Exelixis: The Biotech Phoenix That Bet Everything on One Molecule

The Central Question

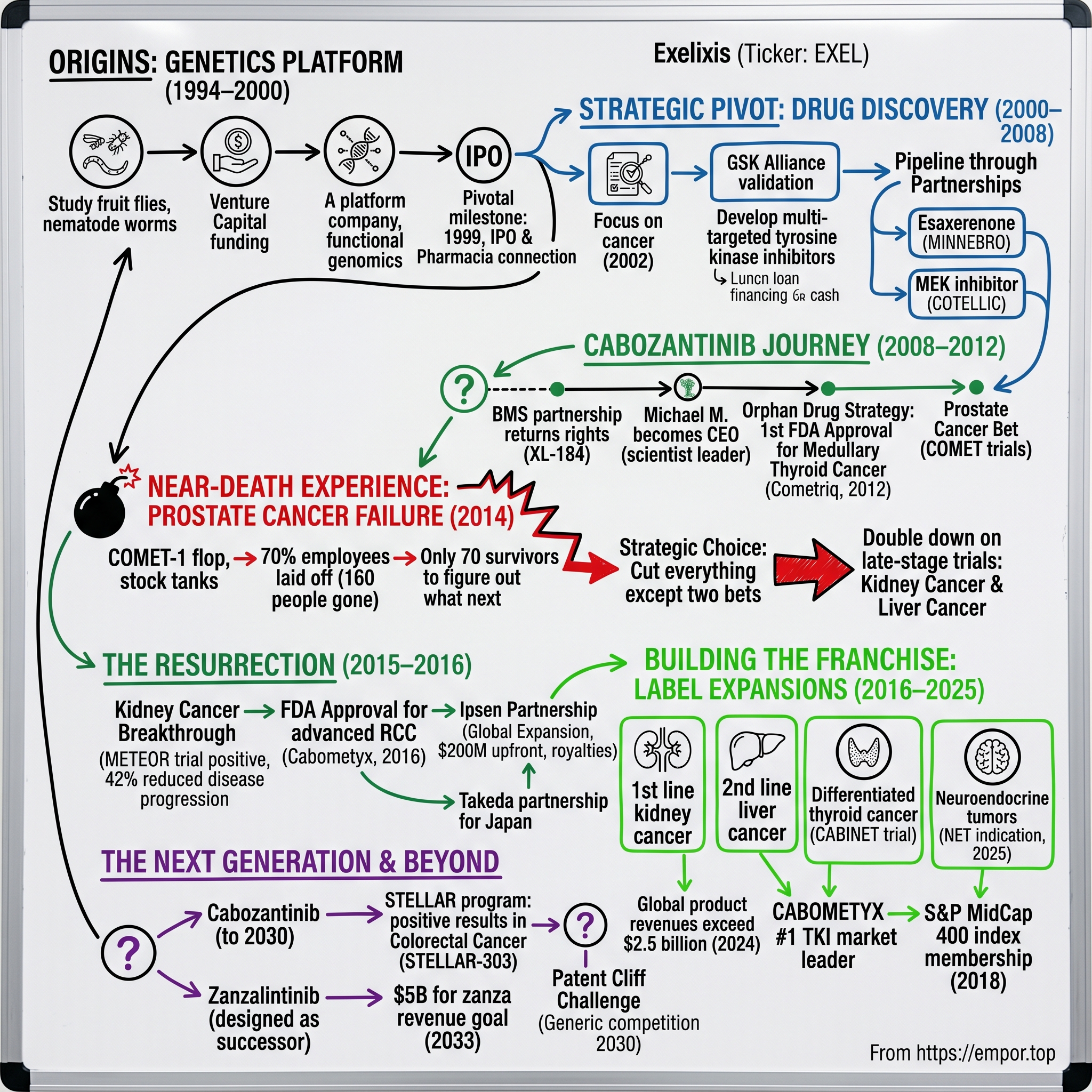

In the antiseptic corridors of a South San Francisco biotech lab, September 2014 brought a quiet devastation. The announcement came early on a Monday morning: cabozantinib, the drug that Exelixis had bet its entire future on, had failed to extend survival in prostate cancer patients. Within hours, the company's stock price had been cut in half. Within weeks, 70% of employees would be gone—160 people clearing their desks, leaving just 70 survivors to figure out what came next.

The story of Exelixis is one of the most dramatic turnarounds in biotech history. In 2014, the company suffered a late-stage clinical trial failure in prostate cancer with its lead drug candidate. Combined with a quickly fading cash runway, the study disaster caused the company's stock to tank, forcing leaders to cut 70% of the workforce. Now, Exelixis has regained its reputation among investors through the drug Cabometyx, which has picked up several cancer indications, as well as a growth trajectory that raised annual sales forecasts to $2.25 billion in 2025.

How did a company studying fruit flies in the 1990s transform into a $10+ billion oncology powerhouse? How did near-bankruptcy become the springboard for building one of biotech's most successful commercial franchises? And now, with patents expiring in 2030, can Exelixis do it all over again with a new molecule?

Today, Exelixis's stock price stands at $44.26 with a market cap of $12.1 billion and trailing twelve-month revenue of $2.23 billion. The central themes of this story—the power of persistence, the brutal economics of drug development, betting the company on a single molecule, and the art of the strategic pivot—offer a masterclass in biotech survival and reinvention.

Origins: When Scientists Studied Flies to Cure Cancer (1994–2000)

The Founding Vision

The late 1980s and early 1990s were heady times for geneticists. The Human Genome Project had just begun, and scientists were racing to decode the fundamental blueprints of life. At universities across America, researchers studying humble organisms—fruit flies, nematode worms, zebrafish—were making discoveries that would reshape our understanding of human disease.

Exelixis was founded in 1994; the scientific founders were Spyridon Artavanis–Tsakonas, at Yale at that time, and Corey Goodman and Gerry Rubin who were then at the University of California, Berkeley. These weren't drug developers in the traditional sense—they were academics, basic scientists who had spent their careers teasing apart the genetic machinery of model organisms.

The name "Exelixis" itself revealed the founders' ambition. The name is derived from the Greek word meaning "pursuit of excellence," reflecting the company's commitment to advancing healthcare through cutting-edge research and development.

The initial funding for the company came from venture capital firms, including Kleiner Perkins Caufield & Byers, which invested $9 million in the Series A round. Kleiner Perkins, the legendary Silicon Valley firm that had backed Genentech in the early days of biotech, saw potential in Exelixis's unconventional approach.

The Unconventional Science

The business plan was to use model organisms (fruit flies, nematodes, and zebrafish) and functional genomics to identify pathways and biological targets that could be exploited in the fields of agriculture and medicine. This was radical thinking for the time. Most drug companies worked backwards—starting with a known disease and hunting for compounds that might treat it. Exelixis wanted to work forwards—using genetics to identify the fundamental pathways that controlled cell growth and death, then developing drugs against those targets.

It eventually set up a subsidiary, Exelixis Plant Sciences, for the agricultural work. The early Exelixis was genuinely a platform company, not a drug company. Its scientists believed that the same genetic insights that could improve crop yields might also cure cancer.

George Scangos joined the company as CEO in 1996. Scangos, a microbiologist by training who had held senior positions at Chiron, brought operational discipline and a commercial orientation to the academic founders' vision. Under his leadership, Exelixis would begin the slow transformation from genetics platform to drug discovery engine.

Going Public & The Genomics Boom

The late 1990s genomics boom created a perfect window for companies like Exelixis. As sequencing costs fell and databases of genetic information grew, investors became convinced that genomics would revolutionize drug discovery. In 1999, Exelixis goes public, raising funds to support its research and development efforts.

A pivotal early milestone occurred in February 1999, when Exelixis entered a five-year collaboration with Pharmacia & Upjohn, delivering multiple novel drug targets derived from its genetics platform in exchange for research funding and milestone payments. This agreement underscored the commercial viability of Exelixis' model organism strategy.

The IPO arrived at precisely the right moment. Genomics companies were hot, and Exelixis rode the wave. But unlike many of its contemporaries—companies that would flame out when the genomics bubble burst—Exelixis was already evolving.

By 2000 it had left the radical exploratory phase behind and became focused on drug discovery and had a chemical library of 4 million compounds. This transition—from pure genomics platform to integrated drug discovery company—would prove crucial to Exelixis's survival. While other genomics companies spent the early 2000s searching for business models, Exelixis was building the capabilities to take drugs from target identification through clinical development.

For investors, the origin story reveals a fundamental truth about Exelixis: this company has always been willing to transform itself. The fruit fly researchers became genomics entrepreneurs became drug developers. That adaptability would be tested severely in the years ahead.

The Strategic Pivot: From Genomics Platform to Drug Discovery (2000–2008)

Focus on Cancer

The genomics bubble burst in 2000-2001, devastating the stocks of platform companies that couldn't demonstrate clear paths to products. Exelixis survived, but barely—its stock cratered along with the rest of the sector. Management responded with a strategic focus that would define the company's next two decades.

By 2002 the company had limited its internal efforts to cancer, and had settled its strategy on discovering and developing drugs that could inhibit targeted small sets of tyrosine kinases that are needed for cancer formation, growth, and metastasis. The sets of TKs had been identified by means of its prior functional genomics work. This approach was controversial at the time; most companies try to selectively target just one protein in their discovery efforts.

This strategic decision was both scientifically bold and commercially risky. The pharmaceutical industry's conventional wisdom held that drug candidates should be as selective as possible—hitting one target to minimize side effects. Exelixis's scientists believed that cancer's complexity required a multi-targeted approach. Their genomics work had revealed that tumors don't depend on single pathways; they're driven by networks of interacting signals.

The company's founders' background in basic biology shaped this thinking. When you study development in fruit flies, you learn that biological systems are redundant. Block one pathway, and another takes over. To truly stop a tumor, you might need to hit multiple targets simultaneously.

The GSK Alliance: A Validation Moment

Exelixis's strategy gained critical validation in 2002. In 2002 the company signed a broad alliance with GSK to discover new drugs in the fields of cancer, inflammatory diseases, and vascular conditions; GSK paid it $30 million in cash, bought $14 million in stock at twice the market rate, and committed to providing Exelixis with $90 million in research funding; it also offered loan financing of up to $85 million.

This was a transformative deal for a company Exelixis's size. GSK was one of the world's largest pharmaceutical companies, and their willingness to pay premium prices for Exelixis stock sent a clear signal: sophisticated industry insiders believed in the platform. The research funding and loan facilities provided crucial runway during years when many genomics-era companies were going bankrupt.

Building the Pipeline Through Partnerships

Throughout the mid-2000s, Exelixis pursued an aggressive partnership strategy. In 2006 Exelixis partnered with Daiichi Sankyo on compounds that targeted mineralocorticoid receptors; esaxerenone was part of this collaboration. Esaxerenone would eventually become MINNEBRO, a cardiovascular drug now marketed in Japan.

In 2007, the company partnered its MEK inhibitor program with Genentech; cobimetinib (at that time XL-518) was part of this collaboration. Exelixis had filed an IND on XL-518 prior to the partnership, committed to funding and running the Phase I trial, and retained rights to co-market it in the US. Cobimetinib would eventually become COTELLIC, approved for melanoma.

These partnerships revealed Exelixis's approach to risk management. By partnering compounds early—retaining some rights while letting larger companies shoulder development costs—Exelixis could build a diversified portfolio without the capital requirements of running multiple large clinical programs. The downside: if a partnered compound succeeded, Exelixis would capture only a fraction of the value.

By 2007, Exelixis had emerged from the genomics crash with a transformed identity. It was no longer a platform company selling access to targets; it was a drug discovery company with multiple clinical programs and deep relationships with industry giants. One compound in particular was generating excitement: XL-184, a multi-kinase inhibitor targeting VEGF receptors, MET, AXL, and RET. This molecule—which would eventually be called cabozantinib—would become the foundation of everything Exelixis built afterward.

The Cabozantinib Journey: From BMS Partnership to Go-It-Alone (2008–2012)

The Bristol-Myers Squibb Deal and Its Unwinding

In 2008 the company partnered its lead cancer drug candidate, XL-184 (which would become called cabozantinib) and another cancer candidate, XL-281, with Bristol Myers Squibb. The partnership followed the same model Exelixis had used before: trade development rights for upfront payments and milestone potential, reducing risk while giving up future upside.

But something unexpected happened. BMS returned the rights to XL-184 to Exelixis in 2010 and returned the rights to other drug candidate in 2011.

When a major pharmaceutical company walks away from your lead asset, it's rarely a vote of confidence. BMS's decision to return cabozantinib rights sent a troubling signal to investors and industry watchers. What did BMS's scientists see in the data that made them want out?

The timing was particularly awkward because Exelixis was simultaneously going through a leadership transition. In 2010 Scangos departed as CEO to take over at Biogen and the company appointed Michael M. Morrissey as president and CEO; Morrissey had joined the company in 2000 as Vice President of Discovery Research.

Morrissey, 49, joined Exelixis in 2000 and served as Executive Vice President, Discovery, before his appointment as President of Research and Development in January 2007. He is the author of numerous scientific publications in medicinal chemistry and drug discovery and an inventor on 70 issued U.S. patents.

Morrissey represented a different kind of CEO than Scangos. He was a scientist first—a medicinal chemist who had risen through the research ranks. He knew cabozantinib intimately, having been involved in its discovery and early development. Where an outside CEO might have seen BMS's departure as a reason to pivot away from the molecule, Morrissey saw it as an opportunity.

At that time the company had eight drugs in clinical trials. But Morrissey made a calculated bet: cabozantinib was the one that mattered.

First FDA Approval: The Orphan Drug Strategy

Exelixis' first drug approval came in 2012, when cabozantinib was approved for medullary thyroid cancer, an orphan indication.

Medullary thyroid cancer affects only a few hundred patients per year in the United States. It was never going to be a commercial blockbuster. But that was precisely the point. Orphan drugs—treatments for rare diseases—receive special regulatory incentives, including faster review times, tax credits, and market exclusivity. By pursuing approval in a small indication first, Exelixis could get cabozantinib on the market, generate real-world safety data, and build infrastructure for larger opportunities ahead.

The capsule formulation, branded as Cometriq, launched with minimal commercial fanfare. The approval brought the drug from treating medullary thyroid cancer—affecting just a few hundred patients a year—to begin generating revenue. But Morrissey had bigger plans. Cabozantinib was showing promising activity across multiple tumor types. The question was which ones to prioritize with limited resources.

The company's scientists were particularly excited about prostate cancer. The drug showed dramatic effects on bone scans in early trials—in some patients, metastatic lesions seemed to disappear entirely. Cabozantinib initially generated excitement through the demonstration of dramatic bone scan activity in patients with CRPC in phase II data presented at the 2011 ASCO Annual Meeting. In the 9-arm study, complete or partial bone scan resolution was seen in 86% of patients with CRPC.

Exelixis bet big on prostate cancer. It was a potentially massive market, and the early data looked compelling. The company committed the bulk of its resources to the COMET trial program—Phase III studies that would determine whether those dramatic bone scan responses translated into longer survival.

The Near-Death Experience: The Prostate Cancer Failure (2014)

The COMET-1 Disaster

September 2, 2014, was the darkest day in Exelixis's history.

On Monday, the biotech reported that its cabozantinib--marketed in the U.S. as Cometriq for a rare type of thyroid cancer--flopped in a comparison study with prednisone for castration-resistant prostate cancer, failing to show a statistically significant increase in overall survival.

The numbers were devastating. The drug that had shown such dramatic activity in early trials—making bone metastases disappear on scans—couldn't keep patients alive any longer than a simple steroid. According to Exelixis, this reconfiguration of the company should enable it to maintain several ongoing phase III studies, specifically those focused on hepatocellular carcinoma (HCC) and renal cell carcinoma (RCC). In response to the news, Exelixis' shares fell by more than 50% in early morning trading.

The market's verdict was swift and brutal. What had been a company with a $800 million market cap was suddenly worth half that. For a clinical-stage biotech dependent on a single drug, this kind of failure typically signals the end.

"And 160 employees will pay the price. Only 70 employees will make it out of the layoff sweep, with those job cuts allowing the company to double down on late-stage clinical trials of the drug in advanced liver cancer and a form of kidney cancer, Exelixis said."

The Pivot That Saved the Company

What happened next defines the Exelixis story. Most companies facing this situation would have retreated entirely—perhaps selling the remaining assets or merging with another struggling biotech. Morrissey chose a different path.

"The workforce reduction we have announced today is necessary to significantly reduce our corporate operating expenses," CEO Michael Morrissey said in a statement.

Behind that corporate language was a stark strategic choice. Exelixis would cut everything except two bets: kidney cancer and liver cancer. Both indications had ongoing Phase III trials. Both showed promising early data. And critically, both were large enough markets to rebuild the company if the trials succeeded.

By rebuilding in an area "where they could ultimately play and win," the company focused solely on oncology, "playing the long game … and putting a stake in the ground around cancer."

The math was brutal but clear. With only 70 employees, Exelixis couldn't run multiple large clinical programs. It had to pick its battles. The phase III METEOR study is comparing cabozantinib to everolimus in patients with advanced RCC following frontline treatment with a VEGFR TKI. PFS is the primary endpoint of the study, with secondary outcome measures focused on OS and ORR.

Lessons in Capital Preservation

Morrissey's handling of the crisis offers a case study in biotech survival. Several principles stand out:

Focus beats diversification when resources are scarce. Many biotechs respond to failure by diversifying—spinning up new programs, exploring new indications. Exelixis did the opposite, concentrating everything on its two best remaining shots.

The courage to abandon sunk costs. Prostate cancer represented years of investment and effort. Walking away from it entirely was psychologically difficult but strategically necessary.

Preserve the platform. Despite the layoffs, Exelixis kept its core scientific and clinical capabilities intact. The 70 survivors included the people who would run the kidney and liver cancer programs.

For the remaining employees, the period after the layoffs was intensely focused. Everything depended on the METEOR trial readout.

The Resurrection: Kidney Cancer Breakthrough (2015–2016)

CABOMETYX Approval: The Phoenix Rises

The METEOR trial results, when they came, exceeded even optimistic expectations.

The approval of CABOMETYX is based on results of the phase 3 METEOR trial, which met its primary endpoint of improving progression-free survival. Compared with everolimus, a standard of care therapy for second-line RCC, CABOMETYX was associated with a 42 percent reduction in the rate of disease progression or death. Median progression-free survival for cabozantinib was 7.4 months versus 3.8 months for everolimus.

On April 25, 2016, the FDA approved cabozantinib (Cabometyx; Exelixis, Inc.) for the treatment of advanced renal cell carcinoma (RCC) in patients who have received prior antiangiogenic therapy.

The drug didn't just work—it worked dramatically better than the existing standard of care. A 42% reduction in disease progression was exactly the kind of differentiated clinical profile that would drive physician adoption and market share.

Two years after a failed trial and an uncertain future, Exelixis has finally turned around its misfortunes after being granted U.S. approval for cabozantinib.

The FDA previously granted Breakthrough Therapy and Fast Track designations to cabozantinib for its potential advanced RCC indication. These designations—reserved for drugs that show substantial improvement over existing treatments—signaled the FDA's view that cabozantinib represented meaningful clinical progress.

The Ipsen Partnership: Global Expansion

Exelixis had proven cabozantinib worked. But commercializing a cancer drug globally requires substantial infrastructure—sales forces, regulatory expertise in dozens of countries, established relationships with healthcare systems. Building all of that from scratch would take years and hundreds of millions of dollars.

Exelixis and Ipsen today jointly announced an exclusive licensing agreement for the commercialization and further development of cabozantinib, Exelixis' lead oncology drug. Under the agreement, Ipsen will have exclusive commercialization rights for current and potential future cabozantinib indications outside of Japan. This agreement includes rights to COMETRIQ®, which is currently approved in the European Union for the treatment of adult patients with progressive, unresectable, locally advanced or metastatic medullary thyroid cancer. The companies have agreed to collaborate on the development of cabozantinib for current and potential future indications.

Exelixis will receive $200 million upfront and is eligible to receive regulatory milestones, including $60 million upon approval of cabozantinib in Europe for advanced renal cell carcinoma and $50 million for approval in advanced hepatocellular carcinoma, as well as milestones for potential further indications.

The agreement also includes up to $545 million of potential commercial milestones and provides for Exelixis to receive tiered royalties of up to 26% on Ipsen's net sales of cabozantinib in its territories.

The strategic logic was sound: Exelixis would keep the most valuable market—the United States—while Ipsen would handle the rest of the world. The $200 million upfront provided crucial capital to rebuild. The milestone payments and royalties created long-term upside participation.

In 2016, Exelixis granted Ipsen exclusive rights for the commercialization and further clinical development of Cabometyx outside of the U.S. and Japan. In 2017, Exelixis granted exclusive rights to Takeda Pharmaceutical Company Limited for the commercialization and further clinical development of Cabometyx for all future indications in Japan.

With three partners covering different geographies—Exelixis in the U.S., Ipsen in Europe and rest-of-world, and Takeda in Japan—cabozantinib had true global reach. Exelixis had transformed from a company barely surviving to a company with a blockbuster franchise.

Building the Franchise: Label Expansions (2016–2025)

Systematic Label Expansion

The CABOMETYX story after 2016 is a masterclass in franchise building. Rather than resting on the kidney cancer approval, Exelixis methodically pursued label expansions across multiple tumor types.

In April 2016 the FDA granted approval for marketing the tablet formulation as a second line treatment for kidney cancer. In December 2017, the FDA granted approval for the use of cabozantinib for first line treatment of kidney cancer.

Moving from second-line (after other treatments have failed) to first-line (as initial treatment) dramatically expanded the addressable patient population. First-line patients are typically healthier and remain on treatment longer.

The liver cancer approval came next. The European Commission approved CABOMETYX tablets as a monotherapy for hepatocellular carcinoma in adults who have previously been treated with sorafenib. Under the terms of the Collaboration Agreement with Ipsen, Exelixis will receive a milestone payment of $40 million for the approval of the second-line treatment of HCC.

Each new approval built on the last. Physicians became familiar with CABOMETYX in kidney cancer, making them more willing to prescribe it in liver cancer. The sales force could promote across multiple indications, spreading fixed costs. The commercial engine gained momentum.

In September 2021, another milestone: The FDA approval for CABOMETYX in differentiated thyroid cancer was based on results from CABINET, which evaluated CABOMETYX compared with placebo. Final progression-free survival results were presented at the 2024 European Society for Medical Oncology Congress and published in The New England Journal of Medicine.

Then came the most recent expansion. On March 26, 2025, the Food and Drug Administration approved cabozantinib (Cabometyx, Exelixis, Inc.) for adult and pediatric patients 12 years of age and older with previously treated, unresectable, locally advanced or metastatic, well-differentiated pancreatic neuroendocrine tumors (pNET) and well-differentiated extra-pancreatic neuroendocrine tumors (epNET).

CABOMETYX is now the first and only systemic treatment that is FDA approved for previously treated neuroendocrine tumors regardless of primary tumor site, grade, somatostatin receptor expression and functional status.

Market Dominance

The label expansion strategy has yielded extraordinary market results. CABOMETYX continued to strengthen its market leadership position in renal cell carcinoma (RCC), maintaining its status as the #1 prescribed TKI+IO combination therapy with nivolumab for the eleventh consecutive quarter. The drug captured approximately 45% of the TKI market share in Q2 2025, up from 41% in Q2 2024.

In July 2018, Exelixis was added to the Standard & Poor's (S&P) MidCap 400 index, which measures the performance of profitable mid-sized companies.

From 70 employees in 2014 to S&P index membership in 2018—that transformation took less than four years.

Financial Transformation & Capital Allocation

Revenue Growth Story

The financial transformation at Exelixis has been remarkable. For the year ended December 31, 2024, net product revenues generated by the cabozantinib franchise in the U.S. were $1,809.4 million, with net product revenues of $1,798.2 million from CABOMETYX and $11.2 million from COMETRIQ.

In 2024, global cabozantinib franchise net product revenues generated by Exelixis and its partners exceeded $2.5 billion.

The Q2 2025 results showed continued momentum: Exelixis reported cabozantinib net product revenues of $520 million in Q2 2025, marking a substantial 19% year-over-year increase from $438 million in Q2 2024.

Revenue growth comes from multiple sources: price increases, volume growth in existing indications, and new indication launches. The neuroendocrine tumor approval in March 2025 is already contributing. The NET indication contributed approximately 4% to overall CABOMETYX Q2 volume, with the drug rapidly capturing approximately 35% of new patient share for second-line and beyond oral therapies in this segment.

Capital Returns

With profitability came questions about capital allocation. Biotech companies typically reinvest everything into R&D. Exelixis has taken a different approach, returning substantial capital to shareholders while still investing heavily in pipeline development.

The company continued its stock repurchase program, buying back $301.8 million worth of shares in Q2 2025 at an average price of $40.10 per share. Combined with Q1 repurchases, the company has bought back $590.6 million in shares during the first half of 2025. Since March 2023, Exelixis has repurchased approximately $1.8 billion in stock at an average price of $26.32 per share.

The buyback strategy serves multiple purposes. It returns capital when the stock looks undervalued. It signals management confidence. And it concentrates remaining shares in the hands of long-term shareholders.

The balance sheet provides flexibility. Cash and marketable securities for the year ended December 31, 2024, was approximately $1.75 billion. That cash pile—nearly $2 billion—gives Exelixis optionality for M&A, partnerships, or accelerated clinical development.

The Next Generation: Zanzalintinib & Pipeline Diversification

Building Beyond Cabozantinib

Exelixis's success with cabozantinib created a new problem: concentration risk. When one drug generates almost all of a company's revenue, any disruption—generic competition, new competitors, unexpected safety issues—becomes existential.

The company's answer is zanzalintinib (XL092), designed as a next-generation successor to cabozantinib. These receptor tyrosine kinases are involved in both normal cellular function and in pathologic processes such as oncogenesis, metastasis, tumor angiogenesis and resistance to multiple therapies, including immune checkpoint inhibitors. With zanzalintinib, Exelixis sought to build upon its extensive experience with the target profile of cabozantinib, the company's flagship medicine, while improving key characteristics, including pharmacokinetic half-life.

Exelixis has built significant momentum to establish a multi-compound multi-franchise oncology business, as we advance our cabozantinib, zanzalintinib, and early pipeline priorities to meet our aspirational revenue goals of $3 billion for cabo in 2030 and $5 billion for zanza in 2033.

Management's public commitment to a "$5 billion for zanza in 2033" target is bold. It implies that zanzalintinib can eventually surpass cabozantinib's peak revenues.

STELLAR Trial Program

The STELLAR program represents Exelixis's systematic effort to establish zanzalintinib across multiple tumor types. The first major success came in colorectal cancer.

Exelixis announced positive topline results from the STELLAR-303 phase 3 pivotal trial in which zanzalintinib in combination with atezolizumab (Tecentriq®) demonstrated a statistically significant improvement in overall survival versus regorafenib in the intent-to-treat population of patients with previously treated non-microsatellite instability-high metastatic colorectal cancer.

As previously announced, the study met one of its dual primary endpoints, demonstrating a 20% reduction in the risk of death with the combination in the intention-to-treat population at the final analysis.

Colorectal cancer represents a major commercial opportunity. The global metastatic colorectal cancer market is expected to reach $9.78 billion by 2034. Cabozantinib isn't approved in colorectal cancer, so this would be entirely incremental for Exelixis.

The STELLAR program extends beyond colorectal cancer. In July, Exelixis announced several updates to the zanzalintinib development program, including the initiation of the STELLAR-311 phase 3 pivotal trial in advanced NET. STELLAR-311 is evaluating zanzalintinib versus everolimus as a first oral therapy in patients with advanced NET, regardless of site of origin.

However, not every indication will succeed. STELLAR-305: Based on emerging phase 2 data, competitive landscape assessment, and evaluation of other potentially larger commercial opportunities, Exelixis decided not to advance this study in head and neck squamous cell carcinoma (HNSCC) to phase 3.

This discipline—willingness to kill programs that don't look promising—echoes Exelixis's response to the 2014 prostate cancer failure. Focus beats diversification.

The Patent Cliff Challenge

The elephant in the room for Exelixis investors is patent expiration. The court ruled that the '439, '440, and '015 patents, which expire on January 15, 2030, are infringed by MSN's proposed product. January 15, 2030, subject to any appeals or additional regulatory exclusivity.

Exelixis recently won a significant legal victory with the U.S. District Court affirming the validity of three patents associated with cabozantinib, effectively blocking a generic version from entering the market until at least January 2030.

The legal victories buy time, but 2030 is coming. Once generics enter, cabozantinib revenues could decline dramatically—potentially 80% or more within two years, based on typical patterns for oral oncology drugs.

Exelixis is hoping the drug will succeed cabozantinib—its current blockbuster sold under the brand names Cabometyx and Cometriq—which generated $1.8 billion in 2024. Sales are projected to rise to $2.2 billion in 2025 and peak at $2.8 billion by 2029, before generic competition begins to erode revenues following patent expiry. Analysts expect Exelixis's top line to begin declining from 2030, exposing a gap that zanzalintinib alone is unlikely to close.

This sets up the strategic challenge for Exelixis over the next five years: can zanzalintinib and other pipeline programs generate enough revenue to offset the inevitable cabozantinib decline?

Playbook: Business & Strategy Lessons

Lesson 1: The Power of the Pivot

Exelixis's 2014 restructuring offers lessons for any company facing strategic crisis:

Cut deep, cut once. Half-measures don't work in crisis. Exelixis didn't trim 20%—it cut 70%. The remaining employees knew their jobs were safe and could focus entirely on execution.

Focus on your best bets. With limited resources, you can't hedge across multiple options. Exelixis chose kidney cancer and liver cancer and put everything behind them.

Preserve institutional knowledge. The 70 survivors included the scientists and clinicians who understood cabozantinib deeply. Rebuilding would have been much harder with a fresh team.

Lesson 2: Drug Discovery Economics

The orphan drug strategy that started Exelixis's commercial journey illustrates important principles:

Small markets can be stepping stones. Medullary thyroid cancer approval provided regulatory experience, safety data, and commercial infrastructure that enabled larger launches.

Label expansion is a growth engine. Each new indication increases revenue without the full cost of developing a new drug. CABOMETYX's expansion from thyroid cancer to kidney cancer to liver cancer to neuroendocrine tumors followed this playbook.

Combination therapy extends life cycles. The CABOMETYX + nivolumab combination in first-line kidney cancer created a new revenue stream and strengthened the franchise against competitive threats.

Lesson 3: Partnership Strategy

Exelixis's approach to partnerships evolved over time:

Early partnerships reduce risk. The GSK, Genentech, and Daiichi Sankyo deals provided funding and validation while Exelixis was still unproven.

Geographic licensing preserves upside. The Ipsen and Takeda deals kept U.S. rights—the most valuable market—while monetizing international rights Exelixis couldn't efficiently exploit alone.

Know when to go it alone. After BMS returned cabozantinib rights, Exelixis chose to develop and commercialize the drug independently in the U.S. That decision, though risky at the time, created enormous value.

Lesson 4: Capital Allocation in Biotech

Exelixis's approach to capital breaks with biotech conventions:

Buybacks signal confidence. The $1.8 billion in repurchases since 2023 demonstrates management's belief that the stock is undervalued relative to the company's prospects.

Maintain strategic flexibility. The $1.75 billion cash position allows for acquisitions, partnerships, or accelerated development without dilutive financing.

Balance reinvestment with returns. Unlike many biotechs that never return capital, Exelixis balances substantial R&D spending ($925-975 million guided for 2025) with shareholder returns.

Bull and Bear Case Analysis

The Bull Case

Franchise strength. CABOMETYX's market position—45% TKI market share in kidney cancer, #1 prescribed TKI+IO combination—provides durable competitive advantages. Physicians are familiar with the drug, and switching costs exist once patients are established on treatment.

Zanzalintinib potential. The STELLAR-303 success in colorectal cancer validates the molecule's potential. If zanzalintinib achieves approvals across multiple indications, it could ultimately exceed cabozantinib revenues.

Execution track record. Management's handling of the 2014 crisis and subsequent franchise building demonstrates operational capability. CEO Morrissey has been with the company for 25 years and knows the science intimately.

Financial strength. With nearly $2 billion in cash, no debt, and strong free cash flow generation, Exelixis has resources for strategic flexibility—M&A, accelerated development, or weathering setbacks.

The Bear Case

Patent cliff concentration. Despite the franchise's current strength, 2030 represents a hard deadline. Generic entry could compress revenues rapidly, and zanzalintinib may not be large enough to fill the gap.

Pipeline execution risk. Drug development remains highly uncertain. STELLAR-305's termination in head and neck cancer shows that not every indication will succeed. Zanzalintinib's ultimate commercial potential is unproven.

Competitive pressure. The oncology market is intensely competitive. New entrants in kidney cancer, liver cancer, and colorectal cancer could erode CABOMETYX and zanzalintinib market share.

Single-product dependency. Despite label expansions, Exelixis remains fundamentally dependent on one molecule (cabozantinib) and hoping that a second molecule (zanzalintinib) can eventually take over. This concentration creates vulnerability.

Porter's Five Forces Analysis

Threat of new entrants: High. Oncology attracts massive R&D investment from both large pharma and emerging biotechs. New checkpoint inhibitor combinations, ADCs, and targeted therapies constantly threaten established positions.

Bargaining power of buyers: Moderate and increasing. Payers (insurance companies, PBMs) are becoming more aggressive about oncology drug pricing. The Inflation Reduction Act's Medicare negotiation provisions could affect future pricing power.

Bargaining power of suppliers: Low. Contract manufacturers for small molecule drugs are numerous and largely interchangeable.

Threat of substitutes: High. Cancer treatment continues to evolve rapidly. Bispecific antibodies, cell therapies, and new drug classes could potentially displace TKI-based approaches.

Industry rivalry: Intense. Major pharmaceutical companies (Merck, Bristol-Myers, Roche) and focused oncology companies compete aggressively for market share in each tumor type.

Hamilton Helmer's 7 Powers Analysis

Scale economies: Limited. Drug development costs don't decline dramatically with scale, and manufacturing efficiency gains are modest for small molecule drugs.

Network effects: None. Oncology drugs don't benefit from user network effects.

Counter-positioning: Weak. Exelixis's multi-kinase approach was once differentiated but is now well-understood and replicable.

Switching costs: Moderate. Once patients are established on treatment, physicians may be reluctant to switch, but new patients remain contested.

Branding: Limited in B2B healthcare. Physician prescribing is driven by clinical data, not brand preference.

Cornered resource: Moderate. The cabozantinib molecule and associated know-how represent proprietary assets, but patents expire and competitors can develop alternative molecules.

Process power: Moderate. Exelixis's drug discovery capabilities and clinical development expertise represent real organizational advantages, though these can be competed away over time.

Key Performance Indicators for Ongoing Monitoring

For investors tracking Exelixis, three KPIs stand out as most critical:

1. U.S. Net Product Revenue Growth Rate (Quarterly)

This is the primary measure of franchise health. CABOMETYX's ability to maintain double-digit growth despite increasing competition indicates market position durability. Q2 2025 showed 19% year-over-year growth—a healthy figure. Any sustained deceleration below mid-single digits would signal competitive challenges.

2. TKI Market Share in Renal Cell Carcinoma

Exelixis currently holds approximately 45% TKI market share in kidney cancer. This metric captures competitive dynamics directly. Share gains indicate successful commercial execution; share losses might presage revenue declines regardless of overall market growth.

3. Zanzalintinib Clinical Milestones

With 2030 approaching, zanzalintinib's clinical progress determines Exelixis's post-patent future. Key milestones include: STELLAR-304 (kidney cancer) topline results expected H1 2026; regulatory submission for colorectal cancer expected late 2025; and advancement of STELLAR-311 (neuroendocrine tumors). Each success de-risks the transition; each failure increases patent cliff vulnerability.

Regulatory and Legal Overhangs

Patent litigation: While Exelixis has won key rulings, additional challenges remain possible. Exelixis entered into a settlement agreement with Cipla. This agreement resolved two patent litigations brought by Exelixis in response to Cipla's ANDA seeking approval to market generic versions of Cabometyx tablets prior to the expiration of the applicable patents. Per the terms of the agreement, Exelixis granted Cipla a license to market generic versions of Cabometyx in the United States beginning January 1, 2031, if approved by the FDA. Similar settlements with other generic challengers could create earlier entry dates.

Drug pricing regulation: The Inflation Reduction Act's Medicare drug negotiation provisions could affect CABOMETYX pricing in coming years. Oral oncology drugs are particularly vulnerable to payer pressure.

Clinical trial risk: Zanzalintinib's development program involves multiple pivotal trials. Unexpected safety signals or efficacy failures could materially affect the company's value.

Conclusion

The Exelixis story is one of biotech's most remarkable turnarounds. From fruit fly genetics to a $10+ billion oncology company, with a near-death experience in between, the company has demonstrated extraordinary adaptability.

The 2014 crisis—cutting 70% of employees after a crushing clinical failure—tested whether the organization could survive. Not only did it survive, it rebuilt into something substantially more valuable. That rebuilding was driven by scientific persistence (the belief that cabozantinib had value despite the prostate cancer failure), strategic focus (betting everything on kidney and liver cancer), and operational excellence (building a commercial organization that captured dominant market share).

Today, Exelixis faces a different kind of challenge. The 2030 patent cliff is coming, and the company must transition from a one-drug company to a multi-franchise enterprise. Zanzalintinib represents the primary bridge to that future—but bridge construction is still underway.

The company's track record suggests it can navigate this transition. Management has navigated worse before. The scientific foundation is strong. The balance sheet provides flexibility. But execution risk remains real, and 2030 will arrive faster than anyone expects.

For long-term investors, Exelixis offers a case study in biotech resilience—and a front-row seat to watch whether that resilience can overcome the industry's most predictable challenge: the patent cliff. The next five years will determine whether the phoenix rises again.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube