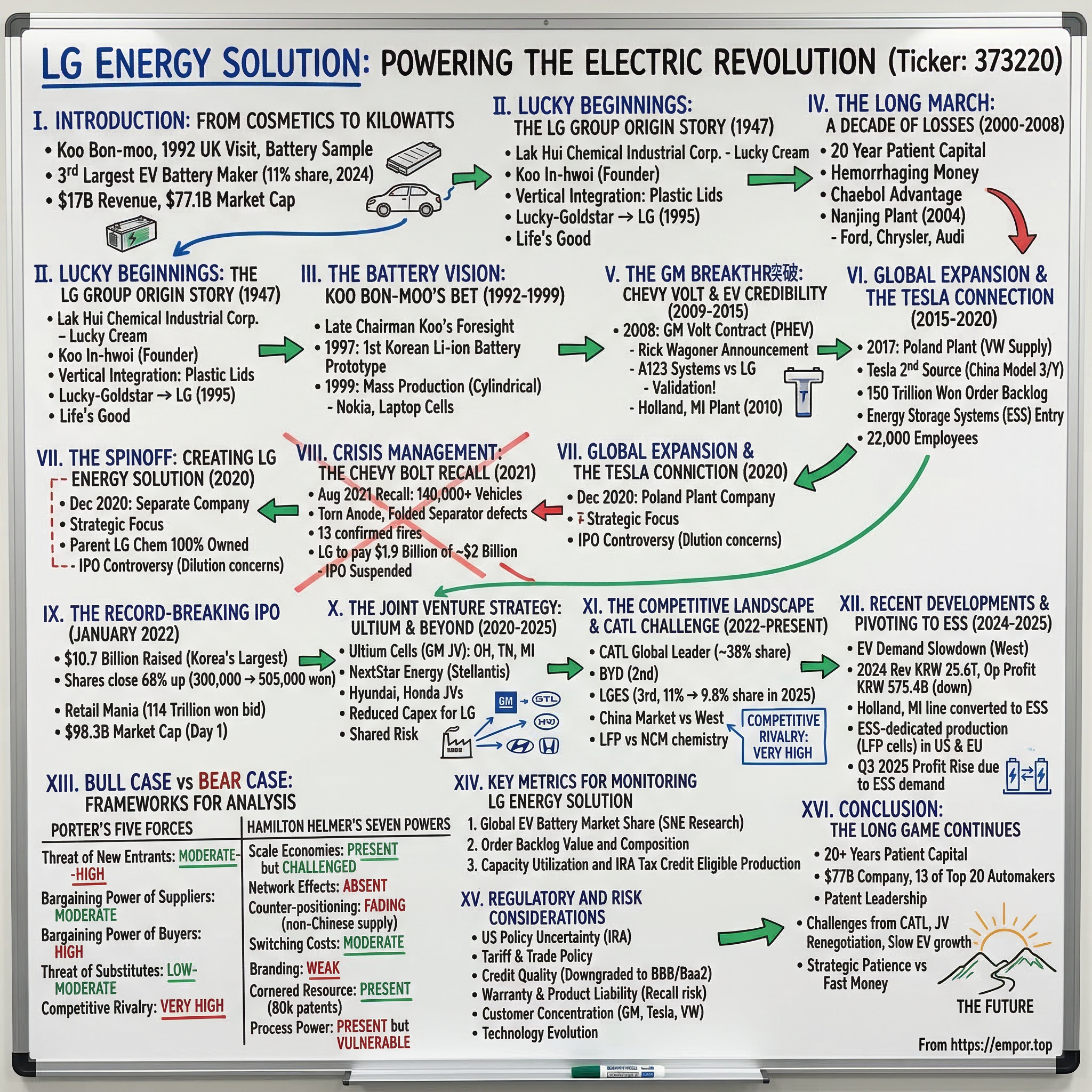

LG Energy Solution: Powering the Electric Revolution

I. Introduction: From Cosmetics to Kilowatts

In the fluorescent-lit corridors of Seoul's sprawling corporate headquarters, a photograph hangs in quiet prominence: a middle-aged Korean executive holding what appears to be a small rectangular object, something that looks remarkably unremarkable. The year was 1992. The executive was Koo Bon-moo, the third-generation chairman of the Lucky-Goldstar conglomerate. The object in his hands was a rechargeable battery sample he had just brought back from a visit to the United Kingdom Atomic Energy Authority. That modest souvenir would set in motion one of the most consequential industrial transformations of the modern era.

LG Energy Solution is now the third-largest battery maker for electric vehicles with about 11% global share in 2024. Its trailing twelve-month revenue stands at $17 billion, with a current market capitalization of approximately $77.1 billion. The company supplies the beating hearts—the lithium-ion battery packs—that power everything from Tesla's Model Y to GM's electric Silverado trucks, from Volkswagen's ID series to Hyundai's Ioniq lineup.

But rewind the tape far enough, and you'll find this battery giant's origins in an altogether different business: face cream. How did a Korean cosmetics company become the battery supplier powering the global EV revolution? The answer involves three generations of a family dynasty, two decades of patient losses, a billion-dollar recall crisis, and a strategic playbook that transformed chemical expertise into electrochemical dominance.

LG Energy Solution is a leading global manufacturer of lithium-ion batteries for electric vehicles, mobility, IT, and energy storage systems. With 30 years of experience in revolutionary battery technology and extensive research and development, the company is the top battery-related patent holder in the world with over 80,000 patents.

The company's story is a masterclass in patient capital, technological persistence, and the advantages that accrue to companies willing to lose money for decades while building capabilities that competitors cannot easily replicate. It is also a cautionary tale about the risks of rapid scaling in complex manufacturing, the geopolitical chess match playing out in the EV supply chain, and the challenges of competing against Chinese rivals whose cost structures seem to defy gravity.

For investors trying to understand the future of transportation and energy storage, LG Energy Solution represents a critical case study in how chemical expertise, government partnership, and strategic patience can create durable competitive positions—and how quickly those positions can be challenged.

II. Lucky Beginnings: The LG Group Origin Story

The monsoon rains of 1947 battered the makeshift factories of post-liberation Korea. The country had just emerged from 35 years of Japanese colonial rule, and its industrial base lay in ruins. Into this chaos stepped a young entrepreneur named Koo In-hwoi with an improbable vision: he would build Korea's chemical industry from scratch, starting with something every woman wanted—face cream.

The group's first truly successful business, Lak Hui Chemical Industrial Corporation, opened in 1947. It began selling a new face cream called Lucky, which quickly sold out despite its relatively high price thanks to its high-quality ingredients. But though sales were soaring, because of a big problem with the cream's lid, many people were returning the product.

This quality control disaster turned into an unexpected opportunity. The LG we know today came from Lucky Chemical Co., Ltd., established in 1947. Chairman In-hwoi Koo initially named his company "Lucky" (which sounds like "Lak Hui," meaning giving joy to all) after the huge success of "Lucky Cream," Korea's first makeup cream. The "Lucky" brand became the face of Lak Hui Chemical, with hit products like "Lucky toothpaste." In 1974, due to the company and brand's success, Lak Hui Chemical changed its name to Lucky Co., Ltd. and grew into a leading chemical company.

Rather than simply fix the lid supplier, Koo made a decision that would define his conglomerate's DNA: he brought plastic manufacturing in-house. This vertical integration philosophy—if something breaks, learn to make it yourself—would echo through decades of LG's expansion into electronics, displays, and eventually batteries.

LG Corporation (or LG Group), formerly known as Lucky-Goldstar, is a South Korean multinational conglomerate founded by Koo In-hwoi in 1947 and managed by successive generations of his family. It is the fourth-largest company in South Korea.

The family succession followed Korea's chaebol tradition with almost mechanical precision. Koo In-hwoi led the corporation until his death in 1969, at which time his son Koo Cha-kyung took over. He then passed the leadership to his son, Koo Bon-moo, in 1995. Koo Bon-moo renamed the company to LG in that year. The company then trademarked the letters LG with the company's tagline "Life's Good."

Goldstar, founded in 1958, also played a huge role in LG's history. As the first electronics company in Korea, Goldstar developed many of the first pivotal electronic products in the country. Lak Hui and Goldstar quickly grew into the leading companies in their respective industries.

The Korean context here is crucial. The chaebol system—massive family-controlled conglomerates with close government ties—allowed companies like LG to pursue multi-decade investment horizons that would be impossible for publicly traded Western companies answering to quarterly-focused shareholders. This patient capital structure would prove essential when LG decided to enter the battery business, a venture that would hemorrhage money for twenty consecutive years before turning profitable.

In the 1970s, Lucky entered the petrochemical business, building massive refining and polymer operations that would provide two essential ingredients for future battery dominance: deep expertise in chemical processes and a cash-generating machine that could subsidize money-losing ventures indefinitely.

Investor Takeaway: The LG origin story illuminates a key competitive advantage that remains relevant today: the company's chemical heritage provides fundamental expertise in the cathode materials, electrolytes, and separator technologies that determine battery performance. Unlike competitors who entered batteries from electronics (Samsung SDI) or automotive (CATL), LG came from chemistry itself.

III. The Battery Vision: Koo Bon-moo's Bet (1992–1999)

The story of LG's battery business begins not in a laboratory but in an English office park. In 1992, Koo Bon-moo—then an executive being groomed to lead the family conglomerate—made a routine visit to the United Kingdom Atomic Energy Authority, the government body responsible for Britain's nuclear research.

LG Chem started a battery business after LG Group chairman Koo Bon-moo visited the United Kingdom Atomic Energy Authority office in 1992. After the visit, Koo brought rechargeable battery samples and began research into the emerging technology.

The late chairman of the LG Group, Koo Bon-moo, was one of the first to notice the vast possibilities of the rechargeable battery. With a vision that rechargeable batteries will change the world, he launched research and development in 1992 and never looked back. Thanks to this leap of faith, in 1999, LGES (at the time a part of LG Chem) became the first Korean company to successfully mass produce cylindrical lithium-ion batteries.

What exactly did Koo see that others missed? Context matters here. Sony had just commercialized the first lithium-ion battery in 1991, opening a new era of portable electronics. But the technology was crude, expensive, and primarily useful for camcorders. Most business executives saw a niche product; Koo saw the future of energy storage.

The timing was critical. Japan's electronics giants—Sony, Panasonic, Sanyo—dominated the nascent lithium-ion market. Korea had no meaningful battery industry. The logical business decision would have been to source batteries from Japan and focus on what Korea did best: manufacturing consumer electronics cheaply.

Koo made the opposite choice. He bet that a chemicals company could learn battery technology faster than electronics companies could learn chemistry. Batteries, after all, are fundamentally chemistry problems: electrochemical reactions, material science, and manufacturing process control. LG Chem had spent four decades mastering exactly those disciplines.

This led to the formation of a dedicated R&D team within LG Chem, marking the start of Korea's domestic battery industry. Building on this foundation, LG Chem achieved significant technical progress by 1997, when it developed the nation's first lithium-ion battery prototype, focusing on cathode materials like lithium cobalt oxide to enhance energy density. Two years later, in 1999, the company commissioned its Cheongju plant—the first mass-production facility for secondary batteries in Korea and the second globally after Sony.

The initial focus was consumer electronics—batteries for Nokia's burgeoning mobile phone business, cells for laptop computers. This wasn't yet about electric vehicles, which existed only as research curiosities. It was about building manufacturing capabilities and establishing commercial relationships.

In 2009, LG Chem supplies the world's first mass-produced Plug-In Hybrid EV batteries to GM (Chevy Volt). In 2004, LG Chem establishes the Nanjing plant in China.

By 1999, when LG Chem began mass production of cylindrical lithium-ion cells, the company had invested seven years and untold sums in a business that had yet to generate meaningful revenue. But the foundation was laid. The company understood lithium-ion chemistry at a molecular level. It had manufacturing processes that could scale. And it had accumulated the first of what would become more than 80,000 battery-related patents—an intellectual property fortress that would later prove invaluable.

Investor Takeaway: LG's entry into batteries illustrates a common pattern among successful technology companies: entering markets before they exist. The seven-year gap between Koo's 1992 vision and 1999 commercial production represented a bet on uncertain technology with no clear path to profitability. Such bets require patient capital and conviction—qualities more commonly found in family-controlled conglomerates than in publicly traded corporations.

IV. The Long March: A Decade of Losses (2000–2008)

The year 2000 arrived with the promise of a new millennium and the sting of the dot-com crash. For LG Chem's battery division, it marked the beginning of what employees grimly called "the long march"—a decade of relentless investment, technical progress, and steadily mounting losses.

As the world started to take note of EVs, the company entered the North American battery market ahead of other competitors. In 2000, LGES established an R&D facility in Colorado for the development of lithium-ion batteries, one of few domestic EV battery R&D facilities at the time, which later moved to Detroit, the hub of the U.S. auto industry.

The strategic rationale was clear, even if the economics were not. Electric vehicles remained a scientific curiosity in 2000—the Toyota Prius had launched in Japan in 1997 with a nickel-metal hydride battery, but EVs were years away from mass production. LG's bet was that lithium-ion technology would eventually prove superior for automotive applications, despite significant technical challenges.

The challenges were formidable. Automotive batteries required energy densities far beyond what consumer electronics demanded. They needed to survive extreme temperatures—from Phoenix summers to Minnesota winters—while maintaining performance. They had to last 10-15 years, not the 2-3 years acceptable for a laptop. And critically, they had to be safe: a laptop battery fire is inconvenient; a car battery fire can be lethal.

This milestone positioned LG Chem as an early player in the lithium-ion market, despite initial challenges with product quality and yield rates. Throughout the 2000s, LG Chem's battery operations evolved into a structured division known as the Energy Solution Business Division, concentrating on lithium-ion advancements such as higher capacity and cycle life improvements. Key growth came from securing major automotive supply contracts.

The patient capital advantage of the chaebol structure proved essential during these years. LG Chem's petrochemicals division—manufacturing polyethylene, ABS plastics, and specialty chemicals—generated consistent profits that subsidized the battery division's losses. A Western public company would have faced intense pressure to cut the losses, sell the division, or pivot to more immediately profitable ventures.

Instead, LG doubled down. In 2004, the company completed construction of a battery plant in Nanjing, China, establishing manufacturing presence in what would become the world's largest EV market. The Ochang facility in South Korea expanded into dedicated automotive battery production. Patent filings accelerated, building the intellectual property moat that would later become a strategic weapon.

The late 2000s finally brought validation. Oil prices spiked to $147 per barrel in 2008, suddenly making electric vehicles economically relevant. General Motors, humbled by rising fuel costs and facing an existential crisis, launched an aggressive EV program. And LG Chem was ready.

Key growth came from securing major automotive supply contracts, including a 2008 agreement with General Motors to provide lithium-ion battery systems for the Chevrolet Volt plug-in hybrid, which helped pioneer the electric vehicle sector. This was followed by partnerships with Ford, Chrysler, Audi, Renault, Volvo, and SAIC Motor, expanding the division's footprint in hybrid and EV applications.

The two decades of losses had achieved their purpose: LG Chem had developed manufacturing expertise, secured intellectual property, established global production footprint, and built relationships with the automotive customers who would drive future demand. The long march was ending, and the profitable sprint was about to begin.

Investor Takeaway: The battery industry's economics reward companies that can sustain losses long enough to achieve manufacturing scale. LG's twenty-year investment before profitability demonstrates the capital intensity and patience required—barriers that protect incumbent players from well-funded but late-arriving competitors.

V. The GM Breakthrough: Chevy Volt & EV Credibility (2009–2015)

On a crisp January morning in 2009, at the North American International Auto Show in Detroit, General Motors CEO Rick Wagoner made an announcement that would reshape the automotive industry. GM had selected LG Chem to supply lithium-ion battery cells for the Chevrolet Volt, the company's flagship plug-in hybrid electric vehicle.

General Motors Corp. selects South Korea's LG Chem Ltd. and its Compact Power Inc. subsidiary in Troy, MI, to supply lithium-ion cells for the Chevrolet Volt extended-range electric vehicle. GM also will locate a plant in Michigan to assemble the cells into the t-shaped battery pack for the Volt, pending the approval of state incentives. "GM is back in the battery business," says GM Chairman and CEO Rick Wagoner, in reference to the auto maker's EV1 electric vehicle from 1996.

The selection came after a brutal two-year competition. GM first announced in the summer of 2007 that they had chosen two supplier teams to compete against one another to build the Chevy Volt's battery packs. From an initial field of 27 applicants, LG Chem and Compact Power Inc were one team and A123 Systems/Continental were the other.

For LG Chem, the GM contract represented far more than revenue—it was validation. The Volt would be the first mass-produced plug-in hybrid from a major automaker, and its battery supplier would gain credibility that money alone couldn't buy. The selection demonstrated that LG's technology could meet the demanding requirements of automotive-grade manufacturing.

The deal also established a pattern that would define LG's expansion strategy: government partnership to defray capital costs. LG Chem announced it would invest $303 Million to build a lithium-ion cell manufacturing plant in Holland, Michigan. The U.S. Department of Energy provided matching stimulus funds under the Obama administration's push to establish domestic battery manufacturing.

With a 30-year history in the battery business, LG Energy Solution has made consistent, large-scale investments to accumulate enough stability, credibility and manufacturing experience to invent its own cutting-edge technologies. The company established its first research facility in the U.S. in the early 2000s. In 2010, the company built its first U.S. battery plant in Holland, Michigan.

The Volt battery represented a technical triumph. Its T-shaped lithium-ion pack weighed approximately 400 pounds and enabled 40 miles of all-electric driving—enough for most Americans' daily commutes. The manganese-spinel chemistry combined with a ceramic-coated separator provided the thermal stability required for automotive applications.

Success with GM opened doors across the industry. LG Chem produced Korea's first lithium-ion battery in 1999 and began supplying automotive batteries for the Chevrolet Volt produced by General Motors in the late 2000s. Later, the company became a battery supplier to global car makers, including Ford, Chrysler, Audi, Renault, Volvo and SAIC Motor.

By 2015, LG Chem had transformed from a Korean chemicals company with battery ambitions into a global automotive supplier with relationships spanning continents. The decade of losses had yielded to the decade of growth, but the real scaling was yet to come.

Investor Takeaway: The GM contract exemplifies how anchor customers can validate technology companies and provide the credibility needed to win subsequent deals. LG's willingness to invest in U.S. manufacturing with government support established a template that competitors later copied—and that now provides strategic advantage as Western automakers seek non-Chinese battery suppliers.

VI. Global Expansion & The Tesla Connection (2015–2020)

By the mid-2010s, the electric vehicle revolution was no longer a distant possibility—it was accelerating faster than even optimists had predicted. Tesla's Model S had proven that EVs could be desirable, not just dutiful. China had committed to electrification as national policy. European emissions regulations were tightening inexorably. And LG Chem, having spent two decades preparing for this moment, was sprinting to meet surging demand.

In 2017, LG Chem builds an EV battery plant in Poland, the first large-scale automotive lithium battery production facility in Europe.

The Poland plant represented a strategic masterstroke. Located in Wrocław, the facility could supply Volkswagen's European EV production while qualifying for EU local content requirements. European automakers, facing existential pressure to electrify, needed battery partners who could deliver at scale—and LG was building the capacity to do exactly that.

The new company is apparently also going to significantly increase the production of battery cells for Tesla, which will include Giga Berlin in Germany. The new spin-off company LG Energy Solution employs around 22,000 people, about 7,000 of them in South Korea and 15,000 in other countries. The division has grown strongly with the demand for rechargeable batteries, not only for electric cars, but also for mobile devices such as smartphones.

The Tesla relationship deserves particular attention. While Panasonic had been Tesla's primary battery supplier since 2010, LG Chem emerged as a second source—first for the China-built Model 3 and Model Y, then potentially for European and American production. The increased production is not only to be delivered to the Tesla plant in Shanghai but also to Tesla's factories in Germany and the USA. LG Chem will initially be the sole supplier for the Shanghai-built Model Y.

The order backlog told the story of explosive growth. LG Chem currently has an order backlog worth 150 trillion won and will need to spend around 3 trillion won per year for facilities expansion. At approximately $130 billion, this backlog represented years of committed future revenue—the kind of visibility that capital-intensive manufacturing businesses crave.

But expansion at this pace created strains. Quality control became increasingly challenging as new plants ramped production. Supply chain complexity multiplied. And the battery division's capital requirements were consuming ever-larger shares of LG Chem's cash flow.

In parallel, the division ventured into energy storage systems (ESS) in the early 2010s, supplying batteries for grid-scale projects in Korea, while establishing the Ochang plant in 2004 as its first dedicated EV battery facility in South Korea. By the late 2010s, the division had solidified its role within LG Chem, driving innovations in pouch-type cells for automotive use and contributing substantially to the company's revenue through diversified applications in EVs and ESS. In 2020, recognizing the explosive growth in the global battery market driven by EV adoption, LG Chem announced plans to spin off the Energy Solution Business Division into an independent subsidiary.

The late 2010s brought one additional complication: legal warfare. In April 2019, LG Chem sued rival SK Innovation for allegedly stealing trade secrets related to EV battery manufacturing—a case that would drag through U.S. International Trade Commission proceedings and underscore the strategic value of battery intellectual property.

By 2020, the battery division accounted for approximately 38 trillion won of LG Chem's 48 trillion won market capitalization. The tail had grown large enough to wag the dog. Something had to change.

Investor Takeaway: The 2015-2020 period illustrates both the opportunity and the challenge of rapid scaling in capital-intensive industries. LG captured major customer wins but strained corporate resources. The multi-customer strategy—supplying Tesla, GM, Volkswagen, and others simultaneously—reduced concentration risk but required massive capital deployment.

VII. The Spinoff: Creating LG Energy Solution (2020)

In a glass-walled conference room in Seoul, LG Chem's board gathered in September 2020 to make one of the most consequential decisions in the company's 73-year history. After decades of nurturing its battery division through losses and into profitability, the parent company would set its most valuable child free.

In September 2020, LG Chem announced that it would spin off its battery business to cope with growing demand from global automotive manufacturers. LG Chem's battery business officially became a separate company and changed its name to LG Energy Solution Ltd. in December 2020.

The strategic logic was compelling on multiple dimensions. Enhance corporate value and stockholder value through concentration on the business area of expertise. Physical division where LG Chem possesses 100% of new battery corporation. Official launching of the new battery corporation 'LG Energy Solutions (tentative name)' from December 1. Expected to strengthen expertise in business sector and improve operational efficiency.

Through this corporate spin-off, LG Chem will be able to receive appropriate evaluation of business value for each of its business fields including the battery business. In addition, the increased corporate value with the growth of the new corporation will make it possible to increase corporate value of the mother company while maximizing stockholder value. In addition, it is expected that it will be possible to focus capacities on areas of expertise while allowing independent and prompt decision-making according to the business features, while upgrading management and operational efficiency. LG Chem plans to foster the new corporation to become the world's best energy solutions company.

The financial imperative was equally clear. LG Chem explained the decision was aimed at tackling two problems the company faces. First, the company said it was "under increasing financial pressure," as the need for investment continues to grow as it tries to increase battery production capacity at its facilities. When LG Energy Solution is set up, LG Chem can be free from funding pressure stemming from its battery business and its other businesses can cover their investments on their own.

The new spin-off company LG Energy Solution employs around 22,000 people, about 7,000 of them in South Korea and 15,000 in other countries. This global footprint reflected the extraordinary expansion of the previous five years—from a single Korean facility to a multi-continental manufacturing network.

The spinoff wasn't without controversy. Though LG Chem said "there is nothing confirmed about an IPO," the company's individual investors have opposed the spinoff with concerns that the listing will dilute the value of their stakes in LG Chem. In addition to the individual investors, the National Pension Service, which holds a 10.3 percent stake in LG Chem as the No. 2 stakeholder of the company, also announced that it would oppose the spinoff. Though the spinoff plan was approved, individual investors are still expressing their dissatisfaction with the decision by dumping their shares.

The concerns proved prescient. When LG Energy Solution eventually went public, LG Chem shareholders found themselves holding a stake in a petrochemicals company whose most valuable asset had been extracted—without a share swap that would have preserved their exposure to the battery business.

The decision was announced at a Sept. 17 board meeting. LG Chem expects to receive approval at an Oct. 30 stockholders meeting with LG Energy Solution officially taking charge of the battery business on Dec. 1, 2020.

The newly independent LG Energy Solution faced a world transformed by pandemic and possibility. COVID-19 had disrupted global supply chains but accelerated automotive electrification as governments poured stimulus money into green infrastructure. The company's order backlog stretched beyond the horizon, but so did its capital requirements.

Investor Takeaway: The spinoff structure—where LG Chem retained 100% ownership while preparing for an eventual IPO—allowed the parent company to capture full value from the battery business while giving LGES the operational independence to raise external capital. The shareholder controversy, however, illustrates the governance risks inherent in chaebol restructurings.

VIII. Crisis Management: The Chevy Bolt Recall (2021)

The phone call that every manufacturing executive dreads came in the summer of 2021. General Motors was recalling the Chevrolet Bolt—not a handful of vehicles, not a production run, but every single one built since 2016. The culprit: batteries from LG Energy Solution that could spontaneously catch fire.

In August 2021, GM recalled all 2017-2022 model year Bolt EVs and 2022 Bolt electric utility vehicles after multiple reports of battery fires. The recall covered an additional 59,392 Bolt EVs not covered under the previous recalls in November 2020 and July 2021.

The technical details were damning. The full battery recall was announced on August 20, 2021. Cause: manufacturing defects (a torn anode tab and folded separator) in lithium-ion battery cells (pouch type) supplied by LG Chem's LG Energy Solution may lead to a battery fire "in rare circumstances." Cells were produced in plants in South Korea and in Michigan.

Every Chevrolet Bolt EV and Bolt EUV that GM has made is under recall because their batteries could be defective and cause a fire. What is it about the batteries—lithium-ion cells sourced from LG Energy Solution and made on two different continents—that could have led to this?

The defects were subtle but lethal. A torn anode tab and a folded separator—each alone might not cause problems—but when both occurred in the same cell, they created conditions for internal short circuits and thermal runaway. The combination was rare enough to escape standard quality control but common enough to cause at least 13 confirmed vehicle fires.

GM and LG launched their own investigation into the Bolt EV battery fires and discovered what they described as "two rare manufacturing defects" as the root cause, which led to the recall of all Bolts EVs. At the time, GM asked Bolt owners to park their vehicles outdoors as a safety precaution and to not charge them overnight. The automaker also instructed Bolt owners to set their vehicle's battery charging limit to 90% state of charge.

For LG Energy Solution, the timing could not have been worse. The company was preparing for what would become South Korea's largest-ever IPO. Last June, the Seoul-based firm suspended its IPO process on the heels of a series of recalls from General Motors' Chevrolet Bolt electric vehicles due to possible battery cell defects that could increase fire risk.

The financial cost was staggering. LG Energy Solution agreed to pay $1.9 billion of the approximate $2 billion in costs. This represented a substantial portion of the company's annual revenue—a painful but necessary acknowledgment of responsibility.

General Motors and LG are establishing a $150 million fund to compensate Chevrolet Bolt owners after a faulty battery caused some of the electric vehicles to burst into flames. The $150 million is part of a legal settlement between GM and Bolt owners who filed a class-action suit against the Michigan automaker in 2020 for allegedly selling them a vehicle with a defective battery. Bolt owners who installed special software that GM offered to fix the battery issue can receive $1,400 from the fund, according to court documents filed late Thursday in Michigan. Bolt owners who sold their car before that date, or drivers who leased the Bolt before then, are eligible for a $700 payment. "GM, LG Energy Solution and LG Electronics have agreed to a settlement with plaintiffs to resolve class-action litigation related to the Bolt EV battery recall."

The recovery required more than money—it demanded operational transformation. LG Energy Solution implemented enhanced quality controls, including updated manufacturing processes to eliminate the identified cell defects. Production resumed under stricter inspections, with GM engineers embedded in LG facilities to oversee quality assurance.

Investor Takeaway: The Bolt recall illustrates the catastrophic risks inherent in battery manufacturing. Defects measured in fractions of a percentage can translate into billions of dollars in costs and lasting reputational damage. The episode likely strengthened GM-LG collaboration through shared adversity but also highlighted the quality control challenges of rapid capacity expansion.

IX. The Record-Breaking IPO (January 2022)

Seven months after agreeing to pay GM $1.9 billion for the Bolt recall, LG Energy Solution returned to the IPO market—and shattered every record in Korean financial history.

South Korea's LG Energy Solution soared in its first day of trading in Seoul, following the country's biggest initial public offering on record. The world's second-largest battery maker soared to close 68% above its IPO price of 300,000 won, even as the nation's benchmark Kospi tumbled into a bear market. Now worth over $98 billion, it's bigger than every other listed Korean company except Samsung Electronics Co.

The numbers were staggering. LG Energy's IPO raised about $10.7 billion, with shares being sold at the top of an offered range. It was the second-largest offering in the world over the past year after Rivian Automotive Inc., and was about 2.5 times the size of Korea's previous record listing, Samsung Life Insurance Co.

Retail investor demand bordered on mania. More than 4.4 million retail investors bid a record 114 trillion won ($95bn) to subscribe to shares in the IPO, Asia's largest equity fund raising since China's Alibaba Group Holding Ltd raised $12.9 billion in its Hong Kong secondary listing in 2019.

The market capitalization of LG Energy stood at $98.3 billion (118 trillion KRW) at the close of trading on local stock exchanges, making it the country's second most valuable firm after Samsung Electronics.

The confidence reflected the company's market position. The battery maker supplies key automakers like Tesla, General Motors, Hyundai Motor and Stellantis and maintains the highest number of joint ventures with them among local rivals. LG Energy Solution CEO Kwon Young-soo was confident in the firm's growth, saying its market share would soon overtake that of China's CATL.

LG Corp. co-CEO Kwon Young-soo was appointed as the chief executive officer of LG Energy Solution Ltd. The incoming CEO, co-chief executive of LG Corp. along with group Chairman Koo Kwang-mo, is expected to push forward with the battery maker's initial public offering shelved after the recall of General Motors' electric vehicles equipped with LG's battery cells this year.

The IPO proceeds were earmarked for aggressive expansion. The company announced plans to increase manufacturing capacity across North America, Europe, and Asia, with a particular focus on markets where Western automakers were seeking alternatives to Chinese suppliers. The geopolitical tensions between the U.S. and China had created an unexpected opportunity: customers willing to pay premium prices for non-Chinese batteries.

Yet the IPO also revealed tensions. LG Chem shareholders complained that the spinoff structure—which kept 81.8% of LGES shares with the parent but didn't offer LG Chem investors direct shares in the battery company—had diluted their stake in the group's most valuable asset. The controversy highlighted governance concerns that would continue to shadow the company.

LGES was listed on the Korea Exchange (KRX) on January 27, 2022 and the closing price after the first day was 68% above the IPO - 505,000 won ($418). It was even higher during the beginning of the day - 598,000 won ($494).

Investor Takeaway: The IPO priced LG Energy Solution at a substantial premium, reflecting investor confidence in the EV transition and the company's position as a non-Chinese supplier to Western automakers. The 68% first-day pop suggested shares were underpriced—or that retail enthusiasm had become detached from fundamentals. The subsequent share price decline would prove the latter interpretation correct.

X. The Joint Venture Strategy: Ultium & Beyond (2020–2025)

If the 2010s established LG as a battery supplier, the 2020s positioned it as a strategic manufacturing partner. The Ultium Cells joint venture with General Motors became the template for a new kind of relationship between battery makers and automakers—one based on shared investment, shared risk, and deep operational integration.

Ultium Cells, a joint venture of LG Energy Solution and General Motors, announced a $2.6 billion investment to build its third battery cell manufacturing plant in the United States. The facility will be located in Lansing, Michigan. The new battery cell plant is expected to create 1,700 new jobs when the facility is fully operational.

The Ultium partnership went beyond simple supply relationships. GM contributed $2.3 billion to a facility in Spring Hill, Tennessee, while the partners invested jointly in Warren, Ohio, and Lansing, Michigan. Ultium Cells expects the facility will have 50 gigawatt hours of battery cell capacity when running full production. GM's proprietary Ultium battery technology is at the heart of the company's strategy to compete for nearly every EV customer in the marketplace. Ultium batteries are unique in the industry because the large-format, pouch-style cells can be stacked vertically or horizontally inside the battery pack.

The partnership dynamics evolved as the EV market matured. In late 2024, GM announced a restructuring that highlighted both the challenges and opportunities of the JV model. General Motors has reached a non-binding agreement to sell its stake in the nearly completed Ultium Cells LLC battery cell plant in Lansing, Michigan to its joint venture partner LG Energy Solution. The transaction is expected to close in the 2025 first quarter, subject to customary closing conditions. GM expects to recoup its investment in the facility. The transaction does not change GM's ownership interest in Ultium Cells LLC. GM will continue to leverage the Ultium Cells plants in Warren, Ohio and Spring Hill, Tennessee to meet growing demand for its electric vehicles.

General Motors Co. is selling its stake in the Lansing Ultium Cells LLC battery plant to its joint-venture partner LG Energy Solution in another move to generate better returns on its invested capital. GM expects to recoup $1 billion from the investment.

The staff will become LG employees upon completion of the sale, which is expected to close by May 31. LG will instead manufacture batteries for Toyota at the plant, as the carmaker has agreed to shift a $1.5 million battery order from a different Michigan plant to the Lansing plant after LG's deal with GM is finalized.

Technology evolution remained central to the partnership's value. The companies announced development of next-generation chemistries that could maintain LG's technological edge. The Spring Hill facility began converting to lithium iron phosphate (LFP) production—a chemistry previously dominated by Chinese manufacturers—to offer lower-cost options for mass-market vehicles.

The JV model extended beyond GM. LG Energy Solution established similar partnerships with Stellantis (NextStar Energy in Canada), Hyundai Motor Group, and Honda. Each partnership brought capital contributions from automakers, reducing LG's balance sheet strain while locking in long-term customer relationships.

LG Energy Solution and Stellantis' joint venture (JV), NextStar Energy, operator of Canada's first large-scale lithium-ion (Li-ion) battery manufacturing plant, is expanding to produce energy storage system (ESS) batteries. Beginning in November, the Windsor, Ontario, plant will start producing battery cells designed for commercial and grid-scale energy storage solutions. NextStar notes the expansion of AI data centres as an important driver of demand for ESS cells. To support this expansion, the company has added lithium iron phosphate (LFP) cell chemistry to its production.

Investor Takeaway: The JV strategy allows LG to expand capacity with reduced capital intensity while building customer stickiness. However, the GM Lansing transaction revealed that automaker partners may scale back commitments when EV demand disappoints, creating asset repurposing challenges. The model works best when interests align; misalignment creates renegotiation risk.

XI. The Competitive Landscape & CATL Challenge (2022–Present)

The battery industry's competitive dynamics shifted dramatically after LG Energy Solution's IPO. The company that once led global market share found itself in a fierce battle with Chinese giant CATL—and losing ground.

CATL continued to remain the world's largest power battery maker in 2024, with a 37.9 percent share that is higher than the 36.6 percent in 2023. CATL continued to be the world's largest power battery manufacturer in 2024, followed by BYD. The Chinese power battery giant continued to rank first in the world with a 37.9 percent share in 2024 and remained the only battery supplier in the world with a market share of more than 30 percent.

The Chinese battery giant maintained its global leadership with a 36.6 percent market share during January-September 2025, remaining the only supplier exceeding 30 percent market share worldwide. The South Korean company maintained third place with a 9.8 percent share during January-September, down from 11.5 percent in the same period last year.

The market share decline reflected structural challenges. CATL benefited from dominant position in China—the world's largest EV market—while LG's strength lay in Western markets growing more slowly than expected. CATL's lithium iron phosphate (LFP) technology also gained ground over LG's nickel-cobalt-manganese (NCM) chemistry, particularly in cost-sensitive standard-range vehicles.

CATL is the biggest EV and energy storage battery manufacturer in the world, with a global market share of around 38% and 36.5% respectively in 2025. It is headquartered in Ningde, Fujian province.

Geopolitics created both threats and opportunities. Western automakers' efforts to diversify supply chains away from China benefited LG as a Korean alternative. CATL holds 38% global market share — well ahead of competitors like BYD and LG Energy Solution — and has been the global leader in EV battery installed capacity since 2017. Chemistry splits are shifting fast.

LG's response emphasized its non-Chinese positioning. LG Energy Solution is the third-largest battery maker for electric vehicles with about 11% global share in 2024, according to SNE Research. The EV battery segment is the largest revenue contributor, which accounted for more than 60% of total revenue in 2024. LGES also manufactures batteries for mobility, mobile phones, laptops, electrical devices, and energy storage systems. The company was spun off from LG Chem's battery division in December 2020 and listed on the Korea Exchange in January 2022. It has global manufacturing facilities in Korea, China, Poland, and the United States. Key customers include General Motors, Tesla, Volkswagen, Hyundai, and Stellantis.

Credit rating agencies took note of the challenging environment. S&P Global Ratings downgraded LG Energy Solution to 'BBB' from 'BBB+' on March 4, 2025. The downgrade is attributed to high capital expenditure and challenging operating conditions for the chemical and electric vehicle (EV) battery businesses.

Global credit rating agency Moody's has downgraded the credit ratings of both LG Chem and its subsidiary LG Energy Solution by one notch each. According to the financial investment industry on November 17, Moody's recently lowered LG Chem's credit rating from 'Baa1' to 'Baa2.' This marks another downgrade in less than a year since it was reduced from A3 to Baa1 in December last year. The credit rating for LG Energy Solution was also changed to 'Baa2,' the same as LG Chem. Baa2 is equivalent to 'BBB' by other major global credit rating agencies.

Investor Takeaway: The competitive dynamic increasingly resembles a two-tier market: CATL dominates China and cost-sensitive global segments; Korean suppliers like LG command premiums in Western markets where geopolitical concerns outweigh cost differentials. Sustainability of this premium depends on maintaining Western government support and customer willingness to pay for supply chain security.

XII. Recent Developments & Pivoting to ESS (2024–2025)

The headquarters of LG Energy Solution in Seoul's Yeouido district hums with strategic recalculation. As EV demand growth slowed across Western markets in 2024-2025, the company executed a pivot that may define its next decade: an aggressive push into energy storage systems (ESS).

For the full year 2024, the company reported KRW 25.6 trillion in consolidated revenue and KRW 575.4 billion in operating profit, a year-on-year decrease of 24.1 percent and 73.4 percent, respectively.

"Last year, we actively responded to EV demand in North America," said Chang Sil Lee, CFO of LG Energy Solution. "At the same time, sales in Europe decreased due to slow EV market growth, while average selling price (ASP) also declined because of continued metal price impact, leading to a decrease in our full-year revenue."

The ESS pivot emerged from strategic necessity. Despite a slowdown in electric vehicle (EV) sales in the US, LG Energy Solution experienced a quarterly rise in profits, driven in part by increasing demand for energy storage. The South Korean battery and energy storage system manufacturer announced its Q3 2025 financial results yesterday, posting KRW601.3 billion in operating profit for the quarter and KRW5.7 trillion in consolidated revenue.

LG ES has retooled EV battery production lines at its Holland, Michigan, gigafactory complex to achieve 17GWh of annual production capacity for lithium iron phosphate (LFP) energy storage system (ESS) cells. LG ES plans to ramp that up to 30GWh of LFP ESS cell production in the US by the end of 2026.

The rationale was compelling. LG ES will nearly double energy storage cell production capacity at its Michigan, US, factory by the end of 2026. Although EVs look set to remain the much bigger overall market, in the short term, LG ES identified recent policy changes that presented uncertainties, including the phaseout of the consumer EV subsidy in the US by the end of September and import tariffs creating cost pressures for OEMs. For the rest of 2025, its investment activities in the EV space are more R&D-focused. The company hopes to develop EV batteries that can be charged in under ten minutes.

Rather than build new ESS-dedicated facilities, LG converted existing EV lines—a capital-efficient approach that leveraged sunk costs. Putting on hold a dedicated 16GWh ESS battery factory in Arizona is related to that, as the company is now looking at adapting EV lines to the ESS segment, rather than build ESS lines from scratch.

LG Energy Solution said on Monday that it will start manufacturing in 2027 lithium iron phosphate (LFP) batteries for energy storage systems (ESS) applications in South Korea. Construction for the new line to be at its Ochang facility will start near the end of this year.

The European strategy mirrored the U.S. pivot. LG Energy Solution will unveil a new 20-foot container-type energy storage system equipped with made-in-Europe lithium iron phosphate battery cells at InterBattery Europe 2025 held at Messe Munich. LG Energy Solution plans to begin producing ESS batteries at its Wroclaw plant in Poland at the end of this year after setting up ESS-dedicated production lines there. Through this, the company expects to secure a stable local supply and a capacity that efficiently manages the needs of customers in Europe.

The company maintained optimism despite near-term headwinds. The global battery market, encompassing the EV, ESS, and IT sectors, is expected to grow by over 20 percent annually starting in 2025. For the EV market, the company expects its first-mover advantages in the North American battery market to continue to expand, driven by the growing trend of protectionism. Based on its key business initiatives for this year, LG Energy Solution announced its goal to achieve a 5-10 percent year-on-year increase in annual consolidated revenue in 2025.

The company also aims to reduce this year's capex by 20-30 percent compared to last year, by adjusting the pace of investment and maximizing the utilization of existing sites. In addition, the estimated capacity eligible for the IRA tax credits this year is expected to be around 45-50GWh.

Investor Takeaway: The ESS pivot demonstrates operational flexibility and capital discipline. Converting EV lines to ESS production preserves optionality while reducing cash burn. The success of this strategy depends on ESS demand materializing at sufficient margins—a bet on the renewable energy transition that parallels the original bet on EVs.

XIII. Bull Case vs. Bear Case: Frameworks for Analysis

Understanding LG Energy Solution requires systematic analysis through multiple strategic lenses. Here we apply Porter's Five Forces and Hamilton Helmer's Seven Powers frameworks to illuminate the company's competitive position.

Porter's Five Forces Analysis

Threat of New Entrants: MODERATE-HIGH The battery industry's capital requirements exceed $1 billion per gigafactory, creating significant barriers. However, Chinese manufacturers have demonstrated willingness to build unprofitable capacity, and automakers (Tesla, BYD) increasingly bring manufacturing in-house. Government subsidies in multiple countries lower barriers for politically favored entrants.

Bargaining Power of Suppliers: MODERATE Critical raw materials (lithium, cobalt, nickel) concentrate in few geographies, giving mining companies pricing power. LG has invested upstream (lithium mining stakes) to mitigate this, but remains vulnerable to commodity cycles and supply disruptions.

Bargaining Power of Buyers: HIGH Automotive customers are sophisticated, well-capitalized, and increasingly willing to dual-source or vertically integrate. Tesla produces batteries in-house; GM and Ford maintain multiple suppliers. Customers can credibly threaten to switch suppliers or bring production in-house.

Threat of Substitutes: LOW-MODERATE Lithium-ion chemistry dominates EVs and will for this decade. Solid-state batteries remain years from commercialization. Hydrogen fuel cells serve different applications (heavy trucking, long-haul). However, chemistry evolution (LFP vs NCM) creates substitution risk within lithium-ion.

Competitive Rivalry: VERY HIGH CATL, BYD, Panasonic, Samsung SDI, and SK On compete aggressively. Chinese manufacturers operate with lower margin expectations and government backing. Overcapacity drives pricing pressure. Technology advantages prove temporary as competitors rapidly iterate.

Hamilton Helmer's Seven Powers Analysis

Scale Economies: PRESENT but CHALLENGED Battery manufacturing benefits from scale, with costs declining roughly 15-20% for each doubling of cumulative production (Wright's Law). However, CATL's scale advantage over LG creates ongoing cost disadvantage that requires premium pricing to offset.

Network Effects: ABSENT Unlike platforms, batteries gain no value from other users. However, the JV model creates customer lock-in through co-investment—a quasi-network effect based on shared capital commitment rather than usage.

Counter-positioning: FADING LG's original counter-position—chemistry expertise from a chemical company—has been replicated by competitors. The current counter-position—non-Chinese supplier to Western markets—depends on geopolitical dynamics rather than structural advantage.

Switching Costs: MODERATE Automotive battery integration requires 18-24 months of validation, creating meaningful switching costs. However, standardization trends and dual-sourcing reduce these barriers over time.

Branding: WEAK End consumers don't choose vehicles based on battery supplier. Brand value accrues to automakers, not component suppliers.

Cornered Resource: PRESENT LG's 80,000+ battery patents create defensive intellectual property. The company has demonstrated willingness to litigate (SK Innovation case). However, CATL's patent portfolio is comparable, and Chinese IP enforcement remains uncertain.

Process Power: PRESENT but VULNERABLE Decades of manufacturing experience create embedded organizational knowledge. The Bolt recall demonstrated that this advantage can be undermined by rapid expansion. Process power requires continuous reinvestment and quality focus.

Summary: Competitive Position

LG Energy Solution occupies a defensible but challenged position. The company benefits from scale, intellectual property, customer relationships, and geographic diversification. However, CATL's cost leadership, Chinese manufacturers' government backing, and EV demand volatility create persistent headwinds.

The bull case rests on: (1) sustained Western demand for non-Chinese batteries, (2) successful ESS pivot creating revenue diversification, (3) next-generation battery technologies (solid-state, high-nickel) where LG maintains R&D leadership, and (4) improved manufacturing discipline following the Bolt recall.

The bear case encompasses: (1) CATL's cost advantage proving insurmountable without tariff protection, (2) EV demand disappointing structurally rather than cyclically, (3) automaker vertical integration reducing addressable market, and (4) Chinese ESS competition repeating the EV pattern.

XIV. Key Metrics for Monitoring LG Energy Solution

For investors tracking LG Energy Solution's ongoing performance, three KPIs merit particular attention:

1. Global EV Battery Market Share (quarterly, via SNE Research)

Why it matters: Market share directly measures competitive position against CATL and other rivals. LG's share has declined from ~25% in 2020 to ~11% in 2024, reflecting CATL's gains and Chinese market dominance. Stabilization or recovery would signal improved competitiveness; continued decline suggests structural disadvantage.

What to watch: Share trends in North America and Europe specifically (where LG has advantages) versus global share (which includes China, where LG is weak). Relative performance against Korean peers (Samsung SDI, SK On) indicates whether challenges are company-specific or industry-wide.

2. Order Backlog Value and Composition

Why it matters: Multi-year order backlogs provide revenue visibility rare in most industries. The composition—EV vs ESS, geography, customer concentration—reveals strategic positioning. Changes in backlog signal future revenue trajectory 12-24 months ahead.

What to watch: Not just total backlog but whether additions come from existing customers or new relationships. ESS backlog growth would validate the strategic pivot. Customer concentration risk (particularly Tesla and GM dependence) deserves monitoring.

3. Capacity Utilization and IRA Tax Credit Eligible Production

Why it matters: With substantial fixed costs, utilization rates drive profitability more than almost any other factor. IRA tax credits (~$35/kWh for domestic production) provide margin support that makes U.S. production profitable at utilizations that would lose money elsewhere. The company guides 45-50GWh of IRA-eligible production for 2025.

What to watch: Quarterly utilization rates by geography (higher in North America is better). Any changes to IRA eligibility rules under new U.S. administration. Ratio of IRA credits to reported operating profit—currently, U.S. production incentives represent the majority of profitability.

XV. Regulatory and Risk Considerations

Investors should carefully consider several material risks and regulatory factors:

U.S. Policy Uncertainty: The Inflation Reduction Act's production tax credits (~$35/kWh) significantly enhance LG's U.S. profitability. Changes to these policies under the current administration could substantially impact economics. The company disclosed that IRA credits of approximately KRW 1.4 trillion contributed to 2024 results; without these credits, the battery business would have reported operating losses.

Tariff and Trade Policy: U.S. tariffs on Chinese battery components benefit LG as a Korean alternative. However, tariff policy changes could either strengthen or undermine this advantage. The recently implemented rules requiring non-Chinese content for ITC investment tax credit eligibility particularly favor Korean manufacturers.

Credit Quality: Both S&P and Moody's downgraded LG Energy Solution and parent LG Chem in 2025, citing elevated debt from capacity expansion and challenging operating conditions. The company's debt-to-EBITDA ratio reached approximately 3.5x in 2025. Further downgrades could increase financing costs and constrain capital spending flexibility.

Warranty and Product Liability: The Bolt recall resulted in approximately $1.9 billion in costs to LG. While quality controls have been enhanced, battery fires remain a tail risk. The company maintains warranty provisions for potential recalls; the adequacy of these provisions involves management judgment about defect rates and repair costs.

Customer Concentration: Key customers GM, Tesla, and Volkswagen represent substantial revenue concentration. Loss of any major customer relationship, or significant reduction in their EV production plans, would materially impact results.

Technology Evolution: Next-generation battery chemistries (solid-state, sodium-ion) could disrupt lithium-ion dominance within the decade. LG has research programs in these areas but commercialization timelines remain uncertain. CATL's recent solid-state announcements suggest competitive pressure in emerging technologies.

XVI. Conclusion: The Long Game Continues

The story of LG Energy Solution is ultimately a story about time horizons. The company's founders bet in 1992 that rechargeable batteries would transform transportation—a bet that took three decades to validate. They absorbed twenty years of losses while competitors dismissed the EV market as a curiosity. They built manufacturing capabilities that couldn't be replicated quickly, accumulated intellectual property that couldn't be invented overnight, and cultivated customer relationships that couldn't be purchased at any price.

That patient capital created today's LG Energy Solution: a $77 billion company supplying batteries to thirteen of the world's top twenty automakers, operating factories on three continents, holding more battery patents than any competitor, and generating—finally, after all those years—real profits.

But the game isn't over. CATL's relentless cost reductions challenge LG's margins. Chinese manufacturers' government backing creates unfair competitive dynamics. EV adoption has slowed in Western markets just as capacity investments peaked. Credit ratings have declined. The ESS pivot, while strategically sound, remains unproven at scale.

The next chapter will test whether LG Energy Solution's historical advantages—chemical expertise, Western customer relationships, non-Chinese positioning—can sustain premium pricing as battery commoditization accelerates. The company that once bet everything on a technology the world didn't yet need must now prove it can compete in a market the world very much wants.

For investors, LG Energy Solution represents a levered bet on the electric future—and on the proposition that in complex manufacturing, patient capability-building creates advantages that fast money cannot easily replicate. The Koo family's cosmetics company has come a long way from Lucky Cream. Where it goes from here depends on whether the qualities that built this business—technical depth, strategic patience, operational discipline—can overcome the challenges of competing against a Chinese industrial juggernaut with different economics and different time horizons.

The long march continues.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube