Tenaris: The Pipe Empire That Built the Energy Industry

The Rocca Dynasty & Techint Origins

Agostino Rocca: The Visionary Founder

Agostino Rocca was born in 1895 in Milan. His family relocated to Rome early in his childhood, and he completed secondary school studies at the Collegio Militare di Roma. He enrolled at the Accademia Militare di Torino in 1913, but left to enroll in the Italian Army at the outset of World War I, where he saw combat against Austro-Hungarian forces. Following the war, he enrolled in the Politecnico di Milano in 1921 to study engineering.

After graduating, Rocca began as an engineering apprentice at Dalmine, a steel maker, in 1923. He later became a financial advisor, and worked for a number of prominent Italian firms, mainly in the manufacturing sector. He was made part of the Istituto per la Ricostruzione Industriale (IRI), the centerpiece of the Mussolini regime's corporate state.

After working in steel and engineering firms, he joined Mussolini's government in the wake of the Great Depression to help oversee the reconstruction of Italy's industry. His role shoring up companies and rejiggering them as defense contractors during the 1930s earned him the title of "inventor of Italy's steel industry," according to Italian newspaper Corriere della Sera. He broke with Mussolini before the end of World War II.

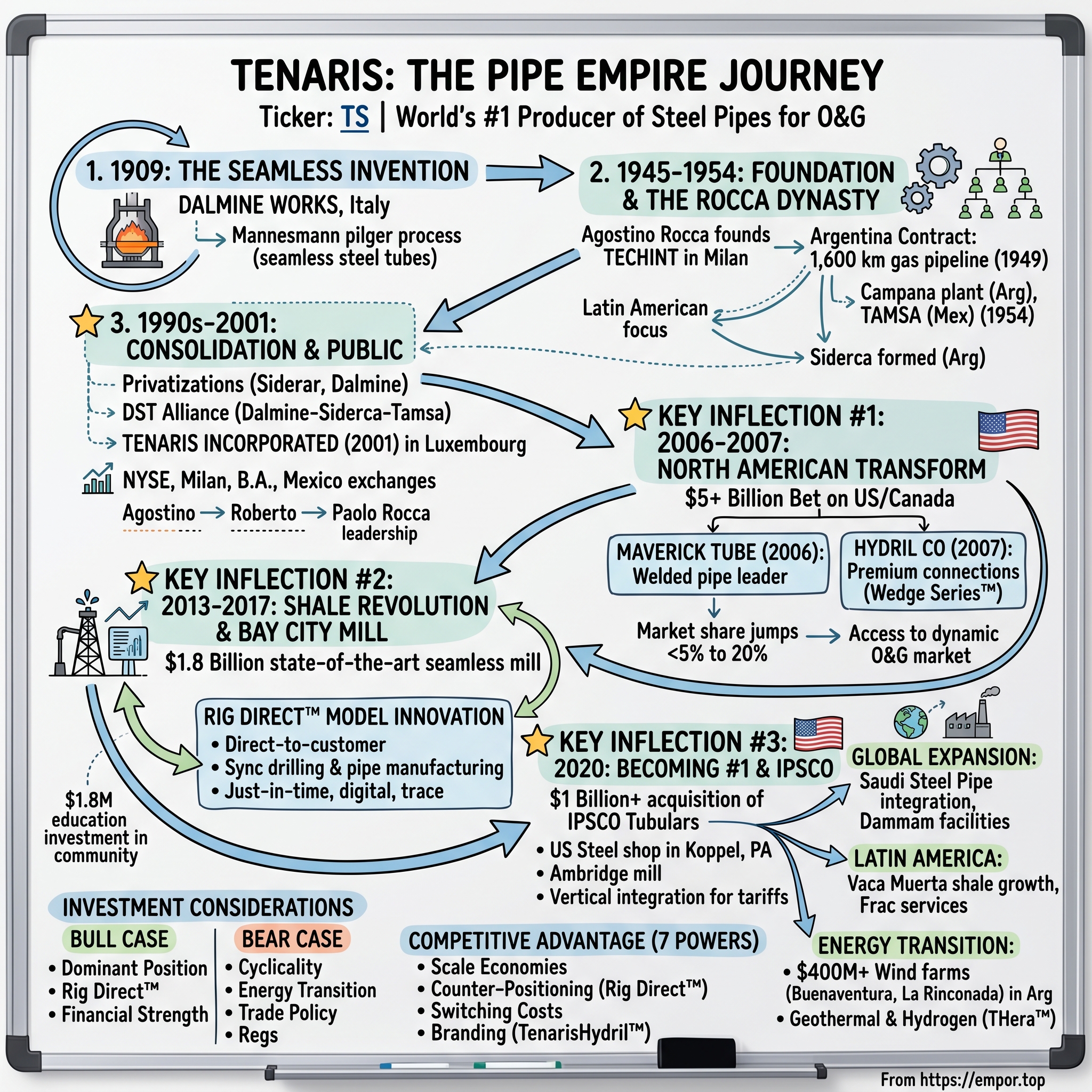

This experience at the commanding heights of Italian industry gave Rocca something invaluable: a deep understanding of how to build and restructure heavy industrial enterprises. He founded Techint in Milan in 1945 to bid for engineering contracts around the world. Founded in Milan, Rocca's fledgling company was renamed as Techint, its abbreviated telex code.

The Argentina Connection

The question of why an Italian industrialist would relocate to Argentina post-World War II reveals the strategic thinking that would define the Rocca family for generations. Argentina in the mid-1940s was experiencing an industrial boom under the nationalist policies of Juan Perón, who was determined to modernize the country's infrastructure. Rocca saw opportunity where others saw risk.

Awarded a contract to build a 1,600 km gas pipeline from Comodoro Rivadavia to Buenos Aires in 1949 by President Juan Perón, Techint became a leading government contractor during Perón's ambitious infrastructure program.

This single pipeline contract proved transformative. It established Techint as a major player in Latin American infrastructure and generated the capital and expertise that would fuel decades of expansion. Establishing subsidiaries in Brazil (1947), Chile (1951), and Mexico (1954), the company purchased a majority stake in Dalmine (Rocca's erstwhile employer), in 1954, and opened its first seamless steel tube plant in Campana, the same year.

The Campana plant, located outside Buenos Aires, would become the heart of the Rocca industrial empire. Together with the Tamsa facility in Veracruz, Mexico—also commissioned in 1954—these two plants established Techint as a serious player in seamless steel tube manufacturing for the nascent oil and gas industry.

The Techint Group Structure

Techint Group is a multinational conglomerate specializing in steel production, energy, engineering and construction, mining technologies, and healthcare, with operations spanning over 45 countries and employing approximately 89,000 people worldwide. Founded in 1945 by Italian engineer Agostino Rocca as "Compagnia Tecnica Internazionale" (Techint), the group initially focused on providing engineering services in Europe and Latin America before expanding into diverse industrial sectors.

Today, the group's structure reflects decades of strategic diversification. The family-owned business controls two publicly traded steel units, Tenaris and Ternium, as well as closely held oil producer Tecpetrol, industrial-machinery maker Tenova, contractor Techint Engineering & Construction and hospital operator Humanitas.

Understanding the ownership structure is crucial for investors. The company is 60.45% owned by Techint, which is controlled by San Faustin S.A., which is in turn controlled by Rocca & Partners Stichting Administratiekantoor Aandelen San Faustin, a Stichting, while 38.41% of the company is publicly traded. This structure gives the Rocca family effective control over strategic decisions while providing public shareholders with exposure to one of the world's premier industrial franchises.

The aging industrialist transferred management of the company to his elder son, Roberto Rocca, in 1975, and died in Buenos Aires on February 17, 1978, at age 83. Techint was, by then, a conglomerate with 15,000 employees, two steel manufacturing facilities in Argentina and with international engineering and construction interests.

Building the Foundation: Siderca, Tamsa & Dalmine

The Original Steel Pipe Assets

The technical heritage of Tenaris originated with the establishment of seamless steel pipe manufacturing at the Dalmine mill in Italy in 1909, marking one of the earliest industrial applications of the Mannesmann pilger process for producing tubes without welds. This technology—licensed from the German Mannesmann Tube Company—enabled the creation of high-strength pipes suitable for emerging pressure-intensive applications like gas transport and early oilfield use, surpassing the limitations of riveted or welded alternatives.

Tenaris traces its roots to the formation of Siderca, the sole Argentine producer of seamless steel pipe products by the predecessor of San Faustin in 1948. This facility in Campana, combined with the Tamsa plant in Mexico, formed the backbone of the Techint Group's steel tube operations.

The decision to build twin facilities in Argentina and Mexico was strategically brilliant. Both countries had growing oil industries, both offered favorable government relations, and both provided access to distinct regional markets. This geographic diversification would prove valuable during countless political and economic disruptions over the following decades.

The Technology Advantage: Seamless vs. Welded

For investors unfamiliar with steel pipe technology, the distinction between seamless and welded pipes matters enormously. Seamless pipes are produced by heating a solid steel billet and piercing it to create a hollow tube—a process that eliminates the potential weak point created by a welded seam. For high-pressure applications like oil and gas extraction, where pipes must withstand enormous downhole pressures and corrosive environments, seamless construction offers critical advantages in reliability and safety.

This technological focus shaped the Rocca family's strategy for decades. Rather than compete across all pipe categories, they concentrated on the highest-value, most technically demanding applications—a classic focus strategy that would generate superior margins.

The Latin American Expansion Strategy

Buffeted by problems in the Argentine economy during the 1980s, Techint expanded its Latin American activities. Techint participated in the privatization drive adopted by President Carlos Menem in the early 1990s, purchasing a majority stake in Argentina's then-leading steel manufacturer, the state-owned Somisa, in 1992.

The Somisa acquisition was transformative. Rocca converted Somisa into Siderar, and integrated Techint's cold rolled steel operations into Siderca. Between 1992 and 1996 Siderar raised its share of domestic consumption of flat steel from about 56 percent to about 79 percent. This demonstrated the Rocca family's ability to acquire underperforming state assets and dramatically improve their operational efficiency—a playbook they would apply repeatedly.

The 1990s saw rapid geographic expansion. The company acquired controlling interests across Latin America and Europe, including the privatized Dalmine in Italy in 1996. By the end of the decade, Tenaris traces its roots to the formation of Siderca, the sole Argentine producer of seamless steel pipe products by the predecessor of San Faustin in 1948. but had grown into a genuine multinational with significant operations across three continents.

The DST Alliance & Birth of Tenaris (2001-2002)

Creating the Global Platform

By the late 1990s, the Techint steel pipe operations had grown organically and through acquisition, but they operated as separate entities with different ownership structures, trading independently and sometimes competing with each other. The creation of a unified global platform would unlock significant strategic and operational synergies.

The strategic alliance that became DST (Dalmine-Siderca-Tamsa) represented the first step toward integration. Tenaris was organized on December 17, 2001. The timing was terrible—the Argentine economy was collapsing, oil prices were volatile, and global capital markets were still reeling from the dot-com bust.

But Paolo Rocca, who had assumed leadership following his brother Agostino's tragic death in a 2001 plane crash, pressed forward. Agostino's brother, Paolo, was an assistant to the Executive Director of the World Bank before joining the Techint Group in 1985. Paolo became the company's CEO in 2002 after the tragic 2001 plane crash that killed Agostino.

Why Luxembourg?

The decision to incorporate Tenaris in Luxembourg reflected sophisticated financial engineering. Luxembourg offered tax efficiency for a holding company structure, favorable treaty networks, and access to global capital markets. The company simultaneously listed on the New York, Milan, Buenos Aires, and Mexico City stock exchanges—an unusual approach that reflected its genuinely multinational character.

The Consolidation Challenge

The formal creation of Tenaris was only the beginning. Though Techint had united its steel pipe operations under the new brand, ownership remained fragmented. The early 2000s saw intensive efforts to consolidate minority shareholdings and create a cleaner corporate structure.

The family was shaken by the April 28, 2001, aviation death of Agostino Rocca, president of Techint and Roberto Rocca's successor. Agostino's younger brother, Paolo Rocca, was appointed to the post. Subsequently, Siderca was listed on the NYSE, and Techint's steel operations, the group's centerpiece, were reorganized as Tenaris in October 2002, basing the subsidiary in Luxembourg and converting Techint into a holding company.

Roberto Rocca was elected the first chairman of Tenaris, but died in his native Milan, on June 10, 2003, at the age of 81. With his passing, the second generation of Rocca leadership ended, and the company's future rested entirely on Paolo's shoulders.

The North American Transformation: Maverick & Hydril (2006-2007)

⭐ KEY INFLECTION POINT #1

The $5+ Billion Bet on America

In the mid-2000s, Tenaris faced a strategic problem. Despite its global reach, the company had minimal presence in the world's largest and most dynamic oil country tubular goods market: the United States and Canada. North American shale drilling was accelerating, deepwater Gulf of Mexico exploration was booming, and Tenaris was watching from the sidelines with less than 5% market share.

Tenaris was virtually unheard of in Texas until a decade ago when it bought St. Louis-based Maverick Tube Corp. and Houston-based Hydril Co. for a combined $5 billion. In short order, Tenaris grew from about 50 Houston employees to more than 2,000.

This wasn't incremental expansion—it was a transformational bet on America.

The Maverick Acquisition (2006)

In June 2006, the company acquired Maverick Tube for $3.185 billion. Valued at US$3,185 million, the transaction also includes Maverick's net debt. The share price represents a premium of approximately 42% to Maverick's closing share price of June 12, 2006, and a premium of approximately 24% to its 90-day average trading price.

Tenaris Chairman and CEO Paolo Rocca commented, "This is a major step for Tenaris. With Maverick, we will gain full access to the energy sector in the United States and Canada. We will be able to support the growing requirements of our customers in the full range of applications from onshore shallow wells to extremely demanding deepwater wells in the Gulf of Mexico."

Maverick is a leading North American producer of welded oil country tubular goods (OCTG), line pipe and coiled tubing for use in oil and gas wells. With operations in the United States, Canada and Colombia, it has a combined annual capacity of two million short tons of steel pipes with a size range from one-quarter inch to 16 inches. Maverick has approximately 4,650 employees and in 2005 had sales of US$1.8 billion, of which 82% were from its energy products division.

The strategic rationale was compelling. Maverick's welded pipe production complemented Tenaris's seamless pipe expertise. The combined entity could offer customers a complete product range while achieving significant operational synergies.

The Hydril Acquisition (2007)

In 2007, the company acquired Hydril for $2.16 billion. If Maverick gave Tenaris scale in North American welded pipe, Hydril gave it something even more valuable: proprietary technology.

Hydril is a leading North American manufacturer of premium connections and pressure control products for oil and gas drilling and production, which has established an outstanding reputation in the industry for the quality and reliability of its technology. Paolo Rocca, Tenaris' Chairman and CEO, commented, "This is another major step for Tenaris. Hydril is a company with an extraordinary track record and an outstanding know-how built over more than 70 years of serving the oil and gas industry. With Hydril, we will be able to offer our customers worldwide a full range of integral and coupled premium connection products for the industry's most demanding applications. The combined R&D and industrial know-how of the two companies will make a substantial contribution in the new frontiers for exploration and production."

Premium connections—the threaded joints that connect pipe sections—are crucial for well integrity. In deep wells with high pressures and harsh conditions, connection failure can be catastrophic. Hydril's Wedge Series connections, developed over decades, represented the gold standard in the industry.

Since its acquisition of Hydril Company in May 2007, Tenaris has integrated Hydril's premium connection business into its core tubular business and managed the Hydril pressure control business separately. Tenaris S.A. has entered into an agreement with General Electric Company (GE), pursuant to which it will sell the pressure control business acquired as part of the Hydril transaction to GE for an amount equivalent on a debt-free basis to US$1,115 million.

This disposition was strategically astute. Tenaris kept the premium connection technology—which had high synergies with its core pipe business—while monetizing the pressure control equipment business where synergies were limited.

Strategic Impact

With the acquisition of Maverick, Tenaris' stake in the U.S.-Canadian market is expected to jump from 5% to 20%, according to Reuters. This transformation happened in just eighteen months, fundamentally repositioning Tenaris as a major player in the world's largest OCTG market.

The acquisitions also brought something intangible but crucial: deep customer relationships with North American operators. These relationships would prove essential for the next phase of Tenaris's evolution—the development of its revolutionary Rig Direct service model.

The Shale Revolution & Bay City Mill (2013-2017)

⭐ KEY INFLECTION POINT #2

Building the World's Most Advanced Pipe Mill

On a sweltering December day in 2017, on land that had been a grass farm four years earlier, Tenaris unveiled its $1.8 billion state-of-the-art seamless pipe mill in Bay City, Texas, before local, state and federal representatives, including U.S. Department of Energy Secretary Rick Perry and Texas Governor Greg Abbott. Tenaris customers, community members and employees also joined the ceremonial launch.

The 1.2 million square foot mill incorporates a high level of automation and cutting edge technologies into its production of seamless pipe. The facility is also the company's most environmentally efficient mill, seeking LEED certification.

Tenaris's mill in Bay City is strategically located near key shale plays and reaffirms the company's commitment to the U.S. market and domestic manufacturing. The facility is a direct response to the resurgence in the U.S. energy industry and the opportunity to shorten and make the industry more competitive through domestic manufacturing of seamless pipes as a key input for drilling shale wells.

U.S. Energy Secretary Rick Perry was Texas Governor when he first announced the greenfield investment in 2013. That Perry returned as Energy Secretary for the opening ceremony underscored the political significance of domestic manufacturing during the shale revolution.

The Rig Direct™ Business Model Innovation

The Bay City mill wasn't just about manufacturing—it was the physical infrastructure for an entirely new way of doing business in the steel pipe industry.

Tenaris's new mill has the capacity to produce 600,000 tons of OCTG, annually, and is a critical piece of infrastructure driving the company's services oriented strategy known as Rig Direct™. The direct-to-customer model synchronizes customers' drilling operations with pipe manufacturing, delivering products and services when needed, as needed. To date, nearly two-thirds of Tenaris's oil and gas customers in the U.S. are using Rig Direct™. OCTG produced at the seamless pipe mill in Bay City, Texas, will be shipped directly to customer rig sites or stored at Tenaris service centers in Bay City, Freeport, Midland or Oklahoma.

This just-in-time model represented a fundamental reimagining of the steel pipe supply chain. Traditionally, oil companies purchased pipes from distributors who maintained large inventories, adding costs and complexity. With the tubular supply chain integrated under our responsibility from the mill to the well and materials supplied ready to be run in the well, you benefit from a proven model that maximizes material and supply chain efficiency and features digital processes to further integrate operations and administration. We enhance well integrity through assuring high quality at every stage of the supply chain, pipe by pipe traceability and advanced digital solutions for optimal pipe running operations.

"Tenaris is the architect of a new business model in the steel pipe sector – and the heart of this transformation is in Bay City with the most advanced pipe manufacturing facility in the world," said Germán Curá, Tenaris' president for North America.

Ten years ago, Tenaris launched the Rig Direct® brand to introduce a new approach to serving the U.S. market, one centered on supply chain integration, minimizing redundancy and waste, and staying close to customer operations.

Community Investment & The Tenaris Way

The Bay City investment was not just in company but in community. Tenaris has invested nearly $1.8 million in education in Matagorda County. This includes nearly 30 scholarships and awards as well as its partnership with the Wharton County Junior College for the manufacturing technology program.

This community-focused approach reflects a broader Tenaris philosophy. In every location where the company operates—from Argentina to Saudi Arabia—it invests heavily in technical education and local development. Investment in Community projects continues to grow, reaching $17.6 million USD in 2024, as the company focuses on extending the reach of its technical education programs, exemplified by the success of the Roberto Rocca Technical Schools.

The IPSCO Acquisition & Trade Dynamics (2020)

⭐ KEY INFLECTION POINT #3

Becoming #1 in North America

Tenaris S.A. announced today the completion of its previously announced acquisition of IPSCO Tubulars, Inc., a U.S. manufacturer of steel pipe, from PAO TMK. The acquisition price was determined on a cash-free, debt-free basis, and the final amount paid in cash, following contractual adjustments, was US$1,067 million (including approximately US$220 million in working capital).

"The IPSCO acquisition marks a new chapter in our U.S. expansion and represents another milestone in Tenaris's history. Together, we are uniquely positioned to serve the U.S. oil and gas industry, with an extensive geographic deployment throughout North America and an unmatched product range," said Tenaris chairman and chief executive Paolo Rocca.

Tenaris's existing U.S. industrial and service network will be complemented by IPSCO's facilities in the Midwest and Northeast. IPSCO's steel shop in Koppel, Pa., USA, will be Tenaris's first in the U.S., and its Ambridge, Pa., mill will be its second seamless manufacturing facility.

The IPSCO acquisition was particularly significant because it included steelmaking capacity. IPSCO's steel shop in Koppel, PA, is Tenaris's first in the United States, providing vertical integration through domestic production of a relevant part of its steel bar needs. Its Ambridge, PA, mill adds a second seamless manufacturing facility and complements Tenaris's seamless plant in Bay City, Texas.

Trade War & Tariff Strategy

The timing of the IPSCO acquisition—announced in 2019 and closed in January 2020—reflected acute awareness of shifting trade dynamics. The Trump administration's Section 232 tariffs on steel imports fundamentally altered the competitive landscape for foreign pipe suppliers.

For Tenaris, which had historically imported significant volumes from its Argentine and Mexican facilities, vertical integration of U.S. steelmaking wasn't just strategically attractive—it was becoming competitively necessary. "With IPSCO, we will be able to strengthen our Rig Direct® offering with shorter lead times and more responsive service capabilities," added Rocca.

In connection with the closing of the transaction, the parties entered into a 6-year master distribution agreement whereby, Tenaris will be the exclusive distributor of TMK's OCTG and line pipe products in the United States and Canada. Tenaris's existing U.S. industrial and service network located primarily in the south is complemented by IPSCO's facilities located mainly in the mid-western and northeastern regions of the country.

This distribution agreement with TMK—Russia's largest pipe producer—added another dimension to Tenaris's market position, giving it access to additional product lines without requiring capital investment.

Global Expansion & Vertical Integration

Middle East Moves

Tenaris S.A. announced today that it closed its previously-announced acquisition from a private group of 47.79% of the shares of Saudi Steel Pipe Company ("SSP"), a welded steel pipes producer listed on the Saudi stock market, for a total amount of US$141 million.

"The official integration of Saudi Steel Pipe into Tenaris marks an important step to further expand the company's footprint and capabilities in Saudi Arabia," said Mariano Armengol, who has been appointed as Managing Director and Chief Executive Officer of SSP. "We see clear opportunities for business growth in the Kingdom and the region, through expanding SSP's products and services portfolio and maximizing local preference." Tenaris has been serving the Kingdom for nearly a decade and operates two premium threading facilities in Dammam, in the Eastern Province of the Kingdom of Saudi Arabia.

TenarisSaudiSteelPipes facilities are located in the Eastern Province of the Kingdom of Saudi Arabia and have a manufacturing capacity of 500,000 tons per year. The company is qualified to supply products with major national oil companies in the region, including Saudi Aramco.

Latin America & Vaca Muerta

Argentina's Vaca Muerta shale formation—the world's second largest reservoir for shale gas and fourth largest for shale oil—has become a crucial growth driver for Tenaris. The synergies with sister company Tecpetrol, which operates in the formation, create a powerful competitive advantage.

Tenaris is now performing hydraulic fracturing operations, a first for the company, in the Vaca Muerta formation, the world's second largest reservoir for shale gas and fourth for shale oil in Argentina. With this milestone, Tenaris is expanding its offer of services to customers in the region. As of June, 90 fractures have been completed in three wells with very good efficiency indicators, accompanying the increase of production levels in Fortín de Piedra's unconventional gas field, operated by Tecpetrol.

Following a $110 million USD investment, Tenaris is strengthening its hydraulic fracturing capabilities in Argentina with the addition of a third frac set for Vaca Muerta, one of the world's largest shale gas reservoirs. This equipment will expand Tenaris's well completion capacity in Vaca Muerta, following the acquisition of its first hydraulic fracturing set in 2020 and a second in 2024. Tenaris is now the third-largest provider of frac services in the local market.

"By 2026, we will have invested more than $240 million USD to provide services for unconventional wells since making the strategic decision to acquire our first hydraulic fracturing and coiled tubing assemblies in 2020," said Javier Martínez Álvarez, Tenaris president for the Southern Cone.

Energy Transition Investments

The Buena Ventura wind farm is now delivering 103.2 MW of renewable energy to the company's Argentine seamless mill through the interconnected grid. The first project, constructed in 15 months, is located in Gonzales Chaves district, in the province of Buenos Aires, a favorable location for wind electricity generation with a projected utilization capacity factor of 58%. This includes 24 turbines (4.2 MW installed power each) generating a total of 509GWh annual electricity production, supplying close to 50% of the electrical energy required by Tenaris's mill in Campana, with a reduction in CO2 emissions of 152,000 tons per year. The total investment has amounted $203 million USD.

The construction phase of Tenaris's second wind farm in Argentina has started. La Rinconada, located in Olavarría, in the province of Buenos Aires, will feature 21 wind turbines and a total installed capacity of 94.5 megawatts. Following a $214 million USD investment, it is expected to become operational by the end of 2025. Once operational, Tenaris's two wind farms will produce renewable energy to cover the electricity needs of Siderca, its seamless pipe manufacturing facility in Campana.

With the construction of its first two wind farms, Tenaris will have invested more than $400 million USD over four years in renewable energy in Argentina to reduce its environmental footprint and advance its decarbonization efforts.

"With the investment in the wind farms and our ongoing investments in energy efficiency, we expect to meet almost 100% of our energy requirements in Argentina through renewable energy," said Paolo Rocca, Tenaris Chairman and CEO. Tenaris has established a plan to reduce its CO2 emissions intensity per ton of steel by 30% by 2030.

Challenges & Controversies

Regulatory Issues

Tenaris's global operations have occasionally generated regulatory scrutiny. In May 2011, Tenaris agreed to pay the United States Department of Justice US$8.9 million in the first ever deferred prosecution agreement with the U.S. Securities and Exchange Commission, after Tenaris voluntarily disclosed details of bribes made to officials of an Uzbek state-controlled oil firm to obtain competitor's bid information, which it used to submit revised bids in order to secure tenders.

More significantly, The Securities and Exchange Commission announced that Tenaris, a Luxembourg-based global manufacturer and supplier of steel pipe products, will pay more than $78 million to resolve charges that it violated the Foreign Corrupt Practices Act (FCPA) in connection with a bribery scheme involving its Brazilian subsidiary. Tenaris consented to the SEC's order without admitting or denying the findings that it violated the anti-bribery, books and records, and internal accounting controls provisions of the Securities Exchange Act of 1934 and agreed to pay more than $78 million in combined disgorgement, prejudgment interest, and civil penalties.

According to the SEC Order, between 2008 and 2013 Tenaris' Brazilian subsidiary, Confab Industrial SA (Confab), through a third-party intermediary, paid at least $10.4 million in bribes to a high-ranking manager in the procurement and tender department of Brazil's state-owned petroleum company, Petróleo Brasileiro S.A. (Petrobras), in order to obtain and retain over $1 billion in contracts.

The US Department of Justice closed its investigation without bringing charges. The SEC credited Tenaris's cooperation and remedial efforts, noting that the company had implemented enhanced compliance programs.

Venezuela Nationalization

Venezuela has nationalized Tenaris' majority-owned subsidiaries Tavsa, Tubos de Acero de Venezuela S.A. and Matesi, Materiales Siderurgicos S.A. and its minority interest in Complejo Siderurgico de Guayana, C.A. Tenaris announced today that Venezuela's President Hugo Chavez has announced the decision to nationalize its majority-owned subsidiaries.

Tenaris S.A. announced that pursuant to Decree Law 6058 and Decree 6796, Venezuela, acting through PDVSA Industrial S.A. (a subsidiary of Petroleos de Venezuela S.A.), formally assumed exclusive operational control over the assets of Tavsa, Tubos de Acero de Venezuela S.A. ("Tavsa"). Following this formal change in operational control, PDVSA Industrial has assumed complete responsibility over Tavsa's operations and management.

Tenaris pursued international arbitration through ICSID. On December 12, 2016, the tribunal issued its award upholding Tenaris's and Talta's claim that Venezuela had expropriated their investments in Tavsa and Comsigua in violation of the bilateral investment treaties entered into by Venezuela with the Belgium-Luxembourg Economic Union and Portugal. Similarly, on December 12, 2016, the tribunal issued its award for the expropriation of our investments in Tavsa and Comsigua, granted compensation in the amount of $137 million and ordered Venezuela to reimburse Tenaris and Talta $3.3 million in legal fees and ICSID administrative costs.

Cyclicality & Oil Price Dependency

The OCTG industry is highly cyclical, directly tied to drilling activity and oil and gas prices. OCTG inventories have risen and prices continue to fall. This sensitivity to commodity cycles creates significant earnings volatility—a reality investors must factor into their analysis.

The Modern Era: 2024-2025 & Current Position

Financial Performance

"We consolidated our leading industry position with a number of distinct achievements, delivered solid financial results accompanied by higher returns for shareholders, and completed several investments which are improving our industrial efficiency and reducing our environmental footprint," noted by Tenaris Chairman & CEO Paolo Rocca in his opening letter. Tenaris's robust financial performance in 2024 includes net sales of $12.5 billion, EBITDA of $3.1 billion, and net income of $2.1 billion. During this period, Tenaris completed investments across its industrial system aimed at improving operational efficiency and contributing to its decarbonization and environmental objectives.

Tenaris reported full-year 2024 revenue of $12.5 billion, representing a 16% decrease compared to 2023. The company maintained a strong financial position with a net cash position of $3.6 billion. Free cash flow amounted to $2.2 billion in 2024. The board proposed an annual dividend of $0.83 per share.

Cash flow provided by operating activities amounted to $2.9 billion during 2024. This was used to fund capital expenditures of $694 million, with the remainder distributed to shareholders through dividend payments of $758 million and share buybacks for $1,440 million in the year. We maintained a net cash position of $3.6 billion at the end of December 2024.

Geographic Revenue Mix

In 2023, 53% of the company's sales were to North America, 22% of sales were to South America, 18% of sales were to the Asia-Pacific, and 7% of sales were to Europe.

This geographic diversification provides valuable stability. When North American drilling slows, Middle Eastern or South American activity often provides offset. The company's global footprint also enables it to serve international oil companies across multiple operating regions.

Paolo Rocca: The Steward

Paolo Rocca was born in Milan, Italy, in 1952. He is the son of Roberto Rocca, who was Honorary Chairman of Techint, and grandson of Agostino Rocca, founder of this industrial group. Paolo Rocca earned a degree in political science from the Università degli Studi di Milano. In 1985 he attended the PMD at Harvard Business School. After having been an assistant to the executive director of the World Bank, in 1985 Paolo Rocca began his career at Techint Group as assistant to the chairman of the board of directors. In 1990 he assumed as executive vice-president of Siderca. Since 2002, he is the CEO of Tenaris and Techint.

As of July 2024, Forbes estimated his net worth at US$5.0 billion. Paolo Rocca is a member of the executive committee of the World Steel Association and was the chairman of this association during the 2009–2010 period. He was a member of the International Advisory Committee of New York Stock Exchange, and of the advisory board of the Inter-American Development Bank (IDB) private sector. In 2004 within the "Argentina-México: Visión y Perspectivas" forum, he was awarded with the Orden Mexicana del Aguila Azteca. In 2008 he was recognized by Fundación Konex with the "2008 Platinum Konex Prize: Industry businessmen"; and in 2011 he was chosen "Steelmaker of the Year" by the Association of Iron and Steel Technology (AIST). In 2013 the Columbia Business School honored Paolo Rocca with the "Deming Cup" in recognition to the impact of his leadership on Tenaris's competitiveness.

Paolo Rocca is a private person who shuns the limelight. He is known for his work ethic and dedication to his family and company. Paolo Rocca is a dual citizen of Italy and Argentina. He is a fluent speaker of Italian, Spanish, English, and French. Rocca is a passionate art collector and has a private collection of over 1,000 works of art. He is a member of the board of trustees of the Metropolitan Museum of Art in New York City.

Competitive Landscape & Strategic Analysis

Industry Position

Global Powerhouses: Companies such as Vallourec, Tenaris, Nippon Steel & Sumitomo Metal, and TMK stand as stalwarts, leveraging expansive production capabilities, cutting-edge technologies, and well-established distribution networks.

Tenaris is the second-largest manufacturer of OCTG in the world, it has a market share of 19.09% in value.

The steel pipe and tube industry can be categorized as having high barriers to entry, low concentration and high revenue volatility (a function of oil and gas demand). In the U.S., Tenaris has the largest market share of the metal pipe and tubing industry (8.20%), with the four largest companies having a combined 20% market share. The industry encompasses dozens of products, so concentration occurs within more niche markets.

Porter's Five Forces Analysis

Threat of New Entrants: LOW High capital expenditure requirements, legal barriers, start-up costs and labor costs all combine to erect high barriers to entry that protect the incumbents' margins. Building a modern seamless pipe mill requires $1-2 billion in capital, decades of accumulated metallurgical expertise, and established customer relationships with major oil companies.

Supplier Power: MODERATE All of its manufacturing facilities use electric arc furnaces, where the feedstock is predominantly steel scrap and is less energy-intensive than the basic oxygen furnace method. Electric arc furnaces are also less greenhouse gas-intensive and typically more productive with less overhead costs. Only 4% of steel pipe costs for Tenaris are due to direct energy (86% of which is supplied from local electricity grids), whilst 23% are derived from steel scrap costs. Tenaris's vertical integration into steelmaking (particularly after IPSCO) reduces supplier dependency.

Buyer Power: MODERATE TO HIGH Major oil companies like ExxonMobil, Chevron, and Saudi Aramco have significant purchasing power. However, Tenaris's technical expertise, quality reputation, and integrated service model (Rig Direct) create switching costs that moderate buyer power.

Threat of Substitutes: LOW For high-pressure oil and gas applications, there are no practical substitutes for steel pipe. Alternative materials lack the necessary strength, durability, and temperature resistance.

Competitive Rivalry: HIGH Tubacex, Metallus, Vallourec, Voestalpine, and Marcegaglia are some of the 6 competitors of Tenaris. Competition is intense, particularly during downturns when excess capacity leads to price pressure.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Tenaris's position as the world's #1 OCTG producer generates significant scale economies in purchasing, manufacturing, and R&D. The Bay City mill—designed for 600,000 tons annually—represents state-of-the-art efficiency.

Network Effects: Limited direct network effects, though the Rig Direct digital platform creates some switching costs and data advantages.

Counter-Positioning: The Rig Direct model represents genuine counter-positioning. Traditional distributors cannot easily replicate Tenaris's integrated mill-to-well approach without cannibalizing their existing business model.

Switching Costs: Technical qualification processes, integrated service relationships, and proprietary connection technologies create meaningful switching costs. Oil companies invest significant time qualifying pipe suppliers for specific applications.

Branding: TenarisHydril connections enjoy strong brand recognition in premium applications. The Hydril name has represented quality and reliability for over 70 years.

Cornered Resource: Tenaris's proprietary connection technologies, particularly the Wedge series, represent cornered resources that competitors cannot easily replicate.

Process Power: Decades of accumulated metallurgical and manufacturing expertise create process power that enables superior quality at competitive costs.

The Investment Case

Bull Case

Dominant Market Position: Tenaris is the world's largest OCTG producer with unmatched geographic reach and product breadth. The company's position in North America—the world's largest drilling market—is particularly strong following the Maverick, Hydril, and IPSCO acquisitions.

Rig Direct Competitive Advantage: The integrated mill-to-well service model creates genuine differentiation. For over 13 years, Tenaris has supported the Permian Basin shale driller with OCTG, and Pioneer served as one of the initial Rig Direct® customers. Tenaris and Pioneer executed its first Rig Direct® shipment in August 2015. Customer adoption continues to grow, creating recurring revenue streams and switching costs.

Financial Strength: The net cash position of $3.6 billion provides flexibility for acquisitions, shareholder returns, or investment through the cycle. Few industrial companies maintain such fortress balance sheets.

Energy Transition Positioning: While oil and gas remain the core business, Tenaris is investing in geothermal and hydrogen applications. The company's THera™ hydrogen storage systems position it for emerging clean energy applications.

Family Ownership Alignment: With the Rocca family controlling ~60% of shares, management's interests align with long-term value creation rather than short-term earnings management.

Bear Case

Oil & Gas Cyclicality: The business remains fundamentally tied to drilling activity and oil prices. Extended periods of low oil prices—as in 2015-2016—can devastate earnings.

Energy Transition Risk: Long-term decline in oil and gas drilling would structurally impair demand for OCTG. While the timeline is uncertain, peak oil demand could arrive within the next decade or two.

Emerging Market Exposure: Significant operations in Argentina, Mexico, and other emerging markets create currency, political, and regulatory risks. The Venezuela nationalization demonstrated these risks in extreme form.

Trade Policy Uncertainty: Beyond that, likely changes in US tariffs and their possible ramifications on trade flows will introduce a new dynamic with a high level of uncertainty for costs and prices to our results.

Regulatory History: The FCPA settlements in 2011 (Uzbekistan) and 2022 (Brazil) raise governance questions, though the company has significantly enhanced its compliance programs.

Myth vs. Reality

Myth: Tenaris is a commodity steel company with no differentiation. Reality: Premium connections, proprietary technologies (Dopeless, TenarisHydril Wedge), and the Rig Direct service model create genuine differentiation that supports above-average margins.

Myth: The company is too dependent on North America. Reality: While North America represents ~46% of sales, the company maintains significant presence in South America (19%), Asia Pacific/Middle East/Africa (26%), and Europe (10%), providing geographic diversification.

Myth: Shale drilling decline will destroy the business. Reality: While U.S. shale activity has moderated, deepwater, international, and unconventional development globally provide multiple demand drivers. The company's geographic diversification reduces single-market dependency.

Key Performance Indicators for Investors

For long-term fundamental investors, three KPIs deserve particular attention:

1. EBITDA Margin (Target: 20-28%) This metric captures Tenaris's ability to maintain pricing power and operational efficiency through the cycle. In peak years like 2023, margins approached 28%; in downturns, they can compress to the mid-teens. The trajectory of margins—combined with volume trends—provides the clearest picture of fundamental business health.

2. Free Cash Flow Conversion Tenaris's capital-intensive nature makes free cash flow conversion crucial. Free cash flow amounted to $2.2 billion in 2024. Consistent ability to convert earnings to cash enables shareholder returns and strategic flexibility. Watch for capital expenditure cycles that may temporarily depress conversion.

3. North American OCTG Market Share In the U.S., Tenaris has the largest market share of the metal pipe and tubing industry (8.20%). Given the importance of North America to profitability, tracking market share trends provides early warning of competitive dynamics or market positioning changes.

Conclusion

The story of Tenaris is, in many ways, the story of modern industrial capitalism. A visionary entrepreneur builds something from nothing, transfers it to the next generation, navigates crisis and opportunity, expands globally, and creates lasting value.

From Agostino Rocca's post-war vision in Argentina to Paolo Rocca's stewardship of a global industrial franchise, the Tenaris story demonstrates what long-term, patient capital allocation can achieve. The company has survived nationalizations, navigated currency crises, and transformed itself from a regional player to the world's dominant OCTG producer.

Tenaris has demonstrated resilience in 2024, achieving a net income of $2.1 billion. The company's diversified global presence and strong positioning in deepwater and unconventional projects have helped it navigate market challenges.

For investors, Tenaris offers exposure to a well-managed industrial franchise with leading market positions, strong cash generation, and meaningful competitive advantages. The risks—cyclicality, energy transition, emerging market exposure—are real but manageable. The family ownership structure ensures alignment with long-term value creation.

As the world continues to require energy—whether from traditional hydrocarbons or emerging sources—it will need the pipes and connections that Tenaris provides. That's a business worth understanding.

Material Legal/Regulatory Overhangs: The company completed its 2022 SEC settlement related to FCPA violations involving its Brazilian subsidiary. Ongoing litigation related to the Usiminas acquisition in Brazil has resulted in provisions reflected in recent financial results.

Accounting Judgments: Revenue recognition timing, particularly related to Rig Direct contracts and percentage-of-completion accounting for long-term supply agreements, requires management judgment. Impairment testing of goodwill from acquisitions (particularly Maverick and Hydril) depends on assumptions about future cash flows and discount rates.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube