Takeda Pharmaceutical: From Edo-Era Medicine Shop to Global Biopharma Giant

How did a 244-year-old medicine shop founded in feudal Japan pull off the largest foreign acquisition ever by a Japanese company?

I. Introduction & Episode Roadmap

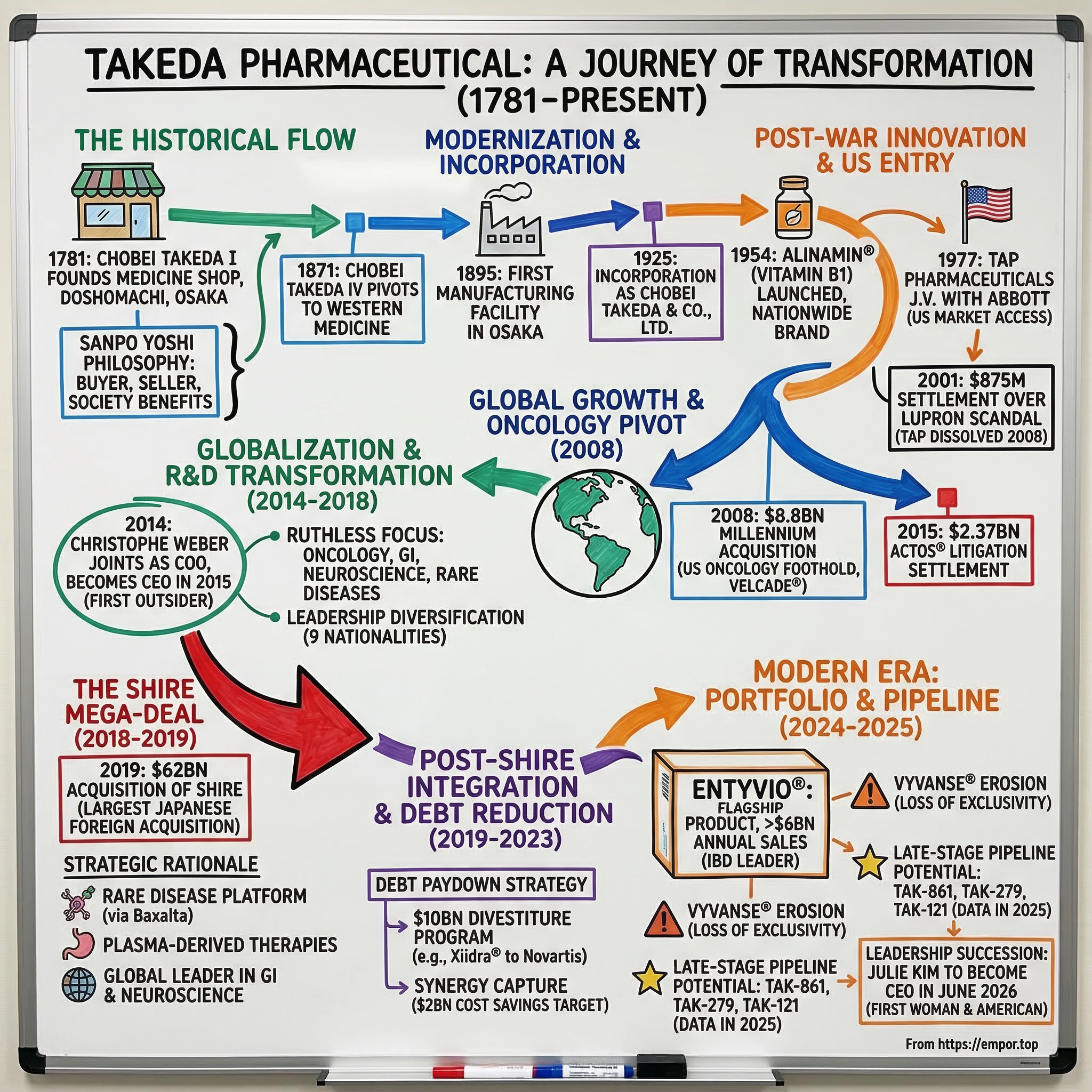

The year is 1781. In Doshomachi, Osaka's bustling medicine district, a 32-year-old merchant named Chobei Takeda opens a small shop selling traditional Japanese and Chinese herbal remedies. He buys medicines from wholesalers, divides them into smaller batches, and sells them to local doctors and merchants. Over two centuries ago in 1781, 32-year-old Chobei Takeda I started a business selling traditional Japanese and Chinese medicines in Doshomachi, Osaka, the center of the medicine trade in Japan.

Fast forward 237 years. In January 2019, that humble medicine shop has transformed into Takeda Pharmaceutical Company—and it has just completed the largest foreign acquisition in Japanese corporate history. Only eight months after the acceptance of its offer, Japanese pharma company Takeda completed its acquisition of international biotech Shire in January 2019. The deal was worth $62bn, making it Japan's largest foreign acquisition to date, by a significant margin and one of the largest pharmaceutical deals of the 21st century.

The Takeda Pharmaceutical Company Limited is a Japanese multinational pharmaceutical company. It is the third largest pharmaceutical company in Asia, behind Sinopharm and Shanghai Pharmaceuticals, and one of the top 20 largest pharmaceutical companies in the world by revenue (top 10 following its merger with Shire).

With a rich history spanning over 240 years and a presence in approximately 80 countries, including leading positions in Japan and the U.S., Takeda has evolved into a global biopharmaceutical leader.

The story of Takeda is ultimately about transformation—how a family business that began selling "old-fashioned Japanese and Chinese remedies" navigated the Meiji Restoration, two world wars, patent cliffs, billion-dollar litigation, and fierce global competition to become the only pharmaceutical company listed on both the Tokyo Stock Exchange and the New York Stock Exchange.

This article traces three pivotal inflection points in Takeda's modern history: the 2008 Millennium acquisition that planted Takeda's flag in U.S. oncology, the arrival of outsider CEO Christophe Weber in 2014, and the audacious $62 billion Shire bet that redefined what a Japanese company could accomplish on the global stage.

II. Origins & Founding Philosophy: The Edo Period to Modernization (1781–1914)

The Founding Story

Picture the narrow streets of 18th-century Osaka, Japan's commercial heart during the Edo period. Takeda established his business, initially known as the Chobei Omiya Store, in 1781 when he was approximately 32 years old, during the Edo period. Chobei Takeda I was born in Osaka during the 18th century.

He established his shop in Dōshōmachi, a district in Osaka recognized as the center of the medicine trade in Japan, and specialized in selling traditional Japanese medicines and traditional Chinese medicines (herbal medicines). As a merchant, Takeda developed a reputation for business integrity and high-quality products and services. His business model involved purchasing bulk medicines from wholesalers and dividing them into smaller quantities for sale to local merchants and medical practitioners.

In 1781, Takeda founder, Chobei I, began selling traditional Japanese and Chinese herbal medicines in Doshomachi, the medicine district of Osaka, Japan. He soon gained a reputation for business integrity and quality products and services.

The "Sanpo Yoshi" Philosophy

What set Chobei Takeda I apart from other merchants wasn't his inventory—it was his operating philosophy. As a merchant, Chobei I was noted for his business motto "Sanpo Yoshi Philosophy," which posited "There should be benefits on all three sides: Benefits for the buyer, Benefits for the seller and Benefits for society."

But there was another guiding principle, one that would prove even more enduring. The most important one was the Confucian teaching: "walk on no bypaths." It means accepting reality as the way it is and dealing with problems without compromising values or taking shortcuts.

The values and standards set by Chobei Takeda I are considered foundational to the modern Takeda Pharmaceutical Company. His emphasis on ethical business practices and product reliability is reflected in the company's long-standing corporate philosophy, often referred to as Takeda-ism by later generations.

Generational Leadership & Transition to Western Medicine

Into the 19th century, Takeda expanded under the leadership of Chobei I and his successors. Successive leaders inherited the name Chobei, until Chobei VI.

The critical pivot came during Japan's dramatic opening to the West. In 1852, Chobei Takeda III demolished the old family mansion in Osaka and built a new home and warehouse. In 1871, Chobei Takeda IV formed a cooperative union for purchasing Western medicines in Yokohama and began transactions with foreign trading companies.

The family business founded by Chobei Takeda I transitioned from traditional herbal medicine to the import of Western pharmaceuticals starting with Chobei Takeda IV in 1871.

In 1895, while Japan was at war with China in the First Sino-Japanese War, the company established its own factory in Osaka and became a pharmaceutical manufacturer. In parallel with the factory construction, Takeda began direct imports from England, the U.S., Germany, Spain, and other countries. Thus, the business that began as a shop selling old-fashioned Japanese and Chinese remedies quickly shifted its basic orientation toward Western medicines.

Becoming a Manufacturer

Following the Meiji Restoration in 1868, which spurred Japan's rapid industrialization and opening to Western influences, Takeda expanded its offerings to include imported Western medicines during the late 19th century. In 1895, the company acquired the Uchibayashi Drug Works, establishing its first manufacturing facility in Osaka and initiating domestic production of compounds such as bismuth subgallate and quinine hydrochloride, thereby reducing dependence on imports.

The research division, which researched and developed new pharmaceutical products, was also formed in 1915.

In 1914, a research division was established. Around the time when imports from Germany ended due to World War I, Takeda began the sales of its own products.

The transition from reseller to manufacturer marked Takeda's evolution from a merchant house into what would eventually become a modern pharmaceutical company. The foundation was laid not just in manufacturing capability, but in the values that would guide the company through centuries of change.

III. Building Japan's Pharmaceutical Champion (1925–1990s)

Incorporation & Modern Structure

Takeda Pharmaceuticals was founded in 1781 by Chobei Takeda, and was incorporated on January 29, 1925.

In 1925, the Company was incorporated as Chobei Takeda & Co., Ltd., with a capital of 5.3 million yen and Chobei Takeda V as president.

Takeda Pharmaceutical Company merged with Chobei Takeda & Co., Ltd in 1925 and became the main factory of the pharmaceutical division.

Post-War Innovation & Vitamin B1 Breakthrough

Japan's post-war devastation created unexpected opportunity. The nation faced severe malnutrition, and Takeda moved quickly to address it.

In 1953, Takeda and ACC each provided half of the capital to establish Lederle (Japan), now Wyeth K.K. This was the first pharmaceutical joint venture in Japan after the war. Lederle (Japan) manufactured the antibiotic Aureomycin, which Takeda marketed.

In 1954, Takeda successfully developed and began sales of the vitamin B1 derivative Alinamin®, a prodrug that increased absorption of vitamin B1. Around the same time, the Company also started supplying vitamins for food enrichment to ease the malnutrition caused by postwar food shortages.

Alinamin became a cultural phenomenon in Japan—one of the nation's most recognized pharmaceutical brands. It demonstrated Takeda's ability to identify critical health needs and develop products that resonated deeply with consumers.

The TAP Pharmaceuticals Partnership

Takeda's first major international venture came through its partnership with Abbott Laboratories in 1977, forming TAP Pharmaceuticals. TAP Pharmaceuticals was formed in 1977 as a joint venture between the two global pharmaceutical companies, Abbott Laboratories and Takeda Pharmaceutical Co. and was dissolved in 2008; its two most lucrative products were proton-pump inhibitor lansoprazole (Prevacid) and the prostate cancer drug, leuprorelin (Lupron). The intention of the joint venture was to get products that Takeda had discovered developed, approved, and marketed in the US and Canada.

The company was established at a time when Japanese pharmaceutical companies were seeking partnerships to access the US market. These efforts were supported by the Japanese government at the time to help the national economy compete in higher technology, as countries like South Korea, Taiwan were beginning to catch up with Japan in commodity production. Japanese pharmaceutical companies were especially strong in the fields of generating analogs of known cephalosporin antibiotics, cancer drugs, and cardiovascular drugs.

The partnership proved enormously successful commercially—but would also deliver a devastating scandal.

The Bittersweet Legacy

TAP Pharmaceutical Products Inc. ("TAP"), a major American pharmaceutical manufacturer, has agreed to pay $875,000,000 to resolve criminal charges and civil liabilities in connection with its fraudulent drug pricing and marketing conduct with regard to Lupron, a drug sold by TAP primarily for treatment of advanced prostate cancer in men.

TAP Pharmaceutical Products Inc., a major pharmaceutical manufacturer that is a joint venture between Abbott Laboratories and Takeda Chemical Industries, Ltd., agreed on October 3, 2001 to pay $875 million to settle criminal charges and civil liabilities with regard to its pricing and marketing of the drug Lupron.

The global agreement includes: (a) TAP has agreed to plead guilty to a conspiracy to violate the Prescription Drug Marketing Act and to pay a $290,000,000 criminal fine, the largest criminal fine ever in a health care fraud prosecution.

In the largest health-care fraud settlement in U.S. history, drugmaker TAP Pharmaceutical Products Inc. of Lake Forest Wednesday agreed to pay $875 million and plead guilty to a criminal charge of conspiring with doctors to overbill government insurers for its prostate cancer drug Lupron.

The TAP scandal taught Takeda a painful lesson about the reputational risks of operating in the U.S. market. It would later prove deeply relevant as the company prepared for far larger American ambitions.

IV. Inflection Point #1: The Millennium Acquisition & Oncology Pivot (2008)

Context: The Need to Go Global

By 2008, Takeda faced an existential strategic question. Japan's aging demographics meant a shrinking domestic market. Government pricing pressures were intensifying. And the company's core products—including the diabetes blockbuster Actos—would eventually face patent cliffs.

The TAP partnership was ending. In March 2008, the deal comes against the backdrop of a significant restructuring of its business operations in the wake of the dissolution of TAP, its joint venture in the United States with Abbott Laboratories.

The Millennium Bet

On April 10, 2008, Takeda made its boldest move yet. On May 14, 2008, Japanese company Takeda Pharmaceutical announced the completion of its acquisition of Millennium for US$25.00 per share in cash—a deal worth $8.8 billion.

Takeda Pharmaceutical has unveiled the largest-ever acquisition of a foreign biotech by a Japanese drug-maker, paying US$8.8 billion for Millennium Pharmaceuticals—best known as the manufacturer of leading multiple myeloma drug Velcade (bortezomib). The deal dwarfs even the US$3.9-billion acquisition of another U.S. firm, MGI Pharma, by fellow Japanese operation Eisai in December 2007.

In April, Takeda acquired Millennium Pharmaceuticals of Cambridge, Massachusetts, a company specializing in cancer drug research, for US$8.8 billion. The acquisition brought in Velcade, a drug indicated for hematological malignancies, as well as a portfolio of pipeline candidates in the oncology, inflammation, and cardiovascular therapeutic areas.

The acquisition of Millennium accelerates Takeda's vision of becoming a global leader in oncology with critical mass in the areas of oncology discovery, development, regulatory affairs and commercialization. Millennium and Takeda have complementary research, development and commercialization capabilities, which have the potential to create a powerful new drug development engine and accelerate the potential of an emerging drug pipeline.

Yasuchika Hasegawa, president of Takeda Pharmaceutical Company, had a vision to make Takeda a top tier company in oncology by 2015. In 2008, Takeda acquired Millennium Pharmaceuticals, a respected oncology company with annual sales of $528 million in 2007 and a promising pipeline of new drugs.

Upon completion of the acquisition, Millennium will become a wholly-owned subsidiary of Takeda Pharmaceutical Company Limited, and will continue operations in Cambridge, Massachusetts, as a standalone business unit. Millennium will be known as Millennium Pharmaceuticals, Inc., a Takeda Company.

The Millennium deal established Takeda's foothold in the Boston biotech ecosystem—a strategic position that would prove invaluable for future deals and talent acquisition. Cambridge became Takeda's U.S. R&D headquarters.

The Actos Era & Challenges

While building its oncology franchise, Takeda faced mounting trouble from its biggest commercial product. One of the firm's mainstay drugs is Actos (pioglitazone), a compound in the thiazolidinedione class of drugs used in the treatment of type 2 diabetes. It was launched in 1999.

Prior to the end of its patent in 2012, Actos brought in a significant amount of money and business for Takeda Pharmaceuticals. According to a court filing in Louisiana, U.S. Actos sales reportedly topped $24 billion between its release in 1999 and the court filing in 2014.

But the litigation storm was gathering. Patients who took the drug for more than a year had double the risk of those who did not take the drug. Because of the settlement, the company will take a historic loss – its first since it appeared on Japan's Nikkei stock exchange in 1949.

In April 2015 Takeda agreed to pay a settlement of $2.37 billion to an estimated 9,000 people who submitted claims alleging that pioglitazone was responsible for giving them bladder cancer. The company said the decision is expected to resolve the "vast majority" of these cases.

In 2015, manufacturer Takeda Pharmaceuticals agreed to pay a $2.37 billion in Actos® settlements to resolve over 9,000 state and federal cases. This is one of the highest settlement amounts in the history of pharmaceutical litigation.

The first bellwether case, tried in 2014, saw a $9 billion punitive damages jury award, which was among the top ten punitive awards in U.S. history. Plaintiff Terrence Allen of New York was prescribed Actos® beginning in 2006 and was diagnosed with bladder cancer in 2011.

The Actos litigation underscored both the rewards and risks of building blockbuster franchises. It would also drain capital and management attention just as Takeda was contemplating its next strategic leap.

V. Inflection Point #2: Christophe Weber & The Globalization Transformation (2014–2018)

The Outsider CEO

In April 2014, Takeda made a decision that shocked corporate Japan: it hired a foreigner as its next chief executive. Christophe Weber is president, chief executive officer (CEO) and representative director of Takeda. He joined the company in April 2014 as chief operating officer, was named president and representative director in June 2014, and was subsequently appointed CEO in April 2015.

Prior to joining Takeda, Christophe spent 20 years at GlaxoSmithKline where he held senior leadership roles in Europe, Asia and the United States.

Prior to joining Takeda, he spent 20 years at GlaxoSmithKline (GSK) in Europe, the US, and Emerging Markets. He held positions of increasing responsibility in Europe and then the USA as VP Competitive Excellence and Corporate Strategy before his appointment as chairman and CEO of GSK France in 2003. There, he maintained the profitability of GSK's largest European business. He moved to Singapore in 2008, where he successfully restored revenue growth across 13 Asia Pacific countries. He returned to Europe in 2011 to continue his development as a global leader.

He has worked in the pharmaceutical industry for more than 25 years, amassing experience in nine countries. He worked for more than 20 years at the British company GlaxoSmithKline, rising through the ranks to hold several leadership positions including president and general manager at GSK Vaccines and CEO of GSK Biologicals SA in Belgium.

The Transformation Agenda

Christophe has focused on ensuring the company's competitiveness through globalization and R&D transformation - all while creating a diverse and inclusive working environment and strengthening Takeda's ethical values and corporate governance. Through this transformation, Takeda has become one of the leading global biopharmaceutical companies.

The numbers tell the story of Weber's transformation. In 2008, 90 percent of the company's employees were in Japan. Today, 70 percent are outside Japan. Weber has also diversified the company's leadership team—which comprises nine nationalities and 70 percent of which has joined Takeda in the past two years—as well as its board of trustees.

Weber served as the keynote speaker Tuesday morning at the latest installment of Northeastern's CEO Breakfast Forum, where he noted significant transformations to position the company for success, including expanding the company's global footprint, diversifying its leadership and workforce, and being as agile as possible for a company operating in more than 70 countries worldwide. In particular, he discussed the strategic decision to hone the pharmaceutical company's focus on innovation in three areas of therapy: oncology, gastrointestinal disease and disorders, and mental health. Under his leadership, Takeda has consolidated its research operations in Japan and the U.S.

Weber's strategic vision centered on ruthless focus. Rather than trying to compete across every therapeutic area, Takeda would concentrate resources on a few high-potential domains where it could achieve global leadership.

Building the War Chest

Between 2014 and 2018, Weber systematically prepared Takeda for a transformational deal. The company divested non-core assets, streamlined operations, and built relationships with global investment banks. The quiet buildup of capabilities went largely unnoticed—until March 2018, when the world learned what Weber had been planning.

VI. Inflection Point #3: The Shire Mega-Deal (2018–2019)

The Courtship

The Japanese pharma began its courtship of mid-sized, rare disease-focused Shire in March 2018. A range of analysts predicted an offer would spark interest from other larger pharma companies; Irish-headquartered Allergan emerged as a rival competitor. However, within two months Takeda's proposal was accepted by both companies' boards of directors.

The courtship was intense. Takeda made multiple offers, each increasing the price as Shire's board held out for better terms. This was linked to Takeda increasing its offer for the entire issued and to be issued ordinary capital of Shire; the highest offer made saw Shire's shareholders receiving $30.33 in cash for each Shire share, or 0.839 new Takeda shares. The equivalent value was £48.17 per Shire share based on the closing price of Takeda shares on 2 May 2018 and relevant exchange rates.

Deal Structure & Financing

Under the terms of the acquisition, each Shire shareholder will be entitled to receive $30.33 in cash for each Shire share and either 0.839 new Takeda shares or 1.678 Takeda ADSs.

Takeda has entered into a bridge facility agreement of $30.85 billion with, among others, J.P. Morgan Chase Bank N.A., Sumitomo Mitsui Banking Corporation and MUFG Bank, Ltd., part of the proceeds of which will be used to fund the cash consideration payable to Shire shareholders in connection with the acquisition.

The acquisition of Shire placed about $30 billion of debt on the back of Takeda.

The divestiture of Xiidra is not surprising given the notable $62 billion takeover of Shire. When the Takeda-Shire deal was first announced in April 2018, there were some concerns that Takeda would not be able to afford this purchase, as it had only $4.3 billion in cash to hand and the deal could have over-stretched its finances. As a result, Takeda had to take on a significant amount of debt to afford its pricy takeover of Shire, and rumours of potential divestments were immediate.

Strategic Rationale

Why Shire? The strategic logic was multifaceted.

The core motivation behind the acquisition noted by Takeda throughout the process was to create a company centred on research and development (R&D). Takeda continually emphasised the complementary portfolio the two companies have in gastroenterology (GI) and neuroscience, as well as how Shire will bring its strength in rare diseases and plasma-derived therapies to add to Takeda's assets in oncology and vaccines.

Shire itself had transformed through acquisition. Ireland-based Shire on Monday announced a $32 billion stock and cash deal to buy Baxalta, bringing its months-long pursuit of the Illinois-based drug company to a close. Baxalta had previously rejected earlier all-stock offers from Shire. Shire will pay $18.00 plus 0.1482 of its American Depository shares for each Baxalta share. Based on Shire's closing price on January 8th, the deal values each Baxalta share at $45.57, or about $32 billion in aggregate.

Through the combination, Shire expects to deliver double-digit compound annual top-line growth, with over $20 billion in annual projected revenue by 2020 and approximately 65% of total annual revenues being immediately generated by its rare disease products.

By acquiring Shire, Takeda was gaining the rare disease platform that Shire had built through the Baxalta transaction. Baxalta is a biopharmaceutical company founded on 1 July 2015 after its parent company, Baxter International, spun off biopharmaceutical division. The company began its operation with a revenue of $6 billion, and is now a subsidiary of Takeda Pharmaceutical Company.

Shareholder Approval & Closing

At Takeda's extraordinary general meeting on 5 December 2018, the vast majority of shareholders approved the acquisition of Shire. The approval rates were 89.1% from Takeda and 99.8% from Shire. The deal was sanctioned by the Royal Court of Jersey in early January 2019; the acquisition was closed on 8 January, and integration of the two companies could begin.

Takeda today announced the completion of its acquisition of Shire plc ("Shire"), becoming a global, values-based, R&D-driven biopharmaceutical leader headquartered in Japan. Takeda now has an attractive, expanded geographic footprint and leading position in Japan and the U.S., bringing its highly-innovative medicines to approximately 80 countries/regions with dedicated employees worldwide. Takeda's R&D efforts are focused on its four therapeutic areas of Oncology, Gastroenterology (GI), Neuroscience and Rare Diseases, with targeted R&D investment also committed to Plasma-Derived Therapies (PDT) and Vaccines.

With the acquisition of Shire, the combined annual revenue of Takeda now exceeds US$30 billion.

VII. Post-Shire Integration & Debt Reduction (2019–2023)

The $10 Billion Divestiture Program

At the beginning of 2019, Takeda Pharmaceutical announced plans to sell about $10 billion worth of assets to offset some of the debt the company garnered in its $62 billion acquisition of Shire.

The divestiture program proceeded at remarkable speed.

Takeda completed the divestiture of Xiidra® to Novartis for up to $5.3 billion USD in July, announced the sale of TachoSil® to Ethicon for $400 million USD in May, and last month announced its sale of non-core assets in countries spanning Near East, Middle East and Africa to Acino for over $200 million USD. This is Takeda's fourth divestment transaction in the past six months that contributes to the Company's goal to divest approximately $10 billion USD in non-core assets to focus on its five key business areas and commitment to accelerating its deleveraging following its acquisition of Shire.

As previously rumored, Takeda is selling Shire's dry-eye drug Xiidra. To take it in, Novartis is shelling out $3.4 billion upfront and commits potential milestone payments of up to $1.9 billion.

The sale of Xiidra to Novartis and TachoSil to Ethicon is part of Takeda's strategy to pare down debt from its $62 billion acquisition of Shire. "These initial divestitures represent important steps in advancing the growth strategy Takeda outlined following our transformational acquisition of Shire earlier this year," Christophe Weber, Takeda's president and chief executive officer said in a statement. "We are working to strategically simplify and optimize our portfolio, while also rapidly deleveraging and continuing to invest in our growth drivers as a global, values-based, R&D-driven biopharmaceutical leader."

Takeda has announced a series of divestments in the past twelve months, contributing to the Company's goal to divest approximately $10 billion USD in non-core assets and focus on its key business areas. Takeda announced last month the sale of non-core products in Latin America to Hypera Pharma for $825 million USD. Takeda also completed sales of non-core assets spanning the Russia-CIS region to STADA for $660 million USD and in countries spanning the Near East, Middle East and Africa region to Acino for over $200 million USD last month.

Synergy Capture & Cost Savings

In May 2019, Nikkei reported Weber increased the company's cost-savings target for the integration with Shire from $1.4bn to $2bn by the end of 2021.

The company met—and exceeded—its targets. Takeda is confident that the acquisition will create an opportunity to recognize significant recurring cost synergies, with potential for additional revenue synergies from the combination of Shire and Takeda's combined infrastructure, market presence and development capabilities. Takeda expects recurring pre-tax cost synergies for the combined group to reach a run-rate of at least $1.4 billion per annum by the end of the third fiscal year following completion of the acquisition.

Strategic Focus

While these trusted products continue to play important roles in meeting patient needs, they are not within Takeda's chosen business areas – Gastroenterology, Rare Diseases, Plasma-Derived Therapies, Oncology and Neuroscience – that are core to its global long-term growth.

In July 2019, Takeda completed the sale of Xiidra® to Novartis for up to $5.3 billion USD. Takeda intends to use the proceeds from its divestitures to continue to reduce its debt towards its target of 2x net debt/adjusted EBITDA within March 2022 – March 2024.

VIII. Modern Era: Current Portfolio & Pipeline (2024–2025)

Financial Performance

Takeda Pharmaceutical Co. Ltd. (TAK) has reported a noteworthy 7.5% boost in annual revenue, reaching ¥4,581.6 billion for the fiscal year 2024.

Takeda (TAK) reported strong FY2024 financial results with core revenue growth of 7.4% (AER) and 2.8% (CER), driven by Growth & Launch Products momentum. Core Operating Profit increased by 4.9% at CER, supported by efficiency program cost savings.

The company's core operating profit margin improved to 25.4%, up from 24.7%. Operating cash flow surged by 47.6% to ¥1,057.2 billion, while adjusted free cash flow jumped 171.3% to ¥769.0 billion.

"Takeda is now at an inflection point, with multiple anticipated Phase 3 data readouts this fiscal year, and I'm excited about our growth trajectory."

Key Products

Entyvio, Takeda's treatment for inflammatory bowel disease, has become the company's flagship product. ENTYVIO sales have seen steady growth due to increased biologic uptake, earlier-line use, and the launch of subcutaneous (SC) formulations in key markets. In 2024, global ENTYVIO sales surpassed $6 billion, solidifying its position as a top-selling biologic.

Despite the enthusiasm around AbbVie's fast-rising up-and-coming blockbuster Skyrizi, Entyvio's growth "continues to outperform" the overall IBD market, according to Takeda's recent investor presentation. With a new subcutaneous formulation for Entyvio, the company isn't worried about new entrants affecting its leading spot in the first-line IBD market.

In the U.S., the drug commands the No. 1 position in both ulcerative colitis (UC) and Crohn's disease, the two types of IBD, according to the drugmaker.

In the U.S., things are still looking good for Entyvio. The drug has been pulling its weight as the company's top sales driver and continues to hold the line as the No.1 most prescribed brand in the crowded U.S. IBD market, according to Takeda.

Vyvanse Erosion Challenge

Besides the Entyvio spotlight in Takeda's earnings, the company said its growth products "more than offset" the loss of exclusivity impacts from former big sellers, including attention-deficit hyperactivity disorder Vyvanse, during the first quarter. Vyvanse sales are still declining after a U.S. loss of exclusivity in August, albeit at rates "slightly milder than anticipated" thanks to supply struggles for many generics makers, Takeda said. Still, U.S. Vyvanse revenues dipped 32% during the quarter and are expected to fall more in upcoming quarters as generic supply picks back up.

FY2025 Management Guidance at CER reflects residual carry-over of VYVANSE® generic impact, continued efficiency savings and investment in R&D and launch preparation for Takeda's late-stage pipeline.

The Late-Stage Pipeline

The late-stage pipeline includes oveporexton (TAK-861), zasocitinib (TAK-279), rusfertide (TAK-121), mezagitamab (TAK-079), fazirsiran (TAK-999) and elritercept (TAK-226). Combined these programs have potential peak revenue of $10B - $20B.

Data from three Phase 3 programs is expected to read out in 2025: oveporexton, a potential best-in-class and first-in-class investigational oral orexin receptor 2 agonist will report Phase 3 results in narcolepsy type 1; zasocitinib, an investigational next-generation, highly selective and potent oral allosteric tyrosine kinase 2 (TYK2) inhibitor will deliver Phase 3 results in psoriasis; and rusfertide, an investigational injectable hepcidin mimetic in development with partner Protagonist Therapeutics, will have Phase 3 results in polycythemia vera.

At JPM, Takeda CEO Christophe Weber said the company is focused on six pipeline assets that could each reel in blockbuster-level sales down the line. Assuming they all win approval, the clutch of potential new drugs could collectively generate peak sales between $10 billion and $20 billion—representative of roughly one-third to two-thirds of Takeda's current annual revenue.

Of those assets, Weber put the most emphasis on the narcolepsy type 1 candidate oveporexton, the psoriasis asset zasocitinib and the company's potential polycythemia vera treatment rusfertide, all of which are expected to deliver phase 3 data this year. Takeda's oral orexin receptor 2 agonist oveporexton could eventually hit peak sales between $2 billion and $3 billion, Takeda noted in its presentation. The "key" to the narcolepsy type 1 asset, according to Weber, is its ability to mimic the body's natural orexin cycle. Orexin is a neuropeptide lacking in patients with narcolepsy that helps regulate waking, wakefulness, appetite and energy.

As for Takeda's psoriasis and psoriatic arthritis candidate zasocitinib, the company expects its drug "will have a much higher efficacy" than the current TYK2 inhibitor on the market, Weber said. If approved, the drug would challenge Bristol Myers Squibb's Sotyktu, the first-in-class TYK2 inhibitor. Takeda expects that zasocitinib, if approved, could generated peak sales in a range of $3 billion to $6 billion.

Leadership Transition

Takeda announced today that its Board of Directors made the decision unanimously to appoint Julie Kim, currently president of Takeda's U.S. Business Unit, as the successor to Christophe Weber, Takeda's president, chief executive officer (CEO) and representative director, when Mr. Weber retires from the company in June 2026.

She will replace Christophe Weber who plans to step down in June of 2026 after leading Japan's largest drugmaker for 11 years. The company called the promotion of Kim part of a "multi-year succession process."

Julie joined Takeda in 2019 through the acquisition of Shire and has held several diverse roles with increasing responsibility, including president of the Plasma-Derived Therapies Business Unit.

Christophe Weber broke a major barrier at Takeda when he was named CEO 10 years ago – he was the first non-Japanese to serve as the company's top decision maker. His successor Julie Kim will break two more when she takes over in June of next year; she'll become the first woman and the first American to lead the nearly 250-year-old company. And Kim isn't just American – her most recent leadership experience has come in the American marketplace, having spent the last three years leading Takeda's U.S. business. Her appointment is another clear signal from a company whose strategic vision has moved far beyond a prior focus on its home country; since Weber took over the American share of Takeda's business has risen from less than a quarter to more than half, while the Japanese share has fallen from 40 percent to just 9 percent.

IX. Competitive Analysis & Strategic Position

Industry Landscape

Takeda operates in one of the world's most competitive industries. Takeda Pharmaceutical's top 19 competitors are Janssen, AbbVie, UCB, AstraZeneca, EMD Serono, Pfizer, Bayer, Sanofi, CSL, Novo Nordisk, Octapharma, Roche, Sanofi Genzyme, Bristol-Myers Squibb, Lilly, Gilead Sciences, Teva, Abbott and Mylan.

Merck & Co. remains the "big dog" in the pharma industry in 2025, with roughly $64.17 billion in FY2024 revenue. It claimed the top position a year earlier. Drawing on continued Keytruda momentum, which continues its reign as the world's best-selling drug with sales that rose 18% to $29.5 billion in 2024. In all, Keytruda accounts for about 46% of Merck's sales.

Established giants like Johnson & Johnson (pharma revenue of $57.07B), AbbVie ($56.33B), and AstraZeneca ($54.07B), round out the top five slots. J&J has sustained momentum in oncology and immunology.

Competitive Positioning in Immunology

The drugmaker has a cushion over Takeda and Sanofi, which, respectively, ranked fourth and fifth with scores of 34 and 14, but has reasons to be glancing over its shoulder. Takeda is mounting a charge, ZoomRx said, as shown by positive perception scores in the latest data. The drugmaker has won approval for Eohilia and spent $4 billion on Nimbus Therapeutics' TYK2 inhibitor, leading ZoomRx to call it a "strong contender in the competitive landscape."

S&P Global Assessment

Johnson & Johnson and Roche are at the top of S&P Global's pharmaceutical industry power ratings, which assess the strength of the world's top 17 drugmakers.

Also tabbed as "strong" in the business risk category were Merck, AbbVie, Bristol Myers Squibb, Takeda and Amgen. As to financial risk, Merck ranks with Lilly as having "modest" risk, while AbbVie, BMS and Takeda were a slot below, at "intermediate."

X. Bull & Bear Case Analysis

Bull Case

1. Pipeline Optionality Worth $10-20 Billion Takeda's six late-stage programs represent substantial upside. If even half succeed, the company could add $5-10 billion in peak annual revenues—roughly a 20-30% increase from current levels. The diversity of therapeutic areas (narcolepsy, psoriasis, blood cancers, liver disease) provides multiple shots on goal.

2. Entyvio's Durable Franchise Despite competitive threats from AbbVie's Skyrizi and Rinvoq, Entyvio maintains its #1 position in first-line IBD treatment. The subcutaneous formulation extends the franchise's runway and improves patient convenience. With IBD prevalence rising globally, the addressable market continues to expand.

3. Rare Disease Moat The Shire acquisition gave Takeda a rare disease portfolio with high barriers to entry. Plasma-derived therapies require specialized manufacturing infrastructure that takes years to build. Patient populations are small but loyal, and pricing power remains strong.

4. Post-Vyvanse Trough FY2025 represents the final year of major generic erosion from Vyvanse. Once this headwind subsides, underlying growth from newer products should become more visible in reported results.

5. Management Continuity Julie Kim's appointment signals strategic continuity. Her experience running the U.S. business—now over 50% of revenues—positions her well to execute on pipeline launches.

Bear Case

1. Entyvio Competition Intensifies AbbVie's Skyrizi and Rinvoq are gaining share rapidly. Biosimilar risk looms, though timing remains uncertain. Any negative clinical data or competitive displacement could significantly impact Takeda's largest franchise.

2. Pipeline Execution Risk Phase 3 trials frequently fail. Takeda's peak revenue estimates assume regulatory approval and commercial success for multiple assets—each with meaningful clinical and commercial risk.

3. Leverage Concerns While significantly reduced from 2019 peaks, Takeda's debt load remains substantial. Rising interest rates have increased financing costs. Any major acquisition would be constrained until leverage decreases further.

4. Japan Exposure Although reduced to 9% of revenues, Japan remains Takeda's second-largest market. Government pricing pressures continue, and demographic headwinds show no signs of abating.

5. Geographic Concentration With over 50% of revenues from the U.S., Takeda is heavily exposed to U.S. healthcare policy changes, including potential Medicare drug price negotiations under the Inflation Reduction Act.

Porter's Five Forces Analysis

| Force | Assessment |

|---|---|

| Supplier Power | Low. Drug manufacturing inputs are largely commoditized. Specialized APIs can create dependency, but Takeda's scale provides negotiating leverage. |

| Buyer Power | Moderate-High. U.S. PBMs and government payers exert significant pricing pressure. However, specialty drugs in rare diseases face less pressure than mass-market therapies. |

| Threat of New Entrants | Low-Moderate. Pharma has enormous barriers: R&D costs exceeding $2 billion per approved drug, regulatory complexity, and decade-long development timelines. However, biotech startups continually emerge with novel approaches. |

| Threat of Substitutes | Moderate. Biosimilars threaten biologics after patent expiry. Novel modalities (gene therapy, cell therapy) could disrupt traditional drug paradigms. |

| Competitive Rivalry | High. Global pharma is intensely competitive with well-capitalized players. Therapeutic area specialization creates pockets of differentiation. |

Hamilton Helmer's 7 Powers Framework

| Power | Takeda's Position |

|---|---|

| Scale Economies | Moderate. Global manufacturing and commercial infrastructure provide unit cost advantages, though not decisive versus larger competitors. |

| Network Effects | Limited. Healthcare data networks and patient registries create some network value in rare diseases. |

| Counter-Positioning | Weak. Takeda's strategy (focused therapeutic areas, global biopharma) is well-understood and replicable. |

| Switching Costs | Moderate. Patients on chronic therapies face switching costs (titration, side effect uncertainty), but payers actively manage therapeutic substitution. |

| Branding | Moderate-Strong in Japan; moderate elsewhere. "Takeda-ism" and 240+ year heritage create trust with patients and physicians in certain markets. |

| Cornered Resource | Limited. Cambridge R&D hub provides talent access, but Boston is highly competitive for scientific talent. |

| Process Power | Moderate. Plasma-derived therapy manufacturing requires specialized know-how built over decades. |

XI. Key Metrics for Investors

For long-term fundamental investors tracking Takeda's ongoing performance, three KPIs merit particular attention:

1. Growth & Launch Products Revenue Growth (Constant Currency)

Takeda defines "Growth & Launch Products" as the subset of its portfolio driving organic expansion. This metric strips out legacy products facing generic erosion and currency fluctuations, revealing the underlying health of newer franchises. Watch for: - Entyvio volume and share trends in IBD - Immunoglobulin demand and supply dynamics - Takhzyro penetration in hereditary angioedema

2. Core Operating Profit Margin

Takeda reports both IFRS and "Core" results, with Core excluding one-time items and acquisition-related accounting. Core Operating Profit margin reveals whether commercial success is translating to bottom-line leverage. The company has targeted margin expansion as integration synergies flow through; any reversal would signal execution issues.

3. Net Debt / Adjusted EBITDA Ratio

Post-Shire deleveraging remains a central management priority. The company has targeted returning to 2.0x net debt/adjusted EBITDA. Progress on this metric directly impacts financial flexibility for business development, dividend sustainability, and credit ratings.

XII. Myth vs. Reality

| Consensus Myth | Reality |

|---|---|

| "Takeda overpaid for Shire" | The jury is still out. Shire's rare disease portfolio and plasma business have performed well. However, significant divestitures (Xiidra, TachoSil) suggest some assets were never central to strategy. True value creation depends on pipeline success from Shire-inherited programs. |

| "Japanese pharma can't compete globally" | Takeda has disproven this. With 70% of employees outside Japan, 50%+ of revenue from the U.S., and leadership drawn from nine nationalities, Takeda is functionally a global company headquartered in Japan—not a Japanese company with global aspirations. |

| "Entyvio faces imminent biosimilar risk" | Entyvio's patent situation is more complex than headline expiry dates suggest. Multiple formulation patents, manufacturing complexity, and the subcutaneous launch create runway. However, competition from novel mechanisms (not just biosimilars) is the more immediate threat. |

| "Weber's successor lacks experience" | Julie Kim brings 30 years of healthcare experience, ran Takeda's largest business unit, and came to the company through Shire—meaning she understands both legacy organizations. Her appointment represents continuity, not disruption. |

XIII. Legal & Regulatory Considerations

Investors should note several material overhangs:

Ongoing RICO Litigation: June 16, 2025: The Ninth Circuit affirmed a class certification order in Painters & Allied Trades District Council 82 Health Care Fund v. Takeda Pharmaceutical Company Limited. This marks a watershed moment in a first-of-its-kind class action that our class action attorneys have been litigating for roughly 11 years. Painters is the first non-settlement national RICO class action certified against a Big Pharma, and legal experts estimate the total damages in the case could exceed $7 billion.

This case relates to historical Actos marketing practices and could result in material additional liability.

U.S. Drug Pricing Policy: Takeda's significant U.S. revenue exposure creates uncertainty around Medicare price negotiations under the Inflation Reduction Act. Entyvio could eventually become subject to negotiated pricing, potentially impacting the company's largest franchise.

Pipeline Regulatory Risk: Late-stage clinical programs face inherent regulatory approval uncertainty. Any complete response letters or additional clinical requirements could delay launches and impact revenue projections.

XIV. Conclusion: The 244-Year Bet

In 1781, Chobei Takeda I opened his medicine shop with a simple philosophy: benefits for the buyer, benefits for the seller, benefits for society. Nearly two and a half centuries later, that philosophy—"walk on no bypaths"—remains embedded in the company he founded.

The Takeda of 2025 would be unrecognizable to its founder. It operates in 80 countries, generates over $30 billion in annual revenue, and develops medicines for diseases Chobei could never have imagined. Yet the through-line is unmistakable: a willingness to adapt, an appetite for calculated risk, and an obsession with quality that transcends any single product or market.

The Shire acquisition represented Takeda's boldest strategic bet—a $62 billion wager that a 237-year-old Japanese company could integrate a global rare disease leader and emerge stronger. Six years later, the integration is complete, the debt is declining, and the pipeline is maturing. Whether the bet pays off depends on execution over the next five years.

Takeda chief executive officer, Christophe Weber, commented: "Takeda delivered excellent results in FY2024. Our return to Core Operating Profit margin growth underscores the strength of our Growth & Launch Products portfolio and the ability of our multi-year efficiency program to deliver meaningful cost savings."

As Weber prepares to hand the reins to Julie Kim—the first woman and first American to lead the company—Takeda stands at another inflection point. The company has transformed from Japan's largest pharmaceutical company into a truly global biopharma leader. The question now is whether it can sustain that position against competitors with deeper pockets, stronger pipelines, and equally global ambitions.

For investors, Takeda offers a differentiated exposure to specialty pharmaceuticals: rare diseases, plasma-derived therapies, and gastroenterology franchises that face less price pressure than mass-market drugs. The late-stage pipeline provides meaningful optionality. But the company trades at a discount to larger peers—reflecting both the complexity of its story and lingering questions about execution.

The medicine shop in Doshomachi is long gone. But the values that Chobei Takeda I established—integrity, quality, and societal benefit—continue to shape decisions made in boardrooms from Tokyo to Boston. In an industry often criticized for prioritizing profits over patients, that heritage may prove to be Takeda's most durable competitive advantage.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube