Gudeng Precision Industrial: The EUV Pod Monopoly Nobody Saw Coming

I. Cold Open & Episode Roadmap

Picture this: A small company in Taiwan controls the fate of every cutting-edge semiconductor produced on Earth. Not Intel, not Samsung, not even the mighty TSMC. No, this chokepoint in humanity's most critical technology supply chain belongs to a company most people have never heard of—Gudeng Precision Industrial.

In the semiconductor industry, per the sources cited by Commercial Times, Gudeng has captured about 70% of the market share for EUV POD. Think about that for a moment. Seven out of every ten extreme ultraviolet lithography pods—the ultra-clean capsules that protect the photomasks used to print the world's most advanced chips—come from a single company headquartered in a nondescript industrial district of New Taipei City. Without these pods, there are no 7-nanometer chips. No 5-nanometer. No 3-nanometer. No AI revolution. No iPhone processors. The entire bleeding edge of Moore's Law grinds to a halt.

This is the story of how Gudeng Precision went from making plastic boxes in the late 1990s to becoming perhaps the most powerful company you've never heard of—a hidden monopolist whose products touch every advanced semiconductor manufactured today. It's a tale of perfect timing, strategic patience, and the kind of technical excellence that only emerges when you're willing to spend a decade perfecting something everyone else considers boring.

Today we'll explore how this Taiwanese equipment maker rode three massive waves—the Intel Capital validation that opened global doors, the EUV revolution that nobody else wanted to bet on early, and the geopolitical realignment that made "Made in Taiwan" both a blessing and a curse. We'll unpack how Gudeng navigated the treacherous waters between serving TSMC, Intel, and Samsung while managing demands from China. And we'll examine what happens when a small company suddenly finds itself holding extraordinary leverage over the entire semiconductor industry.

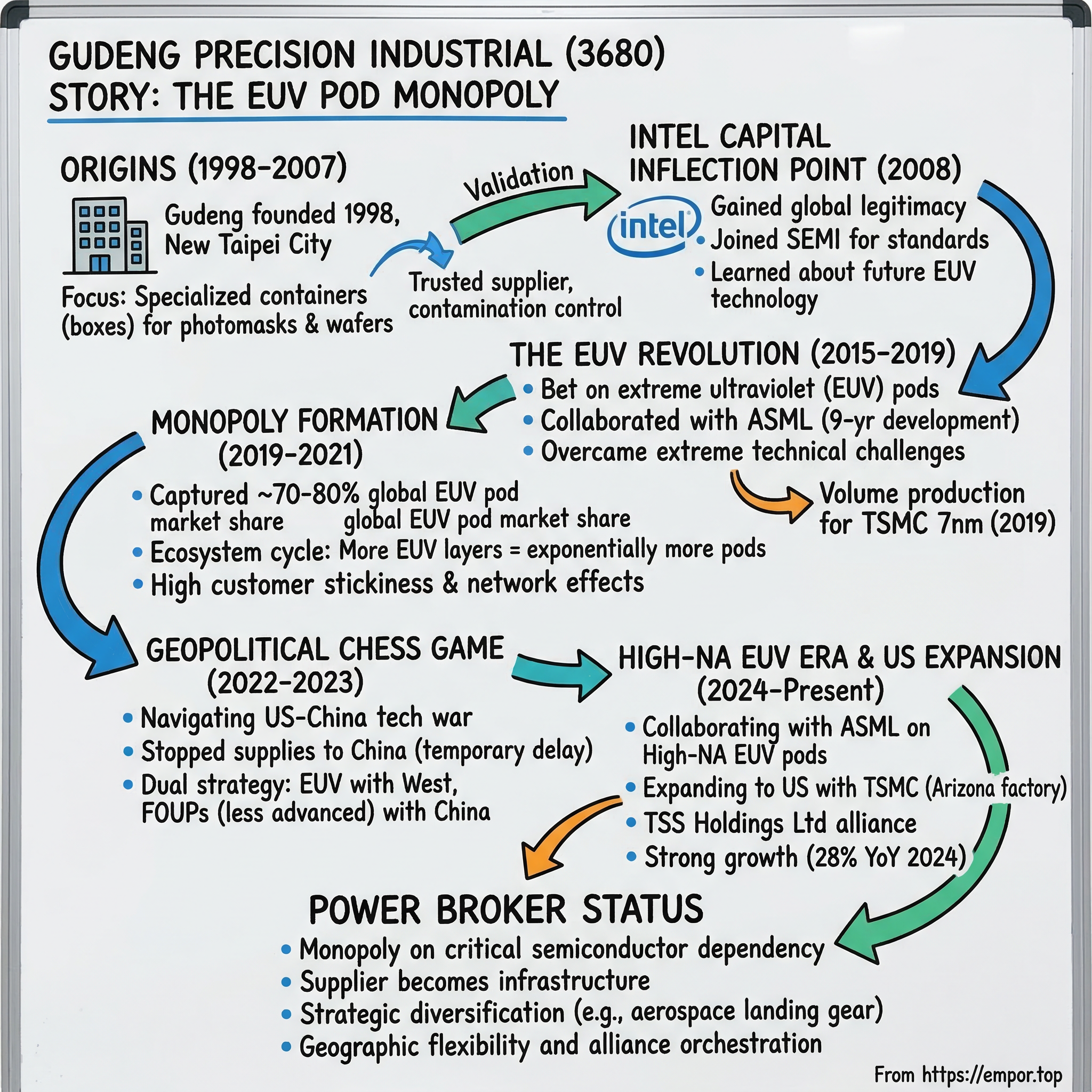

II. Origins: The Humble Beginning (1998-2007)

Gudeng Precision Industrial Co., Ltd. was incorporated in 1998 and is headquartered in New Taipei City, Taiwan. The late 1990s in Taiwan buzzed with semiconductor ambition. TSMC had already proven the foundry model could work, and dozens of equipment suppliers were sprouting up around Hsinchu Science Park, each hoping to catch the rising tide.

But Gudeng's founders didn't chase the glamorous side of chipmaking. While others rushed toward lithography tools or deposition equipment—the headline-grabbing machinery—Gudeng focused on something decidedly unglamorous: boxes. Specifically, the specialized containers that protect photomasks and wafers as they move through semiconductor fabs. The company offers wafer handling solutions, including shipping boxes, cassette boxes, wafer cassettes, and front opening wafer transfer boxes, as well as FOUP products; and reticle handling solutions, such as reticle boxes, nikon / canon reticle boxes, RSP 150, RSP 200, EUV PODs, TFT-LCD large size reticle boxes, assembled large-size reticle boxes, and other accessories.

Imagine trying to explain your business at a dinner party: "We make the boxes that hold the templates that print circuits onto silicon wafers." Not exactly riveting conversation. But this boring foundation would prove to be Gudeng's greatest strategic asset.

In those early years, the company built its reputation through relentless focus on contamination control. A single particle of dust—smaller than a virus—could ruin an entire batch of chips worth millions. Gudeng's boxes weren't just containers; they were mobile clean rooms, maintaining particle counts that made hospital operating theaters look filthy by comparison. The company developed proprietary materials and sealing technologies that pushed cleanliness to new extremes.

By 2005, Gudeng had become a trusted supplier to Taiwan's semiconductor ecosystem, but remained largely unknown outside the island. Revenue grew steadily but unremarkably. The company was profitable, reliable, and thoroughly regional—a solid tier-two supplier in a market dominated by American and Japanese giants like Entegris and Shin-Etsu. Nobody outside Taiwan's semiconductor cluster paid much attention to this maker of specialized plastic boxes.

That anonymity was about to end. Because sometimes in technology, the most powerful position isn't at the cutting edge—it's in the boring infrastructure that everyone needs but nobody wants to build.

III. The Intel Capital Inflection Point (2008)

November 2009, Huntington Beach, California. At Intel Capital's 10th annual CEO Summit, something unusual happened. Among the cloud computing pioneers and social media platforms receiving investment, The new investments, almost all led by Intel Capital, include U.S.-based Joyent (cloud computing) and Active Storage (RAID storage systems for Apple* users), Korea-based Crucialtec (optical modulation technology), Taiwan-based Gudeng Precision Industrial Co (semiconductor front-end equipment manufacturing), Japan-based V-cube (Web-based videoconferencing systems), China-based Phoenix New Media (Web information portal) and United Arab Emirates-based NeuString (telco pricing analytics software). Gudeng Precision Industrial Co (Taipei, Taiwan) is a semiconductor front-end equipment manufacturer that helps customers enhance product yield and reduce production cost by providing customized products with innovative design concepts. Presently, Gudeng Precision is the world's leading photomask and wafer handling total solution provider, and the company's products are accepted and certificated by worldwide tier-one customers. Gudeng Precision will use the funding to expand business in China and enhance working capital.

But the Intel investment wasn't really about the money. It was about what came next. Gudeng Precision Industrial, a member of TSMC Grand Alliance and Taiwan's first semiconductor equipment maker allowed to join SEMI in setting next-generation equipment standards after gaining investment from Intel Capital in 2008, suddenly had access to something far more valuable than cash: legitimacy on the global stage.

Think about the psychology here. You're a semiconductor purchasing manager at a major chipmaker. Two suppliers pitch you on photomask storage solutions. One is a well-known American company. The other is a Taiwanese firm you've never heard of—except wait, Intel Capital just invested in them. Intel doesn't make small bets on semiconductor infrastructure. If they're backing this company, what do they know that you don't?

The SEMI membership was even more significant. SEMI—the Semiconductor Equipment and Materials International association—essentially functions as the United Nations of chip equipment. When new standards are set for next-generation tools, SEMI members get to shape those standards. For a Taiwanese equipment maker to join this club in 2008 was like a minor league baseball player suddenly getting invited to rewrite the rules of Major League Baseball.

Bill Chiu, Gudeng's chairman, understood the moment perfectly. This wasn't just investment; it was an invitation to the global semiconductor equipment oligopoly. Intel had essentially vouched for Gudeng's technology and, more importantly, signaled that the era of Western equipment monopolies might be ending. Asian suppliers weren't just manufacturers anymore—they could be innovators.

The Intel validation also came with unexpected benefits. Suddenly, Gudeng engineers were in rooms with Intel's advanced development teams, learning about process nodes that wouldn't reach production for years. They heard whispers about something called extreme ultraviolet lithography—a technology so complex and expensive that most equipment makers considered it science fiction. Intel believed EUV would eventually work. And now Gudeng knew it too.

This knowledge would prove invaluable. Because while competitors focused on optimizing for existing deep ultraviolet (DUV) processes, Gudeng quietly began developing products for a future that hadn't arrived yet—a future where light itself would be pushed to its physical limits.

IV. The EUV Revolution: Betting on the Future (2015-2019)

The year 2015 marked a turning point in semiconductor manufacturing. After decades of delays and billions in development costs, ASML's extreme ultraviolet lithography machines were finally approaching commercial viability. The industry held its breath. Would EUV actually work at scale, or would it join the graveyard of promising technologies that never quite delivered?

For Gudeng, this wasn't a theoretical question. The company had spent years preparing for this moment, developing specialized pods designed specifically for EUV photomasks. These weren't just upgraded versions of existing products. EUV masks operate in near-vacuum conditions, exposed to radiation that would destroy conventional materials. The pods needed to maintain cleanliness levels that pushed the boundaries of what was physically possible while surviving an environment more hostile than outer space.

Gudeng Precision Industrial will soon obtain ASML's validation for its new-generation extreme ultraviolet (EUV) pods, joining rival Entegris, according to August 2018 industry reports. But this simple sentence understates the marathon that preceded it. Nine years. That's how long Gudeng had been working on EUV pod technology before receiving ASML's blessing.

The technical challenges were staggering. EUV light has a wavelength of just 13.5 nanometers—so short that it's absorbed by air itself. The pods couldn't just be clean; they had to maintain a perfect vacuum seal while allowing for rapid loading and unloading in production environments. A single molecular contaminant could scatter EUV light and ruin the pattern. Gudeng developed new polymers, revolutionary sealing mechanisms, and contamination detection systems that operated at the molecular level.

Then came the moment of truth. Gudeng Precision Industrial is scheduled to kick off volume production of extreme ultraviolet (EUV) pods for TSMC's EUV-based 7nm node manufacturing at the end of March 2019. TSMC had committed. The world's most advanced foundry would trust its EUV production to Gudeng's pods.

The dominos fell quickly. TSMC's adoption meant validation at the highest level. Intel and Samsung, the only other companies with the resources to afford ASML's EUV machines, took notice. Chiu said the firm's shipments of EUV pods will continue to grow robustly in 2021 along with increasing adoption of ASML's EUV lithography systems by leading foundries TSMC, Intel and Samsung.

Competitors scrambled to catch up, but Gudeng had a nine-year head start. By the time rivals achieved ASML certification, Gudeng had already optimized its manufacturing, built dedicated facilities, and most crucially, accumulated thousands of hours of real-world production data from TSMC's fabs. In semiconductor equipment, experience compounds. Every batch of pods provided data that improved the next generation. Every customer issue solved became institutional knowledge that competitors couldn't replicate.

The bet on EUV transformed Gudeng from a regional supplier to a global powerhouse. But this was just the beginning. The real power move was yet to come.

V. The Monopoly Formation: Scaling the Unscalable (2019-2021)

By late 2020, something extraordinary had happened in the semiconductor equipment market. Gudeng now commands over 80% of the global supply of EUV pods as it is the major supplier of such devices for TSMC, which has dominated the 7/5nm foundry processes, according to industry sources. Eighty percent. In an industry where 30% market share usually counts as dominance, Gudeng had achieved something approaching total control.

How does a company go from newcomer to near-monopolist in under three years? The answer lies in the vicious cycle of semiconductor economics—except this time, it was virtuous for Gudeng.

EUV lithography is catastrophically expensive. A single ASML EUV machine costs over $200 million and requires a small army of PhD engineers to operate. Only three companies on Earth—TSMC, Samsung, and Intel—can afford to deploy EUV at scale. This concentration of customers might seem like a weakness, but for Gudeng, it became an incredible strength.

Chiu said Gudeng is enforcing capacity expansion for EUV pods at its plant in Tainan, southern Taiwan, able to satisfy ever-expanding demand from global clients. The Tainan facility represented more than just production capacity—it was a statement of intent. Built specifically for EUV pod manufacturing, the plant incorporated clean room technology that exceeded even TSMC's stringent requirements.

The economics were beautiful in their simplicity. Each new EUV machine ASML shipped created recurring demand for Gudeng's pods. But here's the kicker: as chip architectures grew more complex, they required more EUV layers. Earlier in the year, Gudeng was optimistic about TSMC's 3-nanometer mass production, through which it believes that it will experience growth for the next year and a half. Its EUV pods see higher demand as the transistor node size drops, with advanced processes such as 3-nanometer using up to eight times as many pods as the older 7-nanometer processes.

Eight times. When TSMC moved from 7nm to 3nm, they didn't just need more pods—they needed exponentially more. Every advance in Moore's Law became a multiplier for Gudeng's business.

The monopoly also had powerful network effects. As Gudeng dominated the market, they accumulated more production data than all competitors combined. This data improved their processes, which improved yields, which lowered costs, which made it even harder for competitors to justify entering the market. Why spend billions developing EUV pods when Gudeng already had 80% share and years of production experience?

But perhaps the most powerful moat was customer stickiness. Semiconductor fabs are the most expensive factories ever built, with TSMC's advanced facilities costing over $20 billion each. In this environment, nobody switches suppliers to save a few percent on pod costs. The risk of contamination, the cost of requalification, the potential for production delays—all these factors made Gudeng's customers incredibly reluctant to change suppliers once production was running smoothly.

By 2021, Gudeng wasn't just a supplier to the semiconductor industry. They were infrastructure—as essential and invisible as the clean room air filtration systems. You couldn't build advanced chips without them.

VI. The Geopolitical Chess Game (2022-2023)

December 2022 brought a moment that crystallized Gudeng's delicate position in the new semiconductor cold war. Taiwan's Gudeng Precision Industrial Co, which supplies equipment such as masks for EUV manufacturing, has stopped supplies to China, stating that this is not a suspension but instead a temporary delay.

The language—"not a suspension but instead a temporary delay"—was diplomatic poetry, a masterclass in saying everything while committing to nothing. Behind this carefully crafted statement lay months of agonizing strategic decisions.

Consider Gudeng's impossible position. On one side: the United States, wielding export controls like a sword, demanding that allies prevent China from accessing advanced semiconductor technology. On the other: China, Taiwan's largest trading partner, representing massive growth potential and, more ominously, making increasingly aggressive claims on Taiwan itself.

China is also trying to enter the advanced chip manufacturing market via Huawei Technologies Inc (華為), an industry insider said. Huawei wants Gudeng to build a production line in China to back a chip manufacturing fab, the person said. The request from Huawei wasn't just business—it was a test of loyalty, a demand that Gudeng choose sides in the technology war.

But Gudeng had another card to play: product differentiation. While EUV pods were clearly restricted technology, the company also manufactured FOUPs (Front Opening Unified Pods) for less advanced processes. As Chinese chipmakers accelerate new factory construction to reach self-sufficiency amid an intensifying trade dispute with the US, demand for Gudeng's 12-inch FOUPs is spiking, Chiu said. Gudeng, which commands a 40 percent share of China's FOUP market, expects FOUP revenue to grow up to 40 percent year-on-year, Chiu said, adding that similar growth is expected next year. The box-like FOUPs are used to ship, transport and store 12-inch wafers, which are unloaded from the FOUP within processing equipment to keep the wafers sterile.

This dual-track strategy was brilliant. Gudeng could maintain its critical EUV pod business with TSMC, Intel, and Samsung while still capturing growth from China's massive investment in trailing-edge capacity. They were simultaneously essential to both sides of the technology divide.

The numbers told the story. Revenue from China surged from 17% of Gudeng's total in 2022 to 31% in 2023, even as the company maintained its monopolistic position in EUV pods. They had somehow managed to have their cake and eat it too—at least for now.

But the tightrope act required constant balance. In board meetings, executives debated scenarios that sounded like spy novels. What if China invades Taiwan? What if the US demands complete cessation of all China business? What if TSMC itself is forced to choose between its American and Chinese customers?

Building a localized supply chain, rather than cost efficiency, has become the top priority for semiconductor companies when selecting new factory sites, as the COVID-19 pandemic has upended the normal production and supply of components and raw materials, Chiu said. "This [building localized supply chains] will be the top priority for us in the next three to five years," he said.

The message was clear: in the new world order, geography was destiny. Gudeng couldn't just be a Taiwanese company anymore. They had to be everywhere their customers needed them to be.

VII. The High-NA EUV Era & US Expansion (2024-Present)

The conference room at TSMC's Arizona facility hummed with tension in early 2024. Across the table, executives from Gudeng Precision outlined their plans for American expansion. But this wasn't just about following TSMC to the desert. Two years ago, Gudeng initiated the idea of forming an alliance with eight local semiconductor companies, creating a new company, TSS Holdings Ltd (德鑫半導體控股), focusing on its operations in the US. Member companies distribute and supply products to customers in the US, as well as provide real-time services through a more cost-effective approach, Gudeng said.

The TSS Holdings structure was unprecedented—a Taiwanese equipment alliance designed to recreate Taiwan's semiconductor ecosystem on American soil. Rather than going alone, Gudeng brought partners: automated material handling specialists, cleaning equipment suppliers, component manufacturers. It was supply chain replication at its most ambitious.

Meanwhile, the technology landscape was shifting again. Among them, Gudeng Precision is actively collaborating with ASML on next-generation High-NA EUV development, pushing into territory where even fewer companies could follow. High-NA EUV, with its promise of even smaller feature sizes, represented another multiplier opportunity. If regular EUV had created Gudeng's monopoly, High-NA might cement it permanently.

The collaboration with ASML went beyond customer-supplier dynamics. Gudeng engineers were embedded in ASML's development process, creating pods for machines that wouldn't ship for years. This forward integration meant Gudeng would be ready the moment High-NA reached production—another insurmountable head start over potential competitors.

About 10 companies are participating, including specialty plastic compounds producer Nytex Composites Co (耐特科技) and AblePrint Technology Co (印能科技), which specializes in key equipment used in advanced chip packaging technology, such as chip-on-wafer-on-substrate (CoWoS). The new products are expected to fuel the company's growth momentum, as one of its major customers is boosting CoWoS capacity in the second half of this year and another key customer is restarting its CoWoS projects following a two-year suspension, Gudeng said.

The CoWoS opportunity revealed another dimension of Gudeng's strategy. Advanced packaging had become critical as Moore's Law slowed. Instead of making transistors smaller, chipmakers were stacking chips vertically, creating 3D architectures that required entirely new types of protective containers. Gudeng was ready with products most competitors didn't even know they needed to develop.

Gudeng Precision, a key player in the semiconductor foundry supply chain, reported an October 2024 consolidated revenue of NT$389 million (approx. US$12.16 million). Cumulative revenue for the first ten months reached NT$5.458 billion, marking a 28% year-over-year growth and exceeding 2023's full-year total. The numbers were staggering. In an industry where 10% annual growth is considered healthy, Gudeng was putting up software-company-like expansion rates.

The US expansion wasn't just about following customers—it was about becoming undisplaceable. With production on three continents, deep technical partnerships with ASML, and a product portfolio spanning from legacy FOUPs to cutting-edge High-NA pods, Gudeng had evolved from monopolist to something more powerful: infrastructure too critical to displace.

VIII. Power Broker Status: Small Company, Big Leverage

In the pristine conference rooms of TSMC, Intel, and Samsung, a curious dynamic plays out. These companies—with market caps in the hundreds of billions—find themselves dependent on a supplier worth a fraction of their value. Gudeng controls about 70 percent of the world's EUV pod market, with TSMC and Intel Corp topping its customer list.

The leverage dynamics are fascinating. When you control 70% of a critical component with no ready substitutes, traditional supplier-customer relationships invert. Gudeng doesn't bid for contracts—customers compete for allocation. Price negotiations? When your product represents 0.01% of a fab's operating cost but could shut down the entire facility if unavailable, nobody haggles over price.

Gudeng Precision Industrial Co (家登精密), a key supplier of extreme ultraviolet (EUV) pods to Taiwan Semiconductor Manufacturing Co (TSMC, 台積電), yesterday said it is positive about growth for the next 18 months, as demand is expected to spike after its major customer's 3-nanometer chip begins mass production later this year. The consumption of EUV pods should increase rapidly in tandem with upgrades of process technologies, as more EUV layers would be used. Chipmakers use eight times more EUV pods for 3-nanometer process technology than for 7-nanometer technology, Gudeng said.

The exponential scaling created a beautiful business model. Every improvement in semiconductor technology directly multiplied Gudeng's revenue. They didn't need to innovate faster—they just needed their customers to keep pushing Moore's Law forward.

But with great power comes great scrutiny. Gudeng's executives learned to navigate a world where every decision had geopolitical implications. Expand to China? Washington watches. Restrict supplies to Huawei? Beijing notices. Build capacity in Japan? Seoul wonders why not Korea.

Gudeng has clinched agreements from General Electric Co, Boeing Co and Parker Hannifin Corp to supply aircraft landing gear barrels. To cope with rising demand, Gudeng plans to raise about NT$2.8 billion through issuing corporate bonds to fund the construction of a new factory in Tainan. Chiu said that Gudeng would become a major supplier in the aerospace segment, Aerospace Industrial Development Corp (漢翔航空) and EVA Airways Corp (長榮航空).

The aerospace diversification was strategic genius. By expanding beyond semiconductors, Gudeng reduced customer concentration risk while leveraging its core competency: making incredibly precise, incredibly clean containers for incredibly valuable objects. Whether photomasks or aircraft components, the underlying technology was the same.

The alliance strategy amplified Gudeng's influence further. Gudeng, which initiated the idea of forming an alliance at the beginning of this year, has joined forces with 7 local semiconductor companies, creating a new company TSS Holdings Ltd (德鑫半導體控股). TSS Holdings was formed in July with an initial capital of NT$160 million (US$5.02 million). Most of the alliance's members are equipment or key material, or component suppliers to TSMC, or hold crucial importance in the global semiconductor supply chain.

This wasn't just business development—it was ecosystem architecture. By organizing Taiwan's equipment suppliers into coordinated alliances, Gudeng positioned itself as the orchestrator of supply chain expansion. When TSMC needed suppliers in Arizona, they didn't have to negotiate with dozens of companies. They could work through Gudeng's alliance.

The power broker status came with unexpected benefits. Governments courted Gudeng, offering incentives to build local facilities. Competitors sought partnerships rather than confrontation. Even mighty ASML, the only company that could theoretically pressure Gudeng, chose collaboration over conflict.

IX. Playbook: Lessons from the Niche Dominator

Let's distill the Gudeng playbook—the repeatable strategies that transformed a plastic box manufacturer into a semiconductor kingmaker.

First, find the boring chokepoint. Everyone wants to build the sexy technology—the lithography machines, the AI chips, the quantum computers. But the real power often lies in the mundane components that everyone needs but nobody wants to make. Gudeng's photomask pods are perhaps the most boring product in the semiconductor stack. They're also utterly irreplaceable.

Second, commit early to uncertain technology. When Gudeng started developing EUV pods in 2010, many industry experts believed EUV would never work. The technology had been "five years away" for two decades. But Gudeng bet their future on it anyway, spending nine years perfecting products for machines that might never ship. When EUV finally arrived, they were the only ones ready.

Third, leverage anchor customers for development. Gudeng Precision Industrial is scheduled to kick off volume production of extreme ultraviolet (EUV) pods for TSMC's EUV-based 7nm node manufacturing at the end of March 2019. TSMC's commitment wasn't just a purchase order—it was product validation at the highest level. Once TSMC approved, Intel and Samsung had little choice but to follow. The anchor customer strategy de-risked the entire market development process.

Fourth, build switching costs through customization. Every semiconductor fab has slightly different requirements. Different clean room protocols, different handling systems, different contamination standards. Gudeng customizes pods for each customer's specific needs, creating products so integrated into the production process that switching suppliers would require re-engineering entire workflows.

Fifth, use geographic positioning as strategic advantage. Taiwan's location—physically close to major Asian markets, politically aligned with the West, culturally bridge between both—gave Gudeng unique flexibility. They could serve Chinese customers while maintaining US relationships, support Japanese expansion while working with Korean competitors. Geography became strategy.

Sixth, compound advantages through standards participation. Taiwan's first semiconductor equipment maker allowed to join SEMI in setting next-generation equipment standards after gaining investment from Intel Capital in 2008. By helping write the rules, Gudeng ensured their products would always be compliant. Competitors had to follow standards that Gudeng helped create.

The playbook's elegance lies in its simplicity. None of these strategies require massive capital or revolutionary technology. They require patience, focus, and the willingness to excel at something others consider beneath them. In a world obsessed with disruption, Gudeng achieved dominance through the decidedly undisruptive act of making better boxes.

X. Bear vs. Bull Case: The Future of Monopoly

Bear Case: The Cracks in the Foundation

The bear thesis on Gudeng starts with concentration risk that would make any risk manager sweat. Taiwan generates 70% of revenue. TSMC represents an even higher percentage of EUV pod sales. If anything happens to Taiwan—invasion, earthquake, political crisis—Gudeng's core business evaporates overnight.

The geopolitical tightrope grows more precarious daily. Taiwan's Gudeng Precision Industrial Co, which supplies equipment such as masks for EUV manufacturing, has stopped supplies to China, stating that this is not a suspension but instead a temporary delay. How long can Gudeng maintain this balancing act? Eventually, they may be forced to choose sides completely, losing either Chinese growth or Western technology access.

Customer concentration presents another vulnerability. Three companies—TSMC, Intel, and Samsung—represent essentially all EUV pod demand. If any develops internal capabilities or sponsors a competitor, Gudeng's monopoly could crumble. Intel, particularly, has a history of vertical integration when suppliers become too powerful.

Technology transitions loom. What happens after High-NA EUV? Directed self-assembly? Quantum lithography? Some future breakthrough that makes photomasks obsolete? Gudeng's entire business model depends on photolithography remaining the dominant chip manufacturing method.

Competition, while currently minimal, could emerge from unexpected directions. ASML itself could backward integrate. Chinese companies, freed from intellectual property concerns, could develop "good enough" alternatives. The monopoly that seems impregnable today could face assault from multiple directions tomorrow.

Bull Case: The Expanding Moat

But the bull case remains compelling. Start with the numbers: Cumulative revenue for the first ten months reached NT$5.458 billion, marking a 28% year-over-year growth in 2024. That suggests the firm's revenue could grow as much as 53 percent this year, after it posted a 28.91 percent increase to NT$6.55 billion last year, exceeding its 20 percent growth target. These aren't mature company growth rates—they're expansion phase dynamics.

High-NA EUV extends the runway considerably. Gudeng Precision is actively collaborating with ASML on next-generation High-NA EUV development. With machines costing $380 million each and only ASML making them, Gudeng's position as the pod supplier becomes even more entrenched. The capital requirements to compete have moved from difficult to essentially impossible.

The US expansion reduces geographic risk while opening new opportunities. Gudeng Precision Industrial Co (家登), the sole supplier of extreme ultraviolet (EUV) pods to Taiwan Semiconductor Manufacturing Co (TSMC, 台積電), yesterday said it is looking at setting up a factory in the US to align itself with TSMC's capacity expansion there. Gudeng is one of several TSMC suppliers that are considering following their customer in setting up operations in the US to provide on-site services. With production facilities across multiple continents, supply chain resilience improves dramatically.

Advanced packaging creates an entirely new growth vector. AblePrint Technology Co (印能科技), which specializes in key equipment used in advanced chip packaging technology, such as chip-on-wafer-on-substrate (CoWoS). The new products are expected to fuel the company's growth momentum, as one of its major customers is boosting CoWoS capacity in the second half of this year. As Moore's Law slows, advanced packaging becomes critical, and Gudeng is already positioned.

The learning curve advantages continue to compound. Every year of production data makes Gudeng's products better and competitors' catch-up efforts harder. With over a decade of EUV experience, the knowledge moat may be unbridgeable.

Market dynamics favor the incumbent. Semiconductor fabs represent hundreds of billions in capital investment. No procurement manager risks production delays to save basis points on pod costs. The asymmetric risk—tiny savings versus catastrophic failure—ensures customer retention remains high.

Finally, the semiconductor supercycle shows no signs of slowing. AI requires more advanced chips. Advanced chips require more EUV layers. More EUV layers require more pods. Gudeng sits at the beneficiary end of multiple exponential trends.

XI. Reflection: The Invisible Giant

There's something profound about Gudeng's anonymity. Here's a company that could, theoretically, single-handedly halt the production of every advanced semiconductor on Earth, yet most technology professionals have never heard its name. No Gudeng, no GPUs for AI training. No advanced processors for smartphones. No high-performance chips for data centers. The entire digital economy would freeze.

This invisibility is both weakness and strength. Weakness because Gudeng lacks the brand power to command premium valuations or attract top talent globally. Strength because anonymity means less scrutiny, less political pressure, less attention from potential competitors or regulators.

The Taiwan semiconductor ecosystem advantage cannot be overstated. Within a 100-kilometer radius of Gudeng's headquarters, you can find every type of supplier, service provider, and expertise needed for semiconductor manufacturing. This density of specialized knowledge doesn't exist anywhere else on Earth—not in Silicon Valley, not in Shenzhen, not in Seoul. It's the kind of ecosystem advantage that takes decades to build and may be impossible to replicate.

Building a localized supply chain, rather than cost efficiency, has become the top priority for semiconductor companies when selecting new factory sites, as the COVID-19 pandemic has upended the normal production and supply of components and raw materials, Chiu said. "This [building localized supply chains] will be the top priority for us in the next three to five years," he said. Gudeng is looking to form an alliance with local semiconductor equipment manufacturers and raw material suppliers to minimize the risk of supply disruptions, Chiu said.

The lesson for finding and building narrow but deep moats is clear: excellence beats breadth. Gudeng could have diversified into dozens of semiconductor equipment categories. Instead, they focused relentlessly on pods, becoming so good at this one thing that replacement became unthinkable. In a world that celebrates platforms and ecosystems, there's still enormous power in doing one thing better than anyone else.

What does this tell us about supply chain power in the AI era? As artificial intelligence drives demand for ever more powerful chips, the companies controlling key bottlenecks in the production process gain extraordinary leverage. Gudeng doesn't make AI chips, but without them, AI chips can't be made. They're the perfect example of how value accrues to chokepoints—not always to the most visible players, but to those who control critical dependencies.

Consider the broader implications. If a company making plastic boxes can achieve near-monopoly status in advanced semiconductors, what other "boring" industries hide similar opportunities? What other unsexy niches could provide leverage over entire technological ecosystems? The Gudeng story suggests we're looking in the wrong places for the next generation of powerful companies.

The specialized manufacturing excellence demonstrated by Gudeng represents something increasingly rare: deep, patient, technical mastery developed over decades. In an era of software eating everything and winner-take-all digital platforms, Gudeng reminds us that atoms still matter, that manufacturing still matters, that the physical instantiation of digital dreams still requires extraordinary expertise.

As we stand on the brink of the AI revolution, as we push toward quantum computing and whatever comes next, remember this: somewhere in Taiwan, a company you've never heard of is making the boxes that protect the templates that print the circuits that power the future. They're not the heroes of the semiconductor story. They're something more important: the foundation upon which all the heroes stand.

The next time you use ChatGPT, or unlock your phone with facial recognition, or stream a 4K movie, remember that none of it would be possible without Gudeng's pods. The future isn't just built by the companies whose names we know. It's built by the invisible giants, the boring monopolists, the companies that perfect one critical thing while everyone else chases the next big thing.

And perhaps that's Gudeng's greatest lesson: in a world obsessed with disruption, there's enormous power in being indispensable infrastructure. You don't need to change the world. Sometimes, you just need to make the boxes that protect the tools that change the world. And if you make those boxes better than anyone else, if you make them so well that nobody can imagine using anything else, then you don't just participate in the future—you become a prerequisite for it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube