pattern the tiny features on advanced chips. The alternative—deep ultraviolet (DUV) lithography—uses longer wavelengths and, in theory, cannot achieve the same level of precision.

SMIC's Response

In response to US sanctions on the Chinese chip industry in the early 2020s, SMIC started on a wave of expansion in the form of joint ventures with China's state semiconductor fund.

Rather than retreat, SMIC accelerated its expansion. New fabs were announced across China. Investment continued to flow in. And behind closed doors, Liang Mong-Song's engineers were working on something that would shock the semiconductor world.

X. The 7nm Breakthrough: Huawei Mate 60 Pro (2023)

On August 29, 2023, Huawei quietly released a new smartphone, the Mate 60 Pro. Within days, semiconductor analysts around the world were tearing one apart—and what they found inside stunned the industry.

The team found evidence of SMIC 7nm (N+2) which represents a made-in-China design and manufacturing milestone for the most advanced Chinese foundry TechInsights has documented. Some of the highlights include: The Kirin 9000s die measured 107 mm2, which is 2% larger than the Kirin 9000 (105 mm2).

HiSilicon Kirin 9000s (Hi36A0) powers the Huawei Mate 60 Pro, manufactured in SMIC's 7nm N+2 technology (its second-generation 7nm process). This is the first commercial use TechInsights has identified of the most advanced logic process node without extreme ultraviolet (EUV), manufactured by a Chinese foundry, that supports full system-on-chip (SoC) functional elements like bit cells (embedded SRAM).

"Discovering a Kirin chip using SMIC's 7nm (N+2) foundry process in the new Huawei Mate 60 Pro smartphone demonstrates the technical progress China's semiconductor industry has been able to make without EUV lithography tools," said Dan Hutcheson, Vice Chair of TechInsights. "The difficulty of this achievement also shows the resilience of the country's chip technological ability. At the same time, it is a great geopolitical challenge to the countries who have sought to restrict its access to critical manufacturing technologies."

This was supposed to be impossible. Without EUV, conventional wisdom held that mass production of 7nm chips couldn't be done economically. Yet here was a 7nm chip, in a mass-market smartphone, manufactured by a company cut off from the world's most advanced equipment.

How They Did It

Using 193nm argon-fluoride lasers, immersion DUV systems comfortably support 28nm nodes, with yields and costs increasing dramatically as nodes shrink further. With multi-patterning (exposing the same wafer multiple times with different masks) they can be stretched down to 7nm-class geometries.

EUV equipment only requires 9 steps to perform 7nm process, but DUV equipment requires 34 steps.

The engineering challenge was immense. What EUV accomplishes in a single exposure, DUV requires multiple passes. Each additional pass introduces more opportunities for errors, more time, and more cost.

Chip engineers said it's technically possible to use immersion deep-ultraviolet (DUV) lithography to produce 5nm chips but the cost can be several times higher than those made with extreme-ultraviolet (EUV) lithography.

They said SMIC may be able to make 7nm and 5nm chips with yields of 50% and 30-40%, respectively.

The Yield Challenge and Cost Premium

It said SMIC is pricing its 5nm and 7nm products at a 40-50% premium over what TSMC charges for similar technology nodes. Citing some experts, the FT said the yield of SMIC's 7nm chips is less than one-third that of TSMC's similar products.

The economics are stark. SMIC's 7nm chips cost significantly more to produce than TSMC's, and yield rates—the percentage of good chips per wafer—are reportedly much lower. For a normal commercial enterprise, this would be economically unsustainable.

But SMIC isn't a normal commercial enterprise. Commentators said Huawei and SMIC are determined to push forward with this costly project as Beijing wants to show the world that Chinese companies can achieve technological breakthroughs despite the US chip export ban. They said it is more likely a political project than a commercially feasible one.

"Could this be just a demonstration by Huawei and SMIC to show the Chinese government it can be done?" said Douglas Fuller, an expert on China's semiconductor industry asked rhetorically in a conversation with Financial Times. "If money is no object, then it might happen."

Path to 5nm and Beyond

According to Wccftech, industry sources suggest that SMIC is on track to finalize its 5nm chip development by 2025. For instance, SMIC's 5nm wafers will reportedly be up to 50 percent more expensive than TSMC's on the same manufacturing process, with the yields said to reach a measly 33 percent.

Wccftech reported that SMIC will complete the development of its 5nm process technology in 2025, but because it can only rely on deep ultraviolet (DUV) equipment, the current yield is estimated to be 33%, only 1/3 of TSMC's, yield on the same technology. The US magazine Tom's Hardware has pointed out that SMIC and Huawei have applied for patents for 3nm process using DUV and multiple patterning.

The 7nm breakthrough, while remarkable, comes with important caveats. SMIC cannot produce these chips in the volumes or at the costs that TSMC can. But it proved that with sufficient engineering talent and willingness to absorb losses, the EUV chokepoint could be partially circumvented.

XI. Current Financials & Market Position

According to the unaudited financial results, the Company's revenue in 2024 increased by 27% year-over-year to $8.03 billion, and gross margin was 18%. The Company's capital expenditure in 2024 was $7.33 billion.

The full year revenue increased by 27% year-over-year to $8.03 billion, hit a record high. Gross margin was 18%, and capacity utilization rate was 85.6%.

The revenue growth is impressive—27% year-over-year in a difficult semiconductor environment. But profitability tells a more complex story.

Net profit attributable to shareholders fell 23.3% to CNY3.7 billion, with earnings per share at CNY0.46.

In its annual report filed to the Hong Kong stock exchange, the company said full-year revenue grew 27 per cent to US$8 billion but net profit plunged 45.4 per cent to US$493 million. In comparison, the world's top foundry, Taiwan Semiconductor Manufacturing Co (TSMC), said earlier that its net profit for 2024 surged nearly 40 per cent from a year earlier to hit an all-time high of US$35 billion, or over 70 times that of SMIC.

The gap with TSMC is enormous. TSMC's profit in 2024 exceeded SMIC's revenue by a factor of four. TSMC's profit was 70 times SMIC's profit. This reflects the fundamental economics of the foundry business: leading-edge chips command premium prices and higher margins.

Capacity and Production

Monthly capacity was 948 thousand standard logic 8-inch equivalent wafers by the end of the year.

Wafer shipments hit a record 8.02 million 8-inch-equivalent units in 2024, up 36.7% from the previous year.

Market Segmentation

Consumer electronics became SMIC's largest end-market in 2024, accounting for 37.8% of total revenue, up 12.8 percentage points year-over-year. Smartphones contributed 27.8%, while revenue from computers and tablets dropped to 16.6%. Wearables and IoT made up 10%, and industrial and automotive segments comprised 7.8%.

Global Market Position

SMIC held a 6% market share in terms of global foundry revenue in the first quarter, up from 5% last year, overtaking GlobalFoundries and Taiwan's United Microelectronics Corporation. This places SMIC only behind Taiwan's TSMC and South Korea's Samsung Foundry.

This places SMIC behind only Taiwan Semiconductor Manufacturing Company and South Korea's Samsung Foundry which held 62% and 13% of market share in the first quarter respectively.

In the second quarter of 2024, TSMC remained in first place in the foundry rankings with a dominate 62.3% market share, followed in order by Samsung (11.5% share), SMIC (5.7%), UMC (5.3%), GlobalFoundries (4.9%), HuaHong Group (2.1%), and Tower (1.1%).

Dividend Policy

SMIC said it does not plan to issue a dividend for the fiscal year 2024, subject to approval at its 2025 annual shareholder meeting. Since its STAR Market listing in July 2020, the company has not initiated any dividend payouts.

This reflects SMIC's position as a capital-intensive growth company that needs to reinvest earnings into expansion and R&D rather than return capital to shareholders.

XII. Playbook: Business & Strategic Lessons

The SMIC story offers profound lessons for understanding technology competition, state capitalism, and the limits of export controls.

The Talent Game

Two individuals—Richard Chang and Liang Mong-Song—fundamentally shaped SMIC's trajectory. Chang brought the vision, connections, and experience to build a foundry from scratch. Liang brought the technical brilliance to push it toward the leading edge.

Both came from TSMC. Both left under circumstances involving conflict. Both brought teams of engineers with them. The semiconductor industry's most valuable assets walk out the door every evening—and sometimes they don't come back.

But TSMC's patent suit raised some questions about SMIC's sudden rise in the foundry business. Questions about intellectual-property (IP) became a central theme at SMIC as well for China as a whole, according to analysts.

The talent game cuts both ways. The skills that built TSMC into a semiconductor superpower could be—and were—transferred to competitors. This reality underpins both the lawsuits and the export controls. Technology, in the end, lives in people's heads.

State Capitalism: The SMIC Model

SMIC also became involved in two projects in Chengdu and Wuhan, which reversed a common pattern in Chinese development of government building, operating, then transferring industrial projects, such that SMIC operated the company, but the capital costs were borne by municipal government, relieving SMIC of the major cost of its fab plants.

This model—public capital, private execution—enabled SMIC to expand far faster than its balance sheet would have allowed. Municipal governments bore the billions in capex required for new fabs, while SMIC provided operational expertise.

The approach reflects China's broader industrial policy: using state resources to nurture strategic industries until they can stand on their own. Whether this creates sustainable competitive advantage or merely delays an inevitable reckoning with market realities remains to be seen.

The IP Paradox

SMIC's foundation was built on allegedly stolen intellectual property. The lawsuits, the settlements, the forced departure of Richard Chang—all attest to this uncomfortable reality.

And yet, SMIC survives and thrives. The IP theft accusations, while resulting in hundreds of millions in settlements, did not destroy the company. Instead, they might be viewed as the cost of technology transfer—a cost that China, apparently, was willing to bear.

This creates a profound strategic question: If IP theft enables technology catch-up, and the penalties for theft are merely financial, does IP protection actually protect against determined state-backed actors?

Sanctions as Accelerant

The US export controls were designed to slow or halt China's semiconductor advancement. In the short term, they clearly constrained SMIC's access to cutting-edge equipment.

But they also had unintended consequences. ASML's chief executive has said China is ten to fifteen years behind. That may be true in technology, but sanctions are accelerating the drive to close the gap.

The sanctions forced Chinese chipmakers to develop alternatives. They accelerated domestic equipment development. They created political will for semiconductor self-sufficiency that might otherwise have remained diffuse. Each ban entrenches the incentive to localize, and each domestic stepper tested at SMIC or Huawei's labs makes the next round of controls less decisive.

Yield vs. Capability

There is a crucial distinction between being able to produce something and being able to produce it profitably at scale. SMIC has demonstrated the capability to produce 7nm chips. What it has not demonstrated is the ability to do so at competitive costs and yields.

SMIC might be able to produce 7-nm with its existing technology, but without the use of EUV lithography, the chips will be more costly to make, and their quality will be questionable. With the continued ban of EUV exports, SMIC is unlikely to be able to reach mass production and expand the global market share of high-tech chips in the foreseeable future.

For strategic applications—military, AI, national champions like Huawei—cost may be secondary to capability. But for commercial viability, yield and cost matter enormously.

XIII. Competitive Analysis: Porter's Five Forces and Helmer's 7 Powers

Porter's Five Forces

Threat of New Entrants: LOW The barriers to entry in semiconductor foundry are astronomical. A leading-edge fab costs $20+ billion to build. The technology is extraordinarily complex. Access to key equipment is limited. SMIC itself took decades to reach even third place globally.

Bargaining Power of Suppliers: VERY HIGH ASML's monopoly on EUV lithography gives it extraordinary power. Equipment suppliers more broadly hold significant leverage. This is SMIC's greatest vulnerability—its access to advanced equipment is controlled by entities subject to US pressure.

Bargaining Power of Buyers: MODERATE Large customers like Huawei and Qualcomm have some leverage, but in a capacity-constrained environment, foundries hold power. SMIC's relationship with Huawei is particularly symbiotic—both need each other.

Threat of Substitutes: LOW There is no substitute for semiconductor manufacturing. Chips underpin all digital technology. The foundry model itself faces no substitution threat.

Competitive Rivalry: HIGH Competition with TSMC, Samsung, and others is intense. SMIC competes on price in trailing-edge nodes but cannot compete on technology at the leading edge. The China market provides some insulation, as domestic sourcing becomes mandatory for strategic applications.

Hamilton Helmer's 7 Powers

Scale Economies: PRESENT but LIMITED SMIC benefits from scale, but TSMC's scale advantages are far greater. TSMC's volume enables lower per-unit costs and more R&D spending.

Network Effects: MINIMAL The foundry business has limited network effects. Customers choose based on technology, capacity, and price, not network size.

Counter-Positioning: PRESENT SMIC's state backing allows it to operate in ways that TSMC or Samsung cannot or will not. It can absorb losses in pursuit of strategic goals. This is a form of counter-positioning enabled by its state ownership structure.

Switching Costs: MODERATE Customers invest in design integration with specific foundry processes. Switching is costly but not prohibitive, especially for less advanced nodes.

Branding: LIMITED In a B2B industry, branding matters less than technological capability. TSMC's reputation for reliability is a brand asset, but it's earned through performance.

Cornered Resource: PRESENT SMIC has cornered the resource of being the only capable foundry in China. For Chinese companies that need domestic sourcing—whether by choice or by regulatory mandate—SMIC is often the only option.

Process Power: DEVELOPING SMIC is developing process expertise, particularly in extending DUV to advanced nodes. Whether this constitutes true process power comparable to TSMC's remains to be seen.

XIV. Bull and Bear Case

Bull Case

-

Captive Market: China consumes nearly 50% of global semiconductors. SMIC has an effective monopoly on domestic leading-edge manufacturing. As US-China decoupling accelerates, Chinese customers have no alternative.

-

State Support: The Chinese government has demonstrated willingness to invest whatever is required in semiconductor self-sufficiency. SMIC is the primary vehicle for that investment.

-

Technical Progress: The 7nm breakthrough proves that sanctions are not absolute barriers. With continued R&D investment and engineering talent, further advances are possible.

-

Legacy Chip Opportunity: The world needs enormous quantities of chips at older nodes—for automobiles, industrial applications, IoT. SMIC can compete effectively in these markets without EUV.

-

Valuation: If SMIC can close even a portion of the technology gap with TSMC, current valuations may prove modest.

Bear Case

-

Technology Ceiling: Without EUV, there may be a hard limit to how advanced SMIC can go. The 7nm achievement was remarkable, but economically unviable at scale. The 5nm and 3nm nodes may prove insurmountable.

-

Yield and Cost Disadvantages: Even where SMIC can produce advanced chips, it does so at far higher costs and lower yields than TSMC. This makes commercial competitiveness doubtful outside captive markets.

-

Equipment Dependency: SMIC remains dependent on existing stocks of foreign equipment. Without access to spare parts, maintenance, and software updates, equipment degradation is a real risk.

-

Sanctions Escalation: Further US restrictions could target even more of SMIC's supply chain. Dutch restrictions on DUV equipment have already begun.

-

Geopolitical Risk: Any conflict over Taiwan would have profound implications for SMIC and the entire semiconductor industry. SMIC's connections to Chinese military entities create reputational and investment risks.

XV. Key Performance Indicators

For investors tracking SMIC's progress, three KPIs stand out as most critical:

1. Gross Margin

SMIC's gross margin (18% in 2024) reflects its competitive position. Higher margins would indicate success in moving to more advanced, higher-value nodes or achieving cost efficiencies. Declining margins would suggest pricing pressure or rising production costs. Compare to TSMC's gross margin of ~55% to understand the gap.

2. Revenue from 12-inch Wafers / Advanced Nodes

Revenue from 8-inch wafers declined to 22.7% in 2024, down from 26.3% the prior year, while 12-inch wafers increased their share to 77.3%, up from 73.7%.

The shift from 8-inch to 12-inch wafers indicates technological advancement. Within 12-inch, the proportion of revenue from FinFET (14nm and below) versus older nodes reveals SMIC's progress up the technology ladder.

3. Capacity Utilization Rate

At 85.6% in 2024, SMIC's utilization is healthy but not exceptional. Utilization below 80% would indicate demand weakness. Consistently high utilization (90%+) would suggest pricing power and capacity constraints that could justify expansion.

XVI. Regulatory and Legal Overhangs

Entity List Status: SMIC remains on the US Entity List, requiring licenses for US technology exports. Items for advanced nodes face presumption of denial. This creates ongoing uncertainty around equipment access.

Chinese Military Company Designation: The US Department of Defense designation as a Chinese military company prohibits US investment and creates reputational issues.

Equipment Maintenance: As existing foreign equipment ages, questions arise about access to spare parts and service. Some maintenance may require workarounds or domestic alternatives.

TSMC Stake: TSMC's 10% stake in SMIC (acquired as part of the 2009 settlement) creates an unusual situation where a competitor holds a significant ownership position. The relationship between these stakes and current competition is unclear.

XVII. Conclusion: What This Means for the Semiconductor World Order

SMIC represents both the ambitions and limitations of China's semiconductor strategy. It demonstrates that determined state backing, combined with world-class engineering talent, can achieve remarkable technological breakthroughs. The 7nm chip in the Huawei Mate 60 Pro proved that export controls are not absolute barriers.

But SMIC also reveals the limitations. Even with billions in state investment, cutting-edge manufacturing equipment remains out of reach. Yield rates and costs lag far behind industry leaders. The gap with TSMC, measured in profits, is staggering—and may be widening even as SMIC's technology advances.

The semiconductor industry finds itself at an inflection point. The US strategy of denying China access to advanced equipment has clearly slowed Chinese progress. But it has also galvanized China's determination to achieve self-sufficiency and may ultimately create a more formidable competitor.

For the global semiconductor industry, SMIC's trajectory has profound implications:

- Equipment makers like ASML face the loss of a major potential market and the risk of Chinese domestic alternatives eventually emerging

- TSMC and Samsung face a competitor that doesn't play by normal commercial rules—one backed by a nation-state willing to subsidize losses indefinitely

- Chip designers must navigate an increasingly bifurcated world, where geopolitics determines which foundries they can use

- National security planners must reckon with a world where critical technology production is increasingly concentrated and contested

Richard Chang's vision—born of refugee experience and technical brilliance—has created something that transcends its origins. SMIC is no longer just a company. It is an instrument of national strategy, a symbol of technological ambition, and a test case for whether great power competition can be conducted through economic means rather than military ones.

The rice fields of Zhangjiang are long gone, replaced by gleaming fabs producing chips that power everything from smartphones to AI systems. What happens within those fabs, and what limits are placed upon them, will shape the technological future of the 21st century.

The central question remains unanswered: Can a company operating under crushing sanctions, dependent on older equipment, and facing a technology gap of multiple generations, ever truly catch the industry leaders? Or will SMIC remain what it is today—formidable enough to matter, but forever relegated to second-tier status?

The next decade will tell. The stakes—for SMIC, for China, and for the global technology order—could not be higher.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube