Jazz Pharmaceuticals: From Near-Bankruptcy to Billion-Dollar Biotech

I. Introduction & Episode Roadmap

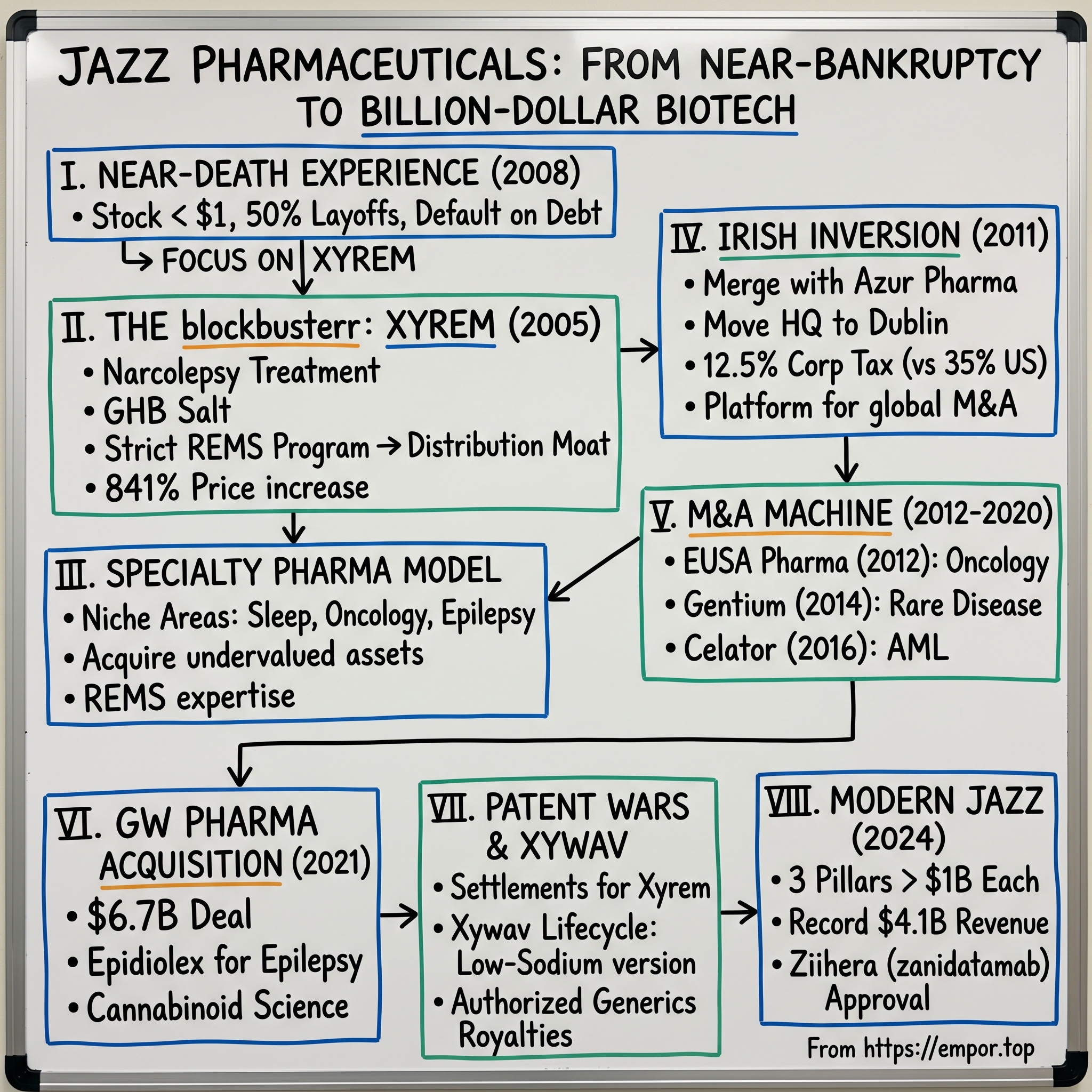

In early 2009, Bruce Cozadd sat in a conference room at Jazz Pharmaceuticals' Palo Alto headquarters, preparing to do something no CEO ever wants to do: lay off half of his workforce. The company's stock price had collapsed to 53 cents per share. Debt covenants had been breached. The specter of bankruptcy loomed over everything the team had built since founding the company just six years earlier.

What happened next would become one of the most remarkable turnaround stories in specialty pharmaceuticals.

Today, Jazz Pharmaceuticals' stock trades around $135 with a market cap of $8.23 billion. The company reported record total revenues of $4.1 billion in 2024, representing a 6% year-over-year growth. "Our diversified portfolio spanning sleep, epilepsy and oncology, with each annualizing at over $1 billion, continued to drive growth," noted Chairman Bruce Cozadd in the company's latest earnings release.

The Jazz story offers a masterclass in several dimensions of business strategy. There's the specialty pharma model—finding undervalued assets in therapeutic areas others overlooked. There's the power of a single blockbuster drug, Xyrem, and the disciplined lifecycle management that extended its franchise for two decades. There's the Irish tax inversion that positioned Jazz for global expansion. And there's the M&A engine that transformed a single-product company into a diversified biopharma leader.

Just days ago, on November 17, 2025, Jazz announced positive top-line results from the Phase 3 HERIZON-GEA-01 trial evaluating Ziihera in combination with chemotherapy for HER2-positive gastroesophageal cancer, with both treatment arms demonstrating "highly statistically significant and clinically meaningful improvements in progression-free survival." The stock surged more than 25% on the news, signaling that investors believe the next chapter may be even more compelling than the last.

But to understand where Jazz is going, we need to understand where it came from—and particularly how one drug, derived from one of the most controversial substances in medicine, built an empire.

II. The Founding Vision: Bruce Cozadd & ALZA Roots (2001-2003)

The ALZA Connection

Before Jazz Pharmaceuticals existed, there was ALZA Corporation—a pioneering drug delivery company founded by the legendary Alejandro Zaffaroni. Bruce Cozadd spent 10 years at ALZA, holding various leadership roles including Executive Vice President and Chief Operating Officer. Those years would prove formative in ways that shaped everything that followed.

At ALZA, Cozadd was profoundly influenced by the company's founder, Alejandro Zaffaroni, who instilled in him the importance of building a strong corporate culture centered around innovation, collaboration, and a patient-focused approach. Zaffaroni's mentorship played a pivotal role in shaping Cozadd's leadership philosophy.

Zaffaroni was a giant in pharmaceutical innovation—he had previously founded Syntex and would go on to found multiple other biotech companies. His philosophy was simple but radical for the time: build companies around culture first, products second. Cozadd credits the late founder of ALZA Corp. "with not only giving him his first break by hiring him at ALZA in 1991, but also for being an inspirational mentor on what it takes to become a maestro of creating a company culture that can persist through turmoil and transition."

Cozadd is himself an accomplished pianist—a detail that would later influence the company's very name. He played piano at Zaffaroni's memorial service in 2014, a fitting tribute to the man who taught him that building great companies was as much art as science.

After ALZA was acquired by Johnson & Johnson in 2001, Cozadd took some time off to focus on his family before embarking on his entrepreneurial journey. But the lessons he'd learned were already crystallizing into a vision for something new.

Founding Jazz

Jazz Pharmaceuticals was co-founded on March 5, 2003, in Palo Alto, California, by Bruce C. Cozadd, who assumed the role of chairman. Co-founder Sam Saks served as the initial CEO, allowing Cozadd to focus on building the company's infrastructure and culture.

In 2003, Cozadd co-founded Jazz Pharmaceuticals with the goal of creating a company that would not only develop innovative treatments for areas of high unmet medical need but also cultivate a culture of excellence, integrity, and a deep commitment to improving the lives of patients. He intentionally assembled a team of like-minded individuals, many of whom were former colleagues from ALZA, who shared his vision and values. Together, they defined the core principles that would guide the company's actions and decisions, emphasizing collaboration, passion, the pursuit of excellence, and a relentless drive for innovation.

The company name itself reflected this philosophy. "The first thing you notice about the company is its name. Where pharma companies often resort to obscure derivations of product names for their corporate branding, Jazz is concise, non-medical and presents easily understood connotations." For a music lover like Cozadd, it represented improvisation, collaboration, and artistry—exactly the culture he wanted to build.

Jazz Pharmaceuticals plc secured $70 million in a Series A financing round led by entities associated with KKR in 2003. KKR later led the Series B round with a $130 million investment, making it one of KKR's first ventures into biotech investing—a bet that would ultimately "make over half a billion dollars off of Jazz Pharmaceuticals."

The Specialty Pharma Model

From the beginning, Jazz pursued a distinctive strategy that set it apart from traditional biotech companies. Rather than betting everything on R&D moonshots and novel drug discovery, Jazz focused on acquiring and commercializing underappreciated drugs for niche patient populations. Cozadd, drawing from prior executive experience at ALZA Corporation, established the company with a focus on developing and commercializing therapies for unmet medical needs, particularly in neuroscience and sleep disorders.

This wasn't a lesser strategy—it was a smarter one for a company with limited resources. Find drugs that larger pharma companies overlooked or couldn't be bothered to commercialize properly. Build deep expertise in specialty markets where relationships with prescribers and patients matter more than massive sales forces. Create regulatory and distribution moats that would protect the franchise for years.

It would take an acquisition to prove the model could work—and that acquisition would change everything.

III. The Xyrem Acquisition: The Drug That Made Jazz (2005)

The Orphan Medical Acquisition

In April 2005, Jazz Pharmaceuticals and Orphan Medical, Inc. announced that they had entered into an agreement and plan of merger pursuant to which Jazz Pharmaceuticals, through a wholly owned subsidiary, would acquire Orphan Medical. Under the agreement, Orphan Medical common stockholders would receive $10.75 per share in cash upon the close of the transaction.

Jazz Pharmaceuticals added its leading drug, Xyrem, to its portfolio in 2005 with the acquisition of Orphan Medical for about $123 million. This was a great price for the then newly approved drug, which became a blockbuster.

At the time, the deal raised eyebrows. Orphan Medical was a small specialty pharmaceutical company, and Xyrem was a drug with an unusual—some would say troubling—molecular profile. But Jazz saw something others had missed.

"Orphan Medical provides Jazz Pharmaceuticals with a great platform for the launch of our commercial efforts, with an experienced specialty sales force and established relationships with neurologists and psychiatrists," the company explained. The acquisition brought not just a drug, but a commercial organization and deep expertise in a therapeutic area Jazz intended to dominate.

Understanding Narcolepsy & The GHB Challenge

Narcolepsy is a chronic neurological condition that affects how the brain regulates sleep-wake cycles. Patients experience excessive daytime sleepiness, often falling asleep at inappropriate times, and many suffer from cataplexy—sudden muscle weakness triggered by emotions like laughter or surprise. Narcolepsy affects an estimated one in 2,000 people in the United States, and more than half of narcolepsy patients report that their symptoms begin when they are teenagers or in childhood. It is estimated that 50 percent or more patients with narcolepsy have not been diagnosed.

The burden of this disease is often underestimated. For a condition associated with excessive sleepiness, narcolepsy carries a disability rate that exceeds multiple sclerosis or Parkinson's disease—a fact that surprises most people who learn it.

Xyrem is the sodium salt of gamma hydroxybutyrate (GHB). Abuse of GHB, either alone or in combination with other CNS depressants, is associated with CNS adverse reactions, including seizure, respiratory depression, decreases in the level of consciousness, coma, and death.

GHB's notoriety as a "date rape drug" created unprecedented regulatory challenges. Sodium oxybate was approved for use by the US Food and Drug Administration to treat symptoms of narcolepsy in 2002, with a strict risk evaluation and mitigation strategy (REMS) program mandated by the FDA. In 2000, GHB was placed on Schedule I of the Controlled Substances Act, but sodium oxybate, when used under an IND or NDA from the US FDA, was considered a Schedule III substance, but with Schedule I trafficking penalties. Sodium oxybate was approved by the FDA in 2002 under the brand name Xyrem with a strict risk control strategy to prevent drug diversion and control the risk of abuse.

The REMS Program: Turning Liability into Moat

What could have been Xyrem's fatal flaw—its association with a dangerous street drug—became its most powerful competitive advantage.

Because of the risks of CNS depression, abuse, and misuse, Xyrem is available only through a restricted distribution program called the Xyrem REMS Program, using the central pharmacy that is specially certified. Jazz advocated for a single-pharmacy distribution protocol in its REMS.

This wasn't just regulatory compliance—it was strategic genius. The REMS program meant that:

- Every Xyrem prescription flowed through a single specialty pharmacy, giving Jazz unprecedented visibility into its patient base

- Generic competitors would face enormous challenges replicating the distribution infrastructure

- Physician and patient relationships became stickier as the centralized system provided support services alongside medication

- The complexity created an additional barrier that standard patent protection alone could never provide

Jazz Pharmaceuticals raised the price of Xyrem 841% over time, earning $569 million in 2013 and representing more than 50% of Jazz Pharmaceutical's revenues. In 2007 it cost $2.04; by 2014 it cost $19.40 per 1-milliliter dose. While this pricing power would later create controversy and legal challenges, it demonstrated the strength of the competitive position Jazz had built.

The Xyrem acquisition transformed Jazz from a platform company in search of products into a specialty pharmaceutical company with a genuine franchise—and a playbook for building more.

IV. Near-Death Experience: The 2008 Financial Crisis

The Brink of Collapse

By late 2008, Jazz Pharmaceuticals was in crisis. The global financial meltdown had frozen credit markets, and Jazz—still burning cash as it tried to build its commercial organization and development pipeline—found itself unable to service its debt.

One of the defining moments in Jazz Pharmaceuticals' history occurred during the financial crisis of 2008, when the company faced the real possibility of bankruptcy. With a stock price hovering around 53 cents per share, negative equity, and significant debt, Cozadd and his team were forced to make difficult decisions, including laying off half of the company's workforce.

On March 31, 2009, Jazz Pharmaceuticals did not pay $5.1 million in interest due to the holders of the $119.5 million principal amount of its senior secured notes due June 2011, and Jazz Pharmaceuticals remained in default on the notes. The total overdue interest due on the notes through March 31, 2009 was $9.6 million.

Risks discussed in SEC filings included "the company's potential need to seek protection under the provisions of the U.S. Bankruptcy Code in the event of an acceleration of the senior secured notes or otherwise and the resulting risk to the stockholders' receipt of any value for their shares."

For a young company with a controversial drug and substantial debt, this was existential. Bankruptcy would likely mean the end of Jazz Pharmaceuticals as an independent company.

The Turnaround

Co-founder Sam Saks retired as Jazz CEO in 2009 and Bruce Cozadd stepped into the CEO role in April 2009. What followed was a masterclass in crisis management.

Rather than diversifying or hedging bets, Cozadd doubled down on what was working: Xyrem. The company streamlined operations, cutting non-core programs and focusing resources on commercializing its sleep franchise. "Our focus for the remainder of 2009 will be on increasing sales of our commercial products for their approved indications," Cozadd announced.

The decision was vindicated almost immediately. "I am tremendously proud of the accomplishments of the company during the second quarter. We reported product sales exceeding a $100 million annual run-rate," Cozadd noted in August 2009.

In July 2009 Jazz Pharmaceuticals raised $7.0 million in a private placement and paid $14.6 million in accrued interest to the holders of its senior secured notes. Jazz Pharmaceuticals believed that it had cured all material defaults under the agreement governing the notes.

Leadership Through Crisis

What distinguished Cozadd's handling of the crisis wasn't just the strategic decisions—it was how he managed the human dimension.

Even in these challenging circumstances, Cozadd remained steadfast in his commitment to treating employees with respect and empathy. Cozadd personally informed each affected employee and held a company-wide meeting where he acknowledged the value and talent of those who had been let go, emphasizing that their departure was not a reflection of their abilities but rather a necessary step for the company's survival. This approach not only fostered a sense of unity and resilience during a trying time but also paved the way for many employees to return to the company once it regained stability.

The early days of Jazz Pharmaceuticals were marked by both vision and adversity. The company's commitment to its mission, even in the face of financial hardship, laid the foundation for its future.

The REMS program that protected Xyrem from competition also protected Jazz during the crisis. Generic competitors couldn't simply swoop in while Jazz was weakened, and the drug's unique position as the only treatment for narcolepsy symptoms provided a floor of demand that allowed the company to work through its financial challenges.

By the end of 2009, Jazz had stabilized. The question now was how to grow from a $100 million specialty pharma company into something much larger. The answer would come from an unlikely direction: Ireland.

V. The Irish Inversion: Azur Pharma Merger (2011)

The Transaction

On September 19, 2011, Jazz Pharmaceuticals merged with Irish Azur Pharma plc to form Jazz Pharmaceuticals plc. The Azur Pharma seat in Dublin became the headquarters of the combined company.

Jazz Pharmaceuticals and Azur Pharma announced that the companies agreed to combine in an all-stock transaction that creates a specialty pharmaceutical company incorporated in Ireland with a diversified portfolio of products currently marketed in the United States. The combined company would be named Jazz Pharmaceuticals plc. Azur Pharma is a privately-held, profitable specialty pharmaceutical company headquartered in Dublin, Ireland with US operations in Philadelphia.

The company marketed ten specialty pharmaceutical products in the US in the central nervous system (CNS) and women's health areas, with expected 2011 net sales of approximately $95 to $100 million.

Upon completion of the merger, shareholders of Jazz Pharmaceuticals, Inc. would own slightly under 80 percent of Jazz Pharmaceuticals plc, and Azur Pharma shareholders would own slightly over 20 percent. Shareholders of Jazz Pharmaceuticals, Inc. would receive one ordinary share of Jazz Pharmaceuticals plc in exchange for each share of Jazz Pharmaceuticals, Inc. common stock they own at closing. The combined company is expected to have a capitalization of approximately 60 million fully diluted shares.

The Tax Inversion Strategy

The deal was structured as what would become known as a corporate "inversion"—moving the headquarters of an American company to a lower-tax jurisdiction through a merger with a foreign partner.

Jazz's board specifically noted the "tax efficient corporate structure...as an Irish tax resident." Ireland's corporate tax rate at the time was 12.5 percent compared with 35 percent in the U.S.

The 2012 deal came at the foot of a recent wave of so-called tax inversions in which U.S. companies merge with a foreign partner and reincorporate abroad to generate tax savings.

Jazz was ahead of a trend that would later encompass much larger companies—including Medtronic and attempted inversions by Pfizer—before regulatory changes made such transactions more difficult. Jazz's relocation to Ireland is an example of corporate inversion, a practice that has attracted significant negative comment at the highest levels of US government. But the company managed to stay clear of the debate. In part, that was due to its size but also, Cozadd argues, Jazz has gone much further than simply using Ireland as a convenient tax base.

Strategic Benefits Beyond Tax

The Azur merger wasn't just about taxes—it provided genuine strategic benefits.

"We are a growing, profitable specialty biopharmaceutical company with a diverse portfolio of products in the central nervous system and women's health areas," said Bruce Cozadd. "We now have a strengthened management team, a broader commercial organization and an efficient platform for further growth."

In 2011 Jazz acquired Dublin's Azur Pharma in a $500 million all-share deal that saw the company move its corporate HQ to Ireland. While Jazz's subsequent M&A activity has been ever more ambitious in scale financially, Cozadd says the Irish deal remains a game-changer, not least for the fact that it turned a largely one-product business focused solely on the US market into a group with a broader portfolio and an international outlook.

"When we merged with Azur, it had 20 staff working in Ireland," Cozadd noted. "We now have approaching 100. We also have the manufacturing plant in Athlone. If tax were the only thing we wanted, we would not be increasing headcount here or locating facilities here."

Seamus Mulligan, a founder and principal investor of Azur Pharma, joined Jazz's board and brought valuable perspective on international pharmaceutical operations and European market dynamics.

The Irish base would prove essential for Jazz's next phase: aggressive expansion through acquisition.

VI. The M&A Machine: Building Through Acquisitions (2012-2020)

EUSA Pharma (2012)

On 26 April 2012, the company acquired EUSA Pharma for $650 million (plus $50 million in milestone payments).

This acquisition extended Jazz's reach into oncology, adding Erwinaze (asparaginase Erwinia chrysanthemi) to the portfolio—a critical treatment for patients with acute lymphoblastic leukemia who develop allergies to E. coli-derived asparaginase products. More importantly, the acquisition "helped us establish our European commercial infrastructure."

Portfolio Optimization

In September 2012, the company sold its Women's Health business to Meda for $95 million.

This divestiture illustrated Jazz's disciplined approach to M&A. The company wasn't accumulating assets for the sake of growth—it was building a focused portfolio in therapeutic areas where it could develop genuine expertise and competitive advantage. Women's health didn't fit that strategy, so it was divested.

In 2012, a few months after completing the Azur deal, Jazz acquired Eusa Pharmaceuticals for $700 million, followed by Italian group Gentium in a $1 billion move in late 2013.

Gentium & Celator Acquisitions

In January 2014, the company announced it would acquire the rare disease drug developer Gentium SpA and its lead product Defitelio for $1 billion. This acquisition added Defitelio (defibrotide) to Jazz's product portfolio and enabled the European commercial launch.

At the end of May 2016, the company announced its largest acquisition to date, with the purchase of Celator Pharmaceuticals for $1.5 billion. As a result, Jazz obtained the rights to breakthrough therapy Vyxeos (liposomal daunorubicin and cytarabine) for treatment of acute myeloid leukemia.

The Xywav Development Story

While Jazz was building through acquisitions, it was also innovating internally—and the Xywav story represents one of the best examples of lifecycle management in recent pharmaceutical history.

"We have been working for nearly a decade to develop Xywav, a unique oxybate product with a significant reduction in sodium. We are proud to advance the science behind our sleep research program in order to continue making a difference for people living with narcolepsy," said Bruce Cozadd in 2020.

The U.S. Food and Drug Administration approved Xywav (calcium, magnesium, potassium, and sodium oxybates) oral solution on July 21, 2020 for the treatment of cataplexy or excessive daytime sleepiness in patients 7 years of age and older with narcolepsy. Xywav is an oxybate product with a unique composition of cations resulting in 92 percent less sodium—or approximately 1,000 to 1,500 mg/night—than sodium oxybate at the recommended dosage range.

Xywav was the first FDA approved new treatment option indicated for both cataplexy and excessive daytime sleepiness in people living with narcolepsy in more than 15 years.

The clinical rationale was elegant. Xyrem contains 109% of the American Heart Association's recommended daily allowance for sodium intake. Given that narcolepsy is a chronic condition requiring lifelong treatment, the cumulative cardiovascular effects of that sodium load were concerning. Xywav addressed this directly while maintaining the therapeutic efficacy.

The seven-year market exclusivity for Xywav began on July 21, 2020, the date of FDA approval. This meant that even as generic competition threatened original Xyrem, Jazz had a protected follow-on product to which patients could transition—the textbook example of franchise lifecycle management.

In August 2021, Xywav became the first and only FDA-approved treatment for idiopathic hypersomnia, expanding the drug's addressable market significantly beyond narcolepsy.

VII. The GW Pharmaceuticals Blockbuster: Epidiolex & Cannabinoid Science (2021)

The Transformative Acquisition

On May 5, 2021, Jazz Pharmaceuticals announced the completion of its acquisition of GW Pharmaceuticals plc, a leader in the science, development and commercialization of cannabinoid-based prescription medicines.

Jazz acquired GW for $220.00 per American Depositary Share, for a total of $6.7 billion net of GW cash. Jazz agreed to pony up $7.2 billion for cannabinoid hotshot GW Pharmaceuticals, whose epilepsy med Epidiolex could be on its way to blockbuster sales.

This was by far Jazz's largest deal ever—a bet that would either validate the company's M&A strategy or burden it with unmanageable debt.

Why Epidiolex

Epidiolex (cannabidiol) oral solution is a transformative treatment for childhood-onset epilepsy that provides a critical therapeutic option for refractory seizures.

Epidiolex was approved by the US FDA in 2018 after extensive clinical trials and was the first approved cannabis-based medicine which only contained CBD. For patients with severe forms of epilepsy—Lennox-Gastaut syndrome, Dravet syndrome, and seizures associated with tuberous sclerosis complex—who hadn't responded to other treatments, Epidiolex offered hope.

The transaction enhances product diversification through the addition of a third high-growth commercial franchise for critical unmet patient needs within: 1) sleep disorders, 2) oncology, and 3) epilepsies. Specifically, the acquisition will expand Jazz's growing neuroscience business by adding Epidiolex, a global, high-growth childhood-onset epilepsy franchise with near-term blockbuster potential.

Strategic Rationale

"The addition of GW further diversifies our commercial portfolio and innovative pipeline with therapies that are complementary to our existing business, including Epidiolex, a high-growth commercial product with near-term blockbuster potential. We are fortunate to be combining two companies that share a passion for, and track record of, developing differentiated therapies that advance science and the care of patients with often-overlooked diseases."

The deal also brought GW's cannabinoid science platform—capabilities in cultivation, extraction, formulation, and regulatory management that could enable future product development in this emerging therapeutic area.

Jazz raised $5.35 billion of financing to fund the GW transaction. The financing structure supports the Company's plans for rapid deleveraging to its stated targets while also continuing to make investments to grow the business.

The commitment to rapid deleveraging would prove important. Jazz took on substantial debt to fund the acquisition, but the company's strong cash flows from its existing franchises would allow it to pay down that debt faster than many analysts expected.

VIII. Patent Wars & The Generic Threat

The Xyrem Antitrust Battles

Jazz's success with Xyrem eventually attracted unwanted attention—not just from generic competitors, but from regulators and plaintiffs' attorneys.

Jazz agreed to pay $145 million to settle lawsuits claiming it illegally acted to prevent generic versions of its narcolepsy therapy Xyrem from entering the US market. The lawsuits—which date back to 2020 in some cases—claimed that Jazz entered into a series of "reverse payment" agreements—sometimes referred to as "pay-for-delay" deals—designed to extend its monopoly by blocking access to more affordable generic drugs.

Early in 2025, the company inked a settlement agreement with a group of indirect purchaser plaintiffs who took the company to court over an alleged "pay-for-delay" arrangement to thwart generic competition to Xyrem. In 2020, the allegations were consolidated into a multidistrict litigation (MDL) case.

Jazz and Hikma came to a patent settlement in 2017, ending a yearslong dispute between the two. The terms of the settlement stipulated that Hikma would be allowed to market an "authorized generic" version of Xyrem through Jazz's restricted distribution program. As part of that deal, Hikma agreed to pay Jazz a "meaningful royalty" on net sales.

Jazz plans to pay the settlement in a lump sum using cash on hand, but it continues to deny all alleged wrongdoing and "remains confident" in its defenses.

The Xywav Transition Strategy

The genius of Jazz's lifecycle strategy becomes clear when examining how revenue transitioned from Xyrem to Xywav and the authorized generics.

While sales on the branded medicine dropped by 59% to $233.8 million last year amid the authorized generic launches, the company's royalties associated with the copycats grew significantly to $217.6 million. Meanwhile, Jazz also has a newer low-sodium version of the drug called Xywav. That drug pulled down a whopping $1.47 billion last year, an increase of 16% from the prior year.

This three-pronged approach—royalties from authorized generics, continued branded Xyrem sales to patients who prefer it, and growth from the patent-protected Xywav franchise—demonstrates how thoughtful lifecycle management can extend a drug's commercial life far beyond its original patents.

Xywav received orphan drug exclusivity in December 2021, extending protection until approximately July 2028 for cataplexy or EDS in patients aged 7 and older.

Regulatory Moats

The REMS program remains a key competitive advantage. Because of the risks of central nervous system depression and abuse and misuse, Xywav is available only through a restricted program under a Risk Evaluation and Mitigation Strategy (REMS) called the XYWAV and XYREM REMS.

In January 2017, the FDA approved the first generic sodium oxybate product for narcolepsy symptoms, which is also subject to the same REMS program conditions as the original. This means generic competitors must build the same complex distribution infrastructure Jazz operates—a significant barrier that has limited competition even after patent expiry.

IX. The Modern Jazz: Current Portfolio & Pipeline (2024-2025)

Three Pillars Over $1 Billion Each

Jazz reported record total revenues of $4.1 billion in 2024 and $1.1 billion in Q4 2024. More impressively, the company has achieved true portfolio diversification:

"2024 was another strong year as our proven team delivered significant top- and bottom-line growth along with record total revenues of over $4 billion. Our diversified portfolio spanning sleep, epilepsy and oncology, with each annualizing at over $1 billion, continued to drive growth."

Xywav net product sales increased 16% to $1.47 billion in 2024, with approximately 14,150 active patients by Q4 end.

Epidiolex/Epidyolex also grew 15% in 2024 to $972 million in sales.

Oncology revenues grew 9% year-over-year in 2024, surpassing $1.1 billion.

Key Growth Drivers

The FDA granted accelerated approval of Ziihera (zanidatamab-hrii) on November 20, 2024, for the treatment of adults with previously treated, unresectable or metastatic HER2-positive (IHC 3+) biliary tract cancer. Ziihera was approved based on a 52% objective response rate and a median duration of response of 14.9 months.

On November 17, 2025, Jazz announced positive top-line results from the Phase 3 HERIZON-GEA-01 trial evaluating Ziihera in combination with chemotherapy, with or without the PD-1 inhibitor Tevimbra, as first-line treatment for HER2-positive locally advanced or metastatic gastroesophageal adenocarcinoma. Both Ziihera plus chemotherapy and Ziihera plus tislelizumab and chemotherapy demonstrated highly statistically significant and clinically meaningful improvements in progression-free survival compared to the control arm.

"Based on the positive results seen in the HERIZON-GEA-01 trial, the zanidatamab plus chemotherapy combination, with and without tislelizumab, has the potential to become the new standard of care for patients in HER2+ first-line locally advanced unresectable or metastatic GEA. This is the first Phase 3 trial to demonstrate a benefit for a novel HER2-targeted therapy compared to trastuzumab as part of a combination regimen in HER2+ first-line GEA."

At the time of the original approval, then-CEO Bruce Cozadd told Fierce Pharma that Jazz believed the drug could generate more than $2 billion in peak sales.

Financial Strength

As of December 31, 2024, cash, cash equivalents and investments were $3.0 billion, and the outstanding principal balance of the Company's long-term debt was $6.2 billion. For the year ended December 31, 2024, the Company generated $1.4 billion of cash from operations reflecting strong business performance and continued financial discipline.

For 2025, Jazz provided revenue guidance of $4.15-$4.40 billion, representing 5% growth at the midpoint.

In January 2025, the Company made a voluntary prepayment of $750.0 million principal amount on the Term Loan B, demonstrating commitment to deleveraging ahead of schedule.

X. Leadership Transition: The Cozadd Era Ends

CEO Succession

After more than two decades building Jazz Pharmaceuticals from a startup to a multi-billion dollar enterprise, Bruce Cozadd announced his intention to step back from day-to-day leadership.

On July 10, 2025, Jazz announced that the Jazz Board of Directors had unanimously selected Renee Gala, Jazz's President and Chief Operating Officer, as the President and Chief Executive Officer, effective August 11, 2025. She will succeed co-founder, Chairperson and CEO Bruce Cozadd, who informed the Board in December 2024 of his intent to retire as CEO upon the identification of the Company's next leader.

Ms. Gala was promoted to the role of President and COO in October 2023, after having served as Executive Vice President and Chief Financial Officer of the Company since March 2020. She brings more than 30 years of experience across finance, strategy, corporate development and commercialization.

Gala has played a critical role in driving Jazz's ongoing transformation, including architecting a business development strategy that has diversified the Company's portfolio, driven total revenue growth of nearly 90%, built broad capabilities, and established a pipeline that has positioned the Company for value creation and sustainable growth.

The Legacy

Mr. Cozadd will continue to serve as Chairperson of the Board, providing strategic input as the Company continues to execute on its growth strategy.

"From the beginning, our mission has been to work tirelessly to transform patient lives," said Mr. Cozadd. "We have since grown into an innovative biopharma company with expanded commercial and scientific capabilities to drive the next phase of our evolution, and a value rich pipeline poised to reach even more patients than we ever thought possible. I am thrilled to be handing over the reins to Renee and am excited for her to lead Jazz into our next phase of growth."

Cozadd, who co-founded Jazz 22 years ago, expressed confidence in his successor, noting Gala's leadership has been "critical in Jazz's transformation into a high-growth biopharmaceutical company."

The transition from founder-CEO to professional management is a critical moment for any company. Jazz appears to have executed it thoughtfully, with Gala having been groomed for the role through progressively larger responsibilities and Cozadd remaining as Chairman to ensure continuity.

XI. Playbook: Business & Investing Lessons

The Specialty Pharma Model

Jazz's success offers several lessons for investors and executives:

Finding Undervalued Assets: The Xyrem acquisition perfectly illustrates the specialty pharma opportunity. Larger companies overlooked or undervalued a drug with genuine clinical utility because of its regulatory complexity. Jazz saw past the challenges to the opportunity.

Commercial Excellence Before Scale: Jazz built deep expertise in sleep medicine before expanding into oncology and epilepsy. Each therapeutic area received dedicated attention, not just product licensing.

Turning Constraints Into Advantages: The REMS program requirements that many would view as burdens became Jazz's most durable competitive moat.

M&A as a Core Competency

"While Jazz's subsequent M&A activity has been ever more ambitious in scale financially, Cozadd says the Irish deal remains a game-changer, not least for the fact that it turned a largely one-product business focused solely on the US market into a group with a broader portfolio and an international outlook."

Jazz's M&A approach follows consistent principles: - Acquire products in specialty areas where Jazz has or can build commercial expertise - Focus on high unmet need conditions where smaller patient populations support premium pricing - Prioritize products with regulatory or distribution moats - Divest non-core assets quickly (the Women's Health sale to Meda)

Lifecycle Management

The Xyrem-to-Xywav transition represents a textbook case of franchise extension:

- Identify a genuine clinical improvement (lower sodium content for chronic use)

- Invest in the clinical development to prove the benefit

- Time the approval to provide overlap with original patent protection

- Ensure distribution infrastructure advantages carry forward

- Negotiate authorized generic arrangements that capture value even from competition

Regulatory Moats

The REMS program demonstrates that regulatory complexity can be a source of competitive advantage, not just cost: - Centralized distribution creates barriers generic competitors must replicate - Patient and prescriber enrollment creates switching costs - The program provides valuable data on patient outcomes and usage patterns - Complexity discourages less committed competitors

Culture in Crisis

"I was lucky enough to work at a company with an exceptional culture and equally successful business, and I wanted to replicate that. So I helped found a company focused on creating an environment in which top talent can do their best and work inclusively as a team."

The way Cozadd handled the 2008-2009 crisis—personally communicating with affected employees, maintaining respect and dignity throughout the layoffs—built loyalty that paid dividends for years afterward.

XII. Analysis: Porter's Five Forces & Hamilton's Seven Powers

Porter's Five Forces Analysis

1. Threat of New Entrants: LOW

The barriers to entering Jazz's core markets are substantial: - FDA approvals require years of clinical development and hundreds of millions in investment - REMS programs require complex distribution infrastructure that takes years to build - Controlled substance designations add regulatory layers that deter many competitors - Orphan drug exclusivity provides additional protection in key indications - Specialty commercial capabilities for rare diseases aren't easily replicated

2. Bargaining Power of Suppliers: MODERATE

Jazz faces typical pharmaceutical supply chain dynamics: - Active pharmaceutical ingredient suppliers have some leverage, particularly for controlled substances with complex manufacturing - The GW acquisition brought in-house capabilities for cannabinoid cultivation and extraction - Manufacturing facilities in Ireland, England, and Italy provide some vertical integration - Single-source dependencies remain a risk for certain products

3. Bargaining Power of Buyers: MODERATE-HIGH

The U.S. healthcare payment landscape creates significant buyer pressure: - Pharmacy Benefit Manager (PBM) consolidation concentrates purchasing power - Government payers (Medicare/Medicaid) exert pricing pressure - Specialty pharmacy distribution for controlled substances limits channels - However, orphan drug designation and limited alternatives provide some protection - The REMS programs create direct relationships with patients that bypass some PBM influence

4. Threat of Substitutes: MODERATE

Competition varies by therapeutic area: - In narcolepsy, Xyrem/Xywav remain the leading oxybate therapies, though Avadel's Lumryz, approved in May 2023, offers once-nightly dosing - Epidiolex as the first FDA-approved cannabidiol provides unique positioning in severe epilepsy - New mechanisms of action (orexin agonists) could eventually disrupt the sleep franchise - In oncology, Jazz competes in fragmented markets where multiple treatment options exist

5. Competitive Rivalry: MODERATE

Jazz competes differently in each therapeutic area: "One of Jazz Pharmaceuticals's 20 competitors is Gilead, a Formerly VC-backed company based in Foster City, CA." - In specialty sleep medicine, competition is limited but intensifying - In epilepsy, Jazz competes with established anti-epileptic drugs - In oncology, competition is fierce with multiple large and small players

Hamilton's Seven Powers Analysis

1. Scale Economies: MODERATE

Jazz leverages commercial infrastructure across its neuroscience and oncology portfolios. The same specialty sales representatives who discuss Xywav can also promote Epidiolex. Fixed costs of the REMS distribution system are spread across growing patient volumes.

2. Network Economics: LOW-MODERATE

The REMS distribution system creates some network effects—as more patients enroll, the infrastructure becomes more valuable and harder to replicate. However, these are weaker than true network businesses.

3. Counter-Positioning: HIGH

Jazz's specialty pharma model represents counter-positioning against big pharma. Large companies are structurally unable or unwilling to focus on the small patient populations and regulatory complexity that Jazz embraces. Their commercial organizations, cost structures, and growth requirements make Jazz's markets unattractive.

4. Switching Costs: HIGH

For patients on chronic therapies like Xywav or Epidiolex, switching costs are substantial: - Physician relationships and familiarity with dosing - Patient enrollment in REMS programs - Risk of symptom recurrence during transitions - Insurance authorization for new medications

5. Branding: MODERATE

Jazz has strong brand recognition in sleep medicine through decades of Xyrem commercialization. The "Jazz Pharma" name carries weight with neurologists and sleep specialists. However, pharmaceutical branding is generally weaker than consumer branding.

6. Cornered Resource: HIGH

Jazz's most valuable cornered resources are: - The REMS infrastructure and expertise for controlled substance distribution - Deep relationships with the narcolepsy treatment community built over two decades - GW's cannabinoid science platform and cultivation capabilities - The zanidatamab license from Zymeworks

7. Process Power: MODERATE-HIGH

Jazz has developed distinctive capabilities in: - Lifecycle management (the Xyrem-to-Xywav transition) - Specialty pharma M&A integration - REMS program management and compliance - Commercial execution in rare disease markets

Key Performance Indicators for Investors

For long-term investors tracking Jazz Pharmaceuticals, two metrics matter most:

1. Xywav Active Patient Count Growth

Approximately 14,150 active Xywav patients by Q4 2024 end represents the core of Jazz's sleep franchise. This metric reflects: - Conversion success from Xyrem to Xywav - New patient starts in narcolepsy - Expansion into idiopathic hypersomnia - Competitive dynamics with Avadel's Lumryz

Quarterly net patient additions should trend positive. Any sustained decline would signal competitive or commercial execution issues.

2. Key Growth Driver Combined Revenue Growth Rate

The combined 15% year-over-year revenue increase from key growth drivers (Xywav, Epidiolex and Rylaze) demonstrates portfolio strength beyond the original Xyrem franchise. This metric captures: - Epidiolex's progress toward blockbuster status - Xywav's continued adoption - Oncology franchise expansion (now including Ziihera)

Double-digit combined growth suggests the post-Xyrem transition is succeeding. Deceleration to single digits before oncology products mature would be concerning.

Myth vs. Reality

| Consensus Narrative | Reality |

|---|---|

| "Jazz is just a Xyrem company" | Each of Jazz's three portfolios—sleep, epilepsy, and oncology—now annualizes at over $1 billion. Xyrem/Xywav remains important but diversification is real. |

| "Generic competition will devastate Jazz" | The authorized generic strategy and royalty arrangements mean Jazz captures value even from competition. Royalties from generics grew to $217.6 million in 2024. |

| "The Irish headquarters is just a tax play" | "We have the manufacturing plant in Athlone. If tax were the only thing we wanted, we would not be increasing headcount here or locating facilities here." |

| "GW was an overpay at $7.2B" | Epidiolex is approaching blockbuster status with $972M in 2024 sales and continued double-digit growth. |

Material Risks & Regulatory Considerations

Legal Overhangs: Not included in the 2025 settlement class are bigger insurance companies including UnitedHealthcare, Blue Cross Blue Shield and Humana. Additional antitrust litigation remains possible. Jazz also agreed to pay $90 million to Avadel to settle US antitrust claims.

Pipeline Setbacks: "We are disappointed that the trial did not meet its primary endpoint," Jazz stated regarding suvecaltamide's Phase 2b failure in essential tremor. Not all pipeline bets will succeed.

Debt Levels: With $6.2 billion in long-term debt, Jazz carries substantial leverage from the GW acquisition. Strong cash flows provide coverage, but rising interest rates increase costs.

Concentration Risk: While improved, significant revenue still depends on the oxybate franchise and a limited number of products.

CEO Transition: Leadership transitions carry execution risk. Gala's track record is strong, but the proof comes in continued performance.

Conclusion

Jazz Pharmaceuticals' journey from a 53-cent stock price on the brink of bankruptcy to a $4+ billion revenue enterprise stands as one of the most remarkable turnarounds in specialty pharmaceutical history. The company's success rests on a distinctive model: find undervalued drugs in therapeutic areas others overlook, build commercial expertise that creates lasting advantages, use M&A to expand while maintaining focus, and manage product lifecycles to extend value far beyond original patent protection.

"We have since grown into an innovative biopharma company with expanded commercial and scientific capabilities to drive the next phase of our evolution," Cozadd noted in passing the CEO role to Gala.

The next chapter will test whether Jazz can replicate its success in new therapeutic areas. The Ziihera results in gastroesophageal cancer suggest the oncology franchise could become as significant as sleep medicine. The cannabinoid science platform from GW remains largely untapped beyond Epidiolex.

For investors, Jazz offers a case study in what disciplined specialty pharmaceutical execution looks like—and the potential returns when a company gets the model right. The 2008-2009 near-death experience forged a culture of resilience and focus that continues to define the company today. Whether that culture persists under new leadership will determine whether Jazz's next twenty years match its first.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube